DEBT VALUATION AND INTEREST. Chapter 9

|

|

|

- Bertina Poole

- 6 years ago

- Views:

Transcription

1 DEBT VALUATION AND INTEREST Chapter 9

2 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value

3 Corporate Borrowings There are two main sources of borrowing for a corporation: 1. Loan from a financial institution (known as private debt since it involves only two parties) 2. Bonds (known as public debt since they can be traded in the public financial markets)

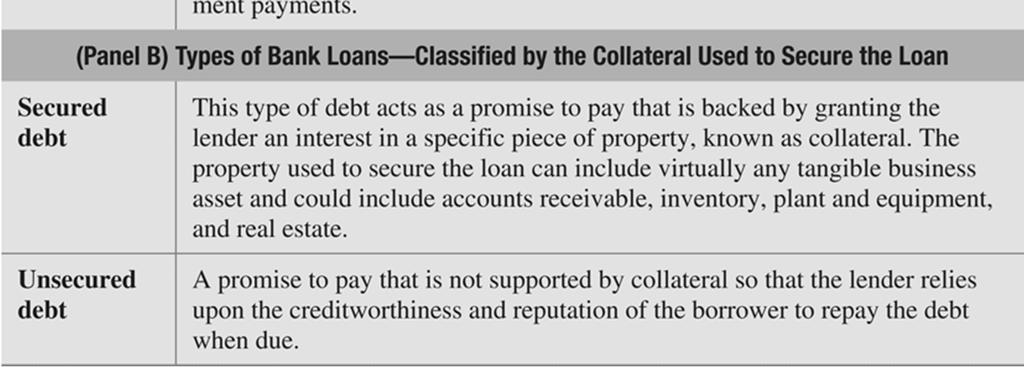

4 Borrowing Money in the Private Financial Market Financial Institutions provide loans Working capital loans to finance firm s day-to-day operations Transaction loans for the purchase of equipment or property Loans may or may not be secured by a collateral.

5 Table 9-1 Types of Bank Debt

6 Floating-Rate Loans In the private financial market, loans are typically floating rate loans The interest rate is adjusted based on a specific benchmark rate. The most popular benchmark rate is the London Interbank Offered Rate (LIBOR), rate at which banks offer to lend in the London wholesale or interbank market

7 Floating-Rate Loans For example, a corporation may get a 1-year loan with a rate of 300 basis points (or 3%) over LIBOR with a ceiling of 11% and a floor of 4%.

8 CHECKPOINT 9.1: CHECK YOURSELF Calculating the Rate of Interest on a Floating-Rate Loan Consider a 1 year loan period Spread over LIBOR is 75 basis points (00.75%). Ceiling = 2.50%, floor = 1.75% Is the ceiling rate or floor rate violated during the loan period?

9 Step 1: Picture the Problem 3.00% Floating Rate Loans 2.50% 2.00% Interest Rate 1.50% 1.00% Series1 Series2 Series3 Series4 0.50% 0.00%

10 Step 2: Decide on a Solution Strategy We have to determine the floating rate for every week and see if it exceeds the ceiling or falls below the floor. Floating rate on Loan = LIBOR for the previous week + spread of.75% The floating rate on loan cannot exceed the ceiling rate of 2.5% or drop below the floor rate of 1.75%.

11 Step 3: Solve LIBOR LIBOR + Spread (.75%) 2/29/ % Loan Rate 3/7/ % 2.73% 2.50% 3/14/ % 2.44% 2.41% 3/21/ % 2.27% 2.27% 3/28/ % 2.10% 2.10% 4/4/ % 2.35% 2.35% 4/11/ % 2.38% 2.38% 4/18/ % 2.42% 2.42% 4/25/ % 2.63% 2.50% 5/2/ % 2.50% Ceiling Violated

12 Step 4: Analyze If there were no ceiling, the loan rate would have been 2.73% during the first week of the loan, and 2.63% and 2.68% during the last two weeks of the loan. The rate was set to the ceiling of 2.50% for those three weeks.

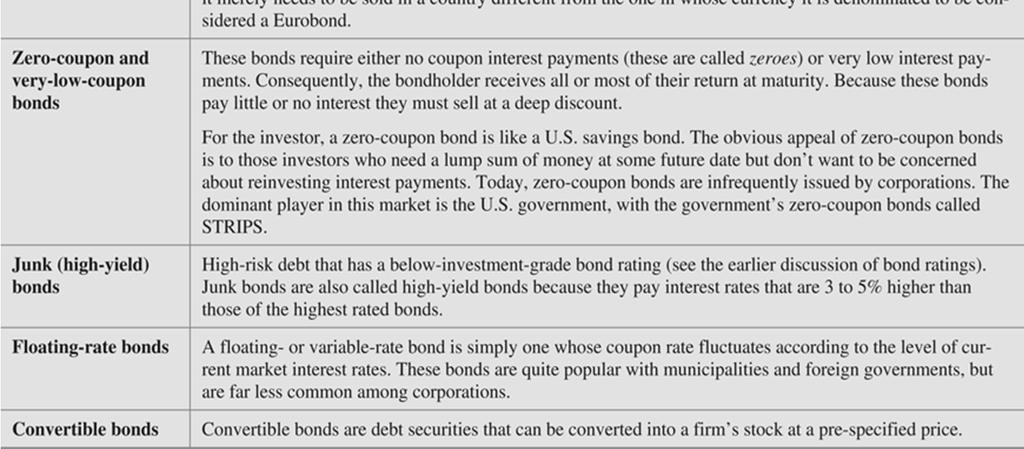

13 Corporate Bonds Corporate bond is a debt security issued by corporation that has promised future payments and a maturity date. If the firm fails to pay the promised future payments of interest and principal, the bond trustee can classify the firm as insolvent and force the firm into bankruptcy.

14 Basic Bond Features The basic features of a bond include the following: Bond indenture Claims on assets and income Par or face value Coupon interest rate Maturity and repayment of principal Call provision and conversion features

15 Bond Terminology

16 Types of Corporate Bonds

17 Borrowing Money in the Public Financial Market Corporations engage the services of an investment banker while raising long-term funds in the public financial market. The investment banker performs three basic functions: Underwriting: assuming risk of selling a security issued. The client is given the money before the securities are sold to the public. Distributing Advising

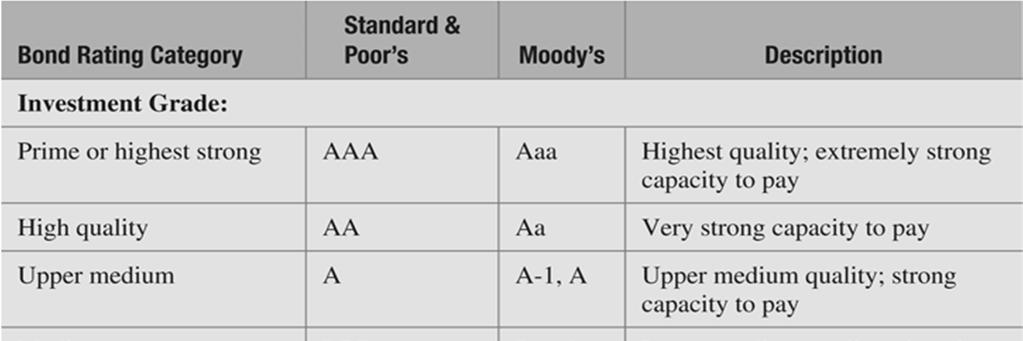

18 Interpreting Bond Ratings

19 Valuing Corporate Debt The value of corporate debt is equal to the present value of the contractually promised principal and interest payments (the cash flows) discounted back to the present using the market s required yield to maturity on similar risk.

20 Valuing Corporate Debt Step 1: Determine bondholder cash flows, which are the the amount and timing of the bond s promised interest and principal payments to the bondholders. Annual Interest = Par value coupon rate Example 9.1: The annual interest for a 10-year bond with coupon interest rate of 7% and a par value of $1,000 is equal to $70, (.07 $1,000 = $70). This bond will pay $70 every year and $1,000 at the end of 10-years.

21 Valuing Corporate Debt Step 2: Estimate the appropriate discount rate on a bond of similar risk. Discount rate is the return the bond will yield if it is held to maturity and all bond payments are made.

22 Valuing Corporate Debt Step 3: Calculate the present value of the bond s interest and principal payments from Step 1 using the discount rate in step 2.

23 Calculating a Bond s Yield to Maturity (YTM) We can think of YTM as the discount rate that makes the present value of the bond s promised interest and principal equal to the bond s observed market price.

24 CHECKPOINT 9.2: CHECK YOURSELF Calculating the Yield to Maturity on a Corporate Bond Calculate the YTM on the Ford bond where the bond price rises to $900 (holding all other things equal). 11 year maturity 6.5% coupon rate $1000 face value

25 Step 1: Picture the Problem YTM=? Years Cash flow -$900 $65 $65 $65 $1,065 Purchase price = $900 Interest payments = $65 per year for years 1-11 Final payment = $1,000 in year 11 of principal.

26 Step 2: Decide on a Solution Strategy YTM is the solution to

27 Step 3: Solve Using a Financial Calculator Need to find interest rate N = 11 PV = -90 PMT = 65 FV = 1,000 I/Y = 7.89

28 Step 4: Analyze The yield to maturity on the bond is 7.89%. The yield is higher than the coupon rate of interest of 6.5%. Since the coupon rate is lower than the yield to maturity, the bond is trading at a price below $1,000. We call this a discount bond.

29 Corporate Bond Credit Spread Tables

30 Promised versus Expected Yield to Maturity The yield to maturity calculation assumes that the bond performs according to the terms of the bond contract or indenture. Since corporate bonds are subject to risk of default, the promised yield to maturity may not be equal to expected yield to maturity. That is, we need to take account of the default risk in our YTM calculation

31 Promised versus Expected Yield to Maturity Example Consider a one-year bond that promises a coupon rate of 8% and has a principal (par value) of $1,000. Further assume the bond is currently trading for $850. Promised YTM = {(Interest year 1 + Principal) (Bond Value)} 1 = {($80+$1,000) ($850)} 1 = 27.06%

32 Promised versus Expected Yield to Maturity Assume there is a 40% probability of default on this bond If the bond defaults, the bondholders will receive only 60% of the principal and interest owed. What is the expected YTM on this bond? YTM default = {(Interest year 1 + Principal)} (Bond Value)} 1 = {($80+$1000).60} ($850)} 1= %

33 Promised versus Expected Yield to Maturity

34 34 Ratings and Default Risk

35 35 Recovery Rates on Defaulted Bonds

36 CHECKPOINT 9.3: CHECK YOURSELF Valuing a Bond Issue Calculate the value of the AT&T bond should the yield to maturity for comparable risk bonds rise to 9% (holding all other things equal). 20 year bond 8.5% coupon rate $1000 par value

37 Step 1: Picture the Problem Years i= 9% Cash flows $85 $85 $85 $1,085 PV of all Cash flows =? $85 annual interest $85 interest + $1,000 Principal

38 Step 2: Decide on a Solution Strategy Here we know the following: Annual interest payments = $85 Principal amount or par value = $1,000 Time = 20 years YTM or discount rate = 9% We can use the above information to determine the value of the bond by discounting future interest and principal payment to the present.

39 Step 3: Solve Using a Mathematical Formula = $ 85{[1-(1/(1.09) 20 ] (.09)}+ 1,000/(1.09) 20 = $85 (9.128) + $ = $954.36

40 Step 3: Solve Using a Financial Calculator N = 20 I/Y = 9.0 PMT = 85 FV = 1000 PV =

41 Step 4: Analyze The value of AT&T bond falls to $ when the yield to maturity rises to 9%. The bonds are now trading at a discount as the coupon rate on AT&T bonds is lower than the market yield. An investor who buys AT&T bonds at its current discounted price will earn a promised yield to maturity of 9%.

42 Semiannual Interest Payments Corporate bonds typically pay interest to bondholders semiannually.

43 CHECKPOINT 9.4: CHECK YOURSELF Valuing a Bond Issue That Pays Semiannual Interest Calculate the present value of the AT&T bond should the yield to maturity on comparable bonds rise to 9% (holding all other things equal).

44 Step 1: Picture the Problem Periods i= 9% month periods Cash flow PV=? $ $42.5 $1, $42.50 Semiannual interest $42.5 interest + $1,000 Principal

45 Step 2: Decide on a Solution Strategy Here we know the following: Semiannual interest payments = $42.50 Principal amount or par value = $1,000 Time = 20 years or 40 periods YTM or discount rate = 9% or 4.5% for 6-months We can use the above information to determine the value of the bond by discounting future interest and principal payment to the present.

46 Step 3: Solve Using a Mathematical Formula = $ 42.5{[1-(1/(1.045) 40 ] (.20)} + $1,000/(1.045) 40 = $42.5 (18.40) + $ = $

47 Step 3: Solve Using a Financial Calculator N = 40 1/y = 4.50 PMT = FV = 1000 PV =

48 Step 4: Analyze Using semi-annual compounding we get a value of $ for AT&T bonds. This is very close to the value of $ found using annual compounding.

49 Bond Valuation: Four Key Relationships First Relationship The value of bond is inversely related to changes in the yield to maturity. YTM = 12% YTM rises to 15% Par value $1,000 $1,000 Coupon rate 12% 12% Maturity date 5 years 5 years Bond Value $1,000 $ Bond Value Drops

50 Figure 9-1 Bond Value and the Market s Required Yield to Maturity (5-Year Bond, 12% Coupon Rate)

51 Bond Valuation: Four Key Relationships Second Relationship: The market value of a bond will be less than the par value (discount bond) if the market s required yield to maturity is above the coupon interest rate and will be valued above par value (premium bond) if the market s required yield to maturity is below the coupon interest rate.

52 Bond Valuation: Four Key Relationships Third Relationship As the maturity date approaches, the market value of a bond approaches its par value. That s because at maturity the bond will be taken away and the investor will receive the par value of the bond.

53 Value of a 12% Coupon Bond during the Life of the Bond

54 Bond Valuation: Four Key Relationships Fourth Relationship Long term bonds have greater interest-rate risk than short-term bonds. While all bonds are affected by a change in interest rates, the prices of longer-term bonds fluctuate more when interest rates change than do the prices of shorter-term bonds (see Table 9.6)

55 Bond Valuation: Four Key Relationships First Relationship The value of bond is inversely related to changes in the yield to maturity. YTM = 12% YTM rises to 15% YTM rises to 15% Par value $1,000 $1,000 $1,000 Coupon rate 12% 12% 12% Maturity date 5 years 5 years 10 years Bond Value $1,000 $ $839.44

56 Determinants of Interest Rates As we observed earlier, bond prices vary inversely with interest rates. Therefore in order to understand how bond prices fluctuate, we need to know the determinants of interest rates.

57 Inflation and Real versus Nominal Interest Rates Quotes of interest rates in the financial press are commonly referred to as the nominal (or quoted) interest rates. Real rate of interest adjusts for the effects of inflation.

58 Fisher Effect: The Nominal and Real Rate of Interest The relationship between the nominal rate of interest, r nominal, the anticipated rate of inflation, r inflation, and the real rate of interest is known as the Fisher effect. 1+ r nominal = (1+ r real )(1+ r inflation ) = 1+r real +r inflation +r real *r inflation 1+ r real + r inflation

59 Interest Rate Determinants We can think of the reported nominal = interest rate on a bond as having five components: Real risk-free rate The inflation premium Default risk premium Maturity-risk premium Liquidity-risk premium

60 The Maturity-Risk Premium and the Term Structure of Interest Rates The relationship between interest rates and time to maturity with risk held constant is known as the term structure of interest rates or the yield curve. Figure 9-3 illustrates a hypothetical term structure of U.S. Treasury Bonds.

61 Figure 9-3 The Term Structure of Interest Rates or Yield Curve

62 The Shape of the Yield Curve By reviewing equation 9-5, we can gain insight into the shape of the yield curve for US Treasuries. Since there is no default risk or liquidity risk and the realrisk free rate of interest is unlikely to change, the shape of the yield curve is driven by inflation premium and maturity risk premium.

63 The Shape of the Yield Curve During periods when inflation is expected to subside, the inflation premium should decrease over longer maturities, resulting in a downward sloping Treasury yield curve as shown in Figure 9.5. The reverse is also true as shown in Figure 9.4

64 Figure 9.4 Treasury Yield Curve during Period of Increasing Inflation

65 Figure 9.5 Treasury Yield Curve during Period of Decreasing Inflation

66 Shifts in the Yield Curve The yield curve changes over time as expectations regarding each of the four factors that underlie interest rates change. Figure 9-6 shows the yield curve one day before 911 attack and again two weeks later. Investors shifted their funds to the safety of Treasuries, pushing up the prices and bringing down the yields.

67 Figure 9-6 Changes in the Term Structure of Interest Rates around September 11, 2001

68 Shifts in the Yield Curve The yield curve is generally upward sloping but it can assume different shapes i.e. downward sloping or flat. Figure 9-7 illustrates different shapes of yield curves at different dates, observed within a span of only 13 months.

69 Figure 9.7 Historical Term Structure of Interest Rates for Government Securities

70 US Treasury Yield Curve 70

71 International Yield Curves 71

Chapter 9 Debt Valuation and Interest Rates

Chapter 9 Debt Valuation and Interest Rates Slide Contents Learning Objectives Principles Used in This Chapter 1.Overview of Corporate Debt 2.Valuing Corporate Debt 3.Bond Valuation: Four Key Relationships

Chapter 9 Debt Valuation and Interest Rates Slide Contents Learning Objectives Principles Used in This Chapter 1.Overview of Corporate Debt 2.Valuing Corporate Debt 3.Bond Valuation: Four Key Relationships

KEY CONCEPTS AND SKILLS

Chapter 5 INTEREST RATES AND BOND VALUATION 5-1 KEY CONCEPTS AND SKILLS Know the important bond features and bond types Comprehend bond values (prices) and why they fluctuate Compute bond values and fluctuations

Chapter 5 INTEREST RATES AND BOND VALUATION 5-1 KEY CONCEPTS AND SKILLS Know the important bond features and bond types Comprehend bond values (prices) and why they fluctuate Compute bond values and fluctuations

Chapter 5. Learning Objectives. Principals Applied in this Chapter. Time Value of Money. Principle 1: Money Has a Time Value.

Chapter 5 Time Value of Money Learning Objectives 1. Construct cash flow timelines to organize your analysis of problems involving the time value of money. 2. Understand compounding and calculate the future

Chapter 5 Time Value of Money Learning Objectives 1. Construct cash flow timelines to organize your analysis of problems involving the time value of money. 2. Understand compounding and calculate the future

Chapter 5. Time Value of Money

Chapter 5 Time Value of Money Using Timelines to Visualize Cashflows A timeline identifies the timing and amount of a stream of payments both cash received and cash spent - along with the interest rate

Chapter 5 Time Value of Money Using Timelines to Visualize Cashflows A timeline identifies the timing and amount of a stream of payments both cash received and cash spent - along with the interest rate

Chapter 5. Interest Rates and Bond Valuation. types. they fluctuate. relationship to bond terms and value. interest rates

Chapter 5 Interest Rates and Bond Valuation } Know the important bond features and bond types } Compute bond values and comprehend why they fluctuate } Appreciate bond ratings, their meaning, and relationship

Chapter 5 Interest Rates and Bond Valuation } Know the important bond features and bond types } Compute bond values and comprehend why they fluctuate } Appreciate bond ratings, their meaning, and relationship

1) Which one of the following is NOT a typical negative bond covenant?

Which one of the following is NOT a typical negative bond covenant?") Questions in Chapter 7 concept.qz 1) Which one of the following is NOT a typical negative bond covenant? [A] The firm must limit dividend payments. [B] The firm cannot merge with another firm. [C] The

Questions in Chapter 7 concept.qz 1) Which one of the following is NOT a typical negative bond covenant? [A] The firm must limit dividend payments. [B] The firm cannot merge with another firm. [C] The

CHAPTER 8. Valuing Bonds. Chapter Synopsis

CHAPTER 8 Valuing Bonds Chapter Synopsis 8.1 Bond Cash Flows, Prices, and Yields A bond is a security sold at face value (FV), usually $1,000, to investors by governments and corporations. Bonds generally

CHAPTER 8 Valuing Bonds Chapter Synopsis 8.1 Bond Cash Flows, Prices, and Yields A bond is a security sold at face value (FV), usually $1,000, to investors by governments and corporations. Bonds generally

Bond Prices and Yields

Bond Characteristics 14-2 Bond Prices and Yields Bonds are debt. Issuers are borrowers and holders are creditors. The indenture is the contract between the issuer and the bondholder. The indenture gives

Bond Characteristics 14-2 Bond Prices and Yields Bonds are debt. Issuers are borrowers and holders are creditors. The indenture is the contract between the issuer and the bondholder. The indenture gives

Fin 5633: Investment Theory and Problems: Chapter#15 Solutions

Fin 5633: Investment Theory and Problems: Chapter#15 Solutions 1. Expectations hypothesis: The yields on long-term bonds are geometric averages of present and expected future short rates. An upward sloping

Fin 5633: Investment Theory and Problems: Chapter#15 Solutions 1. Expectations hypothesis: The yields on long-term bonds are geometric averages of present and expected future short rates. An upward sloping

Fixed income security. Face or par value Coupon rate. Indenture. The issuer makes specified payments to the bond. bondholder

Bond Prices and Yields Bond Characteristics Fixed income security An arragement between borrower and purchaser The issuer makes specified payments to the bond holder on specified dates Face or par value

Bond Prices and Yields Bond Characteristics Fixed income security An arragement between borrower and purchaser The issuer makes specified payments to the bond holder on specified dates Face or par value

CHAPTER 14. Bond Characteristics. Bonds are debt. Issuers are borrowers and holders are creditors.

Bond Characteristics 14-2 CHAPTER 14 Bond Prices and Yields Bonds are debt. Issuers are borrowers and holders are creditors. The indenture is the contract between the issuer and the bondholder. The indenture

Bond Characteristics 14-2 CHAPTER 14 Bond Prices and Yields Bonds are debt. Issuers are borrowers and holders are creditors. The indenture is the contract between the issuer and the bondholder. The indenture

BOND ANALYTICS. Aditya Vyas IDFC Ltd.

BOND ANALYTICS Aditya Vyas IDFC Ltd. Bond Valuation-Basics The basic components of valuing any asset are: An estimate of the future cash flow stream from owning the asset The required rate of return for

BOND ANALYTICS Aditya Vyas IDFC Ltd. Bond Valuation-Basics The basic components of valuing any asset are: An estimate of the future cash flow stream from owning the asset The required rate of return for

Understanding Interest Rates

Money & Banking Notes Chapter 4 Understanding Interest Rates Measuring Interest Rates Present Value (PV): A dollar paid to you one year from now is less valuable than a dollar paid to you today. Why? -

Money & Banking Notes Chapter 4 Understanding Interest Rates Measuring Interest Rates Present Value (PV): A dollar paid to you one year from now is less valuable than a dollar paid to you today. Why? -

I. Asset Valuation. The value of any asset, whether it is real or financial, is the sum of all expected future earnings produced by the asset.

1 I. Asset Valuation The value of any asset, whether it is real or financial, is the sum of all expected future earnings produced by the asset. 2 1 II. Bond Features and Prices Definitions Bond: a certificate

1 I. Asset Valuation The value of any asset, whether it is real or financial, is the sum of all expected future earnings produced by the asset. 2 1 II. Bond Features and Prices Definitions Bond: a certificate

CHAPTER 14. Bond Prices and Yields INVESTMENTS BODIE, KANE, MARCUS. Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved.

CHAPTER 14 Bond Prices and Yields McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 14-2 Bond Characteristics Bonds are debt. Issuers are borrowers and holders are

CHAPTER 14 Bond Prices and Yields McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 14-2 Bond Characteristics Bonds are debt. Issuers are borrowers and holders are

FINS2624 Summary. 1- Bond Pricing. 2 - The Term Structure of Interest Rates

FINS2624 Summary 1- Bond Pricing Yield to Maturity: The YTM is a hypothetical and constant interest rate which makes the PV of bond payments equal to its price; considered an average rate of return. It

FINS2624 Summary 1- Bond Pricing Yield to Maturity: The YTM is a hypothetical and constant interest rate which makes the PV of bond payments equal to its price; considered an average rate of return. It

4. D Spread to treasuries. Spread to treasuries is a measure of a corporate bond s default risk.

www.liontutors.com FIN 301 Final Exam Practice Exam Solutions 1. C Fixed rate par value bond. A bond is sold at par when the coupon rate is equal to the market rate. 2. C As beta decreases, CAPM will decrease

www.liontutors.com FIN 301 Final Exam Practice Exam Solutions 1. C Fixed rate par value bond. A bond is sold at par when the coupon rate is equal to the market rate. 2. C As beta decreases, CAPM will decrease

Security Analysis. Bond Valuation

Security Analysis Bond Valuation Background on Bonds Bonds represent long-term debt securities Contractual Promise to pay future cash flows to investors The issuer of the bond is obligated to pay: Interest

Security Analysis Bond Valuation Background on Bonds Bonds represent long-term debt securities Contractual Promise to pay future cash flows to investors The issuer of the bond is obligated to pay: Interest

FIN 6160 Investment Theory. Lecture 9-11 Managing Bond Portfolios

FIN 6160 Investment Theory Lecture 9-11 Managing Bond Portfolios Bonds Characteristics Bonds represent long term debt securities that are issued by government agencies or corporations. The issuer of bond

FIN 6160 Investment Theory Lecture 9-11 Managing Bond Portfolios Bonds Characteristics Bonds represent long term debt securities that are issued by government agencies or corporations. The issuer of bond

Chapter 6. Learning Objectives. Principals Applies in this Chapter. Time Value of Money

Chapter 6 Time Value of Money 1 Learning Objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate the present and future values of each. 2. Calculate the present value of

Chapter 6 Time Value of Money 1 Learning Objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate the present and future values of each. 2. Calculate the present value of

I. Introduction to Bonds

University of California, Merced ECO 163-Economics of Investments Chapter 10 Lecture otes I. Introduction to Bonds Professor Jason Lee A. Definitions Definition: A bond obligates the issuer to make specified

University of California, Merced ECO 163-Economics of Investments Chapter 10 Lecture otes I. Introduction to Bonds Professor Jason Lee A. Definitions Definition: A bond obligates the issuer to make specified

Lecture 4. The Bond Market. Mingzhu Wang SKKU ISS 2017

Lecture 4 The Bond Market Mingzhu Wang SKKU ISS 2017 Bond Terminologies 2 Agenda Types of Bonds 1. Treasury Notes and Bonds 2. Municipal Bonds 3. Corporate Bonds Financial Guarantees for Bonds Current

Lecture 4 The Bond Market Mingzhu Wang SKKU ISS 2017 Bond Terminologies 2 Agenda Types of Bonds 1. Treasury Notes and Bonds 2. Municipal Bonds 3. Corporate Bonds Financial Guarantees for Bonds Current

FUNDAMENTALS OF THE BOND MARKET

FUNDAMENTALS OF THE BOND MARKET Bonds are an important component of any balanced portfolio. To most they represent a conservative investment vehicle. However, investors purchase bonds for a variety of

FUNDAMENTALS OF THE BOND MARKET Bonds are an important component of any balanced portfolio. To most they represent a conservative investment vehicle. However, investors purchase bonds for a variety of

CHAPTER 15: THE TERM STRUCTURE OF INTEREST RATES

CHAPTER : THE TERM STRUCTURE OF INTEREST RATES. Expectations hypothesis: The yields on long-term bonds are geometric averages of present and expected future short rates. An upward sloping curve is explained

CHAPTER : THE TERM STRUCTURE OF INTEREST RATES. Expectations hypothesis: The yields on long-term bonds are geometric averages of present and expected future short rates. An upward sloping curve is explained

Valuing Bonds. Professor: Burcu Esmer

Valuing Bonds Professor: Burcu Esmer Valuing Bonds A bond is a debt instrument issued by governments or corporations to raise money The successful investor must be able to: Understand bond structure Calculate

Valuing Bonds Professor: Burcu Esmer Valuing Bonds A bond is a debt instrument issued by governments or corporations to raise money The successful investor must be able to: Understand bond structure Calculate

SECURITY ANALYSIS AND PORTFOLIO MANAGEMENT. 2) A bond is a security which typically offers a combination of two forms of payments:

A bond is a security which typically offers a combination of two forms of payments:") Solutions to Problem Set #: ) r =.06 or r =.8 SECURITY ANALYSIS AND PORTFOLIO MANAGEMENT PVA[T 0, r.06] j 0 $8000 $8000 { {.06} t.06 &.06 (.06) 0} $8000(7.36009) $58,880.70 > $50,000 PVA[T 0, r.8] $8000(4.49409)

Solutions to Problem Set #: ) r =.06 or r =.8 SECURITY ANALYSIS AND PORTFOLIO MANAGEMENT PVA[T 0, r.06] j 0 $8000 $8000 { {.06} t.06 &.06 (.06) 0} $8000(7.36009) $58,880.70 > $50,000 PVA[T 0, r.8] $8000(4.49409)

Debt. Last modified KW

Debt The debt markets are far more complicated and filled with jargon than the equity markets. Fixed coupon bonds, loans and bills will be our focus in this course. It's important to be aware of all of

Debt The debt markets are far more complicated and filled with jargon than the equity markets. Fixed coupon bonds, loans and bills will be our focus in this course. It's important to be aware of all of

Chapter 3: Debt financing. Albert Banal-Estanol

Corporate Finance Chapter 3: Debt financing Albert Banal-Estanol Debt issuing as part of a leverage buyout (LBO) What is an LBO? How to decide among these options? In this chapter we should talk about

Corporate Finance Chapter 3: Debt financing Albert Banal-Estanol Debt issuing as part of a leverage buyout (LBO) What is an LBO? How to decide among these options? In this chapter we should talk about

Appendix A Financial Calculations

Derivatives Demystified: A Step-by-Step Guide to Forwards, Futures, Swaps and Options, Second Edition By Andrew M. Chisholm 010 John Wiley & Sons, Ltd. Appendix A Financial Calculations TIME VALUE OF MONEY

Derivatives Demystified: A Step-by-Step Guide to Forwards, Futures, Swaps and Options, Second Edition By Andrew M. Chisholm 010 John Wiley & Sons, Ltd. Appendix A Financial Calculations TIME VALUE OF MONEY

INVESTMENTS. Instructor: Dr. Kumail Rizvi, PhD, CFA, FRM

INVESTMENTS Instructor: Dr. KEY CONCEPTS & SKILLS Understand bond values and why they fluctuate How Bond Prices Vary With Interest Rates Four measures of bond price sensitivity to interest rate Maturity

INVESTMENTS Instructor: Dr. KEY CONCEPTS & SKILLS Understand bond values and why they fluctuate How Bond Prices Vary With Interest Rates Four measures of bond price sensitivity to interest rate Maturity

CHAPTER 9 DEBT SECURITIES. by Lee M. Dunham, PhD, CFA, and Vijay Singal, PhD, CFA

CHAPTER 9 DEBT SECURITIES by Lee M. Dunham, PhD, CFA, and Vijay Singal, PhD, CFA LEARNING OUTCOMES After completing this chapter, you should be able to do the following: a Identify issuers of debt securities;

CHAPTER 9 DEBT SECURITIES by Lee M. Dunham, PhD, CFA, and Vijay Singal, PhD, CFA LEARNING OUTCOMES After completing this chapter, you should be able to do the following: a Identify issuers of debt securities;

Questions 1. What is a bond? What determines the price of this financial asset?

BOND VALUATION Bonds are debt instruments issued by corporations, as well as state, local, and foreign governments to raise funds for growth and financing of public projects. Since bonds are long-term

BOND VALUATION Bonds are debt instruments issued by corporations, as well as state, local, and foreign governments to raise funds for growth and financing of public projects. Since bonds are long-term

CHAPTER 5 Bonds and Their Valuation

5-1 5-2 CHAPTER 5 Bonds and Their Valuation Key features of bonds Bond valuation Measuring yield Assessing risk Key Features of a Bond 1 Par value: Face amount; paid at maturity Assume $1,000 2 Coupon

5-1 5-2 CHAPTER 5 Bonds and Their Valuation Key features of bonds Bond valuation Measuring yield Assessing risk Key Features of a Bond 1 Par value: Face amount; paid at maturity Assume $1,000 2 Coupon

Disclaimer: This resource package is for studying purposes only EDUCATION

Disclaimer: This resource package is for studying purposes only EDUCATION Chapter 6: Valuing stocks Bond Cash Flows, Prices, and Yields - Maturity date: Final payment date - Term: Time remaining until

Disclaimer: This resource package is for studying purposes only EDUCATION Chapter 6: Valuing stocks Bond Cash Flows, Prices, and Yields - Maturity date: Final payment date - Term: Time remaining until

The following pages explain some commonly used bond terminology, and provide information on how bond returns are generated.

1 2 3 Corporate bonds play an important role in a diversified portfolio. The opportunity to receive regular income streams from corporate bonds can be appealing to investors, and the focus on capital preservation

1 2 3 Corporate bonds play an important role in a diversified portfolio. The opportunity to receive regular income streams from corporate bonds can be appealing to investors, and the focus on capital preservation

CHAPTER 16: MANAGING BOND PORTFOLIOS

CHAPTER 16: MANAGING BOND PORTFOLIOS 1. The percentage change in the bond s price is: Duration 7.194 y = 0.005 = 0.0327 = 3.27% or a 3.27% decline. 1+ y 1.10 2. a. YTM = 6% (1) (2) (3) (4) (5) PV of CF

CHAPTER 16: MANAGING BOND PORTFOLIOS 1. The percentage change in the bond s price is: Duration 7.194 y = 0.005 = 0.0327 = 3.27% or a 3.27% decline. 1+ y 1.10 2. a. YTM = 6% (1) (2) (3) (4) (5) PV of CF

The Cost of Capital. Principles Applied in This Chapter. The Cost of Capital: An Overview

The Cost of Capital Chapter 14 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value. Principle

The Cost of Capital Chapter 14 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value. Principle

The Cost of Capital. Chapter 14

The Cost of Capital Chapter 14 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value. Principle

The Cost of Capital Chapter 14 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value. Principle

Chapter 2: BASICS OF FIXED INCOME SECURITIES

Chapter 2: BASICS OF FIXED INCOME SECURITIES 2.1 DISCOUNT FACTORS 2.1.1 Discount Factors across Maturities 2.1.2 Discount Factors over Time 2.1 DISCOUNT FACTORS The discount factor between two dates, t

Chapter 2: BASICS OF FIXED INCOME SECURITIES 2.1 DISCOUNT FACTORS 2.1.1 Discount Factors across Maturities 2.1.2 Discount Factors over Time 2.1 DISCOUNT FACTORS The discount factor between two dates, t

CFAspace. CFA Level I. Provided by APF. Academy of Professional Finance 专业金融学院 FIXED INCOME: Lecturer: Nan Chen

CFAspace Provided by APF CFA Level I FIXED INCOME: Introduction to the Valuation of Debt Securities Lecturer: Nan Chen Framework Estimate CFs: Coupon and Principal 1. Steps in Bond Valuation Process Determine

CFAspace Provided by APF CFA Level I FIXED INCOME: Introduction to the Valuation of Debt Securities Lecturer: Nan Chen Framework Estimate CFs: Coupon and Principal 1. Steps in Bond Valuation Process Determine

FINA Homework 2

FINA3313-005 Homework 2 Chapter 04 Measuring Corporate Performance True / False Questions 1. The higher the times interest earned ratio, the higher the interest expense. 2. The asset turnover ratio and

FINA3313-005 Homework 2 Chapter 04 Measuring Corporate Performance True / False Questions 1. The higher the times interest earned ratio, the higher the interest expense. 2. The asset turnover ratio and

Chapter 5. Valuing Bonds

Chapter 5 Valuing Bonds 5-2 Topics Covered Bond Characteristics Reading the financial pages after introducing the terminologies of bonds in the next slide (p.119 Figure 5-2) Bond Prices and Yields Bond

Chapter 5 Valuing Bonds 5-2 Topics Covered Bond Characteristics Reading the financial pages after introducing the terminologies of bonds in the next slide (p.119 Figure 5-2) Bond Prices and Yields Bond

BOND VALUATION. YTM Of An n-year Zero-Coupon Bond

BOND VALUATION BOND VALUATIONS BOND: A security sold by governments and corporations to raise money from investors today in exchange for promised future payments 1. ZERO COUPON BONDS ZERO COUPON BONDS:

BOND VALUATION BOND VALUATIONS BOND: A security sold by governments and corporations to raise money from investors today in exchange for promised future payments 1. ZERO COUPON BONDS ZERO COUPON BONDS:

MFE8812 Bond Portfolio Management

MFE8812 Bond Portfolio Management William C. H. Leon Nanyang Business School January 16, 2018 1 / 63 William C. H. Leon MFE8812 Bond Portfolio Management 1 Overview Value of Cash Flows Value of a Bond

MFE8812 Bond Portfolio Management William C. H. Leon Nanyang Business School January 16, 2018 1 / 63 William C. H. Leon MFE8812 Bond Portfolio Management 1 Overview Value of Cash Flows Value of a Bond

Chapter. Bond Basics, I. Prices and Yields. Bond Basics, II. Straight Bond Prices and Yield to Maturity. The Bond Pricing Formula

Chapter 10 Bond Prices and Yields Bond Basics, I. A Straight bond is an IOU that obligates the issuer of the bond to pay the holder of the bond: A fixed sum of money (called the principal, par value, or

Chapter 10 Bond Prices and Yields Bond Basics, I. A Straight bond is an IOU that obligates the issuer of the bond to pay the holder of the bond: A fixed sum of money (called the principal, par value, or

A CLEAR UNDERSTANDING OF THE INDUSTRY

A CLEAR UNDERSTANDING OF THE INDUSTRY IS CFA INSTITUTE INVESTMENT FOUNDATIONS RIGHT FOR YOU? Investment Foundations is a certificate program designed to give you a clear understanding of the investment

A CLEAR UNDERSTANDING OF THE INDUSTRY IS CFA INSTITUTE INVESTMENT FOUNDATIONS RIGHT FOR YOU? Investment Foundations is a certificate program designed to give you a clear understanding of the investment

SECURITY VALUATION BOND VALUATION

SECURITY VALUATION BOND VALUATION When a corporation (or the government) wants to borrow money, it often sells a bond. An investor gives the corporation money for the bond, and the corporation promises

SECURITY VALUATION BOND VALUATION When a corporation (or the government) wants to borrow money, it often sells a bond. An investor gives the corporation money for the bond, and the corporation promises

Lecture 9. Basics on Swaps

Lecture 9 Basics on Swaps Agenda: 1. Introduction to Swaps ~ Definition: ~ Basic functions ~ Comparative advantage: 2. Swap quotes and LIBOR zero rate ~ Interest rate swap is combination of two bonds:

Lecture 9 Basics on Swaps Agenda: 1. Introduction to Swaps ~ Definition: ~ Basic functions ~ Comparative advantage: 2. Swap quotes and LIBOR zero rate ~ Interest rate swap is combination of two bonds:

Introduction to Bonds. Part One describes fixed-income market analysis and the basic. techniques and assumptions are required.

PART ONE Introduction to Bonds Part One describes fixed-income market analysis and the basic concepts relating to bond instruments. The analytic building blocks are generic and thus applicable to any market.

PART ONE Introduction to Bonds Part One describes fixed-income market analysis and the basic concepts relating to bond instruments. The analytic building blocks are generic and thus applicable to any market.

CHAPTER 14. Bond Prices and Yields INVESTMENTS BODIE, KANE, MARCUS. Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved.

CHAPTER 14 Bond Prices and Yields INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. INVESTMENTS BODIE, KANE, MARCUS 14-2 Bond Characteristics

CHAPTER 14 Bond Prices and Yields INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. INVESTMENTS BODIE, KANE, MARCUS 14-2 Bond Characteristics

BOND NOTES BOND TERMS

BOND NOTES DEFINITION: A bond is a commitment by the issuer (the company that is borrowing the money) to pay a rate of interest for a pre-determined period of time. By selling bonds, the issuing company

BOND NOTES DEFINITION: A bond is a commitment by the issuer (the company that is borrowing the money) to pay a rate of interest for a pre-determined period of time. By selling bonds, the issuing company

BBK3413 Investment Analysis

BBK3413 Investment Analysis Topic 4 Fixed Income Securities www.notes638.wordpress.com Content 7.1 CHARACTERISTICS OF BOND 7.2 RISKS ASSOCIATED WITH BONDS 7.3 BOND PRICING 7.4 BOND YIELDS 7.5 VOLATILITY

BBK3413 Investment Analysis Topic 4 Fixed Income Securities www.notes638.wordpress.com Content 7.1 CHARACTERISTICS OF BOND 7.2 RISKS ASSOCIATED WITH BONDS 7.3 BOND PRICING 7.4 BOND YIELDS 7.5 VOLATILITY

Savings and Investment. July 23, 2014

Savings and Investment July 23, 2014 Personal Financial Planning Process The personal financial planning process includes four main elements: Setting financial goals; Financial assessment; Developing and

Savings and Investment July 23, 2014 Personal Financial Planning Process The personal financial planning process includes four main elements: Setting financial goals; Financial assessment; Developing and

CHAPTER 17: MORTGAGE BASICS (Ch.17, sects.17.1 & 17.2 only)

") CHAPTER 17: MORTGAGE BASICS (Ch.17, sects.17.1 & 17.2 only) The Four Rules of Loan Payment & Balance Computation... Rule 1: The interest owed in each payment equals the applicable interest rate times the

CHAPTER 17: MORTGAGE BASICS (Ch.17, sects.17.1 & 17.2 only) The Four Rules of Loan Payment & Balance Computation... Rule 1: The interest owed in each payment equals the applicable interest rate times the

Chapter 4 Interest Rate Measurement and Behavior Chapter 5 The Risk and Term Structure of Interest Rates

Chapter 4 Interest Rate Measurement and Behavior Chapter 5 The Risk and Term Structure of Interest Rates Fisher Effect (risk-free rate) Interest rate has 2 components: (1) real rate (2) inflation premium

Chapter 4 Interest Rate Measurement and Behavior Chapter 5 The Risk and Term Structure of Interest Rates Fisher Effect (risk-free rate) Interest rate has 2 components: (1) real rate (2) inflation premium

Economic Equivalence. Lecture 5 Shahid Iqbal

Economic Equivalence Lecture 5 Shahid Iqbal What do we mean by economic equivalence? Why do we need to establish an economic equivalence? How do we establish an economic equivalence? Economic equivalence

Economic Equivalence Lecture 5 Shahid Iqbal What do we mean by economic equivalence? Why do we need to establish an economic equivalence? How do we establish an economic equivalence? Economic equivalence

SECTION A: MULTIPLE CHOICE QUESTIONS. 1. All else equal, which of the following would most likely increase the yield to maturity on a debt security?

SECTION A: MULTIPLE CHOICE QUESTIONS 2 (40 MARKS) 1. All else equal, which of the following would most likely increase the yield to maturity on a debt security? 1. Put option. 2. Conversion option. 3.

SECTION A: MULTIPLE CHOICE QUESTIONS 2 (40 MARKS) 1. All else equal, which of the following would most likely increase the yield to maturity on a debt security? 1. Put option. 2. Conversion option. 3.

Interest Rate Forwards and Swaps

Interest Rate Forwards and Swaps 1 Outline PART ONE Chapter 1: interest rate forward contracts and their pricing and mechanics 2 Outline PART TWO Chapter 2: basic and customized swaps and their pricing

Interest Rate Forwards and Swaps 1 Outline PART ONE Chapter 1: interest rate forward contracts and their pricing and mechanics 2 Outline PART TWO Chapter 2: basic and customized swaps and their pricing

INTERNATIONAL BOND MARKETS

INTERNATIONAL BOND MARKETS International Bond Markets The bond market (debt, credit, or fixed income market) is the financial market where participants buy and sell debt securities, usually bonds. Size

INTERNATIONAL BOND MARKETS International Bond Markets The bond market (debt, credit, or fixed income market) is the financial market where participants buy and sell debt securities, usually bonds. Size

Outline Types Measures Spot rate Bond pricing Bootstrap Forward rates FRA Duration Convexity Term structure. Interest Rates.

Haipeng Xing Department of Applied Mathematics and Statistics Outline 1 Types of interest rates 2 Measuring interest rates 3 The n-year spot rate 4 ond pricing 5 Determining treasury zero rates the bootstrap

Haipeng Xing Department of Applied Mathematics and Statistics Outline 1 Types of interest rates 2 Measuring interest rates 3 The n-year spot rate 4 ond pricing 5 Determining treasury zero rates the bootstrap

Solutions For the benchmark maturity sectors in the United States Treasury bill markets,

FIN 684 Professor Robert Hauswald Fixed-Income Analysis Kogod School of Business, AU Solutions 1 1. For the benchmark maturity sectors in the United States Treasury bill markets, Bloomberg reported the

FIN 684 Professor Robert Hauswald Fixed-Income Analysis Kogod School of Business, AU Solutions 1 1. For the benchmark maturity sectors in the United States Treasury bill markets, Bloomberg reported the

Review for Exam #2. Review for Exam #2. Exam #2. Don t Forget: Scan Sheet Calculator Pencil Picture ID Cheat Sheet.

Review for Exam #2 Exam #2 Don t Forget: Scan Sheet Calculator Pencil Picture ID Cheat Sheet Things To Do Study both the notes and the book. Do suggested problems. Do more problems! Be comfortable with

Review for Exam #2 Exam #2 Don t Forget: Scan Sheet Calculator Pencil Picture ID Cheat Sheet Things To Do Study both the notes and the book. Do suggested problems. Do more problems! Be comfortable with

Bonds and Their Value

140 Yost Rocks, Inc. wants to borrow money, and it decides to issue bonds. Each bondholder lends the firm money today for 30 years at 12 percent interest.yost Rocks pays each bondholder $120 per year and

140 Yost Rocks, Inc. wants to borrow money, and it decides to issue bonds. Each bondholder lends the firm money today for 30 years at 12 percent interest.yost Rocks pays each bondholder $120 per year and

Summary. Chapter 6. Bond Valuation

Summary Chapter 6 Bond Valuation Learning objectives: This chapter will help you understand the important concepts relating to bonds and bond investing including bonds valuation. It will also take you

Summary Chapter 6 Bond Valuation Learning objectives: This chapter will help you understand the important concepts relating to bonds and bond investing including bonds valuation. It will also take you

FINC3019 FIXED INCOME SECURITIES

FINC3019 FIXED INCOME SECURITIES WEEK 1 BONDS o Debt instrument requiring the issuer to repay the lender the amount borrowed + interest over specified time period o Plain vanilla (typical) bond:! Fixed

FINC3019 FIXED INCOME SECURITIES WEEK 1 BONDS o Debt instrument requiring the issuer to repay the lender the amount borrowed + interest over specified time period o Plain vanilla (typical) bond:! Fixed

[Image of Investments: Analysis and Behavior textbook]

![[Image of Investments: Analysis and Behavior textbook]](/thumbs/83/88392803.jpg "[Image of Investments: Analysis and Behavior textbook]") Finance 527: Lecture 19, Bond Valuation V1 [John Nofsinger]: This is the first video for bond valuation. The previous bond topics were more the characteristics of bonds and different kinds of bonds. And

Finance 527: Lecture 19, Bond Valuation V1 [John Nofsinger]: This is the first video for bond valuation. The previous bond topics were more the characteristics of bonds and different kinds of bonds. And

ACC 501 Solved MCQ'S For MID & Final Exam 1. Which of the following is an example of positive covenant? Maintaining firm s working capital at or above some specified minimum level Furnishing audited financial

ACC 501 Solved MCQ'S For MID & Final Exam 1. Which of the following is an example of positive covenant? Maintaining firm s working capital at or above some specified minimum level Furnishing audited financial

Swap Markets CHAPTER OBJECTIVES. The specific objectives of this chapter are to: describe the types of interest rate swaps that are available,

15 Swap Markets CHAPTER OBJECTIVES The specific objectives of this chapter are to: describe the types of interest rate swaps that are available, explain the risks of interest rate swaps, identify other

15 Swap Markets CHAPTER OBJECTIVES The specific objectives of this chapter are to: describe the types of interest rate swaps that are available, explain the risks of interest rate swaps, identify other

I. Interest Rate Sensitivity

University of California, Merced ECO 163-Economics of Investments Chapter 11 Lecture otes I. Interest Rate Sensitivity Professor Jason Lee We saw in the previous chapter that there exists a negative relationship

University of California, Merced ECO 163-Economics of Investments Chapter 11 Lecture otes I. Interest Rate Sensitivity Professor Jason Lee We saw in the previous chapter that there exists a negative relationship

Lecture 7 Foundations of Finance

Lecture 7: Fixed Income Markets. I. Reading. II. Money Market. III. Long Term Credit Markets. IV. Repurchase Agreements (Repos). 0 Lecture 7: Fixed Income Markets. I. Reading. A. BKM, Chapter 2, Sections

Lecture 7: Fixed Income Markets. I. Reading. II. Money Market. III. Long Term Credit Markets. IV. Repurchase Agreements (Repos). 0 Lecture 7: Fixed Income Markets. I. Reading. A. BKM, Chapter 2, Sections

Chapter 3 Mathematics of Finance

Chapter 3 Mathematics of Finance Section R Review Important Terms, Symbols, Concepts 3.1 Simple Interest Interest is the fee paid for the use of a sum of money P, called the principal. Simple interest

Chapter 3 Mathematics of Finance Section R Review Important Terms, Symbols, Concepts 3.1 Simple Interest Interest is the fee paid for the use of a sum of money P, called the principal. Simple interest

Investments 4: Bond Basics

Personal Finance: Another Perspective Investments 4: Bond Basics Updated 2017/06/28 1 Objectives A. Understand risk and return for bonds B. Understand bond terminology C. Understand the major types of

Personal Finance: Another Perspective Investments 4: Bond Basics Updated 2017/06/28 1 Objectives A. Understand risk and return for bonds B. Understand bond terminology C. Understand the major types of

BUSI 370 Business Finance

Review Session 2 February 7 th, 2016 Road Map 1. BONDS 2. COMMON SHARES 3. PREFERRED SHARES 4. TREASURY BILLS (T Bills) ANSWER KEY WITH COMMENTS 1. BONDS // Calculate the price of a ten-year annual pay

Review Session 2 February 7 th, 2016 Road Map 1. BONDS 2. COMMON SHARES 3. PREFERRED SHARES 4. TREASURY BILLS (T Bills) ANSWER KEY WITH COMMENTS 1. BONDS // Calculate the price of a ten-year annual pay

Chapter 6 Homework Math 373 Fall 2014

Chapter 6 Homework Math 373 Fall 2014 Chapter 6, Section 2 1. Changyue purchases a zero coupon bond for 600. The bond will mature in 8 years for 1000. Calculate the annual effective yield rate earned by

Chapter 6 Homework Math 373 Fall 2014 Chapter 6, Section 2 1. Changyue purchases a zero coupon bond for 600. The bond will mature in 8 years for 1000. Calculate the annual effective yield rate earned by

COPYRIGHTED MATERIAL FEATURES OF DEBT SECURITIES CHAPTER 1 I. INTRODUCTION

CHAPTER 1 FEATURES OF DEBT SECURITIES I. INTRODUCTION In investment management, the most important decision made is the allocation of funds among asset classes. The two major asset classes are equities

CHAPTER 1 FEATURES OF DEBT SECURITIES I. INTRODUCTION In investment management, the most important decision made is the allocation of funds among asset classes. The two major asset classes are equities

Bond Prices and Yields

Bond Prices and Yields BKM 10.1-10.4 Eric M. Aldrich Econ 133 UC Santa Cruz Bond Basics A bond is a financial asset used to facilitate borrowing and lending. A borrower has an obligation to make pre-specified

Bond Prices and Yields BKM 10.1-10.4 Eric M. Aldrich Econ 133 UC Santa Cruz Bond Basics A bond is a financial asset used to facilitate borrowing and lending. A borrower has an obligation to make pre-specified

Bond Valuation. FINANCE 100 Corporate Finance

Bond Valuation FINANCE 100 Corporate Finance Prof. Michael R. Roberts 1 Bond Valuation An Overview Introduction to bonds and bond markets» What are they? Some examples Zero coupon bonds» Valuation» Interest

Bond Valuation FINANCE 100 Corporate Finance Prof. Michael R. Roberts 1 Bond Valuation An Overview Introduction to bonds and bond markets» What are they? Some examples Zero coupon bonds» Valuation» Interest

1. The real risk-free rate is the increment to purchasing power that the lender earns in order to induce him or her to forego current consumption.

Chapter 02 Determinants of Interest Rates True / False Questions 1. The real risk-free rate is the increment to purchasing power that the lender earns in order to induce him or her to forego current consumption.

Chapter 02 Determinants of Interest Rates True / False Questions 1. The real risk-free rate is the increment to purchasing power that the lender earns in order to induce him or her to forego current consumption.

Chapter 4. The Valuation of Long-Term Securities

Chapter 4 The Valuation of Long-Term Securities 4-1 Pearson Education Limited 2004 Fundamentals of Financial Management, 12/e Created by: Gregory A. Kuhlemeyer, Ph.D. Carroll College, Waukesha, WI After

Chapter 4 The Valuation of Long-Term Securities 4-1 Pearson Education Limited 2004 Fundamentals of Financial Management, 12/e Created by: Gregory A. Kuhlemeyer, Ph.D. Carroll College, Waukesha, WI After

CHAPTER 4 TIME VALUE OF MONEY

CHAPTER 4 TIME VALUE OF MONEY 1 Learning Outcomes LO.1 Identify various types of cash flow patterns (streams) seen in business. LO.2 Compute the future value of different cash flow streams. Explain the

CHAPTER 4 TIME VALUE OF MONEY 1 Learning Outcomes LO.1 Identify various types of cash flow patterns (streams) seen in business. LO.2 Compute the future value of different cash flow streams. Explain the

Measuring Interest Rates. Interest Rates Chapter 4. Continuous Compounding (Page 77) Types of Rates

Types of Rates") Interest Rates Chapter 4 Measuring Interest Rates The compounding frequency used for an interest rate is the unit of measurement The difference between quarterly and annual compounding is analogous to

Interest Rates Chapter 4 Measuring Interest Rates The compounding frequency used for an interest rate is the unit of measurement The difference between quarterly and annual compounding is analogous to

Reading. Valuation of Securities: Bonds

Valuation of Securities: Bonds Econ 422: Investment, Capital & Finance University of Washington Last updated: April 11, 2010 Reading BMA, Chapter 3 http://finance.yahoo.com/bonds http://cxa.marketwatch.com/finra/marketd

Valuation of Securities: Bonds Econ 422: Investment, Capital & Finance University of Washington Last updated: April 11, 2010 Reading BMA, Chapter 3 http://finance.yahoo.com/bonds http://cxa.marketwatch.com/finra/marketd

Pricing Fixed-Income Securities

Pricing Fixed-Income Securities The Relationship Between Interest Rates and Option- Free Bond Prices Bond Prices A bond s price is the present value of the future coupon payments (CPN) plus the present

Pricing Fixed-Income Securities The Relationship Between Interest Rates and Option- Free Bond Prices Bond Prices A bond s price is the present value of the future coupon payments (CPN) plus the present

Foundations of Finance

Lecture 7: Bond Pricing, Forward Rates and the Yield Curve. I. Reading. II. Discount Bond Yields and Prices. III. Fixed-income Prices and No Arbitrage. IV. The Yield Curve. V. Other Bond Pricing Issues.

Lecture 7: Bond Pricing, Forward Rates and the Yield Curve. I. Reading. II. Discount Bond Yields and Prices. III. Fixed-income Prices and No Arbitrage. IV. The Yield Curve. V. Other Bond Pricing Issues.

Powered by TCPDF (www.tcpdf.org) 10.1 Fixed Income Securities Study Session 10 LOS 1 : Introduction (Fixed Income Security) Bonds are the type of long term obligation which pay periodic interest & repay

Powered by TCPDF (www.tcpdf.org) 10.1 Fixed Income Securities Study Session 10 LOS 1 : Introduction (Fixed Income Security) Bonds are the type of long term obligation which pay periodic interest & repay

2. A FRAMEWORK FOR FIXED-INCOME PORTFOLIO MANAGEMENT 3. MANAGING FUNDS AGAINST A BOND MARKET INDEX

2. A FRAMEWORK FOR FIXED-INCOME PORTFOLIO MANAGEMENT The four activities in the investment management process are as follows: 1. Setting the investment objectives i.e. return, risk and constraints. 2.

2. A FRAMEWORK FOR FIXED-INCOME PORTFOLIO MANAGEMENT The four activities in the investment management process are as follows: 1. Setting the investment objectives i.e. return, risk and constraints. 2.

ACC 471 Practice Problem Set #2 Fall Suggested Solutions

ACC 471 Practice Problem Set #2 Fall 2002 Suggested Solutions 1. Text Problems: 11-6 a. i. Current ield: 70 960 7 29%. ii. Yield to maturit: solving 960 35 1 1 1 000 1 for gives a ield to maturit of 4%

ACC 471 Practice Problem Set #2 Fall 2002 Suggested Solutions 1. Text Problems: 11-6 a. i. Current ield: 70 960 7 29%. ii. Yield to maturit: solving 960 35 1 1 1 000 1 for gives a ield to maturit of 4%

FINA 1082 Financial Management

FINA 1082 Financial Management Dr Cesario MATEUS Senior Lecturer in Finance and Banking Room QA259 Department of Accounting and Finance c.mateus@greenwich.ac.uk www.cesariomateus.com Contents Session 1

FINA 1082 Financial Management Dr Cesario MATEUS Senior Lecturer in Finance and Banking Room QA259 Department of Accounting and Finance c.mateus@greenwich.ac.uk www.cesariomateus.com Contents Session 1

Building a Zero Coupon Yield Curve

Building a Zero Coupon Yield Curve Clive Bastow, CFA, CAIA ABSTRACT Create and use a zero- coupon yield curve from quoted LIBOR, Eurodollar Futures, PAR Swap and OIS rates. www.elpitcafinancial.com Risk-

Building a Zero Coupon Yield Curve Clive Bastow, CFA, CAIA ABSTRACT Create and use a zero- coupon yield curve from quoted LIBOR, Eurodollar Futures, PAR Swap and OIS rates. www.elpitcafinancial.com Risk-

SOLUTIONS. Solution. The liabilities are deterministic and their value in one year will be $ = $3.542 billion dollars.

Illinois State University, Mathematics 483, Fall 2014 Test No. 1, Tuesday, September 23, 2014 SOLUTIONS 1. You are the investment actuary for a life insurance company. Your company s assets are invested

Illinois State University, Mathematics 483, Fall 2014 Test No. 1, Tuesday, September 23, 2014 SOLUTIONS 1. You are the investment actuary for a life insurance company. Your company s assets are invested

Chapter 4. Characteristics of Bonds. Chapter 4 Topic Overview. Bond Characteristics

Chapter 4 Topic Overview Chapter 4 Valuing Bond Characteristics Annual and Semi-Annual Bond Valuation Reading Bond Quotes Finding Returns on Bond Risk and Other Important Bond Valuation Relationships Bond

Chapter 4 Topic Overview Chapter 4 Valuing Bond Characteristics Annual and Semi-Annual Bond Valuation Reading Bond Quotes Finding Returns on Bond Risk and Other Important Bond Valuation Relationships Bond

Discover Financial Services InterNotes Due From 9 Months or More From Date of Issue

Page 1 of 88 PROSPECTUS SUPPLEMENT (To Prospectus dated June 26, 2015) Filed pursuant to Rule 424(b)(2) Registration Statement No. 333-205280 Discover Financial Services InterNotes Due From 9 Months or

Page 1 of 88 PROSPECTUS SUPPLEMENT (To Prospectus dated June 26, 2015) Filed pursuant to Rule 424(b)(2) Registration Statement No. 333-205280 Discover Financial Services InterNotes Due From 9 Months or

Part A: Corporate Finance

Finance: Common Body of Knowledge Review Part A: Corporate Finance Time Value of Money Financial managers always want to determine how much a periodic receipt of future cash flow is worth in today s dollars.

Finance: Common Body of Knowledge Review Part A: Corporate Finance Time Value of Money Financial managers always want to determine how much a periodic receipt of future cash flow is worth in today s dollars.

1. Why is it important for corporate managers to understand how bonds and shares are priced?

CHAPTER 4 CONCEPT REVIEW QUESTIONS 1. Why is it important for corporate managers to understand how bonds and shares are priced? Managers need to know this because (1) firms regularly issue stocks and bonds

CHAPTER 4 CONCEPT REVIEW QUESTIONS 1. Why is it important for corporate managers to understand how bonds and shares are priced? Managers need to know this because (1) firms regularly issue stocks and bonds

Mathematics of Financial Derivatives

Mathematics of Financial Derivatives Lecture 11 Solesne Bourguin bourguin@math.bu.edu Boston University Department of Mathematics and Statistics Table of contents 1. Mechanics of interest rate swaps (continued)

Mathematics of Financial Derivatives Lecture 11 Solesne Bourguin bourguin@math.bu.edu Boston University Department of Mathematics and Statistics Table of contents 1. Mechanics of interest rate swaps (continued)

MIDTERM EXAMINATION Spring 2009 ACC501- Business Finance (Session - 1)

") http://vudesk.com MIDTERM EXAMINATION Spring 2009 ACC501- Business Finance (Session - 1) Question No: 1 The debt a firm has (as a percentage of assets); the is the degree of financial leverage. More; greater

http://vudesk.com MIDTERM EXAMINATION Spring 2009 ACC501- Business Finance (Session - 1) Question No: 1 The debt a firm has (as a percentage of assets); the is the degree of financial leverage. More; greater

INTEREST RATE SWAP POLICY

INTEREST RATE SWAP POLICY I. INTRODUCTION The purpose of this Interest Rate Swap Policy (Policy) of the Riverside County Transportation Commission (RCTC) is to establish guidelines for the use and management

INTEREST RATE SWAP POLICY I. INTRODUCTION The purpose of this Interest Rate Swap Policy (Policy) of the Riverside County Transportation Commission (RCTC) is to establish guidelines for the use and management

Understanding Financial Management: A Practical Guide Problems and Answers

Understanding Financial Management: A Practical Guide Problems and Answers Chapter 1 Raising Funds and Cost of Capital 1.1 Financial Markets 1. What is the difference between a financial market and a financial

Understanding Financial Management: A Practical Guide Problems and Answers Chapter 1 Raising Funds and Cost of Capital 1.1 Financial Markets 1. What is the difference between a financial market and a financial

Lecture 20: Bond Portfolio Management. I. Reading. A. BKM, Chapter 16, Sections 16.1 and 16.2.

Lecture 20: Bond Portfolio Management. I. Reading. A. BKM, Chapter 16, Sections 16.1 and 16.2. II. Risks associated with Fixed Income Investments. A. Reinvestment Risk. 1. If an individual has a particular

Lecture 20: Bond Portfolio Management. I. Reading. A. BKM, Chapter 16, Sections 16.1 and 16.2. II. Risks associated with Fixed Income Investments. A. Reinvestment Risk. 1. If an individual has a particular

20. Investing 4: Understanding Bonds

20. Investing 4: Understanding Bonds Introduction The purpose of an investment portfolio is to help individuals and families meet their financial goals. These goals differ from person to person and change

20. Investing 4: Understanding Bonds Introduction The purpose of an investment portfolio is to help individuals and families meet their financial goals. These goals differ from person to person and change