THE CHALLENGES OF TRANSITIONING FROM THE ACCUMULATION TO THE DISTRIBUTION PHASE IN RETIREMENT PLANNING

|

|

|

- Gladys McDowell

- 5 years ago

- Views:

Transcription

1 THE CHALLENGES OF TRANSITIONING FROM THE ACCUMULATION TO THE DISTRIBUTION PHASE IN RETIREMENT PLANNING

2 Overview 1. Specializing in retirement income planning 2. Helping Clients Understand Retirement Income Planning 3. Process of building a plan 4. Choosing a retirement income strategy 5. Concluding thoughts

3 Specializing in Retirement Income Planning

4 So Many Ways to Provide Value Help clients discover goals Manage retirement budget Determine when to retire Medicare planning Tax efficient savings and withdrawals Roth conversions Using home equity Social Security claiming Executive benefits Long-term care planning Planning in case of incapacity Converting assets into income Retirement risk mitigation Distribution options from employer plans

5 Does Advice Help? Strategies Increase in income* Social Security Claiming 9.0% Dynamic Withdrawal Strategy 8.5% Tax Efficiency 8.2% Total Wealth Asset Allocation 6.1% Annuity Allocation 3.8% Liability Relative Optimization 2.2% Total 38% Blanchett, video discussing article Alpha, Beta and now Gamma

6 Helping Clients Understand Retirement Income Planning

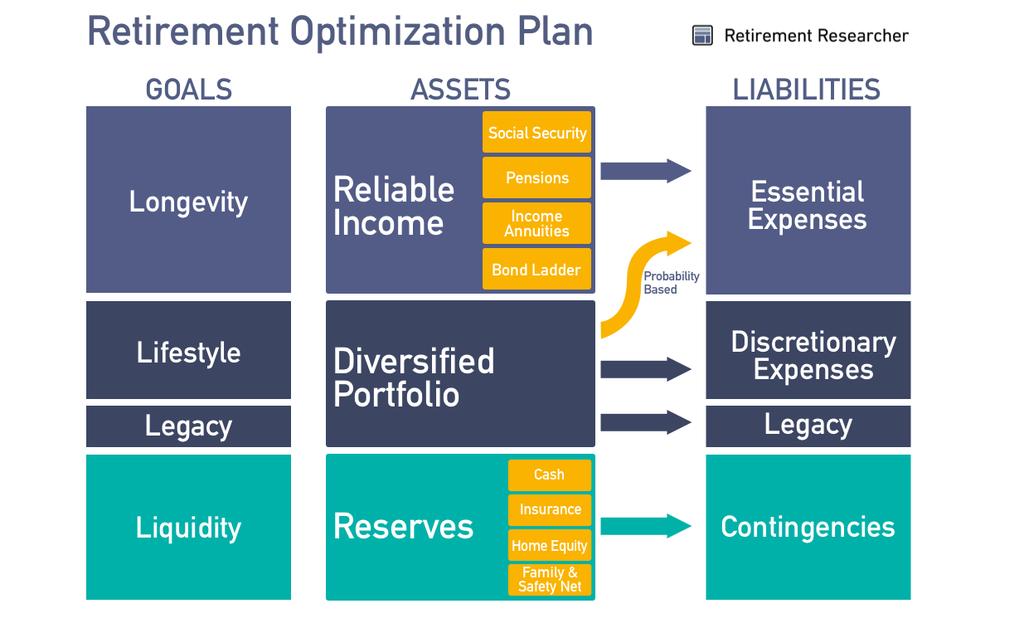

7 What is Retirement Income Planning? Meeting client s financial goals Income needs Contingent expenses Legacy goals Address retirement risks Longevity Inflation Health and long-term care costs Investment-sequence of returns risk Public policy changes

8 What Are You (the Advisor) Going to Do? Help clients determine their needs Evaluate and maximize all available resources Determine strategies to match resources with needs Help them choose a plan that make sense to them Review and modify the plan to make sure that you stay on track Most important is likely behavioral coaching!

9 Maximize Resources Social Security Financial assets Medicare benefits Family support Home equity Community support Employer benefits Employment income Government resources Maintaining health

10 Introduction: Importance of Investor Behavior in Defined-Contribution Plans

11 Investing is simple, but not east -Warren Buffett

12 IMPORTANCE OF DC PLANS FOR RETIREMENT SECURITY DC plans have become the go-to employer sponsored retirement savings vehicle 1975 fewer than 11 million DC participants 1990 roughly 24 million DC participants 2014 over 72 million DC participants Participants now have investment control 88.6% of DC plans allow full investment control of assets Additional, 2.7% allows for some participant investment direction Roughly 9% do not allow any participant investment direction

13 IMPORTANCE OF INVESTOR BEHAVIOR IN DC PLANS Traditional financial theories rely on rational consumer decision making Markets are supposed to be efficient, but there is more volatility than explained by financial models alone Over time, psychology research has shown irrational decision making biases This has caused the development of behavioral finance Aligning traditional financial models and theories with real world planning Nobel Prize Winner Richard Thaler called for the end of behavioral finance as separate from traditional finance nearly 20 years ago Successful outcomes in defined contribution plans, as defined by participation, investment performance, and sufficient retirement savings are hindered by biases and human behaviors

14 Understanding the Human Element in Decision Making

15 UNDERSTANDING THE HUMAN ELEMENT IN DECISION MAKING People react to differently depending on how information is presented People are messy, overconfident, and ill-prepared for many situations The dual-self decision making Can you improve outcomes without losing freedom of choice? Nudge and creating better models

16 THE DUAL- SELF Daniel Kohneman s Thinking, Fast and Slow Detailed work on how people make decisions System 1 Quickly sorts through feelings and memories to make a recommendation System 2 Is slow and effortful, making more calculated and rational decisions The issue is that System 1 often wins out over System 2 Takes effort and work to allow System 2 to prevail This is the dual-self a conflict and partnership between emotional and rational

17 WHO IS HUNGRY? Read & Van Leeuwen Study Participants that were not hungry were given two food options They picked the health food for delivery in one week 74% of the time Participants that were hungry were given two food options for immediate consumption They picked the unhealthy food option for immediate consumption 70% of time

18 BEHAVIORAL BIASES IMPEDE GOOD FINANCIAL DECISIONS In daily activities System 1 performs well Essentially an evolutionary process for survival quick thinking Long-term, System 1 has flaws Tends to lead to mistakes for investors Poor at assessing risks and predicting future events Too reactive to current information Behavioral finance is essentially here to define and quantify the mistakes and biases made by System 1 thinking to improve investor outcomes

19 Understanding Behavioral Biases

20 IMPACT OF BIASES ON INVESTMENT PERFORMANCE Francis Kinniry Study (2014) Found that most important underperformance factor for individual investors was the lack of behavioral coaching Staying the course would have resulted in 1.5% of additional annualized returns David Blanchett & Paul Kaplan Developed gamma to quantify cost of poor and good decision making Found that making decisions around asset allocation throughout life and in retirement was extremely important Retirement success could be improved by better decision making

21 RANGE OF BIASES Anchoring Basing estimates on the first piece of information acquired o Example: People tend to rely on the first number that they see, even when it has no relevance to the matter on hand. This can drive people to irrationally believe the price of something is worth more or less than it is today. Framing Reacting differently based on whether the same outcome is presented as a loss or as a gain o Example: Talking about survival rates in medical procedures or success is viewed much more optimistically than discussing the mortality or failure rates, even when the percentages are the same.

22 RANGE OF BIASES PART 2 Endowment Effect Reacting differently based on whether an item is already in possession o Example: People think items that they already own are worth more. If someone is gifted property, they attach more value to it after they have it than when it was gifted. Home Bias Preferring what is most familiar o Example: This leads people to feeling comfortable investing in companies in their home town and their own company stock. This often leads to a lack of diversification overtime.

23 BEHAVIORAL CYCLE OF INVESTING Greed-and-Fear Cycle Buy into market at peak Sell out of market at lows Cycle Strong markets attract more money Poor markets lose money

24 HOW TO HELP CLIENTS Education alone is not enough Need help staying the course Need a plan and course to stay on Need tax planning and asset allocation help

25 Process of Building a Retirement Income Plan

26 Retirement Income Process Preparation 1. Create engagement and evaluate the client s current situation 2. Identify/prioritize retirement goals/expectations 3. Estimate the costs of retirement 4. Evaluate available resources (pension, savings, Social Security, life insurance) 5. Make a preliminary calculation of the client s preparedness for retirement 7. Determine the theoretical approach 8. Consider key retirement decisions and strategies 9. Address risks faced in retirement 10. Test alternatives and measure outcomes 11. Present alternatives to client and decide on a plan 12. Implement the plan Building the Plan 13. Review and revise the plan 6. Modify plan if a shortfall

27 Determine and Prioritize Goals and Expectations Explore retirement life Health Family Work Housing Leisure Life s purpose Legacy -- Long-term care Identify actual retirement activities What activities take on new meaning? What new activities fill the void of work? Create a calendar of a particular day Educate clients about risks and have them prioritize concerns (discuss in a later section)

28 Determine and Prioritize Goals and Expectations Understand the transition into retirement Is the framework of retirement even meaningful? Is retirement voluntary or involuntary? Is deferring retirement voluntary or involuntary? Is the goal a crisp end of work or phasing into retirement? Identify and prioritize financial goals/concerns Relative importance of insuring an income floor Relative Importance of possibility of increasing income Relative importance of leaving a legacy Risk tolerance Willingness to spend more now with possibility of reducing spending later Risk tolerance--tolerance of portfolio losses

29 Choosing a Retirement Income Strategy

30 Determine Approach For Meeting Client s Goals Safety first (flooring) approach Systematic Withdrawals from a single portfolio Bucket or multiple portfolio approach

31 Safety First Approach Based on life cycle finance theory maximize spending over lifetime, not maximizing wealth Based on utility theory goals are determined and prioritized (1) basic needs, (2) emergency funds, (3) discretionary expenses, (4) legacy goals Consider household balance sheet (financial assets, human capital (work), social capital (Social Security) Unfavorable view of safe-withdrawal rate literature Retirees cannot rely on averages Only get one opportunity for a successful retirement

32 Investment Strategies Assets are matched to goals (liabilities) so that risk levels are comparable Volatile assets are not appropriate for basic needs or emergency fund To ensure that basic needs are met look to low risk investments (annuities/government bonds) Lower priority needs can be met with risky assets resulting in potential for reduction/increase in spending Systematic withdrawals from a diversified portfolio Multiple portfolio (bucket) approach

33 Building an Income Base Choosing the amount of income Enough to meet basic needs Enough to meet lifestyle goals Other Low-risk income products Social Security Employer provided pensions Bond ladder that provides income for specified period Annuities Income annuities Variable or indexed with GLWB

34 Strengths/Limitations Ensures minimum needs are met Purchasing income may limit other financial objectives Income base addresses retirement risks Longevity/excess withdrawal/frailty/long-term care/elder financial abuse Annuitizing maximizes spending Spreads spending over uncertain life expectancy Retirees spend income easier than assets

35 Retirement Goals

36

37 Spending, Liquidity, and Legacy for Bonds, Annuities, & Stocks 65-Year Old Female $1 million at retirement Seeks Real $40,000 Spending Through Age % fixed real yield curve Society of Actuaries Individual Annuitant Mortality Table Life-only, CPI-Adjusted Income Annuity True Liquidity: Discretionary Wealth Not Earmarked to Meet Spending Goal 100,000 Monte Carlo Simulations for stock and bond portfolios. Bonds earn a fixed real return of 0.5%. Stocks earn an arithmetic average real return of 6.5% with a 20% annual volatility. Research by Wade Pfau

38 Dr. Wade Pfau s Conclusions Risk Pooling Guarantee supports income for life (protection from longevity and market risk) Less assets earmarked for spending goal Greater clarity about true liquidity availability for spending shocks Mortality credits provide unique source of returns competitive with the risk premium Lifetime spending is guaranteed Greater legacy in the long run Greater true liquidity for spending shocks Partial annuitization integrates risk pooling and risk premium Risk Premium (Investments Only) More legacy in event of short retirement Upside growth may support greater spending and legacy Self-management for longevity & market risk requires conservative spending w/o guarantee

39 Partial Annuitization Impact on Portfolio Sustainability Partial annuitization can have a positive impact on the sustainability of the portfolio if the annuity payout rate is more than the withdrawal rate from the portfolio If payout rate is higher, then a lower withdrawal rate can be used with remaining assets, which extends portfolio sustainability If the payout rate is lower, then portfolio sustainability may decline. However, even if financial assets are depleted, guaranteed payments will continue. This is only a partial failure

40 How A Partial Annuitization Strategy Addresses Retirement Risks Role of diversified portfolio o Inflation risk o Public policy risk o Liquidity o Unexpected expenses o Long-term care o Health care expenses Role of guaranteed income o Longevity risk o Frailty o Financial elder abuse o Market risk o Excess withdrawal risk o Timing risk o Loss of spouse

41 Wealthier People Tend to Live Longer Poorest 10% 11%-20% 21%-30% 31%-40% 41%-50% 51%-60% 61%-70% 71%-80% 81%-90% Richest 10% Change in average additional life expectancy (in years) at age 55, by wealth, between cohorts born in 1920 and Women Men Change (in Years) Source: Barry Bosworth, Brookings Institution Michael Finke, Ph.D. 41

42 Probability Based Approaches Goals not prioritized must meet lifestyle goal or have a failure Safe withdrawal rate is a floor as it always provides upside except for the worst-case scenario Investment approach can be total returns or multiple portfolio approach Focus is on financial assets failure defined as depletion of financial assets Annuitizing considered too costly for marginal increase in safety and lowers chances to fully achieve lifestyle goals Probability approaches include the systematic withdrawal approach and the various bucket strategies

43 Systematic Withdrawal Approach Maintain a diversified portfolio and withdraw lifestyle needs Choosing the safe withdrawal rate arguably provides a floor No guarantees risk of reduction in spending Flexible, good for legacy goal possibility of increased spending

44 Safe Withdrawal Research Worst case scenario using historical analysis and a 30 year time horizon Withdrawal rate based on initial portfolio value plus inflation Look to combine asset classes for best combinations of expected return and volatility 4% becomes 4.5% adding small cap stocks Withdrawal rate ties to time horizon Withdrawal rate can be much higher if you retire when asset values are low

45 Safe Withdrawal Research Impact of adjusting spending Flat withdrawal rate Withdrawal rate based on current values Adjustments based on investment performance Will 4% work today?* Historically, it did not work in most developed countries With today s low fixed investment environment * Pfau, An International Perspective on Safe Withdrawal Rates: The Demise of the 4% Rule? Market Expectations, Asset Allocation and Safe Withdrawal Rates, Both in the Journal of Financial Planning. (2012).

46 Choosing a Withdrawal Rate How is withdrawal rate defined? What is the asset allocation? What is the time horizon? How important is a legacy goal? Willingness to adjust when the market is down? Willingness to take risk (willingness to reduce spending later)? Capacity to take risk (are there other sources of income)?

47 Multiple Portfolio (Buckets) Mental accounting Portfolio management Liability matching Primary strength is helping the client stay on course Limitations can include No guarantees Costs associated with transactions Harder to test

48 Time Segmentation The three phases of retirement Phase one The client is the same as he was before retirement. This typically means the client has no limitations (fully active). Phase two The client experiences moderate limitations. Occurs at different times for different people in the relationship Relationships and interactions with others become more meaningful Phase three The client experiences significant limitations. Appropriate and regular support are needed Family caregivers may need to leave their own jobs Asset allocation Build portfolios to match time segmentations Match asset allocation with income allocation More conservative allocation for nearest time segments

49 Cash Reserve Cash reserve (Evansky) Investment portfolio combined with cash reserve Use cash reserve to meet expenses when the market is down Use portfolio gains to meet expenses and replenish cash reserve when market is up Consider alternatives to cash Reverse mortgage Life insurance cash value

50 Social Security Single largest income source for most retirees 2/3rds of retirees its more than 50% 1/5 th its all of income Provides a floor of income beats any annuity so the first annuity you should every buy is S.S. Deferral Well tested strategy is defer S.S. till 70 and spend based on RMDs

51 Don t Forget Home Equity Housing costs are largest for retirees Home equity also represents America s largest asset 2/3 wealth in home 1/3 other assets for average 65 couple Reverse Mortgages Non-market correlated asset Cash flow Tax benefits Line of credit

52 Time Segmentation Can accommodate different risks that occur in different phases of retirement Bucket approach may resonate well with clients: Stocks are for later time periods, so the client can buy and hold rather than worry about short-term market fluctuations. Without looking at a bucket approach, it is difficult to rationalize to a client why stocks should be in a retirement fund. Clients can sleep better at night. Total asset allocation may be similar to systematic withdrawals

53 Concluding Thoughts

54 Determine Approach For Meeting Client s Goals Safety first (flooring) approach Systematic Withdrawals from a single portfolio Bucket or multiple portfolio approach Consider advisor s preferences Consider client's preferences (safety of income, potential for upside, legacy) Consider client's funding status

55 What We Learn from Each Approach From the safety first approach we learn that we need to prioritize client s goals and determine which are most important From the systematic withdrawal approach we learn that we need to carefully consider how much can be withdrawn from resources and still have them last a lifetime From the bucket approach we learn that a plan has to tell a story so that the client understands how the plan works when things happen

56 Staying the Course Does the client understand the plan? Did the client choose the plan? Was all information considered? Do assets match up with liabilities? Is there enough reevaluation and review?

57 Rewirement Book Rewirement: Rewiring The Way You Think About Retirement!

58 THANK YOU THEAMERICANCOLLEGE.EDU

Low Returns and Optimal Retirement Savings

Low Returns and Optimal Retirement Savings Title Goes Here David Blanchett, Morningstar Michael Finke, The American College Wade Pfau, The American College Retirement According to the Life Cycle Hypothesis

Low Returns and Optimal Retirement Savings Title Goes Here David Blanchett, Morningstar Michael Finke, The American College Wade Pfau, The American College Retirement According to the Life Cycle Hypothesis

Jamie Hopkins, Esq., MBA, LLM, CFP, CLU, RICP Co-Director of the New York Life Center for Retirement Income, Associate Professor of Taxation

Jamie Hopkins, Esq., MBA, LLM, CFP, CLU, RICP Co-Director of the New York Life Center for Retirement Income, Associate Professor of Taxation Jamie.Hopkins@theamericancollege.edu Twitter @RetirementRisks

Jamie Hopkins, Esq., MBA, LLM, CFP, CLU, RICP Co-Director of the New York Life Center for Retirement Income, Associate Professor of Taxation Jamie.Hopkins@theamericancollege.edu Twitter @RetirementRisks

Sustainable Spending for Retirement

What s Different About Retirement? RETIREMENT BEGINS WITH A PLAN TM Sustainable Spending for Retirement Presented by: Wade Pfau, Ph.D., CFA Reduced earnings capacity Visible spending constraint Heightened

What s Different About Retirement? RETIREMENT BEGINS WITH A PLAN TM Sustainable Spending for Retirement Presented by: Wade Pfau, Ph.D., CFA Reduced earnings capacity Visible spending constraint Heightened

Retirement Income Planning for the 99%

Retirement Income Planning for the 99% David Littell, JD, ChFC, Director of the New York Life Center for Retirement Income Don Graves, President and Chief Conversation Starter, HECM Advisors Group Agenda

Retirement Income Planning for the 99% David Littell, JD, ChFC, Director of the New York Life Center for Retirement Income Don Graves, President and Chief Conversation Starter, HECM Advisors Group Agenda

Retirement Income Showdown: RISK POOLING VS. RISK PREMIUM. by Wade D. Pfau

Retirement Income Showdown: RISK POOLING VS. RISK PREMIUM by Wade D. Pfau ABSTRACT The retirement income showdown regards finding the most efficient approach for meeting retirement spending goals: obtaining

Retirement Income Showdown: RISK POOLING VS. RISK PREMIUM by Wade D. Pfau ABSTRACT The retirement income showdown regards finding the most efficient approach for meeting retirement spending goals: obtaining

The case for professional financial advice

The case for professional financial advice Professional financial advisors provide several services that may help the performance of a long-term financial program, and offer value to investors who might

The case for professional financial advice Professional financial advisors provide several services that may help the performance of a long-term financial program, and offer value to investors who might

RETIREMENT PLANNING. Created by Raymond James using Ibbotson Presentation Materials 2011 Morningstar, Inc. All rights reserved. Used with permission.

RETIREMENT PLANNING Erik Melville 603 N Indian River Drive, Suite 300 Fort Pierce, FL 34950 772-460-2500 erik.melville@raymondjames.com www.melvillewealthmanagement.com Created by Raymond James using Ibbotson

RETIREMENT PLANNING Erik Melville 603 N Indian River Drive, Suite 300 Fort Pierce, FL 34950 772-460-2500 erik.melville@raymondjames.com www.melvillewealthmanagement.com Created by Raymond James using Ibbotson

Key Competencies for Proper Retirement Income Planning

The American College TAC Digital Commons Faculty Publications Spring 2011 Key Competencies for Proper Retirement Income Planning David Littell The American College of Financial Services Kenn B. Tachino

The American College TAC Digital Commons Faculty Publications Spring 2011 Key Competencies for Proper Retirement Income Planning David Littell The American College of Financial Services Kenn B. Tachino

Planning for Income to Last

Planning for Income to Last Retirement Income Planning Not FDIC Insured May Lose Value No Bank Guarantee This guide explains why you should consider developing a retirement income plan. It also discusses

Planning for Income to Last Retirement Income Planning Not FDIC Insured May Lose Value No Bank Guarantee This guide explains why you should consider developing a retirement income plan. It also discusses

INVESTMENT POLICY GUIDANCE REPORT. Living in Retirement. A Successful Foundation

INVESTMENT POLICY GUIDANCE REPORT Living in Retirement A Successful Foundation Developing Your The process for creating a strategy Plan for the Expected Your Retirement Journey It all starts with you.

INVESTMENT POLICY GUIDANCE REPORT Living in Retirement A Successful Foundation Developing Your The process for creating a strategy Plan for the Expected Your Retirement Journey It all starts with you.

Planning for income to last

For Investors Planning for income to last Retirement Income Planning Understand the five key financial risks facing retirees Determine how to maximize your income sources Develop a retirement income plan

For Investors Planning for income to last Retirement Income Planning Understand the five key financial risks facing retirees Determine how to maximize your income sources Develop a retirement income plan

Institutional Investment Advisors and Consultants Forum: Developing Expertise and Insights

Institutional Investment Advisors and Consultants Forum: Developing Expertise and Insights OPTIMIZING OUTCOMES WITH AVAILABLE SOLUTIONS Steve Vernon Stanford Center on Longevity June 9, 2015 2 Key Takeaways

Institutional Investment Advisors and Consultants Forum: Developing Expertise and Insights OPTIMIZING OUTCOMES WITH AVAILABLE SOLUTIONS Steve Vernon Stanford Center on Longevity June 9, 2015 2 Key Takeaways

How to Use Reverse Mortgages to Secure Your Retirement

How to Use Reverse Mortgages to Secure Your Retirement October 10, 2016 by Wade D. Pfau, Ph.D., CFA The following is excerpted from Wade Pfau s new book, Reverse Mortgages: How to use Reverse Mortgages

How to Use Reverse Mortgages to Secure Your Retirement October 10, 2016 by Wade D. Pfau, Ph.D., CFA The following is excerpted from Wade Pfau s new book, Reverse Mortgages: How to use Reverse Mortgages

WHAT MATTERS MOST. A woman s guide to an inspired retirement strategy

WHAT MATTERS MOST A woman s guide to an inspired retirement strategy Issued by Pruco Life Insurance Company (in New York, issued by Pruco Life Insurance Company of New Jersey). 0250519-00002-00 Ed. 01/2014

WHAT MATTERS MOST A woman s guide to an inspired retirement strategy Issued by Pruco Life Insurance Company (in New York, issued by Pruco Life Insurance Company of New Jersey). 0250519-00002-00 Ed. 01/2014

Jamie Hopkins, Esq., JD, MBA, LLM, RICP Co-Director of the New York Life Center for Retirement Income Associate Professor of Taxation

Jamie Hopkins, Esq., JD, MBA, LLM, RICP Co-Director of the New York Life Center for Retirement Income Associate Professor of Taxation Jamie.hopkins@theamericancollege.edu Our Discussion The American College

Jamie Hopkins, Esq., JD, MBA, LLM, RICP Co-Director of the New York Life Center for Retirement Income Associate Professor of Taxation Jamie.hopkins@theamericancollege.edu Our Discussion The American College

SOCIAL SECURITY WON T BE ENOUGH:

SOCIAL SECURITY WON T BE ENOUGH: 6 REASONS TO CONSIDER AN INCOME ANNUITY How long before you retire? For some of us it s 20 to 30 years away, and for others it s closer to 5 or 0 years. The key here is

SOCIAL SECURITY WON T BE ENOUGH: 6 REASONS TO CONSIDER AN INCOME ANNUITY How long before you retire? For some of us it s 20 to 30 years away, and for others it s closer to 5 or 0 years. The key here is

Enhancing Your Retirement Planning Toolkit

Enhancing Your Retirement Planning Toolkit Wade Pfau, Ph.D., CFA RetirementResearcher.com/retirement-toolkit What s Different About Retirement? Reduced earnings capacity Visible spending constraint Heightened

Enhancing Your Retirement Planning Toolkit Wade Pfau, Ph.D., CFA RetirementResearcher.com/retirement-toolkit What s Different About Retirement? Reduced earnings capacity Visible spending constraint Heightened

How Much Can Clients Spend in Retirement? A Test of the Two Most Prominent Approaches By Wade Pfau December 10, 2013

How Much Can Clients Spend in Retirement? A Test of the Two Most Prominent Approaches By Wade Pfau December 10, 2013 In my last article, I described research based innovations for variable withdrawal strategies

How Much Can Clients Spend in Retirement? A Test of the Two Most Prominent Approaches By Wade Pfau December 10, 2013 In my last article, I described research based innovations for variable withdrawal strategies

Are Managed-Payout Funds Better than Annuities?

Are Managed-Payout Funds Better than Annuities? July 28, 2015 by Joe Tomlinson Managed-payout funds promise to meet retirees need for sustainable lifetime income without relying on annuities. To see whether

Are Managed-Payout Funds Better than Annuities? July 28, 2015 by Joe Tomlinson Managed-payout funds promise to meet retirees need for sustainable lifetime income without relying on annuities. To see whether

Evaluating Investments versus Insurance in Retirement

Evaluating Investments versus Insurance in Retirement June 30, 2015 by Wade Pfau Retirement-income planning has emerged as a distinct field in the financial services profession. But because it is still

Evaluating Investments versus Insurance in Retirement June 30, 2015 by Wade Pfau Retirement-income planning has emerged as a distinct field in the financial services profession. But because it is still

Breaking Free from the Safe Withdrawal Rate Paradigm: Extending the Efficient Frontier for Retiremen

Breaking Free from the Safe Withdrawal Rate Paradigm: Extending the Efficient Frontier for Retiremen March 5, 2013 by Wade Pfau Combining stocks with single-premium immediate annuities (SPIAs) may be the

Breaking Free from the Safe Withdrawal Rate Paradigm: Extending the Efficient Frontier for Retiremen March 5, 2013 by Wade Pfau Combining stocks with single-premium immediate annuities (SPIAs) may be the

RBC retirement income planning process

Page 1 of 6 RBC retirement income planning process Create income for your retirement At RBC Wealth Management, we believe managing your wealth to produce an income during retirement is fundamentally different

Page 1 of 6 RBC retirement income planning process Create income for your retirement At RBC Wealth Management, we believe managing your wealth to produce an income during retirement is fundamentally different

Retirement. Optimal Asset Allocation in Retirement: A Downside Risk Perspective. JUne W. Van Harlow, Ph.D., CFA Director of Research ABSTRACT

Putnam Institute JUne 2011 Optimal Asset Allocation in : A Downside Perspective W. Van Harlow, Ph.D., CFA Director of Research ABSTRACT Once an individual has retired, asset allocation becomes a critical

Putnam Institute JUne 2011 Optimal Asset Allocation in : A Downside Perspective W. Van Harlow, Ph.D., CFA Director of Research ABSTRACT Once an individual has retired, asset allocation becomes a critical

Take control. Help your clients understand the role of risk control in a portfolio A GUIDE TO CONDUCTING A RISK CONTROL REVIEW

A GUIDE TO CONDUCTING A RISK CONTROL REVIEW Take control Help your clients understand the role of risk control in a portfolio MGA-1658740 FOR REGISTERED REPRESENTATIVE USE ONLY. NOT FOR USE BY THE GENERAL

A GUIDE TO CONDUCTING A RISK CONTROL REVIEW Take control Help your clients understand the role of risk control in a portfolio MGA-1658740 FOR REGISTERED REPRESENTATIVE USE ONLY. NOT FOR USE BY THE GENERAL

Alpha, Beta, and Now Gamma

Alpha, Beta, and Now Gamma David Blanchett, CFA, CFP Head of Retirement Research, Morningstar Investment Management Paul D. Kaplan, Ph.D., CFA Director of Research, Morningstar Canada 2012 Morningstar.

Alpha, Beta, and Now Gamma David Blanchett, CFA, CFP Head of Retirement Research, Morningstar Investment Management Paul D. Kaplan, Ph.D., CFA Director of Research, Morningstar Canada 2012 Morningstar.

How Do You Measure Which Retirement Income Strategy Is Best?

How Do You Measure Which Retirement Income Strategy Is Best? April 19, 2016 by Michael Kitces Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those

How Do You Measure Which Retirement Income Strategy Is Best? April 19, 2016 by Michael Kitces Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those

FPO THE VALUE OF INTEGRATING RETIREMENT ASSETS: CREATING A RELIABLE INCOME IN RETIREMENT

THE NORTHWESTERN MUTUAL LIFE INSURANCE COMPANY (NORTHWESTERN MUTUAL) THE VALUE OF INTEGRATING RETIREMENT ASSETS: CREATING A RELIABLE INCOME IN RETIREMENT FPO 90-2596 (1016) You save and sacrifice throughout

THE NORTHWESTERN MUTUAL LIFE INSURANCE COMPANY (NORTHWESTERN MUTUAL) THE VALUE OF INTEGRATING RETIREMENT ASSETS: CREATING A RELIABLE INCOME IN RETIREMENT FPO 90-2596 (1016) You save and sacrifice throughout

GUARANTEES. Income Diversification. Creating a Plan to Support Your Lifestyle in Retirement

GUARANTEES GROWTH FLEXIBILITY Income Diversification Creating a Plan to Support Your Lifestyle in Retirement Contents Build a Retirement Plan that Can Last a Lifetime 2 Retirement Is Different Today 4

GUARANTEES GROWTH FLEXIBILITY Income Diversification Creating a Plan to Support Your Lifestyle in Retirement Contents Build a Retirement Plan that Can Last a Lifetime 2 Retirement Is Different Today 4

2015 The Self-Made Pension

2015 The Self-Made Pension Using guaranteed income to help secure the retirement you deserve Many workers in decades past relied on company pension plans to provide them with steady income through retirement.

2015 The Self-Made Pension Using guaranteed income to help secure the retirement you deserve Many workers in decades past relied on company pension plans to provide them with steady income through retirement.

A Better Systematic Withdrawal Strategy--The Actuarial Approach Ken Steiner, Fellow, Society of Actuaries, Retired February 2014

A Better Systematic Withdrawal Strategy--The Actuarial Approach Ken Steiner, Fellow, Society of Actuaries, Retired February 2014 Retirees generally have at least two potentially conflicting financial goals:

A Better Systematic Withdrawal Strategy--The Actuarial Approach Ken Steiner, Fellow, Society of Actuaries, Retired February 2014 Retirees generally have at least two potentially conflicting financial goals:

Fitting Home Equity into a Retirement Income Strategy

Fitting Home Equity into a Retirement Income Strategy Wade Pfau, Ph.D., CFA RetirementResearcher.com/reverse-mortgages What s Different About Retirement? Reduced earnings capacity Visible spending constraint

Fitting Home Equity into a Retirement Income Strategy Wade Pfau, Ph.D., CFA RetirementResearcher.com/reverse-mortgages What s Different About Retirement? Reduced earnings capacity Visible spending constraint

Optimal Retirement Income Solutions in DC Retirement Plans Phase 1: Baseline, Interim Results and Commentary

Optimal Retirement Income Solutions in DC Retirement Plans Phase 1: Baseline, Interim Results and Commentary July 2015 0 Acknowledgments Authors: Steve Vernon, FSA, svernon@stanford.edu Dr. Wade Pfau,

Optimal Retirement Income Solutions in DC Retirement Plans Phase 1: Baseline, Interim Results and Commentary July 2015 0 Acknowledgments Authors: Steve Vernon, FSA, svernon@stanford.edu Dr. Wade Pfau,

Establishing Your Retirement Income Stream

1 Establishing Your Retirement Income Stream What is important about retirement planning to you? 2 Building your retirement house 4 Legacy Benefits 3 2 Retirement income planning Accumulation 1 Expenses

1 Establishing Your Retirement Income Stream What is important about retirement planning to you? 2 Building your retirement house 4 Legacy Benefits 3 2 Retirement income planning Accumulation 1 Expenses

Random returns: What investors should know about an unpredictable retirement risk

Wealth Protection Expertise SM Random returns: What investors should know about an unpredictable retirement risk Not a deposit Not FDIC-insured May go down in value Not insured by any federal government

Wealth Protection Expertise SM Random returns: What investors should know about an unpredictable retirement risk Not a deposit Not FDIC-insured May go down in value Not insured by any federal government

Optimizing Retirement Income Solutions in Defined Contribution Retirement Plans. A Framework for Building Retirement Income Portfolios

Optimizing Retirement Income Solutions in Defined Contribution Retirement Plans A Framework for Building Retirement Income Portfolios Dr. Wade Pfau Joe Tomlinson, FSA, CFP Steve Vernon, FSA MAY 2016 Acknowledgements

Optimizing Retirement Income Solutions in Defined Contribution Retirement Plans A Framework for Building Retirement Income Portfolios Dr. Wade Pfau Joe Tomlinson, FSA, CFP Steve Vernon, FSA MAY 2016 Acknowledgements

How to Rescue an Underfunded Retirement

How to Rescue an Underfunded Retirement February 19, 2018 by Joe Tomlinson Americans have under-saved and will need more than withdrawals from savings to survive retirement. An optimal withdrawal strategy

How to Rescue an Underfunded Retirement February 19, 2018 by Joe Tomlinson Americans have under-saved and will need more than withdrawals from savings to survive retirement. An optimal withdrawal strategy

Be out living your life, not outliving your savings.

Talk to your financial advisor to learn more about how an annuity can benefit your retirement plan. Discover the value of an annuity. Be out living your life, not outliving your savings. Discover the value

Talk to your financial advisor to learn more about how an annuity can benefit your retirement plan. Discover the value of an annuity. Be out living your life, not outliving your savings. Discover the value

TOPICS IN RETIREMENT INCOME

TOPICS IN RETIREMENT INCOME Defined Contribution Plan Design: Facilitating Income Replacement in Retirement For plan sponsors, facilitating the ability of defined contribution (DC) plan participants to

TOPICS IN RETIREMENT INCOME Defined Contribution Plan Design: Facilitating Income Replacement in Retirement For plan sponsors, facilitating the ability of defined contribution (DC) plan participants to

Time Segmentation as the Compromise Solution for Retirement Income

Time Segmentation as the Compromise Solution for Retirement Income March 27, 2017 by Wade D. Pfau The Financial Planning Association (FPA) divides retirement income strategies into three categories: systematic

Time Segmentation as the Compromise Solution for Retirement Income March 27, 2017 by Wade D. Pfau The Financial Planning Association (FPA) divides retirement income strategies into three categories: systematic

Low Returns and Optimal Retirement Savings

Low Returns and Optimal Retirement Savings David Blanchett, Michael Finke, and Wade Pfau September 2017 PRC WP2017 Pension Research Council Working Paper Pension Research Council The Wharton School, University

Low Returns and Optimal Retirement Savings David Blanchett, Michael Finke, and Wade Pfau September 2017 PRC WP2017 Pension Research Council Working Paper Pension Research Council The Wharton School, University

CFA Level III - LOS Changes

CFA Level III - LOS Changes 2016-2017 Ethics Ethics Ethics Ethics Ethics Ethics Ethics Ethics Topic LOS Level III - 2016 (332 LOS) LOS Level III - 2017 (337 LOS) Compared 1.1.a 1.1.b 1.2.a 1.2.b 2.3.a

CFA Level III - LOS Changes 2016-2017 Ethics Ethics Ethics Ethics Ethics Ethics Ethics Ethics Topic LOS Level III - 2016 (332 LOS) LOS Level III - 2017 (337 LOS) Compared 1.1.a 1.1.b 1.2.a 1.2.b 2.3.a

BUILDING INVESTMENT PORTFOLIOS WITH AN INNOVATIVE APPROACH

BUILDING INVESTMENT PORTFOLIOS WITH AN INNOVATIVE APPROACH Asset Management Services ASSET MANAGEMENT SERVICES WE GO FURTHER When Bob James founded Raymond James in 1962, he established a tradition of

BUILDING INVESTMENT PORTFOLIOS WITH AN INNOVATIVE APPROACH Asset Management Services ASSET MANAGEMENT SERVICES WE GO FURTHER When Bob James founded Raymond James in 1962, he established a tradition of

PREPARING FOR A MORE COMFORTABLE RETIREMENT

PREPARING FOR A MORE COMFORTABLE RETIREMENT As financial professionals who specialize in helping government employees transition from work to retirement, we understand that you may have questions about

PREPARING FOR A MORE COMFORTABLE RETIREMENT As financial professionals who specialize in helping government employees transition from work to retirement, we understand that you may have questions about

Safe Withdrawal Rates from your Retirement Portfolio

American Association of Individual Investors Silicon Valley Chapter presents Financial Planning Workshop Safe Withdrawal Rates from your Retirement Portfolio Fred Smith fred@fredsmithfinance.com Financial

American Association of Individual Investors Silicon Valley Chapter presents Financial Planning Workshop Safe Withdrawal Rates from your Retirement Portfolio Fred Smith fred@fredsmithfinance.com Financial

Managing Your Retirement Income

Managing Your Retirement Income Developed by: 2006, National Association of Foundation for Retirement Education. All rights reserved. This presentation may not to be used without permission by NAVA or

Managing Your Retirement Income Developed by: 2006, National Association of Foundation for Retirement Education. All rights reserved. This presentation may not to be used without permission by NAVA or

$$ Behavioral Finance 1

$$ Behavioral Finance 1 Why do financial advisors exist? Know active stock picking rarely produces winners Efficient markets tells us information immediately is reflected in prices If buy baskets/indices

$$ Behavioral Finance 1 Why do financial advisors exist? Know active stock picking rarely produces winners Efficient markets tells us information immediately is reflected in prices If buy baskets/indices

Advantage IV Variable Annuity

Advantage IV Variable Annuity IT S ALWAYS THE RIGHT TIME It s never too late to get where you want to go When you begin saving for retirement at the beginning of your career, you re giving yourself the

Advantage IV Variable Annuity IT S ALWAYS THE RIGHT TIME It s never too late to get where you want to go When you begin saving for retirement at the beginning of your career, you re giving yourself the

A plan for tomorrow can make all the difference

Nationwide Variable Universal Life Accumulator Client guide A plan for tomorrow can make all the difference Make your future count 1 NATIONWIDE LIFE AND ANNUITY INSURANCE COMPANY 2 Tomorrow starts today

Nationwide Variable Universal Life Accumulator Client guide A plan for tomorrow can make all the difference Make your future count 1 NATIONWIDE LIFE AND ANNUITY INSURANCE COMPANY 2 Tomorrow starts today

Protect what you have

Nationwide Variable Universal Life Protector Client guide Protect what you have Plan for what you want 1 NATIONWIDE LIFE AND ANNUITY INSURANCE COMPANY 2 Tomorrow starts today As the world continues to

Nationwide Variable Universal Life Protector Client guide Protect what you have Plan for what you want 1 NATIONWIDE LIFE AND ANNUITY INSURANCE COMPANY 2 Tomorrow starts today As the world continues to

Retirement Plan Solutions GUIDED SIMPLE TRANSPARENT

Retirement Plan Solutions GUIDED SIMPLE TRANSPARENT Are You Ready for Your Retirement? Consider these grim statistics: The average working household has virtually no retirement savings, with the median

Retirement Plan Solutions GUIDED SIMPLE TRANSPARENT Are You Ready for Your Retirement? Consider these grim statistics: The average working household has virtually no retirement savings, with the median

The Hidden Peril in Sequence of Returns Risk

The Hidden Peril in Sequence of Returns Risk March 10, 2015 by Wade Pfau Should retirees place greater faith in stocks ability to outperform bonds over reasonable holding periods or in insurance companies

The Hidden Peril in Sequence of Returns Risk March 10, 2015 by Wade Pfau Should retirees place greater faith in stocks ability to outperform bonds over reasonable holding periods or in insurance companies

2015 ERISA Advisory Council Model Notices and Disclosures for Pension Risk Transfers May 28, 2015

2015 ERISA Advisory Council Model Notices and Disclosures for Pension Risk Transfers May 28, 2015 Good afternoon, members of the Council. My name is Roberta Rafaloff. I am a vice president in Corporate

2015 ERISA Advisory Council Model Notices and Disclosures for Pension Risk Transfers May 28, 2015 Good afternoon, members of the Council. My name is Roberta Rafaloff. I am a vice president in Corporate

Eight Core Ideas to Guide Retirement Income Planning

Eight Core Ideas to Guide Retirement Income Planning February 15, 2016 by Wade D. Pfau Eight key messages and themes have underscored my writing and research. Those guidelines serve as a manifesto for

Eight Core Ideas to Guide Retirement Income Planning February 15, 2016 by Wade D. Pfau Eight key messages and themes have underscored my writing and research. Those guidelines serve as a manifesto for

Secure your future with guaranteed lifetime income

An Educational Guide for Consumers Secure your future with guaranteed lifetime income MassMutual RetireEase Choice SM Flexible Premium Deferred Income Annuity Table of contents 1 What does retirement mean

An Educational Guide for Consumers Secure your future with guaranteed lifetime income MassMutual RetireEase Choice SM Flexible Premium Deferred Income Annuity Table of contents 1 What does retirement mean

PHOENIX PERSONAL PROTECTION CHOICE

Protect your financial future: Your income, your family, your lifestyle. PHOENIX PERSONAL PROTECTION CHOICE A single-premium fixed indexed annuity with flexibility to address multiple needs IRS Circular

Protect your financial future: Your income, your family, your lifestyle. PHOENIX PERSONAL PROTECTION CHOICE A single-premium fixed indexed annuity with flexibility to address multiple needs IRS Circular

BETTER PARTICIPANT OUTCOMES

BETTER PARTICIPANT OUTCOMES through in-plan guaranteed retirement income Christine C. Marcks John J. Kalamarides President Senior Vice President Full Service Solutions Prudential Retirement Prudential

BETTER PARTICIPANT OUTCOMES through in-plan guaranteed retirement income Christine C. Marcks John J. Kalamarides President Senior Vice President Full Service Solutions Prudential Retirement Prudential

BEYOND THE 4% RULE J.P. MORGAN RESEARCH FOCUSES ON THE POTENTIAL BENEFITS OF A DYNAMIC RETIREMENT INCOME WITHDRAWAL STRATEGY.

BEYOND THE 4% RULE RECENT J.P. MORGAN RESEARCH FOCUSES ON THE POTENTIAL BENEFITS OF A DYNAMIC RETIREMENT INCOME WITHDRAWAL STRATEGY. Over the past decade, retirees have been forced to navigate the dual

BEYOND THE 4% RULE RECENT J.P. MORGAN RESEARCH FOCUSES ON THE POTENTIAL BENEFITS OF A DYNAMIC RETIREMENT INCOME WITHDRAWAL STRATEGY. Over the past decade, retirees have been forced to navigate the dual

Estimating The True Cost of Retirement

MARCH 22, 2017 Estimating The True Cost of Retirement TD Ameritrade, Inc., member FINRA/SIPC. TD Ameritrade is a trademark jointly owned by TD Ameritrade IP Company, Inc. and The Toronto-Dominion Bank.

MARCH 22, 2017 Estimating The True Cost of Retirement TD Ameritrade, Inc., member FINRA/SIPC. TD Ameritrade is a trademark jointly owned by TD Ameritrade IP Company, Inc. and The Toronto-Dominion Bank.

We re here to help YOU plan for the future

We re here to help YOU plan for the future RETIREMENT PLANNING Annuity Fund of the International Union of Operating Engineers, Local Union 94-94A-94B, AFL-CIO John Hancock Retirement Plan Services LLC

We re here to help YOU plan for the future RETIREMENT PLANNING Annuity Fund of the International Union of Operating Engineers, Local Union 94-94A-94B, AFL-CIO John Hancock Retirement Plan Services LLC

RETIREMENT QUESTIONS GOVERNMENT EMPLOYEES SHOULD BE ASKING

RETIREMENT QUESTIONS GOVERNMENT EMPLOYEES SHOULD BE ASKING 8/25/16 Preparing For a More Comfortable Retirement As financial professionals who specialize in helping government employees transition from

RETIREMENT QUESTIONS GOVERNMENT EMPLOYEES SHOULD BE ASKING 8/25/16 Preparing For a More Comfortable Retirement As financial professionals who specialize in helping government employees transition from

Income Mindsets. Why segmentation is key to winning in the Baby Boomer market (1/11/18)

") Income Mindsets Why segmentation is key to winning in the Baby Boomer market 1678298 (1/11/18) 1 Retirement income isn t one-size-fits-all 2 Retirement planning and advice is different, too. Accumulation

Income Mindsets Why segmentation is key to winning in the Baby Boomer market 1678298 (1/11/18) 1 Retirement income isn t one-size-fits-all 2 Retirement planning and advice is different, too. Accumulation

Retirement Withdrawal Strategies WITHDRAWAL STRATEGIES DURING RETIREMENT MEET MARY ELLEN DUGGAN. I. Taking inventory of available resources

Retirement Withdrawal Strategies Not FDIC-insured. Not bank-guaranteed. May lose value. Dreyfus Service Corporation, Distributor CONVERGENT RETIREMENT PLAN SOLUTIONS, LLC WITHDRAWAL STRATEGIES DURING RETIREMENT

Retirement Withdrawal Strategies Not FDIC-insured. Not bank-guaranteed. May lose value. Dreyfus Service Corporation, Distributor CONVERGENT RETIREMENT PLAN SOLUTIONS, LLC WITHDRAWAL STRATEGIES DURING RETIREMENT

A New Generation Retirement Strategy

A New Generation Retirement Strategy Today, Optimizing Retirement Income Requires an Increased Focus on Efficiency 8/13 80060-13A No bank guarantee Not a deposit May lose value Not FDIC/NCUA insured Not

A New Generation Retirement Strategy Today, Optimizing Retirement Income Requires an Increased Focus on Efficiency 8/13 80060-13A No bank guarantee Not a deposit May lose value Not FDIC/NCUA insured Not

USING DEFINED MATURITY BOND FUNDS AND QLACs TO BETTER MANAGE RETIREMENT RISKS

USING DEFINED MATURITY BOND FUNDS AND QLACs TO BETTER MANAGE RETIREMENT RISKS A Whitepaper for Franklin Templeton and MetLife by WADE D. PFAU, PH.D., CFA Professor of Retirement Income The American College

USING DEFINED MATURITY BOND FUNDS AND QLACs TO BETTER MANAGE RETIREMENT RISKS A Whitepaper for Franklin Templeton and MetLife by WADE D. PFAU, PH.D., CFA Professor of Retirement Income The American College

The 15 Minute Retirement Planner

The 15 Minute Retirement Planner!!What do you need?!!where are you Now?!!What do you do to get inside the Curve? The Old Rules Don t Apply Once upon a time, you worked for the same company most of your

The 15 Minute Retirement Planner!!What do you need?!!where are you Now?!!What do you do to get inside the Curve? The Old Rules Don t Apply Once upon a time, you worked for the same company most of your

ACHIEVING RETIREMENT SECURITY IN AN ERA OF UNCERTAINTY: Three Important Steps

ACHIEVING RETIREMENT SECURITY IN AN ERA OF UNCERTAINTY: Three Important Steps Christine C. Marcks President, Prudential Retirement While the goal of achieving retirement security is arguably more challenging

ACHIEVING RETIREMENT SECURITY IN AN ERA OF UNCERTAINTY: Three Important Steps Christine C. Marcks President, Prudential Retirement While the goal of achieving retirement security is arguably more challenging

Why Advisors Should Use Deferred-Income Annuities

Why Advisors Should Use Deferred-Income Annuities November 24, 2015 by Michael Finke Retirement income planning is a mathematical problem in which an investor begins with a lump sum of wealth and withdraws

Why Advisors Should Use Deferred-Income Annuities November 24, 2015 by Michael Finke Retirement income planning is a mathematical problem in which an investor begins with a lump sum of wealth and withdraws

WHY PURCHASE A DEFERRED FIXED ANNUITY IN A RISING INTEREST-RATE ENVIRONMENT?

WHY PURCHASE A DEFERRED FIXED ANNUITY IN A RISING INTEREST-RATE ENVIRONMENT? A White Paper for Pacific Life by Wade D. Pfau, Ph.D., CFA FAC0904-1217 Pacific Life Insurance Company commissioned The American

WHY PURCHASE A DEFERRED FIXED ANNUITY IN A RISING INTEREST-RATE ENVIRONMENT? A White Paper for Pacific Life by Wade D. Pfau, Ph.D., CFA FAC0904-1217 Pacific Life Insurance Company commissioned The American

SURVIVAL GUIDE FOR PRODUCTIVE DISCUSSIONS

SURVIVAL GUIDE FOR PRODUCTIVE DISCUSSIONS Representatives must be sure to obtain all pertinent information about their clients in order to better understand them and make appropriate recommendations. This

SURVIVAL GUIDE FOR PRODUCTIVE DISCUSSIONS Representatives must be sure to obtain all pertinent information about their clients in order to better understand them and make appropriate recommendations. This

QLACs. Qualified Longevity Annuity Contracts. Annuity Product Guides. Defer RMDs and convert your retirement savings into guaranteed lifetime income

Annuity Product s QLACs Qualified Longevity Annuity Contracts Defer RMDs and convert your retirement savings into guaranteed lifetime income Modernizing retirement security through trust, transparency

Annuity Product s QLACs Qualified Longevity Annuity Contracts Defer RMDs and convert your retirement savings into guaranteed lifetime income Modernizing retirement security through trust, transparency

Guaranteed income for life. In any market.

Guaranteed income for life. In any market. Schwab Retirement Income Variable Annuity with optional Guaranteed Lifetime Withdrawal Benefit. A variable annuity from Charles Schwab, issued by Pacific Life.*

Guaranteed income for life. In any market. Schwab Retirement Income Variable Annuity with optional Guaranteed Lifetime Withdrawal Benefit. A variable annuity from Charles Schwab, issued by Pacific Life.*

No Portfolio is an Island

No Portfolio is an Island David Blanchett, PhD, CFA, CFP Head of Retirement Research Morningstar Investment Management LLC 2018 Morningstar. All Rights Reserved. For Financial Professional Use Only. These

No Portfolio is an Island David Blanchett, PhD, CFA, CFP Head of Retirement Research Morningstar Investment Management LLC 2018 Morningstar. All Rights Reserved. For Financial Professional Use Only. These

Optimal Withdrawal Strategy for Retirement Income Portfolios

Optimal Withdrawal Strategy for Retirement Income Portfolios David Blanchett, CFA Head of Retirement Research Maciej Kowara, Ph.D., CFA Senior Research Consultant Peng Chen, Ph.D., CFA President September

Optimal Withdrawal Strategy for Retirement Income Portfolios David Blanchett, CFA Head of Retirement Research Maciej Kowara, Ph.D., CFA Senior Research Consultant Peng Chen, Ph.D., CFA President September

Determining a Realistic Withdrawal Amount and Asset Allocation in Retirement

Determining a Realistic Withdrawal Amount and Asset Allocation in Retirement >> Many people look forward to retirement, but it can be one of the most complicated stages of life from a financial planning

Determining a Realistic Withdrawal Amount and Asset Allocation in Retirement >> Many people look forward to retirement, but it can be one of the most complicated stages of life from a financial planning

Vanguard s Principles for Financing Retirement

Vanguard s Principles for Financing Retirement At Vanguard, years of experience have taught us that our clients focus changes fundamentally as they approach and enter retirement. After years of accumulating

Vanguard s Principles for Financing Retirement At Vanguard, years of experience have taught us that our clients focus changes fundamentally as they approach and enter retirement. After years of accumulating

Transition to a lifetime of financial security.

A Variable Annuity Guide for Individuals Transition to a lifetime of financial security. MassMutual Transitions Select SM variable annuity Financial security starts with good decisions Your future financial

A Variable Annuity Guide for Individuals Transition to a lifetime of financial security. MassMutual Transitions Select SM variable annuity Financial security starts with good decisions Your future financial

Alpha, Beta, and Now Gamma

Alpha, Beta, and Now Gamma Scott Mackenzie President & CEO Morningstar Canada 2013 Morningstar. All Rights Reserved. These materials are for information and/or illustrative purposes only. The Morningstar

Alpha, Beta, and Now Gamma Scott Mackenzie President & CEO Morningstar Canada 2013 Morningstar. All Rights Reserved. These materials are for information and/or illustrative purposes only. The Morningstar

Sun Life Financial Advisor Guide

Sun Life Financial Advisor Guide managed by CI Investments Inc. issued by Sun Life Assurance Company of Canada SunWise Essential Series 2.............................. 1 Retirement risks.......................................

Sun Life Financial Advisor Guide managed by CI Investments Inc. issued by Sun Life Assurance Company of Canada SunWise Essential Series 2.............................. 1 Retirement risks.......................................

Age-dependent or target-driven investing?

Age-dependent or target-driven investing? New research identifies the best funding and investment strategies in defined contribution pension plans for rational econs and for human investors When designing

Age-dependent or target-driven investing? New research identifies the best funding and investment strategies in defined contribution pension plans for rational econs and for human investors When designing

ONcore Variable Annuities

ONcore Variable Annuities Plan Accumulate Protect Access Table of Contents 2 Plan Overcome Risk Through Planning 6 Accumulate Accumulate Wealth and Manage Risk Using ONcore Variable Annuities 8 Protect

ONcore Variable Annuities Plan Accumulate Protect Access Table of Contents 2 Plan Overcome Risk Through Planning 6 Accumulate Accumulate Wealth and Manage Risk Using ONcore Variable Annuities 8 Protect

Behavioral Economics. Student Presentations. Daniel Kahneman, Thinking, Fast and Slow

Student Presentations Daniel Kahneman, Thinking, Fast and Slow Chapter 26, Prospect Theory The main idea or concept of this chapter: Diminishing Sensitivity When people have different amounts of wealth,

Student Presentations Daniel Kahneman, Thinking, Fast and Slow Chapter 26, Prospect Theory The main idea or concept of this chapter: Diminishing Sensitivity When people have different amounts of wealth,

Retirement planning YOUR GUIDE

Retirement planning YOUR GUIDE Choices today can lead to freedom tomorrow What s inside Introduction...1 Lifestyle planning...2 Potential sources of retirement income..5 Life insurance...6 Maximizing after-tax

Retirement planning YOUR GUIDE Choices today can lead to freedom tomorrow What s inside Introduction...1 Lifestyle planning...2 Potential sources of retirement income..5 Life insurance...6 Maximizing after-tax

Initial Conditions and Optimal Retirement Glide Paths

Initial Conditions and Optimal Retirement Glide Paths by David M., CFP, CFA David M., CFP, CFA, is head of retirement research at Morningstar Investment Management. He is the 2015 recipient of the Journal

Initial Conditions and Optimal Retirement Glide Paths by David M., CFP, CFA David M., CFP, CFA, is head of retirement research at Morningstar Investment Management. He is the 2015 recipient of the Journal

Sustainable Withdrawal Rate During Retirement

FINANCIAL PLANNING UPDATE APRIL 24, 2017 Sustainable Withdrawal Rate During Retirement A recurring question we address with clients during all phases of planning to ensure financial independence is How

FINANCIAL PLANNING UPDATE APRIL 24, 2017 Sustainable Withdrawal Rate During Retirement A recurring question we address with clients during all phases of planning to ensure financial independence is How

CFA Level III - LOS Changes

CFA Level III - LOS Changes 2017-2018 Ethics Ethics Ethics Ethics Ethics Ethics Ethics Topic LOS Level III - 2017 (337 LOS) LOS Level III - 2018 (340 LOS) Compared 1.1.a 1.1.b 1.2.a 1.2.b 2.3.a 2.3.b 2.4.a

CFA Level III - LOS Changes 2017-2018 Ethics Ethics Ethics Ethics Ethics Ethics Ethics Topic LOS Level III - 2017 (337 LOS) LOS Level III - 2018 (340 LOS) Compared 1.1.a 1.1.b 1.2.a 1.2.b 2.3.a 2.3.b 2.4.a

Do We Invest with Our Hearts or Minds? How Behavioral Finance Can Dramatically Affect Your Wealth

Do We Invest with Our Hearts or Minds? How Behavioral Finance Can Dramatically Affect Your Wealth PART ONE In the first part of a two-part series on how advisors can deliver value to their clients, George

Do We Invest with Our Hearts or Minds? How Behavioral Finance Can Dramatically Affect Your Wealth PART ONE In the first part of a two-part series on how advisors can deliver value to their clients, George

INVESTMENT SERVICES. Topics in... AN INTRODUCTION TO GOALS DRIVEN WEALTH MANAGEMENT

Topics in... INVESTMENT SERVICES AN INTRODUCTION TO GOALS DRIVEN WEALTH MANAGEMENT A disciplined investment approach that empowers you with confidence. At first glance, the notion of setting goals for

Topics in... INVESTMENT SERVICES AN INTRODUCTION TO GOALS DRIVEN WEALTH MANAGEMENT A disciplined investment approach that empowers you with confidence. At first glance, the notion of setting goals for

Nearly optimal asset allocations in retirement

MPRA Munich Personal RePEc Archive Nearly optimal asset allocations in retirement Wade Donald Pfau National Graduate Institute for Policy Studies (GRIPS) 31. July 2011 Online at https://mpra.ub.uni-muenchen.de/32506/

MPRA Munich Personal RePEc Archive Nearly optimal asset allocations in retirement Wade Donald Pfau National Graduate Institute for Policy Studies (GRIPS) 31. July 2011 Online at https://mpra.ub.uni-muenchen.de/32506/

CLS ADVISOR IQ SERIES MAKING RETIREMENT INCOME LAST: A ROADMAP FOR GUIDING INVESTORS THROUGH RETIREMENT INCOME ISSUES

CLS ADVISOR IQ SERIES MAKING RETIREMENT INCOME LAST: A ROADMAP FOR GUIDING INVESTORS THROUGH RETIREMENT INCOME ISSUES Table of Contents Executive Summary Introduction The Magic Number Income Considerations

CLS ADVISOR IQ SERIES MAKING RETIREMENT INCOME LAST: A ROADMAP FOR GUIDING INVESTORS THROUGH RETIREMENT INCOME ISSUES Table of Contents Executive Summary Introduction The Magic Number Income Considerations

A Planning Guide for Participants Nearing Retirement

A Planning Guide for Participants Nearing Retirement What are your plans for retirement? For some, retirement is about living out dreams they didn t have time for during their working years. For others,

A Planning Guide for Participants Nearing Retirement What are your plans for retirement? For some, retirement is about living out dreams they didn t have time for during their working years. For others,

David M. Jones, MBA, CFP

White Paper: How Traditional Investing Can Fail Baby Boomers David M. Jones, MBA, CFP www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities

White Paper: How Traditional Investing Can Fail Baby Boomers David M. Jones, MBA, CFP www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities

developed by the National Association of Variable Annuities (NAVA) and the International Foundation for Retirement Education (InFRE) V.5 rev

and the International Foundation for Retirement Education (InFRE) V.5 rev") Managing Retirement Income Planning Worksheet developed by the National Association of Variable Annuities (NAVA) and the International Foundation for Retirement Education (InFRE) V.5 rev 10.03.06 Managing

Managing Retirement Income Planning Worksheet developed by the National Association of Variable Annuities (NAVA) and the International Foundation for Retirement Education (InFRE) V.5 rev 10.03.06 Managing

Dalbar 2017: Investors Suck At Investing & Tips For Advisors

Dalbar 2017: Investors Suck At Investing & Tips For Advisors September 25, 2017 by Lance Roberts of Real Investment Advice Several years ago, I began writing an annual update discussing Dalbar s Quantitative

Dalbar 2017: Investors Suck At Investing & Tips For Advisors September 25, 2017 by Lance Roberts of Real Investment Advice Several years ago, I began writing an annual update discussing Dalbar s Quantitative

SPIAs. Single Premium Immediate Annuities. Annuity Product Guides. Convert your retirement savings into a guaranteed lifetime income stream

Annuity Product s SPIAs Single Premium Immediate Annuities Convert your retirement savings into a guaranteed lifetime income stream Modernizing retirement security through trust, transparency and by putting

Annuity Product s SPIAs Single Premium Immediate Annuities Convert your retirement savings into a guaranteed lifetime income stream Modernizing retirement security through trust, transparency and by putting

Mile Marker CONVERSATIONS RETIREMENT ROADMAP TO. Issued by Pruco Life Insurance Company and by Pruco Life Insurance Company of New Jersey.

Mile Marker CONVERSATIONS ROADMAP TO RETIREMENT Issued by Pruco Life Insurance Company and by Pruco Life Insurance Company of New Jersey. 0287505-00003-00 Ed. 04/2017 Knowing what s down the road can help

Mile Marker CONVERSATIONS ROADMAP TO RETIREMENT Issued by Pruco Life Insurance Company and by Pruco Life Insurance Company of New Jersey. 0287505-00003-00 Ed. 04/2017 Knowing what s down the road can help

Generational Distinctions in Retirement Planning

Generational Distinctions in Retirement Planning Frank O Connor - VP, Research and Outreach IRI Steve Cooney VP Annuity Business Development & Innovation Nationwide David Laster, PhD, CFA Managing Director,

Generational Distinctions in Retirement Planning Frank O Connor - VP, Research and Outreach IRI Steve Cooney VP Annuity Business Development & Innovation Nationwide David Laster, PhD, CFA Managing Director,

2016 MDRT Annual Meeting e-handout Material. 4th Generation Retirement Planning. 3:30 5:00 p.m.

2016 MDRT Annual Meeting e-handout Material Title: Speaker: 4th Generation Retirement Planning Guy E. Baker, MSFS, CLU Presentation Date: Tuesday, June 14, 2016 Presentation Time: 10:00-11:30 a.m. AND

2016 MDRT Annual Meeting e-handout Material Title: Speaker: 4th Generation Retirement Planning Guy E. Baker, MSFS, CLU Presentation Date: Tuesday, June 14, 2016 Presentation Time: 10:00-11:30 a.m. AND

Measuring Retirement Plan Effectiveness

T. Rowe Price Measuring Retirement Plan Effectiveness T. Rowe Price Plan Meter helps sponsors assess and improve plan performance Retirement Insights Once considered ancillary to defined benefit (DB) pension

T. Rowe Price Measuring Retirement Plan Effectiveness T. Rowe Price Plan Meter helps sponsors assess and improve plan performance Retirement Insights Once considered ancillary to defined benefit (DB) pension

Comparing a Bucket Strategy and a Systematic Withdrawal Strategy

Comparing a Bucket Strategy and a Systematic Withdrawal Strategy By Noelle E. Fox Article Highlights Advisers often present retirees with either a systematic withdrawal strategy or a bucket strategy. A

Comparing a Bucket Strategy and a Systematic Withdrawal Strategy By Noelle E. Fox Article Highlights Advisers often present retirees with either a systematic withdrawal strategy or a bucket strategy. A

Hello and good morning/afternoon. I m with MetLife, and today I d like to talk to you about a new way that your clients can build future, pension

Hello and good morning/afternoon. I m with MetLife, and today I d like to talk to you about a new way that your clients can build future, pension like lifetime income. But this new annuity product from

Hello and good morning/afternoon. I m with MetLife, and today I d like to talk to you about a new way that your clients can build future, pension like lifetime income. But this new annuity product from