IEOR E4602: Quantitative Risk Management

|

|

|

- Ashlynn Lyons

- 6 years ago

- Views:

Transcription

1 IEOR E4602: Quantitative Risk Management Basic Concepts and Techniques of Risk Management Martin Haugh Department of Industrial Engineering and Operations Research Columbia University References: Chapter 2 of 2 nd ed. of MFE by McNeil, Frey and Embrechts.

2 Outline Risk Factors and Loss Distributions Linear Approximations to the Loss Function Conditional and Unconditional Loss Distributions Risk Measurement Scenario Analysis and Stress Testing Value-at-Risk Expected Shortfall (ES) Standard Techniques for Risk Measurement Evaluating Risk Measurement Techniques Other Considerations 2 (Section 0)

3 Risk Factors and Loss Distributions Notation (to be used throughout the course): a fixed period of time such as 1 day or 1 week. Let V t be the value of a portfolio at time t. So portfolio loss between t and (t + 1) is given by L t+1 := (V t+1 V t ) - note that a loss is a positive quantity - it (of course) depends on change in values of the securities. More generally, may wish to define a set of d risk factors Z t := (Z t,1,..., Z t,d ) so that V t = f (t, Z t ). for some function f : R + R d R. 3 (Section 1)

4 Risk Factors and Loss Distributions e.g. In a stock portfolio might take the stock prices or some function of the stock prices as our risk factors. e.g. In an options portfolio Z t might contain stock factors together with implied volatility and interest rate factors. Let X t := Z t Z t 1 denote the change in values of the risk factors between times t and t + 1. Then have L t+1 (X t+1 ) = (f (t + 1, Z t + X t+1 ) f (t, Z t )) Given the value of Z t, the distribution of L t+1 depends only on the distribution of X t+1. Estimating the (conditional) distribution of X t+1 is then a very important goal in much of risk management. 4 (Section 1)

5 Linear Approximations to the Loss Function Assuming f (, ) is differentiable, can use a first order Taylor expansion to approximate L t+1 : ˆL t+1 (X t+1 ) := ( f t (t, Z t ) + ) d f zi (t, Z t ) X t+1,i i=1 (1) where f -subscripts denote partial derivatives. First order approximation commonly used when X t+1 is likely to be small - often the case when is small, e.g. = 1/365 1 day, and market not too volatile. Second and higher order approximations also based on Taylor s Theorem can also be used. Important to note, however, that if X t+1 is likely to be very large then Taylor approximations can fail. 5 (Section 1)

6 Conditional and Unconditional Loss Distributions Important to distinguish between the conditional and unconditional loss distributions. Consider the series X t of risk factor changes and assume that they form a stationary time series with stationary distribution F X. Let F t denote all information available in the system at time t including in particular {X s : s t}. Definition: The unconditional loss distribution is the distribution of L t+1 given the time t composition of the portfolio and assuming the CDF of X t+1 is given by F X. Definition: The conditional loss distribution is the distribution of L t+1 given the time t composition of the portfolio and conditional on the information in F t. 6 (Section 1)

7 Conditional and Unconditional Loss Distributions If the X t s are IID then the conditional and unconditional distributions coincide. For long time horizons, e.g. = 6 months, we might be more inclined to use the unconditional loss distribution. However, for short horizons, e.g. 1 day or 10 days, then the conditional loss distribution is clearly the appropriate distribution - true in particular in times of high market volatility when the unconditional distribution would bear little resemblance to the true conditional distribution. 7 (Section 1)

8 Example: A Stock Portfolio Consider a portfolio of d stocks with S t,i denoting time t price of the i th stock and λ i denoting number of units of i th stock. Take log stock prices as risk factors so X t+1,i = ln S t+1,i ln S t,i and L t+1 Linear approximation satisfies d ( = λ i S t,i e X t+1,i 1 ). i=1 where ω t,i ˆL t+1 d d = λ i S t,i X t+1,i = V t ω t,i X t+1,i i=1 i=1 := λ i S t,i /V t is the i th portfolio weight. If E[X t+1,i ] = µ and Covar(X t+1,i ) = Σ, then E t [ˆLt+1 ] = V t ω µ and Var t (ˆLt+1 ) = V 2 t ω Σω. 8 (Section 1)

9 Example: An Options Portfolio Recall the Black-Scholes formula for time t price of a European call option with strike K and maturity T on a non-dividend paying stock satisfies C(S t, t, σ) = S t Φ(d 1 ) e r(t t) KΦ(d 2 ) and where: where d 1 = log ( S t K ) + (r + σ 2 /2)(T t) σ T t d 2 = d 1 σ T t Φ( ) is the standard normal distribution CDF S t = time t price of underlying security r = continuously compounded risk-free interest rate. In practice use an implied volatility, σ(k, T, t), that depends on strike, maturity and current time, t. 9 (Section 1)

10 Example: An Options Portfolio Consider a portfolio of European options all on the same underlying security. If the portfolio contains d different options with a position of λ i in the i th option, then L t+1 = λ 0 (S t+1 S t ) d λ i (C(S t+1, t + 1, σ(k i, T i, t + 1) C(S t, t, σ(k i, T i, t))) i=1 where λ 0 is the position in the underlying security. Note that by put-call parity we can assume that all options are call options. Can also use linear approximation technique to approximate L t+1 - would result in a delta-vega-theta approximation. For derivatives portfolios, the linear approximation based on 1 st order Greeks is often inadequate - 2 nd order approximations involving gamma, volga and vanna might then be used but see earlier warning regarding use of Taylor approximations. 10 (Section 1)

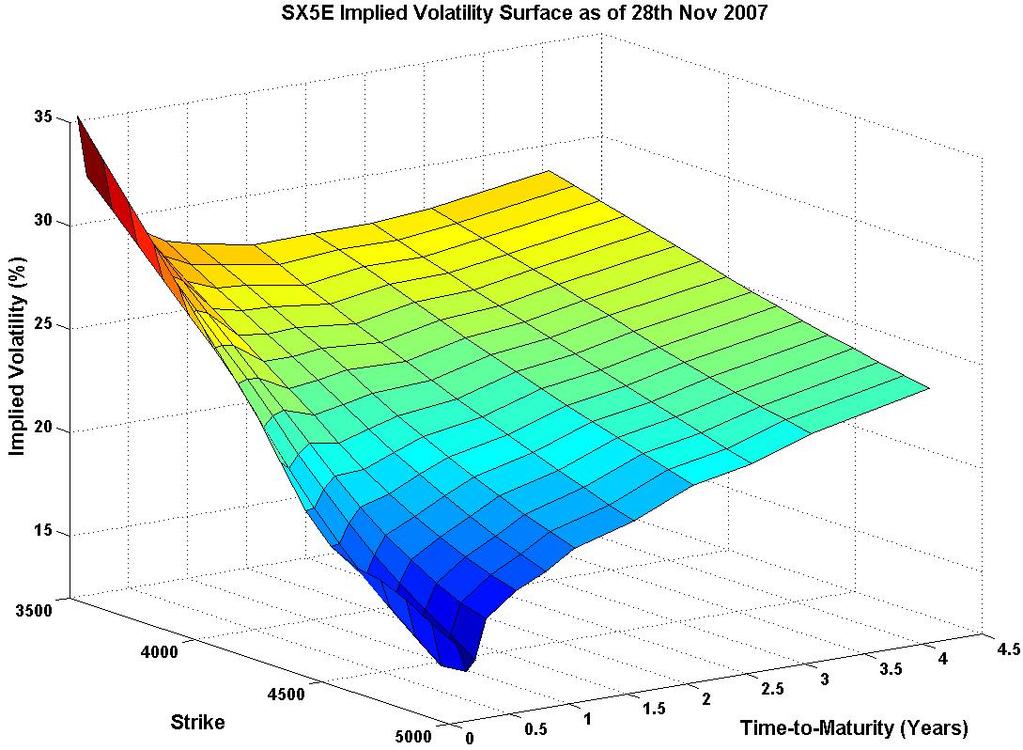

11 Risk Factors in the Options Portfolio Can again take log stock prices as risk factors but not clear how to handle the implied volatilities. There are several possibilities: 1. Assume the σ(k, T, t) s simply do not change - not very satisfactory but commonly assumed when historical simulation is used to approximate the loss distribution and historical data on the changes in implied volatilities are not available. 2. Let each σ(k, T, t) be a separate factor. Not good for two reasons: (a) It introduces a large number of factors. (b) Implied volatilities are not free to move independently since no-arbitrage assumption imposes strong restrictions on how volatility surface may move. Therefore important to choose factors in such a way that no-arbitrage restrictions are easily imposed when we estimate the loss distribution. 11 (Section 1)

12 Risk Factors in the Options Portfolio 3. In light of previous point, it may be a good idea to parameterize the volatility surface with just a few parameters - and assume that only those parameters can move from one period to the next - parameterization should be so that no-arbitrage restrictions are easy to enforce. 4. Use dimension reduction techniques such as principal components analysis (PCA) to identify just two or three factors that explain most of the movements in the volatility surface. 12 (Section 1)

13

14 Example: A Bond Portfolio Consider a portfolio containing quantities of d different default-free zero-coupon bonds. Thei th bond has price P t,i, maturity T i and face value 1. s t,ti is the continuously compounded spot interest rate for maturity T i so that P t,i = exp( s t,ti (T i t)). There are λ i units of i th bond in the portfolio so total portfolio value given by V t = d λ i exp( s t,ti (T i t)). i=1 14 (Section 1)

15 Example: A Bond Portfolio Assume now only parallel changes in the spot rate curve are possible - while unrealistic, a common assumption in practice - this is the assumption behind the use of duration and convexity. Then if spot curve moves by δ the portfolio loss satisfies L t+1 = d i=1 λ i ( e (s t+,t i +δ)(t i t ) e s t,t i (T i t) ) d λ i (s t,ti (T i t) (s t+,ti + δ)(t i t )). i=1 Therefore have a single risk factor, δ. 15 (Section 1)

16 Approaches to Risk Measurement 1. Notional Amount Approach. 2. Factor Sensitivity Measures. 3. Scenario Approach. 4. Measures based on loss distribution, e.g. Value-at-Risk (VaR) or Conditional Value-at-Risk (CVaR). 16 (Section 2)

17 An Example of Factor Sensitivity Measures: the Greeks Scenario analysis for derivatives portfolios is often combined with the Greeks to understand the riskiness of a portfolio - and sometimes to perform a P&L attribution. Suppose then we have a portfolio of options and futures - all written on the same underlying security. Portfolio value is the sum of values of individual security positions - and the same is true for the portfolio Greeks, e.g. the portfolio delta, portfolio gamma and portfolio vega. Why? Consider now a single option in the portfolio with price C(S, σ,...). Will use a delta-gamma-vega approximation to estimate risk of the position - but approximation also applies (why?) to the entire portfolio. Note approximation only holds for small moves in underlying risk factors - a very important observation that is lost on many people! 17 (Section 2)

18 Delta-Gamma-Vega Approximations to Option Prices A simple application of Taylor s Theorem yields C(S + S, σ + σ) C(S, σ) + S C S ( S)2 2 C C + σ S 2 σ Therefore obtain = C(S, σ) + S δ ( S)2 Γ + σ vega. P&L δ S + Γ 2 ( S)2 + vega σ = delta P&L + gamma P&L + vega P&L. When σ = 0, obtain the well-known delta-gamma approximation - often used, for example, in historical Value-at-Risk (VaR) calculations. Can also write P&L δs ( ) S + ΓS 2 S 2 ( ) 2 S + vega σ S = ESP Return + $ Gamma Return 2 + vega σ (2) where ESP denotes the equivalent stock position or dollar delta. 18 (Section 2)

19 Scenario Analysis and Stress Testing Stress testing an options portfolio written on the Eurostoxx (Section 2)

20 Scenario Analysis and Stress Testing In general we want to stress the risk factors in our portfolio. Therefore very important to understand the dynamics of the risk factors. e.g. The implied volatility surface almost never experiences parallel shifts. Why? - In fact changes in volatility surface tend to follow a square root of time rule. When stressing a portfolio, it is also important to understand what risk factors the portfolio is exposed to. e.g. A portfolio may be neutral with respect to the two most important" risk factors but have very significant exposure to a third risk factor - Important then to conduct stresses of that third risk factor - Especially if the trader or portfolio manager knows what stresses are applied! 20 (Section 2)

21

22 Value-at-Risk Value-at-Risk (VaR) the most widely (mis-)used risk measure in the financial industry. Despite the many weaknesses of VaR, financial institutions are required to use it under the Basel II capital-adequacy framework. And many institutions routinely report VaR numbers to shareholders, investors or regulatory authorities. VaR is calculated from the loss distribution - could be conditional or unconditional - could be a true loss distribution or some approximation to it. Will assume that horizon has been fixed so that L represents portfolio loss over time interval. Will use F L ( ) to denote the CDF of L. 22 (Section 2)

23 Value-at-Risk Definition: Let F : R [0, 1] be an arbitrary CDF. Then for α (0, 1) the α-quantile of F is defined by q α (F) := inf{x R : F(x) α}. If F is continuous and strictly increasing, then q α (F) = F 1 (α). For a random variable L with CDF F L ( ), will often write q α (L) instead of q α (F L ). Since any CDF is by definition right-continuous, immediately obtain the following result: Lemma: A point x 0 R is the α-quantile of F L if and only if (i) F L (x 0 ) α and (ii) F L (x) < α for all x < x 0. Definition: Let α (0, 1) be some fixed confidence level. Then the VaR of the portfolio loss at the confidence interval, α, is given by VaR α := q α (L), the α-quantile of the loss distribution. 23 (Section 2)

24 VaR for the Normal Distributions Because the normal CDF is both continuous and strictly increasing, it is straightforward to calculate VaR α. So suppose L N(µ, σ 2 ). Then where Φ( ) is the standard normal CDF. VaR α = µ + σφ 1 (α) (3) This follows from previous lemma if we can show F L (VaR α ) = α - but this follows immediately from (3). 24 (Section 2)

25 VaR for the t Distributions The t CDF also continuous and strictly increasing so again straightforward to calculate VaR α. So let L t(ν, µ, σ 2 ), i.e. (L µ)/σ has a standard t distribution with ν > 2 degrees-of-freedom (dof). Then VaR α = µ + σtν 1 (α) where t ν is the CDF for the t distribution with ν dof. Note that now E[L] = µ and Var(L) = νσ 2 /(ν 2). 25 (Section 2)

26 Weaknesses of VaR 1. VaR attempts to describe the entire loss distribution with just a single number! - so significant information is lost - this criticism applies to all scalar risk measures - one way around it is to report VaR α for several values of α. 2. Significant model risk attached to VaR - e.g. if loss distribution is heavy-tailed but a light-tailed, e.g. normal, distribution is assumed, then VaR α will be severely underestimated as α A fundamental problem with VaR is that it can be very difficult to estimate the loss distribution - true of all risk measures based on the loss distribution. 4. VaR is not a sub-additive risk measure so that it doesn t lend itself to aggregation. 26 (Section 2)

27 (Non-) Sub-Additivity of VaR e.g. Let L = L 1 + L 2 be the total loss associated with two portfolios, each with respective losses, L 1 and L 2. Then q α (F L ) > q α (F L1 ) + q α (F L2 ) is possible! An undesirable property as we would expect some diversification benefits when we combine two portfolios together. Such a benefit would be reflected by the combined portfolio having a smaller risk measure than the sum of the two individual risk measures. Will discuss sub-additivity property when we study coherent risk measures later in course. 27 (Section 2)

28 Advantages of VaR VaR is generally easier to estimate: True of quantile estimation in general since quantiles are not very sensitive to outliers. - not true of other risk measures such as Expected Shortfall / CVaR Even then, it becomes progressively more difficult to estimate VaR α as α 1 - may be able to use Extreme Value Theory (EVT) in these circumstances. But VaR easier to estimate only if we have correctly specified the appropriate probability model - often an unjustifiable assumption! Value of that is used in practice generally depends on the application: For credit, operational and insurance risk often on the order of 1 year. For financial risks typical values of are on the order of days. 28 (Section 2)

29 Expected Shortfall (ES) Definition: For a portfolio loss, L, satisfying E[ L ] < the expected shortfall at confidence level α (0, 1) is given by ES α := 1 1 α 1 α q u (F L ) du. (4) Relationship between ES α and VaR α is therefore given by ES α := 1 1 α 1 α VaR u (L) du - so clear that ES α (L) VaR α (L). 29 (Section 2)

30 Expected Shortfall (ES) A more well known representation of ES α (L) holds when F L is continuous: Lemma: If F L is a continuous CDF then ES α := E [L; L q α(l)] 1 α = E [L L VaR α ]. (5) Proof: See Lemma 2.13 in McNeil, Frey and Embrechts (MFE). Expected Shortfall also known as Conditional Value-at-Risk (CVaR) - when there are atoms in the distribution CVaR is defined slightly differently - but we will continue to take (4) as our definition. 30 (Section 2)

31 Example: Expected Shortfall for a Normal Distribution Can use (5) to compute expected shortfall of an N(µ, σ 2 ) random variable. We find ES α = µ + σ φ (Φ 1 (α)) 1 α where φ( ) is the PDF of the standard normal distribution. (6) 31 (Section 2)

32 Example: Expected Shortfall for a t Distribution Let L t(ν, µ, σ 2 ) so that L := (L µ)/σ has a standard t distribution with ν > 2 dof. Then easy to see that ES α (L) = µ + σes α ( L). Straightforward using direct integration to check that ES α ( L) = g ν (tν 1 (α)) 1 α ( ν + (t 1 ν (α)) 2 ) ν 1 (7) where t ν ( ) and g ν ( ) are the CDF and PDF, respectively, of the standard t distribution with ν dof. Remark: The t distribution is a much better model of stock (and other asset) returns than the normal model. In empirical studies, values of ν around 5 or 6 are often found to fit best. 32 (Section 2)

33 The Shortfall-to-Quantile Ratio Can compare VaR α and ES α by considering their ratio as α 1. Not too difficult to see that in the case of the normal distribution ES α VaR α 1 as α 1. However, in the case of the t distribution with ν > 1 dof we have ES α ν VaR α ν 1 > 1 as α (Section 2)

34 Standard Techniques for Risk Measurement 1. Historical simulation. 2. Monte-Carlo simulation. 3. Variance-covariance approach. 34 (Section 3)

35 Historical Simulation Instead of using a probabilistic model to estimate distribution of L t+1 (X t+1 ), we could estimate the distribution using a historical simulation. In particular, if we know the values of X t i+1 for i = 1,..., n, then can use this data to create a set of historical losses: { L i := L t+1 (X t i+1 ) : i = 1,..., n} - so L i is the portfolio loss that would occur if the risk factor returns on date t i + 1 were to recur. To calculate value of a given risk measure we simply assume the distribution of L t+1 (X t+1 ) is discrete and takes on each of the values L i w.p. 1/n for i = 1,..., n, i.e., we use the empirical distribution of the X t s. e.g. Suppose we wish to estimate VaR α. Then can do so by computing the α-quantile of the L i s. 35 (Section 3)

36 Historical Simulation Suppose the L i s are ordered by L n,n L 1,n. Then an estimator of VaR α (L t+1 ) is L [n(1 α)],n where [n(1 α)] is the largest integer not exceeding n(1 α). Can estimate ES α using ẼS α = L [n(1 α)],n + + L 1,n. [n(1 α)] Historical simulation approach generally difficult to apply for derivative portfolios. Why? But if applicable, then easy to apply. Historical simulation estimates the unconditional loss distribution - so not good for financial applications! 36 (Section 3)

37 Monte-Carlo Simulation Monte-Carlo approach similar to historical simulation approach. But now use some parametric distribution for the change in risk factors to generate sample portfolio losses. The (conditional or unconditional) distribution of the risk factors is estimated and m portfolio loss samples are generated. Free to make m as large as possible Subject to constraints on computational time. Variance reduction methods often employed to obtain improved estimates of required risk measures. While Monte-Carlo is an excellent tool, it is only as good as the model used to generate the data: if the estimated distribution of X t+1 is poor, then Monte-Carlo of little value. 37 (Section 3)

38 The Variance-Covariance Approach In the variance-covariance approach assume that X t+1 has a multivariate normal distribution so that X t+1 MVN (µ, Σ). Also assume the linear approximation ( ˆL t+1 (X t+1 ) := is sufficiently accurate. Then can write f t (t, Z t ) + ) d f zi (t, Z t ) X t+1,i i=1 ˆL t+1 (X t+1 ) = (c t + b t X t+1 ) for a constant scalar, c t, and constant vector, b t. Therefore obtain ) ˆL t+1 (X t+1 ) N ( c t b t µ, b t Σb t. and can calculate any risk measures of interest. 38 (Section 3)

39 The Variance-Covariance Approach This technique can be either conditional or unconditional - depends on how µ and Σ are estimated. The approach provides straightforward analytically tractable method of determining the loss distribution. But it has several weaknesses: risk factor distributions are often fat- or heavy-tailed but the normal distribution is light-tailed - this is easy to overcome as there are other multivariate distributions that are also closed under linear operations. e.g. If X t+1 has a multivariate t distribution so that X t+1 t (ν, µ, Σ) then ) ˆL t+1 (X t+1 ) t (ν, c t b t µ, b t Σb t. A more serious problem is that the linear approximation will often not work well - particularly true for portfolios of derivative securities. 39 (Section 3)

40 Evaluating Risk Measurement Techniques Important for any risk manger to constantly evaluate the reported risk measures. e.g. If daily 95% VaR is reported then should see daily losses exceeding the reported VaR approximately 95% of the time. So suppose reported VaR numbers are correct and define Y i := { 1, Li VaR i 0, otherwise where VaR i and L i are the reported VaR and realized loss for period i. If Y i s are IID, then n Y i Binomial(n,.05) i=1 Can use standard statistical tests to see if this is indeed the case. Similar tests can be constructed for ES and other risk measures. 40 (Section 3)

41 Other Considerations Risk-Neutral and Data-Generating (Empirical) Probability Measures. Data Risk. Multi-Period Risk Measures and Scaling. Model Risk. Data Aggregation. Liquidity Risk. P&L Attribution. 41 (Section 4)

Introduction to Risk Management

Introduction to Risk Management ACPM Certified Portfolio Management Program c 2010 by Martin Haugh Introduction to Risk Management We introduce some of the basic concepts and techniques of risk management

Introduction to Risk Management ACPM Certified Portfolio Management Program c 2010 by Martin Haugh Introduction to Risk Management We introduce some of the basic concepts and techniques of risk management

Statistical Methods in Financial Risk Management

Statistical Methods in Financial Risk Management Lecture 1: Mapping Risks to Risk Factors Alexander J. McNeil Maxwell Institute of Mathematical Sciences Heriot-Watt University Edinburgh 2nd Workshop on

Statistical Methods in Financial Risk Management Lecture 1: Mapping Risks to Risk Factors Alexander J. McNeil Maxwell Institute of Mathematical Sciences Heriot-Watt University Edinburgh 2nd Workshop on

The Black-Scholes Model

IEOR E4706: Foundations of Financial Engineering c 2016 by Martin Haugh The Black-Scholes Model In these notes we will use Itô s Lemma and a replicating argument to derive the famous Black-Scholes formula

IEOR E4706: Foundations of Financial Engineering c 2016 by Martin Haugh The Black-Scholes Model In these notes we will use Itô s Lemma and a replicating argument to derive the famous Black-Scholes formula

IEOR E4602: Quantitative Risk Management

IEOR E4602: Quantitative Risk Management Risk Measures Martin Haugh Department of Industrial Engineering and Operations Research Columbia University Email: martin.b.haugh@gmail.com Reference: Chapter 8

IEOR E4602: Quantitative Risk Management Risk Measures Martin Haugh Department of Industrial Engineering and Operations Research Columbia University Email: martin.b.haugh@gmail.com Reference: Chapter 8

Calculating VaR. There are several approaches for calculating the Value at Risk figure. The most popular are the

VaR Pro and Contra Pro: Easy to calculate and to understand. It is a common language of communication within the organizations as well as outside (e.g. regulators, auditors, shareholders). It is not really

VaR Pro and Contra Pro: Easy to calculate and to understand. It is a common language of communication within the organizations as well as outside (e.g. regulators, auditors, shareholders). It is not really

Example 5 European call option (ECO) Consider an ECO over an asset S with execution date T, price S T at time T and strike price K.

Consider an ECO over an asset S with execution date T, price S T at time T and strike price K.") Example 5 European call option (ECO) Consider an ECO over an asset S with execution date T, price S T at time T and strike price K. Value of the ECO at time T: max{s T K,0} Price of ECO at time t < T:

Example 5 European call option (ECO) Consider an ECO over an asset S with execution date T, price S T at time T and strike price K. Value of the ECO at time T: max{s T K,0} Price of ECO at time t < T:

Risk and Management: Goals and Perspective

Etymology: Risicare Risk and Management: Goals and Perspective Risk (Oxford English Dictionary): (Exposure to) the possibility of loss, injury, or other adverse or unwelcome circumstance; a chance or situation

Etymology: Risicare Risk and Management: Goals and Perspective Risk (Oxford English Dictionary): (Exposure to) the possibility of loss, injury, or other adverse or unwelcome circumstance; a chance or situation

Risk Management and Time Series

IEOR E4602: Quantitative Risk Management Spring 2016 c 2016 by Martin Haugh Risk Management and Time Series Time series models are often employed in risk management applications. They can be used to estimate

IEOR E4602: Quantitative Risk Management Spring 2016 c 2016 by Martin Haugh Risk Management and Time Series Time series models are often employed in risk management applications. They can be used to estimate

RISKMETRICS. Dr Philip Symes

1 RISKMETRICS Dr Philip Symes 1. Introduction 2 RiskMetrics is JP Morgan's risk management methodology. It was released in 1994 This was to standardise risk analysis in the industry. Scenarios are generated

1 RISKMETRICS Dr Philip Symes 1. Introduction 2 RiskMetrics is JP Morgan's risk management methodology. It was released in 1994 This was to standardise risk analysis in the industry. Scenarios are generated

Risk management. VaR and Expected Shortfall. Christian Groll. VaR and Expected Shortfall Risk management Christian Groll 1 / 56

Risk management VaR and Expected Shortfall Christian Groll VaR and Expected Shortfall Risk management Christian Groll 1 / 56 Introduction Introduction VaR and Expected Shortfall Risk management Christian

Risk management VaR and Expected Shortfall Christian Groll VaR and Expected Shortfall Risk management Christian Groll 1 / 56 Introduction Introduction VaR and Expected Shortfall Risk management Christian

Market Risk: FROM VALUE AT RISK TO STRESS TESTING. Agenda. Agenda (Cont.) Traditional Measures of Market Risk

Traditional Measures of Market Risk") Market Risk: FROM VALUE AT RISK TO STRESS TESTING Agenda The Notional Amount Approach Price Sensitivity Measure for Derivatives Weakness of the Greek Measure Define Value at Risk 1 Day to VaR to 10 Day

Market Risk: FROM VALUE AT RISK TO STRESS TESTING Agenda The Notional Amount Approach Price Sensitivity Measure for Derivatives Weakness of the Greek Measure Define Value at Risk 1 Day to VaR to 10 Day

A Brief Review of Derivatives Pricing & Hedging

IEOR E4602: Quantitative Risk Management Spring 2016 c 2016 by Martin Haugh A Brief Review of Derivatives Pricing & Hedging In these notes we briefly describe the martingale approach to the pricing of

IEOR E4602: Quantitative Risk Management Spring 2016 c 2016 by Martin Haugh A Brief Review of Derivatives Pricing & Hedging In these notes we briefly describe the martingale approach to the pricing of

Quantitative Risk Management

Quantitative Risk Management Asset Allocation and Risk Management Martin B. Haugh Department of Industrial Engineering and Operations Research Columbia University Outline Review of Mean-Variance Analysis

Quantitative Risk Management Asset Allocation and Risk Management Martin B. Haugh Department of Industrial Engineering and Operations Research Columbia University Outline Review of Mean-Variance Analysis

Risk and Management: Goals and Perspective

Etymology: Risicare Risk and Management: Goals and Perspective Risk (Oxford English Dictionary): (Exposure to) the possibility of loss, injury, or other adverse or unwelcome circumstance; a chance or situation

Etymology: Risicare Risk and Management: Goals and Perspective Risk (Oxford English Dictionary): (Exposure to) the possibility of loss, injury, or other adverse or unwelcome circumstance; a chance or situation

2 Modeling Credit Risk

2 Modeling Credit Risk In this chapter we present some simple approaches to measure credit risk. We start in Section 2.1 with a short overview of the standardized approach of the Basel framework for banking

2 Modeling Credit Risk In this chapter we present some simple approaches to measure credit risk. We start in Section 2.1 with a short overview of the standardized approach of the Basel framework for banking

Market Risk Analysis Volume IV. Value-at-Risk Models

Market Risk Analysis Volume IV Value-at-Risk Models Carol Alexander John Wiley & Sons, Ltd List of Figures List of Tables List of Examples Foreword Preface to Volume IV xiii xvi xxi xxv xxix IV.l Value

Market Risk Analysis Volume IV Value-at-Risk Models Carol Alexander John Wiley & Sons, Ltd List of Figures List of Tables List of Examples Foreword Preface to Volume IV xiii xvi xxi xxv xxix IV.l Value

MFM Practitioner Module: Quantitative Risk Management. John Dodson. September 6, 2017

MFM Practitioner Module: Quantitative September 6, 2017 Course Fall sequence modules quantitative risk management Gary Hatfield fixed income securities Jason Vinar mortgage securities introductions Chong

MFM Practitioner Module: Quantitative September 6, 2017 Course Fall sequence modules quantitative risk management Gary Hatfield fixed income securities Jason Vinar mortgage securities introductions Chong

Introduction to Algorithmic Trading Strategies Lecture 8

Introduction to Algorithmic Trading Strategies Lecture 8 Risk Management Haksun Li haksun.li@numericalmethod.com www.numericalmethod.com Outline Value at Risk (VaR) Extreme Value Theory (EVT) References

Introduction to Algorithmic Trading Strategies Lecture 8 Risk Management Haksun Li haksun.li@numericalmethod.com www.numericalmethod.com Outline Value at Risk (VaR) Extreme Value Theory (EVT) References

Derivative Securities

Derivative Securities he Black-Scholes formula and its applications. his Section deduces the Black- Scholes formula for a European call or put, as a consequence of risk-neutral valuation in the continuous

Derivative Securities he Black-Scholes formula and its applications. his Section deduces the Black- Scholes formula for a European call or put, as a consequence of risk-neutral valuation in the continuous

Financial Risk Measurement/Management

550.446 Financial Risk Measurement/Management Week of September 23, 2013 Interest Rate Risk & Value at Risk (VaR) 3.1 Where we are Last week: Introduction continued; Insurance company and Investment company

550.446 Financial Risk Measurement/Management Week of September 23, 2013 Interest Rate Risk & Value at Risk (VaR) 3.1 Where we are Last week: Introduction continued; Insurance company and Investment company

Market risk measurement in practice

Lecture notes on risk management, public policy, and the financial system Allan M. Malz Columbia University 2018 Allan M. Malz Last updated: October 23, 2018 2/32 Outline Nonlinearity in market risk Market

Lecture notes on risk management, public policy, and the financial system Allan M. Malz Columbia University 2018 Allan M. Malz Last updated: October 23, 2018 2/32 Outline Nonlinearity in market risk Market

IEOR E4703: Monte-Carlo Simulation

IEOR E4703: Monte-Carlo Simulation Generating Random Variables and Stochastic Processes Martin Haugh Department of Industrial Engineering and Operations Research Columbia University Email: martin.b.haugh@gmail.com

IEOR E4703: Monte-Carlo Simulation Generating Random Variables and Stochastic Processes Martin Haugh Department of Industrial Engineering and Operations Research Columbia University Email: martin.b.haugh@gmail.com

FIN FINANCIAL INSTRUMENTS SPRING 2008

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 The Greeks Introduction We have studied how to price an option using the Black-Scholes formula. Now we wish to consider how the option price changes, either

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 The Greeks Introduction We have studied how to price an option using the Black-Scholes formula. Now we wish to consider how the option price changes, either

INTEREST RATES AND FX MODELS

INTEREST RATES AND FX MODELS 7. Risk Management Andrew Lesniewski Courant Institute of Mathematical Sciences New York University New York March 8, 2012 2 Interest Rates & FX Models Contents 1 Introduction

INTEREST RATES AND FX MODELS 7. Risk Management Andrew Lesniewski Courant Institute of Mathematical Sciences New York University New York March 8, 2012 2 Interest Rates & FX Models Contents 1 Introduction

The Fundamental Review of the Trading Book: from VaR to ES

The Fundamental Review of the Trading Book: from VaR to ES Chiara Benazzoli Simon Rabanser Francesco Cordoni Marcus Cordi Gennaro Cibelli University of Verona Ph. D. Modelling Week Finance Group (UniVr)

The Fundamental Review of the Trading Book: from VaR to ES Chiara Benazzoli Simon Rabanser Francesco Cordoni Marcus Cordi Gennaro Cibelli University of Verona Ph. D. Modelling Week Finance Group (UniVr)

Practical example of an Economic Scenario Generator

Practical example of an Economic Scenario Generator Martin Schenk Actuarial & Insurance Solutions SAV 7 March 2014 Agenda Introduction Deterministic vs. stochastic approach Mathematical model Application

Practical example of an Economic Scenario Generator Martin Schenk Actuarial & Insurance Solutions SAV 7 March 2014 Agenda Introduction Deterministic vs. stochastic approach Mathematical model Application

NEWCASTLE UNIVERSITY SCHOOL OF MATHEMATICS, STATISTICS & PHYSICS SEMESTER 1 SPECIMEN 2 MAS3904. Stochastic Financial Modelling. Time allowed: 2 hours

NEWCASTLE UNIVERSITY SCHOOL OF MATHEMATICS, STATISTICS & PHYSICS SEMESTER 1 SPECIMEN 2 Stochastic Financial Modelling Time allowed: 2 hours Candidates should attempt all questions. Marks for each question

NEWCASTLE UNIVERSITY SCHOOL OF MATHEMATICS, STATISTICS & PHYSICS SEMESTER 1 SPECIMEN 2 Stochastic Financial Modelling Time allowed: 2 hours Candidates should attempt all questions. Marks for each question

HANDBOOK OF. Market Risk CHRISTIAN SZYLAR WILEY

HANDBOOK OF Market Risk CHRISTIAN SZYLAR WILEY Contents FOREWORD ACKNOWLEDGMENTS ABOUT THE AUTHOR INTRODUCTION XV XVII XIX XXI 1 INTRODUCTION TO FINANCIAL MARKETS t 1.1 The Money Market 4 1.2 The Capital

HANDBOOK OF Market Risk CHRISTIAN SZYLAR WILEY Contents FOREWORD ACKNOWLEDGMENTS ABOUT THE AUTHOR INTRODUCTION XV XVII XIX XXI 1 INTRODUCTION TO FINANCIAL MARKETS t 1.1 The Money Market 4 1.2 The Capital

Risk e-learning. Modules Overview.

Risk e-learning Modules Overview Risk Sensitivities Market Risk Foundation (Banks) Understand delta risk sensitivity as an introduction to a broader set of risk sensitivities Explore the principles of

Risk e-learning Modules Overview Risk Sensitivities Market Risk Foundation (Banks) Understand delta risk sensitivity as an introduction to a broader set of risk sensitivities Explore the principles of

Naked & Covered Positions

The Greek Letters 1 Example A bank has sold for $300,000 a European call option on 100,000 shares of a nondividend paying stock S 0 = 49, K = 50, r = 5%, σ = 20%, T = 20 weeks, μ = 13% The Black-Scholes

The Greek Letters 1 Example A bank has sold for $300,000 a European call option on 100,000 shares of a nondividend paying stock S 0 = 49, K = 50, r = 5%, σ = 20%, T = 20 weeks, μ = 13% The Black-Scholes

IEOR E4703: Monte-Carlo Simulation

IEOR E4703: Monte-Carlo Simulation Simulation Efficiency and an Introduction to Variance Reduction Methods Martin Haugh Department of Industrial Engineering and Operations Research Columbia University

IEOR E4703: Monte-Carlo Simulation Simulation Efficiency and an Introduction to Variance Reduction Methods Martin Haugh Department of Industrial Engineering and Operations Research Columbia University

Lecture Note 8 of Bus 41202, Spring 2017: Stochastic Diffusion Equation & Option Pricing

Lecture Note 8 of Bus 41202, Spring 2017: Stochastic Diffusion Equation & Option Pricing We shall go over this note quickly due to time constraints. Key concept: Ito s lemma Stock Options: A contract giving

Lecture Note 8 of Bus 41202, Spring 2017: Stochastic Diffusion Equation & Option Pricing We shall go over this note quickly due to time constraints. Key concept: Ito s lemma Stock Options: A contract giving

Chapter 15: Jump Processes and Incomplete Markets. 1 Jumps as One Explanation of Incomplete Markets

Chapter 5: Jump Processes and Incomplete Markets Jumps as One Explanation of Incomplete Markets It is easy to argue that Brownian motion paths cannot model actual stock price movements properly in reality,

Chapter 5: Jump Processes and Incomplete Markets Jumps as One Explanation of Incomplete Markets It is easy to argue that Brownian motion paths cannot model actual stock price movements properly in reality,

The Statistical Mechanics of Financial Markets

The Statistical Mechanics of Financial Markets Johannes Voit 2011 johannes.voit (at) ekit.com Overview 1. Why statistical physicists care about financial markets 2. The standard model - its achievements

The Statistical Mechanics of Financial Markets Johannes Voit 2011 johannes.voit (at) ekit.com Overview 1. Why statistical physicists care about financial markets 2. The standard model - its achievements

Numerical schemes for SDEs

Lecture 5 Numerical schemes for SDEs Lecture Notes by Jan Palczewski Computational Finance p. 1 A Stochastic Differential Equation (SDE) is an object of the following type dx t = a(t,x t )dt + b(t,x t

Lecture 5 Numerical schemes for SDEs Lecture Notes by Jan Palczewski Computational Finance p. 1 A Stochastic Differential Equation (SDE) is an object of the following type dx t = a(t,x t )dt + b(t,x t

Lecture Quantitative Finance Spring Term 2015

and Lecture Quantitative Finance Spring Term 2015 Prof. Dr. Erich Walter Farkas Lecture 06: March 26, 2015 1 / 47 Remember and Previous chapters: introduction to the theory of options put-call parity fundamentals

and Lecture Quantitative Finance Spring Term 2015 Prof. Dr. Erich Walter Farkas Lecture 06: March 26, 2015 1 / 47 Remember and Previous chapters: introduction to the theory of options put-call parity fundamentals

LECTURE 2: MULTIPERIOD MODELS AND TREES

LECTURE 2: MULTIPERIOD MODELS AND TREES 1. Introduction One-period models, which were the subject of Lecture 1, are of limited usefulness in the pricing and hedging of derivative securities. In real-world

LECTURE 2: MULTIPERIOD MODELS AND TREES 1. Introduction One-period models, which were the subject of Lecture 1, are of limited usefulness in the pricing and hedging of derivative securities. In real-world

Bloomberg. Portfolio Value-at-Risk. Sridhar Gollamudi & Bryan Weber. September 22, Version 1.0

Portfolio Value-at-Risk Sridhar Gollamudi & Bryan Weber September 22, 2011 Version 1.0 Table of Contents 1 Portfolio Value-at-Risk 2 2 Fundamental Factor Models 3 3 Valuation methodology 5 3.1 Linear factor

Portfolio Value-at-Risk Sridhar Gollamudi & Bryan Weber September 22, 2011 Version 1.0 Table of Contents 1 Portfolio Value-at-Risk 2 2 Fundamental Factor Models 3 3 Valuation methodology 5 3.1 Linear factor

Financial Risk Forecasting Chapter 6 Analytical value-at-risk for options and bonds

Financial Risk Forecasting Chapter 6 Analytical value-at-risk for options and bonds Jon Danielsson 2017 London School of Economics To accompany Financial Risk Forecasting www.financialriskforecasting.com

Financial Risk Forecasting Chapter 6 Analytical value-at-risk for options and bonds Jon Danielsson 2017 London School of Economics To accompany Financial Risk Forecasting www.financialriskforecasting.com

Analysis of the Models Used in Variance Swap Pricing

Analysis of the Models Used in Variance Swap Pricing Jason Vinar U of MN Workshop 2011 Workshop Goals Price variance swaps using a common rule of thumb used by traders, using Monte Carlo simulation with

Analysis of the Models Used in Variance Swap Pricing Jason Vinar U of MN Workshop 2011 Workshop Goals Price variance swaps using a common rule of thumb used by traders, using Monte Carlo simulation with

Alternative VaR Models

Alternative VaR Models Neil Roeth, Senior Risk Developer, TFG Financial Systems. 15 th July 2015 Abstract We describe a variety of VaR models in terms of their key attributes and differences, e.g., parametric

Alternative VaR Models Neil Roeth, Senior Risk Developer, TFG Financial Systems. 15 th July 2015 Abstract We describe a variety of VaR models in terms of their key attributes and differences, e.g., parametric

1 Geometric Brownian motion

Copyright c 05 by Karl Sigman Geometric Brownian motion Note that since BM can take on negative values, using it directly for modeling stock prices is questionable. There are other reasons too why BM is

Copyright c 05 by Karl Sigman Geometric Brownian motion Note that since BM can take on negative values, using it directly for modeling stock prices is questionable. There are other reasons too why BM is

FINANCIAL OPTION ANALYSIS HANDOUTS

FINANCIAL OPTION ANALYSIS HANDOUTS 1 2 FAIR PRICING There is a market for an object called S. The prevailing price today is S 0 = 100. At this price the object S can be bought or sold by anyone for any

FINANCIAL OPTION ANALYSIS HANDOUTS 1 2 FAIR PRICING There is a market for an object called S. The prevailing price today is S 0 = 100. At this price the object S can be bought or sold by anyone for any

Pricing of minimum interest guarantees: Is the arbitrage free price fair?

Pricing of minimum interest guarantees: Is the arbitrage free price fair? Pål Lillevold and Dag Svege 17. 10. 2002 Pricing of minimum interest guarantees: Is the arbitrage free price fair? 1 1 Outline

Pricing of minimum interest guarantees: Is the arbitrage free price fair? Pål Lillevold and Dag Svege 17. 10. 2002 Pricing of minimum interest guarantees: Is the arbitrage free price fair? 1 1 Outline

Risk Minimization Control for Beating the Market Strategies

Risk Minimization Control for Beating the Market Strategies Jan Večeř, Columbia University, Department of Statistics, Mingxin Xu, Carnegie Mellon University, Department of Mathematical Sciences, Olympia

Risk Minimization Control for Beating the Market Strategies Jan Večeř, Columbia University, Department of Statistics, Mingxin Xu, Carnegie Mellon University, Department of Mathematical Sciences, Olympia

Master s in Financial Engineering Foundations of Buy-Side Finance: Quantitative Risk and Portfolio Management. > Teaching > Courses

Master s in Financial Engineering Foundations of Buy-Side Finance: Quantitative Risk and Portfolio Management www.symmys.com > Teaching > Courses Spring 2008, Monday 7:10 pm 9:30 pm, Room 303 Attilio Meucci

Master s in Financial Engineering Foundations of Buy-Side Finance: Quantitative Risk and Portfolio Management www.symmys.com > Teaching > Courses Spring 2008, Monday 7:10 pm 9:30 pm, Room 303 Attilio Meucci

Portfolio Optimization with Alternative Risk Measures

Portfolio Optimization with Alternative Risk Measures Prof. Daniel P. Palomar The Hong Kong University of Science and Technology (HKUST) MAFS6010R- Portfolio Optimization with R MSc in Financial Mathematics

Portfolio Optimization with Alternative Risk Measures Prof. Daniel P. Palomar The Hong Kong University of Science and Technology (HKUST) MAFS6010R- Portfolio Optimization with R MSc in Financial Mathematics

ADVANCED OPERATIONAL RISK MODELLING IN BANKS AND INSURANCE COMPANIES

Small business banking and financing: a global perspective Cagliari, 25-26 May 2007 ADVANCED OPERATIONAL RISK MODELLING IN BANKS AND INSURANCE COMPANIES C. Angela, R. Bisignani, G. Masala, M. Micocci 1

Small business banking and financing: a global perspective Cagliari, 25-26 May 2007 ADVANCED OPERATIONAL RISK MODELLING IN BANKS AND INSURANCE COMPANIES C. Angela, R. Bisignani, G. Masala, M. Micocci 1

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Fall 2017 Instructor: Dr. Sateesh Mane.

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Fall 2017 Instructor: Dr. Sateesh Mane c Sateesh R. Mane 2017 9 Lecture 9 9.1 The Greeks November 15, 2017 Let

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Fall 2017 Instructor: Dr. Sateesh Mane c Sateesh R. Mane 2017 9 Lecture 9 9.1 The Greeks November 15, 2017 Let

Lecture 9: Practicalities in Using Black-Scholes. Sunday, September 23, 12

Lecture 9: Practicalities in Using Black-Scholes Major Complaints Most stocks and FX products don t have log-normal distribution Typically fat-tailed distributions are observed Constant volatility assumed,

Lecture 9: Practicalities in Using Black-Scholes Major Complaints Most stocks and FX products don t have log-normal distribution Typically fat-tailed distributions are observed Constant volatility assumed,

Chapter 7: Estimation Sections

1 / 40 Chapter 7: Estimation Sections 7.1 Statistical Inference Bayesian Methods: Chapter 7 7.2 Prior and Posterior Distributions 7.3 Conjugate Prior Distributions 7.4 Bayes Estimators Frequentist Methods:

1 / 40 Chapter 7: Estimation Sections 7.1 Statistical Inference Bayesian Methods: Chapter 7 7.2 Prior and Posterior Distributions 7.3 Conjugate Prior Distributions 7.4 Bayes Estimators Frequentist Methods:

Homework Assignments

Homework Assignments Week 1 (p 57) #4.1, 4., 4.3 Week (pp 58-6) #4.5, 4.6, 4.8(a), 4.13, 4.0, 4.6(b), 4.8, 4.31, 4.34 Week 3 (pp 15-19) #1.9, 1.1, 1.13, 1.15, 1.18 (pp 9-31) #.,.6,.9 Week 4 (pp 36-37)

Homework Assignments Week 1 (p 57) #4.1, 4., 4.3 Week (pp 58-6) #4.5, 4.6, 4.8(a), 4.13, 4.0, 4.6(b), 4.8, 4.31, 4.34 Week 3 (pp 15-19) #1.9, 1.1, 1.13, 1.15, 1.18 (pp 9-31) #.,.6,.9 Week 4 (pp 36-37)

MEASURING PORTFOLIO RISKS USING CONDITIONAL COPULA-AR-GARCH MODEL

MEASURING PORTFOLIO RISKS USING CONDITIONAL COPULA-AR-GARCH MODEL Isariya Suttakulpiboon MSc in Risk Management and Insurance Georgia State University, 30303 Atlanta, Georgia Email: suttakul.i@gmail.com,

MEASURING PORTFOLIO RISKS USING CONDITIONAL COPULA-AR-GARCH MODEL Isariya Suttakulpiboon MSc in Risk Management and Insurance Georgia State University, 30303 Atlanta, Georgia Email: suttakul.i@gmail.com,

Advanced Topics in Derivative Pricing Models. Topic 4 - Variance products and volatility derivatives

Advanced Topics in Derivative Pricing Models Topic 4 - Variance products and volatility derivatives 4.1 Volatility trading and replication of variance swaps 4.2 Volatility swaps 4.3 Pricing of discrete

Advanced Topics in Derivative Pricing Models Topic 4 - Variance products and volatility derivatives 4.1 Volatility trading and replication of variance swaps 4.2 Volatility swaps 4.3 Pricing of discrete

Linda Allen, Jacob Boudoukh and Anthony Saunders, Understanding Market, Credit and Operational Risk: The Value at Risk Approach

P1.T4. Valuation & Risk Models Linda Allen, Jacob Boudoukh and Anthony Saunders, Understanding Market, Credit and Operational Risk: The Value at Risk Approach Bionic Turtle FRM Study Notes Reading 26 By

P1.T4. Valuation & Risk Models Linda Allen, Jacob Boudoukh and Anthony Saunders, Understanding Market, Credit and Operational Risk: The Value at Risk Approach Bionic Turtle FRM Study Notes Reading 26 By

Financial Risk Measurement/Management

550.446 Financial Risk Measurement/Management Week of September 23, 2013 Interest Rate Risk & Value at Risk (VaR) 3.1 Where we are Last week: Introduction continued; Insurance company and Investment company

550.446 Financial Risk Measurement/Management Week of September 23, 2013 Interest Rate Risk & Value at Risk (VaR) 3.1 Where we are Last week: Introduction continued; Insurance company and Investment company

Week 2 Quantitative Analysis of Financial Markets Hypothesis Testing and Confidence Intervals

Week 2 Quantitative Analysis of Financial Markets Hypothesis Testing and Confidence Intervals Christopher Ting http://www.mysmu.edu/faculty/christophert/ Christopher Ting : christopherting@smu.edu.sg :

Week 2 Quantitative Analysis of Financial Markets Hypothesis Testing and Confidence Intervals Christopher Ting http://www.mysmu.edu/faculty/christophert/ Christopher Ting : christopherting@smu.edu.sg :

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2011, Mr. Ruey S. Tsay. Solutions to Final Exam.

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2011, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (32 pts) Answer briefly the following questions. 1. Suppose

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2011, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (32 pts) Answer briefly the following questions. 1. Suppose

Chapter 9 - Mechanics of Options Markets

Chapter 9 - Mechanics of Options Markets Types of options Option positions and profit/loss diagrams Underlying assets Specifications Trading options Margins Taxation Warrants, employee stock options, and

Chapter 9 - Mechanics of Options Markets Types of options Option positions and profit/loss diagrams Underlying assets Specifications Trading options Margins Taxation Warrants, employee stock options, and

Dynamic Relative Valuation

Dynamic Relative Valuation Liuren Wu, Baruch College Joint work with Peter Carr from Morgan Stanley October 15, 2013 Liuren Wu (Baruch) Dynamic Relative Valuation 10/15/2013 1 / 20 The standard approach

Dynamic Relative Valuation Liuren Wu, Baruch College Joint work with Peter Carr from Morgan Stanley October 15, 2013 Liuren Wu (Baruch) Dynamic Relative Valuation 10/15/2013 1 / 20 The standard approach

P&L Attribution and Risk Management

P&L Attribution and Risk Management Liuren Wu Options Markets (Hull chapter: 15, Greek letters) Liuren Wu ( c ) P& Attribution and Risk Management Options Markets 1 / 19 Outline 1 P&L attribution via the

P&L Attribution and Risk Management Liuren Wu Options Markets (Hull chapter: 15, Greek letters) Liuren Wu ( c ) P& Attribution and Risk Management Options Markets 1 / 19 Outline 1 P&L attribution via the

Course information FN3142 Quantitative finance

Course information 015 16 FN314 Quantitative finance This course is aimed at students interested in obtaining a thorough grounding in market finance and related empirical methods. Prerequisite If taken

Course information 015 16 FN314 Quantitative finance This course is aimed at students interested in obtaining a thorough grounding in market finance and related empirical methods. Prerequisite If taken

Optimizing S-shaped utility and risk management

Optimizing S-shaped utility and risk management Ineffectiveness of VaR and ES constraints John Armstrong (KCL), Damiano Brigo (Imperial) Quant Summit March 2018 Are ES constraints effective against rogue

Optimizing S-shaped utility and risk management Ineffectiveness of VaR and ES constraints John Armstrong (KCL), Damiano Brigo (Imperial) Quant Summit March 2018 Are ES constraints effective against rogue

Lecture 1 Definitions from finance

Lecture 1 s from finance Financial market instruments can be divided into two types. There are the underlying stocks shares, bonds, commodities, foreign currencies; and their derivatives, claims that promise

Lecture 1 s from finance Financial market instruments can be divided into two types. There are the underlying stocks shares, bonds, commodities, foreign currencies; and their derivatives, claims that promise

MTH6154 Financial Mathematics I Stochastic Interest Rates

MTH6154 Financial Mathematics I Stochastic Interest Rates Contents 4 Stochastic Interest Rates 45 4.1 Fixed Interest Rate Model............................ 45 4.2 Varying Interest Rate Model...........................

MTH6154 Financial Mathematics I Stochastic Interest Rates Contents 4 Stochastic Interest Rates 45 4.1 Fixed Interest Rate Model............................ 45 4.2 Varying Interest Rate Model...........................

Log-Robust Portfolio Management

Log-Robust Portfolio Management Dr. Aurélie Thiele Lehigh University Joint work with Elcin Cetinkaya and Ban Kawas Research partially supported by the National Science Foundation Grant CMMI-0757983 Dr.

Log-Robust Portfolio Management Dr. Aurélie Thiele Lehigh University Joint work with Elcin Cetinkaya and Ban Kawas Research partially supported by the National Science Foundation Grant CMMI-0757983 Dr.

Lecture 17. The model is parametrized by the time period, δt, and three fixed constant parameters, v, σ and the riskless rate r.

Lecture 7 Overture to continuous models Before rigorously deriving the acclaimed Black-Scholes pricing formula for the value of a European option, we developed a substantial body of material, in continuous

Lecture 7 Overture to continuous models Before rigorously deriving the acclaimed Black-Scholes pricing formula for the value of a European option, we developed a substantial body of material, in continuous

Statistical Tables Compiled by Alan J. Terry

Statistical Tables Compiled by Alan J. Terry School of Science and Sport University of the West of Scotland Paisley, Scotland Contents Table 1: Cumulative binomial probabilities Page 1 Table 2: Cumulative

Statistical Tables Compiled by Alan J. Terry School of Science and Sport University of the West of Scotland Paisley, Scotland Contents Table 1: Cumulative binomial probabilities Page 1 Table 2: Cumulative

Business Statistics 41000: Probability 3

Business Statistics 41000: Probability 3 Drew D. Creal University of Chicago, Booth School of Business February 7 and 8, 2014 1 Class information Drew D. Creal Email: dcreal@chicagobooth.edu Office: 404

Business Statistics 41000: Probability 3 Drew D. Creal University of Chicago, Booth School of Business February 7 and 8, 2014 1 Class information Drew D. Creal Email: dcreal@chicagobooth.edu Office: 404

Estimating the Greeks

IEOR E4703: Monte-Carlo Simulation Columbia University Estimating the Greeks c 207 by Martin Haugh In these lecture notes we discuss the use of Monte-Carlo simulation for the estimation of sensitivities

IEOR E4703: Monte-Carlo Simulation Columbia University Estimating the Greeks c 207 by Martin Haugh In these lecture notes we discuss the use of Monte-Carlo simulation for the estimation of sensitivities

VaR Estimation under Stochastic Volatility Models

VaR Estimation under Stochastic Volatility Models Chuan-Hsiang Han Dept. of Quantitative Finance Natl. Tsing-Hua University TMS Meeting, Chia-Yi (Joint work with Wei-Han Liu) December 5, 2009 Outline Risk

VaR Estimation under Stochastic Volatility Models Chuan-Hsiang Han Dept. of Quantitative Finance Natl. Tsing-Hua University TMS Meeting, Chia-Yi (Joint work with Wei-Han Liu) December 5, 2009 Outline Risk

EVA Tutorial #1 BLOCK MAXIMA APPROACH IN HYDROLOGIC/CLIMATE APPLICATIONS. Rick Katz

1 EVA Tutorial #1 BLOCK MAXIMA APPROACH IN HYDROLOGIC/CLIMATE APPLICATIONS Rick Katz Institute for Mathematics Applied to Geosciences National Center for Atmospheric Research Boulder, CO USA email: rwk@ucar.edu

1 EVA Tutorial #1 BLOCK MAXIMA APPROACH IN HYDROLOGIC/CLIMATE APPLICATIONS Rick Katz Institute for Mathematics Applied to Geosciences National Center for Atmospheric Research Boulder, CO USA email: rwk@ucar.edu

Asset Allocation Model with Tail Risk Parity

Proceedings of the Asia Pacific Industrial Engineering & Management Systems Conference 2017 Asset Allocation Model with Tail Risk Parity Hirotaka Kato Graduate School of Science and Technology Keio University,

Proceedings of the Asia Pacific Industrial Engineering & Management Systems Conference 2017 Asset Allocation Model with Tail Risk Parity Hirotaka Kato Graduate School of Science and Technology Keio University,

Dependence Modeling and Credit Risk

Dependence Modeling and Credit Risk Paola Mosconi Banca IMI Bocconi University, 20/04/2015 Paola Mosconi Lecture 6 1 / 53 Disclaimer The opinion expressed here are solely those of the author and do not

Dependence Modeling and Credit Risk Paola Mosconi Banca IMI Bocconi University, 20/04/2015 Paola Mosconi Lecture 6 1 / 53 Disclaimer The opinion expressed here are solely those of the author and do not

AN ANALYTICALLY TRACTABLE UNCERTAIN VOLATILITY MODEL

AN ANALYTICALLY TRACTABLE UNCERTAIN VOLATILITY MODEL FABIO MERCURIO BANCA IMI, MILAN http://www.fabiomercurio.it 1 Stylized facts Traders use the Black-Scholes formula to price plain-vanilla options. An

AN ANALYTICALLY TRACTABLE UNCERTAIN VOLATILITY MODEL FABIO MERCURIO BANCA IMI, MILAN http://www.fabiomercurio.it 1 Stylized facts Traders use the Black-Scholes formula to price plain-vanilla options. An

Chapter 7: Estimation Sections

1 / 31 : Estimation Sections 7.1 Statistical Inference Bayesian Methods: 7.2 Prior and Posterior Distributions 7.3 Conjugate Prior Distributions 7.4 Bayes Estimators Frequentist Methods: 7.5 Maximum Likelihood

1 / 31 : Estimation Sections 7.1 Statistical Inference Bayesian Methods: 7.2 Prior and Posterior Distributions 7.3 Conjugate Prior Distributions 7.4 Bayes Estimators Frequentist Methods: 7.5 Maximum Likelihood

continuous rv Note for a legitimate pdf, we have f (x) 0 and f (x)dx = 1. For a continuous rv, P(X = c) = c f (x)dx = 0, hence

0 and f (x)dx = 1. For a continuous rv, P(X = c) = c f (x)dx = 0, hence") continuous rv Let X be a continuous rv. Then a probability distribution or probability density function (pdf) of X is a function f(x) such that for any two numbers a and b with a b, P(a X b) = b a f (x)dx.

continuous rv Let X be a continuous rv. Then a probability distribution or probability density function (pdf) of X is a function f(x) such that for any two numbers a and b with a b, P(a X b) = b a f (x)dx.

Assessing Value-at-Risk

Lecture notes on risk management, public policy, and the financial system Allan M. Malz Columbia University 2018 Allan M. Malz Last updated: April 1, 2018 2 / 18 Outline 3/18 Overview Unconditional coverage

Lecture notes on risk management, public policy, and the financial system Allan M. Malz Columbia University 2018 Allan M. Malz Last updated: April 1, 2018 2 / 18 Outline 3/18 Overview Unconditional coverage

Value at Risk Risk Management in Practice. Nikolett Gyori (Morgan Stanley, Internal Audit) September 26, 2017

September 26, 2017") Value at Risk Risk Management in Practice Nikolett Gyori (Morgan Stanley, Internal Audit) September 26, 2017 Overview Value at Risk: the Wake of the Beast Stop-loss Limits Value at Risk: What is VaR? Value

Value at Risk Risk Management in Practice Nikolett Gyori (Morgan Stanley, Internal Audit) September 26, 2017 Overview Value at Risk: the Wake of the Beast Stop-loss Limits Value at Risk: What is VaR? Value

Long-Term Risk Management

Long-Term Risk Management Roger Kaufmann Swiss Life General Guisan-Quai 40 Postfach, 8022 Zürich Switzerland roger.kaufmann@swisslife.ch April 28, 2005 Abstract. In this paper financial risks for long

Long-Term Risk Management Roger Kaufmann Swiss Life General Guisan-Quai 40 Postfach, 8022 Zürich Switzerland roger.kaufmann@swisslife.ch April 28, 2005 Abstract. In this paper financial risks for long

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2012, Mr. Ruey S. Tsay. Solutions to Final Exam

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2012, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (40 points) Answer briefly the following questions. 1. Consider

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2012, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (40 points) Answer briefly the following questions. 1. Consider

Department of Mathematics. Mathematics of Financial Derivatives

Department of Mathematics MA408 Mathematics of Financial Derivatives Thursday 15th January, 2009 2pm 4pm Duration: 2 hours Attempt THREE questions MA408 Page 1 of 5 1. (a) Suppose 0 < E 1 < E 3 and E 2

Department of Mathematics MA408 Mathematics of Financial Derivatives Thursday 15th January, 2009 2pm 4pm Duration: 2 hours Attempt THREE questions MA408 Page 1 of 5 1. (a) Suppose 0 < E 1 < E 3 and E 2

CHAPTER 9. Solutions. Exercise The payoff diagrams will look as in the figure below.

CHAPTER 9 Solutions Exercise 1 1. The payoff diagrams will look as in the figure below. 2. Gross payoff at expiry will be: P(T) = min[(1.23 S T ), 0] + min[(1.10 S T ), 0] where S T is the EUR/USD exchange

CHAPTER 9 Solutions Exercise 1 1. The payoff diagrams will look as in the figure below. 2. Gross payoff at expiry will be: P(T) = min[(1.23 S T ), 0] + min[(1.10 S T ), 0] where S T is the EUR/USD exchange

DRAFT. 1 exercise in state (S, t), π(s, t) = 0 do not exercise in state (S, t) Review of the Risk Neutral Stock Dynamics

, π(s, t) = 0 do not exercise in state (S, t) Review of the Risk Neutral Stock Dynamics") Chapter 12 American Put Option Recall that the American option has strike K and maturity T and gives the holder the right to exercise at any time in [0, T ]. The American option is not straightforward

Chapter 12 American Put Option Recall that the American option has strike K and maturity T and gives the holder the right to exercise at any time in [0, T ]. The American option is not straightforward

Term Structure Lattice Models

IEOR E4706: Foundations of Financial Engineering c 2016 by Martin Haugh Term Structure Lattice Models These lecture notes introduce fixed income derivative securities and the modeling philosophy used to

IEOR E4706: Foundations of Financial Engineering c 2016 by Martin Haugh Term Structure Lattice Models These lecture notes introduce fixed income derivative securities and the modeling philosophy used to

Martingale Pricing Theory in Discrete-Time and Discrete-Space Models

IEOR E4707: Foundations of Financial Engineering c 206 by Martin Haugh Martingale Pricing Theory in Discrete-Time and Discrete-Space Models These notes develop the theory of martingale pricing in a discrete-time,

IEOR E4707: Foundations of Financial Engineering c 206 by Martin Haugh Martingale Pricing Theory in Discrete-Time and Discrete-Space Models These notes develop the theory of martingale pricing in a discrete-time,

- 1 - **** d(lns) = (µ (1/2)σ 2 )dt + σdw t

= (µ (1/2)σ 2 )dt + σdw t") - 1 - **** These answers indicate the solutions to the 2014 exam questions. Obviously you should plot graphs where I have simply described the key features. It is important when plotting graphs to label

- 1 - **** These answers indicate the solutions to the 2014 exam questions. Obviously you should plot graphs where I have simply described the key features. It is important when plotting graphs to label

Basel II and the Risk Management of Basket Options with Time-Varying Correlations

Basel II and the Risk Management of Basket Options with Time-Varying Correlations AmyS.K.Wong Tinbergen Institute Erasmus University Rotterdam The impact of jumps, regime switches, and linearly changing

Basel II and the Risk Management of Basket Options with Time-Varying Correlations AmyS.K.Wong Tinbergen Institute Erasmus University Rotterdam The impact of jumps, regime switches, and linearly changing

1 The continuous time limit

Derivative Securities, Courant Institute, Fall 2008 http://www.math.nyu.edu/faculty/goodman/teaching/derivsec08/index.html Jonathan Goodman and Keith Lewis Supplementary notes and comments, Section 3 1

Derivative Securities, Courant Institute, Fall 2008 http://www.math.nyu.edu/faculty/goodman/teaching/derivsec08/index.html Jonathan Goodman and Keith Lewis Supplementary notes and comments, Section 3 1

Chapter 5 Univariate time-series analysis. () Chapter 5 Univariate time-series analysis 1 / 29

Chapter 5 Univariate time-series analysis 1 / 29") Chapter 5 Univariate time-series analysis () Chapter 5 Univariate time-series analysis 1 / 29 Time-Series Time-series is a sequence fx 1, x 2,..., x T g or fx t g, t = 1,..., T, where t is an index denoting

Chapter 5 Univariate time-series analysis () Chapter 5 Univariate time-series analysis 1 / 29 Time-Series Time-series is a sequence fx 1, x 2,..., x T g or fx t g, t = 1,..., T, where t is an index denoting

Pricing theory of financial derivatives

Pricing theory of financial derivatives One-period securities model S denotes the price process {S(t) : t = 0, 1}, where S(t) = (S 1 (t) S 2 (t) S M (t)). Here, M is the number of securities. At t = 1,

Pricing theory of financial derivatives One-period securities model S denotes the price process {S(t) : t = 0, 1}, where S(t) = (S 1 (t) S 2 (t) S M (t)). Here, M is the number of securities. At t = 1,

Sampling Distribution

MAT 2379 (Spring 2012) Sampling Distribution Definition : Let X 1,..., X n be a collection of random variables. We say that they are identically distributed if they have a common distribution. Definition

MAT 2379 (Spring 2012) Sampling Distribution Definition : Let X 1,..., X n be a collection of random variables. We say that they are identically distributed if they have a common distribution. Definition

ACTSC 445 Final Exam Summary Asset and Liability Management

CTSC 445 Final Exam Summary sset and Liability Management Unit 5 - Interest Rate Risk (References Only) Dollar Value of a Basis Point (DV0): Given by the absolute change in the price of a bond for a basis

CTSC 445 Final Exam Summary sset and Liability Management Unit 5 - Interest Rate Risk (References Only) Dollar Value of a Basis Point (DV0): Given by the absolute change in the price of a bond for a basis

A gentle introduction to the RM 2006 methodology

A gentle introduction to the RM 2006 methodology Gilles Zumbach RiskMetrics Group Av. des Morgines 12 1213 Petit-Lancy Geneva, Switzerland gilles.zumbach@riskmetrics.com Initial version: August 2006 This

A gentle introduction to the RM 2006 methodology Gilles Zumbach RiskMetrics Group Av. des Morgines 12 1213 Petit-Lancy Geneva, Switzerland gilles.zumbach@riskmetrics.com Initial version: August 2006 This

Modeling Co-movements and Tail Dependency in the International Stock Market via Copulae

Modeling Co-movements and Tail Dependency in the International Stock Market via Copulae Katja Ignatieva, Eckhard Platen Bachelier Finance Society World Congress 22-26 June 2010, Toronto K. Ignatieva, E.

Modeling Co-movements and Tail Dependency in the International Stock Market via Copulae Katja Ignatieva, Eckhard Platen Bachelier Finance Society World Congress 22-26 June 2010, Toronto K. Ignatieva, E.

Volatility Trading Strategies: Dynamic Hedging via A Simulation

Volatility Trading Strategies: Dynamic Hedging via A Simulation Approach Antai Collage of Economics and Management Shanghai Jiao Tong University Advisor: Professor Hai Lan June 6, 2017 Outline 1 The volatility

Volatility Trading Strategies: Dynamic Hedging via A Simulation Approach Antai Collage of Economics and Management Shanghai Jiao Tong University Advisor: Professor Hai Lan June 6, 2017 Outline 1 The volatility

IEOR E4703: Monte-Carlo Simulation

IEOR E4703: Monte-Carlo Simulation Further Variance Reduction Methods Martin Haugh Department of Industrial Engineering and Operations Research Columbia University Email: martin.b.haugh@gmail.com Outline

IEOR E4703: Monte-Carlo Simulation Further Variance Reduction Methods Martin Haugh Department of Industrial Engineering and Operations Research Columbia University Email: martin.b.haugh@gmail.com Outline

Forwards and Futures. Chapter Basics of forwards and futures Forwards

Chapter 7 Forwards and Futures Copyright c 2008 2011 Hyeong In Choi, All rights reserved. 7.1 Basics of forwards and futures The financial assets typically stocks we have been dealing with so far are the

Chapter 7 Forwards and Futures Copyright c 2008 2011 Hyeong In Choi, All rights reserved. 7.1 Basics of forwards and futures The financial assets typically stocks we have been dealing with so far are the

( ) since this is the benefit of buying the asset at the strike price rather

since this is the benefit of buying the asset at the strike price rather") Review of some financial models for MAT 483 Parity and Other Option Relationships The basic parity relationship for European options with the same strike price and the same time to expiration is: C( KT

Review of some financial models for MAT 483 Parity and Other Option Relationships The basic parity relationship for European options with the same strike price and the same time to expiration is: C( KT

Slides for Risk Management

Slides for Risk Management Introduction to the modeling of assets Groll Seminar für Finanzökonometrie Prof. Mittnik, PhD Groll (Seminar für Finanzökonometrie) Slides for Risk Management Prof. Mittnik,

Slides for Risk Management Introduction to the modeling of assets Groll Seminar für Finanzökonometrie Prof. Mittnik, PhD Groll (Seminar für Finanzökonometrie) Slides for Risk Management Prof. Mittnik,