Church and Taxes. San Jacinto Baptist Association October 2015

|

|

|

- August Lyons

- 5 years ago

- Views:

Transcription

1 Church and Taxes San Jacinto Baptist Association October 2015

2 Updates for Standard mileage rate 56 cents per mile, 14 cents charity 2. $18,000 maximum contribution deferral to 403(b) or 401(k) plan 3. $6,000 catch-up limit for contributions deferral to 403(b) or 401(k) age 50 or older 4. Personal exemption $4,000 each individual, with phaseouts 5. Standard deduction $12,600 for joint returns $6,300 for filing single and married filing separately 6. Tax brackets 10%, 15%, 25%, 28%, 33%, 35% & 39.6%

3 Minister Criteria Five key questions 1. Is the person ordained, licensed, commissioned? 2. Does the person administer ordinances (Sacerdotal functions) i.e. baptism and the Lord s Supper? 3. Does the person conduct religious worship? 4. Does the person have management responsibilities in the church? 5. Is the person considered to be a religious leader by the church?

4 Minister Credentials General Rule Ministry begins with ordination Exception for Licensed Minister - who has been granted authority to perform substantially all the religious functions of an ordained minister - Marriages - Funerals - Baptisms - Communion - Preaching - Teaching

5 Unique Tax Issues for Ministers Ministers have a dual tax status 1. Employee for IRS purposes (W-2) 2. Self-Employed for Social Security (SECA) - file form SE on never ever never ever withhold social security - IRC Sec 3121 states that ministers wages are not wages for FICA

6 Unique Tax Provisions for Ministers 1. Eligible for housing allowance exclusion IRC Sec Self-employed status for Social Security IRC Sec 1402(c) 3. Exemption from mandatory income tax withholding IRC Sec 1401(a)(9) 4. Voluntary income tax withholding Reg (p)-1 5. Exemption for Social Security coverage IRC Sec 1402(e) (very limited circumstances) 6. Double dipping benefit for deducting mortgage interest and real estate taxes as itemized deductions (Schedule A) and inclusion in housing allowance computation

7 Minister Housing Available only to those meet the IRS criteria for Minister Must be the lesser of: - Fair rental value of similar furnished house - Amount designated - Actual housing expense incurred Exempt from Federal Income taxes Taxable as Self-employment income (Social Security)

8 Minister Housing Must be designated by the employer/payer (the church) and Must be designated in advance of being paid and Must be designated in writing Can be amended during the year => amendment is only effective on a prospective bases Responsibility falls on the minister to notify the church of any inaccurate estimates for changes

9 Qualified Housing Expense Down Payment on home Mortgage payment (principal & interest) Rental payment Real estate taxes Homeowners insurance Utilities ( gas. Electricity, water, sewerage/trash, telephone, cable/satellite) Furnishings and appliances Repairs and remodeling Yard care/landscape Maintenance items (cleaners, light bulbs, pest control, etc) HOA dues Not Maid services Not food

10 Housing Form Housing Allowance Designation I hereby designate the following expenses for housing allowance shall apply to calendar year 2013 and all future years unless otherwise changed. Item Amount 1 Down payment on a home $ 2 Mortgage payments on a loan to purchase or improve your home (include principal and interest) $ 3 Monthly Rental 4 Real Estate taxes $ 5 Home Owners Insurance $ 6 Utilities (electricity, gas, water, trash pickup, local telepone charges) $ 7Furnishings and appliances (purchase and repair) $ 8 Structural repairs and remodeling $ 9 Yard maintenance and improvements $ 10 Maintenance items (pest control, etc.) $ 11 HOA dues $ 12 Miscellaneous $ $ $ $ $ $ $ Total Expenses: $ Signature: Date: Company Officer signature: Date:

11 Compensation Base salary/wages Personal portion of cell phones Bonuses Life insurance outside of group plan Reimbursement for portion of SE tax Special occasion gifts Incentive compensation Severance pay Below market loans Gift Cards Noncash Gifts Travel advances without subsequent documentation Reimbursements through a nonaccountable reimbursement plan Travel for spouses & family Forgiveness of minister s debt to the church. Personal use of employer provided auto Payment of auto expenses Auto allowances

12 Write It Down!!!!! Compensation packages should be approved by a governing body of the church and documented noting the date it was approved and who approved it. For certain persons, the church must also document the outside sources used to determine reasonable compensation.

13 Fringe Benefits Nontaxable - Normally Housing Allowance Contributions to Qualified Retirement Plans Health Insurance Premiums (group plan provided) Employer provided room and board (for the convenience of the employer) Reimbursements under an accountable plan Taxable - Maybe???? Group term life insurance ($50,000 and greater taxable) Payment of out of pocket medical expenses (Sec 125, MSA s) Dependent Care plan Tuition assistance plan Benefits provided through a cafeteria plan Employer provided auto personal use always taxable

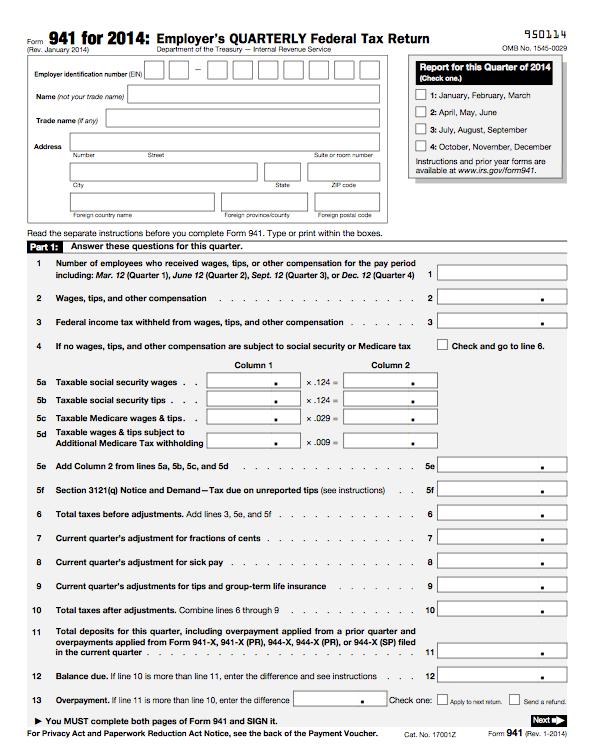

14 Payroll - Reporting It Right Form 941- Quarterly Reporting Taxable items are included on the quarterly reports Minister s housing allowance is never included since it is not taxable Should always reconcile with ledgers

15

16 Payroll - Reporting It Right W-2 Annual Reporting Taxable items included along with appropriate taxes that have been withheld Special reporting required for certain benefits and forms of compensation in Box 12 - Dependent care - Elective deferrals into retirement plans - Value of employer provided health insurance benefits required to be disclosed Housing allowance can be reported in Box 14, but not mandatory. Should never ever be included anywhere else on W-2

17 Payroll - Reporting It Right

18 Payroll - Reporting It Right

19 Payroll - Reporting It Right Form Misc Report payments of $600 or more to nonemployees for personal services rendered Exceptions - Corporations unless attorney fees - Payments to vendors for merchandise Penalties apply if church doesn t send 1099 s Due to the payee by January 31, 2016 Due to the Social Security Adm by February 29, 2016

20 Payroll - Reporting It Right

21 Employee or Independent Contractor Tax Court s 8 Factor Test 1. Degree of control exercised by employer over details of work 2. Which party invest in facilities used in work 3. Opportunity of individual to profit or loss 4. Whether employer has right to discharge the worker 5. Whether the work is part of employer s regular business 6. Permanency of relationship 7. Relationship the parties believe they are creating 8. Provision of benefits typical to those provided to employees

22 Employee or Independent Contractor Degree of control over the worker IRS 20 Factor Test 1. Training 2. Integration services integrated into church operations 3. Services rendered personally 4. Hiring, supervising or paying assistants 5. Instruction 6. Continuing relationship 7. Setting hours or work 8. Full time required 9. Working on employers premises 10. Order or sequence of work 11. Oral or written reports

23 Employee or Independent Contractor Degree of control over the worker IRS 20 Factor Test - cont 12. Payments by hour, week, or month 13. Payment of business expenses 14. Furnish tools or materials 15. Significant investment church furnish all necessary facilities 16. Realization of profit or loss 17. Working for more than one org at a time 18. Making services available to general public 19. Right to discharge 20. Right to resign

24 Correction options A. Voluntary Classification Settlement Program - allows qualifying employers to reclassify workers from independent contractor to employees by paying a small amount representing potential taxes from prior years. 1. Qualifying employer 2. Procedure must be presently treating the workers as nonemployees must have filed all Forms 1099-Misc for 3 prior calendar years consistently treated the workers as nonemployees not currently under examination for this issue by the IRS, DOL, or any state employment agencies. employer must file Form 8952 at least 60 days prior to the effective date of the reclassification reclassify on January 1, 2016 must be filed by November 2, 2015 must pay the taxes assessed on Form 8952 tax works is approximately 1% of the total wages paid for recently completed tax year not currently under examination for this issue by the IRS, DOL, or any state employment agencies. 3. Prior Tax Assessments IRS agrees not to assess any additional payroll taxes for the open years prior to the reclassification for the workers reclassified

25 Texas State Taxes Texas Tax Code provides tax exemptions for religious organizations for sales tax, hotel occupancy tax and franchise. Requirements - Organized group of people, - Regularly meeting at a particular location with an established congregation, - conducting and sponsoring religious worship services according to rites of their sect. File Texas Application for Exemption Religious Organizations Form AP This is not an exemption from collecting sales tax.

26 Texas Sales & Use Tax Churches that have received a letter of sales tax exemption do not pay sales tax on items bought, leased or rented if the items are necessary to the exempt function. To claim exemption use Texas Sales and Use Tax Exemption Certificate provide to retailer. Retailers not required by law to honor the exemption. - Seller to provide a completed Assignment of Right to Refund, then request a refund directly from Comptroller. Items purchased tax free cannot be used by employee or individual for personal benefit. Does not include purchase or use of motor vehicle. Remember => exemption from tax is for purchases not for sales. Exempt organizations must get a sales tax permit and collect and remit sales tax for all taxable items it sales.

27 Tax-Free Sales Meals and Food Products (including candy & soft drinks) if sold by churches or at church functions conducted under the authority of a church Annual banquets and suppers provided - It is not professionally catered; - Not held at a restaurant, hotel or similar place; - Not in competition with a retailer required to collect tax; - Food is prepared, served and sold by members of the church. Auctions, Rummage sales & other Fundraisers - Exempt orgs can hold two one-day tax-free sales Periodicals and writings are tax exempt if published and distributed by a religious or 501(c)(3).

28 Two One-day Tax-Free Sales Exempt orgs not required to collect tax. Does not apply to items sold for more than $5,000. Counted as 24 consecutive hours Designated day is either the day the vendor delivers the items or the day the organization delivers the items to customers. - Church selling cook books may accept pre-orders without collecting tax if the day the cookbooks will be delivered is designated tax-free day. - Surplus cook books sold during the same day qualify as tax-free. Surplus cook books sold on other days will be subject to tax.

29 Charitable Contribution What is it As defined by IRC Sec 170 A gift of cash or property Given before the end of the year Unconditional Without personal benefit to the donor Made to or for the use of the qualified charity Properly substantiated

30 Never Deductible Donated Services - Value of personal services is not deductible member who donates labor may not deduct value of the labor Contributions of less than donor s entire interest in the property a. contribution of irrevocable remainder interest in personal residence or farm b. contribution of undivided interest in property c. contribution of irrevocable remainder interest in property to a charitable remainder trust

31 Noncash Contributions Transportation Equipment Cars, Boats, things that go a. must provide a Form 1098-C b. must be attached to donor s tax return c. must be issued to donor within 30 days of the date of the sale or donation to the church d. must be filed with the IRS by February 29th Clothing & Household Goods a. must be in good condition b. no contribution for old & worn out items

32 Quid Pro Quo Contributions Contributions that include a product or service a. Contributions greater than $75 must be issued a receipt b. Receipt must include a good faith estimate of the fair value of the item given/received c. Penalties $10 per contribution not properly receipted d. If value is less than $9.60, contribution is fully deductible

33 Substantiation and Disclosure Requirements Gift of $250 or more - Must be in writing - Name donor - Itemize date and amount of each donation $250 or more - Provide the value of any goods or services received by the donor in return for the contribution - Must include the following language on the statement No goods or services were provided in exchange for the contributions, except for intangible religious benefits - Furnished contemporaneously to the donor Note: It is the donor s responsibility, not the church, to obtain the contribution statement

34 Substantiation and Disclosure Requirements Non cash contributions acknowledgement - Must be in writing - Name donor - Date of gift - Description of property or gift given - Never ever state a value or amount of the gift (this is the donor s responsibility) - Provide the value of any goods or services received by the donor in return for the contribution - Must include the following language on the statement No goods or services were provided in exchange for the contributions, except for intangible religious benefits - Furnished contemporaneously to the donor Note: It is the donor s responsibility, not the church, to obtain the contribution statement

35 Reimbursement Plans Accountable Plans - Must be written - Reimbursement is not taxable - Not reportable on W-2 Nonaccountable Plans - Reimbursement is taxable - Reportable as wages on W-2

36 Accountable Plans Requirements 1. Reimbursements are made only with adequate substantiation. 2. Written evidence required for all expenses, and receipts are required for expenses of $75 or more. 3. Receipts must substantiate the amount, date, place and business nature of each expense. 4. Expenses must be substantiated and excess reimbursements returned to the church within a reasonable period of time. - no more than 60 days after expense incurred - excess reimbursement no later than 120 days from payment Reimbursements are not made out of salary reductions - reimbursement of expenses comes out of employers fund not by reducing employees salary

37 NonAccountable Expense Plans 1. Any sort of plan that does not require an accounting 2. A plan that is deemed to not be timely carried out 3. Netting arrangement - Pastor receives $1,000 each week. Finance committee tells pastor that if he turns in his business expenses each week, then he can split the payment into part business expense and part salary payment. All of $1,000 is taxable.

38 Advantages of Accountable Plans 1. Avoids the reimbursement being includable as taxable income 2. Avoids employee losing deduction because of standard deduction 3. Eliminates loss of itemized deduction due to 2% floor on miscellaneous deductions 4. Avoids 50% deduction for meal and entertainment expenses 5. Avoids reduction to Deason rule

39 Disadvantages of Accountable Plans 1. Employee keeps detailed expense records - Documentation falls on employees shoulders 2. Plan cannot be considered part of compensation package 3. Church has full authority to deny reimbursements for unsubstantiated expenses 4. Amount budgeted is not payable unless expense is incurred and substantiated to the church

40 Examples of Business Expenses Transportation Travel Entertainment Books and subscriptions Educational Cell Phones

41 IRS Resources Telephone Numbers: General Information Tax Forms and Publications Status of Refund Web Site: Publications: Pub 15 Circular E, Employer s Tax Guide Pub 15-A Employer s Supplemental Tax Guide Pub 15-B Employer s Tax Guide to Fringe Benefits Pub 463 Travel, Entertainment, & Auto Expenses Pub 517 Social Security and Other Information for Clergy Pub 526 Charitable Contributions Pub 1771 Charitable Contributions Substantiation & Disclosure Pub 571 Tax-Sheltered Annuity Plans (403(b) plans) Pub 1828 Tax Guide for Churches and Religious Organizations

42 Other Resources Other Publications GuideStone Financial - Ministers Tax Guide Church & Clergy Tax Guide - Richard Hammer Minister s Tax & Financial Guide Dan Busby Church Law & Tax Report Church Finance Today Web Sites: Christian Ministry Resources NACBA Evangelical Council of Financial Accountability (ECFA)

43 Thank you Randy Reid, CPA

Church and Taxes. San Jacinto Baptist Association October 2014

Church and Taxes San Jacinto Baptist Association October 2014 The Affordable Care Act 1. Health FSA (flexible spending accounts) capped $2,500 2. Modified the itemized deduction for medical expenses increased

Church and Taxes San Jacinto Baptist Association October 2014 The Affordable Care Act 1. Health FSA (flexible spending accounts) capped $2,500 2. Modified the itemized deduction for medical expenses increased

Minister Taxes San Jacinto Baptist Association October 2014

Minister Taxes San Jacinto Baptist Association October 2014 Minister Criteria Credential - Licensed - Commissioned or - Ordained Performance - Conduct of religious worship - Administration & maintenance

Minister Taxes San Jacinto Baptist Association October 2014 Minister Criteria Credential - Licensed - Commissioned or - Ordained Performance - Conduct of religious worship - Administration & maintenance

8/3/2016. Presented by: John L Crandell EA MBA CTRS

Presented by: John L Crandell EA MBA CTRS 1 2 1 At the end of this webinar, you should be able to: Understand what Clergy means Understand what a Housing Allowance is Be able to calculate Self Employment

Presented by: John L Crandell EA MBA CTRS 1 2 1 At the end of this webinar, you should be able to: Understand what Clergy means Understand what a Housing Allowance is Be able to calculate Self Employment

Top 10 Questions that Ministers, Missionaries, and Church Treasurers Ask Tax Preparers (Updated: December 11, 2014)

") Based on our experience, the following are frequent questions asked by ministers, missionaries, church treasurers, and others serving in ministry positions as licensed or ordained ministers. Our answers

Based on our experience, the following are frequent questions asked by ministers, missionaries, church treasurers, and others serving in ministry positions as licensed or ordained ministers. Our answers

CONGREGATIONAL/MINISTERIAL INCOME TAX GUIDELINES

CONGREGATIONAL/MINISTERIAL INCOME TAX GUIDELINES Updated For 2016 Tax Returns By Carl A. Hess The new year brings a reminder that tax season is also here and deserves our attention. This document is to

CONGREGATIONAL/MINISTERIAL INCOME TAX GUIDELINES Updated For 2016 Tax Returns By Carl A. Hess The new year brings a reminder that tax season is also here and deserves our attention. This document is to

SAMPLE FEDERAL REPORTING REQUIREMENTS. for Churches. Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report

Attachment 1. Computation of expenses, allocable to tax-free ministerial income, that are nondeductible. % of Nondeductible Expenses Parsonage allowance: Taxable Tax-Free Total M inisterial retirement

Attachment 1. Computation of expenses, allocable to tax-free ministerial income, that are nondeductible. % of Nondeductible Expenses Parsonage allowance: Taxable Tax-Free Total M inisterial retirement

Frequently asked Questions: Donations. General Council of the Assemblies of God Division of the Treasury

Frequently asked Questions: Donations General Council of the Assemblies of God Division of the Treasury 1 FREQUENTLY ASKED QUESTIONS CONCERNING DONATIONS QUESTIONS ADDRESSED IN THIS PAMPHLET What are appropriate

Frequently asked Questions: Donations General Council of the Assemblies of God Division of the Treasury 1 FREQUENTLY ASKED QUESTIONS CONCERNING DONATIONS QUESTIONS ADDRESSED IN THIS PAMPHLET What are appropriate

Federal Reporting Requirements for Churches

Federal Reporting Requirements for Churches Prepared by Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2014 Christianity Today International. Federal Reporting Requirements

Federal Reporting Requirements for Churches Prepared by Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2014 Christianity Today International. Federal Reporting Requirements

Financial Best Practices for Congregations

Financial Best Practices for Congregations Separation of Financial Duties Keep written policies and procedures for key responsibilities (not person specific, but duty specific) Avoid conflicts of interest

Financial Best Practices for Congregations Separation of Financial Duties Keep written policies and procedures for key responsibilities (not person specific, but duty specific) Avoid conflicts of interest

PAYROLL & RELATED TAX ISSUES. Bruce A. Beyler, CPA

PAYROLL & RELATED TAX ISSUES Bruce A. Beyler, CPA Index of Topics u u u Worker Classification Compensation Fringe Benefits u Some New Items for 2016 u u u u Wage & Tax Statement (Form W-2) and Box 12 Codes

PAYROLL & RELATED TAX ISSUES Bruce A. Beyler, CPA Index of Topics u u u Worker Classification Compensation Fringe Benefits u Some New Items for 2016 u u u u Wage & Tax Statement (Form W-2) and Box 12 Codes

TABLE OF CONTENTS. Overview Who Qualifies for Special Tax Treatment as a Minister Income to Be Reported The Parsonage Allowance...

TABLE OF CONTENTS Overview... 1 Who Qualifies for Special Tax Treatment as a Minister... 2 Income to Be Reported... 5 The Parsonage Allowance... 6 Business Expenses... 11 Self-Employment Tax: Exemption...

TABLE OF CONTENTS Overview... 1 Who Qualifies for Special Tax Treatment as a Minister... 2 Income to Be Reported... 5 The Parsonage Allowance... 6 Business Expenses... 11 Self-Employment Tax: Exemption...

Federal Reporting Requirements for Churches*

Federal Reporting Requirements for Churches* Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2016 Christianity Today International. Federal Reporting Requirements by

Federal Reporting Requirements for Churches* Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2016 Christianity Today International. Federal Reporting Requirements by

CLERGY TAX & BENEFITS SEMINAR. Insight Into the World of Clergy Taxes and Benefits

CLERGY TAX & BENEFITS SEMINAR Insight Into the World of Clergy Taxes and Benefits AGENDA Welcome and Prayer Introductions & Overview Clergy Compensation Clergy Benefits Other Tax Matters Q&A 2 Clergy Tax

CLERGY TAX & BENEFITS SEMINAR Insight Into the World of Clergy Taxes and Benefits AGENDA Welcome and Prayer Introductions & Overview Clergy Compensation Clergy Benefits Other Tax Matters Q&A 2 Clergy Tax

New IRS Audit Guidelines for Ministers

New IRS Audit Guidelines for Ministers In April 2009 the IRS released the new audit guidelines for ministers. Now this doesn t necessarily mean that ministers will be targets of audits in 2010 but it could

New IRS Audit Guidelines for Ministers In April 2009 the IRS released the new audit guidelines for ministers. Now this doesn t necessarily mean that ministers will be targets of audits in 2010 but it could

Planning Guide. Compensation. V isit. For ministers and church employees. BudgetResources

Compensation Planning Guide V isit www.guidestone.org/ BudgetResources to view this material online along with our other helpful resources. For ministers and church employees Three things you need to know

Compensation Planning Guide V isit www.guidestone.org/ BudgetResources to view this material online along with our other helpful resources. For ministers and church employees Three things you need to know

Letter of Agreement between Clergy and Congregation. Presenter: The Rev. Lee Powers Retired Canon to the Ordinary Diocese of New Jersey

Letter of Agreement between Clergy and Congregation Presenter: The Rev. Lee Powers Retired Canon to the Ordinary Diocese of New Jersey Letters of Agreement Topics explored in this workshop: - Purpose and

Letter of Agreement between Clergy and Congregation Presenter: The Rev. Lee Powers Retired Canon to the Ordinary Diocese of New Jersey Letters of Agreement Topics explored in this workshop: - Purpose and

Handling Financial Matters in the Congregation

Handling Financial Matters in the Congregation Separation of Financial Duties Written policies and procedures for key responsibilities (not person specific) Avoiding conflicts of Interest Handling/recording

Handling Financial Matters in the Congregation Separation of Financial Duties Written policies and procedures for key responsibilities (not person specific) Avoiding conflicts of Interest Handling/recording

Accounting for Churches. Jerry L Walker, CPA

Accounting for Churches By Jerry L Walker, CPA TABLE OF CONTENTS Worker Classifications... 1 Do ministers receive special tax treatment?... 1 Who is considered a minister for tax purposes?... 1 Is a part-time

Accounting for Churches By Jerry L Walker, CPA TABLE OF CONTENTS Worker Classifications... 1 Do ministers receive special tax treatment?... 1 Who is considered a minister for tax purposes?... 1 Is a part-time

Compensation Guidelines

Compensation Guidelines For Rostered Leaders: Ordained Ministers, Associates in Ministry, Deaconesses, and Diaconal Ministers 2016 New England Synod Evangelical Lutheran Church in America Endorsed by Synod

Compensation Guidelines For Rostered Leaders: Ordained Ministers, Associates in Ministry, Deaconesses, and Diaconal Ministers 2016 New England Synod Evangelical Lutheran Church in America Endorsed by Synod

JANUARY 2017 EMPLOYEE OR INDEPENDENT CONTRACTOR

JANUARY 2017 GUIDELINES TO OBLIGATIONS OF BRANCH CHURCHES AND SOCIETIES TO WITHHOLD FEDERAL INCOME AND SOCIAL SECURITY TAXES AND TO REPORT COMPENSATION; AND OTHER INFORMATION EMPLOYEE OR INDEPENDENT CONTRACTOR

JANUARY 2017 GUIDELINES TO OBLIGATIONS OF BRANCH CHURCHES AND SOCIETIES TO WITHHOLD FEDERAL INCOME AND SOCIAL SECURITY TAXES AND TO REPORT COMPENSATION; AND OTHER INFORMATION EMPLOYEE OR INDEPENDENT CONTRACTOR

Compensation Guidelines

Compensation Guidelines For Rostered Ministers: Pastors and Deacons 2018 New England Synod Evangelical Lutheran Church in America Proposal to Synod Assembly June 2017 As approved by Synod Council on April

Compensation Guidelines For Rostered Ministers: Pastors and Deacons 2018 New England Synod Evangelical Lutheran Church in America Proposal to Synod Assembly June 2017 As approved by Synod Council on April

FEDERAL REPORTING REQUIREMENTS FOR CHURCHES Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law and Tax Report

FEDERAL REPORTING REQUIREMENTS FOR CHURCHES 2014 Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law and Tax Report Federal Reporting Requirements for Churches* Richard R. Hammar, J.D., LL.M.,

FEDERAL REPORTING REQUIREMENTS FOR CHURCHES 2014 Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law and Tax Report Federal Reporting Requirements for Churches* Richard R. Hammar, J.D., LL.M.,

2011 Tax Return Preparation

2011 Tax Return Preparation and Federal Reporting Guide Tax Guide for 2010 Returns for Ministers Prepared by Richard R. Hammar, J.D., LL.M., CPA Edited by GuideStone Financial Resources of the Southern

2011 Tax Return Preparation and Federal Reporting Guide Tax Guide for 2010 Returns for Ministers Prepared by Richard R. Hammar, J.D., LL.M., CPA Edited by GuideStone Financial Resources of the Southern

Taxable income (Federal and Social Security) The following are various types of income commonly found on a priest s tax filing:

The following are various types of income commonly found on a priest s tax filing:") Diocese of Madison Policy for Priest Compensation Taxable income (Federal and Social Security) The following are various types of income commonly found on a priest s tax filing: A. Salary and Supplements

Diocese of Madison Policy for Priest Compensation Taxable income (Federal and Social Security) The following are various types of income commonly found on a priest s tax filing: A. Salary and Supplements

Financial Controls, Policies and Procedures

Church Funds, A Trust: A Legal Note Financial Controls, Policies and Procedures Church income ordinarily consists of designated and undesignated contributions, interest on bank accounts, gain on investments,

Church Funds, A Trust: A Legal Note Financial Controls, Policies and Procedures Church income ordinarily consists of designated and undesignated contributions, interest on bank accounts, gain on investments,

2017 Year-End Tax Memo

2017 Year-End Tax Memo An Annual Publication of Large & Gilbert, Inc. January 2018 Large & Gilbert, Inc., is a full service CPA firm specializing in Accounting, Tax, Consulting, Business Advisory, Wealth

2017 Year-End Tax Memo An Annual Publication of Large & Gilbert, Inc. January 2018 Large & Gilbert, Inc., is a full service CPA firm specializing in Accounting, Tax, Consulting, Business Advisory, Wealth

Part 3. Step-by-Step Tax Return Preparation

Part 3. Step-by-Step Tax Return Preparation TAX FORMS AND SCHEDULES This step-by-step analysis covers these forms and schedules: Form 1040 is the basic document you will use. It summarizes all of your

Part 3. Step-by-Step Tax Return Preparation TAX FORMS AND SCHEDULES This step-by-step analysis covers these forms and schedules: Form 1040 is the basic document you will use. It summarizes all of your

Clergy ************************************************************************

Clergy Contents In this webinar, the student will learn the tax treatment of income received by a minister. Objectives After completing this webinar, the student will be able to: Determine if clergy are

Clergy Contents In this webinar, the student will learn the tax treatment of income received by a minister. Objectives After completing this webinar, the student will be able to: Determine if clergy are

Federal Reporting Requirements for Churches

Federal Reporting Requirements for Churches Prepared by Richard R. Hammar, J.D., LL.M., CPA Senior Editor, CHURCH LAW & TAX REPORT Copyright 2013 Christianity Today International. Federal Reporting Requirements

Federal Reporting Requirements for Churches Prepared by Richard R. Hammar, J.D., LL.M., CPA Senior Editor, CHURCH LAW & TAX REPORT Copyright 2013 Christianity Today International. Federal Reporting Requirements

1099 LETTER REPEAL OF NEW INFORMATION REPORTING REQUIREMENTS INSIDE THIS ISSUE:

DECEMBER 2011 INSIDE THIS ISSUE: Repeal of New Information Reporting Requirements IRS Voluntary Classification Settlement Program California s New Penalties for Misclassifying Employees as Independent

DECEMBER 2011 INSIDE THIS ISSUE: Repeal of New Information Reporting Requirements IRS Voluntary Classification Settlement Program California s New Penalties for Misclassifying Employees as Independent

Ministerial Taxation

Ministerial Taxation Minister s Taxation & Reporting Ministers qualify for four special tax rules: Housing allowance exclusion Self-employed status for social security taxation Exemption from withholding

Ministerial Taxation Minister s Taxation & Reporting Ministers qualify for four special tax rules: Housing allowance exclusion Self-employed status for social security taxation Exemption from withholding

Compensation Guidelines

Compensation Guidelines For Rostered Ministers: Pasrs and Deacons 2019 New England Synod Evangelical Lutheran Church in America Approved by Synod Assembly June 2018 Introduction Let the elders who rule

Compensation Guidelines For Rostered Ministers: Pasrs and Deacons 2019 New England Synod Evangelical Lutheran Church in America Approved by Synod Assembly June 2018 Introduction Let the elders who rule

Clergy Compensation Archdiocese of Baltimore Parish/School Management Training April/May 2008

Clergy Compensation Archdiocese of Baltimore Parish/School Management Training April/May 2008 Archdiocese of Baltimore ~ Parish/School Management Training Agenda 1. Tax Treatment 2. Taxable Income 3. Administrative

Clergy Compensation Archdiocese of Baltimore Parish/School Management Training April/May 2008 Archdiocese of Baltimore ~ Parish/School Management Training Agenda 1. Tax Treatment 2. Taxable Income 3. Administrative

Part 4. Comprehensive Examples and Forms Example One: Active minister

Part 4. Comprehensive Examples and Forms Example One: Active minister Note: This example is based on an illustrated example contained at the end of IRS Publication 517. Rev. John Michaels is the minister

Part 4. Comprehensive Examples and Forms Example One: Active minister Note: This example is based on an illustrated example contained at the end of IRS Publication 517. Rev. John Michaels is the minister

Federal Reporting. The Pension Boards United Church of Christ, Inc.

The Pension Boards United Church of Christ, Inc. 2019 Federal Reporting Requirements for Churches Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Click

The Pension Boards United Church of Christ, Inc. 2019 Federal Reporting Requirements for Churches Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Click

Bus. Admin: Ministers Tax Issues Course #E913

Bus. Admin: Ministers Tax Issues Course #E913 Presented by: Stephanie Buduhan, CPA PSK LLP 2018 Shelby Systems, Inc. Other brand and product names are trademarks or registered trademarks of the respective

Bus. Admin: Ministers Tax Issues Course #E913 Presented by: Stephanie Buduhan, CPA PSK LLP 2018 Shelby Systems, Inc. Other brand and product names are trademarks or registered trademarks of the respective

Orthodox Church in America Tax Help for Parish Treasurers

Orthodox Church in America Tax Help for Parish Treasurers INTRODUCTION Taxes in the United States are complex and consequences for noncompliance can be significant. Furthermore, there are nuances in the

Orthodox Church in America Tax Help for Parish Treasurers INTRODUCTION Taxes in the United States are complex and consequences for noncompliance can be significant. Furthermore, there are nuances in the

MEMO #3. Tax and Reporting Procedures for Congregations. Pensions and Benefits USA. Caution! Determine employee classifications accurately.

MEMO #3 Tax and Reporting Procedures for Congregations Pensions and Benefits USA The tax and reporting requirements with which churches must comply often seem to complicate the task of the local church

MEMO #3 Tax and Reporting Procedures for Congregations Pensions and Benefits USA The tax and reporting requirements with which churches must comply often seem to complicate the task of the local church

Federal Reporting. The Pension Boards United Church of Christ, Inc.

The Pension Boards United Church of Christ, Inc. 2015 Federal Reporting Requirements for Churches Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Federal

The Pension Boards United Church of Christ, Inc. 2015 Federal Reporting Requirements for Churches Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Federal

Federal Reporting. The Pension Boards United Church of Christ, Inc.

The Pension Boards United Church of Christ, Inc. 2018 Federal Reporting Requirements for Churches Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Federal

The Pension Boards United Church of Christ, Inc. 2018 Federal Reporting Requirements for Churches Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Federal

PARENT ORGANIZATIONS TAX FILING REQUIREMENTS

PARENT ORGANIZATIONS TAX FILING REQUIREMENTS Leland Dushkin, CPA Tax Manager Hereford, Lynch, Sellars & Kirkham, PC ldushkin@hlsk.com 1406 Wilson Road, Suite 100 Conroe, TX 77304 936-756-8127 or 936-441-1338

PARENT ORGANIZATIONS TAX FILING REQUIREMENTS Leland Dushkin, CPA Tax Manager Hereford, Lynch, Sellars & Kirkham, PC ldushkin@hlsk.com 1406 Wilson Road, Suite 100 Conroe, TX 77304 936-756-8127 or 936-441-1338

Moving Expenses. Unreimbursed Business Expenses. Became effective January 1, 2018

Became effective January 1, 2018 Moving Expenses Prior law generally deductible, or a non-taxable reimbursement by an employer New law No longer deductible and taxable if paid for or reimbursed by an employer

Became effective January 1, 2018 Moving Expenses Prior law generally deductible, or a non-taxable reimbursement by an employer New law No longer deductible and taxable if paid for or reimbursed by an employer

PART 3 Step-by-Step Tax Return Preparation

PART 3 Step-by-Step Tax Return Preparation TAX FORMS AND SCHEDULES This step-by-step analysis covers these forms and schedules: Form 1040 is the basic document you will use. It summarizes all of your tax

PART 3 Step-by-Step Tax Return Preparation TAX FORMS AND SCHEDULES This step-by-step analysis covers these forms and schedules: Form 1040 is the basic document you will use. It summarizes all of your tax

2018 Compensation Policy

Summary 2018 Compensation Policy It is the policy of Newark Presbytery that its member churches shall provide equitable compensation of pastors and shall meet or exceed the minimum amounts specified for

Summary 2018 Compensation Policy It is the policy of Newark Presbytery that its member churches shall provide equitable compensation of pastors and shall meet or exceed the minimum amounts specified for

Exempt Organizations: Sales and Purchases

Exempt Organizations: Sales and Purchases Susan Combs, Texas Comptroller of Public Accounts NOVEMBER 2012 Organizations that have applied for and received a letter of exemption from sales tax don t have

Exempt Organizations: Sales and Purchases Susan Combs, Texas Comptroller of Public Accounts NOVEMBER 2012 Organizations that have applied for and received a letter of exemption from sales tax don t have

TAXATION OF CLERGY & OTHER CALLED WORKERS

TAXATION OF CLERGY & OTHER CALLED WORKERS January 2017 Presented by David Mellem, EA This text is written to provide accurate and authoritative information regarding the subject matter. The information

TAXATION OF CLERGY & OTHER CALLED WORKERS January 2017 Presented by David Mellem, EA This text is written to provide accurate and authoritative information regarding the subject matter. The information

Financial Controls, Policies and Procedures

Financial Controls, Policies and Procedures Church Funds, A Trust: A Legal Note Church income ordinarily consists of designated and undesignated contributions, interest on bank accounts, gain on investments,

Financial Controls, Policies and Procedures Church Funds, A Trust: A Legal Note Church income ordinarily consists of designated and undesignated contributions, interest on bank accounts, gain on investments,

2014 COMPENSATION WORKSHEET THE PRESBYTERY OF NEW COVENANT

THE PRESBYTERY OF NEW COVENANT The 2013 Compensation Worksheet is intended to assist clerks, treasurers and pastors as they define and report income to Presbytery, the Board of Pensions and, of course,

THE PRESBYTERY OF NEW COVENANT The 2013 Compensation Worksheet is intended to assist clerks, treasurers and pastors as they define and report income to Presbytery, the Board of Pensions and, of course,

P&B. Memo #3. The tax and reporting requirements with which churches must comply. Tax and Reporting Procedures for Congregations

P&B Memo #3 Pensions and Benefits USA, Church of the Nazarene Tax and Reporting Procedures for Congregations The tax and reporting requirements with which churches must comply often seem to complicate

P&B Memo #3 Pensions and Benefits USA, Church of the Nazarene Tax and Reporting Procedures for Congregations The tax and reporting requirements with which churches must comply often seem to complicate

Understanding Effective Salary

Understanding Effective Salary 1 The Community of Faith and the Benefits Plan Following a biblical understanding of sharing based on need, the Benefits Plan calls on the entire community of faith to contribute

Understanding Effective Salary 1 The Community of Faith and the Benefits Plan Following a biblical understanding of sharing based on need, the Benefits Plan calls on the entire community of faith to contribute

ANNUAL INFORMATION RETURNS NEWSLETTER

ANNUAL INFORMATION RETURNS NEWSLETTER J A N U A R Y 2 0 1 9 INSIDE THIS ISSUE: F O R M W - 2 Form W-2 1 Foreign Bank Account Reporting Foreign Bank Account Reporting Household Employee (Nanny Tax) Form

ANNUAL INFORMATION RETURNS NEWSLETTER J A N U A R Y 2 0 1 9 INSIDE THIS ISSUE: F O R M W - 2 Form W-2 1 Foreign Bank Account Reporting Foreign Bank Account Reporting Household Employee (Nanny Tax) Form

Congregational Treasurers and Bookkeepers Financial and Accounting Guide

Congregational Treasurers and Bookkeepers Financial and Accounting Guide A resource provided by the Office of the Treasurer of the Evangelical Lutheran Church in America Preface These resources for congregational

Congregational Treasurers and Bookkeepers Financial and Accounting Guide A resource provided by the Office of the Treasurer of the Evangelical Lutheran Church in America Preface These resources for congregational

TAX MATTERS FOR YOUR MINISTRY

TAX MATTERS FOR YOUR MINISTRY Amos Smith, Attorney at Law The Church Law & Tax Attorney (312) 560-6725 Attorney Amos Smith - 312 560-6725 This is not legal advice. Please consult with an attorney. 1 DO

TAX MATTERS FOR YOUR MINISTRY Amos Smith, Attorney at Law The Church Law & Tax Attorney (312) 560-6725 Attorney Amos Smith - 312 560-6725 This is not legal advice. Please consult with an attorney. 1 DO

Tax & Money S E R I E S PREPARING TAX RETURNS FOR CLERGY. Federal, state, and other reporting made easy. by Dan Busby, CPA John Van Drunen, JD, CPA

2 0 1 2 Tax & Money S E R I E S E D I T I O N PREPARING TAX RETURNS FOR CLERGY Federal, state, and other reporting made easy. by Dan Busby, CPA John Van Drunen, JD, CPA The federal tax laws offer you special

2 0 1 2 Tax & Money S E R I E S E D I T I O N PREPARING TAX RETURNS FOR CLERGY Federal, state, and other reporting made easy. by Dan Busby, CPA John Van Drunen, JD, CPA The federal tax laws offer you special

Example Two: Retired Minister

Example Two: Retired Minister Form 1040 Rev. William K. Green is a retired minister. He is 69 years old. He is married to Sarah J. Green. She is 65 years old and is also retired. For 2010, Rev. Green received

Example Two: Retired Minister Form 1040 Rev. William K. Green is a retired minister. He is 69 years old. He is married to Sarah J. Green. She is 65 years old and is also retired. For 2010, Rev. Green received

Planning Financial Support. Planning Financial Support. For ministers and church employees. Visit

Planning Financial Support Visit www.guidestone.org for an online version of this workbook or view the Planning Financial Support presentation. For ministers and church employees Well done... M A T T H

Planning Financial Support Visit www.guidestone.org for an online version of this workbook or view the Planning Financial Support presentation. For ministers and church employees Well done... M A T T H

The Lee Accountancy Group, Inc th Street Oakland, CA

January 22, 2016 The Lee Accountancy Group, Inc. 369 13th Street Oakland, CA 94612-2636 Client, Dear : The Tax Organizer will assist you in collecting and reporting information necessary for us to properly

January 22, 2016 The Lee Accountancy Group, Inc. 369 13th Street Oakland, CA 94612-2636 Client, Dear : The Tax Organizer will assist you in collecting and reporting information necessary for us to properly

This is a list of items you should gather for the Income Tax Preparation

This is a list of items you should gather for the Income Tax Preparation 1. Social Security Card(s) - Your Social Security number, which is your taxpayer identification number, is printed on your Social

This is a list of items you should gather for the Income Tax Preparation 1. Social Security Card(s) - Your Social Security number, which is your taxpayer identification number, is printed on your Social

Tax Issues From Volume 2005, Issue Proper treatment of fringe benefits

Tax Issues From Volume 2005, Issue 5-5 2005 Proper treatment of fringe benefits

Tax Issues From Volume 2005, Issue 5-5 2005 Proper treatment of fringe benefits

Legal and Business Issues Pertaining to Church Life

Legal and Business Issues Pertaining to Church Life There are various government entities and businesses with whom an established church will transact business on a regular basis and with whom a new church

Legal and Business Issues Pertaining to Church Life There are various government entities and businesses with whom an established church will transact business on a regular basis and with whom a new church

PROVIDED THROUGH THE RESOURCES OF THE BAPTIST GENERAL CONVENTION OF TEXAS

PROVIDED THROUGH THE RESOURCES OF THE BAPTIST GENERAL CONVENTION OF TEXAS 1 My church has just asked me to serve in a capacity where I have a number of questions about payroll, taxes, reporting, and accounting.

PROVIDED THROUGH THE RESOURCES OF THE BAPTIST GENERAL CONVENTION OF TEXAS 1 My church has just asked me to serve in a capacity where I have a number of questions about payroll, taxes, reporting, and accounting.

Compensation and Benefits Guidelines for Lay and Clergy Employees. Revised October 2014

2015 Compensation and Benefits Guidelines for Lay and Clergy Employees Revised October 2014 Page 2 Page 3 Table of Contents INTRODUCTION... 5 COMPENSATION... 6 COMPENSATION FOR PRIESTS AND TRANSITIONAL

2015 Compensation and Benefits Guidelines for Lay and Clergy Employees Revised October 2014 Page 2 Page 3 Table of Contents INTRODUCTION... 5 COMPENSATION... 6 COMPENSATION FOR PRIESTS AND TRANSITIONAL

Form 1099 Instructions and General Discussion

Form 1099 Instructions and General Discussion 1 2017 New Mexico Association of Counties Annual Conference Chip Low, CPA CGMA Lea County Finance Director (o) 575-396-8653 (c) 575-704-6500 clow@leacounty.net

Form 1099 Instructions and General Discussion 1 2017 New Mexico Association of Counties Annual Conference Chip Low, CPA CGMA Lea County Finance Director (o) 575-396-8653 (c) 575-704-6500 clow@leacounty.net

Oregon-Idaho Annual Conference

Oregon-Idaho Annual Conference The United Methodist Church 1505 SW 18 th Avenue Portland OR 97201 503.226.7931 1.800.593.7539 www.umoi.org W-2 Instructions and other General Tax Information Remember that

Oregon-Idaho Annual Conference The United Methodist Church 1505 SW 18 th Avenue Portland OR 97201 503.226.7931 1.800.593.7539 www.umoi.org W-2 Instructions and other General Tax Information Remember that

[Type here] PRESBYTERY of EASTERN VIRGINIA

![[Type here] PRESBYTERY of EASTERN VIRGINIA](/thumbs/92/110259386.jpg "[Type here] PRESBYTERY of EASTERN VIRGINIA") [Type here] PRESBYTERY of EASTERN VIRGINIA GUIDELINES for FAIR COMPENSATION for INSTALLED PASTORS, COMMISSIONED RULING ELDERS and CERTIFIED CHRISTIAN EDUCATORS 2019 This document was approved by COM on

[Type here] PRESBYTERY of EASTERN VIRGINIA GUIDELINES for FAIR COMPENSATION for INSTALLED PASTORS, COMMISSIONED RULING ELDERS and CERTIFIED CHRISTIAN EDUCATORS 2019 This document was approved by COM on

RE: W-2 REPORTING REQUIREMENTS FOR FRINGE BENEFITS TO BE ADDED TO EMPLOYEES' W-2 AS COMPENSATION

December 2017 To Our Clients: RE: - 2017 W-2 REPORTING REQUIREMENTS FOR FRINGE BENEFITS TO BE ADDED TO EMPLOYEES' W-2 AS COMPENSATION - SPECIAL RULES FOR S-CORPORATION SHAREHOLDERS In this letter, we will

December 2017 To Our Clients: RE: - 2017 W-2 REPORTING REQUIREMENTS FOR FRINGE BENEFITS TO BE ADDED TO EMPLOYEES' W-2 AS COMPENSATION - SPECIAL RULES FOR S-CORPORATION SHAREHOLDERS In this letter, we will

Charitable Contributions. Substantiation and Disclosure Requirements

Charitable Contributions Substantiation and Disclosure Requirements 1 Are you an organization that receives contributions of $250 or more? or Are you an organization that provides goods or services to

Charitable Contributions Substantiation and Disclosure Requirements 1 Are you an organization that receives contributions of $250 or more? or Are you an organization that provides goods or services to

Charitable Contributions

Charitable Contributions Substantiation and Disclosure Requirements INTERNAL REVENUE SERVICE Tax Exempt and Government Entities Exempt Organizations Are you an organization that receives contributions

Charitable Contributions Substantiation and Disclosure Requirements INTERNAL REVENUE SERVICE Tax Exempt and Government Entities Exempt Organizations Are you an organization that receives contributions

Local Church Treasurer/Finance Training

Local Church Treasurer/Finance Training 2018 Welcome!! Christine Dodson, Treasurer JoAnna Ezuka, Benefits Coordinator Sandy Lee, Benefits Specialist Chrisy Powell, Property Management & Insurance Katherine

Local Church Treasurer/Finance Training 2018 Welcome!! Christine Dodson, Treasurer JoAnna Ezuka, Benefits Coordinator Sandy Lee, Benefits Specialist Chrisy Powell, Property Management & Insurance Katherine

Examination Issues. Resources. Public Employers Toolkit

Tax Exempt Government Entities IRS Examination Issues Examination Issues Public Employers Toolkit Resources Publication 963 Federal State Reference Guide Publication 5137 Fringe Benefit Guide Publication

Tax Exempt Government Entities IRS Examination Issues Examination Issues Public Employers Toolkit Resources Publication 963 Federal State Reference Guide Publication 5137 Fringe Benefit Guide Publication

RE: W-2 REPORTING REQUIREMENTS FOR FRINGE BENEFITS TO BE ADDED TO EMPLOYEES' W-2 AS COMPENSATION

To Our Clients: November 2018 RE: - 2018 W-2 REPORTING REQUIREMENTS FOR FRINGE BENEFITS TO BE ADDED TO EMPLOYEES' W-2 AS COMPENSATION - SPECIAL RULES FOR S-CORPORATION SHAREHOLDERS In this letter, we will

To Our Clients: November 2018 RE: - 2018 W-2 REPORTING REQUIREMENTS FOR FRINGE BENEFITS TO BE ADDED TO EMPLOYEES' W-2 AS COMPENSATION - SPECIAL RULES FOR S-CORPORATION SHAREHOLDERS In this letter, we will

Part 4. Comprehensive Example and Sample Forms Example One: Senior Minister

Part 4. Comprehensive Example and Sample Forms Example One: Senior Minister Note: This example is based on an illustrated example contained at the end of IRS Publication 517. Rev. John Michaels is the

Part 4. Comprehensive Example and Sample Forms Example One: Senior Minister Note: This example is based on an illustrated example contained at the end of IRS Publication 517. Rev. John Michaels is the

1040 US Client Information 1

Page 1 1040 US Client Information 1 Coleman Tax & Bookkeeping P.O. Box 843 Weaverville, CA 96093 Telephone number: Fax number: E-mail address: (530) 623-4787 (530) 623-4560 ccoleman@velotech.net Tax Return

Page 1 1040 US Client Information 1 Coleman Tax & Bookkeeping P.O. Box 843 Weaverville, CA 96093 Telephone number: Fax number: E-mail address: (530) 623-4787 (530) 623-4560 ccoleman@velotech.net Tax Return

Personal Income Tax Questionnaire Taxpayer Social Security No. Occupation Birth Date. Spouse Social Security No. Occupation Birth Date

Taxpayer Social Security No. Occupation Birth Date Spouse Social Security No. Occupation Birth Date Address County Home Phone ( ) City, State, Zip Bus. Phone ( ) E-mail Address Fax Number ( ) If we have

Taxpayer Social Security No. Occupation Birth Date Spouse Social Security No. Occupation Birth Date Address County Home Phone ( ) City, State, Zip Bus. Phone ( ) E-mail Address Fax Number ( ) If we have

SUMMARY PLAN DESCRIPTION FOR. The Roman Catholic Diocese of Raleigh 403(b) Retirement Plan

Retirement Plan") SUMMARY PLAN DESCRIPTION FOR The Roman Catholic Diocese of Raleigh 403(b) Retirement Plan 7-1-2014 Table of Contents Article 1... Introduction Article 2... General Plan Information and Key Definitions

SUMMARY PLAN DESCRIPTION FOR The Roman Catholic Diocese of Raleigh 403(b) Retirement Plan 7-1-2014 Table of Contents Article 1... Introduction Article 2... General Plan Information and Key Definitions

Development of year-end work plan Create the year-end team (e.g., Payroll, HR, IT, and Accounting) and focus on the following tasks:

and focus on the following tasks:") Presentation topics > Development of year-end work plan > Management and completion of year-end tasks > Form W-4 compliance > Social Security number (SSN) verification > Form W-2 reporting > IRS Publication

Presentation topics > Development of year-end work plan > Management and completion of year-end tasks > Form W-4 compliance > Social Security number (SSN) verification > Form W-2 reporting > IRS Publication

JOYNER, KIRKHAM, KEEL & ROBERTSON, P.C INDIVIDUAL TAX ORGANIZER

Please provide a copy of your 2013 federal and state tax returns, and complete pages 1 through 3. Other pages: complete only those sections that apply to you. Your Name SS# Occupation Birth Date Spouse

Please provide a copy of your 2013 federal and state tax returns, and complete pages 1 through 3. Other pages: complete only those sections that apply to you. Your Name SS# Occupation Birth Date Spouse

Contents. Key Federal Tax Limits, Rates and Other Data Reporting as an Employer Information Reporting Requirements...

Contents Key Federal Tax Limits, Rates and Other Data......................... 3 Reporting as an Employer........................................................ 4 Information Reporting Requirements........................................

Contents Key Federal Tax Limits, Rates and Other Data......................... 3 Reporting as an Employer........................................................ 4 Information Reporting Requirements........................................

DETERMINATION OF EMPLOYEE STATUS. Following are the procedures to be followed to determine the status of each employee:

DETERMINATION OF EMPLOYEE STATUS Following are the procedures to be followed to determine the status of each employee: Archdiocesan Priests Priests of the Archdiocese are considered employees for federal,

DETERMINATION OF EMPLOYEE STATUS Following are the procedures to be followed to determine the status of each employee: Archdiocesan Priests Priests of the Archdiocese are considered employees for federal,

KENNETH M. WEINSTEIN,

Dear Client: KENNETH M. WEINSTEIN, CPA AND CFP 1450 Niagara Falls Boulevard, Suite #202 Tonawanda, NY 14150-8440 (716) 837-2525 ~ FAX (716) 837-2527 E-Mail: kweinsteincpa@gmail.com The enclosed 2015 Tax

Dear Client: KENNETH M. WEINSTEIN, CPA AND CFP 1450 Niagara Falls Boulevard, Suite #202 Tonawanda, NY 14150-8440 (716) 837-2525 ~ FAX (716) 837-2527 E-Mail: kweinsteincpa@gmail.com The enclosed 2015 Tax

2017 Minister s Tax Organizer Supplement

Please make a copy of this tax organizer for your records before you send to us. 2017 Minister s Tax Organizer Supplement Peachtree Tax Advisors, LLC 500 East Second Street Rome, GA 30161-3112 706-234-7468

Please make a copy of this tax organizer for your records before you send to us. 2017 Minister s Tax Organizer Supplement Peachtree Tax Advisors, LLC 500 East Second Street Rome, GA 30161-3112 706-234-7468

Congregational Treasurers and Bookkeepers Financial and Accounting Guide

Congregational Treasurers and Bookkeepers Financial and Accounting Guide A resource provided by the Office of the Treasurer of the Evangelical Lutheran Church in America Preface These resources for congregational

Congregational Treasurers and Bookkeepers Financial and Accounting Guide A resource provided by the Office of the Treasurer of the Evangelical Lutheran Church in America Preface These resources for congregational

1040 US Tax Organizer

40 US Tax Organizer Page 1 CLIENT INFORMATION First name and initial..... Last name............... Title/suffix............... Social security number... Occupation.............. Date of birth (m/d/y)......

40 US Tax Organizer Page 1 CLIENT INFORMATION First name and initial..... Last name............... Title/suffix............... Social security number... Occupation.............. Date of birth (m/d/y)......

JOYNER, KIRKHAM, KEEL & ROBERTSON, P.C INDIVIDUAL TAX ORGANIZER

Please provide a copy of your 2017 federal and state tax returns, and complete pages 1 through 3. Other pages: complete only those sections that apply to you. Taxpayer Name SS# Occupation Birth Date Spouse

Please provide a copy of your 2017 federal and state tax returns, and complete pages 1 through 3. Other pages: complete only those sections that apply to you. Taxpayer Name SS# Occupation Birth Date Spouse

Mennonite Church USA Treasurer s Handbook

Mennonite Church USA Treasurer s Handbook Sample Guidelines/Policies 1. Counting the money how to play it safe 2. Pastor s housing allowance worksheet 3. Pastor s living in a parsonage worksheet 4. Memorial

Mennonite Church USA Treasurer s Handbook Sample Guidelines/Policies 1. Counting the money how to play it safe 2. Pastor s housing allowance worksheet 3. Pastor s living in a parsonage worksheet 4. Memorial

Tax & Money. Federal, state, and other reporting made easy. by Dan Busby Michael Martin John Van Drunen S E R I E S MINISTERS TAXES MADE EASY

2 0 1 7 Tax & Money S E R I E S E D I T I O N MINISTERS TAXES MADE EASY Federal, state, and other reporting made easy. by Dan Busby Michael Martin John Van Drunen Dan Busby is president of ECFA, an organization

2 0 1 7 Tax & Money S E R I E S E D I T I O N MINISTERS TAXES MADE EASY Federal, state, and other reporting made easy. by Dan Busby Michael Martin John Van Drunen Dan Busby is president of ECFA, an organization

403(b)(9) Retirement Plan Plan Summary. Self-Employed Ministers and Chaplains

(9) Retirement Plan Plan Summary. Self-Employed Ministers and Chaplains") 403(b)(9) Retirement Plan Plan Summary Self-Employed Ministers and Chaplains 2 Overview Your retirement plan This 403(b)(9) Retirement Plan for Self-Employed Ministers and Chaplains is funded by the contributions

403(b)(9) Retirement Plan Plan Summary Self-Employed Ministers and Chaplains 2 Overview Your retirement plan This 403(b)(9) Retirement Plan for Self-Employed Ministers and Chaplains is funded by the contributions

Definition of Compensation and Benefits for Rostered Leaders Rocky Mountain Synod Evangelical Lutheran Church in America

Definition of Compensation and Benefits for Rostered Leaders Rocky Mountain Synod Evangelical Lutheran Church in America Now to one who works, wages are not reckoned as a gift but as something due. (Romans

Definition of Compensation and Benefits for Rostered Leaders Rocky Mountain Synod Evangelical Lutheran Church in America Now to one who works, wages are not reckoned as a gift but as something due. (Romans

THE PRESBYTERY OF ELIZABETH Compensation Committee of the Committee on Ministry Recommendations regarding Compensation for 2015.

THE PRESBYTERY OF ELIZABETH Compensation Committee of the Committee on Ministry Recommendations regarding Compensation for 2015 December 9, 2014 Congregations support their pastor to free them from secular

THE PRESBYTERY OF ELIZABETH Compensation Committee of the Committee on Ministry Recommendations regarding Compensation for 2015 December 9, 2014 Congregations support their pastor to free them from secular

ESTATE OR TRUST TAX ORGANIZER FORM New Estate or Trust Administrators Information Needed

ESTATE OR TRUST TAX ORGANIZER FORM 1041 New Estate or Trust Administrators Information Needed This is a list of information which will be typically needed for us to work with you on tax issues for an estate

ESTATE OR TRUST TAX ORGANIZER FORM 1041 New Estate or Trust Administrators Information Needed This is a list of information which will be typically needed for us to work with you on tax issues for an estate

The Pastor and His Income Tax. For 2015 Tax Year. 38 th

The Pastor and His Income Tax For 2015 Tax Year Our 38 th Year Please Note You must completely fill out the Tax Data Questionnaire (green sheets). Please send your information to us as soon as possible

The Pastor and His Income Tax For 2015 Tax Year Our 38 th Year Please Note You must completely fill out the Tax Data Questionnaire (green sheets). Please send your information to us as soon as possible

Please check the appropriate box and provide additional information if necessary. Did your marital status change during the year?

Page 1 Miscellaneous Questions Please check the appropriate box and provide additional information if necessary. PERSONAL INFORMATION Yes No Do you want a PDF copy of your return emailed to you instead

Page 1 Miscellaneous Questions Please check the appropriate box and provide additional information if necessary. PERSONAL INFORMATION Yes No Do you want a PDF copy of your return emailed to you instead

PAYROLL AND THE CHURCH 5 THINGS THAT MINISTRIES GET WRONG

PAYROLL AND THE CHURCH 5 THINGS THAT MINISTRIES GET WRONG 1 MINISTRY PAYROLL: IT S COMPLICATED PAYROLL CAN BE COMPLICATED. FOR THAT, THERE S MINISTRYWORKS. Whether you re a small church using a volunteer

PAYROLL AND THE CHURCH 5 THINGS THAT MINISTRIES GET WRONG 1 MINISTRY PAYROLL: IT S COMPLICATED PAYROLL CAN BE COMPLICATED. FOR THAT, THERE S MINISTRYWORKS. Whether you re a small church using a volunteer

1040 US Client Information 1

Page 1 1040 US Client Information 1 DENISE M. BROLIN, CPA 1205 THIRD STREET GILROY CA 95020 Telephone number: Fax number: E-mail address: (408) 848-3861 (408) 413-1988 denise@denisebrolin-cpa.com Tax Return

Page 1 1040 US Client Information 1 DENISE M. BROLIN, CPA 1205 THIRD STREET GILROY CA 95020 Telephone number: Fax number: E-mail address: (408) 848-3861 (408) 413-1988 denise@denisebrolin-cpa.com Tax Return

Taxation for Clergy. The Rev. Robert L. Rible, M.A., M.Div., C.P.A. January 24, 2009 Salinas, California

The Rev. Robert L. Rible, M.A., M.Div., C.P.A. January 24, 2009 Salinas, California Keep in Mind: This presentation contains general information only and should not be relied upon for accounting, business,

The Rev. Robert L. Rible, M.A., M.Div., C.P.A. January 24, 2009 Salinas, California Keep in Mind: This presentation contains general information only and should not be relied upon for accounting, business,

TAX DEDUCTIONS FOR SMALL BUSINESS

TAX DEDUCTIONS FOR SMALL BUSINESS JEAN KRUSE SCORE MENTOR jekcpa@msn.com If you email me, please put SCORE on the subject line ORDINARY & NECESSARY Whether an expense is ordinary and necessary is based

TAX DEDUCTIONS FOR SMALL BUSINESS JEAN KRUSE SCORE MENTOR jekcpa@msn.com If you email me, please put SCORE on the subject line ORDINARY & NECESSARY Whether an expense is ordinary and necessary is based

Tax Law Reminders & LowTax Tips Rev

Tax Law Reminders & LowTax Tips Rev 1-21-19 The most frequently encountered missing information that delays our tax preparation is the cost basis for securities that have been sold. Please check with your

Tax Law Reminders & LowTax Tips Rev 1-21-19 The most frequently encountered missing information that delays our tax preparation is the cost basis for securities that have been sold. Please check with your

S U M M A R Y P L A N D E S C R I P T I O N Marvell Semiconductor 401(k) Retirement Plan

Retirement Plan") S U M M A R Y P L A N D E S C R I P T I O N Marvell Semiconductor 401(k) Retirement Plan This information is not intended to be a substitute for specific individualized tax, legal, or investment planning

S U M M A R Y P L A N D E S C R I P T I O N Marvell Semiconductor 401(k) Retirement Plan This information is not intended to be a substitute for specific individualized tax, legal, or investment planning

Index (Volumes 1 and 2)

") Index (Volumes 1 and 2) The digit(s) to the left of the decimal indicate the chapter; those to the right indicate the paragraph within that chapter. accountable reimbursement plan...6.110 accounting (see

Index (Volumes 1 and 2) The digit(s) to the left of the decimal indicate the chapter; those to the right indicate the paragraph within that chapter. accountable reimbursement plan...6.110 accounting (see

SECTION 1: FILLING OUT THE COMPENSATION PACKAGE

STATED SUPPLY AGREEMENT for Minister Members of New Hope Presbytery Section 1. Filling out the Compensation Pkg. Page 1-2 Section 3. Min. Standards of Compensation Page 4 Section 2. Effective Salary Information

STATED SUPPLY AGREEMENT for Minister Members of New Hope Presbytery Section 1. Filling out the Compensation Pkg. Page 1-2 Section 3. Min. Standards of Compensation Page 4 Section 2. Effective Salary Information