36106 Managerial Decision Modeling Monte Carlo Simulation in Excel: Part I

|

|

|

- Osborne Hensley

- 6 years ago

- Views:

Transcription

1 36106 Managerial Decision Modeling Monte Carlo Simulation in Excel: Part I Kipp Martin University of Chicago Booth School of Business November 1, 2017

2 Reading and Excel Files Reading: Powell and Baker: Chapter 14, See the Documentation and Examples folders in the Palisade RISK6 directory that was installed with your software. Files used in this lecture: retirement.xlsx retirementrisk.xlsx riskstatic.xlsx retirementriskgoal.xlsx

3 Learning Objectives 1. Understand why stochastic models are important 2. Understand the Flaw of Averages a truly critical concept for anyone working with spreadsheets perhaps the biggest takeaway of the quarter 3. Learn to run a basic Monte Carlo simulation learn how to replace a parameter with a distribution learn how to use simulation result statistical functions 4. Learn to Goal Seek

4 Lecture Outline Software Install Motivation The Flaw of Averages Simulation Basics Simulation Goal Seek Summary

5 5 Software Install DecisionTools Suite After installing the Precision Tools Suite: 1. Click on icon on your desktop 2. Use AddIns to on the Ribbon for future use.

6 Software Install DecisionTools Suite 6 From now on, you can open Excel and do not need to use the desktop icons. You should see Tab items for both PrecisionTree

7 7 Software Install DecisionTools Suite Tips: turn off extra CPU s close other apps minimize number of open workbooks

8 Software Install DecisionTools Suite 8 Tips: Mac User Setting for VM Ware

9 Where We Are Headed The natural progression of modeling: 1. Build a purely deterministic model all parameters known with certainty 2. Build a model (like Markowitz) where certain parameters are means and variances of a statistical distribution 3. Build a model where parameters are actually a random variable (a statistical distribution)

10 Where We Are Headed We are taking tools from earlier in the quarter and extending them to allow for stochastic parameters. Deterministic Tool Stochastic Tool Goal Goal Seek (Week 7) Data RiskSimtable (Week 8) Optimizer (Week 10) Important: Understand the difference between a deterministic model and stochastic model.

11 Motivation The Flaw of Averages Here is the key concept or big take away: If there are numbers in your spreadsheet that are not known with certainty, putting in estimated average values can lead to terrible results! we will enter distributions rather than numbers into cells. Consider the following retirement example:

12 Motivation The Flaw of Averages 12 Assume a retirement 401 K account of $200,000 in the S&P. You want to withdraw equal amounts for the next 20 years until the fund is depleted. How much can you withdraw each year before hitting 0 at the end of year 20? Please open Workbook retirement.xlsx.

13 Motivation The Flaw of Averages In Workbook retirement.xlsx there are two spreadsheets: S&P 500: this spreadsheet has the S&P returns for This also has the calculations: 1. mean = standard deviation = model: this spreadsheet has the retirement calculations

14 Motivation The Flaw of Averages 14 A Few Things: 1. I am using the arithmetic mean not the geometric mean. 2. I am using annual compounding. 3. You may wish to use continuous compounding. 4. With continuous compounding, the arithmetic and geometric mean the same. 5. Using continuous does not affect the result I am demonstrating.

15 Motivation The Flaw of Averages Take a first cut using the PMT function in Excel. See cell B6, it has range name payment. There are five arguments: rate the interest rate to use in the calculation nper the number of payment periods pv the present value of your money, in this example the $200,000 at the beginning of the period fv the future value what you want to end up with after all the payments are made, in our case 0 type 0 if payments made at the end of the period, 1 if made at the beginning, the value is 0 if this argument is omitted

16 Motivation The Flaw of Averages 16 In this example we use the formula in cell named payment which is =PMT(interest_rate,years,-savings,0,1) and this translates to PMT(.1155, 20, , 0, 1) The value is $23, If you take out $23,327.72, while earning 11.55% on your money each year, you will drawn the account down to 0 at the end of 20 years.

17 17 Motivation The Flaw of Averages See the spreadsheet retirement.xls.

18 Motivation The Flaw of Averages See the spreadsheet retirement.xls. The key formulas are in columns B and E. For example, in cell B14 we have E13 This says that the amount of money at the start of year 3 is equal to the amount of money at the end of year 2. In cell E14 we have =IF(D14 > B14, 0, (1 + C14)*(B14-D14)) In the formula above we are saying that if the withdrawal amount is less than what we have in the account, the amount in the account at the end of the year is the beginning balance minus the withdrawal times (1 + return).

19 Motivation The Flaw of Averages In this analysis we assume that the S&P return is a constant 11.55% per year. But 11.55% per year is the average from Historically, the standard deviation over this period is 20.62% There is a serious problem with this!

20 Motivation The Flaw of Averages In the spreadsheet retirement.xls we make calculations based on the average interest rate. Everything is deterministic! In the spreadsheet retirementrisk.xls we use random interest rates with a mean of 11.55% and standard deviation of 20.62%. We simulate reality. Don t worry about how to generate random interest rates for now. First, let s look at some potential retirement scenarios. Then we will recreate retirementrisk.xls from retirement.xlsx.

21 21 Motivation The Flaw of Averages Argle Bargle!!! I am out of money after only five years! Handout anyone?

22 22 Motivation The Flaw of Averages What! Now I die with $561,151 left unspent. That is NOT fair!

23 23 Motivation The Flaw of Averages Argle Bargle!!! Out of money yet again.

24 Motivation The Flaw of Averages 24 Living a thousand lives. Distribution of years.

25 Motivation The Flaw of Averages 25 Living a thousand lives, cumulative probabilities.

26 Motivation The Flaw of Averages Sam Savage has a good explanation for what is going on. See his book the Flaw of Averages YouTube link

27 Motivation The Flaw of Averages This lecture is best summed up by the pictures on the following slides. The first picture was shamelessly stolen from the Web site of Sam Savage. But Sam is a nice guy and probably will not sue me. The second picture was from the San Jose Mercury Times. Hopefully they won t sue either.

28 Motivation The Flaw of Averages 28

29 Motivation The Flaw of Averages 29

30 Motivation The Flaw of Averages The bottom line the average can be pretty useless! A second rule of thumb: The more nonlinear the problem, the worse our results will be by using average values. Here is the problem: E(f (X )) f (E(X )) When you put average values into the cells (i.e. E(X )) you are calculating f (E(X )) but you really want E(f (X )). What is X in our retirement example? What is f (X ) in our case? Warning: f (X ) is a real ARGLE BARGLE!

31 Motivation The Flaw of Averages 31 In our case, f (X ) is COUNTIF(E12:E31,">0") and X corresponds to the values in C12:31. Not only is an IF involved, but we are counting IF statements! Pass me the defibrillator please!

32 32 Motivation The Flaw of Averages The Trace Precedents for f (X )!

33 Motivation The Flaw of Averages Here is a good example to help your intuition on why E(f (X )) f (E(X )) Consider a random variable X that can take on two values: the two values are X = 1 and X = 1 (the market is either up or down). Assume each event is equally likely and so the probabilities are: p(x = 1) =.5 and p(x = 1) =.5. The function of interest is: f (X ) = max(0, X ). What is f (E(X ))? What is E(f (X ))?

34 Motivation The Flaw of Averages What is f (E(X ))? E(X ) = = 0 f (E(X )) = f (0) = max(0, 0) = 0 What is E(f (X ))? E(f (X )) =.5 max(0, 1) +.5 max(0, 1) = =.5 E(f (X )) f (E(X ))

35 Motivation The Flaw of Averages Remember: A linear life is a good life. Some bad functions: IF MAX, MIN COUNTIF Before you took this course, you probably thought the IF function in Excel was pretty nice. Little did you know of the dangers that lurked below.

36 Simulation Basics Our goal is to replace parameters with distributions. We then sample from the distributions.

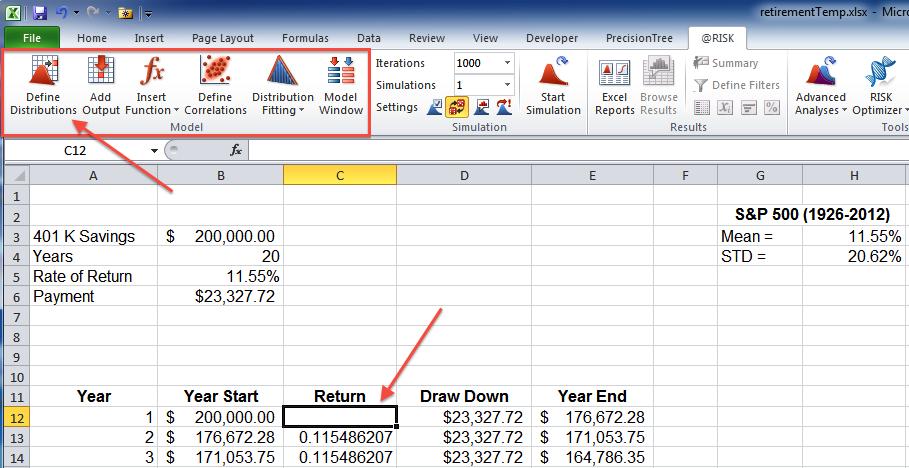

37 Simulation Basics In the following slides we take the workbook retirement.xlsx and create the content in workbook retirementrisk.xlsx. Step 1: use the Excel function COUNTIF. Put the formula =COUNTIF(E12:E31,">0") in cell E32. This will count the number of years where we end the year with a positive amount of money. Objective: run a 1000 trials and see the behavior of this number.

38 Simulation Basics Step 2 Incorporate Uncertainty: Here is how we incorporate uncertainty. We were using average values for the rates of return. This changes. In Column C, replace the fixed rates with random draws. Select Tab in the Ribbon. Select and clear the contents of cell C12. Select Cell C12 and then Define Distribution from the Model group. See next slide.

39 Simulation Basics 39

40 Simulation Basics 40 When you click on Define Distribution you will see: Select the Normal Distribution.

41 Simulation Basics 41 Put in the mean and standard deviation. Note the absolute addressing $H$3 and $H$4. We could have used the range names mean and std.

42 Simulation Basics We used Define Distributions to put in a distribution. Other options include: Use the Insert Function Just type it in (there is auto completion available)

43 Simulation Basics Step 3: Copy Cell C12 and paste it to Cells C13 to C31. Every time you recalculate the spreadsheet (F9 or recalculate under Formulas). We make a draw of a rate of return from the normal distribution with mean.1155 and standard deviation.2062 for cells C12 - C31. These draws are all independent of each other. That is, they are not correlated. More on this topic later. Make the font in cells C12 - C31 magenta. We are going to make our uncertain parameter cells magenta. I am open to other color selections.

44 Simulation Basics Step 4: Now, back to Cell E32. This is the cell we care about. It is telling how many years we end with a positive amount of money (a good thing). Key Idea: Cell E32 is really a random variable. Its value depends on other random variables. We care about the probability distribution of Cell E32! We to consider Cell E32 an output cell. See next slide.

45 Simulation Basics 45 Select Cell E32 and then click Add Output from the Model group.

46 Simulation Basics In Cell E32 you should see will now treat Cell E32 as a random variable and generate probability distribution information for the cell output.

47 Simulation Basics 47 Step 5: Run the simulation! My default is set for a 1000 trials. Don t worry about how many trials for now.

48 Simulation Basics 48 Step 5: Examine the output for Cell E32.

49 Simulation Basics 49 Here is the cumulative histogram.

50 Simulation Basics 50 How to stop the simulation. What to do if your simulation seems to be taking too long.

51 Simulation Basics 51 You can adjust the tails of the histogram by dragging or typing in the tail value you care about.

52 Simulation Basics 52 Other Hints: 1. The simulation will run much faster if you turn demo off. 2. I recommend you turn on Automatically Show Output Graph.

53 Simulation Basics Other Distributions: In Week 9 we will discuss more thoroughly selecting distributions for simulation. For now we consider two other distributions: (see riskstatic.xlsx) 1. RiskDiscrete 2. RiskUniform

54 Simulation Basics 54 Risk Discrete Distribution

55 Simulation Basics 55 Risk Uniform Distribution

56 Simulation Basics Sample Exam Question 1: In the retirement example, what is f(e(x)) when the payment is $23, and f(payment, returns) = COUNTIF(E12:E31,">0") Sample Exam Question 2: In this example, what is E(f(X)) when the payment is $23, and f(payment, returns) = COUNTIF(E12:E31,">0")

57 Simulation Basics The bottom line using averages can lead to bad results when the standard deviation is large! A rule of thumb: The greater the variance, the worse our results will be by using average values. The average high temperature for Chicago on April 1 is 53 degrees. Conclusion: If I wear a light jacket walking to the Harper Center I will be comfortable. The average high temperature for Honolulu on April 1 is 82 degrees. Conclusion: If I wear a tee shirt and jeans I will be comfortable.

58 Simulation Basics The bottom line using averages can lead to bad results when the standard deviation is large! Running Running Back 1 Back 2 Avg. yrds. per carry Std. Dev Situation 1: Own 20, ahead by 1 point, 5 minutes left in fourth quarter. Which back should carry? Situation 2: Own 20, down by 1 point, 5 minutes left in fourth quarter. Which back should carry?

59 Simulation Basics Summary: Using an expected value instead of a distribution is bad. Nonlinearity makes this even worse. Big standard deviations make this even worse.

60 Simulation Basics Color Coding: Black a parameter cell known with certainty (or at least treated as such) Magenta an uncertain parameter cell, one with distribution Blue an adjustable cell, a variable cell, something that we choose using Goal Seek or RiskSimtable() Green output cell (contains =RiskOutput() from Add Output)

61 Simulation Goal Seek 61 If we withdraw $23, per year, on average, it will last years. Not very satisfying. Even worse, there was a draw of only 3 years. Let turn the question around and see how much we can take out each year, and have a minimum draw of 18. there is a Goal Seek very similar to the Excel Goal Seek we used earlier in the quarter.

62 Simulation Goal Seek 62 The Goal cell is E32. This is the cell that counts the number of periods with a positive amount of money. We are interested in recording the minimum number of years for this cell. We change cell B6 which is the amount of money we withdraw each year.

63 Simulation Goal Seek 63 Notice we are restricting our search to be between 0 dollars and dollars.

64 Simulation Goal Seek 64 We should withdraw $4, Notice we did only 500 iterations per simulation. This should probably be larger.

65 Simulation Goal Seek Note: If you did not invest in the market, and got a 0 percent rate of return each year, you could withdraw $10,000 a year and die with zero dollars left. This suggests running a more complicated simulation where you can allocate your money between the stock market and a less risky asset.

66 Summary 66 Running a simulation creates a histogram for each cell in the spreadsheet that contains a RiskOutput(). You can put the summary statistics from the simulation directly in the spreadsheet.

67 Summary 67 You can insert functions with Insert Function, Statistic Functions, then Simulation Result.

68 Summary See the workbook retirementrisk. 1. In cell E33 I have inserted =RiskMean(E32,1). 2. In cell E34 I have inserted =RiskVariance(E32,1). After running a new simulation, these cells will hold, respectively, the simulation sample mean and variance. Cell E32 is the output of the simulation, it is =RiskOutput()+COUNTIF(E12:E31,">0").

69 Summary What we are doing is called Monte Carlo Simulation. The process was developed by Stanislaw Ulam and Nicholas Metropolis. Process developed while working on nuclear weapons projects at Los Alamos. Named after Monte Carlo where Ulam s uncle often gambled. Building a Monte Carlo Simulation Model: 1. Identify model inputs: deterministic inputs (black cells) random inputs (magenta cells) must also determine the distribution 2. Identify decision variable or variables (blue cells) 3. Identify model outputs (green cells) 4. Run the simulation 5. Analyze the outputs

70 Summary The benefit of Monte Carlo simulation Booth Students winning the 2012 SABR (Society for American Baseball Research) Competition. One of the things that distinguished the Booth (presentation) was their outstanding use of risk analysis, particularly their Monte Carlo simulations on playoff probabilities and (looking at) some of the other considerations that weighed into their decision, Gennaro (society president) said.

71 Summary Deja Vu all over again. Sample Exam Question: In this example, what is f(e(x))? Sample Exam Question: In this example, what is E(f(X))? You must understand the difference between E(f (X )) and f (E(X )). KEY CONCEPT: Even when E(f (X )) = f (E(X )) simulation is very useful. Why?

36106 Managerial Decision Modeling Monte Carlo Simulation in Excel: Part II

36106 Managerial Decision Modeling Monte Carlo Simulation in Excel: Part II Kipp Martin University of Chicago Booth School of Business November 8, 2017 Reading and Excel Files Reading: Powell and Baker:

36106 Managerial Decision Modeling Monte Carlo Simulation in Excel: Part II Kipp Martin University of Chicago Booth School of Business November 8, 2017 Reading and Excel Files Reading: Powell and Baker:

36106 Managerial Decision Modeling Decision Analysis in Excel

36106 Managerial Decision Modeling Decision Analysis in Excel Kipp Martin University of Chicago Booth School of Business October 19, 2017 Reading and Excel Files Reading: Powell and Baker: Sections 13.1,

36106 Managerial Decision Modeling Decision Analysis in Excel Kipp Martin University of Chicago Booth School of Business October 19, 2017 Reading and Excel Files Reading: Powell and Baker: Sections 13.1,

36106 Managerial Decision Modeling Monte Carlo Simulation in Excel: Part IV

36106 Managerial Decision Modeling Monte Carlo Simulation in Excel: Part IV Kipp Martin University of Chicago Booth School of Business November 29, 2017 Reading and Excel Files 2 Reading: Handout: Optimal

36106 Managerial Decision Modeling Monte Carlo Simulation in Excel: Part IV Kipp Martin University of Chicago Booth School of Business November 29, 2017 Reading and Excel Files 2 Reading: Handout: Optimal

36106 Managerial Decision Modeling Monte Carlo Simulation in Excel: Part III

36106 Managerial Decision Modeling Monte Carlo Simulation in Excel: Part III Kipp Martin University of Chicago Booth School of Business November 15, 2017 Reading and Excel Files 2 Reading: Powell and Baker:

36106 Managerial Decision Modeling Monte Carlo Simulation in Excel: Part III Kipp Martin University of Chicago Booth School of Business November 15, 2017 Reading and Excel Files 2 Reading: Powell and Baker:

Decision Trees: Booths

DECISION ANALYSIS Decision Trees: Booths Terri Donovan recorded: January, 2010 Hi. Tony has given you a challenge of setting up a spreadsheet, so you can really understand whether it s wiser to play in

DECISION ANALYSIS Decision Trees: Booths Terri Donovan recorded: January, 2010 Hi. Tony has given you a challenge of setting up a spreadsheet, so you can really understand whether it s wiser to play in

36106 Managerial Decision Modeling Sensitivity Analysis

1 36106 Managerial Decision Modeling Sensitivity Analysis Kipp Martin University of Chicago Booth School of Business September 26, 2017 Reading and Excel Files 2 Reading (Powell and Baker): Section 9.5

1 36106 Managerial Decision Modeling Sensitivity Analysis Kipp Martin University of Chicago Booth School of Business September 26, 2017 Reading and Excel Files 2 Reading (Powell and Baker): Section 9.5

DECISION SUPPORT Risk handout. Simulating Spreadsheet models

DECISION SUPPORT MODELS @ Risk handout Simulating Spreadsheet models using @RISK 1. Step 1 1.1. Open Excel and @RISK enabling any macros if prompted 1.2. There are four on-line help options available.

DECISION SUPPORT MODELS @ Risk handout Simulating Spreadsheet models using @RISK 1. Step 1 1.1. Open Excel and @RISK enabling any macros if prompted 1.2. There are four on-line help options available.

PSCM_ Data Analytics

PSCM_7217.1.1 Data Analytics Excel Functions and Simulation Sang Jo Kim July 4, 2015 * Reference - Business Analytics: Methods, Models, and Decisions (1 st edition, James R. Evans, Pearson) Contents Excel

PSCM_7217.1.1 Data Analytics Excel Functions and Simulation Sang Jo Kim July 4, 2015 * Reference - Business Analytics: Methods, Models, and Decisions (1 st edition, James R. Evans, Pearson) Contents Excel

Business Statistics 41000: Probability 4

Business Statistics 41000: Probability 4 Drew D. Creal University of Chicago, Booth School of Business February 14 and 15, 2014 1 Class information Drew D. Creal Email: dcreal@chicagobooth.edu Office:

Business Statistics 41000: Probability 4 Drew D. Creal University of Chicago, Booth School of Business February 14 and 15, 2014 1 Class information Drew D. Creal Email: dcreal@chicagobooth.edu Office:

Lecture 10. Ski Jacket Case Profit calculation Spreadsheet simulation Analysis of results Summary and Preparation for next class

Decision Models Lecture 10 1 Lecture 10 Ski Jacket Case Profit calculation Spreadsheet simulation Analysis of results Summary and Preparation for next class Yield Management Decision Models Lecture 10

Decision Models Lecture 10 1 Lecture 10 Ski Jacket Case Profit calculation Spreadsheet simulation Analysis of results Summary and Preparation for next class Yield Management Decision Models Lecture 10

Business Statistics 41000: Probability 3

Business Statistics 41000: Probability 3 Drew D. Creal University of Chicago, Booth School of Business February 7 and 8, 2014 1 Class information Drew D. Creal Email: dcreal@chicagobooth.edu Office: 404

Business Statistics 41000: Probability 3 Drew D. Creal University of Chicago, Booth School of Business February 7 and 8, 2014 1 Class information Drew D. Creal Email: dcreal@chicagobooth.edu Office: 404

Full Monte. Looking at your project through rose-colored glasses? Let s get real.

Realistic plans for project success. Looking at your project through rose-colored glasses? Let s get real. Full Monte Cost and schedule risk analysis add-in for Microsoft Project that graphically displays

Realistic plans for project success. Looking at your project through rose-colored glasses? Let s get real. Full Monte Cost and schedule risk analysis add-in for Microsoft Project that graphically displays

Excel Tutorial 9: Working with Financial Tools and Functions TRUE/FALSE 1. The fv argument is required in the PMT function.

Excel Tutorial 9: Working with Financial Tools and Functions TRUE/FALSE 1. The fv argument is required in the PMT function. ANS: F PTS: 1 REF: EX 493 2. Cash flow has nothing to do with who owns the money.

Excel Tutorial 9: Working with Financial Tools and Functions TRUE/FALSE 1. The fv argument is required in the PMT function. ANS: F PTS: 1 REF: EX 493 2. Cash flow has nothing to do with who owns the money.

Simulation. Decision Models

Lecture 9 Decision Models Decision Models: Lecture 9 2 Simulation What is Monte Carlo simulation? A model that mimics the behavior of a (stochastic) system Mathematically described the system using a set

Lecture 9 Decision Models Decision Models: Lecture 9 2 Simulation What is Monte Carlo simulation? A model that mimics the behavior of a (stochastic) system Mathematically described the system using a set

The Binomial Distribution

The Binomial Distribution January 31, 2018 Contents The Binomial Distribution The Normal Approximation to the Binomial The Binomial Hypothesis Test Computing Binomial Probabilities in R 30 Problems The

The Binomial Distribution January 31, 2018 Contents The Binomial Distribution The Normal Approximation to the Binomial The Binomial Hypothesis Test Computing Binomial Probabilities in R 30 Problems The

36106 Managerial Decision Modeling Modeling with Integer Variables Part 1

1 36106 Managerial Decision Modeling Modeling with Integer Variables Part 1 Kipp Martin University of Chicago Booth School of Business September 26, 2017 Reading and Excel Files 2 Reading (Powell and Baker):

1 36106 Managerial Decision Modeling Modeling with Integer Variables Part 1 Kipp Martin University of Chicago Booth School of Business September 26, 2017 Reading and Excel Files 2 Reading (Powell and Baker):

The Binomial Distribution

The Binomial Distribution January 31, 2019 Contents The Binomial Distribution The Normal Approximation to the Binomial The Binomial Hypothesis Test Computing Binomial Probabilities in R 30 Problems The

The Binomial Distribution January 31, 2019 Contents The Binomial Distribution The Normal Approximation to the Binomial The Binomial Hypothesis Test Computing Binomial Probabilities in R 30 Problems The

CHAPTER 11. Topics. Cash Flow Estimation and Risk Analysis. Estimating cash flows: Relevant cash flows Working capital treatment

CHAPTER 11 Cash Flow Estimation and Risk Analysis 1 Topics Estimating cash flows: Relevant cash flows Working capital treatment Risk analysis: Sensitivity analysis Scenario analysis Simulation analysis

CHAPTER 11 Cash Flow Estimation and Risk Analysis 1 Topics Estimating cash flows: Relevant cash flows Working capital treatment Risk analysis: Sensitivity analysis Scenario analysis Simulation analysis

MA 1125 Lecture 14 - Expected Values. Wednesday, October 4, Objectives: Introduce expected values.

MA 5 Lecture 4 - Expected Values Wednesday, October 4, 27 Objectives: Introduce expected values.. Means, Variances, and Standard Deviations of Probability Distributions Two classes ago, we computed the

MA 5 Lecture 4 - Expected Values Wednesday, October 4, 27 Objectives: Introduce expected values.. Means, Variances, and Standard Deviations of Probability Distributions Two classes ago, we computed the

This homework assignment uses the material on pages ( A moving average ).

.") Module 2: Time series concepts HW Homework assignment: equally weighted moving average This homework assignment uses the material on pages 14-15 ( A moving average ). 2 Let Y t = 1/5 ( t + t-1 + t-2 +

Module 2: Time series concepts HW Homework assignment: equally weighted moving average This homework assignment uses the material on pages 14-15 ( A moving average ). 2 Let Y t = 1/5 ( t + t-1 + t-2 +

Yield Management. Decision Models

Decision Models: Lecture 10 2 Decision Models Yield Management Yield management is the process of allocating different types of capacity to different customers at different prices in order to maximize

Decision Models: Lecture 10 2 Decision Models Yield Management Yield management is the process of allocating different types of capacity to different customers at different prices in order to maximize

How to Consider Risk Demystifying Monte Carlo Risk Analysis

How to Consider Risk Demystifying Monte Carlo Risk Analysis James W. Richardson Regents Professor Senior Faculty Fellow Co-Director, Agricultural and Food Policy Center Department of Agricultural Economics

How to Consider Risk Demystifying Monte Carlo Risk Analysis James W. Richardson Regents Professor Senior Faculty Fellow Co-Director, Agricultural and Food Policy Center Department of Agricultural Economics

Real Options Valuation, Inc. Software Technical Support

Real Options Valuation, Inc. Software Technical Support HELPFUL TIPS AND TECHNIQUES Johnathan Mun, Ph.D., MBA, MS, CFC, CRM, FRM, MIFC 1 P a g e Helpful Tips and Techniques The following are some quick

Real Options Valuation, Inc. Software Technical Support HELPFUL TIPS AND TECHNIQUES Johnathan Mun, Ph.D., MBA, MS, CFC, CRM, FRM, MIFC 1 P a g e Helpful Tips and Techniques The following are some quick

ExcelSim 2003 Documentation

ExcelSim 2003 Documentation Note: The ExcelSim 2003 add-in program is copyright 2001-2003 by Timothy R. Mayes, Ph.D. It is free to use, but it is meant for educational use only. If you wish to perform

ExcelSim 2003 Documentation Note: The ExcelSim 2003 add-in program is copyright 2001-2003 by Timothy R. Mayes, Ph.D. It is free to use, but it is meant for educational use only. If you wish to perform

ExcelBasics.pdf. Here is the URL for a very good website about Excel basics including the material covered in this primer.

Excel Primer for Finance Students John Byrd, November 2015. This primer assumes you can enter data and copy functions and equations between cells in Excel. If you aren t familiar with these basic skills

Excel Primer for Finance Students John Byrd, November 2015. This primer assumes you can enter data and copy functions and equations between cells in Excel. If you aren t familiar with these basic skills

ESD.70J Engineering Economy

ESD.70J Engineering Economy Fall 2010 Session One Xin Zhang xinzhang@mit.edu Prof. Richard de Neufville ardent@mit.edu http://ardent.mit.edu/real_options/rocse_excel_latest/excel_class.html ESD.70J Engineering

ESD.70J Engineering Economy Fall 2010 Session One Xin Zhang xinzhang@mit.edu Prof. Richard de Neufville ardent@mit.edu http://ardent.mit.edu/real_options/rocse_excel_latest/excel_class.html ESD.70J Engineering

Project your expenses

Welcome to the Victory Cashflow worksheet. Spending just half an hour each month will ensure your budget is maintained and your finances are in order. The objective of this budget is to predict the future

Welcome to the Victory Cashflow worksheet. Spending just half an hour each month will ensure your budget is maintained and your finances are in order. The objective of this budget is to predict the future

Expected Return Methodologies in Morningstar Direct Asset Allocation

Expected Return Methodologies in Morningstar Direct Asset Allocation I. Introduction to expected return II. The short version III. Detailed methodologies 1. Building Blocks methodology i. Methodology ii.

Expected Return Methodologies in Morningstar Direct Asset Allocation I. Introduction to expected return II. The short version III. Detailed methodologies 1. Building Blocks methodology i. Methodology ii.

Steps for Software to Do Simulation Modeling (New Update 02/15/01)

") Steps for Using @RISK Software to Do Simulation Modeling (New Update 02/15/01) Important! Before we get to the steps, we want to provide several notes to help you do the steps. Use the browser s Back button

Steps for Using @RISK Software to Do Simulation Modeling (New Update 02/15/01) Important! Before we get to the steps, we want to provide several notes to help you do the steps. Use the browser s Back button

FORECASTING & BUDGETING

FORECASTING & BUDGETING W I T H E X C E L S S O L V E R WHAT IS SOLVER? Solver is an add-in that comes pre-built into Microsoft Excel. Simply put, it allows you to set an objective value which is subject

FORECASTING & BUDGETING W I T H E X C E L S S O L V E R WHAT IS SOLVER? Solver is an add-in that comes pre-built into Microsoft Excel. Simply put, it allows you to set an objective value which is subject

Further Mathematics 2016 Core: RECURSION AND FINANCIAL MODELLING Chapter 6 Interest and depreciation

Further Mathematics 2016 Core: RECURSION AND FINANCIAL MODELLING Chapter 6 Interest and depreciation Key knowledge the use of first- order linear recurrence relations to model flat rate and unit cost and

Further Mathematics 2016 Core: RECURSION AND FINANCIAL MODELLING Chapter 6 Interest and depreciation Key knowledge the use of first- order linear recurrence relations to model flat rate and unit cost and

A Probabilistic Approach to Determining the Number of Widgets to Build in a Yield-Constrained Process

A Probabilistic Approach to Determining the Number of Widgets to Build in a Yield-Constrained Process Introduction Timothy P. Anderson The Aerospace Corporation Many cost estimating problems involve determining

A Probabilistic Approach to Determining the Number of Widgets to Build in a Yield-Constrained Process Introduction Timothy P. Anderson The Aerospace Corporation Many cost estimating problems involve determining

The following content is provided under a Creative Commons license. Your support

MITOCW Recitation 6 The following content is provided under a Creative Commons license. Your support will help MIT OpenCourseWare continue to offer high quality educational resources for free. To make

MITOCW Recitation 6 The following content is provided under a Creative Commons license. Your support will help MIT OpenCourseWare continue to offer high quality educational resources for free. To make

Historic Volatility Calculator (HVC) Tutorial (Ver )

Tutorial (Ver )") Historic Volatility Calculator (HVC) Tutorial (Ver 1.03.01) Welcome to the Historic Volatility Calculator (HVC) provided to members of the Society of Financial Service Professionals by Hause Actuarial

Historic Volatility Calculator (HVC) Tutorial (Ver 1.03.01) Welcome to the Historic Volatility Calculator (HVC) provided to members of the Society of Financial Service Professionals by Hause Actuarial

Quantitative Trading System For The E-mini S&P

AURORA PRO Aurora Pro Automated Trading System Aurora Pro v1.11 For TradeStation 9.1 August 2015 Quantitative Trading System For The E-mini S&P By Capital Evolution LLC Aurora Pro is a quantitative trading

AURORA PRO Aurora Pro Automated Trading System Aurora Pro v1.11 For TradeStation 9.1 August 2015 Quantitative Trading System For The E-mini S&P By Capital Evolution LLC Aurora Pro is a quantitative trading

Pro Strategies Help Manual / User Guide: Last Updated March 2017

Pro Strategies Help Manual / User Guide: Last Updated March 2017 The Pro Strategies are an advanced set of indicators that work independently from the Auto Binary Signals trading strategy. It s programmed

Pro Strategies Help Manual / User Guide: Last Updated March 2017 The Pro Strategies are an advanced set of indicators that work independently from the Auto Binary Signals trading strategy. It s programmed

A useful modeling tricks.

.7 Joint models for more than two outcomes We saw that we could write joint models for a pair of variables by specifying the joint probabilities over all pairs of outcomes. In principal, we could do this

.7 Joint models for more than two outcomes We saw that we could write joint models for a pair of variables by specifying the joint probabilities over all pairs of outcomes. In principal, we could do this

Enventive Monte Carlo Analysis Tutorial Version 4.1.x

Enventive Monte Carlo Analysis Tutorial Version 4.1.x Copyright 2017 Enventive, Inc. All rights reserved. Table of Contents Welcome to the Monte Carlo Analysis Tutorial 1 Getting started 1 Complete the

Enventive Monte Carlo Analysis Tutorial Version 4.1.x Copyright 2017 Enventive, Inc. All rights reserved. Table of Contents Welcome to the Monte Carlo Analysis Tutorial 1 Getting started 1 Complete the

TIE2140 / IE2140e Engineering Economy Tutorial 6 (Lab 2) Engineering-Economic Decision Making Process using EXCEL

Engineering-Economic Decision Making Process using EXCEL") TIE2140 / IE2140e Engineering Economy Tutorial 6 (Lab 2) Engineering-Economic Decision Making Process using EXCEL Solutions Guide by Wang Xin, Hong Lanqing & Mei Wenjie 1. Learning Objectives In this lab-based

TIE2140 / IE2140e Engineering Economy Tutorial 6 (Lab 2) Engineering-Economic Decision Making Process using EXCEL Solutions Guide by Wang Xin, Hong Lanqing & Mei Wenjie 1. Learning Objectives In this lab-based

Copyright 2011 Pearson Education, Inc. Publishing as Addison-Wesley.

Appendix: Statistics in Action Part I Financial Time Series 1. These data show the effects of stock splits. If you investigate further, you ll find that most of these splits (such as in May 1970) are 3-for-1

Appendix: Statistics in Action Part I Financial Time Series 1. These data show the effects of stock splits. If you investigate further, you ll find that most of these splits (such as in May 1970) are 3-for-1

Simulation Lecture Notes and the Gentle Lentil Case

Simulation Lecture Notes and the Gentle Lentil Case General Overview of the Case What is the decision problem presented in the case? What are the issues Sanjay must consider in deciding among the alternative

Simulation Lecture Notes and the Gentle Lentil Case General Overview of the Case What is the decision problem presented in the case? What are the issues Sanjay must consider in deciding among the alternative

Definition 4.1. In a stochastic process T is called a stopping time if you can tell when it happens.

102 OPTIMAL STOPPING TIME 4. Optimal Stopping Time 4.1. Definitions. On the first day I explained the basic problem using one example in the book. On the second day I explained how the solution to the

102 OPTIMAL STOPPING TIME 4. Optimal Stopping Time 4.1. Definitions. On the first day I explained the basic problem using one example in the book. On the second day I explained how the solution to the

CHAPTER 12 APPENDIX Valuing Some More Real Options

CHAPTER 12 APPENDIX Valuing Some More Real Options This appendix demonstrates how to work out the value of different types of real options. By assuming the world is risk neutral, it is ignoring the fact

CHAPTER 12 APPENDIX Valuing Some More Real Options This appendix demonstrates how to work out the value of different types of real options. By assuming the world is risk neutral, it is ignoring the fact

STA Module 3B Discrete Random Variables

STA 2023 Module 3B Discrete Random Variables Learning Objectives Upon completing this module, you should be able to 1. Determine the probability distribution of a discrete random variable. 2. Construct

STA 2023 Module 3B Discrete Random Variables Learning Objectives Upon completing this module, you should be able to 1. Determine the probability distribution of a discrete random variable. 2. Construct

Demo 3 - Forecasting Calculator with F.A.S.T. Graphs. Transcript for video located at:

Demo 3 - Forecasting Calculator with F.A.S.T. Graphs Transcript for video located at: http://www.youtube.com/watch?v=de29rsru9js This FAST Graphs, Demo Number 3, will look at the FAST Graphs forecasting

Demo 3 - Forecasting Calculator with F.A.S.T. Graphs Transcript for video located at: http://www.youtube.com/watch?v=de29rsru9js This FAST Graphs, Demo Number 3, will look at the FAST Graphs forecasting

Real Options for Engineering Systems

Real Options for Engineering Systems Session 1: What s wrong with the Net Present Value criterion? Stefan Scholtes Judge Institute of Management, CU Slide 1 Main issues of the module! Project valuation:

Real Options for Engineering Systems Session 1: What s wrong with the Net Present Value criterion? Stefan Scholtes Judge Institute of Management, CU Slide 1 Main issues of the module! Project valuation:

Chapter 8 Statistical Intervals for a Single Sample

Chapter 8 Statistical Intervals for a Single Sample Part 1: Confidence intervals (CI) for population mean µ Section 8-1: CI for µ when σ 2 known & drawing from normal distribution Section 8-1.2: Sample

Chapter 8 Statistical Intervals for a Single Sample Part 1: Confidence intervals (CI) for population mean µ Section 8-1: CI for µ when σ 2 known & drawing from normal distribution Section 8-1.2: Sample

1) Cash Flow Pattern Diagram for Future Value and Present Value of Irregular Cash Flows

Cash Flow Pattern Diagram for Future Value and Present Value of Irregular Cash Flows") Topics Excel & Business Math Video/Class Project #45 Cash Flow Analysis for Annuities: Savings Plans, Asset Valuation, Retirement Plans and Mortgage Loan. FV, PV and PMT. 1) Cash Flow Pattern Diagram for

Topics Excel & Business Math Video/Class Project #45 Cash Flow Analysis for Annuities: Savings Plans, Asset Valuation, Retirement Plans and Mortgage Loan. FV, PV and PMT. 1) Cash Flow Pattern Diagram for

Intro to Retirement. Part 2: Types of Retirement Accounts

Intro to Retirement Part 2: Types of Retirement Accounts There are 7 slides you are expected to read and understand on your own. You will be quizzed on all concepts that are underlined, bolded, or boxed.

Intro to Retirement Part 2: Types of Retirement Accounts There are 7 slides you are expected to read and understand on your own. You will be quizzed on all concepts that are underlined, bolded, or boxed.

STA Rev. F Learning Objectives. What is a Random Variable? Module 5 Discrete Random Variables

STA 2023 Module 5 Discrete Random Variables Learning Objectives Upon completing this module, you should be able to: 1. Determine the probability distribution of a discrete random variable. 2. Construct

STA 2023 Module 5 Discrete Random Variables Learning Objectives Upon completing this module, you should be able to: 1. Determine the probability distribution of a discrete random variable. 2. Construct

FEEG6017 lecture: The normal distribution, estimation, confidence intervals. Markus Brede,

FEEG6017 lecture: The normal distribution, estimation, confidence intervals. Markus Brede, mb8@ecs.soton.ac.uk The normal distribution The normal distribution is the classic "bell curve". We've seen that

FEEG6017 lecture: The normal distribution, estimation, confidence intervals. Markus Brede, mb8@ecs.soton.ac.uk The normal distribution The normal distribution is the classic "bell curve". We've seen that

CHAPTER 11. Proposed Project Data. Topics. Cash Flow Estimation and Risk Analysis. Estimating cash flows:

CHAPTER 11 Cash Flow Estimation and Risk Analysis 1 Topics Estimating cash flows: Relevant cash flows Working capital treatment Inflation Risk Analysis: Sensitivity Analysis, Scenario Analysis, and Simulation

CHAPTER 11 Cash Flow Estimation and Risk Analysis 1 Topics Estimating cash flows: Relevant cash flows Working capital treatment Inflation Risk Analysis: Sensitivity Analysis, Scenario Analysis, and Simulation

We use probability distributions to represent the distribution of a discrete random variable.

Now we focus on discrete random variables. We will look at these in general, including calculating the mean and standard deviation. Then we will look more in depth at binomial random variables which are

Now we focus on discrete random variables. We will look at these in general, including calculating the mean and standard deviation. Then we will look more in depth at binomial random variables which are

Handout 5: Summarizing Numerical Data STAT 100 Spring 2016

In this handout, we will consider methods that are appropriate for summarizing a single set of numerical measurements. Definition Numerical Data: A set of measurements that are recorded on a naturally

In this handout, we will consider methods that are appropriate for summarizing a single set of numerical measurements. Definition Numerical Data: A set of measurements that are recorded on a naturally

Acritical aspect of any capital budgeting decision. Using Excel to Perform Monte Carlo Simulations TECHNOLOGY

Using Excel to Perform Monte Carlo Simulations By Thomas E. McKee, CMA, CPA, and Linda J.B. McKee, CPA Acritical aspect of any capital budgeting decision is evaluating the risk surrounding key variables

Using Excel to Perform Monte Carlo Simulations By Thomas E. McKee, CMA, CPA, and Linda J.B. McKee, CPA Acritical aspect of any capital budgeting decision is evaluating the risk surrounding key variables

Monte Carlo Introduction

Monte Carlo Introduction Probability Based Modeling Concepts moneytree.com Toll free 1.877.421.9815 1 What is Monte Carlo? Monte Carlo Simulation is the currently accepted term for a technique used by

Monte Carlo Introduction Probability Based Modeling Concepts moneytree.com Toll free 1.877.421.9815 1 What is Monte Carlo? Monte Carlo Simulation is the currently accepted term for a technique used by

Validating TIP$TER Can You Trust Its Math?

Validating TIP$TER Can You Trust Its Math? A Series of Tests Introduction: Validating TIP$TER involves not just checking the accuracy of its complex algorithms, but also ensuring that the third party software

Validating TIP$TER Can You Trust Its Math? A Series of Tests Introduction: Validating TIP$TER involves not just checking the accuracy of its complex algorithms, but also ensuring that the third party software

4. INTERMEDIATE EXCEL

Winter 2019 CS130 - Intermediate Excel 1 4. INTERMEDIATE EXCEL Winter 2019 Winter 2019 CS130 - Intermediate Excel 2 Problem 4.1 Import and format: zeus.cs.pacificu.edu/chadd/cs130w17/problem41.html For

Winter 2019 CS130 - Intermediate Excel 1 4. INTERMEDIATE EXCEL Winter 2019 Winter 2019 CS130 - Intermediate Excel 2 Problem 4.1 Import and format: zeus.cs.pacificu.edu/chadd/cs130w17/problem41.html For

SECTION 4.4: Expected Value

15 SECTION 4.4: Expected Value This section tells you why most all gambling is a bad idea. And also why carnival or amusement park games are a bad idea. Random Variables Definition: Random Variable A random

15 SECTION 4.4: Expected Value This section tells you why most all gambling is a bad idea. And also why carnival or amusement park games are a bad idea. Random Variables Definition: Random Variable A random

Functions, Amortization Tables, and What-If Analysis

Functions, Amortization Tables, and What-If Analysis Absolute and Relative References Q1: How do $A1 and A$1 differ from $A$1? Use the following table to answer the questions listed below: A B C D E 1

Functions, Amortization Tables, and What-If Analysis Absolute and Relative References Q1: How do $A1 and A$1 differ from $A$1? Use the following table to answer the questions listed below: A B C D E 1

Corporate Finance, Module 21: Option Valuation. Practice Problems. (The attached PDF file has better formatting.) Updated: July 7, 2005

Updated: July 7, 2005") Corporate Finance, Module 21: Option Valuation Practice Problems (The attached PDF file has better formatting.) Updated: July 7, 2005 {This posting has more information than is needed for the corporate

Corporate Finance, Module 21: Option Valuation Practice Problems (The attached PDF file has better formatting.) Updated: July 7, 2005 {This posting has more information than is needed for the corporate

To complete this workbook, you will need the following file:

CHAPTER 7 Excel More Skills 11 Create Amortization Tables Amortization tables track loan payments for the life of a loan. Each row in an amortization table tracks how much of a payment is applied to the

CHAPTER 7 Excel More Skills 11 Create Amortization Tables Amortization tables track loan payments for the life of a loan. Each row in an amortization table tracks how much of a payment is applied to the

Chapter 4 Probability Distributions

Slide 1 Chapter 4 Probability Distributions Slide 2 4-1 Overview 4-2 Random Variables 4-3 Binomial Probability Distributions 4-4 Mean, Variance, and Standard Deviation for the Binomial Distribution 4-5

Slide 1 Chapter 4 Probability Distributions Slide 2 4-1 Overview 4-2 Random Variables 4-3 Binomial Probability Distributions 4-4 Mean, Variance, and Standard Deviation for the Binomial Distribution 4-5

Event A Value. Value. Choice

Solutions.. No. t least, not if the decision tree and influence diagram each represent the same problem (identical details and definitions). Decision trees and influence diagrams are called isomorphic,

Solutions.. No. t least, not if the decision tree and influence diagram each represent the same problem (identical details and definitions). Decision trees and influence diagrams are called isomorphic,

Financial Econometrics Jeffrey R. Russell Midterm 2014

Name: Financial Econometrics Jeffrey R. Russell Midterm 2014 You have 2 hours to complete the exam. Use can use a calculator and one side of an 8.5x11 cheat sheet. Try to fit all your work in the space

Name: Financial Econometrics Jeffrey R. Russell Midterm 2014 You have 2 hours to complete the exam. Use can use a calculator and one side of an 8.5x11 cheat sheet. Try to fit all your work in the space

Expectation Exercises.

Expectation Exercises. Pages Problems 0 2,4,5,7 (you don t need to use trees, if you don t want to but they might help!), 9,-5 373 5 (you ll need to head to this page: http://phet.colorado.edu/sims/plinkoprobability/plinko-probability_en.html)

Expectation Exercises. Pages Problems 0 2,4,5,7 (you don t need to use trees, if you don t want to but they might help!), 9,-5 373 5 (you ll need to head to this page: http://phet.colorado.edu/sims/plinkoprobability/plinko-probability_en.html)

Problem Set 1 Due in class, week 1

Business 35150 John H. Cochrane Problem Set 1 Due in class, week 1 Do the readings, as specified in the syllabus. Answer the following problems. Note: in this and following problem sets, make sure to answer

Business 35150 John H. Cochrane Problem Set 1 Due in class, week 1 Do the readings, as specified in the syllabus. Answer the following problems. Note: in this and following problem sets, make sure to answer

... About Monte Cario Simulation

WHAT PRACTITIONERS NEED TO KNOW...... About Monte Cario Simulation Mark Kritzman As financial analysts, we are often required to anticipate the future. Monte Carlo simulation is a numerical technique that

WHAT PRACTITIONERS NEED TO KNOW...... About Monte Cario Simulation Mark Kritzman As financial analysts, we are often required to anticipate the future. Monte Carlo simulation is a numerical technique that

Statistics 431 Spring 2007 P. Shaman. Preliminaries

Statistics 4 Spring 007 P. Shaman The Binomial Distribution Preliminaries A binomial experiment is defined by the following conditions: A sequence of n trials is conducted, with each trial having two possible

Statistics 4 Spring 007 P. Shaman The Binomial Distribution Preliminaries A binomial experiment is defined by the following conditions: A sequence of n trials is conducted, with each trial having two possible

THE UNIVERSITY OF TEXAS AT AUSTIN Department of Information, Risk, and Operations Management

THE UNIVERSITY OF TEXAS AT AUSTIN Department of Information, Risk, and Operations Management BA 386T Tom Shively PROBABILITY CONCEPTS AND NORMAL DISTRIBUTIONS The fundamental idea underlying any statistical

THE UNIVERSITY OF TEXAS AT AUSTIN Department of Information, Risk, and Operations Management BA 386T Tom Shively PROBABILITY CONCEPTS AND NORMAL DISTRIBUTIONS The fundamental idea underlying any statistical

Student Guide: RWC Simulation Lab. Free Market Educational Services: RWC Curriculum

Free Market Educational Services: RWC Curriculum Student Guide: RWC Simulation Lab Table of Contents Getting Started... 4 Preferred Browsers... 4 Register for an Account:... 4 Course Key:... 4 The Student

Free Market Educational Services: RWC Curriculum Student Guide: RWC Simulation Lab Table of Contents Getting Started... 4 Preferred Browsers... 4 Register for an Account:... 4 Course Key:... 4 The Student

Jacob: What data do we use? Do we compile paid loss triangles for a line of business?

PROJECT TEMPLATES FOR REGRESSION ANALYSIS APPLIED TO LOSS RESERVING BACKGROUND ON PAID LOSS TRIANGLES (The attached PDF file has better formatting.) {The paid loss triangle helps you! distinguish between

PROJECT TEMPLATES FOR REGRESSION ANALYSIS APPLIED TO LOSS RESERVING BACKGROUND ON PAID LOSS TRIANGLES (The attached PDF file has better formatting.) {The paid loss triangle helps you! distinguish between

Trading Diary Manual. Introduction

Trading Diary Manual Introduction Welcome, and congratulations! You ve made a wise choice by purchasing this software, and if you commit to using it regularly and consistently you will not be able but

Trading Diary Manual Introduction Welcome, and congratulations! You ve made a wise choice by purchasing this software, and if you commit to using it regularly and consistently you will not be able but

Volatility Lessons Eugene F. Fama a and Kenneth R. French b, Stock returns are volatile. For July 1963 to December 2016 (henceforth ) the

the") First draft: March 2016 This draft: May 2018 Volatility Lessons Eugene F. Fama a and Kenneth R. French b, Abstract The average monthly premium of the Market return over the one-month T-Bill return is substantial,

First draft: March 2016 This draft: May 2018 Volatility Lessons Eugene F. Fama a and Kenneth R. French b, Abstract The average monthly premium of the Market return over the one-month T-Bill return is substantial,

Computing interest and composition of functions:

Computing interest and composition of functions: In this week, we are creating a simple and compound interest calculator in EXCEL. These two calculators will be used to solve interest questions in week

Computing interest and composition of functions: In this week, we are creating a simple and compound interest calculator in EXCEL. These two calculators will be used to solve interest questions in week

Uncertainty in Economic Analysis

Risk and Uncertainty Uncertainty in Economic Analysis CE 215 28, Richard J. Nielsen We ve already mentioned that interest rates reflect the risk involved in an investment. Risk and uncertainty can affect

Risk and Uncertainty Uncertainty in Economic Analysis CE 215 28, Richard J. Nielsen We ve already mentioned that interest rates reflect the risk involved in an investment. Risk and uncertainty can affect

January 29. Annuities

January 29 Annuities An annuity is a repeating payment, typically of a fixed amount, over a period of time. An annuity is like a loan in reverse; rather than paying a loan company, a bank or investment

January 29 Annuities An annuity is a repeating payment, typically of a fixed amount, over a period of time. An annuity is like a loan in reverse; rather than paying a loan company, a bank or investment

Market Volatility and Risk Proxies

Market Volatility and Risk Proxies... an introduction to the concepts 019 Gary R. Evans. This slide set by Gary R. Evans is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International

Market Volatility and Risk Proxies... an introduction to the concepts 019 Gary R. Evans. This slide set by Gary R. Evans is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International

Bond Amortization. amortization schedule. the PV, FV, and PMT functions. elements. macros

8 Bond Amortization N LY O LEARNING OBJECTIVES a bond amortization schedule Use the PV, FV, and PMT functions Protect worksheet elements Automate processes with macros A T IO N Create E V A LU Financial

8 Bond Amortization N LY O LEARNING OBJECTIVES a bond amortization schedule Use the PV, FV, and PMT functions Protect worksheet elements Automate processes with macros A T IO N Create E V A LU Financial

Risk Neutral Valuation, the Black-

Risk Neutral Valuation, the Black- Scholes Model and Monte Carlo Stephen M Schaefer London Business School Credit Risk Elective Summer 01 C = SN( d )-PV( X ) N( ) N he Black-Scholes formula 1 d (.) : cumulative

Risk Neutral Valuation, the Black- Scholes Model and Monte Carlo Stephen M Schaefer London Business School Credit Risk Elective Summer 01 C = SN( d )-PV( X ) N( ) N he Black-Scholes formula 1 d (.) : cumulative

Lessons from two case-studies: How to Build Accurate and models

Lessons from two case-studies: How to Build Accurate and Decision-Focused @RISK models Palisade Risk Conference New Orleans, LA Nov, 2014 Huybert Groenendaal, PhD, MBA Managing Partner EpiX Analytics Two

Lessons from two case-studies: How to Build Accurate and Decision-Focused @RISK models Palisade Risk Conference New Orleans, LA Nov, 2014 Huybert Groenendaal, PhD, MBA Managing Partner EpiX Analytics Two

Intermediate Excel. Winter Winter 2011 CS130 - Intermediate Excel 1

Intermediate Excel Winter 2011 Winter 2011 CS130 - Intermediate Excel 1 Combination Cell References How do $A1 and A$1 differ from $A$1? A B C D E 1 4 8 =A1/$A$3 2 6 4 =A$1*$B4+B2 3 =A1+A2 1 4 5 What formula

Intermediate Excel Winter 2011 Winter 2011 CS130 - Intermediate Excel 1 Combination Cell References How do $A1 and A$1 differ from $A$1? A B C D E 1 4 8 =A1/$A$3 2 6 4 =A$1*$B4+B2 3 =A1+A2 1 4 5 What formula

New Research on How to Choose Portfolio Return Assumptions

New Research on How to Choose Portfolio Return Assumptions July 1, 2014 by Wade Pfau Care must be taken with portfolio return assumptions, as small differences compound into dramatically different financial

New Research on How to Choose Portfolio Return Assumptions July 1, 2014 by Wade Pfau Care must be taken with portfolio return assumptions, as small differences compound into dramatically different financial

Martingales, Part II, with Exercise Due 9/21

Econ. 487a Fall 1998 C.Sims Martingales, Part II, with Exercise Due 9/21 1. Brownian Motion A process {X t } is a Brownian Motion if and only if i. it is a martingale, ii. t is a continuous time parameter

Econ. 487a Fall 1998 C.Sims Martingales, Part II, with Exercise Due 9/21 1. Brownian Motion A process {X t } is a Brownian Motion if and only if i. it is a martingale, ii. t is a continuous time parameter

Economics 483. Midterm Exam. 1. Consider the following monthly data for Microsoft stock over the period December 1995 through December 1996:

University of Washington Summer Department of Economics Eric Zivot Economics 3 Midterm Exam This is a closed book and closed note exam. However, you are allowed one page of handwritten notes. Answer all

University of Washington Summer Department of Economics Eric Zivot Economics 3 Midterm Exam This is a closed book and closed note exam. However, you are allowed one page of handwritten notes. Answer all

Software Tutorial ormal Statistics

Software Tutorial ormal Statistics The example session with the teaching software, PG2000, which is described below is intended as an example run to familiarise the user with the package. This documented

Software Tutorial ormal Statistics The example session with the teaching software, PG2000, which is described below is intended as an example run to familiarise the user with the package. This documented

Personal Finance Amortization Table. Name: Period:

Personal Finance Amortization Table Name: Period: Ch 8 Project using Excel In this project you will complete a loan amortization table (payment schedule) for the purchase of a home with a $235,500 loan

Personal Finance Amortization Table Name: Period: Ch 8 Project using Excel In this project you will complete a loan amortization table (payment schedule) for the purchase of a home with a $235,500 loan

Probability Models. Grab a copy of the notes on the table by the door

Grab a copy of the notes on the table by the door Bernoulli Trials Suppose a cereal manufacturer puts pictures of famous athletes in boxes of cereal, in the hope of increasing sales. The manufacturer announces

Grab a copy of the notes on the table by the door Bernoulli Trials Suppose a cereal manufacturer puts pictures of famous athletes in boxes of cereal, in the hope of increasing sales. The manufacturer announces

<Partner Name> <Partner Product> RSA ARCHER GRC Platform Implementation Guide. 6.3

RSA ARCHER GRC Platform Implementation Guide Palisade Jeffrey Carlson, RSA Partner Engineering Last Modified: 12/21/2016 Solution Summary Palisade @RISK is risk and decision

RSA ARCHER GRC Platform Implementation Guide Palisade Jeffrey Carlson, RSA Partner Engineering Last Modified: 12/21/2016 Solution Summary Palisade @RISK is risk and decision

Lesson Plan for Simulation with Spreadsheets (8/31/11 & 9/7/11)

") Jeremy Tejada ISE 441 - Introduction to Simulation Learning Outcomes: Lesson Plan for Simulation with Spreadsheets (8/31/11 & 9/7/11) 1. Students will be able to list and define the different components

Jeremy Tejada ISE 441 - Introduction to Simulation Learning Outcomes: Lesson Plan for Simulation with Spreadsheets (8/31/11 & 9/7/11) 1. Students will be able to list and define the different components

Navigating RRM. 6 Question Client Fact Finder. Tri-Fold Prospecting Brochure Stand Alone Paper Fact Finder

Navigating RRM Welcome to the Retirement Road Map Navigation tutorial. This tutorial will walk you through entering client data and creating product recommendations so that you can create powerful retirement

Navigating RRM Welcome to the Retirement Road Map Navigation tutorial. This tutorial will walk you through entering client data and creating product recommendations so that you can create powerful retirement

Corporate Finance, Module 3: Common Stock Valuation. Illustrative Test Questions and Practice Problems. (The attached PDF file has better formatting.

Corporate Finance, Module 3: Common Stock Valuation Illustrative Test Questions and Practice Problems (The attached PDF file has better formatting.) These problems combine common stock valuation (module

Corporate Finance, Module 3: Common Stock Valuation Illustrative Test Questions and Practice Problems (The attached PDF file has better formatting.) These problems combine common stock valuation (module

BEx Analyzer (Business Explorer Analyzer)

") BEx Analyzer (Business Explorer Analyzer) Purpose These instructions describe how to use the BEx Analyzer, which is utilized during budget development by account managers, deans, directors, vice presidents,

BEx Analyzer (Business Explorer Analyzer) Purpose These instructions describe how to use the BEx Analyzer, which is utilized during budget development by account managers, deans, directors, vice presidents,

CS134: Networks Spring Random Variables and Independence. 1.2 Probability Distribution Function (PDF) Number of heads Probability 2 0.

Number of heads Probability 2 0.") CS134: Networks Spring 2017 Prof. Yaron Singer Section 0 1 Probability 1.1 Random Variables and Independence A real-valued random variable is a variable that can take each of a set of possible values in

CS134: Networks Spring 2017 Prof. Yaron Singer Section 0 1 Probability 1.1 Random Variables and Independence A real-valued random variable is a variable that can take each of a set of possible values in

Flex ib ility :Adju s ting SocialSecu rity Benefits

Thomas C. B. Davison, MA, PhD, CFP NAPFA Registered Financial Advisor Partner Emeritus, Summit Financial Strategies, Inc. toolsforretirementplanning.com tcbdavison@gmail.com You may want to delay the start

Thomas C. B. Davison, MA, PhD, CFP NAPFA Registered Financial Advisor Partner Emeritus, Summit Financial Strategies, Inc. toolsforretirementplanning.com tcbdavison@gmail.com You may want to delay the start

MLLunsford 1. Activity: Mathematical Expectation

MLLunsford 1 Activity: Mathematical Expectation Concepts: Mathematical Expectation for discrete random variables. Includes expected value and variance. Prerequisites: The student should be familiar with

MLLunsford 1 Activity: Mathematical Expectation Concepts: Mathematical Expectation for discrete random variables. Includes expected value and variance. Prerequisites: The student should be familiar with

The Assumption(s) of Normality

of Normality") The Assumption(s) of Normality Copyright 2000, 2011, 2016, J. Toby Mordkoff This is very complicated, so I ll provide two versions. At a minimum, you should know the short one. It would be great if you

The Assumption(s) of Normality Copyright 2000, 2011, 2016, J. Toby Mordkoff This is very complicated, so I ll provide two versions. At a minimum, you should know the short one. It would be great if you

Foreign Exchange Risk Management at Merck: Background. Decision Models

Decision Models: Lecture 11 2 Decision Models Foreign Exchange Risk Management at Merck: Background Merck & Company is a producer and distributor of pharmaceutical products worldwide. Lecture 11 Using

Decision Models: Lecture 11 2 Decision Models Foreign Exchange Risk Management at Merck: Background Merck & Company is a producer and distributor of pharmaceutical products worldwide. Lecture 11 Using

Simple Random Sample

Simple Random Sample A simple random sample (SRS) of size n consists of n elements from the population chosen in such a way that every set of n elements has an equal chance to be the sample actually selected.

Simple Random Sample A simple random sample (SRS) of size n consists of n elements from the population chosen in such a way that every set of n elements has an equal chance to be the sample actually selected.

Project: The American Dream!

Project: The American Dream! The goal of Math 52 and 95 is to make mathematics real for you, the student. You will be graded on correctness, quality of work, and effort. You should put in the effort on

Project: The American Dream! The goal of Math 52 and 95 is to make mathematics real for you, the student. You will be graded on correctness, quality of work, and effort. You should put in the effort on