FIN 6160 Investment Theory. Lecture 7-10

|

|

|

- Meghan Bates

- 5 years ago

- Views:

Transcription

1 FIN 6160 Investment Theory Lecture 7-10

2 Optimal Asset Allocation Minimum Variance Portfolio is the portfolio with lowest possible variance. To find the optimal asset allocation for the efficient frontier with the starting point (min variance portfolio) we can set first differentiation of the variance to zero and solve for w 1. Variance of Portfolio, w w 2w w We know, w w 1; w 1 w d dw p d [ ] [ w (1 w ) 2 w(1 w ) ] p dw1 d d 2w 2(1 w )( 1) 2 [ w (1 w ) (1 w ) ( w )] dw1 dw1 2 2w 2(1 w ) 2 [ w ( 1) (1 w )] w 2 2w 2 [1 2w ] w 2 2w 2 4w

3 Optimal Asset Allocation 2 For min variance portfolio, [ p] 0 dw1 i. e.2w 2 2w 2 4w or, w (2 2 4 ) 2 2 or, w d 3

4 Risk Aversion and its Implications for Portfolio Selection A risk-averse investor is simply one that dislikes risk (i.e. prefers less risk to more risk). Given two investment that have equal expected returns, a risk-averse investor will choose the one with less risk. A risk-seeking (risk-loving) investor actually prefers more risk to less and, given equal expected returns, will choose the more risky investment. A risk-neutral investor has no preference regarding risk and would be indifferent between two such investments. Consider this gamble: A coin will be flipped; if it comes up head, you receive $100; if it comes up tails, you receive nothing. The expected payoff is 0.5($100)+0.5($0)=$50. A risk averse investor would choose a payment of $50 (a certain outcome) over the gamble. A risk-seeking investor would prefer the gamble to a certain payment of $50. A risk-neutral investor would be indifferent between the gamble and a certain payment of $50. If expected returns are identical, a risk-averse investor will always choose the investment with the least risk. However, an investor may select a very risky portfolio despite being risk-averse; a risk-averse investor will hold very risky assets if he feels that the extra return he expects to earn is adequate compensation for the additional risk. 4

5 Risk Aversion and its Implications for Portfolio Selection An investor s utility function represents the investor s preferences in terms of risk and return (i.e. his degree of risk aversion). Investors maximize their utility function for various investments. 2 U E( R) a R The parameter a above measures the degree of risk aversion. The larger a, the more risk averse the investor is. An indifference curve plots combinations of risk and expected return among which an investor is indifferent. In constructing indifference curves for portfolios based on only their expected return and standard deviation of returns, we are assuming that these are the only portfolio characteristics that investors care about. The investor s expected utility is the same for all points along a single indifference curve. Indifference curves slope upward for risk-averse investors because they will only take on more risk if they are compensated with greater expected returns. An investor who is relatively more risk-averse requires a relatively greater increase in expected return to compensate for a given increase in risk. In other words, a more risk averse investor will have steeper indifference curves. 5

6 Utility Function to Measure the degree of Risk

7 Diversification with Risk-less Assets We have learned to construct portfolios with risky assets. An investor can alternatively combine a risky investment with an investment in a riskless or risk-free asset security such as Treasury bills. Merville Company Risk-free Asset Expected Return 14% 10% Standard Dev Suppose an investor chooses to invest $350 on Merville and $650 on risk-free asset. Expected Return, E(r ) r ) r ) % p w1 1 w2 2 x x Risk-free asset has no variance, thus both covariance between the assets and variance of risk free asset is zero. Variance of Portfolio, w w 2w w Here, i.e. w p 1 1 or, w 0.35x p p

8 Diversification with Risk-less Assets 8

9 Diversification with Risk-less Assets Combining a risky portfolio with a risk-free asset is the process that supports the two fund separation theorem, which states that all investors optimum portfolios will be made up of some combination of an optimal portfolio of risky assets and the risk free asset. The line representing these possible combinations of risk-free assets and the optimal risky asset portfolio is referred to as the capital allocation line (CAL). 9

10 Investors who are less risk-averse will select portfolios that are more risky. We know that the less an investor s risk aversion, the flatter his indifference curves. As in the figure, the flatter indifference curve for investor B (I B ) results in an optimal (tangency) portfolio that lies to the right of the one that results from a steeper indifference curve, such as that for investor A (I A ). An investor who is less risk averse should optimally choose a portfolio with more invested in the risky asset portfolio and less invested in the risk-free asset. 10

11 Diversification with Risk-less Assets 11

12 A simplifying assumption underlying modern portfolio theory and the capital asset pricing model is that investors have homogeneous expectations (i.e. they all have the same estimates of risk, return, and correlations with other risky assets for all risky assets). Under this assumption, all investors face the same efficient frontier of risky portfolios and will all have the same optimal risky portfolio and the optimal CAL (capital market line-cml) for any investor is the one that is just tangent to the efficient frontier. The tangent point of the CML and efficient frontier is market portfolio that gives maximum return for a given risk. CML states that an optimal investment strategy is to split capital between risk-free asset and the market portfolio. Market portfolio is a market value weighted portfolio of all existing securities. In the mean-variance world, a risk averse investor has to decide what portion of his wealth he should invest in an optimally formed (efficient) portfolio of risky assets (e.g. mutual fund) and what portion in the risk free asset. 12

13 13

14 Efficient Frontier vs. CML CML E(R p ) E.F M R f STDV(P)

15 Along CML, expected portfolio return is a linear function of portfolio risk. The equation of this line is as follows: E(R m)-r f Expected Return, E(r p) R f [ ] p The difference between the expected return on the market and the risk free rate is termed the market risk premium. We can rewrite the CML equation as: Expected Return, E(r p ) Rf [E(R m)- Rf ] An investor can expect to get one unit of market risk premium above the risk free rate for every unit of market risk that the investor is willing to accept. m p m 15

16 Systematic and Non-systematic Risk When an investor diversifies across assets that are not perfectly correlated, the portfolio s risk is less than the weighted average of the risks of the individual securities in the portfolio. The risk that is eliminated by diversification is called unsystematic risk ( also called unique, diversifiable, or firm specific risk). Since the market portfolio contains all the risky assets, it must be well a diversified portfolio. The risk that remains and can not be diversified away, is called the systematic risk ( also called nondiversifiable or market risk). The concept of systematic risk applies to individual securities as well as to portfolios. Some securities returns are highly correlated with overall market returns. Examples of firms that are highly correlated with market returns are luxury goods manufactures such as Ferrari Automobiles and Harley Davidson Motorcycles. These firms have high systematic risk (i.e they are very responsive to market). Other firms, such as utility companies, respond very little to changes in the systematic risk factors. These firms have very little systematic risk. Hence total risk (measured by standard deviation) can be broken down into its component parts: unsystematic risk and systematic risk. 16

17 Systematic and Non-systematic Risk 17

18 Multi-factor model vs Single Factor or Single Index Model Multi-factor models to predict expected returns commonly use macro economic factors such as GDP growth, inflation, consumer confidence, along with fundamental factors such as earnings, earnings growth, firm size and research expenditures. The general form of a multi factor model with k factors is as follows: Expected Return, E(r ) R E(factor ) E(factor )... E(factor ) i f k k Single index model in contrast is a single factor or market model. The only factor is the expected excess return on the market portfolio (market index). The form of the single index model is as follows: Expected Return, E(r ) R E(r ) R ] or,e(r ) R E(r ) R ] i f i m f i f i m f In this case, the beta for asset i is a measure of how sensitive the excess return on asset i is to the excess return on the overall market portfolio. 18

19 Calculate and Interpret Beta The sensitivity of an asset s return to the return on the market index in the context of the market model is referred to as its beta. Beta measures the responsiveness of a security to movements in the market portfolio. The contribution of a security to the variance of a diversified portfolio is best measured by beta. Therefore, beta is the proper measure of the risk of an individual security for a diversified investor. Beta measures the systematic risk of a security. Thus, diversified investors pay attention to the systematic risk of each security. However, they ignore the unsystematic risk of individual securities, since unsystematic risks are diversified away in a large portfolio Cov( i, m) ( im, ) i ( im, ) i m i 2 2 m m m One useful property is that the average beta across all securities, when weighted by the proportion of each security s market value to that of the market portfolio, is 1. That is, the beta of the market portfolio is 1. For aggressive securities beta>1; for defensive securities beta<1 and for neutral securities beta=1 19

20 20

21 Relationship between Risk and Expected Return Capital Asset Pricing Model (CAPM) implies that the expected return on a security is linearly related to its beta. Because the average return on the market has been higher than the average risk free rate over long periods of time, market premium is presumably positive. Thus the formula implies that the expected return on a security is positively related to its beta. Capital Asset Pricing Model (CAPM): R R x [ R R ] i f i m f Expected Risk- Beta of Market Return on = free + the x Risk a Security rate security Premium If β=0, Ri R f that is, the expected return on the security is equal to the risk free rate. Because a security with zero beta has no relevant risk, its expected return should equal the risk-free rate. If β=1, Ri Rm that is, the expected return on the security is equal to the expected return on the market. This makes sense because the beta of the market portfolio is also 1. 21

22 Relationship between Risk and Expected Return Security Market Line (SML) is the graphical depiction of the capital asset pricing model (CAPM) The CML uses total risk σ on the X-axis. Hence only efficient portfolios will plot on the CML. On the other hand, the SML uses beta (systematic risk) on the X-axis. So in a CAPM world, all properly priced securities and portfolios of securities will plot on the SML. 22

23 CAPM Example: The expected return on the market is 15%, the risk free rate is 8%, and the beta for the stock A is 1.2. Compute the rate of return that would be expected (required) on this stock. Answer: E( R ) ( ) %; Here, 1; E( R ) E( R ) A A A M Example: The expected return on the market is 15%, the risk free rate is 8%, and the beta for the stock B is 0.8. Compute the rate of return that would be expected (required) on this stock. Answer: E( R ) ( ) %; Here, 1; E( R ) E( R ) B B B M Example: Acme, Inc., has a capital structure that is 40% debt and 60% equity. The expected return on the market is 12%, and the risk free rate is 4%. What discount rate should an analyst use to calculate the NPV of a project with an equity beta of 0.9 if the firm s after tax cost of debt is 5% Answer: The required return on equity for this project is, ( )=0.112=11.2% The appropriate discount rate is a weighted average of the costs of debt and equity for this project, 0.40x x0.112=0.0872=8.72% 23

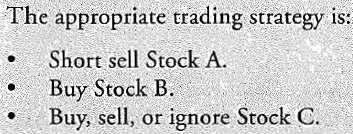

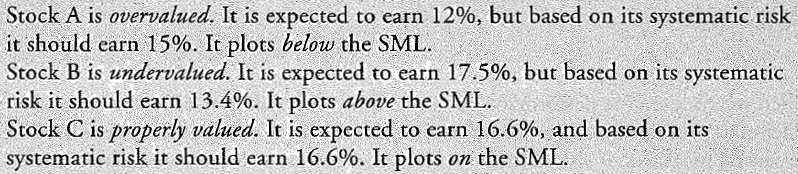

24 Suppose risk free rate and market return are 7% and 15% respectively. Compute the expected and required return on each stock, determine whether each stock is undervalued, overvalued or properly valued an outline an appropriate trading strategy.

25

26 Assumptions of CAPM Investors make their investment decisions according to meanvariance rule Investors can borrow or lend at the risk-free rate. No transactions cost for diversification Investors are price takers and have homogeneous expectations or beliefs regarding future expected returns, variances and covariance. All assets are marketable and perfectly divisible. There are no market imperfections such as taxes, regulations, or restrictions on short selling. 26

27 Portfolio Performance Evaluation When we evaluate the performance of a portfolio with risk that differs from that of a benchmark, we need to adjust the portfolio returns for the risk of the portfolio. There are several measures of risk-adjusted returns that are used to evaluate relative portfolio performance. Sharpe Ratio: The Sharpe Ratio (SR) of a portfolio is the ratio of the risk-premium to the portfolio`s standard deviation, and higher Sharpe ratios indicate better riskadjusted portfolio performance. It tells us the extra return we would get from a portfolio to extra unit of STDV. Sharpe ratio uses total risk, rather than systematic risk, it accounts for any unsystematic that the portfolio manager has taken. The value of the Sharpe ratio is only useful for comparison with the Sharpe ratio of another portfolio. Sharpe ratio is a slope measure and are same for all portfolios along the CML Sharpe Ratio E( R ) r p p f 27

28 Portfolio Performance Evaluation 28

29 Example 1-Sharpe ratio Stock A Stock B Risk Free rate Average ret: 7% 15% 2% StDev ret. 8% 1.96% Covariance ret Percentage of stock A =30% stock B = 70% Exp. Port. Ret. = 12.60% Port. stadev = 10.32% Excess ret. = 10.60% --- Sharpe ratio =

30 Example 2-Sharpe ratio Stock A Stock B Risk Free rate Average ret. 7% 15% 2% StDev ret. 8%% 1.96% Covariance ret Percentage of stock A =40% stock B = 60% Exp. Port. Ret. = 11.80% Port. stadev = 9.28% Excess ret. = 9.80% --- Sharpe ratio = Portfolio 2 is the best combination of risky assets available

31 Portfolio Performance Evaluation M-squared: The M-squared measure produces the same portfolio rankings as the Sharpe ratio but is stated in percentage terms. It is calculated as: M M squared ( Rp R f ) ( RM R f ) Treynor Measure and Jensen s Alpha: Treynor Measure and Jensen s Alpha is based on systematic risk (beta) rather than total risk. Treynor Measure ( R R ) p Jensen's Alpha, ( R R ) ( R R ) p f p p p f p M f Under the assumptions of the CAPM we expect Jensen s Alpha α=0. We get an estimate of this alpha from standard regression analysis but we need to take into account the statistical significance of the alpha. A positive and statistically significant Jensen s alpha implies outperformance. Jensen s alpha is a measure of managerial ability because it shows whether the manager had added any value over and above the return implied by the beta risk he had undertaken. 31

32 Passive vs Active Portfolio Management Investors who believe market prices are informationally efficient often follow a passive investment strategy (i.e. invest in an index of risky assets that serves as a proxy for the market portfolio and allocate a portion of their investable assets to a risk-free asset, such as short term govt securities) In practice, many investors and portfolio managers believe their estimates of security values are correct and market prices are incorrect. Such investors will not use the weights of the market portfolio but will invest more than the market weights in securities that they believe are undervalued and less than the market weights in securities which they believe are overvalued. This is referred to as active portfolio management to differentiate it from a passive investment strategy that utilizes a market index for the optimal risky asset portfolio. 32

Return and Risk: The Capital-Asset Pricing Model (CAPM)

") Return and Risk: The Capital-Asset Pricing Model (CAPM) Expected Returns (Single assets & Portfolios), Variance, Diversification, Efficient Set, Market Portfolio, and CAPM Expected Returns and Variances

Return and Risk: The Capital-Asset Pricing Model (CAPM) Expected Returns (Single assets & Portfolios), Variance, Diversification, Efficient Set, Market Portfolio, and CAPM Expected Returns and Variances

RETURN AND RISK: The Capital Asset Pricing Model

RETURN AND RISK: The Capital Asset Pricing Model (BASED ON RWJJ CHAPTER 11) Return and Risk: The Capital Asset Pricing Model (CAPM) Know how to calculate expected returns Understand covariance, correlation,

RETURN AND RISK: The Capital Asset Pricing Model (BASED ON RWJJ CHAPTER 11) Return and Risk: The Capital Asset Pricing Model (CAPM) Know how to calculate expected returns Understand covariance, correlation,

Archana Khetan 05/09/ MAFA (CA Final) - Portfolio Management

- Portfolio Management") Archana Khetan 05/09/2010 +91-9930812722 Archana090@hotmail.com MAFA (CA Final) - Portfolio Management 1 Portfolio Management Portfolio is a collection of assets. By investing in a portfolio or combination

Archana Khetan 05/09/2010 +91-9930812722 Archana090@hotmail.com MAFA (CA Final) - Portfolio Management 1 Portfolio Management Portfolio is a collection of assets. By investing in a portfolio or combination

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

Ch. 8 Risk and Rates of Return. Return, Risk and Capital Market. Investment returns

Ch. 8 Risk and Rates of Return Topics Measuring Return Measuring Risk Risk & Diversification CAPM Return, Risk and Capital Market Managers must estimate current and future opportunity rates of return for

Ch. 8 Risk and Rates of Return Topics Measuring Return Measuring Risk Risk & Diversification CAPM Return, Risk and Capital Market Managers must estimate current and future opportunity rates of return for

Lecture 5. Return and Risk: The Capital Asset Pricing Model

Lecture 5 Return and Risk: The Capital Asset Pricing Model Outline 1 Individual Securities 2 Expected Return, Variance, and Covariance 3 The Return and Risk for Portfolios 4 The Efficient Set for Two Assets

Lecture 5 Return and Risk: The Capital Asset Pricing Model Outline 1 Individual Securities 2 Expected Return, Variance, and Covariance 3 The Return and Risk for Portfolios 4 The Efficient Set for Two Assets

Lecture 10-12: CAPM.

Lecture 10-12: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Minimum Variance Mathematics. VI. Individual Assets in a CAPM World. VII. Intuition

Lecture 10-12: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Minimum Variance Mathematics. VI. Individual Assets in a CAPM World. VII. Intuition

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS. BKM Ch 7

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS BKM Ch 7 ASSET ALLOCATION Idea from bank account to diversified portfolio Discussion principles are the same for any number of stocks A. bonds and stocks B.

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS BKM Ch 7 ASSET ALLOCATION Idea from bank account to diversified portfolio Discussion principles are the same for any number of stocks A. bonds and stocks B.

University 18 Lessons Financial Management. Unit 12: Return, Risk and Shareholder Value

University 18 Lessons Financial Management Unit 12: Return, Risk and Shareholder Value Risk and Return Risk and Return Security analysis is built around the idea that investors are concerned with two principal

University 18 Lessons Financial Management Unit 12: Return, Risk and Shareholder Value Risk and Return Risk and Return Security analysis is built around the idea that investors are concerned with two principal

CHAPTER 11 RETURN AND RISK: THE CAPITAL ASSET PRICING MODEL (CAPM)

") CHAPTER 11 RETURN AND RISK: THE CAPITAL ASSET PRICING MODEL (CAPM) Answers to Concept Questions 1. Some of the risk in holding any asset is unique to the asset in question. By investing in a variety of

CHAPTER 11 RETURN AND RISK: THE CAPITAL ASSET PRICING MODEL (CAPM) Answers to Concept Questions 1. Some of the risk in holding any asset is unique to the asset in question. By investing in a variety of

Risk and Return. CA Final Paper 2 Strategic Financial Management Chapter 7. Dr. Amit Bagga Phd.,FCA,AICWA,Mcom.

Risk and Return CA Final Paper 2 Strategic Financial Management Chapter 7 Dr. Amit Bagga Phd.,FCA,AICWA,Mcom. Learning Objectives Discuss the objectives of portfolio Management -Risk and Return Phases

Risk and Return CA Final Paper 2 Strategic Financial Management Chapter 7 Dr. Amit Bagga Phd.,FCA,AICWA,Mcom. Learning Objectives Discuss the objectives of portfolio Management -Risk and Return Phases

Adjusting discount rate for Uncertainty

Page 1 Adjusting discount rate for Uncertainty The Issue A simple approach: WACC Weighted average Cost of Capital A better approach: CAPM Capital Asset Pricing Model Massachusetts Institute of Technology

Page 1 Adjusting discount rate for Uncertainty The Issue A simple approach: WACC Weighted average Cost of Capital A better approach: CAPM Capital Asset Pricing Model Massachusetts Institute of Technology

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice A. Mean-Variance Analysis 1. Thevarianceofaportfolio. Consider the choice between two risky assets with returns R 1 and R 2.

QR43, Introduction to Investments Class Notes, Fall 2003 IV. Portfolio Choice A. Mean-Variance Analysis 1. Thevarianceofaportfolio. Consider the choice between two risky assets with returns R 1 and R 2.

Foundations of Finance

Lecture 5: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Individual Assets in a CAPM World. VI. Intuition for the SML (E[R p ] depending

Lecture 5: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Individual Assets in a CAPM World. VI. Intuition for the SML (E[R p ] depending

u (x) < 0. and if you believe in diminishing return of the wealth, then you would require

< 0. and if you believe in diminishing return of the wealth, then you would require") Chapter 8 Markowitz Portfolio Theory 8.7 Investor Utility Functions People are always asked the question: would more money make you happier? The answer is usually yes. The next question is how much more

Chapter 8 Markowitz Portfolio Theory 8.7 Investor Utility Functions People are always asked the question: would more money make you happier? The answer is usually yes. The next question is how much more

Chapter 13 Return, Risk, and Security Market Line

1 Chapter 13 Return, Risk, and Security Market Line Konan Chan Financial Management, Spring 2018 Topics Covered Expected Return and Variance Portfolio Risk and Return Risk & Diversification Systematic

1 Chapter 13 Return, Risk, and Security Market Line Konan Chan Financial Management, Spring 2018 Topics Covered Expected Return and Variance Portfolio Risk and Return Risk & Diversification Systematic

ECO 317 Economics of Uncertainty Fall Term 2009 Tuesday October 6 Portfolio Allocation Mean-Variance Approach

ECO 317 Economics of Uncertainty Fall Term 2009 Tuesday October 6 ortfolio Allocation Mean-Variance Approach Validity of the Mean-Variance Approach Constant absolute risk aversion (CARA): u(w ) = exp(

ECO 317 Economics of Uncertainty Fall Term 2009 Tuesday October 6 ortfolio Allocation Mean-Variance Approach Validity of the Mean-Variance Approach Constant absolute risk aversion (CARA): u(w ) = exp(

Solutions to questions in Chapter 8 except those in PS4. The minimum-variance portfolio is found by applying the formula:

Solutions to questions in Chapter 8 except those in PS4 1. The parameters of the opportunity set are: E(r S ) = 20%, E(r B ) = 12%, σ S = 30%, σ B = 15%, ρ =.10 From the standard deviations and the correlation

Solutions to questions in Chapter 8 except those in PS4 1. The parameters of the opportunity set are: E(r S ) = 20%, E(r B ) = 12%, σ S = 30%, σ B = 15%, ρ =.10 From the standard deviations and the correlation

Financial Mathematics III Theory summary

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

Financial Mathematics III Theory summary Table of Contents Lecture 1... 7 1. State the objective of modern portfolio theory... 7 2. Define the return of an asset... 7 3. How is expected return defined?...

For each of the questions 1-6, check one of the response alternatives A, B, C, D, E with a cross in the table below:

November 2016 Page 1 of (6) Multiple Choice Questions (3 points per question) For each of the questions 1-6, check one of the response alternatives A, B, C, D, E with a cross in the table below: Question

November 2016 Page 1 of (6) Multiple Choice Questions (3 points per question) For each of the questions 1-6, check one of the response alternatives A, B, C, D, E with a cross in the table below: Question

Chapter 11. Return and Risk: The Capital Asset Pricing Model (CAPM) Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.") Chapter 11 Return and Risk: The Capital Asset Pricing Model (CAPM) McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. 11-0 Know how to calculate expected returns Know

Chapter 11 Return and Risk: The Capital Asset Pricing Model (CAPM) McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. 11-0 Know how to calculate expected returns Know

Capital Allocation Between The Risky And The Risk- Free Asset

Capital Allocation Between The Risky And The Risk- Free Asset Chapter 7 Investment Decisions capital allocation decision = choice of proportion to be invested in risk-free versus risky assets asset allocation

Capital Allocation Between The Risky And The Risk- Free Asset Chapter 7 Investment Decisions capital allocation decision = choice of proportion to be invested in risk-free versus risky assets asset allocation

Microéconomie de la finance

Microéconomie de la finance 7 e édition Christophe Boucher christophe.boucher@univ-lorraine.fr 1 Chapitre 6 7 e édition Les modèles d évaluation d actifs 2 Introduction The Single-Index Model - Simplifying

Microéconomie de la finance 7 e édition Christophe Boucher christophe.boucher@univ-lorraine.fr 1 Chapitre 6 7 e édition Les modèles d évaluation d actifs 2 Introduction The Single-Index Model - Simplifying

Portfolio Management

Portfolio Management Risk & Return Return Income received on an investment (Dividend) plus any change in market price( Capital gain), usually expressed as a percent of the beginning market price of the

Portfolio Management Risk & Return Return Income received on an investment (Dividend) plus any change in market price( Capital gain), usually expressed as a percent of the beginning market price of the

3. Capital asset pricing model and factor models

3. Capital asset pricing model and factor models (3.1) Capital asset pricing model and beta values (3.2) Interpretation and uses of the capital asset pricing model (3.3) Factor models (3.4) Performance

3. Capital asset pricing model and factor models (3.1) Capital asset pricing model and beta values (3.2) Interpretation and uses of the capital asset pricing model (3.3) Factor models (3.4) Performance

Session 10: Lessons from the Markowitz framework p. 1

Session 10: Lessons from the Markowitz framework Susan Thomas http://www.igidr.ac.in/ susant susant@mayin.org IGIDR Bombay Session 10: Lessons from the Markowitz framework p. 1 Recap The Markowitz question:

Session 10: Lessons from the Markowitz framework Susan Thomas http://www.igidr.ac.in/ susant susant@mayin.org IGIDR Bombay Session 10: Lessons from the Markowitz framework p. 1 Recap The Markowitz question:

Models of Asset Pricing

appendix1 to chapter 5 Models of Asset Pricing In Chapter 4, we saw that the return on an asset (such as a bond) measures how much we gain from holding that asset. When we make a decision to buy an asset,

appendix1 to chapter 5 Models of Asset Pricing In Chapter 4, we saw that the return on an asset (such as a bond) measures how much we gain from holding that asset. When we make a decision to buy an asset,

Financial Markets. Laurent Calvet. John Lewis Topic 13: Capital Asset Pricing Model (CAPM)

") Financial Markets Laurent Calvet calvet@hec.fr John Lewis john.lewis04@imperial.ac.uk Topic 13: Capital Asset Pricing Model (CAPM) HEC MBA Financial Markets Risk-Adjusted Discount Rate Method We need a

Financial Markets Laurent Calvet calvet@hec.fr John Lewis john.lewis04@imperial.ac.uk Topic 13: Capital Asset Pricing Model (CAPM) HEC MBA Financial Markets Risk-Adjusted Discount Rate Method We need a

CHAPTER 2 RISK AND RETURN: Part I

CHAPTER 2 RISK AND RETURN: Part I (Difficulty Levels: Easy, Easy/Medium, Medium, Medium/Hard, and Hard) Please see the preface for information on the AACSB letter indicators (F, M, etc.) on the subject

CHAPTER 2 RISK AND RETURN: Part I (Difficulty Levels: Easy, Easy/Medium, Medium, Medium/Hard, and Hard) Please see the preface for information on the AACSB letter indicators (F, M, etc.) on the subject

CHAPTER 8: INDEX MODELS

Chapter 8 - Index odels CHATER 8: INDEX ODELS ROBLE SETS 1. The advantage of the index model, compared to the arkowitz procedure, is the vastly reduced number of estimates required. In addition, the large

Chapter 8 - Index odels CHATER 8: INDEX ODELS ROBLE SETS 1. The advantage of the index model, compared to the arkowitz procedure, is the vastly reduced number of estimates required. In addition, the large

Efficient Frontier and Asset Allocation

Topic 4 Efficient Frontier and Asset Allocation LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Explain the concept of efficient frontier and Markowitz portfolio theory; 2. Discuss

Topic 4 Efficient Frontier and Asset Allocation LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Explain the concept of efficient frontier and Markowitz portfolio theory; 2. Discuss

KEIR EDUCATIONAL RESOURCES

INVESTMENT PLANNING 2017 Published by: KEIR EDUCATIONAL RESOURCES 4785 Emerald Way Middletown, OH 45044 1-800-795-5347 1-800-859-5347 FAX E-mail customerservice@keirsuccess.com www.keirsuccess.com TABLE

INVESTMENT PLANNING 2017 Published by: KEIR EDUCATIONAL RESOURCES 4785 Emerald Way Middletown, OH 45044 1-800-795-5347 1-800-859-5347 FAX E-mail customerservice@keirsuccess.com www.keirsuccess.com TABLE

CHAPTER 2 RISK AND RETURN: PART I

1. The tighter the probability distribution of its expected future returns, the greater the risk of a given investment as measured by its standard deviation. False Difficulty: Easy LEARNING OBJECTIVES:

1. The tighter the probability distribution of its expected future returns, the greater the risk of a given investment as measured by its standard deviation. False Difficulty: Easy LEARNING OBJECTIVES:

Risk and Return and Portfolio Theory

Risk and Return and Portfolio Theory Intro: Last week we learned how to calculate cash flows, now we want to learn how to discount these cash flows. This will take the next several weeks. We know discount

Risk and Return and Portfolio Theory Intro: Last week we learned how to calculate cash flows, now we want to learn how to discount these cash flows. This will take the next several weeks. We know discount

Answers to Concepts in Review

Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest expected

Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest expected

CHAPTER 6: PORTFOLIO SELECTION

CHAPTER 6: PORTFOLIO SELECTION 6-1 21. The parameters of the opportunity set are: E(r S ) = 20%, E(r B ) = 12%, σ S = 30%, σ B = 15%, ρ =.10 From the standard deviations and the correlation coefficient

CHAPTER 6: PORTFOLIO SELECTION 6-1 21. The parameters of the opportunity set are: E(r S ) = 20%, E(r B ) = 12%, σ S = 30%, σ B = 15%, ρ =.10 From the standard deviations and the correlation coefficient

Copyright 2009 Pearson Education Canada

Operating Cash Flows: Sales $682,500 $771,750 $868,219 $972,405 $957,211 less expenses $477,750 $540,225 $607,753 $680,684 $670,048 Difference $204,750 $231,525 $260,466 $291,722 $287,163 After-tax (1

Operating Cash Flows: Sales $682,500 $771,750 $868,219 $972,405 $957,211 less expenses $477,750 $540,225 $607,753 $680,684 $670,048 Difference $204,750 $231,525 $260,466 $291,722 $287,163 After-tax (1

Return, Risk, and the Security Market Line

Chapter 13 Key Concepts and Skills Return, Risk, and the Security Market Line Know how to calculate expected returns Understand the impact of diversification Understand the systematic risk principle Understand

Chapter 13 Key Concepts and Skills Return, Risk, and the Security Market Line Know how to calculate expected returns Understand the impact of diversification Understand the systematic risk principle Understand

ECMC49F Midterm. Instructor: Travis NG Date: Oct 26, 2005 Duration: 1 hour 50 mins Total Marks: 100. [1] [25 marks] Decision-making under certainty

![ECMC49F Midterm. Instructor: Travis NG Date: Oct 26, 2005 Duration: 1 hour 50 mins Total Marks: 100. [1] [25 marks] Decision-making under certainty](/thumbs/83/88403560.jpg "ECMC49F Midterm. Instructor: Travis NG Date: Oct 26, 2005 Duration: 1 hour 50 mins Total Marks: 100. [1] [25 marks] Decision-making under certainty") ECMC49F Midterm Instructor: Travis NG Date: Oct 26, 2005 Duration: 1 hour 50 mins Total Marks: 100 [1] [25 marks] Decision-making under certainty (a) [5 marks] Graphically demonstrate the Fisher Separation

ECMC49F Midterm Instructor: Travis NG Date: Oct 26, 2005 Duration: 1 hour 50 mins Total Marks: 100 [1] [25 marks] Decision-making under certainty (a) [5 marks] Graphically demonstrate the Fisher Separation

Analysis INTRODUCTION OBJECTIVES

Chapter5 Risk Analysis OBJECTIVES At the end of this chapter, you should be able to: 1. determine the meaning of risk and return; 2. explain the term and usage of statistics in determining risk and return;

Chapter5 Risk Analysis OBJECTIVES At the end of this chapter, you should be able to: 1. determine the meaning of risk and return; 2. explain the term and usage of statistics in determining risk and return;

23.1. Assumptions of Capital Market Theory

NPTEL Course Course Title: Security Analysis and Portfolio anagement Course Coordinator: Dr. Jitendra ahakud odule-12 Session-23 Capital arket Theory-I Capital market theory extends portfolio theory and

NPTEL Course Course Title: Security Analysis and Portfolio anagement Course Coordinator: Dr. Jitendra ahakud odule-12 Session-23 Capital arket Theory-I Capital market theory extends portfolio theory and

Performance Measurement and Attribution in Asset Management

Performance Measurement and Attribution in Asset Management Prof. Massimo Guidolin Portfolio Management Second Term 2019 Outline and objectives The problem of isolating skill from luck Simple risk-adjusted

Performance Measurement and Attribution in Asset Management Prof. Massimo Guidolin Portfolio Management Second Term 2019 Outline and objectives The problem of isolating skill from luck Simple risk-adjusted

CHAPTER 8: INDEX MODELS

CHTER 8: INDEX ODELS CHTER 8: INDEX ODELS ROBLE SETS 1. The advantage of the index model, compared to the arkoitz procedure, is the vastly reduced number of estimates required. In addition, the large number

CHTER 8: INDEX ODELS CHTER 8: INDEX ODELS ROBLE SETS 1. The advantage of the index model, compared to the arkoitz procedure, is the vastly reduced number of estimates required. In addition, the large number

CHAPTER 8 Risk and Rates of Return

CHAPTER 8 Risk and Rates of Return Stand-alone risk Portfolio risk Risk & return: CAPM The basic goal of the firm is to: maximize shareholder wealth! 1 Investment returns The rate of return on an investment

CHAPTER 8 Risk and Rates of Return Stand-alone risk Portfolio risk Risk & return: CAPM The basic goal of the firm is to: maximize shareholder wealth! 1 Investment returns The rate of return on an investment

Chapter 11. Topics Covered. Chapter 11 Objectives. Risk, Return, and Capital Budgeting

Chapter 11 Risk, Return, and Capital Budgeting Topics Covered Measuring Market Risk Portfolio Betas Risk and Return CAPM and Expected Return Security Market Line Capital Budgeting and Project Risk Chapter

Chapter 11 Risk, Return, and Capital Budgeting Topics Covered Measuring Market Risk Portfolio Betas Risk and Return CAPM and Expected Return Security Market Line Capital Budgeting and Project Risk Chapter

Final Exam Suggested Solutions

University of Washington Fall 003 Department of Economics Eric Zivot Economics 483 Final Exam Suggested Solutions This is a closed book and closed note exam. However, you are allowed one page of handwritten

University of Washington Fall 003 Department of Economics Eric Zivot Economics 483 Final Exam Suggested Solutions This is a closed book and closed note exam. However, you are allowed one page of handwritten

Investment In Bursa Malaysia Between Returns And Risks

Investment In Bursa Malaysia Between Returns And Risks AHMED KADHUM JAWAD AL-SULTANI, MUSTAQIM MUHAMMAD BIN MOHD TARMIZI University kebangsaan Malaysia,UKM, School of Business and Economics, 43600, Pangi

Investment In Bursa Malaysia Between Returns And Risks AHMED KADHUM JAWAD AL-SULTANI, MUSTAQIM MUHAMMAD BIN MOHD TARMIZI University kebangsaan Malaysia,UKM, School of Business and Economics, 43600, Pangi

Risk and Return. Nicole Höhling, Introduction. Definitions. Types of risk and beta

Risk and Return Nicole Höhling, 2009-09-07 Introduction Every decision regarding investments is based on the relationship between risk and return. Generally the return on an investment should be as high

Risk and Return Nicole Höhling, 2009-09-07 Introduction Every decision regarding investments is based on the relationship between risk and return. Generally the return on an investment should be as high

Define risk, risk aversion, and riskreturn

Risk and 1 Learning Objectives Define risk, risk aversion, and riskreturn tradeoff. Measure risk. Identify different types of risk. Explain methods of risk reduction. Describe how firms compensate for

Risk and 1 Learning Objectives Define risk, risk aversion, and riskreturn tradeoff. Measure risk. Identify different types of risk. Explain methods of risk reduction. Describe how firms compensate for

Lecture 2: Fundamentals of meanvariance

Lecture 2: Fundamentals of meanvariance analysis Prof. Massimo Guidolin Portfolio Management Second Term 2018 Outline and objectives Mean-variance and efficient frontiers: logical meaning o Guidolin-Pedio,

Lecture 2: Fundamentals of meanvariance analysis Prof. Massimo Guidolin Portfolio Management Second Term 2018 Outline and objectives Mean-variance and efficient frontiers: logical meaning o Guidolin-Pedio,

Expected Return Methodologies in Morningstar Direct Asset Allocation

Expected Return Methodologies in Morningstar Direct Asset Allocation I. Introduction to expected return II. The short version III. Detailed methodologies 1. Building Blocks methodology i. Methodology ii.

Expected Return Methodologies in Morningstar Direct Asset Allocation I. Introduction to expected return II. The short version III. Detailed methodologies 1. Building Blocks methodology i. Methodology ii.

Financial Economics: Capital Asset Pricing Model

Financial Economics: Capital Asset Pricing Model Shuoxun Hellen Zhang WISE & SOE XIAMEN UNIVERSITY April, 2015 1 / 66 Outline Outline MPT and the CAPM Deriving the CAPM Application of CAPM Strengths and

Financial Economics: Capital Asset Pricing Model Shuoxun Hellen Zhang WISE & SOE XIAMEN UNIVERSITY April, 2015 1 / 66 Outline Outline MPT and the CAPM Deriving the CAPM Application of CAPM Strengths and

General Notation. Return and Risk: The Capital Asset Pricing Model

Return and Risk: The Capital Asset Pricing Model (Text reference: Chapter 10) Topics general notation single security statistics covariance and correlation return and risk for a portfolio diversification

Return and Risk: The Capital Asset Pricing Model (Text reference: Chapter 10) Topics general notation single security statistics covariance and correlation return and risk for a portfolio diversification

Econ 422 Eric Zivot Fall 2005 Final Exam

Econ 422 Eric Zivot Fall 2005 Final Exam This is a closed book exam. However, you are allowed one page of notes (double-sided). Answer all questions. For the numerical problems, if you make a computational

Econ 422 Eric Zivot Fall 2005 Final Exam This is a closed book exam. However, you are allowed one page of notes (double-sided). Answer all questions. For the numerical problems, if you make a computational

Principles of Finance

Principles of Finance Grzegorz Trojanowski Lecture 7: Arbitrage Pricing Theory Principles of Finance - Lecture 7 1 Lecture 7 material Required reading: Elton et al., Chapter 16 Supplementary reading: Luenberger,

Principles of Finance Grzegorz Trojanowski Lecture 7: Arbitrage Pricing Theory Principles of Finance - Lecture 7 1 Lecture 7 material Required reading: Elton et al., Chapter 16 Supplementary reading: Luenberger,

MBA 203 Executive Summary

MBA 203 Executive Summary Professor Fedyk and Sraer Class 1. Present and Future Value Class 2. Putting Present Value to Work Class 3. Decision Rules Class 4. Capital Budgeting Class 6. Stock Valuation

MBA 203 Executive Summary Professor Fedyk and Sraer Class 1. Present and Future Value Class 2. Putting Present Value to Work Class 3. Decision Rules Class 4. Capital Budgeting Class 6. Stock Valuation

Mean-Variance Analysis

Mean-Variance Analysis If the investor s objective is to Maximize the Expected Rate of Return for a given level of Risk (or, Minimize Risk for a given level of Expected Rate of Return), and If the investor

Mean-Variance Analysis If the investor s objective is to Maximize the Expected Rate of Return for a given level of Risk (or, Minimize Risk for a given level of Expected Rate of Return), and If the investor

EQUITIES & INVESTMENT ANALYSIS MAF307 EXAM SUMMARY

EQUITIES & INVESTMENT ANALYSIS MAF307 EXAM SUMMARY TOPIC 1 INVESTMENT ENVIRONMENT & FINANCIAL INSTRUMENTS 4 FINANCIAL ASSETS - INTANGIBLE 4 BENEFITS OF INVESTING IN FINANCIAL ASSETS 4 REAL ASSETS 4 CLIENTS

EQUITIES & INVESTMENT ANALYSIS MAF307 EXAM SUMMARY TOPIC 1 INVESTMENT ENVIRONMENT & FINANCIAL INSTRUMENTS 4 FINANCIAL ASSETS - INTANGIBLE 4 BENEFITS OF INVESTING IN FINANCIAL ASSETS 4 REAL ASSETS 4 CLIENTS

Portfolio Management

MCF 17 Advanced Courses Portfolio Management Final Exam Time Allowed: 60 minutes Family Name (Surname) First Name Student Number (Matr.) Please answer all questions by choosing the most appropriate alternative

MCF 17 Advanced Courses Portfolio Management Final Exam Time Allowed: 60 minutes Family Name (Surname) First Name Student Number (Matr.) Please answer all questions by choosing the most appropriate alternative

Techniques for Calculating the Efficient Frontier

Techniques for Calculating the Efficient Frontier Weerachart Kilenthong RIPED, UTCC c Kilenthong 2017 Tee (Riped) Introduction 1 / 43 Two Fund Theorem The Two-Fund Theorem states that we can reach any

Techniques for Calculating the Efficient Frontier Weerachart Kilenthong RIPED, UTCC c Kilenthong 2017 Tee (Riped) Introduction 1 / 43 Two Fund Theorem The Two-Fund Theorem states that we can reach any

- P P THE RELATION BETWEEN RISK AND RETURN. Article by Dr. Ray Donnelly PhD, MSc., BComm, ACMA, CGMA Examiner in Strategic Corporate Finance

THE RELATION BETWEEN RISK AND RETURN Article by Dr. Ray Donnelly PhD, MSc., BComm, ACMA, CGMA Examiner in Strategic Corporate Finance 1. Introduction and Preliminaries A fundamental issue in finance pertains

THE RELATION BETWEEN RISK AND RETURN Article by Dr. Ray Donnelly PhD, MSc., BComm, ACMA, CGMA Examiner in Strategic Corporate Finance 1. Introduction and Preliminaries A fundamental issue in finance pertains

The mean-variance portfolio choice framework and its generalizations

The mean-variance portfolio choice framework and its generalizations Prof. Massimo Guidolin 20135 Theory of Finance, Part I (Sept. October) Fall 2014 Outline and objectives The backward, three-step solution

The mean-variance portfolio choice framework and its generalizations Prof. Massimo Guidolin 20135 Theory of Finance, Part I (Sept. October) Fall 2014 Outline and objectives The backward, three-step solution

SDMR Finance (2) Olivier Brandouy. University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School)

Olivier Brandouy. University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School)") SDMR Finance (2) Olivier Brandouy University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School) Outline 1 Formal Approach to QAM : concepts and notations 2 3 Portfolio risk and return

SDMR Finance (2) Olivier Brandouy University of Paris 1, Panthéon-Sorbonne, IAE (Sorbonne Graduate Business School) Outline 1 Formal Approach to QAM : concepts and notations 2 3 Portfolio risk and return

Capital Asset Pricing Model

Topic 5 Capital Asset Pricing Model LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Explain Capital Asset Pricing Model (CAPM) and its assumptions; 2. Compute Security Market Line

Topic 5 Capital Asset Pricing Model LEARNING OUTCOMES By the end of this topic, you should be able to: 1. Explain Capital Asset Pricing Model (CAPM) and its assumptions; 2. Compute Security Market Line

Econ 422 Eric Zivot Summer 2005 Final Exam Solutions

Econ 422 Eric Zivot Summer 2005 Final Exam Solutions This is a closed book exam. However, you are allowed one page of notes (double-sided). Answer all questions. For the numerical problems, if you make

Econ 422 Eric Zivot Summer 2005 Final Exam Solutions This is a closed book exam. However, you are allowed one page of notes (double-sided). Answer all questions. For the numerical problems, if you make

Use partial derivatives just found, evaluate at a = 0: This slope of small hyperbola must equal slope of CML:

Derivation of CAPM formula, contd. Use the formula: dµ σ dσ a = µ a µ dµ dσ = a σ. Use partial derivatives just found, evaluate at a = 0: Plug in and find: dµ dσ σ = σ jm σm 2. a a=0 σ M = a=0 a µ j µ

Derivation of CAPM formula, contd. Use the formula: dµ σ dσ a = µ a µ dµ dσ = a σ. Use partial derivatives just found, evaluate at a = 0: Plug in and find: dµ dσ σ = σ jm σm 2. a a=0 σ M = a=0 a µ j µ

MATH 4512 Fundamentals of Mathematical Finance

MATH 451 Fundamentals of Mathematical Finance Solution to Homework Three Course Instructor: Prof. Y.K. Kwok 1. The market portfolio consists of n uncorrelated assets with weight vector (x 1 x n T. Since

MATH 451 Fundamentals of Mathematical Finance Solution to Homework Three Course Instructor: Prof. Y.K. Kwok 1. The market portfolio consists of n uncorrelated assets with weight vector (x 1 x n T. Since

Measuring the Systematic Risk of Stocks Using the Capital Asset Pricing Model

Journal of Investment and Management 2017; 6(1): 13-21 http://www.sciencepublishinggroup.com/j/jim doi: 10.11648/j.jim.20170601.13 ISSN: 2328-7713 (Print); ISSN: 2328-7721 (Online) Measuring the Systematic

Journal of Investment and Management 2017; 6(1): 13-21 http://www.sciencepublishinggroup.com/j/jim doi: 10.11648/j.jim.20170601.13 ISSN: 2328-7713 (Print); ISSN: 2328-7721 (Online) Measuring the Systematic

CHAPTER 6: RISK AVERSION AND CAPITAL ALLOCATION TO RISKY ASSETS

CHAPTER 6: RISK AVERSION AND CAPITAL ALLOCATION TO RISKY ASSETS PROBLEM SETS 1. (e) 2. (b) A higher borrowing is a consequence of the risk of the borrowers default. In perfect markets with no additional

CHAPTER 6: RISK AVERSION AND CAPITAL ALLOCATION TO RISKY ASSETS PROBLEM SETS 1. (e) 2. (b) A higher borrowing is a consequence of the risk of the borrowers default. In perfect markets with no additional

Uniwersytet Ekonomiczny. George Matysiak. Presentation outline. Motivation for Performance Analysis

Uniwersytet Ekonomiczny George Matysiak Performance measurement 30 th November, 2015 Presentation outline Risk adjusted performance measures Assessing investment performance Risk considerations and ranking

Uniwersytet Ekonomiczny George Matysiak Performance measurement 30 th November, 2015 Presentation outline Risk adjusted performance measures Assessing investment performance Risk considerations and ranking

Chapter 8: CAPM. 1. Single Index Model. 2. Adding a Riskless Asset. 3. The Capital Market Line 4. CAPM. 5. The One-Fund Theorem

Chapter 8: CAPM 1. Single Index Model 2. Adding a Riskless Asset 3. The Capital Market Line 4. CAPM 5. The One-Fund Theorem 6. The Characteristic Line 7. The Pricing Model Single Index Model 1 1. Covariance

Chapter 8: CAPM 1. Single Index Model 2. Adding a Riskless Asset 3. The Capital Market Line 4. CAPM 5. The One-Fund Theorem 6. The Characteristic Line 7. The Pricing Model Single Index Model 1 1. Covariance

Mean-Variance Portfolio Theory

Mean-Variance Portfolio Theory Lakehead University Winter 2005 Outline Measures of Location Risk of a Single Asset Risk and Return of Financial Securities Risk of a Portfolio The Capital Asset Pricing

Mean-Variance Portfolio Theory Lakehead University Winter 2005 Outline Measures of Location Risk of a Single Asset Risk and Return of Financial Securities Risk of a Portfolio The Capital Asset Pricing

Aversion to Risk and Optimal Portfolio Selection in the Mean- Variance Framework

Aversion to Risk and Optimal Portfolio Selection in the Mean- Variance Framework Prof. Massimo Guidolin 20135 Theory of Finance, Part I (Sept. October) Fall 2018 Outline and objectives Four alternative

Aversion to Risk and Optimal Portfolio Selection in the Mean- Variance Framework Prof. Massimo Guidolin 20135 Theory of Finance, Part I (Sept. October) Fall 2018 Outline and objectives Four alternative

From optimisation to asset pricing

From optimisation to asset pricing IGIDR, Bombay May 10, 2011 From Harry Markowitz to William Sharpe = from portfolio optimisation to pricing risk Harry versus William Harry Markowitz helped us answer

From optimisation to asset pricing IGIDR, Bombay May 10, 2011 From Harry Markowitz to William Sharpe = from portfolio optimisation to pricing risk Harry versus William Harry Markowitz helped us answer

Money & Capital Markets Fall 2011 Homework #1 Due: Friday, Sept. 9 th. Answer Key

Money & Capital Markets Fall 011 Homework #1 Due: Friday, Sept. 9 th Answer Key 1. (6 points) A pension fund manager is considering two mutual funds. The first is a stock fund. The second is a long-term

Money & Capital Markets Fall 011 Homework #1 Due: Friday, Sept. 9 th Answer Key 1. (6 points) A pension fund manager is considering two mutual funds. The first is a stock fund. The second is a long-term

ECON FINANCIAL ECONOMICS

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Fall 2017 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Fall 2017 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

ECMC49S Midterm. Instructor: Travis NG Date: Feb 27, 2007 Duration: From 3:05pm to 5:00pm Total Marks: 100

ECMC49S Midterm Instructor: Travis NG Date: Feb 27, 2007 Duration: From 3:05pm to 5:00pm Total Marks: 100 [1] [25 marks] Decision-making under certainty (a) [10 marks] (i) State the Fisher Separation Theorem

ECMC49S Midterm Instructor: Travis NG Date: Feb 27, 2007 Duration: From 3:05pm to 5:00pm Total Marks: 100 [1] [25 marks] Decision-making under certainty (a) [10 marks] (i) State the Fisher Separation Theorem

ECON FINANCIAL ECONOMICS

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Spring 2018 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Spring 2018 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

Aversion to Risk and Optimal Portfolio Selection in the Mean- Variance Framework

Aversion to Risk and Optimal Portfolio Selection in the Mean- Variance Framework Prof. Massimo Guidolin 20135 Theory of Finance, Part I (Sept. October) Fall 2017 Outline and objectives Four alternative

Aversion to Risk and Optimal Portfolio Selection in the Mean- Variance Framework Prof. Massimo Guidolin 20135 Theory of Finance, Part I (Sept. October) Fall 2017 Outline and objectives Four alternative

Mean Variance Analysis and CAPM

Mean Variance Analysis and CAPM Yan Zeng Version 1.0.2, last revised on 2012-05-30. Abstract A summary of mean variance analysis in portfolio management and capital asset pricing model. 1. Mean-Variance

Mean Variance Analysis and CAPM Yan Zeng Version 1.0.2, last revised on 2012-05-30. Abstract A summary of mean variance analysis in portfolio management and capital asset pricing model. 1. Mean-Variance

LECTURE NOTES 3 ARIEL M. VIALE

LECTURE NOTES 3 ARIEL M VIALE I Markowitz-Tobin Mean-Variance Portfolio Analysis Assumption Mean-Variance preferences Markowitz 95 Quadratic utility function E [ w b w ] { = E [ w] b V ar w + E [ w] }

LECTURE NOTES 3 ARIEL M VIALE I Markowitz-Tobin Mean-Variance Portfolio Analysis Assumption Mean-Variance preferences Markowitz 95 Quadratic utility function E [ w b w ] { = E [ w] b V ar w + E [ w] }

Module 3: Factor Models

Module 3: Factor Models (BUSFIN 4221 - Investments) Andrei S. Gonçalves 1 1 Finance Department The Ohio State University Fall 2016 1 Module 1 - The Demand for Capital 2 Module 1 - The Supply of Capital

Module 3: Factor Models (BUSFIN 4221 - Investments) Andrei S. Gonçalves 1 1 Finance Department The Ohio State University Fall 2016 1 Module 1 - The Demand for Capital 2 Module 1 - The Supply of Capital

Corporate Finance Finance Ch t ap er 1: I t nves t men D i ec sions Albert Banal-Estanol

Corporate Finance Chapter : Investment tdecisions i Albert Banal-Estanol In this chapter Part (a): Compute projects cash flows : Computing earnings, and free cash flows Necessary inputs? Part (b): Evaluate

Corporate Finance Chapter : Investment tdecisions i Albert Banal-Estanol In this chapter Part (a): Compute projects cash flows : Computing earnings, and free cash flows Necessary inputs? Part (b): Evaluate

FNCE 4030 Fall 2012 Roberto Caccia, Ph.D. Midterm_2a (2-Nov-2012) Your name:

Your name:") Answer the questions in the space below. Written answers require no more than few compact sentences to show you understood and master the concept. Show your work to receive partial credit. Points are as

Answer the questions in the space below. Written answers require no more than few compact sentences to show you understood and master the concept. Show your work to receive partial credit. Points are as

LECTURE 1. EQUITY Ownership Not a promise to pay Downside/Upside Bottom of Waterfall

LECTURE 1 FIN 3710 REVIEW Risk/Economy DEFINITIONS: Value Creation (Cost < Result) Investment Return Vs Risk - Analysis Managing / Hedging Real Assets Vs Financial Assets (Land/Building Vs Stock/Bonds)

LECTURE 1 FIN 3710 REVIEW Risk/Economy DEFINITIONS: Value Creation (Cost < Result) Investment Return Vs Risk - Analysis Managing / Hedging Real Assets Vs Financial Assets (Land/Building Vs Stock/Bonds)

Chapter. Return, Risk, and the Security Market Line. McGraw-Hill/Irwin. Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter Return, Risk, and the Security Market Line McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Return, Risk, and the Security Market Line Our goal in this chapter

Chapter Return, Risk, and the Security Market Line McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Return, Risk, and the Security Market Line Our goal in this chapter

Statistically Speaking

Statistically Speaking August 2001 Alpha a Alpha is a measure of a investment instrument s risk-adjusted return. It can be used to directly measure the value added or subtracted by a fund s manager. It

Statistically Speaking August 2001 Alpha a Alpha is a measure of a investment instrument s risk-adjusted return. It can be used to directly measure the value added or subtracted by a fund s manager. It

E(r) The Capital Market Line (CML)

The Capital Market Line (CML)") The Capital Asset Pricing Model (CAPM) B. Espen Eckbo 2011 We have so far studied the relevant portfolio opportunity set (mean- variance efficient portfolios) We now study more specifically portfolio demand,

The Capital Asset Pricing Model (CAPM) B. Espen Eckbo 2011 We have so far studied the relevant portfolio opportunity set (mean- variance efficient portfolios) We now study more specifically portfolio demand,

FINC 430 TA Session 7 Risk and Return Solutions. Marco Sammon

FINC 430 TA Session 7 Risk and Return Solutions Marco Sammon Formulas for return and risk The expected return of a portfolio of two risky assets, i and j, is Expected return of asset - the percentage of

FINC 430 TA Session 7 Risk and Return Solutions Marco Sammon Formulas for return and risk The expected return of a portfolio of two risky assets, i and j, is Expected return of asset - the percentage of

Lecture #2. YTM / YTC / YTW IRR concept VOLATILITY Vs RETURN Relationship. Risk Premium over the Standard Deviation of portfolio excess return

REVIEW Lecture #2 YTM / YTC / YTW IRR concept VOLATILITY Vs RETURN Relationship Sharpe Ratio: Risk Premium over the Standard Deviation of portfolio excess return (E(r p) r f ) / σ 8% / 20% = 0.4x. A higher

REVIEW Lecture #2 YTM / YTC / YTW IRR concept VOLATILITY Vs RETURN Relationship Sharpe Ratio: Risk Premium over the Standard Deviation of portfolio excess return (E(r p) r f ) / σ 8% / 20% = 0.4x. A higher

FIN Second (Practice) Midterm Exam 04/11/06

Midterm Exam 04/11/06") FIN 3710 Investment Analysis Zicklin School of Business Baruch College Spring 2006 FIN 3710 Second (Practice) Midterm Exam 04/11/06 NAME: (Please print your name here) PLEDGE: (Sign your name here) SESSION:

FIN 3710 Investment Analysis Zicklin School of Business Baruch College Spring 2006 FIN 3710 Second (Practice) Midterm Exam 04/11/06 NAME: (Please print your name here) PLEDGE: (Sign your name here) SESSION:

Chapters 10&11 - Debt Securities

Chapters 10&11 - Debt Securities Bond characteristics Interest rate risk Bond rating Bond pricing Term structure theories Bond price behavior to interest rate changes Duration and immunization Bond investment

Chapters 10&11 - Debt Securities Bond characteristics Interest rate risk Bond rating Bond pricing Term structure theories Bond price behavior to interest rate changes Duration and immunization Bond investment

The Capital Assets Pricing Model & Arbitrage Pricing Theory: Properties and Applications in Jordan

Modern Applied Science; Vol. 12, No. 11; 2018 ISSN 1913-1844E-ISSN 1913-1852 Published by Canadian Center of Science and Education The Capital Assets Pricing Model & Arbitrage Pricing Theory: Properties

Modern Applied Science; Vol. 12, No. 11; 2018 ISSN 1913-1844E-ISSN 1913-1852 Published by Canadian Center of Science and Education The Capital Assets Pricing Model & Arbitrage Pricing Theory: Properties

Estimating Betas in Thinner Markets: The Case of the Athens Stock Exchange

Estimating Betas in Thinner Markets: The Case of the Athens Stock Exchange Thanasis Lampousis Department of Financial Management and Banking University of Piraeus, Greece E-mail: thanosbush@gmail.com Abstract

Estimating Betas in Thinner Markets: The Case of the Athens Stock Exchange Thanasis Lampousis Department of Financial Management and Banking University of Piraeus, Greece E-mail: thanosbush@gmail.com Abstract

Portfolio Management

Portfolio Management 010-011 1. Consider the following prices (calculated under the assumption of absence of arbitrage) corresponding to three sets of options on the Dow Jones index. Each point of the

Portfolio Management 010-011 1. Consider the following prices (calculated under the assumption of absence of arbitrage) corresponding to three sets of options on the Dow Jones index. Each point of the

Risk and Return. Return. Risk. M. En C. Eduardo Bustos Farías

Risk and Return Return M. En C. Eduardo Bustos Farías Risk 1 Inflation, Rates of Return, and the Fisher Effect Interest Rates Conceptually: Interest Rates Nominal risk-free Interest Rate krf = Real risk-free

Risk and Return Return M. En C. Eduardo Bustos Farías Risk 1 Inflation, Rates of Return, and the Fisher Effect Interest Rates Conceptually: Interest Rates Nominal risk-free Interest Rate krf = Real risk-free

Derivation Of The Capital Asset Pricing Model Part I - A Single Source Of Uncertainty

Derivation Of The Capital Asset Pricing Model Part I - A Single Source Of Uncertainty Gary Schurman MB, CFA August, 2012 The Capital Asset Pricing Model CAPM is used to estimate the required rate of return

Derivation Of The Capital Asset Pricing Model Part I - A Single Source Of Uncertainty Gary Schurman MB, CFA August, 2012 The Capital Asset Pricing Model CAPM is used to estimate the required rate of return

CHAPTER 5: ANSWERS TO CONCEPTS IN REVIEW

CHAPTER 5: ANSWERS TO CONCEPTS IN REVIEW 5.1 A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest

CHAPTER 5: ANSWERS TO CONCEPTS IN REVIEW 5.1 A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest

Chapter 5: Answers to Concepts in Review

Chapter 5: Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest

Chapter 5: Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest