Lecture 10 Financial Functions Excel 2007

|

|

|

- Sydney Reeves

- 6 years ago

- Views:

Transcription

1 Lecture 10 Financial Functions Excel

2 Negative numbers = cash you pay out, such as deposits to savings. Positive numbers = cash you receive, such as salary. PV Present(Today s) value. FV just the number you get in future. FV = 100 is a value in future that is less than 100 today.

3 If I deposit V today (9% FD for 5 years), how much can I get after Y years with fixed interest rate of r%. After Y years = Capital * Rate * years

4 Payment Functions PMT,IPMT,CUMIPMT,PPMT,ISPMT

5 PMT - PAYMENT function payment of a loan based on constant payments and a fixed interest rate. With the PMT function we can also calculate how much money we need to deposit each month in order to save X amount of money in X amount of years. how we can save in 5 years, with an interest rate of 6%.

6 PMT(rate, nper, pv, [fv], [type]) Rate The interest rate for the loan. Nper The total number of payments for the loan. Pv Fv Type The present value, or the total amount that a series of future payments is worth now; also known as the principal. Optional. The future value, or a cash balance you want to attain after the last payment is made. If fv is omitted, it is assumed to be 0 (zero), that is, the future value of a loan is 0. Optional. The number 0 (zero) (end) or 1(beginning) and indicates when payments are due.

7 To get 10 million in 10 years if you want to save $100,000 ($100,000 is the future value) to pay for a project in 10 years, then determine how much you must save each month under conservative guess of fixed interest rate of 8%. PMT(8%, 10, 0, , 0)

8 PMT(rate,#per,pv,[fv],[type]) I am borrowing $10,000 on a 10 month loan with an annual interest rate of 8 percent. What will my monthly payments be? How much principal and interest am I paying each month?

9 Loans

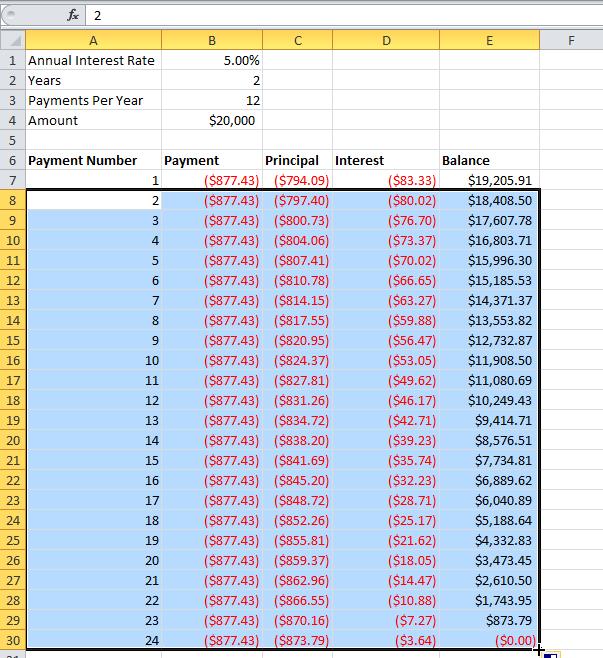

10 PMT(rate,#per,pv,[fv],[type]) What would be the monthly payment of a loan with, an annual interest rate of 6%, a 20- year duration, a present value of $150,000 (amount borrowed) and a future value of 0.

11 RATE(nper, pmt, pv, [fv], [type], [guess]) If Rate is the only unknown variable, we can use the RATE function to calculate the interest rate.

12 NPER(rate,pmt,pv,[fv],[type]) If you can monthly payment $2, on a 20-year loan, with an annual interest rate of 6%, how long will take to pay off this loan?.

13 PV(rate, nper, pmt, [fv], [type]) If we make monthly payments of $1, on a 20-year loan, with an annual interest rate of 6%, how much can we borrow?

14 FV(rate, #per, [pmt], [pv], [type]) Future value of an investment based on periodic, constant payments and a constant interest rate. Rate Nper Pmt Pv Type - The interest rate per period. - The total number of payment periods in an annuity. - The payment(fixed) made each period; Typically, pmt contains principal and interest but no other fees or taxes. If pmt is omitted, you must include the pv argument. - The present value, or the lump-sum (Down payment) amount that a series of future payments is worth right now. If pv is omitted, it is assumed to be 0 (zero), and you must include the pmt argument. - When payments are due, 0 (end) / 1 (beginning) of the period. If type is omitted, it is assumed to be 0.

![FV(rate,nper,pmt,[pv],[type]) if we make monthly](/docs-images/74/70506153/images/15-0.jpg "payments of only $1,000.")

15 FV(rate,nper,pmt,[pv],[type]) if we make monthly payments of only $1,000.00, we still have debt after 20 years.

16 More on Loans

17 calculate the monthly payment on a loan with an annual interest rate of 5%, a 2-year duration and a present value (amount borrowed) of $20,000.

18 PPMT(rate, per, nper, pv, [fv], [type]) Use the PPMT function to calculate the principal part of the payment.

19 IPMT(rate, per, nper, pv, [fv], [type]) Use the IPMT function to calculate the interest part of the payment.

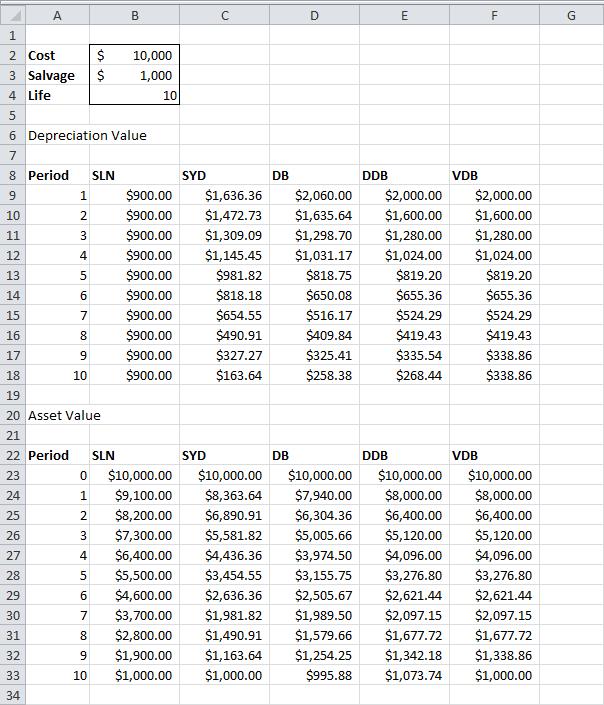

20 Update the balance.

21

22 PPMT(rate, per, nper, pv, [fv], [type]) Returns the payment on the principal for a given period for an investment based on periodic, constant payments and a constant interest rate. Payment on principle for the first month of loan? loan fraction

23 IPMT Returns the interest payment for a given period for an investment based on periodic, constant payments and a constant interest rate. How much interest do I pay for the first month? How much interest do I pay for the last year?

24 IPMT(rate, per, nper, pv, [fv], [type]) Rate Required. The interest rate per period. Per Required. The period for which you want to find the interest and must be in the range 1 to nper. Nper Required. The total number of payment periods in an annuity. Pv Required. The present value, or the lump-sum amount that a series of future payments is worth right now. Fv Optional. The future value, or a cash balance you want to attain after the last payment is made. If fv is omitted, it is assumed to be 0 (the future value of a loan, for example, is 0). Type Optional. The number 0 or 1 and indicates when payments are due. If type is omitted, it is assumed to be 0.

25 ISPMT(rate, per, nper, pv) Calculates the interest paid during a specific period of an investment. How much interest do I pay during first two year?

26 CUMIPMT(rate, nper, pv, start_period, end_period, type) Returns the cumulative interest paid on a loan between start_period and end_period. Ex: Total interest paid in the second year of payments, periods 13 through 24

27 Asset Depreciation Functions DB,DDB,SYD,SLN,VBD

28 SLN(cost, salvage, life) The SLN (Straight Line) function is easy. Each year the depreciation value is the same.

29 SYD(cost, salvage, life, per) Returns the sum-of-years' digits depreciation of an asset for a specified period. A useful life of 10 years results in a sum of years of = 55. The asset loses 9000 in value. Depreciation value period 1 = 10/55 * 9000 = 1, Deprecation value period 2 = 9/55 * 9000 = 1,472,73, etc. If we subtract these values, the asset depreciates from 10,000 to 1000 in 10 years

![DB(cost, salvage, life, period, [month]) Returns the depreciation of](/docs-images/74/70506153/images/30-0.jpg "an asset for a specified period using the fixed-declining balance")

30 DB(cost, salvage, life, period, [month]) Returns the depreciation of an asset for a specified period using the fixed-declining balance method.

31 DDB(cost, salvage, life, period, [factor]) Returns the depreciation of an asset for a specified period using the double-declining balance method or some other method you specify.

32 VDB(cost, salvage, life, start_period, end_period, [factor], [no_switch])

33 VDB(cost, salvage, life, start_period, end_period, [factor], [no_switch]) Returns the depreciation of an asset for any period you specify, including partial periods, using the double-declining balance method or some other method you specify. VDB stands for variable declining balance. The VDB function performs the same calculations as the DDB function. However, it switches to Straight Line calculation (yellow values) to make sure you reach the salvage value

34

35

36 DB Returns the depreciation of an asset for a specified period using the fixed-declining balance method. The fixed-declining balance method computes depreciation at a fixed rate. DB(cost, salvage, life, period, [month])

37 DB.. Data Description 1,000,000 Initial cost 100,000 Salvage value 6 Lifetime in years Formula =DB(A2,A3,A4,1,7) Description (Result) Depreciation in first year, with only 7 months calculated (186,083.33) =DB(A2,A3,A4,2,7) Depreciation in second year (259,639.42) =DB(A2,A3,A4,3,7) Depreciation in third year (176,814.44) =DB(A2,A3,A4,4,7) Depreciation in fourth year (120,410.64) =DB(A2,A3,A4,5,7) Depreciation in fifth year (81,999.64) =DB(A2,A3,A4,6,7) Depreciation in sixth year (55,841.76) =DB(A2,A3,A4,7,7) Depreciation in seventh year, with only 5 months calculated (15,845.10)

38 DB(PurchasePrice, SalvageValue, Life, PeriodToCalculate[, FirstYearMonth]) Calculates deprecation based upon a fixed percentage. To calculates the deprecation monthly basis, multiplying the years (PeriodToCalculate) by 12. If the item was purchased part way through the financial year, the first years depreciation will be based on the remaining part of the year. Last one is optional. KasunKosala@yahoo.com 38

")

39 DB(PurchasePrice, SalvageValue, Life, PeriodToCalculate[, FirstYearMonth]) 39

40 Investment Value Functions FV, NPV, PV

41 FV Returns the future value of an investment based on periodic, constant payments and a constant interest rate. FV(rate, nper, pmt, [pv], [type]) If I invest $2,000 a year for 40 years toward my retirement and earn 8 percent a year on my investments, how much will I have when I retire? Initially your are paying $3000

42 FV(rate, nper, pmt, [pv], [type]) Annual interest rate 8% 0.67% Number of payments Amount of the payment Present value (lump-sum) Payment is due at the beginning (1) of the period 0 $1,924,073.32

43 FV(rate,#per,[pmt],[pv],[type]) NPV Should I pay $11,000 today for a copier or $3,000 a year for 5 years? net present value of -$10, (The negative sign means we are paying money out.) present value of the payments is $12,112.05, so it's better to pay $11,000 today than to make payments at the beginning of the year.

44 PV Returns the present value of an investment. The present value is the total amount that a series of future payments is worth now. For example, when you borrow money, the loan amount is the present value to the lender. PV(rate, nper, pmt, [fv], [type]) Should I pay $11,000 today for a copier or $3,000 a year for 5 years?

45 PV(rate, nper, pmt, [fv], [type]) Rate The interest rate per period. Nper The total number of payment periods in an annuity. Pmt The fixed payment made each period over the life of the annuity. If pmt is omitted, you must include the fv argument. Fv Type Optional. The future value, or a cash balance you want to attain after the last payment is made. If fv is omitted, it is assumed to be 0 (the future value of a loan, for example, is 0). If fv is omitted, you must include the pmt argument. Optional. 0 (end) / 1 (beginning) of the period.

46 PV.. Data Description 500 Money paid out of an insurance annuity at the end of every month 8% Interest rate earned on the money paid out 20 Years the money will be paid out Formula =PV(A3/12, 12*A4, A2,, 0) Description (Result) Present value of an annuity with the terms above (-59,777.15).

47 NPV(rate,value1,[value2],...) Calculates the Net Present Value of an investment by using a discount rate and a series of future payments (negative values) and income (positive values).

48 NPV Data Description 8% Annual discount rate. This might represent the rate of inflation or the interest rate of a competing investment. -40,000 Initial cost of investment 8,000 Return from first year 9,200 Return from second year 10,000 Return from third year 12,000 Return from fourth year 14,500 Return from fifth year Formula Description (Result) =NPV(A2, A4:A8)+A3 Net present value of this investment (1,922.06) =NPV(A2, A4:A8, -9000)+A3 Net present value of this investment, with a loss in the sixth year of 9000 (-3,749.47)

49 FV(rate, #per, [pmt], [pv], [type]) If I deposit V today (10% FD for 5 years), how much can I get after Y years with compound interest rate of r%. After Y years = FV ( r%/12, Y*12, V, 0, 0 )

50 FV(rate, #per, [pmt], [pv], [type]) If I deposit V today and P every month, how much can I get after Y years with fixed interest rate of r%. After Y years = FV ( r%/12, Y*12, V, P, 0 )

51 If a parent deposit for a their new born and monthly deposit 5000 for five years time. If the interest rate is 10%, what would they get after 25 years? FV(8%/12,12*20,5000,100000,0)

52 Internal Rate of Return Functions IRR,MIRR,XIRR

53 IRR Returns the internal rate of return for a series of cash flows represented by the numbers in values. cash flows must occur at regular intervals, such as monthly or annually. The IRR is the interest rate received for an investment consisting of payments (negative values) and income (positive values) that occur at regular periods.

54 IRR(values, [guess]) Data Description -70,000 Initial cost of a business 12,000 Net income for the first year 15,000 Net income for the second year 18,000 Net income for the third year 21,000 Net income for the fourth year 26,000 Net income for the fifth year Formula Description (Result) =IRR(A2:A6) Investment's internal rate of return after four years (-2%) =IRR(A2:A7) Internal rate of return after five years (9%) =IRR(A2:A4,-10%) To calculate the internal rate of return after two years, you need to include a guess (-44%)

55 MIRR(values, finance_rate, reinvest_rate) Values Required. An array or a reference to cells that contain numbers. These numbers represent a series of payments (negative values) and income (positive values) occurring at regular periods. Finance_rate Required. The interest rate you pay on the money used in the cash flows. Reinvest_rate Required. The interest rate you receive on the cash flows as you reinvest them.

56 A B Data Description -$120,000 Initial cost 39,000 Return first year 30,000 Return second year 21,000 Return third year 37,000 Return fourth year 46,000 Return fifth year 10.00% Annual interest rate for the 120,000 loan 12.00% Annual interest rate for the reinvested profits Formula Description (Result) =MIRR(A2:A7, A8, A9) Investment's modified rate of return after five years (13%) =MIRR(A2:A5, A8, A9) Modified rate of return after three years (-5%) =MIRR(A2:A7, A8, 14%) Five-year modified rate of return based on a reinvest_rate of 14 percent (13%)

57 Example You will receive $15,000 in 5 years time. You are able to borrow and lend at a rate of 4% per year. What is the Present Value of the Investment? Answer: PV = $15,000(1.04) -5 = $12,328.91

58 Example You have $12, in your bank account. You are able to invest the full amount for 5 years, continuously compounded at a rate of 4%. What is the Future Value of the investment? Answer: FV = $12,280.96(e0.2) = $15,000

59 Example You are offered the option of choosing between an immediate, one-time, lump sum payment of $12,000, and $1,500 per year for 10 years. You are able to borrow and lend at an annual rate of 4%. Which option should you choose? Answer: PV = $1,500[(0.3244)/0.04] = $1,500(8.1108) = $12, Therefore, you should choose the annuity because it is worth about $166 more in today s dollars than the lump sum payment.

60 Problems 1. You have won a scholarship. At the end of each of the next 10 years, you'll receive a payment of $5,000. If the inflation is 10% per year, what's the present value of your scholarship winnings? 2. A perpetuity is an annuity that is received forever. If I rent my house and at the beginning of each year receive $14,000, what is the value of this perpetuity? Assume an annual cost of capital of 10 percent. (Hint: use the PV function and let the number of periods be large!) 3. I now have $250,000 in the bank. At the end of each of the next 20 years, I withdraw $15,000 to live on. If I earn 8 percent per year on my investments, how much money will I have in 20 years? 4. I deposit $1,000 per month (at the end of each month) over the next 10 years. My investments earn 0.8 percent per month. I would like to have $1,000,000 in 10 years. How much money should I deposit now? 5. A player is receiving $15 million at the end of each of the next 7 years. He can earn 6% per year on his investments. What is the present value of his future revenues?

61 Problems Use the FV function to determine the value to which $100 accumulates in three years if you are earning 7 percent per year. You have a liability of $1,000,000 due in 10 years. The cost of capital is 10 percent per year. What amount of money would you need to set aside at the end of each of the next 10 years to meet this liability? I currently have $10,000 in the bank. At the beginning of each of the next 20 years, I am going to invest $4,000, and I expect to earn 6 percent per year on my investments. How much money will I have in 20 years?

62 Problems At the end of each of the next 20 years, I will receive the following amounts: Years Amounts 1-5 $ $ $400 Use the PV function to find the present value of these cash flows if the cost of capital is 10 percent. Hint: Begin by computing the value of receiving $400 a year for 20 years, and then subtract the value of receiving $100 a year for 10 years, and so on. We are borrowing $200,000 on a 30-year mortgage with an annual interest rate of 10 percent. Assuming end of month payments, determine the monthly payment, interest payment each month, and amount paid toward principal each month.

63 Problems You are going to buy a new car. The cost of the car is $50,000. You have been offered two payment plans: A 10 percent discount on the cost of the car, followed by 60 monthly payments financed at 9 percent per year. No discount on the cost of the car, but the 60 monthly payments are financed at only 2 percent per year. If you believe your annual cost of capital is 9 percent, which payment plan is a better deal? Assume all payments occur at the end of the month. A balloon mortgage requires you to pay off part of a loan during a specified time period, and then make a lump sum payment to pay off the remaining portion of the loan. Suppose you borrow $400,000 on a 20-year balloon mortgage and the interest rate is.5 percent per month. Your end of month payments during the first 20 years are required to pay off $300,000 of your loan, and 20 years from now you will have to pay off the remaining $100,000. Determine your monthly payments for this loan.

64 Stock market

Financial Functions HNDA 1 st Year Computer Applications. By Nadeeshani Aththanagoda. Bsc,Msc ATI-Section Anuradhapura

Financial Functions HNDA 1 st Year Computer Applications By Nadeeshani Aththanagoda. Bsc,Msc ATI-Section Anuradhapura Financial Functions This section will cover the built-in Excel Financial Functions.

Financial Functions HNDA 1 st Year Computer Applications By Nadeeshani Aththanagoda. Bsc,Msc ATI-Section Anuradhapura Financial Functions This section will cover the built-in Excel Financial Functions.

Although most Excel users even most advanced business users will have scant occasion

Chapter 5 FINANCIAL CALCULATIONS In This Chapter EasyRefresher : Applying Time Value of Money Concepts Using the Standard Financial Functions Using the Add-In Financial Functions Although most Excel users

Chapter 5 FINANCIAL CALCULATIONS In This Chapter EasyRefresher : Applying Time Value of Money Concepts Using the Standard Financial Functions Using the Add-In Financial Functions Although most Excel users

Chapter 6. Evaluating the Financial Impact of Loans and Investments

Chapter 6 Evaluating the Financial Impact of Loans and Investments Chapter Introduction Fundamental financial calculations used to evaluate different financing options Developing an amortization table

Chapter 6 Evaluating the Financial Impact of Loans and Investments Chapter Introduction Fundamental financial calculations used to evaluate different financing options Developing an amortization table

Excel Tutorial 9: Working with Financial Tools and Functions TRUE/FALSE 1. The fv argument is required in the PMT function.

Excel Tutorial 9: Working with Financial Tools and Functions TRUE/FALSE 1. The fv argument is required in the PMT function. ANS: F PTS: 1 REF: EX 493 2. Cash flow has nothing to do with who owns the money.

Excel Tutorial 9: Working with Financial Tools and Functions TRUE/FALSE 1. The fv argument is required in the PMT function. ANS: F PTS: 1 REF: EX 493 2. Cash flow has nothing to do with who owns the money.

FINANCE FOR EVERYONE SPREADSHEETS

FINANCE FOR EVERYONE SPREADSHEETS Some Important Stuff Make sure there are at least two decimals allowed in each cell. Otherwise rounding off may create problems in a multi-step problem Always enter the

FINANCE FOR EVERYONE SPREADSHEETS Some Important Stuff Make sure there are at least two decimals allowed in each cell. Otherwise rounding off may create problems in a multi-step problem Always enter the

FINANCIAL DECISION RULES FOR PROJECT EVALUATION SPREADSHEETS

FINANCIAL DECISION RULES FOR PROJECT EVALUATION SPREADSHEETS This note is some basic information that should help you get started and do most calculations if you have access to spreadsheets. You could

FINANCIAL DECISION RULES FOR PROJECT EVALUATION SPREADSHEETS This note is some basic information that should help you get started and do most calculations if you have access to spreadsheets. You could

Engineering Economics

Economic Analysis Methods Engineering Economics Day 3: Rate of Return Analysis Three commonly used economic analysis methods are 1. Present Worth Analysis 2. Annual Worth Analysis 3. www.engr.sjsu.edu/bjfurman/courses/me195/presentations/engeconpatel3nov4.ppt

Economic Analysis Methods Engineering Economics Day 3: Rate of Return Analysis Three commonly used economic analysis methods are 1. Present Worth Analysis 2. Annual Worth Analysis 3. www.engr.sjsu.edu/bjfurman/courses/me195/presentations/engeconpatel3nov4.ppt

IE2140 Engineering Economy Tutorial 3 (Lab 1) Using Excel Financial Functions for Project Evaluation

Using Excel Financial Functions for Project Evaluation") IE2140 Engineering Economy Tutorial 3 (Lab 1) Using Excel Financial Functions for Project Evaluation 1. Objectives and Overview Solutions Guide by Hong Lanqing, Wang Xin and Mei Wenjie The objective of

IE2140 Engineering Economy Tutorial 3 (Lab 1) Using Excel Financial Functions for Project Evaluation 1. Objectives and Overview Solutions Guide by Hong Lanqing, Wang Xin and Mei Wenjie The objective of

Capital Leases I: Present and Future Value

Spreadsheet Models for Managers 9/1 Session 9 Capital Leases I: Present and Future Value Worksheet Functions Non-Uniform Payments Last revised: July 6, 2011 Review of last time: Financial Models 9/2 Three

Spreadsheet Models for Managers 9/1 Session 9 Capital Leases I: Present and Future Value Worksheet Functions Non-Uniform Payments Last revised: July 6, 2011 Review of last time: Financial Models 9/2 Three

CHAPTER 4. The Time Value of Money. Chapter Synopsis

CHAPTER 4 The Time Value of Money Chapter Synopsis Many financial problems require the valuation of cash flows occurring at different times. However, money received in the future is worth less than money

CHAPTER 4 The Time Value of Money Chapter Synopsis Many financial problems require the valuation of cash flows occurring at different times. However, money received in the future is worth less than money

1) Cash Flow Pattern Diagram for Future Value and Present Value of Irregular Cash Flows

Cash Flow Pattern Diagram for Future Value and Present Value of Irregular Cash Flows") Topics Excel & Business Math Video/Class Project #45 Cash Flow Analysis for Annuities: Savings Plans, Asset Valuation, Retirement Plans and Mortgage Loan. FV, PV and PMT. 1) Cash Flow Pattern Diagram for

Topics Excel & Business Math Video/Class Project #45 Cash Flow Analysis for Annuities: Savings Plans, Asset Valuation, Retirement Plans and Mortgage Loan. FV, PV and PMT. 1) Cash Flow Pattern Diagram for

3. Time value of money. We will review some tools for discounting cash flows.

1 3. Time value of money We will review some tools for discounting cash flows. Simple interest 2 With simple interest, the amount earned each period is always the same: i = rp o where i = interest earned

1 3. Time value of money We will review some tools for discounting cash flows. Simple interest 2 With simple interest, the amount earned each period is always the same: i = rp o where i = interest earned

3. Time value of money

1 Simple interest 2 3. Time value of money With simple interest, the amount earned each period is always the same: i = rp o We will review some tools for discounting cash flows. where i = interest earned

1 Simple interest 2 3. Time value of money With simple interest, the amount earned each period is always the same: i = rp o We will review some tools for discounting cash flows. where i = interest earned

Lecture 3. Chapter 4: Allocating Resources Over Time

Lecture 3 Chapter 4: Allocating Resources Over Time 1 Introduction: Time Value of Money (TVM) $20 today is worth more than the expectation of $20 tomorrow because: a bank would pay interest on the $20

Lecture 3 Chapter 4: Allocating Resources Over Time 1 Introduction: Time Value of Money (TVM) $20 today is worth more than the expectation of $20 tomorrow because: a bank would pay interest on the $20

(Refer Slide Time: 00:50)

") Engineering Economic Analysis Professor Dr. Pradeep K Jha Department of Mechanical and Industrial Engineering Indian Institute of Technology Roorkee Lecture 22 Basic Depreciation Methods: S-L Method, Declining

Engineering Economic Analysis Professor Dr. Pradeep K Jha Department of Mechanical and Industrial Engineering Indian Institute of Technology Roorkee Lecture 22 Basic Depreciation Methods: S-L Method, Declining

Section 5.1 Simple and Compound Interest

Section 5.1 Simple and Compound Interest Question 1 What is simple interest? Question 2 What is compound interest? Question 3 - What is an effective interest rate? Question 4 - What is continuous compound

Section 5.1 Simple and Compound Interest Question 1 What is simple interest? Question 2 What is compound interest? Question 3 - What is an effective interest rate? Question 4 - What is continuous compound

Principles of Corporate Finance. Brealey and Myers. Sixth Edition. ! How to Calculate Present Values. Slides by Matthew Will.

Principles of Corporate Finance Brealey and Myers Sixth Edition! How to Calculate Present Values Slides by Matthew Will Chapter 3 3-2 Topics Covered " Valuing Long-Lived Assets " PV Calculation Short Cuts

Principles of Corporate Finance Brealey and Myers Sixth Edition! How to Calculate Present Values Slides by Matthew Will Chapter 3 3-2 Topics Covered " Valuing Long-Lived Assets " PV Calculation Short Cuts

Calc Guide. Appendix B Description of Functions

Calc Guide Appendix B of Functions Copyright This document is Copyright 2005 2011 by its contributors as listed below. You may distribute it and/or modify it under the terms of either the GNU General Public

Calc Guide Appendix B of Functions Copyright This document is Copyright 2005 2011 by its contributors as listed below. You may distribute it and/or modify it under the terms of either the GNU General Public

ExcelBasics.pdf. Here is the URL for a very good website about Excel basics including the material covered in this primer.

Excel Primer for Finance Students John Byrd, November 2015. This primer assumes you can enter data and copy functions and equations between cells in Excel. If you aren t familiar with these basic skills

Excel Primer for Finance Students John Byrd, November 2015. This primer assumes you can enter data and copy functions and equations between cells in Excel. If you aren t familiar with these basic skills

Chapter 6. Learning Objectives. Principals Applies in this Chapter. Time Value of Money

Chapter 6 Time Value of Money 1 Learning Objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate the present and future values of each. 2. Calculate the present value of

Chapter 6 Time Value of Money 1 Learning Objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate the present and future values of each. 2. Calculate the present value of

Copyright 2015 by the McGraw-Hill Education (Asia). All rights reserved.

. All rights reserved.") Copyright 2015 by the McGraw-Hill Education (Asia). All rights reserved. Key Concepts and Skills Be able to compute the future value of multiple cash flows Be able to compute the present value of multiple

Copyright 2015 by the McGraw-Hill Education (Asia). All rights reserved. Key Concepts and Skills Be able to compute the future value of multiple cash flows Be able to compute the present value of multiple

If the Basic Salary of an employee is Rs. 20,000 and Allowances are of Rs then What percentage of the Basic Salary are the Allowances?

Lecture:2 Q#1: Marks =3 (a) Convert 17.5% in the fraction. (b) Convert 40 / 240 in percent. (c) x% of 200 =? (a) 0.175 (b) 16.66% (c) 2x Q#2: Marks =2 What percent of 30 is 9? 30 Q#3: Marks =2 Write an

Lecture:2 Q#1: Marks =3 (a) Convert 17.5% in the fraction. (b) Convert 40 / 240 in percent. (c) x% of 200 =? (a) 0.175 (b) 16.66% (c) 2x Q#2: Marks =2 What percent of 30 is 9? 30 Q#3: Marks =2 Write an

Real Estate. Refinancing

Introduction This Solutions Handbook has been designed to supplement the HP-12C Owner's Handbook by providing a variety of applications in the financial area. Programs and/or step-by-step keystroke procedures

Introduction This Solutions Handbook has been designed to supplement the HP-12C Owner's Handbook by providing a variety of applications in the financial area. Programs and/or step-by-step keystroke procedures

Chapter 2 Time Value of Money ANSWERS TO END-OF-CHAPTER QUESTIONS

Chapter 2 Time Value of Money ANSWERS TO END-OF-CHAPTER QUESTIONS 2-1 a. PV (present value) is the value today of a future payment, or stream of payments, discounted at the appropriate rate of interest.

Chapter 2 Time Value of Money ANSWERS TO END-OF-CHAPTER QUESTIONS 2-1 a. PV (present value) is the value today of a future payment, or stream of payments, discounted at the appropriate rate of interest.

Life Cycle Analysis Money... and More

Life Cycle Analysis Money... and More Dorothy McCarty, AIA, LEED AP Lakeisha Lindsey October 15, 2015 listen engage advise deliver Factors affecting decision making Goals of the organization Market-driven

Life Cycle Analysis Money... and More Dorothy McCarty, AIA, LEED AP Lakeisha Lindsey October 15, 2015 listen engage advise deliver Factors affecting decision making Goals of the organization Market-driven

Lecture 15. Thursday Mar 25 th. Advanced Topics in Capital Budgeting

Lecture 15. Thursday Mar 25 th Equal Length Projects If 2 Projects are of equal length, but unequal scale then: Positive NPV says do projects Profitability Index allows comparison ignoring scale If cashflows

Lecture 15. Thursday Mar 25 th Equal Length Projects If 2 Projects are of equal length, but unequal scale then: Positive NPV says do projects Profitability Index allows comparison ignoring scale If cashflows

And you also pay an additional amount which is rent on the use of the money while you have it and the lender doesn t

Professor Shoemaker When you borrow money you must eventually return the amount you borrow And you also pay an additional amount which is rent on the use of the money while you have it and the lender doesn

Professor Shoemaker When you borrow money you must eventually return the amount you borrow And you also pay an additional amount which is rent on the use of the money while you have it and the lender doesn

Time Value of Money CHAPTER. Will You Be Able to Retire?

CHAPTER 5 Goodluz/Shutterstock.com Time Value of Money Will You Be Able to Retire? Your reaction to that question is probably, First things first! I m worried about getting a job, not about retiring! However,

CHAPTER 5 Goodluz/Shutterstock.com Time Value of Money Will You Be Able to Retire? Your reaction to that question is probably, First things first! I m worried about getting a job, not about retiring! However,

The simplest of the five is the SLN Function which uses the straight-line depreciation

An asset is defined as a resource with an inherent economic value that is owned by an individual, corporation or country which will yield future economic benefit. Accountants list assets on balance sheets,

An asset is defined as a resource with an inherent economic value that is owned by an individual, corporation or country which will yield future economic benefit. Accountants list assets on balance sheets,

บทท 3 ม ลค าของเง นตามเวลา (Time Value of Money)

") บทท 3 ม ลค าของเง นตามเวลา (Time Value of Money) Topic Coverage: The Interest Rate Simple Interest Rate Compound Interest Rate Amortizing a Loan Compounding Interest More Than Once per Year The Time Value

บทท 3 ม ลค าของเง นตามเวลา (Time Value of Money) Topic Coverage: The Interest Rate Simple Interest Rate Compound Interest Rate Amortizing a Loan Compounding Interest More Than Once per Year The Time Value

Intermediate Excel. Winter Winter 2011 CS130 - Intermediate Excel 1

Intermediate Excel Winter 2011 Winter 2011 CS130 - Intermediate Excel 1 Combination Cell References How do $A1 and A$1 differ from $A$1? A B C D E 1 4 8 =A1/$A$3 2 6 4 =A$1*$B4+B2 3 =A1+A2 1 4 5 What formula

Intermediate Excel Winter 2011 Winter 2011 CS130 - Intermediate Excel 1 Combination Cell References How do $A1 and A$1 differ from $A$1? A B C D E 1 4 8 =A1/$A$3 2 6 4 =A$1*$B4+B2 3 =A1+A2 1 4 5 What formula

Full file at https://fratstock.eu

Chapter 2 Time Value of Money ANSWERS TO END-OF-CHAPTER QUESTIONS 2-1 a. PV (present value) is the value today of a future payment, or stream of payments, discounted at the appropriate rate of interest.

Chapter 2 Time Value of Money ANSWERS TO END-OF-CHAPTER QUESTIONS 2-1 a. PV (present value) is the value today of a future payment, or stream of payments, discounted at the appropriate rate of interest.

CHAPTER 2 TIME VALUE OF MONEY

CHAPTER 2 TIME VALUE OF MONEY True/False Easy: (2.2) Compounding Answer: a EASY 1. One potential benefit from starting to invest early for retirement is that the investor can expect greater benefits from

CHAPTER 2 TIME VALUE OF MONEY True/False Easy: (2.2) Compounding Answer: a EASY 1. One potential benefit from starting to invest early for retirement is that the investor can expect greater benefits from

I. Warnings for annuities and

Outline I. More on the use of the financial calculator and warnings II. Dealing with periods other than years III. Understanding interest rate quotes and conversions IV. Applications mortgages, etc. 0

Outline I. More on the use of the financial calculator and warnings II. Dealing with periods other than years III. Understanding interest rate quotes and conversions IV. Applications mortgages, etc. 0

Functions, Amortization Tables, and What-If Analysis

Functions, Amortization Tables, and What-If Analysis Absolute and Relative References Q1: How do $A1 and A$1 differ from $A$1? Use the following table to answer the questions listed below: A B C D E 1

Functions, Amortization Tables, and What-If Analysis Absolute and Relative References Q1: How do $A1 and A$1 differ from $A$1? Use the following table to answer the questions listed below: A B C D E 1

Time Value of Money. Part III. Outline of the Lecture. September Growing Annuities. The Effect of Compounding. Loan Type and Loan Amortization

Time Value of Money Part III September 2003 Outline of the Lecture Growing Annuities The Effect of Compounding Loan Type and Loan Amortization 2 Growing Annuities The present value of an annuity in which

Time Value of Money Part III September 2003 Outline of the Lecture Growing Annuities The Effect of Compounding Loan Type and Loan Amortization 2 Growing Annuities The present value of an annuity in which

Time Value of Money. Ex: How much a bond, which can be cashed out in 2 years, is worth today

Time Value of Money The time value of money is the idea that money available now is worth more than the same amount in the future - this is essentially why interest exists. Present value is the current

Time Value of Money The time value of money is the idea that money available now is worth more than the same amount in the future - this is essentially why interest exists. Present value is the current

Chapter 2 Time Value of Money

Chapter 2 Time Value of Money Learning Objectives After reading this chapter, students should be able to: Convert time value of money (TVM) problems from words to time lines. Explain the relationship between

Chapter 2 Time Value of Money Learning Objectives After reading this chapter, students should be able to: Convert time value of money (TVM) problems from words to time lines. Explain the relationship between

Fin 5413: Chapter 06 - Mortgages: Additional Concepts, Analysis, and Applications Page 1

Fin 5413: Chapter 06 - Mortgages: Additional Concepts, Analysis, and Applications Page 1 INTRODUCTION Solutions to Problems - Chapter 6 Mortgages: Additional Concepts, Analysis, and Applications The following

Fin 5413: Chapter 06 - Mortgages: Additional Concepts, Analysis, and Applications Page 1 INTRODUCTION Solutions to Problems - Chapter 6 Mortgages: Additional Concepts, Analysis, and Applications The following

REVIEW MATERIALS FOR REAL ESTATE FUNDAMENTALS

REVIEW MATERIALS FOR REAL ESTATE FUNDAMENTALS 1997, Roy T. Black J. Andrew Hansz, Ph.D., CFA REAE 3325, Fall 2005 University of Texas, Arlington Department of Finance and Real Estate CONTENTS ITEM ANNUAL

REVIEW MATERIALS FOR REAL ESTATE FUNDAMENTALS 1997, Roy T. Black J. Andrew Hansz, Ph.D., CFA REAE 3325, Fall 2005 University of Texas, Arlington Department of Finance and Real Estate CONTENTS ITEM ANNUAL

Tutorial 3: Working with Formulas and Functions

Tutorial 3: Working with Formulas and Functions Microsoft Excel 2010 Objectives Copy formulas Build formulas containing relative, absolute, and mixed references Review function syntax Insert a function

Tutorial 3: Working with Formulas and Functions Microsoft Excel 2010 Objectives Copy formulas Build formulas containing relative, absolute, and mixed references Review function syntax Insert a function

JEM034 Corporate Finance Winter Semester 2017/2018

JEM034 Corporate Finance Winter Semester 2017/2018 Lecture #1 Olga Bychkova Topics Covered Today Review of key finance concepts Present value (chapter 2 in BMA) Valuation of bonds (chapter 3 in BMA) Present

JEM034 Corporate Finance Winter Semester 2017/2018 Lecture #1 Olga Bychkova Topics Covered Today Review of key finance concepts Present value (chapter 2 in BMA) Valuation of bonds (chapter 3 in BMA) Present

Chapter 5 Time Value of Money

Chapter 5 Time Value of Money Answers to End-of-Chapter 5 Questions 5-1 The opportunity cost is the rate of interest one could earn on an alternative investment with a risk equal to the risk of the investment

Chapter 5 Time Value of Money Answers to End-of-Chapter 5 Questions 5-1 The opportunity cost is the rate of interest one could earn on an alternative investment with a risk equal to the risk of the investment

1. Assume that monthly payments begin in one month. What will each payment be? A) $ B) $1, C) $1, D) $1, E) $1,722.

$ B) $1, C) $1, D) $1, E) $1,722.") Name: Date: You and your spouse have found your dream home. The selling price is $220,000; you will put $50,000 down and obtain a 30-year fixed-rate mortgage at 7.5% APR for the balance. 1. Assume that

Name: Date: You and your spouse have found your dream home. The selling price is $220,000; you will put $50,000 down and obtain a 30-year fixed-rate mortgage at 7.5% APR for the balance. 1. Assume that

Computational Mathematics/Information Technology

Computational Mathematics/Information Technology 2009 10 Financial Functions in Excel This lecture starts to develop the background for the financial functions in Excel that deal with, for example, loan

Computational Mathematics/Information Technology 2009 10 Financial Functions in Excel This lecture starts to develop the background for the financial functions in Excel that deal with, for example, loan

CHAPTER 4 TIME VALUE OF MONEY

CHAPTER 4 TIME VALUE OF MONEY 1 Learning Outcomes LO.1 Identify various types of cash flow patterns (streams) seen in business. LO.2 Compute the future value of different cash flow streams. Explain the

CHAPTER 4 TIME VALUE OF MONEY 1 Learning Outcomes LO.1 Identify various types of cash flow patterns (streams) seen in business. LO.2 Compute the future value of different cash flow streams. Explain the

Principles of Corporate Finance

Principles of Corporate Finance Professor James J. Barkocy Time is money really McGraw-Hill/Irwin Copyright 2015 by The McGraw-Hill Companies, Inc. All rights reserved. Time Value of Money Money has a

Principles of Corporate Finance Professor James J. Barkocy Time is money really McGraw-Hill/Irwin Copyright 2015 by The McGraw-Hill Companies, Inc. All rights reserved. Time Value of Money Money has a

Chapter 5. Interest Rates ( ) 6. % per month then you will have ( 1.005) = of 2 years, using our rule ( ) = 1.

6. % per month then you will have ( 1.005) = of 2 years, using our rule ( ) = 1.") Chapter 5 Interest Rates 5-. 6 a. Since 6 months is 24 4 So the equivalent 6 month rate is 4.66% = of 2 years, using our rule ( ) 4 b. Since one year is half of 2 years ( ).2 2 =.0954 So the equivalent

Chapter 5 Interest Rates 5-. 6 a. Since 6 months is 24 4 So the equivalent 6 month rate is 4.66% = of 2 years, using our rule ( ) 4 b. Since one year is half of 2 years ( ).2 2 =.0954 So the equivalent

Worksheet-2 Present Value Math I

What you will learn: Worksheet-2 Present Value Math I How to compute present and future values of single and annuity cash flows How to handle cash flow delays and combinations of cash flow streams How

What you will learn: Worksheet-2 Present Value Math I How to compute present and future values of single and annuity cash flows How to handle cash flow delays and combinations of cash flow streams How

ANSWERS TO CHAPTER QUESTIONS. The Time Value of Money. 1) Compounding is interest paid on principal and interest accumulated.

Compounding is interest paid on principal and interest accumulated.") ANSWERS TO CHAPTER QUESTIONS Chapter 2 The Time Value of Money 1) Compounding is interest paid on principal and interest accumulated. It is important because normal compounding over many years can result

ANSWERS TO CHAPTER QUESTIONS Chapter 2 The Time Value of Money 1) Compounding is interest paid on principal and interest accumulated. It is important because normal compounding over many years can result

Simple Interest: Interest earned only on the original principal amount invested.

53 Future Value (FV): The amount an investment is worth after one or more periods. Simple Interest: Interest earned only on the original principal amount invested. Compound Interest: Interest earned on

53 Future Value (FV): The amount an investment is worth after one or more periods. Simple Interest: Interest earned only on the original principal amount invested. Compound Interest: Interest earned on

Our Own Problems and Solutions to Accompany Topic 11

Our Own Problems and Solutions to Accompany Topic. A home buyer wants to borrow $240,000, and to repay the loan with monthly payments over 30 years. A. Compute the unchanging monthly payments for a standard

Our Own Problems and Solutions to Accompany Topic. A home buyer wants to borrow $240,000, and to repay the loan with monthly payments over 30 years. A. Compute the unchanging monthly payments for a standard

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture - 01 Introduction Welcome to the course Time value

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture - 01 Introduction Welcome to the course Time value

FinQuiz Notes

Reading 6 The Time Value of Money Money has a time value because a unit of money received today is worth more than a unit of money to be received tomorrow. Interest rates can be interpreted in three ways.

Reading 6 The Time Value of Money Money has a time value because a unit of money received today is worth more than a unit of money to be received tomorrow. Interest rates can be interpreted in three ways.

SOLUTION METHODS FOR SELECTED BASIC FINANCIAL RELATIONSHIPS

SVEN THOMMESEN FINANCE 2400/3200/3700 Spring 2018 [Updated 8/31/16] SOLUTION METHODS FOR SELECTED BASIC FINANCIAL RELATIONSHIPS VARIABLES USED IN THE FOLLOWING PAGES: N = the number of periods (months,

SVEN THOMMESEN FINANCE 2400/3200/3700 Spring 2018 [Updated 8/31/16] SOLUTION METHODS FOR SELECTED BASIC FINANCIAL RELATIONSHIPS VARIABLES USED IN THE FOLLOWING PAGES: N = the number of periods (months,

Time Value of Money. PV of Multiple Cash Flows. Present Value & Discounting. Future Value & Compounding. PV of Multiple Cash Flows

Chapter 4-6 Time Value of Money Net Present Value Capital Budgeting Konan Chan Financial Management, 2018 Time Value of Money Present values Future values Annuity and Perpetuity APR vs. EAR Five factor

Chapter 4-6 Time Value of Money Net Present Value Capital Budgeting Konan Chan Financial Management, 2018 Time Value of Money Present values Future values Annuity and Perpetuity APR vs. EAR Five factor

Chapter 4-6 Time Value of Money Net Present Value Capital Budgeting. Konan Chan Financial Management, Time Value of Money

Chapter 4-6 Time Value of Money Net Present Value Capital Budgeting Konan Chan Financial Management, 2018 Time Value of Money Present values Future values Annuity and Perpetuity APR vs. EAR Five factor

Chapter 4-6 Time Value of Money Net Present Value Capital Budgeting Konan Chan Financial Management, 2018 Time Value of Money Present values Future values Annuity and Perpetuity APR vs. EAR Five factor

Time Value of Money. All time value of money problems involve comparisons of cash flows at different dates.

Time Value of Money The time value of money is a very important concept in Finance. This section is aimed at giving you intuitive and hands-on training on how to price securities (e.g., stocks and bonds),

Time Value of Money The time value of money is a very important concept in Finance. This section is aimed at giving you intuitive and hands-on training on how to price securities (e.g., stocks and bonds),

Quick Guide to Using the HP12C

Quick Guide to Using the HP12C Introduction: The HP- 12C is a powerful financial calculator that has become the de facto standard in the financial services industry. However, its operation differs from

Quick Guide to Using the HP12C Introduction: The HP- 12C is a powerful financial calculator that has become the de facto standard in the financial services industry. However, its operation differs from

3.1 Simple Interest. Definition: I = Prt I = interest earned P = principal ( amount invested) r = interest rate (as a decimal) t = time

r = interest rate (as a decimal) t = time") 3.1 Simple Interest Definition: I = Prt I = interest earned P = principal ( amount invested) r = interest rate (as a decimal) t = time An example: Find the interest on a boat loan of $5,000 at 16% for

3.1 Simple Interest Definition: I = Prt I = interest earned P = principal ( amount invested) r = interest rate (as a decimal) t = time An example: Find the interest on a boat loan of $5,000 at 16% for

Copyright 2016 by the UBC Real Estate Division

DISCLAIMER: This publication is intended for EDUCATIONAL purposes only. The information contained herein is subject to change with no notice, and while a great deal of care has been taken to provide accurate

DISCLAIMER: This publication is intended for EDUCATIONAL purposes only. The information contained herein is subject to change with no notice, and while a great deal of care has been taken to provide accurate

TIME VALUE OF MONEY. (Difficulty: E = Easy, M = Medium, and T = Tough) Multiple Choice: Conceptual. Easy:

Multiple Choice: Conceptual. Easy:") TIME VALUE OF MONEY (Difficulty: E = Easy, M = Medium, and T = Tough) Multiple Choice: Conceptual Easy: PV and discount rate Answer: a Diff: E. You have determined the profitability of a planned project

TIME VALUE OF MONEY (Difficulty: E = Easy, M = Medium, and T = Tough) Multiple Choice: Conceptual Easy: PV and discount rate Answer: a Diff: E. You have determined the profitability of a planned project

5-1 FUTURE VALUE If you deposit $10,000 in a bank account that pays 10% interest ann~ally, how much will be in your account after 5 years?

174 Part 2 Fundamental Concepts in Financial Management QuESTIONS 5-1 What is an opportunity cost? How is this concept used in TVM analysis, and where is it shown on a time line? Is a single number used

174 Part 2 Fundamental Concepts in Financial Management QuESTIONS 5-1 What is an opportunity cost? How is this concept used in TVM analysis, and where is it shown on a time line? Is a single number used

Chapter 4. Discounted Cash Flow Valuation

Chapter 4 Discounted Cash Flow Valuation Appreciate the significance of compound vs. simple interest Describe and compute the future value and/or present value of a single cash flow or series of cash flows

Chapter 4 Discounted Cash Flow Valuation Appreciate the significance of compound vs. simple interest Describe and compute the future value and/or present value of a single cash flow or series of cash flows

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture 08 Present Value Welcome to the lecture series on Time

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture 08 Present Value Welcome to the lecture series on Time

Chapter 02 Test Bank - Static KEY

Chapter 02 Test Bank - Static KEY 1. The present value of $100 expected two years from today at a discount rate of 6 percent is A. $112.36. B. $106.00. C. $100.00. D. $89.00. 2. Present value is defined

Chapter 02 Test Bank - Static KEY 1. The present value of $100 expected two years from today at a discount rate of 6 percent is A. $112.36. B. $106.00. C. $100.00. D. $89.00. 2. Present value is defined

Chapter 03 - Basic Annuities

3-1 Chapter 03 - Basic Annuities Section 3.0 - Sum of a Geometric Sequence The form for the sum of a geometric sequence is: Sum(n) a + ar + ar 2 + ar 3 + + ar n 1 Here a = (the first term) n = (the number

3-1 Chapter 03 - Basic Annuities Section 3.0 - Sum of a Geometric Sequence The form for the sum of a geometric sequence is: Sum(n) a + ar + ar 2 + ar 3 + + ar n 1 Here a = (the first term) n = (the number

The three formulas we use most commonly involving compounding interest n times a year are

Section 6.6 and 6.7 with finance review questions are included in this document for your convenience for studying for quizzes and exams for Finance Calculations for Math 11. Section 6.6 focuses on identifying

Section 6.6 and 6.7 with finance review questions are included in this document for your convenience for studying for quizzes and exams for Finance Calculations for Math 11. Section 6.6 focuses on identifying

Chapter Organization. The future value (FV) is the cash value of. an investment at some time in the future.

is the cash value of. an investment at some time in the future.") Chapter 5 The Time Value of Money Chapter Organization 5.2. Present Value and Discounting The future value (FV) is the cash value of an investment at some time in the future Suppose you invest 100 in a

Chapter 5 The Time Value of Money Chapter Organization 5.2. Present Value and Discounting The future value (FV) is the cash value of an investment at some time in the future Suppose you invest 100 in a

Time Value of Money. Lakehead University. Outline of the Lecture. Fall Future Value and Compounding. Present Value and Discounting

Time Value of Money Lakehead University Fall 2004 Outline of the Lecture Future Value and Compounding Present Value and Discounting More on Present and Future Values 2 Future Value and Compounding Future

Time Value of Money Lakehead University Fall 2004 Outline of the Lecture Future Value and Compounding Present Value and Discounting More on Present and Future Values 2 Future Value and Compounding Future

CHAPTER 2 How to Calculate Present Values

CHAPTER How to Calculate Present Values Answers to Problem Sets. If the discount factor is.507, then.507 x. 6 = $. Est time: 0-05. DF x 39 = 5. Therefore, DF =5/39 =.899. Est time: 0-05 3. PV = 374/(.09)

CHAPTER How to Calculate Present Values Answers to Problem Sets. If the discount factor is.507, then.507 x. 6 = $. Est time: 0-05. DF x 39 = 5. Therefore, DF =5/39 =.899. Est time: 0-05 3. PV = 374/(.09)

Solutions to EA-1 Examination Spring, 2001

Solutions to EA-1 Examination Spring, 2001 Question 1 1 d (m) /m = (1 d (2m) /2m) 2 Substituting the given values of d (m) and d (2m), 1 - = (1 - ) 2 1 - = 1 - + (multiplying the equation by m 2 ) m 2

Solutions to EA-1 Examination Spring, 2001 Question 1 1 d (m) /m = (1 d (2m) /2m) 2 Substituting the given values of d (m) and d (2m), 1 - = (1 - ) 2 1 - = 1 - + (multiplying the equation by m 2 ) m 2

(Refer Slide Time: 2:56)

") Depreciation, Alternate Investment and Profitability Analysis. Professor Dr. Bikash Mohanty. Department of Chemical Engineering. Indian Institute of Technology, Roorkee. Lecture-5. Depreciation Sum of

Depreciation, Alternate Investment and Profitability Analysis. Professor Dr. Bikash Mohanty. Department of Chemical Engineering. Indian Institute of Technology, Roorkee. Lecture-5. Depreciation Sum of

Jeopardy. Financial Literacy 1 Q $100 Q $100 Q $100 Q $100 Q $100 Q $200 Q $200 Q $200 Q $200 Q $200 Q $300 Q $300 Q $300 Q $300 Q $300

Jeopardy Multiplying Fractions Dividing Fractions Word Problems Financial Literacy 1 Financial Literacy 2 Q $100 Q $200 Q $300 Q $400 Q $500 Q $100 Q $100 Q $100 Q $100 Q $200 Q $200 Q $200 Q $200 Q $300

Jeopardy Multiplying Fractions Dividing Fractions Word Problems Financial Literacy 1 Financial Literacy 2 Q $100 Q $200 Q $300 Q $400 Q $500 Q $100 Q $100 Q $100 Q $100 Q $200 Q $200 Q $200 Q $200 Q $300

1 Week Recap Week 2

1 Week 3 1.1 Recap Week 2 pv, fv, timeline pmt - we don t have to keep it the same every period. Ex.: Suppose you are exactly 30 years old. You believe that you will be able to save for the next 20 years,

1 Week 3 1.1 Recap Week 2 pv, fv, timeline pmt - we don t have to keep it the same every period. Ex.: Suppose you are exactly 30 years old. You believe that you will be able to save for the next 20 years,

Financial Economics: Household Saving and Investment Decisions

Financial Economics: Household Saving and Investment Decisions Shuoxun Hellen Zhang WISE & SOE XIAMEN UNIVERSITY Oct, 2016 1 / 32 Outline 1 A Life-Cycle Model of Saving 2 Taking Account of Social Security

Financial Economics: Household Saving and Investment Decisions Shuoxun Hellen Zhang WISE & SOE XIAMEN UNIVERSITY Oct, 2016 1 / 32 Outline 1 A Life-Cycle Model of Saving 2 Taking Account of Social Security

AFM 271 Practice Problem Set #2 Spring 2005 Suggested Solutions

AFM 271 Practice Problem Set #2 Spring 2005 Suggested Solutions 1. Text Problems: 6.2 (a) Consider the following table: time cash flow cumulative cash flow 0 -$1,000,000 -$1,000,000 1 $150,000 -$850,000

AFM 271 Practice Problem Set #2 Spring 2005 Suggested Solutions 1. Text Problems: 6.2 (a) Consider the following table: time cash flow cumulative cash flow 0 -$1,000,000 -$1,000,000 1 $150,000 -$850,000

PRIME ACADEMY CAPITAL BUDGETING - 1 TIME VALUE OF MONEY THE EIGHT PRINCIPLES OF TIME VALUE

Capital Budgeting 11 CAPITAL BUDGETING - 1 Where should you put your money? In business you should put it in those assets that maximize wealth. How do you know that a project would maximize wealth? Enter

Capital Budgeting 11 CAPITAL BUDGETING - 1 Where should you put your money? In business you should put it in those assets that maximize wealth. How do you know that a project would maximize wealth? Enter

Interest and present value Simple Interest Interest amount = P x i x n p = principle i = interest rate n = number of periods Assume you invest $1,000 at 6% simple interest for 3 years. You would earn $180

Interest and present value Simple Interest Interest amount = P x i x n p = principle i = interest rate n = number of periods Assume you invest $1,000 at 6% simple interest for 3 years. You would earn $180

Exploring Microsoft Office Excel 2007 Comprehensive Grauer Scheeren Mulbery Second Edition

Exploring Microsoft Office Excel 2007 Comprehensive Grauer Scheeren Mulbery Second Edition Pearson Education Limited Edinburgh Gate Harlow Essex CM20 2JE England and Associated Companies throughout the

Exploring Microsoft Office Excel 2007 Comprehensive Grauer Scheeren Mulbery Second Edition Pearson Education Limited Edinburgh Gate Harlow Essex CM20 2JE England and Associated Companies throughout the

Mortgages & Equivalent Interest

Mortgages & Equivalent Interest A mortgage is a loan which you then pay back with equal payments at regular intervals. Thus a mortgage is an annuity! A down payment is a one time payment you make so that

Mortgages & Equivalent Interest A mortgage is a loan which you then pay back with equal payments at regular intervals. Thus a mortgage is an annuity! A down payment is a one time payment you make so that

10. Estimate the MIRR for the project described in Problem 8. Does it change your decision on accepting this project?

1 CHAPTER 5 Problems and Questions 1. You have been given the following information on a project: It has a five-year lifetime The initial investment in the project will be $25 million, and the investment

1 CHAPTER 5 Problems and Questions 1. You have been given the following information on a project: It has a five-year lifetime The initial investment in the project will be $25 million, and the investment

Chapter Outline. Problem Types. Key Concepts and Skills 8/27/2009. Discounted Cash Flow. Valuation CHAPTER

8/7/009 Slide CHAPTER Discounted Cash Flow 4 Valuation Chapter Outline 4.1 Valuation: The One-Period Case 4. The Multiperiod Case 4. Compounding Periods 4.4 Simplifications 4.5 What Is a Firm Worth? http://www.gsu.edu/~fnccwh/pdf/ch4jaffeoverview.pdf

8/7/009 Slide CHAPTER Discounted Cash Flow 4 Valuation Chapter Outline 4.1 Valuation: The One-Period Case 4. The Multiperiod Case 4. Compounding Periods 4.4 Simplifications 4.5 What Is a Firm Worth? http://www.gsu.edu/~fnccwh/pdf/ch4jaffeoverview.pdf

Name: Date: Period: MATH MODELS (DEC 2017) 1 st Semester Exam Review

1 st Semester Exam Review") Name: Date: Period: MATH MODELS (DEC 2017) 1 st Semester Exam Review Unit 1 Vocabulary: Match the following definitions to the words below. 1) Money charged on transactions that goes to fund state and

Name: Date: Period: MATH MODELS (DEC 2017) 1 st Semester Exam Review Unit 1 Vocabulary: Match the following definitions to the words below. 1) Money charged on transactions that goes to fund state and

Time Value of Money and Economic Equivalence

Time Value of Money and Economic Equivalence Lecture No.4 Chapter 3 Third Canadian Edition Copyright 2012 Chapter Opening Story Take a Lump Sum or Annual Installments q q q Millionaire Life is a lottery

Time Value of Money and Economic Equivalence Lecture No.4 Chapter 3 Third Canadian Edition Copyright 2012 Chapter Opening Story Take a Lump Sum or Annual Installments q q q Millionaire Life is a lottery

ANNUITIES AND AMORTISATION WORKSHOP

OBJECTIVE: 1. Able to calculate the present value of annuities 2. Able to calculate the future value of annuities 3. Able to complete an amortisation schedule TARGET: QMI1500 and BNU1501, any other modules

OBJECTIVE: 1. Able to calculate the present value of annuities 2. Able to calculate the future value of annuities 3. Able to complete an amortisation schedule TARGET: QMI1500 and BNU1501, any other modules

Fahmi Ben Abdelkader HEC, Paris Fall Students version 9/11/2012 7:50 PM 1

Financial Economics Time Value of Money Fahmi Ben Abdelkader HEC, Paris Fall 2012 Students version 9/11/2012 7:50 PM 1 Chapter Outline Time Value of Money: introduction Time Value of money Financial Decision

Financial Economics Time Value of Money Fahmi Ben Abdelkader HEC, Paris Fall 2012 Students version 9/11/2012 7:50 PM 1 Chapter Outline Time Value of Money: introduction Time Value of money Financial Decision

Future Value of Multiple Cash Flows

Future Value of Multiple Cash Flows FV t CF 0 t t r CF r... CF t You open a bank account today with $500. You expect to deposit $,000 at the end of each of the next three years. Interest rates are 5%,

Future Value of Multiple Cash Flows FV t CF 0 t t r CF r... CF t You open a bank account today with $500. You expect to deposit $,000 at the end of each of the next three years. Interest rates are 5%,

MATH 373 Fall 2016 Test 1 September27, 2016

MATH 373 Fall 2016 Test 1 September27, 2016 1. Ellie lends Aakish 10,000 to be repaid over the next three years with level annual payments of 4000. Ellie takes each payment and reinvests it at an annual

MATH 373 Fall 2016 Test 1 September27, 2016 1. Ellie lends Aakish 10,000 to be repaid over the next three years with level annual payments of 4000. Ellie takes each payment and reinvests it at an annual

Principles of Finance with Excel, 2 nd edition. Instructor materials. Chapter 2 Time Value of Money

Principles of Finance with Excel, 2 nd edition Instructor materials Chapter 2 Time Value of Money This chapter Future value Present value Net present value Internal rate of return Pension and savings plans

Principles of Finance with Excel, 2 nd edition Instructor materials Chapter 2 Time Value of Money This chapter Future value Present value Net present value Internal rate of return Pension and savings plans

RULE OF TIME VALUE OF MONEY

RULE OF TIME VALUE OF MONEY 1. CMPD : a. We can set our calculator either begin mode or end mode when we don t use pmt. We can say that in case of using n, I, pv, fv, c/y we can set out calculator either

RULE OF TIME VALUE OF MONEY 1. CMPD : a. We can set our calculator either begin mode or end mode when we don t use pmt. We can say that in case of using n, I, pv, fv, c/y we can set out calculator either

Format: True/False. Learning Objective: LO 3

Parrino/Fundamentals of Corporate Finance, Test Bank, Chapter 6 1.Calculating the present and future values of multiple cash flows is relevant only for individual investors. 2.Calculating the present and

Parrino/Fundamentals of Corporate Finance, Test Bank, Chapter 6 1.Calculating the present and future values of multiple cash flows is relevant only for individual investors. 2.Calculating the present and

MTH302- Business Mathematics

MIDTERM EXAMINATION MTH302- Business Mathematics Question No: 1 ( Marks: 1 ) - Please choose one Store A marked down a $ 50 perfume to $ 40 with markdown of $10 The % Markdown is 10% 20% 30% 40% Question

MIDTERM EXAMINATION MTH302- Business Mathematics Question No: 1 ( Marks: 1 ) - Please choose one Store A marked down a $ 50 perfume to $ 40 with markdown of $10 The % Markdown is 10% 20% 30% 40% Question

The time value of money and cash-flow valuation

The time value of money and cash-flow valuation Readings: Ross, Westerfield and Jordan, Essentials of Corporate Finance, Chs. 4 & 5 Ch. 4 problems: 13, 16, 19, 20, 22, 25. Ch. 5 problems: 14, 15, 31, 32,

The time value of money and cash-flow valuation Readings: Ross, Westerfield and Jordan, Essentials of Corporate Finance, Chs. 4 & 5 Ch. 4 problems: 13, 16, 19, 20, 22, 25. Ch. 5 problems: 14, 15, 31, 32,

Lesson TVM xx. Present Value Annuity Due

Lesson TVM-10-060-xx Present Value Annuity Due This workbook contains notes and worksheets to accompany the corresponding video lesson available online at: Permission is granted for educators and students

Lesson TVM-10-060-xx Present Value Annuity Due This workbook contains notes and worksheets to accompany the corresponding video lesson available online at: Permission is granted for educators and students

January 29. Annuities

January 29 Annuities An annuity is a repeating payment, typically of a fixed amount, over a period of time. An annuity is like a loan in reverse; rather than paying a loan company, a bank or investment

January 29 Annuities An annuity is a repeating payment, typically of a fixed amount, over a period of time. An annuity is like a loan in reverse; rather than paying a loan company, a bank or investment

ACF719 Financial Management

ACF719 Financial Management Bonds and bond management Reading: BEF chapter 5 Topics Key features of bonds Bond valuation and yield Assessing risk 2 1 Key features of bonds Bonds are relevant to the financing

ACF719 Financial Management Bonds and bond management Reading: BEF chapter 5 Topics Key features of bonds Bond valuation and yield Assessing risk 2 1 Key features of bonds Bonds are relevant to the financing

Understanding Interest Rates

Money & Banking Notes Chapter 4 Understanding Interest Rates Measuring Interest Rates Present Value (PV): A dollar paid to you one year from now is less valuable than a dollar paid to you today. Why? -

Money & Banking Notes Chapter 4 Understanding Interest Rates Measuring Interest Rates Present Value (PV): A dollar paid to you one year from now is less valuable than a dollar paid to you today. Why? -

HPM Module_6_Capital_Budgeting_Exercise

HPM Module_6_Capital_Budgeting_Exercise OK, class, welcome back. We are going to do our tutorial on the capital budgeting module. And we've got two worksheets that we're going to look at today. We have

HPM Module_6_Capital_Budgeting_Exercise OK, class, welcome back. We are going to do our tutorial on the capital budgeting module. And we've got two worksheets that we're going to look at today. We have

MTH 302,QUIZES BY CH SALMAN RASUL JATTALA

The amount added to a cost to arrive at a selling price is Markup margin both markup & margin Mth302 - Business Mathematics (Online quiz # 1) 1 percent on cost At break even point, the company has a positive

The amount added to a cost to arrive at a selling price is Markup margin both markup & margin Mth302 - Business Mathematics (Online quiz # 1) 1 percent on cost At break even point, the company has a positive