SPECIAL CONSIDERATIONS WOMEN FACE IN RETIREMENT SECURITY

|

|

|

- Bruno Chandler

- 5 years ago

- Views:

Transcription

1 SPECIAL CONSIDERATIONS WOMEN FACE IN RETIREMENT SECURITY 2019 EBRIEFING SERIES FEBRUARY 6, 2019

2 SPECIAL CONSIDERATIONS WOMEN FACE IN RETIREMENT SECURITY Jack VanDerhei Research Director, EBRI The Cost of Living Longer: How Retirement Readiness Varies by Gender and Family Status Anna M. Rappaport, President, Anna Rappaport Consulting Women Take the Wheel: Destination Retirement Moderated by Lori Lucas, CFA, President and CEO, EBRI COPYRIGHT

3 3

4 HOW RETIREMENT READINESS VARIES BY GENDER AND FAMILY STATUS 2019 EBRIefing Series February 6, 2019 Jack VanDerhei, Director of Research, EBRI

5 EBRI RETIREMENT SECURITY PROJECTION MODEL Accumulation phase Simulates retirement income/wealth for households currently ages from defined contribution, defined benefit, IRA, Social Security and net housing equity Pension plan parameters coded from a time series of several hundred plans. 401(k) asset allocation and contribution behavior based on individual administrative records oannual linked records dating back to 1996 omore than 27 million employees in 110,000 plans o More than 25 million IRA accounts owned by 20 million unique individuals Retirement phase Simulates 1,000 alternative life-paths for each household, starting at 65 Deterministic modeling of costs for food, apparel and services, transportation, entertainment, reading and education, housing, and basic health expenditures. Stochastic modeling of longevity risk, investment risk, nursing facility care and home based health care. Produces the following output metrics: Retirement Readiness Rating (RRR) = Percentage of simulated life-paths that do NOT run short of money in retirement Retirement Savings Shortfalls (RSS) = Present value of deficits for those who run short of money in retirement 5 For a list of approximately 40 studies using RSPM please see: bit.ly/ebri-rspm

6 MODIFICATIONS FOR TODAY Recently we have been asked to look more specifically at the retirement income adequacy for widows Recoded the decumulation module for RSPM to change this to: single male single female married married (husband dies first) married (wife dies first) 6

7 AVERAGE RETIREMENT DEFICITS BY MARITAL STATUS AND GENDER Means of Retirement Savings Shortfalls for Gen Xers by marital status and gender (includes bifurcation for sequence of death for married) $80,000 $70,000 $72,883 $60,000 $50,000 $40,000 $37,690 $30,000 $20,000 $10,000 $- $18,476 $22,783 married, female dies first married, male dies first single female single male Source: EBRI Retirement Security Projection Model, Version Employee Benefit Research Institute 2019

8 AVERAGE RETIREMENT DEFICITS FOR THOSE WITH A DEFICIT Means of Retirement Savings Shortfalls for Gen Xers by marital status and gender (includes bifurcation for sequence of death for married) $140,000 $131,674 $128,417 $120,000 $100,000 $80,000 $60,000 $40,000 $20,000 $- $82,937 $76,896 married, female dies first married, male dies first single female single male Source: EBRI Retirement Security Projection Model, Version Employee Benefit Research Institute 2019

9 RETIREMENT DEFICITS BY (PRE-RETIREMENT) WAGE QUARTILES Means of Retirement Savings Shortfalls for Gen Xers by age-specific pre-retirement income quartile, marital status and gender (includes bifurcation for sequence of death for married) $120,000 $100,000 $80,000 $60,000 $40,000 $20,000 $- lowest second third highest married, female dies first $67,829 $48,105 $27,868 $8,522 married, male dies first $86,479 $55,887 $30,109 $11,354 single female $110,412 $72,673 $46,208 $28,951 single male $80,676 $46,615 $31,027 $16,487 Source: EBRI Retirement Security Projection Model, Version Employee Benefit Research Institute 2019

10 RETIREMENT DEFICITS GREATER THAN $100,000 (PER INDIVIDUAL) BY WAGE Percentage of Gen Xer households with RSS > $100,000 per individual by age-specific preretirement income quartile, marital status and gender (includes bifurcation for sequence of death 60% 50% 40% 30% 20% 10% 0% lowest second third highest married, female dies first 29% 17% 8% 3% married, male dies first 42% 24% 11% 4% single female 48% 32% 21% 13% single male 33% 21% 14% 7% Source: EBRI Retirement Security Projection Model, Version Employee Benefit Research Institute 2019

11 RETIREMENT DEFICITS BY FUTURE YEARS OF DEFINED CONTRIBUTION ELIGIBILITY Means of Retirement Savings Shortfalls for Gen Xers by future years of defined contribution eligibility, marital status and gender (includes bifurcation for sequence of death for married) $100,000 $90,000 $80,000 $70,000 $60,000 $50,000 $40,000 $30,000 $20,000 $10,000 $- zero 1-10 years years years married, female dies first $25,287 $15,324 $11,219 $6,720 married, male dies first $31,815 $18,937 $13,131 $7,100 single female $97,325 $68,891 $48,990 $24,486 single male $58,309 $38,086 $21,632 $12,251 Source: EBRI Retirement Security Projection Model, Version Employee Benefit Research Institute 2019

12 RETIREMENT DEFICITS GREATER THAN $100,000 (PER INDIVIDUAL) BY DC ELIGIBILITY Percentage of Gen Xer households with RSS > $100,000 per individual by future years of defined contribution eligibility, marital status and gender (includes bifurcation for sequence of death for married) 45% 40% 35% 30% 25% 20% 15% 10% 5% 0% zero 1-10 years years years married, female dies first 9% 4% 4% 1% married, male dies first 13% 8% 4% 3% single female 42% 30% 22% 11% single male 25% 17% 10% 5% Source: EBRI Retirement Security Projection Model, Version Employee Benefit Research Institute 2019

13 NEXT STEPS? How would various public policy and plan design changes impact these retirement deficits? We have previously analyzed the impact of the Automatic Retirement Plan Act of 2017 (ARPA) proposal on retirement deficits (VanDerhei, May 2018) Also analyzed the additional decrease in retirement deficits If auto portability were adopted (VanDerhei, July 2018) If auto portability were added to ARPA (VanDerhei, September 2018) Currently working on ARPA II Next slide shows the impact of auto portability (in isolation) on retirement deficits for the same four groups COPYRIGHT

14 IMPACT OF AUTO PORTABILITY BY DC ELIGIBILITY 45% Reduction in Retirement Savings Shortfalls from the introduction of Auto Portability for Gen Xers by future years of defined contribution eligibility, marital status and gender (includes bifurcation for sequence of death for married) 40% 37% 38% 35% 30% 29% 29% 31% 25% 20% 15% 22% 13% 20% 15% 22% 22% 21% 10% 5% 0% 1-10 years years years married, female dies first married, male dies first single female single male Source: EBRI Retirement Security Projection Model, Version Employee Benefit Research Institute 2019

15 REFERENCES VanDerhei, Jack (September 2018), How Much Would Auto-Portability Help Retirement Reform Proposals to Reduce Retirement Deficits? EBRI Fast Facts VanDerhei, Jack (May 2018), EBRI Retirement Security Projection Model (RSPM) Analyzing Policy and Design Proposals. EBRI Issue Brief VanDerhei, Jack (July 2018), How Much Might Defined Contribution Savings Benefit From Auto Portability? EBRI Fast Facts VanDerhei, Jack (February 2015), Retirement Savings Shortfalls: Evidence from EBRI's Retirement Security Projection Model, EBRI Issue Brief VanDerhei, Jack (June 2014), "Short" Falls: Who's Most Likely to Come up Short in Retirement, and When?, EBRI Notes VanDerhei, Jack (February 2014), What Causes EBRI Retirement Readiness Ratings to Vary: Results from the 2014 Retirement Security Projection Model EBRI Issue Brief VanDerhei, Jack (June 2013a), "What a Sustained Low-yield Rate Environment Means for Retirement Income Adequacy: Results From the 2013 EBRI Retirement Security Projection Model, " EBRI Notes VanDerhei, Jack (November 2012). All or Nothing? An Expanded Perspective on Retirement Readiness, EBRI Notes VanDerhei, Jack (June 2012). Retirement Readiness Ratings and Retirement Savings Shortfalls for Gen Xers: The Impact of Eligibility for Participation in a 401(k) Plan, EBRI Notes VanDerhei, Jack (May 2012). Retirement Income Adequacy for Boomers and Gen Xers: Evidence from the 2012 EBRI Retirement Security Projection Model, EBRI Notes VanDerhei, Jack, April 2011, Retirement Income Adequacy: Alternative Thresholds and the Importance of Future Eligibility in Defined Contribution Retirement Plans, April 2011, Vol. 32, No. 4 VanDerhei, Jack, A Post-Crisis Assessment of Retirement Income Adequacy for Baby Boomers and Gen Xers, February 2011, EBRI Issue Brief #354 VanDerhei, Jack, Retirement Savings Shortfalls for Today's Workers, October 2010, Vol. 31, No. 10, EBRI Notes VanDerhei, Jack, "Retirement Income Adequacy for Today's Workers: How Certain, How Much Will It Cost, and How Does Eligibility for Participation in a Defined Contribution Plan Help?" EBRI Notes September 2010, Vol. 31, No.9 VanDerhei, J., Copeland, C. (July 2010). The EBRI Retirement Readiness Rating: Retirement Income Preparation and Future Prospects. EBRI Issue Brief. 15

16 APPENDIX COPYRIGHT

17 DECILE ANALYSIS (NO BREAKOUTS) Decile analysis of Retirement Savings Shortfalls for Gen Xers by marital status and gender (includes bifurcation for sequence of death for married) $250,000 $200,000 $150,000 $100,000 $50,000 $- median 60th percentile 70th percentile 80th percentile 90th percentile married, female dies first $- $- $- $25,160 $80,337 married, male dies first $- $- $- $44,878 $95,650 single female $19,900 $57,936 $114,486 $158,130 $222,592 single male $- $- $- $67,871 $156,466 Source: EBRI Retirement Security Projection Model, Version Employee Benefit Research Institute 2019

18 DECILE ANALYSIS (BY PRE-RETIREMENT INCOME) Decile analysis of Retirement Savings Shortfalls for Gen Xers by marital status and gender (includes bifurcation for sequence of death for married): lowest age-specific pre-retirement income quartile $300,000 $250,000 $200,000 $150,000 $100,000 $50,000 $- 10th 20th 30th 40th 60th 70th 80th 90th median percentile percentile percentile percentile percentile percentile percentile percentile married, female dies first $- $- $11,142 $28,780 $54,164 $78,907 $92,858 $127,832 $169,405 married, male dies first $- $14,389 $43,296 $61,423 $83,992 $103,205 $131,347 $147,954 $181,083 single female $- $10,087 $30,070 $50,860 $91,466 $130,089 $156,344 $199,579 $253,982 single male $- $- $- $1,578 $12,426 $60,348 $112,316 $170,106 $236,323 Source: EBRI Retirement Security Projection Model, Version Employee Benefit Research Institute 2019

19 DECILE ANALYSIS (BY PRE-RETIREMENT INCOME) Decile analysis of Retirement Savings Shortfalls for Gen Xers by marital status and gender (includes bifurcation for sequence of death for married): second age-specific pre-retirement income quartile $250,000 $200,000 $150,000 $100,000 $50,000 $- 10th 20th 30th 40th 60th 70th 80th 90th median percentile percentile percentile percentile percentile percentile percentile percentile married, female dies first $- $- $- $- $25,456 $53,272 $80,337 $97,781 $137,764 married, male dies first $- $- $- $5,542 $41,372 $61,541 $87,486 $111,788 $151,373 single female $- $- $- $- $7,381 $55,459 $108,229 $160,395 $219,903 single male $- $- $- $- $- $- $22,175 $103,796 $173,302 Source: EBRI Retirement Security Projection Model, Version Employee Benefit Research Institute 2019

20 DECILE ANALYSIS (BY PRE-RETIREMENT INCOME) Decile analysis of Retirement Savings Shortfalls for Gen Xers by marital status and gender (includes bifurcation for sequence of death for married): third age-specific pre-retirement income quartile $200,000 $180,000 $160,000 $140,000 $120,000 $100,000 $80,000 $60,000 $40,000 $20,000 $- 10th 20th 30th 40th 60th 70th 80th 90th median percentile percentile percentile percentile percentile percentile percentile percentile married, female dies first $- $- $- $- $- $- $37,953 $62,995 $95,134 married, male dies first $- $- $- $- $- $728 $38,515 $65,576 $112,461 single female $- $- $- $- $- $- $31,022 $104,606 $176,038 single male $- $- $- $- $- $- $- $21,272 $136,400 Source: EBRI Retirement Security Projection Model, Version Employee Benefit Research Institute 2019

21 DECILE ANALYSIS (BY PRE-RETIREMENT INCOME) Decile analysis of Retirement Savings Shortfalls for Gen Xers by marital status and gender (includes bifurcation for sequence of death for married): highest age-specific pre-retirement income quartile $160,000 $140,000 $120,000 $100,000 $80,000 $60,000 $40,000 $20,000 $- 10th 20th 30th 40th 60th 70th 80th 90th median percentile percentile percentile percentile percentile percentile percentile percentile married, female dies first $- $- $- $- $- $- $- $- $18,343 married, male dies first $- $- $- $- $- $- $- $- $45,845 single female $- $- $- $- $- $- $- $30,974 $134,037 single male $- $- $- $- $- $- $- $- $62,611 Source: EBRI Retirement Security Projection Model, Version Employee Benefit Research Institute 2019

22 DECILE ANALYSIS (BY DC ELIGIBILITY) Decile analysis of Retirement Savings Shortfalls for Gen Xers by marital status and gender (includes bifurcation for sequence of death for married): zero future years of defined contribution plan eligibility $300,000 $250,000 $200,000 $150,000 $100,000 $50,000 $- 10th 20th 30th 40th 60th 70th 80th 90th median percentile percentile percentile percentile percentile percentile percentile percentile married, female dies first $- $- $- $- $- $- $5,897 $53,174 $96,884 married, male dies first $- $- $- $- $- $- $32,902 $68,302 $116,274 single female $- $- $11,282 $35,367 $64,112 $114,519 $146,305 $185,560 $245,034 single male $- $- $- $- $- $4,785 $62,611 $126,193 $193,753 Source: EBRI Retirement Security Projection Model, Version Employee Benefit Research Institute 2019

23 DECILE ANALYSIS (BY DC ELIGIBILITY) Decile analysis of Retirement Savings Shortfalls for Gen Xers by marital status and gender (includes bifurcation for sequence of death for married): 1-10 future years of defined contribution plan eligibility $250,000 $200,000 $150,000 $100,000 $50,000 $- 10th 20th 30th 40th 60th 70th 80th 90th median percentile percentile percentile percentile percentile percentile percentile percentile married, female dies first $- $- $- $- $- $- $- $2,012 $67,322 married, male dies first $- $- $- $- $- $- $- $28,088 $86,188 single female $- $- $- $- $4,181 $47,671 $102,589 $151,872 $216,416 single male $- $- $- $- $- $- $- $77,687 $156,821 Source: EBRI Retirement Security Projection Model, Version Employee Benefit Research Institute 2019

24 DECILE ANALYSIS (BY DC ELIGIBILITY) Decile analysis of Retirement Savings Shortfalls for Gen Xers by marital status and gender (includes bifurcation for sequence of death for married): future years of defined contribution plan eligibility $200,000 $180,000 $160,000 $140,000 $120,000 $100,000 $80,000 $60,000 $40,000 $20,000 $- 10th 20th 30th 40th 60th 70th 80th 90th median percentile percentile percentile percentile percentile percentile percentile percentile married, female dies first $- $- $- $- $- $- $- $- $37,424 married, male dies first $- $- $- $- $- $- $- $- $55,320 single female $- $- $- $- $- $- $41,625 $114,685 $183,211 single male $- $- $- $- $- $- $- $- $98,276 Source: EBRI Retirement Security Projection Model, Version Employee Benefit Research Institute 2019

25 DECILE ANALYSIS (BY DC ELIGIBILITY) Decile analysis of Retirement Savings Shortfalls for Gen Xers by marital status and gender (includes bifurcation for sequence of death for married): future years of defined contribution plan eligibility $140,000 $120,000 $100,000 $80,000 $60,000 $40,000 $20,000 $- 10th 20th 30th 40th 60th 70th 80th 90th median percentile percentile percentile percentile percentile percentile percentile percentile married, female dies first $- $- $- $- $- $- $- $- $1,308 married, male dies first $- $- $- $- $- $- $- $- $15,912 single female $- $- $- $- $- $- $- $8,624 $126,496 single male $- $- $- $- $- $- $- $- $2,000 Source: EBRI Retirement Security Projection Model, Version Employee Benefit Research Institute 2019

26 Click to edit Master title style Women Take the Wheel Anna Rappaport February 6, 2019

27 Agenda SOA Research on Post-Retirement Risk The Reality for Women SOA Research on Individuals Age 85+ Long-Term Care Practical Ideas Note: More information in Appendix 27

28 SOA Research Overview

29 Committee on Post-Retirement Needs and Risks Society of Actuaries post-retirement risk research: nearly 20 years of work Overall program goal: Understand and improve post-retirement risk management Focus on middle-income market age 50 and older Housing value is largest asset for many (excluding value of Social Security) Many lack adequate assets to maintain living standard Decisions will require trade-offs on living standards Focus on multiple stakeholders Started biennial Risk Survey in 2001 and added focus groups in 2005, 2013 and 2015 Survey, focus groups and interviews with those over 85 added in 2017 and 2018 Generational survey added in 2018 Consumer information of several types Research on women summarized in Understanding and Managing Post-Retirement Risks: Women and Post-Retirement Risk

30 Listening to Retirees: Findings from Focus Groups and Interviews Women are generally more concerned about risks than men Planning horizons are too short Dealing with shocks may be difficult Retirees are resilient Older people need help Women are more likely to be caregivers

31 The Reality for Women: Women and Retirement Risks

32 Differences by Gender Longevity Older women are more likely to be alone Career differences Family responsibility Higher long-term care costs More focus on others Less likely to remarry

33 Retirement Concerns by Gender

34 Where to Live in Retirement

35 Risks with Direct Greater Impact on Women Loss of spouse Decline in functional status Lower lifetime earnings and wealth

36 Longevity Risk

37 Risks with Greater Impact due to Longevity Outliving assets Health care risks Inflation

38 Inflation Over Time Impact of Inflation Value % 3% Year

39 SOA Research on Individuals Age 85 and Over

40 Highlights Marital demographics Financial security Spending and debt Importance of family Living arrangements Advice

41 Marital Status

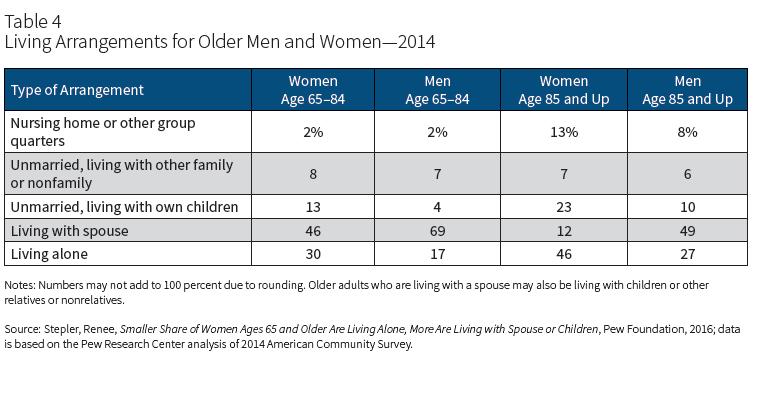

42 Living Arrangements

43 Long-Term Care

44 Key Observations Women are more likely than men to need long-term care Very few people plan for it or think they will need it Family can be important source of help Husbands are more likely than wives to expect to have family caregivers Women generally live longer and are more likely to need caregivers

45 Life Expectancy by Health Status

46 Long-Term Care Premiums Average annual premium for a 55-year-old couple - $3,050. Average annual premium for age 55 single male - $2,050. Average annual premium for age 55 single female - $2,700. Single female premium is 31.7% higher than single male premium Married couples benefit from significant spousal discount Source:

47 Practical Ideas

48 First Things First Get legal matters and papers in order Figure out how much retirement will cost Review the retirement plan Review divorce and family issues Assess long-term care needs Examine social security options

49 Social Security

50 Traps to Avoid Having too much debt Giving too much money to children Quitting job for caregiving Spending too much on housing Not understanding family finances Not having an emergency fund

51 Personal Tips Be knowledgeable about household finances, including passwords Check beneficiary designations on employer plans and life insurance Evaluate long-term care and Social Security claiming options Make sure credit cards and bank accounts are set up with access for both members of couple Check credit card rating agencies Update wills, advance directives and powers of attorney Put together list of financial information and contacts

52 Essential Papers

53 Questions?

54 Appendix: More on SOA Research

55 Risk Surveys Risks and Process of Retirement Survey. Each biennial survey includes topics of special focus Risks and Process of Retirement Survey: Key Findings and Issues, Impact of Retirement Risks on Women, Society of Actuaries, Risks and Process of Retirement Survey: Key Findings and Issues, Shocks and Unexpected Spending in Retirement, Society of Actuaries, 2016 Survey of Individuals Over Age 85, Society of Actuaries,

56 Focus Groups and In-Depth Interviews Post-Retirement Experiences of Individuals 85+ Years Old (2017) Post-Retirement Experiences of Individuals Retired for 15 Years or More (2015) The Decision to Retire and Post-Retirement Financial Strategies: A Report on Eight Focus Groups (2013) Spending and Investing in Retirement: Is There a Strategy, Society of Actuaries, LIMRA, and INFRE (2006) 56

57 Consumer Information Managing Post-Retirement Risks (a guide to the risks) Managing Retirement Decisions Briefs - Women Take the Wheel:,

58 Essays and Papers Diverse Risk Essay Collection - Women and Retirement Risk: What Should Plan Sponsors, Planners, Software Developers and Product Developers Know? Managing the Impact of Long-Term Care Needs and Expense on Retirement Security monograph - Improving Retirement by Integrating Family, Friends, Housing and Support: Lessons Learned from Personal Experience and The 65-Plus Age Wave and the Caregiving Conundrum: The Often Forgotten Piece of the Long-Term Care Puzzle 58

59 Infographics and Tools Age Wise series of 5 infographics life expectancy, unexpected expenses, inflation, housing and longterm care Actuaries Longevity Illustrator

60 Example of data from the Longevity Illustrator: Probability of Living to a Certain Age: 35 year old female

61 Probability of Living for a Specified Number of Years - Couple age 65

62

63 Q&A 63

64 ENGAGE WITH EBRI Here are some ways: Check out our new website Attend our free Policy Forum on May 9 th in Washington, D.C. After our December event, 100% of our surveyed attendees would recommend it to a friend and everyone found the networking opportunities valuable. Participate in the April 30 th American Savings Education Council Partners Meeting on the Retirement Confidence Survey Support our Research Centers Sponsor our events and webinars Sign up for EBRI Insights Join EBRI as a Member

65 NEXT WEBINAR MARCH 1 CADILLAC TAX COPYRIGHT

How Retirement Readiness Varies by Gender and Family Status: A Retirement Savings Shortfall Assessment of Gen Xers

January 17, 2019 No. 471 How Retirement Readiness Varies by Gender and Family Status: A Retirement Savings Shortfall Assessment of Gen Xers By Jack VanDerhei, Ph.D., Employee Benefit Research Institute

January 17, 2019 No. 471 How Retirement Readiness Varies by Gender and Family Status: A Retirement Savings Shortfall Assessment of Gen Xers By Jack VanDerhei, Ph.D., Employee Benefit Research Institute

Retirement Plans and Prospects for Retirement Income Adequacy

Retirement Plans and Prospects for Retirement Income Adequacy 2014 Pension Research Council Symposium: Reimagining Pensions: The Next 40 Years May 1, 2014 Jack VanDerhei Employee Benefit Research Institute

Retirement Plans and Prospects for Retirement Income Adequacy 2014 Pension Research Council Symposium: Reimagining Pensions: The Next 40 Years May 1, 2014 Jack VanDerhei Employee Benefit Research Institute

Women and Post-Retirement Risks

Understanding and Managing Post-Retirement Risks A series of reports presenting highlights from the Society of Actuaries extensive body of research on post-retirement risks and issues. Women and Post-Retirement

Understanding and Managing Post-Retirement Risks A series of reports presenting highlights from the Society of Actuaries extensive body of research on post-retirement risks and issues. Women and Post-Retirement

How long will Baby Boomers and Gen Xers need to work for a 50, 70, and 80 percent probability of adequate retirement income?

How long will Baby Boomers and Gen Xers need to work for a 50, 70, and 80 percent probability of adequate retirement income? Jack VanDerhei and Craig Copeland, EBRI Is There a Future for Retirement? EBRI-ERF

How long will Baby Boomers and Gen Xers need to work for a 50, 70, and 80 percent probability of adequate retirement income? Jack VanDerhei and Craig Copeland, EBRI Is There a Future for Retirement? EBRI-ERF

EBRI Retirement Security Projection Model (RSPM) Analyzing Policy and Design Proposals

Analyzing Policy and Design Proposals") May 31, 2018 No. 451 EBRI Retirement Security Projection Model (RSPM) Analyzing Policy and Design Proposals By Jack VanDerhei, Ph.D., Employee Benefit Research Institute A T A G L A N C E At various times,

May 31, 2018 No. 451 EBRI Retirement Security Projection Model (RSPM) Analyzing Policy and Design Proposals By Jack VanDerhei, Ph.D., Employee Benefit Research Institute A T A G L A N C E At various times,

A Post Crisis Assessment of Retirement Income Adequacy for Baby Boomers and Gen Xers

February 2011 No. 354 A Post Crisis Assessment of Retirement Income Adequacy for Baby Boomers and Gen Xers By Jack VanDerhei, Employee Benefit Research Institute E X E C U T I V E S U M M A R Y DETERMINING

February 2011 No. 354 A Post Crisis Assessment of Retirement Income Adequacy for Baby Boomers and Gen Xers By Jack VanDerhei, Employee Benefit Research Institute E X E C U T I V E S U M M A R Y DETERMINING

Retirement Savings 2.0: Updating Savings Policy for the Modern Economy

T-181 United States Senate Committee on Finance Hearing on: Retirement Savings 2.0: Updating Savings Policy for the Modern Economy Tuesday, September 16, 2014, 10:00 AM 215 Dirksen Senate Office Building

T-181 United States Senate Committee on Finance Hearing on: Retirement Savings 2.0: Updating Savings Policy for the Modern Economy Tuesday, September 16, 2014, 10:00 AM 215 Dirksen Senate Office Building

ERISA Advisory Council U.S. Department of Labor

T-180 ERISA Advisory Council U.S. Department of Labor Hearing on: LIFETIME PARTICIPATION IN PLANS June 17, 2014 C5320 Room 6 at the U.S. Department of Labor Statement for the Record by Jack VanDerhei,

T-180 ERISA Advisory Council U.S. Department of Labor Hearing on: LIFETIME PARTICIPATION IN PLANS June 17, 2014 C5320 Room 6 at the U.S. Department of Labor Statement for the Record by Jack VanDerhei,

EBRI Retirement Security Projection Model. ICI Retirement Summit: A Close Look at Retirement Preparedness in America

EBRI Retirement Security Projection Model ICI Retirement Summit: A Close Look at Retirement Preparedness in America Jack VanDerhei Research Director, EBRI April 4, 2014 Background of RSPM RSPM grew out

EBRI Retirement Security Projection Model ICI Retirement Summit: A Close Look at Retirement Preparedness in America Jack VanDerhei Research Director, EBRI April 4, 2014 Background of RSPM RSPM grew out

United States Senate Committee on Banking, Housing & Urban Affairs SUBCOMMITTEE ON ECONOMIC POLICY

T-177 United States Senate Committee on Banking, Housing & Urban Affairs SUBCOMMITTEE ON ECONOMIC POLICY Hearing on: THE STATE OF U.S. RETIREMENT SECURITY: CAN THE MIDDLE CLASS AFFORD TO RETIRE? Wednesday,

T-177 United States Senate Committee on Banking, Housing & Urban Affairs SUBCOMMITTEE ON ECONOMIC POLICY Hearing on: THE STATE OF U.S. RETIREMENT SECURITY: CAN THE MIDDLE CLASS AFFORD TO RETIRE? Wednesday,

United States Senate Committee on Finance Subcommittee on Social Security, Pensions, and Family Policy

T-176 United States Senate Committee on Finance Subcommittee on Social Security, Pensions, and Family Policy Hearing on: Retirement Savings for Low-Income Workers Wednesday, February 26, 2014, 10:00 AM

T-176 United States Senate Committee on Finance Subcommittee on Social Security, Pensions, and Family Policy Hearing on: Retirement Savings for Low-Income Workers Wednesday, February 26, 2014, 10:00 AM

How People Plan for Retirement

Understanding and Managing Post-Retirement Risks A series of reports presenting highlights from the Society of Actuaries extensive body of research on post-retirement risks and issues. How People Plan

Understanding and Managing Post-Retirement Risks A series of reports presenting highlights from the Society of Actuaries extensive body of research on post-retirement risks and issues. How People Plan

A T A G L A N C E. Short Falls: Who s Most Likely to Come up Short in Retirement, and When? by Jack VanDerhei, Ph.D., EBRI

June 2014 Vol. 35, No. 6 Short Falls: Who s Most Likely to Come up Short in Retirement, and When? p. 2 Consumer Engagement Among HSA and HRA Enrollees: Findings from the 2013 EBRI/Greenwald & Associates

June 2014 Vol. 35, No. 6 Short Falls: Who s Most Likely to Come up Short in Retirement, and When? p. 2 Consumer Engagement Among HSA and HRA Enrollees: Findings from the 2013 EBRI/Greenwald & Associates

Post-Retirement Risks and

Understanding and Managing Post-Retirement Risks A series of reports presenting highlights from the Society of Actuaries extensive body of research on post-retirement risks and issues. Post-Retirement

Understanding and Managing Post-Retirement Risks A series of reports presenting highlights from the Society of Actuaries extensive body of research on post-retirement risks and issues. Post-Retirement

The EBRI Retirement Readiness Rating: Retirement Income Preparation and Future Prospects

July 2010 No. 344 The EBRI Retirement Readiness Rating: Retirement Income Preparation and Future Prospects By Jack VanDerhei and Craig Copeland, Employee Benefit Research Institute E X E C U T I V E S

July 2010 No. 344 The EBRI Retirement Readiness Rating: Retirement Income Preparation and Future Prospects By Jack VanDerhei and Craig Copeland, Employee Benefit Research Institute E X E C U T I V E S

Statement for the Record

T-175 United States Senate Committee on Finance Subcommittee on Social Security, Pensions, and Family Policy Hearing on: The Role of Social Security, Defined Benefits, and Private Retirement Accounts in

T-175 United States Senate Committee on Finance Subcommittee on Social Security, Pensions, and Family Policy Hearing on: The Role of Social Security, Defined Benefits, and Private Retirement Accounts in

Retirement Plans and Prospects for Retirement Income Adequacy

Retirement Plans and Prospects for Retirement Income Adequacy Jack VanDerhei September 2014 PRC WP2014-06 Pension Research Council The Wharton School, University of Pennsylvania 3620 Locust Walk, 3000

Retirement Plans and Prospects for Retirement Income Adequacy Jack VanDerhei September 2014 PRC WP2014-06 Pension Research Council The Wharton School, University of Pennsylvania 3620 Locust Walk, 3000

The Impact of Repealing PPACA on Savings Needed for Health Expenses for Persons Eligible for Medicare, p. 2

August 2011 Vol. 32, No. 8 The Impact of Repealing PPACA on Savings Needed for Health Expenses for Persons Eligible for Medicare, p. 2 The Importance of Defined Benefit Plans for Retirement Income Adequacy,

August 2011 Vol. 32, No. 8 The Impact of Repealing PPACA on Savings Needed for Health Expenses for Persons Eligible for Medicare, p. 2 The Importance of Defined Benefit Plans for Retirement Income Adequacy,

Deferred Income Annuity Purchases: Optimal Levels for Retirement Income Adequacy

January 3, 2019 No. 469 Deferred Income Annuity Purchases: Optimal Levels for Retirement Income Adequacy By Jack VanDerhei, Ph.D., Employee Benefit Research Institute A T A G L A N C E The prospect of

January 3, 2019 No. 469 Deferred Income Annuity Purchases: Optimal Levels for Retirement Income Adequacy By Jack VanDerhei, Ph.D., Employee Benefit Research Institute A T A G L A N C E The prospect of

Misperceptions and Management of Retirement Risks

Misperceptions and Management of Retirement Risks FPA of Greater Indiana and CFA Society Indianapolis Joint Meeting September 20, 2013 Presenter: Carol Bogosian, ASA President of CAB Consulting 1 1 Learning

Misperceptions and Management of Retirement Risks FPA of Greater Indiana and CFA Society Indianapolis Joint Meeting September 20, 2013 Presenter: Carol Bogosian, ASA President of CAB Consulting 1 1 Learning

w w w. I C A o r g

w w w. I C A 2 0 1 4. o r g SOA Post-Retirement Risk Research what it tells about the state and direction of retirement security in the US Presenter: Anna M. Rappaport Anna Rappaport Consulting Agenda

w w w. I C A 2 0 1 4. o r g SOA Post-Retirement Risk Research what it tells about the state and direction of retirement security in the US Presenter: Anna M. Rappaport Anna Rappaport Consulting Agenda

Perspectives on SOA Post-Retirement Risk Research and what it tells about the implications of long life

Perspectives on SOA Post-Retirement Risk Research and what it tells about the implications of long life By Anna M. Rappaport, FSA, MAAA Note: This is a paper which has been submitted to the Society of

Perspectives on SOA Post-Retirement Risk Research and what it tells about the implications of long life By Anna M. Rappaport, FSA, MAAA Note: This is a paper which has been submitted to the Society of

Shocks and the Unexpected: An Important Factor in Retirement

Understanding and Managing Post-Retirement Risks A series of reports presenting highlights from the Society of Actuaries extensive body of research on post-retirement risks and issues. Shocks and the Unexpected:

Understanding and Managing Post-Retirement Risks A series of reports presenting highlights from the Society of Actuaries extensive body of research on post-retirement risks and issues. Shocks and the Unexpected:

OUP CORRECTED PROOF FINAL,

OUP CORRECTED PROOF FINAL, 11/12/2015, SPi Reimagining Pensions The Next 40 Years EDITED BY Olivia S. Mitchell and Richard C. Shea 1 OUP CORRECTED PROOF FINAL, 11/12/2015, SPi 3 Great Clarendon Street,

OUP CORRECTED PROOF FINAL, 11/12/2015, SPi Reimagining Pensions The Next 40 Years EDITED BY Olivia S. Mitchell and Richard C. Shea 1 OUP CORRECTED PROOF FINAL, 11/12/2015, SPi 3 Great Clarendon Street,

A T A G L A N C E. In the case of females, only 5 of the 16 combinations have break-even rates under 1.5 percent.

February 7, 2019 No. 473 How Much Would It Take? Achieving Retirement Income Equivalency Between Final-Average-Pay Defined Benefit Plan Accruals and Automatic Enrollment 401(k) Plans in the Private Sector

February 7, 2019 No. 473 How Much Would It Take? Achieving Retirement Income Equivalency Between Final-Average-Pay Defined Benefit Plan Accruals and Automatic Enrollment 401(k) Plans in the Private Sector

By Jack VanDerhei, Ph.D., Employee Benefit Research Institute

June 2013 No. 387 Reality Checks: A Comparative Analysis of Future Benefits from Private-Sector, Voluntary-Enrollment 401(k) Plans vs. Stylized, Final-Average-Pay Defined Benefit and Cash Balance Plans

June 2013 No. 387 Reality Checks: A Comparative Analysis of Future Benefits from Private-Sector, Voluntary-Enrollment 401(k) Plans vs. Stylized, Final-Average-Pay Defined Benefit and Cash Balance Plans

Testimony of M. Cindy Hounsell, President Women s Institute for a Secure Retirement

Senate Committee on Health, Education, Labor and Pensions Hearing on Pension Savings: Are Workers Saving Enough for Retirement? 430 Dirksen Senate Office Building Testimony of M. Cindy Hounsell, President

Senate Committee on Health, Education, Labor and Pensions Hearing on Pension Savings: Are Workers Saving Enough for Retirement? 430 Dirksen Senate Office Building Testimony of M. Cindy Hounsell, President

A NATIONAL FRAMEWORK FOR CLOSING THE RETIREMENT SAVINGS COVERAGE GAP RONALD P. O HANLEY PRESIDENT & CEO STATE STREET GLOBAL ADVISORS

A NATIONAL FRAMEWORK FOR CLOSING THE RETIREMENT SAVINGS COVERAGE GAP RONALD P. O HANLEY PRESIDENT & CEO STATE STREET GLOBAL ADVISORS Source: Pensions & Investments, February 17, 2015 2 Gen Xers Retirement

A NATIONAL FRAMEWORK FOR CLOSING THE RETIREMENT SAVINGS COVERAGE GAP RONALD P. O HANLEY PRESIDENT & CEO STATE STREET GLOBAL ADVISORS Source: Pensions & Investments, February 17, 2015 2 Gen Xers Retirement

Senate Committee on Health, Education, Labor and Pensions. The Power of Pensions: Building a Strong. Middle Class and Strong Economy

T-169 Senate Committee on Health, Education, Labor and Pensions Hearing on: The Power of Pensions: Building a Strong Middle Class and Strong Economy Tuesday, July 12, 2011 SD-430 Dirksen Senate Office

T-169 Senate Committee on Health, Education, Labor and Pensions Hearing on: The Power of Pensions: Building a Strong Middle Class and Strong Economy Tuesday, July 12, 2011 SD-430 Dirksen Senate Office

Senate Committee on Banking, Housing & Urban Affairs

T-171 Senate Committee on Banking, Housing & Urban Affairs SUBCOMMITTEE ON ECONOMIC POLICY Hearing on: Retirement (In)security: Examining the Retirement Savings Deficit March 28, 2010 538 Dirksen Senate

T-171 Senate Committee on Banking, Housing & Urban Affairs SUBCOMMITTEE ON ECONOMIC POLICY Hearing on: Retirement (In)security: Examining the Retirement Savings Deficit March 28, 2010 538 Dirksen Senate

A T A G L A N C E. June 2013 Vol. 34, No. 6

June 2013 Vol. 34, No. 6 What a Sustained Low-yield Rate Environment Means for Retirement Income Adequacy: Results From the 2013 EBRI Retirement Security Projection Model, p. 2 Use of Health Care Services

June 2013 Vol. 34, No. 6 What a Sustained Low-yield Rate Environment Means for Retirement Income Adequacy: Results From the 2013 EBRI Retirement Security Projection Model, p. 2 Use of Health Care Services

The Impact of Auto- enrollment and Automatic Contribution Escalation on Retirement Income Adequacy

The Impact of Auto- enrollment and Automatic Contribution Escalation on Retirement Income Adequacy By Jack VanDerhei, Employee Benefit Research Institute, and Lori Lucas, Callan Associates New Simulation

The Impact of Auto- enrollment and Automatic Contribution Escalation on Retirement Income Adequacy By Jack VanDerhei, Employee Benefit Research Institute, and Lori Lucas, Callan Associates New Simulation

Background. Risk Survey and Public Attitude Research Series. Context. Background Post-Retirement Needs and Risk Committee 11/3/2015

Agenda Post-Retirement Needs and Risks: What Do We Really Know? PRESENTER Anna M. Rappaport, FSA, MAAA Chicago Actuarial Club October 2015 Background Risk Survey and Public Attitude Research Managing Risks

Agenda Post-Retirement Needs and Risks: What Do We Really Know? PRESENTER Anna M. Rappaport, FSA, MAAA Chicago Actuarial Club October 2015 Background Risk Survey and Public Attitude Research Managing Risks

Actuaries Respond to an Aging Society

ANNA RAPPAPORT CONSULTING STRATEGIES FOR A SECURE RETIREMENT SM Actuaries Respond to an Aging Society Chicago Actuarial Association Meeting November 14, 2007 Today s Presentation Helps us think about the

ANNA RAPPAPORT CONSULTING STRATEGIES FOR A SECURE RETIREMENT SM Actuaries Respond to an Aging Society Chicago Actuarial Association Meeting November 14, 2007 Today s Presentation Helps us think about the

IMPACT OF RETIREMENT RISKS ON WOMEN. Report: Society of Actuaries & WISER Presented by: Linda Stone, WISER Senior Fellow

IMPACT OF RETIREMENT RISKS ON WOMEN Report: Society of Actuaries & WISER Presented by: Linda Stone, WISER Senior Fellow SOA RESEARCH 2013 Survey on Process of Retirement and Retirement Risks Covers retirees

IMPACT OF RETIREMENT RISKS ON WOMEN Report: Society of Actuaries & WISER Presented by: Linda Stone, WISER Senior Fellow SOA RESEARCH 2013 Survey on Process of Retirement and Retirement Risks Covers retirees

Ready or Not... The Impact of Retirement-Plan Design

Ready or Not... The Impact of Retirement-Plan Design Some 10,000 baby boomers a day are heading into retirement. Will they have enough income to finance retirements that, for some, may last as long as

Ready or Not... The Impact of Retirement-Plan Design Some 10,000 baby boomers a day are heading into retirement. Will they have enough income to finance retirements that, for some, may last as long as

SOA 2009 Risks and Process of Retirement Survey

SOA 2009 Risks and Process of Retirement Survey The Impact of Retirement Risks on Women WISER Symposium December 2, 2010 Cindy Levering, SOA Committee on Post-Retirement Needs and Risks Agenda Introduction,

SOA 2009 Risks and Process of Retirement Survey The Impact of Retirement Risks on Women WISER Symposium December 2, 2010 Cindy Levering, SOA Committee on Post-Retirement Needs and Risks Agenda Introduction,

The Impact of Long-Term Care Costs on Retirement Wealth Needs

The Impact of Long-Term Care Costs on Retirement Wealth Needs (Selections from Society of Actuaries Monograph: Managing the Impact of Long-Term Care Needs and Expense on Retirement Secturiy: A Holistic

The Impact of Long-Term Care Costs on Retirement Wealth Needs (Selections from Society of Actuaries Monograph: Managing the Impact of Long-Term Care Needs and Expense on Retirement Secturiy: A Holistic

Self-Insured Health Plans: State Variation and Recent Trends by Firm Size, p. 2 All or Nothing? An Expanded Perspective on Retirement Readiness, p.

November 2012 Vol. 33, No. 11 Self-Insured Health Plans: State Variation and Recent Trends by Firm Size, p. 2 All or Nothing? An Expanded Perspective on Retirement Readiness, p. 11 A T A G L A N C E Self-Insured

November 2012 Vol. 33, No. 11 Self-Insured Health Plans: State Variation and Recent Trends by Firm Size, p. 2 All or Nothing? An Expanded Perspective on Retirement Readiness, p. 11 A T A G L A N C E Self-Insured

What is the status of Social Security? When should you draw benefits? How a Job Impacts Benefits... 8

TABLE OF CONTENTS Executive Summary... 2 What is the status of Social Security?... 3 When should you draw benefits?... 4 How do spousal benefits work? Plan for Surviving Spouse... 5 File and Suspend...

TABLE OF CONTENTS Executive Summary... 2 What is the status of Social Security?... 3 When should you draw benefits?... 4 How do spousal benefits work? Plan for Surviving Spouse... 5 File and Suspend...

Changes in Retirement Handling the Expected and Unexpected

Changes in Retirement Handling the Expected and Unexpected Presenters: Ruth Helman, Greenwald & Associates Anna M. Rappaport, FSA, MAAA July 1, 2015 Reference Documents Society of Actuaries 2014 Report:

Changes in Retirement Handling the Expected and Unexpected Presenters: Ruth Helman, Greenwald & Associates Anna M. Rappaport, FSA, MAAA July 1, 2015 Reference Documents Society of Actuaries 2014 Report:

Retirement Income Strategies: How Social Security Can Maximize Client s Lifestyle, Legacy, and Livelihood

Retirement Income Strategies: How Can Maximize Client s Lifestyle, Legacy, and Livelihood Karen Remmele 2013 This material is not intended to replace the advice of a qualified attorney, tax advisor, investment

Retirement Income Strategies: How Can Maximize Client s Lifestyle, Legacy, and Livelihood Karen Remmele 2013 This material is not intended to replace the advice of a qualified attorney, tax advisor, investment

How Economic Security Changes during Retirement

How Economic Security Changes during Retirement Barbara A. Butrica March 2007 The Retirement Project Discussion Paper 07-02 How Economic Security Changes during Retirement Barbara A. Butrica March 2007

How Economic Security Changes during Retirement Barbara A. Butrica March 2007 The Retirement Project Discussion Paper 07-02 How Economic Security Changes during Retirement Barbara A. Butrica March 2007

Social Security Reform: How Benefits Compare March 2, 2005 National Press Club

Social Security Reform: How Benefits Compare March 2, 2005 National Press Club Employee Benefit Research Institute Dallas Salisbury, CEO Craig Copeland, senior research associate Jack VanDerhei, Temple

Social Security Reform: How Benefits Compare March 2, 2005 National Press Club Employee Benefit Research Institute Dallas Salisbury, CEO Craig Copeland, senior research associate Jack VanDerhei, Temple

Social Security: Is a Key Foundation of Economic Security Working for Women?

Committee on Finance United States Senate Hearing on Social Security: Is a Key Foundation of Economic Security Working for Women? Statement of Janet Barr, MAAA, ASA, EA on behalf of the American Academy

Committee on Finance United States Senate Hearing on Social Security: Is a Key Foundation of Economic Security Working for Women? Statement of Janet Barr, MAAA, ASA, EA on behalf of the American Academy

Retirement Annuity and Employment-Based Pension Income, Among Individuals Aged 50 and Over: 2006

Retirement Annuity and Employment-Based Pension Income, Among Individuals d 50 and Over: 2006 by Ken McDonnell, EBRI Introduction This article looks at one slice of the income pie of the older population:

Retirement Annuity and Employment-Based Pension Income, Among Individuals d 50 and Over: 2006 by Ken McDonnell, EBRI Introduction This article looks at one slice of the income pie of the older population:

Use of Health Care Services and Access Issues by Type of Health Plan: Findings from the EBRI/MGA Consumer Engagement in Health Care Survey, p.

June 2012 Vol. 33, No. 6 Use of Health Care Services and Access Issues by Type of Health Plan: Findings from the EBRI/MGA Consumer Engagement in Health Care Survey, p. 2 Retirement Readiness Ratings and

June 2012 Vol. 33, No. 6 Use of Health Care Services and Access Issues by Type of Health Plan: Findings from the EBRI/MGA Consumer Engagement in Health Care Survey, p. 2 Retirement Readiness Ratings and

Your Future Paycheck:

Your Future Paycheck: What You Need to Know about Social Security, Pensions, Savings & Investments Presenters: Lara Hinz, MSW Director of Programs, WISER Linda K. Stone, FSA Society of Actuaries & WISER

Your Future Paycheck: What You Need to Know about Social Security, Pensions, Savings & Investments Presenters: Lara Hinz, MSW Director of Programs, WISER Linda K. Stone, FSA Society of Actuaries & WISER

For Your Name and Spouse Here. Presented by: Dolph Janis Clear Income Strategies Phone:

For and Here Presented by: Dolph Janis Phone: 74-99-49 Email: dolph@cisforlife.com Important Notes This analysis provides only broad, general guidelines, which may be helpful in shaping your thinking about

For and Here Presented by: Dolph Janis Phone: 74-99-49 Email: dolph@cisforlife.com Important Notes This analysis provides only broad, general guidelines, which may be helpful in shaping your thinking about

HOW TO POTENTIALLY OPTIMIZE SOCIAL SECURITY BENEFITS

HOW TO POTENTIALLY OPTIMIZE SOCIAL SECURITY BENEFITS TABLE OF CONTENTS Executive Summary... 2 The Status of Social Security... 2 Timing Your Benefit Distributions... 3 A Look at Spousal Benefits Plan for

HOW TO POTENTIALLY OPTIMIZE SOCIAL SECURITY BENEFITS TABLE OF CONTENTS Executive Summary... 2 The Status of Social Security... 2 Timing Your Benefit Distributions... 3 A Look at Spousal Benefits Plan for

SOA Research: Misperceptions and Management of Retirement Risks

SOA Research: Misperceptions and Management of Retirement Risks Actuaries Clubs of Boston and Hartford & Springfield Joint Meeting November 14, 2013 Presenter: Carol Bogosian, ASA President of CAB Consulting

SOA Research: Misperceptions and Management of Retirement Risks Actuaries Clubs of Boston and Hartford & Springfield Joint Meeting November 14, 2013 Presenter: Carol Bogosian, ASA President of CAB Consulting

HOW DOES WOMEN WORKING AFFECT SOCIAL SECURITY REPLACEMENT RATES?

June 2013, Number 13-10 RETIREMENT RESEARCH HOW DOES WOMEN WORKING AFFECT SOCIAL SECURITY REPLACEMENT RATES? By April Yanyuan Wu, Nadia S. Karamcheva, Alicia H. Munnell, and Patrick Purcell* Introduction

June 2013, Number 13-10 RETIREMENT RESEARCH HOW DOES WOMEN WORKING AFFECT SOCIAL SECURITY REPLACEMENT RATES? By April Yanyuan Wu, Nadia S. Karamcheva, Alicia H. Munnell, and Patrick Purcell* Introduction

Funding Savings Needed for Health Expenses For Persons Eligible for Medicare

December 2010 No. 351 Funding Savings Needed for Health Expenses For Persons Eligible for Medicare By Paul Fronstin, Dallas Salisbury, and Jack VanDerhei, Employee Benefit Research Institute E X E C U

December 2010 No. 351 Funding Savings Needed for Health Expenses For Persons Eligible for Medicare By Paul Fronstin, Dallas Salisbury, and Jack VanDerhei, Employee Benefit Research Institute E X E C U

Senate Committee on Finance

T-167 Senate Committee on Finance Hearing on: How Do Complexity, Uncertainty and Other Factors Impact Responses to Tax Incentives? Wednesday, March 30, 2011 10:00 a.m. 215 Dirksen Senate Office Building

T-167 Senate Committee on Finance Hearing on: How Do Complexity, Uncertainty and Other Factors Impact Responses to Tax Incentives? Wednesday, March 30, 2011 10:00 a.m. 215 Dirksen Senate Office Building

Women and Money. Taking Charge of Your Financial Future

Women and Money Taking Charge of Your Financial Future Presented By: James Lindner, CFP, CLU, ChFC President & CEO Retirement Strategies, Ltd. 614.799.8668 jlindner@retirement-strategies.com www.retirement-strategies.com

Women and Money Taking Charge of Your Financial Future Presented By: James Lindner, CFP, CLU, ChFC President & CEO Retirement Strategies, Ltd. 614.799.8668 jlindner@retirement-strategies.com www.retirement-strategies.com

Challenges to Successful Later Retirement

ANNA RAPPAPORT CONSULTING STRATEGIES FOR A SECURE RETIREMENT SM Challenges to Successful Later Retirement EBRI Policy Forum Anna Rappaport May 2011 Agenda Disability benefit issues Findings from research

ANNA RAPPAPORT CONSULTING STRATEGIES FOR A SECURE RETIREMENT SM Challenges to Successful Later Retirement EBRI Policy Forum Anna Rappaport May 2011 Agenda Disability benefit issues Findings from research

The Current State of Retirement Security in the United States. April 5, 2017

Hearing Statement The Before the U.S. Senate Committee on Banking, Housing, & Urban Development Subcommittee on Economic Policy The Current State of Retirement Security in the United States April 5, 2017

Hearing Statement The Before the U.S. Senate Committee on Banking, Housing, & Urban Development Subcommittee on Economic Policy The Current State of Retirement Security in the United States April 5, 2017

U.S. Household Savings for Retirement in 2010

U.S. Household Savings for Retirement in 2010 John J. Topoleski Analyst in Income Security April 30, 2013 CRS Report for Congress Prepared for Members and Committees of Congress Congressional Research

U.S. Household Savings for Retirement in 2010 John J. Topoleski Analyst in Income Security April 30, 2013 CRS Report for Congress Prepared for Members and Committees of Congress Congressional Research

Debt of the Elderly and Near Elderly,

March 5, 2018 No. 443 Debt of the Elderly and Near Elderly, 1992 2016 By Craig Copeland, Ph.D., Employee Benefit Research Institute A T A G L A N C E Much of the attention to retirement preparedness focuses

March 5, 2018 No. 443 Debt of the Elderly and Near Elderly, 1992 2016 By Craig Copeland, Ph.D., Employee Benefit Research Institute A T A G L A N C E Much of the attention to retirement preparedness focuses

Retirement Plan Coverage: How to Close the Gap

Retirement Plan Coverage: How to Close the Gap WISER Symposium, Melissa Kahn, Esq., Managing Director SSGA September 19, 2017 This material is solely for the private use of WISER Symposium attendees and

Retirement Plan Coverage: How to Close the Gap WISER Symposium, Melissa Kahn, Esq., Managing Director SSGA September 19, 2017 This material is solely for the private use of WISER Symposium attendees and

A fresh look at the 5 key findings that impact Russell s target date fund glide path design

A fresh look at the 5 key findings that impact Russell s target date fund glide path design John Greves, CFA, Portfolio Manager Dan Gardner, CFA, Defined Contribution Analyst Kevin Knowles, CFA, Product

A fresh look at the 5 key findings that impact Russell s target date fund glide path design John Greves, CFA, Portfolio Manager Dan Gardner, CFA, Defined Contribution Analyst Kevin Knowles, CFA, Product

Retirement vulnerability of new retirees:

Retirement vulnerability of new retirees: The likelihood of outliving their assets by Ernst & Young LLP for Americans for Secure Retirement July 2008 Executive summary Many of the 77 million baby boomers

Retirement vulnerability of new retirees: The likelihood of outliving their assets by Ernst & Young LLP for Americans for Secure Retirement July 2008 Executive summary Many of the 77 million baby boomers

Financial Shocks, Unexpected Expenses and Financial Experiences of Older Americans

Financial Shocks, Unexpected Expenses and Financial Experiences of Older Americans Anna M. Rappaport Presented at the Living to 100 Symposium Orlando, Fla. January 4 6, 2017 Copyright 2017 by the Society

Financial Shocks, Unexpected Expenses and Financial Experiences of Older Americans Anna M. Rappaport Presented at the Living to 100 Symposium Orlando, Fla. January 4 6, 2017 Copyright 2017 by the Society

How Much Should Americans Be Saving for Retirement?

How Much Should Americans Be Saving for Retirement? by B. Douglas Bernheim Stanford University The National Bureau of Economic Research Lorenzo Forni The Bank of Italy Jagadeesh Gokhale The Federal Reserve

How Much Should Americans Be Saving for Retirement? by B. Douglas Bernheim Stanford University The National Bureau of Economic Research Lorenzo Forni The Bank of Italy Jagadeesh Gokhale The Federal Reserve

Session 159 PD Retirement Risk Survey & Late-in-Life Survey. Moderator: Anna M. Rappaport, FSA, MAAA

Session 159 PD - 2017 Retirement Risk Survey & Late-in-Life Survey Moderator: Anna M. Rappaport, FSA, MAAA Presenters: Mathew Greenwald Anna M. Rappaport, FSA, MAAA SOA Antitrust Compliance Guidelines

Session 159 PD - 2017 Retirement Risk Survey & Late-in-Life Survey Moderator: Anna M. Rappaport, FSA, MAAA Presenters: Mathew Greenwald Anna M. Rappaport, FSA, MAAA SOA Antitrust Compliance Guidelines

The New Retirement Emerging Issues Affecting Financial Security

The New Retirement Emerging Issues Affecting Financial Security Anna Rappaport Chairperson, Committee on Post-Retirement Needs and Risks, Society of Actuaries Mathew Greenwald President, Mathew Greenwald

The New Retirement Emerging Issues Affecting Financial Security Anna Rappaport Chairperson, Committee on Post-Retirement Needs and Risks, Society of Actuaries Mathew Greenwald President, Mathew Greenwald

RETIREMENT PLAN COVERAGE AND SAVING TRENDS OF BABY BOOMER COHORTS BY SEX: ANALYSIS OF THE 1989 AND 1998 SCF

PPI PUBLIC POLICY INSTITUTE RETIREMENT PLAN COVERAGE AND SAVING TRENDS OF BABY BOOMER COHORTS BY SEX: ANALYSIS OF THE AND SCF D A T A D I G E S T Introduction Over the next three decades, the retirement

PPI PUBLIC POLICY INSTITUTE RETIREMENT PLAN COVERAGE AND SAVING TRENDS OF BABY BOOMER COHORTS BY SEX: ANALYSIS OF THE AND SCF D A T A D I G E S T Introduction Over the next three decades, the retirement

Solving the Social Security Puzzle

Solving the Social Security Puzzle What You Need to Know About Your Social Security Benefits Before You Claim Robin Brewton VP of Client Services This presentation is provided by Social Security Solutions.

Solving the Social Security Puzzle What You Need to Know About Your Social Security Benefits Before You Claim Robin Brewton VP of Client Services This presentation is provided by Social Security Solutions.

Savings Needed for Health Expenses for People Eligible for Medicare: Some Rare Good News, p. 2 IRA Asset Allocation, 2010, p. 8

October 2012 Vol. 33, No. 10 Savings Needed for Health Expenses for People Eligible for Medicare: Some Rare Good News, p. 2 IRA Asset Allocation, 2010, p. 8 A T A G L A N C E Savings Needed for Health

October 2012 Vol. 33, No. 10 Savings Needed for Health Expenses for People Eligible for Medicare: Some Rare Good News, p. 2 IRA Asset Allocation, 2010, p. 8 A T A G L A N C E Savings Needed for Health

Retirement and Investment Webinar Series

Retirement and Investment Webinar Series September 30, 2015 Retirement and Investment Great Expectations: Retirement Perceptions Don t Always Meet Reality Grace Lattyak Rob Reiskytl Heather Tredup Retirement

Retirement and Investment Webinar Series September 30, 2015 Retirement and Investment Great Expectations: Retirement Perceptions Don t Always Meet Reality Grace Lattyak Rob Reiskytl Heather Tredup Retirement

Aging Seminar Series:

Aging Seminar Series: Income and Wealth of Older Americans Domestic Social Policy Division Congressional Research Service November 19, 2008 Introduction Aging Seminar Series Focus on important issues regarding

Aging Seminar Series: Income and Wealth of Older Americans Domestic Social Policy Division Congressional Research Service November 19, 2008 Introduction Aging Seminar Series Focus on important issues regarding

In Meyer and Reichenstein (2010) and

and") M EYER R EICHENSTEIN Contributions How the Social Security Claiming Decision Affects Portfolio Longevity by William Meyer and William Reichenstein, Ph.D., CFA William Meyer is founder and CEO of Retiree

M EYER R EICHENSTEIN Contributions How the Social Security Claiming Decision Affects Portfolio Longevity by William Meyer and William Reichenstein, Ph.D., CFA William Meyer is founder and CEO of Retiree

The Role of Information and Expectations in Retirement Planning Communicating Income vs. Lump Sums. By Anna M. Rappaport, FSA, MAAA

The Role of Information and Expectations in Retirement Planning Communicating Income vs. Lump Sums By Anna M. Rappaport, FSA, MAAA Paper Prepared for Retirement 20/20 Abstract In defined contribution plans,

The Role of Information and Expectations in Retirement Planning Communicating Income vs. Lump Sums By Anna M. Rappaport, FSA, MAAA Paper Prepared for Retirement 20/20 Abstract In defined contribution plans,

Savings Medicare Beneficiaries Need for Health Expenses: Some Couples Could Need as Much as $400,000, Up From $370,000 in 2017

September 2010 No. 346 October 8, 2018 No. 460 Savings Medicare Beneficiaries Need for Health Expenses: Some Couples Could Need as Much as $400,000, Up From $370,000 in 2017 By Paul Fronstin, Ph.D., and

September 2010 No. 346 October 8, 2018 No. 460 Savings Medicare Beneficiaries Need for Health Expenses: Some Couples Could Need as Much as $400,000, Up From $370,000 in 2017 By Paul Fronstin, Ph.D., and

Income and Assets of Medicare Beneficiaries,

Income and Assets of Medicare Beneficiaries, 2014 2030 Gretchen Jacobson, Christina Swoope, and Tricia Neuman, Kaiser Family Foundation Karen Smith, Urban Institute Many Medicare, including seniors and

Income and Assets of Medicare Beneficiaries, 2014 2030 Gretchen Jacobson, Christina Swoope, and Tricia Neuman, Kaiser Family Foundation Karen Smith, Urban Institute Many Medicare, including seniors and

Generational Distinctions in Retirement Planning

Generational Distinctions in Retirement Planning Frank O Connor - VP, Research and Outreach IRI Steve Cooney VP Annuity Business Development & Innovation Nationwide David Laster, PhD, CFA Managing Director,

Generational Distinctions in Retirement Planning Frank O Connor - VP, Research and Outreach IRI Steve Cooney VP Annuity Business Development & Innovation Nationwide David Laster, PhD, CFA Managing Director,

The Long-Term Care Challenge

The Long-Term Care Challenge Developing a Plan Can Lead to Greater Confidence November 2012 About the Insured Retirement Institute: The Insured Retirement Institute (IRI) is a notfor-profit organization

The Long-Term Care Challenge Developing a Plan Can Lead to Greater Confidence November 2012 About the Insured Retirement Institute: The Insured Retirement Institute (IRI) is a notfor-profit organization

2018 American Academy of Actuaries. All rights reserved. May not be reproduced without express permission.

Today s Objective Advance retirement policy by focusing on new or emerging ideas that have the potential to better align public policy with current and future retirement needs. 2 Policy Must Keep Up Drivers

Today s Objective Advance retirement policy by focusing on new or emerging ideas that have the potential to better align public policy with current and future retirement needs. 2 Policy Must Keep Up Drivers

Student Loans: Is it Time for Employers to Step In?

Student Loans: Is it Time for Employers to Step In? Michael Doshier, Global Head of Retirement Marketing, Franklin Templeton Investments Cindy Silva, Head of Financial Wellness Strategy, Fidelity Investments

Student Loans: Is it Time for Employers to Step In? Michael Doshier, Global Head of Retirement Marketing, Franklin Templeton Investments Cindy Silva, Head of Financial Wellness Strategy, Fidelity Investments

PENTEGRA RETIREMENT SERVICES DISTRIBUTION PATHTM. The path to helping participants plan successfully

PENTEGRA RETIREMENT SERVICES DISTRIBUTION PATHTM The path to helping participants plan successfully Making a secure retirement a reality. What are your choices? What s the right amount? What s the best

PENTEGRA RETIREMENT SERVICES DISTRIBUTION PATHTM The path to helping participants plan successfully Making a secure retirement a reality. What are your choices? What s the right amount? What s the best

Social Security The Choice of a Lifetime. Timothy O Mara, Vice President, Nationwide Retirement Institute

Social Security The Choice of a Lifetime Timothy O Mara, Vice President, Nationwide Retirement Institute FOR BROKER/DEALER USE ONLY NOT FOR USE WITH THE GENERAL PUBLIC Important things to keep in mind

Social Security The Choice of a Lifetime Timothy O Mara, Vice President, Nationwide Retirement Institute FOR BROKER/DEALER USE ONLY NOT FOR USE WITH THE GENERAL PUBLIC Important things to keep in mind

A Look at the End-of-Life Financial Situation in America, p. 2

April 2015 Vol. 36, No. 4 A Look at the End-of-Life Financial Situation in America, p. 2 A T A G L A N C E A Look at the End-of-Life Financial Situation in America, by Sudipto Banerjee, Ph.D., EBRI This

April 2015 Vol. 36, No. 4 A Look at the End-of-Life Financial Situation in America, p. 2 A T A G L A N C E A Look at the End-of-Life Financial Situation in America, by Sudipto Banerjee, Ph.D., EBRI This

Retirement Security: Public Perceptions and Misperceptions

Retirement Security: Public Perceptions and Misperceptions Anna M. Rappaport, MAAA, EA, FSA Chairperson, Committee on Post-Retirement Risks and Needs, Society of Actuaries Mathew Greenwald President, Mathew

Retirement Security: Public Perceptions and Misperceptions Anna M. Rappaport, MAAA, EA, FSA Chairperson, Committee on Post-Retirement Risks and Needs, Society of Actuaries Mathew Greenwald President, Mathew

Life expectancy: A statistical measure of the average length of life from birth to death.

STUDENT MODULE 6.2 RETIREMENT PLANNING PAGE 1 Standard 6: The student will explain and evaluate the importance of planning for retirement. Longevity and Retirement Keisha, are you ready for the party?

STUDENT MODULE 6.2 RETIREMENT PLANNING PAGE 1 Standard 6: The student will explain and evaluate the importance of planning for retirement. Longevity and Retirement Keisha, are you ready for the party?

OLD-AGE POVERTY: SINGLE WOMEN & WIDOWS & A LACK OF RETIREMENT SECURITY

AUG 18 1 OLD-AGE POVERTY: SINGLE WOMEN & WIDOWS & A LACK OF RETIREMENT SECURITY by Teresa Ghilarducci, Bernard L. and Irene Schwartz Professor of Economics at The New School for Social Research and Director

AUG 18 1 OLD-AGE POVERTY: SINGLE WOMEN & WIDOWS & A LACK OF RETIREMENT SECURITY by Teresa Ghilarducci, Bernard L. and Irene Schwartz Professor of Economics at The New School for Social Research and Director

Women and Retirement. From Need to Opportunity: Engaging this Growing and Powerful Investor Segment

Women and Retirement From Need to Opportunity: Engaging this Growing and Powerful Investor Segment January 2011 Overview When planning for retirement, the opportunities presented by female clients are

Women and Retirement From Need to Opportunity: Engaging this Growing and Powerful Investor Segment January 2011 Overview When planning for retirement, the opportunities presented by female clients are

The 2007 Retiree Survey

The Ariel-Schwab Black Investor Survey: The 00 Retiree Survey October 11, 00 BACKGROUND, OBJECTIVES, AND METHODOLOGY Ariel Mutual Funds and The Charles Schwab Corporation commissioned Argosy Research to

The Ariel-Schwab Black Investor Survey: The 00 Retiree Survey October 11, 00 BACKGROUND, OBJECTIVES, AND METHODOLOGY Ariel Mutual Funds and The Charles Schwab Corporation commissioned Argosy Research to

The Influence of DC Plan Design on Retirement Outcomes. On Behalf of the DCIIA Retirement Research Board

july 2017 www.dciia.org Design Matters The Influence of DC Plan Design on Retirement Outcomes On Behalf of the DCIIA Retirement Research Board Primary Authors: Robin Green, Ann Schleck & Company Lori Lucas,

july 2017 www.dciia.org Design Matters The Influence of DC Plan Design on Retirement Outcomes On Behalf of the DCIIA Retirement Research Board Primary Authors: Robin Green, Ann Schleck & Company Lori Lucas,

WHAT MATTERS MOST. A woman s guide to an inspired retirement strategy

WHAT MATTERS MOST A woman s guide to an inspired retirement strategy Issued by Pruco Life Insurance Company (in New York, issued by Pruco Life Insurance Company of New Jersey). 0250519-00002-00 Ed. 01/2014

WHAT MATTERS MOST A woman s guide to an inspired retirement strategy Issued by Pruco Life Insurance Company (in New York, issued by Pruco Life Insurance Company of New Jersey). 0250519-00002-00 Ed. 01/2014

Savings Medicare Beneficiaries Need for Health Expenses: Some Couples Could Need as Much as $370,000, Up from $350,000 in 2016

Dec. 20, 2017 Vol. 38, No. 10 Savings Medicare Beneficiaries Need for Health Expenses: Some Couples Could Need as Much as $370,000, Up from $350,000 in 2016 by Paul Fronstin, Ph.D., and Jack VanDerhei,

Dec. 20, 2017 Vol. 38, No. 10 Savings Medicare Beneficiaries Need for Health Expenses: Some Couples Could Need as Much as $370,000, Up from $350,000 in 2016 by Paul Fronstin, Ph.D., and Jack VanDerhei,

INADEQUATE RETIREMENT SAVINGS FOR WORKERS NEARING RETIREMENT

SEPT 17 1 INADEQUATE RETIREMENT SAVINGS FOR WORKERS NEARING RETIREMENT by Teresa Ghilarducci, Bernard L. and Irene Schwartz Professor of Economics at The New School for Social Research and Director of

SEPT 17 1 INADEQUATE RETIREMENT SAVINGS FOR WORKERS NEARING RETIREMENT by Teresa Ghilarducci, Bernard L. and Irene Schwartz Professor of Economics at The New School for Social Research and Director of

4/3/2017. Charting Your Course: A financial guide for women. Today s agenda. Savings challenges women may face. Alicia Brady April 11, 2107

SAVING FOR LIFE S MILESTONES: A TIAA FINANCIAL ESSENTIALS WORKSHOP Charting Your Course: A financial guide for women Alicia Brady April 11, 2107 Today s agenda Evaluate your financial health Set financial

SAVING FOR LIFE S MILESTONES: A TIAA FINANCIAL ESSENTIALS WORKSHOP Charting Your Course: A financial guide for women Alicia Brady April 11, 2107 Today s agenda Evaluate your financial health Set financial

ACHIEVING RETIREMENT SECURITY IN AN ERA OF UNCERTAINTY: Three Important Steps

ACHIEVING RETIREMENT SECURITY IN AN ERA OF UNCERTAINTY: Three Important Steps Christine C. Marcks President, Prudential Retirement While the goal of achieving retirement security is arguably more challenging

ACHIEVING RETIREMENT SECURITY IN AN ERA OF UNCERTAINTY: Three Important Steps Christine C. Marcks President, Prudential Retirement While the goal of achieving retirement security is arguably more challenging

Demographic Change, Retirement Saving, and Financial Market Returns

Preliminary and Partial Draft Please Do Not Quote Demographic Change, Retirement Saving, and Financial Market Returns James Poterba MIT and NBER and Steven Venti Dartmouth College and NBER and David A.

Preliminary and Partial Draft Please Do Not Quote Demographic Change, Retirement Saving, and Financial Market Returns James Poterba MIT and NBER and Steven Venti Dartmouth College and NBER and David A.

Retirement Adequacy in the United States: Should We Be Concerned?

Retirement Adequacy in the United States: Should We Be Concerned? March 2018 2 Retirement Adequacy in the United States: Should We Be Concerned? AUTHORS Vickie Bajtelsmit, JD, PhD Professor, Colorado State

Retirement Adequacy in the United States: Should We Be Concerned? March 2018 2 Retirement Adequacy in the United States: Should We Be Concerned? AUTHORS Vickie Bajtelsmit, JD, PhD Professor, Colorado State

Retirement Risks and Solutions in the Middle Market

Retirement Risks and Solutions in the Middle Market Presented by Noel Abkemeier, FSA, MAAA Milliman Anna Rappaport, FSA, MAAA Anna Rappaport Consulting RIIA Webinar March 16, 2011 Context: Society of Actuaries

Retirement Risks and Solutions in the Middle Market Presented by Noel Abkemeier, FSA, MAAA Milliman Anna Rappaport, FSA, MAAA Anna Rappaport Consulting RIIA Webinar March 16, 2011 Context: Society of Actuaries

Appendix 1V Baby Boomer Contemplating Retirement

Checkpoint Contents Federal Library Federal Editorial Materials PPC's Tax and Financial Planning Library Retirement Planning Chapter 1 A Step-by-step Planning Approach Appendix 1V Baby Boomer Contemplating

Checkpoint Contents Federal Library Federal Editorial Materials PPC's Tax and Financial Planning Library Retirement Planning Chapter 1 A Step-by-step Planning Approach Appendix 1V Baby Boomer Contemplating

Retirement Redefined: Income Planning for the Modern Retiree

Retirement Redefined: Income Planning for the Modern Retiree Challenges and choices facing pre-retiree baby boomers For investors. Not FDIC Insured May Lose Value No Bank Guarantee Retirement Income Planning

Retirement Redefined: Income Planning for the Modern Retiree Challenges and choices facing pre-retiree baby boomers For investors. Not FDIC Insured May Lose Value No Bank Guarantee Retirement Income Planning

Big Question: When Should I Retire? MANAGING RETIREMENT DECISIONS SERIES

MANAGING RETIREMENT DECISIONS SERIES May 2017 Advertisements frame retirement as an extended vacation, brimming with fulfillment of life-long passions and dreams. But for many people, retirement is more

MANAGING RETIREMENT DECISIONS SERIES May 2017 Advertisements frame retirement as an extended vacation, brimming with fulfillment of life-long passions and dreams. But for many people, retirement is more

2005 Survey of Owners of Non-Qualified Annuity Contracts

2005 Survey of Owners of Non-Qualified Annuity Contracts Conducted by The Gallup Organization and Mathew Greenwald & Associates for The Committee of Annuity Insurers 2 2005 SURVEY OF OWNERS OF NON-QUALIFIED

2005 Survey of Owners of Non-Qualified Annuity Contracts Conducted by The Gallup Organization and Mathew Greenwald & Associates for The Committee of Annuity Insurers 2 2005 SURVEY OF OWNERS OF NON-QUALIFIED