Title: Introduction to Risk, Return and the Opportunity Cost of Capital Speaker: Rebecca Stull Created by: Gene Lai. online.wsu.

|

|

|

- Mervyn Hill

- 6 years ago

- Views:

Transcription

1 Title: Introduction to Risk, Return and the Opportunity Cost of Capital Speaker: Rebecca Stull Created by: Gene Lai online.wsu.edu

2 MODULE 8 INTRODUCTION TO RISK AND RETURN, AND THE OPPORTUNITY COST OF CAPITAL Revised by Gene Lai 2

3 Risk and Return Risk and Return are related. How? This module will focus on risk and return and their relationship to the opportunity cost of capital. 11-3

4 Outline Rates of Return A Century of Capital Market History Measuring Risk Risk & Diversification Thinking About Risk 11-4

5 Equity Rates of Return: A Review Percentage Return = Capital Gain + Dividend Initial Share Price Dividend Yield = Dividend Initial Share Price Capital Gain Yield = Capital Gain Initial Share Price 11-5

6 Rates of Return: Example Example: You purchase shares of GE stock at $15.13 on December 31, You sell them exactly one year later for $ During this time GE paid $.46 in dividends per share. Ignoring transaction costs, what is your rate of return, dividend yield and capital gain yield? Percentage Return $18.29 $15.13 $.46 $ % $.46 Dividend Yield = 3.04% $15.13 Capital Gain Yield $18.29 $15.13 $ % 11-6

7 Real Rates of Return Recall the relationship between real rates and nominal rates: 1 real rate of return = 1 + nominal rate of return 1 + inflation rate Example: Suppose inflation from December 2009 to December 2010 was 1.5%. What was GE stock s real rate of return, if its nominal rate of return was 23.93%? 11-7

8 Capital Market History: Market Indexes Market Index - Measure of the investment performance of the overall market. Dow Jones Industrial Average (The Dow) Value of a portfolio holding one share in each of 30 large industrial firms. Standard & Poor s Composite Index (S&P 500) Value of a portfolio holding shares in 500 firms. Holdings are proportional to the number of shares in the issues. 11-8

9 Total Returns for Different Asset Classes The Value of an Investment of $1 in

10 Annual Total Returns, Average Return Standard Deviation Distribution Small-company stocks 17.4% 33.8% Large-company stocks Long-term corporate bonds Long-term government Intermediate-term government U.S. Treasury bills % % 0 6.1% 0 5.7% 0 5.5% 0 3.8% Inflation % 11-10

11 The Difference in Total Returns? Risk Premium: Expected return in excess of risk-free return as compensation for risk. Maturity Premium: Extra average return from investing in long- versus short-term Treasury securities

12 Risk Premium: Example Interest Rate on Expected Market Return = + Treasury Bills Normal Risk Premium 1981: 21.4% = 14% + 7.4% 2008: 9.6% = 2.2% + 7.4% 2012: 7.47% = 0.07% + 7.4% 11-12

13 Returns and Risk We next show how to measure expected return and risk

14 Measuring Expected Rate of Return (for a Single Stock) r = or E (r) = expected rate of return. E(r) = n i i=1 rp. i 11-14

15 Measuring Risk (for a Single Stock) What is risk? Uncertainty How can it be measured? Variance: Average value of squared deviations from mean. A measure of volatility. Standard Deviation: Square root of variance. Also a measure of volatility

16 Standard Deviation of a Single Stock = Standard deviation. = Variance = 2 = n i1 (r i E(r)) 2 P. i 11-16

17 Investment Alternatives There are five possible states of economy next year. The probability associated each state is presented below. In addition, the returns associated with each state is also presented below. Economy Prob. T-Bill HT Coll USR MP Recession % -22.0% 28.0% 10.0% -13.0% Below avg Average Above avg Boom

18 Do the returns of HT and Coll. move with or counter to the economy? HT: Moves with the economy, and has a positive correlation. This is typical. HT is for high tech Coll: Is countercyclical of the economy, and has a negative correlation. This is unusual. Coll is for collection agency 11-18

= n i i=1 rp. i E(r) = (-22%)0.1 + (-2%)0.20 + (20%)0.40 + (35%)0.20 + (50%)0.")

19 Calculate the Expected Rate of Return for HT r = Expected rate of return. E(r) = n i i=1 rp. i E(r) = (-22%)0.1 + (-2%) (20%) (35%) (50%)0.1 = 17.4%

20 r HT 17.4% Market 15.0 USR 13.8 T-bill 8.0 Coll. 1.7 HT appears to be the best, but is it really? 11-20

) 2 2 P.")

21 What s the standard deviation of returns for each alternative? = Standard deviation. = Variance = = n i1 (r i E(r)) 2 2 P. i 11-21

22 Standard deviation for T-Bill n i1 (r i E(r)) 2 P. i T - bills = ( ) ( ) ( ) ( ) ( ) /2 T-bills = 0.0%. 22

2 0.2 + (.2.174) 2 0.4 + (.35.174) 2 0.2 + (.50.174) 2 0.1 1/2 HT = 20.0%.")

23 Standard deviation for HT HT = n i1 (r i E(r)) 2 P. i ( ) ( ) (.2.174) ( ) ( ) /2 HT = 20.0%. 23

24 Expected Returns vs. Risk Security Expected return Risk, HT 17.4% 20.0% Market USR 13.8* 18.8* T-bills Coll. 1.7* 13.4* *Seems misplaced

25 Portfolio Risk and Return Assume a two-stock portfolio with $50,000 in HT and $50,000 in Collections. Calculate E(r p ) and Calculate E(r p ) and p

26 Portfolio Expected Return, r p E(r P ) is a weighted average: n E(r p ) = S w i r i. i = 1 E(r p ) = 0.5(17.4%) + 0.5(1.7%) = 9.6%. Note: This is one method to calculate portfolio return

27 Portfolio Return for 2 Assets Portfolio rate of return ( )( ) fraction of portfolio rate of return = x in first asset on first asset ( )( ) fraction of portfolio rate of return + x in second asset on second asset Note that we can calculate portfolio rate of return for each scenario first, please see next slide

28 Alternative Method to Calculate Mean Estimated Return Economy Prob. HT Coll. Port. Recession % 28.0% 3.0% Below avg Average Above avg Boom ? What is Port. Return if the economy is booming? 15% = (50 + (-20))/

29 Alternative Method to Calculate Mean Estimated Return Economy Prob. HT Coll. Port. Recession % 28.0% 3.0% Below avg Average Above avg Boom r p = (3.0%) (6.4%) (10.0%) (12.5%) (15.0%)0.10 = 9.6%. Note: we can treat port. as a single security when calculating and variance

30 Alternative Method to Calculate Standard Deviation 1 / 2 ( ) ( ) p = + ( ) = 3.3%. + ( ) ( )

31 Some Comments p = 3.3% is much lower than that of either stock (20% and 13.4%). p = 3.3% is lower than the average of HT and Coll s standard deviation = (.5)(20%) + (.5)(13.4%) = 16.7%. The Portfolio provides average r but lower risk. Reason: negative correlation for this specific case

32 Returns Distribution for Two Perfectly Negatively Correlated Stocks (-1.0) and for Portfolio WM σ WM = correlation coefficient between W and M 25.. Stock W Stock M Portfolio WM

33 Returns Distributions for Two Perfectly Positively Correlated Stocks (+1.0) and for Portfolio MM 25 Stock M Stock M Portfolio MM

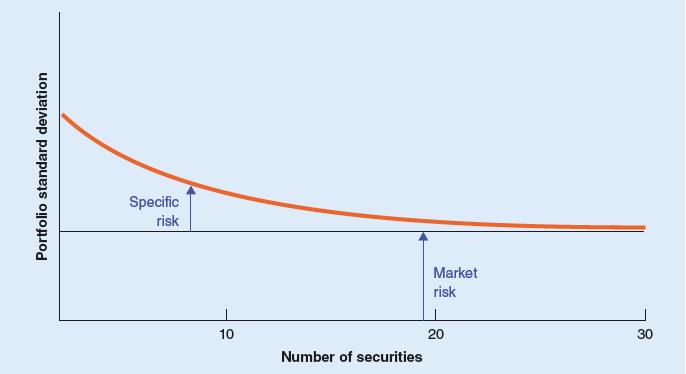

34 Diversification Risk and Diversification Strategy designed to reduce risk by spreading a portfolio across many investments. Unique Risk: Risk factors affecting only that firm. Also called diversifiable risk. Market Risk: Economy-wide sources of risk that affect the overall stock market. Also called systematic risk

35 Correlation Coefficient and Diversification Maximum diversification: correlation of coefficient = -1 No diversification: correlation of coefficient = +1 Correlation of coefficient <1, there is still diversification

36 Risk and Diversification 11-36

37 Thinking About Risk Message 1 Some Risks Look Big and Dangerous but Really Are Diversifiable Message 2 Market Risks Are Macro Risks Message 3 Risk Can Be Measured 11-37

Chapter 10. Chapter 10 Topics. What is Risk? The big picture. Introduction to Risk, Return, and the Opportunity Cost of Capital

1 Chapter 10 Introduction to Risk, Return, and the Opportunity Cost of Capital Chapter 10 Topics Risk: The Big Picture Rates of Return Risk Premiums Expected Return Stand Alone Risk Portfolio Return and

1 Chapter 10 Introduction to Risk, Return, and the Opportunity Cost of Capital Chapter 10 Topics Risk: The Big Picture Rates of Return Risk Premiums Expected Return Stand Alone Risk Portfolio Return and

Risk and Return (Introduction) Professor: Burcu Esmer

Professor: Burcu Esmer") Risk and Return (Introduction) Professor: Burcu Esmer 1 Overview Rates of Return: A Review A Century of Capital Market History Measuring Risk Risk & Diversification Thinking About Risk Measuring Market

Risk and Return (Introduction) Professor: Burcu Esmer 1 Overview Rates of Return: A Review A Century of Capital Market History Measuring Risk Risk & Diversification Thinking About Risk Measuring Market

Title: Risk, Return, and Capital Budgeting Speaker: Rebecca Stull Created by: Gene Lai. online.wsu.edu

Title: Risk, Return, and Capital Budgeting Speaker: Rebecca Stull Created by: Gene Lai online.wsu.edu MODULE 9 RISK, RETURN, AND CAPITAL BUDGETING Revised by Gene Lai 12-2 Risk, Return and the Capital

Title: Risk, Return, and Capital Budgeting Speaker: Rebecca Stull Created by: Gene Lai online.wsu.edu MODULE 9 RISK, RETURN, AND CAPITAL BUDGETING Revised by Gene Lai 12-2 Risk, Return and the Capital

CHAPTER 8 Risk and Rates of Return

CHAPTER 8 Risk and Rates of Return Stand-alone risk Portfolio risk Risk & return: CAPM The basic goal of the firm is to: maximize shareholder wealth! 1 Investment returns The rate of return on an investment

CHAPTER 8 Risk and Rates of Return Stand-alone risk Portfolio risk Risk & return: CAPM The basic goal of the firm is to: maximize shareholder wealth! 1 Investment returns The rate of return on an investment

Chapter 7. Introduction to Risk, Return, and the Opportunity Cost of Capital. Principles of Corporate Finance. Slides by Matthew Will

Principles of Corporate Finance Seventh Edition Richard A. Brealey Stewart C. Myers Chapter 7 Introduction to Risk, Return, and the Opportunity Cost of Capital Slides by Matthew Will - Topics Covered 75

Principles of Corporate Finance Seventh Edition Richard A. Brealey Stewart C. Myers Chapter 7 Introduction to Risk, Return, and the Opportunity Cost of Capital Slides by Matthew Will - Topics Covered 75

Risk and Return. Return. Risk. M. En C. Eduardo Bustos Farías

Risk and Return Return M. En C. Eduardo Bustos Farías Risk 1 Inflation, Rates of Return, and the Fisher Effect Interest Rates Conceptually: Interest Rates Nominal risk-free Interest Rate krf = Real risk-free

Risk and Return Return M. En C. Eduardo Bustos Farías Risk 1 Inflation, Rates of Return, and the Fisher Effect Interest Rates Conceptually: Interest Rates Nominal risk-free Interest Rate krf = Real risk-free

An investment s return is your reward for investing. An investment s risk is the uncertainty of what will happen with your investment dollar.

Chapter 7 An investment s return is your reward for investing. An investment s risk is the uncertainty of what will happen with your investment dollar. The relationship between risk and return is a tradeoff.

Chapter 7 An investment s return is your reward for investing. An investment s risk is the uncertainty of what will happen with your investment dollar. The relationship between risk and return is a tradeoff.

Ch. 8 Risk and Rates of Return. Return, Risk and Capital Market. Investment returns

Ch. 8 Risk and Rates of Return Topics Measuring Return Measuring Risk Risk & Diversification CAPM Return, Risk and Capital Market Managers must estimate current and future opportunity rates of return for

Ch. 8 Risk and Rates of Return Topics Measuring Return Measuring Risk Risk & Diversification CAPM Return, Risk and Capital Market Managers must estimate current and future opportunity rates of return for

Chapter 13 Return, Risk, and Security Market Line

1 Chapter 13 Return, Risk, and Security Market Line Konan Chan Financial Management, Spring 2018 Topics Covered Expected Return and Variance Portfolio Risk and Return Risk & Diversification Systematic

1 Chapter 13 Return, Risk, and Security Market Line Konan Chan Financial Management, Spring 2018 Topics Covered Expected Return and Variance Portfolio Risk and Return Risk & Diversification Systematic

Handout 4: Gains from Diversification for 2 Risky Assets Corporate Finance, Sections 001 and 002

Handout 4: Gains from Diversification for 2 Risky Assets Corporate Finance, Sections 001 and 002 Suppose you are deciding how to allocate your wealth between two risky assets. Recall that the expected

Handout 4: Gains from Diversification for 2 Risky Assets Corporate Finance, Sections 001 and 002 Suppose you are deciding how to allocate your wealth between two risky assets. Recall that the expected

Portfolio Management

Portfolio Management Risk & Return Return Income received on an investment (Dividend) plus any change in market price( Capital gain), usually expressed as a percent of the beginning market price of the

Portfolio Management Risk & Return Return Income received on an investment (Dividend) plus any change in market price( Capital gain), usually expressed as a percent of the beginning market price of the

10. Lessons From Capital Market History

10. Lessons From Capital Market History Chapter Outline How to measure returns The lessons from the capital market history Return: Expected returns Risk: the variability of returns 1 1 Risk, Return and

10. Lessons From Capital Market History Chapter Outline How to measure returns The lessons from the capital market history Return: Expected returns Risk: the variability of returns 1 1 Risk, Return and

Lecture 5. Return and Risk: The Capital Asset Pricing Model

Lecture 5 Return and Risk: The Capital Asset Pricing Model Outline 1 Individual Securities 2 Expected Return, Variance, and Covariance 3 The Return and Risk for Portfolios 4 The Efficient Set for Two Assets

Lecture 5 Return and Risk: The Capital Asset Pricing Model Outline 1 Individual Securities 2 Expected Return, Variance, and Covariance 3 The Return and Risk for Portfolios 4 The Efficient Set for Two Assets

Return, Risk, and the Security Market Line

Chapter 13 Key Concepts and Skills Return, Risk, and the Security Market Line Know how to calculate expected returns Understand the impact of diversification Understand the systematic risk principle Understand

Chapter 13 Key Concepts and Skills Return, Risk, and the Security Market Line Know how to calculate expected returns Understand the impact of diversification Understand the systematic risk principle Understand

Sample Midterm Questions Foundations of Financial Markets Prof. Lasse H. Pedersen

Sample Midterm Questions Foundations of Financial Markets Prof. Lasse H. Pedersen 1. Security A has a higher equilibrium price volatility than security B. Assuming all else is equal, the equilibrium bid-ask

Sample Midterm Questions Foundations of Financial Markets Prof. Lasse H. Pedersen 1. Security A has a higher equilibrium price volatility than security B. Assuming all else is equal, the equilibrium bid-ask

Appendix S: Content Portfolios and Diversification

Appendix S: Content Portfolios and Diversification 1188 The expected return on a portfolio is a weighted average of the expected return on the individual id assets; but estimating the risk, or standard

Appendix S: Content Portfolios and Diversification 1188 The expected return on a portfolio is a weighted average of the expected return on the individual id assets; but estimating the risk, or standard

Gatton College of Business and Economics Department of Finance & Quantitative Methods. Chapter 13. Finance 300 David Moore

Gatton College of Business and Economics Department of Finance & Quantitative Methods Chapter 13 Finance 300 David Moore Weighted average reminder Your grade 30% for the midterm 50% for the final. Homework

Gatton College of Business and Economics Department of Finance & Quantitative Methods Chapter 13 Finance 300 David Moore Weighted average reminder Your grade 30% for the midterm 50% for the final. Homework

Risk and Return: From Securities to Portfolios

FIN 614 Risk and Return 2: Portfolios Professor Robert B.H. Hauswald Kogod School of Business, AU Risk and Return: From Securities to Portfolios From securities individual risk and return characteristics

FIN 614 Risk and Return 2: Portfolios Professor Robert B.H. Hauswald Kogod School of Business, AU Risk and Return: From Securities to Portfolios From securities individual risk and return characteristics

... possibly the most important and least understood topic in finance

Correlation...... possibly the most important and least understood topic in finance 2017 Gary R. Evans. This lecture is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International

Correlation...... possibly the most important and least understood topic in finance 2017 Gary R. Evans. This lecture is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International

MBF2263 Portfolio Management. Lecture 8: Risk and Return in Capital Markets

MBF2263 Portfolio Management Lecture 8: Risk and Return in Capital Markets 1. A First Look at Risk and Return We begin our look at risk and return by illustrating how the risk premium affects investor

MBF2263 Portfolio Management Lecture 8: Risk and Return in Capital Markets 1. A First Look at Risk and Return We begin our look at risk and return by illustrating how the risk premium affects investor

Chapter. Diversification and Risky Asset Allocation. McGraw-Hill/Irwin. Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter Diversification and Risky Asset Allocation McGraw-Hill/Irwin Copyright 008 by The McGraw-Hill Companies, Inc. All rights reserved. Diversification Intuitively, we all know that if you hold many

Chapter Diversification and Risky Asset Allocation McGraw-Hill/Irwin Copyright 008 by The McGraw-Hill Companies, Inc. All rights reserved. Diversification Intuitively, we all know that if you hold many

Chapter 5. Asset Allocation - 1. Modern Portfolio Concepts

Asset Allocation - 1 Asset Allocation: Portfolio choice among broad investment classes. Chapter 5 Modern Portfolio Concepts Asset Allocation between risky and risk-free assets Asset Allocation with Two

Asset Allocation - 1 Asset Allocation: Portfolio choice among broad investment classes. Chapter 5 Modern Portfolio Concepts Asset Allocation between risky and risk-free assets Asset Allocation with Two

Chapter 11. Return and Risk: The Capital Asset Pricing Model (CAPM) Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.") Chapter 11 Return and Risk: The Capital Asset Pricing Model (CAPM) McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. 11-0 Know how to calculate expected returns Know

Chapter 11 Return and Risk: The Capital Asset Pricing Model (CAPM) McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. 11-0 Know how to calculate expected returns Know

CHAPTER 1 AN OVERVIEW OF THE INVESTMENT PROCESS

CHAPTER 1 AN OVERVIEW OF THE INVESTMENT PROCESS TRUE/FALSE 1. The rate of exchange between certain future dollars and certain current dollars is known as the pure rate of interest. ANS: T 2. An investment

CHAPTER 1 AN OVERVIEW OF THE INVESTMENT PROCESS TRUE/FALSE 1. The rate of exchange between certain future dollars and certain current dollars is known as the pure rate of interest. ANS: T 2. An investment

Homework #4 Suggested Solutions

JEM034 Corporate Finance Winter Semester 2017/2018 Instructor: Olga Bychkova Homework #4 Suggested Solutions Problem 1. (7.2) The following table shows the nominal returns on the U.S. stocks and the rate

JEM034 Corporate Finance Winter Semester 2017/2018 Instructor: Olga Bychkova Homework #4 Suggested Solutions Problem 1. (7.2) The following table shows the nominal returns on the U.S. stocks and the rate

INTRODUCTION TO RISK AND RETURN IN CAPITAL BUDGETING Chapters 7-9

INTRODUCTION TO RISK AND RETURN IN CAPITAL BUDGETING Chapters 7-9 WE ALL KNOW: THE GREATER THE RISK THE GREATER THE REQUIRED (OR EXPECTED) RETURN... Expected Return Risk-free rate Risk... BUT HOW DO WE

INTRODUCTION TO RISK AND RETURN IN CAPITAL BUDGETING Chapters 7-9 WE ALL KNOW: THE GREATER THE RISK THE GREATER THE REQUIRED (OR EXPECTED) RETURN... Expected Return Risk-free rate Risk... BUT HOW DO WE

All else equal, people dislike risk.

All else equal, people like returns. All else equal, people dislike risk. On October 7, 07, Home Depot stock closed at $64.. It paid dividends of $0.89 per share on November 9, 07, and $.03 per share on

All else equal, people like returns. All else equal, people dislike risk. On October 7, 07, Home Depot stock closed at $64.. It paid dividends of $0.89 per share on November 9, 07, and $.03 per share on

Introduction to Risk, Return and Opportunity Cost of Capital

Introduction to Risk, Return and Opportunity Cost of Capital Thomas Emilsson, --5 Risk, Return and Portfolio Variance Risk and Return When making investments, there needs to be an estimation of the risks

Introduction to Risk, Return and Opportunity Cost of Capital Thomas Emilsson, --5 Risk, Return and Portfolio Variance Risk and Return When making investments, there needs to be an estimation of the risks

Chapter 6 Efficient Diversification. b. Calculation of mean return and variance for the stock fund: (A) (B) (C) (D) (E) (F) (G)

(B) (C) (D) (E) (F) (G)") Chapter 6 Efficient Diversification 1. E(r P ) = 12.1% 3. a. The mean return should be equal to the value computed in the spreadsheet. The fund's return is 3% lower in a recession, but 3% higher in a boom.

Chapter 6 Efficient Diversification 1. E(r P ) = 12.1% 3. a. The mean return should be equal to the value computed in the spreadsheet. The fund's return is 3% lower in a recession, but 3% higher in a boom.

Notes on: J. David Cummins, Allocation of Capital in the Insurance Industry Risk Management and Insurance Review, 3, 2000, pp

Notes on: J. David Cummins Allocation of Capital in the Insurance Industry Risk Management and Insurance Review 3 2000 pp. 7-27. This reading addresses the standard management problem of allocating capital

Notes on: J. David Cummins Allocation of Capital in the Insurance Industry Risk Management and Insurance Review 3 2000 pp. 7-27. This reading addresses the standard management problem of allocating capital

CHAPTER 5. Introduction to Risk, Return, and the Historical Record INVESTMENTS BODIE, KANE, MARCUS. McGraw-Hill/Irwin

CHAPTER 5 Introduction to Risk, Return, and the Historical Record McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 5-2 Interest Rate Determinants Supply Households

CHAPTER 5 Introduction to Risk, Return, and the Historical Record McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 5-2 Interest Rate Determinants Supply Households

CHAPTER 2 RISK AND RETURN: Part I

CHAPTER 2 RISK AND RETURN: Part I (Difficulty Levels: Easy, Easy/Medium, Medium, Medium/Hard, and Hard) Please see the preface for information on the AACSB letter indicators (F, M, etc.) on the subject

CHAPTER 2 RISK AND RETURN: Part I (Difficulty Levels: Easy, Easy/Medium, Medium, Medium/Hard, and Hard) Please see the preface for information on the AACSB letter indicators (F, M, etc.) on the subject

CHAPTER 11 RETURN AND RISK: THE CAPITAL ASSET PRICING MODEL (CAPM)

") CHAPTER 11 RETURN AND RISK: THE CAPITAL ASSET PRICING MODEL (CAPM) Answers to Concept Questions 1. Some of the risk in holding any asset is unique to the asset in question. By investing in a variety of

CHAPTER 11 RETURN AND RISK: THE CAPITAL ASSET PRICING MODEL (CAPM) Answers to Concept Questions 1. Some of the risk in holding any asset is unique to the asset in question. By investing in a variety of

Chapter. Return, Risk, and the Security Market Line. McGraw-Hill/Irwin. Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter Return, Risk, and the Security Market Line McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Return, Risk, and the Security Market Line Our goal in this chapter

Chapter Return, Risk, and the Security Market Line McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Return, Risk, and the Security Market Line Our goal in this chapter

Financial Markets 11-1

Financial Markets Laurent Calvet calvet@hec.fr John Lewis john.lewis04@imperial.ac.uk Topic 11: Measuring Financial Risk HEC MBA Financial Markets 11-1 Risk There are many types of risk in financial transactions

Financial Markets Laurent Calvet calvet@hec.fr John Lewis john.lewis04@imperial.ac.uk Topic 11: Measuring Financial Risk HEC MBA Financial Markets 11-1 Risk There are many types of risk in financial transactions

Advanced Financial Economics Homework 2 Due on April 14th before class

Advanced Financial Economics Homework 2 Due on April 14th before class March 30, 2015 1. (20 points) An agent has Y 0 = 1 to invest. On the market two financial assets exist. The first one is riskless.

Advanced Financial Economics Homework 2 Due on April 14th before class March 30, 2015 1. (20 points) An agent has Y 0 = 1 to invest. On the market two financial assets exist. The first one is riskless.

Lecture 10-12: CAPM.

Lecture 10-12: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Minimum Variance Mathematics. VI. Individual Assets in a CAPM World. VII. Intuition

Lecture 10-12: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Minimum Variance Mathematics. VI. Individual Assets in a CAPM World. VII. Intuition

FIN 6160 Investment Theory. Lecture 7-10

FIN 6160 Investment Theory Lecture 7-10 Optimal Asset Allocation Minimum Variance Portfolio is the portfolio with lowest possible variance. To find the optimal asset allocation for the efficient frontier

FIN 6160 Investment Theory Lecture 7-10 Optimal Asset Allocation Minimum Variance Portfolio is the portfolio with lowest possible variance. To find the optimal asset allocation for the efficient frontier

Risk and Return and Portfolio Theory

Risk and Return and Portfolio Theory Intro: Last week we learned how to calculate cash flows, now we want to learn how to discount these cash flows. This will take the next several weeks. We know discount

Risk and Return and Portfolio Theory Intro: Last week we learned how to calculate cash flows, now we want to learn how to discount these cash flows. This will take the next several weeks. We know discount

COMM 324 INVESTMENTS AND PORTFOLIO MANAGEMENT ASSIGNMENT 1 Due: October 3

COMM 324 INVESTMENTS AND PORTFOLIO MANAGEMENT ASSIGNMENT 1 Due: October 3 1. The following information is provided for GAP, Incorporated, which is traded on NYSE: Fiscal Yr Ending January 31 Close Price

COMM 324 INVESTMENTS AND PORTFOLIO MANAGEMENT ASSIGNMENT 1 Due: October 3 1. The following information is provided for GAP, Incorporated, which is traded on NYSE: Fiscal Yr Ending January 31 Close Price

FINC 430 TA Session 7 Risk and Return Solutions. Marco Sammon

FINC 430 TA Session 7 Risk and Return Solutions Marco Sammon Formulas for return and risk The expected return of a portfolio of two risky assets, i and j, is Expected return of asset - the percentage of

FINC 430 TA Session 7 Risk and Return Solutions Marco Sammon Formulas for return and risk The expected return of a portfolio of two risky assets, i and j, is Expected return of asset - the percentage of

General Notation. Return and Risk: The Capital Asset Pricing Model

Return and Risk: The Capital Asset Pricing Model (Text reference: Chapter 10) Topics general notation single security statistics covariance and correlation return and risk for a portfolio diversification

Return and Risk: The Capital Asset Pricing Model (Text reference: Chapter 10) Topics general notation single security statistics covariance and correlation return and risk for a portfolio diversification

Adjusting discount rate for Uncertainty

Page 1 Adjusting discount rate for Uncertainty The Issue A simple approach: WACC Weighted average Cost of Capital A better approach: CAPM Capital Asset Pricing Model Massachusetts Institute of Technology

Page 1 Adjusting discount rate for Uncertainty The Issue A simple approach: WACC Weighted average Cost of Capital A better approach: CAPM Capital Asset Pricing Model Massachusetts Institute of Technology

Capital Budgeting-Part II

Capital Budgeting-Part II Dr. Ram Chandra Rai Sr.Professor (Finance Management) Railway Staff College, Vadodara, 390004 Risk Management Risk indicates extent of uncertainty of future cash flows Risk assessment

Capital Budgeting-Part II Dr. Ram Chandra Rai Sr.Professor (Finance Management) Railway Staff College, Vadodara, 390004 Risk Management Risk indicates extent of uncertainty of future cash flows Risk assessment

CHAPTER 2 RISK AND RETURN: PART I

1. The tighter the probability distribution of its expected future returns, the greater the risk of a given investment as measured by its standard deviation. False Difficulty: Easy LEARNING OBJECTIVES:

1. The tighter the probability distribution of its expected future returns, the greater the risk of a given investment as measured by its standard deviation. False Difficulty: Easy LEARNING OBJECTIVES:

Answers to Concepts in Review

Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest expected

Answers to Concepts in Review 1. A portfolio is simply a collection of investment vehicles assembled to meet a common investment goal. An efficient portfolio is a portfolio offering the highest expected

Risk, return, and diversification

Risk, return, and diversification A reading prepared by Pamela Peterson Drake O U T L I N E 1. Introduction 2. Diversification and risk 3. Modern portfolio theory 4. Asset pricing models 5. Summary 1.

Risk, return, and diversification A reading prepared by Pamela Peterson Drake O U T L I N E 1. Introduction 2. Diversification and risk 3. Modern portfolio theory 4. Asset pricing models 5. Summary 1.

Finance Concepts I: Present Discounted Value, Risk/Return Tradeoff

Finance Concepts I: Present Discounted Value, Risk/Return Tradeoff Federal Reserve Bank of New York Central Banking Seminar Preparatory Workshop in Financial Markets, Instruments and Institutions Anthony

Finance Concepts I: Present Discounted Value, Risk/Return Tradeoff Federal Reserve Bank of New York Central Banking Seminar Preparatory Workshop in Financial Markets, Instruments and Institutions Anthony

Principles of Finance Risk and Return. Instructor: Xiaomeng Lu

Principles of Finance Risk and Return Instructor: Xiaomeng Lu 1 Course Outline Course Introduction Time Value of Money DCF Valuation Security Analysis: Bond, Stock Capital Budgeting (Fundamentals) Portfolio

Principles of Finance Risk and Return Instructor: Xiaomeng Lu 1 Course Outline Course Introduction Time Value of Money DCF Valuation Security Analysis: Bond, Stock Capital Budgeting (Fundamentals) Portfolio

Chapter 10: Capital Markets and the Pricing of Risk

Chapter 0: Capital Markets and the Pricing of Risk- Chapter 0: Capital Markets and the Pricing of Risk Big Picture: ) To value a project, we need an interest rate to calculate present values ) The interest

Chapter 0: Capital Markets and the Pricing of Risk- Chapter 0: Capital Markets and the Pricing of Risk Big Picture: ) To value a project, we need an interest rate to calculate present values ) The interest

FIN Chapter 8. Risk and Return: Capital Asset Pricing Model. Liuren Wu

FIN 3000 Chapter 8 Risk and Return: Capital Asset Pricing Model Liuren Wu Overview 1. Portfolio Returns and Portfolio Risk Calculate the expected rate of return and volatility for a portfolio of investments

FIN 3000 Chapter 8 Risk and Return: Capital Asset Pricing Model Liuren Wu Overview 1. Portfolio Returns and Portfolio Risk Calculate the expected rate of return and volatility for a portfolio of investments

Define risk, risk aversion, and riskreturn

Risk and 1 Learning Objectives Define risk, risk aversion, and riskreturn tradeoff. Measure risk. Identify different types of risk. Explain methods of risk reduction. Describe how firms compensate for

Risk and 1 Learning Objectives Define risk, risk aversion, and riskreturn tradeoff. Measure risk. Identify different types of risk. Explain methods of risk reduction. Describe how firms compensate for

CHAPTER 5: LEARNING ABOUT RETURN AND RISK FROM THE HISTORICAL RECORD

CHAPTER 5: LEARNING ABOUT RETURN AND RISK FROM THE HISTORICAL RECORD PROBLEM SETS 1. The Fisher equation predicts that the nominal rate will equal the equilibrium real rate plus the expected inflation

CHAPTER 5: LEARNING ABOUT RETURN AND RISK FROM THE HISTORICAL RECORD PROBLEM SETS 1. The Fisher equation predicts that the nominal rate will equal the equilibrium real rate plus the expected inflation

Port(A,B) is a combination of two stocks, A and B, with standard deviations A and B. A,B = correlation (A,B) = 0.

is a combination of two stocks, A and B, with standard deviations A and B. A,B = correlation (A,B) = 0.") Corporate Finance, Module 6: Risk, Return, and Cost of Capital Practice Problems (The attached PDF file has better formatting.) Updated: July 19, 2007 Exercise 6.1: Minimum Variance Portfolio Port(A,B)

Corporate Finance, Module 6: Risk, Return, and Cost of Capital Practice Problems (The attached PDF file has better formatting.) Updated: July 19, 2007 Exercise 6.1: Minimum Variance Portfolio Port(A,B)

Lecture 18 Section Mon, Feb 16, 2009

The s the Lecture 18 Section 5.3.4 Hampden-Sydney College Mon, Feb 16, 2009 Outline The s the 1 2 3 The 4 s 5 the 6 The s the Exercise 5.12, page 333. The five-number summary for the distribution of income

The s the Lecture 18 Section 5.3.4 Hampden-Sydney College Mon, Feb 16, 2009 Outline The s the 1 2 3 The 4 s 5 the 6 The s the Exercise 5.12, page 333. The five-number summary for the distribution of income

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS. BKM Ch 7

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS BKM Ch 7 ASSET ALLOCATION Idea from bank account to diversified portfolio Discussion principles are the same for any number of stocks A. bonds and stocks B.

OPTIMAL RISKY PORTFOLIOS- ASSET ALLOCATIONS BKM Ch 7 ASSET ALLOCATION Idea from bank account to diversified portfolio Discussion principles are the same for any number of stocks A. bonds and stocks B.

When we model expected returns, we implicitly model expected prices

Week 1: Risk and Return Securities: why do we buy them? To take advantage of future cash flows (in the form of dividends or selling a security for a higher price). How much should we pay for this, considering

Week 1: Risk and Return Securities: why do we buy them? To take advantage of future cash flows (in the form of dividends or selling a security for a higher price). How much should we pay for this, considering

Global Journal of Finance and Banking Issues Vol. 5. No Manu Sharma & Rajnish Aggarwal PERFORMANCE ANALYSIS OF HEDGE FUND INDICES

PERFORMANCE ANALYSIS OF HEDGE FUND INDICES Dr. Manu Sharma 1 Panjab University, India E-mail: manumba2000@yahoo.com Rajnish Aggarwal 2 Panjab University, India Email: aggarwalrajnish@gmail.com Abstract

PERFORMANCE ANALYSIS OF HEDGE FUND INDICES Dr. Manu Sharma 1 Panjab University, India E-mail: manumba2000@yahoo.com Rajnish Aggarwal 2 Panjab University, India Email: aggarwalrajnish@gmail.com Abstract

Lecture 18 Section Mon, Sep 29, 2008

The s the Lecture 18 Section 5.3.4 Hampden-Sydney College Mon, Sep 29, 2008 Outline The s the 1 2 3 The 4 s 5 the 6 The s the Exercise 5.12, page 333. The five-number summary for the distribution of income

The s the Lecture 18 Section 5.3.4 Hampden-Sydney College Mon, Sep 29, 2008 Outline The s the 1 2 3 The 4 s 5 the 6 The s the Exercise 5.12, page 333. The five-number summary for the distribution of income

Basic Finance Exam #2

Basic Finance Exam #2 Chapter 10: Capital Budget list of planned investment project Sensitivity Analysis analysis of the effects on project profitability of changes in sales, costs and so on Fixed Cost

Basic Finance Exam #2 Chapter 10: Capital Budget list of planned investment project Sensitivity Analysis analysis of the effects on project profitability of changes in sales, costs and so on Fixed Cost

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

CHAPTER 9: THE CAPITAL ASSET PRICING MODEL 1. E(r P ) = r f + β P [E(r M ) r f ] 18 = 6 + β P(14 6) β P = 12/8 = 1.5 2. If the security s correlation coefficient with the market portfolio doubles (with

Econ 422 Eric Zivot Fall 2005 Final Exam

Econ 422 Eric Zivot Fall 2005 Final Exam This is a closed book exam. However, you are allowed one page of notes (double-sided). Answer all questions. For the numerical problems, if you make a computational

Econ 422 Eric Zivot Fall 2005 Final Exam This is a closed book exam. However, you are allowed one page of notes (double-sided). Answer all questions. For the numerical problems, if you make a computational

Diversification. Finance 100

Diversification Finance 100 Prof. Michael R. Roberts 1 Topic Overview How to measure risk and return» Sample risk measures for some classes of securities Brief Statistics Review» Realized and Expected

Diversification Finance 100 Prof. Michael R. Roberts 1 Topic Overview How to measure risk and return» Sample risk measures for some classes of securities Brief Statistics Review» Realized and Expected

Lecture 8 & 9 Risk & Rates of Return

Lecture 8 & 9 Risk & Rates of Return We start from the basic premise that investors LIKE return and DISLIKE risk. Therefore, people will invest in risky assets only if they expect to receive higher returns.

Lecture 8 & 9 Risk & Rates of Return We start from the basic premise that investors LIKE return and DISLIKE risk. Therefore, people will invest in risky assets only if they expect to receive higher returns.

The Performance of Farmland Investments. Bruce J. Sherrick University of Illinois Dept. of Ag and Consumer Econ.

The Performance of Farmland Investments Bruce J. Sherrick University of Illinois Dept. of Ag and Consumer Econ. Farmland Investments: Historical Context and Modern Times Unique features as asset class

The Performance of Farmland Investments Bruce J. Sherrick University of Illinois Dept. of Ag and Consumer Econ. Farmland Investments: Historical Context and Modern Times Unique features as asset class

For each of the questions 1-6, check one of the response alternatives A, B, C, D, E with a cross in the table below:

November 2016 Page 1 of (6) Multiple Choice Questions (3 points per question) For each of the questions 1-6, check one of the response alternatives A, B, C, D, E with a cross in the table below: Question

November 2016 Page 1 of (6) Multiple Choice Questions (3 points per question) For each of the questions 1-6, check one of the response alternatives A, B, C, D, E with a cross in the table below: Question

University of Colorado at Boulder Leeds School of Business Dr. Roberto Caccia

Applied Derivatives Risk Management Value at Risk Risk Management, ok but what s risk? risk is the pain of being wrong Market Risk: Risk of loss due to a change in market price Counterparty Risk: Risk

Applied Derivatives Risk Management Value at Risk Risk Management, ok but what s risk? risk is the pain of being wrong Market Risk: Risk of loss due to a change in market price Counterparty Risk: Risk

Solutions to questions in Chapter 8 except those in PS4. The minimum-variance portfolio is found by applying the formula:

Solutions to questions in Chapter 8 except those in PS4 1. The parameters of the opportunity set are: E(r S ) = 20%, E(r B ) = 12%, σ S = 30%, σ B = 15%, ρ =.10 From the standard deviations and the correlation

Solutions to questions in Chapter 8 except those in PS4 1. The parameters of the opportunity set are: E(r S ) = 20%, E(r B ) = 12%, σ S = 30%, σ B = 15%, ρ =.10 From the standard deviations and the correlation

Financial Management_MGT201. Lecture 19 to 22. Important Notes

Financial Management_MGT201 7 th Week of Lectures Lecture 19 to 22 Important Notes Explanation noted by me has shown with & symbols. Lecture No 19: 6 Dec 2015_Tuesday_ 2:13pm 3:02pm RISKS: Its very important

Financial Management_MGT201 7 th Week of Lectures Lecture 19 to 22 Important Notes Explanation noted by me has shown with & symbols. Lecture No 19: 6 Dec 2015_Tuesday_ 2:13pm 3:02pm RISKS: Its very important

RETURN AND RISK: The Capital Asset Pricing Model

RETURN AND RISK: The Capital Asset Pricing Model (BASED ON RWJJ CHAPTER 11) Return and Risk: The Capital Asset Pricing Model (CAPM) Know how to calculate expected returns Understand covariance, correlation,

RETURN AND RISK: The Capital Asset Pricing Model (BASED ON RWJJ CHAPTER 11) Return and Risk: The Capital Asset Pricing Model (CAPM) Know how to calculate expected returns Understand covariance, correlation,

CHAPTER 5. Introduction to Risk, Return, and the Historical Record INVESTMENTS BODIE, KANE, MARCUS. McGraw-Hill/Irwin

CHAPTER 5 Introduction to Risk, Return, and the Historical Record McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 5-2 Interest Rate Determinants Supply Households

CHAPTER 5 Introduction to Risk, Return, and the Historical Record McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 5-2 Interest Rate Determinants Supply Households

P2.T8. Risk Management & Investment Management. Jorion, Value at Risk: The New Benchmark for Managing Financial Risk, 3rd Edition.

P2.T8. Risk Management & Investment Management Jorion, Value at Risk: The New Benchmark for Managing Financial Risk, 3rd Edition. Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM and Deepa Raju

P2.T8. Risk Management & Investment Management Jorion, Value at Risk: The New Benchmark for Managing Financial Risk, 3rd Edition. Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM and Deepa Raju

CHAPTER 1 THE INVESTMENT SETTING

CHAPTER 1 THE INVESTMENT SETTING TRUE/FALSE 1. The rate of exchange between certain future dollars and certain current dollars is known as the pure rate of interest. ANS: T PTS: 1 2. An investment is the

CHAPTER 1 THE INVESTMENT SETTING TRUE/FALSE 1. The rate of exchange between certain future dollars and certain current dollars is known as the pure rate of interest. ANS: T PTS: 1 2. An investment is the

3.3-Measures of Variation

3.3-Measures of Variation Variation: Variation is a measure of the spread or dispersion of a set of data from its center. Common methods of measuring variation include: 1. Range. Standard Deviation 3.

3.3-Measures of Variation Variation: Variation is a measure of the spread or dispersion of a set of data from its center. Common methods of measuring variation include: 1. Range. Standard Deviation 3.

Statistics vs. statistics

Statistics vs. statistics Question: What is Statistics (with a capital S)? Definition: Statistics is the science of collecting, organizing, summarizing and interpreting data. Note: There are 2 main ways

Statistics vs. statistics Question: What is Statistics (with a capital S)? Definition: Statistics is the science of collecting, organizing, summarizing and interpreting data. Note: There are 2 main ways

Chapter 3. Numerical Descriptive Measures. Copyright 2016 Pearson Education, Ltd. Chapter 3, Slide 1

Chapter 3 Numerical Descriptive Measures Copyright 2016 Pearson Education, Ltd. Chapter 3, Slide 1 Objectives In this chapter, you learn to: Describe the properties of central tendency, variation, and

Chapter 3 Numerical Descriptive Measures Copyright 2016 Pearson Education, Ltd. Chapter 3, Slide 1 Objectives In this chapter, you learn to: Describe the properties of central tendency, variation, and

Foundations of Finance. Lecture 8: Portfolio Management-2 Risky Assets and a Riskless Asset.

Lecture 8: Portfolio Management-2 Risky Assets and a Riskless Asset. I. Reading. A. BKM, Chapter 8: read Sections 8.1 to 8.3. II. Standard Deviation of Portfolio Return: Two Risky Assets. A. Formula: σ

Lecture 8: Portfolio Management-2 Risky Assets and a Riskless Asset. I. Reading. A. BKM, Chapter 8: read Sections 8.1 to 8.3. II. Standard Deviation of Portfolio Return: Two Risky Assets. A. Formula: σ

EG, Ch. 12: International Diversification

1 EG, Ch. 12: International Diversification I. Overview. International Diversification: A. Reduces Risk. B. Increases or Decreases Expected Return? C. Performance is affected by Exchange Rates. D. How

1 EG, Ch. 12: International Diversification I. Overview. International Diversification: A. Reduces Risk. B. Increases or Decreases Expected Return? C. Performance is affected by Exchange Rates. D. How

B6302 Sample Placement Exam Academic Year

Revised June 011 B630 Sample Placement Exam Academic Year 011-01 Part 1: Multiple Choice Question 1 Consider the following information on three mutual funds (all information is in annualized units). Fund

Revised June 011 B630 Sample Placement Exam Academic Year 011-01 Part 1: Multiple Choice Question 1 Consider the following information on three mutual funds (all information is in annualized units). Fund

05/05/2011. Degree of Risk. Degree of Risk. BUSA 4800/4810 May 5, Uncertainty

BUSA 4800/4810 May 5, 2011 Uncertainty We must believe in luck. For how else can we explain the success of those we don t like? Jean Cocteau Degree of Risk We incorporate risk and uncertainty into our

BUSA 4800/4810 May 5, 2011 Uncertainty We must believe in luck. For how else can we explain the success of those we don t like? Jean Cocteau Degree of Risk We incorporate risk and uncertainty into our

FNCE 4030 Fall 2012 Roberto Caccia, Ph.D. Midterm_2a (2-Nov-2012) Your name:

Your name:") Answer the questions in the space below. Written answers require no more than few compact sentences to show you understood and master the concept. Show your work to receive partial credit. Points are as

Answer the questions in the space below. Written answers require no more than few compact sentences to show you understood and master the concept. Show your work to receive partial credit. Points are as

Final Exam Suggested Solutions

University of Washington Fall 003 Department of Economics Eric Zivot Economics 483 Final Exam Suggested Solutions This is a closed book and closed note exam. However, you are allowed one page of handwritten

University of Washington Fall 003 Department of Economics Eric Zivot Economics 483 Final Exam Suggested Solutions This is a closed book and closed note exam. However, you are allowed one page of handwritten

Introduction To Risk & Return

Calculating the Rate of Return on Assets Introduction o Risk & Return Econ 422: Investment, Capital & Finance University of Washington Summer 26 August 5, 26 Denote today as time the price of the asset

Calculating the Rate of Return on Assets Introduction o Risk & Return Econ 422: Investment, Capital & Finance University of Washington Summer 26 August 5, 26 Denote today as time the price of the asset

Stock Prices and the Stock Market

Stock Prices and the Stock Market ECON 40364: Monetary Theory & Policy Eric Sims University of Notre Dame Fall 2017 1 / 47 Readings Text: Mishkin Ch. 7 2 / 47 Stock Market The stock market is the subject

Stock Prices and the Stock Market ECON 40364: Monetary Theory & Policy Eric Sims University of Notre Dame Fall 2017 1 / 47 Readings Text: Mishkin Ch. 7 2 / 47 Stock Market The stock market is the subject

Behavioral Finance 1-1. Chapter 2 Asset Pricing, Market Efficiency and Agency Relationships

Behavioral Finance 1-1 Chapter 2 Asset Pricing, Market Efficiency and Agency Relationships 1 The Pricing of Risk 1-2 The expected utility theory : maximizing the expected utility across possible states

Behavioral Finance 1-1 Chapter 2 Asset Pricing, Market Efficiency and Agency Relationships 1 The Pricing of Risk 1-2 The expected utility theory : maximizing the expected utility across possible states

Chapter 3 Descriptive Statistics: Numerical Measures Part A

Slides Prepared by JOHN S. LOUCKS St. Edward s University Slide 1 Chapter 3 Descriptive Statistics: Numerical Measures Part A Measures of Location Measures of Variability Slide Measures of Location Mean

Slides Prepared by JOHN S. LOUCKS St. Edward s University Slide 1 Chapter 3 Descriptive Statistics: Numerical Measures Part A Measures of Location Measures of Variability Slide Measures of Location Mean

Foundations of Finance

Lecture 5: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Individual Assets in a CAPM World. VI. Intuition for the SML (E[R p ] depending

Lecture 5: CAPM. I. Reading II. Market Portfolio. III. CAPM World: Assumptions. IV. Portfolio Choice in a CAPM World. V. Individual Assets in a CAPM World. VI. Intuition for the SML (E[R p ] depending

Overview of Concepts and Notation

Overview of Concepts and Notation (BUSFIN 4221: Investments) - Fall 2016 1 Main Concepts This section provides a list of questions you should be able to answer. The main concepts you need to know are embedded

Overview of Concepts and Notation (BUSFIN 4221: Investments) - Fall 2016 1 Main Concepts This section provides a list of questions you should be able to answer. The main concepts you need to know are embedded

Asset Pricing Model 2

Outline Note 6 Return, Risk, and the Capital Risk Aversion Portfolio Returns and Risk Portfolio and Diversification Systematic Risk: Beta (β) The Capital Asset Pricing Model and the Security Market Line

Outline Note 6 Return, Risk, and the Capital Risk Aversion Portfolio Returns and Risk Portfolio and Diversification Systematic Risk: Beta (β) The Capital Asset Pricing Model and the Security Market Line

Monetary Economics Risk and Return, Part 2. Gerald P. Dwyer Fall 2015

Monetary Economics Risk and Return, Part 2 Gerald P. Dwyer Fall 2015 Reading Malkiel, Part 2, Part 3 Malkiel, Part 3 Outline Returns and risk Overall market risk reduced over longer periods Individual

Monetary Economics Risk and Return, Part 2 Gerald P. Dwyer Fall 2015 Reading Malkiel, Part 2, Part 3 Malkiel, Part 3 Outline Returns and risk Overall market risk reduced over longer periods Individual

Chapter 8. Portfolio Selection. Learning Objectives. INVESTMENTS: Analysis and Management Second Canadian Edition

INVESTMENTS: Analysis and Management Second Canadian Edition W. Sean Cleary Charles P. Jones Chapter 8 Portfolio Selection Learning Objectives State three steps involved in building a portfolio. Apply

INVESTMENTS: Analysis and Management Second Canadian Edition W. Sean Cleary Charles P. Jones Chapter 8 Portfolio Selection Learning Objectives State three steps involved in building a portfolio. Apply

Portfolio Diversification and Performance

Portfolio Diversification and Performance Not Complete Without Accompanying Disclosures 2015 Morningstar Investment Services, Inc. All rights reserved. The Morningstar name and logo are registered marks

Portfolio Diversification and Performance Not Complete Without Accompanying Disclosures 2015 Morningstar Investment Services, Inc. All rights reserved. The Morningstar name and logo are registered marks

Chapter 13 Return, Risk, and the Security Market Line

T13.1 Chapter Outline Chapter Organization Chapter 13 Return, Risk, and the Security Market Line! 13.1 Expected Returns and Variances! 13.2 Portfolios! 13.3 Announcements, Surprises, and Expected Returns!

T13.1 Chapter Outline Chapter Organization Chapter 13 Return, Risk, and the Security Market Line! 13.1 Expected Returns and Variances! 13.2 Portfolios! 13.3 Announcements, Surprises, and Expected Returns!

Week 1 Quantitative Analysis of Financial Markets Basic Statistics A

Week 1 Quantitative Analysis of Financial Markets Basic Statistics A Christopher Ting http://www.mysmu.edu/faculty/christophert/ Christopher Ting : christopherting@smu.edu.sg : 6828 0364 : LKCSB 5036 October

Week 1 Quantitative Analysis of Financial Markets Basic Statistics A Christopher Ting http://www.mysmu.edu/faculty/christophert/ Christopher Ting : christopherting@smu.edu.sg : 6828 0364 : LKCSB 5036 October

Lecture #2. YTM / YTC / YTW IRR concept VOLATILITY Vs RETURN Relationship. Risk Premium over the Standard Deviation of portfolio excess return

REVIEW Lecture #2 YTM / YTC / YTW IRR concept VOLATILITY Vs RETURN Relationship Sharpe Ratio: Risk Premium over the Standard Deviation of portfolio excess return (E(r p) r f ) / σ 8% / 20% = 0.4x. A higher

REVIEW Lecture #2 YTM / YTC / YTW IRR concept VOLATILITY Vs RETURN Relationship Sharpe Ratio: Risk Premium over the Standard Deviation of portfolio excess return (E(r p) r f ) / σ 8% / 20% = 0.4x. A higher

Capital Budgeting in Global Markets

Capital Budgeting in Global Markets Fall 2013 Stephen Sapp Yes, our chief analyst is recommending further investments in the new year. 1 Introduction Capital budgeting is the process of determining which

Capital Budgeting in Global Markets Fall 2013 Stephen Sapp Yes, our chief analyst is recommending further investments in the new year. 1 Introduction Capital budgeting is the process of determining which

Sessions 11 and 12: Capital Budgeting and Risk

6049 Lecture Slides, Academic Year 2010/2011 Sessions 11 and 12: Capital Budgeting and Risk Hannes Wagner 6049-1- 1 Topics Covered Cost of capital for projects and firms Measuring the cost of equity Setting

6049 Lecture Slides, Academic Year 2010/2011 Sessions 11 and 12: Capital Budgeting and Risk Hannes Wagner 6049-1- 1 Topics Covered Cost of capital for projects and firms Measuring the cost of equity Setting

Week 2 Quantitative Analysis of Financial Markets Hypothesis Testing and Confidence Intervals

Week 2 Quantitative Analysis of Financial Markets Hypothesis Testing and Confidence Intervals Christopher Ting http://www.mysmu.edu/faculty/christophert/ Christopher Ting : christopherting@smu.edu.sg :

Week 2 Quantitative Analysis of Financial Markets Hypothesis Testing and Confidence Intervals Christopher Ting http://www.mysmu.edu/faculty/christophert/ Christopher Ting : christopherting@smu.edu.sg :

PowerPoint. to accompany. Chapter 11. Systematic Risk and the Equity Risk Premium

PowerPoint to accompany Chapter 11 Systematic Risk and the Equity Risk Premium 11.1 The Expected Return of a Portfolio While for large portfolios investors should expect to experience higher returns for

PowerPoint to accompany Chapter 11 Systematic Risk and the Equity Risk Premium 11.1 The Expected Return of a Portfolio While for large portfolios investors should expect to experience higher returns for

J B GUPTA CLASSES , Copyright: Dr JB Gupta. Chapter 4 RISK AND RETURN.

J B GUPTA CLASSES 98184931932, drjaibhagwan@gmail.com, www.jbguptaclasses.com Copyright: Dr JB Gupta Chapter 4 RISK AND RETURN Chapter Index Systematic and Unsystematic Risk Capital Asset Pricing Model

J B GUPTA CLASSES 98184931932, drjaibhagwan@gmail.com, www.jbguptaclasses.com Copyright: Dr JB Gupta Chapter 4 RISK AND RETURN Chapter Index Systematic and Unsystematic Risk Capital Asset Pricing Model