In the Financial World TDS is Tax deducted at. TDS contributes 40% to the gross direct tax

|

|

|

- Gwendoline Terry

- 6 years ago

- Views:

Transcription

1

2 In the Financial World TDS is Tax deducted at Source TDS contributes 40% to the gross direct tax collections

3 It has been brought with the principle of Pay As you Earn i.e. Collection of Tax in Advance. If no TDS is deducted, expenses are Disallowed u/s 40a(ia).

4 Who : Every deductor When : Where : Within one month of first deduction of Tax TIN FCs/NSDL How : In form 49B

5 1 ST Step 2 nd Step 3 rd Step 4 th Step Deduct Tax as per provision Deposit to Govt Account in Challan 281 File Quarterly statements Issue TDS Certificates

Non obtaining a TAN ii) Non Quoting of TAN iii) Providing false TAN PENALTY OF Rs.")

6 Mandatory to quote TAN on Quarterly statements Challans TDS Certificates Other documents pertaining to transactions i) Non obtaining a TAN ii) Non Quoting of TAN iii) Providing false TAN PENALTY OF Rs. 10,000/- in each case (Sec 272BB)

7 Chapter XVII of the Income Tax Act deals with TDS & TCS -Section 190 to 206CA deal with laws and procedures for both TDS and TCS

8 DEDUCTOR- ANY PERSON DEDUCTEE- RESIDENT OR NON RESIDENT RATE OF TDS : SLAB RATE APPLICABLE TO SPECIFIC EMPLOYEES ON THE BASIS OF HIS ESTIMATED INCOME. ON ACTUAL PAYMENT

9 DEDUCTOR - ANY PERSON DEDUCTEE RESIDENT RATE OF TDS 10% LIMIT : >=5000. NOTE: NO TDS IF:- 1. SECURITIES IS IN DEMAT FORM AND 2. IS LISTED ON STOCK EXCHANGE

10 DEDUCTOR- ANY PERSON DEDUCTEE- RESIDENT OR NON RESIDENT RATE -10% LIMIT : >=2500. NOTE : NO TDS ON DIVIDEND EXEMPT U/S 115-O, TDS ON DEEMED DIVIDEND U/S 2(22)(e).

11 DEDUCTOR- PERSON LIABLE TO GET THEIR BOOKS AUDITED DEDUCTEE RESIDENT RATE 10% LIMITS: >=10000 WHERE PAYER IS BANKING CO., CO-OP. SOCIETY BANK, POST OFFICE >=5000 IN OTHER CASE NOTES: NO TDS : 1. PAYMENT IS MADE TO BANK; FINANCIAL CORP. ESTB. UNDER ANY CENTRAL, STATE, PROVINCIAL ACT; PARTNER OF FIRM.. 2. INT. UNDER INCOME TAX 3. ON ZERO COUPOUN BOND Note:- Even if the amount is credited to suspense account or any other account, TDS to be made

12 Person to be an individual or HUF Person to be a Resident Indian Individual should be less than 60 years old Tax calculated on Total Income is nil The total interest income for the year is less than the minimum exemption limit of that year, which is Rs 2,50,000 for financial year the CBDT has issued Notification No. 6/2017to provide that New Form 15G/15H needs to be filed whenever estimated total income changes and new investments are made by the taxpayer.

13 DEDUCTOR ANY PERSON DEDUCTEE ANY PERSON RATE 30% LIMIT : >=10000

14 DEDUCTOR- PERSON LIABLE TO GET THEIR BOOKS AUDITED DEDUCTEE RESIDENT RATE: PAYEE IS IND. OR HUF 1% ANY OTHER ASSESSEE 2% LIMIT: SINGLE CONTRACT >=30000 ANNUAL AGG. AMOUNT >= NOTES : 1. NO TDS IF PAYMENT IS FOR PERSONAL PURPOSE OF IND. OR HUF. 2. NO TDS IF TRANSPORTER FURNISHES HIS PAN, DECLARATION OF HAVING LESS THAN 10 TRUCKS. 3. TDS ON INVOICE VALUE EXCLUDING MATERIALS AMOUNT IF SEPARATELY SHOWN, ELSE ON WHOLE AMOUNT

15 DEDUCTOR- PERSON LIABLE TO GET THEIR BOOKS AUDITED DEDUCTEE RESIDENT RATE : 5% LIMIT: =>15000 NOTE : NO TDS ON PAYMENT BY BSNL & MTNL TO THEIR PCO FRANCHISEES NO TDS ON TRANSACTION RELATED TO SECURITIES

16 DEDUCTOR- PERSON LIABLE TO GET THEIR BOOKS AUDITED DEDUCTEE RESIDENT RATE : FOR USE OF PLANT & MACHINERY 2% FOR USE OF LAND,BUILDING, FURNITURE AND FITTING 10% LIMIT : =>1,80,000 NOTE : 1. TDS TO BE DEDUCTED ON WAREHOUSING CHARGES AND NON REFUNDABLE DEPOSITS ALSO 2. NO TDS ON SERVICE TAX COMPONENT

17 DEDUCTOR PERSON LIABLE TO GET THEIR BOOKS AUDITED DEDUCTEE ANY RESIDENT RATE : 1% LIMIT: >50,00,000 NOTE : NO TDS ON ACQUISITION OF AGRICULTURE LAND.

18 new section 194-IB in the Act provide that Individuals or a HUF (other than those covered under 44AB of the Act), responsible for paying to a resident any income by way of rent exceeding fifty thousand rupees for a month or part of month during the previous year, shall deduct an amount equal to five per cent. of such income as income-tax thereon. tax shall be deducted on such income at the time of credit of rent, for the last month of the previous year or the last month of tenancy if the property is vacated during the year, as the case may be, to the account of the payee or at the time of payment thereof in cash or by issue of a cheque or draft or by any other mode, whichever is earlier. In order to reduce the compliance burden, the deductor shall not be required to obtain tax deduction account number (TAN) as per section 203A of the Act. It is also proposed that the deductor shall be liable to deduct tax only once in a previous year.

19 It starts with non-obstante clause to exclude applicability of section 194-IA. The payer or tax deductor would be any person. The payee would be an individual or a HUF being a resident. There is monetary consideration payable under specified agreement WHICH is registered. Tax would be 10%. Tax at source should be deducted at earliest of credit to the account of payee or actual payment of money consideration. No threshold limit provided.

20 DEDUCTOR- PERSON LIABLE TO GET THEIR BOOKS AUDITED DEDUCTEE RESIDENT RATE : 10% LIMIT :=>30,000 NOTE: NO TDS IF PROFESSIONAL FEES PAID BY NON RESIDENT TO RESIDENT THROUGH BANKING CHANNELS AND NON RESIDENT DO NOT HAVE ANY AGENT IN INDIA NO TDS ON PAYMENT MADE BY IND. & HUF FOR PERSONAL PURPOSE.

21 DEDUCTOR ANY PERSON DEDUCTEE NON RESIDENT OR FOREIGN COMPANY RATE : AT THE RATE IN FORCE

For March month : It is 30 th")

22 7 th of Next Month (except for month of March) For March month : It is 30 th April

23 If any person does not deduct or doesn t pay or after so deducting fails to pay whole or part of the tax as required by or under this Act, he or it shall, without prejudice to any other consequences which he or it may incur, be deemed to be an assessee in default in respect of such tax. Such person shall also be liable to pay interest U/s 201(1A) & Penalty.

24 Where the assessee after deducting TDS fails to pay the tax as required by or under this Act Liable to simple 18% p.a [i.e. 1.5% p.m.] from the date on which the tax was deducted till the date on which the payment is actually made. Where the assessee fails to deduct TDS and make the payment as required by or under this Act Liable to simple 12% p.a [i.e. 1% p.m.] from the date on which the tax was deductible till the date on which the TDS deducted.

25 Interest U/s 201(1A) shall be paid before filing TDS returns. Where tax has not been paid after deduction, the tax + interest shall be charged.

26 Section 234 E Applicable to Returns due after 01/07/2012 Non filing & Late filing of TDS, TCS Returns ` 200/- per day maximum to the extent of TDS/TCS To be paid while filing TDS Statement.

27 Form 24Q Quaterly Last Day of Next Month of quarter & 31 st May for the Last Quarter Form 27Q Quaterly As Above Form 26Q Quarterly Same as for Form 24Q, 27Q Form 27EQ Quaterly 15 th of Next month of quarter & 15 th May for last quarter

28 Sec 271C: Penalty equal to the amount that the deductor failed to deduct/collect Prosecution (Sec 276B): If a person fails to pay to the credit of the Central Government, Rigorous imprisonment for a term which shall not be less than three months but which may extend to seven years and with fine.

29 Sr No. Section Reason Penalty / Interest B Non Payment of TDS Prosecution Proceedings with Imprisonment for a Term of 3 months extend up to 7 year (2) Compounding of section 276 B Assesse in default u/s 201(1A) Penalty equals to total of Tax in Arrears 4 40(a)(i)/(ii) Non Deduction of TDS Expenses Are disallowed (2) Demand u/s 156 Additional Interest of 1 % per month

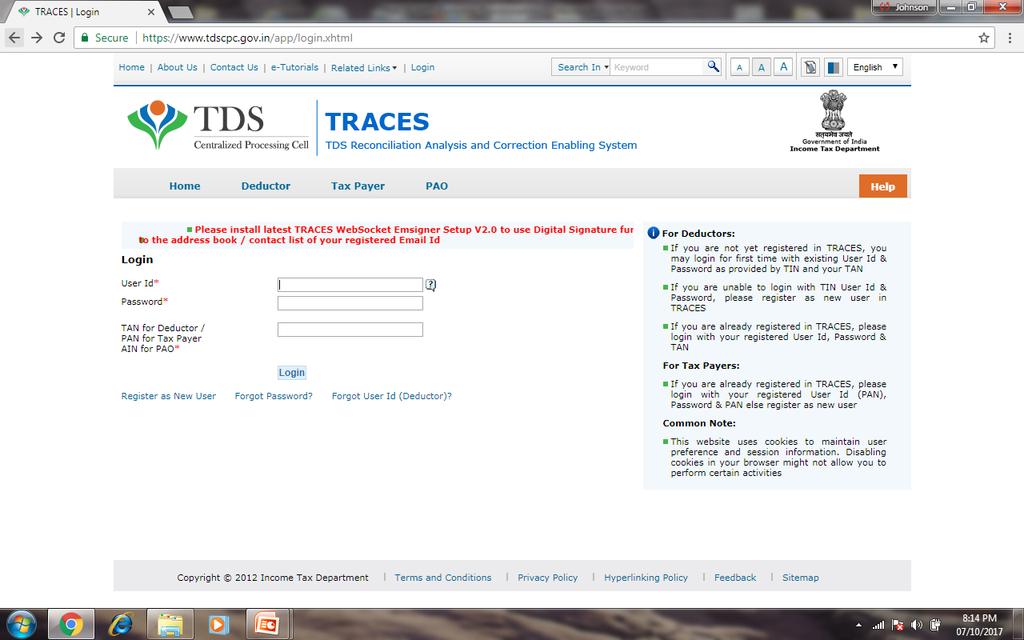

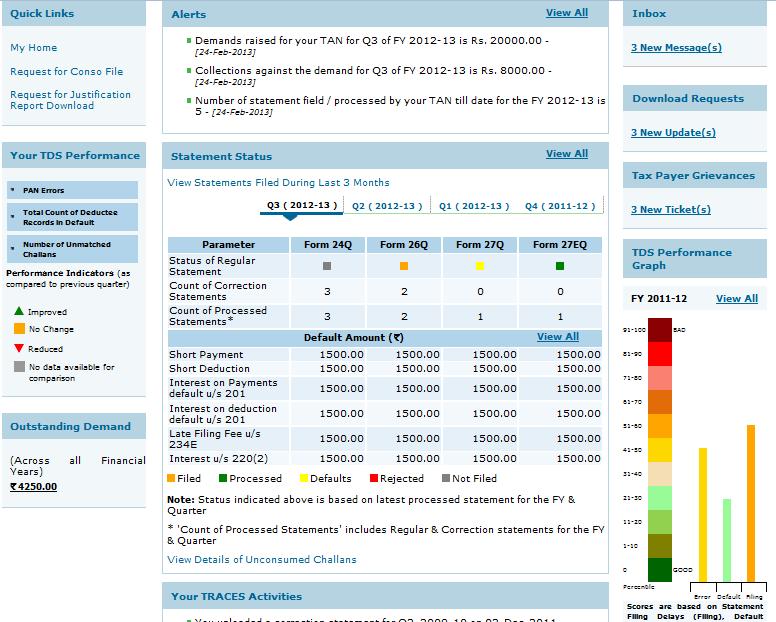

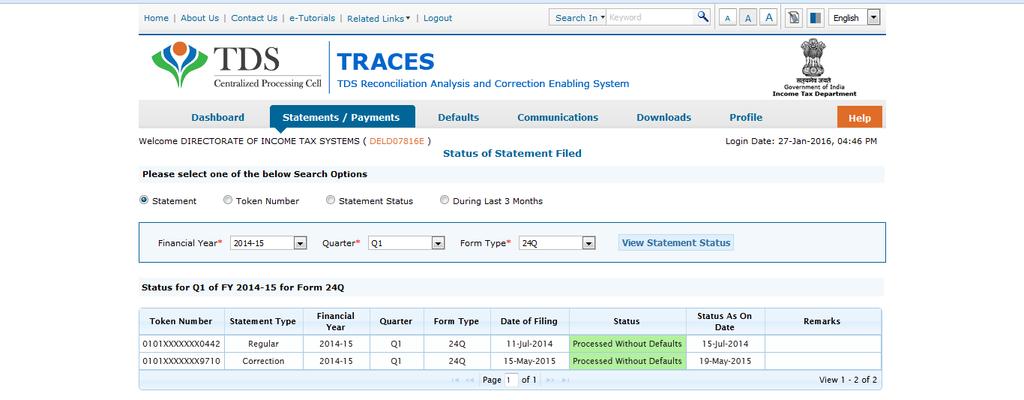

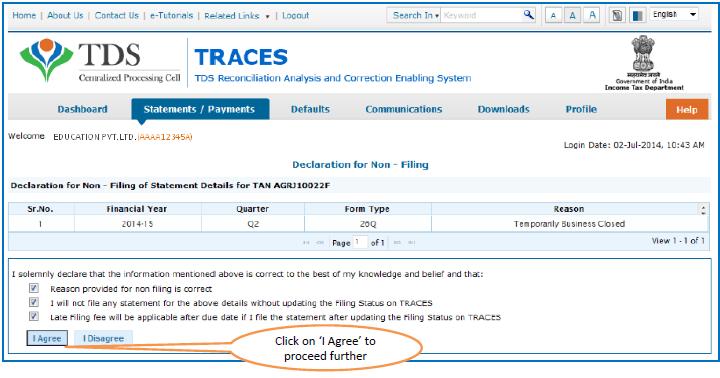

30 6 201(2) After Deduction Non Charge is created Payment on the Asset of the Entity 7 201(1A) Late Payment of TDS Interest is charged at a rate of 1.5 % per month 8 271C On Failure to Deduct TDS as required to be Deducted H Failure to File TDS Return/ Incorrect return Filed Penalty is equal to the amount of failure Penalty of minimum Rs.10,000/- up to Rs.1,00,000/- Rs. 200/- Per Day E Fees for Late Filing TDS Return A (2) Non Issuance of TDS Rs. 100/- per Day Certificate BB Non Compliance of Penalty of Provision under sec Rs.10,000/- 203 A

31 EVERY PERSON WHOSE TDS IS DEDUCTED IS MANDATORY REQUIRED TO FURNISH PAN.FROM THIS F.YR IT IS MANDATORY FOR TCS TOO NON FURNISHING THE PAN SHALL LET TAX TO BE DEDUCTED/COLLECTED AT THE HIGHER OF THE FOLLOWING : AT THE RATE SPECIFIED IN THE ACT. AT THE RATE IN FORCE AT THE RATE OF 20%.

32 CONCEPT OF TCS: In this concept the seller of specified goods collect tax from the buyer under the section 206C (1). The whole concept of TCS is from the income tax act is to widen the income tax scope and to include more and more persons into tax grip.

33 Buyer is a person who buys the goods for sale. The mode of buying may be direct purchase, tender or any auction to the specified goods. These are not covered as buyers under the section: - Central/State government. - Public company. - Embassy, High commission or representation of foreign country. - Any club. - Any person who buys the goods for personal consumption & not for sale.

34 Seller of the specified goods is covered in TCS act. Seller may be - individual or huf - firm - co-operative society - company - state or central government - local authority

35 Specified goods are those goods, sale or purchase of which attracts TCS. The list of such goods is: 1- Alcoholic liquor for human consumption. 2- Timber 3- Tendu leaves. 4- Forest produce other than timber and tendu leaves. 5- Scrap or waste 6- Minerals 7- Toll plaza & Parking Lot 8- Minerals being Coal or lignite or iron ore ( )

36 Alcoholic liquor for human consumption 1% Timber 2.5% Tendu leaves 5% Forest produce other than timber and tendu leaves 2.5% Scrap 1% Minerals 2% Toll plaza, Parking lot, Mining and quarrying * 2 %

37 The TCS will be zero or exempt when the buyer buys the goods for manufacturing or Reproduction and not for sale. In this condition the buyer supplies Form 27C to the seller mentioning that he is the not a trader and will reprocess the goods which are purchased with duly stamped and signature. The seller needs to deliver copy of Form 27C to the Commissioner of income tax.

38 Time limit for TDS / TCS Certificates: Form 16 To be issued annually, within 15 days from due date of filing of TDS/TCS statements. Form 16A Within 15 days from due date of filing of TDS/TCS statements Form 27D Within 15 days from due date of filing of TDS/TCS statements

39 TRACES is a web-based application of the Income Tax Department that provides an interface to all stakeholders associated with TDS administration. It enables viewing of challan status, downloading of NSDL Conso File, Default reports, making correction in statement, allows to correct PAN, A.Yr and download TDS Certificates Form 16 / 16A.

40 CPC (TDS) for Deductors TRACES: Dashboard Statement Status and Default payable Deductor Compliance Profile Online Corrections View Defaults Summary Online PAN Verification Statement and Challan Status Downloads TDS Certificates Form 16/ 16A Form 27D Transaction Based Report for Non Residents Consolidated Statement File Justification Reports e-tutorials and FAQs Circular and Notifications CPC (TDS) Communications TAN PAN Consolidated File 13 October

41

42

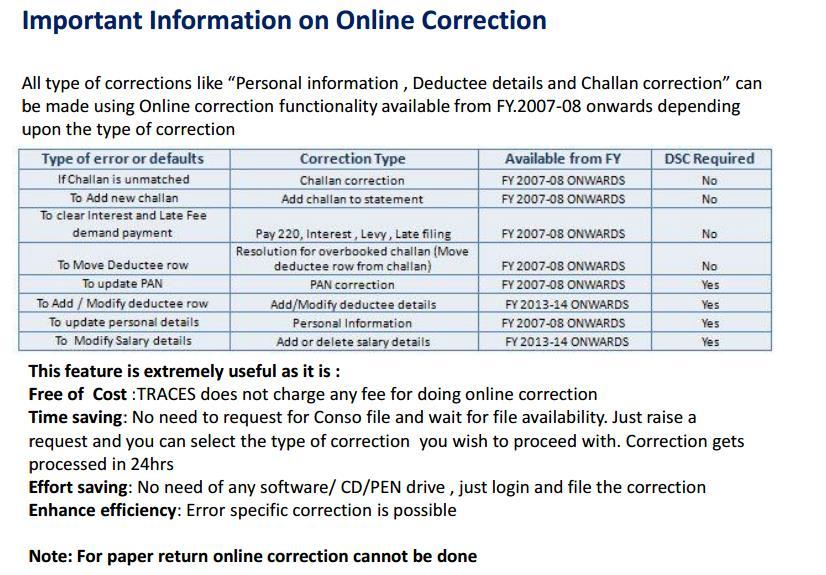

43 Statement Status Challan Status Challan Status for statement View TDS/TCS Credit Pan Verification Request for Conso File 197 Certificate validation Request for refund Track Correction Request Declaration for Non- filing of Statement Declaration to Deposit Lower TDS OLTAS Challan Correction Request for 26A/27BA

44

45 Click here to agree the declaration Click here to go to challan status. If challan is not consumed in any statement, detail will not be displayed Click on Cancel and go to previous page If the user disagree to the declaration, gets two option either add another challan or move back to the challan detail page to accept the declaration 45

46 Furnish Form 26B acknowledgement to your Jurisdictional Assessing Officer within 14 days from the date of transmitting the data electronically. Failing to do so will lead to rejection of your refund request. View the 26B acknowledgement 46

47

48 OLTAS Challan Correction

49 OLTAS Challan Correction

50 Request for 26A/27BA

51 View Default Summary Request for Correction Request for Justification Report Download Track Correction Request View Saved Statement Correction Ready for Submission Tag/Replace Challan Track Request for Tag/Replace Challan

52 This feature enables the Deductor to file Online Correction statements through TRACES portal without downloading TDS/TCS Consolidated File. Following facilities are allowed in Online corrections: PAN Correction Challan Correction Modify Salary details Add challan to statement Modify/Add deductee row Movement of Deductee Rows Update of Personal Information Pay 220I, Late Payment, Late Deduction and Late Filing Interest

53

54 Pay 220I, LPI, LDI and LF Select Pay 220I, LP,LD, Interest, Late filing, Levy from drop down

55 Inbox- Contains notices, intimations from TDS-CPC Request For resolution Resolution Tracking Declaration for Paperless Intimation Notices from Assessing Officer

56 Requested Downloads Form 16/16A/27D Transaction based Report Download Challan Status Inquiry View Your BIN-For Govt. Deductors

57 Aggregated TDS Compliance Functionality If a PAN is associated with more that one TANs for example PAN of the Central Office, Headquarter etc. having more that one TAN of its branches, said PAN can review the "Aggregated TDS Compliance" report on a regular basis to improve TDS compliance at Organization level. PAN can view TDS performance for all of its respective TANs by logging into TRACES as a Taxpayer. The download of the list of defaults of various TANs associated with a PAN will be available in Excel Format for which a request has to be placed.

58 Aggregated TDS Compliance Download Request Page Default can be viewed across all F.Y from F.Y onwards for all TANs Drop Down Values: Total Default, Short Deduction, Short Payment and so on

59 In TRACES website, e-tutorial is given, which is self explanatory. Will help to resolve your problems without coming to the department.

60 THANK YOU

T.D.S/T.C.S AT GLANCE FOR A.Y

T.D.S/T.C.S AT GLANCE FOR A.Y. 2012-2013 Tax Deducted at Source (TDS) was introduced to facilitate the payment of Tax while receiving the income and it follows the concept Pay as you Earn. The tax deducted

T.D.S/T.C.S AT GLANCE FOR A.Y. 2012-2013 Tax Deducted at Source (TDS) was introduced to facilitate the payment of Tax while receiving the income and it follows the concept Pay as you Earn. The tax deducted

TDS & TCS Recent Updates & Amendments.

TDS & TCS Recent Updates & Amendments. By. CA. Tarun Jain. B.com, FCA. Synopsis of Discussion Amendments in Finance act 2016. Amendment to Section 206AA New provisions relating to TCS Other Miscellaneous

TDS & TCS Recent Updates & Amendments. By. CA. Tarun Jain. B.com, FCA. Synopsis of Discussion Amendments in Finance act 2016. Amendment to Section 206AA New provisions relating to TCS Other Miscellaneous

TCS Provision at a Glance for FY

TCS Provision at a Glance for FY 2017-18 Who is Liable to Collect TCS As per Section 206C(1), Every Person being a seller of Goods of nature specified in table below shall, At the time of debiting to the

TCS Provision at a Glance for FY 2017-18 Who is Liable to Collect TCS As per Section 206C(1), Every Person being a seller of Goods of nature specified in table below shall, At the time of debiting to the

TDS Seminar for Residents Welfare Associations

TDS Seminar for Residents Welfare Associations 27 th July 2018 What is TDS? Mode of quick and efficient collection of taxes Tax deducted at the point of generation of income Tax deducted by the payer &

TDS Seminar for Residents Welfare Associations 27 th July 2018 What is TDS? Mode of quick and efficient collection of taxes Tax deducted at the point of generation of income Tax deducted by the payer &

Section - 206C, Income-tax Act,

1 of 8 29-Feb-16 2:27 PM Section - 206C, Income-tax Act, 1961-2015 57 [BB. Collection at source Profits and gains from the business of trading in alcoholic liquor, forest produce, scrap, etc. 58 59 206C.

1 of 8 29-Feb-16 2:27 PM Section - 206C, Income-tax Act, 1961-2015 57 [BB. Collection at source Profits and gains from the business of trading in alcoholic liquor, forest produce, scrap, etc. 58 59 206C.

RECENT AMENDMENTS REGARDING TDS/TCS w.e.f

RECENT AMENDMENTS REGARDING TDS/TCS w.e.f. 01.06.2016 There are continuous changes in the Tax Deduction at Source/Tax Collection at source provisions of Income tax Act from year to year. During this year

RECENT AMENDMENTS REGARDING TDS/TCS w.e.f. 01.06.2016 There are continuous changes in the Tax Deduction at Source/Tax Collection at source provisions of Income tax Act from year to year. During this year

CA RAKESH M. VORA. R P J & ASSOCIATES Chartered Accountants

CA RAKESH M. VORA R P J & ASSOCIATES Chartered Accountants Thursday - 8th March, 2018 1 INDEX Introduction to TDS Compliance Provisions Important Payments covered under the scheme of TDS. Details of TDS

CA RAKESH M. VORA R P J & ASSOCIATES Chartered Accountants Thursday - 8th March, 2018 1 INDEX Introduction to TDS Compliance Provisions Important Payments covered under the scheme of TDS. Details of TDS

TDS & TCS RATE CHART FY

TDS & TCS RATE CHART FY 2017-18 Sl. No Section Of Act Nature of Payment in brief Threshold Limit Rate % From 01.04.17 to 31.03.18 HUF/IND Others 1 192 Salaries Salary income must be more than exemption

TDS & TCS RATE CHART FY 2017-18 Sl. No Section Of Act Nature of Payment in brief Threshold Limit Rate % From 01.04.17 to 31.03.18 HUF/IND Others 1 192 Salaries Salary income must be more than exemption

TDS / TCS IMPLICATIONS ANUJ PATCHIGAR & ASSOCIATES CHARTERED ACCOUNTANTS

TDS / TCS IMPLICATIONS Compiled by ANUJ PATCHIGAR & ASSOCIATES CHARTERED ACCOUNTANTS DISCLAIMER: Anuj Patchigar & Associates has taken due care and caution in compilation and presenting factually correct

TDS / TCS IMPLICATIONS Compiled by ANUJ PATCHIGAR & ASSOCIATES CHARTERED ACCOUNTANTS DISCLAIMER: Anuj Patchigar & Associates has taken due care and caution in compilation and presenting factually correct

Practical difficulties for TDS returns & Previous year defaults.

Practical difficulties for TDS returns & Previous year defaults. Topics covered Basics of TDS TRACES introduction Procedure of TDS return Revision of TDS return Notice and reasons for defaults Causes of

Practical difficulties for TDS returns & Previous year defaults. Topics covered Basics of TDS TRACES introduction Procedure of TDS return Revision of TDS return Notice and reasons for defaults Causes of

Tax Deduction at Source FY (AY )

") Tax Deduction at Source FY 2017-18 (AY 2018-19) CA Pranjal Joshi M.com, F.C.A., DipIFR (ACCA-UK), Cert. Business Valuation (ICAI) M/s Pranjal Joshi & Co Chartered Accountants TDS introduction - Income

Tax Deduction at Source FY 2017-18 (AY 2018-19) CA Pranjal Joshi M.com, F.C.A., DipIFR (ACCA-UK), Cert. Business Valuation (ICAI) M/s Pranjal Joshi & Co Chartered Accountants TDS introduction - Income

CA. Mehul Shah. Payment to Transport Contractors implications under the Income-tax Act Overview of Companies Act Care, Pair, and Share

Payment to Transport Contractors implications under the Income-tax Act 1961 Overview of Companies Act 2013 CA. Mehul Shah B. Com, F.C.A., DISA (ICAI). Care, Pair, and Share The way s not Smooth 03/06/2015

Payment to Transport Contractors implications under the Income-tax Act 1961 Overview of Companies Act 2013 CA. Mehul Shah B. Com, F.C.A., DISA (ICAI). Care, Pair, and Share The way s not Smooth 03/06/2015

CHAPTER 8: RECOVERY OF TAX TAX DEDUCTED AT SOURCE

CHAPTER 8: RECOVERY OF TAX TAX DEDUCTED AT SOURCE SECTIONS RATE PARTICULARS 192: Deduction of Tax on Slab Every Employer has a liability to deduct TDS on salary on monthly basis on tax from salary Rate

CHAPTER 8: RECOVERY OF TAX TAX DEDUCTED AT SOURCE SECTIONS RATE PARTICULARS 192: Deduction of Tax on Slab Every Employer has a liability to deduct TDS on salary on monthly basis on tax from salary Rate

TRACES Site and Issues in Deemed, Recovery & online resolution

TRACES Site and Issues in Deemed, Recovery & online resolution The material contained in the ensuing slides is for general information, compilation is from various websites, views of the experts and the

TRACES Site and Issues in Deemed, Recovery & online resolution The material contained in the ensuing slides is for general information, compilation is from various websites, views of the experts and the

NOTIFICATION NO. 31/2009[F.NO.142/22/2008-TPL]/S.O.858(E), DATED

![NOTIFICATION NO. 31/2009[F.NO.142/22/2008-TPL]/S.O.858(E), DATED](/thumbs/78/78635266.jpg "NOTIFICATION NO. 31/2009[F.NO.142/22/2008-TPL]/S.O.858(E), DATED") INCOME-TAX (EIGHT AMENDMENT) RULES, 2009 - AMENDMENT IN RULES 24Q AND 26Q; SUBSTITUTION OF RULES 30, 31, 31A, 31AA, 37CA, 37D AND FORMS 16, 16A, 16AA, 27D, 27Q AND 27EQ; INSERTION OF FORM 24C; OMISSION

INCOME-TAX (EIGHT AMENDMENT) RULES, 2009 - AMENDMENT IN RULES 24Q AND 26Q; SUBSTITUTION OF RULES 30, 31, 31A, 31AA, 37CA, 37D AND FORMS 16, 16A, 16AA, 27D, 27Q AND 27EQ; INSERTION OF FORM 24C; OMISSION

Income Tax Reckoner AY:

1. Rates of Income Tax Individuals having income > 5 Lacs* Individuals & Charitable Trust Senior Citizen (60 to 79) Very Senior citizen (80 and above) Rates Up to ` 2.00 Lacs Up to ` 2.50 Lacs Up to `

1. Rates of Income Tax Individuals having income > 5 Lacs* Individuals & Charitable Trust Senior Citizen (60 to 79) Very Senior citizen (80 and above) Rates Up to ` 2.00 Lacs Up to ` 2.50 Lacs Up to `

E-TDS FILING PRESENTED BY. Vinod Kumar Jain FCA

E-TDS FILING PRESENTED BY Vinod Kumar Jain FCA What is E- TDS? E-TDS stands for Electronic Tax Deducted at Source introduced by the IT department. Filing e TDS return is compulsory for all assessee and

E-TDS FILING PRESENTED BY Vinod Kumar Jain FCA What is E- TDS? E-TDS stands for Electronic Tax Deducted at Source introduced by the IT department. Filing e TDS return is compulsory for all assessee and

Form No. 26AS (See Section 203AA and second provisio to Section 206C(5) and Rule 31AB)

and Rule 31AB)") Form No. 26AS (See Section 203AA and second provisio to Section 206C(5) and Rule 31AB) PDF generated on 18-12-2012 Annual Tax Statement under section 203AA Permanent Account Number: AJQPP9482N Financial

Form No. 26AS (See Section 203AA and second provisio to Section 206C(5) and Rule 31AB) PDF generated on 18-12-2012 Annual Tax Statement under section 203AA Permanent Account Number: AJQPP9482N Financial

CHANGES IN INCOME TAX BY UNION BUDGET 2017

CHANGES IN INCOME TAX BY UNION BUDGET 2017 CA SOHRABH JINDAL The Hon ble Finance Minister has announced the Union Budget 2017 on 1-2-2017. There are various changes in Law related to Income Tax. I have

CHANGES IN INCOME TAX BY UNION BUDGET 2017 CA SOHRABH JINDAL The Hon ble Finance Minister has announced the Union Budget 2017 on 1-2-2017. There are various changes in Law related to Income Tax. I have

DEDUCTION, COLLECTION AND RECOVERY OF TAX

DEDUCTION, COLLECTION AND RECOVERY OF TAX Section Particulars 190 different modes of payment of tax: tds, tcs, advance tax, tax u/s 192(1A) 191 failure to deduct tax, and direct payment of tax 192 tds

DEDUCTION, COLLECTION AND RECOVERY OF TAX Section Particulars 190 different modes of payment of tax: tds, tcs, advance tax, tax u/s 192(1A) 191 failure to deduct tax, and direct payment of tax 192 tds

Presentation on TDS Salary & TDS in respect of Residents

Presentation on TDS Salary & TDS in respect of Residents R. J. Soni & Associates Corporate Office: MUMBAI Kamla Niwas Plot No. 136/141 Gorai-1 Borivali (W) Mumbai-091. Offices:- MUMBAI JAIPUR PUNE AHEMDABAD

Presentation on TDS Salary & TDS in respect of Residents R. J. Soni & Associates Corporate Office: MUMBAI Kamla Niwas Plot No. 136/141 Gorai-1 Borivali (W) Mumbai-091. Offices:- MUMBAI JAIPUR PUNE AHEMDABAD

Income Tax Reckoner AY:

General* 1. Rates of Income Tax Individuals & Charitable Trust, Senior Citizen (60 to 79) Very Senior citizen (80 and above) (Amount in `) Rates Up to ` 2.00 Lacs Up to ` 2.50 Lacs Up to ` 5.00 Lacs Nil

General* 1. Rates of Income Tax Individuals & Charitable Trust, Senior Citizen (60 to 79) Very Senior citizen (80 and above) (Amount in `) Rates Up to ` 2.00 Lacs Up to ` 2.50 Lacs Up to ` 5.00 Lacs Nil

Note on Tax Deduction at Source

www.legale-services.com Note on Tax Deduction at Source What is Tax Deduction at Source (TDS)? TDS is a way by which a certain percentage of amounts are deducted by a person at the time of making/crediting

www.legale-services.com Note on Tax Deduction at Source What is Tax Deduction at Source (TDS)? TDS is a way by which a certain percentage of amounts are deducted by a person at the time of making/crediting

Evolution and history of TCS

Revised update on provisions relating to Tax Collection at Source u/s 206C of Income Tax Act, 1961 with special reference to amendments made by the Finance Act, 2012 and the Finance Act, 2016 Evolution

Revised update on provisions relating to Tax Collection at Source u/s 206C of Income Tax Act, 1961 with special reference to amendments made by the Finance Act, 2012 and the Finance Act, 2016 Evolution

PENALTY, INTEREST & SURVEY (TDS) 12/02/2011 SANGHVI SANGHVI & SANGHVI

12/02/2011 SANGHVI SANGHVI & SANGHVI") 12/02/2011 SANGHVI SANGHVI & SANGHVI 1 PENAL AND OTHER CONSEQUENCES FOR NON- COMPLIANCE WITH THE PROVISIONS OF TDS DISALLOWANCE OF EXPENDITURE Sec. 40(a)(i) : Expenditure in respect of certain payments

12/02/2011 SANGHVI SANGHVI & SANGHVI 1 PENAL AND OTHER CONSEQUENCES FOR NON- COMPLIANCE WITH THE PROVISIONS OF TDS DISALLOWANCE OF EXPENDITURE Sec. 40(a)(i) : Expenditure in respect of certain payments

Form 26AS. Annual Tax Statement under Section 203AA of the Income Tax Act, 1961

Data updated till 14Feb2013 Form 26AS Annual Tax Statement under Section 203AA of the Income Tax Act, 1961 Permanent Account Number Name of Assessee Address of Assessee AANPK4324N Financial Year 201213

Data updated till 14Feb2013 Form 26AS Annual Tax Statement under Section 203AA of the Income Tax Act, 1961 Permanent Account Number Name of Assessee Address of Assessee AANPK4324N Financial Year 201213

Issues in filing TDS returns

Issues in filing TDS returns Contents Components of TIN Correction statement Consolidated TDS/TCS statement Online TAN registration Annual Tax Statement New @ TIN FILER DEDUCTOR TAX PAYER TIN FC ERACS

Issues in filing TDS returns Contents Components of TIN Correction statement Consolidated TDS/TCS statement Online TAN registration Annual Tax Statement New @ TIN FILER DEDUCTOR TAX PAYER TIN FC ERACS

GOVERNMENT OF INDIA MINISTRY OF FINANCE (DEPARTMENT OF REVENUE) CENTRAL BOARD OF DIRECT TAXES

CENTRAL BOARD OF DIRECT TAXES") GOVERNMENT OF INDIA MINISTRY OF FINANCE (DEPARTMENT OF REVENUE) CENTRAL BOARD OF DIRECT TAXES DEDUCTION OF TAX AT SOURCE- INCOME-TAX DEDUCTION FROM SALARIES UNDER SECTION 192 OF THE INCOME-TAX ACT, 1961

GOVERNMENT OF INDIA MINISTRY OF FINANCE (DEPARTMENT OF REVENUE) CENTRAL BOARD OF DIRECT TAXES DEDUCTION OF TAX AT SOURCE- INCOME-TAX DEDUCTION FROM SALARIES UNDER SECTION 192 OF THE INCOME-TAX ACT, 1961

Analysis of new system for TDS -TCS payment and information reporting

Analysis of new system for TDS -TCS payment and information reporting Income Tax Department has introduced a scheme for centralized processing of annual income-tax returns which envisages no interface

Analysis of new system for TDS -TCS payment and information reporting Income Tax Department has introduced a scheme for centralized processing of annual income-tax returns which envisages no interface

Major direct tax proposals in Finance Bill, 2017

Major direct tax proposals in Finance Bill, 2017 Member firm Individual, HUF, BOI, AOP, AJP Tax Rates There is no change in the basic exemption limit for individuals/hufs. It is proposed to reduce the

Major direct tax proposals in Finance Bill, 2017 Member firm Individual, HUF, BOI, AOP, AJP Tax Rates There is no change in the basic exemption limit for individuals/hufs. It is proposed to reduce the

F.No. 142/22/2008-TPL Government of India Ministry of Finance Department of Revenue Central Board of Direct Taxes

F.No. 142/22/2008-TPL Government of India Ministry of Finance Department of Revenue Central Board of Direct Taxes. New Delhi, the 21 st May, 2009 Subject:- New TDS and TCS payment and information reporting

F.No. 142/22/2008-TPL Government of India Ministry of Finance Department of Revenue Central Board of Direct Taxes. New Delhi, the 21 st May, 2009 Subject:- New TDS and TCS payment and information reporting

Amout over which BB Income by way of winnings horse race 10,000 30% 30% 8 194C Payment to contractors/subcontractors.

TDS Rate Chart Tds Rate chart applicable for Financial Year 2017-18 S.no Section Nature of Income Amout over which Rate of TDS TDS to be deducted If PAN is available If PAN is not available 1 192 Salary

TDS Rate Chart Tds Rate chart applicable for Financial Year 2017-18 S.no Section Nature of Income Amout over which Rate of TDS TDS to be deducted If PAN is available If PAN is not available 1 192 Salary

Tax Deduction and Collection at Source

(iii) Ravi Kumar aged 67 years derived ` 6,00,000 as salary from his employer, XYZ Ltd. for the year ended 31-03- 2019. The following details are provided by him to the employer: Particulars ` Loss from

(iii) Ravi Kumar aged 67 years derived ` 6,00,000 as salary from his employer, XYZ Ltd. for the year ended 31-03- 2019. The following details are provided by him to the employer: Particulars ` Loss from

TDS Provisions and Compliances under GST

GST Alert 09/2018-19 Date 15.09.2018 TDS Provisions and Compliances under GST Government vide Notification No. 33/2017-Central Tax dated 15.09.2017 had notified Section 51 of CGST Act, 2017 relating Tax

GST Alert 09/2018-19 Date 15.09.2018 TDS Provisions and Compliances under GST Government vide Notification No. 33/2017-Central Tax dated 15.09.2017 had notified Section 51 of CGST Act, 2017 relating Tax

IMPORTANT DATES DIRECT TAXES. TDS / TCS returns are to be filed Quarterly.

IMPORTANT DATES DIRECT TAXES TDS / TCS returns are to be filed Quarterly. QUARTER ENDING DUE DATE 30 TH JUNE 15 TH JULY 30 TH SEPTEMBER 15 TH OCTOBER 31 ST DECEMBER 15 TH JANUARY 31 ST MARCH 15 TH MAY

IMPORTANT DATES DIRECT TAXES TDS / TCS returns are to be filed Quarterly. QUARTER ENDING DUE DATE 30 TH JUNE 15 TH JULY 30 TH SEPTEMBER 15 TH OCTOBER 31 ST DECEMBER 15 TH JANUARY 31 ST MARCH 15 TH MAY

CONSEQUENCES OF DEFAULTS IN e-tds RETURNS

CONSEQUENCES OF DEFAULTS IN e-tds RETURNS 1 The material contained in the ensuing slides is for general information, compilation and the views of the speaker and is purely for general discussion at the

CONSEQUENCES OF DEFAULTS IN e-tds RETURNS 1 The material contained in the ensuing slides is for general information, compilation and the views of the speaker and is purely for general discussion at the

PUNJAB STATE TRANSMISSION CORPORATION LIMITED

PUNJAB STATE TRANSMISSION CORPORATION LIMITED (Regd. Office: PSEB, Head Office, The Mall, Patiala-147001, Punjab, India) Corporate Identity Number - U40109PB2010SGC033814, Office of CFO, AO/Taxation, Shakti

PUNJAB STATE TRANSMISSION CORPORATION LIMITED (Regd. Office: PSEB, Head Office, The Mall, Patiala-147001, Punjab, India) Corporate Identity Number - U40109PB2010SGC033814, Office of CFO, AO/Taxation, Shakti

PAN intimation, AIR reporting & recent changes in TCS. D K Bholusaria

PAN intimation, AIR reporting & recent changes in TCS D K Bholusaria dk@bholusaria.com Today s Goal! Understanding background Section 139A(5) and 285BA(1) Rule 114B~114E Changes as compared to previous

PAN intimation, AIR reporting & recent changes in TCS D K Bholusaria dk@bholusaria.com Today s Goal! Understanding background Section 139A(5) and 285BA(1) Rule 114B~114E Changes as compared to previous

GOVERNMENT OF INDIA MINISTRY OF FINANCE (DEPARTMENT OF REVENUE) CENTRAL BOARD OF DIRECT TAXES

CENTRAL BOARD OF DIRECT TAXES") GOVERNMENT OF INDIA MINISTRY OF FINANCE (DEPARTMENT OF REVENUE) CENTRAL BOARD OF DIRECT TAXES DEDUCTION OF TAX AT SOURCE- INCOME-TAX DEDUCTION FROM SALARIES UNDER SECTION 192 OF THE INCOME-TAX ACT, 1961

GOVERNMENT OF INDIA MINISTRY OF FINANCE (DEPARTMENT OF REVENUE) CENTRAL BOARD OF DIRECT TAXES DEDUCTION OF TAX AT SOURCE- INCOME-TAX DEDUCTION FROM SALARIES UNDER SECTION 192 OF THE INCOME-TAX ACT, 1961

TaxPro. Key Features File Validation Utility (FVU) version 5.7

version 5.7") TaxPro Key Features File Validation Utility (FVU) version 5.7 In case of non-availability of PAN of deductee for Form 27EQ, two new fields are introduced under deductee details which are as below: Field

TaxPro Key Features File Validation Utility (FVU) version 5.7 In case of non-availability of PAN of deductee for Form 27EQ, two new fields are introduced under deductee details which are as below: Field

Instructions for filling ITR-1 SAHAJ A.Y

Instructions for filling ITR-1 SAHAJ A.Y. 2018-19 General Instructions These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant

Instructions for filling ITR-1 SAHAJ A.Y. 2018-19 General Instructions These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant

CIRCULAR NO. 8/2012, Dated: October 5, 2012

CIRCULAR NO. 8/2012, Dated: October 5, 2012 Suject: Income Tax Deduction From Salaries during the Financial Year 2012-2013 under Section 192 of The Income Tax Act, 1961. Reference is invited to Circular

CIRCULAR NO. 8/2012, Dated: October 5, 2012 Suject: Income Tax Deduction From Salaries during the Financial Year 2012-2013 under Section 192 of The Income Tax Act, 1961. Reference is invited to Circular

Latest Changes in AIR Reporting norms, Form 15CA-CB and E-initiative(s) of the Income Tax Department

of the Income Tax Department") Latest Changes in AIR Reporting norms, Form 15CA-CB and E-initiative(s) of the Income Tax Department Suresh Wadhwa, LL.B., FCA Time: 19:30 Hrs to 21:30 Hrs Monday, February 15, 2016 at East Delhi C.A.

Latest Changes in AIR Reporting norms, Form 15CA-CB and E-initiative(s) of the Income Tax Department Suresh Wadhwa, LL.B., FCA Time: 19:30 Hrs to 21:30 Hrs Monday, February 15, 2016 at East Delhi C.A.

SEMINAR ON TAX DEDUCTED AT SOURCE PRESENTED BY CA B. D SOUZA

SEMINAR ON TAX DEDUCTED AT SOURCE PRESENTED BY CA B. D SOUZA IS TDS TEDIOUS??? SET UP OF TDS TAN (TAX DEDUCTION ACCOUNT NUMBER) Every deductor is required to obtain a unique identification number called

SEMINAR ON TAX DEDUCTED AT SOURCE PRESENTED BY CA B. D SOUZA IS TDS TEDIOUS??? SET UP OF TDS TAN (TAX DEDUCTION ACCOUNT NUMBER) Every deductor is required to obtain a unique identification number called

RATES OF INCOME-TAX. Nil

1 of 33 07-Oct-11 2:10 AM CIRCULAR INCOME-TAX ACT Section 192 of the Income-tax Act, 1961 - Deduction of tax at source - Salaries - Income-tax deduction from salaries during the financial year 2010-11

1 of 33 07-Oct-11 2:10 AM CIRCULAR INCOME-TAX ACT Section 192 of the Income-tax Act, 1961 - Deduction of tax at source - Salaries - Income-tax deduction from salaries during the financial year 2010-11

Total turnover/ Gross receipts 30% 30% of FY > Rs 50 Cr No change in rate of Surcharge

1. Income Tax Rates: Category of Income New rate of tax Old rate Taxpayer for FY 2017-18 of tax Individuals/ Upto Rs 2.5 L Nil Nil HUF/ BOI/ Rs 2.5 to 5 L 5% 10% AOP/ Rs 5 to 10 L 20% 20% Artificial Above

1. Income Tax Rates: Category of Income New rate of tax Old rate Taxpayer for FY 2017-18 of tax Individuals/ Upto Rs 2.5 L Nil Nil HUF/ BOI/ Rs 2.5 to 5 L 5% 10% AOP/ Rs 5 to 10 L 20% 20% Artificial Above

Webinar on Tax Deduction at Source (TDS) Provisions in GST Regime

Provisions in GST Regime") Webinar on Tax Deduction at Source (TDS) Provisions in GST Regime Mr Rajeev Agarwal, IRS Sr.VP, GSTN In association with National e Governance Division, Department of Electronics & Information Technology

Webinar on Tax Deduction at Source (TDS) Provisions in GST Regime Mr Rajeev Agarwal, IRS Sr.VP, GSTN In association with National e Governance Division, Department of Electronics & Information Technology

Tax is imposition financial charge or other levy upon a taxpayer by a state or other the functional equivalent of the state.

1. What is Tax What is Tax? Tax is imposition financial charge or other levy upon a taxpayer by a state or other the functional equivalent of the state. How many Types of Taxes are there and what are they?

1. What is Tax What is Tax? Tax is imposition financial charge or other levy upon a taxpayer by a state or other the functional equivalent of the state. How many Types of Taxes are there and what are they?

As proposed in The Finance Bill, 2017 introduced by Finance Minister of India on 1 st February, 2017.

Budget 2017-18 Highlights for Non-Residents As proposed in The Finance Bill, 2017 introduced by Finance Minister of India on 1 st February, 2017. The Indian Budget has provisions affecting the taxability

Budget 2017-18 Highlights for Non-Residents As proposed in The Finance Bill, 2017 introduced by Finance Minister of India on 1 st February, 2017. The Indian Budget has provisions affecting the taxability

Highlights of Easwar Committee s Draft Report on Income Tax Law Simplification in India

Highlights of Easwar Committee s Draft Report on Income Tax Law Simplification in India Executive Summary India is leaving no stone unturned to simplify the tax situation. Recently formed Easwar Committee,

Highlights of Easwar Committee s Draft Report on Income Tax Law Simplification in India Executive Summary India is leaving no stone unturned to simplify the tax situation. Recently formed Easwar Committee,

Chapter IX Returns Statutory Provision 37. Furnishing details of outward supplies

Chapter IX Returns Statutory Provision 37. Furnishing details of outward supplies (1) Every registered taxable person, other than an input service distributor, a non-resident taxable person and a person

Chapter IX Returns Statutory Provision 37. Furnishing details of outward supplies (1) Every registered taxable person, other than an input service distributor, a non-resident taxable person and a person

Area/locality; Town/City/District; State; Country. Pin code is mandatory. Tick mark the appropriate box for residential status. For non-residents cert

(ii) (iii) (iv) by furnishing the return electronically under digital signature; by transmitting the data in the return electronically under electronic verification code; by transmitting the data in the

(ii) (iii) (iv) by furnishing the return electronically under digital signature; by transmitting the data in the return electronically under electronic verification code; by transmitting the data in the

Implementation of TCS in Tally.ERP 9

Implementation of TCS in Tally.ERP 9 The information contained in this document is current as of the date of publication and subject to change. Because Tally must respond to changing market conditions,

Implementation of TCS in Tally.ERP 9 The information contained in this document is current as of the date of publication and subject to change. Because Tally must respond to changing market conditions,

FINANCE BILL 2017-DIRECT TAX PROPOSALS AT GLANCE

FINANCE BILL 2017-DIRECT TAX PROPOSALS AT GLANCE COMPILED BY: CA.ARUN GUPTA ca.arungupta77@gmail.com A. Rates of Taxes: 1. It is proposed to make the following changes in tax rates: In case of Resident

FINANCE BILL 2017-DIRECT TAX PROPOSALS AT GLANCE COMPILED BY: CA.ARUN GUPTA ca.arungupta77@gmail.com A. Rates of Taxes: 1. It is proposed to make the following changes in tax rates: In case of Resident

Foreign Contribution (Regulation) Act, 2010 and Rules, By CA R.Durai Rengaswamy Partner Sambandam Associates Chennai

Act, 2010 and Rules, By CA R.Durai Rengaswamy Partner Sambandam Associates Chennai") Foreign Contribution (Regulation) Act, 2010 and Rules, 2011 By CA R.Durai Rengaswamy Partner Sambandam Associates Chennai 1 1. Formalities and Procedures 1.1. Introduction The Foreign Contribution( Regulation)

Foreign Contribution (Regulation) Act, 2010 and Rules, 2011 By CA R.Durai Rengaswamy Partner Sambandam Associates Chennai 1 1. Formalities and Procedures 1.1. Introduction The Foreign Contribution( Regulation)

Tax Deduction / Collection at Source (TDS/ TCS) Part 2. CA Final Course Paper 7 Direct Tax Laws Chapter 28 Rajeev Khandelwal FCA, DISA(ICAI)

Part 2. CA Final Course Paper 7 Direct Tax Laws Chapter 28 Rajeev Khandelwal FCA, DISA(ICAI)") Tax Deduction / Collection at Source (TDS/ TCS) Part 2 CA Final Course Paper 7 Direct Tax Laws Chapter 28 Rajeev Khandelwal FCA, DISA(ICAI) Learning Objective Sectionwise TDS Issues for each section TCS

Tax Deduction / Collection at Source (TDS/ TCS) Part 2 CA Final Course Paper 7 Direct Tax Laws Chapter 28 Rajeev Khandelwal FCA, DISA(ICAI) Learning Objective Sectionwise TDS Issues for each section TCS

List of Issues raised by BCAS for discussion on 26/07/2017

List of Issues raised by BCAS for discussion on 26/07/2017 1 Difference in the fields in ITR form as notified by the CBDT and as put up in the utility on the e-filing site: In ITR 5, in Part B TTI, in

List of Issues raised by BCAS for discussion on 26/07/2017 1 Difference in the fields in ITR form as notified by the CBDT and as put up in the utility on the e-filing site: In ITR 5, in Part B TTI, in

NATURE & REMEDIES. A Presentation by K.M. SHAHI, ITO(TDS) 2(4), MUMBAI

2(4), MUMBAI") NATURE & REMEDIES A Presentation by K.M. SHAHI, ITO(TDS) 2(4), MUMBAI DEFAULTs u/s. 201(1) & MISMATCHEs u/s. 200A Reasons for Default Types of Default How to Correct? What is the Advantage? Show Cause

NATURE & REMEDIES A Presentation by K.M. SHAHI, ITO(TDS) 2(4), MUMBAI DEFAULTs u/s. 201(1) & MISMATCHEs u/s. 200A Reasons for Default Types of Default How to Correct? What is the Advantage? Show Cause

BUDGET 2016 SONALEE GODBOLE

1 BUDGET 2016 SONALEE GODBOLE Penalties 2 3 Section 270A Section 271 levying penalty for failure to furnish returns, comply with notices, concealment of income, etc. will be applicable upto A.Y. 2016-17.

1 BUDGET 2016 SONALEE GODBOLE Penalties 2 3 Section 270A Section 271 levying penalty for failure to furnish returns, comply with notices, concealment of income, etc. will be applicable upto A.Y. 2016-17.

As approved by Income Tax Department

As approved by Income Tax Department "Form No. 26Q [See section 193, 194, 194A, 194B, 194BB, 194C, 194D, 194EE, 194F, 194G, 194H, 194I, 194J, 194LA, and rule 31A] Quarterly statement of deduction of tax

As approved by Income Tax Department "Form No. 26Q [See section 193, 194, 194A, 194B, 194BB, 194C, 194D, 194EE, 194F, 194G, 194H, 194I, 194J, 194LA, and rule 31A] Quarterly statement of deduction of tax

Key changes / amendments to take effect from June 1, 2016

1. Equalisation Levy Section 10 Key changes / amendments to take effect from June 1, 2016 Under section 10, a new Clause 50 has been inserted that provides for exemption of income from specified services

1. Equalisation Levy Section 10 Key changes / amendments to take effect from June 1, 2016 Under section 10, a new Clause 50 has been inserted that provides for exemption of income from specified services

At a Glance Jun 2011 (Brief Updates from the world of Tax and Finance)

") At a Glance Jun (Brief Updates from the world of Tax and Finance) I. Income Tax a. New facility of downloading Form 16A from TIN-NSDL Website To address the problems of mismatch of details between TDS

At a Glance Jun (Brief Updates from the world of Tax and Finance) I. Income Tax a. New facility of downloading Form 16A from TIN-NSDL Website To address the problems of mismatch of details between TDS

PAN Quoting & Reporting of financial transactions

PAN Quoting & Reporting of financial transactions By. CA. Tarun Jain. B.com, FCA. OBJECTIVE To tap the flow of black money To curtail & track unaccounted transactions Discourage cash transactions Encourage

PAN Quoting & Reporting of financial transactions By. CA. Tarun Jain. B.com, FCA. OBJECTIVE To tap the flow of black money To curtail & track unaccounted transactions Discourage cash transactions Encourage

DEDUCTION OF TAX AT SOURCE

DEDUCTION OF TAX AT SOURCE SECTION 190 TO 206AA Section 190 Deduction at source and advance payment Section 191 Direct payment Section 192 Deduction of tax from salary income Section 193 Deduction of tax

DEDUCTION OF TAX AT SOURCE SECTION 190 TO 206AA Section 190 Deduction at source and advance payment Section 191 Direct payment Section 192 Deduction of tax from salary income Section 193 Deduction of tax

TAX AUDIT POINTS TO BE CONSIDERED

TAX AUDIT POINTS TO BE CONSIDERED Contributed by : CA. Tejas Gangar As per section 44AB of the Income tax act, 1961 ( the Act ), certain persons are required to get their accounts audited till 30th September

TAX AUDIT POINTS TO BE CONSIDERED Contributed by : CA. Tejas Gangar As per section 44AB of the Income tax act, 1961 ( the Act ), certain persons are required to get their accounts audited till 30th September

6. Detailed information to be given on amount debited to P & L a/c of Capital Expenses, Personal Expenses, and Advertisement.

CBDT has vide Notification no. 33/2014 dated 25.07.2014 revised the format of Tax Audit Report to be furnished under section 44AB of the Income tax Act with effect from 25.07.2014. We have compiled below

CBDT has vide Notification no. 33/2014 dated 25.07.2014 revised the format of Tax Audit Report to be furnished under section 44AB of the Income tax Act with effect from 25.07.2014. We have compiled below

T. P. Ostwal & Associates (Regd.) Key Budget Proposal Budget 2012 CHARTERED ACCOUNTANTS

Key Budget Proposal Budget 2012 CHARTERED ACCOUNTANTS") IMPORTANT AMENDMENTS & MAJOR DIRECT TAX PROPOSALS IN FINANCE BILL, 2012 CORPORATE TAX No change in the head corporate tax. Extension of sunset date for tax holiday for power sector to 2013; Initial depreciation

IMPORTANT AMENDMENTS & MAJOR DIRECT TAX PROPOSALS IN FINANCE BILL, 2012 CORPORATE TAX No change in the head corporate tax. Extension of sunset date for tax holiday for power sector to 2013; Initial depreciation

Union Budget 2014 Analysis of Major Direct tax proposals

RATES OF INCOME TAX Union Budget 2014 Analysis of Major Direct tax proposals Basic exemption limit has been increased from Rs 2 lacs to Rs 2.50 lacs for resident individuals or HUF. Income slabs Income

RATES OF INCOME TAX Union Budget 2014 Analysis of Major Direct tax proposals Basic exemption limit has been increased from Rs 2 lacs to Rs 2.50 lacs for resident individuals or HUF. Income slabs Income

Beginners Course on GST (Registration, Returns, Payment & Documentation) organised by WIRC 3rd October Presenter CA Mandar Telang

organised by WIRC 3rd October Presenter CA Mandar Telang") Beginners Course on GST (Registration, Returns, Payment & Documentation) organised by WIRC Presenter CA Mandar Telang 1 Registration 2 Registration Legal Framework v Taxable Person means a person who carries

Beginners Course on GST (Registration, Returns, Payment & Documentation) organised by WIRC Presenter CA Mandar Telang 1 Registration 2 Registration Legal Framework v Taxable Person means a person who carries

Web:

PRESENTED ON 1st FEB 2017 HIGHLIGHTS 1 A Rates of Income-tax Rates of income-tax in respect of income liable to tax for the assessment year 2017-18. Rates for deduction of income-tax at source during the

PRESENTED ON 1st FEB 2017 HIGHLIGHTS 1 A Rates of Income-tax Rates of income-tax in respect of income liable to tax for the assessment year 2017-18. Rates for deduction of income-tax at source during the

Guidelines for reporting TDS transactions where amount paid to deductee has not exceeded the threshold limit

Twitter Linkedin RSS Facebook Corporate Law FEMA Finance General Info Government Policy IRDA Articles News Notifications/Circulars Home Income Tax ITR 11-12 Service Tax Excise C. Law Judiciary DGFT GST

Twitter Linkedin RSS Facebook Corporate Law FEMA Finance General Info Government Policy IRDA Articles News Notifications/Circulars Home Income Tax ITR 11-12 Service Tax Excise C. Law Judiciary DGFT GST

WESTERN INDIA REGIONAL COUNCIL OF ICAI

1 WESTERN INDIA REGIONAL COUNCIL OF ICAI E-Filing of Income Tax Returns PDF processed with CutePDF evaluation edition www.cutepdf.com Endeavor of CPC to promote voluntary compliance; to educate tax payers

1 WESTERN INDIA REGIONAL COUNCIL OF ICAI E-Filing of Income Tax Returns PDF processed with CutePDF evaluation edition www.cutepdf.com Endeavor of CPC to promote voluntary compliance; to educate tax payers

UNION BUDGET

UNION BUDGET 2017-18 Hon ble Prime Minister Narendra Modi has shown his determination to come heavily on tax evaders. He has also shown his commitment to eliminate high value cash transactions from the

UNION BUDGET 2017-18 Hon ble Prime Minister Narendra Modi has shown his determination to come heavily on tax evaders. He has also shown his commitment to eliminate high value cash transactions from the

MONTHLY COMMUNIQUÉ JUNE 2011

INCOME TAX Income Tax Issuance and Authentication of Form 16A: Presently, in relation to withholding Service Tax taxes/tds, the certificate in Form 16A is generated by the deductors and issued to FEMA

INCOME TAX Income Tax Issuance and Authentication of Form 16A: Presently, in relation to withholding Service Tax taxes/tds, the certificate in Form 16A is generated by the deductors and issued to FEMA

Current Issues & Vat Compliance in Maharashtra by CA Deepak Thakkar, Mumbai at STPAM Mumbai 3 Oct 2013

Current Issues & Vat Compliance in Maharashtra by, Mumbai at STPAM Mumbai Mahalaxmi Cotton. Vs St. of Mah. (11 May 2012) 51 VST 1 (Bom) & SLP # 10081 of 2013 dt 25 Feb 2013 (SC dismissed the SLP)... Mah.

Current Issues & Vat Compliance in Maharashtra by, Mumbai at STPAM Mumbai Mahalaxmi Cotton. Vs St. of Mah. (11 May 2012) 51 VST 1 (Bom) & SLP # 10081 of 2013 dt 25 Feb 2013 (SC dismissed the SLP)... Mah.

TDS under section 195 of the Income-tax Act. CA Vishal Palwe 16 December 2017 Seminar on International Taxation at WIRC

TDS under section 195 of the Income-tax Act CA Vishal Palwe 16 December 2017 Seminar on International Taxation at WIRC Overview of section 195 Overview of section 195 195(1) Any person paying to non-resident

TDS under section 195 of the Income-tax Act CA Vishal Palwe 16 December 2017 Seminar on International Taxation at WIRC Overview of section 195 Overview of section 195 195(1) Any person paying to non-resident

MAJOR Income Tax Proposals in UNION BUDGET 2017

MAJOR Income Tax Proposals in UNION BUDGET 2017 LUNAWAT & CO. Chartered Accountants 3 rd February 2017, Nehru Place CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA THE CRUX TIMELY FILING OF RETURNS No

MAJOR Income Tax Proposals in UNION BUDGET 2017 LUNAWAT & CO. Chartered Accountants 3 rd February 2017, Nehru Place CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA THE CRUX TIMELY FILING OF RETURNS No

EXECUTIVE SUMMARY FEMA Regulations

Doha Chapter of ICAI 5 th January 2014 Relevant Changes in FEMA regulations and Direct & Indirect Taxation affecting Real Estate Transactions, with reference to NRI by CA R.BUPATHY PAST PRESIDENT - ICAI

Doha Chapter of ICAI 5 th January 2014 Relevant Changes in FEMA regulations and Direct & Indirect Taxation affecting Real Estate Transactions, with reference to NRI by CA R.BUPATHY PAST PRESIDENT - ICAI

FB.COM/SUPERWHIZZ4U Income Tax Amendment for the Assessment

FB.COM/SUPERWHIZZ4U Income Tax Amendment for the Assessment Year 2014-15 - SIPOY SATISH Highlights of Change in Direct Taxes in the Union Budget 2013 1. Rate of Income Tax for Individual a) Slab Rate Assessment

FB.COM/SUPERWHIZZ4U Income Tax Amendment for the Assessment Year 2014-15 - SIPOY SATISH Highlights of Change in Direct Taxes in the Union Budget 2013 1. Rate of Income Tax for Individual a) Slab Rate Assessment

Tax Payers Information Series - 35 TDS ON SALARIES INCOME TAX DEPARTMENT

Tax Payers Information Series - 35 TDS ON SALARIES INCOME TAX DEPARTMENT Directorate of Income Tax (PR, PP & OL) 6 th Floor, Mayur Bhawan, Connaught Circus New Delhi-110001 PREFACE The provisions of the

Tax Payers Information Series - 35 TDS ON SALARIES INCOME TAX DEPARTMENT Directorate of Income Tax (PR, PP & OL) 6 th Floor, Mayur Bhawan, Connaught Circus New Delhi-110001 PREFACE The provisions of the

BCAS LECTURE MEETING 20 st May by CA Raman Jokhakar B. D. Jokhakar & Co.

BCAS LECTURE MEETING 20 st May 2008 by CA Raman Jokhakar B. D. Jokhakar & Co. Who is required to file a return When is it required to be filed Which form is required to be used How is the return to be

BCAS LECTURE MEETING 20 st May 2008 by CA Raman Jokhakar B. D. Jokhakar & Co. Who is required to file a return When is it required to be filed Which form is required to be used How is the return to be

25 Penalties Introduction Penalties

25 Penalties 25.1 Introduction The Income-tax Act, 1961 provides for the imposition of a penalty on an assessee who wilfully commits any offence under the provisions of the Act. Penalty is levied over

25 Penalties 25.1 Introduction The Income-tax Act, 1961 provides for the imposition of a penalty on an assessee who wilfully commits any offence under the provisions of the Act. Penalty is levied over

BUSINESS PROCESSES ON GST RETURN

Content provided by Mr. Vineet Bhatia, Advocate BUSINESS PROCESSES ON GST RETURN Proposed returns in the GST regime are quite detailed in nature, with emphasis on cross-matching of data submitted by various

Content provided by Mr. Vineet Bhatia, Advocate BUSINESS PROCESSES ON GST RETURN Proposed returns in the GST regime are quite detailed in nature, with emphasis on cross-matching of data submitted by various

Income-tax and Death are the only two inevitable things in life In India, taxes were levied even in ancient times refer to Manu Smriti & Arthashastra

Income-tax and Death are the only two inevitable things in life In India, taxes were levied even in ancient times refer to Manu Smriti & Arthashastra Why to Pay Tax? It was only for the good of his subjects

Income-tax and Death are the only two inevitable things in life In India, taxes were levied even in ancient times refer to Manu Smriti & Arthashastra Why to Pay Tax? It was only for the good of his subjects

Amendment of Direct Tax Dhruv Coaching Classes Pvt. Ltd. CMA Akshay Sen Direct Tax

1 Direct Tax (AMENDMENTS) Finance Act, 2017 For CMA Inter & Final (June-18 & Dec-18 Exam.) By CMA AKSHAY SEN Dhruv Coaching Classes Pvt. Ltd. A1-A2,opposite Saras Dairy,Janta Store, Jaipur E-mail-dhruvcoachingclasses@gmail.com

1 Direct Tax (AMENDMENTS) Finance Act, 2017 For CMA Inter & Final (June-18 & Dec-18 Exam.) By CMA AKSHAY SEN Dhruv Coaching Classes Pvt. Ltd. A1-A2,opposite Saras Dairy,Janta Store, Jaipur E-mail-dhruvcoachingclasses@gmail.com

The Institute of Chartered Accountants of India Western India Regional Council

The Institute of Chartered Accountants of India Western India Regional Council Seminar on E-filing of Returns and Forms under Various Acts Mumbai 11 th June 2011 E-filing of Returns and Forms under MVAT

The Institute of Chartered Accountants of India Western India Regional Council Seminar on E-filing of Returns and Forms under Various Acts Mumbai 11 th June 2011 E-filing of Returns and Forms under MVAT

6. PROFITS AND GAINS OF BUSINESS OR PROFESSION 2

Ph: 98851 25025/26 www.mastermindsindia.com 6. PROFITS AND GAINS OF BUSINESS OR PROFESSION 2 SOLUTIONS TO ASSIGNMENT PROBLEMS Problem No. 1 Computing business income for A.Y.2015-16 is as follows Amount

Ph: 98851 25025/26 www.mastermindsindia.com 6. PROFITS AND GAINS OF BUSINESS OR PROFESSION 2 SOLUTIONS TO ASSIGNMENT PROBLEMS Problem No. 1 Computing business income for A.Y.2015-16 is as follows Amount

Instructions for filling out FORM ITR-2

Instructions for filling out FORM ITR-2 1. Legal status of instructions These instructions though stated to be non-statutory, may be taken as guidelines for filling the particulars in this Form. In case

Instructions for filling out FORM ITR-2 1. Legal status of instructions These instructions though stated to be non-statutory, may be taken as guidelines for filling the particulars in this Form. In case

Issues in E-filing of Tax Audit Report. Bombay Chartered Accountants Society

Issues in E-filing of Tax Audit Report Bombay Chartered Accountants Society 8 th November, 2014 AMEET N. PATEL Partner Sudit K Parekh & Co. Chartered Accountants Mumbai Pune Hyderabad New Delhi Bangalore

Issues in E-filing of Tax Audit Report Bombay Chartered Accountants Society 8 th November, 2014 AMEET N. PATEL Partner Sudit K Parekh & Co. Chartered Accountants Mumbai Pune Hyderabad New Delhi Bangalore

DIRECT TAX. E TAXATION August Salary Under Section 17(1) does not includes : A. Wages B. Pension C. Interest D.

does not includes : A. Wages B. Pension C. Interest D.") 1 DIRECT TAX 1 Salary Under Section 17(1) does not includes : A. Wages B. Pension C. Interest D. Gratuity 2 Taxable Allowance from Salary : A. Conveyance allowance B. Dearness Allowances C. Children education

1 DIRECT TAX 1 Salary Under Section 17(1) does not includes : A. Wages B. Pension C. Interest D. Gratuity 2 Taxable Allowance from Salary : A. Conveyance allowance B. Dearness Allowances C. Children education

Specified Date And Tax Audit Penalty Reasonable Causes Tax Auditor & Limit

Western India Regional Council Student Workshop on 7th August, 2015 Tax Audit Under Section 44AB of The Income-Tax Act, 1961 Presented By RAKESH M. VORA RPJ & ASSOCIATES COVERAGE Clause by Clause 23 to

Western India Regional Council Student Workshop on 7th August, 2015 Tax Audit Under Section 44AB of The Income-Tax Act, 1961 Presented By RAKESH M. VORA RPJ & ASSOCIATES COVERAGE Clause by Clause 23 to

GST (GOODS AND SERVICES TAX) TDS MECHANISM UNDER GST

TDS MECHANISM UNDER GST") GST (GOODS AND SERVICES TAX) TDS MECHANISM UNDER GST Tax Deduction at Source (TDS) is a system, initially introduced by the Income Tax Department. It is one of the modes/methods to collect tax, under which,

GST (GOODS AND SERVICES TAX) TDS MECHANISM UNDER GST Tax Deduction at Source (TDS) is a system, initially introduced by the Income Tax Department. It is one of the modes/methods to collect tax, under which,

Updates by Tax & Accounting Professional Forum (TAPF) September 2018

September 2018") Updates by Tax & Accounting Professional Forum (TAPF) September 2018 PREFACE Tax and Accounting Professional Forum (TAPF) is a group of Chartered Accountants, Financial Consultants and Other Professionals.

Updates by Tax & Accounting Professional Forum (TAPF) September 2018 PREFACE Tax and Accounting Professional Forum (TAPF) is a group of Chartered Accountants, Financial Consultants and Other Professionals.

GOODS AND SERVICE TAX FILING OF RETURN. Prepared by Dharmendra Academy of GST Awareness

GOODS AND SERVICE TAX FILING OF RETURN 1 Returns Chapter IX of the CGST/SGST Act, 2017 GST Return Rules, 2017 2 RETURNS: SALIENT FEATURES A return is a statement of specified particulars relating to business

GOODS AND SERVICE TAX FILING OF RETURN 1 Returns Chapter IX of the CGST/SGST Act, 2017 GST Return Rules, 2017 2 RETURNS: SALIENT FEATURES A return is a statement of specified particulars relating to business

SECTION 192 & 194H OF INCOME TAX ACT, 1961

SECTION 192 & 194H OF INCOME TAX ACT, 1961 SONALEE GODBOLE KALYANIWALLA & MISTRY 1 KALYANIWALLA & MISTRY 2 Definition of Salary under section 17 is inclusive - Salary interalia includes wages, annuity

SECTION 192 & 194H OF INCOME TAX ACT, 1961 SONALEE GODBOLE KALYANIWALLA & MISTRY 1 KALYANIWALLA & MISTRY 2 Definition of Salary under section 17 is inclusive - Salary interalia includes wages, annuity

Payment of tax, interest, penalty and other amounts (Section 49)

") FAQ s Chapter VIII Payment of Tax Payment of tax, interest, penalty and other amounts (Section 49) Section 49 of the CGST Act, 2017 made applicable to IGST vide Section 20 of the IGST Act, 2017 and UTGST

FAQ s Chapter VIII Payment of Tax Payment of tax, interest, penalty and other amounts (Section 49) Section 49 of the CGST Act, 2017 made applicable to IGST vide Section 20 of the IGST Act, 2017 and UTGST

(i) Rental income against investment Rs. 15,51,613/- (ii) Signage rent Rs. 7,98,000/- (iii) Parking rent Rs. 24,50,237/-

Rental income against investment Rs. 15,51,613/- (ii) Signage rent Rs. 7,98,000/- (iii) Parking rent Rs. 24,50,237/-") ITAT DELHI JMD Realtors (P.) Ltd. v. Deputy Commissioner of Income-tax IT Appeal No. 5346 (Delhi) of 2011 [Assessment year 2006-07] February 29, 2012 ORDER B.C. Meena, Accountant Member This appeal filed

ITAT DELHI JMD Realtors (P.) Ltd. v. Deputy Commissioner of Income-tax IT Appeal No. 5346 (Delhi) of 2011 [Assessment year 2006-07] February 29, 2012 ORDER B.C. Meena, Accountant Member This appeal filed

F. No. 275/27/2013-IT(B) Government of India Ministry of Finance Department of Revenue Central Board of Direct Taxes

Government of India Ministry of Finance Department of Revenue Central Board of Direct Taxes") Circular No. 07/2014 All Chief Commissioners of Income-tax All Directors General of Income-tax Sub: Ex-post facto extension of due date for filing TDS/TCS statements for FYs 2012-13 and 2013-14 regarding

Circular No. 07/2014 All Chief Commissioners of Income-tax All Directors General of Income-tax Sub: Ex-post facto extension of due date for filing TDS/TCS statements for FYs 2012-13 and 2013-14 regarding

Supplementary Memorandum Explaining the Official Amendments Moved in the Finance Bill, 2012 As Reflected In The Finance Act, 2012

Supplementary Memorandum Explaining the Official Amendments Moved in the Finance Bill, 2012 As Reflected In The Finance Act, 2012 Circular no. 3/2012, dated 12-6-2012 FINANCE ACT, 2012 - PROVISIONS RELATING

Supplementary Memorandum Explaining the Official Amendments Moved in the Finance Bill, 2012 As Reflected In The Finance Act, 2012 Circular no. 3/2012, dated 12-6-2012 FINANCE ACT, 2012 - PROVISIONS RELATING

Supplementary Memorandum Explaining the Official Amendments Moved in the Finance Bill, 2012 AS REFLECTED IN THE FINANCE ACT, 2012.

INCOME TAX CIRCULAR No. 3/2012, Dated 12 th June, 2012. Supplementary Memorandum Explaining the Official Amendments Moved in the Finance Bill, 2012 AS REFLECTED IN THE FINANCE ACT, 2012. FINANCE ACT, 2012

INCOME TAX CIRCULAR No. 3/2012, Dated 12 th June, 2012. Supplementary Memorandum Explaining the Official Amendments Moved in the Finance Bill, 2012 AS REFLECTED IN THE FINANCE ACT, 2012. FINANCE ACT, 2012