|

|

|

- Adrian Norton

- 5 years ago

- Views:

Transcription

1

2

3

4

5

6

7

8

9

10 Interest and present value Simple Interest Interest amount = P x i x n p = principle i = interest rate n = number of periods Assume you invest $1,000 at 6% simple interest for 3 years. You would earn $180 interest ($1000 x.06 x 3 = $180). Compound interest When we compound interest we assume you earn interest on both principal and interest Assume we will save $1,000 for three years and earn 8% interest compounded annually 1

11 Compound interest Original balance $1,000 First year interest 60 Balance, end of year $1,060 Balance, beginning of year two $ 1,060 Second year interest balance, end of year two $ 1, Compound interest Balance, beginning of year three $1, Third year interest Balance, end of year three $1, future value of a single amount writing in a more efficient way, we can say x 1.06 x 1.06 x 1.06 = $ or x (1.06) = $1,

12 future value of a single amount we can generalize the formula as... Present value FV=PV (1+i) n Number of periods Future value Interest rate Present value of a single amount Instead of asking what is the future value of a current amount, we might want to know what amount we must invest today to accumulate a known future amount. This is a present value question. present value of a single amount Remember our equation? FV=PV(1+i) n We can solve for PV and get... PV= FV (1+i) n 3

13 Question Assume you plan to buy a new car in 5 years. You think it will cost $20,000 at that time. What amount must you invest today in order to accumulate $20,000 in 5 years, if you can earn 8% interest compounded annually. Consistent interest periods and rates How would we calculate the amount to be invested today in order to accumulate $20,000 in 5 years, if you can earn 8% interest compounded quarterly? Consistent interest periods and rates Because there are 4 compounding periods 8%/4 = 2% rate 5 x 4 = 20 periods we will use 2% as the interest rate and 20 as the number of periods 4

14 Present Value of a set of cash flows the present value of each cash flow is given by the following PV = C1 (1+i) (1+i) C n + C2 (1+i) n Net present value rule: Accept if the project has a positive net present value: NVP = -C 0 + C 1 (1+i) + C C 2 (1+i) n (1+i) n Example 1: Suppose a project requires an initial investment of $60,000 At the end of the first year you expect to lose $20,000 At the end of the second year(also the end of the project) you expect to gain $100,000 You asses that, given the risk of the project, a cost of capital of 12% is appropriate. Should you accept the project? 5

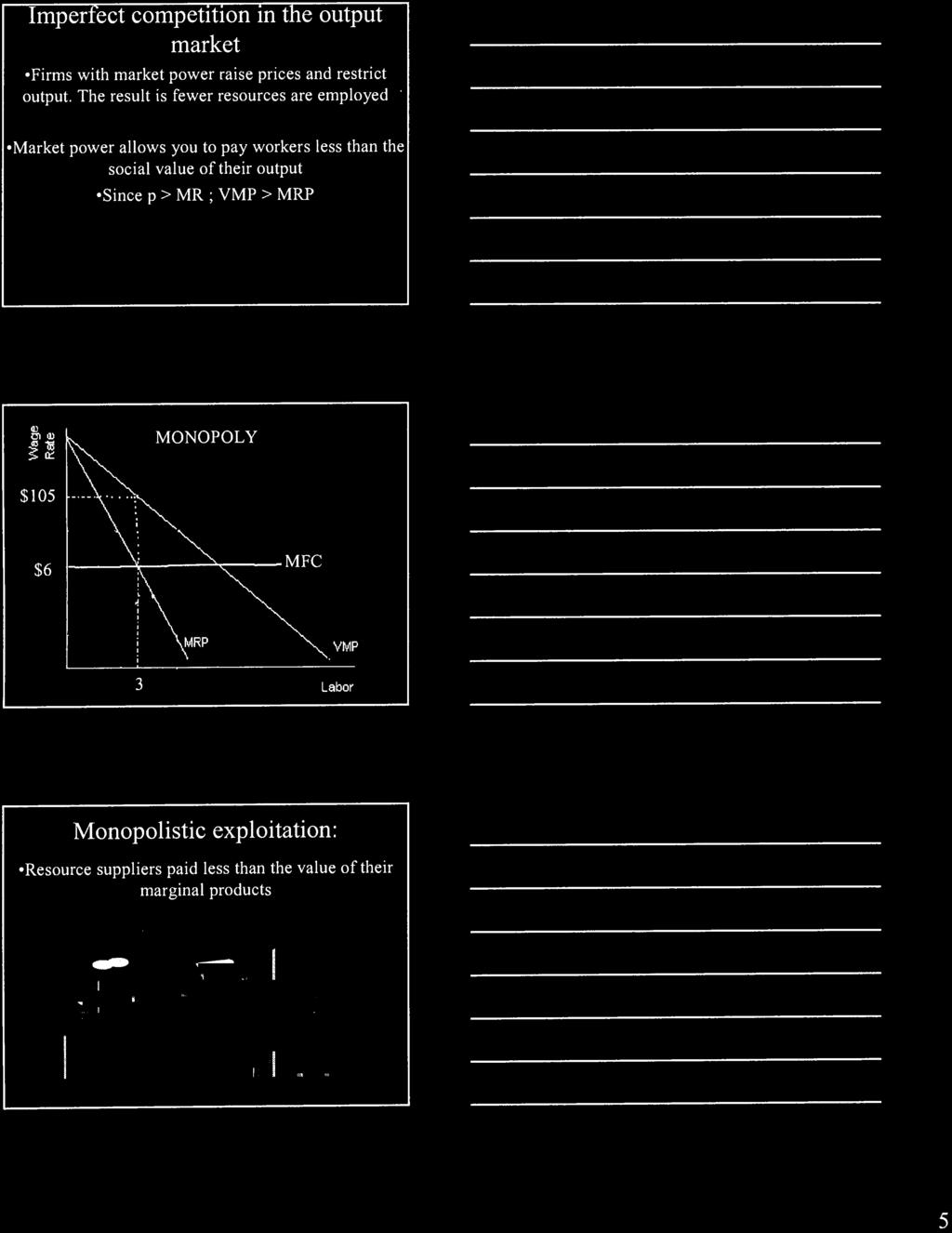

15 Example 1: Do the project because it has a positive NPV NPV = -60, ,000 ( ) + 100,000 ( ) 2 = -60,000-17, , = > 0 Expanding capital stock: A firm can finance its purchase of capital in several ways funds on hand sell shares of stock borrow from a bank sell its own bonds Regardless of the method of financing chosen, a critical factor in the firm s decision on whether to acquire capital is the interest rate Expanding capital stock: The interest rate gives the opportunity cost of using funds to acquire capital rather than putting the funds to the best alternative use to the firm 6

16 Demand for loanable funds: A firm s decision to acquire capital depends on the net present value of capital The lower the interest rate, the greater the amount of capital firms will want to acquire. Lower interest rates translate into more capital with positive net present values. The desire for more capital means, in turn, a desire for more loanable funds. Supply of loanable funds: Lenders supply funds to the loanable funds market. Lenders are consumers or firms that determine that they are willing to forgo some current use of their funds in order to have more available in the future. In general, higher interest rates make the lending option more attractive. Shifts: An increase in the demand for capital will cause an increase in the demand for loanable funds. Example: If firms are optimistic about the future of the economy, they will want to invest in capital. To buy the capital the need loanable funds. The supply of loanable funds is affected by the willingness of people to save. Exanple: People expect high inflation in the future and do not want to save. The supply of loanable funds will decreade 7

Chapter 5. Finance 300 David Moore

Chapter 5 Finance 300 David Moore Time and Money This chapter is the first chapter on the most important skill in this course: how to move money through time. Timing is everything. The simple techniques

Chapter 5 Finance 300 David Moore Time and Money This chapter is the first chapter on the most important skill in this course: how to move money through time. Timing is everything. The simple techniques

Chapter 5. Time Value of Money

Chapter 5 Time Value of Money Using Timelines to Visualize Cashflows A timeline identifies the timing and amount of a stream of payments both cash received and cash spent - along with the interest rate

Chapter 5 Time Value of Money Using Timelines to Visualize Cashflows A timeline identifies the timing and amount of a stream of payments both cash received and cash spent - along with the interest rate

Chapter 5. Learning Objectives. Principals Applied in this Chapter. Time Value of Money. Principle 1: Money Has a Time Value.

Chapter 5 Time Value of Money Learning Objectives 1. Construct cash flow timelines to organize your analysis of problems involving the time value of money. 2. Understand compounding and calculate the future

Chapter 5 Time Value of Money Learning Objectives 1. Construct cash flow timelines to organize your analysis of problems involving the time value of money. 2. Understand compounding and calculate the future

Simple Interest: Interest earned only on the original principal amount invested.

53 Future Value (FV): The amount an investment is worth after one or more periods. Simple Interest: Interest earned only on the original principal amount invested. Compound Interest: Interest earned on

53 Future Value (FV): The amount an investment is worth after one or more periods. Simple Interest: Interest earned only on the original principal amount invested. Compound Interest: Interest earned on

Measuring Interest Rates

Measuring Interest Rates Economics 301: Money and Banking 1 1.1 Goals Goals and Learning Outcomes Goals: Learn to compute present values, rates of return, rates of return. Learning Outcomes: LO3: Predict

Measuring Interest Rates Economics 301: Money and Banking 1 1.1 Goals Goals and Learning Outcomes Goals: Learn to compute present values, rates of return, rates of return. Learning Outcomes: LO3: Predict

Time Value of Money. Ex: How much a bond, which can be cashed out in 2 years, is worth today

Time Value of Money The time value of money is the idea that money available now is worth more than the same amount in the future - this is essentially why interest exists. Present value is the current

Time Value of Money The time value of money is the idea that money available now is worth more than the same amount in the future - this is essentially why interest exists. Present value is the current

Chapter Organization. The future value (FV) is the cash value of. an investment at some time in the future.

is the cash value of. an investment at some time in the future.") Chapter 5 The Time Value of Money Chapter Organization 5.2. Present Value and Discounting The future value (FV) is the cash value of an investment at some time in the future Suppose you invest 100 in a

Chapter 5 The Time Value of Money Chapter Organization 5.2. Present Value and Discounting The future value (FV) is the cash value of an investment at some time in the future Suppose you invest 100 in a

An Introduction to Capital Budgeting Methods

An Introduction to Capital Budgeting Methods Econ 466 Spring, 2010 Chapters 9 and 10 Consider the following choice You have an opportunity to invest $20,000 in one of the following capital assets. You

An Introduction to Capital Budgeting Methods Econ 466 Spring, 2010 Chapters 9 and 10 Consider the following choice You have an opportunity to invest $20,000 in one of the following capital assets. You

3. Time value of money. We will review some tools for discounting cash flows.

1 3. Time value of money We will review some tools for discounting cash flows. Simple interest 2 With simple interest, the amount earned each period is always the same: i = rp o where i = interest earned

1 3. Time value of money We will review some tools for discounting cash flows. Simple interest 2 With simple interest, the amount earned each period is always the same: i = rp o where i = interest earned

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture 09 Future Value Welcome to the lecture series on Time

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture 09 Future Value Welcome to the lecture series on Time

Introduction to the Compound Interest Formula

Introduction to the Compound Interest Formula Lesson Objectives: students will be introduced to the formula students will learn how to determine the value of the required variables in order to use the

Introduction to the Compound Interest Formula Lesson Objectives: students will be introduced to the formula students will learn how to determine the value of the required variables in order to use the

3. Time value of money

1 Simple interest 2 3. Time value of money With simple interest, the amount earned each period is always the same: i = rp o We will review some tools for discounting cash flows. where i = interest earned

1 Simple interest 2 3. Time value of money With simple interest, the amount earned each period is always the same: i = rp o We will review some tools for discounting cash flows. where i = interest earned

Copyright 2015 Pearson Education, Inc. All rights reserved.

Chapter 4 Mathematics of Finance Section 4.1 Simple Interest and Discount A fee that is charged by a lender to a borrower for the right to use the borrowed funds. The funds can be used to purchase a house,

Chapter 4 Mathematics of Finance Section 4.1 Simple Interest and Discount A fee that is charged by a lender to a borrower for the right to use the borrowed funds. The funds can be used to purchase a house,

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture 08 Present Value Welcome to the lecture series on Time

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture 08 Present Value Welcome to the lecture series on Time

Finance Notes AMORTIZED LOANS

Amortized Loans Page 1 of 10 AMORTIZED LOANS Objectives: After completing this section, you should be able to do the following: Calculate the monthly payment for a simple interest amortized loan. Calculate

Amortized Loans Page 1 of 10 AMORTIZED LOANS Objectives: After completing this section, you should be able to do the following: Calculate the monthly payment for a simple interest amortized loan. Calculate

Section 4B: The Power of Compounding

Section 4B: The Power of Compounding Definitions The principal is the amount of your initial investment. This is the amount on which interest is paid. Simple interest is interest paid only on the original

Section 4B: The Power of Compounding Definitions The principal is the amount of your initial investment. This is the amount on which interest is paid. Simple interest is interest paid only on the original

Chapter 4 The Time Value of Money

Chapter 4 The Time Value of Money Copyright 2011 Pearson Prentice Hall. All rights reserved. Chapter Outline 4.1 The Timeline 4.2 The Three Rules of Time Travel 4.3 Valuing a Stream of Cash Flows 4.4 Calculating

Chapter 4 The Time Value of Money Copyright 2011 Pearson Prentice Hall. All rights reserved. Chapter Outline 4.1 The Timeline 4.2 The Three Rules of Time Travel 4.3 Valuing a Stream of Cash Flows 4.4 Calculating

Copyright 2015 by the McGraw-Hill Education (Asia). All rights reserved.

. All rights reserved.") Copyright 2015 by the McGraw-Hill Education (Asia). All rights reserved. Key Concepts and Skills Be able to compute: The future value of an investment made today The present value of cash to be received

Copyright 2015 by the McGraw-Hill Education (Asia). All rights reserved. Key Concepts and Skills Be able to compute: The future value of an investment made today The present value of cash to be received

Financial Management I

Financial Management I Workshop on Time Value of Money MBA 2016 2017 Slide 2 Finance & Valuation Capital Budgeting Decisions Long-term Investment decisions Investments in Net Working Capital Financing

Financial Management I Workshop on Time Value of Money MBA 2016 2017 Slide 2 Finance & Valuation Capital Budgeting Decisions Long-term Investment decisions Investments in Net Working Capital Financing

Understanding Interest Rates

Money & Banking Notes Chapter 4 Understanding Interest Rates Measuring Interest Rates Present Value (PV): A dollar paid to you one year from now is less valuable than a dollar paid to you today. Why? -

Money & Banking Notes Chapter 4 Understanding Interest Rates Measuring Interest Rates Present Value (PV): A dollar paid to you one year from now is less valuable than a dollar paid to you today. Why? -

FINANCE FOR EVERYONE SPREADSHEETS

FINANCE FOR EVERYONE SPREADSHEETS Some Important Stuff Make sure there are at least two decimals allowed in each cell. Otherwise rounding off may create problems in a multi-step problem Always enter the

FINANCE FOR EVERYONE SPREADSHEETS Some Important Stuff Make sure there are at least two decimals allowed in each cell. Otherwise rounding off may create problems in a multi-step problem Always enter the

Sample Investment Device CD (Certificate of Deposit) Savings Account Bonds Loans for: Car House Start a business

Savings Account Bonds Loans for: Car House Start a business") Simple and Compound Interest (Young: 6.1) In this Lecture: 1. Financial Terminology 2. Simple Interest 3. Compound Interest 4. Important Formulas of Finance 5. From Simple to Compound Interest 6. Examples

Simple and Compound Interest (Young: 6.1) In this Lecture: 1. Financial Terminology 2. Simple Interest 3. Compound Interest 4. Important Formulas of Finance 5. From Simple to Compound Interest 6. Examples

Chapter 3 Mathematics of Finance

Chapter 3 Mathematics of Finance Section R Review Important Terms, Symbols, Concepts 3.1 Simple Interest Interest is the fee paid for the use of a sum of money P, called the principal. Simple interest

Chapter 3 Mathematics of Finance Section R Review Important Terms, Symbols, Concepts 3.1 Simple Interest Interest is the fee paid for the use of a sum of money P, called the principal. Simple interest

Chapter 5: Introduction to Valuation: The Time Value of Money

Chapter 5: Introduction to Valuation: The Time Value of Money Faculty of Business Administration Lakehead University Spring 2003 May 12, 2003 Outline of Chapter 5 5.1 Future Value and Compounding 5.2 Present

Chapter 5: Introduction to Valuation: The Time Value of Money Faculty of Business Administration Lakehead University Spring 2003 May 12, 2003 Outline of Chapter 5 5.1 Future Value and Compounding 5.2 Present

1. The real risk-free rate is the increment to purchasing power that the lender earns in order to induce him or her to forego current consumption.

Chapter 02 Determinants of Interest Rates True / False Questions 1. The real risk-free rate is the increment to purchasing power that the lender earns in order to induce him or her to forego current consumption.

Chapter 02 Determinants of Interest Rates True / False Questions 1. The real risk-free rate is the increment to purchasing power that the lender earns in order to induce him or her to forego current consumption.

FINANCIAL DECISION RULES FOR PROJECT EVALUATION SPREADSHEETS

FINANCIAL DECISION RULES FOR PROJECT EVALUATION SPREADSHEETS This note is some basic information that should help you get started and do most calculations if you have access to spreadsheets. You could

FINANCIAL DECISION RULES FOR PROJECT EVALUATION SPREADSHEETS This note is some basic information that should help you get started and do most calculations if you have access to spreadsheets. You could

FinQuiz Notes

Reading 6 The Time Value of Money Money has a time value because a unit of money received today is worth more than a unit of money to be received tomorrow. Interest rates can be interpreted in three ways.

Reading 6 The Time Value of Money Money has a time value because a unit of money received today is worth more than a unit of money to be received tomorrow. Interest rates can be interpreted in three ways.

Chapter 5 Time Value of Money

Chapter 5 Time Value of Money Answers to End-of-Chapter 5 Questions 5-1 The opportunity cost is the rate of interest one could earn on an alternative investment with a risk equal to the risk of the investment

Chapter 5 Time Value of Money Answers to End-of-Chapter 5 Questions 5-1 The opportunity cost is the rate of interest one could earn on an alternative investment with a risk equal to the risk of the investment

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture - 01 Introduction Welcome to the course Time value

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture - 01 Introduction Welcome to the course Time value

CS 413 Software Project Management LECTURE 8 COST MANAGEMENT FOR SOFTWARE PROJECT - II CASH FLOW ANALYSIS TECHNIQUES

LECTURE 8 COST MANAGEMENT FOR SOFTWARE PROJECT - II CASH FLOW ANALYSIS TECHNIQUES PAYBACK PERIOD: The payback period is the length of time it takes the company to recoup the initial costs of producing

LECTURE 8 COST MANAGEMENT FOR SOFTWARE PROJECT - II CASH FLOW ANALYSIS TECHNIQUES PAYBACK PERIOD: The payback period is the length of time it takes the company to recoup the initial costs of producing

Understanding Interest Rates

Understanding Interest Rates Leigh Tesfatsion (Iowa State University) Notes on Mishkin Chapter 4: Part A (pp. 68-80) Last Revised: 14 February 2011 Mishkin Chapter 4: Part A -- Selected Key In-Class Discussion

Understanding Interest Rates Leigh Tesfatsion (Iowa State University) Notes on Mishkin Chapter 4: Part A (pp. 68-80) Last Revised: 14 February 2011 Mishkin Chapter 4: Part A -- Selected Key In-Class Discussion

Chapter 6. Learning Objectives. Principals Applies in this Chapter. Time Value of Money

Chapter 6 Time Value of Money 1 Learning Objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate the present and future values of each. 2. Calculate the present value of

Chapter 6 Time Value of Money 1 Learning Objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate the present and future values of each. 2. Calculate the present value of

Principles of Corporate Finance. Brealey and Myers. Sixth Edition. ! How to Calculate Present Values. Slides by Matthew Will.

Principles of Corporate Finance Brealey and Myers Sixth Edition! How to Calculate Present Values Slides by Matthew Will Chapter 3 3-2 Topics Covered " Valuing Long-Lived Assets " PV Calculation Short Cuts

Principles of Corporate Finance Brealey and Myers Sixth Edition! How to Calculate Present Values Slides by Matthew Will Chapter 3 3-2 Topics Covered " Valuing Long-Lived Assets " PV Calculation Short Cuts

CHAPTER 8 STOCK VALUATION. Copyright 2016 by McGraw-Hill Education. All rights reserved CASH FLOWS FOR STOCKHOLDERS

CHAPTER 8 STOCK VALUATION Copyright 2016 by McGraw-Hill Education. All rights reserved CASH FLOWS FOR STOCKHOLDERS If you buy a share of stock, you can receive cash in two ways: The company pays dividends

CHAPTER 8 STOCK VALUATION Copyright 2016 by McGraw-Hill Education. All rights reserved CASH FLOWS FOR STOCKHOLDERS If you buy a share of stock, you can receive cash in two ways: The company pays dividends

FNCE 370v8: Assignment 3

FNCE 370v8: Assignment 3 Assignment 3 is worth 5% of your final mark. Complete and submit Assignment 3 after you complete Lesson 9. There are 12 questions in this assignment. The break-down of marks for

FNCE 370v8: Assignment 3 Assignment 3 is worth 5% of your final mark. Complete and submit Assignment 3 after you complete Lesson 9. There are 12 questions in this assignment. The break-down of marks for

Lecture 2 Time Value of Money FINA 614

Lecture 2 Time Value of Money FINA 614 Basic Defini?ons Present Value earlier money on a?me line Future Value later money on a?me line Interest rate exchange rate between earlier money and later money

Lecture 2 Time Value of Money FINA 614 Basic Defini?ons Present Value earlier money on a?me line Future Value later money on a?me line Interest rate exchange rate between earlier money and later money

6.1 Simple and Compound Interest

6.1 Simple and Compound Interest If P dollars (called the principal or present value) earns interest at a simple interest rate of r per year (as a decimal) for t years, then Interest: I = P rt Accumulated

6.1 Simple and Compound Interest If P dollars (called the principal or present value) earns interest at a simple interest rate of r per year (as a decimal) for t years, then Interest: I = P rt Accumulated

Chapter 4. Discounted Cash Flow Valuation

Chapter 4 Discounted Cash Flow Valuation Appreciate the significance of compound vs. simple interest Describe and compute the future value and/or present value of a single cash flow or series of cash flows

Chapter 4 Discounted Cash Flow Valuation Appreciate the significance of compound vs. simple interest Describe and compute the future value and/or present value of a single cash flow or series of cash flows

Management 3 Quantitative Methods. The Time Value of Money Part 1A

Management 3 Quantitative Methods The Time Value of Money Part 1A Money: Today? Tomorrow? money now is not the same as money tomorrow Money now is better: It can be used now; It can invested now; There

Management 3 Quantitative Methods The Time Value of Money Part 1A Money: Today? Tomorrow? money now is not the same as money tomorrow Money now is better: It can be used now; It can invested now; There

CHAPTER 15 INVESTMENT, TIME, AND CAPITAL MARKETS

CHAPTER 15 INVESTMENT, TIME, AND CAPITAL MARKETS REVIEW QUESTIONS 1. A firm uses cloth and labor to produce shirts in a factory that it bought for $10 million. Which of its factor inputs are measured as

CHAPTER 15 INVESTMENT, TIME, AND CAPITAL MARKETS REVIEW QUESTIONS 1. A firm uses cloth and labor to produce shirts in a factory that it bought for $10 million. Which of its factor inputs are measured as

Chapter 03 - Basic Annuities

3-1 Chapter 03 - Basic Annuities Section 3.0 - Sum of a Geometric Sequence The form for the sum of a geometric sequence is: Sum(n) a + ar + ar 2 + ar 3 + + ar n 1 Here a = (the first term) n = (the number

3-1 Chapter 03 - Basic Annuities Section 3.0 - Sum of a Geometric Sequence The form for the sum of a geometric sequence is: Sum(n) a + ar + ar 2 + ar 3 + + ar n 1 Here a = (the first term) n = (the number

2. I =interest (in dollars and cents, accumulated over some period)

") A. Recap of the Variables 1. P = principal (as designated at some point in time) a. we shall use PV for present value. Your text and others use P for PV (We shall do it sometimes too!) 2. I =interest (in

A. Recap of the Variables 1. P = principal (as designated at some point in time) a. we shall use PV for present value. Your text and others use P for PV (We shall do it sometimes too!) 2. I =interest (in

Worksheet-2 Present Value Math I

What you will learn: Worksheet-2 Present Value Math I How to compute present and future values of single and annuity cash flows How to handle cash flow delays and combinations of cash flow streams How

What you will learn: Worksheet-2 Present Value Math I How to compute present and future values of single and annuity cash flows How to handle cash flow delays and combinations of cash flow streams How

Lecture 3. Chapter 4: Allocating Resources Over Time

Lecture 3 Chapter 4: Allocating Resources Over Time 1 Introduction: Time Value of Money (TVM) $20 today is worth more than the expectation of $20 tomorrow because: a bank would pay interest on the $20

Lecture 3 Chapter 4: Allocating Resources Over Time 1 Introduction: Time Value of Money (TVM) $20 today is worth more than the expectation of $20 tomorrow because: a bank would pay interest on the $20

BUSI 370 Business Finance

Review Session 2 February 7 th, 2016 Road Map 1. BONDS 2. COMMON SHARES 3. PREFERRED SHARES 4. TREASURY BILLS (T Bills) ANSWER KEY WITH COMMENTS 1. BONDS // Calculate the price of a ten-year annual pay

Review Session 2 February 7 th, 2016 Road Map 1. BONDS 2. COMMON SHARES 3. PREFERRED SHARES 4. TREASURY BILLS (T Bills) ANSWER KEY WITH COMMENTS 1. BONDS // Calculate the price of a ten-year annual pay

The Time Value of Money

Chapter 2 The Time Value of Money Time Discounting One of the basic concepts of business economics and managerial decision making is that the value of an amount of money to be received in the future depends

Chapter 2 The Time Value of Money Time Discounting One of the basic concepts of business economics and managerial decision making is that the value of an amount of money to be received in the future depends

3.1 Mathematic of Finance: Simple Interest

3.1 Mathematic of Finance: Simple Interest Introduction Part I This chapter deals with Simple Interest, and teaches students how to calculate simple interest on investments and loans. The Simple Interest

3.1 Mathematic of Finance: Simple Interest Introduction Part I This chapter deals with Simple Interest, and teaches students how to calculate simple interest on investments and loans. The Simple Interest

CHAPTER 2 How to Calculate Present Values

CHAPTER How to Calculate Present Values Answers to Problem Sets. If the discount factor is.507, then.507 x. 6 = $. Est time: 0-05. DF x 39 = 5. Therefore, DF =5/39 =.899. Est time: 0-05 3. PV = 374/(.09)

CHAPTER How to Calculate Present Values Answers to Problem Sets. If the discount factor is.507, then.507 x. 6 = $. Est time: 0-05. DF x 39 = 5. Therefore, DF =5/39 =.899. Est time: 0-05 3. PV = 374/(.09)

A central precept of financial analysis is money s time value. This essentially means that every dollar (or

INTRODUCTION TO THE TIME VALUE OF MONEY 1. INTRODUCTION A central precept of financial analysis is money s time value. This essentially means that every dollar (or a unit of any other currency) received

INTRODUCTION TO THE TIME VALUE OF MONEY 1. INTRODUCTION A central precept of financial analysis is money s time value. This essentially means that every dollar (or a unit of any other currency) received

Texas Credit Opening/Closing Date: 7/19/08 08/18/08

Anatomy of a Credit Card Statement The following is a monthly statement from a typical credit card company. Parts left out intentionally are denoted by??? and highlighted in gray. Texas Credit Opening/Closing

Anatomy of a Credit Card Statement The following is a monthly statement from a typical credit card company. Parts left out intentionally are denoted by??? and highlighted in gray. Texas Credit Opening/Closing

Financial institutions pay interest when you deposit your money into one of their accounts.

KEY CONCEPTS Financial institutions pay interest when you deposit your money into one of their accounts. Often, financial institutions charge fees or service charges for providing you with certain services

KEY CONCEPTS Financial institutions pay interest when you deposit your money into one of their accounts. Often, financial institutions charge fees or service charges for providing you with certain services

Name Date. Goal: Solve problems that involve credit.

F Math 12 2.3 Solving Problems Involving Credit p. 104 Name Date Goal: Solve problems that involve credit. 1. line of credit: A pre-approved loan that offers immediate access to funds, up to a predefined

F Math 12 2.3 Solving Problems Involving Credit p. 104 Name Date Goal: Solve problems that involve credit. 1. line of credit: A pre-approved loan that offers immediate access to funds, up to a predefined

LO.a: Interpret interest rates as required rates of return, discount rates, or opportunity costs.

LO.a: Interpret interest rates as required rates of return, discount rates, or opportunity costs. 1. The minimum rate of return that an investor must receive in order to invest in a project is most likely

LO.a: Interpret interest rates as required rates of return, discount rates, or opportunity costs. 1. The minimum rate of return that an investor must receive in order to invest in a project is most likely

Interest: The money earned from an investment you have or the cost of borrowing money from a lender.

8.1 Simple Interest Interest: The money earned from an investment you have or the cost of borrowing money from a lender. Simple Interest: "I" Interest earned or paid that is calculated based only on the

8.1 Simple Interest Interest: The money earned from an investment you have or the cost of borrowing money from a lender. Simple Interest: "I" Interest earned or paid that is calculated based only on the

2, , , , ,220.21

11-7 a. Project A: CF 0-6000; CF 1-5 2000; I/YR 14. Solve for NPV A $866.16. IRR A 19.86%. MIRR calculation: 0 14% 1 2 3 4 5-6,000 2,000 (1.14) 4 2,000 (1.14) 3 2,000 (1.14) 2 2,000 1.14 2,000 2,280.00

11-7 a. Project A: CF 0-6000; CF 1-5 2000; I/YR 14. Solve for NPV A $866.16. IRR A 19.86%. MIRR calculation: 0 14% 1 2 3 4 5-6,000 2,000 (1.14) 4 2,000 (1.14) 3 2,000 (1.14) 2 2,000 1.14 2,000 2,280.00

The Time Value. The importance of money flows from it being a link between the present and the future. John Maynard Keynes

The Time Value of Money The importance of money flows from it being a link between the present and the future. John Maynard Keynes Get a Free $,000 Bond with Every Car Bought This Week! There is a car

The Time Value of Money The importance of money flows from it being a link between the present and the future. John Maynard Keynes Get a Free $,000 Bond with Every Car Bought This Week! There is a car

The Time Value of Money: Present Value and Future Value

The Time Value of Money: Present Value and Future Value 1. [Future Value] (A) You deposit $1,000 into a savings account which pays an interest rate of 5%. How much will be in the account in one year? FV

The Time Value of Money: Present Value and Future Value 1. [Future Value] (A) You deposit $1,000 into a savings account which pays an interest rate of 5%. How much will be in the account in one year? FV

I. Warnings for annuities and

Outline I. More on the use of the financial calculator and warnings II. Dealing with periods other than years III. Understanding interest rate quotes and conversions IV. Applications mortgages, etc. 0

Outline I. More on the use of the financial calculator and warnings II. Dealing with periods other than years III. Understanding interest rate quotes and conversions IV. Applications mortgages, etc. 0

1) Cash Flow Pattern Diagram for Future Value and Present Value of Irregular Cash Flows

Cash Flow Pattern Diagram for Future Value and Present Value of Irregular Cash Flows") Topics Excel & Business Math Video/Class Project #45 Cash Flow Analysis for Annuities: Savings Plans, Asset Valuation, Retirement Plans and Mortgage Loan. FV, PV and PMT. 1) Cash Flow Pattern Diagram for

Topics Excel & Business Math Video/Class Project #45 Cash Flow Analysis for Annuities: Savings Plans, Asset Valuation, Retirement Plans and Mortgage Loan. FV, PV and PMT. 1) Cash Flow Pattern Diagram for

Chapter 04 Future Value, Present Value and Interest Rates

Chapter 04 Future Value, Present Value and Interest Rates Multiple Choice Questions 1. (p. 66) A promise of a $100 payment to be received one year from today is: a. More valuable than receiving the payment

Chapter 04 Future Value, Present Value and Interest Rates Multiple Choice Questions 1. (p. 66) A promise of a $100 payment to be received one year from today is: a. More valuable than receiving the payment

Key Terms: exponential function, exponential equation, compound interest, future value, present value, compound amount, continuous compounding.

4.2 Exponential Functions Exponents and Properties Exponential Functions Exponential Equations Compound Interest The Number e and Continuous Compounding Exponential Models Section 4.3 Logarithmic Functions

4.2 Exponential Functions Exponents and Properties Exponential Functions Exponential Equations Compound Interest The Number e and Continuous Compounding Exponential Models Section 4.3 Logarithmic Functions

Investment, Time, and Capital Markets

C H A P T E R 15 Investment, Time, and Capital Markets Prepared by: Fernando & Yvonn Quijano CHAPTER 15 OUTLINE 15.1 Stocks versus Flows 15.2 Present Discounted Value 15.3 The Value of a Bond 15.4 The

C H A P T E R 15 Investment, Time, and Capital Markets Prepared by: Fernando & Yvonn Quijano CHAPTER 15 OUTLINE 15.1 Stocks versus Flows 15.2 Present Discounted Value 15.3 The Value of a Bond 15.4 The

Introduction. Once you have completed this chapter, you should be able to do the following:

Introduction This chapter continues the discussion on the time value of money. In this chapter, you will learn how inflation impacts your investments; you will also learn how to calculate real returns

Introduction This chapter continues the discussion on the time value of money. In this chapter, you will learn how inflation impacts your investments; you will also learn how to calculate real returns

Principles of Accounting II Chapter 14: Time Value of Money

Principles of Accounting II Chapter 14: Time Value of Money What Is Accounting? Process of,, and information To facilitate informed. Accounting is the of. Operating, Investing, Financing Businesses plan

Principles of Accounting II Chapter 14: Time Value of Money What Is Accounting? Process of,, and information To facilitate informed. Accounting is the of. Operating, Investing, Financing Businesses plan

JEM034 Corporate Finance Winter Semester 2017/2018

JEM034 Corporate Finance Winter Semester 2017/2018 Lecture #1 Olga Bychkova Topics Covered Today Review of key finance concepts Present value (chapter 2 in BMA) Valuation of bonds (chapter 3 in BMA) Present

JEM034 Corporate Finance Winter Semester 2017/2018 Lecture #1 Olga Bychkova Topics Covered Today Review of key finance concepts Present value (chapter 2 in BMA) Valuation of bonds (chapter 3 in BMA) Present

MBF1223 Financial Management Prepared by Dr Khairul Anuar

MBF1223 Financial Management Prepared by Dr Khairul Anuar L4 Time Value of Money www.mba638.wordpress.com 2 Learning Objectives 1. Calculate future values and understand compounding. 2. Calculate present

MBF1223 Financial Management Prepared by Dr Khairul Anuar L4 Time Value of Money www.mba638.wordpress.com 2 Learning Objectives 1. Calculate future values and understand compounding. 2. Calculate present

MBF1223 Financial Management Prepared by Dr Khairul Anuar

MBF1223 Financial Management Prepared by Dr Khairul Anuar L3 Time Value of Money www.mba638.wordpress.com 2 4 Learning Objectives 1. Calculate future values and understand compounding. 2. Calculate present

MBF1223 Financial Management Prepared by Dr Khairul Anuar L3 Time Value of Money www.mba638.wordpress.com 2 4 Learning Objectives 1. Calculate future values and understand compounding. 2. Calculate present

Math of Finance Exponential & Power Functions

The Right Stuff: Appropriate Mathematics for All Students Promoting the use of materials that engage students in meaningful activities that promote the effective use of technology to support mathematics,

The Right Stuff: Appropriate Mathematics for All Students Promoting the use of materials that engage students in meaningful activities that promote the effective use of technology to support mathematics,

Chapter 7. SAVING, INVESTMENT and FINIANCE. Income not spent is saved. Where do those dollars go?

Chapter 7 SAVING, INVESTMENT and FINIANCE Income not spent is saved. Where do those dollars go? Describe financial markets. Explain how financial markets channel saving to investment. Explain how government

Chapter 7 SAVING, INVESTMENT and FINIANCE Income not spent is saved. Where do those dollars go? Describe financial markets. Explain how financial markets channel saving to investment. Explain how government

Session 1, Monday, April 8 th (9:45-10:45)

") Session 1, Monday, April 8 th (9:45-10:45) Time Value of Money and Capital Budgeting v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Time Value of Money:

Session 1, Monday, April 8 th (9:45-10:45) Time Value of Money and Capital Budgeting v2.0 2014 Association for Financial Professionals. All rights reserved. Session 3-1 Chapters Covered Time Value of Money:

1. Interest Rate. Three components of interest: Principal Interest rate Investment horizon (Time)

") 1 Key Concepts The future value of an investment made today The present value of cash to be received at some future date The return on an investment The number of periods that equates a present value and

1 Key Concepts The future value of an investment made today The present value of cash to be received at some future date The return on an investment The number of periods that equates a present value and

2/22/2016. Compound Interest, Annuities, Perpetuities and Geometric Series. Windows User

2/22/2016 Compound Interest, Annuities, Perpetuities and Geometric Series Windows User - Compound Interest, Annuities, Perpetuities and Geometric Series A Motivating Example for Module 3 Project Description

2/22/2016 Compound Interest, Annuities, Perpetuities and Geometric Series Windows User - Compound Interest, Annuities, Perpetuities and Geometric Series A Motivating Example for Module 3 Project Description

Computer Technology MSIS 22:198:605 Homework 1

Computer Technology MSIS 22:198:605 Homework 1 Instructor: Farid Alizadeh Due Date: Friday October 3, 2003 by midnight Submission: by e-mail See below for detailed instructions) last updated on September

Computer Technology MSIS 22:198:605 Homework 1 Instructor: Farid Alizadeh Due Date: Friday October 3, 2003 by midnight Submission: by e-mail See below for detailed instructions) last updated on September

Chapter 4. Discounted Cash Flow Valuation

Chapter 4 Discounted Cash Flow Valuation 1 Acknowledgement This work is reproduced, based on the book [Ross, Westerfield, Jaffe and Jordan Core Principles and Applications of Corporate Finance ]. This

Chapter 4 Discounted Cash Flow Valuation 1 Acknowledgement This work is reproduced, based on the book [Ross, Westerfield, Jaffe and Jordan Core Principles and Applications of Corporate Finance ]. This

Monetary Economics Valuation: Cash Flows over Time. Gerald P. Dwyer Fall 2015

Monetary Economics Valuation: Cash Flows over Time Gerald P. Dwyer Fall 2015 WSJ Material to be Studied This lecture, Chapter 6, Valuation, in Cuthbertson and Nitzsche Next topic, Chapter 7, Cost of Capital,

Monetary Economics Valuation: Cash Flows over Time Gerald P. Dwyer Fall 2015 WSJ Material to be Studied This lecture, Chapter 6, Valuation, in Cuthbertson and Nitzsche Next topic, Chapter 7, Cost of Capital,

The cost price equals R Cash inflow from the new machinery excluding wear and tear-, service- and maintenance cost are as follows:

Simphiwe & Sons Ltd 1 Current capital structure: The company has a target D : E ratio of 40% : 60% The current market value of debt is R4 million The current market value of equity is R9 million Cost of

Simphiwe & Sons Ltd 1 Current capital structure: The company has a target D : E ratio of 40% : 60% The current market value of debt is R4 million The current market value of equity is R9 million Cost of

9. Time Value of Money 1: Understanding the Language of Finance

9. Time Value of Money 1: Understanding the Language of Finance Introduction The language of finance has unique terms and concepts that are based on mathematics. It is critical that you understand this

9. Time Value of Money 1: Understanding the Language of Finance Introduction The language of finance has unique terms and concepts that are based on mathematics. It is critical that you understand this

Stock valuation. A reading prepared by Pamela Peterson-Drake, Florida Atlantic University

Stock valuation A reading prepared by Pamela Peterson-Drake, Florida Atlantic University O U T L I N E. Valuation of common stock. Returns on stock. Summary. Valuation of common stock "[A] stock is worth

Stock valuation A reading prepared by Pamela Peterson-Drake, Florida Atlantic University O U T L I N E. Valuation of common stock. Returns on stock. Summary. Valuation of common stock "[A] stock is worth

AFP Financial Planning & Analysis Learning System Session 1, Monday, April 3 rd (9:45-10:45) Time Value of Money and Capital Budgeting

Time Value of Money and Capital Budgeting") AFP Financial Planning & Analysis Learning System Session 1, Monday, April 3 rd (9:45-10:45) Time Value of Money and Capital Budgeting Chapters Covered Time Value of Money: Part I, Domain B Chapter 6 Net

AFP Financial Planning & Analysis Learning System Session 1, Monday, April 3 rd (9:45-10:45) Time Value of Money and Capital Budgeting Chapters Covered Time Value of Money: Part I, Domain B Chapter 6 Net

M d = PL( Y,i) P = price level. Y = real income or output. i = nominal interest rate earned by alternative nonmonetary assets

P = price level. Y = real income or output. i = nominal interest rate earned by alternative nonmonetary assets") Chapter 7 Demand for Money: the quantity of monetary assets people choose to hold. In our treatment of money as an asset we need to briefly discuss three aspects of any asset 1. Expected Return: Wealth

Chapter 7 Demand for Money: the quantity of monetary assets people choose to hold. In our treatment of money as an asset we need to briefly discuss three aspects of any asset 1. Expected Return: Wealth

Solution to Problem Set 1

M.I.T. Spring 999 Sloan School of Management 5.45 Solution to Problem Set. Investment has an NPV of 0000 + 20000 + 20% = 6667. Similarly, investments 2, 3, and 4 have NPV s of 5000, -47, and 267, respectively.

M.I.T. Spring 999 Sloan School of Management 5.45 Solution to Problem Set. Investment has an NPV of 0000 + 20000 + 20% = 6667. Similarly, investments 2, 3, and 4 have NPV s of 5000, -47, and 267, respectively.

Engineering Economics

Economic Analysis Methods Engineering Economics Day 3: Rate of Return Analysis Three commonly used economic analysis methods are 1. Present Worth Analysis 2. Annual Worth Analysis 3. www.engr.sjsu.edu/bjfurman/courses/me195/presentations/engeconpatel3nov4.ppt

Economic Analysis Methods Engineering Economics Day 3: Rate of Return Analysis Three commonly used economic analysis methods are 1. Present Worth Analysis 2. Annual Worth Analysis 3. www.engr.sjsu.edu/bjfurman/courses/me195/presentations/engeconpatel3nov4.ppt

Chapter 5: How to Value Bonds and Stocks

Chapter 5: How to Value Bonds and Stocks 5.1 The present value of any pure discount bond is its face value discounted back to the present. a. PV = F / (1+r) 10 = $1,000 / (1.05) 10 = $613.91 b. PV = $1,000

Chapter 5: How to Value Bonds and Stocks 5.1 The present value of any pure discount bond is its face value discounted back to the present. a. PV = F / (1+r) 10 = $1,000 / (1.05) 10 = $613.91 b. PV = $1,000

5.3 Amortization and Sinking Funds

5.3 Amortization and Sinking Funds Sinking Funds A sinking fund is an account that is set up for a specific purpose at some future date. Typical examples of this are retirement plans, saving money for

5.3 Amortization and Sinking Funds Sinking Funds A sinking fund is an account that is set up for a specific purpose at some future date. Typical examples of this are retirement plans, saving money for

January 29. Annuities

January 29 Annuities An annuity is a repeating payment, typically of a fixed amount, over a period of time. An annuity is like a loan in reverse; rather than paying a loan company, a bank or investment

January 29 Annuities An annuity is a repeating payment, typically of a fixed amount, over a period of time. An annuity is like a loan in reverse; rather than paying a loan company, a bank or investment

Solutions to Problems

Solutions to Problems 1. The investor would earn income of $2.25 and a capital gain of $52.50 $45 =$7.50. The total gain is $9.75 or 21.7%. $8.25 on a stock that paid $3.75 in income and sold for $67.50.

Solutions to Problems 1. The investor would earn income of $2.25 and a capital gain of $52.50 $45 =$7.50. The total gain is $9.75 or 21.7%. $8.25 on a stock that paid $3.75 in income and sold for $67.50.

Financial Economics: Household Saving and Investment Decisions

Financial Economics: Household Saving and Investment Decisions Shuoxun Hellen Zhang WISE & SOE XIAMEN UNIVERSITY Oct, 2016 1 / 32 Outline 1 A Life-Cycle Model of Saving 2 Taking Account of Social Security

Financial Economics: Household Saving and Investment Decisions Shuoxun Hellen Zhang WISE & SOE XIAMEN UNIVERSITY Oct, 2016 1 / 32 Outline 1 A Life-Cycle Model of Saving 2 Taking Account of Social Security

Practice Problems: Chapter 10 Savings, Investment Spending, and the Financial System

Practice Problems: Chapter 10 Savings, Investment Spending, and the Financial System 1. In a closed economy, all investment spending must come from: A) government. B) domestic savings. C) foreign savings.

Practice Problems: Chapter 10 Savings, Investment Spending, and the Financial System 1. In a closed economy, all investment spending must come from: A) government. B) domestic savings. C) foreign savings.

SECTION 6.1: Simple and Compound Interest

1 SECTION 6.1: Simple and Compound Interest Chapter 6 focuses on and various financial applications of interest. GOAL: Understand and apply different types of interest. Simple Interest If a sum of money

1 SECTION 6.1: Simple and Compound Interest Chapter 6 focuses on and various financial applications of interest. GOAL: Understand and apply different types of interest. Simple Interest If a sum of money

Time Value of Money. Lakehead University. Outline of the Lecture. Fall Future Value and Compounding. Present Value and Discounting

Time Value of Money Lakehead University Fall 2004 Outline of the Lecture Future Value and Compounding Present Value and Discounting More on Present and Future Values 2 Future Value and Compounding Future

Time Value of Money Lakehead University Fall 2004 Outline of the Lecture Future Value and Compounding Present Value and Discounting More on Present and Future Values 2 Future Value and Compounding Future

Chapter Review Problems

Chapter Review Problems Unit 9. Time-value-of-money terminology For Problems 9, assume you deposit $,000 today in a savings account. You earn 5% compounded quarterly. You deposit an additional $50 each

Chapter Review Problems Unit 9. Time-value-of-money terminology For Problems 9, assume you deposit $,000 today in a savings account. You earn 5% compounded quarterly. You deposit an additional $50 each

3.1 Simple Interest. Definition: I = Prt I = interest earned P = principal ( amount invested) r = interest rate (as a decimal) t = time

r = interest rate (as a decimal) t = time") 3.1 Simple Interest Definition: I = Prt I = interest earned P = principal ( amount invested) r = interest rate (as a decimal) t = time An example: Find the interest on a boat loan of $5,000 at 16% for

3.1 Simple Interest Definition: I = Prt I = interest earned P = principal ( amount invested) r = interest rate (as a decimal) t = time An example: Find the interest on a boat loan of $5,000 at 16% for

Fin 5413: Chapter 04 - Fixed Interest Rate Mortgage Loans Page 1 Solutions to Problems - Chapter 4 Fixed Interest Rate Mortgage Loans

Fin 5413: Chapter 04 - Fixed Interest Rate Mortgage Loans Page 1 Solutions to Problems - Chapter 4 Fixed Interest Rate Mortgage Loans Problem 4-1 A borrower makes a fully amortizing CPM mortgage loan.

Fin 5413: Chapter 04 - Fixed Interest Rate Mortgage Loans Page 1 Solutions to Problems - Chapter 4 Fixed Interest Rate Mortgage Loans Problem 4-1 A borrower makes a fully amortizing CPM mortgage loan.

SAVING, INVESTMENT, AND THE FINANCIAL SYSTEM

13 SAVING, INVESTMENT, AND THE FINANCIAL SYSTEM LEARNING OBJECTIVES: By the end of this chapter, students should understand: some of the important financial institutions in the U.S. economy. how the financial

13 SAVING, INVESTMENT, AND THE FINANCIAL SYSTEM LEARNING OBJECTIVES: By the end of this chapter, students should understand: some of the important financial institutions in the U.S. economy. how the financial

Finance 100 Problem Set 6 Futures (Alternative Solutions)

") Finance 100 Problem Set 6 Futures (Alternative Solutions) Note: Where appropriate, the final answer for each problem is given in bold italics for those not interested in the discussion of the solution.

Finance 100 Problem Set 6 Futures (Alternative Solutions) Note: Where appropriate, the final answer for each problem is given in bold italics for those not interested in the discussion of the solution.

CAPITAL BUDGETING Shenandoah Furniture, Inc.

CAPITAL BUDGETING Shenandoah Furniture, Inc. Shenandoah Furniture is considering replacing one of the machines in its manufacturing facility. The cost of the new machine will be $76,120. Transportation

CAPITAL BUDGETING Shenandoah Furniture, Inc. Shenandoah Furniture is considering replacing one of the machines in its manufacturing facility. The cost of the new machine will be $76,120. Transportation

The three formulas we use most commonly involving compounding interest n times a year are

Section 6.6 and 6.7 with finance review questions are included in this document for your convenience for studying for quizzes and exams for Finance Calculations for Math 11. Section 6.6 focuses on identifying

Section 6.6 and 6.7 with finance review questions are included in this document for your convenience for studying for quizzes and exams for Finance Calculations for Math 11. Section 6.6 focuses on identifying

True or False: Present Worth Analysis is done to maximize the NPV

ENGM 401 & 620 X1 Fundamentals of Engineering Finance Fall 2010 Lecture 24: Present Worth Analysis (2) It takes a lot of money to make these dreams come true. - Walt Disney M.G. Lipsett University of Alberta

ENGM 401 & 620 X1 Fundamentals of Engineering Finance Fall 2010 Lecture 24: Present Worth Analysis (2) It takes a lot of money to make these dreams come true. - Walt Disney M.G. Lipsett University of Alberta

REVIEW MATERIALS FOR REAL ESTATE FUNDAMENTALS

REVIEW MATERIALS FOR REAL ESTATE FUNDAMENTALS 1997, Roy T. Black J. Andrew Hansz, Ph.D., CFA REAE 3325, Fall 2005 University of Texas, Arlington Department of Finance and Real Estate CONTENTS ITEM ANNUAL

REVIEW MATERIALS FOR REAL ESTATE FUNDAMENTALS 1997, Roy T. Black J. Andrew Hansz, Ph.D., CFA REAE 3325, Fall 2005 University of Texas, Arlington Department of Finance and Real Estate CONTENTS ITEM ANNUAL

Math 34: Section 7.2 (Bonds)

") Math 34: 2016 Section 7.2 (Bonds) Bond is a type of promissory note. A bond written agreement between borrower and a lender specifying the terms of the loan. We usually use the word bond when the borrower

Math 34: 2016 Section 7.2 (Bonds) Bond is a type of promissory note. A bond written agreement between borrower and a lender specifying the terms of the loan. We usually use the word bond when the borrower