Note on Tax Deduction at Source

|

|

|

- Noel Potter

- 6 years ago

- Views:

Transcription

1 Note on Tax Deduction at Source What is Tax Deduction at Source (TDS)? TDS is a way by which a certain percentage of amounts are deducted by a person at the time of making/crediting certain specific nature of payment to the other person and deducted amount is remitted to the Government account. It facilitates sharing of responsibility of tax collection between the deductor and the tax administration. It ensures regular inflow of cash resources to the Government. It acts as a powerful instrument to prevent tax evasion as well as expands the tax net. Who shall deduct tax at source in case of the Company? Principal Officer or Director of a company for TDS purpose including the employer in case of private employment or an employee making payment on behalf of the employer. Such person is called Deductor while the person from whom the tax is deducted is called Deductee. Tax must be deducted at the time of payment in cash or cheque or credit to the payee's account whichever is earlier. Credit to payable account or suspense account is also considered to be credit to payee's account and TDS must be made at the time of such credit.

2 What a deductor must do? 1. Principal Officer or Director of a company should deduct the tax at correct rate. 2. The tax deducted has to be deposited in the designated banks within specified time. 3. Use challan no. 92B for depositing TDS amount. 4. File statements of tax deduction in the prescribed time. The due dates for filing of TDS statement are: 15 th of July for Quarter 1, 15 th of October for Quarter 2, 15 th of January for Quarter 3 and 15 th May of the financial year immediately following the financial year in which tax is deducted/ collected for last Quarter 5. Use correct form to file TDS/TCS Returns. Form 24Q for salaries It may be noted that the following persons have to compulsorily file e- TDS /e-tcs statements All government offices/departments All companies /corporations All persons whose cases are auditable All persons whose TDS statements contain more than 50 deductees

3 Dos & Don ts for filing TDS Returns Dos Ensure that TDS return is filed with same TAN against which TDS payment has been made & TDS certificate is issued. Ensure that correct challan particulars including CIN and amount is mentioned. Correct PAN of the deductee is mentioned. Correct section is quoted against each deductee record. Correct rate is quoted against each deductee record. File correction statement as soon as discrepancy is noticed Retain the original FVU file to enable future corrections Make use of free of charge RPU provided through TIN-NSDL.com Download details of challan from challan status enquiry (TAN based view) from TIN-NSDL.com Registration for TAN enables you to avail additional facilities from Tax Information System. Always verify status of TDS returns from Tin NSDL to ascertain the discrepancy, if any, and/or whether your TDS return stands accepted or rejected by the system. Don ts Don't file late returns as it affects deductee tax credit Don't quote incorrect TAN vis-à-vis TDS payments 6. Issue TDS certificates as per existing procedure and within the time prescribed as stated below:

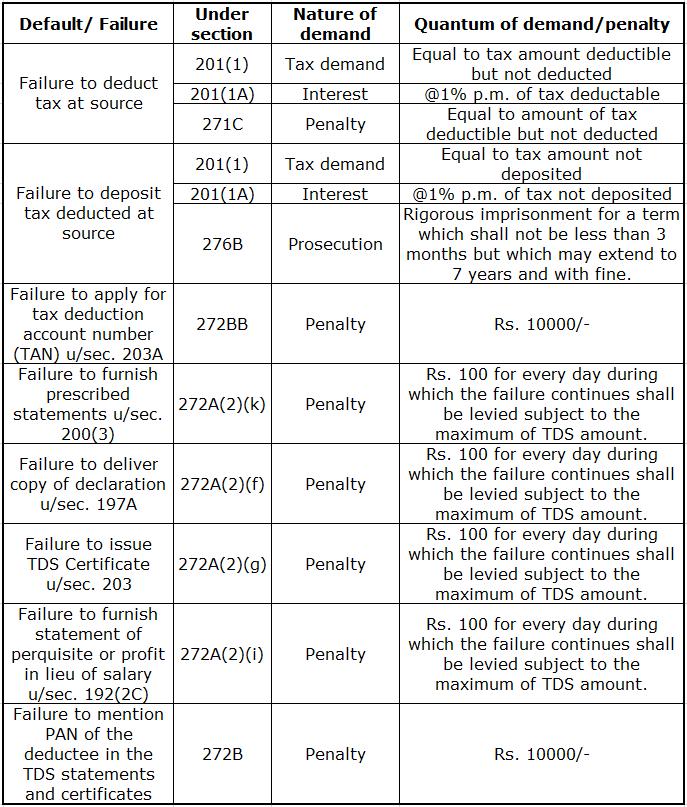

4 The certificate should be issued within one month from the end of the month in which the income is credited however for credit entries made on 31 st March, due date is 7 th June, except in the case of salary where the certificate has to be issued by 30 th of April of the following financial year in which the income was credited. TDS defaults Failure to deduct the whole or part of the Tax at source (non-deduction, short deduction or delay in deduction) 1. Failure to deposit whole or part of the TDS (non-deposit, short deposit or late deposit) 2. Failure to apply for TAN within the prescribed time limit or failure to quote TAN on allotment as required under section 203A. 3. Failure to furnish, in due time, TDS returns or TDS certificates or to deliver or cause to be delivered a copy of declaration in form no. 15H/15G/27C/copy of quarterly statement. 4. Failure to mention the PAN of the deductee in all quarterly statements as well as in all certificates furnished. Consequences of Defaults The following chart indicates the nature of default and its consequences which range from penal interest, penalty to prosecution.

5

6 In addition to the above, there are other consequences in certain cases, as enumerated below; Disallowance of specified expenditure (while computing the income of the deductor) if TDS is not deducted from the payment. (Section 40a (ia)). where the tax has not been paid after its deduction it shall be charge on the asset of the defaulter to recover the amount of TDS. (Section 201(2)).

Issues in filing TDS returns

Issues in filing TDS returns Contents Components of TIN Correction statement Consolidated TDS/TCS statement Online TAN registration Annual Tax Statement New @ TIN FILER DEDUCTOR TAX PAYER TIN FC ERACS

Issues in filing TDS returns Contents Components of TIN Correction statement Consolidated TDS/TCS statement Online TAN registration Annual Tax Statement New @ TIN FILER DEDUCTOR TAX PAYER TIN FC ERACS

Analysis of new system for TDS -TCS payment and information reporting

Analysis of new system for TDS -TCS payment and information reporting Income Tax Department has introduced a scheme for centralized processing of annual income-tax returns which envisages no interface

Analysis of new system for TDS -TCS payment and information reporting Income Tax Department has introduced a scheme for centralized processing of annual income-tax returns which envisages no interface

TDS Seminar for Residents Welfare Associations

TDS Seminar for Residents Welfare Associations 27 th July 2018 What is TDS? Mode of quick and efficient collection of taxes Tax deducted at the point of generation of income Tax deducted by the payer &

TDS Seminar for Residents Welfare Associations 27 th July 2018 What is TDS? Mode of quick and efficient collection of taxes Tax deducted at the point of generation of income Tax deducted by the payer &

E-TDS FILING PRESENTED BY. Vinod Kumar Jain FCA

E-TDS FILING PRESENTED BY Vinod Kumar Jain FCA What is E- TDS? E-TDS stands for Electronic Tax Deducted at Source introduced by the IT department. Filing e TDS return is compulsory for all assessee and

E-TDS FILING PRESENTED BY Vinod Kumar Jain FCA What is E- TDS? E-TDS stands for Electronic Tax Deducted at Source introduced by the IT department. Filing e TDS return is compulsory for all assessee and

NATURE & REMEDIES. A Presentation by K.M. SHAHI, ITO(TDS) 2(4), MUMBAI

2(4), MUMBAI") NATURE & REMEDIES A Presentation by K.M. SHAHI, ITO(TDS) 2(4), MUMBAI DEFAULTs u/s. 201(1) & MISMATCHEs u/s. 200A Reasons for Default Types of Default How to Correct? What is the Advantage? Show Cause

NATURE & REMEDIES A Presentation by K.M. SHAHI, ITO(TDS) 2(4), MUMBAI DEFAULTs u/s. 201(1) & MISMATCHEs u/s. 200A Reasons for Default Types of Default How to Correct? What is the Advantage? Show Cause

To, July 17, 2007 Mr. P. Chidambaram The Hon ble Finance Minister Government of India, North Block, Vijay Chowk, NEW DELHI

To, July 17, 2007 Mr. P. Chidambaram The Hon ble Finance Minister Government of India, North Block, Vijay Chowk, NEW DELHI 110 001. Re : Discrepancies in quarterly e-tds Statements multiple notices issued

To, July 17, 2007 Mr. P. Chidambaram The Hon ble Finance Minister Government of India, North Block, Vijay Chowk, NEW DELHI 110 001. Re : Discrepancies in quarterly e-tds Statements multiple notices issued

CA. Mehul Shah. Payment to Transport Contractors implications under the Income-tax Act Overview of Companies Act Care, Pair, and Share

Payment to Transport Contractors implications under the Income-tax Act 1961 Overview of Companies Act 2013 CA. Mehul Shah B. Com, F.C.A., DISA (ICAI). Care, Pair, and Share The way s not Smooth 03/06/2015

Payment to Transport Contractors implications under the Income-tax Act 1961 Overview of Companies Act 2013 CA. Mehul Shah B. Com, F.C.A., DISA (ICAI). Care, Pair, and Share The way s not Smooth 03/06/2015

In the Financial World TDS is Tax deducted at. TDS contributes 40% to the gross direct tax

In the Financial World TDS is Tax deducted at Source TDS contributes 40% to the gross direct tax collections It has been brought with the principle of Pay As you Earn i.e. Collection of Tax in Advance.

In the Financial World TDS is Tax deducted at Source TDS contributes 40% to the gross direct tax collections It has been brought with the principle of Pay As you Earn i.e. Collection of Tax in Advance.

CONSEQUENCES OF DEFAULTS IN e-tds RETURNS

CONSEQUENCES OF DEFAULTS IN e-tds RETURNS 1 The material contained in the ensuing slides is for general information, compilation and the views of the speaker and is purely for general discussion at the

CONSEQUENCES OF DEFAULTS IN e-tds RETURNS 1 The material contained in the ensuing slides is for general information, compilation and the views of the speaker and is purely for general discussion at the

TRACES Site and Issues in Deemed, Recovery & online resolution

TRACES Site and Issues in Deemed, Recovery & online resolution The material contained in the ensuing slides is for general information, compilation is from various websites, views of the experts and the

TRACES Site and Issues in Deemed, Recovery & online resolution The material contained in the ensuing slides is for general information, compilation is from various websites, views of the experts and the

T.D.S/T.C.S AT GLANCE FOR A.Y

T.D.S/T.C.S AT GLANCE FOR A.Y. 2012-2013 Tax Deducted at Source (TDS) was introduced to facilitate the payment of Tax while receiving the income and it follows the concept Pay as you Earn. The tax deducted

T.D.S/T.C.S AT GLANCE FOR A.Y. 2012-2013 Tax Deducted at Source (TDS) was introduced to facilitate the payment of Tax while receiving the income and it follows the concept Pay as you Earn. The tax deducted

TDS & TCS RATE CHART FY

TDS & TCS RATE CHART FY 2017-18 Sl. No Section Of Act Nature of Payment in brief Threshold Limit Rate % From 01.04.17 to 31.03.18 HUF/IND Others 1 192 Salaries Salary income must be more than exemption

TDS & TCS RATE CHART FY 2017-18 Sl. No Section Of Act Nature of Payment in brief Threshold Limit Rate % From 01.04.17 to 31.03.18 HUF/IND Others 1 192 Salaries Salary income must be more than exemption

GST (GOODS AND SERVICES TAX) TDS MECHANISM UNDER GST

TDS MECHANISM UNDER GST") GST (GOODS AND SERVICES TAX) TDS MECHANISM UNDER GST Tax Deduction at Source (TDS) is a system, initially introduced by the Income Tax Department. It is one of the modes/methods to collect tax, under which,

GST (GOODS AND SERVICES TAX) TDS MECHANISM UNDER GST Tax Deduction at Source (TDS) is a system, initially introduced by the Income Tax Department. It is one of the modes/methods to collect tax, under which,

SEMINAR ON TAX DEDUCTED AT SOURCE PRESENTED BY CA B. D SOUZA

SEMINAR ON TAX DEDUCTED AT SOURCE PRESENTED BY CA B. D SOUZA IS TDS TEDIOUS??? SET UP OF TDS TAN (TAX DEDUCTION ACCOUNT NUMBER) Every deductor is required to obtain a unique identification number called

SEMINAR ON TAX DEDUCTED AT SOURCE PRESENTED BY CA B. D SOUZA IS TDS TEDIOUS??? SET UP OF TDS TAN (TAX DEDUCTION ACCOUNT NUMBER) Every deductor is required to obtain a unique identification number called

GOVERNMENT OF INDIA MINISTRY OF FINANCE (DEPARTMENT OF REVENUE) CENTRAL BOARD OF DIRECT TAXES

CENTRAL BOARD OF DIRECT TAXES") GOVERNMENT OF INDIA MINISTRY OF FINANCE (DEPARTMENT OF REVENUE) CENTRAL BOARD OF DIRECT TAXES DEDUCTION OF TAX AT SOURCE- INCOME-TAX DEDUCTION FROM SALARIES UNDER SECTION 192 OF THE INCOME-TAX ACT, 1961

GOVERNMENT OF INDIA MINISTRY OF FINANCE (DEPARTMENT OF REVENUE) CENTRAL BOARD OF DIRECT TAXES DEDUCTION OF TAX AT SOURCE- INCOME-TAX DEDUCTION FROM SALARIES UNDER SECTION 192 OF THE INCOME-TAX ACT, 1961

TaxPro. Key Features File Validation Utility (FVU) version 5.7

version 5.7") TaxPro Key Features File Validation Utility (FVU) version 5.7 In case of non-availability of PAN of deductee for Form 27EQ, two new fields are introduced under deductee details which are as below: Field

TaxPro Key Features File Validation Utility (FVU) version 5.7 In case of non-availability of PAN of deductee for Form 27EQ, two new fields are introduced under deductee details which are as below: Field

GOVERNMENT OF INDIA MINISTRY OF FINANCE (DEPARTMENT OF REVENUE) CENTRAL BOARD OF DIRECT TAXES

CENTRAL BOARD OF DIRECT TAXES") GOVERNMENT OF INDIA MINISTRY OF FINANCE (DEPARTMENT OF REVENUE) CENTRAL BOARD OF DIRECT TAXES DEDUCTION OF TAX AT SOURCE- INCOME-TAX DEDUCTION FROM SALARIES UNDER SECTION 192 OF THE INCOME-TAX ACT, 1961

GOVERNMENT OF INDIA MINISTRY OF FINANCE (DEPARTMENT OF REVENUE) CENTRAL BOARD OF DIRECT TAXES DEDUCTION OF TAX AT SOURCE- INCOME-TAX DEDUCTION FROM SALARIES UNDER SECTION 192 OF THE INCOME-TAX ACT, 1961

PENALTY, INTEREST & SURVEY (TDS) 12/02/2011 SANGHVI SANGHVI & SANGHVI

12/02/2011 SANGHVI SANGHVI & SANGHVI") 12/02/2011 SANGHVI SANGHVI & SANGHVI 1 PENAL AND OTHER CONSEQUENCES FOR NON- COMPLIANCE WITH THE PROVISIONS OF TDS DISALLOWANCE OF EXPENDITURE Sec. 40(a)(i) : Expenditure in respect of certain payments

12/02/2011 SANGHVI SANGHVI & SANGHVI 1 PENAL AND OTHER CONSEQUENCES FOR NON- COMPLIANCE WITH THE PROVISIONS OF TDS DISALLOWANCE OF EXPENDITURE Sec. 40(a)(i) : Expenditure in respect of certain payments

NEWSLETTER. M. V. DAMANIA & Co. Chartered Accountants CONTENTS

NEWSLETTER M. V. DAMANIA & Co. Chartered Accountants CONTENTS INTERNATIONAL TAX Allen & Hamilton & Co. - Mumbai Tribunal Bosch Ltd. - Bangalore Tribunal DIRECT TAX J.V.Krishna Rao - Hyderabad Tribunal

NEWSLETTER M. V. DAMANIA & Co. Chartered Accountants CONTENTS INTERNATIONAL TAX Allen & Hamilton & Co. - Mumbai Tribunal Bosch Ltd. - Bangalore Tribunal DIRECT TAX J.V.Krishna Rao - Hyderabad Tribunal

Practical difficulties for TDS returns & Previous year defaults.

Practical difficulties for TDS returns & Previous year defaults. Topics covered Basics of TDS TRACES introduction Procedure of TDS return Revision of TDS return Notice and reasons for defaults Causes of

Practical difficulties for TDS returns & Previous year defaults. Topics covered Basics of TDS TRACES introduction Procedure of TDS return Revision of TDS return Notice and reasons for defaults Causes of

F.No. 142/22/2008-TPL Government of India Ministry of Finance Department of Revenue Central Board of Direct Taxes

F.No. 142/22/2008-TPL Government of India Ministry of Finance Department of Revenue Central Board of Direct Taxes. New Delhi, the 21 st May, 2009 Subject:- New TDS and TCS payment and information reporting

F.No. 142/22/2008-TPL Government of India Ministry of Finance Department of Revenue Central Board of Direct Taxes. New Delhi, the 21 st May, 2009 Subject:- New TDS and TCS payment and information reporting

RATES OF INCOME-TAX. Nil

1 of 33 07-Oct-11 2:10 AM CIRCULAR INCOME-TAX ACT Section 192 of the Income-tax Act, 1961 - Deduction of tax at source - Salaries - Income-tax deduction from salaries during the financial year 2010-11

1 of 33 07-Oct-11 2:10 AM CIRCULAR INCOME-TAX ACT Section 192 of the Income-tax Act, 1961 - Deduction of tax at source - Salaries - Income-tax deduction from salaries during the financial year 2010-11

Payment of tax, interest, penalty and other amounts (Section 49)

") FAQ s Chapter VIII Payment of Tax Payment of tax, interest, penalty and other amounts (Section 49) Section 49 of the CGST Act, 2017 made applicable to IGST vide Section 20 of the IGST Act, 2017 and UTGST

FAQ s Chapter VIII Payment of Tax Payment of tax, interest, penalty and other amounts (Section 49) Section 49 of the CGST Act, 2017 made applicable to IGST vide Section 20 of the IGST Act, 2017 and UTGST

Country-specific updates for India

Microsoft Dynamics AX 2009 SP1 Country-specific updates for India White Paper This white paper describes country-specific updates released for India in hotfix rollup 7 for Microsoft Dynamics AX 2009 SP1.

Microsoft Dynamics AX 2009 SP1 Country-specific updates for India White Paper This white paper describes country-specific updates released for India in hotfix rollup 7 for Microsoft Dynamics AX 2009 SP1.

Presentation on TDS Salary & TDS in respect of Residents

Presentation on TDS Salary & TDS in respect of Residents R. J. Soni & Associates Corporate Office: MUMBAI Kamla Niwas Plot No. 136/141 Gorai-1 Borivali (W) Mumbai-091. Offices:- MUMBAI JAIPUR PUNE AHEMDABAD

Presentation on TDS Salary & TDS in respect of Residents R. J. Soni & Associates Corporate Office: MUMBAI Kamla Niwas Plot No. 136/141 Gorai-1 Borivali (W) Mumbai-091. Offices:- MUMBAI JAIPUR PUNE AHEMDABAD

Financial Management

Financial Management of Panchayat Samiti State Institute of Panchayats and Rural Development, Kalyani, Nadia, West Bengal Prepared by Dipyaman Majumder, Faculty Member Reference Act: The West Bengal Panchayat

Financial Management of Panchayat Samiti State Institute of Panchayats and Rural Development, Kalyani, Nadia, West Bengal Prepared by Dipyaman Majumder, Faculty Member Reference Act: The West Bengal Panchayat

CIRCULAR NO. 8/2012, Dated: October 5, 2012

CIRCULAR NO. 8/2012, Dated: October 5, 2012 Suject: Income Tax Deduction From Salaries during the Financial Year 2012-2013 under Section 192 of The Income Tax Act, 1961. Reference is invited to Circular

CIRCULAR NO. 8/2012, Dated: October 5, 2012 Suject: Income Tax Deduction From Salaries during the Financial Year 2012-2013 under Section 192 of The Income Tax Act, 1961. Reference is invited to Circular

FORM NO.12BA {See rule 26A(2)(b)}

(b)}") ANNEXURE-II FORM NO.12BA {See rule 26A(2)(b)} Statement showing particulars of perquisites, other fringe benefits or amenities and profits in lieu of salary with value thereof 1) Name and address of employer

ANNEXURE-II FORM NO.12BA {See rule 26A(2)(b)} Statement showing particulars of perquisites, other fringe benefits or amenities and profits in lieu of salary with value thereof 1) Name and address of employer

Webinar on Tax Deduction at Source (TDS) Provisions in GST Regime

Provisions in GST Regime") Webinar on Tax Deduction at Source (TDS) Provisions in GST Regime Mr Rajeev Agarwal, IRS Sr.VP, GSTN In association with National e Governance Division, Department of Electronics & Information Technology

Webinar on Tax Deduction at Source (TDS) Provisions in GST Regime Mr Rajeev Agarwal, IRS Sr.VP, GSTN In association with National e Governance Division, Department of Electronics & Information Technology

DEDUCTION, COLLECTION AND RECOVERY OF TAX

DEDUCTION, COLLECTION AND RECOVERY OF TAX Section Particulars 190 different modes of payment of tax: tds, tcs, advance tax, tax u/s 192(1A) 191 failure to deduct tax, and direct payment of tax 192 tds

DEDUCTION, COLLECTION AND RECOVERY OF TAX Section Particulars 190 different modes of payment of tax: tds, tcs, advance tax, tax u/s 192(1A) 191 failure to deduct tax, and direct payment of tax 192 tds

(b) for Form No.24Q, the following Form shall be substituted, namely : "Form No. 24Q [See section 192 and rule 31A]

![(b) for Form No.24Q, the following Form shall be substituted, namely : Form No. 24Q [See section 192 and rule 31A]](/thumbs/82/86068219.jpg "(b) for Form No.24Q, the following Form shall be substituted, namely : Form No. 24Q [See section 192 and rule 31A]") (b) for Form No.24Q, the following Form shall be substituted, namely : "Form No. 24Q [See section 192 and rule 31A] 1. (a) Quarterly Statement of deduction of tax under sub section (3) of section 200 of

(b) for Form No.24Q, the following Form shall be substituted, namely : "Form No. 24Q [See section 192 and rule 31A] 1. (a) Quarterly Statement of deduction of tax under sub section (3) of section 200 of

SOME ILLUSTRATIONS. Example 1

ANNEXURE-I SOME ILLUSTRATIONS Example 1 For Assessment Year 2016-17 (A) Calculation of Income tax in the case of an employee (Male or Female) below the age of sixty years and having gross salary income

ANNEXURE-I SOME ILLUSTRATIONS Example 1 For Assessment Year 2016-17 (A) Calculation of Income tax in the case of an employee (Male or Female) below the age of sixty years and having gross salary income

Payments under GST DISCLAIMER:

DISCLAIMER: Payments under GST The views expressed in this article are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe to the views expressed by the author(s).

DISCLAIMER: Payments under GST The views expressed in this article are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe to the views expressed by the author(s).

Tax Withholding Section 195 and CA certification

Tax Withholding Section 195 and CA certification October 1, 2011 Bijal Desai Presentation Outline Non-resident payments Withholding tax Lower or NIL withholding of tax CA Certification Consequences of

Tax Withholding Section 195 and CA certification October 1, 2011 Bijal Desai Presentation Outline Non-resident payments Withholding tax Lower or NIL withholding of tax CA Certification Consequences of

Form No. 26AS (See Section 203AA and second provisio to Section 206C(5) and Rule 31AB)

and Rule 31AB)") Form No. 26AS (See Section 203AA and second provisio to Section 206C(5) and Rule 31AB) PDF generated on 18-12-2012 Annual Tax Statement under section 203AA Permanent Account Number: AJQPP9482N Financial

Form No. 26AS (See Section 203AA and second provisio to Section 206C(5) and Rule 31AB) PDF generated on 18-12-2012 Annual Tax Statement under section 203AA Permanent Account Number: AJQPP9482N Financial

NOTIFICATION NO. 31/2009[F.NO.142/22/2008-TPL]/S.O.858(E), DATED

![NOTIFICATION NO. 31/2009[F.NO.142/22/2008-TPL]/S.O.858(E), DATED](/thumbs/78/78635266.jpg "NOTIFICATION NO. 31/2009[F.NO.142/22/2008-TPL]/S.O.858(E), DATED") INCOME-TAX (EIGHT AMENDMENT) RULES, 2009 - AMENDMENT IN RULES 24Q AND 26Q; SUBSTITUTION OF RULES 30, 31, 31A, 31AA, 37CA, 37D AND FORMS 16, 16A, 16AA, 27D, 27Q AND 27EQ; INSERTION OF FORM 24C; OMISSION

INCOME-TAX (EIGHT AMENDMENT) RULES, 2009 - AMENDMENT IN RULES 24Q AND 26Q; SUBSTITUTION OF RULES 30, 31, 31A, 31AA, 37CA, 37D AND FORMS 16, 16A, 16AA, 27D, 27Q AND 27EQ; INSERTION OF FORM 24C; OMISSION

Tax Payers Information Series - 35 TDS ON SALARIES

Tax Payers Information Series - 35 TDS ON SALARIES INCOME TAX DEPARTMENT Directorate of Income Tax (PR, PP & OL) 6 th Floor, Mayur Bhawan, Connaught Circus New Delhi-110001 i This publication should not

Tax Payers Information Series - 35 TDS ON SALARIES INCOME TAX DEPARTMENT Directorate of Income Tax (PR, PP & OL) 6 th Floor, Mayur Bhawan, Connaught Circus New Delhi-110001 i This publication should not

TDS Provisions and Compliances under GST

GST Alert 09/2018-19 Date 15.09.2018 TDS Provisions and Compliances under GST Government vide Notification No. 33/2017-Central Tax dated 15.09.2017 had notified Section 51 of CGST Act, 2017 relating Tax

GST Alert 09/2018-19 Date 15.09.2018 TDS Provisions and Compliances under GST Government vide Notification No. 33/2017-Central Tax dated 15.09.2017 had notified Section 51 of CGST Act, 2017 relating Tax

6. Detailed information to be given on amount debited to P & L a/c of Capital Expenses, Personal Expenses, and Advertisement.

CBDT has vide Notification no. 33/2014 dated 25.07.2014 revised the format of Tax Audit Report to be furnished under section 44AB of the Income tax Act with effect from 25.07.2014. We have compiled below

CBDT has vide Notification no. 33/2014 dated 25.07.2014 revised the format of Tax Audit Report to be furnished under section 44AB of the Income tax Act with effect from 25.07.2014. We have compiled below

Tax Payers Information Series - 35 TDS ON SALARIES INCOME TAX DEPARTMENT

Tax Payers Information Series - 35 TDS ON SALARIES INCOME TAX DEPARTMENT Directorate of Income Tax (PR, PP & OL) 6 th Floor, Mayur Bhawan, Connaught Circus New Delhi-110001 PREFACE The provisions of the

Tax Payers Information Series - 35 TDS ON SALARIES INCOME TAX DEPARTMENT Directorate of Income Tax (PR, PP & OL) 6 th Floor, Mayur Bhawan, Connaught Circus New Delhi-110001 PREFACE The provisions of the

TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II, SECTION 3, SUB-SECTION (ii)]

![TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II, SECTION 3, SUB-SECTION (ii)]](/thumbs/93/111110471.jpg "TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II, SECTION 3, SUB-SECTION (ii)]") TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II, SECTION 3, SUB-SECTION (ii)] GOVERNMENT OF INDIA MINISTRY OF FINANCE (DEPARTMENT OF REVENUE) (CENTRAL BOARD OF DIRECT TAXES) NOTIFICATION

TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II, SECTION 3, SUB-SECTION (ii)] GOVERNMENT OF INDIA MINISTRY OF FINANCE (DEPARTMENT OF REVENUE) (CENTRAL BOARD OF DIRECT TAXES) NOTIFICATION

FILING OF RETURNS UNDER GST INCLUDING MATCHING OF INPUT TAX CREDIT

FILING OF RETURNS UNDER GST INCLUDING MATCHING OF INPUT TAX CREDIT DRAFT RETURN FORMS FORM NO DETAILS 1. GSTR 1 Details of outward supplies of taxable goods and/or services effected 2. GSTR 01A Details

FILING OF RETURNS UNDER GST INCLUDING MATCHING OF INPUT TAX CREDIT DRAFT RETURN FORMS FORM NO DETAILS 1. GSTR 1 Details of outward supplies of taxable goods and/or services effected 2. GSTR 01A Details

Income Tax Frequently Asked Questions

Income Tax Frequently Asked Questions A. General 1. What is Income Tax? It is a tax imposed by the Government of India on any body who earns income in India. This tax is levied on the strength of an Act

Income Tax Frequently Asked Questions A. General 1. What is Income Tax? It is a tax imposed by the Government of India on any body who earns income in India. This tax is levied on the strength of an Act

TDS & TCS Recent Updates & Amendments.

TDS & TCS Recent Updates & Amendments. By. CA. Tarun Jain. B.com, FCA. Synopsis of Discussion Amendments in Finance act 2016. Amendment to Section 206AA New provisions relating to TCS Other Miscellaneous

TDS & TCS Recent Updates & Amendments. By. CA. Tarun Jain. B.com, FCA. Synopsis of Discussion Amendments in Finance act 2016. Amendment to Section 206AA New provisions relating to TCS Other Miscellaneous

CA RAKESH M. VORA. R P J & ASSOCIATES Chartered Accountants

CA RAKESH M. VORA R P J & ASSOCIATES Chartered Accountants Thursday - 8th March, 2018 1 INDEX Introduction to TDS Compliance Provisions Important Payments covered under the scheme of TDS. Details of TDS

CA RAKESH M. VORA R P J & ASSOCIATES Chartered Accountants Thursday - 8th March, 2018 1 INDEX Introduction to TDS Compliance Provisions Important Payments covered under the scheme of TDS. Details of TDS

ELECTRONIC PAYMENT SYSTEM

ELECTRONIC PAYMENT SYSTEM Instructions for DDOs 1. Each payee is required to be got allocated a unique code (UCP) by furnishing bank details in specified format (Annexure I) at the concerned treasury.

ELECTRONIC PAYMENT SYSTEM Instructions for DDOs 1. Each payee is required to be got allocated a unique code (UCP) by furnishing bank details in specified format (Annexure I) at the concerned treasury.

Applicable from Assessment Year

Recent Developments on TDS. Section 40(a)(ia) No disallowance shall be made, if, after deduction of tax during the previous year, the same is paid by due date of filing return of income. In line with Section

Recent Developments on TDS. Section 40(a)(ia) No disallowance shall be made, if, after deduction of tax during the previous year, the same is paid by due date of filing return of income. In line with Section

25 Penalties Introduction Penalties

25 Penalties 25.1 Introduction The Income-tax Act, 1961 provides for the imposition of a penalty on an assessee who wilfully commits any offence under the provisions of the Act. Penalty is levied over

25 Penalties 25.1 Introduction The Income-tax Act, 1961 provides for the imposition of a penalty on an assessee who wilfully commits any offence under the provisions of the Act. Penalty is levied over

Guidelines for reporting TDS transactions where amount paid to deductee has not exceeded the threshold limit

Twitter Linkedin RSS Facebook Corporate Law FEMA Finance General Info Government Policy IRDA Articles News Notifications/Circulars Home Income Tax ITR 11-12 Service Tax Excise C. Law Judiciary DGFT GST

Twitter Linkedin RSS Facebook Corporate Law FEMA Finance General Info Government Policy IRDA Articles News Notifications/Circulars Home Income Tax ITR 11-12 Service Tax Excise C. Law Judiciary DGFT GST

As approved by Income Tax Department

As approved by Income Tax Department "Form No. 26Q [See section 193, 194, 194A, 194B, 194BB, 194C, 194D, 194EE, 194F, 194G, 194H, 194I, 194J, 194LA, and rule 31A] Quarterly statement of deduction of tax

As approved by Income Tax Department "Form No. 26Q [See section 193, 194, 194A, 194B, 194BB, 194C, 194D, 194EE, 194F, 194G, 194H, 194I, 194J, 194LA, and rule 31A] Quarterly statement of deduction of tax

ANDHRA PRAGATHI GRAMEENA BANK HEAD OFFICE::KADAPA

[ 2) ANDHRA PRAGATHI GRAMEENA BANK HEAD OFFICE::KADAPA Cir.No.90-2006-BC-STF Date: 29.9.06 INCOME TAX e FILING OF TDS RETURNS REF: 1) Cir.No.28-2006-BC-STF, dt.14.7.06, Cir.No.41-2006-BC-STF,dt.31.7.06

[ 2) ANDHRA PRAGATHI GRAMEENA BANK HEAD OFFICE::KADAPA Cir.No.90-2006-BC-STF Date: 29.9.06 INCOME TAX e FILING OF TDS RETURNS REF: 1) Cir.No.28-2006-BC-STF, dt.14.7.06, Cir.No.41-2006-BC-STF,dt.31.7.06

Rectification Manual. Submitting Online Rectification Request. rectify intimation order issued under section 143 (1)

") Rectification Manual Submitting Online Rectification Request to rectify intimation order issued under section 143 (1) by Centralized Processing Center, Bangalore. http://www.itatonline.org If you are thinking

Rectification Manual Submitting Online Rectification Request to rectify intimation order issued under section 143 (1) by Centralized Processing Center, Bangalore. http://www.itatonline.org If you are thinking

The Central Goods and Services Tax Bill, Returns. Arun Kumar Agarwal. 5-May-17

The Central Goods and Services Tax Bill, 2017 Returns Arun Kumar Agarwal info@arsconsultants.net www.arsconsultants.net 1 Statutory Provisions: Chapter Sections 37 to 48 VIII info@arsconsultants.net www.arsconsultants.net

The Central Goods and Services Tax Bill, 2017 Returns Arun Kumar Agarwal info@arsconsultants.net www.arsconsultants.net 1 Statutory Provisions: Chapter Sections 37 to 48 VIII info@arsconsultants.net www.arsconsultants.net

Tax Deduction at Source FY (AY )

") Tax Deduction at Source FY 2017-18 (AY 2018-19) CA Pranjal Joshi M.com, F.C.A., DipIFR (ACCA-UK), Cert. Business Valuation (ICAI) M/s Pranjal Joshi & Co Chartered Accountants TDS introduction - Income

Tax Deduction at Source FY 2017-18 (AY 2018-19) CA Pranjal Joshi M.com, F.C.A., DipIFR (ACCA-UK), Cert. Business Valuation (ICAI) M/s Pranjal Joshi & Co Chartered Accountants TDS introduction - Income

Tax Payers Information Series - 35 TDS ON SALARIES

Tax Payers Information Series - 35 TDS ON SALARIES INCOME TAX DEPARTMENT Directorate of Income Tax (PR, PP & OL) 6 th Floor, Mayur Bhawan, Connaught Circus New Delhi-110001 i This publication should not

Tax Payers Information Series - 35 TDS ON SALARIES INCOME TAX DEPARTMENT Directorate of Income Tax (PR, PP & OL) 6 th Floor, Mayur Bhawan, Connaught Circus New Delhi-110001 i This publication should not

PUNJAB STATE TRANSMISSION CORPORATION LIMITED

PUNJAB STATE TRANSMISSION CORPORATION LIMITED (Regd. Office: PSEB, Head Office, The Mall, Patiala-147001, Punjab, India) Corporate Identity Number - U40109PB2010SGC033814, Office of CFO, AO/Taxation, Shakti

PUNJAB STATE TRANSMISSION CORPORATION LIMITED (Regd. Office: PSEB, Head Office, The Mall, Patiala-147001, Punjab, India) Corporate Identity Number - U40109PB2010SGC033814, Office of CFO, AO/Taxation, Shakti

RECENT AMENDMENTS REGARDING TDS/TCS w.e.f

RECENT AMENDMENTS REGARDING TDS/TCS w.e.f. 01.06.2016 There are continuous changes in the Tax Deduction at Source/Tax Collection at source provisions of Income tax Act from year to year. During this year

RECENT AMENDMENTS REGARDING TDS/TCS w.e.f. 01.06.2016 There are continuous changes in the Tax Deduction at Source/Tax Collection at source provisions of Income tax Act from year to year. During this year

FORM NO. 16. [See rule 31(1)(a)] PART A. Certificate under Section 203 of the Income-tax Act, 1961 for tax deducted at source on salary

![FORM NO. 16. [See rule 31(1)(a)] PART A. Certificate under Section 203 of the Income-tax Act, 1961 for tax deducted at source on salary](/thumbs/82/85338733.jpg "FORM NO. 16. [See rule 31(1)(a)] PART A. Certificate under Section 203 of the Income-tax Act, 1961 for tax deducted at source on salary") FORM NO. 16 [See rule 31(1)(a)] PART A Certificate under Section 23 of the Income-tax Act, 1961 for tax deducted at source on salary Certificate No. SFGNQTI Last updated on 22-May-215 Name and address

FORM NO. 16 [See rule 31(1)(a)] PART A Certificate under Section 23 of the Income-tax Act, 1961 for tax deducted at source on salary Certificate No. SFGNQTI Last updated on 22-May-215 Name and address

Electronic Tax Liability Register of Taxpayer (Part I: Return related liabilities)

") GST Payment of Tax Rule Sr # Form # Payment of Tax Rules Title of Form Analysis 1 Form GST 1) Electronic Tax Liability Register PMT-01 (1) The electronic tax liability register under sub-section (7) of

GST Payment of Tax Rule Sr # Form # Payment of Tax Rules Title of Form Analysis 1 Form GST 1) Electronic Tax Liability Register PMT-01 (1) The electronic tax liability register under sub-section (7) of

CHANGES IN INCOME TAX BY UNION BUDGET 2017

CHANGES IN INCOME TAX BY UNION BUDGET 2017 CA SOHRABH JINDAL The Hon ble Finance Minister has announced the Union Budget 2017 on 1-2-2017. There are various changes in Law related to Income Tax. I have

CHANGES IN INCOME TAX BY UNION BUDGET 2017 CA SOHRABH JINDAL The Hon ble Finance Minister has announced the Union Budget 2017 on 1-2-2017. There are various changes in Law related to Income Tax. I have

Beginners Course on GST (Registration, Returns, Payment & Documentation) organised by WIRC 3rd October Presenter CA Mandar Telang

organised by WIRC 3rd October Presenter CA Mandar Telang") Beginners Course on GST (Registration, Returns, Payment & Documentation) organised by WIRC Presenter CA Mandar Telang 1 Registration 2 Registration Legal Framework v Taxable Person means a person who carries

Beginners Course on GST (Registration, Returns, Payment & Documentation) organised by WIRC Presenter CA Mandar Telang 1 Registration 2 Registration Legal Framework v Taxable Person means a person who carries

Area/locality; Town/City/District; State; Country. Pin code is mandatory. Tick mark the appropriate box for residential status. For non-residents cert

(ii) (iii) (iv) by furnishing the return electronically under digital signature; by transmitting the data in the return electronically under electronic verification code; by transmitting the data in the

(ii) (iii) (iv) by furnishing the return electronically under digital signature; by transmitting the data in the return electronically under electronic verification code; by transmitting the data in the

FORM NO. 16. [See rule 31(1)(a)] PART A. Certificate under Section 203 of the Income-tax Act, 1961 for tax deducted at source on salary

![FORM NO. 16. [See rule 31(1)(a)] PART A. Certificate under Section 203 of the Income-tax Act, 1961 for tax deducted at source on salary](/thumbs/77/76609738.jpg "FORM NO. 16. [See rule 31(1)(a)] PART A. Certificate under Section 203 of the Income-tax Act, 1961 for tax deducted at source on salary") FORM NO. 16 [See rule 31(1)(a)] PART A Certificate under Section 203 of the Income-tax Act, 1961 for tax deducted at source on salary Certificate No. AWQDYQH Last updated on 20-May-2014 HAVELLS INDIA LTD

FORM NO. 16 [See rule 31(1)(a)] PART A Certificate under Section 203 of the Income-tax Act, 1961 for tax deducted at source on salary Certificate No. AWQDYQH Last updated on 20-May-2014 HAVELLS INDIA LTD

MAX HYPERMARKET INDIA PRIVATE LIMITED

MAX HYPERMARKET INDIA PRIVATE LIMITED Form 16 Details in Form 16: Date: 27/05/2016 Employee Name: CHETHAN KUMAR. Employee PAN: BBHPK6665A Financial Year: 2015-16 Assessment Year: 2016-17 Details of signature:

MAX HYPERMARKET INDIA PRIVATE LIMITED Form 16 Details in Form 16: Date: 27/05/2016 Employee Name: CHETHAN KUMAR. Employee PAN: BBHPK6665A Financial Year: 2015-16 Assessment Year: 2016-17 Details of signature:

(d) Has the statement been filed earlier for this quarter (Yes/No) Permanent Account Number (PAN) [See Note 1] of original statement.

![(d) Has the statement been filed earlier for this quarter (Yes/No) Permanent Account Number (PAN) [See Note 1] of original statement.](/thumbs/75/72793927.jpg "(d) Has the statement been filed earlier for this quarter (Yes/No) Permanent Account Number (PAN) [See Note 1] of original statement.") As approved by Income Tax Department "Form No.24Q [See section 192 and rule 31A] Quarterly Statement of deduction of tax under sub section (3) of section 200 of the Income tax Act in respect of salary

As approved by Income Tax Department "Form No.24Q [See section 192 and rule 31A] Quarterly Statement of deduction of tax under sub section (3) of section 200 of the Income tax Act in respect of salary

WESTERN INDIA REGIONAL COUNCIL OF ICAI

1 WESTERN INDIA REGIONAL COUNCIL OF ICAI E-Filing of Income Tax Returns PDF processed with CutePDF evaluation edition www.cutepdf.com Endeavor of CPC to promote voluntary compliance; to educate tax payers

1 WESTERN INDIA REGIONAL COUNCIL OF ICAI E-Filing of Income Tax Returns PDF processed with CutePDF evaluation edition www.cutepdf.com Endeavor of CPC to promote voluntary compliance; to educate tax payers

Tax Audit Clause related 8. Clause 4: What if the assessee is NOT registered under Indirect tax Acts, but is liable to pay tax therein?

Tax Audit Rept Issues F Discussion CA K.Gururaj Acharya, Bangale General Issues 1. Considering the limit of 60 TAs per partner, if a Firm has A & B as Partners and Partner A signs 120 repts & B doesn t

Tax Audit Rept Issues F Discussion CA K.Gururaj Acharya, Bangale General Issues 1. Considering the limit of 60 TAs per partner, if a Firm has A & B as Partners and Partner A signs 120 repts & B doesn t

CIRCULAR NO. 9/2008, Dated: September 29, 2008 GOVERNMENT OF INDIA MINISTRY OF FINANCE (DEPARTMENT OF REVENUE) CENTRAL BOARD OF DIRECT TAXES

CENTRAL BOARD OF DIRECT TAXES") CIRCULAR NO 9/2008, Dated: September 29, 2008 GOVERNMENT OF INDIA MINISTRY OF FINANCE (DEPARTMENT OF REVENUE) CENTRAL BOARD OF DIRECT TAXES DEDUCTION OF TAX AT SOURCE INCOME TAX DEDUCTION FROM SALARIES

CIRCULAR NO 9/2008, Dated: September 29, 2008 GOVERNMENT OF INDIA MINISTRY OF FINANCE (DEPARTMENT OF REVENUE) CENTRAL BOARD OF DIRECT TAXES DEDUCTION OF TAX AT SOURCE INCOME TAX DEDUCTION FROM SALARIES

TCS Provision at a Glance for FY

TCS Provision at a Glance for FY 2017-18 Who is Liable to Collect TCS As per Section 206C(1), Every Person being a seller of Goods of nature specified in table below shall, At the time of debiting to the

TCS Provision at a Glance for FY 2017-18 Who is Liable to Collect TCS As per Section 206C(1), Every Person being a seller of Goods of nature specified in table below shall, At the time of debiting to the

TDS / TCS IMPLICATIONS ANUJ PATCHIGAR & ASSOCIATES CHARTERED ACCOUNTANTS

TDS / TCS IMPLICATIONS Compiled by ANUJ PATCHIGAR & ASSOCIATES CHARTERED ACCOUNTANTS DISCLAIMER: Anuj Patchigar & Associates has taken due care and caution in compilation and presenting factually correct

TDS / TCS IMPLICATIONS Compiled by ANUJ PATCHIGAR & ASSOCIATES CHARTERED ACCOUNTANTS DISCLAIMER: Anuj Patchigar & Associates has taken due care and caution in compilation and presenting factually correct

MONTHLY COMMUNIQUÉ JUNE 2011

INCOME TAX Income Tax Issuance and Authentication of Form 16A: Presently, in relation to withholding Service Tax taxes/tds, the certificate in Form 16A is generated by the deductors and issued to FEMA

INCOME TAX Income Tax Issuance and Authentication of Form 16A: Presently, in relation to withholding Service Tax taxes/tds, the certificate in Form 16A is generated by the deductors and issued to FEMA

F. No. 275/27/2013-IT(B) Government of India Ministry of Finance Department of Revenue Central Board of Direct Taxes

Government of India Ministry of Finance Department of Revenue Central Board of Direct Taxes") Circular No. 07/2014 All Chief Commissioners of Income-tax All Directors General of Income-tax Sub: Ex-post facto extension of due date for filing TDS/TCS statements for FYs 2012-13 and 2013-14 regarding

Circular No. 07/2014 All Chief Commissioners of Income-tax All Directors General of Income-tax Sub: Ex-post facto extension of due date for filing TDS/TCS statements for FYs 2012-13 and 2013-14 regarding

Tax Liability Ledger, will reflect the total tax liability of a tax payer (after netting) for the particular month.

for the particular month.") ELECTRONIC LEDGERS & PAYMENTS Once a tax payer is registered on the common portal GSTN, two e-ledgers Cash Ledger & Input Tax Credit Ledger and an Electronic Tax liability ledger will be automatically

ELECTRONIC LEDGERS & PAYMENTS Once a tax payer is registered on the common portal GSTN, two e-ledgers Cash Ledger & Input Tax Credit Ledger and an Electronic Tax liability ledger will be automatically

UNION BUDGET

UNION BUDGET 2017-18 Hon ble Prime Minister Narendra Modi has shown his determination to come heavily on tax evaders. He has also shown his commitment to eliminate high value cash transactions from the

UNION BUDGET 2017-18 Hon ble Prime Minister Narendra Modi has shown his determination to come heavily on tax evaders. He has also shown his commitment to eliminate high value cash transactions from the

Major direct tax proposals in Finance Bill, 2017

Major direct tax proposals in Finance Bill, 2017 Member firm Individual, HUF, BOI, AOP, AJP Tax Rates There is no change in the basic exemption limit for individuals/hufs. It is proposed to reduce the

Major direct tax proposals in Finance Bill, 2017 Member firm Individual, HUF, BOI, AOP, AJP Tax Rates There is no change in the basic exemption limit for individuals/hufs. It is proposed to reduce the

Instructions for filling up Form 49B

(a) (b) (c) (d) (e) (f) (g) (h) Instructions for filling up Form 49B Form is to be filled legibly in ENGLISH in BLOCK LETTERS and in BLACK INK only. Each box, wherever provided, should contain only one

(a) (b) (c) (d) (e) (f) (g) (h) Instructions for filling up Form 49B Form is to be filled legibly in ENGLISH in BLOCK LETTERS and in BLACK INK only. Each box, wherever provided, should contain only one

An overview of Section 195 and foreign payments of the Income-tax Act at The Institute of Chartered Accountants of India, Seminar of TDS

An overview of Section 195 and foreign payments of the Income-tax Act at The Institute of Chartered Accountants of India, Seminar of TDS by CA Shailendra Sharma 07 April 2018 Agenda Brief overview of the

An overview of Section 195 and foreign payments of the Income-tax Act at The Institute of Chartered Accountants of India, Seminar of TDS by CA Shailendra Sharma 07 April 2018 Agenda Brief overview of the

Instructions for filling up Form No. 49B

Instructions for filling up Form No. 49B (a) (b) (c) (d) (e) (f) (g) (h) Form is to be filled legibly in ENGLISH in BLOCK LETTERS. While filling the form, each box, wherever provided, should contain onl

Instructions for filling up Form No. 49B (a) (b) (c) (d) (e) (f) (g) (h) Form is to be filled legibly in ENGLISH in BLOCK LETTERS. While filling the form, each box, wherever provided, should contain onl

Issues in E-filing of Tax Audit Report. Bombay Chartered Accountants Society

Issues in E-filing of Tax Audit Report Bombay Chartered Accountants Society 8 th November, 2014 AMEET N. PATEL Partner Sudit K Parekh & Co. Chartered Accountants Mumbai Pune Hyderabad New Delhi Bangalore

Issues in E-filing of Tax Audit Report Bombay Chartered Accountants Society 8 th November, 2014 AMEET N. PATEL Partner Sudit K Parekh & Co. Chartered Accountants Mumbai Pune Hyderabad New Delhi Bangalore

Implementation of TCS in Tally.ERP 9

Implementation of TCS in Tally.ERP 9 The information contained in this document is current as of the date of publication and subject to change. Because Tally must respond to changing market conditions,

Implementation of TCS in Tally.ERP 9 The information contained in this document is current as of the date of publication and subject to change. Because Tally must respond to changing market conditions,

TDS under section 195 of the Income-tax Act. CA Vishal Palwe 16 December 2017 Seminar on International Taxation at WIRC

TDS under section 195 of the Income-tax Act CA Vishal Palwe 16 December 2017 Seminar on International Taxation at WIRC Overview of section 195 Overview of section 195 195(1) Any person paying to non-resident

TDS under section 195 of the Income-tax Act CA Vishal Palwe 16 December 2017 Seminar on International Taxation at WIRC Overview of section 195 Overview of section 195 195(1) Any person paying to non-resident

PROCEDURAL ASPECTS OF TAX DEDUCTED AT SOURCE BY: CA SANJAY K. AGARWAL

PROCEDURAL ASPECTS OF TAX DEDUCTED AT SOURCE BY: CA SANJAY K. AGARWAL Mob : 9811080342, E-mail id: agarwal.s.ca@gmail.com Highlights Rates of TDS Procedure and Scheme Relevant statutory provisions Section

PROCEDURAL ASPECTS OF TAX DEDUCTED AT SOURCE BY: CA SANJAY K. AGARWAL Mob : 9811080342, E-mail id: agarwal.s.ca@gmail.com Highlights Rates of TDS Procedure and Scheme Relevant statutory provisions Section

Tax is imposition financial charge or other levy upon a taxpayer by a state or other the functional equivalent of the state.

1. What is Tax What is Tax? Tax is imposition financial charge or other levy upon a taxpayer by a state or other the functional equivalent of the state. How many Types of Taxes are there and what are they?

1. What is Tax What is Tax? Tax is imposition financial charge or other levy upon a taxpayer by a state or other the functional equivalent of the state. How many Types of Taxes are there and what are they?

EXECUTIVE SUMMARY FEMA Regulations

Doha Chapter of ICAI 5 th January 2014 Relevant Changes in FEMA regulations and Direct & Indirect Taxation affecting Real Estate Transactions, with reference to NRI by CA R.BUPATHY PAST PRESIDENT - ICAI

Doha Chapter of ICAI 5 th January 2014 Relevant Changes in FEMA regulations and Direct & Indirect Taxation affecting Real Estate Transactions, with reference to NRI by CA R.BUPATHY PAST PRESIDENT - ICAI

The Centre of Excellence for GST. GST: Returns. JULY 09, 2017 ICAI Tower, BKC MUMBAI. CA. Hemant P. Vastani. The Centre of Excellence for GST

GST: Returns JULY 09, 2017 ICAI Tower, BKC MUMBAI CA. Hemant P. Vastani 1 Sections Covering Returns 37. Furnishing details of outward supplies. 38. Furnishing details of inward supplies. 39. Furnishing

GST: Returns JULY 09, 2017 ICAI Tower, BKC MUMBAI CA. Hemant P. Vastani 1 Sections Covering Returns 37. Furnishing details of outward supplies. 38. Furnishing details of inward supplies. 39. Furnishing

GST Update. Weekly Update N a t i o n a l A c a d e m y o f C u s t o m s, I n d i r e c t T a x e s a n d N a r c o t i c s ( N A C I N )

") GST Update Weekly Update 02.02.2019 1 Background This Presentation covers the GST changes / observations/ press releases/ Tweet FAQs/ Sectoral FAQs released by CBEC since the last update on 26.01.2019.

GST Update Weekly Update 02.02.2019 1 Background This Presentation covers the GST changes / observations/ press releases/ Tweet FAQs/ Sectoral FAQs released by CBEC since the last update on 26.01.2019.

Indian Overseas Bank. RFP Reference No: BSMD/TDS/RFP/01/ Date:

Indian Overseas Bank RFP Reference No: BSMD/TDS/RFP/01/2017-18 Date:24.1.2018 Request for Proposal for Appointment of Consultant for Centralization of TDS Returns of the Bank and Compliance thereof in

Indian Overseas Bank RFP Reference No: BSMD/TDS/RFP/01/2017-18 Date:24.1.2018 Request for Proposal for Appointment of Consultant for Centralization of TDS Returns of the Bank and Compliance thereof in

As proposed in The Finance Bill, 2017 introduced by Finance Minister of India on 1 st February, 2017.

Budget 2017-18 Highlights for Non-Residents As proposed in The Finance Bill, 2017 introduced by Finance Minister of India on 1 st February, 2017. The Indian Budget has provisions affecting the taxability

Budget 2017-18 Highlights for Non-Residents As proposed in The Finance Bill, 2017 introduced by Finance Minister of India on 1 st February, 2017. The Indian Budget has provisions affecting the taxability

FORM NO. 16. [See rule 31(1)(a)] PART A. Certificate under Section 203 of the Income-tax Act, 1961 for tax deducted at source on salary

![FORM NO. 16. [See rule 31(1)(a)] PART A. Certificate under Section 203 of the Income-tax Act, 1961 for tax deducted at source on salary](/thumbs/78/78446801.jpg "FORM NO. 16. [See rule 31(1)(a)] PART A. Certificate under Section 203 of the Income-tax Act, 1961 for tax deducted at source on salary") FORM NO. 16 [See rule 31(1)(a)] PART A Certificate under Section 203 of the Income-tax Act, 1961 for tax deducted at source on salary Certificate No. SMOOPZJ Last updated on 01-Jun-2016 Name and address

FORM NO. 16 [See rule 31(1)(a)] PART A Certificate under Section 203 of the Income-tax Act, 1961 for tax deducted at source on salary Certificate No. SMOOPZJ Last updated on 01-Jun-2016 Name and address

FORM NO. 16. [See rule 31(1)(a)] PART A. Certificate under Section 203 of the Income-tax Act, 1961 for tax deducted at source on salary

![FORM NO. 16. [See rule 31(1)(a)] PART A. Certificate under Section 203 of the Income-tax Act, 1961 for tax deducted at source on salary](/thumbs/77/75514926.jpg "FORM NO. 16. [See rule 31(1)(a)] PART A. Certificate under Section 203 of the Income-tax Act, 1961 for tax deducted at source on salary") FORM NO. 16 [See rule 31(1)(a)] PART A Certificate under Section 23 of the Income-tax Act, 1961 for tax deducted at source on salary Last updated on 4-Oct-216 Name and address of the Employer D S KULKARNI

FORM NO. 16 [See rule 31(1)(a)] PART A Certificate under Section 23 of the Income-tax Act, 1961 for tax deducted at source on salary Last updated on 4-Oct-216 Name and address of the Employer D S KULKARNI

NEW TDS PROCEDURES- NOTIFICATIONS OF MARCH Chartered Accountant New Delhi

NEW TDS PROCEDURES- NOTIFICATIONS OF MARCH 2009 Presentation by : CA. Kapil Goel, ACA, LLB Chartered Accountant New Delhi cakapilgoel @gmail.com OBJECT/SCOPE To deliberate and discuss the new TDS procedures

NEW TDS PROCEDURES- NOTIFICATIONS OF MARCH 2009 Presentation by : CA. Kapil Goel, ACA, LLB Chartered Accountant New Delhi cakapilgoel @gmail.com OBJECT/SCOPE To deliberate and discuss the new TDS procedures

FORM NO.16A. Certificate No : DC/Q1/26Q/ [See rule 31(1)(b)]

![FORM NO.16A. Certificate No : DC/Q1/26Q/ [See rule 31(1)(b)]](/thumbs/77/75515073.jpg "FORM NO.16A. Certificate No : DC/Q1/26Q/ [See rule 31(1)(b)]") Original FORM NO.16A Certificate No : DC/Q1/26Q/1 [See rule 31(1)(b)] Certificate under section 23 of the Income-tax Act, 1961 for Tax deducted at source Name and address of the Deductor Andheri B-1 Sai

Original FORM NO.16A Certificate No : DC/Q1/26Q/1 [See rule 31(1)(b)] Certificate under section 23 of the Income-tax Act, 1961 for Tax deducted at source Name and address of the Deductor Andheri B-1 Sai

Chapter IX Returns Statutory Provision 37. Furnishing details of outward supplies

Chapter IX Returns Statutory Provision 37. Furnishing details of outward supplies (1) Every registered taxable person, other than an input service distributor, a non-resident taxable person and a person

Chapter IX Returns Statutory Provision 37. Furnishing details of outward supplies (1) Every registered taxable person, other than an input service distributor, a non-resident taxable person and a person

CA. Annapurna Kabra

By CA. Annapurna Kabra 9972077441 I) Payment under GST Type of payment Due date Modes of payment with Rules and collection of tax Collection of incorrect amount / rate of GST Omission to collect GST in

By CA. Annapurna Kabra 9972077441 I) Payment under GST Type of payment Due date Modes of payment with Rules and collection of tax Collection of incorrect amount / rate of GST Omission to collect GST in

Virtual Certificate Course on GST

Virtual Certificate Course on GST Presented by: CA Jayesh Gogri On: 18 th June, 2017 MAINTENANCE OF RECORDS AND BOOKS UNDER GST LAW 6/18/2017 CA. Jayesh M. Gogri 2 TYPES OF ELECTRONIC LEDGERS 6/18/2017

Virtual Certificate Course on GST Presented by: CA Jayesh Gogri On: 18 th June, 2017 MAINTENANCE OF RECORDS AND BOOKS UNDER GST LAW 6/18/2017 CA. Jayesh M. Gogri 2 TYPES OF ELECTRONIC LEDGERS 6/18/2017

1 Introduction 2 Tax Return 3 Goods and Services Tax Return 4 GST Model Law and Draft GST Rules 5 Outward supplies return (GSTR-1)

") Topic 1 Introduction 2 Tax Return 3 Goods and Services Tax Return 4 GST Model Law and Draft GST Rules 5 Outward supplies return (GSTR-1) Page 6 Outward Supply details 7 Post ling of GSTR-1 8 Inward Supply

Topic 1 Introduction 2 Tax Return 3 Goods and Services Tax Return 4 GST Model Law and Draft GST Rules 5 Outward supplies return (GSTR-1) Page 6 Outward Supply details 7 Post ling of GSTR-1 8 Inward Supply

DUTIES & RESPONSIBILITIES OF TAX DEDUCTOR UNDER THE GOODS AND SERVICES TAX ACTS

Page 1 of 8 DUTIES & RESPONSIBILITIES OF TAX DEDUCTOR UNDER THE GOODS AND SERVICES TAX ACTS What is GST? Goods and Services Tax (GST) is one indirect tax for the whole Nation, which will make India one

Page 1 of 8 DUTIES & RESPONSIBILITIES OF TAX DEDUCTOR UNDER THE GOODS AND SERVICES TAX ACTS What is GST? Goods and Services Tax (GST) is one indirect tax for the whole Nation, which will make India one

Common Errors made while filling Income Tax returns explained

Common Errors made while filling Income Tax returns explained For AY 2009-10 onwards, E-returns are being processed u/s143 (1) at CPC Bangalore. In some cases, taxpayers have requested for rectification

Common Errors made while filling Income Tax returns explained For AY 2009-10 onwards, E-returns are being processed u/s143 (1) at CPC Bangalore. In some cases, taxpayers have requested for rectification

FORM NO. 24Q (See section 192 and rule 31A)

") FORM NO. 24Q (See section 192 and rule 31A) Quarterly statement of deduction of tax under sub-section (3) of section 200 of the Income-tax Act, 1961 in respect of salary for the quarter ended June/September/December/March

FORM NO. 24Q (See section 192 and rule 31A) Quarterly statement of deduction of tax under sub-section (3) of section 200 of the Income-tax Act, 1961 in respect of salary for the quarter ended June/September/December/March

FSIA E-circular dt ( TDS on Purchase of Property)

") FSIA E-circular dt. 17.6.2013 ( TDS on Purchase of Property) Faridabad Small Industries Association The face of Modern Indian MSMEs www.fsiaindia.com FSIA Park, Opp. Plot No.23, Sector-24, Faridabad- 121005,

FSIA E-circular dt. 17.6.2013 ( TDS on Purchase of Property) Faridabad Small Industries Association The face of Modern Indian MSMEs www.fsiaindia.com FSIA Park, Opp. Plot No.23, Sector-24, Faridabad- 121005,