Financial'Market'Analysis'(FMAx) Module'1

|

|

|

- Adela Robinson

- 5 years ago

- Views:

Transcription

and is intended for use in IMF Institute for Capacity Development (ICD) courses.")

1 Financial'Market'Analysis'(FMAx) Module'1 Pricing Money Market Instruments This training material is the property of the International Monetary Fund (IMF) and is intended for use in IMF Institute for Capacity Development (ICD) courses. Any reuse requires the permission of the ICD.

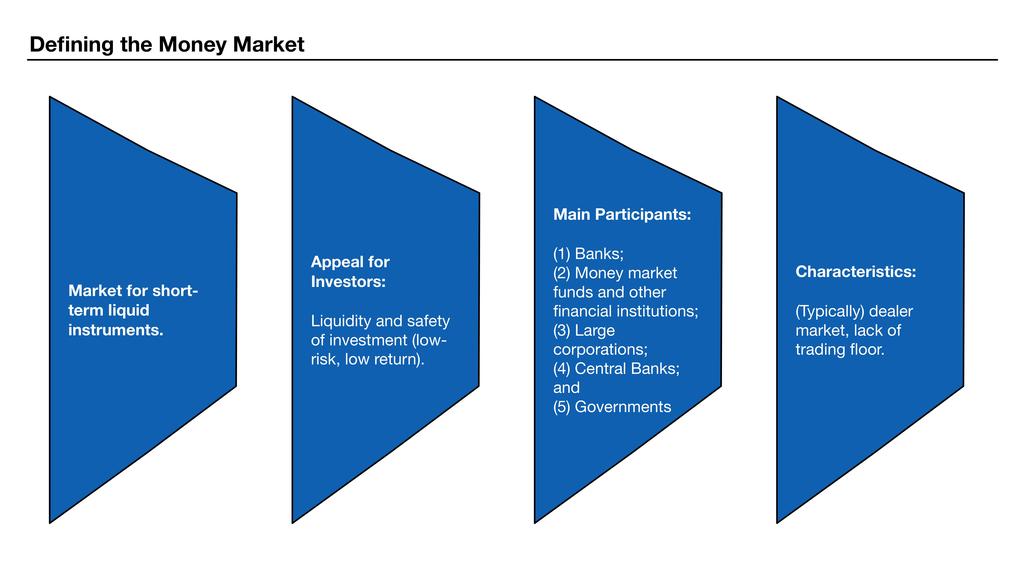

2 Preamble: At'the'end'of'this'module'you'will'be'able'to:! Describe the money market and its relation with the capital market! Explain the nature and use of key money market instruments! Apply fundamental principles of financial mathematics! Calculate the price and return of money market instruments

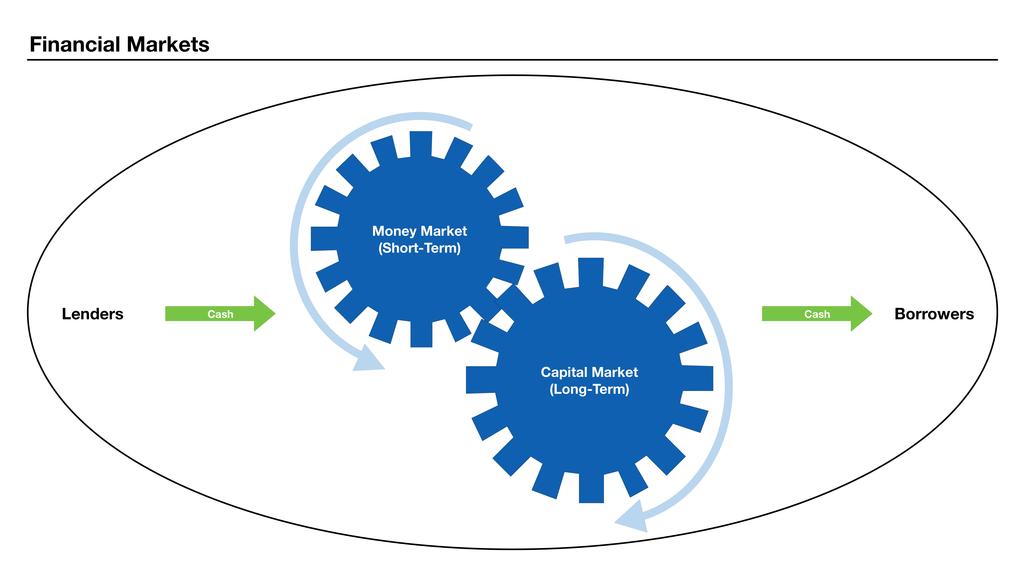

3 The'Relevance'to'You You might be! An investor! A central banker: the first link in monetary policy transmission! A public debt manager or a company treasurer! Source of short-term funding! Facilitates liquidity management! A financial supervisor! Links banks with other financial institutions! Entails a channel for the propagation of financial shocks

4

5

6

7

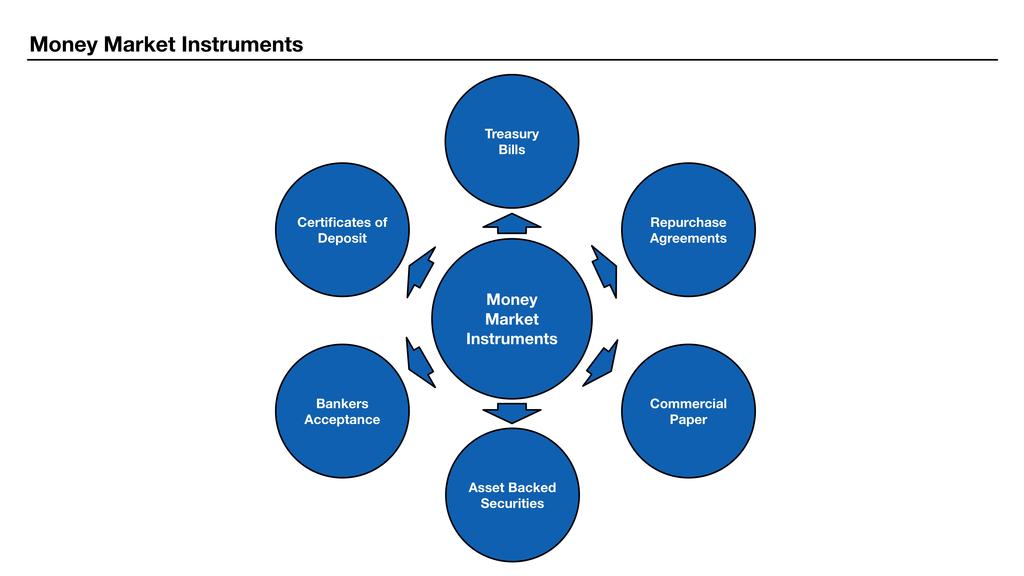

8 Treasury'Bills! Government debt with maturity lower than one-year! Typical maturities: 90 days, 181 days, 360 days! Typical denominations: $1,000 to $1 million! No coupons! The most marketable money market instrument

9

10 Certificates'of'Deposit'(CDs) Characteristics include:! Time deposit with a bank! But traded in secondary markets! Issued in any denomination! Typical maturities 3-month to 5 years! Covered by deposit insurance up to a certain amount

11

12

13

14

15

16 Key'Types'of'Fixed'Income'Securities Coupon Bonds Zero Coupon Bonds (zeros) C C C C C C+M T-1 T T-1 T M time time Annuities and Perpetuities (consols) C C C C C time

17 Pricing'a'FixedJIncome'Security By discounting their future cash flows back to the present! The price of the security is the PV of its cash flows! Need a discount rate: the return required by the market (i.e., investors) = yield! In the case of a T-year zero coupon bond: P = M (1 + y) T

18 Coupon'Bonds'as'Portfolios'of'Zeros Coupon bonds can be interpreted as a portfolio of zeros. A simple illustration: P C C+M time P 1 0 P 2 C 1 C+M time Claim: P = P 1 + P time

19 A'Fundamental'Pricing'Principle: No'Arbitrage'Condition The Law of One Price (LOP): (Identical assets should have the same price) Identical in terms of! Cash flows! Risk / Inflation / Uncertainty If prices differ, then there would be arbitrage opportunities! Possibility to make unlimited riskless profits by buying the lower-priced asset and selling the higher-priced one

20 No'Arbitrage'Condition:'Intuition Suppose two identical securities S 1 and S 2 have different yields. Say: y 1 > y 2 Investors try to purchase S 1 and sell S 2 Then P 1 increases and P 2 drops Consequently, y 1 would fall and y 2 would increase! This process will continue until y 1 = y 2, P 1 = P 2 Market equilibrium is restored and there are no more arbitrage opportunities

21 The'Coupon'Rate'and'Bond'Yield The coupon dictates the periodic cash flows according to bond contract.! Example: 7% coupon, paid semi-annually! If face value is 100, $3.5 paid two times per year The yield is the market interest rate used to discount the periodic flows. The coupon and yield are usually different.! The yield is the market rate, which varies continuously! The coupon rate is (generally) fixed Secondary market price depends on both the coupon, face value, and market interest rate (yield).

22 Alternative'Yield'Definitions Coupon Rate: Sum of coupons paid in a year in percent of par (face) value CouponRate = SumCouponsInYear ParValue Current Yield: Sum of coupons paid in a year in percent of bond (market) price CurrYield = SumCouponsInYear BondPrice Yield-to-Maturity (YTM): Internal rate of return of investing in the bond

23 An'Example: Yields Compare the coupon rate, the current yield and the yield to maturity of a one-year $100 security that pays 5% semi-annual coupons and was purchased for $95 on the issue date. 5% 100 CouponRate = = 5% 100 CurrYield 5% 100 = = 5.26% 95 YTM = YTM 10.4% 2 " y # + 1 " y # = $ + % 1+ & 2 ' $ % & 2 '

24 Day'Count'Conventions Pricing in financial markets started long before computers! People in different countries took different strategies to ease the calculation of accrued interests over time! Example: 30 days per month and 360 days per year (30/360 day count methods) Different markets price the same security differently...! Need to be aware of conventions in different markets to compare prices

25 Useful'Day'Count'Conventions Day'Count Description Excel'Code 30/360 The)number)of)days)between)two)dates)assuming)that) months)have)30)days)and)years)have)360)days 0)(or)omitted)) for)us) NASD 4)for)European Actual/Actual The)actual)number)of)days)between)two)dates 1 Actual/360 Number)of)days)in)year)fixed)to)360 2 Actual/365 Number)of)days)in)year)fixed)to)365 3

26 An'Example: Changing'the'Base'of'the'Yield How to convert ACT/360 rate y into ACT/365 rate y*? y* = y Suppose yield y on ACT/360 is 10.5%. What is the equivalent yield y* on ACT/365? 365 y * = = = 10.64% 360

27 Pricing'Money'Market'Instruments Price equals the present value of future cash flows! This principle applies to all instruments! Money market instruments have maturity in less that one year Use simple interest! Money market is linked to other markets through the principle of no arbitrage

28 Alternative'Ways'to'Quote'Prices: Yield'and'Discount Two alternatives to express the return of fixed income securities:! Using the yield (y) or discount (d) Depending on the jurisdiction, prices are quoted as one or the other! Example: Take a zero with price P and face value M P = 1! days " $ 1+ y % & 365 ' M! days " P= % 1 d & M ' 365 (

29 An'Example: Yield'and'Discount' 1 You pay $80 for a $100 zero that matures in one year. Compute the yield and the discount. 20 Yield = = 0.25 = 25% Discount = = 0.20 = 20% 100

30 Comparing'Yield'and'Discount: Zero'Coupon'Bonds Take: Alternatively: 1 P = M days (1 + y ) days (1 + y ) days 365 P= (1 d ) M 365 days = (1 d ) 365 Thus: d = y days (1 + y ) 365 y > y d = d days (1 d ) 365

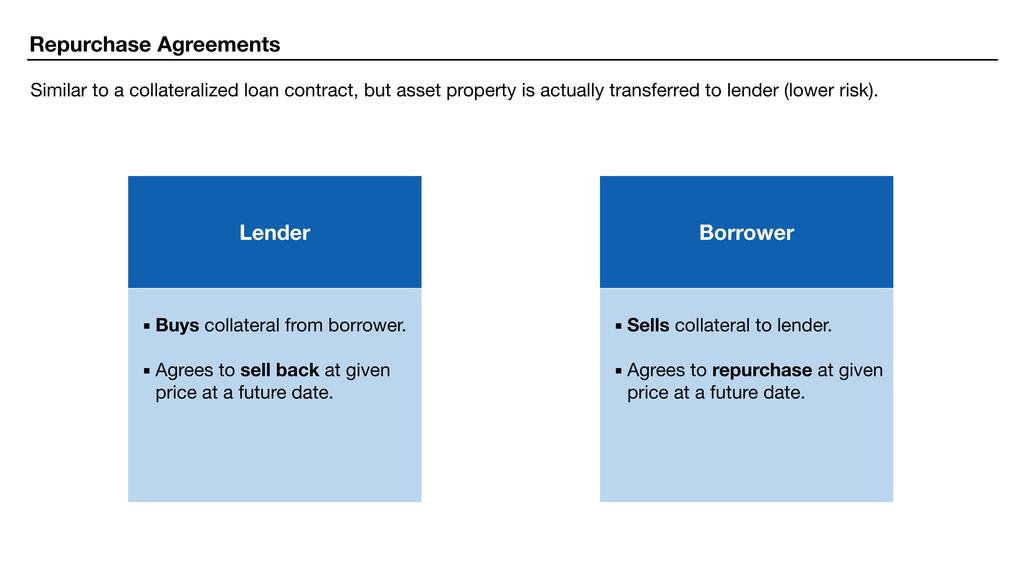

31 Instruments'Quoted'on'a'Discount'Basis USA U.K.! T-bills! Bankers acceptances! Commercial paper! T-bills (in pounds; in Euros quoted on yield basis)! Bankers acceptances

32 An'Example: Yield'and'Discount' 2 Some Questions: What is the 180-day discount factor of 7 percent per year? 1 = ! 180 " $ % & 365 ' What is the price of a $ day zerocoupon bond if the yield is 7 percent? $500 = $483 What is the discount rate on the face value of the bond?! 180 " % 1 d & = ' 365 ( d = = 6.77%

33 Pricing'Discount'U.S.'TJBills Price (per $100 face value): P! days " = % 1 d & 100 ' 360 ( Yield: y! FV " = % 1& ' P ( 365 days Effective yield: EAR 365 days! days " = $ 1+ y % 1 & 365 '

34 How'to'Read'U.S.'TJBill'Quotes US Treasury Bills (Quoted on Discount Basis) as of January 19, 2016 Maturity BID ASK CHANGE YIELD 11/10/ ) * 1/ Treasury bill bid and ask data are representative over-the-counter quotations as of 3pm Eastern time quoted as a discount to face value. Treasury bill yields are to maturity and based on the asked quote. US T-bills are quoted on a discount basis (reference price is face value). Days to maturity BID: discount rate offered by buyers. ASK: discount rate offered by sellers. CHANGE: the difference in bid discounts from the previous day. YIELD: the annualized yield using the ask rate.

35 An'Example: Yields'on'a'US'TJBill Compute the price and yield of the following US T-bill. US Treasury Bills (Quoted on Discount Basis) as of January 19, 2016 Maturity BID ASK CHANGE YIELD 11/10/ ) * 1/ Treasury bill bid and ask data are representative over-the-counter quotations as of 3pm Eastern time quoted as a discount to face value. Treasury bill yields are to maturity and based on the asked quote. Days to maturity: Jan 19 to Nov 10=296 P! days " 296 = % 1 d & 100 = ( ) 100 = $99.70 ' 360 ( 360 y " # 365 = % & = 0.37% ' ( 296

36 An'Example: Pricing'Certificates'of'Deposit' 1 A 90-day CD with $100,000 face value was issued on March 17, 2015, offering a 6 percent coupon (under ACT/360 day convention) with a market yield of 7 percent. a) Compute the payoff (Final Value) b) Compute the price of the CD on March 17, 2015 c) On April 10, 2015, the market yield dropped to 5.5 percent. Compute the price of the CD in the secondary market d) On May 10, the market rate further dropped to 5 percent. Compute the return of an investor that purchased the CD on April 10 and sold it on May 10 (30 days)

37 An'Example: Pricing'Certificates'of'Deposit' 2 a) Compute the payoff. FV & 90 # = 100,000$ 1+.06! = 101,500 % 360 " b) Compute the price of the CD on March 17. P = 101,500 99, 754! 90 " = $ % & 360 ' c) On April 10, 2015, the market rate dropped to 5.5 percent. Compute the price of the CD in the secondary market. P = 101, , 487! 66 " = $ % & 360 '

38 An'Example: Pricing'Certificates'of'Deposit' 3 d) On May 10, the market rate further dropped to 5 percent. Compute the return of an investor that purchased the CD on April 10 and sold it on May 10 (30 days). P 101,500 (April 10) = 100, 487! 66 " = $ % & 360 ' P 101,500 (May 10) = 100,995! 36 " = $ % & 360 '! 100,995 " 360 Return = % 1 = 6.07% 100, 487 & ' ( 30

39 Repurchase'Agreements Recall the way these work! One party sells a security to a second party, while agreeing to buy it back at a set date at a set price! Equivalent to first party borrowing with security acting as collateral! Term typically short! Overnight repo one day maturity! Term repo maturity longer than 30 days! Interest rate (repo rate) implied by prices

40 An'Example: Pricing'Repurchase'Agreements a) Mybank sells 9,876,000 worth of T-bills and agrees to repurchase them in 14 days at 9,895,000. What is the repo rate?! 9,895, 000 " 365 y= % 1 = 5.02% 9,876, 000 & ' ( 14 b) If the overnight repo rate is 4.5% what is the payment tomorrow for a repo of $10,000,000?! 1 " 10, 000, 000 $ % = 10, 001, & 365 '

41 Module'WrapJUp 1 In this module we covered:! The money market and its role in the financial system! The main types of money market instruments! How to price and compute returns on money market instruments Key concepts to remember! Security Price = Present value of future payments computed at market yields! Market equilibrium = No arbitrage

42 Module'WrapJUp' 2 Future value with intra-year compounding: FV " i # = PV $ 1+ % & n ' n t Present value: PV = T t= CFt 1 (1 + i) t PV! 1 1 " = CF % i i (1 1) T & ' + ( Simple interests and discounts (apply to money market instruments): 1 PV = FV! days "! days " PV = % 1 d & FV $ 1+ y % ' 365 ( & 365 '

Financial Market Analysis (FMAx) Module 1

Module 1") Financial Market Analysis (FMAx) Module 1 Pricing Money Market Instruments This training material is the property of the International Monetary Fund (IMF) and is intended for use in IMF Institute for Capacity

Financial Market Analysis (FMAx) Module 1 Pricing Money Market Instruments This training material is the property of the International Monetary Fund (IMF) and is intended for use in IMF Institute for Capacity

Financial Market Analysis (FMAx) Module 2

Module 2") Financial Market Analysis (FMAx) Module 2 Bond Pricing This training material is the property of the International Monetary Fund (IMF) and is intended for use in IMF Institute for Capacity Development

Financial Market Analysis (FMAx) Module 2 Bond Pricing This training material is the property of the International Monetary Fund (IMF) and is intended for use in IMF Institute for Capacity Development

Chapter. Bond Basics, I. Prices and Yields. Bond Basics, II. Straight Bond Prices and Yield to Maturity. The Bond Pricing Formula

Chapter 10 Bond Prices and Yields Bond Basics, I. A Straight bond is an IOU that obligates the issuer of the bond to pay the holder of the bond: A fixed sum of money (called the principal, par value, or

Chapter 10 Bond Prices and Yields Bond Basics, I. A Straight bond is an IOU that obligates the issuer of the bond to pay the holder of the bond: A fixed sum of money (called the principal, par value, or

FINA 1082 Financial Management

FINA 1082 Financial Management Dr Cesario MATEUS Senior Lecturer in Finance and Banking Room QA259 Department of Accounting and Finance c.mateus@greenwich.ac.uk www.cesariomateus.com Contents Session 1

FINA 1082 Financial Management Dr Cesario MATEUS Senior Lecturer in Finance and Banking Room QA259 Department of Accounting and Finance c.mateus@greenwich.ac.uk www.cesariomateus.com Contents Session 1

Financial Market Introduction

Financial Market Introduction Alex Yang FinPricing http://www.finpricing.com Summary Financial Market Definition Financial Return Price Determination No Arbitrage and Risk Neutral Measure Fixed Income

Financial Market Introduction Alex Yang FinPricing http://www.finpricing.com Summary Financial Market Definition Financial Return Price Determination No Arbitrage and Risk Neutral Measure Fixed Income

ACI THE FINANCIAL MARKETS ASSOCIATION

ACI THE FINANCIAL MARKETS ASSOCIATION EXAMINATION FORMULAE page number INTEREST RATE..2 MONEY MARKET..... 3 FORWARD-FORWARDS & FORWARD RATE AGREEMENTS..4 FIXED INCOME.....5 FOREIGN EXCHANGE 7 OPTIONS 8

ACI THE FINANCIAL MARKETS ASSOCIATION EXAMINATION FORMULAE page number INTEREST RATE..2 MONEY MARKET..... 3 FORWARD-FORWARDS & FORWARD RATE AGREEMENTS..4 FIXED INCOME.....5 FOREIGN EXCHANGE 7 OPTIONS 8

Financial Market Analysis (FMAx) Module 3

Module 3") Financial Market Analysis (FMAx) Module 3 Bond Price Sensitivity This training material is the property of the International Monetary Fund (IMF) and is intended for use in IMF Institute for Capacity Development

Financial Market Analysis (FMAx) Module 3 Bond Price Sensitivity This training material is the property of the International Monetary Fund (IMF) and is intended for use in IMF Institute for Capacity Development

Understanding Interest Rates

Money & Banking Notes Chapter 4 Understanding Interest Rates Measuring Interest Rates Present Value (PV): A dollar paid to you one year from now is less valuable than a dollar paid to you today. Why? -

Money & Banking Notes Chapter 4 Understanding Interest Rates Measuring Interest Rates Present Value (PV): A dollar paid to you one year from now is less valuable than a dollar paid to you today. Why? -

Economics 173A and Management 183 Financial Markets

Economics 173A and Management 183 Financial Markets Fixed Income Securities: Bonds Bonds Debt Security corporate or government borrowing Also called a Fixed Income Security Covenants or Indenture define

Economics 173A and Management 183 Financial Markets Fixed Income Securities: Bonds Bonds Debt Security corporate or government borrowing Also called a Fixed Income Security Covenants or Indenture define

Financial Market Analysis (FMAx) Module 3

Module 3") Financial Market Analysis (FMAx) Module 3 Bond Price Sensitivity This training material is the property of the International Monetary Fund (IMF) and is intended for use in IMF Institute for Capacity Development

Financial Market Analysis (FMAx) Module 3 Bond Price Sensitivity This training material is the property of the International Monetary Fund (IMF) and is intended for use in IMF Institute for Capacity Development

KNGX NOTES FINS1613 [FINS1613] Comprehensive Notes

![KNGX NOTES FINS1613 [FINS1613] Comprehensive Notes](/thumbs/89/99612905.jpg "KNGX NOTES FINS1613 [FINS1613] Comprehensive Notes") 1 [] Comprehensive Notes 1 2 TABLE OF CONTENTS Table of Contents... 2 1. Introduction & Time Value of Money... 3 2. Net Present Value & Interest Rates... 8 3. Valuation of Securities I... 19 4. Valuation

1 [] Comprehensive Notes 1 2 TABLE OF CONTENTS Table of Contents... 2 1. Introduction & Time Value of Money... 3 2. Net Present Value & Interest Rates... 8 3. Valuation of Securities I... 19 4. Valuation

I. Introduction to Bonds

University of California, Merced ECO 163-Economics of Investments Chapter 10 Lecture otes I. Introduction to Bonds Professor Jason Lee A. Definitions Definition: A bond obligates the issuer to make specified

University of California, Merced ECO 163-Economics of Investments Chapter 10 Lecture otes I. Introduction to Bonds Professor Jason Lee A. Definitions Definition: A bond obligates the issuer to make specified

CHAPTER 14. Bond Prices and Yields INVESTMENTS BODIE, KANE, MARCUS. Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved.

CHAPTER 14 Bond Prices and Yields McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 14-2 Bond Characteristics Bonds are debt. Issuers are borrowers and holders are

CHAPTER 14 Bond Prices and Yields McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 14-2 Bond Characteristics Bonds are debt. Issuers are borrowers and holders are

ACI DEALING CERTIFICATE

s@lm@n ACI Exam 3I0-008 ACI DEALING CERTIFICATE Version: 5.0 [ Total Questions: 320 ] Topic 0, D D ACI 3I0-008 : Practice Test Question No : 1 - (Topic 0) Click on the Exhibit Button to view the Formula

s@lm@n ACI Exam 3I0-008 ACI DEALING CERTIFICATE Version: 5.0 [ Total Questions: 320 ] Topic 0, D D ACI 3I0-008 : Practice Test Question No : 1 - (Topic 0) Click on the Exhibit Button to view the Formula

Chapter 10: Futures Arbitrage Strategies

Chapter 10: Futures Arbitrage Strategies I. Short-Term Interest Rate Arbitrage 1. Cash and Carry/Implied Repo Cash and carry transaction means to buy asset and sell futures Use repurchase agreement/repo

Chapter 10: Futures Arbitrage Strategies I. Short-Term Interest Rate Arbitrage 1. Cash and Carry/Implied Repo Cash and carry transaction means to buy asset and sell futures Use repurchase agreement/repo

I. Warnings for annuities and

Outline I. More on the use of the financial calculator and warnings II. Dealing with periods other than years III. Understanding interest rate quotes and conversions IV. Applications mortgages, etc. 0

Outline I. More on the use of the financial calculator and warnings II. Dealing with periods other than years III. Understanding interest rate quotes and conversions IV. Applications mortgages, etc. 0

CHAPTER 14. Bond Characteristics. Bonds are debt. Issuers are borrowers and holders are creditors.

Bond Characteristics 14-2 CHAPTER 14 Bond Prices and Yields Bonds are debt. Issuers are borrowers and holders are creditors. The indenture is the contract between the issuer and the bondholder. The indenture

Bond Characteristics 14-2 CHAPTER 14 Bond Prices and Yields Bonds are debt. Issuers are borrowers and holders are creditors. The indenture is the contract between the issuer and the bondholder. The indenture

Practice Test Questions. Exam FM: Financial Mathematics Society of Actuaries. Created By: Digital Actuarial Resources

Practice Test Questions Exam FM: Financial Mathematics Society of Actuaries Created By: (Sample Only Purchase the Full Version) Introduction: This guide from (DAR) contains sample test problems for Exam

Practice Test Questions Exam FM: Financial Mathematics Society of Actuaries Created By: (Sample Only Purchase the Full Version) Introduction: This guide from (DAR) contains sample test problems for Exam

Chapter 7. Interest Rate Forwards and Futures. Copyright 2009 Pearson Prentice Hall. All rights reserved.

Chapter 7 Interest Rate Forwards and Futures Bond Basics U.S. Treasury Bills (

Chapter 7 Interest Rate Forwards and Futures Bond Basics U.S. Treasury Bills (

Understanding Interest Rates

Understanding Interest Rates Leigh Tesfatsion (Iowa State University) Notes on Mishkin Chapter 4: Part A (pp. 68-80) Last Revised: 14 February 2011 Mishkin Chapter 4: Part A -- Selected Key In-Class Discussion

Understanding Interest Rates Leigh Tesfatsion (Iowa State University) Notes on Mishkin Chapter 4: Part A (pp. 68-80) Last Revised: 14 February 2011 Mishkin Chapter 4: Part A -- Selected Key In-Class Discussion

Fixed Income Securities: Bonds

Economics 173A and Management 183 Financial Markets Fixed Income Securities: Bonds Updated 4/24/17 Bonds Debt Security corporate or government borrowing Also called a Fixed Income Security Covenants or

Economics 173A and Management 183 Financial Markets Fixed Income Securities: Bonds Updated 4/24/17 Bonds Debt Security corporate or government borrowing Also called a Fixed Income Security Covenants or

4. Understanding.. Interest Rates. Copyright 2007 Pearson Addison-Wesley. All rights reserved. 4-1

4. Understanding. Interest Rates Copyright 2007 Pearson Addison-Wesley. All rights reserved. 4-1 Present Value A dollar paid to you one year from now is less valuable than a dollar paid to you today Copyright

4. Understanding. Interest Rates Copyright 2007 Pearson Addison-Wesley. All rights reserved. 4-1 Present Value A dollar paid to you one year from now is less valuable than a dollar paid to you today Copyright

CHAPTER 8. Valuing Bonds. Chapter Synopsis

CHAPTER 8 Valuing Bonds Chapter Synopsis 8.1 Bond Cash Flows, Prices, and Yields A bond is a security sold at face value (FV), usually $1,000, to investors by governments and corporations. Bonds generally

CHAPTER 8 Valuing Bonds Chapter Synopsis 8.1 Bond Cash Flows, Prices, and Yields A bond is a security sold at face value (FV), usually $1,000, to investors by governments and corporations. Bonds generally

Global Financial Management

Global Financial Management Bond Valuation Copyright 24. All Worldwide Rights Reserved. See Credits for permissions. Latest Revision: August 23, 24. Bonds Bonds are securities that establish a creditor

Global Financial Management Bond Valuation Copyright 24. All Worldwide Rights Reserved. See Credits for permissions. Latest Revision: August 23, 24. Bonds Bonds are securities that establish a creditor

Bond Market Development in Emerging East Asia

Bond Market Development in Emerging East Asia Fixed Income Valuation Russ Jason Lo AsianBondsOnline Consultant Valuation of an Asset There are many different ways of valuing an asset. In finance, the gold

Bond Market Development in Emerging East Asia Fixed Income Valuation Russ Jason Lo AsianBondsOnline Consultant Valuation of an Asset There are many different ways of valuing an asset. In finance, the gold

Future Value of Multiple Cash Flows

Future Value of Multiple Cash Flows FV t CF 0 t t r CF r... CF t You open a bank account today with $500. You expect to deposit $,000 at the end of each of the next three years. Interest rates are 5%,

Future Value of Multiple Cash Flows FV t CF 0 t t r CF r... CF t You open a bank account today with $500. You expect to deposit $,000 at the end of each of the next three years. Interest rates are 5%,

Debt underwriting and bonds

Debt underwriting and bonds 1 A bond is an instrument issued for a period of more than one year with the purpose of raising capital by borrowing Debt underwriting includes the underwriting of: Government

Debt underwriting and bonds 1 A bond is an instrument issued for a period of more than one year with the purpose of raising capital by borrowing Debt underwriting includes the underwriting of: Government

Bond Valuation. Capital Budgeting and Corporate Objectives

Bond Valuation Capital Budgeting and Corporate Objectives Professor Ron Kaniel Simon School of Business University of Rochester 1 Bond Valuation An Overview Introduction to bonds and bond markets» What

Bond Valuation Capital Budgeting and Corporate Objectives Professor Ron Kaniel Simon School of Business University of Rochester 1 Bond Valuation An Overview Introduction to bonds and bond markets» What

Review Class Handout Corporate Finance, Sections 001 and 002

. Problem Set, Q 3 Review Class Handout Corporate Finance, Sections 00 and 002 Suppose you are given a choice of the following two securities: (a) an annuity that pays $0,000 at the end of each of the

. Problem Set, Q 3 Review Class Handout Corporate Finance, Sections 00 and 002 Suppose you are given a choice of the following two securities: (a) an annuity that pays $0,000 at the end of each of the

MBAX Credit Default Swaps (CDS)

") MBAX-6270 Credit Default Swaps Credit Default Swaps (CDS) CDS is a form of insurance against a firm defaulting on the bonds they issued CDS are used also as a way to express a bearish view on a company

MBAX-6270 Credit Default Swaps Credit Default Swaps (CDS) CDS is a form of insurance against a firm defaulting on the bonds they issued CDS are used also as a way to express a bearish view on a company

Lecture Notes 18: Review Sample Multiple Choice Problems

Lecture Notes 18: Review Sample Multiple Choice Problems 1. Assuming true-model returns are identically independently distributed (i.i.d), which events violate market efficiency? I. Positive correlation

Lecture Notes 18: Review Sample Multiple Choice Problems 1. Assuming true-model returns are identically independently distributed (i.i.d), which events violate market efficiency? I. Positive correlation

Lecture 4. The Bond Market. Mingzhu Wang SKKU ISS 2017

Lecture 4 The Bond Market Mingzhu Wang SKKU ISS 2017 Bond Terminologies 2 Agenda Types of Bonds 1. Treasury Notes and Bonds 2. Municipal Bonds 3. Corporate Bonds Financial Guarantees for Bonds Current

Lecture 4 The Bond Market Mingzhu Wang SKKU ISS 2017 Bond Terminologies 2 Agenda Types of Bonds 1. Treasury Notes and Bonds 2. Municipal Bonds 3. Corporate Bonds Financial Guarantees for Bonds Current

Bond Market Development in Myanmar

Bond Market Development in Myanmar Workshop on Bond Market Development in Emerging East Asia Sule Shangri - La Yangon, Myanmar August 11, 2017 Presented by Nwe Ni Tun Director Financial Market Department

Bond Market Development in Myanmar Workshop on Bond Market Development in Emerging East Asia Sule Shangri - La Yangon, Myanmar August 11, 2017 Presented by Nwe Ni Tun Director Financial Market Department

Lecture 7 Foundations of Finance

Lecture 7: Fixed Income Markets. I. Reading. II. Money Market. III. Long Term Credit Markets. IV. Repurchase Agreements (Repos). 0 Lecture 7: Fixed Income Markets. I. Reading. A. BKM, Chapter 2, Sections

Lecture 7: Fixed Income Markets. I. Reading. II. Money Market. III. Long Term Credit Markets. IV. Repurchase Agreements (Repos). 0 Lecture 7: Fixed Income Markets. I. Reading. A. BKM, Chapter 2, Sections

KEY CONCEPTS AND SKILLS

Chapter 5 INTEREST RATES AND BOND VALUATION 5-1 KEY CONCEPTS AND SKILLS Know the important bond features and bond types Comprehend bond values (prices) and why they fluctuate Compute bond values and fluctuations

Chapter 5 INTEREST RATES AND BOND VALUATION 5-1 KEY CONCEPTS AND SKILLS Know the important bond features and bond types Comprehend bond values (prices) and why they fluctuate Compute bond values and fluctuations

Chapter 6 : Money Markets

1 Chapter 6 : Money Markets Chapter Objectives Provide a background on money market securities Explain how institutional investors use money markets Explain the globalization of money markets 2 Why so

1 Chapter 6 : Money Markets Chapter Objectives Provide a background on money market securities Explain how institutional investors use money markets Explain the globalization of money markets 2 Why so

Efficacy of Interest Rate Futures for Corporate

Efficacy of Interest Rate Futures for Corporate The financial sector, corporate and even households are affected by interest rate risk. Interest rate fluctuations impact portfolios of banks, insurance

Efficacy of Interest Rate Futures for Corporate The financial sector, corporate and even households are affected by interest rate risk. Interest rate fluctuations impact portfolios of banks, insurance

Fixed income security. Face or par value Coupon rate. Indenture. The issuer makes specified payments to the bond. bondholder

Bond Prices and Yields Bond Characteristics Fixed income security An arragement between borrower and purchaser The issuer makes specified payments to the bond holder on specified dates Face or par value

Bond Prices and Yields Bond Characteristics Fixed income security An arragement between borrower and purchaser The issuer makes specified payments to the bond holder on specified dates Face or par value

Bond Prices and Yields

Bond Prices and Yields BKM 10.1-10.4 Eric M. Aldrich Econ 133 UC Santa Cruz Bond Basics A bond is a financial asset used to facilitate borrowing and lending. A borrower has an obligation to make pre-specified

Bond Prices and Yields BKM 10.1-10.4 Eric M. Aldrich Econ 133 UC Santa Cruz Bond Basics A bond is a financial asset used to facilitate borrowing and lending. A borrower has an obligation to make pre-specified

Interest Rates & Credit Derivatives

Interest Rates & Credit Derivatives Ashish Ghiya Derivium Tradition (India) 25/06/14 1 Agenda Introduction to Interest Rate & Credit Derivatives Practical Uses of Derivatives Derivatives Going Wrong Practical

Interest Rates & Credit Derivatives Ashish Ghiya Derivium Tradition (India) 25/06/14 1 Agenda Introduction to Interest Rate & Credit Derivatives Practical Uses of Derivatives Derivatives Going Wrong Practical

E-120: Principles of Engineering Economics. Midterm Exam I Feb 28, 2007

E-120: Principles of Engineering Economics Midterm Exam I Feb 28, 2007 Name: (please print) SID: Clearly state all the formula and mathematical expressions that are needed to solve the problems. No credit

E-120: Principles of Engineering Economics Midterm Exam I Feb 28, 2007 Name: (please print) SID: Clearly state all the formula and mathematical expressions that are needed to solve the problems. No credit

6. Pricing deterministic payoffs

Some of the content of these slides is based on material from the book Introduction to the Economics and Mathematics of Financial Markets by Jaksa Cvitanic and Fernando Zapatero. Pricing Options with Mathematical

Some of the content of these slides is based on material from the book Introduction to the Economics and Mathematics of Financial Markets by Jaksa Cvitanic and Fernando Zapatero. Pricing Options with Mathematical

UNIVERSITY OF TORONTO Joseph L. Rotman School of Management SOLUTIONS. C (1 + r 2. 1 (1 + r. PV = C r. we have that C = PV r = $40,000(0.10) = $4,000.

= $4,000.") UNIVERSITY OF TORONTO Joseph L. Rotman School of Management RSM332 PROBLEM SET #2 SOLUTIONS 1. (a) The present value of a single cash flow: PV = C (1 + r 2 $60,000 = = $25,474.86. )2T (1.055) 16 (b) The

UNIVERSITY OF TORONTO Joseph L. Rotman School of Management RSM332 PROBLEM SET #2 SOLUTIONS 1. (a) The present value of a single cash flow: PV = C (1 + r 2 $60,000 = = $25,474.86. )2T (1.055) 16 (b) The

Chapter 5. Interest Rates and Bond Valuation. types. they fluctuate. relationship to bond terms and value. interest rates

Chapter 5 Interest Rates and Bond Valuation } Know the important bond features and bond types } Compute bond values and comprehend why they fluctuate } Appreciate bond ratings, their meaning, and relationship

Chapter 5 Interest Rates and Bond Valuation } Know the important bond features and bond types } Compute bond values and comprehend why they fluctuate } Appreciate bond ratings, their meaning, and relationship

CHAPTER 14. Bond Prices and Yields INVESTMENTS BODIE, KANE, MARCUS. Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved.

CHAPTER 14 Bond Prices and Yields INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. INVESTMENTS BODIE, KANE, MARCUS 14-2 Bond Characteristics

CHAPTER 14 Bond Prices and Yields INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. INVESTMENTS BODIE, KANE, MARCUS 14-2 Bond Characteristics

Markets: Fixed Income

Markets: Fixed Income Mark Hendricks Autumn 2017 FINM Intro: Markets Outline Hendricks, Autumn 2017 FINM Intro: Markets 2/55 Asset Classes Fixed Income Money Market Bonds Equities Preferred Common contracted

Markets: Fixed Income Mark Hendricks Autumn 2017 FINM Intro: Markets Outline Hendricks, Autumn 2017 FINM Intro: Markets 2/55 Asset Classes Fixed Income Money Market Bonds Equities Preferred Common contracted

FINANCING IN INTERNATIONAL MARKETS

FINANCING IN INTERNATIONAL MARKETS 3. BOND RISK MANAGEMENT Forward Price of a Coupon Bond Consider the following transactions at time T=0: i. Borrow for T 2 days at an interest rate r 2. ii. Buy a coupon

FINANCING IN INTERNATIONAL MARKETS 3. BOND RISK MANAGEMENT Forward Price of a Coupon Bond Consider the following transactions at time T=0: i. Borrow for T 2 days at an interest rate r 2. ii. Buy a coupon

Calculator practice problems

Calculator practice problems The approved calculator for the CPA Preparatory Courses is the BAII Plus calculator. Being efficient in using your calculator is essential for success in the

Calculator practice problems The approved calculator for the CPA Preparatory Courses is the BAII Plus calculator. Being efficient in using your calculator is essential for success in the

Chapter 16. Managing Bond Portfolios

Chapter 16 Managing Bond Portfolios Change in Bond Price as a Function of Change in Yield to Maturity Interest Rate Sensitivity Inverse relationship between price and yield. An increase in a bond s yield

Chapter 16 Managing Bond Portfolios Change in Bond Price as a Function of Change in Yield to Maturity Interest Rate Sensitivity Inverse relationship between price and yield. An increase in a bond s yield

APPENDIX 3 TIME VALUE OF MONEY. Time Lines and Notation

1 APPENDIX 3 TIME VALUE OF MONEY The simplest tools in finance are often the most powerful. Present value is a concept that is intuitively appealing, simple to compute, and has a wide range of applications.

1 APPENDIX 3 TIME VALUE OF MONEY The simplest tools in finance are often the most powerful. Present value is a concept that is intuitively appealing, simple to compute, and has a wide range of applications.

Interest Rate Futures. Arjun Parthasarathy Founder INRBONDS.com

Interest Rate Futures Arjun Parthasarathy Founder INRBONDS.com 1 Interest Rate Futures Agenda Pricing How it works? 2 Interest Rate Futures 3 www.investorsareidiots.com Ten Year Cash Settled IRF IRF on

Interest Rate Futures Arjun Parthasarathy Founder INRBONDS.com 1 Interest Rate Futures Agenda Pricing How it works? 2 Interest Rate Futures 3 www.investorsareidiots.com Ten Year Cash Settled IRF IRF on

Lecture 3. Chapter 4: Allocating Resources Over Time

Lecture 3 Chapter 4: Allocating Resources Over Time 1 Introduction: Time Value of Money (TVM) $20 today is worth more than the expectation of $20 tomorrow because: a bank would pay interest on the $20

Lecture 3 Chapter 4: Allocating Resources Over Time 1 Introduction: Time Value of Money (TVM) $20 today is worth more than the expectation of $20 tomorrow because: a bank would pay interest on the $20

Chapter 2: BASICS OF FIXED INCOME SECURITIES

Chapter 2: BASICS OF FIXED INCOME SECURITIES 2.1 DISCOUNT FACTORS 2.1.1 Discount Factors across Maturities 2.1.2 Discount Factors over Time 2.1 DISCOUNT FACTORS The discount factor between two dates, t

Chapter 2: BASICS OF FIXED INCOME SECURITIES 2.1 DISCOUNT FACTORS 2.1.1 Discount Factors across Maturities 2.1.2 Discount Factors over Time 2.1 DISCOUNT FACTORS The discount factor between two dates, t

Exam FM/2 Study Manual - Spring 2007 Errata and Clarifications February 28, 2007

Exam FM/2 Study Manual - Spring 27 Errata and Clarifications February 28, 27 Jan 3/7 Module 1, Page 28, #8 4 t + 3 δ ( udu ) = du= 4ln( u+ 3) = 4ln ( u + 3) 3 t t t 4 4ln( ( t+ 3 )/3) t 3 + at () = ( e

Exam FM/2 Study Manual - Spring 27 Errata and Clarifications February 28, 27 Jan 3/7 Module 1, Page 28, #8 4 t + 3 δ ( udu ) = du= 4ln( u+ 3) = 4ln ( u + 3) 3 t t t 4 4ln( ( t+ 3 )/3) t 3 + at () = ( e

Sources & Uses 1. Pricing Summary 2. Debt Service Schedule 3. Derivation Of Form 8038 Yield Statistics 6. Proof of D/S for Arbitrage Purposes 7

Table of Contents Report Sources & Uses 1 Pricing Summary 2 Debt Service Schedule 3 Derivation Of Form 8038 Yield Statistics 6 Proof of D/S for Arbitrage Purposes 7 Proof Of Bond Yield @ 3.2996794% 8 Derivation

Table of Contents Report Sources & Uses 1 Pricing Summary 2 Debt Service Schedule 3 Derivation Of Form 8038 Yield Statistics 6 Proof of D/S for Arbitrage Purposes 7 Proof Of Bond Yield @ 3.2996794% 8 Derivation

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION Answers to Concepts Review and Critical Thinking Questions 1. Assuming positive cash flows and interest rates, the future value increases and the present value

CHAPTER 4 DISCOUNTED CASH FLOW VALUATION Answers to Concepts Review and Critical Thinking Questions 1. Assuming positive cash flows and interest rates, the future value increases and the present value

Bond Valuation. Lakehead University. Fall 2004

Bond Valuation Lakehead University Fall 2004 Outline of the Lecture Bonds and Bond Valuation Interest Rate Risk Duration The Call Provision 2 Bonds and Bond Valuation A corporation s long-term debt is

Bond Valuation Lakehead University Fall 2004 Outline of the Lecture Bonds and Bond Valuation Interest Rate Risk Duration The Call Provision 2 Bonds and Bond Valuation A corporation s long-term debt is

Valuing Bonds. Professor: Burcu Esmer

Valuing Bonds Professor: Burcu Esmer Valuing Bonds A bond is a debt instrument issued by governments or corporations to raise money The successful investor must be able to: Understand bond structure Calculate

Valuing Bonds Professor: Burcu Esmer Valuing Bonds A bond is a debt instrument issued by governments or corporations to raise money The successful investor must be able to: Understand bond structure Calculate

The exam will be closed book and notes; only the following calculators will be permitted: TI-30X IIS, TI-30X IIB, TI-30Xa.

21-270 Introduction to Mathematical Finance D. Handron Exam #1 Review The exam will be closed book and notes; only the following calculators will be permitted: TI-30X IIS, TI-30X IIB, TI-30Xa. 1. (25 points)

21-270 Introduction to Mathematical Finance D. Handron Exam #1 Review The exam will be closed book and notes; only the following calculators will be permitted: TI-30X IIS, TI-30X IIB, TI-30Xa. 1. (25 points)

Prof Albrecht s Notes Accounting for Bonds Intermediate Accounting 2

Prof Albrecht s Notes Accounting for Bonds Intermediate Accounting 2 Companies need capital to fund the acquisition of various resources for use in business operations. They get this capital from owners

Prof Albrecht s Notes Accounting for Bonds Intermediate Accounting 2 Companies need capital to fund the acquisition of various resources for use in business operations. They get this capital from owners

FinQuiz Notes

Reading 6 The Time Value of Money Money has a time value because a unit of money received today is worth more than a unit of money to be received tomorrow. Interest rates can be interpreted in three ways.

Reading 6 The Time Value of Money Money has a time value because a unit of money received today is worth more than a unit of money to be received tomorrow. Interest rates can be interpreted in three ways.

Asset Classes and Financial Instruments

Chapter 2 Asset Classes and Financial Instruments Bodie, Kane, and Marcus Essentials of Investments Tenth Edition 2.1 Asset Classes 2 2.1 The Money Market: Instruments Treasury Bills Certificates of Deposit

Chapter 2 Asset Classes and Financial Instruments Bodie, Kane, and Marcus Essentials of Investments Tenth Edition 2.1 Asset Classes 2 2.1 The Money Market: Instruments Treasury Bills Certificates of Deposit

Running head: THE TIME VALUE OF MONEY 1. The Time Value of Money. Ma. Cesarlita G. Josol. MBA - Acquisition. Strayer University

Running head: THE TIME VALUE OF MONEY 1 The Time Value of Money Ma. Cesarlita G. Josol MBA - Acquisition Strayer University FIN 534 THE TIME VALUE OF MONEY 2 Abstract The paper presents computations about

Running head: THE TIME VALUE OF MONEY 1 The Time Value of Money Ma. Cesarlita G. Josol MBA - Acquisition Strayer University FIN 534 THE TIME VALUE OF MONEY 2 Abstract The paper presents computations about

LECTURE 2. Bond Prices, Yields and Portfolio Management (Chapters 10 & 11)

") LECTURE 2 Bond Prices, Yields and Portfolio Management (Chapters 10 & 11) Bond Basics - Money Terms: Amount o Face Value / Par Value ($1,000) o Market Value quoted as a % of Par or the Face Value (priced

LECTURE 2 Bond Prices, Yields and Portfolio Management (Chapters 10 & 11) Bond Basics - Money Terms: Amount o Face Value / Par Value ($1,000) o Market Value quoted as a % of Par or the Face Value (priced

BBK3413 Investment Analysis

BBK3413 Investment Analysis Topic 4 Fixed Income Securities www.notes638.wordpress.com Content 7.1 CHARACTERISTICS OF BOND 7.2 RISKS ASSOCIATED WITH BONDS 7.3 BOND PRICING 7.4 BOND YIELDS 7.5 VOLATILITY

BBK3413 Investment Analysis Topic 4 Fixed Income Securities www.notes638.wordpress.com Content 7.1 CHARACTERISTICS OF BOND 7.2 RISKS ASSOCIATED WITH BONDS 7.3 BOND PRICING 7.4 BOND YIELDS 7.5 VOLATILITY

SWAPS INTEREST RATE AND CURRENCY SWAPS

SWAPS INTEREST RATE AND CURRENCY SWAPS Definition A swap is a contract between two parties to deliver one sum of money against another sum of money at periodic intervals. Obviously, the sums exchanged

SWAPS INTEREST RATE AND CURRENCY SWAPS Definition A swap is a contract between two parties to deliver one sum of money against another sum of money at periodic intervals. Obviously, the sums exchanged

Reading. Valuation of Securities: Bonds

Valuation of Securities: Bonds Econ 422: Investment, Capital & Finance University of Washington Last updated: April 11, 2010 Reading BMA, Chapter 3 http://finance.yahoo.com/bonds http://cxa.marketwatch.com/finra/marketd

Valuation of Securities: Bonds Econ 422: Investment, Capital & Finance University of Washington Last updated: April 11, 2010 Reading BMA, Chapter 3 http://finance.yahoo.com/bonds http://cxa.marketwatch.com/finra/marketd

MBF1223 Financial Management Prepared by Dr Khairul Anuar

MBF1223 Financial Management Prepared by Dr Khairul Anuar L4 Bonds & Bonds Valuation www.mba638.wordpress.com Bonds - Introduction A bond is a debt instrument issued by a borrower which has borrowed a

MBF1223 Financial Management Prepared by Dr Khairul Anuar L4 Bonds & Bonds Valuation www.mba638.wordpress.com Bonds - Introduction A bond is a debt instrument issued by a borrower which has borrowed a

JEM034 Corporate Finance Winter Semester 2017/2018

JEM034 Corporate Finance Winter Semester 2017/2018 Lecture #1 Olga Bychkova Topics Covered Today Review of key finance concepts Present value (chapter 2 in BMA) Valuation of bonds (chapter 3 in BMA) Present

JEM034 Corporate Finance Winter Semester 2017/2018 Lecture #1 Olga Bychkova Topics Covered Today Review of key finance concepts Present value (chapter 2 in BMA) Valuation of bonds (chapter 3 in BMA) Present

Interest Rate Markets

Interest Rate Markets 5. Chapter 5 5. Types of Rates Treasury rates LIBOR rates Repo rates 5.3 Zero Rates A zero rate (or spot rate) for maturity T is the rate of interest earned on an investment with

Interest Rate Markets 5. Chapter 5 5. Types of Rates Treasury rates LIBOR rates Repo rates 5.3 Zero Rates A zero rate (or spot rate) for maturity T is the rate of interest earned on an investment with

Final Examination. ACTU 363- Actuarial Mathematics Lab (1) (10/ H, Time 3H) (5 pages)

(10/ H, Time 3H) (5 pages)") King Saud University Department of Mathematics Exercise 1. [4] Final Examination ACTU 363- Actuarial Mathematics Lab (1) (10/411 438 H, Time 3H) (5 pages) A 30 year annuity is arranged to pay off a loan

King Saud University Department of Mathematics Exercise 1. [4] Final Examination ACTU 363- Actuarial Mathematics Lab (1) (10/411 438 H, Time 3H) (5 pages) A 30 year annuity is arranged to pay off a loan

SECTION HANDOUT #1 : Review of Topics

SETION HANDOUT # : Review of Topics MBA 0 October, 008 This handout contains some of the topics we have covered so far. You are not required to read it, but you may find some parts of it helpful when you

SETION HANDOUT # : Review of Topics MBA 0 October, 008 This handout contains some of the topics we have covered so far. You are not required to read it, but you may find some parts of it helpful when you

Topics in Corporate Finance. Chapter 2: Valuing Real Assets. Albert Banal-Estanol

Topics in Corporate Finance Chapter 2: Valuing Real Assets Investment decisions Valuing risk-free and risky real assets: Factories, machines, but also intangibles: patents, What to value? cash flows! Methods

Topics in Corporate Finance Chapter 2: Valuing Real Assets Investment decisions Valuing risk-free and risky real assets: Factories, machines, but also intangibles: patents, What to value? cash flows! Methods

Bond Prices and Yields

Bond Characteristics 14-2 Bond Prices and Yields Bonds are debt. Issuers are borrowers and holders are creditors. The indenture is the contract between the issuer and the bondholder. The indenture gives

Bond Characteristics 14-2 Bond Prices and Yields Bonds are debt. Issuers are borrowers and holders are creditors. The indenture is the contract between the issuer and the bondholder. The indenture gives

CHAPTER 8 INTEREST RATES AND BOND VALUATION

CHAPTER 8 INTEREST RATES AND BOND VALUATION Answers to Concept Questions 1. No. As interest rates fluctuate, the value of a Treasury security will fluctuate. Long-term Treasury securities have substantial

CHAPTER 8 INTEREST RATES AND BOND VALUATION Answers to Concept Questions 1. No. As interest rates fluctuate, the value of a Treasury security will fluctuate. Long-term Treasury securities have substantial

FINANCE REVIEW. Page 1 of 5

Correlation: A perfect positive correlation means as X increases, Y increases at the same rate Y Corr =.0 X A perfect negative correlation means as X increases, Y decreases at the same rate Y Corr = -.0

Correlation: A perfect positive correlation means as X increases, Y increases at the same rate Y Corr =.0 X A perfect negative correlation means as X increases, Y decreases at the same rate Y Corr = -.0

CHAPTER 4 TIME VALUE OF MONEY

CHAPTER 4 TIME VALUE OF MONEY 1 Learning Outcomes LO.1 Identify various types of cash flow patterns (streams) seen in business. LO.2 Compute the future value of different cash flow streams. Explain the

CHAPTER 4 TIME VALUE OF MONEY 1 Learning Outcomes LO.1 Identify various types of cash flow patterns (streams) seen in business. LO.2 Compute the future value of different cash flow streams. Explain the

BOND & STOCK VALUATION

Chapter 7 BOND & STOCK VALUATION Bond & Stock Valuation 7-2 1. OBJECTIVE # Use PV to calculate what prices of stocks and bonds should be! Basic bond terminology and valuation! Stock and preferred stock

Chapter 7 BOND & STOCK VALUATION Bond & Stock Valuation 7-2 1. OBJECTIVE # Use PV to calculate what prices of stocks and bonds should be! Basic bond terminology and valuation! Stock and preferred stock

FINANCING IN INTERNATIONAL MARKETS

FINANCING IN INTERNATIONAL MARKETS 1. INTERNATIONAL BOND MARKETS International Bond Markets The bond market (debt, credit, or fixed income market) is the financial market where participants buy and sell

FINANCING IN INTERNATIONAL MARKETS 1. INTERNATIONAL BOND MARKETS International Bond Markets The bond market (debt, credit, or fixed income market) is the financial market where participants buy and sell

SEEM 3580 Risk Analysis for Financial Engineering Second term,

SEEM 3580 Risk Analysis for Financial Engineering Second term, 2017 18 Assignment 1 Due date: 5:00 pm, 2, February, 2018 Important notes: 1. You must submit your assignment on time. No late assignment

SEEM 3580 Risk Analysis for Financial Engineering Second term, 2017 18 Assignment 1 Due date: 5:00 pm, 2, February, 2018 Important notes: 1. You must submit your assignment on time. No late assignment

Disclaimer: This resource package is for studying purposes only EDUCATION

Disclaimer: This resource package is for studying purposes only EDUCATION Chapter 1: The Corporation The Three Types of Firms -Sole Proprietorships -Owned and ran by one person -Owner has unlimited liability

Disclaimer: This resource package is for studying purposes only EDUCATION Chapter 1: The Corporation The Three Types of Firms -Sole Proprietorships -Owned and ran by one person -Owner has unlimited liability

DEBT VALUATION AND INTEREST. Chapter 9

DEBT VALUATION AND INTEREST Chapter 9 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value

DEBT VALUATION AND INTEREST Chapter 9 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value

Solutions to Practice Problems

Solutions to Practice Problems CHAPTER 1 1.1 Original exchange rate Reciprocal rate Answer (a) 1 = US$0.8420 US$1 =? 1.1876 (b) 1 = US$1.4565 US$1 =? 0.6866 (c) NZ$1 = US$0.4250 US$1 = NZ$? 2.3529 1.2

Solutions to Practice Problems CHAPTER 1 1.1 Original exchange rate Reciprocal rate Answer (a) 1 = US$0.8420 US$1 =? 1.1876 (b) 1 = US$1.4565 US$1 =? 0.6866 (c) NZ$1 = US$0.4250 US$1 = NZ$? 2.3529 1.2

Adv. Finance Weekly Meetings. Meeting 1 Year 15-16

Adv. Finance Weekly Meetings Meeting 1 Year 15-16 1 Weekly Meeting I Finance 2 Agenda Introduction What can you expect from the following meetings Four types of firms Ownership Liability Conflicts of Interest

Adv. Finance Weekly Meetings Meeting 1 Year 15-16 1 Weekly Meeting I Finance 2 Agenda Introduction What can you expect from the following meetings Four types of firms Ownership Liability Conflicts of Interest

Chapter 4. Characteristics of Bonds. Chapter 4 Topic Overview. Bond Characteristics

Chapter 4 Topic Overview Chapter 4 Valuing Bond Characteristics Annual and Semi-Annual Bond Valuation Reading Bond Quotes Finding Returns on Bond Risk and Other Important Bond Valuation Relationships Bond

Chapter 4 Topic Overview Chapter 4 Valuing Bond Characteristics Annual and Semi-Annual Bond Valuation Reading Bond Quotes Finding Returns on Bond Risk and Other Important Bond Valuation Relationships Bond

Purpose of the Capital Market

BOND MARKETS Purpose of the Capital Market Original maturity is greater than one year, typically for long-term financing or investments Best known capital market securities: Stocks and bonds Capital Market

BOND MARKETS Purpose of the Capital Market Original maturity is greater than one year, typically for long-term financing or investments Best known capital market securities: Stocks and bonds Capital Market

Chapter 14 Exchange Rates and the Foreign Exchange Market: An Asset Approach

Chapter 14 Exchange Rates and the Foreign Exchange Market: An Asset Approach Copyright 2015 Pearson Education, Inc. All rights reserved. 1-1 Preview The basics of exchange rates Exchange rates and the

Chapter 14 Exchange Rates and the Foreign Exchange Market: An Asset Approach Copyright 2015 Pearson Education, Inc. All rights reserved. 1-1 Preview The basics of exchange rates Exchange rates and the

FINC3019 FIXED INCOME SECURITIES

FINC3019 FIXED INCOME SECURITIES WEEK 1 BONDS o Debt instrument requiring the issuer to repay the lender the amount borrowed + interest over specified time period o Plain vanilla (typical) bond:! Fixed

FINC3019 FIXED INCOME SECURITIES WEEK 1 BONDS o Debt instrument requiring the issuer to repay the lender the amount borrowed + interest over specified time period o Plain vanilla (typical) bond:! Fixed

CHAPTER 15: THE TERM STRUCTURE OF INTEREST RATES

CHAPTER : THE TERM STRUCTURE OF INTEREST RATES. Expectations hypothesis: The yields on long-term bonds are geometric averages of present and expected future short rates. An upward sloping curve is explained

CHAPTER : THE TERM STRUCTURE OF INTEREST RATES. Expectations hypothesis: The yields on long-term bonds are geometric averages of present and expected future short rates. An upward sloping curve is explained

BUSI 370 Business Finance

Review Session 2 February 7 th, 2016 Road Map 1. BONDS 2. COMMON SHARES 3. PREFERRED SHARES 4. TREASURY BILLS (T Bills) ANSWER KEY WITH COMMENTS 1. BONDS // Calculate the price of a ten-year annual pay

Review Session 2 February 7 th, 2016 Road Map 1. BONDS 2. COMMON SHARES 3. PREFERRED SHARES 4. TREASURY BILLS (T Bills) ANSWER KEY WITH COMMENTS 1. BONDS // Calculate the price of a ten-year annual pay

INTEREST RATE FORWARDS AND FUTURES

INTEREST RATE FORWARDS AND FUTURES FORWARD RATES The forward rate is the future zero rate implied by today s term structure of interest rates BAHATTIN BUYUKSAHIN, CELSO BRUNETTI 1 0 /4/2009 2 IMPLIED FORWARD

INTEREST RATE FORWARDS AND FUTURES FORWARD RATES The forward rate is the future zero rate implied by today s term structure of interest rates BAHATTIN BUYUKSAHIN, CELSO BRUNETTI 1 0 /4/2009 2 IMPLIED FORWARD

Alan Brazil. Goldman, Sachs & Co.

Alan Brazil Goldman, Sachs & Co. Assumptions: Coupon paid every 6 months, $100 of principal paid at maturity, government guaranteed 1 Debt is a claim on a fixed amount of cashflows in the future A mortgage

Alan Brazil Goldman, Sachs & Co. Assumptions: Coupon paid every 6 months, $100 of principal paid at maturity, government guaranteed 1 Debt is a claim on a fixed amount of cashflows in the future A mortgage

The price of Snyder preferred stock prior to the payment of today s dividend is 1000 assuming a yield rate of 10% convertible quarterly. 0.

Chapter 7 1. The preferred stock of Koenig Industries pays a quarterly dividend of 8. The next dividend will be paid in 3 months. Using the dividend discount method and an annual effective yield rate of

Chapter 7 1. The preferred stock of Koenig Industries pays a quarterly dividend of 8. The next dividend will be paid in 3 months. Using the dividend discount method and an annual effective yield rate of

Financial Markets and Products

Financial Markets and Products 1. Eric sold a call option on a stock trading at $40 and having a strike of $35 for $7. What is the profit of the Eric from the transaction if at expiry the stock is trading

Financial Markets and Products 1. Eric sold a call option on a stock trading at $40 and having a strike of $35 for $7. What is the profit of the Eric from the transaction if at expiry the stock is trading

Credit Derivatives. By A. V. Vedpuriswar

Credit Derivatives By A. V. Vedpuriswar September 17, 2017 Historical perspective on credit derivatives Traditionally, credit risk has differentiated commercial banks from investment banks. Commercial

Credit Derivatives By A. V. Vedpuriswar September 17, 2017 Historical perspective on credit derivatives Traditionally, credit risk has differentiated commercial banks from investment banks. Commercial

Lecture 9. Basics on Swaps

Lecture 9 Basics on Swaps Agenda: 1. Introduction to Swaps ~ Definition: ~ Basic functions ~ Comparative advantage: 2. Swap quotes and LIBOR zero rate ~ Interest rate swap is combination of two bonds:

Lecture 9 Basics on Swaps Agenda: 1. Introduction to Swaps ~ Definition: ~ Basic functions ~ Comparative advantage: 2. Swap quotes and LIBOR zero rate ~ Interest rate swap is combination of two bonds:

FIXED INCOME I EXERCISES

FIXED INCOME I EXERCISES This version: 25.09.2011 Interplay between macro and financial variables 1. Read the paper: The Bond Yield Conundrum from a Macro-Finance Perspective, Glenn D. Rudebusch, Eric

FIXED INCOME I EXERCISES This version: 25.09.2011 Interplay between macro and financial variables 1. Read the paper: The Bond Yield Conundrum from a Macro-Finance Perspective, Glenn D. Rudebusch, Eric

Midterm Review Package Tutor: Chanwoo Yim

COMMERCE 298 Intro to Finance Midterm Review Package Tutor: Chanwoo Yim BCom 2016, Finance 1. Time Value 2. DCF (Discounted Cash Flow) 2.1 Constant Annuity 2.2 Constant Perpetuity 2.3 Growing Annuity 2.4

COMMERCE 298 Intro to Finance Midterm Review Package Tutor: Chanwoo Yim BCom 2016, Finance 1. Time Value 2. DCF (Discounted Cash Flow) 2.1 Constant Annuity 2.2 Constant Perpetuity 2.3 Growing Annuity 2.4

CHAPTER 2: ASSET CLASSES AND FINANCIAL INSTRUMENTS

Chapter 2 - Asset Classes and Financial Instruments CHAPTER 2: ASSET CLASSES AND FINANCIAL INSTRUMENTS PROBLEM SETS 1. Preferred stock is like long-term debt in that it typically promises a fixed payment

Chapter 2 - Asset Classes and Financial Instruments CHAPTER 2: ASSET CLASSES AND FINANCIAL INSTRUMENTS PROBLEM SETS 1. Preferred stock is like long-term debt in that it typically promises a fixed payment

The Financial Markets Foundation Course (FMFC) Certificate. Programme Syllabus

Certificate. Programme Syllabus") The Financial Markets Foundation Course (FMFC) Certificate Programme Syllabus Contents i. Introduction ii. Accreditation iii. Assessment iv. Background Reading v. Structure of the FMFC syllabus vi. Outline

The Financial Markets Foundation Course (FMFC) Certificate Programme Syllabus Contents i. Introduction ii. Accreditation iii. Assessment iv. Background Reading v. Structure of the FMFC syllabus vi. Outline