Designated Roth Accounts From Deferral to Distribution Wednesday, May 1, 2013

|

|

|

- Hillary Floyd

- 6 years ago

- Views:

Transcription

1 Designated Roth Accounts From Deferral to Distribution Wednesday, May 1, 2013 William Grossman, ERPA, QPA, APR Director of Education & Communications McKay Hochman Co., Inc.

2 Agenda Background Benefits and Attributes of a Roth Deferral Qualified Distributions The 5-Year Clock Rollovers: Direct; Participant Distributions Form 1099-R Roth Conversions Qualified Rollover Contributions Differences Between Roth IRA and Designated Roth 2

3 BACKGROUND

4 Background Designated Roth created by the Economic Growth and Tax Relief and Reconciliation Act of 2001 (EGTRRA) for 2006 tax year Section 617(a) of EGTRRA IRC 402A: Designated Roth Tax Code Section Pension Protection Act of 2006 made EGTRRA s retirement provisions permanent 4

5 Background Applies to deferrals under a 401(k) plan or a 403(b) arrangement and as of 2011 a governmental 457(b) Rules and tax treatment are the same Regulations on designated Roth accounts issued in two phases Final regulations for offering designated Roth issued Dec. 29, 2005, Effective Jan. 1, 2006 Final regulations on designated Roth distributions, rollovers and reporting issued April 27, 2007, Effective Jan. 1, 2007 Notice In-plan Roth Rollover Guidance 5

6 Effective Date Designated Roth first available for Plan Years that begin on or after January 1, was the first year that a designated Roth account became 5-years old: if started in 2006 IRS issued sample language for the addition of the Roth provision Off calendar plan may add to plan, but for participant s tax year beginning January 1 6

7 Adding Designated Roth to a Plan Roth is an optional provision Discretionary amendment Must be in plan document to use If adding the Roth must be done by last day of the first year in which it is used (per IRS Notice and Rev. Proc, and Rev. Proc , Section 5.05) Example: Plan year ending June 30, 2012, Roth Deferrals permitted Jan. 1, 2012, provided plan amendment to add Roth is adopted by June 30, Note: IRS issued sample Roth amendment Notice

8 Adding Roth to a Safe Harbor 401(k) Amendment Timing Can add Designated Roth to a Safe Harbor 401(k) plan after the plan year has started, per IRS Announcement Can add in plan Roth conversion to a safe harbor 401(k) after the plan year has started, per IRS Notice Neither of these will spoil the SH, even though the safe harbor notice was given out prior to the beginning of the plan year 8

9 Roth Treated as Elective Deferrals Roth deferrals are treated as elective deferrals under the terms of the plan and document Contribution limits ADP testing Matching formulas Vesting, 100% vested Nondiscrimination Coverage Top heavy QJSA, $5,000 consent and cash out rule combined 415 annual additions RMDs The major difference being the tax treatment 9

10 Operational Issues Roth only plans not permitted by the regulations. The participant must designate the contribution as a Roth prior to deposit to the plan Roth needs to be explained at enrollment meetings and on enrollment forms Roth must be included in Summary Plan Description Automatic Enrollment plans may default deferrals as Roth. Check your plan document. Prior to the first dollar being deferred, participants will have the right to opt out or change their deferral 10

11 BENEFITS AND ATTRIBUTES OF ROTH DEFERRALS

12 Three Required Conditions for Roth 1. Deferral irrevocably designated at the time of election as a Roth deferral (unlike IRA) 2. Deferral treated as includible in employee s income (not pre-tax) 3. Designated Roth deferrals maintained in a separate account from pre-tax deferrals Contributions and distributions must be record kept as separate Roth source Gains, losses, expenses, etc. separately allocated on a reasonable and consistent basis No forfeitures may be allocated to a Roth 12

13 Benefits and Attributes Roth Deferrals - Tax Free Earnings If deferrals left in plan long enough the earnings will be distributed tax FREE!!!! W-2 Reporting Roth included in taxable income and as deferral Pretax deferrals excluded from gross income and included as deferrals Box 12 Codes Roth = Code AA, plus amount of Roth deferrals Pretax = Code D, plus amount of pretax deferrals 13

14 Benefits and Attributes Roth Deferrals - Deferral Limit Roths are part of the annual deferral limit 2013 = $17,500, Catch-up = $5,500 Compared to 2013 IRA Roth Limit: $5,500/$1,000 Examples 1. Participant = Mack, age 51 Defers = $17,500 as Roth and $5,500 as Catch-up (also as a Roth) 2. Participant = Jen, age 55 Maximum $17,500 + $5,500 = $23,000 Defers = $11,500 Roth, $11,500 Pre-tax (Salary deferral agreement completed to place 50% in Roth and 50% in pre-tax deferrals) 14

15 Benefits & Attributes Roth Deferrals Roth IRA & Designated Roth Contributions to an IRA (even a Roth IRA) will not affect the Roth 401(k) limit Example In 2013, Matt (age 35) contributes $17,500 in his Roth 401(k) plan and $5,500 in his Roth IRA Roth IRA has income limitation, See next slide Note: the Roth IRA has been around since

16 Eligibility rules Roth IRA Annual Contribution Rules Earned income from personal services Contributions may be made after age 70½ Eligibility for Roth IRA limited by AGI: 2013 Full Contribution Partial Contribution No Contribution Single or head of household $112,000 or less $112,001 to $126,999 $127,000 or more Married filing jointly $178,000 or less $178,001 to $187,999 $188,000 or more Married, filing separately $9,999 or less N/A $10,000 or more

17 Benefits & Attributes Roth Deferrals 401(k) Advantages to Roth IRA Eligible Employees may find the fee structure in a 401(k) plan is better than in a Roth IRA Designated Roth may receive match No income limitations for eligibility to contribute to designated Roth (Roth IRA has income limitations) Therefore, higher income employees will be able to contribute to Roth 401(k) 17

18 QUALIFIED DISTRIBUTIONS 18

19 Qualified Distributions Distribution is qualified if: The Roth has satisfied the 5 year requirement AND Distributable event is: After attainment of age 59½, or After the death of the participant, or If the participant is disabled Any other distribution is treated as nonqualified 19

20 Qualified Distributions Example 1 James first made a Roth deferral in 2006 Leaves her company in 2013 at age 50 Wants a distribution This is a non-qualified distribution Although the funds have been in the plan for more than 5 years, the age 59½ requirement was not met 20

21 Qualified Distributions Example 2 Sarah first made a Roth deferral in 2010 Leaves her company in 2013 at age 65 Wants a distribution This is a non-qualified distribution Although Sarah has satisfied the age 59½ requirement, the 5 year period did not elapse 21

22 Qualified Distributions Example 3 David first made a Roth deferral in 2006 Leaves his company in 2013 due to disability David is age 45 Takes a distribution This is a qualified distribution Although David has not satisfied the age 59½ requirement, the distribution is qualified because: Disability that meets Section 72(m)(7), and the 5 year period did elapse 22

23 Qualified Distributions Example 4 Robin first made a Roth deferral in 2011 Dies in 2013 at age 62 Beneficiary wants a distribution This is a non-qualified distribution Although Robin has satisfied the age 59½ requirement and the distribution is because of death, the 5 year period did not elapse 23

24 Qualified Distributions Beneficiary or Alternate Payee The age, death or disability of the participant is used to determine whether a distribution is qualified in the case of an alternate payee or a beneficiary Example: Participant dies in 2009 and the surviving spouse leaves the funds in the plan until 2014 the five year rule will have been satisfied and the distribution will be tax free Exception: If the alternate payee or surviving spouse rolls money to their own Roth account, then you base the qualified status on their information 24

25 Distributions That Will Never be Qualified Certain Distributions will never be considered qualified (tax-free): Excess deferrals Excess contribution Deemed Loan defaults Life Insurance Protection ESOP Dividends 25

26 THE FIVE-YEAR CLOCK

27 The 5-Year Clock Year One 5 years measured on a calendar year basis If first contribution is made in 2013, it does not matter if the deferrals start in January or December 2013 is year number 1!!!! 27

28 The 5-Year Clock Annual Contributions Not Required The 5 year clock does not require that a contribution be made every year. It merely starts from the time the first contribution is made I contribute in 2006 and 2007 I do not contribute in 2008, 2009, 2010 I have still satisfied the 5-year requirement as of January 1, 2011 (2006, 2007, 2008, 2009, 2010) 28

29 The 5-Year Clock Per Plan Rule Participants may have more than one 5-year clock Every new plan that I contribute Roth deferrals to has a separate 5 year clock UNLESS I roll over my previous funds directly 29

30 The 5-Year Clock Example 1 TJ deferred to a Roth with Employer #1 in 2009 and 2010 Left Employer #1 in 2013 and left his money in Employer #1 s plan. 5 Year clock is still running Joins Employer #2 in 2013 and defers (Roth) A new 5 year clock starts in that plan 30

31 The 5-Year Clock Example 2 BJ deferred to a Roth with Employer #1 in 2009 and 2010 Left Employer #1 in 2013 and directly rolled his money into Employer #2 s plan. Joins Employer #2 in 2013 and defers (Roth) The 5 year clock in Employer # 2 s plan is considered to have started in 2009 Employer 1 is required to send a report of the first year of the Roth contributions and the amount to employer 2 31

32 The 5-Year Clock Rollover to Roth IRA Rules are different if I move funds from a 401(k) plan to a Roth IRA The Roth IRA has a separate tracking period and the years in the Roth 401(k) will not apply to the Roth IRA 32

33 The 5-Year Clock Rollover to Roth IRA Example 1 Michelle leaves employment in She had deferred into her Roth 401(k) for 2010 and 2013 She rolls her money into her first ever NEW Roth IRA in 2013 The 5 year clock starts over again in 2013!!! 33

34 The 5-Year Clock Rollover to Roth IRA Example 2 Raquel leaves employment in She had deferred into her Roth 401(k) for 2010 and 2012 She rolls her money to a Roth IRA in 2013 She had opened the Roth IRA in 1999 The 5-year clock on the amount rolled into the Roth IRA has been satisfied (as it picks up the Roth IRA clock which started in 1999)!! 34

35 Rollover to Roth IRA After 401(k) Roth Reaches Qualified Distribution Status If the plan Roth dollars are qualified, then they are considered basis when entering the IRA. If qualified distribution rolled into a new Roth IRA, Earnings made by the new Roth IRA (after the qualified distribution is rolled in), must wait 5- years to be tax free. 35

36 The 5-Year Clock USERRA Affected Participants If a returning military veteran makes up deferrals, the year the veteran selects to make up is the first year of the Roth contribution If an election is not made by the participant, then you assume it is made in the first possible year for the makeup of a Roth deferral under the terms of the plan Polly, a returning veteran in 2013, makes up deferrals for the 2010, 2011 and 2012 years. The Roth deferral would be attributable to the 2010 year, unless Polly chose 2011 or

37 DIRECT ROLLOVERS PARTICIPANT ROLLOVERS

38 Direct Rollovers From 401(k) or 403(b) Direct rollover is the only way to move designated Roth contributions with the earnings DIRECT ROLLOVER - PORTABILITY CHART FROM: Roth 401(k) Roth 403(b) Gov t. Roth 457(b) TO: Roth 401(k) Roth 403(b) G. Roth 457(b) Roth IRA Y Y Y Y Y Y Y Y Y Y Y Y Roth IRA N N N Y 38

39 Direct Rollovers - Accepting Plan Must Permit Designated Roth A rollover of designated Roth to a qualified plan can only be to a plan that allows Roth deferrals You cannot accept Roth rollovers into a Profit Sharing, 401(k) or Money Purchase plan without a designated Roth deferral feature 39

40 Direct Rollovers Reporting First Year of Clock How does the receiving plan in a rollover situation know how many years on the 5 year clock have expired??? It is the obligation of the distributing plan to report within 30 days of the rollover, the amount of basis and the first year of the 5 year clock 40

41 Direct Rollovers Reporting Requirements Recipient plan provides a report to the IRS regarding the acceptance of a Roth rollover It must include: Name and SS # Amount rolled over Year rollover is made Any other information required to determine the validity of the rollover Pending issuance of the IRS form for this reporting, still waiting 41

42 Participant Distributions Participant Rollover If a participant takes a distribution payable to himself and later (within 60 days) wants to make a participant rollover to Roth 401(k): only the pre-tax amount (earnings not yet qualified) may be rolled to another qualified plan Note: Employee has the right to receive the same rollover information (status of 5 year clock) within 30 days after it is requested 42

43 Participant Distributions Participant Rollover If a participant takes a distribution payable to himself and later (within 60 days) wants to rollover to a Roth IRA: then the entire distribution may be rolled to the Roth IRA Use Form 8606 to track 43

44 DISTRIBUTIONS

45 Participant Distributions General Rule Roth contributions are deferrals and are subject to the same withdrawal restrictions for active employees Age 59½ Financial Hardship If not taking the entire Roth account out, and it is not a qualified distribution, the distribution must be pro-rated between the original contributions and earnings 45

46 10% Penalty Roth Amount When distributions of Roth amounts are made what is subject to the 10% penalty if under age 59½? Only the amounts that will be taxed i.e. earnings not Roth deferrals 46

47 Pro-Rata Distributions, Not Ordering The Roth 401(k) and 403(b) will not have the same distribution ordering rules as the Roth IRA Roth IRA you can take after-tax contributions out first and leave the earnings Roth plans as stated earlier, you must withdraw pro-rata (if not taking the entire amount) 47

48 Participant Distributions Separate Plan for Cash-out Rules Roth amounts are considered a separate plan for application of the involuntary cashout and automatic rollover rules, IRS created a separate model 402(f) Notice For example if I have $800 in a Roth and $900 in pre-tax, those can be cashed out (even though the total is more than $1,000) If there is less then $200 in Roth, and $1,000 in other sources. The Roth is not subject to the eligible rollover distribution rules, nor 20 percent withholding whereas the other sources are 48

49 Hardship Distributions If a participant has both pre-tax and Roth deferrals, the hardship may be calculated using aggregate of both, but the hardship distribution may be limited to pre-tax deferrals Why would a plan want to limit the access to the Roth deferrals for hardship purposes? See the next slides 49

50 Hardship Distributions Designated Roth Issue 1. Basic concept about all hardship distributions of elective deferrals cannot take earnings out (at least post-1988) 2. Basic concept about Roth distributions you must take a pro-rata distribution of earnings and contribution How do these conflicting concepts get resolved?? 50

51 Hardship Distributions Designated Roth Issue 1. You are limited to taking hardships from the Roth deferrals (you cannot tap into the earnings) 2. But for tax purposes, you treat the hardship as being pro-rata earnings/contribution See next slide for an example Question to ponder Who thinks of these things? 51

52 Hardship Distributions Designated Roth Issue Joe has a Roth account of $10,000 ($7,000 in contributions and $3,000 in earnings) Hardship is limited to $7,000 If he takes all $7,000, he is taxed as if $4,900 (70%) is after-tax deferral and $2,100 (30%) is earnings 52

53 Hardship Distributions Designated Roth Issue If Joe comes back for a second hardship: the hardship calculation is treated as if all $7,000 came from the original deferrals so that is the amount that the next hardship is offset by The participant may be confused because he was taxed as if only $4,900 were Roth deferrals so why is $7,000 being considered? Plus, Joe lost the ability for $2,100 in earnings to ever achieve tax-free status This is why plans may want to limit hardships to pre-tax 53

54 RMDs for Roth 401(k) Not Roth IRA Difference in treatment for the Roth IRA and the Roth 401(k) when it comes to RMDs Roth IRA not subject to RMD at 70½ Designated Roth is subject to RMD rules due to Code Section 401(a)(9)! RMD may be taken from just non-roth account until designated Roth is a qualified distribution amount, though Roth must be included in the calculation of the RMD Participant can opt to have RMD amount be taken just from just the designated Roth account. You can still rollover plan amounts to Roth IRA prior to RMD beginning date 54

55 RMDs Is there a way to avoid Designated Roth RMD Payments? YES Roll the designated Roth to a Roth IRA The RMD for the year must be taken at the time of the rollover, but thereafter, as part of Roth IRA, there are no RMDs Beware that Roth IRA 5-year clock is satisfied when making rollover from designated Roth 55

56 Participant Loan Roth Issues For loans that are partly from designated Roth accounts, the quarterly amortized repayments must partly repay the designated Roth account and may not fully repay either the Roth or non- Roth alone Loan defaults will never be a qualified tax-free Roth distribution, per the final Roth regs. Therefore, for ease of administration and employee communications, some document sponsors are not offering the Roth as a source for loans 56

57 Return of Excess Deferrals Excess deferrals returned by April 15 will have no tax impact on participant After all, they are post tax $ But earnings will be taxable Even if participant has attained age 59½ and has the 5 year requirement met Makes sense since this money never should have had Roth treatment Excess deferrals returned after April 15 th Taxed again upon distribution Not eligible for rollover 57

58 ADP Test Refund Document can be written to give the participants the choice of which dollars (pre-tax or Roth) are returned This assumes both types of deferrals are made in the testing year Document can be written to dictate which dollars are returned first If Roth deferrals being returned, earnings must be included. If excess contribution is $3000 of Roth, of the $3000 Roth returned, $250 is earnings. If returned late, 10% employer penalty on the $3,

59 Form 1099-R

60 Designated Roth and Form 1099-R A separate Form 1099-R must be issued for designated Roth account distributions. Code B is for all Roth distributions. (Qualified distributions and distributions which have not yet become qualified). Box 11 is for reporting the first year of the designated Roth account Box 10 is for reporting the distribution of an Inplan Roth Rollover (IRR) that has been distributed before 5 years after the conversion 60

61 Designated ROTH Distribution Severance and Partial Distribution Participant has $10,000 balance $9,400 of designated Roth contributions $600 of earnings Participant withdraws $5,000 $4,700 is Roth; $300 earnings Form 1099-R Box 1 $5,000 Box 2a $300 Box 4 $60 (20% mandatory withholding) Box 5 $4,700 (Roth basis) Box 7 Code B Box 11 First year of 5-year clock. 61

62 Designated ROTH Distribution Severance & Direct Rollover to Roth IRA Participant has $10,000 balance $9,400 of designated Roth contributions $600 of earnings Participant directly rolls $5,000 to Roth IRA $4,700 is Roth; $300 earnings Form 1099-R Box 1 $5,000 Box 2a $0 Box 4 $0 Box 5 $4,700 (Roth basis) Box 7 Code H Box 11 First year of 5-year clock. 62

63 QP Non-ROTH Distribution in 2012; Severance & Direct Rollover to Roth IRA (Conversion) Participant has $120,000 balance $108,000 of ER, EE non-roth contributions. Plus earnings $12,000 of after-tax Participant directly rolls $120,000 to Roth IRA Form 1099-R Box 1 $120,000 Box 2a $108,000 Box 4 $0 Box 5 $12,000 (after-tax basis) Box 7 Code G 63

64 QP Non-ROTH DISTRIBUTION in 2012 Direct Rollover to Traditional IRA JP Participant has $200,000 balance $188,000 of ER, EE non-roth deferrals + earnings $12,000 of after-tax JP Participant directly rolls $200,000 to Traditional IRA Form 1099-R Box 1 $200,000 Box 2a $0 Box 4 $0 Box 5 $12,000 (after-tax basis) Box 7 Code G Form 5498, Traditional IRA Box 2: $188,000 No taxation on entire amount 64

65 QP In-plan ROTH Rollover in 2012 In-plan Roth Conversion Participant M has $75,000 balance and is over age 59½ $75,000 of ER, EE non-roth 401(k) contributions. Plus earnings Participant M makes an in-plan Roth Rollover to a designated Roth account of all $75,000 Form 1099-R Box 1 $75,000 Box 2a $75,000 Box 4 $0 Box 7 Code G 2012 Form 8606, Participant Files with Form 1040 Part III: Report in-plan Roth Rollover 65

66 QP Designated ROTH Direct Rollover to Roth IRA 2012 JP Participant has $50,000 Roth balance $50,000 Roth contributions. $4,000 of which is earnings JP Participant directly rolls $50,000 to ROTH IRA Form 1099-R Box 1 $50,000 Box 2a $0 Box 4 $0 Box 5 $46,000 (after-tax basis) Box 7 Code H 1 st year of Roth 2008 Form 5498, Roth IRA Box 2: $50,000 No taxation on $4,000 66

67 ROTH CONVERSIONS Small Business Jobs Act of 2010, and IRS Notice Updated by American Taxpayer Relief Act of 2012

68 Conversion of Pre-Tax to Roth From 2006 until September 27, 2010, Pre-tax 401(k) balances were not allowed to be converted to a 401(k) Roth account. Small Business Jobs Act of 2010 created in-plan Roth Rollover conversion to designated Roth American Taxpayer Relief Act of 2012 created inplan Roth Transfer as of

69 Conversion Only Within Plans That Have a Designated Roth Provision Conversion can only be made in a plan that has a designated Roth account provision 401(k) and 403(b) and, as of 2011, 457(b) governmental plans Plan may not have designated Roth provision only for conversions Not available for Profit sharing, money purchase or other plans that do not have designated Roth account provision 69

70 Effective Date, Available for Law enacted September 27, 2010, conversion provision effective immediately Available for: 401(k),403(b) or governmental 457(b) participants or surviving spouses Not available to non-spouse beneficiaries, but: non-spouse beneficiaries can convert to a Roth IRA 70

71 Within Plan Conversion to Designated Roth Requires a Distributable Event As with conversion from a QP to a Roth IRA, between 2010 and 2012, a distributable event was required to make a within plan conversion to a designated Roth For 2010 conversions only, Tax may be paid in 2010, or Half amount taxable in 2011 and half in 2012 Under age 59½, 10% penalty waived Any distributable event that is eligible for rollover is valid Withdrawal restrictions apply In-service not available until after age 59½ for: elective deferrals, safe harbor 401(k) contributions QNECs, QMACs 71

72 Within Plan Conversion to Designated Roth Required a Distributable Event In-service for employer NEC or match 2-year rule (Contribution must be in plan for 2 years) 5-year of participation rule New plan provision to limit an in-service withdrawal for only Roth conversions This was in the joint committee report, and IRS Notice In-service of rollovers contributed into the plan 72

73 In-plan Roth Rollovers Not Treated as a Distribution for the Following A plan loan transferred to the designated Roth account (without changing its repayment schedule) is not treated as a new loan; Spousal consent is not required in connection with an election to make an in-plan Roth rollover; The amount rolled over is taken into consideration for determining whether a participant s accrued benefit exceeds $5,000; Optional forms of benefit may not be eliminated. A participant who had a distribution right prior to the rollover cannot have that right eliminated after electing an in-plan Roth rollover. (Q/A-3) 73

74 2013 In-plan Roth Transfers: No Distributable Event Required As of January 1, 2013, a distributable event is not required to make an in-plan Roth Conversion via an in-plan Roth transfer, Section 902 of American Taxpayer Relief Act of 2012, signed into law on January 2, This adds a new transfer option in addition to the in-plan Roth rollover option from the Small Business Jobs Act of

75 2013 In-plan Roth Transfers: No Distributable Event Required As of the time this was written, we are awaiting IRS guidance on this new law. However, the following is known: The plan is required to have Roth provisions before anyone can make an in-plan Roth transfer, section 902 of ATRA Separate sourcing of each conversion is a needed for reporting and tracking of the 5-year conversion tracking of recapture tax From the Form 1099-R instructions for reporting distributions of in-plan conversions before 5 years have elapsed 75

76 2013 In-plan Roth Transfers: No Distributable Event Required Regarding the in-plan transfer conversion, section 902 of ATRA of 2012, provides the following for any plan that offers a qualified Roth contribution program: the plan may allow an individual to elect to have the plan transfer any amount not otherwise distributable under the plan to a designated Roth account maintained for the benefit of the individual 76

77 2013 In-plan Roth Transfers: No Distributable Event Required For example: Elective deferrals prior to age 59½ Safe harbor 401(k) contributions prior to 59½ QNECs, QMACs prior to age 59½ Money purchase plan accounts that were transferred into a 401(k) plan Need IRS guidance but believe J&S will carry over to Roth, and if so, these funds should be separately sourced 77

78 2013 In-plan Roth Transfers: No Distributable Event Required In-plan transfer conversion amendment We await IRS guidance, however, under the discretionary amendment rules, inplan transfers may be permitted by the plan sponsor, provided a discretionary amendment adding this option is made by plan year end. 78

79 Tax Consequences, Form 1099-R Conversions and transfers are taxable events and individual making conversion must have resources to pay the taxes due Form 1099-R necessary to report taxability of transaction Box 1 and 2a: amount of rollover/transfer Box 7: Direct rollover code G NOTE: Awaiting guidance on in-plan transfer box 7 code, but it is a taxable event and will require a Form 1099-R 79

80 Plan Participants Form 8606 Reporting The Form 8606 information is a direct quote from the IRS website information: Plan participants who make an in-plan Roth rollover must: File Form 8606, Nondeductible IRAs, with their tax return Complete Form 8606, Part III, to report their in-plan Roth rollover Complete certain lines of Form 8606, Part IV, if they receive a distribution in that tax year of any amount of their in-plan Roth rollover "Plan participants who make an in-plan Roth rollover must: Complete Form 8606, Part II, to report any amount converted from a non-roth IRA to a Roth IRA in that tax year File and complete a separate Form 8606, Part III, if they also rolled over amounts from a qualified retirement plan to a Roth IRA in that tax year" 80

81 Tax Consequences Recapture Tax For those converting under age 59½, the 10% penalty that was waived will be applied if conversion withdrawn before 5 years Penalty will not apply if distribution was due to severance from service in year age 55 attained or later 81

82 Measuring Five-taxable-year Recapture Period 5-taxable-year period starts with the first day of participant s tax year in which in-plan Roth conversion made, usually Jan 1. ends on last day of individual s 5th taxable year after conversion. Amounts may be rolled to another Roth without penalty. If withdrawn from subsequent Roth before end of 5-year period, 10% recapture tax will apply. A separate designated Roth sub-account should be established for each in-plan Roth conversion in order to appropriately apply the recapture tax or acceleration of income rules. 82

83 Recharacterization In-plan NOT Permitted A conversion from a traditional IRA to a Roth IRA may be recharacterized prior to the individual s tax filing deadline, including extensions There are no recharacterizations of within plan conversions back to pretax qualified plan sources 83

84 Plan Amendment Plan must have a designated Roth provision to permit in-plan Roth conversions Notice Q/A-20 indicates that to have a qualified Roth contribution program in place means to already have deferral elections permitting Roth deferrals available at the point when the in-plan conversion is to be implemented and if that is in place, the amendment to add the designated Roth provision to the document may be made by Dec. 31,

85 Plan Amendment Limiting in-plan conversion to: Only in-plan conversion permitted by Notice guidance Other in-service provisions may be added Caveat: Beware anti-cutback issue Rollovers into the plan Permitting conversions Permitting in-plan conversion via transfer 85

86 Roth IRA Conversion Advantages Vs. In-plan Roth IRA Advantages Traditional IRA to Roth IRA may be recharacterized No RMD during participant lifetime No distributable event required to access In-plan conversion advantages Creditor protection Possibly less fees Possible loan 86

87 Other Considerations Individual must have ability to pay tax on amount converted Withdrawing additional amount above conversion and having 100% withholding Requires distributable event If under 59½, distribution above conversion is subject to 10% penalty Disclosures Disclosure to participant in SMM of plan amendment Don t wait the 210 days Of taxes due upon conversion, 402(f) Notice 87

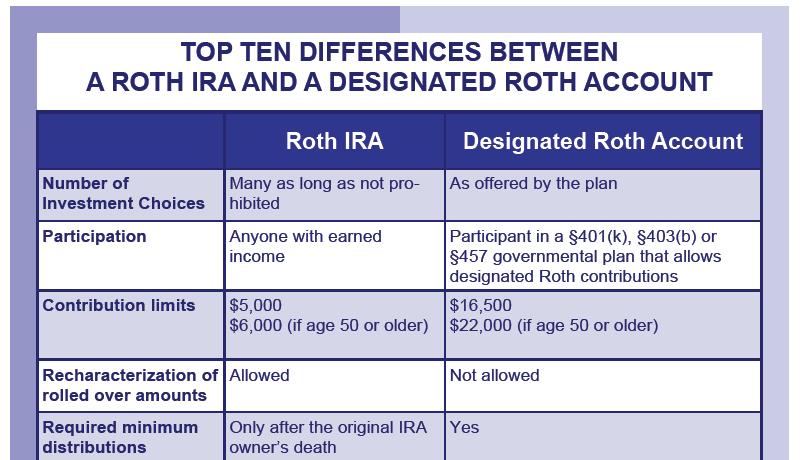

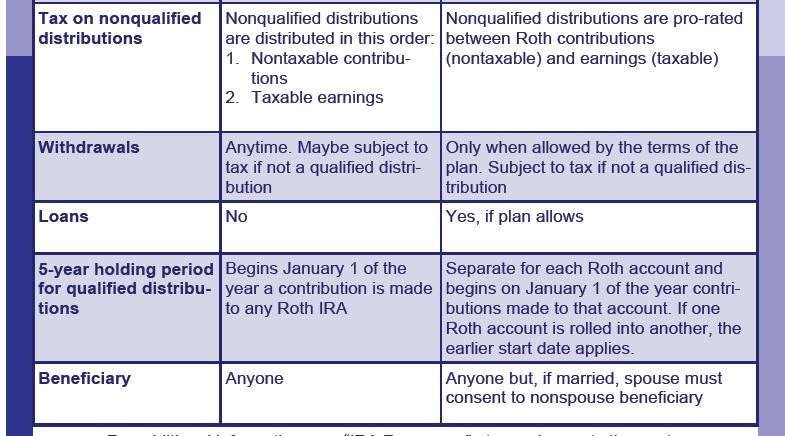

88 Measuring Five-year Designated Roth Clock The five-year designated Roth clock starts on the first day of the calendar year in which the earliest of the following occurs: The in-plan Roth conversion The first designated Roth contribution A direct rollover of designated Roth contributions from a prior employer s plan with an earlier contribution starting year 88

89 QUALIFIED ROLLOVER CONTRIBUTIONS IRS Notice , Rollover to Roth IRA, Pension Protection Act, 824

90 Qualified Rollover Contributions Notice creates new term: Qualified Rollover Contribution (QRC) for rollover from eligible retirement plan to a Roth IRA Any pretax amounts rolled via a QRC must be included in gross income for year of the rollover A QRC from a non Roth IRA to a Roth IRA is also called a conversion 90

91 Qualified Rollover Contributions QRC - taxable event, from a qualified plan, SEP, 403(b), gov t 457(b) plan or SIMPLE IRA, provided after 2 year participation QRC nontaxable event, from Another Roth IRA or a designated Roth 401(k) or 403(b) Note: a non-roth IRA to a Roth IRA is also called a conversion 91

92 Qualified Rollover Contributions Additional Rollovers to Roth IRA HEART ACT: Military Death Gratuity and service members group life insurance payments Maximum $100,000 death gratuity and $400,000 SGLI payment EESA: Exxon Valdez Case settlement; Maximum: $100,000 reduced by prior year s settlement income PPA: Qualified Airline Employee, bankruptcy 9-11 to , up to amount reported on Form

93 Qualified Rollover Contributions Effective date As of January 1, 2008, PPA permits with AGI limit of $100,000 and if married must file jointly As of January 1, 2010, the above restrictions are removed Once a year IRA to IRA rollover rule not invoked by conversion from non-roth to Roth IRA, nor from workplace employer plan to Roth IRA 93

94 Qualified Rollover Contributions Direct Rollover Beneficiary Options Nonspouse Beneficiaries may make a QRC to an inherited Roth IRA, provided eligible Spouse may make QRC to either Their own Roth IRA (or Traditional) Inherited IRA, Roth (or Traditional) 94

95 DIFFERENCE BETWEEN ROTH IRA and DESIGNATED ROTH Designated Roth Pro-rata Versus Roth IRA Ordering Rules IRS Chart

96 Pro-Rata Distributions, Not Ordering The Roth 401(k), 403(b) and governmental 457(b) will not have the same distribution ordering rules as the Roth IRA Roth IRA you can take after-tax contributions out first and leave the earnings Designated Roth plans as stated earlier, you must withdraw pro-rata (Roth and earnings) of nonqualified distributions (if not taking the entire amount) 96

97 Roth IRA Distribution - Ordering Rules When There Are Conversion Funds Roth IRAs have an ordering of which sources are to be distributed first (instead of pro-rata) Note: All Roth are aggregated for these rules (Roth and non-roth are not aggregated) First: Roth IRA contributions OR rollovers from designated Roth accounts Second: Converted funds FIFO: Funds that were taxable FIFO: Funds not taxable such as non-deductible IRA Third: Earnings 97

98 Roth IRA Distribution Ordering Rules - Example In 2009, Roth IRA has a cumulative amount of $15,000 of Roth IRA contributions, excluding earnings In addition, there is $40,000 of conversion from non-roth IRA in 2008 In 2009, individual (age 35) withdraws $16,000 The first $15,000 is treated as from the regular Roth IRA contributions $1,000 is treated as from the conversion amount The $1,000 is subject to the 10% penalty, due to withdrawal being made before 5 years of conversion 98

99 99

100 100

101 Questions & Comments That s All Folks!!! You may any questions or comments to me at: bgrossman@mhco.com 101

Roth Is On the Rise William C. Grossman, ERPA, QPA, APA, MBA

Roth Is On the Rise William C. Grossman, ERPA, QPA, APA, MBA Agenda Conversion Background In-plan Roth Conversions Designated Roth and Roth IRA Plan Design Concept: Add After-tax to Increase Roth Contribution

Roth Is On the Rise William C. Grossman, ERPA, QPA, APA, MBA Agenda Conversion Background In-plan Roth Conversions Designated Roth and Roth IRA Plan Design Concept: Add After-tax to Increase Roth Contribution

Agenda Tax Rates 1/11/2016

Workshop 6: Roth Good Deal or Not: Mathematical Projections, Conversions William C. Grossman, ERPA, QPA, APA, MBA McKay Hochman Co., Inc.; Provided by DST Agenda Roth Projections Conversion Background

Workshop 6: Roth Good Deal or Not: Mathematical Projections, Conversions William C. Grossman, ERPA, QPA, APA, MBA McKay Hochman Co., Inc.; Provided by DST Agenda Roth Projections Conversion Background

ASPPAJournal Roth IRA Conversions THE

SPRING 2010 :: VOL 40, NO 2 ASPPAJournal ASPPA s Quarterly Journal for Actuaries, Consultants, Administrators and Other Retirement Plan Professionals 2010 Roth IRA Conversions by Susan D. Diehl As I am

SPRING 2010 :: VOL 40, NO 2 ASPPAJournal ASPPA s Quarterly Journal for Actuaries, Consultants, Administrators and Other Retirement Plan Professionals 2010 Roth IRA Conversions by Susan D. Diehl As I am

INFORMATION KIT GABELLI FUNDS

STATE STREET BANK AND TRUST COMPANY UNIVERSAL INDIVIDUAL RETIREMENT ACCOUNT INFORMATION KIT -------------- GABELLI FUNDS State Street Bank and Trust Company Universal IRA Information Kit Supplement to

STATE STREET BANK AND TRUST COMPANY UNIVERSAL INDIVIDUAL RETIREMENT ACCOUNT INFORMATION KIT -------------- GABELLI FUNDS State Street Bank and Trust Company Universal IRA Information Kit Supplement to

chart RETIREMENT PLANS 8 RETIREMENT PLAN BENEFITS AVAILABLE RETIREMENT PLANS Retirement plans available to self-employed individuals include:

retirement plans Contributing to retirement plans can provide you with financial security as well as reducing and/or deferring your taxes. However, there are complex rules that govern the type of plans

retirement plans Contributing to retirement plans can provide you with financial security as well as reducing and/or deferring your taxes. However, there are complex rules that govern the type of plans

In-plan Roth Rollovers

REGULATIONS In-plan Roth Rollovers By Susan D. Diehl, ERPA On November 26, 2010, the IRS published much-needed guidance regarding in-plan Roth rollovers (IRRs) in the form of Notice 2010-84. As a result

REGULATIONS In-plan Roth Rollovers By Susan D. Diehl, ERPA On November 26, 2010, the IRS published much-needed guidance regarding in-plan Roth rollovers (IRRs) in the form of Notice 2010-84. As a result

Rollovers from Employer-Sponsored Retirement Plans

Law Office Of Keith R. Miles, LLC Keith Miles Attorney-at-Law 2250 Oak Road PO Box 430 Snellville, GA 30078 678-666-0618 keithmiles@timetoestateplan.com www.timetoestateplan.com Rollovers from Employer-Sponsored

Law Office Of Keith R. Miles, LLC Keith Miles Attorney-at-Law 2250 Oak Road PO Box 430 Snellville, GA 30078 678-666-0618 keithmiles@timetoestateplan.com www.timetoestateplan.com Rollovers from Employer-Sponsored

Stephanie Alden Smithey

Amending Your Qualified Plans for the Pension Protection Act and the Worker, Retiree, and Employer Recovery Act (and Other Pension Laws) September 24, 2009 Presented By: Stephanie Alden Smithey You may

Amending Your Qualified Plans for the Pension Protection Act and the Worker, Retiree, and Employer Recovery Act (and Other Pension Laws) September 24, 2009 Presented By: Stephanie Alden Smithey You may

DESCRIPTION OF THE CHAIRMAN S MARK OF THE RETIREMENT ENHANCEMENT AND SAVINGS ACT OF 2016

DESCRIPTION OF THE CHAIRMAN S MARK OF THE RETIREMENT ENHANCEMENT AND SAVINGS ACT OF 2016 Scheduled for Markup by the SENATE COMMITTEE ON FINANCE on September 21, 2016 Prepared by the Staff of the JOINT

DESCRIPTION OF THE CHAIRMAN S MARK OF THE RETIREMENT ENHANCEMENT AND SAVINGS ACT OF 2016 Scheduled for Markup by the SENATE COMMITTEE ON FINANCE on September 21, 2016 Prepared by the Staff of the JOINT

QUALIFIED RETIREMENT PLAN AND TRUST. Volume Submitter Summary Plan Description Booklet

QUALIFIED RETIREMENT PLAN AND TRUST Volume Submitter Summary Plan Description Booklet Introduction Your Employer has adopted an Employee benefit plan designed to help you meet your financial needs during

QUALIFIED RETIREMENT PLAN AND TRUST Volume Submitter Summary Plan Description Booklet Introduction Your Employer has adopted an Employee benefit plan designed to help you meet your financial needs during

COLLIERS INTERNATIONAL USA, LLC And Affiliated Employers 401(K) Plan NOTICE OF DISTRIBUTION ELECTION

Plan NOTICE OF DISTRIBUTION ELECTION") COLLIERS INTERNATIONAL USA, LLC And Affiliated Employers 401(K) Plan NOTICE OF DISTRIBUTION ELECTION To: (Participant) Date: As a terminated participant in the Colliers International USA, LLC and Affiliated

COLLIERS INTERNATIONAL USA, LLC And Affiliated Employers 401(K) Plan NOTICE OF DISTRIBUTION ELECTION To: (Participant) Date: As a terminated participant in the Colliers International USA, LLC and Affiliated

ASPPA s Quarterly Journal for Actuaries, Consultants, Administrators and Other Retirement Plan Professionals

FALL 2010 :: VOL 40, NO 4 ASPPAJournal ASPPA s Quarterly Journal for Actuaries, Consultants, Administrators and Other Retirement Plan Professionals A Comprehensive Look at Intricate RMD Issues by William

FALL 2010 :: VOL 40, NO 4 ASPPAJournal ASPPA s Quarterly Journal for Actuaries, Consultants, Administrators and Other Retirement Plan Professionals A Comprehensive Look at Intricate RMD Issues by William

Savings Banks Employees Retirement Association

Savings Banks Employees Retirement Association IN-PLAN ROTH CONVERSION ELECTION FORM PLEASE NOTE: Your Plan must allow In-Plan Roth Rollovers Participant Name: (Please Print) Certificate No. Current Address

Savings Banks Employees Retirement Association IN-PLAN ROTH CONVERSION ELECTION FORM PLEASE NOTE: Your Plan must allow In-Plan Roth Rollovers Participant Name: (Please Print) Certificate No. Current Address

The Complex World of RMDs: A Case-Study Approach. William C. Grossman, ERPA, QPA

The Complex World of RMDs: A Case-Study Approach William C. Grossman, ERPA, QPA 1 Agenda Distribution Calendar Year Required Beginning Date Issues Rollovers and RMDs Calculation Issues A Variety of Issues

The Complex World of RMDs: A Case-Study Approach William C. Grossman, ERPA, QPA 1 Agenda Distribution Calendar Year Required Beginning Date Issues Rollovers and RMDs Calculation Issues A Variety of Issues

Qualified Plans Tax Law Changes KANSAS CITY LIFE INSURANCE COMPANY

Qualified Plans Tax Law Changes KANSAS CITY LIFE INSURANCE COMPANY One of the best ways to save for retirement is with a qualified retirement savings plan. Some plans are employer-sponsored. With others,

Qualified Plans Tax Law Changes KANSAS CITY LIFE INSURANCE COMPANY One of the best ways to save for retirement is with a qualified retirement savings plan. Some plans are employer-sponsored. With others,

Plan Sponsor Webcast Series

Plan Sponsor Webcast Series Roth 401(k) Contributions, Safe Harbor 401(k) Plans and Automatic Enrollment Amy Pocino Kelly Julia L. Bringhurst www.morganlewis.com May 5, 2010 Roth 401(k) Contributions 2

Plan Sponsor Webcast Series Roth 401(k) Contributions, Safe Harbor 401(k) Plans and Automatic Enrollment Amy Pocino Kelly Julia L. Bringhurst www.morganlewis.com May 5, 2010 Roth 401(k) Contributions 2

Exploring Your IRA Options

Exploring Your IRA Options Traditional IRA Q & A.................. Page 2 Roth IRA Q & A...................... Page 5 Traditional vs. Roth IRAs............... Page 8 How does a Traditional IRA differ from

Exploring Your IRA Options Traditional IRA Q & A.................. Page 2 Roth IRA Q & A...................... Page 5 Traditional vs. Roth IRAs............... Page 8 How does a Traditional IRA differ from

QUALIFIED RETIREMENT PLAN SUMMARY PLAN DESCRIPTION

QUALIFIED RETIREMENT PLAN SUMMARY PLAN DESCRIPTION SUPER SIMPLIFIED STANDARD INDIVIDUAL 401(K) PROFIT SHARING PLAN Plan Name: Your Employer has adopted the qualified retirement plan named above ( the Plan

QUALIFIED RETIREMENT PLAN SUMMARY PLAN DESCRIPTION SUPER SIMPLIFIED STANDARD INDIVIDUAL 401(K) PROFIT SHARING PLAN Plan Name: Your Employer has adopted the qualified retirement plan named above ( the Plan

QUALIFIED RETIREMENT PLAN AND 403(b)(7) CUSTODIAL ACCOUNT DISTRIBUTION REQUEST FORM

(7) CUSTODIAL ACCOUNT DISTRIBUTION REQUEST FORM") QUALIFIED RETIREMENT PLAN AND 403(b)(7) CUSTODIAL ACCOUNT DISTRIBUTION REQUEST FORM The Employee Retirement Income Security Act of 1974 (ERISA) requires that you receive the information contained in this

QUALIFIED RETIREMENT PLAN AND 403(b)(7) CUSTODIAL ACCOUNT DISTRIBUTION REQUEST FORM The Employee Retirement Income Security Act of 1974 (ERISA) requires that you receive the information contained in this

Table II: Other Key Provisions in HR 1776 of Interest to Governmental Plans

Table II: Other Key Provisions in HR 1776 of Interest to Governmental Plans For a copy of HR 1776, visit http://www.nctr.org/content/pdf/portman_full_bill03.pdf See Table I for Principal Provisions in

Table II: Other Key Provisions in HR 1776 of Interest to Governmental Plans For a copy of HR 1776, visit http://www.nctr.org/content/pdf/portman_full_bill03.pdf See Table I for Principal Provisions in

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS This Special Tax Notice Applies to Distributions from Section 401(a) Plans, Section 403(a) Annuity Plans, Section 403(b) Tax Sheltered Annuities and Section 457

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS This Special Tax Notice Applies to Distributions from Section 401(a) Plans, Section 403(a) Annuity Plans, Section 403(b) Tax Sheltered Annuities and Section 457

Caution: Special rules apply to certain distributions to reservists and national guardsmen called to active duty after September 11, 2001.

LPL Financial Sims & Karr Financial Solutions Roger C. Sims Jason R Karr, Alex M. Means 304 North Main Street Greer, SC 29650 864-879-0337 simsandkarr@lpl.com www.simskarr.com Roth IRAs Page 1 of 13, see

LPL Financial Sims & Karr Financial Solutions Roger C. Sims Jason R Karr, Alex M. Means 304 North Main Street Greer, SC 29650 864-879-0337 simsandkarr@lpl.com www.simskarr.com Roth IRAs Page 1 of 13, see

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS This notice explains how you can continue to defer federal income tax on your retirement plan savings in the Plan and contains important information you will

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS This notice explains how you can continue to defer federal income tax on your retirement plan savings in the Plan and contains important information you will

Individual Retirement Account (IRA) Information Kit

Information Kit") Individual Retirement Account (IRA) Information Kit (Effective January 1, 2013) Pear Tree Funds 55 Old Bedford Road Suite 202 Lincoln, MA 01773 1-800-326-2151 1117-03-0713 PEAR TREE FUNDS Individual Retirement

Individual Retirement Account (IRA) Information Kit (Effective January 1, 2013) Pear Tree Funds 55 Old Bedford Road Suite 202 Lincoln, MA 01773 1-800-326-2151 1117-03-0713 PEAR TREE FUNDS Individual Retirement

UMB Bank, n.a. Universal IRA Information Kit

UMB Bank, n.a. Universal IRA Information Kit INTRODUCTION: What is the Difference between a Traditional IRA and a Roth IRA? With a traditional IRA, an individual may be able to deduct the contribution

UMB Bank, n.a. Universal IRA Information Kit INTRODUCTION: What is the Difference between a Traditional IRA and a Roth IRA? With a traditional IRA, an individual may be able to deduct the contribution

SPJST ROTH INDIVIDUAL RETIREMENT ANNUITY DISCLOSURE STATEMENT

SPJST ROTH INDIVIDUAL RETIREMENT ANNUITY DISCLOSURE STATEMENT This disclosure statement explains the rules governing a Roth IRA. The term IRA will be used in this disclosure statement to refer to a Roth

SPJST ROTH INDIVIDUAL RETIREMENT ANNUITY DISCLOSURE STATEMENT This disclosure statement explains the rules governing a Roth IRA. The term IRA will be used in this disclosure statement to refer to a Roth

SUMMARY PLAN DESCRIPTION Standard Textile 401(k) Profit Sharing Plan

Profit Sharing Plan") SUMMARY PLAN DESCRIPTION Standard Textile 401(k) Profit Sharing Plan This information is not intended to be a substitute for specific individualized tax, legal, or investment planning advice. Where specific

SUMMARY PLAN DESCRIPTION Standard Textile 401(k) Profit Sharing Plan This information is not intended to be a substitute for specific individualized tax, legal, or investment planning advice. Where specific

CHECKLIST OF REQUIRED AND OPTIONAL EGTRRA AMENDMENTS AND OTHER RECENT GUIDANCE FOR QUALIFIED DEFINED CONTRIBUTION PLANS. Nondiscrimination Testing

October 16, 2003 CHECKLIST OF REQUIRED AND OPTIONAL EGTRRA AMENDMENTS AND OTHER RECENT GUIDANCE FOR QUALIFIED DEFINED CONTRIBUTION PLANS Nondiscrimination Testing Required or Repeal of multiple-use test

October 16, 2003 CHECKLIST OF REQUIRED AND OPTIONAL EGTRRA AMENDMENTS AND OTHER RECENT GUIDANCE FOR QUALIFIED DEFINED CONTRIBUTION PLANS Nondiscrimination Testing Required or Repeal of multiple-use test

Makes permanent the provisions of EGTRRA that relate to retirement plans and IRAs. Makes the Saver s Credit permanent.

Leading Proposals Affecting Defined Contribution and Other Retirement Arrangements (Other Than Pension Funding and Hybrid Plan Proposals) [Note: Includes discussion of H.R. 1000, which passed the House

Leading Proposals Affecting Defined Contribution and Other Retirement Arrangements (Other Than Pension Funding and Hybrid Plan Proposals) [Note: Includes discussion of H.R. 1000, which passed the House

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS This notice explains how you can continue to defer federal income tax on your retirement plan savings in the Plan and contains important information you will

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS This notice explains how you can continue to defer federal income tax on your retirement plan savings in the Plan and contains important information you will

Qualified Retirement Plan PENSCO Solo(k) Summary Plan Description. Standardized Individual 401(k) Profit Sharing Plan

Summary Plan Description. Standardized Individual 401(k) Profit Sharing Plan") Qualified Retirement Plan PENSCO Solo(k) Summary Plan Description Standardized Individual 401(k) Profit Sharing Plan Standardized Individual 401(k) Profit Sharing Plan Summary Plan Description Plan Name:

Qualified Retirement Plan PENSCO Solo(k) Summary Plan Description Standardized Individual 401(k) Profit Sharing Plan Standardized Individual 401(k) Profit Sharing Plan Summary Plan Description Plan Name:

Navigating the Rollover Rules

Navigating the Rollover Rules Bill Grossman, APA, APR, QPA, ERPA, GFS, MBA, Director Education and Communications, McKay Hochman Co., Inc. Donald Kieffer, Esq., Tax Law Specialist, IRS Bill Grossman, APA,

Navigating the Rollover Rules Bill Grossman, APA, APR, QPA, ERPA, GFS, MBA, Director Education and Communications, McKay Hochman Co., Inc. Donald Kieffer, Esq., Tax Law Specialist, IRS Bill Grossman, APA,

Roth I R A s. General Informa tion and Instr uctions:

General Informa tion and Instr uctions: Roth I R A s The Roth IRA was created in 1998. Roth IRAs provide an alternative method of saving for retirement, allowing individuals to contribute aftertax monies

General Informa tion and Instr uctions: Roth I R A s The Roth IRA was created in 1998. Roth IRAs provide an alternative method of saving for retirement, allowing individuals to contribute aftertax monies

ftwilliam.com Summary of Amendments and due dates for Defined Contribution plans (including 457(b) and 403(b) plans)

and 403(b) plans)") ftwilliam.com Summary of Amendments and due dates for Defined Contribution plans (including 457(b) and 403(b) plans) NOTE: terminating plans are required to be up to date for all plan amendments before

ftwilliam.com Summary of Amendments and due dates for Defined Contribution plans (including 457(b) and 403(b) plans) NOTE: terminating plans are required to be up to date for all plan amendments before

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy Effective November 2016 TABLE OF CONTENTS DISCLOSURE STATEMENT Introduction 3 Section I

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy Effective November 2016 TABLE OF CONTENTS DISCLOSURE STATEMENT Introduction 3 Section I

-1- Summary of Key Changes From the Pension Protection Act of 2006

Summary of Key Changes From the Pension Protection Act of Following is a list of key required and optional amendments to tax-qualified defined contribution plans (referred to as " plans" in the chart)

Summary of Key Changes From the Pension Protection Act of Following is a list of key required and optional amendments to tax-qualified defined contribution plans (referred to as " plans" in the chart)

Qualified DISTRIBUTION NOTICE Retirement Plan Important Information About Your Qualified Retirement Plan Distribution

Qualified DISTRIBUTION NOTICE Retirement Plan Important Information About Your Qualified Retirement Plan Distribution INTRODUCTION As a participant in your employer s qualified retirement plan, you have

Qualified DISTRIBUTION NOTICE Retirement Plan Important Information About Your Qualified Retirement Plan Distribution INTRODUCTION As a participant in your employer s qualified retirement plan, you have

IRA AND EDUCATION SAVINGS. Retirement and Education Savings Accounts. TRADITIONAL IRAs Who is Eligible for a Traditional IRA?

Retirement and Education Savings Accounts This booklet is designed to highlight traditional individual retirement accounts (IRAs), Roth IRAs, and Coverdell Education Savings Accounts (CESAs). It is not

Retirement and Education Savings Accounts This booklet is designed to highlight traditional individual retirement accounts (IRAs), Roth IRAs, and Coverdell Education Savings Accounts (CESAs). It is not

403(b)/401(k) Comparison for 501(c)(3) Organizations. Your future. Made easier. For Plan Sponsor Use Only. Not For Use With The Public.

/401(k) Comparison for 501(c)(3) Organizations. Your future. Made easier. For Plan Sponsor Use Only. Not For Use With The Public.") 403(b)/401(k) Comparison for 501(c)(3) Organizations For Plan Sponsor Use Only. Not For Use With The Public. Your future. Made easier. 403(b)/401(k) Comparison for 501(c)(3) Organizations As a 501(c)(3)

403(b)/401(k) Comparison for 501(c)(3) Organizations For Plan Sponsor Use Only. Not For Use With The Public. Your future. Made easier. 403(b)/401(k) Comparison for 501(c)(3) Organizations As a 501(c)(3)

SPECIMEN NON-ERISA GOVERNMENTAL 403(b) PLAN Plan Summary

PLAN Plan Summary") SPECIMEN NON-ERISA GOVERNMENTAL 403(b) PLAN Plan Summary University of Maine System Optional Retirement Savings Plan 403(b) VALIC Specimen Governmental 403(b) Plan Plan Summary Plan Name: University of

SPECIMEN NON-ERISA GOVERNMENTAL 403(b) PLAN Plan Summary University of Maine System Optional Retirement Savings Plan 403(b) VALIC Specimen Governmental 403(b) Plan Plan Summary Plan Name: University of

Retirement plans guide Facts at a glance

Retirement plans guide Facts at a glance Contents 1 What s your plan? 2 Small business/employer retirement plans 4 IRAs 5 Retirement plan distributions 7 Rollovers and transfers 9 Federal tax rates and

Retirement plans guide Facts at a glance Contents 1 What s your plan? 2 Small business/employer retirement plans 4 IRAs 5 Retirement plan distributions 7 Rollovers and transfers 9 Federal tax rates and

HARDSHIP DISTRIBUTION REQUEST FORM

HARDSHIP DISTRIBUTION REQUEST FORM Table of Contents Page Employee & Employer Instructions... pg. 1 Section A-D: Employee Section... pg. 2-3 Section E: Employer Section... pg. 3 Special Tax Notice... pg.

HARDSHIP DISTRIBUTION REQUEST FORM Table of Contents Page Employee & Employer Instructions... pg. 1 Section A-D: Employee Section... pg. 2-3 Section E: Employer Section... pg. 3 Special Tax Notice... pg.

403(b) PLANS A GUIDE FOR PUBLIC SCHOOL SYSTEMS

PLANS A GUIDE FOR PUBLIC SCHOOL SYSTEMS") 403(b) PLANS A GUIDE FOR PUBLIC SCHOOL SYSTEMS January 2017 This guide is not intended and may not be used to avoid tax penalties, and was prepared to support the promotion or marketing of the matters

403(b) PLANS A GUIDE FOR PUBLIC SCHOOL SYSTEMS January 2017 This guide is not intended and may not be used to avoid tax penalties, and was prepared to support the promotion or marketing of the matters

Summary Plan Description

Summary Plan Description Prepared for TIAA-CREF Retirement Plan for Faculty and Administrators of Wilkes University To become a Participant in the Plan, you must meet the Plan's eligibility requirements.

Summary Plan Description Prepared for TIAA-CREF Retirement Plan for Faculty and Administrators of Wilkes University To become a Participant in the Plan, you must meet the Plan's eligibility requirements.

DISTRIBUTION REQUEST TIMELINE

Distribution Request Form DISTRIBUTION REQUEST TIMELINE This form is to request a participant withdrawal from your retirement account with your employer. Whether you are rolling over the funds or taking

Distribution Request Form DISTRIBUTION REQUEST TIMELINE This form is to request a participant withdrawal from your retirement account with your employer. Whether you are rolling over the funds or taking

S U M M A R Y P L A N D E S C R I P T I O N PayPal 401(k) Savings Plan

Savings Plan") S U M M A R Y P L A N D E S C R I P T I O N PayPal 401(k) Savings Plan This information is not intended to be a substitute for specific individualized tax, legal, or investment planning advice. Where specific

S U M M A R Y P L A N D E S C R I P T I O N PayPal 401(k) Savings Plan This information is not intended to be a substitute for specific individualized tax, legal, or investment planning advice. Where specific

PENSION PROTECTION ACT OF 2006

AN OVERVIEW OF THE IMPACT OF THE PENSION PROTECTION ACT OF 2006 ON QUALIFIED RETIREMENT PLANS Indiana Benefits Conference January 16, 2007 Indianapolis, Indiana E. Van Olson Introduction The Pension Protection

AN OVERVIEW OF THE IMPACT OF THE PENSION PROTECTION ACT OF 2006 ON QUALIFIED RETIREMENT PLANS Indiana Benefits Conference January 16, 2007 Indianapolis, Indiana E. Van Olson Introduction The Pension Protection

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy March 2018 TABLE OF CONTENTS DISCLOSURE STATEMENT Introduction 3 Section I Revocation 3

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy March 2018 TABLE OF CONTENTS DISCLOSURE STATEMENT Introduction 3 Section I Revocation 3

Addendum to the Traditional IRA Custodial Agreement and Disclosures

Effective January 1, 2018 Addendum to the Traditional IRA Custodial Agreement and Disclosures This Addendum changes the Traditional IRA Custodial Agreement and Disclosures ( Agreement ) document and uses

Effective January 1, 2018 Addendum to the Traditional IRA Custodial Agreement and Disclosures This Addendum changes the Traditional IRA Custodial Agreement and Disclosures ( Agreement ) document and uses

Distributions Options Guide

Distributions Options Guide A Guide to Your Options When Separating from Service Including the Special Tax Notice Retirement Savings, Simplified Your Distribution Options Upon separation of service and

Distributions Options Guide A Guide to Your Options When Separating from Service Including the Special Tax Notice Retirement Savings, Simplified Your Distribution Options Upon separation of service and

Traditional and Roth IRAs. Information Kit, Disclosure Statement and Custodial Agreement

Traditional and Roth IRAs Information Kit, Disclosure Statement and Custodial Agreement UMB Bank, n.a. Universal Individual Retirement Account Disclosure Statement (EFFECTIVE DECEMBER 1, 2016) Part One:

Traditional and Roth IRAs Information Kit, Disclosure Statement and Custodial Agreement UMB Bank, n.a. Universal Individual Retirement Account Disclosure Statement (EFFECTIVE DECEMBER 1, 2016) Part One:

Tax Law 2001 Pension and Benefits. proof

Tax Law 2001 Pension and Benefits Increased contribution limits. Make-up contributions for older individuals. Increased portability of benefits. New tax credits. Reduced regulatory burdens. These are just

Tax Law 2001 Pension and Benefits Increased contribution limits. Make-up contributions for older individuals. Increased portability of benefits. New tax credits. Reduced regulatory burdens. These are just

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS (For Participant) A. TYPES OF PLAN DISTRIBUTIONS

A. TYPES OF PLAN DISTRIBUTIONS") SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS (For Participant) This notice explains how you can continue to defer federal income tax on your retirement plan savings in the Plan and contains important information

SPECIAL TAX NOTICE REGARDING PLAN PAYMENTS (For Participant) This notice explains how you can continue to defer federal income tax on your retirement plan savings in the Plan and contains important information

SPECIAL TAX NOTICE REGARDING PAYMENTS FROM QUALIFIED PLANS Excerpted from IRS Notice

SPECIAL TAX NOTICE REGARDING PAYMENTS FROM QUALIFIED PLANS Excerpted from IRS Notice 2002-3 This notice explains how you can continue to defer federal income tax on your retirement savings in your Employer

SPECIAL TAX NOTICE REGARDING PAYMENTS FROM QUALIFIED PLANS Excerpted from IRS Notice 2002-3 This notice explains how you can continue to defer federal income tax on your retirement savings in your Employer

Distribution Request Form. Instructions

Distribution Request Form (Applicable to Plans that do not include Annuity Distribution Options.) A Distribution Request Form must be completed, signed and returned to the Plan Administrator to request

Distribution Request Form (Applicable to Plans that do not include Annuity Distribution Options.) A Distribution Request Form must be completed, signed and returned to the Plan Administrator to request

Retirement Plans Guide Facts at a glance

Retirement Plans Guide Facts at a glance Retirement Plan Limits for 2013 and 2014 The Internal Revenue Service has released cost-of-living adjustments applicable to dollar limits for retirement plans.

Retirement Plans Guide Facts at a glance Retirement Plan Limits for 2013 and 2014 The Internal Revenue Service has released cost-of-living adjustments applicable to dollar limits for retirement plans.

Retirement Planning Guide

Retirement Planning Guide 2012 Edition Issuers: Integrity Life Insurance Company National Integrity Life Insurance Company Western-Southern Life Assurance Company CF-74-0001-1202 FINANCIAL PROFESSIONAL

Retirement Planning Guide 2012 Edition Issuers: Integrity Life Insurance Company National Integrity Life Insurance Company Western-Southern Life Assurance Company CF-74-0001-1202 FINANCIAL PROFESSIONAL

PENSION EDUCATOR SERIES GLOSSARY

PENSION EDUCATOR SERIES GLOSSARY 2 1% Owner An employee who owns more than 1% of the outstanding stock or more than 1% of the total combined voting power of all stock in a corporation; or more than 1%

PENSION EDUCATOR SERIES GLOSSARY 2 1% Owner An employee who owns more than 1% of the outstanding stock or more than 1% of the total combined voting power of all stock in a corporation; or more than 1%

DESCRIPTION OF CERTAIN REVENUE PROVISIONS CONTAINED IN THE PRESIDENT S FISCAL YEAR 2014 BUDGET PROPOSAL

[JOINT COMMITTEE PRINT] DESCRIPTION OF CERTAIN REVENUE PROVISIONS CONTAINED IN THE PRESIDENT S FISCAL YEAR 2014 BUDGET PROPOSAL Prepared by the Staff of the JOINT COMMITTEE ON TAXATION December 2013 U.S.

[JOINT COMMITTEE PRINT] DESCRIPTION OF CERTAIN REVENUE PROVISIONS CONTAINED IN THE PRESIDENT S FISCAL YEAR 2014 BUDGET PROPOSAL Prepared by the Staff of the JOINT COMMITTEE ON TAXATION December 2013 U.S.

IRA Contribution Limits for 2018 Unchanged at $5,500 and $6,500; 401(k) Limits Do Change

Limits Do Change") Published Since 1984 ALSO IN THIS ISSUE IRA Contribution Limits for 2018 Page 1 IRA Contribution Deductibility Charts 2017 and 2018, Page 2 Roth IRA Contribution Charts for 2017 and 2018, Page 3 SEP and

Published Since 1984 ALSO IN THIS ISSUE IRA Contribution Limits for 2018 Page 1 IRA Contribution Deductibility Charts 2017 and 2018, Page 2 Roth IRA Contribution Charts for 2017 and 2018, Page 3 SEP and

SUMMARY OF DEFINED CONTRIBUTION PLAN PROVISIONS OF THE PENSION PROTECTION ACT OF 2006

SUMMARY OF DEFINED CONTRIBUTION PLAN PROVISIONS OF THE PENSION PROTECTION ACT OF 2006 ISSUE PRIOR LAW PENSION PROTECTION ACT 1 PERMANENCE OF RETIREMENT SAVINGS INCENTIVES RETIREMENT PLANS The Economic

SUMMARY OF DEFINED CONTRIBUTION PLAN PROVISIONS OF THE PENSION PROTECTION ACT OF 2006 ISSUE PRIOR LAW PENSION PROTECTION ACT 1 PERMANENCE OF RETIREMENT SAVINGS INCENTIVES RETIREMENT PLANS The Economic

Last Name First Name MI

Marsh & McLennan Companies 401(k) Savings & Investment Plan IN-PLAN ROTH CONVERSION REQUEST FORM Use this form as an active or terminated participant to request an In-Plan Roth conversion from your after

Marsh & McLennan Companies 401(k) Savings & Investment Plan IN-PLAN ROTH CONVERSION REQUEST FORM Use this form as an active or terminated participant to request an In-Plan Roth conversion from your after

NOTICE TO PARTICIPANTS REQUESTING AN IN-SERVICE WITHDRAWAL

P.O. Box 2069 Woburn, MA 01801-1721 (781) 938-6559 NOTICE TO PARTICIPANTS REQUESTING AN IN-SERVICE WITHDRAWAL Under the terms of the SBERA 401(k) Plan, if you were hired prior to January 1, 2000 and you

P.O. Box 2069 Woburn, MA 01801-1721 (781) 938-6559 NOTICE TO PARTICIPANTS REQUESTING AN IN-SERVICE WITHDRAWAL Under the terms of the SBERA 401(k) Plan, if you were hired prior to January 1, 2000 and you

401(k) Plan Executive Summary January 2018

Plan Executive Summary January 2018") 401(k) Plan Executive Summary January 2018 3000 Lava Ridge Court, Suite 130 Roseville, CA 95661 Tel (916) 773-3480 Fax (916) 773-3484 6400 Canoga Avenue, Suite 250 Woodland Hills, CA 91367 Tel (818) 716-0111

401(k) Plan Executive Summary January 2018 3000 Lava Ridge Court, Suite 130 Roseville, CA 95661 Tel (916) 773-3480 Fax (916) 773-3484 6400 Canoga Avenue, Suite 250 Woodland Hills, CA 91367 Tel (818) 716-0111

Military Benefit Association Roth IRA Conversions. 11/4/2015 Page 1 of 12, see disclaimer on final page

Military Benefit Association mba@militarybenefit.org Roth IRA Conversions 11/4/2015 Page 1 of 12, see disclaimer on final page Roth Conversions: Easier after 2009 What changed? Before 2010 you could only

Military Benefit Association mba@militarybenefit.org Roth IRA Conversions 11/4/2015 Page 1 of 12, see disclaimer on final page Roth Conversions: Easier after 2009 What changed? Before 2010 you could only

403(b)/401(k) Comparison for 501(c)(3) Organizations

/401(k) Comparison for 501(c)(3) Organizations") 403(b)/401(k) Comparison for 501(c)(3) Organizations For plan sponsor use only. Not to be used with participants. 403(b)/401(k) Comparison for 501(c)(3) Organizations As a 501(c)(3) organization, you are

403(b)/401(k) Comparison for 501(c)(3) Organizations For plan sponsor use only. Not to be used with participants. 403(b)/401(k) Comparison for 501(c)(3) Organizations As a 501(c)(3) organization, you are

Western Washington U.A. Supplemental Pension Plan Request for Distribution Form

PERSONAL INFORMATION Western Washington U.A. Supplemental Pension Plan Request for Distribution Form Participant Name (if new, must include documentation of name change) Social Security number Mailing

PERSONAL INFORMATION Western Washington U.A. Supplemental Pension Plan Request for Distribution Form Participant Name (if new, must include documentation of name change) Social Security number Mailing

Roth IRAs The Roth IRA

Roth IRAs The Roth IRA 2017 and 2018 Questions & Answers What is a Roth Individual Retirement Account (Roth IRA)? A Roth IRA is a type of tax-preferred savings and investment account authorized by Internal

Roth IRAs The Roth IRA 2017 and 2018 Questions & Answers What is a Roth Individual Retirement Account (Roth IRA)? A Roth IRA is a type of tax-preferred savings and investment account authorized by Internal

RETIREMENT PLAN LUMP SUM PAYMENT CALCULATION EXPLANATION

RETIREMENT PLAN LUMP SUM PAYMENT CALCULATION EXPLANATION The NKCH RETIREMENT PLAN is designed to provide participants with a monthly benefit at retirement, payable for their lifetime. The benefit is determined

RETIREMENT PLAN LUMP SUM PAYMENT CALCULATION EXPLANATION The NKCH RETIREMENT PLAN is designed to provide participants with a monthly benefit at retirement, payable for their lifetime. The benefit is determined

Plan Comparison for Governmental Plan Sponsors

Comparison for Governmental Sponsors + [Note that enabling legislation is required in order for a governmental employer to sponsor any type of retirement ] Category 457(b) Deferred Compensation 415(m)

Comparison for Governmental Sponsors + [Note that enabling legislation is required in order for a governmental employer to sponsor any type of retirement ] Category 457(b) Deferred Compensation 415(m)

SUMMARY PLAN DESCRIPTION PIXAR Employee's 401(k) Retirement Plan

Retirement Plan") SUMMARY PLAN DESCRIPTION PIXAR Employee's 401(k) Retirement Plan This information is not intended to be a substitute for specific individualized tax, legal, or investment planning advice. Where specific

SUMMARY PLAN DESCRIPTION PIXAR Employee's 401(k) Retirement Plan This information is not intended to be a substitute for specific individualized tax, legal, or investment planning advice. Where specific

TRADITIONAL IRA DISCLOSURE STATEMENT

TRADITIONAL IRA DISCLOSURE STATEMENT RIGHT TO REVOKE YOUR IRA ACCOUNT The W-2 form will have a check in the "retirement plan" box if you are covered by a retirement plan. You can also obtain IRS Notice

TRADITIONAL IRA DISCLOSURE STATEMENT RIGHT TO REVOKE YOUR IRA ACCOUNT The W-2 form will have a check in the "retirement plan" box if you are covered by a retirement plan. You can also obtain IRS Notice

Name of Plan: Name: Date of Birth: Home Address: Phone: City: State: Zip:

PLAN INFORMATION PARTICIPANT INFORMATION DISTRIBUTION FROM A QUALIFIED PLAN SUBJECT TO QUALIFIED JOINT AND SURVIVOR ANNUITY This form must be preceded by or accompanied by QJSA Notices and Rollover Distribution

PLAN INFORMATION PARTICIPANT INFORMATION DISTRIBUTION FROM A QUALIFIED PLAN SUBJECT TO QUALIFIED JOINT AND SURVIVOR ANNUITY This form must be preceded by or accompanied by QJSA Notices and Rollover Distribution

Important Tax Information About Payments From Your TSP Account

Important Tax Information About Payments From Your TSP Account Before you decide how to receive the money in your Thrift Savings Plan (TSP) account, you should review the important information in this

Important Tax Information About Payments From Your TSP Account Before you decide how to receive the money in your Thrift Savings Plan (TSP) account, you should review the important information in this

Retirement Plans 101: An Introduction to Section 403(b)

") Retirement Plans 101: An Introduction to Section 403(b) 2008 Giller & Calhoun LLC I. Overview Educational institutions have been offering annuity contracts to their faculty since the early 1900s. The practice

Retirement Plans 101: An Introduction to Section 403(b) 2008 Giller & Calhoun LLC I. Overview Educational institutions have been offering annuity contracts to their faculty since the early 1900s. The practice

If we receive request by 4:00pm ET on a business day, the transaction will be processed on that day unless you specify a future date below:

Jefferson National Life Insurance Company Regular Delivery: P.O. Box 36750, Louisville, KY 40233 Overnight: 9920 Corporate Campus Drive, Louisville, KY 40223 P: 866.667.0561 F: 866.667.0563 PARTIAL WITHDRAWAL

Jefferson National Life Insurance Company Regular Delivery: P.O. Box 36750, Louisville, KY 40233 Overnight: 9920 Corporate Campus Drive, Louisville, KY 40223 P: 866.667.0561 F: 866.667.0563 PARTIAL WITHDRAWAL

Universal Individual Retirement Account

December 30, 2017 Universal Individual Retirement Account Baron Asset Fund Baron Discovery Fund Baron Durable Advantage Fund Baron Emerging Markets Fund Baron Energy and Resources Fund Baron Fifth Avenue

December 30, 2017 Universal Individual Retirement Account Baron Asset Fund Baron Discovery Fund Baron Durable Advantage Fund Baron Emerging Markets Fund Baron Energy and Resources Fund Baron Fifth Avenue

rollover/transfer out form

1. Client Information rollover/transfer out form For VALIC Annuity 403(b) Plan Accounts Only Original Form Required for Processing The Variable Annuity Life Insurance Company (VALIC), Houston, Texas Mail

1. Client Information rollover/transfer out form For VALIC Annuity 403(b) Plan Accounts Only Original Form Required for Processing The Variable Annuity Life Insurance Company (VALIC), Houston, Texas Mail

CHECKLIST OF REQUIRED AND OPTIONAL EGTRRA AMENDMENTS AND OTHER 2002 GUIDANCE FOR QUALIFIED DEFINED CONTRIBUTION PLANS. Nondiscrimination Testing

CHECKLIST OF REQUIRED AND OPTIONAL EGTRRA AMENDMENTS AND OTHER 2002 GUIDANCE FOR QUALIFIED DEFINED CONTRIBUTION PLANS Nondiscrimination Testing or Repeal of multiple-use test under Treas. Reg. 1.401(m)-2.

CHECKLIST OF REQUIRED AND OPTIONAL EGTRRA AMENDMENTS AND OTHER 2002 GUIDANCE FOR QUALIFIED DEFINED CONTRIBUTION PLANS Nondiscrimination Testing or Repeal of multiple-use test under Treas. Reg. 1.401(m)-2.

Street Address. City, State, ZIP

ROTH IRA CUSTODIAL APPLICATION PACKET (FORM ) Please Print or Type CUID (Credit union will complete.) - - IRA Owner s Social Security Number IRA Owner s Name (First, Initial, Last) Street Address IRA Owner

ROTH IRA CUSTODIAL APPLICATION PACKET (FORM ) Please Print or Type CUID (Credit union will complete.) - - IRA Owner s Social Security Number IRA Owner s Name (First, Initial, Last) Street Address IRA Owner

INSTRUCTIONS TO REQUEST A BENEFIT PAYMENT

INSTRUCTIONS TO REQUEST A BENEFIT PAYMENT Participant 1. Read the enclosed notices, including the Notice to Terminated Participants and the Special Tax Notice Regarding Plan Payments. 2. Complete the enclosed

INSTRUCTIONS TO REQUEST A BENEFIT PAYMENT Participant 1. Read the enclosed notices, including the Notice to Terminated Participants and the Special Tax Notice Regarding Plan Payments. 2. Complete the enclosed

Summary Plan Description

Summary Plan Description Prepared for Aurora University Retirement Plan January 2012 TABLE OF CONTENTS INTRODUCTION...1 ELIGIBILITY...1 Am I eligible to participate in the Plan?...1 What requirements do

Summary Plan Description Prepared for Aurora University Retirement Plan January 2012 TABLE OF CONTENTS INTRODUCTION...1 ELIGIBILITY...1 Am I eligible to participate in the Plan?...1 What requirements do

Taking Money Out of Retirement Plans

Taking Money Out of Retirement Plans Twila Slesnick, PhD, Enrolled Agent John C. Suttle, CPA, Attorney Chapter 1 Types of Retirement Plans... 1 Learning Objectives... 1 Introduction... 1 Qualified Plans...

Taking Money Out of Retirement Plans Twila Slesnick, PhD, Enrolled Agent John C. Suttle, CPA, Attorney Chapter 1 Types of Retirement Plans... 1 Learning Objectives... 1 Introduction... 1 Qualified Plans...

Instructions for Forms 1099-R and 5498

2009 Instructions for Forms 1099-R and 5498 Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted. What s New Form 1099-R Airline

2009 Instructions for Forms 1099-R and 5498 Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted. What s New Form 1099-R Airline

403(b) PLAN BASIC PLAN DOCUMENT

PLAN BASIC PLAN DOCUMENT") 403 PLAN BASIC PLAN DOCUMENT TABLE OF CONTENTS SECTION 1 PLAN DEFINITIONS 1.01 Account... 1 1.02 Account Balance... 1 1.03 Accumulated Benefit... 1 1.04 Actual Contribution Percentage Test (ACP Test)...

403 PLAN BASIC PLAN DOCUMENT TABLE OF CONTENTS SECTION 1 PLAN DEFINITIONS 1.01 Account... 1 1.02 Account Balance... 1 1.03 Accumulated Benefit... 1 1.04 Actual Contribution Percentage Test (ACP Test)...

QRP Distribution Notice

QRP Distribution Notice Important Information About Your Qualified Retirement Plan Distribution INTRODUCTION As a participant in your employer s qualified retirement plan, you have accumulated a vested

QRP Distribution Notice Important Information About Your Qualified Retirement Plan Distribution INTRODUCTION As a participant in your employer s qualified retirement plan, you have accumulated a vested

UMB Bank, n.a. Universal Individual Retirement Account Disclosure Statement

UMB Bank, n.a. Universal Individual Retirement Account Disclosure Statement PART ONE:DESCRIPTION OF TRADITIONAL IRAs Part One of the Disclosure Statement describes the rules applicable to traditional IRAs.

UMB Bank, n.a. Universal Individual Retirement Account Disclosure Statement PART ONE:DESCRIPTION OF TRADITIONAL IRAs Part One of the Disclosure Statement describes the rules applicable to traditional IRAs.

THE EVOLUTION OF THE ROTH 401(K)

") THE EVOLUTION OF THE ROTH 401(K) I. WHAT IS A ROTH 401(K)? A. Legislative History. 1. The Economic Growth and Tax Relief Reconciliation Act of 2001 ( EGTRRA ) authorized the establishment of Roth 401(k)

THE EVOLUTION OF THE ROTH 401(K) I. WHAT IS A ROTH 401(K)? A. Legislative History. 1. The Economic Growth and Tax Relief Reconciliation Act of 2001 ( EGTRRA ) authorized the establishment of Roth 401(k)

Individual Retirement Account (IRA) Information Kit

Information Kit") Individual Retirement Account (IRA) Information Kit (Effective January 1, 2018) Pear Tree Funds 55 Old Bedford Road Suite 202 Lincoln, MA 01773 1-800-326-2151 PEAR TREE FUNDS Individual Retirement Account

Individual Retirement Account (IRA) Information Kit (Effective January 1, 2018) Pear Tree Funds 55 Old Bedford Road Suite 202 Lincoln, MA 01773 1-800-326-2151 PEAR TREE FUNDS Individual Retirement Account

General Information for 401k Plan Sponsor

General Information for 401k Plan Sponsor Welcome to our 401k Guide for the Plan Sponsor! The information contained on this site was designed and developed by various governmental agencies, and compiled

General Information for 401k Plan Sponsor Welcome to our 401k Guide for the Plan Sponsor! The information contained on this site was designed and developed by various governmental agencies, and compiled

Recent Changes to IRAs

Recent Changes to IRAs Federal legislation and new IRS regulations have created several changes to IRAs in the past year. Prohibition on recharacterization of IRA conversions: Effective for taxable years

Recent Changes to IRAs Federal legislation and new IRS regulations have created several changes to IRAs in the past year. Prohibition on recharacterization of IRA conversions: Effective for taxable years

Safe Harbor Explanations Eligible Rollover Distributions. Notice I. PURPOSE

Safe Harbor Explanations Eligible Rollover Distributions Notice 2018-74 I. PURPOSE This notice modifies the two safe harbor explanations in Notice 2014-74, 2014-50 I.R.B. 937, that may be used to satisfy

Safe Harbor Explanations Eligible Rollover Distributions Notice 2018-74 I. PURPOSE This notice modifies the two safe harbor explanations in Notice 2014-74, 2014-50 I.R.B. 937, that may be used to satisfy

IRAs & Roth IRAs. Beneficiary or Inherited IRAs. Questions & Answers

IRAs & Roth IRAs Beneficiary or Inherited IRAs Questions & Answers Purpose The purpose of this brochure is to provide a person who is a beneficiary of a traditional IRA (including SEPs and SIMPLEs) or