29 Week 10. Portfolio theory Overheads

|

|

|

- Elvin Morgan

- 5 years ago

- Views:

Transcription

Options (f) Doubts and opportunities. (g) (Contingent claims approach) (h) (Taming wild weights, Bayesian portfolio theory) 2. The average investor holds the market portfolio.")

1 29 Week 1. Portfolio theory Overheads 1. Outline (a) Mean-variance (b) Multifactor portfolios (value etc.) (c) Outside income, labor income. (d) Taking advantage of predictability. (e) Options (f) Doubts and opportunities. (g) (Contingent claims approach) (h) (Taming wild weights, Bayesian portfolio theory) 2. The average investor holds the market portfolio. (a) Anything other than index is a zero-sum game (relative to the index) (b) We can t all rebalance (c) How are you different from average? Smarter? Risk? (write/buy insurance) 29.1 Mean-variance classic results 1. Mean variance reminder (a) Two fund theorem. The composition of the stock (tangency) portfolio is the same for all investors. We re all out of business. (b) No tailored portfolios. (c) Think of the portfolio, not assets in isolation. (d) Names and styles don t matter. Only means, betas, and covariances matter. 58

2 (e) Passive, then optimally-diversified active. 2. Portfolio maximization problems. Where did this come from? (a) The simplest example: max [( +1 )] [] +1 = +1 = = (1 ) + +1 = + +1 n h³ max io + [] +1 n h³ : i o = Solve for. (Problemset) (b) Hey wait a minute, this is ( +1 ) +1ª = the same = () equation we ve been looking at along! (c) In our theory section, we fixed the properties of consumption and saw how returns would have to adjust. Here we fix the properties (mean, variance) of returns, and see how consumption (i.e. the portfolio weight which governs consumption) adjusts. Resolution: previously what is the question (properties of returns) so the answer is hold the market portfolio? (d) Optimal salads vs optimal portfolios The real portfolio problem Here is the kind of problem we really want to solve. max X ( )or { } = Z ( ); +1 = +1 ( + ); +1 = + +1 = 1portfolioweights +1 = 1 asset excess returns (+1) = (+1 +1) = Σ 581

3 29.3 Mean variance portfolios 1. A special case, easy to solve, easy to interpret. 2. Key result: If the investor has no job =, if returns are independent over time ( ( +1 ) =const), and with power utility and lognormal returns, the investor wants to hold a mean-variance efficient portfolio. 3. Portfolio formula (weights): = 1 Σ 1 ( ) where Σ = ( ); =investorriskaversion (a) Composition: Σ 1 ( ). Optimal diversification Tangency portfolio Formula used in all portfolio optimizing programs! (b) Scale: 1. Two-fund theorem. (c) Optimal diversification: Σ takes care of the correlation of assets. (d) Mean-variance. This is also the solution to min ( )s.t.( ) = min {} Σ = Σ = = Σ 1 (e) Numbers: For a single risky asset ( stocks/bonds ) 4. Portfolio relative to the market: = 1 () 2 () 6 = (a) If the investor lives in an economy where everyone else is the same except risk aversion, investors i s optimal portfolio is = with return = + where and R are the market portfolio, which is on the mean-variance frontier, and is average risk aversion (b) Useful: what s your? vs. Are you more or less risk averse than average? (c) If the investor lives in an economy where everyone else is the same except risk aversion, the CAPM holds. ( )=( ) (and if the CAPM does not hold, somebody is not following this portfolio advice) 582

4 5. Horizon effects. (a) If returns are lognormal iid and the investor has power utility, the allocation to risky assets is independent of investment horizon. (b) Intuition: With iid returns, mean and variance both scale with horizon so = 1 () 2 () is unaffected. (c) The fallacy of time-diversification (oft-repeated). The variance of annualized returns is lower for longer horizon, but not the variance of total returns. 6. Factor models and alphas 2 ( ) = 2 () 1 2 ( ) = 1 2 () (a) If returns follow a factor model, such as the CAPM, = + State the problem as portable alpha how much in the market, and how much to chase, Answer = ( )= + + ( + ) = 1 ( ) 2 ( ) ; = 1 Σ 1 Separately think about your factor exposures and your alpha exposures. Passive vs. active. (b) Σ 1 tells you how much to chase. Not infinite! Themoreyouchase, theless diversified your portfolio. (c) Σ 1 tells you how to diversify optimally across your active managers or alpha bets. This depends on the correlation of their strategies. (d) Small alphas with even smaller Σ can be great bets if you can leverage them enough. 7. What s wrong (a) Assumption 1: No job! (b) Assumption 2: Returns are iid, +1 is constant over time! What about +1 = ( +1 )= +? (Hedge fund use of this formula is particularly silly.) (c) Prediction 1: Returns follow the CAPM. If not, somebody is not using this formula. Maybe you shouldn t either? (d) The portfolio problem also says consume proportionally to wealth. = ( ln ) = ( ln ) = 16%! If you don t want to follow this advice, ( consume steadily, the market will bounce back ) why follow the portfolio advice? 583

5 29.4 Multifactor/Merton How do value/growth/momentum, predictability, and the fact that people have jobs or businesses change this picture? 1. Example: A recession factor. Axes: mean ( ), standard deviation ( ), covariance or of portfolio with recessions. (a) MVF becomes a multifactor efficient frontier E(R) (R) E(R) f R (R) 584

6 (b) The average (and hence market) portfolio is no longer on the mean-variance frontier. (c) Assumption change: Investors do have labor, business income, illiquid portfolio, real estate or other asset that cannot be sold. They want portfolios that hedge against risks to these state variables. (d) Varying ( +1 )worksthesameway. ( Merton )Lower +1 is bad news, so you want assets that go up when +1 (D/P) decline. 2. Math: We solve the problem with job/business and/or with varying ( ) ( ) max X ( )or { } = Z ( ); +1 = +1 ( + ); +1 = + +1 = 1 portfolio weights = 1 asset excess returns An example of a model for time-varying returns and time-varying outside income: state variables, shocks to asset returns +1 and shocks to state variables = ( +1) = Σ +1 = = Result: (weights) investors value mean, want to control variance, and want to control covariance with state variables (outside income, news of future returns) = 1 Σ 1 (+1)+ = market timing/mean-variance + hedging demand = aversion to state variable risk. = beta of returns on state variable shocks We add a) market timing and b) hedging demand for securities. 4. (Returns) Relative to market, and others, if everyone is like this: your portfolio return is +1 = ³ : fitted value in a regression of shocks on = hedge portfolio or mimicking portfolio for state variable risk. market average values. 585

7 5. If everyone is like this, an ICAPM holds 6. Implications of hedging demand: ( )= ( ) ( ) (a) Ifyou relikeeveryoneelse = youjustholdthemarket,despite the value premium. (b) Mean-variance investor ( = ) ( Writes insurance ) and gets better than to do it! ( is no longer mean-variance efficient.) (c) Investors differ by risk aversion and aversion to recession risk. Three (or more) fund theorem. (d) Nonpriced or 6= matter too. Hedging outside income risk is job 1, and does not require any alphas. Our focus on anomalies with, 6= is misplaced. 7. More recipes (a) We can split the optimal portfolio in two parts. 1) Hedge as much of the outside income as possible, by shorting a portfolio that looks as much like outside income as possible 2) The rest of the portfolio is on the mean-variance frontier. (b) Hedge outside income to the extent that you re different from everyone else. Then 2) hold market index = ³ (c) Style coaching is a reason for tailored portfolios! With fees! (d) This is separate business separate management companies can set up 1) hedge portfolios 2) passive indices 3) alphas. 8. Summary: Two big sources of hedging demand. (a) Hedging outside income jobs, businesses, human capital etc. (b) Hedging intertemporal opportunities An example of why extra state variables / intertemporal thinking is important. 1. Normal times, a 6/4 allocation with 6% equity premium and 18% volatility = 1 () 2 () = Oct 28, monthly volatility rose to 7%. How should we adjust our portfolio weights? 1 6 =397 = 4% equity

8 (a) Ok, you say, as prices fall, expected return rose. How much? With prices down you re probably at 4% not 6% equity, so we only need to find 1 ( ) = 4 ( ) = =6 = 6%! (b) If it makes sense for you to dump, why not everyone else? Formula is not new to science (c) Was the market irrationally optimistic, and overvalued? 3. Resolution: This is the wrong formula. Mulitifactor/state variable thinking is really important in the real world. 4. To drive the point home, consider long term bond investor story (a) Liability in 1 years, 1 year zero coupon TIP. Price of a bond that matures in year 1 simulation price What to do??? 1 Bonds: Answer: Do nothing time, years Price of a bond that matures in year 1 simulation bond price time, years 587

9 Bonds: Do nothing Price of a bond that matures in year 1 simulation bond price time, years Bonds: Do nothing (b) For most investors the risk free asset is a coupon-only long-term TIP, not a money market fund, and they should ignore its price fluctuations! (c) Viewed Merton-style risky share = 1 expected return - riskfree rate r.a. return variance + aversion to yield change cov.(return, yield change) Bonds are a perfect hedge against the state variable, yield. Cov.(return, yield change) is a strong negative number. The aversion is also a negative number, so you do hold bonds despite () =,andhuge(). (d) Long-term bonds also overturn the result that the portfolio is the same for all horizon investors. Can the same apply to stocks... (e) Are stocks a bit like bonds, so do nothing is at least partially right? Does a price decline mean higher yield (return)? Yes! DP and returns! 5. Bottom line: (a) Long term bonds are a great example to keep in mind why one-period mean-variance is a terrible guide when there are important state variables (changes in ()) state variable hedge demands really matter. (b) Common practice is to model ( +1 ) Σ, and then use one-period maximizers, ignoring hedging demands. This would be a huge mistake in this example, sending you to short term bonds rather than the correct long term bonds. (c) Looking directly at cashflows is much simpler than these one-period formulas! Intertemporal hedging demands (state variables for expected returns) disappear from the long-run portfolio if you look at it right. 588

10 29.6 Predictability How does stock return forecastability (d/p), bond return forecastability (f-y), exchange rate forecastability ( )affect portfolio decisions? 1. Market timing? Horizon effects? Hedge state variable shifts (e.g. volatility)? 2. Portfolio problem. Just as above, but use our regressions. For example, 3. Answer: +1 = + ( ) = + ( ) ( +1 )=( )+ +1 = 1 Σ 1 (+1)+ ; = For one asset, = 1 (+1 ) 2( +1 ) + ( ) 2( +1 ) Market timing demand plus hedge demand. 4. Hedge demand. An asset can hedge itself. Example: long term bonds! (a) If a bond yield goes down (bad news) then the bond price goes up (it hedges its own bad news). Hence long term bonds are safe for long term investors, despite poor 2. (, ( ) ). (b) Stocks are a bit like bonds poor returns means lower P/D, higher expected returns hedging demand! We saw ( ) is very strong and negative; stocks like bonds are good hedges for their intertemporal opportunities. (c) This hedge value increases with horizon, ( is bigger for longer-lived investors) so justifies some horizon effects. (d) Note varying ( +1 ) (you care) is not enough for hedge demands. You need the covariance () as well. (you can do something about it) (e) The market timing demand is what comes out of a one-period optimizer. When you use one-period optimizers in a dynamic environment, you re ignoring the hedging demand. 5. Market timing demand: (a) Given a regression model, i.e. we have +1 = + ( +1) = + µ µ + +1 ; 2 ( +1) = 2. We can calculate how much the investor should market time ³ =

11 (b) Problem set 1 d/p regression +1 = () ( 12) (266) 2 = 1981% (35) γ=1 15 Allocation to stocks (%) 1 5 γ=2 γ=5 γ=1 γ= d/p ratio (%) ( ) Market timing portfolio allocation. The allocation to risky stocks is = 1 Expected 2 excess returns come from the fitted value of a regression of returns on dividend yields, +1 = + ( )+ +1. The vertical lines mark () ± 2() 59

+ +1.")

12 25 2 γ=2 γ= allocation to stocks (%) γ=5 γ=1 γ= time ( ) 2 Market timing portfolio allocation over time. The allocation to risky stocks is = 1 Expected excess returns come from the fitted value of a regression of returns on dividend yields, +1 = + ( )+ +1. This seems to imply incredibly strong market timing based on d/p! (c) A complete calculation by Campbell and Viceira. (Hard math, includes hedge demand) 591

13 (d) This seems incredibly aggressive! How to tame this wild advice? Bayesian portfolio theory? (e) Hedging demands? Harder to calculate. (f) Reality? This is what hedge funds do. Except without hedging demands! And their portfolio optimizers blow up too. 6. Note: The average investor holds the market. Why doesn t everyone do this? And if they did, the phenomenon would disappear. Was leaving out a good idea? 592

14 3 Mean-Variance Benchmark 1. The idea: Hedging demands are important. People don t use them. A solution? 2. Example: Long-term bonds. : (a) Buy long term (indexed, riskfree) bonds because their one-year returns covary negatively with shocks to their reinvestment risks (b) Buy long term bonds because at a long horizon, they pay the same amount no matter what happens 3. Why not look at long horizon portfolios directly? In a very simple example, max [( )] ( )( ) (a) Dynamic strategies generate more like funds. 4. People don t want a single long horizon. They want streams of dividends, X max ( ) = is the dividend stream from an investment strategy Hence, the paper idea X X ( )= ( )= [( )] = = If you treat time and probability symmetrically and look at the final payoffs, The long horizon problem is the same as a one-period problem 5. Results: With quadratic utility, even with all sorts of dynamics ( +1 ) etc. (a) Investors choose { } on a long-run mean-variance frontier. (b) A long-run CAPM. (c) State variables drop out! (d) Outside income does not drop out. Short a portfolio that hedges your outside income, then invest in a long-run mean-variance efficient portfolio (e) A long-run multifactor model with average outside income. 6. Limitations: Quadratic utility 7. The chat. This isn t easy 593

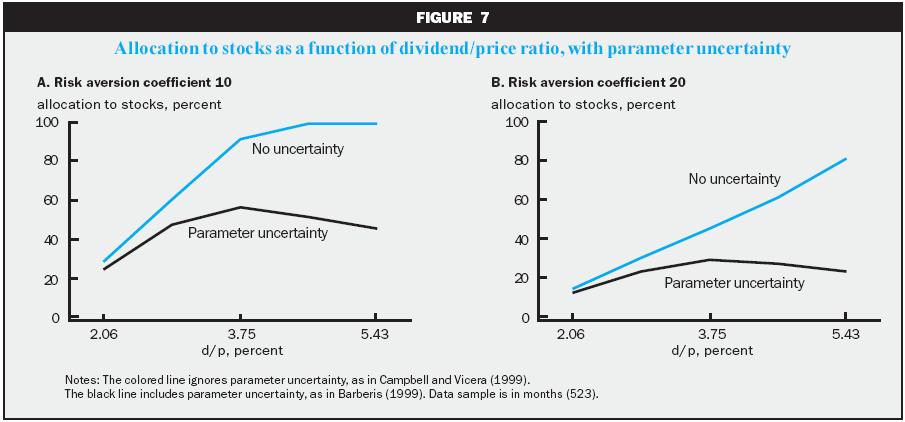

15 3.1 Bayesian portfolios, parameter uncertainty, and taming market timing. 1. What about those wacky portfolio weights? So far we have treated models ( Σ, +1 = + ) as if the parameters were perfectly known, but we don t really know them. Does this matter? Motivation: Think about the DP regression and its wild advice. But ( +1 ) are not well measured. 2. What s the effect of parameter uncertainty on portfolios? How uncertainty adds to your risk. (a) Standard errors are symmetric. They say you re as likely to be underinvested as overinvested (b) Parameter uncertainty is a source of risk to investors, and says to be more conservative. (c) Example: Suppose =5. =or = 2, equally likely. The risk you face is not = () =1 = μ = 1, σ = 5.4 1/2 μ = + 1/2 μ = (d) How do we incorporate that intuition quantitatively? error of the mean to the variance of the return. Bottom line: Add the standard risky share = 1 r.a. expected return - riskfree rate return var.+ uncertainty about E return = 1 ( ) 2 ( )+ 2 (( )) parameter uncertainty makes you take less risk. (e) Important practical application. The average hedge fund runs a complex model for expected returns, and plugs it in to the optimizer as if the parameters are known. 3. Application 1 Parameter uncertainty makes stocks riskier for long-run investors. = 1 A calculation, after Barberis (2). ( ) 2 ( )+ 1 2 ( ) = 1 ( ) 2 ( )(1 + 1 ) 594

16 8 γ = 5, T = 43 4 γ = 1, T = 43 allocation to stocks allocation to stocks horizon horizon 8 γ = 5, T = 9 4 γ = 1, T = 9 allocation to stocks allocation to stocks horizon horizon Portfolio allocation to stocks with parameter uncertainty. The solid lines present the case with parameter uncertainty, and the dashed lines ignore parameter uncertainty. The allocation to stocks is = ( 1) ). =6 =1428 for =43and =78 =151 for =9 with =. (Theextra( 1) allows for continuous rebalancing. See Portfolio Theory. ) So, are stocks safer for long term investors? (a) Classic result: allocation is independent of horizon (iid returns, known parameters, no outside income) (b) dp, mean reversion, with dp shocks negatively correlated to return shocks : Stocks are like bonds, safer in the long run. (not iid returns) (c) Parameter uncertainty: Stocks are riskier in the long run (parameter uncertainty) (d) And we forgot... the stock/bond nature of wages and outside income. 4. Application to DP regressions: Recognizing the uncertainty about predictability variation in E(R) over time leads you to shade portfolios back towards constant weights. +1 = + ( ) = 2 (ˆ)+ 2 (ˆ)( ) 2 +2(ˆ ˆ) 595

17 E(R dp) dp none 1 yr weight in stocks yr 1 yr dp = 1 ˆ + ˆ( ) 2 ()+horiz 2 +1 Widening of the error bands is what matters here. Functional form uncertainty (squared dp etc) would make it much bigger. (a) A much more precise (but very hard) calculation by Barberis (2) 596

18 597

19 3.2 Wacky weights in mean-variance analysis. 1. Example: FF 25 portfolios + 3 factors. 2 years of data (a lot!) Optimal E (%/mo) FF3F.5 rmrf min var σ (%/mo) optimal : = 1 Σ 1 low high small large rmrf hml smb

20 2. Intuition: Mean Apparent optimal portfolio Very long A, short B A in sample True (equal) Risk free B in sample Standard deviation Portfolio optimization problems are very sensitive to mean return inputs, especially when there are highly correlated assets. 3. What do we do to tame wacky weights? (a) Short constraints (b) Ad-hoc rules. But miss the opportunities? (c) Warning: Standard rules fail when faced with hedge funds/derivatives. 1% exposure in a = 1 investment is 1% exposure, so weights don t limit risks. (d) Bayesian approaches? (Optional notes) (e) More generally, fit fancy models, treat the parameters as known, feed the results to a black box portfolio optimizer is a very bad strategy! (Read, typical hedge fund.) 599

21 3.3 Options Writing puts Profit Large chance of a small, riskless gain Stock price Small chance of a huge loss Write put options? But the average investor holds the market. Why are put option premiums so high? A: there is a lot of demand to buy put options despite the high premium. Very sensibly! 1. Leverage. If we lose more than 2%, we default on our debt 2. If we lose more than 2% we have to cut core functions. 3. If we lose more than 2%, our sponsors will give up and fire us. 4. Put options are attractive to these investors despite the cost Probability distribution with and without protective put Market Index With Protective Put probability Lose some gains Eliminate extreme losses year gross return 6

22 5. A stop loss order is not the same as a put option 6. Buy vs. write options? Receive premium or buy insurance despite the large premium? A: Are you more or less able to take crash risks than the average investor? Really, now? 7. Big picture: You can tailor the entire shape of the return distribution. Example 2: Should we rebalance? Wall Street wisdom says yes. 1. The average investor can t rebalance. 2. Rebalancing is just like writing both call and put options. 3. Example: The S&P5 index is 1,, you have $1,, and you start with 5/5 allocation. If you do not rebalance, your wealth follows the red line. If at S&P=5/15 you rebalance, you have the blue lines, and the blue dots after two moves. A bet on low volatility. Just as if you wrote both puts and calls. Wealth S&P5 4. Constantly rebalance? 5 year wealth. A bet on low volatility Rebalanced Constant Probability Wealth outcomes, T=5 σ=.2 α= Wealth S&P5 Index 5. Rebalancing is optimal if you have power utility returns are iid and lognormal. They re not. We can t all rebalance! 61

23 3.4 More portfolio theory doubts 1. The average investor holds the market portfolio. (a) Predictability: Why do ER vary in the first place? (b) Value, size, momentum: Why is there value in the first place? (c) Why are you different? 2. Catch 22. Anomalies only last if you can t use them. (a) Data-dredging?. (b) Mispricing/overlooked?. (c) Mispricing, but can t arbitrage it due to constraints or transactions costs? (d) Mispricing, but needs institutional reform? (e) Risk factor? 3. Implied consumption from portfolio optimization problems is incredibly volatile. If you take the portfolio advice, why don t you buy the consumption advice? If the model is wrong for consumption why do you believe it for portfolios? 4. Transactions costs! 5. Taxes! 3.5 Good things to say 1. Optimal portfolio 1962: High fee Tailored portfolios 2. Optimal portfolio 1972: on market, two fund theorem. No Fee. Maybe chase a little alpha? 3. Optimal portfolio Now: (a) Hedge labor/outside income risks (b) Find desired priced factor allocation rmrf, hml, smb, umd, etc. (c) Find right distribution put options etc. (d) Chase alpha? (alpha=beta you don t understand) (e) Offset implied factor premia in active part. (f) There is a lot for professional advice to offer again! 4. Investors should hedge their labor or proprietary income risks. Find important nonpriced factors! 5. Investors do silly things. 6. If you re going to work for a hedge fund, forget all my doubts and learn to do complex optimal portfolios with good risk management (covariance matrices). 62

Problem Set 6. I did this with figure; bar3(reshape(mean(rx),5,5) );ylabel( size ); xlabel( value ); mean mo return %

,5,5) );ylabel( size ); xlabel( value ); mean mo return %") Business 35905 John H. Cochrane Problem Set 6 We re going to replicate and extend Fama and French s basic results, using earlier and extended data. Get the 25 Fama French portfolios and factors from the

Business 35905 John H. Cochrane Problem Set 6 We re going to replicate and extend Fama and French s basic results, using earlier and extended data. Get the 25 Fama French portfolios and factors from the

Problem set 1 Answers: 0 ( )= [ 0 ( +1 )] = [ ( +1 )]

![Problem set 1 Answers: 0 ( )= [ 0 ( +1 )] = [ ( +1 )]](/thumbs/90/101609040.jpg "Problem set 1 Answers: 0 ( )= [ 0 ( +1 )] = [ ( +1 )]") Problem set 1 Answers: 1. (a) The first order conditions are with 1+ 1so 0 ( ) [ 0 ( +1 )] [( +1 )] ( +1 ) Consumption follows a random walk. This is approximately true in many nonlinear models. Now we

Problem set 1 Answers: 1. (a) The first order conditions are with 1+ 1so 0 ( ) [ 0 ( +1 )] [( +1 )] ( +1 ) Consumption follows a random walk. This is approximately true in many nonlinear models. Now we

Problem Set 4 Answers

Business 3594 John H. Cochrane Problem Set 4 Answers ) a) In the end, we re looking for ( ) ( ) + This suggests writing the portfolio as an investment in the riskless asset, then investing in the risky

Business 3594 John H. Cochrane Problem Set 4 Answers ) a) In the end, we re looking for ( ) ( ) + This suggests writing the portfolio as an investment in the riskless asset, then investing in the risky

Financial Mathematics III Theory summary

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

Problem Set 4 Solutions

Business John H. Cochrane Problem Set Solutions Part I readings. Give one-sentence answers.. Novy-Marx, The Profitability Premium. Preview: We see that gross profitability forecasts returns, a lot; its

Business John H. Cochrane Problem Set Solutions Part I readings. Give one-sentence answers.. Novy-Marx, The Profitability Premium. Preview: We see that gross profitability forecasts returns, a lot; its

FIN 6160 Investment Theory. Lecture 7-10

FIN 6160 Investment Theory Lecture 7-10 Optimal Asset Allocation Minimum Variance Portfolio is the portfolio with lowest possible variance. To find the optimal asset allocation for the efficient frontier

FIN 6160 Investment Theory Lecture 7-10 Optimal Asset Allocation Minimum Variance Portfolio is the portfolio with lowest possible variance. To find the optimal asset allocation for the efficient frontier

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice A. Mean-Variance Analysis 1. Thevarianceofaportfolio. Consider the choice between two risky assets with returns R 1 and R 2.

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice A. Mean-Variance Analysis 1. Thevarianceofaportfolio. Consider the choice between two risky assets with returns R 1 and R 2.

BUSM 411: Derivatives and Fixed Income

BUSM 411: Derivatives and Fixed Income 3. Uncertainty and Risk Uncertainty and risk lie at the core of everything we do in finance. In order to make intelligent investment and hedging decisions, we need

BUSM 411: Derivatives and Fixed Income 3. Uncertainty and Risk Uncertainty and risk lie at the core of everything we do in finance. In order to make intelligent investment and hedging decisions, we need

FF hoped momentum would go away, but it didn t, so the standard factor model became the four-factor model, = ( )= + ( )+ ( )+ ( )+ ( )

= + ( )+ ( )+ ( )+ ( )") 7 New Anomalies This set of notes covers Dissecting anomalies, Novy-Marx Gross Profitability Premium, Fama and French Five factor model and Frazzini et al. Betting against beta. 7.1 Big picture:three rounds

7 New Anomalies This set of notes covers Dissecting anomalies, Novy-Marx Gross Profitability Premium, Fama and French Five factor model and Frazzini et al. Betting against beta. 7.1 Big picture:three rounds

6a. Current holders of Greek bonds face which risk? a) inflation risk

inflation risk") Final Practice Problems 1. Calculate the WACC for a company with 10B in equity, 2B in debt with an average interest rate of 4%, a beta of 1.2, a risk free rate of 0.5%, and a market risk premium of 5%.

Final Practice Problems 1. Calculate the WACC for a company with 10B in equity, 2B in debt with an average interest rate of 4%, a beta of 1.2, a risk free rate of 0.5%, and a market risk premium of 5%.

15.414: COURSE REVIEW. Main Ideas of the Course. Approach: Discounted Cashflows (i.e. PV, NPV): CF 1 CF 2 P V = (1 + r 1 ) (1 + r 2 ) 2

: CF 1 CF 2 P V = (1 + r 1 ) (1 + r 2 ) 2") 15.414: COURSE REVIEW JIRO E. KONDO Valuation: Main Ideas of the Course. Approach: Discounted Cashflows (i.e. PV, NPV): and CF 1 CF 2 P V = + +... (1 + r 1 ) (1 + r 2 ) 2 CF 1 CF 2 NP V = CF 0 + + +...

15.414: COURSE REVIEW JIRO E. KONDO Valuation: Main Ideas of the Course. Approach: Discounted Cashflows (i.e. PV, NPV): and CF 1 CF 2 P V = + +... (1 + r 1 ) (1 + r 2 ) 2 CF 1 CF 2 NP V = CF 0 + + +...

The mean-variance portfolio choice framework and its generalizations

The mean-variance portfolio choice framework and its generalizations Prof. Massimo Guidolin 20135 Theory of Finance, Part I (Sept. October) Fall 2014 Outline and objectives The backward, three-step solution

The mean-variance portfolio choice framework and its generalizations Prof. Massimo Guidolin 20135 Theory of Finance, Part I (Sept. October) Fall 2014 Outline and objectives The backward, three-step solution

B35150 Winter 2014 Quiz Solutions

B35150 Winter 2014 Quiz Solutions Alexander Zentefis March 16, 2014 Quiz 1 0.9 x 2 = 1.8 0.9 x 1.8 = 1.62 Quiz 1 Quiz 1 Quiz 1 64/ 256 = 64/16 = 4%. Volatility scales with square root of horizon. Quiz

B35150 Winter 2014 Quiz Solutions Alexander Zentefis March 16, 2014 Quiz 1 0.9 x 2 = 1.8 0.9 x 1.8 = 1.62 Quiz 1 Quiz 1 Quiz 1 64/ 256 = 64/16 = 4%. Volatility scales with square root of horizon. Quiz

15 Week 5b Mutual Funds

15 Week 5b Mutual Funds 15.1 Background 1. It would be natural, and completely sensible, (and good marketing for MBA programs) if funds outperform darts! Pros outperform in any other field. 2. Except for...

15 Week 5b Mutual Funds 15.1 Background 1. It would be natural, and completely sensible, (and good marketing for MBA programs) if funds outperform darts! Pros outperform in any other field. 2. Except for...

CLASS 4: ASSEt pricing. The Intertemporal Model. Theory and Experiment

CLASS 4: ASSEt pricing. The Intertemporal Model. Theory and Experiment Lessons from the 1- period model If markets are complete then the resulting equilibrium is Paretooptimal (no alternative allocation

CLASS 4: ASSEt pricing. The Intertemporal Model. Theory and Experiment Lessons from the 1- period model If markets are complete then the resulting equilibrium is Paretooptimal (no alternative allocation

+1 = + +1 = X 1 1 ( ) 1 =( ) = state variable. ( + + ) +

1 =( ) = state variable. ( + + ) +") 26 Utility functions 26.1 Utility function algebra Habits +1 = + +1 external habit, = X 1 1 ( ) 1 =( ) = ( ) 1 = ( ) 1 ( ) = = = +1 = (+1 +1 ) ( ) = = state variable. +1 ³1 +1 +1 ³ 1 = = +1 +1 Internal?

26 Utility functions 26.1 Utility function algebra Habits +1 = + +1 external habit, = X 1 1 ( ) 1 =( ) = ( ) 1 = ( ) 1 ( ) = = = +1 = (+1 +1 ) ( ) = = state variable. +1 ³1 +1 +1 ³ 1 = = +1 +1 Internal?

18 Week 6 Hedge funds Overheads

18 Week 6 Hedge funds Overheads Background: 1. What are they? (a) Legal, regulatory: a partnership. (b) Fee structure: 2+2, high water mark, cash benchmark (c) Typically can leverage, short-sell, use derivatives,

18 Week 6 Hedge funds Overheads Background: 1. What are they? (a) Legal, regulatory: a partnership. (b) Fee structure: 2+2, high water mark, cash benchmark (c) Typically can leverage, short-sell, use derivatives,

International Finance. Investment Styles. Campbell R. Harvey. Duke University, NBER and Investment Strategy Advisor, Man Group, plc.

International Finance Investment Styles Campbell R. Harvey Duke University, NBER and Investment Strategy Advisor, Man Group, plc February 12, 2017 2 1. Passive Follow the advice of the CAPM Most influential

International Finance Investment Styles Campbell R. Harvey Duke University, NBER and Investment Strategy Advisor, Man Group, plc February 12, 2017 2 1. Passive Follow the advice of the CAPM Most influential

Understanding Volatility Risk

Understanding Volatility Risk John Y. Campbell Harvard University ICPM-CRR Discussion Forum June 7, 2016 John Y. Campbell (Harvard University) Understanding Volatility Risk ICPM-CRR 2016 1 / 24 Motivation

Understanding Volatility Risk John Y. Campbell Harvard University ICPM-CRR Discussion Forum June 7, 2016 John Y. Campbell (Harvard University) Understanding Volatility Risk ICPM-CRR 2016 1 / 24 Motivation

Lecture 10-12: CAPM.

Lecture 10-12: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Minimum Variance Mathematics. VI. Individual Assets in a CAPM World. VII. Intuition

Lecture 10-12: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Minimum Variance Mathematics. VI. Individual Assets in a CAPM World. VII. Intuition

Should Norway Change the 60% Equity portion of the GPFG fund?

Should Norway Change the 60% Equity portion of the GPFG fund? Pierre Collin-Dufresne EPFL & SFI, and CEPR April 2016 Outline Endowment Consumption Commitments Return Predictability and Trading Costs General

Should Norway Change the 60% Equity portion of the GPFG fund? Pierre Collin-Dufresne EPFL & SFI, and CEPR April 2016 Outline Endowment Consumption Commitments Return Predictability and Trading Costs General

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS. BKM Ch 7

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS BKM Ch 7 ASSET ALLOCATION Idea from bank account to diversified portfolio Discussion principles are the same for any number of stocks A. bonds and stocks B.

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS BKM Ch 7 ASSET ALLOCATION Idea from bank account to diversified portfolio Discussion principles are the same for any number of stocks A. bonds and stocks B.

Problem Set 1 Due in class, week 1

Business 35150 John H. Cochrane Problem Set 1 Due in class, week 1 Do the readings, as specified in the syllabus. Answer the following problems. Note: in this and following problem sets, make sure to answer

Business 35150 John H. Cochrane Problem Set 1 Due in class, week 1 Do the readings, as specified in the syllabus. Answer the following problems. Note: in this and following problem sets, make sure to answer

Models of Asset Pricing

appendix1 to chapter 5 Models of Asset Pricing In Chapter 4, we saw that the return on an asset (such as a bond) measures how much we gain from holding that asset. When we make a decision to buy an asset,

appendix1 to chapter 5 Models of Asset Pricing In Chapter 4, we saw that the return on an asset (such as a bond) measures how much we gain from holding that asset. When we make a decision to buy an asset,

John H. Cochrane. April University of Chicago Booth School of Business

Comments on "Volatility, the Macroeconomy and Asset Prices, by Ravi Bansal, Dana Kiku, Ivan Shaliastovich, and Amir Yaron, and An Intertemporal CAPM with Stochastic Volatility John Y. Campbell, Stefano

Comments on "Volatility, the Macroeconomy and Asset Prices, by Ravi Bansal, Dana Kiku, Ivan Shaliastovich, and Amir Yaron, and An Intertemporal CAPM with Stochastic Volatility John Y. Campbell, Stefano

1.1 Interest rates Time value of money

Lecture 1 Pre- Derivatives Basics Stocks and bonds are referred to as underlying basic assets in financial markets. Nowadays, more and more derivatives are constructed and traded whose payoffs depend on

Lecture 1 Pre- Derivatives Basics Stocks and bonds are referred to as underlying basic assets in financial markets. Nowadays, more and more derivatives are constructed and traded whose payoffs depend on

One-Period Valuation Theory

One-Period Valuation Theory Part 2: Chris Telmer March, 2013 1 / 44 1. Pricing kernel and financial risk 2. Linking state prices to portfolio choice Euler equation 3. Application: Corporate financial leverage

One-Period Valuation Theory Part 2: Chris Telmer March, 2013 1 / 44 1. Pricing kernel and financial risk 2. Linking state prices to portfolio choice Euler equation 3. Application: Corporate financial leverage

Final Exam Suggested Solutions

University of Washington Fall 003 Department of Economics Eric Zivot Economics 483 Final Exam Suggested Solutions This is a closed book and closed note exam. However, you are allowed one page of handwritten

University of Washington Fall 003 Department of Economics Eric Zivot Economics 483 Final Exam Suggested Solutions This is a closed book and closed note exam. However, you are allowed one page of handwritten

Pension Funds Performance Evaluation: a Utility Based Approach

Human Capital and Life-cycle Investing Pension Funds Performance Evaluation: a Utility Based Approach Giovanna Nicodano CeRP-Collegio Carlo Alberto and University of Turin Carolina Fugazza Fabio Bagliano

Human Capital and Life-cycle Investing Pension Funds Performance Evaluation: a Utility Based Approach Giovanna Nicodano CeRP-Collegio Carlo Alberto and University of Turin Carolina Fugazza Fabio Bagliano

The CAPM. (Welch, Chapter 10) Ivo Welch. UCLA Anderson School, Corporate Finance, Winter December 16, 2016

Ivo Welch. UCLA Anderson School, Corporate Finance, Winter December 16, 2016") 1/1 The CAPM (Welch, Chapter 10) Ivo Welch UCLA Anderson School, Corporate Finance, Winter 2017 December 16, 2016 Did you bring your calculator? Did you read these notes and the chapter ahead of time?

1/1 The CAPM (Welch, Chapter 10) Ivo Welch UCLA Anderson School, Corporate Finance, Winter 2017 December 16, 2016 Did you bring your calculator? Did you read these notes and the chapter ahead of time?

1 Asset Pricing: Bonds vs Stocks

Asset Pricing: Bonds vs Stocks The historical data on financial asset returns show that one dollar invested in the Dow- Jones yields 6 times more than one dollar invested in U.S. Treasury bonds. The return

Asset Pricing: Bonds vs Stocks The historical data on financial asset returns show that one dollar invested in the Dow- Jones yields 6 times more than one dollar invested in U.S. Treasury bonds. The return

Consumption- Savings, Portfolio Choice, and Asset Pricing

Finance 400 A. Penati - G. Pennacchi Consumption- Savings, Portfolio Choice, and Asset Pricing I. The Consumption - Portfolio Choice Problem We have studied the portfolio choice problem of an individual

Finance 400 A. Penati - G. Pennacchi Consumption- Savings, Portfolio Choice, and Asset Pricing I. The Consumption - Portfolio Choice Problem We have studied the portfolio choice problem of an individual

Valuing Investments A Statistical Perspective. Bob Stine Department of Statistics Wharton, University of Pennsylvania

Valuing Investments A Statistical Perspective Bob Stine, University of Pennsylvania Overview Principles Focus on returns, not cumulative value Remove market performance (CAPM) Watch for unseen volatility

Valuing Investments A Statistical Perspective Bob Stine, University of Pennsylvania Overview Principles Focus on returns, not cumulative value Remove market performance (CAPM) Watch for unseen volatility

Risk and Return and Portfolio Theory

Risk and Return and Portfolio Theory Intro: Last week we learned how to calculate cash flows, now we want to learn how to discount these cash flows. This will take the next several weeks. We know discount

Risk and Return and Portfolio Theory Intro: Last week we learned how to calculate cash flows, now we want to learn how to discount these cash flows. This will take the next several weeks. We know discount

Corporate Finance, Module 21: Option Valuation. Practice Problems. (The attached PDF file has better formatting.) Updated: July 7, 2005

Updated: July 7, 2005") Corporate Finance, Module 21: Option Valuation Practice Problems (The attached PDF file has better formatting.) Updated: July 7, 2005 {This posting has more information than is needed for the corporate

Corporate Finance, Module 21: Option Valuation Practice Problems (The attached PDF file has better formatting.) Updated: July 7, 2005 {This posting has more information than is needed for the corporate

Do you live in a mean-variance world?

Do you live in a mean-variance world? 76 Assume that you had to pick between two investments. They have the same expected return of 15% and the same standard deviation of 25%; however, investment A offers

Do you live in a mean-variance world? 76 Assume that you had to pick between two investments. They have the same expected return of 15% and the same standard deviation of 25%; however, investment A offers

Problem Set 7 Part I Short answer questions on readings. Note, if I don t provide it, state which table, figure, or exhibit backs up your point

Business 35150 John H. Cochrane Problem Set 7 Part I Short answer questions on readings. Note, if I don t provide it, state which table, figure, or exhibit backs up your point 1. Mitchell and Pulvino (a)

Business 35150 John H. Cochrane Problem Set 7 Part I Short answer questions on readings. Note, if I don t provide it, state which table, figure, or exhibit backs up your point 1. Mitchell and Pulvino (a)

INTERTEMPORAL ASSET ALLOCATION: THEORY

INTERTEMPORAL ASSET ALLOCATION: THEORY Multi-Period Model The agent acts as a price-taker in asset markets and then chooses today s consumption and asset shares to maximise lifetime utility. This multi-period

INTERTEMPORAL ASSET ALLOCATION: THEORY Multi-Period Model The agent acts as a price-taker in asset markets and then chooses today s consumption and asset shares to maximise lifetime utility. This multi-period

Overview of Concepts and Notation

Overview of Concepts and Notation (BUSFIN 4221: Investments) - Fall 2016 1 Main Concepts This section provides a list of questions you should be able to answer. The main concepts you need to know are embedded

Overview of Concepts and Notation (BUSFIN 4221: Investments) - Fall 2016 1 Main Concepts This section provides a list of questions you should be able to answer. The main concepts you need to know are embedded

ECMC49S Midterm. Instructor: Travis NG Date: Feb 27, 2007 Duration: From 3:05pm to 5:00pm Total Marks: 100

ECMC49S Midterm Instructor: Travis NG Date: Feb 27, 2007 Duration: From 3:05pm to 5:00pm Total Marks: 100 [1] [25 marks] Decision-making under certainty (a) [10 marks] (i) State the Fisher Separation Theorem

ECMC49S Midterm Instructor: Travis NG Date: Feb 27, 2007 Duration: From 3:05pm to 5:00pm Total Marks: 100 [1] [25 marks] Decision-making under certainty (a) [10 marks] (i) State the Fisher Separation Theorem

Graduate Macro Theory II: Two Period Consumption-Saving Models

Graduate Macro Theory II: Two Period Consumption-Saving Models Eric Sims University of Notre Dame Spring 207 Introduction This note works through some simple two-period consumption-saving problems. In

Graduate Macro Theory II: Two Period Consumption-Saving Models Eric Sims University of Notre Dame Spring 207 Introduction This note works through some simple two-period consumption-saving problems. In

Week 2 Quantitative Analysis of Financial Markets Hypothesis Testing and Confidence Intervals

Week 2 Quantitative Analysis of Financial Markets Hypothesis Testing and Confidence Intervals Christopher Ting http://www.mysmu.edu/faculty/christophert/ Christopher Ting : christopherting@smu.edu.sg :

Week 2 Quantitative Analysis of Financial Markets Hypothesis Testing and Confidence Intervals Christopher Ting http://www.mysmu.edu/faculty/christophert/ Christopher Ting : christopherting@smu.edu.sg :

Problem Set 6 Answers

Business 9 John H. Cochrane Problem Set 6 Answers Here are my results.. You can see that means rise to the northeast as for FF, with the same exception for small growth. In this case means seem to be pretty

Business 9 John H. Cochrane Problem Set 6 Answers Here are my results.. You can see that means rise to the northeast as for FF, with the same exception for small growth. In this case means seem to be pretty

Problem Set 5 Answers. ( ) 2. Yes, like temperature. See the plot of utility in the notes. Marginal utility should be positive.

2. Yes, like temperature. See the plot of utility in the notes. Marginal utility should be positive.") Business John H. Cochrane Problem Set Answers Part I A simple very short readings questions. + = + + + = + + + + = ( ). Yes, like temperature. See the plot of utility in the notes. Marginal utility should

Business John H. Cochrane Problem Set Answers Part I A simple very short readings questions. + = + + + = + + + + = ( ). Yes, like temperature. See the plot of utility in the notes. Marginal utility should

ECO 317 Economics of Uncertainty Fall Term 2009 Tuesday October 6 Portfolio Allocation Mean-Variance Approach

ECO 317 Economics of Uncertainty Fall Term 2009 Tuesday October 6 ortfolio Allocation Mean-Variance Approach Validity of the Mean-Variance Approach Constant absolute risk aversion (CARA): u(w ) = exp(

ECO 317 Economics of Uncertainty Fall Term 2009 Tuesday October 6 ortfolio Allocation Mean-Variance Approach Validity of the Mean-Variance Approach Constant absolute risk aversion (CARA): u(w ) = exp(

Principles of Finance Risk and Return. Instructor: Xiaomeng Lu

Principles of Finance Risk and Return Instructor: Xiaomeng Lu 1 Course Outline Course Introduction Time Value of Money DCF Valuation Security Analysis: Bond, Stock Capital Budgeting (Fundamentals) Portfolio

Principles of Finance Risk and Return Instructor: Xiaomeng Lu 1 Course Outline Course Introduction Time Value of Money DCF Valuation Security Analysis: Bond, Stock Capital Budgeting (Fundamentals) Portfolio

Consumption and Portfolio Decisions When Expected Returns A

Consumption and Portfolio Decisions When Expected Returns Are Time Varying September 10, 2007 Introduction In the recent literature of empirical asset pricing there has been considerable evidence of time-varying

Consumption and Portfolio Decisions When Expected Returns Are Time Varying September 10, 2007 Introduction In the recent literature of empirical asset pricing there has been considerable evidence of time-varying

Math 5760/6890 Introduction to Mathematical Finance

Math 5760/6890 Introduction to Mathematical Finance Instructor: Jingyi Zhu Office: LCB 335 Telephone:581-3236 E-mail: zhu@math.utah.edu Class web page: www.math.utah.edu/~zhu/5760_12f.html What you should

Math 5760/6890 Introduction to Mathematical Finance Instructor: Jingyi Zhu Office: LCB 335 Telephone:581-3236 E-mail: zhu@math.utah.edu Class web page: www.math.utah.edu/~zhu/5760_12f.html What you should

Risk and Return. Nicole Höhling, Introduction. Definitions. Types of risk and beta

Risk and Return Nicole Höhling, 2009-09-07 Introduction Every decision regarding investments is based on the relationship between risk and return. Generally the return on an investment should be as high

Risk and Return Nicole Höhling, 2009-09-07 Introduction Every decision regarding investments is based on the relationship between risk and return. Generally the return on an investment should be as high

CHAPTER 17 OPTIONS AND CORPORATE FINANCE

CHAPTER 17 OPTIONS AND CORPORATE FINANCE Answers to Concept Questions 1. A call option confers the right, without the obligation, to buy an asset at a given price on or before a given date. A put option

CHAPTER 17 OPTIONS AND CORPORATE FINANCE Answers to Concept Questions 1. A call option confers the right, without the obligation, to buy an asset at a given price on or before a given date. A put option

PORTFOLIO THEORY. Master in Finance INVESTMENTS. Szabolcs Sebestyén

PORTFOLIO THEORY Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master in Finance INVESTMENTS Sebestyén (ISCTE-IUL) Portfolio Theory Investments 1 / 60 Outline 1 Modern Portfolio Theory Introduction Mean-Variance

PORTFOLIO THEORY Szabolcs Sebestyén szabolcs.sebestyen@iscte.pt Master in Finance INVESTMENTS Sebestyén (ISCTE-IUL) Portfolio Theory Investments 1 / 60 Outline 1 Modern Portfolio Theory Introduction Mean-Variance

Stock Market Fluctuations

Stock Market Fluctuations Trevor Gallen Spring, 2016 1 / 54 Introduction Households: Want to be able to save Want higher interest rates (risk held constant) Want their funds to be liquid Firms Want to

Stock Market Fluctuations Trevor Gallen Spring, 2016 1 / 54 Introduction Households: Want to be able to save Want higher interest rates (risk held constant) Want their funds to be liquid Firms Want to

Expected Return Methodologies in Morningstar Direct Asset Allocation

Expected Return Methodologies in Morningstar Direct Asset Allocation I. Introduction to expected return II. The short version III. Detailed methodologies 1. Building Blocks methodology i. Methodology ii.

Expected Return Methodologies in Morningstar Direct Asset Allocation I. Introduction to expected return II. The short version III. Detailed methodologies 1. Building Blocks methodology i. Methodology ii.

Optimization 101. Dan dibartolomeo Webinar (from Boston) October 22, 2013

October 22, 2013") Optimization 101 Dan dibartolomeo Webinar (from Boston) October 22, 2013 Outline of Today s Presentation The Mean-Variance Objective Function Optimization Methods, Strengths and Weaknesses Estimation Error

Optimization 101 Dan dibartolomeo Webinar (from Boston) October 22, 2013 Outline of Today s Presentation The Mean-Variance Objective Function Optimization Methods, Strengths and Weaknesses Estimation Error

Portfolio Management

MCF 17 Advanced Courses Portfolio Management Final Exam Time Allowed: 60 minutes Family Name (Surname) First Name Student Number (Matr.) Please answer all questions by choosing the most appropriate alternative

MCF 17 Advanced Courses Portfolio Management Final Exam Time Allowed: 60 minutes Family Name (Surname) First Name Student Number (Matr.) Please answer all questions by choosing the most appropriate alternative

P s =(0,W 0 R) safe; P r =(W 0 σ,w 0 µ) risky; Beyond P r possible if leveraged borrowing OK Objective function Mean a (Std.Dev.

safe; P r =(W 0 σ,w 0 µ) risky; Beyond P r possible if leveraged borrowing OK Objective function Mean a (Std.Dev.") ECO 305 FALL 2003 December 2 ORTFOLIO CHOICE One Riskless, One Risky Asset Safe asset: gross return rate R (1 plus interest rate) Risky asset: random gross return rate r Mean µ = E[r] >R,Varianceσ 2 =

ECO 305 FALL 2003 December 2 ORTFOLIO CHOICE One Riskless, One Risky Asset Safe asset: gross return rate R (1 plus interest rate) Risky asset: random gross return rate r Mean µ = E[r] >R,Varianceσ 2 =

10 Things We Don t Understand About Finance. 3: The CAPM Is Missing Something!

10 Things We Don t Understand About Finance 3: The CAPM Is Missing Something! Models Need two features Simple enough to understand Complex enough to be generally applicable Does the CAPM satisfy these?

10 Things We Don t Understand About Finance 3: The CAPM Is Missing Something! Models Need two features Simple enough to understand Complex enough to be generally applicable Does the CAPM satisfy these?

Exploiting the Inefficiencies of Leveraged ETFs

Exploiting the Inefficiencies of Leveraged ETFs [Editor s Note: Here at WCI we try to keep things as simple as possible, most of the time. Not today though. Today we re going to be discussing leveraged

Exploiting the Inefficiencies of Leveraged ETFs [Editor s Note: Here at WCI we try to keep things as simple as possible, most of the time. Not today though. Today we re going to be discussing leveraged

Mathematics in Finance

Mathematics in Finance Steven E. Shreve Department of Mathematical Sciences Carnegie Mellon University Pittsburgh, PA 15213 USA shreve@andrew.cmu.edu A Talk in the Series Probability in Science and Industry

Mathematics in Finance Steven E. Shreve Department of Mathematical Sciences Carnegie Mellon University Pittsburgh, PA 15213 USA shreve@andrew.cmu.edu A Talk in the Series Probability in Science and Industry

Extend the ideas of Kan and Zhou paper on Optimal Portfolio Construction under parameter uncertainty

Extend the ideas of Kan and Zhou paper on Optimal Portfolio Construction under parameter uncertainty George Photiou Lincoln College University of Oxford A dissertation submitted in partial fulfilment for

Extend the ideas of Kan and Zhou paper on Optimal Portfolio Construction under parameter uncertainty George Photiou Lincoln College University of Oxford A dissertation submitted in partial fulfilment for

Discount Rates. John H. Cochrane. January 8, University of Chicago Booth School of Business

Discount Rates John H. Cochrane University of Chicago Booth School of Business January 8, 2011 Discount rates 1. Facts: How risk discount rates vary over time and across assets. 2. Theory: Why discount

Discount Rates John H. Cochrane University of Chicago Booth School of Business January 8, 2011 Discount rates 1. Facts: How risk discount rates vary over time and across assets. 2. Theory: Why discount

Birkbeck MSc/Phd Economics. Advanced Macroeconomics, Spring Lecture 2: The Consumption CAPM and the Equity Premium Puzzle

Birkbeck MSc/Phd Economics Advanced Macroeconomics, Spring 2006 Lecture 2: The Consumption CAPM and the Equity Premium Puzzle 1 Overview This lecture derives the consumption-based capital asset pricing

Birkbeck MSc/Phd Economics Advanced Macroeconomics, Spring 2006 Lecture 2: The Consumption CAPM and the Equity Premium Puzzle 1 Overview This lecture derives the consumption-based capital asset pricing

Monetary Economics Risk and Return, Part 2. Gerald P. Dwyer Fall 2015

Monetary Economics Risk and Return, Part 2 Gerald P. Dwyer Fall 2015 Reading Malkiel, Part 2, Part 3 Malkiel, Part 3 Outline Returns and risk Overall market risk reduced over longer periods Individual

Monetary Economics Risk and Return, Part 2 Gerald P. Dwyer Fall 2015 Reading Malkiel, Part 2, Part 3 Malkiel, Part 3 Outline Returns and risk Overall market risk reduced over longer periods Individual

Module 3: Factor Models

Module 3: Factor Models (BUSFIN 4221 - Investments) Andrei S. Gonçalves 1 1 Finance Department The Ohio State University Fall 2016 1 Module 1 - The Demand for Capital 2 Module 1 - The Supply of Capital

Module 3: Factor Models (BUSFIN 4221 - Investments) Andrei S. Gonçalves 1 1 Finance Department The Ohio State University Fall 2016 1 Module 1 - The Demand for Capital 2 Module 1 - The Supply of Capital

Introduction to Computational Finance and Financial Econometrics Introduction to Portfolio Theory

You can t see this text! Introduction to Computational Finance and Financial Econometrics Introduction to Portfolio Theory Eric Zivot Spring 2015 Eric Zivot (Copyright 2015) Introduction to Portfolio Theory

You can t see this text! Introduction to Computational Finance and Financial Econometrics Introduction to Portfolio Theory Eric Zivot Spring 2015 Eric Zivot (Copyright 2015) Introduction to Portfolio Theory

Sample Midterm Questions Foundations of Financial Markets Prof. Lasse H. Pedersen

Sample Midterm Questions Foundations of Financial Markets Prof. Lasse H. Pedersen 1. Security A has a higher equilibrium price volatility than security B. Assuming all else is equal, the equilibrium bid-ask

Sample Midterm Questions Foundations of Financial Markets Prof. Lasse H. Pedersen 1. Security A has a higher equilibrium price volatility than security B. Assuming all else is equal, the equilibrium bid-ask

Uncertain Covariance Models

Uncertain Covariance Models RISK FORECASTS THAT KNOW HOW ACCURATE THEY ARE AND WHERE AU G 1 8, 2 0 1 5 Q WA FA F E W B O S TO N A N I S H R. S H A H, C FA A N I S H R S @ I N V E S T M E N TG R A D E M

Uncertain Covariance Models RISK FORECASTS THAT KNOW HOW ACCURATE THEY ARE AND WHERE AU G 1 8, 2 0 1 5 Q WA FA F E W B O S TO N A N I S H R. S H A H, C FA A N I S H R S @ I N V E S T M E N TG R A D E M

Problem Set 3. Thomas Philippon. April 19, Human Wealth, Financial Wealth and Consumption

Problem Set 3 Thomas Philippon April 19, 2002 1 Human Wealth, Financial Wealth and Consumption The goal of the question is to derive the formulas on p13 of Topic 2. This is a partial equilibrium analysis

Problem Set 3 Thomas Philippon April 19, 2002 1 Human Wealth, Financial Wealth and Consumption The goal of the question is to derive the formulas on p13 of Topic 2. This is a partial equilibrium analysis

Solutions to the problems in the supplement are found at the end of the supplement

www.liontutors.com FIN 301 Exam 2 Chapter 12 Supplement Solutions to the problems in the supplement are found at the end of the supplement Chapter 12 The Capital Asset Pricing Model Risk and Return Higher

www.liontutors.com FIN 301 Exam 2 Chapter 12 Supplement Solutions to the problems in the supplement are found at the end of the supplement Chapter 12 The Capital Asset Pricing Model Risk and Return Higher

1 Funds and Performance Evaluation

Histogram Cumulative Return 1 Funds and Performance Evaluation 1.1 Carhart 1 Return history.8.6.4.2.2.4.6.5 1 1.5 2 2.5 3 3.5 4 4.5 5 Years 25 Distribution of survivor's 5 year returns True Sample 2 15

Histogram Cumulative Return 1 Funds and Performance Evaluation 1.1 Carhart 1 Return history.8.6.4.2.2.4.6.5 1 1.5 2 2.5 3 3.5 4 4.5 5 Years 25 Distribution of survivor's 5 year returns True Sample 2 15

ECMC49F Midterm. Instructor: Travis NG Date: Oct 26, 2005 Duration: 1 hour 50 mins Total Marks: 100. [1] [25 marks] Decision-making under certainty

![ECMC49F Midterm. Instructor: Travis NG Date: Oct 26, 2005 Duration: 1 hour 50 mins Total Marks: 100. [1] [25 marks] Decision-making under certainty](/thumbs/83/88403560.jpg "ECMC49F Midterm. Instructor: Travis NG Date: Oct 26, 2005 Duration: 1 hour 50 mins Total Marks: 100. [1] [25 marks] Decision-making under certainty") ECMC49F Midterm Instructor: Travis NG Date: Oct 26, 2005 Duration: 1 hour 50 mins Total Marks: 100 [1] [25 marks] Decision-making under certainty (a) [5 marks] Graphically demonstrate the Fisher Separation

ECMC49F Midterm Instructor: Travis NG Date: Oct 26, 2005 Duration: 1 hour 50 mins Total Marks: 100 [1] [25 marks] Decision-making under certainty (a) [5 marks] Graphically demonstrate the Fisher Separation

Archana Khetan 05/09/ MAFA (CA Final) - Portfolio Management

- Portfolio Management") Archana Khetan 05/09/2010 +91-9930812722 Archana090@hotmail.com MAFA (CA Final) - Portfolio Management 1 Portfolio Management Portfolio is a collection of assets. By investing in a portfolio or combination

Archana Khetan 05/09/2010 +91-9930812722 Archana090@hotmail.com MAFA (CA Final) - Portfolio Management 1 Portfolio Management Portfolio is a collection of assets. By investing in a portfolio or combination

Quantitative Risk Management

Quantitative Risk Management Asset Allocation and Risk Management Martin B. Haugh Department of Industrial Engineering and Operations Research Columbia University Outline Review of Mean-Variance Analysis

Quantitative Risk Management Asset Allocation and Risk Management Martin B. Haugh Department of Industrial Engineering and Operations Research Columbia University Outline Review of Mean-Variance Analysis

Cost of Capital (represents risk)

") Cost of Capital (represents risk) Cost of Equity Capital - From the shareholders perspective, the expected return is the cost of equity capital E(R i ) is the return needed to make the investment = the

Cost of Capital (represents risk) Cost of Equity Capital - From the shareholders perspective, the expected return is the cost of equity capital E(R i ) is the return needed to make the investment = the

Analyst Disagreement and Aggregate Volatility Risk

Analyst Disagreement and Aggregate Volatility Risk Alexander Barinov Terry College of Business University of Georgia April 15, 2010 Alexander Barinov (Terry College) Disagreement and Volatility Risk April

Analyst Disagreement and Aggregate Volatility Risk Alexander Barinov Terry College of Business University of Georgia April 15, 2010 Alexander Barinov (Terry College) Disagreement and Volatility Risk April

The Diversification of Employee Stock Options

The Diversification of Employee Stock Options David M. Stein Managing Director and Chief Investment Officer Parametric Portfolio Associates Seattle Andrew F. Siegel Professor of Finance and Management

The Diversification of Employee Stock Options David M. Stein Managing Director and Chief Investment Officer Parametric Portfolio Associates Seattle Andrew F. Siegel Professor of Finance and Management

APPENDIX TO LECTURE NOTES ON ASSET PRICING AND PORTFOLIO MANAGEMENT. Professor B. Espen Eckbo

APPENDIX TO LECTURE NOTES ON ASSET PRICING AND PORTFOLIO MANAGEMENT 2011 Professor B. Espen Eckbo 1. Portfolio analysis in Excel spreadsheet 2. Formula sheet 3. List of Additional Academic Articles 2011

APPENDIX TO LECTURE NOTES ON ASSET PRICING AND PORTFOLIO MANAGEMENT 2011 Professor B. Espen Eckbo 1. Portfolio analysis in Excel spreadsheet 2. Formula sheet 3. List of Additional Academic Articles 2011

2013 Final Exam. Directions

Business 35150 John H. Cochrane 2013 Final Exam Name (Print clearly): Section: Mailfolder location: Directions DONOTSTARTUNTILWETELLYOUTODOSO.Read these directions in the meantime. Please do not tear your

Business 35150 John H. Cochrane 2013 Final Exam Name (Print clearly): Section: Mailfolder location: Directions DONOTSTARTUNTILWETELLYOUTODOSO.Read these directions in the meantime. Please do not tear your

ECON FINANCIAL ECONOMICS

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Fall 2017 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Fall 2017 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

Portfolio Risk Management and Linear Factor Models

Chapter 9 Portfolio Risk Management and Linear Factor Models 9.1 Portfolio Risk Measures There are many quantities introduced over the years to measure the level of risk that a portfolio carries, and each

Chapter 9 Portfolio Risk Management and Linear Factor Models 9.1 Portfolio Risk Measures There are many quantities introduced over the years to measure the level of risk that a portfolio carries, and each

Review for Quiz #2 Revised: October 31, 2015

ECON-UB 233 Dave Backus @ NYU Review for Quiz #2 Revised: October 31, 2015 I ll focus again on the big picture to give you a sense of what we ve done and how it fits together. For each topic/result/concept,

ECON-UB 233 Dave Backus @ NYU Review for Quiz #2 Revised: October 31, 2015 I ll focus again on the big picture to give you a sense of what we ve done and how it fits together. For each topic/result/concept,

ECON FINANCIAL ECONOMICS

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Spring 2018 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Spring 2018 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

FNCE 4030 Fall 2012 Roberto Caccia, Ph.D. Midterm_2a (2-Nov-2012) Your name:

Your name:") Answer the questions in the space below. Written answers require no more than few compact sentences to show you understood and master the concept. Show your work to receive partial credit. Points are as

Answer the questions in the space below. Written answers require no more than few compact sentences to show you understood and master the concept. Show your work to receive partial credit. Points are as

Economics of Behavioral Finance. Lecture 3

Economics of Behavioral Finance Lecture 3 Security Market Line CAPM predicts a linear relationship between a stock s Beta and its excess return. E[r i ] r f = β i E r m r f Practically, testing CAPM empirically

Economics of Behavioral Finance Lecture 3 Security Market Line CAPM predicts a linear relationship between a stock s Beta and its excess return. E[r i ] r f = β i E r m r f Practically, testing CAPM empirically

For each of the questions 1-6, check one of the response alternatives A, B, C, D, E with a cross in the table below:

November 2016 Page 1 of (6) Multiple Choice Questions (3 points per question) For each of the questions 1-6, check one of the response alternatives A, B, C, D, E with a cross in the table below: Question

November 2016 Page 1 of (6) Multiple Choice Questions (3 points per question) For each of the questions 1-6, check one of the response alternatives A, B, C, D, E with a cross in the table below: Question

HOW TO PROTECT YOURSELF FROM RISKY FOREX SYSTEMS

BestForexBrokers.com Identifying Flaws in Profitable Forex Systems HOW TO PROTECT YOURSELF FROM RISKY FOREX SYSTEMS JULY 2017 Disclaimer: BestForexBrokers.com and this report are not associated with myfxbook.com

BestForexBrokers.com Identifying Flaws in Profitable Forex Systems HOW TO PROTECT YOURSELF FROM RISKY FOREX SYSTEMS JULY 2017 Disclaimer: BestForexBrokers.com and this report are not associated with myfxbook.com

Pension Funds Performance Evaluation: a Utility Based Approach

Pension Funds Performance Evaluation: a Utility Based Approach Carolina Fugazza Fabio Bagliano Giovanna Nicodano CeRP-Collegio Carlo Alberto and University of of Turin CeRP 10 Anniversary Conference Motivation

Pension Funds Performance Evaluation: a Utility Based Approach Carolina Fugazza Fabio Bagliano Giovanna Nicodano CeRP-Collegio Carlo Alberto and University of of Turin CeRP 10 Anniversary Conference Motivation

Foundations of Finance

Lecture 5: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Individual Assets in a CAPM World. VI. Intuition for the SML (E[R p ] depending

Lecture 5: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Individual Assets in a CAPM World. VI. Intuition for the SML (E[R p ] depending

THINK DIFFERENT. Joe Huber WHAT IS RISK??

THINK DIFFERENT By Joe Huber WHAT IS RISK?? Last month my wife asked me how the returns in our house fund were doing. Not too bad, I replied. She raised a finger, You better not lose any of our money.

THINK DIFFERENT By Joe Huber WHAT IS RISK?? Last month my wife asked me how the returns in our house fund were doing. Not too bad, I replied. She raised a finger, You better not lose any of our money.

Recitation VI. Jiro E. Kondo

Recitation VI Jiro E. Kondo Summer 2003 Today s Recitation: Capital Structure. I. MM Thm: Capital Structure Irrelevance. II. Taxes and Other Deviations from MM. 1 I. MM Theorem. A company is considering

Recitation VI Jiro E. Kondo Summer 2003 Today s Recitation: Capital Structure. I. MM Thm: Capital Structure Irrelevance. II. Taxes and Other Deviations from MM. 1 I. MM Theorem. A company is considering

Advanced Macroeconomics 5. Rational Expectations and Asset Prices

Advanced Macroeconomics 5. Rational Expectations and Asset Prices Karl Whelan School of Economics, UCD Spring 2015 Karl Whelan (UCD) Asset Prices Spring 2015 1 / 43 A New Topic We are now going to switch

Advanced Macroeconomics 5. Rational Expectations and Asset Prices Karl Whelan School of Economics, UCD Spring 2015 Karl Whelan (UCD) Asset Prices Spring 2015 1 / 43 A New Topic We are now going to switch

Appendix to: AMoreElaborateModel

Appendix to: Why Do Demand Curves for Stocks Slope Down? AMoreElaborateModel Antti Petajisto Yale School of Management February 2004 1 A More Elaborate Model 1.1 Motivation Our earlier model provides a

Appendix to: Why Do Demand Curves for Stocks Slope Down? AMoreElaborateModel Antti Petajisto Yale School of Management February 2004 1 A More Elaborate Model 1.1 Motivation Our earlier model provides a

Arbitrage Pricing Theory and Multifactor Models of Risk and Return

Arbitrage Pricing Theory and Multifactor Models of Risk and Return Recap : CAPM Is a form of single factor model (one market risk premium) Based on a set of assumptions. Many of which are unrealistic One

Arbitrage Pricing Theory and Multifactor Models of Risk and Return Recap : CAPM Is a form of single factor model (one market risk premium) Based on a set of assumptions. Many of which are unrealistic One

Illiquidity, Credit risk and Merton s model

Illiquidity, Credit risk and Merton s model (joint work with J. Dong and L. Korobenko) A. Deniz Sezer University of Calgary April 28, 2016 Merton s model of corporate debt A corporate bond is a contingent

Illiquidity, Credit risk and Merton s model (joint work with J. Dong and L. Korobenko) A. Deniz Sezer University of Calgary April 28, 2016 Merton s model of corporate debt A corporate bond is a contingent

Optimal Portfolio Inputs: Various Methods

Optimal Portfolio Inputs: Various Methods Prepared by Kevin Pei for The Fund @ Sprott Abstract: In this document, I will model and back test our portfolio with various proposed models. It goes without

Optimal Portfolio Inputs: Various Methods Prepared by Kevin Pei for The Fund @ Sprott Abstract: In this document, I will model and back test our portfolio with various proposed models. It goes without

Econ 422 Eric Zivot Summer 2004 Final Exam Solutions

Econ 422 Eric Zivot Summer 2004 Final Exam Solutions This is a closed book exam. However, you are allowed one page of notes (double-sided). Answer all questions. For the numerical problems, if you make

Econ 422 Eric Zivot Summer 2004 Final Exam Solutions This is a closed book exam. However, you are allowed one page of notes (double-sided). Answer all questions. For the numerical problems, if you make

Corporate Finance, Module 3: Common Stock Valuation. Illustrative Test Questions and Practice Problems. (The attached PDF file has better formatting.

Corporate Finance, Module 3: Common Stock Valuation Illustrative Test Questions and Practice Problems (The attached PDF file has better formatting.) These problems combine common stock valuation (module

Corporate Finance, Module 3: Common Stock Valuation Illustrative Test Questions and Practice Problems (The attached PDF file has better formatting.) These problems combine common stock valuation (module

How Risky is the Stock Market

How Risky is the Stock Market An Analysis of Short-term versus Long-term investing Elena Agachi and Lammertjan Dam CIBIF-001 18 januari 2018 1871 1877 1883 1889 1895 1901 1907 1913 1919 1925 1937 1943

How Risky is the Stock Market An Analysis of Short-term versus Long-term investing Elena Agachi and Lammertjan Dam CIBIF-001 18 januari 2018 1871 1877 1883 1889 1895 1901 1907 1913 1919 1925 1937 1943

Applying the Basic Model

2 Applying the Basic Model 2.1 Assumptions and Applicability Writing p = E(mx), wedonot assume 1. Markets are complete, or there is a representative investor 2. Asset returns or payoffs are normally distributed

2 Applying the Basic Model 2.1 Assumptions and Applicability Writing p = E(mx), wedonot assume 1. Markets are complete, or there is a representative investor 2. Asset returns or payoffs are normally distributed

PowerPoint. to accompany. Chapter 11. Systematic Risk and the Equity Risk Premium

PowerPoint to accompany Chapter 11 Systematic Risk and the Equity Risk Premium 11.1 The Expected Return of a Portfolio While for large portfolios investors should expect to experience higher returns for

PowerPoint to accompany Chapter 11 Systematic Risk and the Equity Risk Premium 11.1 The Expected Return of a Portfolio While for large portfolios investors should expect to experience higher returns for