USING AUTO-ENROLL TO IMPROVE PARTICIPANT OUTCOMES

|

|

|

- Chester Thompson

- 6 years ago

- Views:

Transcription

1 National Association of Government Defined Contribution Administrators, Inc. USING AUTO-ENROLL TO IMPROVE PARTICIPANT OUTCOMES For decades governmental defined contribution plans were viewed as a supplemental savings tool that could be used to pay extraneous expenses in retirement such as vacations, a new car or boat. The defined benefit pension would replace, in some cases up to 90% of a worker s income in retirement. As the governmental defined benefit plan landscape continues to evolve, more and more responsibility to fund this important benefit is shifting to employees. These former supplemental programs can have an impact as to whether an individual faces a drastic reduction in lifestyle in retirement. Shift in Defined Benefit Formulas Half of all of the public defined benefit systems were founded shortly after the Social Security Act of At the time of its establishment, state and local governmental employees were excluded from the Social Security system. From , states began establishing systems to offer their own employees retirement protection. When these systems were established the average life span was around 60 years. That number has increased by 30% over the past 60 years to 78 years. Men and women who live to age 65 today have a 31% and 40% chance of living to age 90, respectively. Longer lifetime payouts, coupled with a volatile stock market that featured two major recessions in 10 years and a fixed income market that has been providing lower yields since 1980 have placed a tremendous amount of stress on the funding levels state and local defined benefit systems. Many systems have responded by reducing the formula designed to provide the lifetime payout in retirement in order to improve the health of their systems, or considered significant plan design changes. A National Conference of Public Employee Retirement System (NCPERS) conducted survey concluded that in 2014, 23% of all public pension systems reduced or tiered their benefit formula. According to the National Conference of State Legislatures, 43 states legislatures enacted significant changes to their retirement systems between the postrecession years of Changes Included: 1. Higher Employee Contributions 2. Longer Vesting/Age Requirements 3. Reduced Formulas for New Employees 4. Reduced COLAs 5. Consideration of a defined contribution hybrid plan to supplement reduced pension benefits 1

2 Healthcare Impact Public sector retirees with longer life spans and reduced pension payouts face strong headwinds dealing with the rising cost of healthcare. A change in accounting rules known as GASB 45 required public employers to disclose unfunded retiree healthcare liabilities on their balance sheet. As a result of that regulatory change, some states and other public entities chose to discontinue offering retiree medical benefits. A healthy male and female age 65 will need $144,000 and $156,000 respectively, to fund post-medicare health care expenses at the 90% confidence level. Without having significant personal savings to cover rising healthcare costs, seniors could find themselves having to choose between their health and their personal finances. Job Hopping Two decades ago, a job search consisted of looking at classified ads and hoping something matched your qualifications on the day you happened to look at the newspaper. Today, jobs tend to search for you. With hundreds of job search websites, many that will send positions to your inbox every morning based on your experience, it has never been easier to move between organizations. A 25-year-old will have already worked on average 6.3 different jobs today. At that pace they will work different jobs before age 45. With 92% of all governmental defined benefit plans requiring a vesting period of five years or longer, having a portable auto-enrolled and employee directed personal savings plan becomes critical to avoid completely starting over in terms of preparing and saving for retirement at every different job. Although technology has made the job search much easier, baby boomers had similar success in job hopping using the traditional classified ads, averaging 11.6 different jobs before age 45. Employees that spend less than 50% of their career in the public sector can expect to earn on average a 54% income replacement ratio inclusive of both defined benefit pension and social security. Having personal savings is essential to augment lower pension payments to avoid a drastic reduction in retirement lifestyle. Public Sector Defined Contribution Plans Due to their history of being viewed as supplemental, defined contribution plans in the public sector have lagged behind their ERISA counterparts in both innovation and participation. While participation in private sector 401k plans has steadily increased with automation features, supplemental plans in the public sector have remained in the 30-50% participation range for decades. With increased longevity, lower defined benefit pension formulas, a higher burden for healthcare on the employee and the potential to work for multiple employers during a career; it is time for public sector defined contribution plans to improve their plan design in an effort help public sector employees achieve retirement readiness. Impact of Inertia When defined benefit plans were created, enrollment and employee contributions were automatic and the benefits were typically determined by a formula using service time and final average salary/wages. Defined contribution retirement plans were subsequently introduced as supplemental retirement plans and it was historically 2

3 left to the employees to decide whether to save and how much to save. Inertia and other behavioral factors have resulted in inadequate savings as employees often do not enroll in a defined contribution plan or, once enrolled, do not increase the amount of their contributions over time. Behavioral research has identified the negative impact that inertia has on defined contribution savings and has demonstrated how inertia can be turned into a positive force through automatic enrollment and automatic escalation. As previously mentioned, when automatic enrollment is introduced in plans, a vast majority of those enrolled remain in the plan. Similarly, when automatic escalation is introduced, a high proportion of participants continue with automatic escalation over time. The Pension Protection Act (PPA) of 2006 paved the way for the most beneficial design changes to impact defined contribution plans. Instead of continuing to fight against participant inertia, the PPA embraced that inertia to work for participants. Safe Harbors were provided to plan sponsors that designed plans to include auto-enroll, auto-escalation and a diversified qualified default investment alternative. The results have been impressive, with auto-enroll capturing a 90% average stick rate of those continuing to save for retirement. Those in the lowest income group have benefited the most as research has shown autoenrollment to nearly double (82% increase) replacement incomes among that group. Legislative Concerns Because public sector defined contribution plans are not subject to the Employee Retirement Income Security Act (ERISA), many states anti-wage garnishment laws are not preempted with the addition of auto-enrollment. Since public sector plans continue to be subject to state law, some states prevent an employer from deducting any amounts out of an employee s paycheck without that employee s consent. To date, 12 states have passed legislation to allow for auto-enrollment into public DC plans, with Wyoming and Washington being the most recent. For some of these states, the legislation only applies to either state employees or participants in the state run plan, leaving it unavailable to municipal employers within the particular state. Some public plan sponsors are in states that allow creative methods to circumvent state anti-wage garnishment laws. States, such as California, allow unions to negotiate for auto-enrollment for their members through a memorandum of understanding achieved in the collective bargaining process. The City of Los Angeles is the largest employer attempting to utilize this method of autoenroll. The City is currently conducting a pilot program to allow for auto-enroll to its police union members and hopes to successfully expand the program to other unions in the future. Auto-Enroll Process Auto-enroll procedures (e.g. default rate, waiting period, covered employees, etc.) may vary but one of the most popular is the Eligible Automatic Contribution Arrangement (EACA). If each of the specific Internal Revenue Code rules is met, an EACA can allow an employee to opt out after an automatic contribution has been made and request a refund of contribution within 90 days of the first contribution. Typically, the plan sponsor provides employees with a 30-day notice prior to the first withdrawal. Under an EACA, the plan defaults the automatic contributions into the plan s capital preservation fund option for the first 90 days, and then switches the employee to an age appropriate diversified option or life cycle fund; such as a Target Date Fund. 3

4 To further improve an employees retirement readiness, research has found that including auto-escalation is necessary to fight participant inertia and according to a recent SHRM study, 55% of employees would favor an automatic annual increase. If the plan includes auto-escalation, the increase typically begins on the first payroll date of each new calendar year. Employees may opt out of the auto-escalation at any time by making any type of positive deferral election, but additional research has shown that 68% of employees remain enrolled in the auto-escalation. Improved participant outcomes by combining auto-enrollment with autoescalate and increasing the initial default deferral rate, participants can significantly increase their savings over time. Just as participant inertia keeps employees from enrolling in the plan, so, too, can it put them on the path to a more secure retirement when effective auto-features are implemented. Although formula guidelines have been established in the private sector, it is important to consider the defined benefit pension replacement amount and employee contribution rates when constructing public sector auto-enrollment formulas to ensure maximum success. looking at the number of participants in the plan and average participant account balance. Taking into account normal turnover, auto-enroll can have an impact of increasing the number of small balance accounts and negatively affecting the average account balance, particularly if the plan is successful in retaining lower income workers that have never previously been a part of the plan. Over the long term however, one can reasonably expect those who remain employed will have a significant positive impact on the overall growth of the plan size which could lead to reduced plan costs. Having a process in place to transfer the accounts of terminated participants with small balances to an IRA can help alleviate the negative impact to overall plan pricing. Cost and Savings Considerations There are potential costs and savings to consider prior to beginning an auto-enroll and/or auto escalation design change. If the plan provides matching contributions, it will be necessary to determine the impact the increase in participation may have on the employer s budget. It is equally important to consider the financial and organizational impact of having an employee continue to remain employed well past the plan s normal retirement age. Recordkeeping costs should also be considered. Many plans are priced by 4

5 Case Studies State of Texas Auto Enrollment Implemented January 1, 2008 Legislation The passage of H.B. 957 in 2007 authorized the automatic enrollment of newly hired state employees into the Texas Saver 401k plan. The automatic enrollment bill, was an attempt to encourage state employees to save more for retirement. Beginning January 1, 2008 new hires and rehires with a break in service were auto enrolled at 1%. Results Pre-Auto Enroll (2007) Participation Rate 34% 48% 56% Average Contribution $3,408 $1,512 $1,428 Average Balance $21,411 $11,707 $11,583 Stick Rate 89.40% Observations & Lessons Learned: Increased plan participation for new hires. Few make changes after enrollment; 53,682 still at 1% rate. With automatic increase of 1% per year, capping at 6%, the employee would have tripled assets. State of Wyoming Began July 1, 2015 for new employees of the executive, legislative and judicial branches of Wyoming State Government. Default contribution rate of the greater of $20 or 3% of pre-tax gross pay. State of Wyoming 457 Plan Auto Enrollment Summary 7/1/15-12/31/15 Eligible new employees, auto enrolled 260 Returned mail (excluded) 3 Gross eligible new employees 257 Electively enrolled 27 Terminated (before 30 day waiting period ended) 14 Pre-July hire 4 Net eligible new employees 209 Opt outs 4 Permissible withdrawal 1 Auto enrolled employees 204 Auto enrollment "stick" rate - 97% 5

6 Observations & Lessons Learned: Once automatic enrollment was implemented, it was onerous to return the $20 per month employer match to the employer in the event of a permissible withdrawal. The Wyoming Retirement System partnered with a legislative sponsor to adjust the enabling legislation in 2015 to allow the $20 per month employer match to be distributed to the employee in the event of a permissible withdrawal. Indiana Hoosier S.T.A.R.T. Plan State of Indiana introduced auto-enroll at 0.5% 2011-added auto-escalation of 0.5% per year increased auto-enroll rate from 0.5% to 2% Results Pre-Auto Enroll Post Auto-Enroll Participation Rate 51% 64% Stick Rate 97% Observations & Lessons Learned: Of those auto-enrolled, 62% make less than $30,000 per year, dispelling the myth that lower income employees can t afford to save. State of South Dakota South Dakota Supplemental Retirement Plan State legislature passed auto-enroll legislation New employees enrolled at $25 per month Effect of New Policy on Enrollments and Opt-Outs from the SRP Observations & Lessons Learned: New Enrollments State Employees Local Employees and Regents (University Employees) Opt-Outs Received During the Month Opt-Out % Jul % Aug % Sep % Oct % Nov % Dec % Jan % Feb % Totals 1, % 91.3% overall auto-enroll stick rate Employers in the State that did not adopt auto-enroll conversely saw less than a 1% opt-in enrollment rate with 17 of the 2,360 employees choosing to save. 6

7 Conclusion Having a competitive retirement program is essential to attracting and retaining employees for not just a corporation or not for profit entity, but for governmental entities as well Governmental entities will therefore need to provide more competitive and well-designed retirement plan and benefit programs. Employees tend to look for guidance from their employer when it comes to employee benefits. Employers can set an important precedent by offering an automatic enrollment arrangement and impressing upon employees how important it is to begin saving for retirement as soon as possible. Many employees will appreciate the effort made to easily get them into the plan, and most will continue to save as evidence by the 90% stick rates of auto-enroll. Auto-escalation also becomes very important because employees may conclude that if 1% was the suggested rate by the employer, then it must be sufficient, as the Texas case study proves with most participants never changing their deferral amount. Excuses for not beginning a savings program can be made at every phase in life - student debt, getting married, buying a house, having kids, paying for college, etc.; before you know it you are out of time. With so much burden of responsibility being placed on the individual today, it is imperative to change the system to better serve those that serve the public, by working to make autoenrollment and auto-escalation programs available to all public sector employees. REFERENCES: Current 10-Year Treasury Rate: 1.76% At market close Fri Feb 26, 2016 Mean: 4.60% Median: 3.88% Min: 1.53% (Jul 2012) Max: 15.32% (Sep 1981) US 10 Year Treasury Yield. Source 10-year historical yield 7

8 NCPERS Source: pdf (2015 Report) 8

.")

9 The average annual benefit payment for state- and locally-administered pensions (total benefit payments divided by the number of beneficiaries) for the United States was $26,128 in The state with the highest average annual benefit payment from state- and locally-administered pensions in 2013 was Connecticut (averaging $35,486 annually). Connecticut was one of eight states with average annual benefit payments above $30,000. The other seven states were California, Colorado, Rhode Island, Illinois, Nevada, New York, and New Jersey. At the other end of the spectrum, the state with the lowest average annual benefit payment from state- and locally-administered pensions in 2013 was North Dakota (averaging $14,900 annually). North Dakota was one of 16 states with average annual benefit payments below $20,000. See Figure 4 for state 9

10 Empower Institute- Health Care Costs is one of the most significant and worrisome categories of expenses in retirement. These expenses are primarily in the form of premiums for Medicare parts B and D and supplemental insurance, as well as out-of-pocket expenses for copays and cost sharing related to medical treatments and medications. We show that for a healthy 65-year-old male retiree, cumulative savings of approximately $144,000 would be required to fund these expenses for the projected retirement period at a 90% confidence level. For a female, the amount would be $156,000. However, for different health and disease states, the interactions of projected health costs and associated mortality projections often have interesting and counterintuitive effects on retirement planning. For example, the higher retiree healthcare costs of conditions such as diabetes and tobacco use are offset by reduced life expectancies. The net effect is that, in certain health states, less savings are required for healthcare. Baby Boomers avg jobs ages yr olds today have already worked 6.3 jobs Millennials are pace to have jobs before age 45. Source: Source: 10

11 The Pension Protection Act and 401(k)s by Jack VanDerhei, Temple University and EBRI Fellow What Auto-Enrollment Means for Workers Modeling research by the Employee Benefit Research Institute prior to the passage of PPA indicated that the automatic enrollment feature was likely to be particularly helpful to lowincome 401(k) participants (higher-income participants would also benefit, although not as dramatically). Specifically, under a 3 percent) default contribution rate and a life-cycle default investment, median income replacement rates at retirement for the lowest-income group would increase 19 percent points, to 42 percent if automatic enrolment were universally adopted by all 401(k) sponsors. Source: Neither NAGDCA, nor its employees or agents, nor members of its Executive Board, provide tax, financial, accounting or legal advice. This memorandum should not be construed as tax, financial, accounting or legal advice; it is provided solely for informational purposes. NAGDCA members, both government and industry, are urged to consult with their own attorneys and/or taxadvisors about the issues addressed herein. Copyright June 2016 NAGDCA 11

ASSESSING AMERICANS FINANCIAL AND RETIREMENT SECURITY

ASSESSING AMERICANS FINANCIAL AND RETIREMENT SECURITY AMERICAN COUNCIL OF LIFE INSURERS September 2017 OVERVIEW Millions of American households are on track to a financially secure future as a result of

ASSESSING AMERICANS FINANCIAL AND RETIREMENT SECURITY AMERICAN COUNCIL OF LIFE INSURERS September 2017 OVERVIEW Millions of American households are on track to a financially secure future as a result of

Ready or Not... The Impact of Retirement-Plan Design

Ready or Not... The Impact of Retirement-Plan Design Some 10,000 baby boomers a day are heading into retirement. Will they have enough income to finance retirements that, for some, may last as long as

Ready or Not... The Impact of Retirement-Plan Design Some 10,000 baby boomers a day are heading into retirement. Will they have enough income to finance retirements that, for some, may last as long as

Maximizing Your Defined Contribution Plan. Presented by Colleen Kuehnel, Senior Benefit Plan Advisor Michael Tackett, Benefit Plan Advisor

Maximizing Your Defined Contribution Plan Presented by Colleen Kuehnel, Senior Benefit Plan Advisor Michael Tackett, Benefit Plan Advisor 1 Today s Objectives Risks associated with participant directed

Maximizing Your Defined Contribution Plan Presented by Colleen Kuehnel, Senior Benefit Plan Advisor Michael Tackett, Benefit Plan Advisor 1 Today s Objectives Risks associated with participant directed

Adopting Automatic Enrollment in the Public Sector A Case Study

Adopting Automatic Enrollment in the Public Sector A Case Study By Robert L. Clark and Joshua M. Franzel A version of this case study was published on the Retirement Made Simpler Web site, available at

Adopting Automatic Enrollment in the Public Sector A Case Study By Robert L. Clark and Joshua M. Franzel A version of this case study was published on the Retirement Made Simpler Web site, available at

2017 RETIREMENT SECURITY BLUEPRINT

2017 RETIREMENT SECURITY BLUEPRINT Executive Summary of the Insured Retirement Institute 2017 Retirement Security Blueprint Americans face many challenges and obstacles in saving for retirement. In the

2017 RETIREMENT SECURITY BLUEPRINT Executive Summary of the Insured Retirement Institute 2017 Retirement Security Blueprint Americans face many challenges and obstacles in saving for retirement. In the

Sustaining State Retirement Benefits: Recent State Legislation Affecting Public Retirement Plans, Ronald Snell January 2010

Sustaining State Retirement Benefits: Recent State Legislation Affecting Public Retirement Plans, 2005-2009 Ronald Snell January 2010 INTRODUCTION Since 2007, investment losses and the weakness of state

Sustaining State Retirement Benefits: Recent State Legislation Affecting Public Retirement Plans, 2005-2009 Ronald Snell January 2010 INTRODUCTION Since 2007, investment losses and the weakness of state

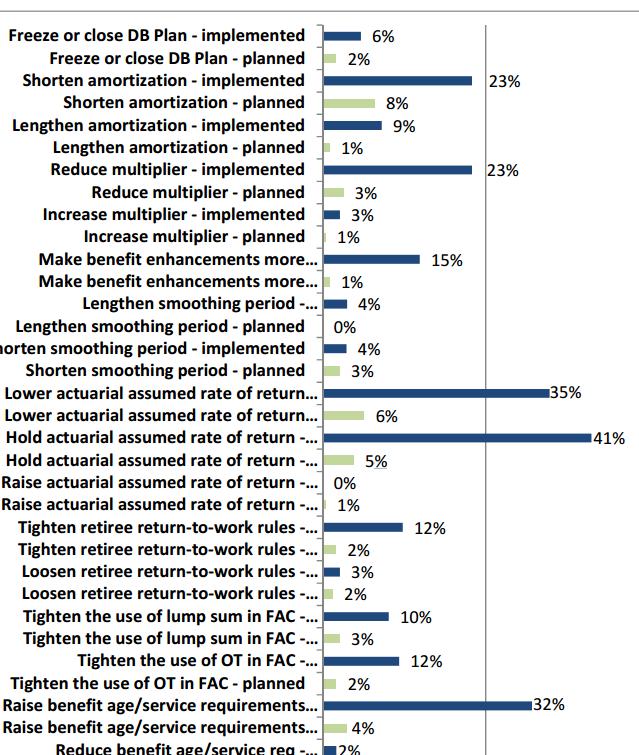

Selected Approved Changes to State Public Pensions to Restore or Preserve Plan Sustainability

Retirement Systems of Alabama Arizona Public Safety Personnel Retirement System Arizona State Retirement System Decreased contribution rates for new employees as follows: general state employees and teachers,

Retirement Systems of Alabama Arizona Public Safety Personnel Retirement System Arizona State Retirement System Decreased contribution rates for new employees as follows: general state employees and teachers,

2018 RETIREMENT SECURITY BLUEPRINT

2018 RETIREMENT SECURITY BLUEPRINT 2018 Retirement Security Blueprint Americans face many challenges and obstacles in saving for retirement. In the past, many Americans relied on employer-based pension

2018 RETIREMENT SECURITY BLUEPRINT 2018 Retirement Security Blueprint Americans face many challenges and obstacles in saving for retirement. In the past, many Americans relied on employer-based pension

ACHIEVING RETIREMENT SECURITY IN AN ERA OF UNCERTAINTY: Three Important Steps

ACHIEVING RETIREMENT SECURITY IN AN ERA OF UNCERTAINTY: Three Important Steps Christine C. Marcks President, Prudential Retirement While the goal of achieving retirement security is arguably more challenging

ACHIEVING RETIREMENT SECURITY IN AN ERA OF UNCERTAINTY: Three Important Steps Christine C. Marcks President, Prudential Retirement While the goal of achieving retirement security is arguably more challenging

Automatic Enrollment Guide

Automatic Enrollment Guide Introducing Automatic Enrollment Almost daily, new statistics are showing employers (plan sponsors) are taking a more proactive role in helping their employees save for retirement.

Automatic Enrollment Guide Introducing Automatic Enrollment Almost daily, new statistics are showing employers (plan sponsors) are taking a more proactive role in helping their employees save for retirement.

Re: RIN 1210-AB71; State Savings Arrangements Safe Harbor

Submitted via http://www.regulations.gov Office of Regulations and Interpretations Employee Benefits Security Administration Room N-5655 U.S. Department of Labor 200 Constitution Ave., NW Washington, DC

Submitted via http://www.regulations.gov Office of Regulations and Interpretations Employee Benefits Security Administration Room N-5655 U.S. Department of Labor 200 Constitution Ave., NW Washington, DC

City of Harlingen 401(a) Retirement Plan

Retirement Plan") City of Harlingen 401(a) Retirement Plan Administered by Investments Managed by Who We Are Operate primarily in public sector and non profit sectors Fee-Only Investing, Consulting and Third-Party Administrator

City of Harlingen 401(a) Retirement Plan Administered by Investments Managed by Who We Are Operate primarily in public sector and non profit sectors Fee-Only Investing, Consulting and Third-Party Administrator

Opting out of Retirement Plan Default Settings

WORKING PAPER Opting out of Retirement Plan Default Settings Jeremy Burke, Angela A. Hung, and Jill E. Luoto RAND Labor & Population WR-1162 January 2017 This paper series made possible by the NIA funded

WORKING PAPER Opting out of Retirement Plan Default Settings Jeremy Burke, Angela A. Hung, and Jill E. Luoto RAND Labor & Population WR-1162 January 2017 This paper series made possible by the NIA funded

How To Encourage Employees To Save For Retirement

How To Encourage Employees To Save For Retirement Plan Sponsors Can Increase 401(k) Participation By: Shortening or eliminating waiting periods for new employees and enrolling them during orientation Providing

How To Encourage Employees To Save For Retirement Plan Sponsors Can Increase 401(k) Participation By: Shortening or eliminating waiting periods for new employees and enrolling them during orientation Providing

Strengthen Public Sector Pensions By Helping All Workers Get Retirement Accounts. Teresa Ghilarducci Professor of Economics

Strengthen Public Sector Pensions By Helping All Workers Get Retirement Accounts Teresa Ghilarducci Professor of Economics Nearly Half of American Workers Have No Retirement Plan Current Population Survey

Strengthen Public Sector Pensions By Helping All Workers Get Retirement Accounts Teresa Ghilarducci Professor of Economics Nearly Half of American Workers Have No Retirement Plan Current Population Survey

Deferred Compensation Plan BOARD REPORT 14-51

Deferred Compensation Plan BOARD REPORT 14-51 Date: November 10, 2014 To: From: Board of Deferred Compensation Administration Staff Subject: Deferred Compensation Plan - Automatic Enrollment Program (AEP)

Deferred Compensation Plan BOARD REPORT 14-51 Date: November 10, 2014 To: From: Board of Deferred Compensation Administration Staff Subject: Deferred Compensation Plan - Automatic Enrollment Program (AEP)

Statement before the Conference Committee on Public Employee Pensions State Capital Sacramento, California

Statement before the Conference Committee on Public Employee Pensions State Capital Sacramento, California For a Hearing Exploring Hybrid Plan Design Options on Wednesday, January 25, 2012 Diane Oakley,

Statement before the Conference Committee on Public Employee Pensions State Capital Sacramento, California For a Hearing Exploring Hybrid Plan Design Options on Wednesday, January 25, 2012 Diane Oakley,

REPORT THE IMPACT OF THE OBAMA ECONOMIC PLAN FOR AMERICA S WORKING WOMEN

REPORT THE IMPACT OF THE OBAMA ECONOMIC PLAN FOR AMERICA S WORKING WOMEN REPORT: The Impact of the Obama Economic Plan for America s Working Women Over the past generation, women have made unparalleled

REPORT THE IMPACT OF THE OBAMA ECONOMIC PLAN FOR AMERICA S WORKING WOMEN REPORT: The Impact of the Obama Economic Plan for America s Working Women Over the past generation, women have made unparalleled

The Current State of Retirement Security in the United States. April 5, 2017

Hearing Statement The Before the U.S. Senate Committee on Banking, Housing, & Urban Development Subcommittee on Economic Policy The Current State of Retirement Security in the United States April 5, 2017

Hearing Statement The Before the U.S. Senate Committee on Banking, Housing, & Urban Development Subcommittee on Economic Policy The Current State of Retirement Security in the United States April 5, 2017

2012 ISSUE BROCHURE GOVERNMENT 457(B) PRIMER

PRIMER") National Association of Government Defined Contribution Administrators, Inc. 2012 ISSUE BROCHURE GOVERNMENT 457(B) PRIMER By: NAGDCA Publications Committee and Executive Board The following provides a

National Association of Government Defined Contribution Administrators, Inc. 2012 ISSUE BROCHURE GOVERNMENT 457(B) PRIMER By: NAGDCA Publications Committee and Executive Board The following provides a

HOW AMERICA SAVES Vanguard 2017 defined contribution plan data

HOW AMERICA SAVES 2018 Vanguard 2017 defined contribution plan data June 2018 Defined contribution (DC) retirement plans are the centerpiece of the privatesector retirement system in the United States.

HOW AMERICA SAVES 2018 Vanguard 2017 defined contribution plan data June 2018 Defined contribution (DC) retirement plans are the centerpiece of the privatesector retirement system in the United States.

How Retirement Readiness Varies by Gender and Family Status: A Retirement Savings Shortfall Assessment of Gen Xers

January 17, 2019 No. 471 How Retirement Readiness Varies by Gender and Family Status: A Retirement Savings Shortfall Assessment of Gen Xers By Jack VanDerhei, Ph.D., Employee Benefit Research Institute

January 17, 2019 No. 471 How Retirement Readiness Varies by Gender and Family Status: A Retirement Savings Shortfall Assessment of Gen Xers By Jack VanDerhei, Ph.D., Employee Benefit Research Institute

Adding Automatic Features to your 401(k) Retirement Plan

Retirement Plan") Adding Automatic Features to your 401(k) Retirement Plan Justin Goldstein, AIF, Director with Bronfman Rothschild Plan Advisors Shane Workman, Client Associate with Bronfman Rothschild Plan Advisors As

Adding Automatic Features to your 401(k) Retirement Plan Justin Goldstein, AIF, Director with Bronfman Rothschild Plan Advisors Shane Workman, Client Associate with Bronfman Rothschild Plan Advisors As

Measuring Retirement Plan Effectiveness

T. Rowe Price Measuring Retirement Plan Effectiveness T. Rowe Price Plan Meter helps sponsors assess and improve plan performance Retirement Insights Once considered ancillary to defined benefit (DB) pension

T. Rowe Price Measuring Retirement Plan Effectiveness T. Rowe Price Plan Meter helps sponsors assess and improve plan performance Retirement Insights Once considered ancillary to defined benefit (DB) pension

Deferred Compensation Plan PLAN GOVERNANCE & ADMINISTRATIVE ISSUES COMMITTEE REPORT 14-01

Deferred Compensation Plan PLAN GOVERNANCE & ADMINISTRATIVE ISSUES COMMITTEE REPORT 14-01 Date: August 8, 2014 To: Plan Governance & Administrative Issues Committee From: Subject: Staff Deferred Compensation

Deferred Compensation Plan PLAN GOVERNANCE & ADMINISTRATIVE ISSUES COMMITTEE REPORT 14-01 Date: August 8, 2014 To: Plan Governance & Administrative Issues Committee From: Subject: Staff Deferred Compensation

1102 Longworth House Office Building 1106 Longworth House Office Building Washington, DC Washington, DC 20515

February 23, 2017 The Honorable Kevin Brady The Honorable Richard Neal Chairman Ranking Member Committee on Ways and Means Committee on Ways and Means U.S. House of Representatives U.S. House of Representatives

February 23, 2017 The Honorable Kevin Brady The Honorable Richard Neal Chairman Ranking Member Committee on Ways and Means Committee on Ways and Means U.S. House of Representatives U.S. House of Representatives

Virginia Retirement System Modernization and Pension Reform Changes

Virginia Retirement System Modernization and Pension Reform Changes Virginia Government Finance Officer s Association Spring Conference May 24, 2013 Barry C. Faison VRS Chief Financial Officer Agenda Overview

Virginia Retirement System Modernization and Pension Reform Changes Virginia Government Finance Officer s Association Spring Conference May 24, 2013 Barry C. Faison VRS Chief Financial Officer Agenda Overview

HSA BANK HEALTH & WEALTH INDEX SM. HSA-Based Plans Drive Engagement Among Consumers

HSA BANK HEALTH & WEALTH INDEX SM HSA-Based Plans Drive Engagement Among Consumers 2018 TABLE OF CONTENTS Introduction... 1 Overview... 1 Outcomes... 2 Key Findings... 7 1: Consumers can improve their

HSA BANK HEALTH & WEALTH INDEX SM HSA-Based Plans Drive Engagement Among Consumers 2018 TABLE OF CONTENTS Introduction... 1 Overview... 1 Outcomes... 2 Key Findings... 7 1: Consumers can improve their

Title: The Role of Retirement Plan Design in Risk Management

MONDAY MAY 22, 2017 4:15-5:30PM Title: The Role of Retirement Plan Design in Risk Management MODERATOR SPEAKERS Casey Srader Budget Manager, City of Plano, TX Leslie Thompson Senior Consultant, Gabriel,

MONDAY MAY 22, 2017 4:15-5:30PM Title: The Role of Retirement Plan Design in Risk Management MODERATOR SPEAKERS Casey Srader Budget Manager, City of Plano, TX Leslie Thompson Senior Consultant, Gabriel,

How America Saves Vanguard 2016 defined contribution plan data

How America Saves 2017 Vanguard 2016 defined contribution plan data 1 June 2017 Defined contribution (DC) retirement plans are the centerpiece of the privatesector retirement system in the United States.

How America Saves 2017 Vanguard 2016 defined contribution plan data 1 June 2017 Defined contribution (DC) retirement plans are the centerpiece of the privatesector retirement system in the United States.

PREPARING FOR A MORE COMFORTABLE RETIREMENT

PREPARING FOR A MORE COMFORTABLE RETIREMENT As financial professionals who specialize in helping government employees transition from work to retirement, we understand that you may have questions about

PREPARING FOR A MORE COMFORTABLE RETIREMENT As financial professionals who specialize in helping government employees transition from work to retirement, we understand that you may have questions about

Millennial, Gen X, and Baby Boomer Workers and Retirees RETIREMENT SAVING & SPENDING STUDY

Millennial, Gen X, and Baby Boomer Workers and Retirees RETIREMENT SAVING & SPENDING STUDY Table of Contents Methodology Workers with 401(k)s: Millennials, Gen X, and Baby boomers Workers 401(k) Accounts

Millennial, Gen X, and Baby Boomer Workers and Retirees RETIREMENT SAVING & SPENDING STUDY Table of Contents Methodology Workers with 401(k)s: Millennials, Gen X, and Baby boomers Workers 401(k) Accounts

RETIREMENT QUESTIONS GOVERNMENT EMPLOYEES SHOULD BE ASKING

RETIREMENT QUESTIONS GOVERNMENT EMPLOYEES SHOULD BE ASKING 8/25/16 Preparing For a More Comfortable Retirement As financial professionals who specialize in helping government employees transition from

RETIREMENT QUESTIONS GOVERNMENT EMPLOYEES SHOULD BE ASKING 8/25/16 Preparing For a More Comfortable Retirement As financial professionals who specialize in helping government employees transition from

10 yrs. The benefit is capped at 80% of FAS. An elected official may. 2% (first 10 yrs.); or 2.25% (second 10 yrs.); or 2.5% over 20 yrs.

; or 2.25% (second 10 yrs.); or 2.5% over 20 yrs.") Table 3.13 STATE LEGISLATIVE RETIREMENT BENEFITS Alabama... Alaska... Age 60 with 10 yrs. Employee 6.75% 2% (first 10 yrs.); or 2.25% (second 10 yrs.); or 2.5% over 20 yrs. x average salary over 5 highest

Table 3.13 STATE LEGISLATIVE RETIREMENT BENEFITS Alabama... Alaska... Age 60 with 10 yrs. Employee 6.75% 2% (first 10 yrs.); or 2.25% (second 10 yrs.); or 2.5% over 20 yrs. x average salary over 5 highest

State-Facilitated Retirement Savings Programs: A Snapshot of Design Features

State-Facilitated Retirement Savings Programs: A Snapshot of Design Features State Brief 18-03 August 15, 2018 UPDATE 1 1This updates State Brief 18-03, dated May 31, 2018. property of the CRI. This document

State-Facilitated Retirement Savings Programs: A Snapshot of Design Features State Brief 18-03 August 15, 2018 UPDATE 1 1This updates State Brief 18-03, dated May 31, 2018. property of the CRI. This document

Getting Beyond Ordinary MANAGING PLAN COSTS IN AUTOMATIC PROGRAMS

PRICE PERSPECTIVE June 2015 In-depth analysis and insights to inform your decision-making. Getting Beyond Ordinary MANAGING PLAN COSTS IN AUTOMATIC PROGRAMS EXECUTIVE SUMMARY Plan sponsors today are faced

PRICE PERSPECTIVE June 2015 In-depth analysis and insights to inform your decision-making. Getting Beyond Ordinary MANAGING PLAN COSTS IN AUTOMATIC PROGRAMS EXECUTIVE SUMMARY Plan sponsors today are faced

NASRA ISSUE BRIEF: Cost-of-Living Adjustments

NASRA ISSUE BRIEF: Cost-of-Living Adjustments February 2014 Cost-of-living adjustments (COLAs) in some form are provided on most state and local government pensions. The purpose of a COLA is to offset

NASRA ISSUE BRIEF: Cost-of-Living Adjustments February 2014 Cost-of-living adjustments (COLAs) in some form are provided on most state and local government pensions. The purpose of a COLA is to offset

STATE UNIVERSITIES RETIREMENT SYSTEM OF ILLINOIS

STATE UNIVERSITIES RETIREMENT SYSTEM OF ILLINOIS GASB STATEMENT NOS. 67 AND 68 ACCOUNTING AND FINANCIAL REPORTING FOR PENSIONS JUNE 30, 2015 November 12, 2015 The Board of Trustees State Universities Retirement

STATE UNIVERSITIES RETIREMENT SYSTEM OF ILLINOIS GASB STATEMENT NOS. 67 AND 68 ACCOUNTING AND FINANCIAL REPORTING FOR PENSIONS JUNE 30, 2015 November 12, 2015 The Board of Trustees State Universities Retirement

A Guide to Planning a Financially Secure Retirement

A Guide to Planning a Financially Secure Retirement The information presented here is for general reference only, and may or may not be appropriate for your specific situation. A conversation with a financial

A Guide to Planning a Financially Secure Retirement The information presented here is for general reference only, and may or may not be appropriate for your specific situation. A conversation with a financial

WikiLeaks Document Release

WikiLeaks Document Release February 2, 2009 Congressional Research Service Report 98-972 Federal Employee Retirement Programs: Summary of Recent Trends Patrick J. Purcell, Domestic Social Policy Division

WikiLeaks Document Release February 2, 2009 Congressional Research Service Report 98-972 Federal Employee Retirement Programs: Summary of Recent Trends Patrick J. Purcell, Domestic Social Policy Division

SPECIAL CONSIDERATIONS WOMEN FACE IN RETIREMENT SECURITY

SPECIAL CONSIDERATIONS WOMEN FACE IN RETIREMENT SECURITY 2019 EBRIEFING SERIES FEBRUARY 6, 2019 SPECIAL CONSIDERATIONS WOMEN FACE IN RETIREMENT SECURITY Jack VanDerhei Research Director, EBRI The Cost

SPECIAL CONSIDERATIONS WOMEN FACE IN RETIREMENT SECURITY 2019 EBRIEFING SERIES FEBRUARY 6, 2019 SPECIAL CONSIDERATIONS WOMEN FACE IN RETIREMENT SECURITY Jack VanDerhei Research Director, EBRI The Cost

Work and Save. Almost Half of Baby Boomers & Gen Xers At Risk. % at risk

Work & Save % at risk Work and Save Almost Half of Baby Boomers & Gen Xers At Risk 100% 90% 80% 70% 60% 50% 40% 30% 20% 10% 0% Early Boomers Late Boomers Gen Xers EBRI 2003 RRR 51.7% 48.5% 51.7% EBRI 2012

Work & Save % at risk Work and Save Almost Half of Baby Boomers & Gen Xers At Risk 100% 90% 80% 70% 60% 50% 40% 30% 20% 10% 0% Early Boomers Late Boomers Gen Xers EBRI 2003 RRR 51.7% 48.5% 51.7% EBRI 2012

The Financial Engines National 401(k) Evaluation. Who benefits from today s 401(k)?

Evaluation. Who benefits from today s 401(k)?") 2010 The Financial Engines National 401(k) Evaluation Who benefits from today s 401(k)? Foreword Welcome to the 2010 edition of The Financial Engines National 401(k) Evaluation. When we first evaluated

2010 The Financial Engines National 401(k) Evaluation Who benefits from today s 401(k)? Foreword Welcome to the 2010 edition of The Financial Engines National 401(k) Evaluation. When we first evaluated

More & More Americans Having to Work Past Age 70

More & More Americans Having to Work Past Age 70 July 18, 2017 by Gary Halbert of Halbert Wealth Management 1. Almost One-Fifth of Americans Are Working Past Age 70 2. Seniors, There s No Guarantee of

More & More Americans Having to Work Past Age 70 July 18, 2017 by Gary Halbert of Halbert Wealth Management 1. Almost One-Fifth of Americans Are Working Past Age 70 2. Seniors, There s No Guarantee of

A Post Crisis Assessment of Retirement Income Adequacy for Baby Boomers and Gen Xers

February 2011 No. 354 A Post Crisis Assessment of Retirement Income Adequacy for Baby Boomers and Gen Xers By Jack VanDerhei, Employee Benefit Research Institute E X E C U T I V E S U M M A R Y DETERMINING

February 2011 No. 354 A Post Crisis Assessment of Retirement Income Adequacy for Baby Boomers and Gen Xers By Jack VanDerhei, Employee Benefit Research Institute E X E C U T I V E S U M M A R Y DETERMINING

Earning for Today and Saving for Tomorrow. Retirement Savings Plan 401(k) inspiring possibilities

inspiring possibilities") Earning for Today and Saving for Tomorrow Retirement Savings Plan 401(k) inspiring possibilities Retirement Savings Plan 401(k) Advocate Health Care Network offers the Advocate Health Care Network Retirement

Earning for Today and Saving for Tomorrow Retirement Savings Plan 401(k) inspiring possibilities Retirement Savings Plan 401(k) Advocate Health Care Network offers the Advocate Health Care Network Retirement

MUNICIPAL EMPLOYEES' RETIREMENT SYSTEM OF MICHIGAN

MUNICIPAL EMPLOYEES' RETIREMENT SYSTEM OF MICHIGAN Summary of Actuarial Assumptions and Actuarial Funding Method as of December 31, 2015 Actuarial Assumptions To calculate MERS contribution requirements,

MUNICIPAL EMPLOYEES' RETIREMENT SYSTEM OF MICHIGAN Summary of Actuarial Assumptions and Actuarial Funding Method as of December 31, 2015 Actuarial Assumptions To calculate MERS contribution requirements,

ERISA Advisory Council U.S. Department of Labor

T-180 ERISA Advisory Council U.S. Department of Labor Hearing on: LIFETIME PARTICIPATION IN PLANS June 17, 2014 C5320 Room 6 at the U.S. Department of Labor Statement for the Record by Jack VanDerhei,

T-180 ERISA Advisory Council U.S. Department of Labor Hearing on: LIFETIME PARTICIPATION IN PLANS June 17, 2014 C5320 Room 6 at the U.S. Department of Labor Statement for the Record by Jack VanDerhei,

Spotlight. Significant Reforms to State Retirement Systems. Executive Summary

Spotlight on Significant Reforms to State Retirement Systems Keith Brainard and Alex Brown National Association of State Retirement Administrators June 2016 Executive Summary Although states have a history

Spotlight on Significant Reforms to State Retirement Systems Keith Brainard and Alex Brown National Association of State Retirement Administrators June 2016 Executive Summary Although states have a history

Member s Guide to: DROP. Deferred Retirement Option Plan.

Member s Guide to: DROP Deferred Retirement Option Plan www.op-f.org PLAN DEFERRED RETIREMENT DROP The Deferred Retirement Option Plan (DROP) is an optional benefit that allows eligible police officers

Member s Guide to: DROP Deferred Retirement Option Plan www.op-f.org PLAN DEFERRED RETIREMENT DROP The Deferred Retirement Option Plan (DROP) is an optional benefit that allows eligible police officers

State Retirement Systems: Rhode Island Versus the Nation

HELIN Consortium HELIN Digital Commons Library Archive HELIN State Law Library 1993 State Retirement Systems: Rhode Island Versus the Nation Follow this and additional works at: http://helindigitalcommons.org/lawarchive

HELIN Consortium HELIN Digital Commons Library Archive HELIN State Law Library 1993 State Retirement Systems: Rhode Island Versus the Nation Follow this and additional works at: http://helindigitalcommons.org/lawarchive

Small business edition

HOW AMERICA SAVES 2018 Small business edition 2018 Vanguard Retirement Plan Access supplement to How America Saves Introduction Defined contribution (DC) retirement plans are the centerpiece of the private-sector

HOW AMERICA SAVES 2018 Small business edition 2018 Vanguard Retirement Plan Access supplement to How America Saves Introduction Defined contribution (DC) retirement plans are the centerpiece of the private-sector

Small business edition

How America Saves 2017 Small business edition 2017 Vanguard Retirement Plan Access supplement to How America Saves Introduction Defined contribution (DC) retirement plans are the centerpiece of the private-sector

How America Saves 2017 Small business edition 2017 Vanguard Retirement Plan Access supplement to How America Saves Introduction Defined contribution (DC) retirement plans are the centerpiece of the private-sector

General Explanations of the Administration s Fiscal Year 2014 Revenue Proposals

General Explanations of the Administration s Fiscal Year 2014 Revenue Proposals Department of the Treasury April 2013 TAX CUTS FOR FAMILIES AND INDIVIDUALS PROVIDE FOR AUTOMATIC ENROLLMENT IN INDIVIDUAL

General Explanations of the Administration s Fiscal Year 2014 Revenue Proposals Department of the Treasury April 2013 TAX CUTS FOR FAMILIES AND INDIVIDUALS PROVIDE FOR AUTOMATIC ENROLLMENT IN INDIVIDUAL

Getting Beyond Ordinary MANAGING PLAN COSTS IN AUTOMATIC PROGRAMS

PRICE PERSPECTIVE In-depth analysis and insights to inform your decision-making. Getting Beyond Ordinary MANAGING PLAN COSTS IN AUTOMATIC PROGRAMS EXECUTIVE SUMMARY Plan sponsors today are faced with unprecedented

PRICE PERSPECTIVE In-depth analysis and insights to inform your decision-making. Getting Beyond Ordinary MANAGING PLAN COSTS IN AUTOMATIC PROGRAMS EXECUTIVE SUMMARY Plan sponsors today are faced with unprecedented

Closing the Gap Between Belief and Behavior

Closing the Gap Between Belief and Behavior BlackRock s 2010 401(k) Participant Behaviors and Attitudes Study DefinedContribution 2 Closing the Gap Between Belief and Behavior The Blackrock survey: Understanding

Closing the Gap Between Belief and Behavior BlackRock s 2010 401(k) Participant Behaviors and Attitudes Study DefinedContribution 2 Closing the Gap Between Belief and Behavior The Blackrock survey: Understanding

How Plan Sponsors of Larger 401(k) Plans Are Aiming for Retirement Preparedness: A Human Resources Perspective

Plans Are Aiming for Retirement Preparedness: A Human Resources Perspective") How Plan Sponsors of Larger 401(k) Plans Are Aiming for Retirement Preparedness: A Human Resources Perspective MORE THAN TEN YEARS after the Pension Protection Act (PPA) was signed into law, along with

How Plan Sponsors of Larger 401(k) Plans Are Aiming for Retirement Preparedness: A Human Resources Perspective MORE THAN TEN YEARS after the Pension Protection Act (PPA) was signed into law, along with

TESTIMONY. James A. Wolf. President, TIAA-CREF Retirement Services. before the. President s Commission to Strengthen Social Security

TESTIMONY of James A. Wolf President, TIAA-CREF Retirement Services before the President s Commission to Strengthen Social Security The Honorable Daniel Patrick Moynihan and Richard Parsons, Co-Chairs

TESTIMONY of James A. Wolf President, TIAA-CREF Retirement Services before the President s Commission to Strengthen Social Security The Honorable Daniel Patrick Moynihan and Richard Parsons, Co-Chairs

COMPARATIVE STUDY

WISCONSIN LEGISLATIVE COUNCIL 2017-18 COMPARATIVE STUDY OF MAJOR PUBLIC EMPLOYEE RETIREMENT SYSTEMS Prepared by: Daniel Schmidt, Principal Analyst Wisconsin Legislative Council February 2019 One East Main

WISCONSIN LEGISLATIVE COUNCIL 2017-18 COMPARATIVE STUDY OF MAJOR PUBLIC EMPLOYEE RETIREMENT SYSTEMS Prepared by: Daniel Schmidt, Principal Analyst Wisconsin Legislative Council February 2019 One East Main

PLAN DESIGN: Defined Contribution Redefined October Labs: Defined Contribution. Highlights

Labs: Defined Contribution PLAN DESIGN: Defined Contribution Redefined October 2018 Highlights + + Auto-enrollment, auto-escalation and qualified default investment alternatives (QDIAs) have helped increase

Labs: Defined Contribution PLAN DESIGN: Defined Contribution Redefined October 2018 Highlights + + Auto-enrollment, auto-escalation and qualified default investment alternatives (QDIAs) have helped increase

Retirement Solutions. Engaging the Next Generations in Retirement Savings

www.calamos.com Retirement Solutions Engaging the Next Generations in Retirement Savings Improving Retirement Readiness for the Next Generations by Applying Behavioral Finance & Thoughtful Plan Design

www.calamos.com Retirement Solutions Engaging the Next Generations in Retirement Savings Improving Retirement Readiness for the Next Generations by Applying Behavioral Finance & Thoughtful Plan Design

Federal Employees Retirement System: Summary of Recent Trends

Federal Employees Retirement System: Summary of Recent Trends Katelin P. Isaacs Analyst in Income Security January 11, 2011 Congressional Research Service CRS Report for Congress Prepared for Members and

Federal Employees Retirement System: Summary of Recent Trends Katelin P. Isaacs Analyst in Income Security January 11, 2011 Congressional Research Service CRS Report for Congress Prepared for Members and

INCREASING STRATEGIES FOR EMPLOYEE SUCCESS. How Plan Sponsors Can Help Participants Save For Retirement

Research shows that employees have better retirement outcomes when plan sponsors provide greater support. We developed this special guide to help sponsors improve employee engagement and savings behavior.

Research shows that employees have better retirement outcomes when plan sponsors provide greater support. We developed this special guide to help sponsors improve employee engagement and savings behavior.

Status of Local Pension Funding Fiscal Year 2012: An Evaluation of Ten Local Government Employee Pension Funds in Cook County

Status of Local Pension Funding Fiscal Year 2012: An Evaluation of Ten Local Government Employee Pension Funds in Cook County October 2, 2014 ACKNOWLEDGEMENTS The Civic Federation would like to thank the

Status of Local Pension Funding Fiscal Year 2012: An Evaluation of Ten Local Government Employee Pension Funds in Cook County October 2, 2014 ACKNOWLEDGEMENTS The Civic Federation would like to thank the

Medicare Part D Retiree Drug Subsidy Payments

Caution: ACA is under constant review. Provisions could be adjusted, re- interpreted and even repealed in the future. This is a snapshot as of December 10, 2014. 2013 W- 2 Health Care Value Reporting January

Caution: ACA is under constant review. Provisions could be adjusted, re- interpreted and even repealed in the future. This is a snapshot as of December 10, 2014. 2013 W- 2 Health Care Value Reporting January

S TAT E U NIVERSITIES R ETIREMENT SYSTEM OF I L LINOIS

S TAT E U NIVERSITIES R ETIREMENT SYSTEM OF I L LINOIS G A S B S T A T E M E N T N O S. 6 7 A N D 6 8 A C C O U N T I N G AND F I N A N C I A L R E P O R T I N G F O R P E N S I O N S J U N E 3 0, 2 0

S TAT E U NIVERSITIES R ETIREMENT SYSTEM OF I L LINOIS G A S B S T A T E M E N T N O S. 6 7 A N D 6 8 A C C O U N T I N G AND F I N A N C I A L R E P O R T I N G F O R P E N S I O N S J U N E 3 0, 2 0

Social Security, Pensions and Politics: National Directions

Social Security, Pensions and Politics: National Directions Dallas L. Salisbury Employee Benefit Research Institute www.ebri.org EBRI Mission To contribute to, to encourage, and to enhance the development

Social Security, Pensions and Politics: National Directions Dallas L. Salisbury Employee Benefit Research Institute www.ebri.org EBRI Mission To contribute to, to encourage, and to enhance the development

Actuarial SECTION. A Tradition of Service

Actuarial SECTION A Tradition of Service We were created by the Michigan Legislature in 1945 with one simple goal: to help municipalities offer affordable, sustainable retirement solutions for their employees.

Actuarial SECTION A Tradition of Service We were created by the Michigan Legislature in 1945 with one simple goal: to help municipalities offer affordable, sustainable retirement solutions for their employees.

State Universities Retirement System of Illinois. GASB Statement Nos. 67 and 68 Accounting and Financial Reporting for Pensions as of June 30, 2017

State Universities Retirement System of Illinois GASB Statement Nos. 67 and 68 Accounting and Financial Reporting for Pensions as of June 30, 2017 November 6, 2017 The Board of Trustees State Universities

State Universities Retirement System of Illinois GASB Statement Nos. 67 and 68 Accounting and Financial Reporting for Pensions as of June 30, 2017 November 6, 2017 The Board of Trustees State Universities

ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, City of Plantation General Employees Retirement System

ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2014 City of Plantation General Employees Retirement System ANNUAL EMPLOYER CONTRIBUTION IS DETERMINED BY THIS VALUATION FOR THE FISCAL YEAR ENDING SEPTEMBER

ACTUARIAL VALUATION REPORT AS OF OCTOBER 1, 2014 City of Plantation General Employees Retirement System ANNUAL EMPLOYER CONTRIBUTION IS DETERMINED BY THIS VALUATION FOR THE FISCAL YEAR ENDING SEPTEMBER

PERS: By The Numbers

PERS: By The Numbers February 2014 Topic Page(s) System Demographics... 2 System Benefits 3-11 System Funding Level and Status 12-14 System Revenue... 15-19 Economic Benefit of PERS... 20-22 Public Employees

PERS: By The Numbers February 2014 Topic Page(s) System Demographics... 2 System Benefits 3-11 System Funding Level and Status 12-14 System Revenue... 15-19 Economic Benefit of PERS... 20-22 Public Employees

SECTION 403(B) PLANS: WHAT NONPROFIT SPONSORS OF EMPLOYEE RETIREMENT PLANS NEED TO KNOW

PLANS: WHAT NONPROFIT SPONSORS OF EMPLOYEE RETIREMENT PLANS NEED TO KNOW") SECTION 403(B) PLANS: WHAT NONPROFIT SPONSORS OF EMPLOYEE RETIREMENT PLANS NEED TO KNOW ROHIT A. NAFDAY, ESQ. AND JONATHAN F. LEWIS, ESQ. June 2011 This publication is available at online at www.probonopartnership.org/pages/publications/all-publicationsfaqs-x

SECTION 403(B) PLANS: WHAT NONPROFIT SPONSORS OF EMPLOYEE RETIREMENT PLANS NEED TO KNOW ROHIT A. NAFDAY, ESQ. AND JONATHAN F. LEWIS, ESQ. June 2011 This publication is available at online at www.probonopartnership.org/pages/publications/all-publicationsfaqs-x

SUMMARY PLAN DESCRIPTION PIXAR Employee's 401(k) Retirement Plan

Retirement Plan") SUMMARY PLAN DESCRIPTION PIXAR Employee's 401(k) Retirement Plan This information is not intended to be a substitute for specific individualized tax, legal, or investment planning advice. Where specific

SUMMARY PLAN DESCRIPTION PIXAR Employee's 401(k) Retirement Plan This information is not intended to be a substitute for specific individualized tax, legal, or investment planning advice. Where specific

Special Report. Retirement Confidence in America: Getting Ready for Tomorrow EBRI EMPLOYEE BENEFIT RESEARCH INSTITUTE. and Issue Brief no.

December 1994 Jan. Feb. Mar. Retirement Confidence in America: Getting Ready for Tomorrow Apr. May Jun. Jul. Aug. EBRI EMPLOYEE BENEFIT RESEARCH INSTITUTE Special Report and Issue Brief no. 156 Most Americans

December 1994 Jan. Feb. Mar. Retirement Confidence in America: Getting Ready for Tomorrow Apr. May Jun. Jul. Aug. EBRI EMPLOYEE BENEFIT RESEARCH INSTITUTE Special Report and Issue Brief no. 156 Most Americans

The Real Deal 2018 Retirement Income Adequacy Study

The Real Deal 2018 Retirement Income Adequacy Study Table of Contents Introduction.... 3 What's New in The Real Deal?... 6 Retirement Readiness The Averages.... 7 Savings Rates... 10 Income.... 15 Generations....

The Real Deal 2018 Retirement Income Adequacy Study Table of Contents Introduction.... 3 What's New in The Real Deal?... 6 Retirement Readiness The Averages.... 7 Savings Rates... 10 Income.... 15 Generations....

Alternative Retirement Financial Plans and Their Features

RETIREMENT ACCOUNTS Gary R. Evans, 2006-2017, September 20, 2017. The various retirement investment accounts discussed in this document all offer the potential for healthy longterm returns with substantial

RETIREMENT ACCOUNTS Gary R. Evans, 2006-2017, September 20, 2017. The various retirement investment accounts discussed in this document all offer the potential for healthy longterm returns with substantial

Background. 401(k) Plans Automatic Enrollment & Safe Harbor after PPA

Plans Automatic Enrollment & Safe Harbor after PPA") 401(k) Plans Automatic Enrollment & Safe Harbor after PPA Pam Thein Partner, Oppenheimer Wolff & Donnelly LLP Kim Wright - Vice President, Regional Director, Wachovia Retirement Services September 10,

401(k) Plans Automatic Enrollment & Safe Harbor after PPA Pam Thein Partner, Oppenheimer Wolff & Donnelly LLP Kim Wright - Vice President, Regional Director, Wachovia Retirement Services September 10,

Auto Enrollment in 401(k) and 403(b) Plans: Can one solution fit every plan s needs?

and 403(b) Plans: Can one solution fit every plan s needs?") Auto Enrollment in 401(k) and 403(b) Plans: Can one solution fit every plan s needs? Executive summary: Automatic enrollment and automatic deferral escalation continue to get a lot of attention in the

Auto Enrollment in 401(k) and 403(b) Plans: Can one solution fit every plan s needs? Executive summary: Automatic enrollment and automatic deferral escalation continue to get a lot of attention in the

Prudential Retirement s Fifth Annual Workplace Report on Retirement Planning

Prudential Retirement s Fifth Annual Workplace Report on Retirement Planning Quantitative research with America s youngest and oldest workers to test attitudes about the new auto-pilot retirement plans.

Prudential Retirement s Fifth Annual Workplace Report on Retirement Planning Quantitative research with America s youngest and oldest workers to test attitudes about the new auto-pilot retirement plans.

Data can inspire plan changes

REFERENCE POINT Data can inspire plan changes TABLE OF CONTENTS Executive Summary... 3 Auto Solutions... 5 Contributions...15 Investments...29 Loan and Disbursement Behavior...40 Need more robust industry

REFERENCE POINT Data can inspire plan changes TABLE OF CONTENTS Executive Summary... 3 Auto Solutions... 5 Contributions...15 Investments...29 Loan and Disbursement Behavior...40 Need more robust industry

S TAT E U NIVERSITIES R E T I REMENT SYSTEM OF I L L INOIS

S TAT E U NIVERSITIES R E T I REMENT SYSTEM OF I L L INOIS G A S B S T A T E M E N T N O. 6 7 P L A N R E P O R T I N G A N D A C C O U N T I N G S C H E D U L E S J U N E 3 0, 2 0 1 4 October 10, 2014

S TAT E U NIVERSITIES R E T I REMENT SYSTEM OF I L L INOIS G A S B S T A T E M E N T N O. 6 7 P L A N R E P O R T I N G A N D A C C O U N T I N G S C H E D U L E S J U N E 3 0, 2 0 1 4 October 10, 2014

Retirement Savings Plan 401(k)

") Retirement Savings Plan 401(k) Retirement Savings Plan 401(k) Advocate Health Care Network offers the Advocate Health Care Network Retirement Savings Plan 401(k) ( 401(k) Plan or Plan ) as part of its

Retirement Savings Plan 401(k) Retirement Savings Plan 401(k) Advocate Health Care Network offers the Advocate Health Care Network Retirement Savings Plan 401(k) ( 401(k) Plan or Plan ) as part of its

2015 COMPARATIVE STUDY OF MAJOR PUBLIC EMPLOYEE RETIREMENT SYSTEMS

WISCONSIN LEGISLATIVE COUNCIL 2015 COMPARATIVE STUDY OF MAJOR PUBLIC EMPLOYEE RETIREMENT SYSTEMS Prepared by: Daniel Schmidt, Principal Analyst Wisconsin Legislative Council December 2016 One East Main

WISCONSIN LEGISLATIVE COUNCIL 2015 COMPARATIVE STUDY OF MAJOR PUBLIC EMPLOYEE RETIREMENT SYSTEMS Prepared by: Daniel Schmidt, Principal Analyst Wisconsin Legislative Council December 2016 One East Main

Low Returns and Optimal Retirement Savings

Low Returns and Optimal Retirement Savings Title Goes Here David Blanchett, Morningstar Michael Finke, The American College Wade Pfau, The American College Retirement According to the Life Cycle Hypothesis

Low Returns and Optimal Retirement Savings Title Goes Here David Blanchett, Morningstar Michael Finke, The American College Wade Pfau, The American College Retirement According to the Life Cycle Hypothesis

Expanded reporting and disclosure requirements Single-employer pension plans under ERISA

2019 Expanded reporting and disclosure requirements Single-employer pension plans under ERISA Table of Contents Reporting Requirements 1 Disclosure Requirements 4 Individual Deferred Vested Pension Statement

2019 Expanded reporting and disclosure requirements Single-employer pension plans under ERISA Table of Contents Reporting Requirements 1 Disclosure Requirements 4 Individual Deferred Vested Pension Statement

17 th Annual Transamerica Retirement Survey Influences of Gender on Retirement Readiness

1 th Annual Transamerica Retirement Survey Influences of Gender on Retirement Readiness December 2016 TCRS 1335-1216 Transamerica Institute, 2016 Welcome to the 1 th Annual Transamerica Retirement Survey

1 th Annual Transamerica Retirement Survey Influences of Gender on Retirement Readiness December 2016 TCRS 1335-1216 Transamerica Institute, 2016 Welcome to the 1 th Annual Transamerica Retirement Survey

PROMOTING PLAN SUCCESS

PROMOTING PLAN SUCCESS BEST PRACTICES FOR IMPROVING EMPLOYEE RETIREMENT READINESS INSIDE Industry Insights I Trends I Best Practices EVERYONE BENEFITS WHEN EMPLOYEES CAN RETIRE ON TIME This paper provides

PROMOTING PLAN SUCCESS BEST PRACTICES FOR IMPROVING EMPLOYEE RETIREMENT READINESS INSIDE Industry Insights I Trends I Best Practices EVERYONE BENEFITS WHEN EMPLOYEES CAN RETIRE ON TIME This paper provides

HOW HAVE WORKERS RESPONDED TO OREGON S AUTO-IRA?

December 2018, Number 18-22 RETIREMENT RESEARCH HOW HAVE WORKERS RESPONDED TO OREGON S AUTO-IRA? By Anek Belbase and Geoffrey T. Sanzenbacher* Introduction Only about half of private sector workers are

December 2018, Number 18-22 RETIREMENT RESEARCH HOW HAVE WORKERS RESPONDED TO OREGON S AUTO-IRA? By Anek Belbase and Geoffrey T. Sanzenbacher* Introduction Only about half of private sector workers are

Governmental Accounting Standards Board: GASB Statement 45

Governmental Accounting Standards Board: GASB Statement 45 GASB 45: New Rules In 2004, the Governmental Accounting Standards Board (GASB) released Statement 45 (GASB 45) concerning health and other non-pension

Governmental Accounting Standards Board: GASB Statement 45 GASB 45: New Rules In 2004, the Governmental Accounting Standards Board (GASB) released Statement 45 (GASB 45) concerning health and other non-pension

Plan Sponsor Webcast Series

Plan Sponsor Webcast Series Roth 401(k) Contributions, Safe Harbor 401(k) Plans and Automatic Enrollment Amy Pocino Kelly Julia L. Bringhurst www.morganlewis.com May 5, 2010 Roth 401(k) Contributions 2

Plan Sponsor Webcast Series Roth 401(k) Contributions, Safe Harbor 401(k) Plans and Automatic Enrollment Amy Pocino Kelly Julia L. Bringhurst www.morganlewis.com May 5, 2010 Roth 401(k) Contributions 2

Member s Guide to: Deferred Retirement Option Plan (DROP)

") Member s Guide to: Deferred Retirement Option Plan (DROP) PLAN DEFERRED RETIREMENT DROP OPTION The Deferred Retirement Option Plan (DROP) is an optional benefit that allows eligible police officers and

Member s Guide to: Deferred Retirement Option Plan (DROP) PLAN DEFERRED RETIREMENT DROP OPTION The Deferred Retirement Option Plan (DROP) is an optional benefit that allows eligible police officers and

Submitted electronically to

April 15, 2013 The ERISA Industry Committee Submitted electronically to tax.reform@mail.house.gov Congressmen Pat Tiberi and Ron Kind Pensions/Retirement Tax Reform Working Group United State House of

April 15, 2013 The ERISA Industry Committee Submitted electronically to tax.reform@mail.house.gov Congressmen Pat Tiberi and Ron Kind Pensions/Retirement Tax Reform Working Group United State House of

The Impact of Auto- enrollment and Automatic Contribution Escalation on Retirement Income Adequacy

The Impact of Auto- enrollment and Automatic Contribution Escalation on Retirement Income Adequacy By Jack VanDerhei, Employee Benefit Research Institute, and Lori Lucas, Callan Associates New Simulation

The Impact of Auto- enrollment and Automatic Contribution Escalation on Retirement Income Adequacy By Jack VanDerhei, Employee Benefit Research Institute, and Lori Lucas, Callan Associates New Simulation

= $22, = $143,211. These considerations yield the following time line.

1 America s Retirement Challenge, (A Mathematical Model) (Preliminary Version) Floyd Vest, August 2013 This article is based on a speech entitled Meeting America s Retirement Challenge, given by Ronald

1 America s Retirement Challenge, (A Mathematical Model) (Preliminary Version) Floyd Vest, August 2013 This article is based on a speech entitled Meeting America s Retirement Challenge, given by Ronald

Written. Before the. Regarding. September 2009

Written Statementt of Larry H. Goldbrum, Esq. General Counsel, The SPARK Institute Before the UNITED STATES DEPARTMENT OF LABOR ERISA ADVISORY COUNCIL Regarding Retirement Security September 2009 The SPARK

Written Statementt of Larry H. Goldbrum, Esq. General Counsel, The SPARK Institute Before the UNITED STATES DEPARTMENT OF LABOR ERISA ADVISORY COUNCIL Regarding Retirement Security September 2009 The SPARK

The evolving retirement landscape

The evolving retirement landscape This report has been sponsored by A Research Report by Lauren Wilkinson and Tim Pike Published by the Pensions Policy Institute May 2018 978-1-906284-52-23 www.pensionspolicyinstitute.org.uk

The evolving retirement landscape This report has been sponsored by A Research Report by Lauren Wilkinson and Tim Pike Published by the Pensions Policy Institute May 2018 978-1-906284-52-23 www.pensionspolicyinstitute.org.uk

TRS UPDATE /13/12

TRS UPDATE 2012 12/13/12 Topics for Discussion Status of the TRS Fund Legislation from 82 nd Session Interim studies TRS-Care Sustainability Pension Plan Design What s Next? Upcoming Legislative Session

TRS UPDATE 2012 12/13/12 Topics for Discussion Status of the TRS Fund Legislation from 82 nd Session Interim studies TRS-Care Sustainability Pension Plan Design What s Next? Upcoming Legislative Session

MUNICIPAL EMPLOYEES' RETIREMENT SYSTEM OF MICHIGAN APPENDIX TO THE ANNUAL ACTUARIAL VALUATION REPORT DECEMBER 31, 2016

MUNICIPAL EMPLOYEES' RETIREMENT SYSTEM OF MICHIGAN APPENDIX TO THE ANNUAL ACTUARIAL VALUATION REPORT DECEMBER 31, 2016 Summary of Plan Provisions, Actuarial Assumptions and Actuarial Funding Method as

MUNICIPAL EMPLOYEES' RETIREMENT SYSTEM OF MICHIGAN APPENDIX TO THE ANNUAL ACTUARIAL VALUATION REPORT DECEMBER 31, 2016 Summary of Plan Provisions, Actuarial Assumptions and Actuarial Funding Method as

State of Minnesota. State-Administered Private Sector Employee Retirement Savings Study

State of Minnesota State-Administered Private Sector Employee Retirement Savings Study Prepared by Deloitte Consulting LLP January 13, 2017 1 Contents INTRODUCTION... 4 APPROACH... 4 EXECUTIVE SUMMARY...

State of Minnesota State-Administered Private Sector Employee Retirement Savings Study Prepared by Deloitte Consulting LLP January 13, 2017 1 Contents INTRODUCTION... 4 APPROACH... 4 EXECUTIVE SUMMARY...

pay, but they able to

Universal Coverage: USA Retirement Funds would provide every working person in America with access to a retirement plan throughh an automatic payroll deduction. Employers with more than 10 employees would

Universal Coverage: USA Retirement Funds would provide every working person in America with access to a retirement plan throughh an automatic payroll deduction. Employers with more than 10 employees would