Jesse Thompson Regional Business Economist The Federal Reserve Bank of Dallas, Houston Branch November 2011

|

|

|

- Colleen Douglas

- 6 years ago

- Views:

Transcription

1 Jesse Thompson Regional Business Economist The Federal Reserve Bank of Dallas, Houston Branch November 2011

2 Drivers in the recovery How re We Doing? The Trails Ahead & Risks to the Outlook

3 Energy Upstream & Downstream Manufacturing and Technology Trade

4

0.5 % rise in GDP (one-fourth earlier effect) Energy industry has buffered Texas from many national downturns")

5 Dallas Fed research: Texas still benefits from higher oil and gas prices Effects of oil price shocks smaller than in the 70s and 80s 10% increase in oil prices leads to: 0.3 % rise in employment (one-third earlier effect) 0.5 % rise in GDP (one-fourth earlier effect) Energy industry has buffered Texas from many national downturns

6 Texas #1 producer of oil and gas in the nation Texas has 25% of U.S. refinery capacity 60% of U.S. petrochemical production Prominence of oil and gas extraction industry has diminished, but remains substantial

7 Percent Share of Total Texas Output WTI Spot Price 2010 $/barrel '63 '66 '69 '72 '75 '78 '81 '84 '87 '90 '93 '96 '99 '02 '05 '08 0

8 160 Oil WTI Crude Oil and Natural Gas Prices NG WTI Natural Gas Feb 2007-Oct 2008-Jun 2009-Feb 2009-Oct 2010-Jun 2011-Feb 2011-Oct 0

9

10

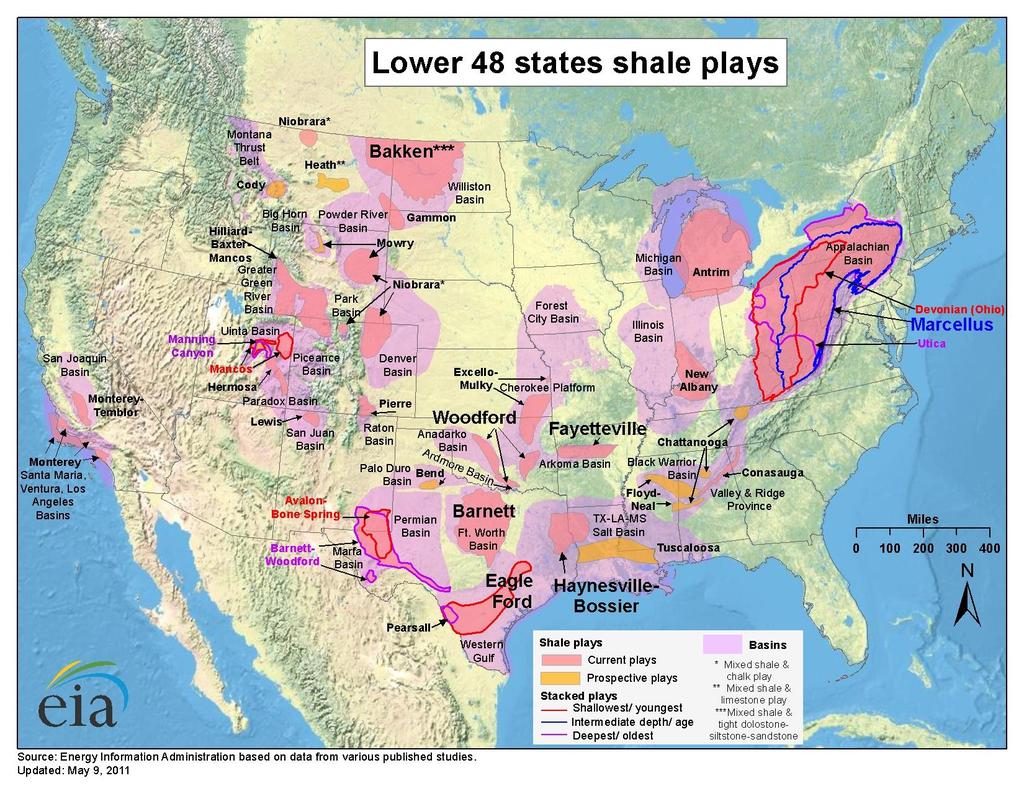

11 Energy sector s resurgence driven by natural gas Improvements in technology key: Horizontal drilling Hydraulic fracturing Share of gas rigs rose to nearly 90% of rig count in 2005 Texas produces 70% of U.S. shale output

12

13 Horizontal drilling continues to displace other technologies 70.0% 60.0% 50.0% 40.0% Directional Horizontal Vertical 30.0% 20.0% 10.0% 0.0% 1/5/2007 1/5/2008 1/5/2009 1/5/2010 1/5/2011

14 Number 2,500 2,000 Gas-directed rigs Oil-directed rigs 1,500 1, Jan-2007 Jan-2008 Jan-2009 Jan-2010 Jan-2011 SOURCE: Baker Hughes

15 Gulf of Mexico U.S. Rig Count /5/07 1/5/08 1/5/09 1/5/10 1/5/11

16

17 Texas #1 in downstream production High oil and gas prices hurt downstream industries Strong growth in foreign demand boosts downstream industry

18 Chemical exports growing because of weak domestic demand at home, strong growth in developing world But also driven by low natural gas prices North America makes many key chemicals and plastics with natural gas, while rest of world uses oil On an energy-equivalent basis, natural gas less than one-third the price of oil North American companies have huge cost advantage

19 Percent TX/LA Gulf Coast West Coast IN/IL/KY East Coast Other 5 0 Note: West Coast is DOE definition of PAD 5, IN/IL/KY is PAD2, and the East Coast is PAD 1; Inland Texas has another 4 percent of U.S. capacity; Operable distillation capacity per calendar day; January 1, 2010.

9 2,325.")

20 Location Houston/Texas City/Baytown New Orleans/Baton Rouge Beaumont/Port Arthur/Lake Charles Number of Refineries Capacity (000 b/d) 9 2, , ,836.9 Corpus Christi Source: Energy Information Administration

21 By destination country Mexico 16.2 Netherlands 9.7 By product shipped Distillate 33.1 Residual 23.4 Canada 9.0 Petroleum Coke 22.1 Singapore 5.8 Chile 4.4 Gasoline 11.0 Other 10.5

22 Values Gulf Coast Downstream Margins Ethylene Cash Margins* Pace Gulf Coast Refining Margins** Jan-2007 Jan-2008 Jan-2009 Jan-2010 Jan-2011 *Based on ethane feedstock (cents/lbs). **Based on West Texas Sour - RFG ($/barrel). SOURCE: Oil and Gas Journal.

Houston/Texas City 16 13,890 New")

23 Location Number of Crackers Capacity (000 ton/yr) Houston/Texas City 16 13,890 New Orleans/Baton Rouge Beaumont/Lake Charles 7 5, ,288 Corpus Christi Source: Oil and Gas Journal

24 Gas Feedstock Oil product feedstock -40 Jan-1997 Jan-1999 Jan-2001 Jan-2003 Jan-2005 Jan-2007 Jan-2009 Jan-2011

25

26

27 B/D, thousands With capacity growth, weak consumption at home, & strong global demand J a n J a n J a n J a n J a n J a n

28 2000 $, millions Plastics Chemicals '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10

29 Index, Jan = Texas U.S. 100 California 50 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10

30 Texas/Louisiana Gulf Coast region is a major producer of oil, oil products, petrochemicals and plastics. Exports have grown rapidly, Recently setting record highs in Refined petroleum products! Texas-Mexico border trade was reshaped by China s 2001 entry into WTO. Exports have come back strongly after the recession, led by autos.

31 Metro Area Peak Trough Decline (%) Texas July 2008 November 2009 El Paso Brownsville February 2008 February 2008 September 2009 Bottom to Today (%) August Laredo August 2007 October McAllen February 2008 March

32 400 Non US Mexico's exports in the lead (Index, January 2000=100, real s.a.) 350 Exports U.S. 20% ROW Exports_US Exports Exports_ROW %

33 Maquiladoras are Rebounding Index July 2007=100, SA Matamoros Nuevo Laredo Reynosa Juarez Nogales Mexicali Tecate Tijuana Source: INEGI

34 10 percent increase in maquiladora output in Ciudad Juarez leads to an increase in El Paso employment as follows: 3.0 percent increase in total employment 5.4 percent in transportation employment 1.4 percent in retail trade employment 2.2 percent in finance, insurance and real estate (FIRE) employment 2.0 percent in services employment (-) 1.2 percent in manufacturing employment

35 Over the years, the bulk of the impact has switch from the manufacturing sector to the services sector. El Paso continues to be a supplier to the maquiladoras in Juarez, but we now supply business services. This is good news to us because these type of jobs pay higher wages than the traditional manufacturing jobs

36

37 High-tech manufacturing and services an important economic driver in the 90s High-tech manufacturing output grew 10X as fast as Texas GDP Austin silicon prairie Dallas telecom corridor Tech bust caused industry downsizing Growth strongest in high-tech manufacturing and computer systems design since bust

38 Percent CA TX OR CA NY TX Manufacturing Services

39 Index, '90=100 Computer Systems Design Telecom Computer & Electronics Mfg. Data Processing

40 Index, '97=

41 The State of the Economy Employment/Unemployment Housing Trade & Autos

42 Jan-07 Apr-07 Jul-07 Oct-07 Jan-08 Apr-08 Jul-08 Oct-08 Jan-09 Apr-09 Jul-09 Oct-09 Jan-10 Apr-10 Jul-10 Oct-10 Jan-11 Apr-11 Jul-11 Oct Houston El Paso San Antonio Texas Fort Worth Austin Dallas McAllen 90

43 Metro Area Peak BCI Trough BCI Peak To Trough Trough to Dec Texas July 2008 November Houston August 2008 December Ft Worth May 2008 November Dallas February 2008 December San Antonio April 2008 September Austin February 2008 December

44 Jan-2007 Apr-2007 Jul-2007 Oct-2007 Jan-2008 Apr-2008 Jul-2008 Oct-2008 Jan-2009 Apr-2009 Jul-2009 Oct-2009 Jan-2010 Apr-2010 Jul-2010 Oct-2010 Jan-2011 Apr-2011 Jul-2011 Oct Nonfarm Payroll Employment Austin Houston San Antonio Ft. Worth Dallas 92

45 Unemployment rates still elevated U.S. 8.5 Texas 8.4 Austin Jan-2007 Oct-2007 Jul-2008 Apr-2009 Jan-2010 Oct-2010 Jul-2011 SOURCE: Bureau of Labor Statistics.

46 Educational & Health Services Three-Period-Average Annualized Monthly Employment Growth Rate* Government Other Services Leisure & Hospitality Professional & Business Svc Financial Activities Information Trade, Transp & Utilities Manufacturing Construction & Mining Total Nonfarm, Austin *Seasonally adjusted. -2% -1% 0% 1% 2% 3% 4% 5% 6% 7%

47 Last three months average annualized monthly Employment Growth Rate* Government Other Services Leisure & Hospitality Educational & Health Services Professional & Business Svc Financial Activities Information Trade, Transp & Utilities Manufacturing Construction & Mining Total Nonfarm, Austin *Seasonally adjusted. -20% -10% 0% 10%

48 Index U.S. Texas Initial claims remain in downward trend Jan-2007 Aug-2007 Mar-2008 Oct-2008 May-2009 Dec-2009 Jul-2010 Feb-2011

49 SARR, Mil. Units Light-vehicle sales August = Change from August 2010 to August2011 GM Ford Toyota Hyundai Chrysler Nissan 9% -1% 11% -13% 16% 28% 27% 11% 24%

50 Index 150 Production levels at pre-recession peak Texas - Total Texas - Manufacturing 120 Q Q Q Q Q Q Q Q3-2010

51 Chemicals Plastics and Resins Manufacturing 55 Computers, Computer 50 Eq, Semiconductors Jan-2007 Sep-2007 May-2008 Jan-2009 Sep-2009 May-2010 Jan-2011 Sep-2011

52

53

54 FOMC Statement: the Committee decided today to continue its program to extend the average maturity of its holdings of securities as announced in September. The Committee is maintaining its existing policies of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction. The Committee also decided to keep the target range for the federal funds rate at 0 to 1/4 percent and currently anticipates that economic conditions--including low rates of resource utilization and a subdued outlook for inflation over the medium run--are likely to warrant exceptionally low levels for the federal funds rate at least through mid The Committee will continue to assess the economic outlook in light of incoming information and is prepared to employ its tools to promote a stronger economic recovery in a context of price stability.

55 FOMC Statement: Still Twisting The Committee is maintaining its existing policies of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction. The Committee also decided to keep the target range for the federal funds rate at 0 to 1/4 percent and currently anticipates that economic conditions-- including low rates of resource utilization and a subdued outlook for inflation over the medium run--are likely to warrant exceptionally low levels for the federal funds rate at least through mid The Committee will continue to assess the economic outlook in light of incoming information and is prepared to employ its tools to promote a stronger economic recovery in a context of

56 FOMC Statement: Still Twisting Holding on To MBS portfolio and of rolling over maturing Treasury securities at auction. The Committee also decided to keep the target range for the federal funds rate at 0 to 1/4 percent and currently anticipates that economic conditions--including low rates of resource utilization and a subdued outlook for inflation over the medium run--are likely to warrant exceptionally low levels for the federal funds rate at least through mid The Committee will continue to assess the economic outlook in light of incoming information and is prepared to employ its tools to promote a stronger economic recovery in a context of price stability.

57 The Committee also decided to keep the target range for the federal funds rate at 0 to 1/4 percent and currently anticipates that economic conditions--including low rates of resource utilization and a subdued outlook for inflation over the medium run--are likely to warrant exceptionally low levels for the federal funds rate at least through mid The Committee will continue to assess the economic outlook in light of incoming information and is prepared to employ its tools to promote a stronger economic recovery in a context of price stability. FOMC Statement: Still Twisting Holding on To MBS portfolio Maintaining the size of the balance sheet

58 FOMC Statement: Still Twisting Holding on To MBS portfolio Maintaining the size of the balance sheet Zero interest rates for foreseeable future The Committee will continue to assess the economic outlook in light of incoming information and is prepared to employ its tools to promote a stronger economic recovery in a context of price stability.

59 FOMC Statement: Still Twisting Holding on To MBS portfolio Maintaining the size of the balance sheet Zero interest rates for foreseeable future We still have tools to use, and of course

60 FOMC Statement: Still Twisting Holding on To MBS portfolio Maintaining the size of the balance sheet Zero interest rates for foreseeable future We still have tools to use, and of course all of the above is subject to CHANGE

61

62 GDP (2005$) CPI Total IP PCE (2005$) Corp. Profit USA Mexico Japan Russia Brazil India China GDP growth forecast trending up since November No acceleration before 2H 2011 Eurozone

63 Euro zone Crisis Federal Regulatory Uncertainty Slowdown or Correction in Emergent Economies Federal Fiscal Uncertainty

64 France $28b Germany $39b U.K. $69b Chart 22: An interconnected Europe Foreign Bank Exposures: Ireland $473b $2b $13b Portugal $213b $3b $5b $4b $13b $4b TOTAL foreign claims on Italy: $912b $15b $10b Belgium $516b $5b Spain $726b $1b Greece $138b

65

66 Health Care Reform Act 1000 pages long Texas Medical Center expects as many as 250,000 pages once all implementation rules are completed. Dodd-Frank Act over 2,000 pages long, contains 16 titles, 38 subtitles and a total of 541 sections Davis Polk & Wardwell: of the 541 rule makings mandated, 31% have not yet been proposed. Environmental and Tax Policies remain volatile

67 Slow growth turned to recession and financial crisis in the US economy; a slowdown in the developing world turned to global recession A sharp reverse in the commodity boom, especially in oil markets caused a setback in We have gotten help from commodity markets to move growth back in front of the US growth rate. Many uncertainties persist space, fracking regulation, cap and trade, healthcare reform, etc Texas Employment Growth forecast for 2012: 2.0%

68 Jesse Thompson Regional Business Economist The Federal Reserve Bank of Dallas, Houston Branch November 2011

69

70

71

72 Plasticsnews.com

73

74 2000-Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q1 50% Non-OECD driving demand growth 40% 30% 20% 10% 0% Non-OECD OECD -10%

75 70% Chinese oil demand growth outpaces U.S. by a wide margin 60% 50% 40% 30% 20% China U.S. 10% 0% -10%

76 Millions of Dollars 80,000 Change in Treasury Holdings by Maturity (12 September- 2 January 60,000 40,000 20, ,000-40,000-60,000-80,000 Within 15 Days Days 91 days to 1 year 1 year to 5 years 5 to 10 years Over 10 Years

NAHEFFA March 26, The views expressed are my own and do not necessarily reflect official positions of the Federal Reserve System.

NAHEFFA March 26, 219 The views expressed are my own and do not necessarily reflect official positions of the Federal Reserve System. National Economy Growing Strongly Jobs grew 1.8% in 218 the fastest

NAHEFFA March 26, 219 The views expressed are my own and do not necessarily reflect official positions of the Federal Reserve System. National Economy Growing Strongly Jobs grew 1.8% in 218 the fastest

2018 Texas Economic Outlook: Firing on All Cylinders

218 Texas Economic Outlook: Firing on All Cylinders Keith Phillips Assistant Vice President and Senior Economist 4/5/218 The views expressed in this presentation are strictly those of the presenter and

218 Texas Economic Outlook: Firing on All Cylinders Keith Phillips Assistant Vice President and Senior Economist 4/5/218 The views expressed in this presentation are strictly those of the presenter and

Texas Economic Outlook: Strong Growth Continues

Texas Economic Outlook: Strong Growth Continues Keith Phillips Assistant Vice President and Senior Economist 1/23/18 The views expressed in this presentation are strictly those of the presenter and do

Texas Economic Outlook: Strong Growth Continues Keith Phillips Assistant Vice President and Senior Economist 1/23/18 The views expressed in this presentation are strictly those of the presenter and do

Texas Economic Outlook: Tapping on the Brakes

National Economy Picking Up After Q1 Pause Texas Economic Outlook: Tapping on the Brakes Keith Phillips Assistant Vice President and Senior Economist Consumer spending picked up in 1 as housing prices

National Economy Picking Up After Q1 Pause Texas Economic Outlook: Tapping on the Brakes Keith Phillips Assistant Vice President and Senior Economist Consumer spending picked up in 1 as housing prices

RECESSION AND RECOVERY IN MISSOURI AND THE U.S.

RECESSION AND RECOVERY IN MISSOURI AND THE U.S. Alison Felix Senior Economist Federal Reserve Bank of Kansas City The views expressed are those of the presenter and do not necessarily reflect the positions

RECESSION AND RECOVERY IN MISSOURI AND THE U.S. Alison Felix Senior Economist Federal Reserve Bank of Kansas City The views expressed are those of the presenter and do not necessarily reflect the positions

Keith Phillips, Sr. Economist and Advisor

The Outlook for the Texas Economy Keith Phillips, Sr. Economist and Advisor National Economic Overview Growth in US Economy Positive But Sluggish Market working to heal itself asset prices falling, inflation

The Outlook for the Texas Economy Keith Phillips, Sr. Economist and Advisor National Economic Overview Growth in US Economy Positive But Sluggish Market working to heal itself asset prices falling, inflation

Texas Mid-Year Economic Outlook: Strong Growth Continues

Texas Mid-Year Economic Outlook: Strong Growth Continues Keith Phillips Assistant Vice President and Senior Economist 9/27/18 The views expressed in this presentation are strictly those of the presenter

Texas Mid-Year Economic Outlook: Strong Growth Continues Keith Phillips Assistant Vice President and Senior Economist 9/27/18 The views expressed in this presentation are strictly those of the presenter

Outlook for the Texas Economy. Luis Bernardo Torres Ruiz, Ph.D. August 26, 2016

Outlook for the Texas Economy Luis Bernardo Torres Ruiz, Ph.D. August 26, 2016 Research Economist Texas Society of Architects Contents 1. U.S. Economic Outlook 2. Texas Economic Outlook 3. Challenges and

Outlook for the Texas Economy Luis Bernardo Torres Ruiz, Ph.D. August 26, 2016 Research Economist Texas Society of Architects Contents 1. U.S. Economic Outlook 2. Texas Economic Outlook 3. Challenges and

Plunging Oil Prices: Impact on the U.S. and State Economies

Plunging Oil Prices: Impact on the U.S. and State Economies Mine Yücel Senior Vice President and Director of Research November 17, 216 Nominal price, weekly 16 14 Oil and gas prices volatile 12 1 Oil price

Plunging Oil Prices: Impact on the U.S. and State Economies Mine Yücel Senior Vice President and Director of Research November 17, 216 Nominal price, weekly 16 14 Oil and gas prices volatile 12 1 Oil price

Single-family home sales and construction are not expected to regain 2005 peaks

Single-family home sales and construction are not expected to regain 25 peaks Millions of units 8. 7. 6. 5. Housing starts (right axis) 4. Home sales (left axis) 3. 2. 1. 198 1985 199 1995 2 25 21 215

Single-family home sales and construction are not expected to regain 25 peaks Millions of units 8. 7. 6. 5. Housing starts (right axis) 4. Home sales (left axis) 3. 2. 1. 198 1985 199 1995 2 25 21 215

A Perspective from the Federal Reserve Institute of Internal Auditors San Antonio Chapter August 19, 2015 Blake Hastings Senior Vice President

A Perspective from the Federal Reserve Institute of Internal Auditors San Antonio Chapter August 19, 215 Blake Hastings Senior Vice President The views expressed in this presentation are strictly those

A Perspective from the Federal Reserve Institute of Internal Auditors San Antonio Chapter August 19, 215 Blake Hastings Senior Vice President The views expressed in this presentation are strictly those

Outlook for the Texas Economy

Outlook for the Economy LUIS TORRES RESEARCH ECONOMIST WESLEY MILLER RESEARCH ASSISTANT TECHNICAL REPORT 2 6 MARCH 217 TR Contents About this Report... 3 January 217 Summary... Economic Activity... 7 Business

Outlook for the Economy LUIS TORRES RESEARCH ECONOMIST WESLEY MILLER RESEARCH ASSISTANT TECHNICAL REPORT 2 6 MARCH 217 TR Contents About this Report... 3 January 217 Summary... Economic Activity... 7 Business

Outlook for the Texas Economy. Luis Bernardo Torres Ruiz, Ph.D. June 29, 2016

Outlook for the Texas Economy Luis Bernardo Torres Ruiz, Ph.D. June 29, 2016 Research Economist Texas Gas Association Contents 1. Economic Outlook 2. Housing Market 3. Challenges and Issues During the

Outlook for the Texas Economy Luis Bernardo Torres Ruiz, Ph.D. June 29, 2016 Research Economist Texas Gas Association Contents 1. Economic Outlook 2. Housing Market 3. Challenges and Issues During the

Plunging Crude Prices: Impact on U.S. and State Economies

Plunging Crude Prices: Impact on U.S. and State Economies Mine Yücel Senior Vice President and Director of Research August 7, 215 Oil and gas prices plunge Nominal price, $, weekly 16 14 12 Oil Price 1

Plunging Crude Prices: Impact on U.S. and State Economies Mine Yücel Senior Vice President and Director of Research August 7, 215 Oil and gas prices plunge Nominal price, $, weekly 16 14 12 Oil Price 1

Texas Economic Outlook: Cruising in Third Gear

Texas Economic Outlook: Cruising in Third Gear Keith Phillips Assistant Vice President and Senior Economist 1/19/17 The views expressed in this presentation are strictly those of the presenter and do not

Texas Economic Outlook: Cruising in Third Gear Keith Phillips Assistant Vice President and Senior Economist 1/19/17 The views expressed in this presentation are strictly those of the presenter and do not

Economic Outlook. William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago

Economic Outlook CRF Credit & A/R Forum & EXPO Salt Lake City, UT October 23, 218 William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago What I said In August The outlook

Economic Outlook CRF Credit & A/R Forum & EXPO Salt Lake City, UT October 23, 218 William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago What I said In August The outlook

Texas Mid-Year Economic Outlook: The Skies are Beginning to Clear Keith Phillips Assistant Vice President and Senior Economist

Texas Mid-Year Economic Outlook: The Skies are Beginning to Clear Keith Phillips Assistant Vice President and Senior Economist The views expressed in this presentation are strictly those of the presenter

Texas Mid-Year Economic Outlook: The Skies are Beginning to Clear Keith Phillips Assistant Vice President and Senior Economist The views expressed in this presentation are strictly those of the presenter

2016 Texas Economic Outlook: Riding the Energy Roller Coaster Keith Phillips Assistant Vice President and Senior Economist

216 Texas Economic Outlook: Riding the Energy Roller Coaster Keith Phillips Assistant Vice President and Senior Economist The views expressed in this presentation are strictly those of the presenter and

216 Texas Economic Outlook: Riding the Energy Roller Coaster Keith Phillips Assistant Vice President and Senior Economist The views expressed in this presentation are strictly those of the presenter and

National & Colorado. Economic Update. Alison Felix Economist & Branch Executive Federal Reserve Bank of Kansas City Denver Branch

National & Colorado Economic Update Alison Felix Economist & Branch Executive Federal Reserve Bank of Kansas City Denver Branch The views expressed are those of the presenter and do not necessarily reflect

National & Colorado Economic Update Alison Felix Economist & Branch Executive Federal Reserve Bank of Kansas City Denver Branch The views expressed are those of the presenter and do not necessarily reflect

Richard W. Fisher. President and CEO Federal Reserve Bank of Dallas. Austin, Texas April 16, 2014

Richard W. Fisher President and CEO Federal Reserve Bank of Dallas Austin, Texas April 16, 2014 U.S. Economic Dashboard 4.5 4 5 3.5 5.5 6 6.5 7 7.5 8 3 7 3.28 Junk-bond spread (%) 7.5 8 8.5 10 8.5 9 9.5

Richard W. Fisher President and CEO Federal Reserve Bank of Dallas Austin, Texas April 16, 2014 U.S. Economic Dashboard 4.5 4 5 3.5 5.5 6 6.5 7 7.5 8 3 7 3.28 Junk-bond spread (%) 7.5 8 8.5 10 8.5 9 9.5

Ontario Economic Accounts

SECOND QUARTER OF 2017 April, May, June Ontario Economic Accounts ONTARIO MINISTRY OF FINANCE Table of Contents ECONOMIC ACCOUNTS Highlights 1 Ontario s Economy Continues to Grow Expenditure Details 2

SECOND QUARTER OF 2017 April, May, June Ontario Economic Accounts ONTARIO MINISTRY OF FINANCE Table of Contents ECONOMIC ACCOUNTS Highlights 1 Ontario s Economy Continues to Grow Expenditure Details 2

Outlook for the Texas Economy

Outlook for the Economy LUIS TORRES RESEARCH ECONOMIST WESLEY MILLER RESEARCH ASSISTANT TECHNICAL REPORT 2 MAY 217 TR Contents About this Report... 3 March 217 Summary... Economic Activity... 7 Business

Outlook for the Economy LUIS TORRES RESEARCH ECONOMIST WESLEY MILLER RESEARCH ASSISTANT TECHNICAL REPORT 2 MAY 217 TR Contents About this Report... 3 March 217 Summary... Economic Activity... 7 Business

Worcester Business Journal Economic Forecast Breakfast February 13, Jeff Fuhrer, EVP and Senior Policy Advisor Federal Reserve Bank of Boston

Worcester Business Journal Economic Forecast Breakfast February 3, 25 Jeff Fuhrer, EVP and Senior Policy Advisor Federal Reserve Bank of Boston X Not this lady X Not this guy 2 26:Jan 26:Sep 27: 28:Jan

Worcester Business Journal Economic Forecast Breakfast February 3, 25 Jeff Fuhrer, EVP and Senior Policy Advisor Federal Reserve Bank of Boston X Not this lady X Not this guy 2 26:Jan 26:Sep 27: 28:Jan

Aug-12. Oct-13. Dec-14. Feb-16

Feb-2 Apr-3 Jun-4 Aug-5 Oct-6 Feb-9 Apr-1 Jun-11 Aug-12 Feb-16 Dec-1 Dec-2 Dec-3 Dec-4 Dec-5 Dec-6 Richard Farr Jim McGovern U.S. Trading European Trading Chief Market Strategist Market Strategist Tourmaline

Feb-2 Apr-3 Jun-4 Aug-5 Oct-6 Feb-9 Apr-1 Jun-11 Aug-12 Feb-16 Dec-1 Dec-2 Dec-3 Dec-4 Dec-5 Dec-6 Richard Farr Jim McGovern U.S. Trading European Trading Chief Market Strategist Market Strategist Tourmaline

Moving On Up Today s Economic Environment

Moving On Up Today s Economic Environment Presented by PFM Asset Management LLC Gray Lepley, Senior Analyst, Portfolio Strategies November 8, 2018 PFM 1 U.S. ECONOMY Today s Agenda MONETARY POLICY GEOPOLITICAL

Moving On Up Today s Economic Environment Presented by PFM Asset Management LLC Gray Lepley, Senior Analyst, Portfolio Strategies November 8, 2018 PFM 1 U.S. ECONOMY Today s Agenda MONETARY POLICY GEOPOLITICAL

U.S. Economic Update and Outlook. Laurel Graefe, REIN Director Federal Reserve Bank of Atlanta October 2, 2013

1 U.S. Economic Update and Outlook Laurel Graefe, REIN Director Federal Reserve Bank of Atlanta October 2, 213 Following the deepest recession since the 193s, the economic recovery is well under way, though

1 U.S. Economic Update and Outlook Laurel Graefe, REIN Director Federal Reserve Bank of Atlanta October 2, 213 Following the deepest recession since the 193s, the economic recovery is well under way, though

U.S. & Missouri Economic Outlook

U.S. & Missouri Economic Outlook Missouri Government Finance Officers Association Jason Brown Economist The views expressed are those of the presenter and do not necessarily reflect the positions of the

U.S. & Missouri Economic Outlook Missouri Government Finance Officers Association Jason Brown Economist The views expressed are those of the presenter and do not necessarily reflect the positions of the

Jason Henderson Vice President and Branch Executive Federal Reserve Bank of Kansas City Omaha Branch September 27, 2011

Jason Henderson Vice President and Branch Executive September 27, 211 The views expressed are those of the author and do not necessarily reflect the opinions of the Federal Reserve Bank of Kansas City

Jason Henderson Vice President and Branch Executive September 27, 211 The views expressed are those of the author and do not necessarily reflect the opinions of the Federal Reserve Bank of Kansas City

U.S. and Oklahoma Economic Update. Megan Williams Associate Economist and Manager, Oklahoma City Branch. The U.S. Economy and Monetary Policy

U.S. and Oklahoma Economic Update Megan Williams Associate Economist and Manager, Oklahoma City Branch The U.S. Economy and Monetary Policy GDP growth was relatively strong in the second half of Growth

U.S. and Oklahoma Economic Update Megan Williams Associate Economist and Manager, Oklahoma City Branch The U.S. Economy and Monetary Policy GDP growth was relatively strong in the second half of Growth

Quarterly Economics Briefing

Quarterly Economics Briefing March 2015 Review of Current Conditions: The Economic Outlook and Its Impact on Workers Compensation The exhibits below are updated to reflect the current economic outlook

Quarterly Economics Briefing March 2015 Review of Current Conditions: The Economic Outlook and Its Impact on Workers Compensation The exhibits below are updated to reflect the current economic outlook

ECONOMIC OUTLOOK FINALLY, SYNCHRONIZED GLOBAL GROWTH

ECONOMIC OUTLOOK FINALLY, SYNCHRONIZED GLOBAL GROWTH Augustine Faucher Chief Economist November 13, 2017 Senior Economic Advisor Chief Economist BETTER GROWTH THIS YEAR, AND AN UPGRADE TO 2018 World output,

ECONOMIC OUTLOOK FINALLY, SYNCHRONIZED GLOBAL GROWTH Augustine Faucher Chief Economist November 13, 2017 Senior Economic Advisor Chief Economist BETTER GROWTH THIS YEAR, AND AN UPGRADE TO 2018 World output,

Chart 1. U.S. Personal Saving Rate and Household Debt (consu plus mortgage) as a % of Disposable Personal Incom

as a % of Disposable Personal Incom") Chart 1 U.S. Personal Saving Rate and Household Debt (consu plus mortgage) as a % of Disposable Personal Incom 16% 14% 12% 10% 8% 6% 4% Last Points 4Q 2015- Saving Rate, 5.4%; HH Debt, 1 140% 130% 120%

Chart 1 U.S. Personal Saving Rate and Household Debt (consu plus mortgage) as a % of Disposable Personal Incom 16% 14% 12% 10% 8% 6% 4% Last Points 4Q 2015- Saving Rate, 5.4%; HH Debt, 1 140% 130% 120%

Outlook for the Texas Economy

Outlook for the Economy LUIS TORRES RESEARCH ECONOMIST WESLEY MILLER RESEARCH ASSOCIATE BAILEY CUADRA RESEARCH ASSISTANT TECHNICAL REPORT 2 4 6 DECEMBER 217 TR Contents About this Report... 3 October 217

Outlook for the Economy LUIS TORRES RESEARCH ECONOMIST WESLEY MILLER RESEARCH ASSOCIATE BAILEY CUADRA RESEARCH ASSISTANT TECHNICAL REPORT 2 4 6 DECEMBER 217 TR Contents About this Report... 3 October 217

RECESSION AND RECOVERY IN NEBRASKA AND THE U.S.

RECESSION AND RECOVERY IN NEBRASKA AND THE U.S. Alison Felix Senior Economist Federal Reserve Bank of Kansas City The views expressed are those of the presenter and do not necessarily reflect the positions

RECESSION AND RECOVERY IN NEBRASKA AND THE U.S. Alison Felix Senior Economist Federal Reserve Bank of Kansas City The views expressed are those of the presenter and do not necessarily reflect the positions

U.S. & District Economic Outlook

U.S. & District Economic Outlook Nebraska LEAD Program February 5, 2015 Jason Brown Senior Economist The views expressed are those of the presenter and do not necessarily reflect the positions of the Federal

U.S. & District Economic Outlook Nebraska LEAD Program February 5, 2015 Jason Brown Senior Economist The views expressed are those of the presenter and do not necessarily reflect the positions of the Federal

Emerging Trends in the U.S. and Colorado Economies

Emerging Trends in the U.S. and Colorado Economies Sam Chapman Associate Economist Federal Reserve Bank of Kansas City Denver Branch The views expressed are those of the presenter and do not necessarily

Emerging Trends in the U.S. and Colorado Economies Sam Chapman Associate Economist Federal Reserve Bank of Kansas City Denver Branch The views expressed are those of the presenter and do not necessarily

HOUSTON-THE WOODLANDS-SUGAR LAND METROPOLITAN STATISTICAL AREA (H-W-S MSA) Visit our website at

Visit our website at") Labor Market Information DECEMBER 2015 Employment Data HOUSTON-THE WOODLANDS-SUGAR LAND METROPOLITAN STATISTICAL AREA () Visit our website at www.wrksolutions.com The Houston-The Woodlands-Sugar Land Metropolitan

Labor Market Information DECEMBER 2015 Employment Data HOUSTON-THE WOODLANDS-SUGAR LAND METROPOLITAN STATISTICAL AREA () Visit our website at www.wrksolutions.com The Houston-The Woodlands-Sugar Land Metropolitan

Southwest Florida Regional Economic Indicators. August 2013

Southwest Florida Regional Economic Indicators August 213 Regional Economic Research Institute Lutgert College Of Business Phone 239-59-7319 Florida Gulf Coast University 151 FGCU Blvd. South Fort Myers,

Southwest Florida Regional Economic Indicators August 213 Regional Economic Research Institute Lutgert College Of Business Phone 239-59-7319 Florida Gulf Coast University 151 FGCU Blvd. South Fort Myers,

Emerging Trends in the U.S. and Colorado Economies

Emerging Trends in the U.S. and Colorado Economies Alison Felix Economist and Branch Executive Federal Reserve Bank of Kansas City Denver Branch The views expressed are those of the presenter and do not

Emerging Trends in the U.S. and Colorado Economies Alison Felix Economist and Branch Executive Federal Reserve Bank of Kansas City Denver Branch The views expressed are those of the presenter and do not

CRA Roundtable August 19, Megan Williams

CRA Roundtable August 19, 214 Megan Williams Associate Economist and Manager, Oklahoma City Branch Federal Reserve Bank of Kansas City www.kansascityfed.org/oklahomacity The U.S. Economy and Monetary Policy

CRA Roundtable August 19, 214 Megan Williams Associate Economist and Manager, Oklahoma City Branch Federal Reserve Bank of Kansas City www.kansascityfed.org/oklahomacity The U.S. Economy and Monetary Policy

RECENT EVOLUTION AND OUTLOOK OF THE MEXICAN ECONOMY BANCO DE MÉXICO OCTOBER 2003

OCTOBER 23 RECENT EVOLUTION AND OUTLOOK OF THE MEXICAN ECONOMY BANCO DE MÉXICO 2 RECENT DEVELOPMENTS OUTLOOK MEDIUM-TERM CHALLENGES 3 RECENT DEVELOPMENTS In tandem with the global economic cycle, the Mexican

OCTOBER 23 RECENT EVOLUTION AND OUTLOOK OF THE MEXICAN ECONOMY BANCO DE MÉXICO 2 RECENT DEVELOPMENTS OUTLOOK MEDIUM-TERM CHALLENGES 3 RECENT DEVELOPMENTS In tandem with the global economic cycle, the Mexican

Economic Outlook In the Shoes of an FOMC Member

Economic Outlook In the Shoes of an FOMC Member This material must be read in conjunction with the disclosure statement. 9 April 2018 PRESENTED BY: MARKUS SCHOMER Chief Economist PineBridge Investments

Economic Outlook In the Shoes of an FOMC Member This material must be read in conjunction with the disclosure statement. 9 April 2018 PRESENTED BY: MARKUS SCHOMER Chief Economist PineBridge Investments

2016 Economic Outlook for Ireland & Eurozone IFP Launch

2016 Economic Outlook for Ireland & Eurozone IFP Launch December 3 rd 2015 Jim Power Global Background US & UK growing at reasonable pace Euro Zone growing well below potential Emerging markets in some

2016 Economic Outlook for Ireland & Eurozone IFP Launch December 3 rd 2015 Jim Power Global Background US & UK growing at reasonable pace Euro Zone growing well below potential Emerging markets in some

THE STATE OF THE ECONOMY

THE STATE OF THE ECONOMY ANGELA GUO Portland State University The United States economy in the fourth quarter of 2013 appears to have a more robust foothold pointing to a healthier outlook for 2014. Much

THE STATE OF THE ECONOMY ANGELA GUO Portland State University The United States economy in the fourth quarter of 2013 appears to have a more robust foothold pointing to a healthier outlook for 2014. Much

The President s Report to the Board of Directors

The President s Report to the Board of Directors April 4, 214 Current Economic Developments - April 4, 214 Data released since your last Directors' meeting show the economy was a bit stronger in the fourth

The President s Report to the Board of Directors April 4, 214 Current Economic Developments - April 4, 214 Data released since your last Directors' meeting show the economy was a bit stronger in the fourth

Finally, A Global Tailwind for U.S. Manufacturing Growth

Finally, A Global Tailwind for U.S. Manufacturing Growth MAPI Foundation Webinar December 12, 217 Cliff Waldman Chief Economist cwaldman@mapi.net Key Takeaways The global economic recovery is both strengthening

Finally, A Global Tailwind for U.S. Manufacturing Growth MAPI Foundation Webinar December 12, 217 Cliff Waldman Chief Economist cwaldman@mapi.net Key Takeaways The global economic recovery is both strengthening

U.S. Chamber of Commerce Economic Outlook

U.S. Chamber of Commerce Economic Outlook December 211 Economic Policy Division Real GDP Outlook Percent Change, Annual Rate 2 1 1 - -1 197 197 198 198 199 199 2 2 21 U.S. GDP Actual and Potential Quarterly,

U.S. Chamber of Commerce Economic Outlook December 211 Economic Policy Division Real GDP Outlook Percent Change, Annual Rate 2 1 1 - -1 197 197 198 198 199 199 2 2 21 U.S. GDP Actual and Potential Quarterly,

Southwest Florida Regional Economic Indicators. June 2013

Southwest Florida Regional Economic Indicators June 213 Regional Economic Research Institute Lutgert College Of Business Phone 239-59-7319 Florida Gulf Coast University 151 FGCU Blvd. South Fort Myers,

Southwest Florida Regional Economic Indicators June 213 Regional Economic Research Institute Lutgert College Of Business Phone 239-59-7319 Florida Gulf Coast University 151 FGCU Blvd. South Fort Myers,

RECOVERY CONTINUES FOR LOGISTICS REAL ESTATE

RECOVERY CONTINUES FOR LOGISTICS REAL ESTATE World events trigger soft patch The global economic soft patch in the first half of 2011 was primarily caused by the cost of oil reaching $114 per barrel, rising

RECOVERY CONTINUES FOR LOGISTICS REAL ESTATE World events trigger soft patch The global economic soft patch in the first half of 2011 was primarily caused by the cost of oil reaching $114 per barrel, rising

Inflation Report. April June 2013

April June 2013 August 7, 2013 1 Outline 1 External Conditions 2 Economic Activity in Mexico 3 Monetary Policy and Inflation Determinants Forecasts and Balance of Risks 2 External Conditions Global Environment

April June 2013 August 7, 2013 1 Outline 1 External Conditions 2 Economic Activity in Mexico 3 Monetary Policy and Inflation Determinants Forecasts and Balance of Risks 2 External Conditions Global Environment

North American Steel Industry Recent Market Developments, Future Prospects and Key Challenges

North American Steel Industry Recent Market Developments, Future Prospects and Key Challenges OECD Steel Committee December 1-11, 29 Paris, France * American Iron and Steel Institute (AISI) Steel Manufacturers

North American Steel Industry Recent Market Developments, Future Prospects and Key Challenges OECD Steel Committee December 1-11, 29 Paris, France * American Iron and Steel Institute (AISI) Steel Manufacturers

THE STATE OF THE ECONOMY

THE STATE OF THE ECONOMY ANGELA GUO Portland State University Moderate growth continued in the United States economy through the second quarter of 2013, though forecasters had anticipated an acceleration

THE STATE OF THE ECONOMY ANGELA GUO Portland State University Moderate growth continued in the United States economy through the second quarter of 2013, though forecasters had anticipated an acceleration

The Oil Market: From Boom to Gloom

The Oil Market: From Boom to Gloom Mine Yücel Senior Vice President and Director of Research February 12, 216 The views expressed are those of the speaker and should not be attributed to the or the Federal

The Oil Market: From Boom to Gloom Mine Yücel Senior Vice President and Director of Research February 12, 216 The views expressed are those of the speaker and should not be attributed to the or the Federal

NORTH TEXAS ECONOMY Emily Kerr Federal Reserve Bank of Dallas October 19, 2017

NORTH TEXAS ECONOMY Emily Kerr October 19, 217 The views expressed are of the speaker and should not be attributed to the Dallas Fed or the Federal Reserve System. North Texas Overview Home to over 7.2

NORTH TEXAS ECONOMY Emily Kerr October 19, 217 The views expressed are of the speaker and should not be attributed to the Dallas Fed or the Federal Reserve System. North Texas Overview Home to over 7.2

World Economy Geopolitics Investment Strategy. The Impact of EU s Sovereign Risks on Turkish Economy. Presentation given by

World Economy Geopolitics Investment Strategy OUTLOOK FOR WORLD S MAJOR FINANCIAL MARKETS The Impact of EU s Sovereign Risks on Turkish Economy Presentation given by Dr. Michael Ivanovitch, President MSI

World Economy Geopolitics Investment Strategy OUTLOOK FOR WORLD S MAJOR FINANCIAL MARKETS The Impact of EU s Sovereign Risks on Turkish Economy Presentation given by Dr. Michael Ivanovitch, President MSI

U.S. Economic Outlook

MIT Enterprise Forum of Texas Kim Chase Senior Economist BBVA Research, Houston TX January 13, 216 Global Outlook Balance of risks tilted to the downside Global Real GDP growth % change 7. 6. 5.7 5.4 5.

MIT Enterprise Forum of Texas Kim Chase Senior Economist BBVA Research, Houston TX January 13, 216 Global Outlook Balance of risks tilted to the downside Global Real GDP growth % change 7. 6. 5.7 5.4 5.

Emerging Trends in the Regional Economy

Emerging Trends in the Regional Economy Alison Felix Economist & Branch Executive Federal Reserve Bank of Kansas City Denver Branch The views expressed are those of the presenter and do not necessarily

Emerging Trends in the Regional Economy Alison Felix Economist & Branch Executive Federal Reserve Bank of Kansas City Denver Branch The views expressed are those of the presenter and do not necessarily

Southwest Florida Regional Economic Indicators. April 2013

Southwest Florida Regional Economic Indicators April 213 Regional Economic Research Institute Lutgert College Of Business Phone 239-59-7319 Florida Gulf Coast University 151 FGCU Blvd. South Fort Myers,

Southwest Florida Regional Economic Indicators April 213 Regional Economic Research Institute Lutgert College Of Business Phone 239-59-7319 Florida Gulf Coast University 151 FGCU Blvd. South Fort Myers,

The light tight oil revolution -- the rollover and the recovery Production in major US shale plays, millions of barrels/day

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Oil Monday, August 1, 1 The light tight oil revolution --

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Oil Monday, August 1, 1 The light tight oil revolution --

Global Themes and Risks

The Goldman Sachs Group, Inc. Goldman Sachs Research Global Themes and Risks April 2013 Abby Joseph Cohen, CFA Goldman, Sachs & Co. 1-212-902-4095 abby.cohen@gs.com Rachel Siu Goldman, Sachs & Co. 1-212-357-0493

The Goldman Sachs Group, Inc. Goldman Sachs Research Global Themes and Risks April 2013 Abby Joseph Cohen, CFA Goldman, Sachs & Co. 1-212-902-4095 abby.cohen@gs.com Rachel Siu Goldman, Sachs & Co. 1-212-357-0493

Eurozone Economic Watch. February 2018

Eurozone Economic Watch February 2018 Eurozone: Strong growth continues in 1Q18, but confidence seems to peak GDP growth moderated slightly in, but there was an upward revision to previous quarters. Available

Eurozone Economic Watch February 2018 Eurozone: Strong growth continues in 1Q18, but confidence seems to peak GDP growth moderated slightly in, but there was an upward revision to previous quarters. Available

Commercial Cards & Payments Leo Abruzzese October 2015 New York

US, China and emerging markets: What s next for the global economy? Commercial Cards & Payments Leo Abruzzese October 2015 New York Overview Key points for 2015-16 Global economy struggling to gain traction

US, China and emerging markets: What s next for the global economy? Commercial Cards & Payments Leo Abruzzese October 2015 New York Overview Key points for 2015-16 Global economy struggling to gain traction

Growing for nearly a decade. 114 months and counting, through December Will become longest Post-War expansion if it lasts through July

Economic Update Closing in on Expansion Record Byron Gangnes Professor of Economics Senior Research Fellow, UHERO University of Hawaii at Manoa VLI February 219 Hawaii Island Growing for nearly a decade

Economic Update Closing in on Expansion Record Byron Gangnes Professor of Economics Senior Research Fellow, UHERO University of Hawaii at Manoa VLI February 219 Hawaii Island Growing for nearly a decade

Eurozone Economic Watch. November 2017

Eurozone Economic Watch November 2017 Eurozone: improved outlook, still subdued inflation Our MICA-BBVA model for growth estimates for the moment a quarterly GDP figure of around -0.7% in, after % QoQ

Eurozone Economic Watch November 2017 Eurozone: improved outlook, still subdued inflation Our MICA-BBVA model for growth estimates for the moment a quarterly GDP figure of around -0.7% in, after % QoQ

There has been considerable discussion of the possibility

NationalEconomicTrends February Housing and the R Word There has been considerable discussion of the possibility that ongoing troubles in the housing market could push the economy into recession 1 But

NationalEconomicTrends February Housing and the R Word There has been considerable discussion of the possibility that ongoing troubles in the housing market could push the economy into recession 1 But

Chapter 1 International economy

Chapter International economy. Main points from the OECD's Economic Outlook A broad-based recovery has taken hold Asia, the US and the UK have taken the lead. Continental Europe will follow Investment

Chapter International economy. Main points from the OECD's Economic Outlook A broad-based recovery has taken hold Asia, the US and the UK have taken the lead. Continental Europe will follow Investment

Overview of the Mexican Economy

Overview of the Mexican Economy Alejandrina Salcedo Banco de México U.S.-Mexico Manufacturing: Back in the Race Federal Reserve Bank of Dallas, El Paso Branch October 9 th, I External Conditions II Inflation

Overview of the Mexican Economy Alejandrina Salcedo Banco de México U.S.-Mexico Manufacturing: Back in the Race Federal Reserve Bank of Dallas, El Paso Branch October 9 th, I External Conditions II Inflation

San Antonio Business and Economics Society October 27, The U.S. Economic Outlook: Soft Patch, Sink Hole, or Springboard?

San Antonio Business and Economics Society October 27, 2004 The U.S. Economic Outlook: Soft Patch, Sink Hole, or Springboard? Kevin L. Kliesen Economist, Federal Reserve Bank of St. Louis Not an official

San Antonio Business and Economics Society October 27, 2004 The U.S. Economic Outlook: Soft Patch, Sink Hole, or Springboard? Kevin L. Kliesen Economist, Federal Reserve Bank of St. Louis Not an official

Inflation Report. July September 2012

July September 1 November 7, 1 1 Outline 1 External Conditions Economic Activity in Mexico 3 Monetary Policy and Inflation Determinants Forecasts and Balance of Risks External Conditions The growth rate

July September 1 November 7, 1 1 Outline 1 External Conditions Economic Activity in Mexico 3 Monetary Policy and Inflation Determinants Forecasts and Balance of Risks External Conditions The growth rate

NationalEconomicTrends

NationalEconomicTrends January 00 Stag-nations Economic growth in the United States has slowed substantially since the days of rapid expansion during the mid to late 1990s. According to preliminary estimates,

NationalEconomicTrends January 00 Stag-nations Economic growth in the United States has slowed substantially since the days of rapid expansion during the mid to late 1990s. According to preliminary estimates,

Regional Economic Update

Regional Economic Update Roberto Coronado Assistant Vice President in Charge and Sr. Economist July 23, 2015 The views expressed in this presentation are strictly those of the authors and do not necessarily

Regional Economic Update Roberto Coronado Assistant Vice President in Charge and Sr. Economist July 23, 2015 The views expressed in this presentation are strictly those of the authors and do not necessarily

Quarterly Report. April June 2015

April June August 12, 1 1 Outline 1 2 Monetary Policy External Conditions 3 Economic Activity in Mexico Inflation Determinants Forecasts and Balance of Risks April-June 2 Monetary Policy Conduction in

April June August 12, 1 1 Outline 1 2 Monetary Policy External Conditions 3 Economic Activity in Mexico Inflation Determinants Forecasts and Balance of Risks April-June 2 Monetary Policy Conduction in

Economic Outlook. William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago

Economic Outlook Chicago Association of Spring Manufacturers, Inc Des Plaines, IL January 15, 215 William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago The Great Recession

Economic Outlook Chicago Association of Spring Manufacturers, Inc Des Plaines, IL January 15, 215 William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago The Great Recession

Recent Recent Developments 0

Recent Developments 0 Global activity has slowed noticeably World Trade (annualized percent change of three month moving average over previous three month moving average) Purchasing Managers Index (PMI)

Recent Developments 0 Global activity has slowed noticeably World Trade (annualized percent change of three month moving average over previous three month moving average) Purchasing Managers Index (PMI)

Southwest Florida Regional Economic Indicators. March 2013

Southwest Florida Regional Economic Indicators March 213 Regional Economic Research Institute Lutgert College Of Business Phone 239-59-7319 Florida Gulf Coast University 151 FGCU Blvd. South Fort Myers,

Southwest Florida Regional Economic Indicators March 213 Regional Economic Research Institute Lutgert College Of Business Phone 239-59-7319 Florida Gulf Coast University 151 FGCU Blvd. South Fort Myers,

Southwest Florida Regional Economic Indicators. March 2013

Southwest Florida Regional Economic Indicators March 213 Regional Economic Research Institute Lutgert College Of Business Phone 239-59-7319 Florida Gulf Coast University 151 FGCU Blvd. South Fort Myers,

Southwest Florida Regional Economic Indicators March 213 Regional Economic Research Institute Lutgert College Of Business Phone 239-59-7319 Florida Gulf Coast University 151 FGCU Blvd. South Fort Myers,

Three-speed recovery. GDP growth. Percent Emerging and developing economies. World

Three-speed recovery GDP growth Percent 1 8 6 4 2-2 -4-6 198 1985 199 1995 2 25 21 215 Source: IMF WEO; Milken Institute. Emerging and developing economies Advanced economies World Output is still below

Three-speed recovery GDP growth Percent 1 8 6 4 2-2 -4-6 198 1985 199 1995 2 25 21 215 Source: IMF WEO; Milken Institute. Emerging and developing economies Advanced economies World Output is still below

Eurozone Economic Watch Higher growth forecasts for January 2018

Eurozone Economic Watch Higher growth forecasts for 2018-19 January 2018 Eurozone Economic Watch January 2018 Eurozone: Higher growth forecasts for 2018-19 Our MICA-BBVA model estimates a broadly stable

Eurozone Economic Watch Higher growth forecasts for 2018-19 January 2018 Eurozone Economic Watch January 2018 Eurozone: Higher growth forecasts for 2018-19 Our MICA-BBVA model estimates a broadly stable

Economic Outlook June Economic Policy Division

Economic Outlook June 215 Economic Policy Division U.S. GDP Actual and Potential Quarterly, Q1 198 to Q4 215 Real GDP Trillion 29 Dollars Log Scale $18. Forecast $15. $12.5 Actual Potential $9. $6.5 198

Economic Outlook June 215 Economic Policy Division U.S. GDP Actual and Potential Quarterly, Q1 198 to Q4 215 Real GDP Trillion 29 Dollars Log Scale $18. Forecast $15. $12.5 Actual Potential $9. $6.5 198

Economic Outlook. William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago

Economic Outlook Mid-West Fastener Association Elk Grove Village, IL February 21, 217 William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago GDP expanded by 1.9% in 216 8

Economic Outlook Mid-West Fastener Association Elk Grove Village, IL February 21, 217 William Strauss Senior Economist and Economic Advisor Federal Reserve Bank of Chicago GDP expanded by 1.9% in 216 8

The real change in private inventories added 0.22 percentage points to the second quarter GDP growth, after subtracting 0.65% in the first quarter.

QIRGRETA Monthly Macroeconomic Commentary United States The U.S. economy bounced back in the second quarter of 2007, growing at the fastest pace in more than a year. According the final estimates released

QIRGRETA Monthly Macroeconomic Commentary United States The U.S. economy bounced back in the second quarter of 2007, growing at the fastest pace in more than a year. According the final estimates released

March 19, Employment. Benchmark Jobs Data Proved More Accurate in Real Time

March 19, 2019 Growth in employment and the business-cycle index slowed for Houston at the start of the year. Leading indicators were mixed but largely painted a softer outlook for 2019. Revisions to 2018

March 19, 2019 Growth in employment and the business-cycle index slowed for Houston at the start of the year. Leading indicators were mixed but largely painted a softer outlook for 2019. Revisions to 2018

Global Economic Outlook

Global Economic Outlook Will growth continue and at what pace? North American Conference San Francisco October 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary Information

Global Economic Outlook Will growth continue and at what pace? North American Conference San Francisco October 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary Information

Contents About this Report July 2017 Border Summary Housing

Contents About this Report... 2 July 2017 Border Summary... 3 Business Cycle Index... 6 Total Construction Values... 6 Residential Construction Values... 7 Nonresidential Construction Values... 7 Employment

Contents About this Report... 2 July 2017 Border Summary... 3 Business Cycle Index... 6 Total Construction Values... 6 Residential Construction Values... 7 Nonresidential Construction Values... 7 Employment

The Federal Reserve has set the target range for the federal

NationalEconomicTrends October Monetary Policy Stance: The View from Consumption Spending The Federal Reserve has set the target range for the federal funds at to 5 percent and intends to keep this near

NationalEconomicTrends October Monetary Policy Stance: The View from Consumption Spending The Federal Reserve has set the target range for the federal funds at to 5 percent and intends to keep this near

ECONOMIC AND FINANCIAL HIGHLIGHTS

ECONOMIC AND FINANCIAL HIGHLIGHTS LABOR MARKET Contributions to Change in Nonfarm Payrolls 2 Unemployment and Labor Force Participation Rate 3 MANUFACTURING ISM Manufacturing Index 4 CONSUMERS Light Vehicle

ECONOMIC AND FINANCIAL HIGHLIGHTS LABOR MARKET Contributions to Change in Nonfarm Payrolls 2 Unemployment and Labor Force Participation Rate 3 MANUFACTURING ISM Manufacturing Index 4 CONSUMERS Light Vehicle

Decline in Economic Activity Larger Than Advance GDP Estimate February 27, 2009

Northern Trust Global Economic Research 5 South LaSalle Chicago, Illinois 663 northerntrust.com Asha G. Bangalore agb3@ntrs.com Decline in Economic Activity Larger Than Advance GDP Estimate February 27,

Northern Trust Global Economic Research 5 South LaSalle Chicago, Illinois 663 northerntrust.com Asha G. Bangalore agb3@ntrs.com Decline in Economic Activity Larger Than Advance GDP Estimate February 27,

B-GUIDE: Market Outlook

Quarterly Market Outlook: Quarter 1 2018 on 5 th January 2018 Investment Outlook for 1 st Quarter 2018 Accelerating Global Economy Supports the Rising Earnings Equity Thailand US Europe Japan Asia Bond

Quarterly Market Outlook: Quarter 1 2018 on 5 th January 2018 Investment Outlook for 1 st Quarter 2018 Accelerating Global Economy Supports the Rising Earnings Equity Thailand US Europe Japan Asia Bond

Chad Wilkerson. Vice President, Economist, and Oklahoma City Branch Executive Federal Reserve Bank of Kansas City

Chad Wilkerson Vice President, Economist, and Oklahoma City Branch Executive Federal Reserve Bank of Kansas City www.kansascityfed.org Overview of the Federal Reserve System The Fed consists of three main

Chad Wilkerson Vice President, Economist, and Oklahoma City Branch Executive Federal Reserve Bank of Kansas City www.kansascityfed.org Overview of the Federal Reserve System The Fed consists of three main

Eurozone Economic Watch. May 2018

Eurozone Economic Watch May 2018 BBVA Research - Eurozone Economic Watch / 2 Eurozone: more moderate growth with higher uncertainty The eurozone GDP growth slowed in more than expected. Beyond temporary

Eurozone Economic Watch May 2018 BBVA Research - Eurozone Economic Watch / 2 Eurozone: more moderate growth with higher uncertainty The eurozone GDP growth slowed in more than expected. Beyond temporary

Weekly Economic Commentary

LPL FINANCIAL RESEARCH Weekly Economic Commentary May 29, 2012 Policymakers, Pundits, and Politicians Eye the May Jobs Report John Canally, CFA Economist LPL Financial Highlights The May jobs report is

LPL FINANCIAL RESEARCH Weekly Economic Commentary May 29, 2012 Policymakers, Pundits, and Politicians Eye the May Jobs Report John Canally, CFA Economist LPL Financial Highlights The May jobs report is

The Korean Economy: Resilience amid Turbulence

The Korean Economy: Resilience amid Turbulence Dr. Il SaKong Special Economic Advisor Adviser to the President Republic of Korea November 17, 17, 2008 November 17, 2008 1. Recent Macroeconomic Developments

The Korean Economy: Resilience amid Turbulence Dr. Il SaKong Special Economic Advisor Adviser to the President Republic of Korea November 17, 17, 2008 November 17, 2008 1. Recent Macroeconomic Developments

U.S. Economic Outlook and Monetary Policy

U.S. Economic Outlook and Monetary Policy March 26, 21 Craig S. Hakkio Senior Vice President and Special Advisor on Economic Policy Overview U.S. growth remains strong, though temporary factors are likely

U.S. Economic Outlook and Monetary Policy March 26, 21 Craig S. Hakkio Senior Vice President and Special Advisor on Economic Policy Overview U.S. growth remains strong, though temporary factors are likely

U.S. Automotive Outlook

2004 FTA Revenue Estimation and Tax Research Conference September 19-22, 2004 Burlington, VT U.S. Automotive Outlook David P. Teolis Senior Economist North America Global Market & Industry Analysis Presentation

2004 FTA Revenue Estimation and Tax Research Conference September 19-22, 2004 Burlington, VT U.S. Automotive Outlook David P. Teolis Senior Economist North America Global Market & Industry Analysis Presentation

An abnormally-slow December caps off the year with a range of bright spots as well as challenges. U.S. employment situation: September 2013

An abnormally-slow December caps off the year with a range of bright spots as well as challenges U.S. employment situation: September 2013 U.S. Release employment date: October situation: 22, December

An abnormally-slow December caps off the year with a range of bright spots as well as challenges U.S. employment situation: September 2013 U.S. Release employment date: October situation: 22, December

Global Economic Outlook

Global Economic Outlook Will growth continue and at what pace? International Containerboard Conference Chicago November 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary

Global Economic Outlook Will growth continue and at what pace? International Containerboard Conference Chicago November 2018 Lasse Sinikallas Director, Macroeconomics Copyright 2018 RISI, Inc. Proprietary

A summary of regional and national economic indicators for the Tenth District states SUMMARY OF CURRENT TENTH DISTRICT ECONOMIC CONDITIONS

Tenth THE District ECONOMIC DATABOOK A summary of regional and national economic indicators for the states FEBRUARY 26, 218 FEDERAL RESERVE BANK of KANSAS CITY SUMMARY OF CURRENT TENTH DISTRICT ECONOMIC

Tenth THE District ECONOMIC DATABOOK A summary of regional and national economic indicators for the states FEBRUARY 26, 218 FEDERAL RESERVE BANK of KANSAS CITY SUMMARY OF CURRENT TENTH DISTRICT ECONOMIC

The US and New Mexico Economies: Recent Developments and Outlook

The US and New Mexico Economies: Recent Developments and Outlook March 2016 A presentation to New Mexico Bankers Association Presented by Jeffrey Mitchell, Director, UNM-BBER National Economy: Review o

The US and New Mexico Economies: Recent Developments and Outlook March 2016 A presentation to New Mexico Bankers Association Presented by Jeffrey Mitchell, Director, UNM-BBER National Economy: Review o

Households: Net Worth Advances, Debt Outstanding Declines. Chart 1

Asha G. Bangalore agb3@ntrs.com Households: Net Worth Advances, Debt Outstanding Declines June 9, 2 Households experienced another quarter of gains in their net worth without improvements in real estate

Asha G. Bangalore agb3@ntrs.com Households: Net Worth Advances, Debt Outstanding Declines June 9, 2 Households experienced another quarter of gains in their net worth without improvements in real estate

Quarterly Report. April June 2014

April June August 1, 1 Outline 1 Monetary Policy External Conditions 5 Economic Activity in Mexico Inflation Determinants Forecasts and Balance of Risks Monetary Policy Conduction Monetary policy has focused

April June August 1, 1 Outline 1 Monetary Policy External Conditions 5 Economic Activity in Mexico Inflation Determinants Forecasts and Balance of Risks Monetary Policy Conduction Monetary policy has focused