California Travel & Tourism Outlook. April 2018

|

|

|

- Amelia Patterson

- 5 years ago

- Views:

Transcription

1 California Travel & Tourism Outlook April 2018

2 California travel forecast overview Total visitation to California is forecast to grow 2.9% in 2018, following a 2.0% expansion in The near-term outlook for California travel has been slightly downgraded by 0.2%pp. International visits to California from overseas will slow from 4.5% in 2017 to 4.3% in 2018, and we expect similar growth to continue each year through Mexico is expect to recover in 2018 and grow by 3.2% after a 3% decline in 2017, as a result of tensions between Mexico and the US, as well as a decrease in demand due to unfriendly immigration policies. Meanwhile, YTD visits from Canada suggest that robust and strong recovery from a decline in 2016 is continuing into Canadian arrivals grew 7.5% in 2017 and are expected to slow to 3.2% in Domestic visitation will expand 2.8% in 2018 after a weaker 2017, which saw 2.0% growth. Overnight travel is expected to accelerate to 2.6% in 2018, before returning to below 2% growth in Domestic business travel is expected to outperform the domestic leisure market this year on strong growth in business investment. Growth in visits to California is easing from robust rates seen during the recovery after the Great Recession. Domestic demand drivers remain strong, and long-term growth in U.S. travel to the state will track close to %. 2

3 Economic overview YTD data suggest healthy international inbound travel to California in the first three months of Solid macroeconomic environment, which includes steady global growth and a weaker US dollar, will help overseas arrivals grow 4.3% in Uncertainty surrounding outcomes of the current administration s immigration policies and trade restrictions present downside risks to our forecasts. Record consumer confidence and healthy employment should support consumer spending, though modest real income growth will be a constraint. We are expecting strong business investment in 2018, which should help prop up business travel. Over the forecast horizon, the business travel segment is expected to moderate. We expect real US GDP to grow 2.8% in 2018, supported by a solid labor market, firm business investment, and a strong global activity. 3

4 California travel forecast summary California Tourism Summary (Annual % change) Total Visits 3.1% 5.6% 3.5% 4.8% 1.9% 2.0% 2.9% 2.7% 2.3% 2.7% 2.6% Domestic Total Visits 3.1% 5.6% 3.4% 4.9% 1.9% 2.0% 2.8% 2.6% 2.2% 2.5% 2.5% Leisure Visits 4.9% 6.8% 4.1% 5.3% 2.2% 2.2% 2.8% 2.6% 2.5% 2.7% 2.7% International Total 3.5% 4.5% 5.1% 3.6% 1.6% 1.3% 3.7% 3.9% 4.3% 4.2% 4.2% Overseas 0.8% 6.7% 9.9% 5.7% 2.2% 4.5% 4.3% 4.2% 4.3% 4.1% 4.0% Mexico 5.7% 3.4% 1.3% 3.0% 1.9% -3.0% 3.2% 3.8% 4.5% 4.6% 4.5% Canada 4.6% 1.6% 3.7% -2.8% -2.4% 7.5% 3.2% 3.0% 3.1% 2.8% 2.9% Total Expenditures ($ billions) % change 4.2% 0.7% 7.1% 3.8% 3.6% 4.8% 5.3% 4.7% 4.4% 4.4% 4.5% Domestic % change 3.9% -1.1% 6.8% 3.4% 3.7% 4.8% 5.6% 4.7% 4.2% 4.2% 4.4% International % change 5.3% 9.1% 8.3% 5.6% 3.4% 4.7% 4.1% 4.6% 5.3% 5.1% 5.3% Source: Tourism Economics; DKSA, TNS Global (domestic); CIC Research; OTTI (international); Dean Runyan (expenditures) 4

5 California travel forecast summary Annual Person Trips to California (Millions) Total Business Leisure Domestic Total Business Leisure Day Overnight International Total Overseas Mexico Canada Business Leisure Source: Tourism Economics; DKSA, TNS Global (domestic); CIC Research, OTTI (international); Dean Runyan, CIC Research (expenditures) 5

6 California travel forecast summary Forecast Comparison Percentage Point Change in the Forecast, May 2018 versus Feb 2018 Vintage Total Visits (0.1) (0.2) (0.4) (0.3) 0.0 Domestic Total Visits (0.2) (0.2) (0.4) (0.3) 0.0 Leisure Visits (0.3) (0.5) (0.5) (0.4) 0.0 International Total % change (0.2) 0.0 (0.0) 0.0 Overseas (0.0) (0.1) 0.0 Mexico (0.5) Canada (0.1) 0.0 Total Expenditures % change (2.8) (2.3) 4.5 (0.6) Domestic % change (1.9) (3.9) 6.1 (0.8) (0.0) (0.1) International % change (7.1) 5.0 (2.8) (0.1) (0.5) 2.1 (0.6) Source: Tourism Economics 6

7 7 California Travel Outlook SUMMARY

8 California underperforms US in room night demand California underperformed the nation in room demand growth in the first three months of Room demand grew 2.3% in March 2018 compared to the same period previous year. Occupancy rates in California hotels increased in the first three months of this year compared to the first three months of Growth in YTD average daily room rate was faster than in the nation and but slower than in the Pacific US. APIS air passenger data through March 2018 shows solid growth across top foreign source markets to the U.S. While Brazil has surpassed China by quite a margin, Germany and Japan have posted year-to-date declines. 8

9 Total visits expected to pick up in 2018 Total demand growth for California will pick up from 2.0% in 2017 to 2.9% in 2018 and 2.7% in Growth will average close to 2.6% through While there are no signs of Middle East recovery, both Australia and Mexico are expected to grow in Growth from Mexico will outpace both overseas and domestic travel to California by Strong domestic fundamentals continue to support travel demand. Growth in the business segment will outpace growth in the leisure segment in the near term. By 2020, we expect this trend to return to its historic trend. 9

10 California Travel Outlook DOMESTIC FORECAST 10

11 Business and leisure travel On the domestic front, growth in both business and leisure travel segments will outperform that of the U.S. in the near term. In 2018, we expect business investment and exports to be strong engines of growth while consumer spending trends will reflect a mature economy. 11

12 Day and overnight travel Our outlook for day visitation has been slightly downgraded on higher gas prices. Growth of close to 4.0% in day visits is expected in A slowdown in pace of growth is expected through the end of the forecast period. Nonetheless, day visitor growth will exceed the overnight segment growth over the next five years. Domestic visitor spending will improve to 4.7% in 2018 from 3.7% in 2017 as lodging costs continue to rise and inflation begins to pick up on the back of the Fed s gradual interest rate tightening cycle. Longer-term, growth in domestic expenditures will average around 4.3%, which is an upgrade compared to our previous outlook. 12

13 Domestic forecast growth Domestic Annual Person Trips to California (Annual % change) Total 3.1% 5.6% 3.4% 4.9% 1.9% 2.0% 2.8% 2.6% 2.2% 2.5% 2.5% Business -3.7% 0.8% 0.3% 2.8% 1.0% 1.1% 3.2% 2.6% 1.0% 1.7% 1.4% Leisure 4.9% 6.8% 4.1% 5.3% 2.2% 2.2% 2.8% 2.6% 2.5% 2.7% 2.7% Day 3.4% 6.1% 3.6% 5.4% 1.6% 2.7% 3.0% 2.8% 2.7% 3.1% 2.9% Overnight 2.8% 5.2% 3.2% 4.2% 2.3% 1.2% 2.6% 2.4% 1.7% 1.9% 1.9% (Annual % change) Drive -0.5% 8.0% 3.4% 5.0% 1.3% 1.8% 2.6% 2.4% 2.1% 2.5% 2.4% Fly 31.2% -8.7% 3.5% 3.8% 6.6% 3.6% 4.5% 4.2% 3.2% 3.1% 3.0% Gateway 3.2% 2.6% 3.1% 2.2% 1.5% 0.8% 2.5% 2.4% 3.0% 2.9% 2.8% Non-Gateway 4.0% 3.7% 4.9% 4.7% 2.6% 2.4% 2.5% 1.9% 1.8% 1.5% 1.5% Paid Accommodation 2.6% 4.3% 3.0% 3.5% 2.2% 1.3% 3.0% 3.2% 1.9% 2.0% 2.0% Non-paid 3.1% 6.9% 3.5% 5.9% 2.5% 1.0% 1.9% 0.7% 1.3% 1.5% 1.8% Source: Tourism Economics, TNS Global, STR Domestic Person Trips to California Gatew ay is defined as visitation to one or more of the follow ing metropolitan areas: San Diego, Anaheim-Orange County, Los Angeles, San Francisco Bay Area; Non-Gatew ay is defined as visitation to one or more non-gatew ay destinations. 13

14 Domestic leisure forecast growth by market Annual Domestic Leisure Trips to California (Annual % change) Total 4.9% 6.8% 4.1% 5.3% 2.2% 2.2% 2.8% 2.6% 2.5% 2.7% 2.7% California 4.9% 7.6% 4.4% 4.7% 2.1% 2.0% 2.7% 2.3% 2.3% 2.7% 2.6% Primary Markets 4.4% 6.6% -1.4% 4.5% 3.9% 3.2% 3.3% 4.2% 3.0% 2.7% 3.0% Arizona 5.4% 6.4% -7.5% 1.4% 2.7% -0.2% 3.3% 4.2% 3.0% 2.4% 3.0% Nevada 2.4% 9.8% 2.0% 6.0% 4.7% 5.3% 3.5% 4.3% 2.9% 2.8% 2.9% Oregon 10.7% 4.6% -3.6% 6.2% 5.5% 4.6% 3.0% 3.8% 2.7% 2.7% 2.8% Washington 3.1% 4.7% 1.6% 6.5% 6.2% 2.7% 3.1% 3.9% 3.0% 2.2% 3.0% Utah 0.4% 5.8% 6.4% 6.1% 3.9% 5.1% 3.4% 4.0% 3.0% 2.9% 3.0% Colorado 5.0% 5.4% 0.9% 4.6% 1.2% 4.8% 3.1% 4.8% 3.5% 3.4% 3.3% Opportunity Markets 3.9% 8.1% 3.6% 6.2% 2.6% 2.3% 3.7% 3.9% 3.3% 3.3% 3.2% Texas 4.0% 9.6% 2.7% 6.6% 2.6% 2.3% 3.6% 4.5% 3.9% 3.8% 3.8% New York 2.6% 7.3% 5.4% 5.8% 1.8% 2.1% 3.7% 3.4% 2.9% 2.9% 2.9% Illinois 5.3% 6.7% 3.0% 5.9% 3.4% 2.4% 3.7% 3.4% 2.9% 2.8% 2.8% Rest of US 6.5% -0.5% 9.5% 12.5% 0.5% 2.4% 2.3% 2.8% 2.8% 2.9% 3.0% Source: Tourism Economics, DKSA, TNS Global Note on volatility of historical data and treatment in forecast: Due to smaller sample sizes and relatively smaller visitor volumes in absolute terms, the historical data of origin markets tends to be more volatile than total visitor volumes. 14

15 Domestic leisure forecast by market (Millions) Total California Primary Markets Arizona Nevada Oregon Washington Utah Colorado Opportunity Markets Texas New York Illinois Rest of US Source: Tourism Economics, DKSA, TNS Global Annual Domestic Leisure Trips to California 15

16 Domestic forecast market segmentation Domestic Person Trips to California (Millions) Drive Fly Gateway Rural/Other Paid Accommodation Non-paid Source: Tourism Economics, TNS Global, STR 16

17 Domestic market comparisons California has been steadily gaining market share from Texas. By the end of 2022, more than 42% of travel from Opportunity Markets will have come from Texas compared to 40% in Illinois position has not changed much since 2009; Illinois has counted for 29% of travel from Opportunity Markets and we don t expect this to change much in the next five years. 17

18 California Travel Outlook INTERNATIONAL FORECAST 18

19 Strong CA international inbound travel Strong double-digit growth from Korea and China helped counter a 3.0% decline from Mexico in California ended the year slightly behind the nation, but we expect a reversal of this trend over the forecast horizon. Growth in international inbound travel will surpass 4.0% mark by Strong growth in arrivals from Asia, and California s key origin markets, Mexico and Canada, will help propel the state to outperform the nation through the forecast period. A weaker dollar and improvements in major source market economies will help make the US a more attractive market for foreign travelers. However, caution remains as uncertainty regarding immigration and international relations continue to linger on. 19

20 YTD data suggest strong beginning of 2018 APIS YTD data suggest strong international arrivals in the first two months of Compared to the same period a year ago, total overseas arrivals into LAX were up 6.1%, while Canada was even stronger at 8.4%. We are also seeing strong arrivals from France, Australia, and China, giving support to our growth projections from these origin markets. Both OAG and APIS YTD data show declining visits from Middle East, suggesting that Middle East has not began to recover. The data also shows declines from Germany. However, given the strength of German economy, and the Eurozone in general, we don t expect this trend to continue throughout the rest of the year. 20

21 Inbound trips forecast growth Annual International Trips to California (Annual % change) Total 3.5% 4.5% 5.1% 3.6% 1.6% 1.3% 3.7% 3.9% 4.3% 4.2% 4.2% China 42.8% 22.1% 21.5% 16.7% 17.1% 11.1% 8.8% 8.2% 8.0% 7.8% 7.7% India 3.0% 26.3% 9.3% 11.2% 9.5% 4.5% 7.0% 6.2% 6.5% 6.1% 6.0% Japan 1.7% -4.0% 7.4% -6.5% 1.9% 1.1% 2.1% 2.0% 1.9% 1.8% 1.5% South Korea -1.7% 0.4% 2.0% 10.3% 7.3% 13.3% 6.0% 6.0% 5.4% 5.5% 5.1% Australia -5.1% 5.9% 6.4% 3.6% -0.9% -0.4% 2.2% 2.0% 1.6% 1.9% 2.0% United Kingdom -3.1% 2.6% 5.3% 2.7% -1.7% 4.0% 2.2% 1.8% 1.8% 2.0% 1.7% Germany -2.4% 5.7% 4.1% -0.6% -2.9% 4.4% 2.1% 2.1% 1.8% 1.7% 1.6% France -16.1% 4.0% 14.7% -0.9% 0.3% 1.6% 3.1% 2.6% 3.0% 2.7% 1.9% Italy -11.4% -4.2% 13.2% -0.8% 0.3% 5.7% 4.5% 2.2% 2.1% 1.6% 1.1% Scandinavia 7.9% 7.0% 11.1% 3.1% 0.9% 1.0% 2.2% 1.9% 2.0% 2.1% 1.9% Brazil 14.2% 12.8% 6.7% 2.0% -18.3% 2.9% 6.2% 5.1% 5.2% 4.8% 4.7% Middle East 26.3% 14.0% 21.9% 4.4% 1.5% -9.1% -3.7% 2.4% 4.5% 4.3% 3.9% Canada 4.6% 1.6% 3.7% -2.8% -2.4% 7.5% 3.2% 3.0% 3.1% 2.8% 2.9% Mexico 5.7% 3.4% 1.3% 3.0% 1.9% -3.0% 3.2% 3.8% 4.5% 4.6% 4.5% Rest of World -4.9% 5.3% 8.5% 8.4% -1.7% 3.7% 3.8% 3.8% 3.9% 3.5% 3.6% Source: Tourism Economics, CIC Research, OTTI Note on volatility of historical data and treatment in forecast: Due to smaller sample sizes and relatively smaller visitor volumes in absolute terms, the historical data of origin markets tends to be more volatile than total visitor volumes. 21

22 Inbound trips forecast (Thousands) Total 14,973 15,654 16,459 17,058 17,338 17,568 18,218 18,935 19,740 20,573 21,428 China ,162 1,361 1,512 1,645 1,780 1,922 2,073 2,233 India Japan South Korea Australia United Kingdom Germany France Italy Scandinavia Brazil Middle East Canada 1,543 1,567 1,625 1,579 1,542 1,657 1,710 1,762 1,816 1,868 1,922 Mexico 7,233 7,477 7,572 7,799 7,949 7,710 7,957 8,263 8,635 9,032 9,442 Rest of World 1,691 1,781 1,932 2,095 2,058 2,135 2,216 2,300 2,390 2,473 2,562 Source: Tourism Economics, CIC Research, OTTI Annual International Trips to California 22

23 Mexico trips forecast by air and land Mexican Trips to California by Mode (Annual % change) Border Crossing 5.9% 3.5% 1.0% 3.1% 2.1% -3.7% 3.9% 5.0% 4.6% 4.1% 4.1% Air 2.7% 2.1% 5.3% 2.2% -0.3% 6.0% 2.6% 3.8% 3.2% 2.6% 2.5% Source: Tourism Economics, CIC Research, OTTI 23

24 California Travel Outlook VISITOR SPENDING 24

25 A weaker US dollar impacts foreign spending Low fuel costs had supported domestic leisure travel, particularly day trips, while tempering average expenditures. High gas prices and inflation will boost domestic expenditures to the 4.0% range through the forecast. A weaker US dollar will prop up foreign buying power in California. California total visitor spending grew 4.8% in 2017 before ramping up to 5.3% as inflation strengthens and a weaker US dollar induces stronger international spend in Direct Visitor Expenditures ($ Billions) Total Expenditures % change 4.2% 0.7% 7.1% 3.8% 3.6% 4.8% 5.3% 4.7% 4.4% 4.4% 4.5% Domestic % change 3.9% -1.1% 6.8% 3.4% 3.7% 4.8% 5.6% 4.7% 4.2% 4.2% 4.4% International % change 5.3% 9.1% 8.3% 5.6% 3.4% 4.7% 4.1% 4.6% 5.3% 5.1% 5.3% Source: Tourism Economics, Dean Runyan, CIC Research

26 Dollar strength has altered spending trajectory 26

27 Macro forecast assumptions / CA travel model drivers US & GLOBAL ECONOMIES 27

28 Oxford Economics forecast highlights World GDP growth for 2018 at 3.2% & for 2019 at 3.0%. Global surveys signal that the global expansion may lose momentum in Q2. The global PMI fell sharply in March. The fall highlights the risk that lingering trade tensions could damage confidence and prompt firms and consumers to delay investment and major spending plans. US economy will remain in 2% growth mode with inflation reaching the Fed s 2% target in Eurozone GDP growth forecast for 2018 nudged down to 2.2%, but the pace is expected to remain well above trend. China s growth picked up markedly in early 2018, which could provide a fillip to global trade growth in the near term. 28

29 Strongest world post-crisis economic growth in 2018 Global economic growth appears synchronized and solid. Expected 3.2% global GDP growth in 2018 will be strongest performance postcrisis. Synchronized growth in both advanced and emerging economies. Low interest rates / supportive credit, and fastest world trade since crisis. 29

30 Global growth at best since

31 A slow start to the year, but momentum still solid 31

32 $300 billion spending bill which will reach up")

32 US economy is ramping up (2.9% GDP growth this year) $1.5 trillion tax cut (TCJA) 32 $300 billion spending bill which will reach up to $1.2 trillion (BBA)

33 Ongoing rotation to business investment in 2018: US Business investment and exports will be stronger engines of growth. Consumer spending trends will reflect a maturing economy. 33

34 US companies are finally investing 34

35 Business investment continues to grow strongly 35

36 Leading surveys point to ongoing momentum 36

37 Private sector confidence remains upbeat 37

38 Labor market dynamics are positive 38

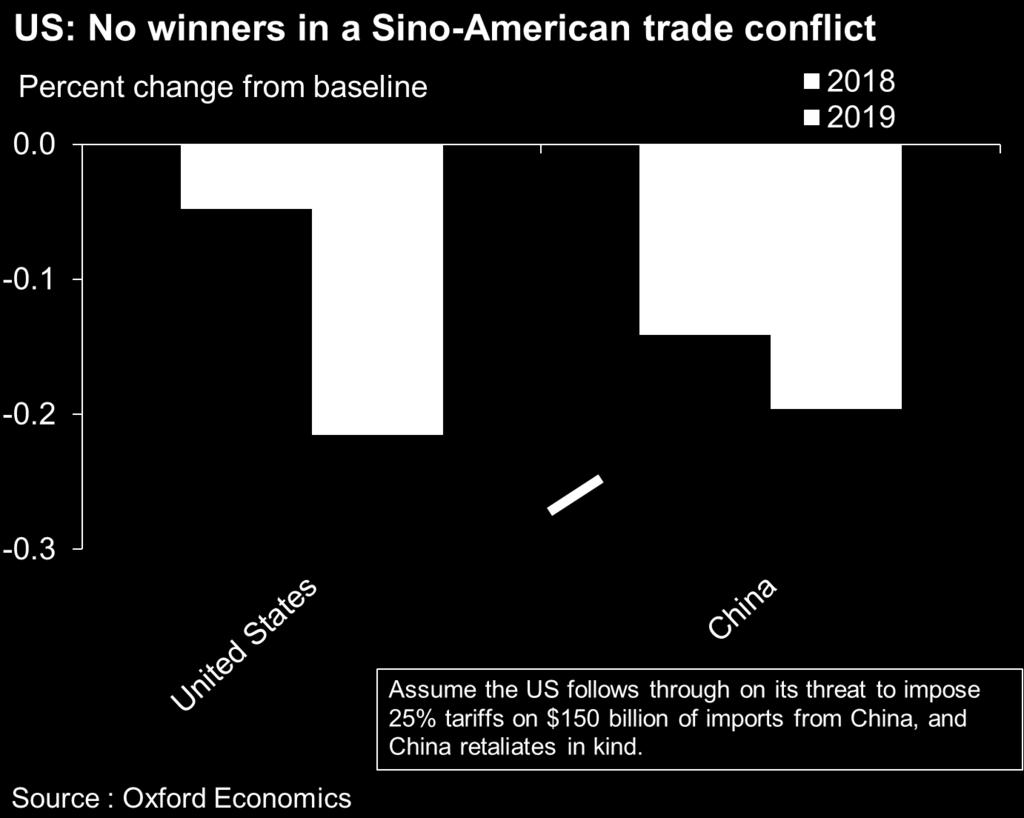

39 What could possibly go wrong? 39

40 Risk #1: Trade protectionism 40

41 Risk #2: Fed s balancing act could prove challenging Recession shading Faster inflation could lead to a more hawkish Fed and a market indigestion. A wider a budget deficit and reduced asset purchases from the Fed could push up long term rates 41

42 Risk #3: Wages must increase 42

43 Monitor savings dip : Savings = ½ consumer spending since 2015 US: Consumer spending growth attribution % Income contribution Savings contribution Real PCE growth Source : Oxford Economics / Haver Analytics

44 But savings dip driven mostly by lower-income families US: The bottom 60% are driving the savings dip US$ billion Total savings EOP (2015) Top 40%: increased savings Bottom 60%: decreased savings Source : Oxford Economics / Consumer Expenditure Survey Total savings (2016) EOP 44

45 Risk 4: Fiscal overdrive and growth exhaustion Key risk for : 1. Reduced marginal fiscal stimulus 2. Higher inflation 3. Tighter Fed stance 4. Wider deficit 5. Higher long-term borrowing cost 6. More protectionism 45

46 The dollar has eased, supporting further inbound gains Value of the US dollar in 2017Q4: 12% stronger than 2014, but just 2.0% stronger than historical average 46

47 Forecast summary We expect GDP growth to average 2.8%, up from 2.3% in 2017 and 1.5% in Recent spending data point to a slow start to the year with Q GDP growth around 1.5%. Substantial late-cycle fiscal stimulus, which we see contributing 0.7pp to GDP, will push up growth in subsequent quarters. Inflation is expected to reach the Fed s 2% target this year. Although recently threatened tariffs between China and the US pose a growing downside risk to our forecast, we note that tangible actions will take months to materialize and will likely be scaled back significantly. 47

48 Macroeconomic forecast for the United States While economic momentum has picked up in early spring, trade tensions have escalated. The economy will grow 2.8% in 2018, with a quarter of the growth coming from tax cuts and increased government spending, and the rest coming from solid fundamentals. Key forecast drivers include: 48 Healthy but maturing labor market: solid employment growth and gradually firming wage growth will support household income, confidence and outlays. The unemployment rate will likely fall towards 3.7% this year. Solid consumer spending but lower savings: fiscal stimulus should combine with robust employment growth, gradually firming wages, record confidence levels and low interest rates to support household outlays in the near term. Consumer spending is expected to grow 2.6% in 2018, but we note the risk posed by the savings dip amid widening income and wealth inequality. Strengthening business investment: stronger global growth, the corporate tax cut and a competitive US dollar will support business investment growth of around 6.3% this year, up from 4.7% in Firming inflation: headline and core personal consumption expenditure (PCE) inflation are expected to reach 2.1% by year end. Policy risks: further trade protectionism will curtail growth, especially if met by retaliation from China and other key partners. Stringent immigration policy remains a risk.

49 Global growth resilient to protectionist concerns 49 Despite the mounting threat of more protectionist trade measures, we expect the impact on global growth and trade to be mild. Given this, and the still fairly solid underlying economic picture, we have left our global GDP growth forecasts for 2018 and 2019 unchanged at 3.2% and 3.0% respectively. Although economic data in Q1 painted a pretty solid picture, there are signs that the global expansion may lose momentum in Q2. Most notably, the global PMI fell sharply in March, more than offsetting the gains of the previous three quarters or som. Some of the decline may reflect an over-reaction to recent trade threats and could be reversed in April and despite the drop, the surveys still point to strong growth. But the fall highlights the risk that lingering trade tensions could damage confidence and prompt firms and consumers to delay investment and major spending plans. On a more positive note, China s economic growth picked up markedly in early 2018, which could provide a fillip to global trade growth in the near term. Given the better-than-expected start to the year, we have made no change to our 2018 China GDP growth forecast (of 6.4%) despite the probably negative effects of trade measures. Meanwhile, most advanced economies remain in the late expansionary stage of the cycle. And those that show signs of slowing, such as the Eurozone, are doing so from multi-year highs. While we have nudged down our 2018 Eurozone GDP growth forecast slightly to 2.2%, the pace is expected to remain well above trend. For now, we see further solid growth for the world economy this year even in the environment of rising protectionism.

50 United States Travel Outlook SUMMARY 50

51 Fuel prices expected to moderate after 2017Q1 spike TPI Components % growth Forecast Lodging (in blue) Motor fuel Food away from home (in red) Source: Tourism Economics 51

52 Leisure trips leading, business trips rebounding Person Trips % growth 5.0 Forecast Business Person Trips (red) Leisure Person Trips (blue) Source: Tourism Economics 52

53 Travel expenditure to pick up in the short-term Total Travel Expenditures % growth 10 Forecast 5 Fall 2017 (blue) Spring 2017 (red) Source: Tourism Economics 53

54 European inbound travel expected to pick up after 2017 European Inbound % growth 12.0% 10.0% 8.0% 6.0% 4.0% 2.0% 0.0% -2.0% Forecast Inbound Tourist Arrivals to US EU GDP Growth -4.0% -6.0% -8.0% Source: Tourism Economics 54

55 Asian inbound travel softening Asia Inbound % growth 25% Forecast 20% 15% 10% 5% Asian GDP Growth (blue) 0% Source: Tourism Economics Inbound Tourist Arrivals to US 55

56 For more information:

California Travel & Tourism Outlook. September 2016

California Travel & Tourism Outlook September 2016 California travel forecast overview Total visitation to California is forecast to grow 2.2% in 2016, following a 4.8% expansion in 2015, which outperformed

California Travel & Tourism Outlook September 2016 California travel forecast overview Total visitation to California is forecast to grow 2.2% in 2016, following a 4.8% expansion in 2015, which outperformed

Outlook for the Economy and Travel Outlook for the Global Economy and Travel

Outlook for the Economy and Travel Outlook for the Global Economy and Travel Adam Sacks President Tourism Economics @adam_sacks Adam Sacks President Tourism Economics @adam_sacks Outline The Outlook for

Outlook for the Economy and Travel Outlook for the Global Economy and Travel Adam Sacks President Tourism Economics @adam_sacks Adam Sacks President Tourism Economics @adam_sacks Outline The Outlook for

OUTLOOK FOR THE GLOBAL ECONOMY AND TRAVEL

January 2018 OUTLOOK FOR THE GLOBAL ECONOMY AND TRAVEL Adam Sacks President Tourism Economics @adam_sacks August 2018 Outline The Outlook for the Economy and Travel Views on the global economy Risks Will

January 2018 OUTLOOK FOR THE GLOBAL ECONOMY AND TRAVEL Adam Sacks President Tourism Economics @adam_sacks August 2018 Outline The Outlook for the Economy and Travel Views on the global economy Risks Will

California Travel & Tourism Outlook. April 2011

California Travel & Tourism Outlook April 2011 Forecast Overview California visits rebounded in 2010: Visitor volumes rose across all measured segments business and leisure, domestic and international.

California Travel & Tourism Outlook April 2011 Forecast Overview California visits rebounded in 2010: Visitor volumes rose across all measured segments business and leisure, domestic and international.

Outlook for the Global Economy and Travel

Outlook for the Global Economy and Travel Adam Sacks President Tourism Economics @adam_sacks November 2018 Let s pose some questions What s happening now? Outline What could go wrong? What s backwards?

Outlook for the Global Economy and Travel Adam Sacks President Tourism Economics @adam_sacks November 2018 Let s pose some questions What s happening now? Outline What could go wrong? What s backwards?

Global Travel Service

15 Nov 2018 Global Travel Service Global Highlights, November 2018 Economists Adam Sacks President of Tourism Economics asacks@oxfordeconomics. com David Goodger Director of Tourism Economics dgoodger@oxfordeconomi

15 Nov 2018 Global Travel Service Global Highlights, November 2018 Economists Adam Sacks President of Tourism Economics asacks@oxfordeconomics. com David Goodger Director of Tourism Economics dgoodger@oxfordeconomi

ECONOMIC OUTLOOK AND THE US LODGING INDUSTRY. Aran Ryan Director Tourism

ECONOMIC OUTLOOK AND THE US LODGING INDUSTRY Aran Ryan Director aran.ryan@tourismeconomics.com @AranRyan1 March 22, 2017 Some historical perspective Room demand expansion continues Pace of demand growth

ECONOMIC OUTLOOK AND THE US LODGING INDUSTRY Aran Ryan Director aran.ryan@tourismeconomics.com @AranRyan1 March 22, 2017 Some historical perspective Room demand expansion continues Pace of demand growth

Missouri Tourism Forecast FY

Current River Missouri Tourism Forecast FY2014-2018 St. Charles Fete de Glace St. Louis Missouri History Museum February 2014 Summary of key points Missouri s tourism economy will continue to expand over

Current River Missouri Tourism Forecast FY2014-2018 St. Charles Fete de Glace St. Louis Missouri History Museum February 2014 Summary of key points Missouri s tourism economy will continue to expand over

Global Macroeconomic Monthly Review

Global Macroeconomic Monthly Review August 14 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department 1 Please see disclaimer on the last page of this report Key Issues Global

Global Macroeconomic Monthly Review August 14 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department 1 Please see disclaimer on the last page of this report Key Issues Global

Eurozone Economic Watch. July 2018

Eurozone Economic Watch July 2018 Eurozone: A shift to more moderate growth with increased downward risks BBVA Research - Eurozone Economic Watch July 2018 / 2 Hard data improved in May but failed to recover

Eurozone Economic Watch July 2018 Eurozone: A shift to more moderate growth with increased downward risks BBVA Research - Eurozone Economic Watch July 2018 / 2 Hard data improved in May but failed to recover

RECOVERY CONTINUES FOR LOGISTICS REAL ESTATE

RECOVERY CONTINUES FOR LOGISTICS REAL ESTATE World events trigger soft patch The global economic soft patch in the first half of 2011 was primarily caused by the cost of oil reaching $114 per barrel, rising

RECOVERY CONTINUES FOR LOGISTICS REAL ESTATE World events trigger soft patch The global economic soft patch in the first half of 2011 was primarily caused by the cost of oil reaching $114 per barrel, rising

The Economic Impact Of Travel on Massachusetts Counties 2015

The Economic Impact Of Travel on Massachusetts Counties 2015 A Study Prepared for the Massachusetts Office of Travel and Tourism By the Research Department of the U.S. Travel Association Washington, D.C.

The Economic Impact Of Travel on Massachusetts Counties 2015 A Study Prepared for the Massachusetts Office of Travel and Tourism By the Research Department of the U.S. Travel Association Washington, D.C.

GLOBAL ECONOMIC OUTLOOK As good as it gets in 2018? Oliver Salmon Lead Economist

GLOBAL ECONOMIC OUTLOOK As good as it gets in 2018? Oliver Salmon Lead Economist osalmon@oxfordeconomics.com March 2018 Global synchronized upturn continues 2 as trade growth maintains healthy momentum

GLOBAL ECONOMIC OUTLOOK As good as it gets in 2018? Oliver Salmon Lead Economist osalmon@oxfordeconomics.com March 2018 Global synchronized upturn continues 2 as trade growth maintains healthy momentum

Economic ProjEctions for

Economic Projections for 2016-2018 ECONOMIC PROJECTIONS FOR 2016-2018 Outlook for the Maltese economy 1 Economic growth is expected to ease Following three years of strong expansion, the Bank s latest

Economic Projections for 2016-2018 ECONOMIC PROJECTIONS FOR 2016-2018 Outlook for the Maltese economy 1 Economic growth is expected to ease Following three years of strong expansion, the Bank s latest

Ireland. Eurozone rebalancing. EY Eurozone Forecast June Portugal Slovakia Slovenia Spain. Latvia Lithuania Luxembourg Malta Netherlands

EY Forecast June 2015 rebalancing recovery Outlook for Rising domestic demand improves prospects for 2015 Published in collaboration with Highlights The Irish economy grew by 4.8% last year, which was

EY Forecast June 2015 rebalancing recovery Outlook for Rising domestic demand improves prospects for 2015 Published in collaboration with Highlights The Irish economy grew by 4.8% last year, which was

San Diego Travel Forecast July 2018

Report Prepared For: San Diego Tourism Authority Contents 1 Executive Summary... 3 2 San Diego Tourism Outlook... 6 2.1 Visitor Trends... 6 2.2 Expenditures... 7 2.3 Hotel Performance... 2 3 US Tourism

Report Prepared For: San Diego Tourism Authority Contents 1 Executive Summary... 3 2 San Diego Tourism Outlook... 6 2.1 Visitor Trends... 6 2.2 Expenditures... 7 2.3 Hotel Performance... 2 3 US Tourism

UNCERTAINTY DIMS EURO AREA GROWTH

EBF Economic Outlook Nr 44 November 2018 2018 AUTUMN OUTLOOK ON THE EURO AREA ECONOMY IN 2018-2019 UNCERTAINTY DIMS EURO AREA GROWTH EDITORIAL TEAM: Francisco Saravia (author), Helge Pedersen, Chair of

EBF Economic Outlook Nr 44 November 2018 2018 AUTUMN OUTLOOK ON THE EURO AREA ECONOMY IN 2018-2019 UNCERTAINTY DIMS EURO AREA GROWTH EDITORIAL TEAM: Francisco Saravia (author), Helge Pedersen, Chair of

WTO lowers forecast after sub-par trade growth in first half of 2014

PRESS RELEASE PRESS/722 26 September 214 (-) WTO lowers forecast after sub-par trade growth in first half of 214 TRADE STATISTICS WTO economists have reduced their forecast for world trade growth in 214

PRESS RELEASE PRESS/722 26 September 214 (-) WTO lowers forecast after sub-par trade growth in first half of 214 TRADE STATISTICS WTO economists have reduced their forecast for world trade growth in 214

Eurozone. EY Eurozone Forecast March 2015

Eurozone EY Eurozone Forecast March 2015 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Lithuania Luxembourg Netherlands Portugal Slovakia Slovenia Spain Outlook for

Eurozone EY Eurozone Forecast March 2015 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Lithuania Luxembourg Netherlands Portugal Slovakia Slovenia Spain Outlook for

ECONOMIC RECOVERY AT CRUISE SPEED

EBF Economic Outlook Nr 43 May 2018 2018 SPRING OUTLOOK ON THE EURO AREA ECONOMIES IN 2018-2019 ECONOMIC RECOVERY AT CRUISE SPEED EDITORIAL TEAM: Francisco Saravia (author), Helge Pedersen - Chair of the

EBF Economic Outlook Nr 43 May 2018 2018 SPRING OUTLOOK ON THE EURO AREA ECONOMIES IN 2018-2019 ECONOMIC RECOVERY AT CRUISE SPEED EDITORIAL TEAM: Francisco Saravia (author), Helge Pedersen - Chair of the

LESS DYNAMIC GROWTH AMID HIGH UNCERTAINTY

OVERVIEW: The European economy has moved into lower gear amid still robust domestic fundamentals. GDP growth is set to continue at a slower pace. LESS DYNAMIC GROWTH AMID HIGH UNCERTAINTY Interrelated

OVERVIEW: The European economy has moved into lower gear amid still robust domestic fundamentals. GDP growth is set to continue at a slower pace. LESS DYNAMIC GROWTH AMID HIGH UNCERTAINTY Interrelated

Eurozone. EY Eurozone Forecast September 2014

Eurozone EY Eurozone Forecast September 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for

Eurozone EY Eurozone Forecast September 2014 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook for

Economic Projections for

Economic Projections for 2015-2017 Article published in the Quarterly Review 2015:3, pp. 86-91 7. ECONOMIC PROJECTIONS FOR 2015-2017 Outlook for the Maltese economy 1 The Bank s latest macroeconomic projections

Economic Projections for 2015-2017 Article published in the Quarterly Review 2015:3, pp. 86-91 7. ECONOMIC PROJECTIONS FOR 2015-2017 Outlook for the Maltese economy 1 The Bank s latest macroeconomic projections

Insolvency forecasts. Economic Research August 2017

Insolvency forecasts Economic Research August 2017 Summary We present our new insolvency forecasting model which offers a broader scope of macroeconomic developments to better predict insolvency developments.

Insolvency forecasts Economic Research August 2017 Summary We present our new insolvency forecasting model which offers a broader scope of macroeconomic developments to better predict insolvency developments.

Eurozone. EY Eurozone Forecast March 2015

Eurozone EY Eurozone Forecast March 2015 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Lithuania Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook

Eurozone EY Eurozone Forecast March 2015 Austria Belgium Cyprus Estonia Finland France Germany Greece Ireland Italy Latvia Lithuania Luxembourg Malta Netherlands Portugal Slovakia Slovenia Spain Outlook

Leumi. Global Economics Monthly Review. Arie Tal, Research Economist. July 12, Capital Markets Division, Economics Department. leumiusa.

Global Economics Monthly Review July 12, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report

Global Economics Monthly Review July 12, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report

THE STATE OF THE ECONOMY

THE STATE OF THE ECONOMY ANGELA GUO Portland State University The United States economy in the fourth quarter of 2013 appears to have a more robust foothold pointing to a healthier outlook for 2014. Much

THE STATE OF THE ECONOMY ANGELA GUO Portland State University The United States economy in the fourth quarter of 2013 appears to have a more robust foothold pointing to a healthier outlook for 2014. Much

Eurozone. Economic Watch FEBRUARY 2017

Eurozone Economic Watch FEBRUARY 2017 EUROZONE WATCH FEBRUARY 2017 Eurozone: A slight upward revision to our GDP growth projections The recovery proceeded at a steady and solid pace in, resulting in an

Eurozone Economic Watch FEBRUARY 2017 EUROZONE WATCH FEBRUARY 2017 Eurozone: A slight upward revision to our GDP growth projections The recovery proceeded at a steady and solid pace in, resulting in an

Global Macroeconomic Monthly Review

Global Macroeconomic Monthly Review October 16 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Please see disclaimer on the last page of this report 1 Key Issues Global

Global Macroeconomic Monthly Review October 16 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Please see disclaimer on the last page of this report 1 Key Issues Global

Slovenia. Eurozone rebalancing. EY Eurozone Forecast June Portugal Slovakia Slovenia Spain. Latvia Lithuania Luxembourg Malta Netherlands

EY Forecast June 215 rebalancing recovery Outlook for Activity to remain solid this year, after growing 2.4% in 214 Published in collaboration with Highlights n GDP grew by 2.4% in 214 and 3% in Q1 215,

EY Forecast June 215 rebalancing recovery Outlook for Activity to remain solid this year, after growing 2.4% in 214 Published in collaboration with Highlights n GDP grew by 2.4% in 214 and 3% in Q1 215,

Leumi. Global Economics Monthly Review. Arie Tal, Research Economist. May 8, The Finance Division, Economics Department. leumiusa.

Global Economics Monthly Review May 8, 2018 Arie Tal, Research Economist The Finance Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report Key

Global Economics Monthly Review May 8, 2018 Arie Tal, Research Economist The Finance Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report Key

Prudential International Investments Advisers, LLC. Global Investment Strategy October 2009

Prudential International Investments Advisers, LLC. Global Investment Strategy October 2009 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Prudential International Investments Advisers, LLC. Global Investment Strategy October 2009 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

1 World Economy. Value of Finnish Forest Industry Exports Fell by Almost a Quarter in 2009

1 World Economy The recovery in the world economy that began during 2009 has started to slow since spring 2010 as stocks are replenished and government stimulus packages are gradually brought to an end.

1 World Economy The recovery in the world economy that began during 2009 has started to slow since spring 2010 as stocks are replenished and government stimulus packages are gradually brought to an end.

Financial Market Outlook: Stock Rally Continues with Faster & Stronger GDP Rebound, Earnings Recovery & Liquidity

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Further Stock Gains with Macro Sweet Spot & Earnings Recovery.

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: Further Stock Gains with Macro Sweet Spot & Earnings Recovery.

Pacific Northwest Economic Development Council Conference Mt. Hood, Oregon June 20, 2005

Pacific Northwest Economic Development Council Conference Mt. Hood, Oregon June 20, 2005 Gary C. Zimmerman, Senior Economist Federal Reserve Bank of San Francisco Gary.Zimmerman@sf.frb.org Overview National

Pacific Northwest Economic Development Council Conference Mt. Hood, Oregon June 20, 2005 Gary C. Zimmerman, Senior Economist Federal Reserve Bank of San Francisco Gary.Zimmerman@sf.frb.org Overview National

Fixed Income. EURO SOVEREIGN OUTLOOK SIX PRINCIPAL INFLUENCES TO CONSIDER IN 2016.

PRICE POINT February 2016 Timely intelligence and analysis for our clients. Fixed Income. EURO SOVEREIGN OUTLOOK SIX PRINCIPAL INFLUENCES TO CONSIDER IN 2016. EXECUTIVE SUMMARY Kenneth Orchard Portfolio

PRICE POINT February 2016 Timely intelligence and analysis for our clients. Fixed Income. EURO SOVEREIGN OUTLOOK SIX PRINCIPAL INFLUENCES TO CONSIDER IN 2016. EXECUTIVE SUMMARY Kenneth Orchard Portfolio

Summary. Economic Update 1 / 7 May Global Global GDP growth is forecast to accelerate to 2.9% in 2017 and maintain at 3.0% in 2018.

Economic Update Economic Update 1 / 7 Summary 2 Global Global GDP growth is forecast to accelerate to 2.9% in 2017 and maintain at 3.0% in 2018. 3 Eurozone The eurozone s recovery appears to strengthen

Economic Update Economic Update 1 / 7 Summary 2 Global Global GDP growth is forecast to accelerate to 2.9% in 2017 and maintain at 3.0% in 2018. 3 Eurozone The eurozone s recovery appears to strengthen

Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy March 2017 Global Stock Markets Rally likely to Continue, Driven by Strong Earnings & Strengthening GDP Growth.

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy March 2017 Global Stock Markets Rally likely to Continue, Driven by Strong Earnings & Strengthening GDP Growth.

What's really happening to house prices. November How big is the fall (so far)?

?") November 2017 David Norman Chief Economist david.norman@aucklandcouncil.govt.nz 021 516 103 What's really happening to house prices Once we account for these seasonal effects, prices have fallen around

November 2017 David Norman Chief Economist david.norman@aucklandcouncil.govt.nz 021 516 103 What's really happening to house prices Once we account for these seasonal effects, prices have fallen around

ASEAN Insights: Regional trends

ASEAN Insights: Regional trends March 2018 1. Global trends BUSINESS AND CONSUMER CONFIDENCE ROBUST; US FED HIKES RATES; EQUITY MARKETS FALL The global economic environment remained positive this month.

ASEAN Insights: Regional trends March 2018 1. Global trends BUSINESS AND CONSUMER CONFIDENCE ROBUST; US FED HIKES RATES; EQUITY MARKETS FALL The global economic environment remained positive this month.

The Return on Investment of Brand USA Marketing Fiscal Year Analysis

The Return on Investment of Brand USA Marketing 2013 Fiscal Year Analysis Contents Executive Summary... 3 1 The Need for Destination Marketing... 5 1.1 Fragmentation of the tourism sector... 6 1.2 The

The Return on Investment of Brand USA Marketing 2013 Fiscal Year Analysis Contents Executive Summary... 3 1 The Need for Destination Marketing... 5 1.1 Fragmentation of the tourism sector... 6 1.2 The

In this report we discuss three important areas of the economy that have received a great deal of attention recently, namely:

March 26, 218 Executive Summary George Mokrzan, PH.D., Director of Economics In this report we discuss three important areas of the economy that have received a great deal of attention recently, namely:

March 26, 218 Executive Summary George Mokrzan, PH.D., Director of Economics In this report we discuss three important areas of the economy that have received a great deal of attention recently, namely:

Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy February 2017 Global Stock Market Rally likely to Continue with Solid Q4 Earnings & Stronger 2017 Earnings, ECB

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy February 2017 Global Stock Market Rally likely to Continue with Solid Q4 Earnings & Stronger 2017 Earnings, ECB

Explore the themes and thinking behind our decisions.

ASSET ALLOCATION COMMITTEE VIEWPOINTS First Quarter 2017 These views are informed by a subjective assessment of the relative attractiveness of asset classes and subclasses over a 6- to 18-month horizon.

ASSET ALLOCATION COMMITTEE VIEWPOINTS First Quarter 2017 These views are informed by a subjective assessment of the relative attractiveness of asset classes and subclasses over a 6- to 18-month horizon.

ASEAN Insights: Regional trends

ASEAN Insights: Regional trends January 2017 1. Global trends GLOBAL ECONOMY AND EQUITY MARKETS ENTER 2017 ON A STRONG NOTE DESPITE GEOPOLITICAL UNCERTAINTIES The global economy entered 2017 on a strong

ASEAN Insights: Regional trends January 2017 1. Global trends GLOBAL ECONOMY AND EQUITY MARKETS ENTER 2017 ON A STRONG NOTE DESPITE GEOPOLITICAL UNCERTAINTIES The global economy entered 2017 on a strong

The Prospects Service

The Prospects Service LEADING ECONOMIC ANALYSIS, FORECASTS AND DATA Global Prospects, January 2017 Toplines The world economy remains in a stage of heightened uncertainty, with ongoing Brexit negotiations,

The Prospects Service LEADING ECONOMIC ANALYSIS, FORECASTS AND DATA Global Prospects, January 2017 Toplines The world economy remains in a stage of heightened uncertainty, with ongoing Brexit negotiations,

FOREIGN INVESTMENT IN U.S. REAL ESTATE Current Trends and Historical Perspective

FOREIGN INVESTMENT IN U.S. REAL ESTATE Current Trends and Historical Perspective Prepared by the Research Division of THE NATIONAL ASSOCIATION OF REALTORS November 2008 Preface Through the early years

FOREIGN INVESTMENT IN U.S. REAL ESTATE Current Trends and Historical Perspective Prepared by the Research Division of THE NATIONAL ASSOCIATION OF REALTORS November 2008 Preface Through the early years

Global PMI. Solid Q2 growth masks widening growth differentials. July 7 th IHS Markit. All Rights Reserved.

Global PMI Solid Q2 growth masks widening growth differentials July 7 th 2017 2 Widening developed and emerging world growth trends The global economy enjoyed further steady growth in June, according to

Global PMI Solid Q2 growth masks widening growth differentials July 7 th 2017 2 Widening developed and emerging world growth trends The global economy enjoyed further steady growth in June, according to

Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy April 2017 Stock Markets likely to Grind Higher as Expectations of Strong Earnings Growth & Improving Global GDP

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy April 2017 Stock Markets likely to Grind Higher as Expectations of Strong Earnings Growth & Improving Global GDP

EUROPEAN COMMISSION DIRECTORATE-GENERAL FOR ECONOMIC AND FINANCIAL AFFAIRS. September 2006 Interim forecast

EUROPEAN COMMISSION DIRECTORATE-GENERAL FOR ECONOMIC AND FINANCIAL AFFAIRS September 26 Interim forecast Press conference of 6 September 26 European economic growth speeding up, boosted by buoyant domestic

EUROPEAN COMMISSION DIRECTORATE-GENERAL FOR ECONOMIC AND FINANCIAL AFFAIRS September 26 Interim forecast Press conference of 6 September 26 European economic growth speeding up, boosted by buoyant domestic

Global PMI. Global economy buoyed by rising US strength. June 12 th IHS Markit. All Rights Reserved.

Global PMI Global economy buoyed by rising US strength June 12 th 2018 2 Global PMI rises but also brings signs of slower future growth At 54.0 in May, the headline JPMorgan Global Composite PMI, compiled

Global PMI Global economy buoyed by rising US strength June 12 th 2018 2 Global PMI rises but also brings signs of slower future growth At 54.0 in May, the headline JPMorgan Global Composite PMI, compiled

International Monetary and Financial Committee

International Monetary and Financial Committee Thirty-Third Meeting April 16, 2016 IMFC Statement by Angel Gurría Secretary-General The Organisation for Economic Co-operation and Development (OECD) IMF

International Monetary and Financial Committee Thirty-Third Meeting April 16, 2016 IMFC Statement by Angel Gurría Secretary-General The Organisation for Economic Co-operation and Development (OECD) IMF

Global Economic Outlook

Global Economic Outlook Will the growth continue and at what pace? Latin American Conference São Paulo August 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary Information

Global Economic Outlook Will the growth continue and at what pace? Latin American Conference São Paulo August 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary Information

BANK OF FINLAND ARTICLES ON THE ECONOMY

BANK OF FINLAND ARTICLES ON THE ECONOMY Table of Contents Global economy to grow steadily 3 FORECAST FOR THE GLOBAL ECONOMY Global economy to grow steadily TODAY 1:00 PM BANK OF FINLAND BULLETIN 1/2017

BANK OF FINLAND ARTICLES ON THE ECONOMY Table of Contents Global economy to grow steadily 3 FORECAST FOR THE GLOBAL ECONOMY Global economy to grow steadily TODAY 1:00 PM BANK OF FINLAND BULLETIN 1/2017

Global Economic Prospects: A Fragile Recovery. June M. Ayhan Kose Four Questions

//7 Global Economic Prospects: A Fragile Recovery June 7 M. Ayhan Kose akose@worldbank.org Four Questions How is the health of the global economy? Recovery underway, broadly as expected How important is

//7 Global Economic Prospects: A Fragile Recovery June 7 M. Ayhan Kose akose@worldbank.org Four Questions How is the health of the global economy? Recovery underway, broadly as expected How important is

A PROPOSAL FOR MONTH YEAR (ALL CAPS) CHARTBOOK. Market Indicators

CHARTBOOK. Market Indicators") A PROPOSAL FOR MONTH YEAR (ALL CAPS) CHARTBOOK Market Indicators November 2015 For more information, contact: Janlo de los Reyes Manager Research and Consultancy janlo.delosreyes@ap.cushwake.com Leo De

A PROPOSAL FOR MONTH YEAR (ALL CAPS) CHARTBOOK Market Indicators November 2015 For more information, contact: Janlo de los Reyes Manager Research and Consultancy janlo.delosreyes@ap.cushwake.com Leo De

Financial Market Outlook: Further Stock Gain on Faster GDP Rebound and Earnings Recovery. Year-end Target Raised

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: FurtherStock Gains Likely, Year-end Target Raised. Bond Under Pressure

For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com Financial Market Outlook & Strategy: FurtherStock Gains Likely, Year-end Target Raised. Bond Under Pressure

Outlook for the Hawai'i Economy

Outlook for the Hawai'i Economy May 3, 2001 Dr. Carl Bonham University of Hawai'i Economic Research Organization Summary The Hawaii economy entered 2001 in its best shape in more than a decade. While the

Outlook for the Hawai'i Economy May 3, 2001 Dr. Carl Bonham University of Hawai'i Economic Research Organization Summary The Hawaii economy entered 2001 in its best shape in more than a decade. While the

INVESTMENT REVIEW Q2 2018

INVESTMENT REVIEW Q2 2018 OVERVIEW Surveys and hard data show the global economy growing at a healthy pace with minimal inflation risk. Activity accelerated in Q2 and our expectation of 3.4% GDP growth

INVESTMENT REVIEW Q2 2018 OVERVIEW Surveys and hard data show the global economy growing at a healthy pace with minimal inflation risk. Activity accelerated in Q2 and our expectation of 3.4% GDP growth

Research Briefing Global

Research Briefing Global Top ten calls for 2017 Trumponomics leads the way Economist Adam Slater Lead Economist +44(0)1865268934 Our top ten calls for 2017 are, not surprisingly, dominated by the impact

Research Briefing Global Top ten calls for 2017 Trumponomics leads the way Economist Adam Slater Lead Economist +44(0)1865268934 Our top ten calls for 2017 are, not surprisingly, dominated by the impact

2018 ECONOMIC OUTLOOK

LPL RESEARCH WEEKLY ECONOMIC COMMENTARY December 4 207 208 ECONOMIC OUTLOOK EXPECT BETTER GROWTH WORLDWIDE John Lynch Chief Investment Strategist, LPL Financial Barry Gilbert, PhD, CFA Asset Allocation

LPL RESEARCH WEEKLY ECONOMIC COMMENTARY December 4 207 208 ECONOMIC OUTLOOK EXPECT BETTER GROWTH WORLDWIDE John Lynch Chief Investment Strategist, LPL Financial Barry Gilbert, PhD, CFA Asset Allocation

San Diego Travel Forecast July 2017

Report Prepared For: San Diego Tourism Authority Contents 1 Executive Summary... 3 2 San Diego Tourism Outlook... 5 2.1 Visitor Trends... 5 2.2 Expenditures... 6 2.3 Hotel Performance... 7 3 US Tourism

Report Prepared For: San Diego Tourism Authority Contents 1 Executive Summary... 3 2 San Diego Tourism Outlook... 5 2.1 Visitor Trends... 5 2.2 Expenditures... 6 2.3 Hotel Performance... 7 3 US Tourism

Economic Update. Port Finance Seminar. Paul Bingham. Global Insight, Inc. Copyright 2006 Global Insight, Inc.

Economic Update Copyright 26 Global Insight, Inc. Port Finance Seminar Paul Bingham Global Insight, Inc. Baltimore, MD May 16, 26 The World Economy: Is the Risk of a Boom-Bust Rising? As the U.S. Economy

Economic Update Copyright 26 Global Insight, Inc. Port Finance Seminar Paul Bingham Global Insight, Inc. Baltimore, MD May 16, 26 The World Economy: Is the Risk of a Boom-Bust Rising? As the U.S. Economy

Prudential International Investments Advisers, LLC. Global Investment Strategy March 2010

Prudential International Investments Advisers, LLC. Global Investment Strategy March 2010 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Prudential International Investments Advisers, LLC. Global Investment Strategy March 2010 By John Praveen, Chief Investment Strategist For Market Commentary Interviews Contact: Lisa Villareal, 973-367-2503/lisa.villareal@prudential.com

Global Economic Outlook - April 2018

Global Economic Outlook - April 2018 April 12, 2018 by Carl Tannenbaum, Ryan James Boyle, Brian Liebovich, Vaibhav Tandon of Northern Trust Entering 2018, our outlook was uniformly upbeat. Fiscal stimulus

Global Economic Outlook - April 2018 April 12, 2018 by Carl Tannenbaum, Ryan James Boyle, Brian Liebovich, Vaibhav Tandon of Northern Trust Entering 2018, our outlook was uniformly upbeat. Fiscal stimulus

New Zealand Economic Outlook. Miles Workman June 2017

New Zealand Economic Outlook Miles Workman June 17 1 Economic Outlook Overview The New Zealand economy is forecast to expand at a solid pace over the next five years With real GDP growth around 3% in 17:

New Zealand Economic Outlook Miles Workman June 17 1 Economic Outlook Overview The New Zealand economy is forecast to expand at a solid pace over the next five years With real GDP growth around 3% in 17:

2017 Mid-Year Commercial Real Estate Outlook for Asia Pacific

2017 Mid-Year Commercial Real Estate Outlook for Asia Pacific REAL ASSETS REAL ESTATE INVESTING TEAM INVESTMENT INSIGHT 2017 The global macroeconomic landscape continues its shift away from highly accommodative

2017 Mid-Year Commercial Real Estate Outlook for Asia Pacific REAL ASSETS REAL ESTATE INVESTING TEAM INVESTMENT INSIGHT 2017 The global macroeconomic landscape continues its shift away from highly accommodative

5. Bulgarian National Bank Forecast of Key

5. Bulgarian National Bank Forecast of Key Macroeconomic Indicators for 2018 2020 The BNB forecast of key macroeconomic indicators is based on data published as of 15 June 2018. ECB, EC and IMF assumptions

5. Bulgarian National Bank Forecast of Key Macroeconomic Indicators for 2018 2020 The BNB forecast of key macroeconomic indicators is based on data published as of 15 June 2018. ECB, EC and IMF assumptions

Quarterly Economic Outlook: Quarter on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War

Foregin Direct Investment (Billion USD) China U.S. Asia World Quarterly Economic Outlook: Quarter 3 2018 on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War Thai Economy: Thai

Foregin Direct Investment (Billion USD) China U.S. Asia World Quarterly Economic Outlook: Quarter 3 2018 on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War Thai Economy: Thai

Short-term indicators and Updated Forecasts. Eurozone NOVEMBER 2016

Short-term indicators and Updated Forecasts Eurozone NOVEMBER 2016 EUROZONE WATCH NOVEMBER 2016 Key messages: resilience and unchanged projections The moderate pace of economic growth continued in the

Short-term indicators and Updated Forecasts Eurozone NOVEMBER 2016 EUROZONE WATCH NOVEMBER 2016 Key messages: resilience and unchanged projections The moderate pace of economic growth continued in the

Global Economic Outlook

Global Economic Outlook Will growth continue and at what pace? North American Conference San Francisco October 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary Information

Global Economic Outlook Will growth continue and at what pace? North American Conference San Francisco October 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary Information

Trade and Economic Trends Evolving Patterns and Attitudes

Trade and Economic Trends Evolving Patterns and Attitudes Paul Bingham AAPA Marine Terminal Management Training Program Long Beach California October 1, 2018 World Economic Growth Increasing Emerging Markets

Trade and Economic Trends Evolving Patterns and Attitudes Paul Bingham AAPA Marine Terminal Management Training Program Long Beach California October 1, 2018 World Economic Growth Increasing Emerging Markets

EY s Global Economic Outlook Ireland

EY s Global Economic Outlook Ireland January 2018 The global economy is healthy Mark Gregory Chief Economist, UK mgregory@uk.ey.com linkedin.com/in/markgregoryuk Neil Gibson Chief Economist, Ireland neil.gibson1@ie.ey.com

EY s Global Economic Outlook Ireland January 2018 The global economy is healthy Mark Gregory Chief Economist, UK mgregory@uk.ey.com linkedin.com/in/markgregoryuk Neil Gibson Chief Economist, Ireland neil.gibson1@ie.ey.com

June 2013 Equities Rally Drive Global Re-rating

June 2013 Equities Rally Drive Global Re-rating Since the lows of 2011, global equities have rallied 30% while Earnings per Share remained flat. This has been the biggest mid-cycle re-rating of global

June 2013 Equities Rally Drive Global Re-rating Since the lows of 2011, global equities have rallied 30% while Earnings per Share remained flat. This has been the biggest mid-cycle re-rating of global

Attractive fundamentals in the face of ongoing market volatility

Canada Outlook October 2018 Attractive fundamentals in the face of ongoing market volatility HSBC outlook Our growth outlook is tempered by concerns about politics, trade tensions and some emerging markets

Canada Outlook October 2018 Attractive fundamentals in the face of ongoing market volatility HSBC outlook Our growth outlook is tempered by concerns about politics, trade tensions and some emerging markets

2012 6 http://www.bochk.com 2 3 4 ECONOMIC REVIEW(A Monthly Issue) June, 2012 Economics & Strategic Planning Department http://www.bochk.com An Analysis on the Plunge in Hong Kong s GDP Growth and Prospects

2012 6 http://www.bochk.com 2 3 4 ECONOMIC REVIEW(A Monthly Issue) June, 2012 Economics & Strategic Planning Department http://www.bochk.com An Analysis on the Plunge in Hong Kong s GDP Growth and Prospects

No. 43/2018 Monetary Policy Report, June 2018 Mr. Jaturong Jantarangs, Assistant Governor of the Bank of Thailand (BOT) and Secretary of the Monetary

and Secretary of the Monetary") No. 43/2018 Monetary Policy Report, June 2018 Mr. Jaturong Jantarangs, Assistant Governor of the Bank of Thailand (BOT) and Secretary of the Monetary Policy Committee (MPC), released the June 2018 issue

No. 43/2018 Monetary Policy Report, June 2018 Mr. Jaturong Jantarangs, Assistant Governor of the Bank of Thailand (BOT) and Secretary of the Monetary Policy Committee (MPC), released the June 2018 issue

The Prospects Service

The Prospects Service LEADING ECONOMIC ANALYSIS, FORECASTS AND DATA Global Prospects, September 2017 Toplines The combination of rising consumer confidence, low borrowing costs and declining unemployment

The Prospects Service LEADING ECONOMIC ANALYSIS, FORECASTS AND DATA Global Prospects, September 2017 Toplines The combination of rising consumer confidence, low borrowing costs and declining unemployment

Global Economic Themes

Global Economic Themes Global economic activity has been strengthening since 2013 though the recovery is modest, labourious, (and) fragile according to the International Monetary Fund s (IMF) Managing

Global Economic Themes Global economic activity has been strengthening since 2013 though the recovery is modest, labourious, (and) fragile according to the International Monetary Fund s (IMF) Managing

Global PMI. Global economic growth kicks higher at start of fourth quarter but outlook darkens. November 14 th 2016

Global PMI Global economic growth kicks higher at start of fourth quarter but outlook darkens November 14 th 2016 2 Global PMI at 11-month high in October Global economic growth kicked higher at the start

Global PMI Global economic growth kicks higher at start of fourth quarter but outlook darkens November 14 th 2016 2 Global PMI at 11-month high in October Global economic growth kicked higher at the start

Quarterly Economic Monitor

Overview of Quarterly Economic Monitor December 214 Queenstown s economy boomed during 214, with ' provisional estimate of GDP showing that the Queenstown-Lakes District economy grew by 4.5% over the year

Overview of Quarterly Economic Monitor December 214 Queenstown s economy boomed during 214, with ' provisional estimate of GDP showing that the Queenstown-Lakes District economy grew by 4.5% over the year

Economic Outlook. Global And Finnish. Technology Industries In Finland Turnover and orders picking up s. 5. Economic Outlook

Economic Outlook Technology Industries of Finland 2 217 Global And Finnish Economic Outlook Broad-Based Global Economic Growth s. 3 Technology Industries In Finland Turnover and orders picking up s. 5

Economic Outlook Technology Industries of Finland 2 217 Global And Finnish Economic Outlook Broad-Based Global Economic Growth s. 3 Technology Industries In Finland Turnover and orders picking up s. 5

Macro Research Economic outlook

Macro Research Economic outlook Macroeconomic Research Itaú Unibanco April 2017 Roadmap Global Economy The global outlook remains favorable Global growth positive momentum continues, with a synchronized

Macro Research Economic outlook Macroeconomic Research Itaú Unibanco April 2017 Roadmap Global Economy The global outlook remains favorable Global growth positive momentum continues, with a synchronized

Ulster Bank Northern Ireland Purchasing Managers Index (PMI)

") Ulster Bank Northern Ireland Purchasing Managers Index (PMI) Includes analysis of Global, Eurozone, UK, UK Regions, NI & Republic of Ireland economic performance by sector February 2016 Survey Update Issued

Ulster Bank Northern Ireland Purchasing Managers Index (PMI) Includes analysis of Global, Eurozone, UK, UK Regions, NI & Republic of Ireland economic performance by sector February 2016 Survey Update Issued

November PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy November 2015 John Praveen, PhD Chief Investment Strategist FOR MORE INFORMATION CONTACT: Theresa Miller Phone:

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy November 2015 John Praveen, PhD Chief Investment Strategist FOR MORE INFORMATION CONTACT: Theresa Miller Phone:

Monthly Economic Review

Monthly Economic Review DECEMBER 2017 Based on November 2017 data releases Bedfordshire Chamber of Commerce Headlines UK GDP growth in Q3 unrevised as business investment and the UK s trade position weakens

Monthly Economic Review DECEMBER 2017 Based on November 2017 data releases Bedfordshire Chamber of Commerce Headlines UK GDP growth in Q3 unrevised as business investment and the UK s trade position weakens

Economic Outlook. William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago

Economic Outlook CRF Credit & A/R Forum & EXPO Salt Lake City, UT October 23, 218 William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago What I said In August The outlook

Economic Outlook CRF Credit & A/R Forum & EXPO Salt Lake City, UT October 23, 218 William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago What I said In August The outlook

BNM Maintains OPR at 3.25%, Hawkish About Economic Outlook

7 March 2018 ECONOMIC REVIEW March 2018 BNM MPC BNM Maintains OPR at 3.25%, Hawkish About Economic Outlook Overnight Policy Rate maintained at 3.25%. In line with our expectation, overnight policy rate,

7 March 2018 ECONOMIC REVIEW March 2018 BNM MPC BNM Maintains OPR at 3.25%, Hawkish About Economic Outlook Overnight Policy Rate maintained at 3.25%. In line with our expectation, overnight policy rate,

Monthly Economic Insight

Monthly Economic Insight Prepared by : TMB Analytics Date: 22 February 2018 Executive Summary Synchronized global economic growth continued to brighten global economic outlook and global trade outlook.

Monthly Economic Insight Prepared by : TMB Analytics Date: 22 February 2018 Executive Summary Synchronized global economic growth continued to brighten global economic outlook and global trade outlook.

Postponed recovery. The advanced economies posted a sluggish growth in CONJONCTURE IN FRANCE OCTOBER 2014 INSEE CONJONCTURE

INSEE CONJONCTURE CONJONCTURE IN FRANCE OCTOBER 2014 Postponed recovery The advanced economies posted a sluggish growth in Q2. While GDP rebounded in the United States and remained dynamic in the United

INSEE CONJONCTURE CONJONCTURE IN FRANCE OCTOBER 2014 Postponed recovery The advanced economies posted a sluggish growth in Q2. While GDP rebounded in the United States and remained dynamic in the United

Eurozone Economic Watch Higher growth forecasts for January 2018

Eurozone Economic Watch Higher growth forecasts for 2018-19 January 2018 Eurozone Economic Watch January 2018 Eurozone: Higher growth forecasts for 2018-19 Our MICA-BBVA model estimates a broadly stable

Eurozone Economic Watch Higher growth forecasts for 2018-19 January 2018 Eurozone Economic Watch January 2018 Eurozone: Higher growth forecasts for 2018-19 Our MICA-BBVA model estimates a broadly stable

Global Economic Outlook 2014 Year Ahead Outlook January 2014

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Economic Outlook 2014 Year Ahead Outlook January 2014 2014 Year Ahead - Global Economic Outlook Global Growth Strengthens as U.S. & U.K. GDP Growth

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Economic Outlook 2014 Year Ahead Outlook January 2014 2014 Year Ahead - Global Economic Outlook Global Growth Strengthens as U.S. & U.K. GDP Growth

Serious Doubts Remain despite Encouraging Signs

APRIL 18, 2019 ECONOMIC & FINANCIAL OUTLOOK Serious Doubts Remain despite Encouraging Signs #1 BEST OVERALL FORECASTER - CANADA HIGHLIGHTS ff The global economy and the volume of trade both remain fragile,

APRIL 18, 2019 ECONOMIC & FINANCIAL OUTLOOK Serious Doubts Remain despite Encouraging Signs #1 BEST OVERALL FORECASTER - CANADA HIGHLIGHTS ff The global economy and the volume of trade both remain fragile,

Latest Macroeconomic Projections - May Vice-Governor Anita Angelovska-Bezhoska

Latest Macroeconomic Projections - May 2018 - Vice-Governor Anita Angelovska-Bezhoska May, 4 2018 Contents Key assumptions on external and domestic environment Macroeconomic scenario 2018-2019 Comparison

Latest Macroeconomic Projections - May 2018 - Vice-Governor Anita Angelovska-Bezhoska May, 4 2018 Contents Key assumptions on external and domestic environment Macroeconomic scenario 2018-2019 Comparison

HKU announces 2015 Q2 HK Macroeconomic Forecast

Press Release HKU announces 2015 Q2 HK Macroeconomic Forecast April 9, 2015 1 Overview The APEC Studies Programme of the Hong Kong Institute of Economics and Business Strategy at the University of Hong

Press Release HKU announces 2015 Q2 HK Macroeconomic Forecast April 9, 2015 1 Overview The APEC Studies Programme of the Hong Kong Institute of Economics and Business Strategy at the University of Hong

Edited Minutes of the Monetary Policy Committee Meeting (No. 2/2018) 28 March 2018, Bank of Thailand Publication Date: 11 April 2018

28 March 2018, Bank of Thailand Publication Date: 11 April 2018") Edited Minutes of the Monetary Policy Committee Meeting (No. 2/2018) Members Present 28 March 2018, Bank of Thailand Publication Date: 11 April 2018 Veerathai Santiprabhob (Chairman), Mathee Supapongse

Edited Minutes of the Monetary Policy Committee Meeting (No. 2/2018) Members Present 28 March 2018, Bank of Thailand Publication Date: 11 April 2018 Veerathai Santiprabhob (Chairman), Mathee Supapongse

April 2016 Market Commentary

April 2016 Market Commentary Domestic equity indices finished the month mixed, while international developed markets ended higher. The falling U.S. dollar continued to reverberate across markets, especially

April 2016 Market Commentary Domestic equity indices finished the month mixed, while international developed markets ended higher. The falling U.S. dollar continued to reverberate across markets, especially

Monetary Policy Report, June 2017

No. 32/2017 Monetary Policy Report, June 2017 Mr. Jaturong Jantarangs, Assistant Governor of the Bank of Thailand (BOT) and Secretary of the Monetary Policy Committee (MPC), released the June 2017 issue

No. 32/2017 Monetary Policy Report, June 2017 Mr. Jaturong Jantarangs, Assistant Governor of the Bank of Thailand (BOT) and Secretary of the Monetary Policy Committee (MPC), released the June 2017 issue

Today s discussion. Traveler..domestic and international spending, origin, purpose and activities. Lodging data. Regional research

November 29, 2012 Today s discussion. Traveler..domestic and international spending, origin, purpose and activities Lodging data Regional research Massachusett's Travel and Tourism Top Line Numbers Direct

November 29, 2012 Today s discussion. Traveler..domestic and international spending, origin, purpose and activities Lodging data Regional research Massachusett's Travel and Tourism Top Line Numbers Direct

Developing Asia: robust growth prevails. Economics and Research Department Asian Development Bank

Developing Asia: robust growth prevails Economics and Research Department Asian Development Bank Preview Prospects for world economy in 2006-2007: positive but risks remain Developing Asia in 2006-2007:

Developing Asia: robust growth prevails Economics and Research Department Asian Development Bank Preview Prospects for world economy in 2006-2007: positive but risks remain Developing Asia in 2006-2007: