Lesson TVM xx. Present Value Annuity Due

|

|

|

- Owen Fields

- 6 years ago

- Views:

Transcription

1 Lesson TVM xx Present Value Annuity Due This workbook contains notes and worksheets to accompany the corresponding video lesson available online at: Permission is granted for educators and students to make copies and redistribute this document without fee provided the copyright notice and page footer is retained. All other intellectual property rights are reserved by the copyright holder. Copyright 2011 by Rocky Spears Enterprises LLC, All Rights Reserved Page 1 of 26

2 Corrections Subsequent to the production of these videos in July 2010, we re-structured and renumbered them to be consistent with a structure that emerged from our later work in which the last two digits of our numbering scheme represents part 1, part 2, part3, etc. of a lesson. This allows us to break lessons into shorter related subsets easier for you as viewer to manage. We re-edited the videos to refer to the new number structure. However, there may be some references to lesson numbers in the videos that still refer to the old numbering scheme. If so, please alert us so that we can correct that in a future release. For your convenience, the numbering systems are as follows: OLD NUMBER SCHEME NEW NUMBER SCHEME TOPIC TVM TVM xx TVM Part 1 TVM Part 2 Future Value of a Single Sum TVM TVM xx TVM Part 1 TVM Part 2 Future Value of an Ordinary Annuity TVM TVM xx TVM Part 1 TVM Part 2 Present Value of a Single Sum TVM TVM xx TVM Part 1 TVM Part 2 Present Value of an Ordinary Annuity TVM TVM xx TVM Part 1 TVM Part 2 Future Value of an Annuity Due TVM TVM xx TVM Part 1 TVM Part 2 Present Value of an Annuity Due We apologize for any confusion this may cause. Copyright 2011 by Rocky Spears Enterprises LLC, All Rights Reserved Page 2 of 26

3 Time Value of Money - Present Value - Annuity Due - Part 1 [Clip 01] Annuity Due Concept Pre-requisites Understand the concepts of future value of a single sum and present value of a single sum. These are covered in Lesson TVM Present Value Single Sum. We will assume you understand the concepts and problems from this earlier lesson and we will refer to prior examples as we study the present value of an Annuity Due. Recommended Understand the concepts of present value of an ordinary annuity covered in Lesson TVM Present Value Ordinary Annuity. The relationship between an ordinary annuity and an annuity due is explained in this lesson and provides an intuitive understanding that otherwise might be not be understood. However, this relationship is not essential to understanding an annuity due, so you do not have to watch the lesson on ordinary annuities to understand this lesson. Objectives: 1. Annuity Due concept 2. Present value of an Annuity Due formula, tables, financial calculator 3. Solve present value of an Annuity Due problems 4. Solve combination problems involving present value of a single sum and present value of an annuity due Concept of an Annuity Due Copyright 2011 by Rocky Spears Enterprises LLC, All Rights Reserved Page 3 of 26

4 In this lesson we study how to determine the present value of an annuity due. An annuity is a cash payment or a cash receipt that occurs at equal intervals (periods) for a number of intervals (periods). The intervals can be years, semiannual periods, quarterly periods, monthly periods, etc. An annuity amount can be fixed, that is, the same each period, or it can be variable. Our interest in this lesson is a fixed annuity amount, because we have special procedures to determine the present value of a fixed annuity. A variable annuity problem is solved using a combination of fixed annuity and single sum procedures. An annuity due is one in which the cash payment or cash receipt occurs at the beginning of a period. This lesson will deal with that situation. Examples of annuities due include: 1. Lottery winnings in which periodic payments are made at the beginning of each period. 2. Retirement annuity payments in which periodic payments are made at the beginning of each period. 3. Insurance annuity payments in which periodic payments are made at the beginning of each period. 4. Lease or rent payments in which periodic payments are made at the beginning of each period. When the cash payment or cash receipt occurs at the end of each period, it is called an ordinary annuity. We study the present value of an ordinary annuity in Lesson TVM An example of an ordinary annuity is an installment loan in which loan payments occur at the end of each month from the point of view of the inception of the loan. Copyright 2011 by Rocky Spears Enterprises LLC, All Rights Reserved Page 4 of 26

5 Comparison of Time Value of Money Situations Period FV SS PV SS FV OA PV OA FV AD PV AD 0 - Today -PMT 0 -PV 0? -PV 0? -PV 0? or -PV 0 -PMT 1 +PMT 1 End of Period 1 -PMT 1 +PMT 1 -PMT 2 +PMT 2 End of Period 2 -PMT 2 +PMT 2 -PMT 3 +PMT 3 End of Period 3 -PMT 3 +PMT 3 +PMT n +FV n? or +FV n -PMT n-1 +PMT n-1 End of Period N -PMT n +FV n? +PMT n FV n? This table compares the cash flow streams for different time value of money situations. Notice how the column for present value of annuity due (PV AD ) differs from the present value of a single sum (PV SS ) and present value of an ordinary annuity (PV OA ). In the present value of a single sum, we typically know a future amount at the end of some future period, call it PMT n or FV n. We want to know the present value of that amount today at some discount rate, call it r. We are asking How much are we willing to pay today for a future amount? In present value of an ordinary annuity, we know a future amount that occurs at the end of every period from period 1 through period n. We want to know the present value of those amounts today at some discount rate, call it r. We are Copyright 2011 by Rocky Spears Enterprises LLC, All Rights Reserved Page 5 of 26

6 asking How much are we willing to pay today for a stream of future amounts that are the same each period? In present value of an annuity due, we know a future amount that occurs at the beginning of every period from period 1 through period n, which is also to say that the future amount occurs today, and at the end of every period from period 1 through n-1. We want to know the present value of those amounts today at some discount rate, call it r. We are asking How much are we willing to pay today for a stream of future amounts at the beginning of each period starting today that are the same each period? We can also turn this around a bit and ask If we have an amount today, call it PV 0, invested at a certain rate of return, r, what is the amount of the future payments we could receive at the beginning of each period starting today through period n? Another question we might ask is If we have an amount today, call it PV 0, and we want to have a certain periodic payment at the beginning of each period starting today for a certain number of periods n, what rate of return is required on that amount today? A final variation is If we have an amount today, call it PV 0, and we want to have a certain periodic payment at the beginning of each period starting today given a certain rate of return, for how many periods can the payment be made? Copyright 2011 by Rocky Spears Enterprises LLC, All Rights Reserved Page 6 of 26

7 Present Value of an Annuity Due Example Suppose you win a local lottery that will pay you either (1) $10,000 a year for three years starting now, or (2) the cash value of your winnings now assuming a 5% discount rate. How much is the cash value of your lottery winnings? Copyright 2011 by Rocky Spears Enterprises LLC, All Rights Reserved Page 7 of 26

![[Clip 02] Contrast an Annuity Due with an Ordinary Annuity [Clip 03] Present Value of an Annuity](/docs-images/71/66145734/images/8-2.jpg "Due Formula Part 1 Copyright 2011 by Rocky Spears Enterprises LLC, All Rights Reserved Page 8 of")

8 [Clip 02] Contrast an Annuity Due with an Ordinary Annuity [Clip 03] Present Value of an Annuity Due Formula Part 1 Copyright 2011 by Rocky Spears Enterprises LLC, All Rights Reserved Page 8 of 26

9 [Clip 04] Present Value of an Annuity Due Formula Part 2 Copyright 2011 by Rocky Spears Enterprises LLC, All Rights Reserved Page 9 of 26

![[Clip 05] Present Value of an Annuity Due of](/docs-images/71/66145734/images/10-0.jpg "$1 Table See Appendix 2 for the Present Value")

10 [Clip 05] Present Value of an Annuity Due of $1 Table See Appendix 2 for the Present Value Tables Used in this clip. [Clip 06] Present Value of an Annuity Due - Using the TI BA II Financial Calculator Copyright 2011 by Rocky Spears Enterprises LLC, All Rights Reserved Page 10 of 26

11 Copyright 2011 by Rocky Spears Enterprises LLC, All Rights Reserved Page 11 of 26

12 Time Value of Money - Present Value - Annuity Due - Part 2 [Clip 07] Problem 1 Annuity Due Solve for PV Problem 1 Annuity Due Solve for PV (see Appendix 1 for the Solution; see Appendix 2 for the Time Value of Money tables) Suppose you buy a factory building under a lease agreement that requires payments of $100,000 per year for 5 years occurring at the beginning of each year. At the end of the lease agreement ownership of the building transfers to your company. This is essentially a financing agreement to buy the factory building and is considered a capital lease. If the implied interest rate of this agreement is 8%, what is the present value of the lease payments (which is also the proper valuation of the acquisition cost of the building)? [Clip 08] Problem 2 Annuity Due Solve for N Problem 2 Annuity Due Solve for N (see Appendix 1 for the Solution; see Appendix 2 for the Time Value of Money tables) Suppose you have a lump sum of $220,000 in a retirement fund that earns 4% annually. Assume you are planning to retire immediately and determine you need at least $20,000 a year from the retirement fund starting now. How many years will the retirement fund be able to pay you $20,000 a year? Copyright 2011 by Rocky Spears Enterprises LLC, All Rights Reserved Page 12 of 26

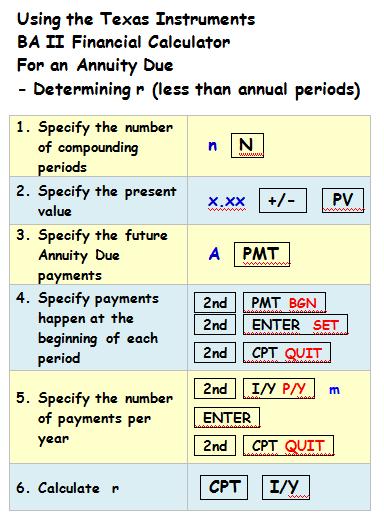

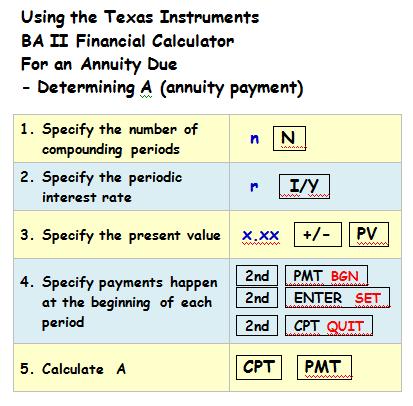

13 [Clip 09] Problem 3 Annuity Due Solve for r Problem 3 Annuity Due Solve for r (see Appendix 1 for the Solution; see Appendix 2 for the Time Value of Money tables) Suppose you have a lump sum of $220,000 in a retirement fund. Assume you are planning to retire immediately and determine you need at least $20,000 a year from the retirement fund starting now. What rate of return on the retirement fund is necessary in order for the fund to pay you $20,000 a year for 20 years? [Clip 10] Problem 4 Annuity Due Solve for A Problem 4 Annuity Due Solve for A (see Appendix 1 for the Solution; see Appendix 2 for the Time Value of Money tables) Suppose you have a lump sum of $220,000 in a retirement fund earning 5% annually. Assume you are planning to retire immediately. What is the maximum amount your retirement fund can pay you each year for 20 years starting now? [Clip 11] Problem 5 Annuity Due Pension Annuity vs. Lump Sum Analysis Problem 5 Annuity Due Pension Annuity vs. Lump Sum Analysis (see Appendix 1 for the Solution; see Appendix 2 for the Time Value of Money tables) Suppose you are retiring at age 65 and have a choice between accepting pension payments for the next 25 years of $50,000 annually starting now, versus a lump sum amount now of a $1,000,000. Assume your discount rate is 7%. Should you take the lump sum amount now? Copyright 2011 by Rocky Spears Enterprises LLC, All Rights Reserved Page 13 of 26

14 [Clip 12] Problem 6 Capital Lease - Combination Single Sum and Annuity Due Problem 6 Capital Lease - Combination Single Sum and Annuity Due (see Appendix 1 for the Solution; see Appendix 2 for the Time Value of Money tables) Suppose you are offered the opportunity to buy a new tractor for your farm with a market price of $40,000. The dealer offers to finance the tractor under a lease purchase agreement in which you must make annual payments of $5,000 beginning immediately, for six years with a balloon payment due at the end of six years of $20,000. How much are you paying for the tractor, assuming the appropriate implied interest rate is 5%? [Clip 13] Problem 7 Capital Lease Combination Single Sum and Annuity Due with annual compounding Problem 7 - Capital Lease Combination Single Sum and Annuity Due with annual compounding (see Appendix 1 for the Solution; see Appendix 2 for the Time Value of Money tables) Suppose you have the opportunity to lease some factory equipment under a capital lease agreement requiring annual lease payments of $60,000 at the beginning of each year of the lease for five years. At the end of the lease term, an additional payment is required of $90,000 as a guarantee on disposal of the equipment by the leasing company. If the implied interest rate is 9%, what is the present value of the capital lease? Copyright 2011 by Rocky Spears Enterprises LLC, All Rights Reserved Page 14 of 26

15 [Clip 14] Problem 8 Capital Lease Combination Single Sum and Annuity Due with monthly compounding Problem 8 - Capital Lease Combination Single Sum and Annuity Due with monthly compounding (see Appendix 1 for the Solution; see Appendix 2 for the Time Value of Money tables) Suppose you have the opportunity to lease some factory equipment under a capital lease agreement requiring monthly lease payments of $5,000 at the beginning of each month of the lease for two years. At the end of the lease term, an additional payment is required of $10,000 as a guarantee on disposal of the equipment by the leasing company. If the implied interest rate is 12%, what is the present value of the capital lease? Copyright 2011 by Rocky Spears Enterprises LLC, All Rights Reserved Page 15 of 26

![APPENDIX 1 - SOLUTIONS [Clip 07] Problem 1 Annuity](/docs-images/71/66145734/images/16-2.jpg "Due Solve for PV SOLUTION: [Clip 08] Problem 2")

16 APPENDIX 1 - SOLUTIONS [Clip 07] Problem 1 Annuity Due Solve for PV SOLUTION: [Clip 08] Problem 2 Annuity Due Solve for N SOLUTION: Copyright 2011 by Rocky Spears Enterprises LLC, All Rights Reserved Page 16 of 26

![[Clip 09] Problem 3 Annuity Due Solve for r](/docs-images/71/66145734/images/17-2.jpg "SOLUTION: [Clip 10] Problem 4 Annuity Due Solve")

17 [Clip 09] Problem 3 Annuity Due Solve for r SOLUTION: [Clip 10] Problem 4 Annuity Due Solve for A SOLUTION: Copyright 2011 by Rocky Spears Enterprises LLC, All Rights Reserved Page 17 of 26

![[Clip 11] Problem 5 Pension Annuity vs.](/docs-images/71/66145734/images/18-1.jpg "Lump Sum Analysis Annuity Due SOLUTION: PROBLEM 6 IS ON THE NEXT PAGE Copyright 2011 by Rocky")

18 [Clip 11] Problem 5 Pension Annuity vs. Lump Sum Analysis Annuity Due SOLUTION: PROBLEM 6 IS ON THE NEXT PAGE Copyright 2011 by Rocky Spears Enterprises LLC, All Rights Reserved Page 18 of 26

![[Clip 12] Problem 6 Combination](/docs-images/71/66145734/images/19-1.jpg "Single Sum and Annuity Due SOLUTION:")

19 [Clip 12] Problem 6 Combination Single Sum and Annuity Due SOLUTION: Copyright 2011 by Rocky Spears Enterprises LLC, All Rights Reserved Page 19 of 26

![[Clip 13] Problem 7 Capital Lease Combination Single Sum and Annuity Due](/docs-images/71/66145734/images/20-2.jpg "with annual compounding SOLUTION: [Clip 14] Problem 8 Capital Lease")

20 [Clip 13] Problem 7 Capital Lease Combination Single Sum and Annuity Due with annual compounding SOLUTION: [Clip 14] Problem 8 Capital Lease Combination Single Sum and Annuity Due with monthly compounding SOLUTION: Copyright 2011 by Rocky Spears Enterprises LLC, All Rights Reserved Page 20 of 26

21 APPENDIX 2 - FUTURE VALUE AND PRESENT VALUE TABLES Table 1. Future Value of a Single Sum of $1 (Cash Flow or Payment Occurs the Beginning of the Period) 1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 11% 12% 13% 14% 15% Copyright 2011 by Rocky Spears Enterprises LLC, All Rights Reserved Page 21 of 26

22 Table 2. Future Value of an Ordinary Annuity of $1 (Cash Flows or Payments Occurs at the End of Each Period) 1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 11% 12% 13% 14% 15% Copyright 2011 by Rocky Spears Enterprises LLC, All Rights Reserved Page 22 of 26

23 Table 3. Present Value of a Single Sum of $1 (Cash Flow or Payment Occurs the End of the Period) 1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 11% 12% 13% 14% 15% Copyright 2011 by Rocky Spears Enterprises LLC, All Rights Reserved Page 23 of 26

24 Table 4. Present Value of an Ordinary Annuity of $1 (Cash Flows or Payments Occur at the End of Each Period) 1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 11% 12% 13% 14% 15% Copyright 2011 by Rocky Spears Enterprises LLC, All Rights Reserved Page 24 of 26

25 Table 5. Future Value of an Annuity Due of $1 (Cash Flows or Payments Occur at the Beginning of the Period) 1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 11% 12% 13% 14% 15% Copyright 2011 by Rocky Spears Enterprises LLC, All Rights Reserved Page 25 of 26

26 Table 6. Present Value of an Annuity Due of $1 (Cash Flows or Payments Occur at the Beginning of Each Period) 1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 11% 12% 13% 14% 15% Copyright 2011 by Rocky Spears Enterprises LLC, All Rights Reserved Page 26 of 26

Lesson FA xx Capital Budgeting Part 2C

- - - - - - Cover Page - - - - - - Lesson FA-20-170-xx Capital Budgeting Part 2C These notes and worksheets accompany the corresponding video lesson available online at: Permission is granted for educators

- - - - - - Cover Page - - - - - - Lesson FA-20-170-xx Capital Budgeting Part 2C These notes and worksheets accompany the corresponding video lesson available online at: Permission is granted for educators

Lesson FA Financial Accounting Fundamentals - Closing Entries and Post-Closing Trial Balance Part 1

Lesson FA-10-040-01 Financial Accounting Fundamentals - Closing Entries and Post-Closing Trial Balance Part 1 This workbook contains notes and worksheets to accompany the corresponding video lesson available

Lesson FA-10-040-01 Financial Accounting Fundamentals - Closing Entries and Post-Closing Trial Balance Part 1 This workbook contains notes and worksheets to accompany the corresponding video lesson available

Lesson FA Financial Accounting Fundamentals - Concepts and Transaction Analysis Part 3

Lesson FA-10-010-03 Financial Accounting Fundamentals - Concepts and Transaction Analysis Part 3 This workbook contains notes and worksheets to accompany the corresponding video lesson available online

Lesson FA-10-010-03 Financial Accounting Fundamentals - Concepts and Transaction Analysis Part 3 This workbook contains notes and worksheets to accompany the corresponding video lesson available online

3. Time value of money. We will review some tools for discounting cash flows.

1 3. Time value of money We will review some tools for discounting cash flows. Simple interest 2 With simple interest, the amount earned each period is always the same: i = rp o where i = interest earned

1 3. Time value of money We will review some tools for discounting cash flows. Simple interest 2 With simple interest, the amount earned each period is always the same: i = rp o where i = interest earned

3. Time value of money

1 Simple interest 2 3. Time value of money With simple interest, the amount earned each period is always the same: i = rp o We will review some tools for discounting cash flows. where i = interest earned

1 Simple interest 2 3. Time value of money With simple interest, the amount earned each period is always the same: i = rp o We will review some tools for discounting cash flows. where i = interest earned

Time Value of Money. Ex: How much a bond, which can be cashed out in 2 years, is worth today

Time Value of Money The time value of money is the idea that money available now is worth more than the same amount in the future - this is essentially why interest exists. Present value is the current

Time Value of Money The time value of money is the idea that money available now is worth more than the same amount in the future - this is essentially why interest exists. Present value is the current

6.1 Simple and Compound Interest

6.1 Simple and Compound Interest If P dollars (called the principal or present value) earns interest at a simple interest rate of r per year (as a decimal) for t years, then Interest: I = P rt Accumulated

6.1 Simple and Compound Interest If P dollars (called the principal or present value) earns interest at a simple interest rate of r per year (as a decimal) for t years, then Interest: I = P rt Accumulated

1) Cash Flow Pattern Diagram for Future Value and Present Value of Irregular Cash Flows

Cash Flow Pattern Diagram for Future Value and Present Value of Irregular Cash Flows") Topics Excel & Business Math Video/Class Project #45 Cash Flow Analysis for Annuities: Savings Plans, Asset Valuation, Retirement Plans and Mortgage Loan. FV, PV and PMT. 1) Cash Flow Pattern Diagram for

Topics Excel & Business Math Video/Class Project #45 Cash Flow Analysis for Annuities: Savings Plans, Asset Valuation, Retirement Plans and Mortgage Loan. FV, PV and PMT. 1) Cash Flow Pattern Diagram for

Chapter 2 Applying Time Value Concepts

Chapter 2 Applying Time Value Concepts Chapter Overview Albert Einstein, the renowned physicist whose theories of relativity formed the theoretical base for the utilization of atomic energy, called the

Chapter 2 Applying Time Value Concepts Chapter Overview Albert Einstein, the renowned physicist whose theories of relativity formed the theoretical base for the utilization of atomic energy, called the

FinQuiz Notes

Reading 6 The Time Value of Money Money has a time value because a unit of money received today is worth more than a unit of money to be received tomorrow. Interest rates can be interpreted in three ways.

Reading 6 The Time Value of Money Money has a time value because a unit of money received today is worth more than a unit of money to be received tomorrow. Interest rates can be interpreted in three ways.

Lesson 39 Appendix I Section 5.6 (part 1)

") Lesson 39 Appendix I Section 5.6 (part 1) Any of you who are familiar with financial plans or retirement investments know about annuities. An annuity is a plan involving payments made at regular intervals.

Lesson 39 Appendix I Section 5.6 (part 1) Any of you who are familiar with financial plans or retirement investments know about annuities. An annuity is a plan involving payments made at regular intervals.

Chapter 2 Applying Time Value Concepts

Chapter 2 Applying Time Value Concepts Chapter Overview Albert Einstein, the renowned physicist whose theories of relativity formed the theoretical base for the utilization of atomic energy, called the

Chapter 2 Applying Time Value Concepts Chapter Overview Albert Einstein, the renowned physicist whose theories of relativity formed the theoretical base for the utilization of atomic energy, called the

Simple Interest. Simple Interest is the money earned (or owed) only on the borrowed. Balance that Interest is Calculated On

only on the borrowed. Balance that Interest is Calculated On") MCR3U Unit 8: Financial Applications Lesson 1 Date: Learning goal: I understand simple interest and can calculate any value in the simple interest formula. Simple Interest is the money earned (or owed)

MCR3U Unit 8: Financial Applications Lesson 1 Date: Learning goal: I understand simple interest and can calculate any value in the simple interest formula. Simple Interest is the money earned (or owed)

PREVIEW OF CHAPTER 6-2

6-1 PREVIEW OF CHAPTER 6 6-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 6 Accounting and the Time Value of Money LEARNING OBJECTIVES After studying this chapter, you should

6-1 PREVIEW OF CHAPTER 6 6-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 6 Accounting and the Time Value of Money LEARNING OBJECTIVES After studying this chapter, you should

Chapter 6. Learning Objectives. Principals Applies in this Chapter. Time Value of Money

Chapter 6 Time Value of Money 1 Learning Objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate the present and future values of each. 2. Calculate the present value of

Chapter 6 Time Value of Money 1 Learning Objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate the present and future values of each. 2. Calculate the present value of

Chapter 3 Mathematics of Finance

Chapter 3 Mathematics of Finance Section R Review Important Terms, Symbols, Concepts 3.1 Simple Interest Interest is the fee paid for the use of a sum of money P, called the principal. Simple interest

Chapter 3 Mathematics of Finance Section R Review Important Terms, Symbols, Concepts 3.1 Simple Interest Interest is the fee paid for the use of a sum of money P, called the principal. Simple interest

Enhanced Instructional Transition Guide

Enhanced Instructional Transition Guide High School Courses/Mathematical Models with Applications Unit 13: Suggested Duration: 5 days Unit 13: Financial Planning (5 days) Possible Lesson 01 (5 days) POSSIBLE

Enhanced Instructional Transition Guide High School Courses/Mathematical Models with Applications Unit 13: Suggested Duration: 5 days Unit 13: Financial Planning (5 days) Possible Lesson 01 (5 days) POSSIBLE

CHAPTER 4 TIME VALUE OF MONEY

CHAPTER 4 TIME VALUE OF MONEY 1 Learning Outcomes LO.1 Identify various types of cash flow patterns (streams) seen in business. LO.2 Compute the future value of different cash flow streams. Explain the

CHAPTER 4 TIME VALUE OF MONEY 1 Learning Outcomes LO.1 Identify various types of cash flow patterns (streams) seen in business. LO.2 Compute the future value of different cash flow streams. Explain the

The TVM Solver. When you input four of the first five variables in the list above, the TVM Solver solves for the fifth variable.

1 The TVM Solver The TVM Solver is an application on the TI-83 Plus graphing calculator. It displays the timevalue-of-money (TVM) variables used in solving finance problems. Prior to using the TVM Solver,

1 The TVM Solver The TVM Solver is an application on the TI-83 Plus graphing calculator. It displays the timevalue-of-money (TVM) variables used in solving finance problems. Prior to using the TVM Solver,

F.3 - Annuities and Sinking Funds

F.3 - Annuities and Sinking Funds Math 166-502 Blake Boudreaux Department of Mathematics Texas A&M University March 22, 2018 Blake Boudreaux (TAMU) F.3 - Annuities March 22, 2018 1 / 12 Objectives Know

F.3 - Annuities and Sinking Funds Math 166-502 Blake Boudreaux Department of Mathematics Texas A&M University March 22, 2018 Blake Boudreaux (TAMU) F.3 - Annuities March 22, 2018 1 / 12 Objectives Know

Math 147 Section 6.4. Application Example

Math 147 Section 6.4 Present Value of Annuities 1 Application Example Suppose an individual makes an initial investment of $1500 in an account that earns 8.4%, compounded monthly, and makes additional

Math 147 Section 6.4 Present Value of Annuities 1 Application Example Suppose an individual makes an initial investment of $1500 in an account that earns 8.4%, compounded monthly, and makes additional

Chapter 2 Applying Time Value Concepts

Chapter 2 Applying Time Value Concepts Chapter Overview Albert Einstein, the renowned physicist whose theories of relativity formed the theoretical base for the utilization of atomic energy, called the

Chapter 2 Applying Time Value Concepts Chapter Overview Albert Einstein, the renowned physicist whose theories of relativity formed the theoretical base for the utilization of atomic energy, called the

บทท 3 ม ลค าของเง นตามเวลา (Time Value of Money)

") บทท 3 ม ลค าของเง นตามเวลา (Time Value of Money) Topic Coverage: The Interest Rate Simple Interest Rate Compound Interest Rate Amortizing a Loan Compounding Interest More Than Once per Year The Time Value

บทท 3 ม ลค าของเง นตามเวลา (Time Value of Money) Topic Coverage: The Interest Rate Simple Interest Rate Compound Interest Rate Amortizing a Loan Compounding Interest More Than Once per Year The Time Value

Time Value of Money, Part 5 Present Value aueof An Annuity. Learning Outcomes. Present Value

Time Value of Money, Part 5 Present Value aueof An Annuity Intermediate Accounting I Dr. Chula King 1 Learning Outcomes The concept of present value Present value of an annuity Ordinary annuity versus

Time Value of Money, Part 5 Present Value aueof An Annuity Intermediate Accounting I Dr. Chula King 1 Learning Outcomes The concept of present value Present value of an annuity Ordinary annuity versus

CP:

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 6-1 6-2 PREVIEW OF CHAPTER 6 6-3

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 6-1 6-2 PREVIEW OF CHAPTER 6 6-3

Unit 9 Financial Mathematics: Borrowing Money. Chapter 10 in Text

Unit 9 Financial Mathematics: Borrowing Money Chapter 10 in Text 9.1 Analyzing Loans Simple vs. Compound Interest Simple Interest: the amount of interest that you pay on a loan is calculated ONLY based

Unit 9 Financial Mathematics: Borrowing Money Chapter 10 in Text 9.1 Analyzing Loans Simple vs. Compound Interest Simple Interest: the amount of interest that you pay on a loan is calculated ONLY based

Unit 9 Financial Mathematics: Borrowing Money. Chapter 10 in Text

Unit 9 Financial Mathematics: Borrowing Money Chapter 10 in Text 9.1 Analyzing Loans Simple vs. Compound Interest Simple Interest: the amount of interest that you pay on a loan is calculated ONLY based

Unit 9 Financial Mathematics: Borrowing Money Chapter 10 in Text 9.1 Analyzing Loans Simple vs. Compound Interest Simple Interest: the amount of interest that you pay on a loan is calculated ONLY based

Time Value of Money. Chapter 5 & 6 Financial Calculator and Examples. Five Factors in TVM. Annual &Non-annual Compound

Chapter 5 & 6 Financial Calculator and Examples Konan Chan Financial Management, Fall 2018 Time Value of Money N: number of compounding periods I/Y: periodic rate (I/Y = APR/m) PV: present value PMT: periodic

Chapter 5 & 6 Financial Calculator and Examples Konan Chan Financial Management, Fall 2018 Time Value of Money N: number of compounding periods I/Y: periodic rate (I/Y = APR/m) PV: present value PMT: periodic

Math 166: Topics in Contemporary Mathematics II

Math 166: Topics in Contemporary Mathematics II Xin Ma Texas A&M University October 28, 2017 Xin Ma (TAMU) Math 166 October 28, 2017 1 / 10 TVM Solver on the Calculator Unlike simple interest, it is much

Math 166: Topics in Contemporary Mathematics II Xin Ma Texas A&M University October 28, 2017 Xin Ma (TAMU) Math 166 October 28, 2017 1 / 10 TVM Solver on the Calculator Unlike simple interest, it is much

Copyright 2015 by the McGraw-Hill Education (Asia). All rights reserved.

. All rights reserved.") Copyright 2015 by the McGraw-Hill Education (Asia). All rights reserved. Key Concepts and Skills Be able to compute the future value of multiple cash flows Be able to compute the present value of multiple

Copyright 2015 by the McGraw-Hill Education (Asia). All rights reserved. Key Concepts and Skills Be able to compute the future value of multiple cash flows Be able to compute the present value of multiple

Annuities and Income Streams

Annuities and Income Streams MATH 151 Calculus for Management J. Robert Buchanan Department of Mathematics Summer 212 Objectives After completing this lesson we will be able to: determine the value of

Annuities and Income Streams MATH 151 Calculus for Management J. Robert Buchanan Department of Mathematics Summer 212 Objectives After completing this lesson we will be able to: determine the value of

Capital Leases I: Present and Future Value

Spreadsheet Models for Managers 9/1 Session 9 Capital Leases I: Present and Future Value Worksheet Functions Non-Uniform Payments Last revised: July 6, 2011 Review of last time: Financial Models 9/2 Three

Spreadsheet Models for Managers 9/1 Session 9 Capital Leases I: Present and Future Value Worksheet Functions Non-Uniform Payments Last revised: July 6, 2011 Review of last time: Financial Models 9/2 Three

Sample Investment Device CD (Certificate of Deposit) Savings Account Bonds Loans for: Car House Start a business

Savings Account Bonds Loans for: Car House Start a business") Simple and Compound Interest (Young: 6.1) In this Lecture: 1. Financial Terminology 2. Simple Interest 3. Compound Interest 4. Important Formulas of Finance 5. From Simple to Compound Interest 6. Examples

Simple and Compound Interest (Young: 6.1) In this Lecture: 1. Financial Terminology 2. Simple Interest 3. Compound Interest 4. Important Formulas of Finance 5. From Simple to Compound Interest 6. Examples

Chapter 5. Learning Objectives. Principals Applied in this Chapter. Time Value of Money. Principle 1: Money Has a Time Value.

Chapter 5 Time Value of Money Learning Objectives 1. Construct cash flow timelines to organize your analysis of problems involving the time value of money. 2. Understand compounding and calculate the future

Chapter 5 Time Value of Money Learning Objectives 1. Construct cash flow timelines to organize your analysis of problems involving the time value of money. 2. Understand compounding and calculate the future

Chapter 5. Time Value of Money

Chapter 5 Time Value of Money Using Timelines to Visualize Cashflows A timeline identifies the timing and amount of a stream of payments both cash received and cash spent - along with the interest rate

Chapter 5 Time Value of Money Using Timelines to Visualize Cashflows A timeline identifies the timing and amount of a stream of payments both cash received and cash spent - along with the interest rate

Chapter 5 & 6 Financial Calculator and Examples

Chapter 5 & 6 Financial Calculator and Examples Konan Chan Financial Management, Fall 2018 Five Factors in TVM Present value: PV Future value: FV Discount rate: r Payment: PMT Number of periods: N Get

Chapter 5 & 6 Financial Calculator and Examples Konan Chan Financial Management, Fall 2018 Five Factors in TVM Present value: PV Future value: FV Discount rate: r Payment: PMT Number of periods: N Get

Lecture 3. Chapter 4: Allocating Resources Over Time

Lecture 3 Chapter 4: Allocating Resources Over Time 1 Introduction: Time Value of Money (TVM) $20 today is worth more than the expectation of $20 tomorrow because: a bank would pay interest on the $20

Lecture 3 Chapter 4: Allocating Resources Over Time 1 Introduction: Time Value of Money (TVM) $20 today is worth more than the expectation of $20 tomorrow because: a bank would pay interest on the $20

Chapter Review Problems

Chapter Review Problems Unit 9. Time-value-of-money terminology For Problems 9, assume you deposit $,000 today in a savings account. You earn 5% compounded quarterly. You deposit an additional $50 each

Chapter Review Problems Unit 9. Time-value-of-money terminology For Problems 9, assume you deposit $,000 today in a savings account. You earn 5% compounded quarterly. You deposit an additional $50 each

Solutions to Questions - Chapter 3 Mortgage Loan Foundations: The Time Value of Money

Solutions to Questions - Chapter 3 Mortgage Loan Foundations: The Time Value of Money Question 3-1 What is the essential concept in understanding compound interest? The concept of earning interest on interest

Solutions to Questions - Chapter 3 Mortgage Loan Foundations: The Time Value of Money Question 3-1 What is the essential concept in understanding compound interest? The concept of earning interest on interest

The Regular Payment of an Annuity with technology

UNIT 7 Annuities Date Lesson Text TOPIC Homework Dec. 7 7.1 7.1 The Amount of an Annuity with technology Pg. 415 # 1 3, 5 7, 12 **check answers withti-83 Dec. 9 7.2 7.2 The Present Value of an Annuity

UNIT 7 Annuities Date Lesson Text TOPIC Homework Dec. 7 7.1 7.1 The Amount of an Annuity with technology Pg. 415 # 1 3, 5 7, 12 **check answers withti-83 Dec. 9 7.2 7.2 The Present Value of an Annuity

CHAPTER 6. Accounting and the Time Value of Money. 2. Use of tables. 13, a. Unknown future amount. 7, 19 1, 5, 13 2, 3, 4, 7

CHAPTER 6 Accounting and the Time Value of Money ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems 1. Present value concepts. 1, 2, 3, 4, 5, 9, 17 2. Use of

CHAPTER 6 Accounting and the Time Value of Money ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems 1. Present value concepts. 1, 2, 3, 4, 5, 9, 17 2. Use of

Session 1, Monday, April 8 th (9:45-10:45)

") Session 1, Monday, April 8 th (9:45-10:45) Time Value of Money and Capital Budgeting v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Time Value of Money:

Session 1, Monday, April 8 th (9:45-10:45) Time Value of Money and Capital Budgeting v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Time Value of Money:

Principles of Corporate Finance

Principles of Corporate Finance Professor James J. Barkocy Time is money really McGraw-Hill/Irwin Copyright 2015 by The McGraw-Hill Companies, Inc. All rights reserved. Time Value of Money Money has a

Principles of Corporate Finance Professor James J. Barkocy Time is money really McGraw-Hill/Irwin Copyright 2015 by The McGraw-Hill Companies, Inc. All rights reserved. Time Value of Money Money has a

REVIEW MATERIALS FOR REAL ESTATE FUNDAMENTALS

REVIEW MATERIALS FOR REAL ESTATE FUNDAMENTALS 1997, Roy T. Black J. Andrew Hansz, Ph.D., CFA REAE 3325, Fall 2005 University of Texas, Arlington Department of Finance and Real Estate CONTENTS ITEM ANNUAL

REVIEW MATERIALS FOR REAL ESTATE FUNDAMENTALS 1997, Roy T. Black J. Andrew Hansz, Ph.D., CFA REAE 3325, Fall 2005 University of Texas, Arlington Department of Finance and Real Estate CONTENTS ITEM ANNUAL

The three formulas we use most commonly involving compounding interest n times a year are

Section 6.6 and 6.7 with finance review questions are included in this document for your convenience for studying for quizzes and exams for Finance Calculations for Math 11. Section 6.6 focuses on identifying

Section 6.6 and 6.7 with finance review questions are included in this document for your convenience for studying for quizzes and exams for Finance Calculations for Math 11. Section 6.6 focuses on identifying

AFP Financial Planning & Analysis Learning System Session 1, Monday, April 3 rd (9:45-10:45) Time Value of Money and Capital Budgeting

Time Value of Money and Capital Budgeting") AFP Financial Planning & Analysis Learning System Session 1, Monday, April 3 rd (9:45-10:45) Time Value of Money and Capital Budgeting Chapters Covered Time Value of Money: Part I, Domain B Chapter 6 Net

AFP Financial Planning & Analysis Learning System Session 1, Monday, April 3 rd (9:45-10:45) Time Value of Money and Capital Budgeting Chapters Covered Time Value of Money: Part I, Domain B Chapter 6 Net

Chapter 03 - Basic Annuities

3-1 Chapter 03 - Basic Annuities Section 3.0 - Sum of a Geometric Sequence The form for the sum of a geometric sequence is: Sum(n) a + ar + ar 2 + ar 3 + + ar n 1 Here a = (the first term) n = (the number

3-1 Chapter 03 - Basic Annuities Section 3.0 - Sum of a Geometric Sequence The form for the sum of a geometric sequence is: Sum(n) a + ar + ar 2 + ar 3 + + ar n 1 Here a = (the first term) n = (the number

Section Compound Interest

Section 5.1 - Compound Interest Simple Interest Formulas If I denotes the interest on a principal P (in dollars) at an interest rate of r (as a decimal) per year for t years, then we have: Interest: Accumulated

Section 5.1 - Compound Interest Simple Interest Formulas If I denotes the interest on a principal P (in dollars) at an interest rate of r (as a decimal) per year for t years, then we have: Interest: Accumulated

Using the Finance Menu of the TI-83/84/Plus calculators

Using the Finance Menu of the TI-83/84/Plus calculators To get to the FINANCE menu On the TI-83 press 2 nd x -1 On the TI-83, TI-83 Plus, TI-84, or TI-84 Plus press APPS and then select 1:FINANCE The FINANCE

Using the Finance Menu of the TI-83/84/Plus calculators To get to the FINANCE menu On the TI-83 press 2 nd x -1 On the TI-83, TI-83 Plus, TI-84, or TI-84 Plus press APPS and then select 1:FINANCE The FINANCE

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION Answers to Concepts Review and Critical Thinking Questions 1. Assuming positive cash flows and interest rates, the future value increases and the present value

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION Answers to Concepts Review and Critical Thinking Questions 1. Assuming positive cash flows and interest rates, the future value increases and the present value

Future Value of Multiple Cash Flows

Future Value of Multiple Cash Flows FV t CF 0 t t r CF r... CF t You open a bank account today with $500. You expect to deposit $,000 at the end of each of the next three years. Interest rates are 5%,

Future Value of Multiple Cash Flows FV t CF 0 t t r CF r... CF t You open a bank account today with $500. You expect to deposit $,000 at the end of each of the next three years. Interest rates are 5%,

Chapter 5. Finance 300 David Moore

Chapter 5 Finance 300 David Moore Time and Money This chapter is the first chapter on the most important skill in this course: how to move money through time. Timing is everything. The simple techniques

Chapter 5 Finance 300 David Moore Time and Money This chapter is the first chapter on the most important skill in this course: how to move money through time. Timing is everything. The simple techniques

Time Value of Money. All time value of money problems involve comparisons of cash flows at different dates.

Time Value of Money The time value of money is a very important concept in Finance. This section is aimed at giving you intuitive and hands-on training on how to price securities (e.g., stocks and bonds),

Time Value of Money The time value of money is a very important concept in Finance. This section is aimed at giving you intuitive and hands-on training on how to price securities (e.g., stocks and bonds),

SECTION 6.1: Simple and Compound Interest

1 SECTION 6.1: Simple and Compound Interest Chapter 6 focuses on and various financial applications of interest. GOAL: Understand and apply different types of interest. Simple Interest If a sum of money

1 SECTION 6.1: Simple and Compound Interest Chapter 6 focuses on and various financial applications of interest. GOAL: Understand and apply different types of interest. Simple Interest If a sum of money

The values in the TVM Solver are quantities involved in compound interest and annuities.

Texas Instruments Graphing Calculators have a built in app that may be used to compute quantities involved in compound interest, annuities, and amortization. For the examples below, we ll utilize the screens

Texas Instruments Graphing Calculators have a built in app that may be used to compute quantities involved in compound interest, annuities, and amortization. For the examples below, we ll utilize the screens

Sections F.1 and F.2- Simple and Compound Interest

Sections F.1 and F.2- Simple and Compound Interest Simple Interest Formulas If I denotes the interest on a principal P (in dollars) at an interest rate of r (as a decimal) per year for t years, then we

Sections F.1 and F.2- Simple and Compound Interest Simple Interest Formulas If I denotes the interest on a principal P (in dollars) at an interest rate of r (as a decimal) per year for t years, then we

The Time Value. The importance of money flows from it being a link between the present and the future. John Maynard Keynes

The Time Value of Money The importance of money flows from it being a link between the present and the future. John Maynard Keynes Get a Free $,000 Bond with Every Car Bought This Week! There is a car

The Time Value of Money The importance of money flows from it being a link between the present and the future. John Maynard Keynes Get a Free $,000 Bond with Every Car Bought This Week! There is a car

The time value of money and cash-flow valuation

The time value of money and cash-flow valuation Readings: Ross, Westerfield and Jordan, Essentials of Corporate Finance, Chs. 4 & 5 Ch. 4 problems: 13, 16, 19, 20, 22, 25. Ch. 5 problems: 14, 15, 31, 32,

The time value of money and cash-flow valuation Readings: Ross, Westerfield and Jordan, Essentials of Corporate Finance, Chs. 4 & 5 Ch. 4 problems: 13, 16, 19, 20, 22, 25. Ch. 5 problems: 14, 15, 31, 32,

Chapter 5. Interest Rates ( ) 6. % per month then you will have ( 1.005) = of 2 years, using our rule ( ) = 1.

6. % per month then you will have ( 1.005) = of 2 years, using our rule ( ) = 1.") Chapter 5 Interest Rates 5-. 6 a. Since 6 months is 24 4 So the equivalent 6 month rate is 4.66% = of 2 years, using our rule ( ) 4 b. Since one year is half of 2 years ( ).2 2 =.0954 So the equivalent

Chapter 5 Interest Rates 5-. 6 a. Since 6 months is 24 4 So the equivalent 6 month rate is 4.66% = of 2 years, using our rule ( ) 4 b. Since one year is half of 2 years ( ).2 2 =.0954 So the equivalent

Chapter Outline. Problem Types. Key Concepts and Skills 8/27/2009. Discounted Cash Flow. Valuation CHAPTER

8/7/009 Slide CHAPTER Discounted Cash Flow 4 Valuation Chapter Outline 4.1 Valuation: The One-Period Case 4. The Multiperiod Case 4. Compounding Periods 4.4 Simplifications 4.5 What Is a Firm Worth? http://www.gsu.edu/~fnccwh/pdf/ch4jaffeoverview.pdf

8/7/009 Slide CHAPTER Discounted Cash Flow 4 Valuation Chapter Outline 4.1 Valuation: The One-Period Case 4. The Multiperiod Case 4. Compounding Periods 4.4 Simplifications 4.5 What Is a Firm Worth? http://www.gsu.edu/~fnccwh/pdf/ch4jaffeoverview.pdf

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION Answers to Concept Questions 1. Assuming positive cash flows and interest rates, the future value increases and the present value decreases. 2. Assuming positive

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION Answers to Concept Questions 1. Assuming positive cash flows and interest rates, the future value increases and the present value decreases. 2. Assuming positive

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture 08 Present Value Welcome to the lecture series on Time

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture 08 Present Value Welcome to the lecture series on Time

Worksheet-2 Present Value Math I

What you will learn: Worksheet-2 Present Value Math I How to compute present and future values of single and annuity cash flows How to handle cash flow delays and combinations of cash flow streams How

What you will learn: Worksheet-2 Present Value Math I How to compute present and future values of single and annuity cash flows How to handle cash flow delays and combinations of cash flow streams How

Chapter. Chapter. Accounting and the Time Value of Money. Time Value of Money. Basic Time Value Concepts. Basic Time Value Concepts

Accounting and the Time Value Money 6 6-1 Prepared by Coby Harmon, University California, Santa Barbara Basic Time Value Concepts Time Value Money In accounting (and finance), the term indicates that a

Accounting and the Time Value Money 6 6-1 Prepared by Coby Harmon, University California, Santa Barbara Basic Time Value Concepts Time Value Money In accounting (and finance), the term indicates that a

Mathematics of Finance

CHAPTER 55 Mathematics of Finance PAMELA P. DRAKE, PhD, CFA J. Gray Ferguson Professor of Finance and Department Head of Finance and Business Law, James Madison University FRANK J. FABOZZI, PhD, CFA, CPA

CHAPTER 55 Mathematics of Finance PAMELA P. DRAKE, PhD, CFA J. Gray Ferguson Professor of Finance and Department Head of Finance and Business Law, James Madison University FRANK J. FABOZZI, PhD, CFA, CPA

Section 5.1 Simple and Compound Interest

Section 5.1 Simple and Compound Interest Question 1 What is simple interest? Question 2 What is compound interest? Question 3 - What is an effective interest rate? Question 4 - What is continuous compound

Section 5.1 Simple and Compound Interest Question 1 What is simple interest? Question 2 What is compound interest? Question 3 - What is an effective interest rate? Question 4 - What is continuous compound

Example. Chapter F Finance Section F.1 Simple Interest and Discount

Math 166 (c)2011 Epstein Chapter F Page 1 Chapter F Finance Section F.1 Simple Interest and Discount Math 166 (c)2011 Epstein Chapter F Page 2 How much should be place in an account that pays simple interest

Math 166 (c)2011 Epstein Chapter F Page 1 Chapter F Finance Section F.1 Simple Interest and Discount Math 166 (c)2011 Epstein Chapter F Page 2 How much should be place in an account that pays simple interest

5-1 FUTURE VALUE If you deposit $10,000 in a bank account that pays 10% interest ann~ally, how much will be in your account after 5 years?

174 Part 2 Fundamental Concepts in Financial Management QuESTIONS 5-1 What is an opportunity cost? How is this concept used in TVM analysis, and where is it shown on a time line? Is a single number used

174 Part 2 Fundamental Concepts in Financial Management QuESTIONS 5-1 What is an opportunity cost? How is this concept used in TVM analysis, and where is it shown on a time line? Is a single number used

A central precept of financial analysis is money s time value. This essentially means that every dollar (or

INTRODUCTION TO THE TIME VALUE OF MONEY 1. INTRODUCTION A central precept of financial analysis is money s time value. This essentially means that every dollar (or a unit of any other currency) received

INTRODUCTION TO THE TIME VALUE OF MONEY 1. INTRODUCTION A central precept of financial analysis is money s time value. This essentially means that every dollar (or a unit of any other currency) received

9. Time Value of Money 1: Understanding the Language of Finance

9. Time Value of Money 1: Understanding the Language of Finance Introduction The language of finance has unique terms and concepts that are based on mathematics. It is critical that you understand this

9. Time Value of Money 1: Understanding the Language of Finance Introduction The language of finance has unique terms and concepts that are based on mathematics. It is critical that you understand this

APPENDIX 3 TIME VALUE OF MONEY. Time Lines and Notation

1 APPENDIX 3 TIME VALUE OF MONEY The simplest tools in finance are often the most powerful. Present value is a concept that is intuitively appealing, simple to compute, and has a wide range of applications.

1 APPENDIX 3 TIME VALUE OF MONEY The simplest tools in finance are often the most powerful. Present value is a concept that is intuitively appealing, simple to compute, and has a wide range of applications.

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION Answers to Concept Questions 1. Assuming positive cash flows and interest rates, the future value increases and the present value decreases. 2. Assuming positive

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION Answers to Concept Questions 1. Assuming positive cash flows and interest rates, the future value increases and the present value decreases. 2. Assuming positive

Chapter 4. Discounted Cash Flow Valuation

Chapter 4 Discounted Cash Flow Valuation Appreciate the significance of compound vs. simple interest Describe and compute the future value and/or present value of a single cash flow or series of cash flows

Chapter 4 Discounted Cash Flow Valuation Appreciate the significance of compound vs. simple interest Describe and compute the future value and/or present value of a single cash flow or series of cash flows

Quantitative. Workbook

Quantitative Investment Analysis Workbook Third Edition Richard A. DeFusco, CFA Dennis W. McLeavey, CFA Jerald E. Pinto, CFA David E. Runkle, CFA Cover image: r.nagy/shutterstock Cover design: Loretta

Quantitative Investment Analysis Workbook Third Edition Richard A. DeFusco, CFA Dennis W. McLeavey, CFA Jerald E. Pinto, CFA David E. Runkle, CFA Cover image: r.nagy/shutterstock Cover design: Loretta

Exponential & Logarithmic

Exponential & Logarithmic Frank C. Wilson Functions I by file Activity Collection m Credit Card Balance Transfer DVD Player Sales Government Employee Salaries Living Longer Low Interest or Cash Back Shopping

Exponential & Logarithmic Frank C. Wilson Functions I by file Activity Collection m Credit Card Balance Transfer DVD Player Sales Government Employee Salaries Living Longer Low Interest or Cash Back Shopping

Calculator Keystrokes (Get Rich Slow) - Hewlett Packard 12C

- Hewlett Packard 12C") Calculator Keystrokes (Get Rich Slow) - Hewlett Packard 12C Keystrokes for the HP 12C are shown in the following order: (1) Quick Start, pages 165-169 of the Appendix. This will provide some basics for

Calculator Keystrokes (Get Rich Slow) - Hewlett Packard 12C Keystrokes for the HP 12C are shown in the following order: (1) Quick Start, pages 165-169 of the Appendix. This will provide some basics for

Simple Interest: Interest earned only on the original principal amount invested.

53 Future Value (FV): The amount an investment is worth after one or more periods. Simple Interest: Interest earned only on the original principal amount invested. Compound Interest: Interest earned on

53 Future Value (FV): The amount an investment is worth after one or more periods. Simple Interest: Interest earned only on the original principal amount invested. Compound Interest: Interest earned on

7.5 Amount of an Ordinary Annuity

7.5 Amount of an Ordinary Annuity Nigel is saving $700 each year for a trip. Rashid is saving $200 at the end of each month for university. Jeanine is depositing $875 at the end of each 3 months for 3

7.5 Amount of an Ordinary Annuity Nigel is saving $700 each year for a trip. Rashid is saving $200 at the end of each month for university. Jeanine is depositing $875 at the end of each 3 months for 3

Appendix 4B Using Financial Calculators

Chapter 4 Discounted Cash Flow Valuation 4B-1 Appendix 4B Using Financial Calculators This appendix is intended to help you use your Hewlett-Packard or Texas Instruments BA II Plus financial calculator

Chapter 4 Discounted Cash Flow Valuation 4B-1 Appendix 4B Using Financial Calculators This appendix is intended to help you use your Hewlett-Packard or Texas Instruments BA II Plus financial calculator

Simple Interest: Interest earned on the original investment amount only. I = Prt

c Kathryn Bollinger, June 28, 2011 1 Chapter 5 - Finance 5.1 - Compound Interest Simple Interest: Interest earned on the original investment amount only If P dollars (called the principal or present value)

c Kathryn Bollinger, June 28, 2011 1 Chapter 5 - Finance 5.1 - Compound Interest Simple Interest: Interest earned on the original investment amount only If P dollars (called the principal or present value)

HAME507: Mastering the Time Value of Money

HAME507: Mastering the Time Value of Money Copyright 2012 ecornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 1 This

HAME507: Mastering the Time Value of Money Copyright 2012 ecornell. All rights reserved. All other copyrights, trademarks, trade names, and logos are the sole property of their respective owners. 1 This

Time Value of Money. Appendix E. Learning Objectives. After studying this chapter, you should be able to:

E- 1 Appendix E Time Value of Money E- 2 Learning Objectives After studying this chapter, you should be able to: 1. Distinguish between simple and compound interest. 2. Solve for future value of a single

E- 1 Appendix E Time Value of Money E- 2 Learning Objectives After studying this chapter, you should be able to: 1. Distinguish between simple and compound interest. 2. Solve for future value of a single

Finance Mathematics. Part 1: Terms and their meaning.

Finance Mathematics Part 1: Terms and their meaning. Watch the video describing call and put options at http://www.youtube.com/watch?v=efmtwu2yn5q and use http://www.investopedia.com or a search. Look

Finance Mathematics Part 1: Terms and their meaning. Watch the video describing call and put options at http://www.youtube.com/watch?v=efmtwu2yn5q and use http://www.investopedia.com or a search. Look

C H A P T E R 6 ACCOUNTING AND THE TIME VALUE OF MONEY. Intermediate Accounting Presented By; Ratna Candra Sari

C H A P T E R 6 ACCOUNTING AND THE TIME VALUE OF MONEY 6-1 Intermediate Accounting Presented By; Ratna Candra Sari Email: ratna_candrasari@uny.ac.id Learning Objectives 1. Identify accounting topics where

C H A P T E R 6 ACCOUNTING AND THE TIME VALUE OF MONEY 6-1 Intermediate Accounting Presented By; Ratna Candra Sari Email: ratna_candrasari@uny.ac.id Learning Objectives 1. Identify accounting topics where

SOLUTION METHODS FOR SELECTED BASIC FINANCIAL RELATIONSHIPS

SVEN THOMMESEN FINANCE 2400/3200/3700 Spring 2018 [Updated 8/31/16] SOLUTION METHODS FOR SELECTED BASIC FINANCIAL RELATIONSHIPS VARIABLES USED IN THE FOLLOWING PAGES: N = the number of periods (months,

SVEN THOMMESEN FINANCE 2400/3200/3700 Spring 2018 [Updated 8/31/16] SOLUTION METHODS FOR SELECTED BASIC FINANCIAL RELATIONSHIPS VARIABLES USED IN THE FOLLOWING PAGES: N = the number of periods (months,

Activity 1.1 Compound Interest and Accumulated Value

Activity 1.1 Compound Interest and Accumulated Value Remember that time is money. Ben Franklin, 1748 Reprinted by permission: Tribune Media Services Broom Hilda has discovered too late the power of compound

Activity 1.1 Compound Interest and Accumulated Value Remember that time is money. Ben Franklin, 1748 Reprinted by permission: Tribune Media Services Broom Hilda has discovered too late the power of compound

Solutions to Problems

Solutions to Problems 1. The investor would earn income of $2.25 and a capital gain of $52.50 $45 =$7.50. The total gain is $9.75 or 21.7%. $8.25 on a stock that paid $3.75 in income and sold for $67.50.

Solutions to Problems 1. The investor would earn income of $2.25 and a capital gain of $52.50 $45 =$7.50. The total gain is $9.75 or 21.7%. $8.25 on a stock that paid $3.75 in income and sold for $67.50.

Manual for SOA Exam FM/CAS Exam 2.

Manual for SOA Exam FM/CAS Exam 2. Chapter 1. Basic Interest Theory. c 2009. Miguel A. Arcones. All rights reserved. Extract from: Arcones Manual for the SOA Exam FM/CAS Exam 2, Financial Mathematics.

Manual for SOA Exam FM/CAS Exam 2. Chapter 1. Basic Interest Theory. c 2009. Miguel A. Arcones. All rights reserved. Extract from: Arcones Manual for the SOA Exam FM/CAS Exam 2, Financial Mathematics.

YIELDS, BONUSES, DISCOUNTS, AND

YIELDS, BONUSES, DISCOUNTS, AND THE SECONDARY MORTGAGE MARKET 7 Introduction: Primary and Secondary Mortgage Markets The market where mortgage loans are initiated and mortgage documents are created is

YIELDS, BONUSES, DISCOUNTS, AND THE SECONDARY MORTGAGE MARKET 7 Introduction: Primary and Secondary Mortgage Markets The market where mortgage loans are initiated and mortgage documents are created is

Math of Finance Exponential & Power Functions

The Right Stuff: Appropriate Mathematics for All Students Promoting the use of materials that engage students in meaningful activities that promote the effective use of technology to support mathematics,

The Right Stuff: Appropriate Mathematics for All Students Promoting the use of materials that engage students in meaningful activities that promote the effective use of technology to support mathematics,

7.7 Technology: Amortization Tables and Spreadsheets

7.7 Technology: Amortization Tables and Spreadsheets Generally, people must borrow money when they purchase a car, house, or condominium, so they arrange a loan or mortgage. Loans and mortgages are agreements

7.7 Technology: Amortization Tables and Spreadsheets Generally, people must borrow money when they purchase a car, house, or condominium, so they arrange a loan or mortgage. Loans and mortgages are agreements

Financial institutions pay interest when you deposit your money into one of their accounts.

KEY CONCEPTS Financial institutions pay interest when you deposit your money into one of their accounts. Often, financial institutions charge fees or service charges for providing you with certain services

KEY CONCEPTS Financial institutions pay interest when you deposit your money into one of their accounts. Often, financial institutions charge fees or service charges for providing you with certain services

CHAPTER 4. The Time Value of Money. Chapter Synopsis

CHAPTER 4 The Time Value of Money Chapter Synopsis Many financial problems require the valuation of cash flows occurring at different times. However, money received in the future is worth less than money

CHAPTER 4 The Time Value of Money Chapter Synopsis Many financial problems require the valuation of cash flows occurring at different times. However, money received in the future is worth less than money

Introduction to Corporate Finance, Fourth Edition. Chapter 5: Time Value of Money

Multiple Choice Questions 11. Section: 5.4 Annuities and Perpetuities B. Chapter 5: Time Value of Money 1 1 n (1 + k) 1 (1.15) PMT $,,(6.5933) $1, 519 k.15 N, I/Y15, PMT,, FV, CPT 1,519 14. Section: 5.7

Multiple Choice Questions 11. Section: 5.4 Annuities and Perpetuities B. Chapter 5: Time Value of Money 1 1 n (1 + k) 1 (1.15) PMT $,,(6.5933) $1, 519 k.15 N, I/Y15, PMT,, FV, CPT 1,519 14. Section: 5.7

Midterm Review Package Tutor: Chanwoo Yim

COMMERCE 298 Intro to Finance Midterm Review Package Tutor: Chanwoo Yim BCom 2016, Finance 1. Time Value 2. DCF (Discounted Cash Flow) 2.1 Constant Annuity 2.2 Constant Perpetuity 2.3 Growing Annuity 2.4

COMMERCE 298 Intro to Finance Midterm Review Package Tutor: Chanwoo Yim BCom 2016, Finance 1. Time Value 2. DCF (Discounted Cash Flow) 2.1 Constant Annuity 2.2 Constant Perpetuity 2.3 Growing Annuity 2.4

Advanced Mathematical Decision Making In Texas, also known as

Advanced Mathematical Decision Making In Texas, also known as Advanced Quantitative Reasoning Unit VI: Decision Making in Finance This course is a project of The Texas Association of Supervisors of Mathematics

Advanced Mathematical Decision Making In Texas, also known as Advanced Quantitative Reasoning Unit VI: Decision Making in Finance This course is a project of The Texas Association of Supervisors of Mathematics

Copyright 2015 by the McGraw-Hill Education (Asia). All rights reserved.

. All rights reserved.") Copyright 2015 by the McGraw-Hill Education (Asia). All rights reserved. Key Concepts and Skills Be able to compute: The future value of an investment made today The present value of cash to be received

Copyright 2015 by the McGraw-Hill Education (Asia). All rights reserved. Key Concepts and Skills Be able to compute: The future value of an investment made today The present value of cash to be received

Fin 5413: Chapter 04 - Fixed Interest Rate Mortgage Loans Page 1 Solutions to Problems - Chapter 4 Fixed Interest Rate Mortgage Loans

Fin 5413: Chapter 04 - Fixed Interest Rate Mortgage Loans Page 1 Solutions to Problems - Chapter 4 Fixed Interest Rate Mortgage Loans Problem 4-1 A borrower makes a fully amortizing CPM mortgage loan.

Fin 5413: Chapter 04 - Fixed Interest Rate Mortgage Loans Page 1 Solutions to Problems - Chapter 4 Fixed Interest Rate Mortgage Loans Problem 4-1 A borrower makes a fully amortizing CPM mortgage loan.

Chapter 4 The Time Value of Money

Chapter 4 The Time Value of Money Copyright 2011 Pearson Prentice Hall. All rights reserved. Chapter Outline 4.1 The Timeline 4.2 The Three Rules of Time Travel 4.3 Valuing a Stream of Cash Flows 4.4 Calculating

Chapter 4 The Time Value of Money Copyright 2011 Pearson Prentice Hall. All rights reserved. Chapter Outline 4.1 The Timeline 4.2 The Three Rules of Time Travel 4.3 Valuing a Stream of Cash Flows 4.4 Calculating

Chapter 2 Time Value of Money

1. Future Value of a Lump Sum 2. Present Value of a Lump Sum 3. Future Value of Cash Flow Streams 4. Present Value of Cash Flow Streams 5. Perpetuities 6. Uneven Series of Cash Flows 7. Other Compounding

1. Future Value of a Lump Sum 2. Present Value of a Lump Sum 3. Future Value of Cash Flow Streams 4. Present Value of Cash Flow Streams 5. Perpetuities 6. Uneven Series of Cash Flows 7. Other Compounding