Session 167 PD, Decumulation Strategies for Retirement: Individual, Advisor and Plan Sponsor Roles. Moderator: Cynthia J. Levering, ASA, MAAA

|

|

|

- Tamsyn Kelley

- 6 years ago

- Views:

Transcription

1 Session 167 PD, Decumulation Strategies for Retirement: Individual, Advisor and Plan Sponsor Roles Moderator: Cynthia J. Levering, ASA, MAAA Presenters: Carol A. Bogosian, ASA Kailan Shang, FSA, ACIA Paul Yakoboski, Ph.D. SOA Antitrust Disclaimer SOA Presentation Disclaimer

2 Moderator: Cindy Levering, ASA Speakers: Kailan Shang, FSA, CFA, PRM, SCJP Paul Yakoboski, Ph.D. Carol A. Bogosian, ASA Session 167 PD Decumulation Strategies for Retirement: Individual, Advisor and Plan Sponsor Roles October 26, 2016

3 Diverse Risks in Retirement SOA s Committee on Post Retirement Needs and Risks call for essays in late 2015, linked to DC environment: 1. defined contribution plan risk management strategies; 2. decumulation strategies for retirement; and 3. long-term care financing. 18 essays published See more Publications/Publications/Essays/2016-diverse-riskessays.aspx as well as various recent and forthcoming issues of the Pension Section News. 2

4 Multiple Objective Asset Allocation for Retirees Using Simulation By Kailan Shang, FSA, CFA, PRM, SCJP Managing Director & Co-Founder Swin Solutions Inc. 3

5 Agenda 1. Multiple Objectives 2. Current Asset Allocation Methods 3. Simulation-Based Multiple Objective Method Business Intelligence & Risk Management 4

6 Multiple Objectives Current Income Liquidity Wealth Growth Purchasing Power Relative Importance Tax Minimization Longevity Risk Estate Business Intelligence & Risk Management 5

7 (100 Age) % Business Intelligence & Risk Management 6

8 Modern Portfolio Theory Mean-variance optimization Asset Class Expected Return Risk free rate: 3% Correlation between bond return and equity return: 20% Required return: 8.5% Risk (Vol) Bond 4.5% 8% Equity 9% 25% Return Efficient Frontier 14% 12% CML 10% 8% 6% 4% 2% 0% 0% 5% 10% 15% 20% 25% Risk - Volatility Business Intelligence & Risk Management 7

9 Risk Pyramid Pinnacle Middle Bottom Investment Types Speculative investment Equity and real estate Bonds and savings Objectives Substantial return Estate, vacation home, etc. Living cost, medical cost, etc. Business Intelligence & Risk Management 8

10 Analytic Hierarchy Process (AHP) Goal Objective 1 Weight: 62% Objective 2 Weight: 24% Objective 3 Weight: 12% Plan A Plan B Plan C Plan A Plan B Plan C Plan A Plan B Plan C Relative Preference Objective 1 Objective 2 Objective 3 Objective Objective 2 1/5 1 3 Objective 3 1/3 1/3 1 Weight Objective 1 62% Objective 2 24% Objective 3 14% Business Intelligence & Risk Management 9

11 Simulation-Based Multiple Objective Asset Allocation Business Intelligence & Risk Management 10

12 Example Five Objectives 1. High current income no less than 2 percent of the asset value (CI) 2. Maintain the purchase power of the portfolio (PP) 3. Maintain sufficient liquidity to cover living costs and unexpected medical costs (AL) 4. Minimize longevity risk (LR) 5. Leave an estate of $100,000 for his children (ES) Relative Preference CI PP AL LR ES CI PP 1/ /2 5 AL 1/3 1/ LR 1 2 1/3 1 7 ES 1/7 1/5 1/5 1/7 1 CI PP AL LR ES Weight 36% 18% 21% 22% 3% Business Intelligence & Risk Management 11

13 Example Measurement Objective CI PP AL LR ES Measure Type of measure Performance measurement (current income rate 2%)/2% (investment return inflation rate)/2% (AL living cost unexpected medical cost)/(living cost + unexpected medical cost) (age at which assets are outlived life expectancy)/ (99th percentile of the age life expectancy) life expectancy 100,000)/ 100,000 Average Average Worst Average Average Business Intelligence & Risk Management 12

14 Example Asset Class Profile Retiree Financial Information Stochastic Scenarios (Economic, Mortality, etc.) Risk Tolerance Business Intelligence & Risk Management 13

15 Example The investor needs to have a minimum expected weighted performance of 0.5 with less than a 1 percent chance of having a performance less than 0.1. Optimal Asset Allocation Savings Bond Equity Real estate Annuity (monthly payment with 2% annual increase) Weighted performance Risk Sharpe ratio 10% 90% 0% 0% Sharpe Ratio = (Weighted Performance 0*) / Risk 0 means minimum requirements are met. Business Intelligence & Risk Management 14

16 Additional Information The essay written by Lingyan Jiang and Kailan Shang can be downloaded at A free online tool that implements the new method can be accessed at The presenter can be contacted at kailan.shang@swinsolutions.com. The opinions expressed and conclusions reached by the presenter are his own and do not represent any official position or opinion of Swin Solutions Inc. Swin Solutions Inc. disclaims responsibility for any private publication or statement by any of its employees. Business Intelligence & Risk Management 15

17 Decisions Misaligned With Priorities By Paul Yakoboski, Ph.D. Senior Economist, TIAA Institute 16

18 About the survey 1,000 retired TIAA participants surveyed (2014) Age 60 or older Retired with at least $400,000 in defined contribution and/or IRA assets No defined benefit pension income 500 receiving annuitized payments (annuitants) 500 not receiving annuitized payments (non-annuitants) 17

19 Top priorities for personal finances in retirement Ensuring the financial security of your spouse if you die first Not outliving savings and financial assets Having a guaranteed income stream to cover basic expenses 18

20 Bottom priorities Having professionals manage your financial assets Leaving an inheritance Earning a high rate of return Having the flexibility to adjust your income as needed 19

21 Mid-level priorities Maintaining direct control of your financial assets Preserving your financial assets Maintaining the same standard of living throughout retirement 20

22 Reasons for annuitizing 21

23 Reasons for not annuitizing 22

24 Impact of advice Worked with a financial advisor in deciding how to manage and draw income from retirement savings Annuitants 54% Non-annuitants 58% Advice received about annuitizing retirement savings Do Don t No advice Annuitants 60% 9% 30% Non-annuitants

25 Impact of plan design Annuitants Nonannuitants Participated in a DC plan that offered a deferred annuity in the investment menu Invested in the deferred annuity (if available) 29% 24% Source: TIAA Institute (2010). 24

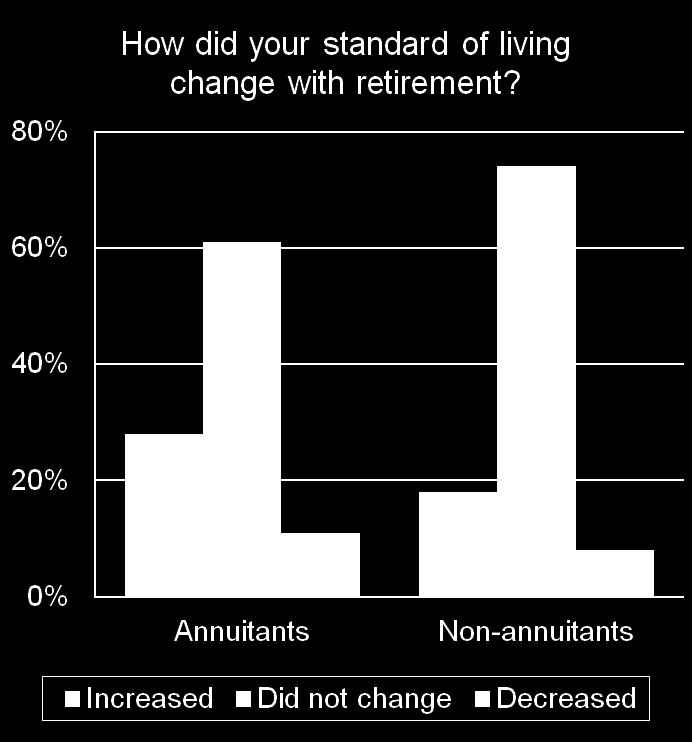

26 In retirement 25

27 Dealing With Multiple Post-Retirement Risks in the Middle Market By Charles S. Yanikoski, President of RetirementWORKS, Inc. Presented by Carol A. Bogosian, ASA 26

28 Focusing the Discussion Principal focus is on middle market retirees Affluent retirees are at less financial risk, and typically have adequate means to cover all of the most significant risks. Low-income people have few options, and therefore their decisions are less complex (not that this is a consolation to them). 27

29 Key Retirement Financial Risks Longevity: living too long; premature death of the primary income recipient Health: medical expenses; long-term care expenses; inability to earn income; need to pay for home maintenance and other chores; need to be a caregiver instead of earning income Investment: low interest rates; poor market performance; opportunity costs of conservatism Expense control: inflation, property value fluctuations, casualty losses Guarantee impairments: pension underfunding; Social security underfunding Family: divorce; remarriage; other family crises Other: fraud; poor advice; poor personal decision-making 28

30 Three Ways to Address Risk Purchasing insurance products Life insurance, annuities, health insurance, long-term care insurance, investment return guarantees, or combinations of these Self-insuring Personal cash, savings, investments, home equity, other assets Reducing exposure Frugality, earned income, benefits claiming strategy, healthier lifestyle, etc. 29

31 Limitations of Insurance Not available for many risks Middle income people cannot afford to insure against every risk Purchases reduce cash, which is already limited, therefore increasing exposure to other risks 30

32 Opportunities and Limitations of Self-Insurance Available virtually for free: self-insurance is another word for "personal wealth" Wealth (even modest wealth) provides some insurance against any financial risk Consumers do not have to guess correctly which risk will strike them Any "claim" against the self-insurance fund increases subsequent exposure to all risks Middle income wealth is usually such that even one severe adverse outcome might not be fully covered 31

33 Opportunities to Reduce Exposure Rigorous, on-going budgeting to keep expenses low, and thereby increase wealth (or at least not deplete) wealth Part-time employment or other income-generating opportunities Smart decisions about Social Security claiming, and choice of a DB plan retirement option Prudence about other financial and life decisions Healthy lifestyle choices Strengthening of social relationships (family, community, church, etc.), so that help is available if needed Attitudinal adjustments -- e.g., learning to love simple living, or accepting Medicaid as a long-term care strategy 32

34 Optimizing These Strategies in the Middle Market Step 1: Assessing risk exposure What risks do not apply (or don't matter much)? What is the likelihood and impact of those that do apply? Step 2: Assessing risk abatement capacity How much wealth (assets, income) is needed for normal needs? (Consider various levels of lifestyle) How much is left for risk abatement, under each lifestyle scenario? 33

35 Optimizing These Strategies in the Middle Market (continued) Step 3: Assessing financial risk-reduction products For which remaining risks is insurance available? For each, does the risks it reduces outweigh the increased exposure to other risks (caused by reduction in wealth) Step 4: Reality test Evaluate, and repeat the process as necessary 34

36 Advantages A holistic approach -- all risks are taken into account, not just one or two Mind over math -- the focus is on maximizing happiness, not money Preserving wealth as a form of "universal insurance" -- making careful decisions about risk-abatement trade-offs 35

37 Enhancing the Model Fully developed and automated model should include Evaluation of financial impact and likelihood of each significant risk including effect of combining risks Education of consumer on meaning and likelihood of the risks, their consequences and nonfinancial options to reduce risks Weighting strategy to evaluate immediate financial costs, long-term financial costs, and psychological effect of each alternative 36

38 Decumulation Strategy for Retirees: Which Assets to Liquidate By Charles S. Yanikoski, President of RetirementWORKS, Inc. Presented by Cindy Levering, ASA 37

39 Which assets should go first? Making poor choices can be harmful Most consumers know little about the subject Most professionals do not have a well-considered and well-organized methodology Wrong guesses can result in regret and recrimination 38

40 Which assets should go first? Difficult with more assets Many factors some cannot be easily quantified Financial and non-financial questions Risk Liquidity Income generation Future growth potential Taxation Timing Liquidation costs Portfolio diversification 39

41 Which assets should go first? Financial questions Risk Liquidity Income generation Future growth potential Taxation Timing Liquidation costs (including penalties) Portfolio diversification Non-financial questions Personal use Sentimental value 40

42 Ideal Situation Good software should Be fully informed about assets and concerns Be fully informed about financial situation Recognize financial desires and fears Evaluate assets against financial and non-financial questions Include asset allocation analysis

43 Asset Disposal Worksheet

44 Reality Test & Decision

45 Conclusion Tools can produce prudent but not necessarily optimal decisions Worksheet is simpler than well-designed automated system Should be sufficient for typical middle-class households Improvement over less rigorous processes

46 A Portfolio Approach to Retirement Income Security By Steve Vernon, FSA Research Scholar - Stanford Center on Longevity Presented by Cindy Levering, ASA 45

47 Classic Investment Portfolio Theory Pre-retirement: Allocate savings among various asset classes Expect performance to balance in up vs. down markets Challenges to address: keep up with inflation until retirement In retirement: Allocate savings among various retirement income classes and retirement income generators (RIGs). Challenges to address: longevity risk, inflation risk, sequence of returns risk, fraud risk, risk of mistakes and cognitive decline. 46

48 Typical Retirement Income Goals Generate income for life Maximize expected amount Minimize stock market impact Provide inflation protection Maintain access for unforeseen events Preserve unused funds as legacy Select solutions that minimize adjustment Protect against fraud and mistakes due to cognitive decline

49 Pros and Cons of Common RIGs

50 Applying Portfolio Techniques Use savings to delay claiming Social Security Balance investment in stocks, bonds and insured products Understand tradeoffs with systematic withdrawal programs

51 Putting it all Together Cover basic expenses with guaranteed lifetime income Social Security, pensions, and annuities become the bond part of a retirement income portfolio Cover discretionary expenses with high allocations to stocks, if risk can be tolerated Work longer if possible Cash-poor house-rich retirees may want to explore appropriate use of home equity

52 Medical & LTC Expenses Address through insurance Consider current and future premiums and copayments Uninsured long-term care events can drain savings used to produce retirement income Leave home equity intact as possible resource if don t purchase long-term care insurance

53 Decumulation for a New Generation By Elizabeth Bauer, FSA Consulting Actuary at Aon Hewitt Presented by Cindy Levering, ASA 52

54 Why Don t Retirees Annuitize? Annuities are perceived to be expensive Consumers distrust annuities and insurance providers Employees want to get full value from their DC money There is more fear of dying too soon than too late 53

55 The Price of Annuities $100,000 => Monthly SLA for age 65 female of: $498 from USAA $553 using Moody s Aa bond rate 90% MWR 100 basis points for expenses and margins Does not include inflation or bequest protection

56 Is this too expensive? 4% rule buys $333 a month Includes inflation and bequest protection Looks like a good deal

57 Pick a Life Expectancy 30 years => $485 using bond rate 5% or 6% return => $535 or $600 Eliminates most longevity risk Does not eliminate investment risk

58 Live off the Interest Current rates are low Reassurance of no capital loss Not locked in if rates rise in future

59 How to Make Annuities a Better Value Government subsidies Pooled retirement fund Counter consumer distrust Transform Social Security to longevity annuity Cover age 85 expenses with annuity

60 ??? Questions??? 59

Multiple Objective Asset Allocation for Retirees Using Simulation

Multiple Objective Asset Allocation for Retirees Using Simulation Kailan Shang and Lingyan Jiang The asset portfolios of retirees serve many purposes. Retirees may need them to provide stable cash flow

Multiple Objective Asset Allocation for Retirees Using Simulation Kailan Shang and Lingyan Jiang The asset portfolios of retirees serve many purposes. Retirees may need them to provide stable cash flow

Institutional Investment Advisors and Consultants Forum: Developing Expertise and Insights

Institutional Investment Advisors and Consultants Forum: Developing Expertise and Insights OPTIMIZING OUTCOMES WITH AVAILABLE SOLUTIONS Steve Vernon Stanford Center on Longevity June 9, 2015 2 Key Takeaways

Institutional Investment Advisors and Consultants Forum: Developing Expertise and Insights OPTIMIZING OUTCOMES WITH AVAILABLE SOLUTIONS Steve Vernon Stanford Center on Longevity June 9, 2015 2 Key Takeaways

Optimal Retirement Income Solutions in DC Retirement Plans Phase 1: Baseline, Interim Results and Commentary

Optimal Retirement Income Solutions in DC Retirement Plans Phase 1: Baseline, Interim Results and Commentary July 2015 0 Acknowledgments Authors: Steve Vernon, FSA, svernon@stanford.edu Dr. Wade Pfau,

Optimal Retirement Income Solutions in DC Retirement Plans Phase 1: Baseline, Interim Results and Commentary July 2015 0 Acknowledgments Authors: Steve Vernon, FSA, svernon@stanford.edu Dr. Wade Pfau,

How Retirees Manage Retirement Savings for Retirement Income

Data Summary How Retirees Manage Retirement Savings for Retirement Income A Survey of TIAA-CREF Participants Paul J. Yakoboski, Ph.D. Senior Economist TIAA-CREF Institute October 2015 About the survey

Data Summary How Retirees Manage Retirement Savings for Retirement Income A Survey of TIAA-CREF Participants Paul J. Yakoboski, Ph.D. Senior Economist TIAA-CREF Institute October 2015 About the survey

Decumulation Strategy for Retirees: Which Assets to Liquidate

Decumulation Strategy for Retirees: Which Assets to Liquidate Charles S. Yanikoski When it s time to decumulate, most people have multiple assets from which they can draw. So which asset(s) should go first?

Decumulation Strategy for Retirees: Which Assets to Liquidate Charles S. Yanikoski When it s time to decumulate, most people have multiple assets from which they can draw. So which asset(s) should go first?

Workshop 4 Decumulating the Accumulation Changing CAP Behaviours

Workshop 4 Decumulating the Accumulation Changing CAP Behaviours Speakers: Wayne Miller, Sun Life Financial René Beaudry, Normandin Beaudry Moderator: Kathryn Bush, Blake, Cassel & Graydon LLP DECUMULATION:

Workshop 4 Decumulating the Accumulation Changing CAP Behaviours Speakers: Wayne Miller, Sun Life Financial René Beaudry, Normandin Beaudry Moderator: Kathryn Bush, Blake, Cassel & Graydon LLP DECUMULATION:

Retirement Risks and Solutions in the Middle Market

Retirement Risks and Solutions in the Middle Market Presented by Noel Abkemeier, FSA, MAAA Milliman Anna Rappaport, FSA, MAAA Anna Rappaport Consulting RIIA Webinar March 16, 2011 Context: Society of Actuaries

Retirement Risks and Solutions in the Middle Market Presented by Noel Abkemeier, FSA, MAAA Milliman Anna Rappaport, FSA, MAAA Anna Rappaport Consulting RIIA Webinar March 16, 2011 Context: Society of Actuaries

Optimizing Retirement Income Solutions in Defined Contribution Retirement Plans. A Framework for Building Retirement Income Portfolios

Optimizing Retirement Income Solutions in Defined Contribution Retirement Plans A Framework for Building Retirement Income Portfolios Dr. Wade Pfau Joe Tomlinson, FSA, CFP Steve Vernon, FSA MAY 2016 Acknowledgements

Optimizing Retirement Income Solutions in Defined Contribution Retirement Plans A Framework for Building Retirement Income Portfolios Dr. Wade Pfau Joe Tomlinson, FSA, CFP Steve Vernon, FSA MAY 2016 Acknowledgements

Optimizing Retirement Income by Integrating Retirement Plans, IRAs, and Home Equity

Optimizing Retirement Income by Integrating Retirement Plans, IRAs, and Home Equity A Framework for Evaluating Retirement Income Decisions Summary Report, Practical Applications, and Technical Discussion

Optimizing Retirement Income by Integrating Retirement Plans, IRAs, and Home Equity A Framework for Evaluating Retirement Income Decisions Summary Report, Practical Applications, and Technical Discussion

Investing for a Lifetime. Guaranteed. Providing guaranteed lifetime-income options can improve participants retirement readiness.

Investing for a Lifetime. Guaranteed. Providing guaranteed lifetime-income options can improve participants retirement readiness. For Institutional Investor Use Only. Not for Use With or Distribution to

Investing for a Lifetime. Guaranteed. Providing guaranteed lifetime-income options can improve participants retirement readiness. For Institutional Investor Use Only. Not for Use With or Distribution to

How People Plan for Retirement

Understanding and Managing Post-Retirement Risks A series of reports presenting highlights from the Society of Actuaries extensive body of research on post-retirement risks and issues. How People Plan

Understanding and Managing Post-Retirement Risks A series of reports presenting highlights from the Society of Actuaries extensive body of research on post-retirement risks and issues. How People Plan

Misperceptions and Management of Retirement Risks

Misperceptions and Management of Retirement Risks FPA of Greater Indiana and CFA Society Indianapolis Joint Meeting September 20, 2013 Presenter: Carol Bogosian, ASA President of CAB Consulting 1 1 Learning

Misperceptions and Management of Retirement Risks FPA of Greater Indiana and CFA Society Indianapolis Joint Meeting September 20, 2013 Presenter: Carol Bogosian, ASA President of CAB Consulting 1 1 Learning

Retirement. Optimal Asset Allocation in Retirement: A Downside Risk Perspective. JUne W. Van Harlow, Ph.D., CFA Director of Research ABSTRACT

Putnam Institute JUne 2011 Optimal Asset Allocation in : A Downside Perspective W. Van Harlow, Ph.D., CFA Director of Research ABSTRACT Once an individual has retired, asset allocation becomes a critical

Putnam Institute JUne 2011 Optimal Asset Allocation in : A Downside Perspective W. Van Harlow, Ph.D., CFA Director of Research ABSTRACT Once an individual has retired, asset allocation becomes a critical

The MassMutual Single Premium Immediate Annuity (SPIA) Synergy Study

Synergy Study") A Research Report for Individuals The MassMutual Single Premium Immediate Annuity (SPIA) Synergy Study New Planning Approaches and Strategies for the Retirement Income Challenge A Research Report August

A Research Report for Individuals The MassMutual Single Premium Immediate Annuity (SPIA) Synergy Study New Planning Approaches and Strategies for the Retirement Income Challenge A Research Report August

Evaluating Investments versus Insurance in Retirement

Evaluating Investments versus Insurance in Retirement June 30, 2015 by Wade Pfau Retirement-income planning has emerged as a distinct field in the financial services profession. But because it is still

Evaluating Investments versus Insurance in Retirement June 30, 2015 by Wade Pfau Retirement-income planning has emerged as a distinct field in the financial services profession. But because it is still

The Impact of Long-Term Care Costs on Retirement Wealth Needs

The Impact of Long-Term Care Costs on Retirement Wealth Needs (Selections from Society of Actuaries Monograph: Managing the Impact of Long-Term Care Needs and Expense on Retirement Secturiy: A Holistic

The Impact of Long-Term Care Costs on Retirement Wealth Needs (Selections from Society of Actuaries Monograph: Managing the Impact of Long-Term Care Needs and Expense on Retirement Secturiy: A Holistic

Planning for Income to Last

Planning for Income to Last Retirement Income Planning Not FDIC Insured May Lose Value No Bank Guarantee This guide explains why you should consider developing a retirement income plan. It also discusses

Planning for Income to Last Retirement Income Planning Not FDIC Insured May Lose Value No Bank Guarantee This guide explains why you should consider developing a retirement income plan. It also discusses

Complete your retirement picture with guaranteed income

Complete your retirement picture with guaranteed income ANNUITIES INCOME Brighthouse Income Annuity SM Add immediate income for more certainty. All guarantees are subject to the claims-paying ability and

Complete your retirement picture with guaranteed income ANNUITIES INCOME Brighthouse Income Annuity SM Add immediate income for more certainty. All guarantees are subject to the claims-paying ability and

PENTEGRA RETIREMENT SERVICES DISTRIBUTION PATHTM. The path to helping participants plan successfully

PENTEGRA RETIREMENT SERVICES DISTRIBUTION PATHTM The path to helping participants plan successfully Making a secure retirement a reality. What are your choices? What s the right amount? What s the best

PENTEGRA RETIREMENT SERVICES DISTRIBUTION PATHTM The path to helping participants plan successfully Making a secure retirement a reality. What are your choices? What s the right amount? What s the best

Sustainable Spending for Retirement

What s Different About Retirement? RETIREMENT BEGINS WITH A PLAN TM Sustainable Spending for Retirement Presented by: Wade Pfau, Ph.D., CFA Reduced earnings capacity Visible spending constraint Heightened

What s Different About Retirement? RETIREMENT BEGINS WITH A PLAN TM Sustainable Spending for Retirement Presented by: Wade Pfau, Ph.D., CFA Reduced earnings capacity Visible spending constraint Heightened

SOA Research: Misperceptions and Management of Retirement Risks

SOA Research: Misperceptions and Management of Retirement Risks Actuaries Clubs of Boston and Hartford & Springfield Joint Meeting November 14, 2013 Presenter: Carol Bogosian, ASA President of CAB Consulting

SOA Research: Misperceptions and Management of Retirement Risks Actuaries Clubs of Boston and Hartford & Springfield Joint Meeting November 14, 2013 Presenter: Carol Bogosian, ASA President of CAB Consulting

A guide to your retirement income options with TIAA-CREF

A guide to your retirement income options with TIAA-CREF Helping you make important decisions about your retirement How will I know when the time is right to retire? Making the decision to retire is no

A guide to your retirement income options with TIAA-CREF Helping you make important decisions about your retirement How will I know when the time is right to retire? Making the decision to retire is no

Planning for income to last

For Investors Planning for income to last Retirement Income Planning Understand the five key financial risks facing retirees Determine how to maximize your income sources Develop a retirement income plan

For Investors Planning for income to last Retirement Income Planning Understand the five key financial risks facing retirees Determine how to maximize your income sources Develop a retirement income plan

Establishing Your Retirement Income Stream

1 Establishing Your Retirement Income Stream What is important about retirement planning to you? 2 Building your retirement house 4 Legacy Benefits 3 2 Retirement income planning Accumulation 1 Expenses

1 Establishing Your Retirement Income Stream What is important about retirement planning to you? 2 Building your retirement house 4 Legacy Benefits 3 2 Retirement income planning Accumulation 1 Expenses

ONcore Variable Annuities

ONcore Variable Annuities Plan Accumulate Protect Access Table of Contents 2 Plan Overcome Risk Through Planning 6 Accumulate Accumulate Wealth and Manage Risk Using ONcore Variable Annuities 8 Protect

ONcore Variable Annuities Plan Accumulate Protect Access Table of Contents 2 Plan Overcome Risk Through Planning 6 Accumulate Accumulate Wealth and Manage Risk Using ONcore Variable Annuities 8 Protect

Life insurance you don't have to die to use. Policies issued by American General Life Insurance Company, a member company of AIG

Life insurance you don't have to die to use AG Secure Lifetime GUL II with AG Asset Protector SM Accelerated Access Solution Lifestyle Income Solution Live Longer. Retire Stronger. Presented by Levi Robinson,

Life insurance you don't have to die to use AG Secure Lifetime GUL II with AG Asset Protector SM Accelerated Access Solution Lifestyle Income Solution Live Longer. Retire Stronger. Presented by Levi Robinson,

STANFORD CENTER ON LONGEVITY

e z i n o i s n e P o t w Ho n a l P ) k ( 1 0 4 r o A R Any I r n o n, FSA Steve Ve S c h o la r Research e v it y r o n Lo n g e t n e C d Stanfor du s t a n f o r d.e svernon@ Novembe r 2017 STANFORD

e z i n o i s n e P o t w Ho n a l P ) k ( 1 0 4 r o A R Any I r n o n, FSA Steve Ve S c h o la r Research e v it y r o n Lo n g e t n e C d Stanfor du s t a n f o r d.e svernon@ Novembe r 2017 STANFORD

INVESTMENT POLICY GUIDANCE REPORT. Living in Retirement. A Successful Foundation

INVESTMENT POLICY GUIDANCE REPORT Living in Retirement A Successful Foundation Developing Your The process for creating a strategy Plan for the Expected Your Retirement Journey It all starts with you.

INVESTMENT POLICY GUIDANCE REPORT Living in Retirement A Successful Foundation Developing Your The process for creating a strategy Plan for the Expected Your Retirement Journey It all starts with you.

ALLOCATION DURING RETIREMENT: ADDING ANNUITIES TO THE MIX

PORTFOLIO STRATEGIES ALLOCATION DURING RETIREMENT: ADDING ANNUITIES TO THE MIX By William Reichenstein At its most basic level, the decision to annuitize involves the trade-off between longevity risk and

PORTFOLIO STRATEGIES ALLOCATION DURING RETIREMENT: ADDING ANNUITIES TO THE MIX By William Reichenstein At its most basic level, the decision to annuitize involves the trade-off between longevity risk and

Changes in Retirement Handling the Expected and Unexpected

Changes in Retirement Handling the Expected and Unexpected Presenters: Ruth Helman, Greenwald & Associates Anna M. Rappaport, FSA, MAAA July 1, 2015 Reference Documents Society of Actuaries 2014 Report:

Changes in Retirement Handling the Expected and Unexpected Presenters: Ruth Helman, Greenwald & Associates Anna M. Rappaport, FSA, MAAA July 1, 2015 Reference Documents Society of Actuaries 2014 Report:

Breaking Free from the Safe Withdrawal Rate Paradigm: Extending the Efficient Frontier for Retiremen

Breaking Free from the Safe Withdrawal Rate Paradigm: Extending the Efficient Frontier for Retiremen March 5, 2013 by Wade Pfau Combining stocks with single-premium immediate annuities (SPIAs) may be the

Breaking Free from the Safe Withdrawal Rate Paradigm: Extending the Efficient Frontier for Retiremen March 5, 2013 by Wade Pfau Combining stocks with single-premium immediate annuities (SPIAs) may be the

2018 American Academy of Actuaries. All rights reserved. May not be reproduced without express permission.

Today s Objective Advance retirement policy by focusing on new or emerging ideas that have the potential to better align public policy with current and future retirement needs. 2 Policy Must Keep Up Drivers

Today s Objective Advance retirement policy by focusing on new or emerging ideas that have the potential to better align public policy with current and future retirement needs. 2 Policy Must Keep Up Drivers

RETIREMENT ISN T THE FINISH LINE... IT S THE STARTING LINE. Unified IncomePlan

RETIREMENT ISN T THE FINISH LINE... IT S THE STARTING LINE. Unified IncomePlan I ve spent my whole life planning for retirement and now I have a plan that gives me the confidence to enjoy retirement. YOUR

RETIREMENT ISN T THE FINISH LINE... IT S THE STARTING LINE. Unified IncomePlan I ve spent my whole life planning for retirement and now I have a plan that gives me the confidence to enjoy retirement. YOUR

SOA 2009 Risks and Process of Retirement Survey

SOA 2009 Risks and Process of Retirement Survey The Impact of Retirement Risks on Women WISER Symposium December 2, 2010 Cindy Levering, SOA Committee on Post-Retirement Needs and Risks Agenda Introduction,

SOA 2009 Risks and Process of Retirement Survey The Impact of Retirement Risks on Women WISER Symposium December 2, 2010 Cindy Levering, SOA Committee on Post-Retirement Needs and Risks Agenda Introduction,

PACIFIC LIFE VARIABLE ANNUITIES

PACIFIC LIFE VARIABLE ANNUITIES Plan Your Retirement. Protect Your Family. 8/16 13141-16B o WHY CHOOSE A VARIABLE ANNUITY A variable annuity is a long-term contract between you and an insurance company

PACIFIC LIFE VARIABLE ANNUITIES Plan Your Retirement. Protect Your Family. 8/16 13141-16B o WHY CHOOSE A VARIABLE ANNUITY A variable annuity is a long-term contract between you and an insurance company

White Paper. The truth about institutional income annuities

White Paper The truth about institutional income annuities More often than not, the word annuity raises concerns because of conventional wisdom that all annuities are costly, complicated, offer limited

White Paper The truth about institutional income annuities More often than not, the word annuity raises concerns because of conventional wisdom that all annuities are costly, complicated, offer limited

The Role of Information and Expectations in Retirement Planning Communicating Income vs. Lump Sums. By Anna M. Rappaport, FSA, MAAA

The Role of Information and Expectations in Retirement Planning Communicating Income vs. Lump Sums By Anna M. Rappaport, FSA, MAAA Paper Prepared for Retirement 20/20 Abstract In defined contribution plans,

The Role of Information and Expectations in Retirement Planning Communicating Income vs. Lump Sums By Anna M. Rappaport, FSA, MAAA Paper Prepared for Retirement 20/20 Abstract In defined contribution plans,

For Your Name and Spouse Here. Presented by: Dolph Janis Clear Income Strategies Phone:

For and Here Presented by: Dolph Janis Phone: 74-99-49 Email: dolph@cisforlife.com Important Notes This analysis provides only broad, general guidelines, which may be helpful in shaping your thinking about

For and Here Presented by: Dolph Janis Phone: 74-99-49 Email: dolph@cisforlife.com Important Notes This analysis provides only broad, general guidelines, which may be helpful in shaping your thinking about

Enhancing Your Retirement Planning Toolkit

Enhancing Your Retirement Planning Toolkit Wade Pfau, Ph.D., CFA RetirementResearcher.com/retirement-toolkit What s Different About Retirement? Reduced earnings capacity Visible spending constraint Heightened

Enhancing Your Retirement Planning Toolkit Wade Pfau, Ph.D., CFA RetirementResearcher.com/retirement-toolkit What s Different About Retirement? Reduced earnings capacity Visible spending constraint Heightened

Post-Retirement Risks and

Understanding and Managing Post-Retirement Risks A series of reports presenting highlights from the Society of Actuaries extensive body of research on post-retirement risks and issues. Post-Retirement

Understanding and Managing Post-Retirement Risks A series of reports presenting highlights from the Society of Actuaries extensive body of research on post-retirement risks and issues. Post-Retirement

Comparing Approaches: RETIREMENT INCOME METHODOLOGIES

PRICE PERSPECTIVE In-depth analysis and insights to inform your decision-making. Comparing Approaches: RETIREMENT INCOME METHODOLOGIES EXECUTIVE SUMMARY There are many approaches to addressing the retirement

PRICE PERSPECTIVE In-depth analysis and insights to inform your decision-making. Comparing Approaches: RETIREMENT INCOME METHODOLOGIES EXECUTIVE SUMMARY There are many approaches to addressing the retirement

USING IRA ASSETS TO ADDRESS YOUR WEALTH TRANSFER GOALS

U.S. TRUST FIDUCIARY SERVICES FOR MERRILL LYNCH CLIENTS USING IRA ASSETS TO ADDRESS YOUR WEALTH TRANSFER GOALS Trusteed IRAs from U.S. Trust WHAT S INSIDE Support from Merrill Lynch and U.S. Trust Beyond

U.S. TRUST FIDUCIARY SERVICES FOR MERRILL LYNCH CLIENTS USING IRA ASSETS TO ADDRESS YOUR WEALTH TRANSFER GOALS Trusteed IRAs from U.S. Trust WHAT S INSIDE Support from Merrill Lynch and U.S. Trust Beyond

T H E N E X T E V O LU T I O N I N D E F I N E D C ON TR IBUTIO N R E TI R E M E N T P L A N DE S IG N

T H E N E X T E V O LU T I O N I N D E F I N E D C ON TR IBUTIO N R E TI R E M E N T P L A N DE S IG N A G u i d e F o r D C P l a n S p o n s o r s To Implementing Retirement Income Pro g rams B y S t

T H E N E X T E V O LU T I O N I N D E F I N E D C ON TR IBUTIO N R E TI R E M E N T P L A N DE S IG N A G u i d e F o r D C P l a n S p o n s o r s To Implementing Retirement Income Pro g rams B y S t

Ready to Retire Webinar Nov. 6, 2018

1 Ready to Retire Webinar Nov. 6, 2018 131-3099 2 Agenda Welcome ELCA Retirement Plan Distribution Options Taxes on Distribution Options Social Security Additional Income Sources Sample Retirement Income

1 Ready to Retire Webinar Nov. 6, 2018 131-3099 2 Agenda Welcome ELCA Retirement Plan Distribution Options Taxes on Distribution Options Social Security Additional Income Sources Sample Retirement Income

Retirement just got real.

Retirement just got real. Retirement challenge #1: Keeping pace with inflation Inflation has been called the silent killer of wealth. It s rarely discussed and many retirement income strategies ignore

Retirement just got real. Retirement challenge #1: Keeping pace with inflation Inflation has been called the silent killer of wealth. It s rarely discussed and many retirement income strategies ignore

SPECIAL CONSIDERATIONS WOMEN FACE IN RETIREMENT SECURITY

SPECIAL CONSIDERATIONS WOMEN FACE IN RETIREMENT SECURITY 2019 EBRIEFING SERIES FEBRUARY 6, 2019 SPECIAL CONSIDERATIONS WOMEN FACE IN RETIREMENT SECURITY Jack VanDerhei Research Director, EBRI The Cost

SPECIAL CONSIDERATIONS WOMEN FACE IN RETIREMENT SECURITY 2019 EBRIEFING SERIES FEBRUARY 6, 2019 SPECIAL CONSIDERATIONS WOMEN FACE IN RETIREMENT SECURITY Jack VanDerhei Research Director, EBRI The Cost

HOW SOCIAL SECURITY IMPACTS YOUR DAY ONE

HOW SOCIAL SECURITY IMPACTS YOUR DAY ONE May 12, 2015 Dave Nocera Stephanie Anthony Paul Adamczyk Prudential Retirement For Institutional Plan Sponsor use Only. Not to be distributed 0276289-00001-00 to

HOW SOCIAL SECURITY IMPACTS YOUR DAY ONE May 12, 2015 Dave Nocera Stephanie Anthony Paul Adamczyk Prudential Retirement For Institutional Plan Sponsor use Only. Not to be distributed 0276289-00001-00 to

Retirement Security: Public Perceptions and Misperceptions

Retirement Security: Public Perceptions and Misperceptions Anna M. Rappaport, MAAA, EA, FSA Chairperson, Committee on Post-Retirement Risks and Needs, Society of Actuaries Mathew Greenwald President, Mathew

Retirement Security: Public Perceptions and Misperceptions Anna M. Rappaport, MAAA, EA, FSA Chairperson, Committee on Post-Retirement Risks and Needs, Society of Actuaries Mathew Greenwald President, Mathew

Financial Wellness Essay Collection

Article from Financial Wellness Essay Collection 2017 Call for Essays Copyright 2017 Society of Actuaries. All rights reserved. Using Sound Actuarial Principles to Enhance Financial Well-Being Ken Steiner

Article from Financial Wellness Essay Collection 2017 Call for Essays Copyright 2017 Society of Actuaries. All rights reserved. Using Sound Actuarial Principles to Enhance Financial Well-Being Ken Steiner

Guaranteeing an Income for Life: An Immediate Fixed Income Annuity Review

Guaranteeing an Income for Life: An Immediate Fixed Income Annuity Review The biggest financial risk that anyone faces during retirement is the risk that savings will be depleted...the risk that income

Guaranteeing an Income for Life: An Immediate Fixed Income Annuity Review The biggest financial risk that anyone faces during retirement is the risk that savings will be depleted...the risk that income

PACIFIC LIFE VARIABLE ANNUITIES

PACIFIC LIFE VARIABLE ANNUITIES Plan Your Retirement. Protect Your Family. VAC0229-0518 o WHY CHOOSE A VARIABLE ANNUITY A variable annuity is a long-term contract between you and an insurance company that

PACIFIC LIFE VARIABLE ANNUITIES Plan Your Retirement. Protect Your Family. VAC0229-0518 o WHY CHOOSE A VARIABLE ANNUITY A variable annuity is a long-term contract between you and an insurance company that

Balancing Income and Bequest Goals in a DB/DC Hybrid Pension Plan

Balancing Income and Bequest Goals in a DB/DC Hybrid Pension Plan Grace Gu Tax Associate PwC One North Wacker Dr, Chicago, IL 60606 (312) 298 3956 yelei.gu@pwc.com David Kausch, FSA, FCA, EA, MAAA, PhD

Balancing Income and Bequest Goals in a DB/DC Hybrid Pension Plan Grace Gu Tax Associate PwC One North Wacker Dr, Chicago, IL 60606 (312) 298 3956 yelei.gu@pwc.com David Kausch, FSA, FCA, EA, MAAA, PhD

Retirement. Mr. Sample and Mrs. Anna 401k Participant. Prepared for: November 19, (Main Scenario)

") Prepared for: Mr Sample and Mrs Anna 401k (Main Scenario) November 19, 2008 Mr Sample and Mrs Anna 401k Retirement Table of Contents Title Page 1 Table of Contents 2 Spending Goal 3 Current Funding 4 Additional

Prepared for: Mr Sample and Mrs Anna 401k (Main Scenario) November 19, 2008 Mr Sample and Mrs Anna 401k Retirement Table of Contents Title Page 1 Table of Contents 2 Spending Goal 3 Current Funding 4 Additional

Retirement Income Strategies

176984567 Retirement Income Strategies Photo collage Taking steps toward planning a fit retirement FINANCIAL LITERACY EDUCATION PROGRAMS [Name of presenter] [Title of presenter] Agenda 1 The new retirement

176984567 Retirement Income Strategies Photo collage Taking steps toward planning a fit retirement FINANCIAL LITERACY EDUCATION PROGRAMS [Name of presenter] [Title of presenter] Agenda 1 The new retirement

Helping Plan Participants Help Themselves: Withdrawal Strategies in a Self-Serve World

Helping Plan Participants Help Themselves: Withdrawal Strategies in a Self-Serve World PSCA Annual Conference May 1-3, 2018 Contributors from the PSCA Investment Committee: Philip Murphy, CFA, S&P Dow

Helping Plan Participants Help Themselves: Withdrawal Strategies in a Self-Serve World PSCA Annual Conference May 1-3, 2018 Contributors from the PSCA Investment Committee: Philip Murphy, CFA, S&P Dow

Mind Shift Process Shift Retirement Income Planning 1

Retirement Income Planning Peter Wouters Director, Tax Retirement & Estate Planning Mar 2015 For advisor/dealer use only 1 AGENDA The Landscape Role of Planning The Market New Norms Protecting the Downside

Retirement Income Planning Peter Wouters Director, Tax Retirement & Estate Planning Mar 2015 For advisor/dealer use only 1 AGENDA The Landscape Role of Planning The Market New Norms Protecting the Downside

BEYOND THE 4% RULE J.P. MORGAN RESEARCH FOCUSES ON THE POTENTIAL BENEFITS OF A DYNAMIC RETIREMENT INCOME WITHDRAWAL STRATEGY.

BEYOND THE 4% RULE RECENT J.P. MORGAN RESEARCH FOCUSES ON THE POTENTIAL BENEFITS OF A DYNAMIC RETIREMENT INCOME WITHDRAWAL STRATEGY. Over the past decade, retirees have been forced to navigate the dual

BEYOND THE 4% RULE RECENT J.P. MORGAN RESEARCH FOCUSES ON THE POTENTIAL BENEFITS OF A DYNAMIC RETIREMENT INCOME WITHDRAWAL STRATEGY. Over the past decade, retirees have been forced to navigate the dual

Important notes. Agenda. Values and Beliefs. Values and Beliefs. Values and Beliefs. Values and Beliefs. If it s to be, it s up to me.

Important notes Agenda Please be advised that this document is not intended as legal or tax advice. Accordingly, any tax information provided in this document is not intended or written to be used, and

Important notes Agenda Please be advised that this document is not intended as legal or tax advice. Accordingly, any tax information provided in this document is not intended or written to be used, and

PHOENIX PERSONAL PROTECTION CHOICE

Protect your financial future: Your income, your family, your lifestyle. PHOENIX PERSONAL PROTECTION CHOICE A single-premium fixed indexed annuity with flexibility to address multiple needs IRS Circular

Protect your financial future: Your income, your family, your lifestyle. PHOENIX PERSONAL PROTECTION CHOICE A single-premium fixed indexed annuity with flexibility to address multiple needs IRS Circular

ADVISOR USE ONLY PAYOUT ANNUITY OVERCOMING OBJECTIONS. Life s brighter under the sun

ADVISOR USE ONLY PAYOUT ANNUITY OVERCOMING OBJECTIONS Life s brighter under the sun Overcoming objections Overview > > Payout annuities are a powerful retirement tool and have been an important product

ADVISOR USE ONLY PAYOUT ANNUITY OVERCOMING OBJECTIONS Life s brighter under the sun Overcoming objections Overview > > Payout annuities are a powerful retirement tool and have been an important product

MAKING THE DECISION TO BUY AN ANNUITY IS AN IMPORTANT STEP IN YOUR RETIREMENT PLAN.

MAKING THE DECISION TO BUY AN ANNUITY IS AN IMPORTANT STEP IN YOUR RETIREMENT PLAN. The key is having enough accurate and reliable information so you know you are making decisions that are right for you.

MAKING THE DECISION TO BUY AN ANNUITY IS AN IMPORTANT STEP IN YOUR RETIREMENT PLAN. The key is having enough accurate and reliable information so you know you are making decisions that are right for you.

The Retirement Income Challenge

The Income Challenge Deferred Income Annuities Before by Michael Finke, Ph.D., CFP and Wade D. Pfau, Ph.D., CFA Brief Biographies: Michael Finke, Ph.D., CFP, is a professor and Ph.D. coordinator in the

The Income Challenge Deferred Income Annuities Before by Michael Finke, Ph.D., CFP and Wade D. Pfau, Ph.D., CFA Brief Biographies: Michael Finke, Ph.D., CFP, is a professor and Ph.D. coordinator in the

New Retirement Plan Designs for the 21 st Century SOA 2008 Retirement 20/20 Conference

November 18, 2008 New Retirement Plan Designs for the 21 st Century SOA 2008 Retirement 20/20 Conference Defining the Characteristics of the 21 st Century Retirement System Self-Adjusting Mechanisms in

November 18, 2008 New Retirement Plan Designs for the 21 st Century SOA 2008 Retirement 20/20 Conference Defining the Characteristics of the 21 st Century Retirement System Self-Adjusting Mechanisms in

USING DEFINED MATURITY BOND FUNDS AND QLACs TO BETTER MANAGE RETIREMENT RISKS

USING DEFINED MATURITY BOND FUNDS AND QLACs TO BETTER MANAGE RETIREMENT RISKS A Whitepaper for Franklin Templeton and MetLife by WADE D. PFAU, PH.D., CFA Professor of Retirement Income The American College

USING DEFINED MATURITY BOND FUNDS AND QLACs TO BETTER MANAGE RETIREMENT RISKS A Whitepaper for Franklin Templeton and MetLife by WADE D. PFAU, PH.D., CFA Professor of Retirement Income The American College

Retirement Income Showdown: RISK POOLING VS. RISK PREMIUM. by Wade D. Pfau

Retirement Income Showdown: RISK POOLING VS. RISK PREMIUM by Wade D. Pfau ABSTRACT The retirement income showdown regards finding the most efficient approach for meeting retirement spending goals: obtaining

Retirement Income Showdown: RISK POOLING VS. RISK PREMIUM by Wade D. Pfau ABSTRACT The retirement income showdown regards finding the most efficient approach for meeting retirement spending goals: obtaining

Alpha, Beta, and Now Gamma

Alpha, Beta, and Now Gamma David Blanchett, CFA, CFP Head of Retirement Research, Morningstar Investment Management Paul D. Kaplan, Ph.D., CFA Director of Research, Morningstar Canada 2012 Morningstar.

Alpha, Beta, and Now Gamma David Blanchett, CFA, CFP Head of Retirement Research, Morningstar Investment Management Paul D. Kaplan, Ph.D., CFA Director of Research, Morningstar Canada 2012 Morningstar.

THE CHALLENGES OF TRANSITIONING FROM THE ACCUMULATION TO THE DISTRIBUTION PHASE IN RETIREMENT PLANNING

THE CHALLENGES OF TRANSITIONING FROM THE ACCUMULATION TO THE DISTRIBUTION PHASE IN RETIREMENT PLANNING Overview 1. Specializing in retirement income planning 2. Helping Clients Understand Retirement Income

THE CHALLENGES OF TRANSITIONING FROM THE ACCUMULATION TO THE DISTRIBUTION PHASE IN RETIREMENT PLANNING Overview 1. Specializing in retirement income planning 2. Helping Clients Understand Retirement Income

SOCIAL SECURITY WON T BE ENOUGH:

SOCIAL SECURITY WON T BE ENOUGH: 6 REASONS TO CONSIDER AN INCOME ANNUITY How long before you retire? For some of us it s 20 to 30 years away, and for others it s closer to 5 or 0 years. The key here is

SOCIAL SECURITY WON T BE ENOUGH: 6 REASONS TO CONSIDER AN INCOME ANNUITY How long before you retire? For some of us it s 20 to 30 years away, and for others it s closer to 5 or 0 years. The key here is

CFA Level III - LOS Changes

CFA Level III - LOS Changes 2016-2017 Ethics Ethics Ethics Ethics Ethics Ethics Ethics Ethics Topic LOS Level III - 2016 (332 LOS) LOS Level III - 2017 (337 LOS) Compared 1.1.a 1.1.b 1.2.a 1.2.b 2.3.a

CFA Level III - LOS Changes 2016-2017 Ethics Ethics Ethics Ethics Ethics Ethics Ethics Ethics Topic LOS Level III - 2016 (332 LOS) LOS Level III - 2017 (337 LOS) Compared 1.1.a 1.1.b 1.2.a 1.2.b 2.3.a

Demystifying Annuities

Demystifying Annuities Agenda Lessons from Mt. Everest Retirement Planning Considerations How do you know what s right for you All About Annuities Tools and Resources Questions The Perils of Descent What

Demystifying Annuities Agenda Lessons from Mt. Everest Retirement Planning Considerations How do you know what s right for you All About Annuities Tools and Resources Questions The Perils of Descent What

Segmenting the Middle Market: RETIREMENT RISKS AND SOLUTIONS PHASE I

Segmenting the Middle Market: RETIREMENT RISKS AND SOLUTIONS PHASE I REPORT April 2009 Prepared for: Society of Actuaries Prepared by: Noel Abkemeier, FSA, MAAA Brent Hamann Segmenting the Middle Market:

Segmenting the Middle Market: RETIREMENT RISKS AND SOLUTIONS PHASE I REPORT April 2009 Prepared for: Society of Actuaries Prepared by: Noel Abkemeier, FSA, MAAA Brent Hamann Segmenting the Middle Market:

Why Advisors Should Use Deferred-Income Annuities

Why Advisors Should Use Deferred-Income Annuities November 24, 2015 by Michael Finke Retirement income planning is a mathematical problem in which an investor begins with a lump sum of wealth and withdraws

Why Advisors Should Use Deferred-Income Annuities November 24, 2015 by Michael Finke Retirement income planning is a mathematical problem in which an investor begins with a lump sum of wealth and withdraws

RBC retirement income planning process

Page 1 of 6 RBC retirement income planning process Create income for your retirement At RBC Wealth Management, we believe managing your wealth to produce an income during retirement is fundamentally different

Page 1 of 6 RBC retirement income planning process Create income for your retirement At RBC Wealth Management, we believe managing your wealth to produce an income during retirement is fundamentally different

RETIREMENT PLANNING. Created by Raymond James using Ibbotson Presentation Materials 2011 Morningstar, Inc. All rights reserved. Used with permission.

RETIREMENT PLANNING Erik Melville 603 N Indian River Drive, Suite 300 Fort Pierce, FL 34950 772-460-2500 erik.melville@raymondjames.com www.melvillewealthmanagement.com Created by Raymond James using Ibbotson

RETIREMENT PLANNING Erik Melville 603 N Indian River Drive, Suite 300 Fort Pierce, FL 34950 772-460-2500 erik.melville@raymondjames.com www.melvillewealthmanagement.com Created by Raymond James using Ibbotson

Lincoln Secured Retirement Income SM Solution: Addressing Participant Retirement Income Risks

C. Frederick Reish (310) 203-4047 Fred.Reish@dbr.com www.drinkerbiddle.com/freish Lincoln Secured Retirement Income SM Solution: Addressing Participant Retirement Income Risks A WHITE PAPER BY FRED REISH

C. Frederick Reish (310) 203-4047 Fred.Reish@dbr.com www.drinkerbiddle.com/freish Lincoln Secured Retirement Income SM Solution: Addressing Participant Retirement Income Risks A WHITE PAPER BY FRED REISH

Session 132 L - New Developments in Mortality Risk Pooling. Moderator: Deborah A. Tully, FSA, EA, FCA, MAAA. Presenter: Rowland Davis, FSA

Session 132 L - New Developments in Mortality Risk Pooling Moderator: Deborah A. Tully, FSA, EA, FCA, MAAA Presenter: Rowland Davis, FSA SOA Antitrust Compliance Guidelines SOA Presentation Disclaimer

Session 132 L - New Developments in Mortality Risk Pooling Moderator: Deborah A. Tully, FSA, EA, FCA, MAAA Presenter: Rowland Davis, FSA SOA Antitrust Compliance Guidelines SOA Presentation Disclaimer

Balancing Retirement With Wealth-Transfer Goals. J u n e 2 011

F I N A N C I A L P L A N N I N G A D V I S O R Y: Balancing Retirement With Wealth-Transfer Goals J u n e 2 011 Balancing Retirement With Wealth-Transfer Goals With the volatile markets of recent years,

F I N A N C I A L P L A N N I N G A D V I S O R Y: Balancing Retirement With Wealth-Transfer Goals J u n e 2 011 Balancing Retirement With Wealth-Transfer Goals With the volatile markets of recent years,

Living in Retirement Guide

Living in Retirement Guide With the right ongoing planning, living in retirement can be a comfortable time of financial independence. 1-866-951-9511 regions.com Expect more in your retirement Your working

Living in Retirement Guide With the right ongoing planning, living in retirement can be a comfortable time of financial independence. 1-866-951-9511 regions.com Expect more in your retirement Your working

Take control. Help your clients understand the role of risk control in a portfolio A GUIDE TO CONDUCTING A RISK CONTROL REVIEW

A GUIDE TO CONDUCTING A RISK CONTROL REVIEW Take control Help your clients understand the role of risk control in a portfolio MGA-1658740 FOR REGISTERED REPRESENTATIVE USE ONLY. NOT FOR USE BY THE GENERAL

A GUIDE TO CONDUCTING A RISK CONTROL REVIEW Take control Help your clients understand the role of risk control in a portfolio MGA-1658740 FOR REGISTERED REPRESENTATIVE USE ONLY. NOT FOR USE BY THE GENERAL

BRIGHT PAPER LIFE INSURANCE. for the WEALTHY: the myth-busting benefits KEY INSIGHTS:

BRIGHT PAPER APRIL 2014 LIFE INSURANCE for the WEALTHY: the myth-busting benefits KEY INSIGHTS: 1. Insurance can help preserve affluent lifestyles 2. Permanent life insurance can protect or enhance financial

BRIGHT PAPER APRIL 2014 LIFE INSURANCE for the WEALTHY: the myth-busting benefits KEY INSIGHTS: 1. Insurance can help preserve affluent lifestyles 2. Permanent life insurance can protect or enhance financial

Personal Financial Plan

Personal Financial Plan Pete and Carrie Mitchell 918 Richmond Street Toronto, Ontario M5N 1V5 Disclaimer This document has been prepared to assist in the analysis of your current financial position, thereby

Personal Financial Plan Pete and Carrie Mitchell 918 Richmond Street Toronto, Ontario M5N 1V5 Disclaimer This document has been prepared to assist in the analysis of your current financial position, thereby

Insight on Estate Planning

Insight on Estate Planning Protect multiple generations with a dynasty trust What s the best option for a pension plan payout? The flexibility of stretch IRAs Learn how your IRA can benefit your spouse

Insight on Estate Planning Protect multiple generations with a dynasty trust What s the best option for a pension plan payout? The flexibility of stretch IRAs Learn how your IRA can benefit your spouse

Issue Number 60 August A publication of the TIAA-CREF Institute

18429AA 3/9/00 7:01 AM Page 1 Research Dialogues Issue Number August 1999 A publication of the TIAA-CREF Institute The Retirement Patterns and Annuitization Decisions of a Cohort of TIAA-CREF Participants

18429AA 3/9/00 7:01 AM Page 1 Research Dialogues Issue Number August 1999 A publication of the TIAA-CREF Institute The Retirement Patterns and Annuitization Decisions of a Cohort of TIAA-CREF Participants

Northwestern Mutual Retirement Strategy. Retirement Income Planning with Confidence

Northwestern Mutual Retirement Strategy Retirement Income Planning with Confidence Over the past decade, the conventional approach to retirement planning has shifted. Retirement planning used to focus

Northwestern Mutual Retirement Strategy Retirement Income Planning with Confidence Over the past decade, the conventional approach to retirement planning has shifted. Retirement planning used to focus

Guaranteed income for life. In any market.

Guaranteed income for life. In any market. Schwab Retirement Income Variable Annuity with optional Guaranteed Lifetime Withdrawal Benefit. A variable annuity from Charles Schwab, issued by Pacific Life.*

Guaranteed income for life. In any market. Schwab Retirement Income Variable Annuity with optional Guaranteed Lifetime Withdrawal Benefit. A variable annuity from Charles Schwab, issued by Pacific Life.*

Drawdown: the guide Drawdown: the guide 1

Drawdown: the guide Drawdown: the guide 1 Drawdown versus annuity Drawdown offers extra flexibility and the potential for better returns or more income from a pension pot - given the relatively low returns

Drawdown: the guide Drawdown: the guide 1 Drawdown versus annuity Drawdown offers extra flexibility and the potential for better returns or more income from a pension pot - given the relatively low returns

The 10 Biggest Social Security Mistakes What Baby Boomers Need to Know

The 10 Biggest Social Security Mistakes What Baby Boomers Need to Know Social Security can play a very important role in a retirement income plan. As one of the few sources of lifetime, inflation-adjusted

The 10 Biggest Social Security Mistakes What Baby Boomers Need to Know Social Security can play a very important role in a retirement income plan. As one of the few sources of lifetime, inflation-adjusted

4 Strategies for Retiring Clients

Sustaining Income Through Retirement: 4 Strategies for Retiring Clients ExecutiveSummary Over the next 15 to 20 years, baby boomers are expected to reallocate nearly $8.4 trillion in retirement assets

Sustaining Income Through Retirement: 4 Strategies for Retiring Clients ExecutiveSummary Over the next 15 to 20 years, baby boomers are expected to reallocate nearly $8.4 trillion in retirement assets

A New Generation Retirement Strategy

A New Generation Retirement Strategy Today, Optimizing Retirement Income Requires an Increased Focus on Efficiency 8/13 80060-13A No bank guarantee Not a deposit May lose value Not FDIC/NCUA insured Not

A New Generation Retirement Strategy Today, Optimizing Retirement Income Requires an Increased Focus on Efficiency 8/13 80060-13A No bank guarantee Not a deposit May lose value Not FDIC/NCUA insured Not

Determining a Realistic Withdrawal Amount and Asset Allocation in Retirement

Determining a Realistic Withdrawal Amount and Asset Allocation in Retirement >> Many people look forward to retirement, but it can be one of the most complicated stages of life from a financial planning

Determining a Realistic Withdrawal Amount and Asset Allocation in Retirement >> Many people look forward to retirement, but it can be one of the most complicated stages of life from a financial planning

Designing a Monthly Paycheck in Retirement MANAGING RETIREMENT DECISIONS SERIES

Designing a Monthly Paycheck in Retirement MANAGING RETIREMENT DECISIONS SERIES August 2017 WHERE S MY PAYCHECK GOING TO COME FROM? That is a common question for new retirees and near-retirees when they

Designing a Monthly Paycheck in Retirement MANAGING RETIREMENT DECISIONS SERIES August 2017 WHERE S MY PAYCHECK GOING TO COME FROM? That is a common question for new retirees and near-retirees when they

Key Competencies for Proper Retirement Income Planning

The American College TAC Digital Commons Faculty Publications Spring 2011 Key Competencies for Proper Retirement Income Planning David Littell The American College of Financial Services Kenn B. Tachino

The American College TAC Digital Commons Faculty Publications Spring 2011 Key Competencies for Proper Retirement Income Planning David Littell The American College of Financial Services Kenn B. Tachino

When Your Outcome Needs to be Income

When Your Outcome Needs to be Income A look at helping employees make good decisions about retirement income Don Harris VALIC Did you know? > In 1940, the first recipient of Social Security retirement

When Your Outcome Needs to be Income A look at helping employees make good decisions about retirement income Don Harris VALIC Did you know? > In 1940, the first recipient of Social Security retirement

Thinking differently about helping your clients measure retirement success

Thinking differently about helping your clients measure retirement success April 2018 For institutional investor use only. Not for use with or distribution to the public. 100 years of dedicated service

Thinking differently about helping your clients measure retirement success April 2018 For institutional investor use only. Not for use with or distribution to the public. 100 years of dedicated service

for INCOME How to optimize your retirement income Client Guide INCOME SOLUTIONS Prime Income Optimizer TM fixed indexed annuity

Prime Income Optimizer TM fixed indexed annuity Preparing How to optimize your retirement income for INCOME Insurance products issued by: The Lincoln National Life Insurance Company Not a deposit Not FDIC-insured

Prime Income Optimizer TM fixed indexed annuity Preparing How to optimize your retirement income for INCOME Insurance products issued by: The Lincoln National Life Insurance Company Not a deposit Not FDIC-insured

Protect your financial future. Your income, your family, your lifestyle.

Protect your financial future. Your income, your family, your lifestyle. P H O E N I X P E R S O N A L P R OT E C T I O N C H O I C E S M A single-premium fixed indexed annuity with flexibility to address

Protect your financial future. Your income, your family, your lifestyle. P H O E N I X P E R S O N A L P R OT E C T I O N C H O I C E S M A single-premium fixed indexed annuity with flexibility to address

New Research: Reverse Mortgages, SPIAs and Retirement Income

New Research: Reverse Mortgages, SPIAs and Retirement Income April 14, 2015 by Joe Tomlinson Retirees need longevity protection and additional funds. Annuities and reverse mortgages can meet those needs.

New Research: Reverse Mortgages, SPIAs and Retirement Income April 14, 2015 by Joe Tomlinson Retirees need longevity protection and additional funds. Annuities and reverse mortgages can meet those needs.

THE ALTERNATIVE USING LIFE INSURANCE. Ruth and Al Sample

THE ALTERNATIVE USING LIFE INSURANCE 00307140 CV Prepared for: Ruth and Al Sample This proposal by Pension Concepts has been designed to illustrate how you may increase your retirement income over your

THE ALTERNATIVE USING LIFE INSURANCE 00307140 CV Prepared for: Ruth and Al Sample This proposal by Pension Concepts has been designed to illustrate how you may increase your retirement income over your

Guaranteeing an Income for Life: An Immediate Income Annuity Review

Guaranteeing an Income for Life: An Immediate Income Annuity Review The biggest financial risk that anyone faces during retirement is the risk that savings will be depleted...the risk that income will

Guaranteeing an Income for Life: An Immediate Income Annuity Review The biggest financial risk that anyone faces during retirement is the risk that savings will be depleted...the risk that income will

The oldest members of the 78 million U.S. baby

A Framework for Managing Retirement Income GWM INVESTMENT MANAGEMENT & GUIDANCE FALL 2009 You ve probably spent most of your life focusing on the accumulation of assets. In retirement, however, you need

A Framework for Managing Retirement Income GWM INVESTMENT MANAGEMENT & GUIDANCE FALL 2009 You ve probably spent most of your life focusing on the accumulation of assets. In retirement, however, you need