Roth Is On the Rise William C. Grossman, ERPA, QPA, APA, MBA

|

|

|

- Adrian Poole

- 5 years ago

- Views:

Transcription

1 Roth Is On the Rise William C. Grossman, ERPA, QPA, APA, MBA

2 Agenda Conversion Background In-plan Roth Conversions Designated Roth and Roth IRA Plan Design Concept: Add After-tax to Increase Roth Contribution Plan Sponsor Roth Conversion Plan Related FAQs Participant Roth Conversion FAQs Substantially Equal Payments For Reference: Roth Contribution and Roth Conversion Calculators Form 1099-R Reporting For Roth Conversions and Roth Distributions 2

3 CONVERSION BACKGROUND

4 Conversion of Pre-Tax to Roth IRA Traditional IRA Conversion to Roth IRA as of 1998 AGI < $100,000; if married file jointly 401(k) roll to traditional IRA convert to a Roth IRA 2008, 401(k) direct rollover to Roth IRA AGI < $100,000; if married file jointly TIPRA* removed AGI as of 2010, Leakage of 401(k) assets: individuals (mostly HCEs) able to do a conversion to a Roth IRA for the first time ever *Tax Increase Prevention and Reconciliation Act of 2005

5 Conversion of Pre-Tax to 401(k) Roth From 2006 until September 27, 2010, Pre-tax 401(k) balances were not allowed to be converted to a 401(k) Roth account. Small Business Jobs Act of 2010 in-plan Roth Rollover conversion to designated Roth with distributable event American Taxpayer Relief Act of 2012 created in-plan Roth Transfer as of 2013 without a distributable event

6 IN-PLAN ROTH CONVERSIONS Small Business Jobs Act of 2010 (SBJA) September 27, 2010; IRS Notice American Taxpayer Relief Act of 2012(ATRA) January 2, 2013; IRS Notice

7 SBJA: Conversion Only for Plans With Designated Roth Provision Conversion only for plan with a Roth account provision i.e. 401(k), 403(b), 457(b) governmental plans May not have Roth provision only for conversions IRRs not allowed in plans that may not have Roth E.g. profit sharing, money purchase IRR Effective upon enactment Sept. 27, 2010 Available for participants or surviving spouses

8 SBJA IRR Requires Distributable Event 2010 to 2012 IRR requires a distributable event Plan may maintain just this provision 2010 conversions only: Tax in 2010; or half in 2011, half in 2012 Any distributable event that is eligible for rollover is valid Withdrawal restrictions apply In-service not available until after age 59½ for: elective deferrals, safe harbor 401(k) contributions, QNECs, QMACs In-service for employer NEC or match 2-year rule (Contribution must be in plan for 2 years) 5-year of participation rule New optional plan provision in-service withdrawal only for Roth conversion In joint committee report, and IRS Notice

9 IRRs Not Treated as a Distribution For: 1. Plan loan transferred to Roth account (without changing its repayment schedule) is not a new loan; 2. Spousal consent is not required to make an IRR; 3. IRRs counted as part of Vested Account Balance when determining if participant s VAB exceeds $5,000; 4. Optional forms of benefit may not be eliminated. Participant s distribution right prior to IRR cannot be eliminated after electing an IRR. (Q/A-3)

10 Tax Consequences: Recapture Tax For IRRs: Under age 59½, 10% penalty waived RECAPTURE TAX The 10% will be applied if the IRR conversion is withdrawn before 5 years unless the participant has a 72(t) exception Recapture tax will not apply if: Attainment of age 59½ Distribution due to severance from service in year age 55 attained or later, A known exception to the penalty occurs

11 Other Considerations Individual must have ability to pay tax on amount converted Disclosures Withdrawing additional amount above conversion and having 100% withholding Requires distributable event If under 59½, distribution above conversion is subject to 10% penalty Disclosure to participant in SMM of plan amendment adding Roth/conversion Of taxes due upon conversion, 402(f) Notice

12 Measuring Five-taxable-year Recapture Period Recapture tax s 5-taxable-year period starts with the first day of participant s tax year in which in-plan Roth conversion made, usually Jan 1. ends on last day of individual s 5th taxable year after conversion. Amounts may be rolled to another Roth without penalty. If withdrawn from subsequent Roth before end of 5-year period, 10% recapture tax will apply. Tracking each year s conversion s 5-year period A separate designated Roth sub-account should be established for each in-plan Roth conversion in order to appropriately apply the recapture tax or acceleration of income rules.

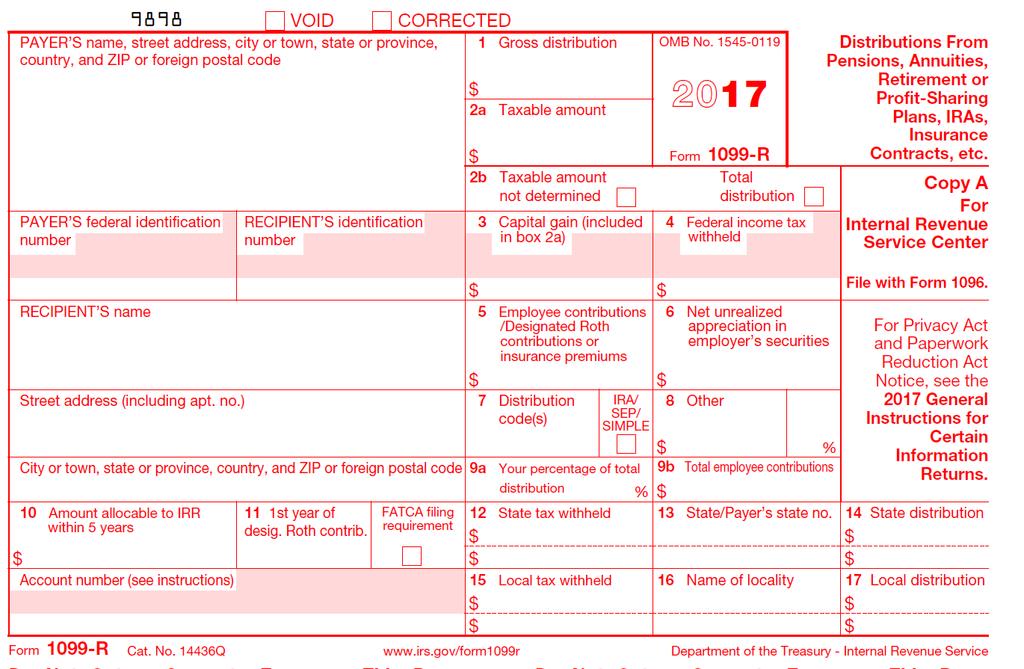

13 Form 1099-R Instructions for Reporting IRR Withdrawn Within Five Years Box 10. Amount Allocable to IRR Within Five Years Enter the amount of the distribution allocable to an IRR made within the five-year period beginning with the first day of the year in which the rollover was made. Do not complete this box if an exception under section 72(t) applies. For further guidance on determining amounts allocable to an IRR, see Notice , Q/A-13.

14 Calculating Earnings on IRR Withdrawn Before Five Years EXAMPLE In 2017, Participant P, age 45, makes a $100,000 in-plan Roth direct rollover from his profit-sharing account At the time of the in-plan Roth direct rollover, P s designated Roth account contains $80,000 of regular Roth contributions and $24,000 of earnings Since this is an in-plan Roth direct rollover, the rollover amount is separately accounted for within the designated Roth account Later in 2017, P takes a $106,000 in-service withdrawal from his designated Roth account The source can only be the in-plan Roth rollover account, since P is under age 59½, which is the earliest the plan allows in-service distributions of elective deferrals from a designated Roth account. However, the plan permitted inservice distributions of the profit sharing amount and that stays on the IRR. At the time of the distribution, P s designated Roth account consists of:

15 Calculating Earnings on IRR Withdrawn Before Five Years In-Plan Roth Rollover Account: In-plan Roth rollover contributions ($10,000 basis). $100,000 Earnings....$6,000 Total...$106,000 Regular Roth Account: Regular Roth contributions..$80,000 Earnings..$24,000 Total.$104,000 Total in designated Roth account..$210,000

16 Calculating Earnings on IRR Withdrawn Before Five Years Under the pro-rata rules of 72, of the $106,000 distribution, $106,000 x 30,000/210,000, or $15,143, is includible in P s gross income All of the $90,857 ($106,000-$15,143) of the distribution that is a return of basis is allocated to the in-plan Roth rollover account P is subject to the additional 10% tax under 72(t) on $105,143 The $90,000 taxable amount of the in-plan Roth rollover under the five-year recapture rule plus $15,143 that is includible in P s gross income under the pro-rata rules of 72

17 Calculating Earnings on IRR Withdrawn Before Five Years Since the amount of the in-plan Roth rollover was $100,000 less $90,857 distributed, there is $9,143 that may still be allocated to the rollover If the $9,143 is distributed within five years of the IRR, none of it will be subject to 72(t) under the five-year recapture rule because all the taxable amount of the in-plan Roth rollover has been used up

18 Series of Conversions An individual may convert a small amount each year instead of converting all at once This enables an individual to spread taxation out Multiple conversion tracking for 5 year recapture tax Required for Form 1099-R, Box 10 is for reporting IRRs withdrawn before 5 years have passed From the Form 1099-R instructions for reporting distributions of in-plan conversions before 5 years have elapsed

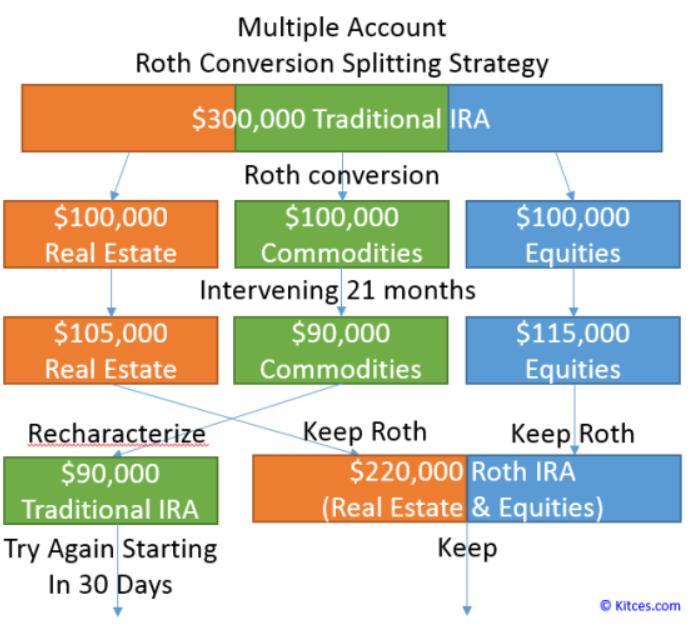

19 Recharacterization: Undoing Roth Conversion Roth IRA conversion reversed by a recharacterization Recharacterization = Roth IRA (with earnings) back to a traditional IRA Recharacterized amount remains tax deferred Deadline to Recharacterize Taxpayers have until the due date of federal income tax return (including extensions) for the year of the Roth IRA conversion to make the recharacterization

20 Recharacterization Example Feb. 2008: John converts $250,000 traditional IRA to Roth IRA. By Feb. 2009, account value has dropped to $150,000. If John takes no further action, he would have to include the $250,000 conversion amount as income for the 2008 tax year, even though it is now worth only $150,000. If John recharacterizes his Roth IRA back into a traditional IRA, the conversion and recharacterization will have no tax consequences for the 2008 tax year. John may again convert this money into a Roth IRA at a later time.

21 Recharacterization Not Permitted for IRR IRR IS NOT PERMITTED TO BE RECHARACTERIZED back to the original 401(k) sources A conversion from 401(k) directly to a Roth IRA may NOT be recharacterized back to a 401(k) plan Note that a conversion from a 401(k) to a Roth IRA may be recharacterized to a traditional IRA

22 Plan Amendment Plan must have Roth deferral provision to permit IRRs Notice Q/A-20: To have a qualified Roth contribution program in place means to have deferral elections permitting Roth deferrals available at the point when the IRR is to be implemented. Document Amendments SBJA snap-on to EGTRRA document, built into PPA document ATRA snap-on amendment to the EGTRRA & PPA document

23 2013 ATRA In-plan Roth Transfers: No Distributable Event Required As of January 1, 2013, a distributable event is not required to make an IRR Section 902 of American Taxpayer Relief Act of 2012, signed into law on January 2, ATRA added an IRR via a transfer option in addition to the IRR option from the Small Business Jobs Act of 2010.

24 N , ATRA & SBJA IRR Rules Otherwise Nondistributable Amounts (ONA) Sources/Amounts not eligible to be distributed but that may be converted by an in-plan Roth rollover (aka Transfer) ATRA Section 903 used this term Otherwise Distributable Amounts (ODA) Sources/Amounts eligible for distribution that could be converted under in-plan Roth Rollover guidance from SBJA 2010

25 Otherwise Nondistributable Amounts Otherwise Nondistributable Amounts (ONAs) Elective deferrals prior to age 59½, plus earnings Matching contributions, plus earnings Safe harbor 401(k) contributions prior to 59½, plus earnings QNECs, QMACs, plus earnings Annual deferrals in Gov t. 457(b), including the federal government s Thrift Savings Plan Money purchase plan accounts that were transferred into a 401(k) plan

26 ATRA IRR Rules for ONAs: Plan Options A plan may restrict: the type of contributions eligible for IRR the frequency of IRRs Subject to 401(a)(4) Benefits, Rights & Features Testing Plan design could provide IRR for only: Otherwise Distributable Amounts (SBJA IRR rules under N ) Both ODA and ONA Amounts In-service for only IRR

27 Notice : Other Rules IRR = not a protected benefit IRR = taxable event triggering net unrealized appreciation IRR = related rollover for top heavy purposes

28 DESIGNATED ROTH AND ROTH IRA

29 Should Individual Make a Roth Deferral or a Roth IRA Contribution? Designated Roth may receive match No income limitations for eligibility to contribute to designated Roth (Roth IRA has income limitations) Higher income employees will be able to contribute to Roth 401(k) 29

30 Roth IRA: Annual Contribution Limits Eligibility rules Earned income from personal services Contributions may be made after age 70½ Eligibility for Roth IRA limited by AGI: 2017 Full Contribution Single or Head of Household Married Filing Jointly Married, Filing Separately $118,000 or less $186,000 or less Partial Contribution $118,001 to $132,999 $186,001 to $195,999 No Contribution $133,000 or more $196,000 or more $9,999 or less N/A $10,000 or more

31 Qualified Distribution Roth distribution is qualified if: 1. Roth has satisfied the 5 year requirement AND 2. Distributable event is: After attainment of age 59½, or After the death of the participant, or If the participant is disabled Any other distribution is treated as non-qualified

32 Pro-Rata Distributions, Not Ordering Designated Roth (401(k), 403(b), gov t. 457(b)) non-qualified distributions: must withdraw pro-rata of Roth and earnings on the Roth Roth IRA non-qualified distributions Roth IRA contributions first Earnings not withdrawn until all other Roth IRA money withdrawn

33 ROTH IRA Ordering Rules Roth IRAs ordering of which sources are to be distributed first (instead of pro-rata) Note: All Roth IRAs are aggregated for these rules (Roth and traditional IRAs are not aggregated) First: Roth IRA contributions OR rollovers from designated Roth accounts Second: Converted funds FIFO: Funds that were taxable FIFO: Funds not taxable such as non-deductible IRA Third: Earnings

34 Roth IRA Distribution Ordering Rules - Example In 2017, Roth IRA: $15,000 cumulative amount of Roth IRA contributions, excluding earnings In addition, there is $40,000 of conversion from a traditional IRA in 2014 In 2017, individual (age 35) withdraws $17,000 The first $15,000 is from Roth IRA contributions $2,000 is from the conversion amount The $2,000 is subject to the 10% penalty, due to withdrawal being made before 5 years of conversion

35 IRS Top 10 Differences Between A ROTH IRA and Designated ROTH

36 Roth IRA Cannot Be Rolled to a 401(k) Roth Law does not permit, there is no conduit Roth IRA Differences in 408 and 401 Differences?

37 What differences? Roth IRA Cannot Be Rolled to a 401(k) Roth 1. Measuring five-year period differences Roth IRA v. Roth 401(k) different clocks Roth IRA, from first Roth IRA Roth 401(k), per employer (unless directly rolled) 2. Ordering Rules for Roth IRA v. Pro-rata rules for Roth 401(k)

38 Roth IRA Conversion Advantages Vs. In-plan Conversion to Roth IRA Traditional IRA to Roth IRA may be recharacterized Roth IRA has no RMD during participant lifetime; beneficiaries subject to RMDs No distributable event required to access Roth IRA cannot be rolled back into 401(k) Possibly less fees In-plan Roth Rollover (conversion) Creditor protection Spousal beneficiary protection Possibly less fees Possible loan Fiduciary provides prudent investments

39 PLAN DESIGN CONCEPT: ADD AFTER-TAX TO INCREASE ROTH CONTRIBUTION

40 Plan Design and After-tax Contributions Notice increased focus by the financial media and created a new interest in after-tax contributions as a plan provision because they can be used to maximize plan contributions and reduce future tax liabilities. Plan design: Provision for after-tax contributions, designated Roth and in-plan Roth rollovers (IRRs). The Concept: 1. Max 415 limit with after-tax $s, then 2. Convert after-tax to Roth via IRR

41 After-tax Conversion via IRR Example Steve is age 60 and earns $225,000 in Steve s 2017 annual additions: $24,000 in 401(k) Roth contributions ($18,000 + $6,000 catch-up) $20,000 in after-tax contributions $16,000 profit sharing contribution In 2017, Steve makes an IRR of $20,200 ($20,000 after-tax, plus $200 earnings) Steve owes taxes on the $200 of earnings for For 2017, Steve added $44,200 to his designated Roth account.

42 Plan Design and After-tax Contributions Caveats for plans with NHCEs include: Excess annual additions. Failed ACP tests. 401(k) safe harbor plans that have matching contributions safe harbored from ACP testing will have an ACP test for just the after-tax amounts. After-tax IRR must include pro-rata amount of earnings on the after-tax (taxed in year of IRR). Note that a plan amendment to add after-tax contributions may be made midyear for safe harbor 401(k) plans, provided midyear amendment guidance is followed.

43 After-tax Conversion via IRR A client inquired: can an after-tax contribution conversion to a designated Roth account be accomplished by contributing after-tax and then rolling just the aftertax amount to the Roth account, leaving the earnings that accrued in the after-tax account in the after-tax source. This is not permitted, as any conversion of after-tax contributions to a designated Roth account must include a pro-rata amount of earnings. A possible option is to convert the after-tax before there are any earnings on it. If there are earnings on after-tax being converted via an IRR, the options are: Include the earnings in the IRR and pay tax on the earnings Roll the after-tax to a Roth IRA and the earnings to a traditional IRA

44 ACP Testing Potential Issues Owner-only One-participant plans face the fewest issues. Plans with NHCEs face ACP testing issues with after-tax contributions. NHCEs generally do not make after-tax contributions, especially in plans that already offer the ability to make designated Roth deferrals. HCEs typically can afford to make after-tax contributions and thus ACP test more likely to fail.

45 ACP Testing Corrections After-tax contribution ACP test failure; correction options: 1. Distribute excess after-tax contributions to HCEs 2. Make a corrective qualified nonelective contribution (QNEC) to NHCEs 3. Make a corrective qualified matching contribution (QMAC) used when an ACP test also involves matching contributions Minimize failures by administratively limiting after-tax contributions.

46 415 Failure Example Ed is age 43 and not an owner. Ed s 2017 annual additions: $18,000 in 401(k) Roth contributions $25,000 in after-tax contributions $13,000 profit sharing contribution, employer made in 2018 for 2017 Ed exceeded 415 limit of $54,000 for 2017 by $2,000 $2,000 refund from his after-tax contributions (adjusted for earnings/losses). (Only the earnings are taxable.) If Ed had already converted all the after-tax and earnings to the Roth account the excess would be distributed from the Roth account.

47 ADP Testing and Recharacterization Failed ADP test amounts may be recharacterized as after-tax contributions and remain in the plan, provided the plan offers after-tax. Re-characterized after-tax contributions are taxed (if from pretax deferrals) and are included in ACP testing. Note: if HCE receiving the refund is catch-up eligible and has not used up the catch-up limit for the year, the refund is required, up to the available catch-up limit, to be recharacterized as catch-up first. If any of the HCEs refund remains, it may be re-characterized as after-tax. The recharacterized after-tax amount is also eligible for an IRR.

48 Rolling After-tax Source to Roth IRA Rolling after-tax to Roth IRA advantages: Back-door contribution to Roth IRA by HCE who is above the annual Roth IRA contribution limit Ordering rules for Roth IRA distributions One Roth IRA 5-year clock for the lifetime of the taxpayer, new money picks up the first Roth IRA s five-year clock No RMDs on Roth IRA, while IRA owner alive For a solo-k, rolling after-tax to a Roth IRA may keep the balance below the $250,000 threshold for Form 5500-EZ

49 PLAN SPONSOR CONVERSION RELATED FAQs

50 FAQs What are some areas of confusion? Understanding The Different Five-Year Clocks Five-year clock for recapture tax Tax-free five-year clock Difference between recapture five-year clock and tax-free five-year clock Roth IRA separate five-year clock from designated Roth

51 Plan Sponsor FAQs Plan Design and Conversions Roth deferrals only? To permit conversions? If conversions: SBJA IRR or ATRA IRR or both? SBJA: Need for a distributable event in order to make a in-plan Roth rollover or conversion to a Roth IRA ATRA: No distributable event for an IRR

52 Plan Sponsor FAQs Plan Design and Conversions Frequency of permitting an IRR conversion? Annual, quarterly, other? Limitation of any sources for conversion? Other than deciding on ONA or ODA Will Money Purchase Source be permitted? After-tax conversions via in-service distribution Adding an in-service provision solely for IRRs Beware of anti-cutback to current in-service provisions

53 PARTICIPANT ROTH CONVERSION FAQs

54 Participant Issues FAQs on Roth Conversions If conversion is for you, what type? IRR, or Roth IRA, or Rollover to traditional IRA and convert to Roth IRA, now or later, or A series of conversions Does participant understand the recapture tax? Does the participant understand recharacterization? Will conversion financially pay off? Paying tax now versus later? Software programs exists CPA for tax advice

55 Participant Considerations Roth Conversions Whether a conversion is right depends on a number of factors Tax free earnings Whether tax rates lower now then when distribution made Estate tax planning, with Roth IRA there are no RMDs, leaving entire amount to beneficiaries Do you need withdrawals within next 5 years? Where is $ coming from to pay taxes on the conversion amount?

56 Participant Considerations Roth Conversions Do you currently maintain IRAs or Roth IRAs? Will the time horizon until retirement enable regeneration of funds used to pay taxes Re-characterization a real possibility? Then it s a Roth IRA conversion (rather than an IRR); and if needed recharacterize to a traditional IRA before tax filing deadline

57

58 Participant Considerations Roth Conversions Is after-tax to be maximized in 401(k) and then moved by IRR? Then, beware 415 limitation; and Beware ACP test Qualified Roth distributions are not included in income for purposes of determining whether Social Security benefits are taxable

59

60 Some Questions to Ponder If under 59 ½, will you need the money in the next five-years? Will you end up in a higher tax bracket? Will your tax bracket be higher now or later? Where will you get the money to pay the conversion taxes?

61 Roth Conversion Issues Long enough time horizon to make up the taxes paid If going to need the Roth conversion to live on before making up the taxes, may never break even If never need to use the Roth money to live on, better odds of coming out ahead

62 Roth Conversion Issues Those best positioned to make up taxes paid, the wealthy and the young. Roth can be used as an estate planning tool, providing heirs with a great source of income-tax free funds. Those subject to estate taxes will find Roth advantageous, since current tax laws penalize the estates of people who die with assets upon which income tax is still owed. Those who inherit a Roth young or convert young have decades of tax-free growth.

63 SUBSTANTIALLY EQUAL PAYMENTS A Different Early Retirement Distribution Strategy

64 Substantially Equal Payments Permits lifetime substantially equal payments to be started at any age. IRC 72(t)(2)(A)(iv) Revenue Ruling QP: must be separated from service IRA: no severance required 10% early distribution penalty waived Must stay with same equal payment until later of: Age 59½, or 5 years of substantially equal payments If break substantially equal payments rule by stopping payments or by taking more, the 10% penalty applies retroactively to all payments

65 Substantially Equal Payments Three methods of calculating the substantially equal payments Amortization Annuitization Required Minimum Distribution Method Uses Uniform Lifetime Table for ages under 70 This uniform lifetime 10 to age 115 Split rollover into more than 1 IRA and apply the substantially equal payment to just 1 IRA. Place enough to get monthly income in 1 IRA Place remainder in another IRA, as available if needed money

66 Uniform Lifetime Table from Rev. Rul For Substantially Equal Payments Using RMD Method

(9), Q&A-1 from")

67 Mortality Table Used To Formulate the Single Life Table in 1.401(a)(9), Q&A-1 from Rev. Rul

68 FOR REFERENCE: ROTH CONTRIBUTION CALCULATORS AND ROTH CONVERSION CALCULATORS

69 2015 and 2017 Tax Rates 2015 tax rates

70 Three Great Unknowns to Guesstimate Tax Rate After You Retire?? What Interest Rate to Use in Your Projection?? How Long Will I Be Retired?? These will each greatly affect the outcome

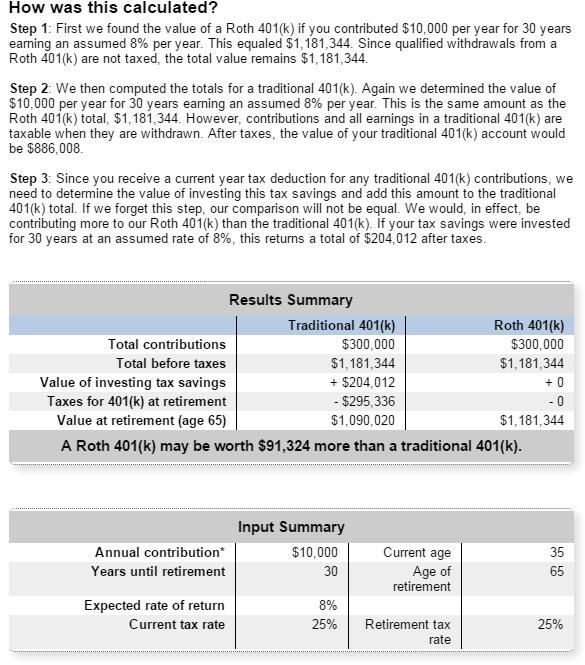

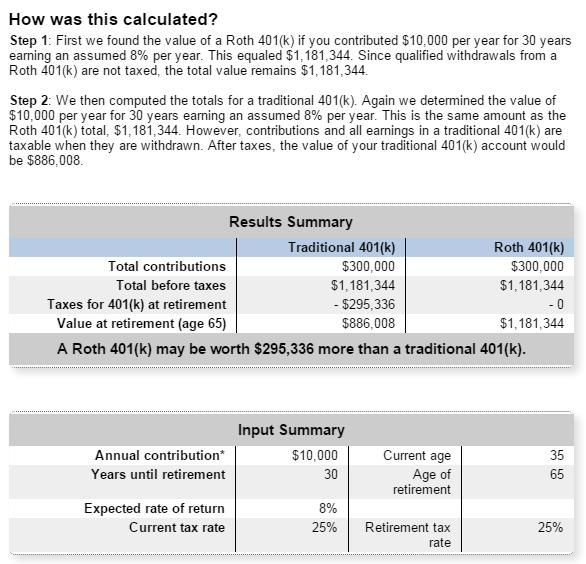

71 30 years of $10,000/year at 8%, Roth 401(k) versus Pre-tax 401(k), 25% Tax Rate, Pre-tax deferral s tax savings not invested Slide 1, great explanation 1 The analyzer calculates average annual withdrawal amounts by assuming that no balance remains when withdrawals end. Early withdrawal penalties and required minimum distributions are not taken into account. The analyzer assumes that all traditional account withdrawals are taxable and that all Roth account withdrawals are qualified, tax-free distributions.

72 30 years of $10,000/year at 8%, Roth 401(k) versus Pre-tax 401(k), 25% Tax Rate, Pre-tax deferral s tax savings not invested Slide 2, great explanation

73 30 years of $10,000/year at 8%, Roth 401(k) versus Pre-tax 401(k), 25% Tax Rate, Pre-tax deferral s tax savings not invested Slide 3, great explanation

74 30 years of $10,000/year at 8%, Roth 401(k) versus Pre-tax 401(k), 25% Tax Rate, Pre-tax deferral s tax savings not invested Slide 4, great explanation 2 A traditional account could provide $2,500 in tax savings on contributions every year before retirement. If invested in a taxable account with the same rates of return as the retirement plan, the tax savings could be worth $210,320 at retirement and could provide $17,579 a year in addition to the traditional account withdrawals. The analyzer deducts federal income taxes from earnings on the taxable account on an annual basis using the income tax rates that you specify. This will tend to understate the performance of the taxable account in circumstances where long-term capital gains and qualified dividends, which are currently taxed at lower rates than ordinary income, are a component of investment returns, as is the case for investments with significant equity holdings.

75 30 years of $10,000/year at 8%, Roth 401(k) versus Pre-tax 401(k), 25% Tax Rate, Pre-tax deferral s tax savings not invested Slide 5, great explanation Future tax rates may change. The analyzer applies tax rates to all taxable income. When estimating your future tax rate, you should consider whether the amount of taxable distributions might push you into a higher tax bracket. Regular investing does not ensure a profit or protect against loss. Hypothetical annual rates of return are not intended to reflect actual results; your results may vary based on market conditions. The analyzer compounds earnings monthly and assumes that withdrawals are made at the beginning of the year. The analyzer does not take certain factors into account, including state and local taxes, required minimum distributions and holding periods, early withdrawal penalties, matching contributions, previous retirement plan contributions and IRS withdrawal rules. Be sure to consult with a financial professional or tax adviser to discuss your specific situation. This analyzer is intended for use in making a rough comparison of Roth and traditional retirement plan accounts. We do not guarantee the accuracy of the results or their relevance to your particular circumstances. Results shown are hypothetical and are not intended to portray actual results. Your results will differ. We encourage you to seek the assistance of your financial professional.

76 401(k) Planner Screen One

77 401(k) Planner Screen 2

78 401(k) Planner Screen 3

79 Roth IRA Conversion or In-plan Roth Rollover $10,000, 20 to Age 65 at 8%, 25% Tax Rate

80 Roth IRA Conversion or In-plan Roth Rollover $10,000, 30 to Age 65 at 8%, 25% Tax Rate

81 Roth IRA Conversion or In-plan Roth Rollover $10,000, 20 to Age 65 at 8%, 25% Tax Rate

82 Roth IRA Conversion or In-plan Roth Rollover $10,000, 10 to Age 65 at 8%, 25% Tax Rate

each year. This calculator assumes that you make 12 equal contributions throughout the year at the beginning of each month. http://www.bankrate.")

83 Some Basics 30 years of $10,000/year at 8%, Roth 401(k) versus Pre-tax 401(k), 25% Tax Rate, Pre-tax deferral s tax savings invested Annual contribution. The amount you will contribute to a 401(k) each year. This calculator assumes that you make 12 equal contributions throughout the year at the beginning of each month.

84

, 25% Tax Rate, Pre-tax deferral s tax savings not")

85 30 years of $10,000/year at 8%, Roth 401(k) versus Pre-tax 401(k), 25% Tax Rate, Pre-tax deferral s tax savings not invested

86

87

88 401(k) Pre-tax deferrals, 30 year contribution, 20 year distribution Tax bracket while working 25%, after 65 25%

89 401(k) Roth contributions, 30 year contribution, 20 year distribution Tax bracket while working 25%, after 65 25%

90 401(k) Pre-tax deferrals, 30 year contribution, 20 year distribution Tax bracket while working increased to 35%, after 65 25%

91 401(k) Roth deferrals, 30 year contribution, 20 year distribution Tax bracket while working increased to 35%, after 65 25%

92 401(k) Pre-tax deferrals, $24,000/year 10 year contribution, 20 year distribution Tax bracket while working increased to 35%, after 65 25%

93 401(k) Roth deferrals, $24,000/year 10 year contribution, 20 year distribution Tax bracket while working increased to 35%, after 65 25%

94 $10,000/Year; 8%, 30 Years until Retirement; 20 Years Payout Pre-tax Monthly = $6,236 Roth Monthly = $8,315

95 $10,000/Year; 8%, 20 Years until Retirement; 20 Years Payout Pre-tax Monthly = $2,519 Roth Monthly = $3,359

96 $10,000/Year; 8%, 10 Years until Retire; 20 Years Payout Pre-tax Monthly = $797 Roth Monthly = $1,063

97 FOR REFERENCE ROTH FORM 1099-R REPORTING EXAMPLES

98

99 Designated Roth & Form 1099-R A separate Form 1099-R issued for designated Roth account distributions. Code B is for all Roth distributions to participants. (Qualified distributions and distributions which have not yet become qualified). Box 11 is for reporting the first year of the designated Roth account Box 10 is for reporting the distribution of an In-plan Roth Rollover (IRR) that has been distributed before 5 years after the conversion unless an exception to the 10% penalty applies

100 QP In-plan ROTH Rollover aka In-plan Roth Conversion Participant M: $75,000 balance; over age 59½; in-service distribution; all pre-tax sources: $75,000 of ER matching and EE pre-tax elective deferrals. Plus earnings Participant M makes an in-plan Roth Rollover to a designated Roth account of all $75,000 Form 1099-R Box 1 $75,000 Box 2a $75,000 Box 4 $0 Box 5 $0 Box 7 Code G

101 QP In-plan ROTH Rollover Pre-tax and After-tax; In-plan Roth Conversion Participant J: $150,000 balance; age 40; in-service distribution for purpose of in-plan Roth rollover under ATRA; pre-tax sources: $145,000 of ER matching, safe harbor QNEC, EE pre-tax elective deferrals; $5,000 after-tax and earnings Participant J makes an in-plan Roth Rollover to a designated Roth account of all $150,000 Form 1099-R Box 1 $150,000 Box 2a $145,000 Box 4 $0 Box 5 $5,000 Box 7 Code G

102 Designated ROTH Distribution Severance and Partial Distribution Participant, age 40, has $10,000 balance $9,400 of designated Roth contributions $600 of earnings Participant withdraws $5,000 $4,700 is Roth; $300 earnings Form 1099-R Box 1 $5,000 Box 2a $300 Box 4 $60 (20% mandatory withholding) Box 5 $4,700 (Roth basis) Box 7 Code B Box 11 First year of 5-year clock.

103 Designated ROTH Distribution Severance & Direct Rollover to Roth IRA 8 Months Later participant has $5,000 balance remaining $4,700 of designated Roth contributions $300 of earnings Participant directly rolls $5,000 to Roth IRA Form 1099-R $4,700 is Roth; $300 earnings Box 1 $5,000 Box 2a $0 Box 4 $0 Box 5 $4,700 (Roth basis) Box 7 Code H Box 11 First year of 5-year clock.

104 Severance: Partial Distribution & Direct Rollover to Roth IRA Participant scheduled both distributions at the same time Starting with $10,000 Roth of which $600 was earnings and requested $5,000 to roll to Roth IRA and $5,000 to be paid to himself Notice , pretax first by direct rollover, So the $600 earnings would go to the Roth IRA; Form 1099-R for direct rollover Box 1 $5,000 Box 2a $0 Box 4 $0 Box 5 $4,400 (Roth basis) Box 7 Code H Box 11 First year of 5-year clock. Form 1099-R for distribution to Participant Box 1 $5,000; Box 2a $0; Box 5 $5,000; Box 7 Code B

105 QP Non-ROTH Distribution Sever & Direct Roll to Roth IRA Participant has $120,000 balance $108,000 of ER, EE non-roth contributions. Plus earnings $12,000 of after-tax Participant directly rolls $120,000 to Roth IRA Form 1099-R Box 1 $120,000 Box 2a $108,000 Box 4 $0 Box 5 $12,000 (after-tax basis) Box 7 Code G

106 QP Non-ROTH DISTRIBUTION Direct Rollover to Traditional IRA JP Participant has $200,000 balance $190,000 of ER, EE non-roth deferrals + earnings $10,000 of after-tax JP Participant directly rolls $200,000 to Traditional IRA Form 1099-R Box 1 $200,000 Box 2a $0 Box 4 $0 Box 5 $10,000 (after-tax basis) Box 7 Code G Form 5498, Traditional IRA Box 2: $190,000 No taxation on entire amount

107 QP Non-ROTH Distribution Partial Direct Rollover to Traditional IRA JP Participant:$200,000 balance; arranges total distribution 1. Direct rollover to traditional IRA of $190,000 of ER, EE pretax deferrals + earnings 2. Participant Distributions of $10,000 of after-tax Form 1099-R Box 1 $190,000 Box 2a $0 Box 4 $0 Box 7 Code G Form 5498, Traditional IRA Box 2: $190,000, No taxation on entire amount Form 1099-R Box 1 $10,000 Box 2a $0 Box 5 $10,000 Per Notice

108 QP Designated ROTH Direct Rollover: 401(k) Roth to Roth IRA JP Participant has $50,000 of 401(k) Roth balance $46,000 Roth contributions. $4,000 earnings JP Participant directly rolls $50,000 to ROTH IRA Form 1099-R Box 1 $50,000 Box 2a $0 Box 4 $0 Box 5 $46,000 (after-tax basis) Box 7 Code H 1st year of Roth 2008 Form 5498, Roth IRA Box 2: $50,000 No taxation on $4,000

109 Thank You for Attending Questions

Agenda Tax Rates 1/11/2016

Workshop 6: Roth Good Deal or Not: Mathematical Projections, Conversions William C. Grossman, ERPA, QPA, APA, MBA McKay Hochman Co., Inc.; Provided by DST Agenda Roth Projections Conversion Background

Workshop 6: Roth Good Deal or Not: Mathematical Projections, Conversions William C. Grossman, ERPA, QPA, APA, MBA McKay Hochman Co., Inc.; Provided by DST Agenda Roth Projections Conversion Background

Designated Roth Accounts From Deferral to Distribution Wednesday, May 1, 2013

Designated Roth Accounts From Deferral to Distribution Wednesday, May 1, 2013 William Grossman, ERPA, QPA, APR Director of Education & Communications McKay Hochman Co., Inc. Agenda Background Benefits

Designated Roth Accounts From Deferral to Distribution Wednesday, May 1, 2013 William Grossman, ERPA, QPA, APR Director of Education & Communications McKay Hochman Co., Inc. Agenda Background Benefits

In-plan Roth Rollovers

REGULATIONS In-plan Roth Rollovers By Susan D. Diehl, ERPA On November 26, 2010, the IRS published much-needed guidance regarding in-plan Roth rollovers (IRRs) in the form of Notice 2010-84. As a result

REGULATIONS In-plan Roth Rollovers By Susan D. Diehl, ERPA On November 26, 2010, the IRS published much-needed guidance regarding in-plan Roth rollovers (IRRs) in the form of Notice 2010-84. As a result

PERSONAL FINANCE. individual retirement accounts (IRAs)

") PERSONAL FINANCE individual retirement accounts (IRAs) 1 our purpose To lead and inspire actions that improve financial readiness for the military and local community. table of contents The Basics Of IRAs...

PERSONAL FINANCE individual retirement accounts (IRAs) 1 our purpose To lead and inspire actions that improve financial readiness for the military and local community. table of contents The Basics Of IRAs...

To Roth or Not Revised September 2013

Introduction To Roth or Not Revised September 2013 Tax law allows all taxpayers (without income limitation) to convert all or part of their traditional IRAs to Roth IRAs. Even though conversion to Roth

Introduction To Roth or Not Revised September 2013 Tax law allows all taxpayers (without income limitation) to convert all or part of their traditional IRAs to Roth IRAs. Even though conversion to Roth

Savings Banks Employees Retirement Association

Savings Banks Employees Retirement Association IN-PLAN ROTH CONVERSION ELECTION FORM PLEASE NOTE: Your Plan must allow In-Plan Roth Rollovers Participant Name: (Please Print) Certificate No. Current Address

Savings Banks Employees Retirement Association IN-PLAN ROTH CONVERSION ELECTION FORM PLEASE NOTE: Your Plan must allow In-Plan Roth Rollovers Participant Name: (Please Print) Certificate No. Current Address

2010 Update. The Rebirth of. Roth. A CPA s Ultimate Guide for Client Care. By: Robert S. Keebler, CPA, MST, AEP (Distinguished)

") 2010 Update The Rebirth of Roth A CPA s Ultimate Guide for Client Care By: Robert S. Keebler, CPA, MST, AEP (Distinguished) The Rebirth of Roth The Small Business Jobs Act of 2010 (SBJA) (P.L. 111-240)

2010 Update The Rebirth of Roth A CPA s Ultimate Guide for Client Care By: Robert S. Keebler, CPA, MST, AEP (Distinguished) The Rebirth of Roth The Small Business Jobs Act of 2010 (SBJA) (P.L. 111-240)

Distributions Options Guide

Distributions Options Guide A Guide to Your Options When Separating from Service Including the Special Tax Notice Retirement Savings, Simplified Your Distribution Options Upon separation of service and

Distributions Options Guide A Guide to Your Options When Separating from Service Including the Special Tax Notice Retirement Savings, Simplified Your Distribution Options Upon separation of service and

Errors and acceptable correction methods Revised May 2017

Revised May 2017 SCP and VCP Error Index Error Description 01 Failure to properly provide the minimum top-heavy benefit or contribution to non-key employees. 02 Failure to satisfy the ADP test, the ACP

Revised May 2017 SCP and VCP Error Index Error Description 01 Failure to properly provide the minimum top-heavy benefit or contribution to non-key employees. 02 Failure to satisfy the ADP test, the ACP

INFORMATION KIT GABELLI FUNDS

STATE STREET BANK AND TRUST COMPANY UNIVERSAL INDIVIDUAL RETIREMENT ACCOUNT INFORMATION KIT -------------- GABELLI FUNDS State Street Bank and Trust Company Universal IRA Information Kit Supplement to

STATE STREET BANK AND TRUST COMPANY UNIVERSAL INDIVIDUAL RETIREMENT ACCOUNT INFORMATION KIT -------------- GABELLI FUNDS State Street Bank and Trust Company Universal IRA Information Kit Supplement to

Rollovers from Employer-Sponsored Retirement Plans

Law Office Of Keith R. Miles, LLC Keith Miles Attorney-at-Law 2250 Oak Road PO Box 430 Snellville, GA 30078 678-666-0618 keithmiles@timetoestateplan.com www.timetoestateplan.com Rollovers from Employer-Sponsored

Law Office Of Keith R. Miles, LLC Keith Miles Attorney-at-Law 2250 Oak Road PO Box 430 Snellville, GA 30078 678-666-0618 keithmiles@timetoestateplan.com www.timetoestateplan.com Rollovers from Employer-Sponsored

A Guide to Roth IRAs. Contribution Limits and Deadlines. Who Can Contribute to a Roth IRA? Retirement Planning

A Guide to Roth IRAs A Roth IRA is an individual retirement account named for the late Senate Finance Committee Chairman, William Roth, Jr. who championed its creation. Traditional and Roth IRAs are both

A Guide to Roth IRAs A Roth IRA is an individual retirement account named for the late Senate Finance Committee Chairman, William Roth, Jr. who championed its creation. Traditional and Roth IRAs are both

chart RETIREMENT PLANS 8 RETIREMENT PLAN BENEFITS AVAILABLE RETIREMENT PLANS Retirement plans available to self-employed individuals include:

retirement plans Contributing to retirement plans can provide you with financial security as well as reducing and/or deferring your taxes. However, there are complex rules that govern the type of plans

retirement plans Contributing to retirement plans can provide you with financial security as well as reducing and/or deferring your taxes. However, there are complex rules that govern the type of plans

PENSION EDUCATOR SERIES GLOSSARY

PENSION EDUCATOR SERIES GLOSSARY 2 1% Owner An employee who owns more than 1% of the outstanding stock or more than 1% of the total combined voting power of all stock in a corporation; or more than 1%

PENSION EDUCATOR SERIES GLOSSARY 2 1% Owner An employee who owns more than 1% of the outstanding stock or more than 1% of the total combined voting power of all stock in a corporation; or more than 1%

ASPPAJournal Roth IRA Conversions THE

SPRING 2010 :: VOL 40, NO 2 ASPPAJournal ASPPA s Quarterly Journal for Actuaries, Consultants, Administrators and Other Retirement Plan Professionals 2010 Roth IRA Conversions by Susan D. Diehl As I am

SPRING 2010 :: VOL 40, NO 2 ASPPAJournal ASPPA s Quarterly Journal for Actuaries, Consultants, Administrators and Other Retirement Plan Professionals 2010 Roth IRA Conversions by Susan D. Diehl As I am

S A M P L E. Roth 401(k) Analysis Report. Pay Uncle Sam Now or Pay Him Later? Mr. Owner HCE. Prepared for

Analysis Report. Pay Uncle Sam Now or Pay Him Later? Mr. Owner HCE. Prepared for") Roth 401(k) Analysis Report Pay Uncle Sam Now or Pay Him Later? Prepared for Mr. Owner HCE Roth 401(k) Analyzer SM 2005-2006 ERISA Expertise LLC All Rights Reserved 5/7/2006 1:34 PM Page 1 of 13 Roth 401(k)

Roth 401(k) Analysis Report Pay Uncle Sam Now or Pay Him Later? Prepared for Mr. Owner HCE Roth 401(k) Analyzer SM 2005-2006 ERISA Expertise LLC All Rights Reserved 5/7/2006 1:34 PM Page 1 of 13 Roth 401(k)

Plan Administration Manual

Plan Administration Manual P a g e 1 Thank you for choosing American United Life Insurance Company (AUL), a OneAmerica company, as the funding vehicle and administrative services provider for your retirement

Plan Administration Manual P a g e 1 Thank you for choosing American United Life Insurance Company (AUL), a OneAmerica company, as the funding vehicle and administrative services provider for your retirement

Individual Retirement Account (IRA) Information Kit

Information Kit") Individual Retirement Account (IRA) Information Kit (Effective January 1, 2013) Pear Tree Funds 55 Old Bedford Road Suite 202 Lincoln, MA 01773 1-800-326-2151 1117-03-0713 PEAR TREE FUNDS Individual Retirement

Individual Retirement Account (IRA) Information Kit (Effective January 1, 2013) Pear Tree Funds 55 Old Bedford Road Suite 202 Lincoln, MA 01773 1-800-326-2151 1117-03-0713 PEAR TREE FUNDS Individual Retirement

Converting or Rolling Over Traditional IRAs to Roth IRAs

Cole FInancial Consulting Jennifer J. Cole, CFA, MBA P.O. Box 1109 Sandia Park, NM 505-286-7915 JCole@ColeFinancialConsulting.com ColeFinancialConsulting.com Converting or Rolling Over Traditional IRAs

Cole FInancial Consulting Jennifer J. Cole, CFA, MBA P.O. Box 1109 Sandia Park, NM 505-286-7915 JCole@ColeFinancialConsulting.com ColeFinancialConsulting.com Converting or Rolling Over Traditional IRAs

The Complex World of RMDs: A Case-Study Approach. William C. Grossman, ERPA, QPA

The Complex World of RMDs: A Case-Study Approach William C. Grossman, ERPA, QPA 1 Agenda Distribution Calendar Year Required Beginning Date Issues Rollovers and RMDs Calculation Issues A Variety of Issues

The Complex World of RMDs: A Case-Study Approach William C. Grossman, ERPA, QPA 1 Agenda Distribution Calendar Year Required Beginning Date Issues Rollovers and RMDs Calculation Issues A Variety of Issues

COLLIERS INTERNATIONAL USA, LLC And Affiliated Employers 401(K) Plan NOTICE OF DISTRIBUTION ELECTION

Plan NOTICE OF DISTRIBUTION ELECTION") COLLIERS INTERNATIONAL USA, LLC And Affiliated Employers 401(K) Plan NOTICE OF DISTRIBUTION ELECTION To: (Participant) Date: As a terminated participant in the Colliers International USA, LLC and Affiliated

COLLIERS INTERNATIONAL USA, LLC And Affiliated Employers 401(K) Plan NOTICE OF DISTRIBUTION ELECTION To: (Participant) Date: As a terminated participant in the Colliers International USA, LLC and Affiliated

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS This Special Tax Notice Applies to Distributions from Section 401(a) Plans, Section 403(a) Annuity Plans, Section 403(b) Tax Sheltered Annuities and Section 457

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS This Special Tax Notice Applies to Distributions from Section 401(a) Plans, Section 403(a) Annuity Plans, Section 403(b) Tax Sheltered Annuities and Section 457

Distribution Request Form. Instructions

Distribution Request Form (Applicable to Plans that do not include Annuity Distribution Options.) A Distribution Request Form must be completed, signed and returned to the Plan Administrator to request

Distribution Request Form (Applicable to Plans that do not include Annuity Distribution Options.) A Distribution Request Form must be completed, signed and returned to the Plan Administrator to request

DESCRIPTION OF THE CHAIRMAN S MARK OF THE RETIREMENT ENHANCEMENT AND SAVINGS ACT OF 2016

DESCRIPTION OF THE CHAIRMAN S MARK OF THE RETIREMENT ENHANCEMENT AND SAVINGS ACT OF 2016 Scheduled for Markup by the SENATE COMMITTEE ON FINANCE on September 21, 2016 Prepared by the Staff of the JOINT

DESCRIPTION OF THE CHAIRMAN S MARK OF THE RETIREMENT ENHANCEMENT AND SAVINGS ACT OF 2016 Scheduled for Markup by the SENATE COMMITTEE ON FINANCE on September 21, 2016 Prepared by the Staff of the JOINT

Individual Retirement Accounts and 401(k) Plans: Early Withdrawals and Required Distributions

Plans: Early Withdrawals and Required Distributions") Order Code RL31770 Individual Retirement Accounts and 401(k) Plans: Early Withdrawals and Required Distributions Updated October 27, 2008 Patrick Purcell Specialist in Income Security Domestic Social Policy

Order Code RL31770 Individual Retirement Accounts and 401(k) Plans: Early Withdrawals and Required Distributions Updated October 27, 2008 Patrick Purcell Specialist in Income Security Domestic Social Policy

403(b)/401(k) Comparison for 501(c)(3) Organizations. Your future. Made easier. For Plan Sponsor Use Only. Not For Use With The Public.

/401(k) Comparison for 501(c)(3) Organizations. Your future. Made easier. For Plan Sponsor Use Only. Not For Use With The Public.") 403(b)/401(k) Comparison for 501(c)(3) Organizations For Plan Sponsor Use Only. Not For Use With The Public. Your future. Made easier. 403(b)/401(k) Comparison for 501(c)(3) Organizations As a 501(c)(3)

403(b)/401(k) Comparison for 501(c)(3) Organizations For Plan Sponsor Use Only. Not For Use With The Public. Your future. Made easier. 403(b)/401(k) Comparison for 501(c)(3) Organizations As a 501(c)(3)

THE EVOLUTION OF THE ROTH 401(K)

") THE EVOLUTION OF THE ROTH 401(K) I. WHAT IS A ROTH 401(K)? A. Legislative History. 1. The Economic Growth and Tax Relief Reconciliation Act of 2001 ( EGTRRA ) authorized the establishment of Roth 401(k)

THE EVOLUTION OF THE ROTH 401(K) I. WHAT IS A ROTH 401(K)? A. Legislative History. 1. The Economic Growth and Tax Relief Reconciliation Act of 2001 ( EGTRRA ) authorized the establishment of Roth 401(k)

-1- Summary of Key Changes From the Pension Protection Act of 2006

Summary of Key Changes From the Pension Protection Act of Following is a list of key required and optional amendments to tax-qualified defined contribution plans (referred to as " plans" in the chart)

Summary of Key Changes From the Pension Protection Act of Following is a list of key required and optional amendments to tax-qualified defined contribution plans (referred to as " plans" in the chart)

A GUIDE TO YOUR OPTIONS WHEN SEPARATING FROM SERVICE, INCLUDING THE SPECIAL TAX NOTICE

Distribution Options Guide A GUIDE TO YOUR OPTIONS WHEN SEPARATING FROM SERVICE, INCLUDING THE SPECIAL TAX NOTICE. www.modeferredcomp.org 800-392-0925 DISTRIBUTION OPTIONS WHEN SEPARATING FROM SERVICE

Distribution Options Guide A GUIDE TO YOUR OPTIONS WHEN SEPARATING FROM SERVICE, INCLUDING THE SPECIAL TAX NOTICE. www.modeferredcomp.org 800-392-0925 DISTRIBUTION OPTIONS WHEN SEPARATING FROM SERVICE

Retirement Issues. Chapter 9 pp National Income Tax Workbook

Retirement Issues Chapter 9 pp. 289-326 2017 National Income Tax Workbook Retirement Issues p. 289 Taxation of Retirement Plan Distributions Impact of Income on Social Security Benefits & Medicare Premiums

Retirement Issues Chapter 9 pp. 289-326 2017 National Income Tax Workbook Retirement Issues p. 289 Taxation of Retirement Plan Distributions Impact of Income on Social Security Benefits & Medicare Premiums

Traditional and Roth IRAs. Information Kit, Disclosure Statement and Custodial Agreement

Traditional and Roth IRAs Information Kit, Disclosure Statement and Custodial Agreement UMB Bank, n.a. Universal Individual Retirement Account Disclosure Statement (EFFECTIVE DECEMBER 1, 2016) Part One:

Traditional and Roth IRAs Information Kit, Disclosure Statement and Custodial Agreement UMB Bank, n.a. Universal Individual Retirement Account Disclosure Statement (EFFECTIVE DECEMBER 1, 2016) Part One:

401(k) Plan Executive Summary January 2018

Plan Executive Summary January 2018") 401(k) Plan Executive Summary January 2018 3000 Lava Ridge Court, Suite 130 Roseville, CA 95661 Tel (916) 773-3480 Fax (916) 773-3484 6400 Canoga Avenue, Suite 250 Woodland Hills, CA 91367 Tel (818) 716-0111

401(k) Plan Executive Summary January 2018 3000 Lava Ridge Court, Suite 130 Roseville, CA 95661 Tel (916) 773-3480 Fax (916) 773-3484 6400 Canoga Avenue, Suite 250 Woodland Hills, CA 91367 Tel (818) 716-0111

UMB Bank, n.a. Universal IRA Information Kit

UMB Bank, n.a. Universal IRA Information Kit INTRODUCTION: What is the Difference between a Traditional IRA and a Roth IRA? With a traditional IRA, an individual may be able to deduct the contribution

UMB Bank, n.a. Universal IRA Information Kit INTRODUCTION: What is the Difference between a Traditional IRA and a Roth IRA? With a traditional IRA, an individual may be able to deduct the contribution

UMB Bank, n.a. Universal Individual Retirement Account Disclosure Statement

UMB Bank, n.a. Universal Individual Retirement Account Disclosure Statement PART ONE:DESCRIPTION OF TRADITIONAL IRAs Part One of the Disclosure Statement describes the rules applicable to traditional IRAs.

UMB Bank, n.a. Universal Individual Retirement Account Disclosure Statement PART ONE:DESCRIPTION OF TRADITIONAL IRAs Part One of the Disclosure Statement describes the rules applicable to traditional IRAs.

Rollover Distribution Notice

Rollover Distribution Notice GENERAL INFORMATION This notice contains important information you need before you decide how to receive your retirement plan benefits. This notice is provided to you by your

Rollover Distribution Notice GENERAL INFORMATION This notice contains important information you need before you decide how to receive your retirement plan benefits. This notice is provided to you by your

OPENING THE DOOR TO EXPANDED RETIREMENT SAVINGS OPPORTUNITIES:

OPENING THE DOOR TO EXPANDED RETIREMENT SAVINGS OPPORTUNITIES: EXPLORING ROTH AND AFTER-TAX FEATURES IN DC PLANS Not FDIC Insured May Lose Value Not Bank Guaranteed RETIREMENT CONTENTS 1 Executive Summary

OPENING THE DOOR TO EXPANDED RETIREMENT SAVINGS OPPORTUNITIES: EXPLORING ROTH AND AFTER-TAX FEATURES IN DC PLANS Not FDIC Insured May Lose Value Not Bank Guaranteed RETIREMENT CONTENTS 1 Executive Summary

ASPPA s Quarterly Journal for Actuaries, Consultants, Administrators and Other Retirement Plan Professionals

FALL 2010 :: VOL 40, NO 4 ASPPAJournal ASPPA s Quarterly Journal for Actuaries, Consultants, Administrators and Other Retirement Plan Professionals A Comprehensive Look at Intricate RMD Issues by William

FALL 2010 :: VOL 40, NO 4 ASPPAJournal ASPPA s Quarterly Journal for Actuaries, Consultants, Administrators and Other Retirement Plan Professionals A Comprehensive Look at Intricate RMD Issues by William

Retirement plans guide Facts at a glance

Retirement plans guide Facts at a glance Contents 1 What s your plan? 2 Small business/employer retirement plans 4 IRAs 5 Retirement plan distributions 7 Rollovers and transfers 9 Federal tax rates and

Retirement plans guide Facts at a glance Contents 1 What s your plan? 2 Small business/employer retirement plans 4 IRAs 5 Retirement plan distributions 7 Rollovers and transfers 9 Federal tax rates and

Plan Sponsor Webcast Series

Plan Sponsor Webcast Series Roth 401(k) Contributions, Safe Harbor 401(k) Plans and Automatic Enrollment Amy Pocino Kelly Julia L. Bringhurst www.morganlewis.com May 5, 2010 Roth 401(k) Contributions 2

Plan Sponsor Webcast Series Roth 401(k) Contributions, Safe Harbor 401(k) Plans and Automatic Enrollment Amy Pocino Kelly Julia L. Bringhurst www.morganlewis.com May 5, 2010 Roth 401(k) Contributions 2

QUALIFIED RETIREMENT PLAN AND 403(b)(7) CUSTODIAL ACCOUNT DISTRIBUTION REQUEST FORM

(7) CUSTODIAL ACCOUNT DISTRIBUTION REQUEST FORM") QUALIFIED RETIREMENT PLAN AND 403(b)(7) CUSTODIAL ACCOUNT DISTRIBUTION REQUEST FORM The Employee Retirement Income Security Act of 1974 (ERISA) requires that you receive the information contained in this

QUALIFIED RETIREMENT PLAN AND 403(b)(7) CUSTODIAL ACCOUNT DISTRIBUTION REQUEST FORM The Employee Retirement Income Security Act of 1974 (ERISA) requires that you receive the information contained in this

403(b)/401(k) Comparison for 501(c)(3) Organizations

/401(k) Comparison for 501(c)(3) Organizations") 403(b)/401(k) Comparison for 501(c)(3) Organizations For plan sponsor use only. Not to be used with participants. 403(b)/401(k) Comparison for 501(c)(3) Organizations As a 501(c)(3) organization, you are

403(b)/401(k) Comparison for 501(c)(3) Organizations For plan sponsor use only. Not to be used with participants. 403(b)/401(k) Comparison for 501(c)(3) Organizations As a 501(c)(3) organization, you are

Individual Retirement Account (IRA) Information Kit

Information Kit") Individual Retirement Account (IRA) Information Kit (Effective January 1, 2018) Pear Tree Funds 55 Old Bedford Road Suite 202 Lincoln, MA 01773 1-800-326-2151 PEAR TREE FUNDS Individual Retirement Account

Individual Retirement Account (IRA) Information Kit (Effective January 1, 2018) Pear Tree Funds 55 Old Bedford Road Suite 202 Lincoln, MA 01773 1-800-326-2151 PEAR TREE FUNDS Individual Retirement Account

Janus Universal IRA. Disclosure Statement & Custodial Agreement

Janus Universal IRA Disclosure Statement & Custodial Agreement Janus Universal Individual Retirement Account Disclosure Statement Part One: Description of Traditional IRAs SPECIAL NOTE State Street Bank

Janus Universal IRA Disclosure Statement & Custodial Agreement Janus Universal Individual Retirement Account Disclosure Statement Part One: Description of Traditional IRAs SPECIAL NOTE State Street Bank

Payment Rights Notice - Savings Plan

Updated January 2018 Your Benefits Resources http://www.yourbenefitsresources.com/ppg Payment Rights Notice - Savings Plan Federal law requires that you receive information about any rights that you may

Updated January 2018 Your Benefits Resources http://www.yourbenefitsresources.com/ppg Payment Rights Notice - Savings Plan Federal law requires that you receive information about any rights that you may

Makes permanent the provisions of EGTRRA that relate to retirement plans and IRAs. Makes the Saver s Credit permanent.

Leading Proposals Affecting Defined Contribution and Other Retirement Arrangements (Other Than Pension Funding and Hybrid Plan Proposals) [Note: Includes discussion of H.R. 1000, which passed the House

Leading Proposals Affecting Defined Contribution and Other Retirement Arrangements (Other Than Pension Funding and Hybrid Plan Proposals) [Note: Includes discussion of H.R. 1000, which passed the House

Roth IRAs The Roth IRA

Roth IRAs The Roth IRA 2017 and 2018 Questions & Answers What is a Roth Individual Retirement Account (Roth IRA)? A Roth IRA is a type of tax-preferred savings and investment account authorized by Internal

Roth IRAs The Roth IRA 2017 and 2018 Questions & Answers What is a Roth Individual Retirement Account (Roth IRA)? A Roth IRA is a type of tax-preferred savings and investment account authorized by Internal

NOTICE TO PARTICIPANTS REQUESTING AN IN-SERVICE WITHDRAWAL

P.O. Box 2069 Woburn, MA 01801-1721 (781) 938-6559 NOTICE TO PARTICIPANTS REQUESTING AN IN-SERVICE WITHDRAWAL Under the terms of the SBERA 401(k) Plan, if you were hired prior to January 1, 2000 and you

P.O. Box 2069 Woburn, MA 01801-1721 (781) 938-6559 NOTICE TO PARTICIPANTS REQUESTING AN IN-SERVICE WITHDRAWAL Under the terms of the SBERA 401(k) Plan, if you were hired prior to January 1, 2000 and you

Expanding Retirement Savings Opportunities with Roth Accounts

Defined Contribution Plans Expanding Retirement Savings Opportunities with Roth Accounts A growing number of plan sponsors are finding that adding Roth features to their retirement plan helps provide the

Defined Contribution Plans Expanding Retirement Savings Opportunities with Roth Accounts A growing number of plan sponsors are finding that adding Roth features to their retirement plan helps provide the

Last Name First Name MI

Marsh & McLennan Companies 401(k) Savings & Investment Plan IN-PLAN ROTH CONVERSION REQUEST FORM Use this form as an active or terminated participant to request an In-Plan Roth conversion from your after

Marsh & McLennan Companies 401(k) Savings & Investment Plan IN-PLAN ROTH CONVERSION REQUEST FORM Use this form as an active or terminated participant to request an In-Plan Roth conversion from your after

Required Minimum Distributions (RMDs)

") Jennifer J. Cole, CFA, MBA P.O. Box 1109 Sandia Park, NM 505-286-7915 JCole@ColeFinancialConsulting.com ColeFinancialConsulting.com Required Minimum Distributions (RMDs) Page 2 of 7 Required Minimum Distributions

Jennifer J. Cole, CFA, MBA P.O. Box 1109 Sandia Park, NM 505-286-7915 JCole@ColeFinancialConsulting.com ColeFinancialConsulting.com Required Minimum Distributions (RMDs) Page 2 of 7 Required Minimum Distributions

Taking Money Out of Retirement Plans

Taking Money Out of Retirement Plans Twila Slesnick, PhD, Enrolled Agent John C. Suttle, CPA, Attorney Chapter 1 Types of Retirement Plans... 1 Learning Objectives... 1 Introduction... 1 Qualified Plans...

Taking Money Out of Retirement Plans Twila Slesnick, PhD, Enrolled Agent John C. Suttle, CPA, Attorney Chapter 1 Types of Retirement Plans... 1 Learning Objectives... 1 Introduction... 1 Qualified Plans...

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS This notice explains how you can continue to defer federal income tax on your retirement plan savings in the Plan and contains important information you will

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS This notice explains how you can continue to defer federal income tax on your retirement plan savings in the Plan and contains important information you will

Western Washington U.A. Supplemental Pension Plan Request for Distribution Form

PERSONAL INFORMATION Western Washington U.A. Supplemental Pension Plan Request for Distribution Form Participant Name (if new, must include documentation of name change) Social Security number Mailing

PERSONAL INFORMATION Western Washington U.A. Supplemental Pension Plan Request for Distribution Form Participant Name (if new, must include documentation of name change) Social Security number Mailing

Distribution Request Form. Instructions

Distribution Request Form (Applicable to Plans that do not include Annuity Distribution Options.) A Distribution Request Form must be completed, signed and returned to the Plan Administrator to request

Distribution Request Form (Applicable to Plans that do not include Annuity Distribution Options.) A Distribution Request Form must be completed, signed and returned to the Plan Administrator to request

Savings Banks Employees Retirement Association

Savings Banks Employees Retirement Association 401(k) PLAN APPLICATION FOR WITHDRAWAL AT AGE 59 1/2 Participant Name: (Please Print) Current Address (required) SS No. (City, State Zip) Employer's Name:

Savings Banks Employees Retirement Association 401(k) PLAN APPLICATION FOR WITHDRAWAL AT AGE 59 1/2 Participant Name: (Please Print) Current Address (required) SS No. (City, State Zip) Employer's Name:

Key Provisions in the Pension Protection Act of 2006

Key Provisions in the Pension Protection Act of 2006 H.R.4, the Pension Protection Act of 2006 (the Act ), was signed into law on August 17, 2006. Among other changes, this massive 800-plus-page law overhauls

Key Provisions in the Pension Protection Act of 2006 H.R.4, the Pension Protection Act of 2006 (the Act ), was signed into law on August 17, 2006. Among other changes, this massive 800-plus-page law overhauls

TRADITIONAL IRA DISCLOSURE STATEMENT

TRADITIONAL IRA DISCLOSURE STATEMENT RIGHT TO REVOKE YOUR IRA ACCOUNT The W-2 form will have a check in the "retirement plan" box if you are covered by a retirement plan. You can also obtain IRS Notice

TRADITIONAL IRA DISCLOSURE STATEMENT RIGHT TO REVOKE YOUR IRA ACCOUNT The W-2 form will have a check in the "retirement plan" box if you are covered by a retirement plan. You can also obtain IRS Notice

IRAs. Your Retirement Advisor

Your Retirement Advisor 508-798-5115 lynnt@yourretirementadvisor.com www.yourretirementadvisor.com IRAs March, 2017 Page 1 of 8, see disclaimer on final page Both traditional and Roth IRAs feature tax-sheltered

Your Retirement Advisor 508-798-5115 lynnt@yourretirementadvisor.com www.yourretirementadvisor.com IRAs March, 2017 Page 1 of 8, see disclaimer on final page Both traditional and Roth IRAs feature tax-sheltered

Taking Money Out of Retirement Plans

Taking Money Out of Retirement Plans 13 th Edition Twila Slesnick, PhD, Enrolled Agent John C. Suttle, CPA, Attorney Chapter 1 Types of Retirement Plans... 1 Learning Objectives... 1 Introduction... 1

Taking Money Out of Retirement Plans 13 th Edition Twila Slesnick, PhD, Enrolled Agent John C. Suttle, CPA, Attorney Chapter 1 Types of Retirement Plans... 1 Learning Objectives... 1 Introduction... 1

Retirement Plans Guide Facts at a glance

Retirement Plans Guide Facts at a glance Retirement Plan Limits for 2013 and 2014 The Internal Revenue Service has released cost-of-living adjustments applicable to dollar limits for retirement plans.

Retirement Plans Guide Facts at a glance Retirement Plan Limits for 2013 and 2014 The Internal Revenue Service has released cost-of-living adjustments applicable to dollar limits for retirement plans.

DATAIR MASS-SUBMITTER PROTOTYPE SUMMARY OF CHANGES FOR EGTRRA RESTATEMENT 401(k) Non-Standardized

Non-Standardized") DATAIR MASS-SUBMITTER PROTOTYPE SUMMARY OF CHANGES FOR EGTRRA RESTATEMENT 401(k) Non-Standardized (Location: Base Plan Provision or Adoption Agreement) Required Minimum Distribution Final Reg.: Adopts

DATAIR MASS-SUBMITTER PROTOTYPE SUMMARY OF CHANGES FOR EGTRRA RESTATEMENT 401(k) Non-Standardized (Location: Base Plan Provision or Adoption Agreement) Required Minimum Distribution Final Reg.: Adopts

Retirement Planning Guide

2017 Retirement Planning Guide IRA Roth SEP SIMPLE DB 401(a) 401(k) 403(b) Life Insurance Issuers: Integrity Life Insurance Company National Integrity Life Insurance Company Western-Southern Life Assurance

2017 Retirement Planning Guide IRA Roth SEP SIMPLE DB 401(a) 401(k) 403(b) Life Insurance Issuers: Integrity Life Insurance Company National Integrity Life Insurance Company Western-Southern Life Assurance

Qualified DISTRIBUTION NOTICE Retirement Plan Important Information About Your Qualified Retirement Plan Distribution

Qualified DISTRIBUTION NOTICE Retirement Plan Important Information About Your Qualified Retirement Plan Distribution INTRODUCTION As a participant in your employer s qualified retirement plan, you have

Qualified DISTRIBUTION NOTICE Retirement Plan Important Information About Your Qualified Retirement Plan Distribution INTRODUCTION As a participant in your employer s qualified retirement plan, you have

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS (For Participant) A. TYPES OF PLAN DISTRIBUTIONS

A. TYPES OF PLAN DISTRIBUTIONS") SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS (For Participant) This notice explains how you can continue to defer federal income tax on your retirement plan savings in the Plan and contains important information

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS (For Participant) This notice explains how you can continue to defer federal income tax on your retirement plan savings in the Plan and contains important information

STATEMENT OF ADDITIONAL INFORMATION. FORM N-4 PART B May 1, 2018

THE VARIABLE ANNUITY LIFE INSURANCE COMPANY SEPARATE ACCOUNT A UNITS OF INTEREST UNDER GROUP UNIT PURCHASE AND GROUP FIXED AND VARIABLE DEFERRED ANNUITY CONTRACTS (GUP AND GTS-VA CONTRACTS) STATEMENT OF

THE VARIABLE ANNUITY LIFE INSURANCE COMPANY SEPARATE ACCOUNT A UNITS OF INTEREST UNDER GROUP UNIT PURCHASE AND GROUP FIXED AND VARIABLE DEFERRED ANNUITY CONTRACTS (GUP AND GTS-VA CONTRACTS) STATEMENT OF

ROTH IRA CONVERSION FREQUENTLY ASKED QUESTIONS

ROTH IRA CONVERSION FREQUENTLY ASKED QUESTIONS Brian Dobbis QPA, QKA, QPFC Director, Retirement Solutions 888-522-2388 A Roth IRA is a tax-deferred and potential tax-free retirement account available to

ROTH IRA CONVERSION FREQUENTLY ASKED QUESTIONS Brian Dobbis QPA, QKA, QPFC Director, Retirement Solutions 888-522-2388 A Roth IRA is a tax-deferred and potential tax-free retirement account available to

Stephanie Alden Smithey

Amending Your Qualified Plans for the Pension Protection Act and the Worker, Retiree, and Employer Recovery Act (and Other Pension Laws) September 24, 2009 Presented By: Stephanie Alden Smithey You may

Amending Your Qualified Plans for the Pension Protection Act and the Worker, Retiree, and Employer Recovery Act (and Other Pension Laws) September 24, 2009 Presented By: Stephanie Alden Smithey You may

EIC VALUE FUND INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA

TRADITIONAL IRA SEP IRA ROTH IRA") EIC VALUE FUND INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA)

EIC VALUE FUND INDIVIDUAL RETIREMENT ACCOUNT (IRA) TRADITIONAL IRA SEP IRA ROTH IRA BNY MELLON INVESTMENT SERVICING TRUST COMPANY Supplement to the Traditional and Roth Individual Retirement Account (IRA)

Instructions for Requesting an In-Service Withdrawal

Instructions for Requesting an In-Service Withdrawal Diocese of Metuchen 403(b) Plan Enclosed are the following items needed to request an In-Service Withdrawal from your retirement plan. Please review

Instructions for Requesting an In-Service Withdrawal Diocese of Metuchen 403(b) Plan Enclosed are the following items needed to request an In-Service Withdrawal from your retirement plan. Please review

TRADITIONAL IRA DISCLOSURE STATMENT

TRADITIONAL IRA DISCLOSURE STATMENT The Traditional Individual Retirement Account ( Traditional IRA ) presented with this Disclosure Statement is a retirement plan made available to individuals. An individual

TRADITIONAL IRA DISCLOSURE STATMENT The Traditional Individual Retirement Account ( Traditional IRA ) presented with this Disclosure Statement is a retirement plan made available to individuals. An individual

summary of key provisions

Pension Protection Act of 2006 PENSION RESOURCE CENTER summary of key provisions CONTENTS EGTRRA Provisions Permanent 2 Automatic Enrollment 3 Investment Advice 4 Increased Portability for Qualified Plans

Pension Protection Act of 2006 PENSION RESOURCE CENTER summary of key provisions CONTENTS EGTRRA Provisions Permanent 2 Automatic Enrollment 3 Investment Advice 4 Increased Portability for Qualified Plans

MASON COMPANIES RETIREMENT AND SAVINGS PLAN SUMMARY PLAN DESCRIPTION

MASON COMPANIES RETIREMENT AND SAVINGS PLAN SUMMARY PLAN DESCRIPTION Additional copies of the Summary Plan Description may be obtained at www.millimanbenefits.com TABLE OF CONTENTS INTRODUCTION TO YOUR

MASON COMPANIES RETIREMENT AND SAVINGS PLAN SUMMARY PLAN DESCRIPTION Additional copies of the Summary Plan Description may be obtained at www.millimanbenefits.com TABLE OF CONTENTS INTRODUCTION TO YOUR

DETAILED METHODOLOGY. Fidelity Planning & Guidance Center Retirement Analysis

DETAILED METHODOLOGY Fidelity Planning & Guidance Center Retirement Analysis DETAILED METHODOLOGY Fidelity Planning & Guidance Center Retirement Analysis 1. Overview 2. User Profile Information 3. Tax

DETAILED METHODOLOGY Fidelity Planning & Guidance Center Retirement Analysis DETAILED METHODOLOGY Fidelity Planning & Guidance Center Retirement Analysis 1. Overview 2. User Profile Information 3. Tax

In this chapter we will discuss federal income taxation of life insurance, annuities, and retirement plans.

Chapter Seven FEDERAL TAX CONSIDERATIONS AND RETIREMENT PLANS LEARNING OBJECTIVES Upon the completion of this chapter, you will be able to: 1. Identify taxation of premiums, cash values, policy loans and

Chapter Seven FEDERAL TAX CONSIDERATIONS AND RETIREMENT PLANS LEARNING OBJECTIVES Upon the completion of this chapter, you will be able to: 1. Identify taxation of premiums, cash values, policy loans and

RETIREMENT PLAN LUMP SUM PAYMENT CALCULATION EXPLANATION

RETIREMENT PLAN LUMP SUM PAYMENT CALCULATION EXPLANATION The NKCH RETIREMENT PLAN is designed to provide participants with a monthly benefit at retirement, payable for their lifetime. The benefit is determined

RETIREMENT PLAN LUMP SUM PAYMENT CALCULATION EXPLANATION The NKCH RETIREMENT PLAN is designed to provide participants with a monthly benefit at retirement, payable for their lifetime. The benefit is determined

DESCRIPTION OF CERTAIN REVENUE PROVISIONS CONTAINED IN THE PRESIDENT S FISCAL YEAR 2014 BUDGET PROPOSAL

[JOINT COMMITTEE PRINT] DESCRIPTION OF CERTAIN REVENUE PROVISIONS CONTAINED IN THE PRESIDENT S FISCAL YEAR 2014 BUDGET PROPOSAL Prepared by the Staff of the JOINT COMMITTEE ON TAXATION December 2013 U.S.

[JOINT COMMITTEE PRINT] DESCRIPTION OF CERTAIN REVENUE PROVISIONS CONTAINED IN THE PRESIDENT S FISCAL YEAR 2014 BUDGET PROPOSAL Prepared by the Staff of the JOINT COMMITTEE ON TAXATION December 2013 U.S.

If we receive request by 4:00pm ET on a business day, the transaction will be processed on that day unless you specify a future date below:

Jefferson National Life Insurance Company Regular Delivery: P.O. Box 36750, Louisville, KY 40233 Overnight: 9920 Corporate Campus Drive, Louisville, KY 40223 P: 866.667.0561 F: 866.667.0563 PARTIAL WITHDRAWAL

Jefferson National Life Insurance Company Regular Delivery: P.O. Box 36750, Louisville, KY 40233 Overnight: 9920 Corporate Campus Drive, Louisville, KY 40223 P: 866.667.0561 F: 866.667.0563 PARTIAL WITHDRAWAL

UMB BANK, N.A INFORMATION KIT

UMB BANK, N.A UNIVERSAL INDIVIDUAL RETIREMENT ACCOUNT INFORMATION KIT (EFFECTIVE DECEMBER 1, 2016) 600 University Street, Suite 2412 Seattle, WA 98101 Main: 206.838.9850 Toll Free: 877.701.2883 Fax: 206.838.9851

UMB BANK, N.A UNIVERSAL INDIVIDUAL RETIREMENT ACCOUNT INFORMATION KIT (EFFECTIVE DECEMBER 1, 2016) 600 University Street, Suite 2412 Seattle, WA 98101 Main: 206.838.9850 Toll Free: 877.701.2883 Fax: 206.838.9851

2017 Year-End Tax Reminders

2017 Year-End Tax Reminders INCOME TAX Wealth Planning Income Tax Rates 1. The following federal tax rates now apply to most types of capital gains for taxpayers in the highest tax brackets: 39.6% (short-term),

2017 Year-End Tax Reminders INCOME TAX Wealth Planning Income Tax Rates 1. The following federal tax rates now apply to most types of capital gains for taxpayers in the highest tax brackets: 39.6% (short-term),

Savings Banks Employees Retirement Association

Savings Banks Employees Retirement Association 401(k) PLAN APPLICATION FOR WITHDRAWAL AT AGE 59 1/2 Participant Name: (Please Print) Certificate No. Current Address (required) (Street) (City, State Zip)

Savings Banks Employees Retirement Association 401(k) PLAN APPLICATION FOR WITHDRAWAL AT AGE 59 1/2 Participant Name: (Please Print) Certificate No. Current Address (required) (Street) (City, State Zip)

Retirement Plans 101: An Introduction to Section 403(b)

") Retirement Plans 101: An Introduction to Section 403(b) 2008 Giller & Calhoun LLC I. Overview Educational institutions have been offering annuity contracts to their faculty since the early 1900s. The practice

Retirement Plans 101: An Introduction to Section 403(b) 2008 Giller & Calhoun LLC I. Overview Educational institutions have been offering annuity contracts to their faculty since the early 1900s. The practice

Year-End Planning 2017

Wealth Management Year-End Planning Executive Summary As we approach the end of, it is time to review traditional year-end planning decisions. We are aware of the significant changes in the tax code currently

Wealth Management Year-End Planning Executive Summary As we approach the end of, it is time to review traditional year-end planning decisions. We are aware of the significant changes in the tax code currently

INDEPENDENCE PLUS CONTRACT SERIES STATEMENT OF ADDITIONAL INFORMATION. FORM N-4 PART B May 1, 2018 TABLE OF CONTENTS

THE VARIABLE ANNUITY LIFE INSURANCE COMPANY SEPARATE ACCOUNT A UNITS OF INTEREST UNDER GROUP AND INDIVIDUAL FIXED AND VARIABLE DEFERRED ANNUITY CONTRACTS INDEPENDENCE PLUS CONTRACT SERIES STATEMENT OF

THE VARIABLE ANNUITY LIFE INSURANCE COMPANY SEPARATE ACCOUNT A UNITS OF INTEREST UNDER GROUP AND INDIVIDUAL FIXED AND VARIABLE DEFERRED ANNUITY CONTRACTS INDEPENDENCE PLUS CONTRACT SERIES STATEMENT OF

Special Tax Notice Regarding Payments YOUR ROLLOVER OPTIONS. Where may I roll over the payment?

Special Tax Notice Regarding Payments Products and financial services provided by American United Life Insurance Company a OneAmerica company One American Square, P.O. Box 368 Indianapolis, IN 46206-0368

Special Tax Notice Regarding Payments Products and financial services provided by American United Life Insurance Company a OneAmerica company One American Square, P.O. Box 368 Indianapolis, IN 46206-0368

EXPLORING IN-SERVICE DISTRIBUTIONS

Many individuals mistakenly believe that all retirement benefits are not available until retirement or at least not until they separate from their employers. This misconception may have originated in the

Many individuals mistakenly believe that all retirement benefits are not available until retirement or at least not until they separate from their employers. This misconception may have originated in the

TERMINATION FORM - 206

INSTRUCTIONS FOR COMPLETING TERMINATION FORM - 206 TERMINATION FORM - 206 Get your money fast! If your Plan Administrator has notified us of your termination, you may be able to easily process this 401(k)

INSTRUCTIONS FOR COMPLETING TERMINATION FORM - 206 TERMINATION FORM - 206 Get your money fast! If your Plan Administrator has notified us of your termination, you may be able to easily process this 401(k)

For Payments Not From a Designated Roth Account

Applies to Sections 401 and 403 SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS Retain For Your Records This notice is provided to you by Prudential Financial, Inc., on behalf of the plan administrator ( Plan

Applies to Sections 401 and 403 SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS Retain For Your Records This notice is provided to you by Prudential Financial, Inc., on behalf of the plan administrator ( Plan

STD N402F ][03/14/16)( (f) NOTICE OF SPECIAL TAX RULES ON DISTRIBUTIONS

![STD N402F ][03/14/16)( (f) NOTICE OF SPECIAL TAX RULES ON DISTRIBUTIONS](/thumbs/85/92934653.jpg "STD N402F ][03/14/16)( (f) NOTICE OF SPECIAL TAX RULES ON DISTRIBUTIONS") 402(f) NOTICE OF SPECIAL TAX RULES ON DISTRIBUTIONS For Payments Not From a Designated Roth Account YOUR ROLLOVER OPTIONS You are receiving this notice because all or a portion of a payment you are receiving

402(f) NOTICE OF SPECIAL TAX RULES ON DISTRIBUTIONS For Payments Not From a Designated Roth Account YOUR ROLLOVER OPTIONS You are receiving this notice because all or a portion of a payment you are receiving

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy Effective November 2016 TABLE OF CONTENTS DISCLOSURE STATEMENT Introduction 3 Section I

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy Effective November 2016 TABLE OF CONTENTS DISCLOSURE STATEMENT Introduction 3 Section I

Understanding IRAs. A Summary of Individual Retirement Accounts VLC

Understanding IRAs A Summary of Individual Retirement Accounts VLC0015-0318 TABLE OF CONTENTS Get Ready for Retirement.... 1 What Is an IRA?.... 1 Types of IRAs.... 2 Traditional IRA.... 2 Roth IRA....

Understanding IRAs A Summary of Individual Retirement Accounts VLC0015-0318 TABLE OF CONTENTS Get Ready for Retirement.... 1 What Is an IRA?.... 1 Types of IRAs.... 2 Traditional IRA.... 2 Roth IRA....

South Carolina Deferred Compensation Program 457 Deferred Compensation Plan Beneficiary Distribution Claim Form

South Carolina Deferred Compensation Program 457 Deferred Compensation Plan Beneficiary Distribution Claim Form PARTICIPANT INFORMATION PLEASE PRINT OR TYPE IN DARK INK. Participant Name Participant Social

South Carolina Deferred Compensation Program 457 Deferred Compensation Plan Beneficiary Distribution Claim Form PARTICIPANT INFORMATION PLEASE PRINT OR TYPE IN DARK INK. Participant Name Participant Social

2017 YEAR-END CHECKLIST. YEO & YEO CPAs & BUSINESS CONSULTANTS YEO & YEO. yeoandyeo.com

2017 YEAR-END YEO & YEO TAX CPAs & BUSINESS PLANNING CONSULTANTS CHECKLIST YEO & YEO CPAs & BUSINESS CONSULTANTS yeoandyeo.com As the end of the year approaches, it is a good time to think of planning

2017 YEAR-END YEO & YEO TAX CPAs & BUSINESS PLANNING CONSULTANTS CHECKLIST YEO & YEO CPAs & BUSINESS CONSULTANTS yeoandyeo.com As the end of the year approaches, it is a good time to think of planning

Roth, Roth & Roth (IRA, 401(k) & Conversion)

& Conversion)") Pension Compliance and Administration Services for Small Businesses Sponsoring Organization Name Continuing Professional Education Roth, Roth & Roth (IRA, 401(k) & Conversion) Presented by Barry R. Milberg