POLICY BRIEFING. ! Institute for Fiscal Studies 2015 Green Budget

|

|

|

- Marilynn Bailey

- 5 years ago

- Views:

Transcription

1 Institute for Fiscal Studies 2015 Green Budget 1 March 2015 Mark Upton, LGIU Associate Summary This briefing is a summary of the key relevant themes in the Institute of Fiscal Studies 2015 Green Budget which discusses some of the issues confronting the Chancellor ahead of his 2015 Budget Statement on Wednesday 18 March. Growth at 2.6% places the UK at the top of the G7 league table, though it did lose momentum towards the end of Growth is expected to be 3% in 2015 and 2.8% in 2016 driven by domestic markets. There are short term risks associated with an uncertain election outcome and the US and euro zone economies. Since the 2008 recession the domestic labour market has been characterised by robust employment and weak earnings growth for particular groups underpinned by weak productivity. Employment is back to its pre-2008 levels. Government debt is forecast to fall from 81.1% of national income in to reach 1% surplus in Nonetheless debt is likely to remain high by international standards for some time. All three of the main political parties have set out slightly different approaches for borrowing, but all want to see debt falling as a share of national income by at least the end of the next parliament. The 2014 Autumn Statement implies a real cut of 14.1% to departmental spending over the next parliament. However for all these parties the cuts may not be as deep as this. There is an apparent political consensus that spending on health, overseas aid (and education) should be protected, leaving considerable uncertainty for other departmental spending. What seems certain is that some will face large cuts regardless of the outcome of the general election.

2 Even if the NHS achieves it productivity target (2.4% per year) it will require a 0.8% a year real terms increase to meet demand and cost pressures. To deliver the 2014 Autumn Statement public borrowing plans without increasing taxation would require a 21 billion reduction in social security spending. Continuing the current policy of freezing most working age benefits for five years would only save 6.9 billion. The last five general elections have all been followed by net tax rises of more than 5 billion per year. This briefing will be of particular interest to elected members and officers in all authorities concerned with finance and strategic planning. Briefing in Full This briefing is a summary of the key relevant themes in the Institute of Fiscal Studies 2015 Green Budget which discusses some of the issues confronting the Chancellor ahead of his 2015 Budget Statement on Wednesday 18 March. The 2015 Green Budget comprises ten chapters spread across 293 pages. Coverage in this briefing is necessarily selective, and focuses on the prognosis for the UK economy, the public finances, and earnings growth. Not included are chapters on the global economy and on the government s financial accounts. Public Finances under the coalition In 2010 the coalition government planned to cut structural borrowing in a package which amounted to 7% of national income with the overall aim to eliminate the structural deficit (i.e. not related to the ups and downs of the economic cycle) by This fiscal tightening comprises 20% of tax rises and 80% of spending cuts to social security and public services. Over the next two years, the outlook for economic growth and tax revenues had deteriorated in large part due to fall in domestic economic output and tax revenues. This led to the coalition not to increase fiscal tightening planned for this parliament.

than was forecast in 2010 Autumn Statement.")

3 Rather it decided to extend the period of consolidation into the next (to ). This means that over the five years of this parliament (i.e. until ) borrowing is estimated to be around 100 billion higher (running at 5.7% of national income in rather than 1.9%) than was forecast in 2010 Autumn Statement. Since the 2012 Autumn Statement the outlook for public finances has little changed; structural borrowing is running at 8.4% of national income. Nonetheless, the coalition government have scheduled further spending cuts for the second half of the next parliament. Increasing the overall size of the post-crisis fiscal consolidation to 10.7% of national income to not only eliminate the deficit but to deliver an overall surplus of 1% (of national income) by This will involve 2% from net tax increases and 98% from spending cuts. This diagram, below, taken from the report shows the pace of austerity over time: Earnings since the recession Since the 2008 recession the UK labour market has been characterised by robust employment and weak earnings growth underpinned by weak productivity. Employment among 16-to-64 year olds is back to its 2008Q1 rate (of 73%) which is close to the highest rate recorded since Employment of men and women has equally held up during this period, though slightly increasing for women, reflecting longer-term trends. Employment has also risen among older adults, highly-educated individuals and relatively skilled occupations. There has also been rises in the proportions of workers who are self-employed from 13% in 2007 to 15% in 2014 Q1-3, and in part-time employment from 25% to 27% over the same period.

4 Productivity is still no higher than before the recession and has not grown since the end of Pay seems to have fallen by even more than productivity. In a competitive labour market, employee remuneration should reflect their productivity. A lack of earnings growth might therefore reflect a lack of productivity growth. But the IFS says that the key puzzle is over why productivity has fallen so much, rather than over the relationship between productivity and pay. Average earnings remain well below their pre-crisis level. This has made this recession, and the recovery from it, very different from previous ones. But while fewer people have faced losing all of their income (through unemployment) falls in (and the continued stagnation of) real earnings has meant that the pain has probably been considerably more widespread. Substantial variations in the fall of real earnings has been larger for men, young adults and in the private sector; falling less at lower points in the earnings distribution. Falls in earnings would have been larger if the characteristics of an employee had not changed since the recession, with increasing education levels pushing average earnings up. The continued weakness of earnings is due to continued weakness for given types of employee, for example (see above). There is little sign of this reversing or slowing down. The UK economic outlook The UK s economy has expanded with GDP growth of 2.6% placing it at the top of the G7 league table; though it lost momentum towards the end of last year. Lower fuel prices boosting consumer spending power is expected to propel growth to 3% in 2015 and 2.8% in Business investment is expected to make a disproportionate contribution with firms displaying confidence to spend their accumulated cash reserves. This is likely to be confined to the domestic market. Export trade is expected to only make a modest contribution over the next five years. The output gap (i.e. difference between actual GDP or actual output and potential GDP) narrowed slightly in 2014 ending the year at 4% of potential output. The prospects for output growth are favourable, with the labour supply boosted by: inward migration; a staged increase in the state pension age; and robust growth in business investment. Providing the conditions for relatively strong growth and low inflation over the medium term, with GDP growth expected to average 2.6% a year from 2015 to These forecasts from the IFS are stronger than those offered by the Office of Budget Responsibility (OBR) and other commentators.

5 However the risks around the IFS forecasts are skewed to the downside, with the forthcoming general election the most immediate source of uncertainty given the wide range of possible outcomes. A decisive result could mean changes to fiscal policy, while an inconclusive result and a minority government could undermine business confidence. However it is international events which have the greatest potential to impact on the UK outlook. Stronger recoveries in the US and the euro zone would boost UK export growth. The biggest threat would be a downturn in those international economies which could push the UK back into recession in late Public finances: a dicey decade ahead? Government debt is forecast to fall from 81.1% of national income in to reach a 1% surplus (of national income) in Maintaining a budget surplus over the longer term would have the advantage of reducing public sector net debt (expenditure less the total receipts) as a share of national income relatively quickly. Nonetheless debt is likely to remain high by international standards for some time. The IFS warns that maintaining low levels of borrowing may prove difficult, given an ageing population putting pressure on spending and given uncertainties around falling tax revenues. Future governments may find it difficult to index fuel duties as currently intended (freezing them for five years would cost 4.1 billion). There may also be pressure for more generous indexation of certain tax thresholds for instance the number of families set to lose child benefit will double in the next ten years. The public finances have also become increasingly reliant on and sensitive to the incomes and behaviour of the highest-income individuals. In , the highest income 1% of taxpayers (or just 0.57% of the adult population) paid over a quarter of all income tax revenues. And it is particularly difficult for the government to control debt interest spending and spending on social security benefits. According to independent forecasters the fiscal tightening needed to bring about a balanced budget range from 1.2% to 5.5% of national income (or 23 billion to 108 billion in real terms). These widely differing forecasts reflect the uncertainties facing public finances, including the growth in tax revenues. The government is currently planning to implement a tightening of 4.9% of national income ( 92 billion) cutting public spending to its lowest level, as a share of national income (to 35.2%) since at least Each of the three main political parties have set out slightly different objectives for borrowing, but all have said that they want to see debt falling as a share of national income by at least the end of the next Parliament. Options for further departmental spending cuts

6 The Coalition s current plans imply departmental spending cuts in real terms of 9.5% between and ; however with the protection afforded to health, overseas aid and current school funding (not capital) other departments have faced cuts averaging 20.6% over this period. The department facing the largest budget cuts is the Department for Communities and Local Government. Its communities budget is forecast to be cut by 52.5% in real terms, while its local government budget is forecast to be cut by 45.5%. The IFS say that this overstates the cut to local authority spending power over this period, since local authorities have other sources of revenue including council tax, retained business rates and user charges which have typically fallen less over this period than central government grants. The OBR forecast that local authority spending would fall in real terms by between 15% and 20% from to Actual spending over this period has differed from these plans. Resource spending has been cut more than planned in cash terms, but inflation turned out lower than forecast, so spending has been cut less than originally expected in real terms (7.8% compared with 8.3%). Real capital spending cuts have also turned out much lower than originally planned (13.6% rather than 25.9%) again, due to lower-than-forecast inflation, but also because of decisions since 2010 to top up these spending plans. The coalition government has not planned departmental expenditure after However the 2014 Autumn Statement implies real cuts of 14.1% to departmental spending between, and , returning departmental spending in real terms to around its level. The OBR forecast that these cuts would entail a cut in general government employment of 900,000 in the next parliament, on top of a cut of 500,000 since reducing the size of the government workforce, and its share of total employment, to its lowest level since at least However cuts post may not be as deep as the 2014 Autumn Statement implies. This is because all three main political parties have announced fiscal rules that would allow them to increase spending relative to those plans. They could also decide to implement a different combination of further tax increases and benefit cuts in order to lighten the load of deficit reduction on public spending. Given their fiscal rules and stated policy intentions, the Conservatives plans could imply cuts to departmental spending as little as 6.7% between and , the Liberal Democrats as little as 2.1% and Labour as little as 1.4%; compared to the 14.1% implied in the 2014 Autumn Statement. On this basis, the IFS calculate that if parties also decide to protect NHS, overseas aid and non-investment spending on schools, then this would require unprotected departmental spending to be cut by a further 13.1% by the Conservatives, 3.3% for Labour and 4.5% for Liberal Democrats (rather than the 27.0% under the Autumn Statement plans). This is illustrated in Table 7.9, taken from the report, below.

7 [Note: The IFS Green Budget was published just before the Conservatives announced that they would protect in cash terms the schools resource budget, and Labour committed to protecting the whole education budget (from early years to 18 years) in real terms, as is Liberal Democrats policy] In terms of employment levels in government the projected cuts for all three parties could also be lower at 550,000 for the Conservatives and around 300,000 for Labour and the Liberal Democrats; compared to 900,000 (see above). A 2015 Spending Review will allocate departmental budgets beyond April The IFS note the apparent political consensus among the three main parties that spending on health and overseas aid will remain protected from cuts. Leaving considerable uncertainty for other departments; though what seems certain is that some will face large cuts on top of those already delivered regardless of the outcome of the general election. Challenges for health spending The Department for Health s budget is currently planned to increase in real terms by an average of 1.2% per year between and compared with a real cut of 3.3% per year to other departmental spending over the same period. However, this is just enough to keep pace with the demands arising from a growing and ageing population. In addition demand will also increase over time as a result of the rising prevalence of some chronic conditions, improvements in access to care,

8 and improvements in technology, combined with government policy increasing the range of healthcare treatments available. NHS England and the Nuffield Trust estimates that the combined impact of demographic and these other pressures could increase demand by around 3% per year. The IFS note that up to now the health service has been assisted in coping with these additional pressures by government policy restraining public sector pay; with low private sector earnings growth helping to contain any adverse effects of this pay restraint on the recruitment, retention and motivation of NHS staff. However, as private sector wages recover, continuing pay restraint without adverse effects is likely to be harder to achieve. NHS England estimates that both those demand pressures and rising costs could create real financial pressures of around 3.5% per year and that it needs real budget increases or improvements in productivity amounting to around 30 billion ( prices) annually by to meet these pressures without a decline in service quality. The 2014 Autumn Statement forecasts, for example, imply departmental spending cuts averaging 3.7% per year between and The IFS calculate that if the NHS achieves the productivity improvements of 2.4% per year it is aiming for (reducing the financial pressures from around 30 billion to 8 billion), the DH budget would still need to increase by 0.8% a year in real terms to meet demand and cost pressures. This would imply the cuts to other departments need to average 6.1% per year rather than 3.7% per year implied by the 2014 Autumn Statement forecasts. Options for reducing spending on social security Total social security spending is forecast to be 220 billion in , around 30% of total government expenditure. According to the IFS this makes it likely that any government taking office after the general election will consider making further cuts to social security. 55% of this expenditure is expected to be spent on pensioners. A growing proportion as a result of: increased numbers of pensioners; greater state pension entitlements; and the fact that pensioners have so far been largely protected from cuts to social security. Indeed spending on pensions is expected to be 6.2% higher in real terms in than it was in , while non-pensioner spending is expected to be 6.5% lower. In other words, over this parliament rising pensioner spending has cancelled out the reduction in expenditure on those of working age. So far (i.e. until ) 17 billion of the total deficit reduction has comprised of cuts to social security benefits and tax credits. But despite these reductions total spending (on social security) is expected to be roughly the same in as it was in in real terms.

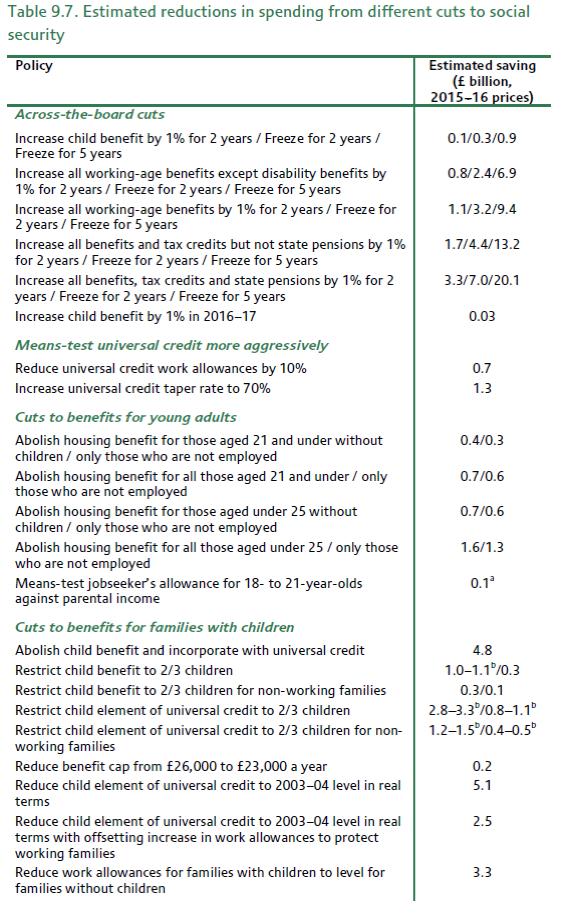

9 The Conservatives have said that they would seek to make further cuts of 12 billion to annual social security spending were they to form the next government. If carried through, this will bring social security spending in relation to national income to its average level between and (10.6%). According to IFS calculations some 21 billion per year reductions in social security would be required to the deliver the coalition s plans for public borrowing without raising taxes. To give an idea of scale of this: freezing all benefits and tax credits other than state pensions for five years would cut spending by 13 billion while continuing the Conservatives proposed freeze of most working-age benefits for five years would only reduce spending by 6.9 billion. IFS provide a range of illustrative options: making all tenants pay at least 10% of their rent ( 2.5 billion); abolishing child benefit and increasing universal credit to compensate low-income families ( 4.8 billion); reducing the generosity of means-tested support for children to its level ( 5.1 billion); and restricting benefits for families with children to the first two children (which would save around 4 billion a year in the long run). They note that many of the policies suggested by the Conservative and Labour parties, such as withdrawing winter fuel payments from higher- and additional-rate taxpayers, cutting housing benefit for young people, reducing the benefit cap, and increasing child benefit by 1% for a further year would reduce spending by relatively little. Table 9.7, below, taken from the report summarises the estimated savings from the options we consider.

10

11 Options for increasing tax The IFS point out that the last five general elections have all been followed by net tax rises of more than 5 billion per year in today s terms. Although just 2% of the remaining fiscal consolidation is currently planned to come from tax rises, and none of the main political parties is proposing significant tax rises, the IFS believe that it would not be surprising to see an incoming government increase taxes in order to limit the scale of public spending cuts required to meet its fiscal targets. The IFS illustrate that of the big three taxes: a 1 percentage point rise in all rates of income tax would raise 5.5 billion;

12 a 1 percentage point rise in all employee and self-employed National Insurance contribution (NIC) rates would raise 4.9 billion; and a 1 percentage point rise in the main rate of VAT would raise 5.2 billion. All according to IFS - would weaken work incentives and hit the rich harder than the poor. The main differences between them are that the VAT rise would be less progressive than the others (as it would affect poor, non-income-tax-paying households) and that the retired and savers would not be affected by a rise in NICs (which only tax the earnings of those below state pension age). Increasing rates of corporation tax, council tax, business rates or fuel duties could also raise significant sums, though the recent trend has been to reduce the rates of these taxes. Politicians from all main parties have indicated that they think the burden of fiscal consolidation should be focused on the better-off though tax payments are already highly concentrated: for example, a quarter of income tax comes from just 0.5% of the adult population and around half comes from 3% of adults. Aside from increasing income tax or NICs rates for high-income individuals, options include increasing inheritance tax or capital gains tax. In both cases reducing thresholds might have greater revenue-raising potential than increasing rates. The IFS takes the view that introducing a separate mansion tax would be unnecessarily complicated when council tax could be brought up to date and refocused on higher-value properties. While removing various tax reliefs would leave the tax system simpler and more efficient than increasing tax rates. They see that increasing stamp duty land tax is particularly damaging and recent governments tendency to turn to it for more revenue should be resisted. And while there are sensible ways to raise more revenue from the taxation of pension saving, the widespread proposal to restrict income tax relief on pension contributions to the basic rate is misguided. Comment The Chancellor s Budget Statement on 18 March is a key milestone on the road to May s General Election. Coming just before the ballot box it will be characterised - as previous pre-election Budgets - by the embellishment of what has come before with one eye on the electorate. Contentious issues may be ignored or kicked into the long grass. In any case they can be addressed in the emergency budget after the election.

13 The election is very likely to be followed regardless of the result - by an emergency Budget in mid-to-late June. This will involve an immediate re-prioritisation of departmental budgets for followed over the summer months by a formal Spending Review setting departmental budgets certainly for and and quite possibly for the rest of the parliament. The outcome of that review can be expected to be announced in late October. External Links IFS Green Budget 2015 Report Related LGIU Briefings Autumn Statement 2014: Analysis Local Government Finance Settlement 2015/16: Analysis For more information about this, or any other LGiU member briefing, please contact Janet Sillett, Briefings Manager, on janet.sillett@lgiu.org.uk

IFS Green Budget Press Release

IFS Green Budget Press Release Still not half way there yet on planned spending cuts Policy on business rates, pensions taxation and childcare needs clearer sense of direction The IFS Green Budget, funded

IFS Green Budget Press Release Still not half way there yet on planned spending cuts Policy on business rates, pensions taxation and childcare needs clearer sense of direction The IFS Green Budget, funded

1 Executive summary. Overview

1 Executive summary Overview 1.1 In headline terms, the UK economy has outperformed our March forecast, with GDP expected to grow by 3.0 per cent this year and unemployment already down to 6.0 per cent.

1 Executive summary Overview 1.1 In headline terms, the UK economy has outperformed our March forecast, with GDP expected to grow by 3.0 per cent this year and unemployment already down to 6.0 per cent.

Spring Statement 2018: more difficult choices ahead

Carl Emmerson Wednesday 14 March 2018 2007 08 2008 09 2009 10 2010 11 2011 12 2012 13 2013 14 2014 15 2015 16 2016 17 2017 18 2018 19 2019 20 2020 21 2021 22 2022 23 Per cent of national income Forecast

Carl Emmerson Wednesday 14 March 2018 2007 08 2008 09 2009 10 2010 11 2011 12 2012 13 2013 14 2014 15 2015 16 2016 17 2017 18 2018 19 2019 20 2020 21 2021 22 2022 23 Per cent of national income Forecast

Government and Public Sector

Government and Public Sector Budget 2016 Digest Government and Public Sector Budget 2016 Digest 1 Economic story The background for the economic forecast is a slowing world economy. 2 The Chancellor talked

Government and Public Sector Budget 2016 Digest Government and Public Sector Budget 2016 Digest 1 Economic story The background for the economic forecast is a slowing world economy. 2 The Chancellor talked

Living standards during the recession

Living standards during the recession IFS Briefing Note 117 James Browne 1. Introduction Living standards during the recession James Browne Institute for Fiscal Studies 1 We are used to our incomes rising

Living standards during the recession IFS Briefing Note 117 James Browne 1. Introduction Living standards during the recession James Browne Institute for Fiscal Studies 1 We are used to our incomes rising

1 Executive summary. Overview

1 Executive summary Overview 1.1 In the first combined Spending Review and Autumn Statement since 2007, the Government has taken advantage of an improvement in the outlook for tax receipts concentrated

1 Executive summary Overview 1.1 In the first combined Spending Review and Autumn Statement since 2007, the Government has taken advantage of an improvement in the outlook for tax receipts concentrated

1 March 2015 Economic and fiscal outlook Executive summary

1 March 2015 Economic and fiscal outlook Executive summary Overview 1.1 In the relatively short period since our last forecast in December, there have been a number of developments affecting prospects

1 March 2015 Economic and fiscal outlook Executive summary Overview 1.1 In the relatively short period since our last forecast in December, there have been a number of developments affecting prospects

November 2018 Budget. Overview. Economic Overview. 30 October 2018

30 October 2018 November 2018 Budget Overview Chancellor Philip Hammond delivered his final Budget before the UK is due to leave the EU and ahead of the 2019 Comprehensive Spending Review with a positive

30 October 2018 November 2018 Budget Overview Chancellor Philip Hammond delivered his final Budget before the UK is due to leave the EU and ahead of the 2019 Comprehensive Spending Review with a positive

Ending austerity? July 2017

Ending austerity? July 2017 Ending austerity: can the government change course? Britain is seven years into a prolonged period of fiscal consolidation, in which constraints on public spending have been

Ending austerity? July 2017 Ending austerity: can the government change course? Britain is seven years into a prolonged period of fiscal consolidation, in which constraints on public spending have been

The Summer budget: Taxes up, borrowing up, departmental spending up

The Summer budget: Taxes up, borrowing up, departmental spending up Rowena Crawford Changes in borrowing forecasts since March Public sector net borrowing, billion 2014 15 2015 16 2016 17 2017 18 2018

The Summer budget: Taxes up, borrowing up, departmental spending up Rowena Crawford Changes in borrowing forecasts since March Public sector net borrowing, billion 2014 15 2015 16 2016 17 2017 18 2018

Autumn Budget 2018: IFS analysis

Autumn Budget 2018: IFS analysis Paul Johnson s Opening Remarks So now we know. When push comes to shove it s not tax rises and it s not the NHS that Mr Hammond is willing to gamble on, it s the public

Autumn Budget 2018: IFS analysis Paul Johnson s Opening Remarks So now we know. When push comes to shove it s not tax rises and it s not the NHS that Mr Hammond is willing to gamble on, it s the public

FISCAL COUNCIL OPINION ON THE SUMMER FORECAST 2018 OF THE MINISTRY OF FINANCE

FISCAL COUNCIL OPINION ON THE SUMMER FORECAST 2018 OF THE MINISTRY OF FINANCE September 2018 Contents Opinion... 3 Explanatory Report... 4 Opinion on the summer forecast 2018 of the Ministry of Finance...

FISCAL COUNCIL OPINION ON THE SUMMER FORECAST 2018 OF THE MINISTRY OF FINANCE September 2018 Contents Opinion... 3 Explanatory Report... 4 Opinion on the summer forecast 2018 of the Ministry of Finance...

Forecast evaluation report October 2012

Forecast evaluation report 2012 16 October 2012 The aim of the FER We publish 2 EFO forecasts a year We emphasise and quantify uncertainty But still publish detail of central forecast and evaluate ex post

Forecast evaluation report 2012 16 October 2012 The aim of the FER We publish 2 EFO forecasts a year We emphasise and quantify uncertainty But still publish detail of central forecast and evaluate ex post

UK public finances and the financial crisis

UK public finances and the financial crisis Carl Emmerson and Gemma Tetlow Presentation given at workshop on European public finances through the financial crisis, ZEW Centre for European Economic Research,

UK public finances and the financial crisis Carl Emmerson and Gemma Tetlow Presentation given at workshop on European public finances through the financial crisis, ZEW Centre for European Economic Research,

MINUTES OF THE MONETARY POLICY COMMITTEE MEETING 4 AND 5 NOVEMBER 2009

Publication date: 18 November 2009 MINUTES OF THE MONETARY POLICY COMMITTEE MEETING 4 AND 5 NOVEMBER 2009 These are the minutes of the Monetary Policy Committee meeting held on 4 and 5 November 2009. They

Publication date: 18 November 2009 MINUTES OF THE MONETARY POLICY COMMITTEE MEETING 4 AND 5 NOVEMBER 2009 These are the minutes of the Monetary Policy Committee meeting held on 4 and 5 November 2009. They

Irish Economic Update AIB Treasury Economic Research Unit

Irish Economic Update AIB Treasury Economic Research Unit 9th October 2018 Budget 2019 Public Finances in Balance The Irish economy has performed strongly in recent years, boosting tax revenues. Corporation

Irish Economic Update AIB Treasury Economic Research Unit 9th October 2018 Budget 2019 Public Finances in Balance The Irish economy has performed strongly in recent years, boosting tax revenues. Corporation

In January 2017 UK Public sector net debt is 1,682.8 billion equivalent to 85.3% of GDP

UK National Debt Budget deficit annual borrowing... 2 UK net borrowing... 3 UK net borrowing as % of GDP... 3 Deficit down but debt up?... 4 Debt as % of GDP... 4 Recent history of UK National Debt...

UK National Debt Budget deficit annual borrowing... 2 UK net borrowing... 3 UK net borrowing as % of GDP... 3 Deficit down but debt up?... 4 Debt as % of GDP... 4 Recent history of UK National Debt...

Finland falling further behind euro area growth

BANK OF FINLAND FORECAST Finland falling further behind euro area growth 30 JUN 2015 2:00 PM BANK OF FINLAND BULLETIN 3/2015 ECONOMIC OUTLOOK Economic growth in Finland has been slow for a prolonged period,

BANK OF FINLAND FORECAST Finland falling further behind euro area growth 30 JUN 2015 2:00 PM BANK OF FINLAND BULLETIN 3/2015 ECONOMIC OUTLOOK Economic growth in Finland has been slow for a prolonged period,

Ageing and wrinkles in public finances

For Investment Professionals Follow us @LGIM #Fundamentals FUNDAMENTALS Ageing and wrinkles in public finances Pay-as-you-go pension and healthcare schemes are under increasing pressure from ageing populations.

For Investment Professionals Follow us @LGIM #Fundamentals FUNDAMENTALS Ageing and wrinkles in public finances Pay-as-you-go pension and healthcare schemes are under increasing pressure from ageing populations.

THE CHANCELLOR S CHOICES

BUDGET 212 BRIEFING AN ECONOMIC STIMULUS FOR THE UK THE CHANCELLOR S CHOICES Kayte Lawton March 212 IPPR 212 Institute for Public Policy Research ABOUT THE AUTHOR Kayte Lawton is a senior research fellow

BUDGET 212 BRIEFING AN ECONOMIC STIMULUS FOR THE UK THE CHANCELLOR S CHOICES Kayte Lawton March 212 IPPR 212 Institute for Public Policy Research ABOUT THE AUTHOR Kayte Lawton is a senior research fellow

Government tax, spending and debt a decade on from the financial crisis

a decade on from the financial crisis Carl Emmerson Presentation to A level students, London, 26 November 2018 http://www.ifs.org.uk/ http://twitter.com/theifs What happened? Financial crisis hits in 2008

a decade on from the financial crisis Carl Emmerson Presentation to A level students, London, 26 November 2018 http://www.ifs.org.uk/ http://twitter.com/theifs What happened? Financial crisis hits in 2008

State pensions. Extract from the July 2017 Fiscal risks report. Drivers of pensions spending: population ageing

Extract from the July 2017 Fiscal risks report 6.15 The state pension is the biggest component of welfare spending. In 2016-17, 12.9 million pensioners received an average 7,110 of state pension payments

Extract from the July 2017 Fiscal risks report 6.15 The state pension is the biggest component of welfare spending. In 2016-17, 12.9 million pensioners received an average 7,110 of state pension payments

Spending on public services

Spending on public services Rowena Crawford IFS analysis for the general election 2017 Big picture Conservatives have not announced large spending policies Labour have announced significant spending policies

Spending on public services Rowena Crawford IFS analysis for the general election 2017 Big picture Conservatives have not announced large spending policies Labour have announced significant spending policies

Spring Budget IFS Director Paul Johnson s opening remarks

Spring Budget 2017 IFS Director Paul Johnson s opening remarks Spring Budgets seem to be going out with something of a whimper. Yesterday s was one of the smallest I can remember in pretty much every dimension

Spring Budget 2017 IFS Director Paul Johnson s opening remarks Spring Budgets seem to be going out with something of a whimper. Yesterday s was one of the smallest I can remember in pretty much every dimension

Housing market. Forecasts

Housing market Forecasts - 2018 Summer COUNTRYWIDE HOUSING MARKET FORECASTS 2018 COUNTRYWIDE HOUSING MARKET FORECASTS 2018 Forecasts Executive summary 2014 2015 2017 2018 It will be a bumpy time ahead,

Housing market Forecasts - 2018 Summer COUNTRYWIDE HOUSING MARKET FORECASTS 2018 COUNTRYWIDE HOUSING MARKET FORECASTS 2018 Forecasts Executive summary 2014 2015 2017 2018 It will be a bumpy time ahead,

Economic Perspectives

Economic Perspectives What might slower economic growth in Scotland mean for Scotland s income tax revenues? David Eiser Fraser of Allander Institute Abstract Income tax revenues now account for over 40%

Economic Perspectives What might slower economic growth in Scotland mean for Scotland s income tax revenues? David Eiser Fraser of Allander Institute Abstract Income tax revenues now account for over 40%

Labour s proposed income tax rises for high-income individuals

Labour s proposed income tax rises for high-income individuals IFS Briefing Note BN209 Stuart Adam Andrew Hood Robert Joyce David Phillips Labour s proposed income tax rises for high-income individuals

Labour s proposed income tax rises for high-income individuals IFS Briefing Note BN209 Stuart Adam Andrew Hood Robert Joyce David Phillips Labour s proposed income tax rises for high-income individuals

Northern Ireland Quarterly Sectoral Forecasts

2017 Quarter 1 Northern Ireland Quarterly Sectoral Forecasts Forecast summary The Northern Ireland economy enjoyed a solid performance in 2016 with overall growth of 1.5%, the strongest rate of growth

2017 Quarter 1 Northern Ireland Quarterly Sectoral Forecasts Forecast summary The Northern Ireland economy enjoyed a solid performance in 2016 with overall growth of 1.5%, the strongest rate of growth

a labour market that has continued to exhibit strong growth in employment, but weak growth in earnings and productivity; and

1 Executive summary 1.1 Twice a year at the OBR, we provide a detailed central forecast for the economy and the public finances. These forecasts provide a transparent benchmark against which to judge the

1 Executive summary 1.1 Twice a year at the OBR, we provide a detailed central forecast for the economy and the public finances. These forecasts provide a transparent benchmark against which to judge the

Eurozone. EY Eurozone Forecast December 2014

Eurozone EY Eurozone Forecast December 2014 Outlook for Road to recovery remains strewn with obstacles Published in collaboration with Highlights GDP growth With the Finnish economy still struggling to

Eurozone EY Eurozone Forecast December 2014 Outlook for Road to recovery remains strewn with obstacles Published in collaboration with Highlights GDP growth With the Finnish economy still struggling to

Conservatives plan to cut public spending to cut National Insurance

Conservatives plan to cut public spending to cut National Insurance The Conservative Party plans to cut central government spending on public services outside the NHS, defence and overseas aid by 6 billion

Conservatives plan to cut public spending to cut National Insurance The Conservative Party plans to cut central government spending on public services outside the NHS, defence and overseas aid by 6 billion

Edexcel (B) Economics A-level

Economics A-level") Edexcel (B) Economics A-level Theme 2: The Wider Economic Environment 2.5 The Economic Cycle 2.5.2 Circular flow of income, expenditure and output Notes The circular flow of income Firms and households

Edexcel (B) Economics A-level Theme 2: The Wider Economic Environment 2.5 The Economic Cycle 2.5.2 Circular flow of income, expenditure and output Notes The circular flow of income Firms and households

RÉMUNÉRATION DES SALARIÉS. ÉTAT ET ÉVOLUTION COMPARÉS 2010 MAIN FINDINGS

RÉMUNÉRATION DES SALARIÉS. ÉTAT ET ÉVOLUTION COMPARÉS 2010 MAIN FINDINGS PART I SALARIES AND TOTAL COMPENSATION All other Quebec employees In 2010, the average salaries of Quebec government employees 1

RÉMUNÉRATION DES SALARIÉS. ÉTAT ET ÉVOLUTION COMPARÉS 2010 MAIN FINDINGS PART I SALARIES AND TOTAL COMPENSATION All other Quebec employees In 2010, the average salaries of Quebec government employees 1

Autumn 2017 Budget: Options for easing the squeeze

Autumn 2017 Budget: Options for easing the squeeze Carl Emmerson and Thomas Pope Presentation at the Institute of Chartered Accountants in England and Wales London, 30 th October 2017 The March Budget

Autumn 2017 Budget: Options for easing the squeeze Carl Emmerson and Thomas Pope Presentation at the Institute of Chartered Accountants in England and Wales London, 30 th October 2017 The March Budget

IFS Post-Budget Briefing 2015

Paul Johnson s opening remarks March 19 2015 There was only one eye-catching change to the fiscal numbers in yesterday s Budget, one that occurs five years out in 2019-20. Instead of allowing public spending

Paul Johnson s opening remarks March 19 2015 There was only one eye-catching change to the fiscal numbers in yesterday s Budget, one that occurs five years out in 2019-20. Instead of allowing public spending

The Outlook for the UK Consumer Sector A Note. Gavyn Davies. 9 May Overview

The Outlook for the UK Consumer Sector A Note Gavyn Davies 9 May 2018 Overview Consumers expenditure accounts for 66 per cent of GDP in the UK. There is therefore a huge variety of investment opportunities

The Outlook for the UK Consumer Sector A Note Gavyn Davies 9 May 2018 Overview Consumers expenditure accounts for 66 per cent of GDP in the UK. There is therefore a huge variety of investment opportunities

The Autumn Statement. Implications for Scotland. November: 2016

The Autumn Statement Implications for Scotland November: 2016 Autumn Statement 2016: why the excitement? UK fiscal policy dominated by George Osborne s 2019/20 fiscal surplus target Brexit vote and downward

The Autumn Statement Implications for Scotland November: 2016 Autumn Statement 2016: why the excitement? UK fiscal policy dominated by George Osborne s 2019/20 fiscal surplus target Brexit vote and downward

TUC Statement on the HM Treasury Spring Statement : Time for action

TUC Statement on the HM Treasury Spring Statement : Time for action Time for action At the Autumn Budget the Chancellor looked to a future that will be full of change; full of new challenges and above

TUC Statement on the HM Treasury Spring Statement : Time for action Time for action At the Autumn Budget the Chancellor looked to a future that will be full of change; full of new challenges and above

EMERGENCY BUDGET 2010 AND LOW EARNERS

EMERGENCY BUDGET 2010 AND LOW EARNERS 1 Overview In our pre emergency Budget report on options for deficit reduction 1 we argued that any fiscal consolidation plan should present a package of measures

EMERGENCY BUDGET 2010 AND LOW EARNERS 1 Overview In our pre emergency Budget report on options for deficit reduction 1 we argued that any fiscal consolidation plan should present a package of measures

Slovenia. Eurozone rebalancing. EY Eurozone Forecast June Portugal Slovakia Slovenia Spain. Latvia Lithuania Luxembourg Malta Netherlands

EY Forecast June 215 rebalancing recovery Outlook for Activity to remain solid this year, after growing 2.4% in 214 Published in collaboration with Highlights n GDP grew by 2.4% in 214 and 3% in Q1 215,

EY Forecast June 215 rebalancing recovery Outlook for Activity to remain solid this year, after growing 2.4% in 214 Published in collaboration with Highlights n GDP grew by 2.4% in 214 and 3% in Q1 215,

Monetary Policy Summary and minutes of the Monetary Policy Committee meeting ending on 15 March 2017

Monetary Policy Summary and minutes of the Monetary Policy Committee meeting ending on 15 March 2017 Publication date: 16 March 2017 These are the minutes of the Monetary Policy Committee meeting ending

Monetary Policy Summary and minutes of the Monetary Policy Committee meeting ending on 15 March 2017 Publication date: 16 March 2017 These are the minutes of the Monetary Policy Committee meeting ending

The Election & the Economy

The Election & the Economy John Van Reenen (Professor of Economics, LSE & Director Centre for Economic Performance) CASE Election Series, April 29 th 2015 Introduction Economy major election issue CEP

The Election & the Economy John Van Reenen (Professor of Economics, LSE & Director Centre for Economic Performance) CASE Election Series, April 29 th 2015 Introduction Economy major election issue CEP

Public sector pay: still time for restraint?

Public sector pay: still time for restraint? IFS Briefing Note BN216 Jonathan Cribb Public sector pay: still time for restraint? Jonathan Cribb Copy-edited by Judith Payne Published by The Institute for

Public sector pay: still time for restraint? IFS Briefing Note BN216 Jonathan Cribb Public sector pay: still time for restraint? Jonathan Cribb Copy-edited by Judith Payne Published by The Institute for

NATIONAL MINIMUM WAGE. Final government evidence to the Low Pay Commission 2012 JANUARY 2013

NATIONAL MINIMUM WAGE Final government evidence to the Low Pay Commission 2012 JANUARY 2013 MINISTERIAL FOREWORD The Coalition Government is fully committed to the National Minimum Wage. We believe that

NATIONAL MINIMUM WAGE Final government evidence to the Low Pay Commission 2012 JANUARY 2013 MINISTERIAL FOREWORD The Coalition Government is fully committed to the National Minimum Wage. We believe that

Incomes and inequality: the last decade and the next parliament

Incomes and inequality: the last decade and the next parliament IFS Briefing Note BN202 Andrew Hood and Tom Waters Incomes and inequality: the last decade and the next parliament Andrew Hood and Tom Waters

Incomes and inequality: the last decade and the next parliament IFS Briefing Note BN202 Andrew Hood and Tom Waters Incomes and inequality: the last decade and the next parliament Andrew Hood and Tom Waters

The end of deficit reduction? Thomas Pope

Thomas Pope Some things didn t change yesterday The medium-term growth forecast is still sluggish Real growth of only 1.6% forecast in 2023 Pessimistic view of productivity remains Small improvement from

Thomas Pope Some things didn t change yesterday The medium-term growth forecast is still sluggish Real growth of only 1.6% forecast in 2023 Pessimistic view of productivity remains Small improvement from

Jan F Qvigstad: Outlook for the Norwegian economy

Jan F Qvigstad: Outlook for the Norwegian economy Address by Mr Jan F Qvigstad, Deputy Governor of Norges Bank (Central Bank of Norway), at Sparebank 1 Fredrikstad, 4 November 2009. The text below may

Jan F Qvigstad: Outlook for the Norwegian economy Address by Mr Jan F Qvigstad, Deputy Governor of Norges Bank (Central Bank of Norway), at Sparebank 1 Fredrikstad, 4 November 2009. The text below may

Summary. Chapter 1 Checking out the supply side of the economy. Chapter 2 The new fiscal framework: an assessment

Chapter 1 Checking out the supply side of the economy Last year, we argued that the UK was likely to find that its productive capacity had been severely impaired by the financial crisis. Accordingly, we

Chapter 1 Checking out the supply side of the economy Last year, we argued that the UK was likely to find that its productive capacity had been severely impaired by the financial crisis. Accordingly, we

APPENDIX: Country analyses

APPENDIX: Country analyses Appendix A Germany: Low economic momentum The economic situation in Germany continues to be lackluster in 2014. Strong growth in the first quarter was followed by a decline

APPENDIX: Country analyses Appendix A Germany: Low economic momentum The economic situation in Germany continues to be lackluster in 2014. Strong growth in the first quarter was followed by a decline

Budget OBR forecast for growth in %, up from +2.4% in the Autumn Statement, and the biggest revision between Budgets for 3 years.

Budget 2014 Preamble There was little in today s budget that impacted directly on the education and skills or workforce agendas beyond the now traditional raising of investment levels in apprenticeships.

Budget 2014 Preamble There was little in today s budget that impacted directly on the education and skills or workforce agendas beyond the now traditional raising of investment levels in apprenticeships.

AUTUMN STATEMENT 2013

AUTUMN STATEMENT 2013 Wells Associates 10 Lonsdale Gardens Tunbridge Wells TN1 1NU info@wellsassociates.com 01892 507 280 www.wellsassociates.com 01 // Autumn Statement 2013 EXECUTIVE SUMMARY Delivering

AUTUMN STATEMENT 2013 Wells Associates 10 Lonsdale Gardens Tunbridge Wells TN1 1NU info@wellsassociates.com 01892 507 280 www.wellsassociates.com 01 // Autumn Statement 2013 EXECUTIVE SUMMARY Delivering

4.4.1 The AD/AS model

4.4.1 The AD/AS model Changes in Aggregate Demand (AD) Aggregate demand is the total demand in the economy. It measures spending on goods and services by consumers, firms, the government and overseas consumers

4.4.1 The AD/AS model Changes in Aggregate Demand (AD) Aggregate demand is the total demand in the economy. It measures spending on goods and services by consumers, firms, the government and overseas consumers

6. Risks to the rules: public spending

6. Risks to the rules: public spending Rowena Crawford, Carl Emmerson, Thomas Pope and Gemma Tetlow (IFS) Summary The government s objective of having a budget surplus in 2019 20 is set to be achieved

6. Risks to the rules: public spending Rowena Crawford, Carl Emmerson, Thomas Pope and Gemma Tetlow (IFS) Summary The government s objective of having a budget surplus in 2019 20 is set to be achieved

GERMANY REVIEW OF PROGRESS ON POLICY MEASURES RELEVANT FOR THE

EUROPEAN COMMISSION DIRECTORATE GENERAL ECONOMIC AND FINANCIAL AFFAIRS Brussels, December 2016 GERMANY REVIEW OF PROGRESS ON POLICY MEASURES RELEVANT FOR THE CORRECTION OF MACROECONOMIC IMBALANCES Table

EUROPEAN COMMISSION DIRECTORATE GENERAL ECONOMIC AND FINANCIAL AFFAIRS Brussels, December 2016 GERMANY REVIEW OF PROGRESS ON POLICY MEASURES RELEVANT FOR THE CORRECTION OF MACROECONOMIC IMBALANCES Table

Spring Statement 2018: The lost decade

Thomas Pope Wednesday 14 th March 2018 2015-16 2016-17 2017-18 2018-19 2019-20 2020-21 2021-22 2022-23 2007 08 =100 Very small improvement in the growth forecast yesterday 120 118 116 114 112 110 108 106

Thomas Pope Wednesday 14 th March 2018 2015-16 2016-17 2017-18 2018-19 2019-20 2020-21 2021-22 2022-23 2007 08 =100 Very small improvement in the growth forecast yesterday 120 118 116 114 112 110 108 106

Introductory remarks. Paul Johnson 4/12/14. Some of yesterday s biggest announcements were not from the Chancellor

Introductory remarks Paul Johnson 4/12/14 Some of yesterday s biggest announcements were not from the Chancellor at all, they were from the independent Office for Budget Responsibility. Robert Chote and

Introductory remarks Paul Johnson 4/12/14 Some of yesterday s biggest announcements were not from the Chancellor at all, they were from the independent Office for Budget Responsibility. Robert Chote and

1 Executive summary. Overview

1 Executive summary Overview 1.1 The UK economy has slowed this year as households real incomes and spending have been squeezed by higher inflation. GDP growth has been a little weaker than we expected

1 Executive summary Overview 1.1 The UK economy has slowed this year as households real incomes and spending have been squeezed by higher inflation. GDP growth has been a little weaker than we expected

AQA Economics A-level

AQA Economics A-level Macroeconomics Topic 5: Fiscal and Supply Side Policies 5.1 Fiscal policy Notes Fiscal policy involves the manipulation of government spending, taxation and the budget balance. It

AQA Economics A-level Macroeconomics Topic 5: Fiscal and Supply Side Policies 5.1 Fiscal policy Notes Fiscal policy involves the manipulation of government spending, taxation and the budget balance. It

The end of austerity? Ben Zaranko

Ben Zaranko Public services spending: what did we learn? In March the Chancellor announced he would set a firm overall path for public spending beyond 2020 in the Budget Mr Hammond instead chose not to

Ben Zaranko Public services spending: what did we learn? In March the Chancellor announced he would set a firm overall path for public spending beyond 2020 in the Budget Mr Hammond instead chose not to

Small changes this Parliament; more big welfare cuts next?

Small changes this Parliament; more big welfare cuts next? Carl Emmerson IFS hosts two ESRC Research Centres 1996 97 1997 98 1998 99 1999 00 2000 01 2001 02 2002 03 2003 04 2004 05 2005 06 2006 07 2007

Small changes this Parliament; more big welfare cuts next? Carl Emmerson IFS hosts two ESRC Research Centres 1996 97 1997 98 1998 99 1999 00 2000 01 2001 02 2002 03 2003 04 2004 05 2005 06 2006 07 2007

PPI Briefing Note Number 97 Page 1 5.9% 5.8% 5.9% 5.7% Source: PPI Aggregate Model

Briefing Note Number 97 Page 1 Introduction Ahead of the June 2017 general election, the is issuing a series of Briefing Notes summarising some of the key issues surrounding pension policy that are relevant

Briefing Note Number 97 Page 1 Introduction Ahead of the June 2017 general election, the is issuing a series of Briefing Notes summarising some of the key issues surrounding pension policy that are relevant

Fiscal sustainability report 2018 and accounting for student loans Robert Chote Chairman, Office for Budget Responsibility

Fiscal sustainability report 2018 and accounting for student loans Robert Chote Chairman, Office for Budget Responsibility Good morning everyone. My name is Robert Chote, Chairman of the OBR, and I would

Fiscal sustainability report 2018 and accounting for student loans Robert Chote Chairman, Office for Budget Responsibility Good morning everyone. My name is Robert Chote, Chairman of the OBR, and I would

Economic Survey December 2006 English Summary

Economic Survey December English Summary. Short term outlook Reaching an annualized growth rate of.5 per cent in the first half of, GDP growth in Denmark has turned out considerably stronger than expected

Economic Survey December English Summary. Short term outlook Reaching an annualized growth rate of.5 per cent in the first half of, GDP growth in Denmark has turned out considerably stronger than expected

Briefing for Members. Budget: March 2016

Briefing for Members Budget: March 2016 1. Headlines Growth forecast cut for the next five years and 3.5bn in extra public spending cuts by 2020 Upgrading of the A66 and A69 routes in the North East A

Briefing for Members Budget: March 2016 1. Headlines Growth forecast cut for the next five years and 3.5bn in extra public spending cuts by 2020 Upgrading of the A66 and A69 routes in the North East A

Irish Economic Update AIB Treasury Economic Research Unit

Irish Economic Update AIB Treasury Economic Research Unit 10th October 2017 Budget 2018 Deficit Close To Being Eliminated The Irish economy has performed strongly in recent years, which has helped to boost

Irish Economic Update AIB Treasury Economic Research Unit 10th October 2017 Budget 2018 Deficit Close To Being Eliminated The Irish economy has performed strongly in recent years, which has helped to boost

1 Executive summary. Overview

1 Executive summary Overview 1.1 Relatively little time has passed since our November forecast and the outlook for the economy and public finances looks broadly the same. The economy has slightly more

1 Executive summary Overview 1.1 Relatively little time has passed since our November forecast and the outlook for the economy and public finances looks broadly the same. The economy has slightly more

Poverty Alliance Briefing 23

Poverty Alliance Briefing 23 Devolved Taxation in Scotland Introduction The Scottish Government has increasing powers to vary tax rates in Scotland. In addition to having full control over local property

Poverty Alliance Briefing 23 Devolved Taxation in Scotland Introduction The Scottish Government has increasing powers to vary tax rates in Scotland. In addition to having full control over local property

UK Economic Forecast Q3 2015

UK Economic Forecast Q3 2015 BUSINESS WITH CONFIDENCE 2 Introduction Welcome to the Q3 2015 ICAEW Economic Forecast, based on the views of the people running UK plc; ICAEW Chartered Accountants working

UK Economic Forecast Q3 2015 BUSINESS WITH CONFIDENCE 2 Introduction Welcome to the Q3 2015 ICAEW Economic Forecast, based on the views of the people running UK plc; ICAEW Chartered Accountants working

Taxes and benefits: the parties plans

Taxes and benefits: the parties plans James Browne and David Phillips What s coming up Go through each party in turn (Labour, Conservative, Lib Dem) Discuss individual measures Reforms to come in by 2014

Taxes and benefits: the parties plans James Browne and David Phillips What s coming up Go through each party in turn (Labour, Conservative, Lib Dem) Discuss individual measures Reforms to come in by 2014

Council Tax Proposals in the Scottish Election 2011

Council Tax Proposals in the Scottish Election 2011 David N.F. Bell Stirling Economics Discussion Paper 2011-10 May 2011 Online at http://www.management.stir.ac.uk/research/economics/workingpapers Council

Council Tax Proposals in the Scottish Election 2011 David N.F. Bell Stirling Economics Discussion Paper 2011-10 May 2011 Online at http://www.management.stir.ac.uk/research/economics/workingpapers Council

Lars Nyberg: Developments in the property market

Lars Nyberg: Developments in the property market Speech by Mr Lars Nyberg, Deputy Governor of the Sveriges Riksbank, at Fastighetsvärlden (Swedish newspaper), Stockholm, 30 May 2007. * * * I would like

Lars Nyberg: Developments in the property market Speech by Mr Lars Nyberg, Deputy Governor of the Sveriges Riksbank, at Fastighetsvärlden (Swedish newspaper), Stockholm, 30 May 2007. * * * I would like

OECD Financial sustainability of healthcare systems Healthcare Productivity in the UK

OECD Financial sustainability of healthcare systems Healthcare Productivity in the UK Anita Charlesworth Chief Economist, Nuffield Trust 26 March 2013 This presentation covers: The budget outlook for publicly

OECD Financial sustainability of healthcare systems Healthcare Productivity in the UK Anita Charlesworth Chief Economist, Nuffield Trust 26 March 2013 This presentation covers: The budget outlook for publicly

COMMISSION OF THE EUROPEAN COMMUNITIES. Recommendation for a COUNCIL OPINION

EN EN EN COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, 30 January 2008 SEC(2008) 107 final Recommendation for a COUNCIL OPINION in accordance with the third paragraph of Article 5 of Council Regulation

EN EN EN COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, 30 January 2008 SEC(2008) 107 final Recommendation for a COUNCIL OPINION in accordance with the third paragraph of Article 5 of Council Regulation

2015: FINALLY, A STRONG YEAR

2015: FINALLY, A STRONG YEAR A Cushman & Wakefield Research Publication U.S. GDP GROWTH IS ACCELERATING 4% 3.5% Percent Change Annual Rate 2% 0% -2% -4% -5.4% -0.5% 1.3% 3.9% 1.7% 3.9% 2.7% 2.5% -1.5%

2015: FINALLY, A STRONG YEAR A Cushman & Wakefield Research Publication U.S. GDP GROWTH IS ACCELERATING 4% 3.5% Percent Change Annual Rate 2% 0% -2% -4% -5.4% -0.5% 1.3% 3.9% 1.7% 3.9% 2.7% 2.5% -1.5%

Venezuela Country Brief

Venezuela Country Brief Venezuela is rich in natural resources, but poor economic policies over the past two decades have led to disappointed economic performance. A demand-led temporary boom in growth

Venezuela Country Brief Venezuela is rich in natural resources, but poor economic policies over the past two decades have led to disappointed economic performance. A demand-led temporary boom in growth

WJEC (Eduqas) Economics A-level Trade Development

Economics A-level Trade Development") WJEC (Eduqas) Economics A-level Trade Development Topic 1: Global Economics 1.3 Non-UK economies Notes Characteristics of developed, developing and emerging (BRICS) economies LEDCs Less economically developed

WJEC (Eduqas) Economics A-level Trade Development Topic 1: Global Economics 1.3 Non-UK economies Notes Characteristics of developed, developing and emerging (BRICS) economies LEDCs Less economically developed

Budget 2014: What does it mean for housing?

Budget 2014: What does it mean for housing? 0 Federation response 1 Key housing announcements Help to Buy: equity loan scheme will be extended to March 2020 to help a further 120,000 households to buy

Budget 2014: What does it mean for housing? 0 Federation response 1 Key housing announcements Help to Buy: equity loan scheme will be extended to March 2020 to help a further 120,000 households to buy

Women s Budget Group Pre-Budget Briefing, March 2012

Women s Budget Group Pre-Budget Briefing, March 2012 Plan A has failed. It is time for Plan F: a feminist economic strategy to stimulate social and economic recovery. Austerity measures are damaging women,

Women s Budget Group Pre-Budget Briefing, March 2012 Plan A has failed. It is time for Plan F: a feminist economic strategy to stimulate social and economic recovery. Austerity measures are damaging women,

Fiscal sustainability report Robert Chote Chairman

Fiscal sustainability report 2013 Robert Chote Chairman 17 July 2013 Preamble OBR set up in 2010 to provide independent and authoritative analysis of the UK public finances BRC responsible for the conclusions,

Fiscal sustainability report 2013 Robert Chote Chairman 17 July 2013 Preamble OBR set up in 2010 to provide independent and authoritative analysis of the UK public finances BRC responsible for the conclusions,

Economic Projections for

Economic Projections for 2015-2017 Article published in the Quarterly Review 2015:3, pp. 86-91 7. ECONOMIC PROJECTIONS FOR 2015-2017 Outlook for the Maltese economy 1 The Bank s latest macroeconomic projections

Economic Projections for 2015-2017 Article published in the Quarterly Review 2015:3, pp. 86-91 7. ECONOMIC PROJECTIONS FOR 2015-2017 Outlook for the Maltese economy 1 The Bank s latest macroeconomic projections

The state of the public finances

The state of the public finances Introduction Since 2010, successive UK governments have been striving to repair damage to the public finances left by the global financial crisis. Austerity measures have

The state of the public finances Introduction Since 2010, successive UK governments have been striving to repair damage to the public finances left by the global financial crisis. Austerity measures have

Eurozone. EY Eurozone Forecast March 2015

Eurozone EY Eurozone Forecast March 2015 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Lithuania Luxembourg Netherlands Portugal Slovakia Slovenia Spain Outlook for

Eurozone EY Eurozone Forecast March 2015 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Lithuania Luxembourg Netherlands Portugal Slovakia Slovenia Spain Outlook for

SAGA. GUIDE TO PENSION REFORM By Paul Lewis MAGAZINE AUGUST 2006 SAGA 1

SAGA MAGAZINE GUIDE TO PENSION REFORM By Paul Lewis AUGUST 2006 SAGA 1 In May 2006 the Government proposed the most radical reform of the state pension for a generation. Nothing like it has happened since

SAGA MAGAZINE GUIDE TO PENSION REFORM By Paul Lewis AUGUST 2006 SAGA 1 In May 2006 the Government proposed the most radical reform of the state pension for a generation. Nothing like it has happened since

Publication will no doubt be overshadowed by the ongoing Brexit debate. But it s important not to lose sight of the domestic policy agenda.

Tomorrow, new statistics on poverty and income inequality will be published. All indications are that levels of poverty and inequality are on the rise in the UK over the longer term, and Scotland is no

Tomorrow, new statistics on poverty and income inequality will be published. All indications are that levels of poverty and inequality are on the rise in the UK over the longer term, and Scotland is no

THE ANDREW MARR SHOW INTERVIEW: GEORGE OSBORNE, MP CHANCELLOR OF THE EXCHEQUER NOVEMBER 30 th 2014

PLEASE NOTE THE ANDREW MARR SHOW MUST BE CREDITED IF ANY PART OF THIS TRANSCRIPT IS USED THE ANDREW MARR SHOW INTERVIEW: GEORGE OSBORNE, MP CHANCELLOR OF THE EXCHEQUER NOVEMBER 30 th 2014 Now what is it

PLEASE NOTE THE ANDREW MARR SHOW MUST BE CREDITED IF ANY PART OF THIS TRANSCRIPT IS USED THE ANDREW MARR SHOW INTERVIEW: GEORGE OSBORNE, MP CHANCELLOR OF THE EXCHEQUER NOVEMBER 30 th 2014 Now what is it

CHAPTER 03. A Modern and. Pensions System

CHAPTER 03 A Modern and Sustainable Pensions System 24 Introduction 3.1 A key objective of pension policy design is to ensure the sustainability of the system over the longer term. Financial sustainability

CHAPTER 03 A Modern and Sustainable Pensions System 24 Introduction 3.1 A key objective of pension policy design is to ensure the sustainability of the system over the longer term. Financial sustainability

Protection & Investment Ltd

istockphoto.com/frank Rotthaus Spring 2012 Protection & Investment Ltd Independent Financial Advisers In this issue: The tax year-end approaches The pensions revolution continues Investing for growth Autumn

istockphoto.com/frank Rotthaus Spring 2012 Protection & Investment Ltd Independent Financial Advisers In this issue: The tax year-end approaches The pensions revolution continues Investing for growth Autumn

Open Seminar Tackling Child Poverty: Lessons from the UK and New Frontiers in Japan Doshisha University Kyoto January

Open Seminar Tackling Child Poverty: Lessons from the UK and New Frontiers in Japan Doshisha University Kyoto January 9 2012 Until 1945 financial needs of children not recognised by the state poor law,

Open Seminar Tackling Child Poverty: Lessons from the UK and New Frontiers in Japan Doshisha University Kyoto January 9 2012 Until 1945 financial needs of children not recognised by the state poor law,

Eurozone. EY Eurozone Forecast June 2014

Eurozone EY Eurozone Forecast June 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Finland

Eurozone EY Eurozone Forecast June 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for Finland

International Monetary and Financial Committee

International Monetary and Financial Committee Thirty-Sixth Meeting October 14, 2017 IMFC Statement by Guy Ryder Director-General International Labour Organization Summary Statement by Mr Guy Ryder, Director-General

International Monetary and Financial Committee Thirty-Sixth Meeting October 14, 2017 IMFC Statement by Guy Ryder Director-General International Labour Organization Summary Statement by Mr Guy Ryder, Director-General

Svein Gjedrem: Inflation targeting in an oil economy

Svein Gjedrem: Inflation targeting in an oil economy Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at Sparebanken Møre, Ålesund, 4 June 2002. Please note that the text

Svein Gjedrem: Inflation targeting in an oil economy Address by Mr Svein Gjedrem, Governor of Norges Bank (Central Bank of Norway), at Sparebanken Møre, Ålesund, 4 June 2002. Please note that the text

THE AUTUMN STATEMENT. Autumn Statement THE KEY ANNOUNCEMENTS AT-A-GLANCE

THE AUTUMN STATEMENT Autumn Statement 2015 THE KEY ANNOUNCEMENTS AT-A-GLANCE 02 SPENDING REVIEW AND AUTUMN STATEMENT 2015 WELCOME 09 Spending Review and Autumn Statement 2015 Presented by Chancellor George

THE AUTUMN STATEMENT Autumn Statement 2015 THE KEY ANNOUNCEMENTS AT-A-GLANCE 02 SPENDING REVIEW AND AUTUMN STATEMENT 2015 WELCOME 09 Spending Review and Autumn Statement 2015 Presented by Chancellor George

Social care funding options

Analysis May 2018 Social care funding options How much and where from? Toby Watt, Michael Varrow, Adam Roberts, Anita Charlesworth All financial data in this report have been adjusted to 2018/19 prices

Analysis May 2018 Social care funding options How much and where from? Toby Watt, Michael Varrow, Adam Roberts, Anita Charlesworth All financial data in this report have been adjusted to 2018/19 prices

Analysis of CBO s Budget Outlook: Fiscal Years

Analysis of CBO s Budget Outlook: Fiscal Years 2012-2022 Feb 01, 2012 INTRODUCTION The Congressional Budget Office's (CBO) latest Budget and Economic Outlook provides sobering new evidence that our nation's

Analysis of CBO s Budget Outlook: Fiscal Years 2012-2022 Feb 01, 2012 INTRODUCTION The Congressional Budget Office's (CBO) latest Budget and Economic Outlook provides sobering new evidence that our nation's

Ranking Country Page. Category 1: Countries with positive CEP Default Index and positive NTE. 1 Estonia 1. 2 Luxembourg 2.

Overview: Single Results of Euro Countries Ranking Country Page Category 1: Countries with positive CEP Default Index and positive NTE 1 Estonia 1 2 Luxembourg 2 3 Germany 3 4 Netherlands 4 5 Austria 5

Overview: Single Results of Euro Countries Ranking Country Page Category 1: Countries with positive CEP Default Index and positive NTE 1 Estonia 1 2 Luxembourg 2 3 Germany 3 4 Netherlands 4 5 Austria 5

PRE BUDGET OUTLOOK. Ottawa, Canada 17 April 2015 [Revised 24 April 2015] dpb.gc.ca

![PRE BUDGET OUTLOOK. Ottawa, Canada 17 April 2015 [Revised 24 April 2015] dpb.gc.ca](/thumbs/81/84692015.jpg "PRE BUDGET OUTLOOK. Ottawa, Canada 17 April 2015 [Revised 24 April 2015] dpb.gc.ca") Ottawa, Canada 17 April 2015 [Revised 24 April 2015] www.pbo dpb.gc.ca The mandate of the Parliamentary Budget Officer (PBO) is to provide independent analysis to Parliament on the state of the nation

Ottawa, Canada 17 April 2015 [Revised 24 April 2015] www.pbo dpb.gc.ca The mandate of the Parliamentary Budget Officer (PBO) is to provide independent analysis to Parliament on the state of the nation

The Labor Force Participation Puzzle

The Labor Force Participation Puzzle May 23, 2013 by David Kelly of J.P. Morgan Funds Slow growth and mediocre job creation have been common themes used to describe the U.S. economy in recent years, as

The Labor Force Participation Puzzle May 23, 2013 by David Kelly of J.P. Morgan Funds Slow growth and mediocre job creation have been common themes used to describe the U.S. economy in recent years, as

remain the same until the end of 2018.

We predict that the European interest rate will remain the same until the end of 2018. Throughout the past three years the interest rate has remained low. In 2017 and 2016 it has been 0.00% and in 2015

We predict that the European interest rate will remain the same until the end of 2018. Throughout the past three years the interest rate has remained low. In 2017 and 2016 it has been 0.00% and in 2015

1 World Economy. Value of Finnish Forest Industry Exports Fell by Almost a Quarter in 2009

1 World Economy The recovery in the world economy that began during 2009 has started to slow since spring 2010 as stocks are replenished and government stimulus packages are gradually brought to an end.

1 World Economy The recovery in the world economy that began during 2009 has started to slow since spring 2010 as stocks are replenished and government stimulus packages are gradually brought to an end.

COMMISSION STAFF WORKING DOCUMENT. Analysis of the Draft Budgetary Plan of Latvia. Accompanying the document COMMISSION OPINION

EUROPEAN COMMISSION Brussels, 21.11.2018 SWD(2018) 522 final COMMISSION STAFF WORKING DOCUMENT Analysis of the Draft Budgetary Plan of Latvia Accompanying the document COMMISSION OPINION on the Draft Budgetary

EUROPEAN COMMISSION Brussels, 21.11.2018 SWD(2018) 522 final COMMISSION STAFF WORKING DOCUMENT Analysis of the Draft Budgetary Plan of Latvia Accompanying the document COMMISSION OPINION on the Draft Budgetary