Clergy ************************************************************************

|

|

|

- Darrell Ryan

- 5 years ago

- Views:

Transcription

1 Clergy Contents In this webinar, the student will learn the tax treatment of income received by a minister. Objectives After completing this webinar, the student will be able to: Determine if clergy are employees or self-employed Identify which clergy income is subject to income tax and which to SE tax Determine the handling and taxation of a housing allowance Prorate business expenses between Schedule C and Schedule A and between taxable wages and nontaxable housing allowance. Additional References Publication 15-A Employer s Supplemental Tax Guide Publication 517 Social Security and Other Information for Members of the Clergy and Religious Workers Publication 463 Travel, Entertainment, Gift, and Car Expenses Publication 1828 The IRS tax guide for Churches and Religious Organizations ************************************************************************ Are Ministers Employees or Self-Employed (Independent Contractors) For Income Tax Purposes? The IRS position that a minister is an employee for income reporting purposes is shown in Publication 517, Social Security and Other Information for Members of the Clergy and Religious Workers: Unlike other exempt organizations or businesses, a church is not required to withhold income tax from the compensation that it pays to its duly ordained, commissioned, or licensed ministers for performing services in the exercise of their ministry. An employee minister may, however, enter into a voluntary withholding agreement with the church by completing IRS Form W-4, Employee s Withholding Allowance Certificate. A church should report compensation paid to a minister on Form W-2, Wage and Tax Statement, if the minister is an employee, or on IRS Form 1099-MISC, Miscellaneous Income, if the minister is an independent contractor. Three federal taxes are paid on wages and self-employment income income tax, social security tax, and Medicare tax. Social security and Medicare taxes are collected under one of two systems. Under the Self-Employment Contributions Act (SECA), the self- Gold Level Document: Clergy 1

2 employed person pays all the taxes. Under the Federal Insurance Contributions Act (FICA), the employee and the employer each pay half of the taxes. No earnings are subject to both systems. Table 1 - Are Ministerial Earnings* Covered Under FICA or SECA? Class Covered under FICA? Covered under SECA? Minister NO. Your ministerial earnings are exempt. YES, if you do not have an approved exemption from the IRS. NO, if you have an approved exemption. Member of a religious order who has not taken a vow of poverty NO. Your ministerial earnings are exempt. YES, if you do not have an approved exemption from the IRS. NO, if you have an approved exemption. Member of a religious order who has taken a vow of poverty Christian Science practitioner or reader Religious worker (church employee) Member of a recognized religious sect YES, if: Your order elected FICA coverage for its members, or You worked outside the order and the work was not required by, or done on behalf of, the order. NO, if neither of the above applies. NO. Your ministerial earnings are exempt. YES, if your employer did not elect to exclude you. NO, if your employer elected to exclude you. YES, if you are an employee and do not have an approved exemption from the IRS. NO. Your ministerial earnings are exempt. YES, if you do not have an approved exemption from the IRS. NO, if you have an approved exemption. YES, if your employer elected to exclude you from FICA. NO, if you are covered under FICA. YES, if you are self-employed and do not have an approved exemption from the IRS. NO, if you have an approved exemption. NO, if you have an approved exemption. * Ministerial earnings are the self-employment earnings that result from ministerial services, defined and discussed later. For more information see IRS Publication 517 Social Security and Other Information for Members of the Clergy and Religious Workers. SOCIAL SECURITY COVERAGE The services performed in the exercise of a ministry, of the duties of a religious order, or of a profession as a Christian Science practitioner or reader are covered by social security and Medicare under SECA (the Self-Employment Contributions Act). Earnings for these ministerial services (defined later) are subject to self-employment (SE) tax unless one of the following applies. 2 Gold Level Document: Clergy

3 You are a member of a religious order who has taken a vow of poverty. You ask the IRS for an exemption from SE tax for your services and the IRS approves your request. You are subject to the social security laws of a foreign country under the provisions of a social security agreement between the U.S. and that country. (For more information see Pub 54.) Ministers The earnings for the services performed as a minister of a church are subject to SE tax, even if these services are performed as an employee of that church. However, a minister can request that the IRS grant an exemption. Employment Status for Other Tax Purposes. Even though a member of the clergy is considered a self-employed individual in performing his or her ministerial services for social security tax purposes, he or she may be considered an employee for income tax or retirement plan purposes. For income tax or retirement plan purposes, some of his or her income may be considered self-employment income and other income may be considered wages. Common-Law Employee. Under common-law rules, a member of the clergy is considered either an employee or a self-employed person depending on all the facts and circumstances. Generally, a minister is an employee if the employer has the legal right to control both what the minister does and how it is done, even if the minister has considerable discretion and freedom of action. For more information about the commonlaw rules, see Publication 15 A, Employer s Supplemental Tax Guide. If a minister is employed by a congregation for a salary, he or she is generally a commonlaw employee and income from the exercise of his or her ministry is considered wages for income tax purposes. However, amounts received directly from members of the congregation, such as fees for performing marriages, baptisms, or other personal services, are considered self-employment income. Example. A church hires and pays its minister a salary to perform ministerial services subject to its control. Under the common-law rules, the minister is an employee of the church while performing those services. Ministers are not treated differently from other taxpayers when determining if they are an employee or self-employed. The same factors as for other professions apply. Very few ministers are considered to be self-employed only. These do not have a regular congregation and do not work for the church congregation headquarters. These ministers may travel to share their message or may be interim pastors and not regularly report to the same congregation. They are self-employed only and should receive a Form MISC, Miscellaneous Income, from any church or congregation paying them $600 or more during the year. If a minister files only a Schedule C, Profit or Loss from Business, Gold Level Document: Clergy 3

4 and does not receive Form W-2, Wage and Tax Statement, from a church, there is greater potential for audit since the IRS considers very few ministers to be self-employed. As an aid in determining whether an individual is an employee under the common-law rules, twenty factors (see Appendix) have been developed. There is no set number of factors that make the individual an employee when applying the IRS twenty-factor test. Each case is evaluated on its own merits. Based on the Seven-factor Test (see Appendix), most ministers serving local congregations will be viewed as employees by the IRS for income tax purposes. An ordained, commissioned and/or licensed minister who is assigned to one church is an employee of that church, as the church has control of what the minister does, how he does it and the church has the right to hire and fire. A minister who is not assigned to any one church would be considered self-employed. Armed forces chaplains are treated as any other armed forces members. They are considered to be commissioned officers and therefore not ministers in the exercise of a ministry. Similarly, services performed by employees of a state, such as chaplains in a state prison or a government-owned hospital, are considered to be performed by civil servants of the state and not by ministers in the exercise of their ministry. Members of Religious Orders and Christian Science Practitioners If a person is a member of a religious order and has not taken a vow of poverty, their earnings for ministerial services are subject to SE tax. If a member of a religious order has taken a vow of poverty, they are already exempt from paying SE tax on their earnings for services performed as an agent of their church or its agencies. For more information on members of a religious order taking a vow of poverty, see Publication 517. Services performed as Christian Science practitioners or readers are generally subject to SE tax. Members of religious orders and Christian Science practitioners or readers can request exemption from SE tax (covered later). Religious Workers Religious workers (a church or employee of a religious organization) are generally subject to social security and Medicare tax under FICA and not SECA, so the employer would withhold these taxes. There are some exceptions to this rule see Pub 517. Treatment for Employment Taxes Per Publication 1828, Tax Guide for Churches and Religious Organizations, these organizations must generally withhold and pay FICA taxes for their employees unless one of the following exceptions applies: 4 Gold Level Document: Clergy

5 Wages are paid for services of a duly ordained, commissioned, or licensed minister of a church or by a member of a religious order in the exercise of their duties of the ministry or order; The church or religious organization pays the employee wages of less than $ in a calendar year, or A church that is opposed to the payment of social security and Medicare taxes for religious reasons files IRS Form 8274, Certification by Churches and Qualified Church-Controlled Organizations Electing Exemption from Employer Social Security and Medicare Taxes, in a timely manner. See the above referenced IRS Tax Guide. Not all church employees are members of the clergy. Examples of non-clergy church employees are custodians, secretaries, musicians, organist, etc. A church employee with no social security or Medicare tax shown as having been withheld on Form W-2 must pay SE tax on his or her wages and file Schedule SE. The Form 8274 election does not relieve the organization of its obligation to withhold income tax on wages paid to its employees. If the church makes the election, affected employees must pay the self-employment tax using Schedule SE. MINISTERIAL SERVICES Ministerial service, in general, is the service you perform in the exercise of your ministry, the duties as required by your religious order, or the profession as a Christian Science practitioner or reader. Income received for performing ministerial services is subject to SE tax unless a person has an exemption. Even if you have an exemption, only the income you receive for performing ministerial services is exempt. The exemption does not apply to any other income. EXEMPTION FROM SELF-EMPLOYMENT (SE) TAX Members of the clergy (ministers, members of a religious order, or Christian Science practitioner or reader) or members of a recognized religious sect can request an exemption from SE tax. Taxpayers who work for a church (or church-controlled nonprofit division) that does not pay the employer s part of the social security tax on wages may be able to choose to be exempt from social security and Medicare taxes, including the SE tax. To do so, they must be a member of a religious sect or division opposed to accepting benefits of public or private insurance, including social security and Medicare benefits and the individual makes the election by filing Form 4029, Application for Exemption from Social Security and Medicare Taxes and Waiver of Benefits. Members of a religious order who have taken a vow of poverty are exempt from selfemployment tax. They are not required to file any form to claim the exempt status. For Gold Level Document: Clergy 5

6 income tax purposes, the earnings are tax free as they are considered to be the income of the religious order, not of the individual. Ministers, members of religious orders who have not taken a vow of poverty, and Christian Science practitioners or readers can also request an exemption from selfemployment tax. If granted, the exemption applies only to earnings received for qualified religious services, not to earnings from other employment or self-employment. To request the exemption, the individual must be conscientiously opposed to public insurance. He or she must file Form 4361, Application for Exemption from Self- Employment Tax for Use By Ministers, Members of Religious Orders and Christian Science Practitioners, by the due date (including extensions) of the income tax return for the second year in which he or she has at least $400 of self-employment earnings, any of which are from religious services. The decision to request this exemption cannot be based solely on economic considerations. Other requirements are listed in Publication 517. On the minister s Form 1040, page 2, write Exempt Form 4361 the line 56 for selfemployment tax. Form 4361 only applies to qualified services performed in the exercise of the ministry or in the exercise of duties as required by the religious order. It does not apply to other types of income. Example. Rev. Jaeger, a clergyman ordained in 2014 has net self-employment earning of $450 in 2014 and $500 in He must file his application for exemption by the due date, including extensions, for his 2015 income tax return. However, if Rev. Jaeger does not receive IRS approval for an exemption by April 18, 2016, his SE tax for 2015 is due by that date. Example. Rev. Kerry, ordained in 2010, has $7,500 in net earnings as a minister in both 2013 and He files Form 4361 on March 5, 2015 if the exemption is granted, it is effective for 2013 and following years. If the minister ever filed Form 2031, Revocation of Exemption From Self-Employment Tax For Use By Ministers, Certain Members of Religious Orders, and Christian Science Practitioners, for his or her 1986, 1987, 2000, or 2001 tax year, or elected before 1968 to be covered under social security, the minister cannot be exempt from SE tax. These elections are irrevocable. If ministers are assigned to a church, they are employees for income tax purposes and self-employed for SE tax purposes (dual status). They should receive Form W-2 from the church. Various incomes received for ministerial services performed outside of the church requirements are self-employment income to be reported on Schedule C. (The minister should receive Form 1099-MISC if the income is more than $600.) Publication 517 contains a chart on page 5 that illustrates The Self-Employment Tax Exemption Application and Approval Process. 6 Gold Level Document: Clergy

7 SE TAX: FIGURING NET EARNINGS Amounts Included in Gross Income to Figure Net Earnings To figure net earnings from self-employment (on Schedule SE), include in gross income: Salaries and fees for qualified services, Money received for marriages, baptisms, funerals, masses, etc., The value of meals and lodging provided to the taxpayer for the employer s convenience, The fair rental value of a parsonage provided to the taxpayer (including the cost of utilities that are furnished), the rental allowance (including an amount for payment of utilities) paid to the taxpayer, and Any amount a church pays toward the taxpayer s income tax or SE tax, other than withholding from the taxpayer s salary. This amount is also subject to income tax. Example: Pastor Adams receives an annual salary of $39,000 as a full-time minister. The $39,000 includes $5,000 that is designated as a rental allowance to pay utilities. His church owns a parsonage that has a fair rental value of $12,000 per year. Pastor Adams is given the use of the parsonage. He is not exempt from SE tax. He must include $51,000 ($39,000 plus $12,000) when figuring his net earnings for SE tax purposes. The results would be the same if, instead of the use of the parsonage and receipt of the rental allowance for utilities, Pastor Adams had received an annual salary of $51,000 of which $17,000 ($5,000 plus $12,000) per year was designated as a rental allowance. Clergy should recognize that bonuses, and many kinds of fringe benefits, are includable in compensation. They are not tax-free gifts. Churches are exempt from withholding taxes or matching social security and medicare taxes as other employers are required to do, however some churches choose to withhold federal income tax that is reported in box 2 of the Form W-2, and often will withhold an extra amount so the church employee will have paid in enough to cover their selfemployment tax liability. Churches that pay unreasonable compensation to a minister jeopardize their tax-exempt status. There is no exact amount of compensation to be considered unreasonable compensation by the IRS for every clergy member. An individual situation being examined would consider the duties being performed, the other payments being received, and the size and income of the church paying the compensation. Amounts Not Included in Gross Income to Figure Net SE Earnings: Do not include the following amounts in gross income when figuring net earnings from self-employment: Gold Level Document: Clergy 7

8 Offerings that others made to the church. Contributions by the church to a tax-sheltered annuity plan set up for the taxpayer, including any salary reduction contributions (elective deferrals) that are not included in gross income. Pension payments or retirement allowances received for past qualified services. The rental value of a parsonage or a parsonage allowance provided to the taxpayer after retirement. Allowable Deductions When figuring net earnings from self-employment, deduct all nonemployee ministerial business expenses. (This is done on Schedule C for qualifying Schedule C income). Also, deduct all allowable unreimbursed trade or business expenses incurred in performing ministerial services as a common-law employee of the church (Form 2106, Employee Business Expenses, can be used as a worksheet for this calculation even if they do not itemize.) The unreimbursed employee business expenses are deducted from the total of the Schedule C, Form W-2, and nontaxable incomes in calculating the amount for line 2 of Schedule SE, Self-Employment Tax. Nonemployee Ministerial Expenses These are qualified expenses incurred while not working as a common-law employee of a church but as a completely self-employed minister. Sometimes such ministers call themselves evangelists and travel from one location to another. Their expenses include those for travel and other expenses incurred in performing marriages and baptisms, and in delivering speeches and are generally deducted on Schedule C with the Net Income or Loss carrying to Schedule SE. Employee Reimbursement Arrangements If the taxpayer received an advance, allowance, or reimbursement for expenses, the method of reporting the amount received depends on whether the reimbursement was paid under an accountable plan or a nonaccountable plan. Accountable Plan. To be an accountable plan, the employer s reimbursement arrangement must include all three of the following rules: 1. The expenses must have a business connection that is, the taxpayer must have paid or incurred deductible expenses while performing services as an employee of the employer. 2. The taxpayer must adequately account to the employer for these expenses within a reasonable period of time. 3. The taxpayer must return any excess reimbursement or allowance within a reasonable period of time. Generally, if the expenses equal the reimbursement, the taxpayer has no deduction on the tax return and the reimbursement is not reported on Form W 2. If the expenses are more than the reimbursement, the taxpayer can deduct the excess expenses for SE tax and income tax purposes. For example, a church has in its minutes to reimburse 30 cents for each mile the minister has accounted to the church with a travel voucher. The minister 8 Gold Level Document: Clergy

9 computes his mileage expenses using the current government standard mileage rate for business miles (57.5 cents per mile for 2015) and subtracts the 30 cents per mile that the church has reimbursed him. This excess is then a reportable deduction on his tax return. Nonaccountable Plan. A nonaccountable plan is a reimbursement arrangement that does not meet at least one of the three rules listed under Accountable Plan. In addition, even if the employer has an accountable plan, the following payments will be treated as being paid under a nonaccountable plan. Excess reimbursements that the taxpayer failed to return to the employer. Reimbursement of nondeductible expenses related to the employer s business. The employer will combine any reimbursement paid to the taxpayer under a nonaccountable plan with wages, salary, or other compensation, and report the combined total in box 1 of Form W 2. The taxpayer can deduct the related expenses (for SE and income tax purposes) regardless of whether they are more than, less than, or equal to the reimbursement. For more information on accountable and nonaccountable plans, see Publication 463, Travel, Entertainment, Gift, and Car Expenses. INCOME TAX: INCOME AND EXPENSES Clergy Income Fees, offerings, or gifts for speaking or for performing weddings, funerals or baptisms are considered professional income which is reported on Schedule C. Payments for writing, lecturing, radio or television appearances, etc., are also types of professional income which is also reported on Schedule C. The income or royalties and expenses from selling religious tapes and books are shown on Schedule C as professional income. Generally, income reported on Schedule C is subject to self-employment tax which requires the completion of Schedule SE. Honorariums and fees for weddings, funerals, etc. paid directly to the employer (church) rather than to the minister are not considered compensation to the minister. Often a church will collect a love offering which is an amount of money over and above the minister s salary. This may occur regularly on the minister s birthday or anniversary date. This amount is simply additional salary to the minister and should be included as gross income on Form W-2. (The courts have repeatedly held that such offerings are taxable because they occur from the employer-employee relationship between minister and church.) A love offering may, on occasion, be a true gift and therefore not taxable. This could happen, for example, if the church made a gift of money to the minister because he or she or a member of their household was facing heavy medical expenses. This would be nontaxable only if it could be demonstrated that the congregation was treating the Gold Level Document: Clergy 9

10 minister in the same way it would treat any other member of the congregation under similar circumstances. A minister may, at times, believe that if he or she gives all earnings from the church back to the church, he or she would have no taxable income. This is not correct. Earnings from the church must still be included on his or her tax return and the money given to the church is reported as an itemized deduction on Schedule A, Itemized Deductions, as, it is a charitable contribution and subject to AGI limitations. Exclusion of Rental Allowance and Fair Rental Value of a Parsonage Ordained, commissioned, or licensed ministers may be able to exclude the rental (parsonage or housing) allowance or fair rental value (FRV) of the parsonage provided as part of their pay for performed services. Housing Allowance. A housing or parsonage allowance, as officially designated in advance by the church, is not subject to income tax as long as the whole amount is spent for that purpose. This amount, however, is subject to SE tax, less allowable business expenses attributed to it. A minister s housing allowance is only computed on his or her main home. The housing allowance is not allowed to be computed on a second home. Housing allowance must be reported in box 14 of a minister s W-2. Designation requirement. The church or organization that employs a minister must officially designate a definite amount as the payment for housing allowance before it makes the payment. It can't determine the amount of the housing allowance at a later date. If the church or organization doesn't officially designate a definite amount as a housing allowance, a minister must include their total salary in their taxable income. If a minister is employed and paid by a local congregation, a resolution by a national church agency of their denomination doesn't effectively designate a housing allowance. The local congregation must officially designate the part of their salary that is a housing allowance. However, a resolution of a national church agency can designate housing allowance if they are directly employed by the national agency. An official designation of an amount as a housing or rental allowance may be shown in an employment contract, in the minutes of a church or qualified organization, in a budget, or any official action taken in advance of payment of the allowance. A designation is sufficient if it permits a payment to be identified as a payment of a rental or housing allowance as distinguished from salary or other remuneration. Amount Actually Spent for Housing. The following list shows typical expenses that are considered in figuring the amount of parsonage allowance. Rent or principal payments (included in the regular mortgage payment), cost of buying a home, and down payments Real estate taxes and mortgage interest (also included in the regular mortgage payment) for the home. (These expenses are deductible again as an itemized 10 Gold Level Document: Clergy

11 deduction. A double deduction, but allowed by the IRS (Revenue Ruling and Sec. 265(a)(6).) Insurance on the home and/or contents Improvements, repairs, and upkeep of the home and/or contents, such as a new roof, room addition, carpet, garage, patio, fence, pool, and appliance repair, etc. Furnishings and appliances: dishwasher, vacuum sweeper, TV, VCR, DVD, stereo, piano, computer (personal use), washer, dryer, beds, small kitchen appliances, cookware, dishes, sewing machine, garage door opener, lawn mower, hedge trimmer, etc. Decorator items: drapes, throw rugs, pictures, knick knacks, paintings, wallpapering, bedspreads, sheets, towels, etc. Miscellaneous any thing that maintains the home and its contents, that has not been included in repairs or decorator items: cleaning supplies for the home, brooms, light bulbs, dry cleaning of drapes, shampooing carpet, expense to run lawn mower, tools for landscaping, garden hose to water the lawn, etc. Utilities heat, electric, non-business telephone, water, cable TV, sewer charges, garbage removal, etc. (Sometimes a church will pay a utility allowance in addition to a parsonage allowance.) Fair Rental Value (FRV) of Parsonage. The fair rental value of a house or parsonage, including utilities for a main home, can be excluded from gross income. The exclusion cannot be more than the reasonable pay for services. If the minister pays for utilities, any designated utility allowance, up to the actual cost, can also be excluded. Example. Rev. Baker is a full-time minister. The church allows her to use a parsonage that has an annual fair rental value of $24,000. The church pays an annual salary of $67,000, of which $7,500 is designated for utility costs. The actual utility costs were $7,000. For income tax purposes, Rev. Baker excludes $31,000 from gross income ($24,000 FRV plus $7,000 for utilities). She will report $60,000 ($59,500 salary plus $500 of unused utility allowance. The income for SE tax purposes, however, is $91,000 ($67,000 salary plus $24,000 FRV of the parsonage). Home Ownership. If the minister owns his or her home and receives a housing or rental allowance as part of ministerial pay, he or she may exclude from gross income the smallest of: The amount actually used to provide a home, The amount officially designated as a housing allowance, or The fair rental value (FRV) of the minister s home including furnishings, utilities, garage, etc. Example. Rev. Bernard, an ordained minister, is vice president of academic affairs at Holy Word Seminary. His compensation package includes a salary of $80,000 per year and a $30,000 housing allowance. His housing costs for the year included mortgage payments (mortgage interest and mortgage principal payments) of $15,000, Gold Level Document: Clergy 11

12 utilities of $3,000, and $3,600 for home maintenance and new furniture. The rental value of the home, as furnished, is $18,000 per year. The three amounts for comparison are: 1. Actual expenses of $21,600 ($15,000 mortgage payments + $3,000 utilities + $3,600 other costs). 2. Designated housing allowance of $30, FRV = rental value of the home ($18,000) + utilities ($3,000) = $21,000. Rev. Bernard may exclude $21,000 from gross income but must add the other $9,000 of the housing allowance previously treated as nontaxable into his income. The entire $30,000 will be considered in arriving at net self-employment income for determining self-employment taxes. Fair Rental Value of Provided Parsonage (includes utilities and furnishings). The fair rental value of a provided parsonage is considered to be the minister s housing allowance. The value amount is nontaxable for income tax purposes but is taxable for SE tax purposes. It is not unusual for a minister with a provided parsonage to also receive a designated allowance to cover utilities, furnishings, etc. The fair rental value of the parsonage plus any funds for utilities, etc., must be reported in Box 14 of Form W-2. If a clergy member does receive additional funds for utilities, furnishings, etc. the tax preparer must be sure that the money is spent for that purpose. If all the money is not spent for utilities, etc. and housing-related expenses, then the excess will be subject to income tax and is entered on line 7 of Form It is also subject to social security tax on Schedule SE. Retired Minister. Retired ministers may exclude from gross income the fair rental value of a home, plus utilities, furnished by a church as a part of the minister s pay for past services or the part of the minister s pension that was designated as a rental allowance. Clergy Member s Business Expenses Keep in mind the following rules when working with a clergy member s expenses: 1. An employee must use Form 2106, Employee Business Expenses, for expenses that include travel and transportation expenses and itemize deductions using Schedule A. 2. A self-employed person uses Schedule C to report business expenses related to self-employment income. 3. Tax law states that when nontaxable income (no income tax is paid on this income) is generated, the expenses incurred for this nontaxable income are not deductible. (Exception: This rule does not apply to deductions for home mortgage interest or real estate taxes paid on the home.) A clergy member s business expenses must be prorated between a ministerial Schedule C and Schedule A (Form 2106 used to deduct expenses against income reported on Form W-2 from the church), if he has both types of ministerial income. In accordance with rules 1 and 2, the minister will have expenses that apply because he or she is an employee 12 Gold Level Document: Clergy

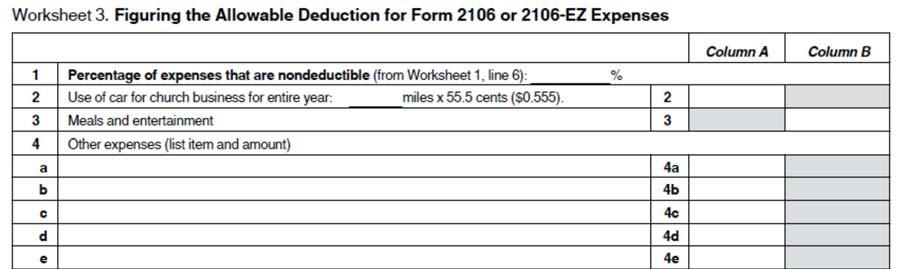

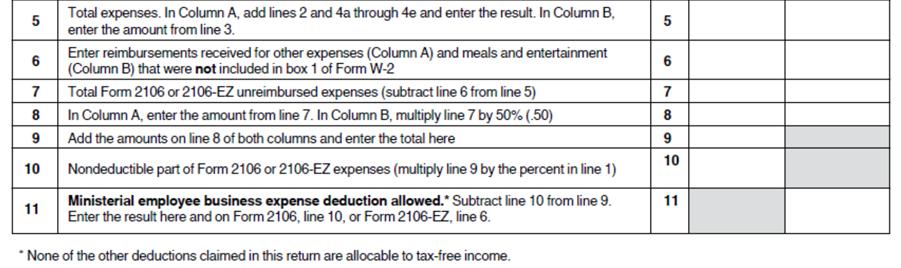

13 and because of self-employment income that was received. It may be difficult for a minister to determine how much of the ministerial supplies were used for Schedule C or for being an employee; an allocation may be made according to gross income of each. A minister s expenses may consist of, but are not limited to, the following: office supplies, religious materials, subscriptions, expendable books (small not a library), seminar/conference registration dues, depreciation (library, equipment), education expenses, travel and transportation expenses, and possibly entertainment expenses. Office-in-home expenses may apply if qualifications are met, taking into consideration any tax-free housing or utility allowance received from the church. Ministers are not allowed expenses for business suits or for the cost of their cleaning. Only pulpit-type apparel (vestments, robes, special collars, etc) and their cleaning are deductible if the minister must purchase and maintain these items. If the minister has an accountable plan with his or her employer, any education and/or travel and transportation allowances from that employer are not taxable, assuming the minister properly accounts for these expenses and the expenses are job related. If the allowance amounts are simply added to the minister s compensation with no reporting requirements (nonaccountable plan), such amounts are taxable and reported on line 7 of Form The related expenses are deductible on Form Expenses that are reimbursed under an accountable plan are not deductible and the reimbursements are not included in form W-2 box 1. The grand total of professional expenses should be calculated before transportation and travel expenses. The professional expenses will then be calculated by a percentage of income as to the portion allocated as Schedule C expenses and the portion as Form 2106, Employee Business Expenses, line 4. Complete accurate record keeping is necessary to justify all expenses. Business mileage can be calculated using the standard mileage rate or actual expenses. The standard meal rate may be used for travel away from home as well as other business-related mileage on a personal vehicle. Entertainment expenses must conform to IRS Code Section 274(d) meaning that place, time, amount spent, business purpose, and who was entertained must be recorded in a timely manner and maintained with records. Once professional expenses have been allocated between Form 2106 and Schedule C, travel and transportation expenses for Form W-2 income will be entered on Form 2106 on the appropriate lines and also on the appropriate lines of Schedule C for the selfemployment income. The total of all business expenses must then be prorated between taxable income and nontaxable housing allowance because of rule number 3 on the previous page. This will cause a reduction (by a prorated percentage) of deductible expenses to be claimed on Schedule C and to be reported on Schedule A from Form Gold Level Document: Clergy 13

14 To figure the deduction amount for each income area (Schedule C, Form 2106, etc.), multiply the expense to be allocated by the following equation: Tax-free rental or parsonage allowance All ministerial income (taxable and tax free) Example. Reverend Brian has total expenses for Schedule C of $2,000 and total expenses for Form 2106 of $4,000. If Reverend Brian s nontaxable housing allowance is $5,000, his Form W-2 salary income is $40,000, and his gross income on Schedule C is $5,000, then Reverend Brian s total compensation is $50,000 ($40,000 from Form W-2 + $5,000 from Schedule C + $5,000 housing allowance). Nontaxable housing allowance: $5,000 Total compensation: $50,000 Allocation percentage to tax-free income = 0.10 or 10% The total employee expenses for Form 2106 will have to be reduced by 10% before entering them on Schedule A. The total expenses for Schedule C will have to be reduced by 10% before entering the deduction on the actual Schedule C. Note. This reduction has to be done in figuring only the taxable income for Reverend Brian, not his income for SE tax purposes. Reverend Brian s income for SE tax purposes will be computed as follows: Form W-2 income $40,000 Gross Schedule C income 5,000 Nontaxable housing allowance 5,000 Minus total expenses from Form ,000 (whether itemizing or not) Minus total expenses from Schedule C - 2,000 Amount subject to SE tax $44,000 This amount of $44,000 will be entered on Schedule SE, line 2. (One-half of the SE tax will be deducted as an adjustment to income in figuring the AGI.) Form 2106 and a statement of clergy income and expenses must be prepared even if the clergy member does not have enough deductions to itemize. The forms are necessary to document the calculation of correct SE income for the SE tax purposes on Schedule SE (Form 1040). The expenses attributable to Form 2106 as an employee can only be used against income (for income tax) if itemizing deductions. Form 2106 expenses cannot be used on Schedule C or anywhere else on the tax return. 14 Gold Level Document: Clergy

15 Minister s Self Employment Tax Worksheet 1 W-2 salary as a minister (from box 1 of Form W-2) 1 2 Net profit from Schedule C, line 31, or Schedule C-EZ, line 3 2 3a Parsonage or rental allowance (from Worksheet 1, line 3a or 4a) b Utility allowance (from Worksheet 1, line 3b or 4b) 3b c Total allowance (add lines 3a and 3b) 3c 4 Add lines 1, 2, and 3c Schedule C or C-EZ expenses allocable to tax-free income (from Worksheet 2, Line 6) Total unreimbursed employee business expenses after the 50% reduction for meals and entertainment (from Worksheet 3, line 9) 7 Total business expenses not deducted in lines 1 and 2 above (add lines 5 and 6) 7 8 Net self-employment income. Subtract line 7 from line 4. Enter here and on Schedule SE, Section A, line 2, or Section B, line 2. What if the Minister Receives Form 1099-MISC Instead of Form W-2? It is important to consider the facts and circumstances of the relationship between the payer and the payee (recipient). A minister who receives an incorrect reporting document needs to educate the payer as to why an employer/employee relationship exists between them and then obtain corrected documents. Completing the first step below will reduce audit exposure for the employee and result in correct forms being issued in the future. The employer should issue a corrected Form 1099-MISC with zero (0) income shown. Then, the employer should issue a Form W-2 correctly reporting the taxable salary in box 1. Copies must be sent to all required agencies. When an employed dual-status minister who is paid by a church or churchcontrolled organization receives Form 1099-MISC instead of a Form W-2 and the employer will not correct the situation, the following procedure is recommended: Prepare the return by entering the amount shown as income on Form MISC onto Schedule C as gross receipts. (IRS computers will scan the return during automatic 1099-matching audits and search for that amount there.) Subtract the same number Schedule C, Part V, Other Expenses with description of wages taken on Form 1040, line 7. The Schedule C will have a net result of zero, the extent of the salary. Then enter the amount as income on Form 1040, line 7, as though it were wages from Form W-2. The IRS computers will accept an amount on line 7 that is greater than the total wages reported on W-2 forms attached to the return. Use Form 2106 and Schedule A to deduct any unreimbursed employee business expenses. 3a Gold Level Document: Clergy 15

16 Court Decisions Affecting Clergy Tax Returns Court Case Warren vs. Commissioner of Revenue and Public Law In the court case of Warren vs. Commissioner of Revenue, 114 TC No. 23 (2000), the tax court held that the exclusion for a parsonage allowance is not limited to the FRV of the home. This differs from the IRS position. Clergy Housing Allowance Clarification Act, P.L. (Public Law) Background. Before its amendment by P.L , Code Sec. 107 provided that the gross income of a minister does not include (1) the rental value of a home furnished to him as part of his compensation (Code Sec. 107(1)); or (2) the rental allowance paid to him as part of his compensation, to the extent used by him to rent or provide a home (Code Sec. 107(2)). For decades, the IRS position had been that the Code Sec. 107(2) exclusion could not exceed the lesser of the amount used to provide a home or the fair market rental value of the home (including furnishings, utilities, garage, etc.). In 2000, the IRS view was rejected in Warren, 114 TC #23. The Tax Court held that neither Code Sec. 107(2), nor the regulations, nor the related legislative history, limited the Code Sec. 107(2) exclusion to the fair market rental value of the residence occupied. It ruled that an excludable rental allowance may be used to rent or buy a home and to pay expenses directly related to providing a home (e.g., landscaping, insurance premiums, property taxes, repairs and maintenance). IRS appealed Warren to the Ninth Circuit, which chose to consider whether the parsonage exclusion violated the constitutional doctrine of Separation of Church and State, and IRS requested supplemental briefs to be filed on this issue. Concerned that the Ninth Circuit might rule that the parsonage exclusion was unconstitutional, Congress acted to resolve the underlying issue in Warren and thereby protect the exclusion. Revised exclusion. As amended by Sec. 2(a) of P.L , Code Sec. 107 provides that the gross income of a minister does not include: (1) the rental value of a home furnished as part of compensation (Code Sec.107 (1)); or (2) the rental allowance paid to him as part of his compensation, to the extent used by him to rent or provide a home, and to the extent such allowance does not exceed the fair rental value of the home, including furnishings and appurtenances such as a garage, plus the cost of utilities. (Code Sec. 107(2)) Effective date. The revised rule for the exclusion generally applies for tax years beginning after It also applies for tax years beginning before 2002 for which the taxpayer: (1) on a return filed before Apr. 17, 2002, limited the Code Sec. 107 exclusion as provided by P.L , or (2) filed a return after Apr. 16, Except as provided in (1) and (2), above, Sec. 2(b)(3) of P.L says that notwithstanding any prior regulation, revenue ruling, or other guidance issued by the Internal Revenue Service, no person shall be subject to the limitations added to section 16 Gold Level Document: Clergy

17 107 of [the Internal Revenue] Code by this Act for any taxable year beginning before January 1, In summary: On May 20, 2002 the President signed the Clergy Housing Allowance Clarification Act of 2002 into law as P.L Effective generally for post-2001 tax years, the Act essentially incorporates the IRS rulings position on the Code Sec.107(2) parsonage allowance exclusion into the code. The legislation is designed to protect the exclusion from a looming constitutional challenge. The taxpayer in Warren and those that followed the holding in that case for pre-2002 years on returns filed before Apr. 17, 2002 are safe from challenge. The effect of (1), above, is to prevent those that followed the IRS position for pre-2002 years from filing an amended returns based on the Warren decision. APPENDIX A: Worksheets for Ministers Worksheet 1 for Ministers Name of Taxpayer SSN Tax Year Computation of percentage for nondeductible expenses: Ministerial Income Taxable (1) Tax-free (2) Total (3) Salary, Wages, etc. Parsonage Allowance Utility Allowance - Costs Excess Gross income, Sch C, line 1 Totals To figure the percentage for nondeductible expenses: Divide tax-free ministerial income (2) by total ministerial income (3). Carry the result to Worksheet 2 for Ministers (percentage of nondeductible expenses). Gold Level Document: Clergy 17

18 Worksheet 2 for Ministers Name of Taxpayer SSN Tax Year Computation of expenses that are allocable to tax-free ministerial income and the amount that is deductible List Form 2106 or Schedule C Description and Amount of Expenses (a) Percentage of Nondeductible Expenses (from Worksheet 1) Multiply Amount of Expenses (a) by Percentage (Result = b) Subtract Nondeductible (b) from expenses (a) (= Deductible Expenses) 18 Gold Level Document: Clergy

19 Worksheets from Publication 517 Name of Taxpayer SSN Tax Year Gold Level Document: Clergy 19

20 20 Gold Level Document: Clergy

21 APPENDIX B: The Twenty Factors of the Common Law Rules 1. Instructions. A worker who is required to comply with other persons instructions about when, where, and how he or she is to work is ordinarily an employee. This control factor is present if the person or persons for whom the services are performed have the right to require compliance with instructions. See, for example, Rev. Ruling , C.B. 464, and Rev. Ruling , C.B Training. Training a worker by requiring an experienced employee to work with the worker, by corresponding with the worker, by requiring the worker to attend meetings, or by using other methods, indicates that the person or persons for whom the services are performed want the services performed in a particular method or manner. See Rev. Ruling , C.B Integration. Integration of the worker s services into the business operations generally shows that the worker is subject to direction and control. When the success or continuation of a business depends to an appreciable degree upon the performance of certain services, the workers who perform those services must necessarily be subject to a certain amount of control by the owner of the business. See United States v. Silk, 331 U.S. 704 (1947), C.B Services Rendered Personally. If the services must be rendered personally, presumably the person or persons for whom the services are performed are interested in the methods used to accomplish the work as well as in the results. See Rev. Ruling , C.B Hiring, Supervising, and Paying Assistants. If the person or persons for whom the services are performed hire, supervise, and pay assistants, that factor generally shows control over the workers on the job. However, if one worker hires, supervises, and pays the other assistants pursuant to a contract under which the worker agrees to provide materials and labor and under which the worker is responsible only for the attainment of a result, this factor indicates an independent contractor status. Compare Rev. Ruling , C.B. 178, with Rev. Ruling , C.B Continuing Relationship. A continuing relationship between the worker and the person or persons for whom the services are performed indicates that an employeremployee relationship exists. A continuing relationship may exist where work is performed at frequently recurring although irregular intervals. See United States v. Silk. 7. Set Hours of Work. The establishment of set hours of work by the person or persons for whom the services are performed is a factor indicating control. See Rev. Ruling , C.B Full Time Required. If the worker must devote substantially full time to the business of the person or persons for whom the services are performed, such person or persons have control over the amount of time the worker spends working and impliedly restrict the worker from doing other gainful work. An independent contractor, on the other hand, is free to work when and for whom he or she chooses. See Rev. Ruling , C.B Gold Level Document: Clergy 21

22 9. Doing Work on Employer s Premises. If the work is performed on the premises of the person or persons for whom the services are performed, that factor suggests control over the worker, especially if the work could be done elsewhere (Rev. Ruling , C.B. 693). Work done off the premises of the person or persons receiving the services, such as at the office of the worker, indicates some freedom from control. However, this fact by itself does not mean that the worker is not an employee. The importance of this factor depends on the nature of the service involved and the extent to which an employer generally would require that employees perform such services on the employer s premises. Control over the place of work is indicated when the person or persons for whom the services are performed have the right to compel the worker to travel a designated route, to canvass a territory within a certain time, or to work at specific places as required. See Rev. Ruling Services Performed in Order or Sequence Set. If a worker must perform services in the order or sequence set by the person or persons for whom the services are performed, that factor shows that the worker is not free to follow the worker s own pattern of work but must follow the established routines and schedules of the person or persons for whom the services are performed. Often, because of the nature of an occupation, the person or persons for whom the services are performed do not set the order of the services or set the order infrequently. It is sufficient to show control, however, if such person or persons retain the right to do so. See Rev. Ruling Oral or Written Reports. A requirement that the worker submit regular or written reports to the person or persons for whom the services are performed indicates a degree of control. See Rev. Ruling , C.B. 199, and Rev. Ruling , C.B Payment by Hour, Week, Month. Payment by the hour, week, or month generally points to an employer-employee relationship, provided that this method of payment is not just a convenient way of paying a lump sum agreed upon as the cost of a job. Payment made by the job or on a straight commission generally indicates that the worker is an independent contractor. See Rev. Ruling , C.B Payment of Business and/or Traveling Expenses. If the person or persons for whom the services are performed ordinarily pay the worker s business and/or traveling expenses, the worker is ordinarily an employee. An employer, to be able to control expenses, generally retains the right to regulate and direct the worker s business activities. See Rev. Ruling , C.B Furnishing of Tools and Materials. The fact that the person or persons for whom the services are performed furnish significant tools, materials, and other equipment tends to show the existence of an employer-employee relationship. See Rev. Ruling , C.B Significant Investment. If the worker invests in facilities that are used by the worker in performing services and are not typically maintained by employees (such as the maintenance of an office rented at fair value from an unrelated party), that factor tends to indicate that the worker is an independent contractor. On the other hand, lack of investment in facilities indicates dependence on the person or persons for whom the services are performed for such facilities and, accordingly, the existence of an 22 Gold Level Document: Clergy

What are the advantages of a housing allowance? 1. All the expenses for housing except food and maid service are nontaxable.

Ministers' Compensation & Housing Allowance What are the advantages of a housing allowance? 1. All the expenses for housing except food and maid service are nontaxable. 2. Everything except food and maid

Ministers' Compensation & Housing Allowance What are the advantages of a housing allowance? 1. All the expenses for housing except food and maid service are nontaxable. 2. Everything except food and maid

8/3/2016. Presented by: John L Crandell EA MBA CTRS

Presented by: John L Crandell EA MBA CTRS 1 2 1 At the end of this webinar, you should be able to: Understand what Clergy means Understand what a Housing Allowance is Be able to calculate Self Employment

Presented by: John L Crandell EA MBA CTRS 1 2 1 At the end of this webinar, you should be able to: Understand what Clergy means Understand what a Housing Allowance is Be able to calculate Self Employment

TABLE OF CONTENTS. Overview Who Qualifies for Special Tax Treatment as a Minister Income to Be Reported The Parsonage Allowance...

TABLE OF CONTENTS Overview... 1 Who Qualifies for Special Tax Treatment as a Minister... 2 Income to Be Reported... 5 The Parsonage Allowance... 6 Business Expenses... 11 Self-Employment Tax: Exemption...

TABLE OF CONTENTS Overview... 1 Who Qualifies for Special Tax Treatment as a Minister... 2 Income to Be Reported... 5 The Parsonage Allowance... 6 Business Expenses... 11 Self-Employment Tax: Exemption...

New IRS Audit Guidelines for Ministers

New IRS Audit Guidelines for Ministers In April 2009 the IRS released the new audit guidelines for ministers. Now this doesn t necessarily mean that ministers will be targets of audits in 2010 but it could

New IRS Audit Guidelines for Ministers In April 2009 the IRS released the new audit guidelines for ministers. Now this doesn t necessarily mean that ministers will be targets of audits in 2010 but it could

TAXATION OF CLERGY & OTHER CALLED WORKERS

TAXATION OF CLERGY & OTHER CALLED WORKERS January 2017 Presented by David Mellem, EA This text is written to provide accurate and authoritative information regarding the subject matter. The information

TAXATION OF CLERGY & OTHER CALLED WORKERS January 2017 Presented by David Mellem, EA This text is written to provide accurate and authoritative information regarding the subject matter. The information

Taxable income (Federal and Social Security) The following are various types of income commonly found on a priest s tax filing:

The following are various types of income commonly found on a priest s tax filing:") Diocese of Madison Policy for Priest Compensation Taxable income (Federal and Social Security) The following are various types of income commonly found on a priest s tax filing: A. Salary and Supplements

Diocese of Madison Policy for Priest Compensation Taxable income (Federal and Social Security) The following are various types of income commonly found on a priest s tax filing: A. Salary and Supplements

Minister Taxes San Jacinto Baptist Association October 2014

Minister Taxes San Jacinto Baptist Association October 2014 Minister Criteria Credential - Licensed - Commissioned or - Ordained Performance - Conduct of religious worship - Administration & maintenance

Minister Taxes San Jacinto Baptist Association October 2014 Minister Criteria Credential - Licensed - Commissioned or - Ordained Performance - Conduct of religious worship - Administration & maintenance

Bus. Admin: Ministers Tax Issues Course #E913

Bus. Admin: Ministers Tax Issues Course #E913 Presented by: Stephanie Buduhan, CPA PSK LLP 2018 Shelby Systems, Inc. Other brand and product names are trademarks or registered trademarks of the respective

Bus. Admin: Ministers Tax Issues Course #E913 Presented by: Stephanie Buduhan, CPA PSK LLP 2018 Shelby Systems, Inc. Other brand and product names are trademarks or registered trademarks of the respective

Church and Taxes. San Jacinto Baptist Association October 2014

Church and Taxes San Jacinto Baptist Association October 2014 The Affordable Care Act 1. Health FSA (flexible spending accounts) capped $2,500 2. Modified the itemized deduction for medical expenses increased

Church and Taxes San Jacinto Baptist Association October 2014 The Affordable Care Act 1. Health FSA (flexible spending accounts) capped $2,500 2. Modified the itemized deduction for medical expenses increased

Part 4. Comprehensive Example and Sample Forms Example One: Senior Minister

Part 4. Comprehensive Example and Sample Forms Example One: Senior Minister Note: This example is based on an illustrated example contained at the end of IRS Publication 517. Rev. John Michaels is the

Part 4. Comprehensive Example and Sample Forms Example One: Senior Minister Note: This example is based on an illustrated example contained at the end of IRS Publication 517. Rev. John Michaels is the

Minister Tax Law. Topics Unique to Ministers. Important Tax Cases and IRS Rulings 8/5/2015

Minister Tax Law Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation August 5, 2015 Topics Unique to Ministers Income Issue: Parsonage/Housing Allowance Gift or Compensation SE Issue:

Minister Tax Law Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation August 5, 2015 Topics Unique to Ministers Income Issue: Parsonage/Housing Allowance Gift or Compensation SE Issue:

Church and Taxes. San Jacinto Baptist Association October 2015

Church and Taxes San Jacinto Baptist Association October 2015 Updates for 2015 1. Standard mileage rate 56 cents per mile, 14 cents charity 2. $18,000 maximum contribution deferral to 403(b) or 401(k)

Church and Taxes San Jacinto Baptist Association October 2015 Updates for 2015 1. Standard mileage rate 56 cents per mile, 14 cents charity 2. $18,000 maximum contribution deferral to 403(b) or 401(k)

From the library of Dear Sir or Madam:

Internal Revenue Service SB/SE Compliance BIRSC, SS-8 Unit Release # SS8 2010020002 Release Date: 3-10-10 Index (UIL) No.: 3121.04-01 Department of the Treasury 1040 Waverly Avenue-Stop 631 Holtsville,

Internal Revenue Service SB/SE Compliance BIRSC, SS-8 Unit Release # SS8 2010020002 Release Date: 3-10-10 Index (UIL) No.: 3121.04-01 Department of the Treasury 1040 Waverly Avenue-Stop 631 Holtsville,

Part 4. Comprehensive Examples and Forms Example One: Active minister

Part 4. Comprehensive Examples and Forms Example One: Active minister Note: This example is based on an illustrated example contained at the end of IRS Publication 517. Rev. John Michaels is the minister

Part 4. Comprehensive Examples and Forms Example One: Active minister Note: This example is based on an illustrated example contained at the end of IRS Publication 517. Rev. John Michaels is the minister

JANUARY 2017 EMPLOYEE OR INDEPENDENT CONTRACTOR

JANUARY 2017 GUIDELINES TO OBLIGATIONS OF BRANCH CHURCHES AND SOCIETIES TO WITHHOLD FEDERAL INCOME AND SOCIAL SECURITY TAXES AND TO REPORT COMPENSATION; AND OTHER INFORMATION EMPLOYEE OR INDEPENDENT CONTRACTOR

JANUARY 2017 GUIDELINES TO OBLIGATIONS OF BRANCH CHURCHES AND SOCIETIES TO WITHHOLD FEDERAL INCOME AND SOCIAL SECURITY TAXES AND TO REPORT COMPENSATION; AND OTHER INFORMATION EMPLOYEE OR INDEPENDENT CONTRACTOR

CONGREGATIONAL/MINISTERIAL INCOME TAX GUIDELINES

CONGREGATIONAL/MINISTERIAL INCOME TAX GUIDELINES Updated For 2016 Tax Returns By Carl A. Hess The new year brings a reminder that tax season is also here and deserves our attention. This document is to

CONGREGATIONAL/MINISTERIAL INCOME TAX GUIDELINES Updated For 2016 Tax Returns By Carl A. Hess The new year brings a reminder that tax season is also here and deserves our attention. This document is to

Taxes and Ministers TOPICS: 2011 edition (rev. 10/11) The IRS s definition of minister. Employment status: W-2 or Housing/Parsonage allowance

The IRS s definition of minister. Employment status: W-2 or Housing/Parsonage allowance") Taxes and Ministers 2011 edition (rev. ) TOPICS: The IRS s definition of minister Employment status: W-2 or 1099 Housing/Parsonage allowance Reporting income and expenses Paying federal and state taxes

Taxes and Ministers 2011 edition (rev. ) TOPICS: The IRS s definition of minister Employment status: W-2 or 1099 Housing/Parsonage allowance Reporting income and expenses Paying federal and state taxes

Compensation and Benefits Guidelines for Lay and Clergy Employees. Revised October 2014

2015 Compensation and Benefits Guidelines for Lay and Clergy Employees Revised October 2014 Page 2 Page 3 Table of Contents INTRODUCTION... 5 COMPENSATION... 6 COMPENSATION FOR PRIESTS AND TRANSITIONAL

2015 Compensation and Benefits Guidelines for Lay and Clergy Employees Revised October 2014 Page 2 Page 3 Table of Contents INTRODUCTION... 5 COMPENSATION... 6 COMPENSATION FOR PRIESTS AND TRANSITIONAL

Ministerial Taxation

Ministerial Taxation Minister s Taxation & Reporting Ministers qualify for four special tax rules: Housing allowance exclusion Self-employed status for social security taxation Exemption from withholding

Ministerial Taxation Minister s Taxation & Reporting Ministers qualify for four special tax rules: Housing allowance exclusion Self-employed status for social security taxation Exemption from withholding

Taxes and Ministers 2012 edition (rev. 10/12)

") Taxes and Ministers 2012 edition (rev. ) TOPICS: The IRS s definition of minister Employment status: W-2 or 1099 Housing/Parsonage allowance Reporting income and expenses Paying federal and state taxes

Taxes and Ministers 2012 edition (rev. ) TOPICS: The IRS s definition of minister Employment status: W-2 or 1099 Housing/Parsonage allowance Reporting income and expenses Paying federal and state taxes

SAMPLE FEDERAL REPORTING REQUIREMENTS. for Churches. Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report

Attachment 1. Computation of expenses, allocable to tax-free ministerial income, that are nondeductible. % of Nondeductible Expenses Parsonage allowance: Taxable Tax-Free Total M inisterial retirement

Attachment 1. Computation of expenses, allocable to tax-free ministerial income, that are nondeductible. % of Nondeductible Expenses Parsonage allowance: Taxable Tax-Free Total M inisterial retirement

DETERMINATION OF EMPLOYEE STATUS. Following are the procedures to be followed to determine the status of each employee:

DETERMINATION OF EMPLOYEE STATUS Following are the procedures to be followed to determine the status of each employee: Archdiocesan Priests Priests of the Archdiocese are considered employees for federal,

DETERMINATION OF EMPLOYEE STATUS Following are the procedures to be followed to determine the status of each employee: Archdiocesan Priests Priests of the Archdiocese are considered employees for federal,

Legal and Business Issues Pertaining to Church Life

Legal and Business Issues Pertaining to Church Life There are various government entities and businesses with whom an established church will transact business on a regular basis and with whom a new church

Legal and Business Issues Pertaining to Church Life There are various government entities and businesses with whom an established church will transact business on a regular basis and with whom a new church

Frequently asked Questions: Donations. General Council of the Assemblies of God Division of the Treasury

Frequently asked Questions: Donations General Council of the Assemblies of God Division of the Treasury 1 FREQUENTLY ASKED QUESTIONS CONCERNING DONATIONS QUESTIONS ADDRESSED IN THIS PAMPHLET What are appropriate

Frequently asked Questions: Donations General Council of the Assemblies of God Division of the Treasury 1 FREQUENTLY ASKED QUESTIONS CONCERNING DONATIONS QUESTIONS ADDRESSED IN THIS PAMPHLET What are appropriate

2017 Minister s Tax Organizer Supplement

Please make a copy of this tax organizer for your records before you send to us. 2017 Minister s Tax Organizer Supplement Peachtree Tax Advisors, LLC 500 East Second Street Rome, GA 30161-3112 706-234-7468

Please make a copy of this tax organizer for your records before you send to us. 2017 Minister s Tax Organizer Supplement Peachtree Tax Advisors, LLC 500 East Second Street Rome, GA 30161-3112 706-234-7468

CLERGY TAX & BENEFITS SEMINAR. Insight Into the World of Clergy Taxes and Benefits

CLERGY TAX & BENEFITS SEMINAR Insight Into the World of Clergy Taxes and Benefits AGENDA Welcome and Prayer Introductions & Overview Clergy Compensation Clergy Benefits Other Tax Matters Q&A 2 Clergy Tax

CLERGY TAX & BENEFITS SEMINAR Insight Into the World of Clergy Taxes and Benefits AGENDA Welcome and Prayer Introductions & Overview Clergy Compensation Clergy Benefits Other Tax Matters Q&A 2 Clergy Tax

Iowa Annual Conference of the United Methodist Church Table II, Part A Church Assets Report Assets/Liabilities from January 1, to December 31,

Table II, Part A Church Assets Report Assets/Liabilities from January 1, to December 31, District Church Church # Pastor Email: Read the instructions with each line item. Round all figures to the nearest

Table II, Part A Church Assets Report Assets/Liabilities from January 1, to December 31, District Church Church # Pastor Email: Read the instructions with each line item. Round all figures to the nearest

PART 3 Step-by-Step Tax Return Preparation

PART 3 Step-by-Step Tax Return Preparation TAX FORMS AND SCHEDULES This step-by-step analysis covers these forms and schedules: Form 1040 is the basic document you will use. It summarizes all of your tax

PART 3 Step-by-Step Tax Return Preparation TAX FORMS AND SCHEDULES This step-by-step analysis covers these forms and schedules: Form 1040 is the basic document you will use. It summarizes all of your tax

Top 10 Questions that Ministers, Missionaries, and Church Treasurers Ask Tax Preparers (Updated: December 11, 2014)

") Based on our experience, the following are frequent questions asked by ministers, missionaries, church treasurers, and others serving in ministry positions as licensed or ordained ministers. Our answers

Based on our experience, the following are frequent questions asked by ministers, missionaries, church treasurers, and others serving in ministry positions as licensed or ordained ministers. Our answers

Minister Audit Technique Guide

This Guide has been reproduced from the IRS website and is provided here as a convenience. Please refer to the IRS website before relying on the information contained in this Guide, as the IRS may have

This Guide has been reproduced from the IRS website and is provided here as a convenience. Please refer to the IRS website before relying on the information contained in this Guide, as the IRS may have

Church Administration Matters

Church Administration Matters Greg Hickle Minnesota District Secretary/Treasurer Housing Allowances Housing Allowances are perhaps the most common and sometimes the least understood of the benefits that

Church Administration Matters Greg Hickle Minnesota District Secretary/Treasurer Housing Allowances Housing Allowances are perhaps the most common and sometimes the least understood of the benefits that

Federal Reporting Requirements for Churches

Federal Reporting Requirements for Churches Prepared by Richard R. Hammar, J.D., LL.M., CPA Senior Editor, CHURCH LAW & TAX REPORT Copyright 2013 Christianity Today International. Federal Reporting Requirements

Federal Reporting Requirements for Churches Prepared by Richard R. Hammar, J.D., LL.M., CPA Senior Editor, CHURCH LAW & TAX REPORT Copyright 2013 Christianity Today International. Federal Reporting Requirements

Dear Pastor & Treasurer:

Dear Pastor & Treasurer: Enclosed you will find tax information for clergy. This information will help your church to properly set salary and expense figures. As most of us know, the tax code is extremely

Dear Pastor & Treasurer: Enclosed you will find tax information for clergy. This information will help your church to properly set salary and expense figures. As most of us know, the tax code is extremely

Compensation and Benefits Guidelines for Lay and Clergy Employees

Compensation and Benefits Guidelines for Lay and Clergy Employees Page 2 Table of Contents INTRODUCTION... 4 For More Information Contact:... 4 The Episcopal Church in Minnesota... 4 COMPENSATION... 5

Compensation and Benefits Guidelines for Lay and Clergy Employees Page 2 Table of Contents INTRODUCTION... 4 For More Information Contact:... 4 The Episcopal Church in Minnesota... 4 COMPENSATION... 5

Federal Reporting Requirements for Churches

Federal Reporting Requirements for Churches Prepared by Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2014 Christianity Today International. Federal Reporting Requirements

Federal Reporting Requirements for Churches Prepared by Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2014 Christianity Today International. Federal Reporting Requirements

Accounting for Churches. Jerry L Walker, CPA

Accounting for Churches By Jerry L Walker, CPA TABLE OF CONTENTS Worker Classifications... 1 Do ministers receive special tax treatment?... 1 Who is considered a minister for tax purposes?... 1 Is a part-time

Accounting for Churches By Jerry L Walker, CPA TABLE OF CONTENTS Worker Classifications... 1 Do ministers receive special tax treatment?... 1 Who is considered a minister for tax purposes?... 1 Is a part-time

Tax Guide. for Ministers. Filing Year. The Pension Boards United Church of Christ, Inc.

The Pension Boards United Church of Christ, Inc. 2017 Filing Year Tax Guide for Ministers Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Tax Guide for

The Pension Boards United Church of Christ, Inc. 2017 Filing Year Tax Guide for Ministers Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Tax Guide for

Orthodox Church in America Tax Help for Parish Treasurers

Orthodox Church in America Tax Help for Parish Treasurers INTRODUCTION Taxes in the United States are complex and consequences for noncompliance can be significant. Furthermore, there are nuances in the

Orthodox Church in America Tax Help for Parish Treasurers INTRODUCTION Taxes in the United States are complex and consequences for noncompliance can be significant. Furthermore, there are nuances in the

Clergy Compensation Archdiocese of Baltimore Parish/School Management Training April/May 2008

Clergy Compensation Archdiocese of Baltimore Parish/School Management Training April/May 2008 Archdiocese of Baltimore ~ Parish/School Management Training Agenda 1. Tax Treatment 2. Taxable Income 3. Administrative

Clergy Compensation Archdiocese of Baltimore Parish/School Management Training April/May 2008 Archdiocese of Baltimore ~ Parish/School Management Training Agenda 1. Tax Treatment 2. Taxable Income 3. Administrative

Federal Reporting Requirements for Churches*

Federal Reporting Requirements for Churches* Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2016 Christianity Today International. Federal Reporting Requirements by

Federal Reporting Requirements for Churches* Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2016 Christianity Today International. Federal Reporting Requirements by

UNITED STATES DISTRICT COURT WESTERN DISTRICT OF WISCONSIN. V. Case No. 11-CV-626 COMPLAINT

UNITED STATES DISTRICT COURT WESTERN DISTRICT OF WISCONSIN FREEDOM FROM RELIGION FOUNDATION, INC.; ANNIE LAURIE GAYLOR; ANNE NICOL GAYLOR; and DAN BARKER, Plaintiffs, V. Case No. 11-CV-626 TIMOTHY GEITHNER,

UNITED STATES DISTRICT COURT WESTERN DISTRICT OF WISCONSIN FREEDOM FROM RELIGION FOUNDATION, INC.; ANNIE LAURIE GAYLOR; ANNE NICOL GAYLOR; and DAN BARKER, Plaintiffs, V. Case No. 11-CV-626 TIMOTHY GEITHNER,

Federal Reporting. The Pension Boards United Church of Christ, Inc.

The Pension Boards United Church of Christ, Inc. 2015 Federal Reporting Requirements for Churches Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Federal

The Pension Boards United Church of Christ, Inc. 2015 Federal Reporting Requirements for Churches Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Federal

Part 3. Step-by-Step Tax Return Preparation

Part 3. Step-by-Step Tax Return Preparation TAX FORMS AND SCHEDULES This step-by-step analysis covers these forms and schedules: Form 1040 is the basic document you will use. It summarizes all of your

Part 3. Step-by-Step Tax Return Preparation TAX FORMS AND SCHEDULES This step-by-step analysis covers these forms and schedules: Form 1040 is the basic document you will use. It summarizes all of your

Chapter 2: Housing Allowance and Parsonage

Chapter 2: Housing Allowance and Parsonage INTRODUCTION...100 ELIGIBILITY...200 HOUSING ALLOWANCE...300 Housing Allowance Income Tax Aspects...310 Tax-free Limits...320 The Designated Amount...321 Use

Chapter 2: Housing Allowance and Parsonage INTRODUCTION...100 ELIGIBILITY...200 HOUSING ALLOWANCE...300 Housing Allowance Income Tax Aspects...310 Tax-free Limits...320 The Designated Amount...321 Use

Definition of Compensation and Benefits for Rostered Ministers Sierra Pacific Synod Evangelical Lutheran Church in America

Definition of Compensation and Benefits for Rostered Ministers Sierra Pacific Synod Evangelical Lutheran Church in America 1. APPROPRIATE COMPENSATION Rostered ministers (pastors and deacons) are not always

Definition of Compensation and Benefits for Rostered Ministers Sierra Pacific Synod Evangelical Lutheran Church in America 1. APPROPRIATE COMPENSATION Rostered ministers (pastors and deacons) are not always

Oregon-Idaho Annual Conference

Oregon-Idaho Annual Conference The United Methodist Church 1505 SW 18 th Avenue Portland OR 97201 503.226.7931 1.800.593.7539 www.umoi.org W-2 Instructions and other General Tax Information Remember that

Oregon-Idaho Annual Conference The United Methodist Church 1505 SW 18 th Avenue Portland OR 97201 503.226.7931 1.800.593.7539 www.umoi.org W-2 Instructions and other General Tax Information Remember that

COMPENSATION GUIDELINES NEW YORK CONFERENCE UNITED CHURCH OF CHRIST 5575 Thompson Road DeWitt, NY

COMPENSATION GUIDELINES 2018 NEW YORK CONFERENCE UNITED CHURCH OF CHRIST 5575 Thompson Road DeWitt, NY 13214-1639 1 TABLE OF CONTENTS Introduction Section I - The Pastor Cash Salary 3 Rental or Housing

COMPENSATION GUIDELINES 2018 NEW YORK CONFERENCE UNITED CHURCH OF CHRIST 5575 Thompson Road DeWitt, NY 13214-1639 1 TABLE OF CONTENTS Introduction Section I - The Pastor Cash Salary 3 Rental or Housing

2014 COMPENSATION WORKSHEET THE PRESBYTERY OF NEW COVENANT

THE PRESBYTERY OF NEW COVENANT The 2013 Compensation Worksheet is intended to assist clerks, treasurers and pastors as they define and report income to Presbytery, the Board of Pensions and, of course,

THE PRESBYTERY OF NEW COVENANT The 2013 Compensation Worksheet is intended to assist clerks, treasurers and pastors as they define and report income to Presbytery, the Board of Pensions and, of course,

The Pastor and His Income Tax. For 2015 Tax Year. 38 th

The Pastor and His Income Tax For 2015 Tax Year Our 38 th Year Please Note You must completely fill out the Tax Data Questionnaire (green sheets). Please send your information to us as soon as possible

The Pastor and His Income Tax For 2015 Tax Year Our 38 th Year Please Note You must completely fill out the Tax Data Questionnaire (green sheets). Please send your information to us as soon as possible

Federal Reporting. The Pension Boards United Church of Christ, Inc.

The Pension Boards United Church of Christ, Inc. 2018 Federal Reporting Requirements for Churches Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Federal

The Pension Boards United Church of Christ, Inc. 2018 Federal Reporting Requirements for Churches Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Federal

2019 MINISTERIAL COMPENSATION GUIDELINES

2019 MINISTERIAL COMPENSATION GUIDELINES Vermont Conference UCC 36 North Main Street Randolph, VT 05060 vtconference@vtcucc.org www.vtcucc.org http://www.facebook.com/vermont.conference.ucc/ Updated by:

2019 MINISTERIAL COMPENSATION GUIDELINES Vermont Conference UCC 36 North Main Street Randolph, VT 05060 vtconference@vtcucc.org www.vtcucc.org http://www.facebook.com/vermont.conference.ucc/ Updated by:

ROSTERED PERSONS COMPENSATION AND BENEFITS GUIDELINES MANUAL. Upper Susquehanna Synod Evangelical Lutheran Church in America

2019 ROSTERED PERSONS COMPENSATION AND BENEFITS GUIDELINES MANUAL SECTION A Pastor s Compensation and Benefits Guidelines SECTION B Deacon s Compensation and Benefits Guidelines Upper Susquehanna Synod

2019 ROSTERED PERSONS COMPENSATION AND BENEFITS GUIDELINES MANUAL SECTION A Pastor s Compensation and Benefits Guidelines SECTION B Deacon s Compensation and Benefits Guidelines Upper Susquehanna Synod

FEDERAL REPORTING REQUIREMENTS FOR CHURCHES Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law and Tax Report

FEDERAL REPORTING REQUIREMENTS FOR CHURCHES 2014 Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law and Tax Report Federal Reporting Requirements for Churches* Richard R. Hammar, J.D., LL.M.,

FEDERAL REPORTING REQUIREMENTS FOR CHURCHES 2014 Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law and Tax Report Federal Reporting Requirements for Churches* Richard R. Hammar, J.D., LL.M.,

UNITED STATES DISTRICT COURT WESTERN DISTRICT OF WISCONSIN. v. Case No. 11-CV-626 AMENDED COMPLAINT

Case: 3:11-cv-00626-bbc Document #: 13 Filed: 01/13/12 Page 1 of 13 UNITED STATES DISTRICT COURT WESTERN DISTRICT OF WISCONSIN FREEDOM FROM RELIGION FOUNDATION, INC.; ANNIE LAURIE GAYLOR; ANNE NICOL GAYLOR;

Case: 3:11-cv-00626-bbc Document #: 13 Filed: 01/13/12 Page 1 of 13 UNITED STATES DISTRICT COURT WESTERN DISTRICT OF WISCONSIN FREEDOM FROM RELIGION FOUNDATION, INC.; ANNIE LAURIE GAYLOR; ANNE NICOL GAYLOR;

Federal Reporting. The Pension Boards United Church of Christ, Inc.

The Pension Boards United Church of Christ, Inc. 2019 Federal Reporting Requirements for Churches Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Click

The Pension Boards United Church of Christ, Inc. 2019 Federal Reporting Requirements for Churches Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Click

Letter of Agreement between Clergy and Congregation. Presenter: The Rev. Lee Powers Retired Canon to the Ordinary Diocese of New Jersey

Letter of Agreement between Clergy and Congregation Presenter: The Rev. Lee Powers Retired Canon to the Ordinary Diocese of New Jersey Letters of Agreement Topics explored in this workshop: - Purpose and

Letter of Agreement between Clergy and Congregation Presenter: The Rev. Lee Powers Retired Canon to the Ordinary Diocese of New Jersey Letters of Agreement Topics explored in this workshop: - Purpose and

Example Two: Retired Minister

Example Two: Retired Minister Form 1040 Rev. William K. Green is a retired minister. He is 69 years old. He is married to Sarah J. Green. She is 65 years old and is also retired. For 2010, Rev. Green received

Example Two: Retired Minister Form 1040 Rev. William K. Green is a retired minister. He is 69 years old. He is married to Sarah J. Green. She is 65 years old and is also retired. For 2010, Rev. Green received

THE PRESBYTERY OF ELIZABETH Compensation Committee of the Committee on Ministry Recommendations regarding Compensation for 2015.