***************************** SAMPLE PAGES FROM TUTORIAL GUIDE *****************************

|

|

|

- Carmel Stevens

- 6 years ago

- Views:

Transcription

1 DCF Modeling Copyright 2008 by Wall Street Prep, Inc.

2 Table of contents SECTION 1: OVERVIEW DCF in theory and in practice Unlevered vs. levered DCF SECTION 2: MODELING THE DCF Modeling unlevered free cash flows Discounting to reflect stub year and mid-year adjustment Terminal value using growth in perpetuity approach Terminal value using exit multiple approach Calculating net debt Shares outstanding using the treasury stock method Modeling the weighted average cost of capital (WACC) Sensitivity analysis using data tables Modeling synergies

3 DCF in theory and in practice DCF in theory The DCF valuation approach is based upon the theory that the value of a business is the sum of its expected future free cash flows, discounted at an appropriate rate. Discounted cash flow (DCF) analysis is one of the most fundamental, commonly-used valuation methodologies. It is a valuation method developed and supported in academia and also widely used in applied business practices. DCF in practice There is no consensus on implementation controversies predominantly over the estimation of the cost of equity. Extremely sensitive to changes in operating, exit and discount rate assumptions. That said, there are general rules of thumb that guide implementation. Two-stage DCF model is prevalent form The prevalent form of the DCF model in practice is the two-stage DCF model. Stage 1 is an explicit projection of free cash flows generally for 5-10 years. Stage 2 is a lump-sum estimate of the cash flows beyond the explicit forecast period. In addition to the two-stage DCF, there are multi-stage manifestations of the DCF model (3-stage, high-low models, etc.) designed to more clearly identify cash flows generated at different phases in a firm s life cycle. We will focus on the two-stage model in this course, given its prevalence in practice. 3

4 DCF in theory and in practice Two-stage DCF model Stage 1: Free cash flow projections What is the projected operating and financial performance of the business? Typical projection period is 5-10 years How do we calculate free cash flows Value t = t=n t=1 FCF t (1 + r) t Stage 2: Terminal value We cannot reasonably project cash flows beyond a certain point. As such, we make simplifying assumptions about cash flows after the explicit projection period to estimate a terminal value that represents the present value of all the free cash flows generated by the company after the explicit forecast period. Analysts use both the perpetual growth and exit multiple methods to estimate terminal value Discount rate Both stages should be discounted to the present using a rate that appropriately reflects the cost of capital (much more on this later) Value t = Value t = FCF t+1 r g Exit EBITDA x multiple 4

5 Modeling unlevered free cash flows Unleveled free cash flows must be projected and then appropriately discounted to determine a present value of the company under analysis. Since firms do not report this figure of free cash flows, analysts must make adjustments to information provided in the reported financial statements. Start with EBIT The typical starting point for calculating unlevered free cash flows is operating income (operating profit before interest and taxes, or EBIT) reported on the income statement. 5

6 Modeling unlevered free cash flows Arriving at unlevered free cash flows from EBIT: Free cash flow calculation Historical Projections EBIT (Operating income) EBIT (1 tax rate) (Tax-effected EBIT, EBIAT or NOPAT) Income Statement (10-K / 10-Q / PR / Company) Use normalized EBIT Use effective tax rate Analyst research Company Internal projections Use marginal tax rate Plus: Depreciation and amortization Less: Increases in working capital assets 2 CFS / IS / Footnotes Analyst research Company Plus: Increases in working capital liabilities Internal projections Less: Increases in deferred tax assets Plus: Increases in deferred tax liabilities Less: Capital expenditures Less: Other required investments Equals: Unlevered free cash flows Footnote calculating levered free cash flows When valuing financial institutions, levered FCFs are projected to arrive at equity value directly. Projected income and cash flow streams are after interest expense and net of any interest income: Net income - Increases in working capital +/- Deferred taxes + D&A - Capital expenditures +/- Net borrowing Levered FCF 6

7 Modeling unlevered free cash flows Always remember to: Footnote assumptions in detail Test your assumptions Use consistent cash flows and costs of capital Reference from core model Input WACC of 10% for now. We will calculate wacc shortly. Calculation = days post-deal date / 365 7

8 Discounting to reflect stub year and mid-year adjustment Discount free cash flows back to the present 8

9 Terminal value using growth in perpetuity approach Mid-year adjustment The mid-year adjustment also applies to the growth in perpetuity formula, which otherwise assumes all future cash flows are generated at year-end. 9

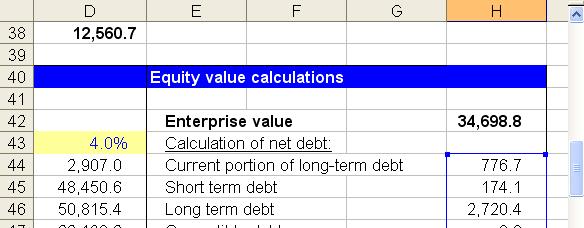

10 Calculating net debt From enterprise value to equity value Now that we calculated enterprise value (read the DCF value of operations), our focus shifts to calculating equity value. Add non-operating assets First, all non-operating assets (typically excess cash and other investments) must be added to the enterprise value. Why? Understand that we just calculated expected cash flows generated from the operating assets of the business the cash flows related to non-operating assets (i.e. interest income) were not reflected in the FCF calculation. Instead the book value of these assets (as identified on the most recent 10-K or 10-Q) is typically used as a proxy for the intrinsic value of these assets (the book value of cash is, after all, typically the market value of cash, right?) Subtract non-equity claims Next, all non-equity claims (debt and equivalents) must be subtracted to identify what the equity in the business is. Include all non-equity claims on the business that have not been accounted for in the calculation of FCF. Common items are debt, preferred stock, minority interests, leases. Use the book values of these items as proxies for the market value unless instructed otherwise. Net Debt is defined as: Short-Term Debt + Current Portion of LT Debt + Long-Term Debt + Minority Interest + Preferred Stock + Leases (Cash + Investments) Net Debt Net Debt Equity Value 10

11 Calculating net debt 11

12 Shares outstanding using the treasury stock method Total $ proceeds In-the-$ shares x avg. strike price Calculate option proceeds using the SUMPRODUCT function Total shares repurchased Proceeds / current share price 12

13 Modeling the weighted average cost of capital (WACC) 13

14 Modeling the weighted average cost of capital (WACC) 14

15 Modeling the weighted average cost of capital (WACC) 15

16 Modeling the weighted average cost of capital (WACC) Now we can relever the weighted average industry beta 16

17 Modeling the weighted average cost of capital (WACC) and calculate the cost of equity 17

18 Modeling the weighted average cost of capital (WACC) and the weighted average cost of capital 18

19 Modeling synergies 19

20 Terms of Use All materials included in Wall StreetPrep s Self Study Program including Step-by-step Tutorial Guide, Wall StreetPrep s proprietary portfolio of financial models, supplementary notes, are not to be duplicated, copied, disseminated or distributed without the expressed, written permission of Wall StreetPrep, Inc. The Self Study Program as well as case studies used during live classes are designed for illustrative purposes only and does not, in any way, constitute and investment thesis or recommendation. Copyright 2008 Wall StreetPrep, Inc. All rights reserved. "Wall StreetPrep", "Wall Street Prep", "The EDGE Self Study Program", and various marks are trademarks of Wall Street Prep, Inc.

Sample Questions and Solutions

Sample Questions and Solutions Public Comparables Question Facts for Company XYZ: Closing stock price is $18.00 1,000 shares outstanding, and 100 outstanding options outstanding with an average exercise

Sample Questions and Solutions Public Comparables Question Facts for Company XYZ: Closing stock price is $18.00 1,000 shares outstanding, and 100 outstanding options outstanding with an average exercise

OFFICE OF CAREER SERVICES INTERVIEWS FINANCIAL MODELING

OFFICE OF CAREER SERVICES INTERVIEWS FINANCIAL MODELING Basic valuation concepts are among the most popular technical tasks you will be asked to discuss in investment banking and other finance interviews.

OFFICE OF CAREER SERVICES INTERVIEWS FINANCIAL MODELING Basic valuation concepts are among the most popular technical tasks you will be asked to discuss in investment banking and other finance interviews.

I m going to cover 6 key points about FCF here:

Free Cash Flow Overview When you re valuing a company with a DCF analysis, you need to calculate their Free Cash Flow (FCF) to figure out what they re worth. While Free Cash Flow is simple in theory, in

Free Cash Flow Overview When you re valuing a company with a DCF analysis, you need to calculate their Free Cash Flow (FCF) to figure out what they re worth. While Free Cash Flow is simple in theory, in

Financial Modeling Fundamentals Module 08 Discounted Cash Flow (DCF) Analysis Quiz Questions

Analysis Quiz Questions") Financial Modeling Fundamentals Module 08 Discounted Cash Flow (DCF) Analysis Quiz Questions 1. How much would you be willing to pay for a company that generates exactly $100 in Free Cash Flow into eternity?

Financial Modeling Fundamentals Module 08 Discounted Cash Flow (DCF) Analysis Quiz Questions 1. How much would you be willing to pay for a company that generates exactly $100 in Free Cash Flow into eternity?

Discounted Cash Flow Analysis Deliverable #6 Sales Gross Profit / Margin

Discounted Cash Flow Analysis Deliverable #6 The discounted cash flow methodology derives the value of a company by calculating the present value of all future projected cash flows. Unlike comparable companies

Discounted Cash Flow Analysis Deliverable #6 The discounted cash flow methodology derives the value of a company by calculating the present value of all future projected cash flows. Unlike comparable companies

Practice Final Exam. Before you do anything else, write your name at the top of every page of the exam.

FOSTER SCHOOL OF BUSINESS FINANCE 350 Business Finance PROF. RAN DUCHIN Practice Final Exam Before you do anything else, write your name at the top of every page of the exam. This exam is worth 35% of

FOSTER SCHOOL OF BUSINESS FINANCE 350 Business Finance PROF. RAN DUCHIN Practice Final Exam Before you do anything else, write your name at the top of every page of the exam. This exam is worth 35% of

Revenues are forecast to be $100 million each year for the next 10 years, beginning next year.

Problem 1: DCF (35 points) Bauer Industries is an automobile manufacturer. Management is currently evaluating a proposal to build a plant that will manufacture lightweight trucks. The proposal contains

Problem 1: DCF (35 points) Bauer Industries is an automobile manufacturer. Management is currently evaluating a proposal to build a plant that will manufacture lightweight trucks. The proposal contains

Market vs Intrinsic Value

Market vs Intrinsic Value Market Value Determined by the consensus of market participants Observed in the market Intrinsic value Present value of expected future cash flows Not observed Estimated using

Market vs Intrinsic Value Market Value Determined by the consensus of market participants Observed in the market Intrinsic value Present value of expected future cash flows Not observed Estimated using

Introduction to Valuation Frameworks. Lecture #2

Introduction to Valuation Frameworks Lecture #2 Approaches to Valuation Income-Based: Value equals the discounted present value of future cash flows Market-Based: Value equals the price on which buyers

Introduction to Valuation Frameworks Lecture #2 Approaches to Valuation Income-Based: Value equals the discounted present value of future cash flows Market-Based: Value equals the price on which buyers

Finance Recruiting Interview Preparation

Finance Recruiting Interview Preparation Discounted Cash Flows Session #3 This presentation is for informational purposes only, and is not an offer to buy or sell or a solicitation to buy or sell any securities,

Finance Recruiting Interview Preparation Discounted Cash Flows Session #3 This presentation is for informational purposes only, and is not an offer to buy or sell or a solicitation to buy or sell any securities,

Finance and Accounting for Interviews

This document was developed and written by Ian Lee. All information is meant for public use and purposed for the free transfer of knowledge to interested parties. Send questions and comments to ianlee@uclalumni.net

This document was developed and written by Ian Lee. All information is meant for public use and purposed for the free transfer of knowledge to interested parties. Send questions and comments to ianlee@uclalumni.net

Calgon Carbon Corporation 6/25/2013 Comparables Analysis USD Millions

Comparables Analysis USD Millions Operating Statistics Enterprise Debt to 5 Yr LTM LTM LTM LTM Company Name Ticker Stock Price Market Cap Net Debt Value Capital Beta GM % NI % EBIT % EBITDA % Cabot Corp.

Comparables Analysis USD Millions Operating Statistics Enterprise Debt to 5 Yr LTM LTM LTM LTM Company Name Ticker Stock Price Market Cap Net Debt Value Capital Beta GM % NI % EBIT % EBITDA % Cabot Corp.

Glossary of Business Valuation Terms

Adjusted Net Assets Method Asset-Based Approach Beta Blockage Discount Business Business Risk Business Valuation Capital Asset Pricing Model (CAPM) Capitalization Capitalization of Earnings Method Capital

Adjusted Net Assets Method Asset-Based Approach Beta Blockage Discount Business Business Risk Business Valuation Capital Asset Pricing Model (CAPM) Capitalization Capitalization of Earnings Method Capital

Valuation: Fundamental Analysis

Valuation: Fundamental Analysis Equity Valuation Models Fundamental analysis models a company s value by assessing its current and future profitability. The purpose of fundamental analysis is to identify

Valuation: Fundamental Analysis Equity Valuation Models Fundamental analysis models a company s value by assessing its current and future profitability. The purpose of fundamental analysis is to identify

Investment Knowledge Series. Valuation

Investment Knowledge Series Valuation INVESTMENT KNOWLEDGE SERIES Valuation capital city training & consulting www.capitalcitytraining.com i Published 2011 by Capital City Training Ltd ISBN: 978-0-9569238-1-3

Investment Knowledge Series Valuation INVESTMENT KNOWLEDGE SERIES Valuation capital city training & consulting www.capitalcitytraining.com i Published 2011 by Capital City Training Ltd ISBN: 978-0-9569238-1-3

Valuation of Warrants

Valuation of Warrants November 9, 2012 Situation Overview ($ in millions) Liberty Media announced that it is spinning off its Starz LLC ( Starz ) business into a new public company through a tax free distribution

Valuation of Warrants November 9, 2012 Situation Overview ($ in millions) Liberty Media announced that it is spinning off its Starz LLC ( Starz ) business into a new public company through a tax free distribution

The Rocky Mountain Beer: It s All Tapped Out.

Brent Ozenbaugh bozenbau@mail.smu.edu Jennifer Pray jenniferpray@yahoo.com Meredith Price mprice@mail.smu.edu Lindsey Price lcprice1@aol.com Financial Summary (In Millions except for per share data) Price:

Brent Ozenbaugh bozenbau@mail.smu.edu Jennifer Pray jenniferpray@yahoo.com Meredith Price mprice@mail.smu.edu Lindsey Price lcprice1@aol.com Financial Summary (In Millions except for per share data) Price:

CAPITAL STRUCTURE AND VALUE

UV3929 Rev. Jun. 30, 2011 CAPITAL STRUCTURE AND VALUE The underlying principle of valuation is that the discount rate must match the risk of the cash flows being valued. Furthermore, when we include the

UV3929 Rev. Jun. 30, 2011 CAPITAL STRUCTURE AND VALUE The underlying principle of valuation is that the discount rate must match the risk of the cash flows being valued. Furthermore, when we include the

Methods and procedures for company valuations in practice

Methods and procedures for company valuations in practice Methods and procedures for company valuation in practice The valuation of a company is an extremely challenging task. The following article gives

Methods and procedures for company valuations in practice Methods and procedures for company valuation in practice The valuation of a company is an extremely challenging task. The following article gives

Financial Modeling Fundamentals Module 06 Equity Value, Enterprise Value, and Valuation Multiples Quiz Questions

Financial Modeling Fundamentals Module 06 Equity Value, Enterprise Value, and Valuation Multiples Quiz Questions 1. Which of the following statements represent the official differences between Equity Value

Financial Modeling Fundamentals Module 06 Equity Value, Enterprise Value, and Valuation Multiples Quiz Questions 1. Which of the following statements represent the official differences between Equity Value

Financial & Valuation Modeling Boot Camp

TARGET AUDIENCE Overview 3-day intensive training program where trainees learn financial & valuation modeling in Excel using in a hands-on, case-study approach. The modeling methodologies covered include:

TARGET AUDIENCE Overview 3-day intensive training program where trainees learn financial & valuation modeling in Excel using in a hands-on, case-study approach. The modeling methodologies covered include:

CORPORATE VALUATION METHODOLOGIES

CORPORATE VALUATION METHODOLOGIES What is the business worth? Although a simple question, determining the value of any business in today s economy requires a sophisticated understanding of financial analysis

CORPORATE VALUATION METHODOLOGIES What is the business worth? Although a simple question, determining the value of any business in today s economy requires a sophisticated understanding of financial analysis

Chapter 1: Comparable Companies Analysis

Chapter 1: Comparable Companies Analysis 1) All of the following are reasons why comparable companies analysis should be used in conjunction with other valuation methodologies EXCEPT: I. Markets may be

Chapter 1: Comparable Companies Analysis 1) All of the following are reasons why comparable companies analysis should be used in conjunction with other valuation methodologies EXCEPT: I. Markets may be

Valuation Methods and Discount Rate Issues: A Comprehensive Example

9-205-116 REV: NOVEMBER 1, 2006 MARC BERTONECHE FAUSTO FEDERICI Valuation Methods and Discount Rate Issues: A Comprehensive Example The objective of this note is to present a comprehensive review of valuation

9-205-116 REV: NOVEMBER 1, 2006 MARC BERTONECHE FAUSTO FEDERICI Valuation Methods and Discount Rate Issues: A Comprehensive Example The objective of this note is to present a comprehensive review of valuation

Entrepreneurship and ventures finance. Venture evaluation (1): Basic models. Prof. Antonio Renzi

: Basic models. Prof. Antonio Renzi") Entrepreneurship and ventures finance Venture evaluation (1): Basic models Prof. Antonio Renzi Agenda Value and prices New business and intangibles The DCF approach The APV (Adusted Present Value) method

Entrepreneurship and ventures finance Venture evaluation (1): Basic models Prof. Antonio Renzi Agenda Value and prices New business and intangibles The DCF approach The APV (Adusted Present Value) method

2014 E 2015 E 2016 E 2017 E

Equity Research 4 December 2014 Interpump Group Hydraulics M&A may power growth Rating BUY Target price EUR13 Interpump is up 25% since the beginning of the year, bolstered by strong interim results and

Equity Research 4 December 2014 Interpump Group Hydraulics M&A may power growth Rating BUY Target price EUR13 Interpump is up 25% since the beginning of the year, bolstered by strong interim results and

Created by Stefan Momic for UTEFA. UTEFA Learning Session #2 Valuation September 27, 2018

UTEFA Learning Session #2 Valuation September 27, 2018 Agenda Introduction to Valuation Relative Valuation Intrinsic Valuation Discounted Cash Flow Analysis Valuation Trade-Offs Introduction to Valuation

UTEFA Learning Session #2 Valuation September 27, 2018 Agenda Introduction to Valuation Relative Valuation Intrinsic Valuation Discounted Cash Flow Analysis Valuation Trade-Offs Introduction to Valuation

Estimating Cash Flows

Estimating Cash Flows From accounts to cashflow Assets Liabilities Existing investments Generate cash flows today include long-lived (fixed) and short-lived (wc) assets Assets in Place Debt Fixed claim

Estimating Cash Flows From accounts to cashflow Assets Liabilities Existing investments Generate cash flows today include long-lived (fixed) and short-lived (wc) assets Assets in Place Debt Fixed claim

Frameworks for Valuation

8 Frameworks for Valuation In Part One, we built a conceptual framework to show what drives the creation of value. A company s value stems from its ability to earn a healthy return on invested capital

8 Frameworks for Valuation In Part One, we built a conceptual framework to show what drives the creation of value. A company s value stems from its ability to earn a healthy return on invested capital

The Art and Science of Valuing Oilfield Equipment and Service Companies

The Art and Science of Valuing Oilfield Equipment and Service Companies In the first of a series of white papers, Founders Investment Banking will address valuation in the context of oilfield equipment

The Art and Science of Valuing Oilfield Equipment and Service Companies In the first of a series of white papers, Founders Investment Banking will address valuation in the context of oilfield equipment

Industry: CABLE TV August 7, 2013 Recommendation: BUY. Company Overview

Price Target $74.09 Price (08/07/2013) $61.11 52-WK ($) 47.71-67.85 Market Cap ($M) $34,000 Outstanding Shares 556 Insider % 7.0 Revenue $30,750 Valuation TEV ($M) $50,590 EBITDA ($M) $7,480 EV/EBITDA

Price Target $74.09 Price (08/07/2013) $61.11 52-WK ($) 47.71-67.85 Market Cap ($M) $34,000 Outstanding Shares 556 Insider % 7.0 Revenue $30,750 Valuation TEV ($M) $50,590 EBITDA ($M) $7,480 EV/EBITDA

Lesson 10 THE MERGERS AND ACQUISITION MARKET. AN OVERVIEW. INTRODUCTION TO COMPANY S VALUE AND VALUATION TECHNIQUES. DCF AND COMPARABLES

Lesson 10 THE MERGERS AND ACQUISITION MARKET. AN OVERVIEW. INTRODUCTION TO COMPANY S VALUE AND VALUATION TECHNIQUES. DCF AND COMPARABLES Internal growth vs. External growth Internal growth investments

Lesson 10 THE MERGERS AND ACQUISITION MARKET. AN OVERVIEW. INTRODUCTION TO COMPANY S VALUE AND VALUATION TECHNIQUES. DCF AND COMPARABLES Internal growth vs. External growth Internal growth investments

Taxes. Financial Statements: Things to Keep in Mind. Cash Flow and Taxes. BUSI 7110/7116 Yost

Cash Flow and Taxes Financial Statements: Things to Keep in Mind Backward vs. Forward Looking Book Values vs. Market Values Accounting Numbers vs. Cash Flows Tax Deductible vs. Taxable Notes to Financial

Cash Flow and Taxes Financial Statements: Things to Keep in Mind Backward vs. Forward Looking Book Values vs. Market Values Accounting Numbers vs. Cash Flows Tax Deductible vs. Taxable Notes to Financial

FN428 : Investment Banking. Lecture 23 : Revision class

FN428 : Investment Banking Lecture 23 : Revision class Recap : Theory of Financial Intermediary An overview of Investment Banking Investment Bank vs. Commercial Bank Which are the various divisions of

FN428 : Investment Banking Lecture 23 : Revision class Recap : Theory of Financial Intermediary An overview of Investment Banking Investment Bank vs. Commercial Bank Which are the various divisions of

COMPANY SNAPSHOT 08/26/2010 Last Closing Stock Price as of 08/25/2010: $10.22

Last Closing Stock Price as of 08/25/2010: $10.22 Company Snapshot This report presents a concise review of our DCF valuation and economic profitability analysis from our MaxVal model. Contributors Equity

Last Closing Stock Price as of 08/25/2010: $10.22 Company Snapshot This report presents a concise review of our DCF valuation and economic profitability analysis from our MaxVal model. Contributors Equity

Oil & Gas Modeling: Quiz Questions Module 3 Valuation and Simplified NAV Model

Oil & Gas Modeling: Quiz Questions Module 3 Valuation and Simplified NAV Model 1. Some people argue that you SHOULD factor in the Net Value of Derivatives used for commodity price hedging when calculating

Oil & Gas Modeling: Quiz Questions Module 3 Valuation and Simplified NAV Model 1. Some people argue that you SHOULD factor in the Net Value of Derivatives used for commodity price hedging when calculating

THE ABC's OF VALUATION

THE ABC's OF VALUATION VALUATION OF COMPANIES AND THEIR SECURITIES FOR ESOP PURPOSES: METHODS OF VALUATION Prepared for the Annual Conference of the Ohio Employee Ownership Center April 20, 2007 BUSINESS

THE ABC's OF VALUATION VALUATION OF COMPANIES AND THEIR SECURITIES FOR ESOP PURPOSES: METHODS OF VALUATION Prepared for the Annual Conference of the Ohio Employee Ownership Center April 20, 2007 BUSINESS

IBP Exam Topics Table of Contents

Table of Contents Accounting...2 Income statement...2 Balance sheet...2 Cash flow statement...2 Financial statement analysis...3 Financial reporting...3 Advanced Accounting...3 Excel...3 PowerPoint...3

Table of Contents Accounting...2 Income statement...2 Balance sheet...2 Cash flow statement...2 Financial statement analysis...3 Financial reporting...3 Advanced Accounting...3 Excel...3 PowerPoint...3

Valuation Principles

Valuation Principles The ACG Cup January 20, 2016 36 East 7 th Street Suite 2400 Cincinnati, OH 45202 513.327.2171 www.comstockadvisors.com Nickolas N. Sypniewski nsypniewski@comstockadvisors.com www.comstockadvisors.com

Valuation Principles The ACG Cup January 20, 2016 36 East 7 th Street Suite 2400 Cincinnati, OH 45202 513.327.2171 www.comstockadvisors.com Nickolas N. Sypniewski nsypniewski@comstockadvisors.com www.comstockadvisors.com

Improved Decision Making Under Uncertainty: Incorporating a Monte Carlo Simulation into a Discounted Cash Flow Valuation for Equities.

Improved Decision Making Under Uncertainty: Incorporating a Monte Carlo Simulation into a Discounted Cash Flow Valuation for Equities Jack Nurminen Bachelor s Thesis Degree Programme in Finance and Economics

Improved Decision Making Under Uncertainty: Incorporating a Monte Carlo Simulation into a Discounted Cash Flow Valuation for Equities Jack Nurminen Bachelor s Thesis Degree Programme in Finance and Economics

Fahmi Ben Abdelkader 5/1/ :34 PM 1. Walking Through From Earnings to Cash Flows. Accrual-based Versus Cash-Flow-based performance measures

Financial Statement Analysis Section 5. The analytical Cash Flow Statement Accrual-based Versus Cash-Flow Flow-based performance measures Students version Fahmi Ben Abdelkader 5/1/2017 10:34 PM 1 Cash-flow

Financial Statement Analysis Section 5. The analytical Cash Flow Statement Accrual-based Versus Cash-Flow Flow-based performance measures Students version Fahmi Ben Abdelkader 5/1/2017 10:34 PM 1 Cash-flow

Week 6 Equity Valuation 1

Week 6 Equity Valuation 1 Overview of Valuation The basic assumption of all these valuation models is that the future value of all returns can be discounted back to today s present value. Where t = time

Week 6 Equity Valuation 1 Overview of Valuation The basic assumption of all these valuation models is that the future value of all returns can be discounted back to today s present value. Where t = time

Forecasting Balance Sheets and Cash Flow Statements for DCF Analyses. Joseph Emanuele ASA, CFA, CPA/ABV/CFF October 8, 2017

Forecasting Balance Sheets and Cash Flow Statements for DCF Analyses Joseph Emanuele ASA, CFA, CPA/ABV/CFF October 8, 2017 What we are NOT doing today: We are NOT going to be learning how to prepare prospective

Forecasting Balance Sheets and Cash Flow Statements for DCF Analyses Joseph Emanuele ASA, CFA, CPA/ABV/CFF October 8, 2017 What we are NOT doing today: We are NOT going to be learning how to prepare prospective

Corporate Finance & Risk Management 06 Financial Valuation

Corporate Finance & Risk Management 06 Financial Valuation Christoph Schneider University of Mannheim http://cf.bwl.uni-mannheim.de schneider@uni-mannheim.de Tel: +49 (621) 181-1949 Topics covered After-tax

Corporate Finance & Risk Management 06 Financial Valuation Christoph Schneider University of Mannheim http://cf.bwl.uni-mannheim.de schneider@uni-mannheim.de Tel: +49 (621) 181-1949 Topics covered After-tax

Homework Solutions - Lecture 2

Homework Solutions - Lecture 2 1. The value of the S&P 500 index is 1312.41 and the treasury rate is 1.83%. In a typical year, stock repurchases increase the average payout ratio on S&P 500 stocks to over

Homework Solutions - Lecture 2 1. The value of the S&P 500 index is 1312.41 and the treasury rate is 1.83%. In a typical year, stock repurchases increase the average payout ratio on S&P 500 stocks to over

Discussion Questions

Understanding the Financial Environment of Public Utility Firms Sanford V. Berg Joel F. Houston 1 Overview Our plan is to help facilitate a series of discussions related to utility finance. We will pose

Understanding the Financial Environment of Public Utility Firms Sanford V. Berg Joel F. Houston 1 Overview Our plan is to help facilitate a series of discussions related to utility finance. We will pose

Global ABV Examination

Accredited in Business Valuation Global ABV Examination content specification outline Effective Aug. 1, 2018 i Valuation Principles Examination This document is nonauthoritative and is included for informational

Accredited in Business Valuation Global ABV Examination content specification outline Effective Aug. 1, 2018 i Valuation Principles Examination This document is nonauthoritative and is included for informational

FREE CASH FLOW VALUATION. Presenter Venue Date

FREE CASH FLOW VALUATION Presenter Venue Date FREE CASH FLOW Free Cash Flow to the Firm Free Cash Flow to Equity = Cash flow available to = Cash flow available to Common stockholders Common stockholders

FREE CASH FLOW VALUATION Presenter Venue Date FREE CASH FLOW Free Cash Flow to the Firm Free Cash Flow to Equity = Cash flow available to = Cash flow available to Common stockholders Common stockholders

One of the major applications of Equity Valuation is the Private companies valuation. Private companies valuation can be applied:

One of the major applications of Equity Valuation is the Private companies valuation. Private companies valuation can be applied: To value a Start up operations of Public companies. To estimate a value

One of the major applications of Equity Valuation is the Private companies valuation. Private companies valuation can be applied: To value a Start up operations of Public companies. To estimate a value

MIDTERM EXAM SOLUTIONS

MIDTERM EXAM SOLUTIONS Finance 40610 Security Analysis Mendoza College of Business Professor Shane A. Corwin Fall Semester 2007 Monday, October 15, 2007 INSTRUCTIONS: 1. You have 75 minutes to complete

MIDTERM EXAM SOLUTIONS Finance 40610 Security Analysis Mendoza College of Business Professor Shane A. Corwin Fall Semester 2007 Monday, October 15, 2007 INSTRUCTIONS: 1. You have 75 minutes to complete

CVX Chevron Corporation Sector: Energy SELL

Analysts: Zachary Haller, Andrew Paley Brown and Sean Miller Washburn University Applied Portfolio Management CVX Sector: Energy SELL Report Date: 4/18/2016 Market Cap (mm) $157,566 Annual Dividend $4.28

Analysts: Zachary Haller, Andrew Paley Brown and Sean Miller Washburn University Applied Portfolio Management CVX Sector: Energy SELL Report Date: 4/18/2016 Market Cap (mm) $157,566 Annual Dividend $4.28

Financial Markets Management 183 Economics 173A. Equity Valuation. Updated 5/13/17

Financial Markets Management 183 Economics 173A Equity Valuation Updated 5/13/17 Perspective and Objective 1. Diversification: Risk reduction. 2. Speculation: I ve got a feeling. 3. Long term: Buy & Hold.

Financial Markets Management 183 Economics 173A Equity Valuation Updated 5/13/17 Perspective and Objective 1. Diversification: Risk reduction. 2. Speculation: I ve got a feeling. 3. Long term: Buy & Hold.

Syneos Health, Inc. Investment Research Presentation

Syneos Health, Inc. Investment Research Presentation NasdaqGS: SYNH Month Sector: Day, Healthcare 20XX Senior Analyst: Jose Grullon Junior Analysts: Garbis Chekerdjian, Ignacio Fimbres Spring 2018 1 Valuation

Syneos Health, Inc. Investment Research Presentation NasdaqGS: SYNH Month Sector: Day, Healthcare 20XX Senior Analyst: Jose Grullon Junior Analysts: Garbis Chekerdjian, Ignacio Fimbres Spring 2018 1 Valuation

ISSUES IN VALUATION UNDER FEMA

ISSUES IN VALUATION UNDER FEMA REGIONAL CONFERENCE OF WIRC CA. SUJAL SHAH AUGUST 31, 2012 1 VALUATION - INTRODUCTION What is Valuation? Valuation means assigning a value to underlying assets The value

ISSUES IN VALUATION UNDER FEMA REGIONAL CONFERENCE OF WIRC CA. SUJAL SHAH AUGUST 31, 2012 1 VALUATION - INTRODUCTION What is Valuation? Valuation means assigning a value to underlying assets The value

Advanced Corporate Finance. 3. Capital structure

Advanced Corporate Finance 3. Capital structure Objectives of the session So far, NPV concept and possibility to move from accounting data to cash flows => But necessity to go further regarding the discount

Advanced Corporate Finance 3. Capital structure Objectives of the session So far, NPV concept and possibility to move from accounting data to cash flows => But necessity to go further regarding the discount

web extension 24A FCF t t 1 TS t (1 r su ) t t 1

t t 1") The Adjusted Present Value (APV) Approachl 24A-1 web extension 24A The Adjusted Present Value (APV) Approach The corporate valuation or residual equity methods described in the textbook chapter work well

The Adjusted Present Value (APV) Approachl 24A-1 web extension 24A The Adjusted Present Value (APV) Approach The corporate valuation or residual equity methods described in the textbook chapter work well

Valuation Principles

Valuation Principles The ACG Cup January 16, 2018 36 East 7 th Street Suite 2400 Cincinnati, OH 45202 513.813.4101 www.comstockadvisors.com Nickolas N. Sypniewski nsypniewski@comstockadvisors.com www.comstockadvisors.com

Valuation Principles The ACG Cup January 16, 2018 36 East 7 th Street Suite 2400 Cincinnati, OH 45202 513.813.4101 www.comstockadvisors.com Nickolas N. Sypniewski nsypniewski@comstockadvisors.com www.comstockadvisors.com

International Glossary of Business Valuation Terms

International Glossary of Business Valuation Terms To enhance and sustain the quality of business valuations for the benefit of the profession and its clientele, the below identified societies and organizations

International Glossary of Business Valuation Terms To enhance and sustain the quality of business valuations for the benefit of the profession and its clientele, the below identified societies and organizations

Capital Structure Questions

Capital Structure Questions What do you think? Will the following firm characteristics result in the use of more or less debt? Large firms More tangible assets More lower risk; better access to capital

Capital Structure Questions What do you think? Will the following firm characteristics result in the use of more or less debt? Large firms More tangible assets More lower risk; better access to capital

CHAPTER 19. Valuation and Financial Modeling: A Case Study. Chapter Synopsis

CHAPTER 19 Valuation and Financial Modeling: A Case Study Chapter Synopsis 19.1 Valuation Using Comparables A valuation using comparable publicly traded firm valuation multiples may be used as a preliminary

CHAPTER 19 Valuation and Financial Modeling: A Case Study Chapter Synopsis 19.1 Valuation Using Comparables A valuation using comparable publicly traded firm valuation multiples may be used as a preliminary

ABV Examination Content Specification Outline

ABV Examination Content Specification Outline AICPA ABV Examination Content Specification Outline 1 2017 American Institute of Certified Public Accountants. All rights reserved. AICPA and American Institute

ABV Examination Content Specification Outline AICPA ABV Examination Content Specification Outline 1 2017 American Institute of Certified Public Accountants. All rights reserved. AICPA and American Institute

FIN 350 Business Finance Homework 7 Fall 2014 Solutions

FIN 350 Business Finance Homework 7 Fall 2014 Solutions 1. Home Builder Supply, a retailer in the home improvement industry, currently operates seven retail outlets in Georgia and South Carolina. Management

FIN 350 Business Finance Homework 7 Fall 2014 Solutions 1. Home Builder Supply, a retailer in the home improvement industry, currently operates seven retail outlets in Georgia and South Carolina. Management

Advanced Corporate Finance. Lorenzo Parrini

Advanced Corporate Finance Lorenzo Parrini May 2017 1 Introduction Course structure Course structure 3 credits 24 h 6 lessons 1. Corporate finance 2. Corporate valuation 3. M&A deals 4. M&A private equity

Advanced Corporate Finance Lorenzo Parrini May 2017 1 Introduction Course structure Course structure 3 credits 24 h 6 lessons 1. Corporate finance 2. Corporate valuation 3. M&A deals 4. M&A private equity

DEFINING AND ESTIMATING THE FUTURE BENEFIT STREAM

Fundamentals, Techniques & Theory DEFINING AND ESTIMATING THE FUTURE BENEFIT STREAM CHAPTER FOUR DEFINING AND ESTIMATING THE FUTURE BENEFIT STREAM Practice Pointer Business without profit is not business

Fundamentals, Techniques & Theory DEFINING AND ESTIMATING THE FUTURE BENEFIT STREAM CHAPTER FOUR DEFINING AND ESTIMATING THE FUTURE BENEFIT STREAM Practice Pointer Business without profit is not business

The implied cost of capital of government s claim and the present value of tax shields: A numerical example

The implied cost of capital of government s claim and the present value of tax shields: A numerical example By M.B.J. Schauten and B. Tans M.B.J. Schauten is Assistant Professor in Finance, Erasmus University

The implied cost of capital of government s claim and the present value of tax shields: A numerical example By M.B.J. Schauten and B. Tans M.B.J. Schauten is Assistant Professor in Finance, Erasmus University

CA - FINAL 1.1 Capital Budgeting LOS No. 1: Introduction Capital Budgeting is the process of Identifying & Evaluating capital projects i.e. projects where the cash flows to the firm will be received

CA - FINAL 1.1 Capital Budgeting LOS No. 1: Introduction Capital Budgeting is the process of Identifying & Evaluating capital projects i.e. projects where the cash flows to the firm will be received

AAPL. Apple Inc. Sector: Information Technology HOLD. Analysts: Alexander Anguiano, Applied Portfolio Management. Bryan Lunzmann and Sam Olberding

AAPL Analysts: Alexander Anguiano, Applied Portfolio Management Bryan Lunzmann and Sam Olberding Apple Inc. Sector: Information Technology HOLD Report Date: 4/4/215 Market Cap (mm) $671,725 Annual Dividend

AAPL Analysts: Alexander Anguiano, Applied Portfolio Management Bryan Lunzmann and Sam Olberding Apple Inc. Sector: Information Technology HOLD Report Date: 4/4/215 Market Cap (mm) $671,725 Annual Dividend

Valuation and Tax Policy

Valuation and Tax Policy Lakehead University Winter 2005 Formula Approach for Valuing Companies Let EBIT t Earnings before interest and taxes at time t T Corporate tax rate I t Firm s investments at time

Valuation and Tax Policy Lakehead University Winter 2005 Formula Approach for Valuing Companies Let EBIT t Earnings before interest and taxes at time t T Corporate tax rate I t Firm s investments at time

Valuation: Fundamental Analysis. Equity Valuation Models. Models of Equity Valuation. Valuation by Comparables

Valuation: Fundamental Analysis 22-2 Equity Valuation Models Fundamental analysis models a company s value by assessing its current and future profitability. The purpose of fundamental analysis is to identify

Valuation: Fundamental Analysis 22-2 Equity Valuation Models Fundamental analysis models a company s value by assessing its current and future profitability. The purpose of fundamental analysis is to identify

Delaware State University College of Business Department of Accounting, Economics and Finance Spring 2013 Course Outline

I. Course Delaware State University College of Business Department of Accounting, Economics and Finance Spring 2013 Course Outline Course Number: FIN 445 90 CRN 18013 Course Title: Security Analysis and

I. Course Delaware State University College of Business Department of Accounting, Economics and Finance Spring 2013 Course Outline Course Number: FIN 445 90 CRN 18013 Course Title: Security Analysis and

CA - FINAL INTERNATIONAL FINANCIAL MANAGEMENT. FCA, CFA L3 Candidate

CA - FINAL INTERNATIONAL FINANCIAL MANAGEMENT FCA, CFA L3 Candidate 12.1 International Financial Management Study Session 12 LOS 1 : International Capital Budgeting Capital Budgeting is the process

CA - FINAL INTERNATIONAL FINANCIAL MANAGEMENT FCA, CFA L3 Candidate 12.1 International Financial Management Study Session 12 LOS 1 : International Capital Budgeting Capital Budgeting is the process

Valuation Principles

Valuation Principles The ACG Cup January 15, 2019 36 East 7 th Street Suite 2400 Cincinnati, OH 45202 513.813.4101 www.comstockadvisors.com Nickolas N. Sypniewski nsypniewski@comstockadvisors.com www.comstockadvisors.com

Valuation Principles The ACG Cup January 15, 2019 36 East 7 th Street Suite 2400 Cincinnati, OH 45202 513.813.4101 www.comstockadvisors.com Nickolas N. Sypniewski nsypniewski@comstockadvisors.com www.comstockadvisors.com

Public Courses. Practical financial skills to get you desk ready. London - Core Skills

Public Courses Practical financial skills to get you desk ready London - Core Skills Contents Why AMT Training 3 About us 3 Public Courses 4 Accounting Fundamentals, The Income Statement and Working Capital

Public Courses Practical financial skills to get you desk ready London - Core Skills Contents Why AMT Training 3 About us 3 Public Courses 4 Accounting Fundamentals, The Income Statement and Working Capital

Samsung / BBRY Pitch Book. Eduard Biller Paul Dawson Mashada Kamal Simon Foucher

Samsung / BBRY Pitch Book Eduard Biller Paul Dawson Mashada Kamal Simon Foucher AGENDA 1 2 3 4 Deal Overview Industry Target Overview- Blackberry Business Valuation 5 Synergies & Forecast 1 DEAL OVERVIEW

Samsung / BBRY Pitch Book Eduard Biller Paul Dawson Mashada Kamal Simon Foucher AGENDA 1 2 3 4 Deal Overview Industry Target Overview- Blackberry Business Valuation 5 Synergies & Forecast 1 DEAL OVERVIEW

NACVA National Association of Certified Valuation Analysts. Professional Standards

NACVA National Association of Certified Valuation Analysts Professional Standards These Professional Standards are effective for engagements accepted on or after January 1, 2008 NACVA PROFESSIONAL STANDARDS

NACVA National Association of Certified Valuation Analysts Professional Standards These Professional Standards are effective for engagements accepted on or after January 1, 2008 NACVA PROFESSIONAL STANDARDS

FINANCIAL MODELING, & VALUATION APRIL 6-7 & APRIL

FINANCIAL MODELING, & VALUATION APRIL 6-7 & APRIL 13-14 2018 4-DAY LIVE BOOT CAMP DETAILED COURSE DESCRIPTIONS +1 (212) 537-6631 +1 (212) 656-1221 (fax) ABOUT WALL STREET TRAINING & ADVISORY, INC. WHY

FINANCIAL MODELING, & VALUATION APRIL 6-7 & APRIL 13-14 2018 4-DAY LIVE BOOT CAMP DETAILED COURSE DESCRIPTIONS +1 (212) 537-6631 +1 (212) 656-1221 (fax) ABOUT WALL STREET TRAINING & ADVISORY, INC. WHY

Homework and Suggested Example Problems Investment Valuation Damodaran. Lecture 2 Estimating the Cost of Capital

Homework and Suggested Example Problems Investment Valuation Damodaran Lecture 2 Estimating the Cost of Capital Lecture 2 begins with a discussion of alternative discounted cash flow models, including

Homework and Suggested Example Problems Investment Valuation Damodaran Lecture 2 Estimating the Cost of Capital Lecture 2 begins with a discussion of alternative discounted cash flow models, including

China Information Technology Inc. (CNIT)

") ` China Information Technology Inc. (CNIT) Rapid Growth Prospects in China s Digital OOH Advertising Industry 150 East 58th Street 20th Floor Equity Research Stock Information (09/15/2017) Exchange-Nasdaq

` China Information Technology Inc. (CNIT) Rapid Growth Prospects in China s Digital OOH Advertising Industry 150 East 58th Street 20th Floor Equity Research Stock Information (09/15/2017) Exchange-Nasdaq

ALTEO MODEL UPDATE 8 FEBRUARY 2018

SUMMARY ALTEO Group is considered as a utility group regarding industry classification. The Group is a key player within the utility sector by offering Smart Energy Management solutions. The Group s activities

SUMMARY ALTEO Group is considered as a utility group regarding industry classification. The Group is a key player within the utility sector by offering Smart Energy Management solutions. The Group s activities

MIDTERM EXAM SOLUTIONS

MIDTERM EXAM SOLUTIONS Finance 70610 Equity Valuation Mendoza College of Business Professor Shane A. Corwin Fall Semester 011 Wednesday, November 16, 011 INSTRUCTIONS: 1. You have 110 minutes to complete

MIDTERM EXAM SOLUTIONS Finance 70610 Equity Valuation Mendoza College of Business Professor Shane A. Corwin Fall Semester 011 Wednesday, November 16, 011 INSTRUCTIONS: 1. You have 110 minutes to complete

LONG OPPORTUNITY: LCI (NYSE) LANNETT CORPORATION: STRUCTURAL BENEFITS OF KREMMERS ACQUISITION: 100% UPSIDE

LANNETT CORPORATION: STRUCTURAL BENEFITS OF KREMMERS ACQUISITION: 100% UPSIDE") LONG OPPORTUNITY: LCI (NYSE) LANNETT CORPORATION: STRUCTURAL BENEFITS OF KREMMERS ACQUISITION: 100% UPSIDE Executive Summary Lannett Corporation ( LCI ) shareholders have a unique opportunity to realize

LONG OPPORTUNITY: LCI (NYSE) LANNETT CORPORATION: STRUCTURAL BENEFITS OF KREMMERS ACQUISITION: 100% UPSIDE Executive Summary Lannett Corporation ( LCI ) shareholders have a unique opportunity to realize

2018 IBP Exam Topics Table of Contents

2018 IBP Exam Topics Table of Contents Level I Accounting... 2 Income statement... 2 Balance sheet... 2 Cash flow statement... 2 Financial statement analysis... 3 Financial reporting... 3 Excel... 3 Powerpoint...

2018 IBP Exam Topics Table of Contents Level I Accounting... 2 Income statement... 2 Balance sheet... 2 Cash flow statement... 2 Financial statement analysis... 3 Financial reporting... 3 Excel... 3 Powerpoint...

IMPORTANT INFORMATION: This study guide contains important information about your module.

217 University of South Africa All rights reserved Printed and published by the University of South Africa Muckleneuk, Pretoria INV371/1/218 758224 IMPORTANT INFORMATION: This study guide contains important

217 University of South Africa All rights reserved Printed and published by the University of South Africa Muckleneuk, Pretoria INV371/1/218 758224 IMPORTANT INFORMATION: This study guide contains important

Advanced Company Analysis Valuation & Financial Modelling. 5-9 March 2017 Manama, Bahrain. euromoneylearningsolutions.

Advanced Company Analysis Valuation & Financial Modelling 5-9 March 2017 Manama, Bahrain euromoneylearningsolutions.com/learnmore Advanced Company Analysis Valuation & Financial Modelling Accelerate your

Advanced Company Analysis Valuation & Financial Modelling 5-9 March 2017 Manama, Bahrain euromoneylearningsolutions.com/learnmore Advanced Company Analysis Valuation & Financial Modelling Accelerate your

Rajesh Exports (RJEX_IN) Earnings Update Report Consumer Discretionary: Gold Jewelry Manufacturer

Earnings Update Report Consumer Discretionary: Gold Jewelry Manufacturer") Monday, February 4, 2019 www.evaluateresearch.com Target Price Rs. 900.00 Current Price Rs. 598.00 Upside Potential 50% Market Cap. Shares Outstanding Rs. 176,802 mn US$ 2.47 bn 295.3 mn Free Float (FF

Monday, February 4, 2019 www.evaluateresearch.com Target Price Rs. 900.00 Current Price Rs. 598.00 Upside Potential 50% Market Cap. Shares Outstanding Rs. 176,802 mn US$ 2.47 bn 295.3 mn Free Float (FF

FINANCIAL MODELING, VALUATION & LBO TRAINING AUGUST 21-25, 2017

FINANCIAL MODELING, VALUATION & LBO TRAINING AUGUST 21-25, 2017 5-DAY LIVE BOOT CAMP DETAILED COURSE DESCRIPTIONS +1 (212) 537-6631 +1 (212) 656-1221 (fax) ABOUT WALL STREET TRAINING & ADVISORY, INC. WHY

FINANCIAL MODELING, VALUATION & LBO TRAINING AUGUST 21-25, 2017 5-DAY LIVE BOOT CAMP DETAILED COURSE DESCRIPTIONS +1 (212) 537-6631 +1 (212) 656-1221 (fax) ABOUT WALL STREET TRAINING & ADVISORY, INC. WHY

Note on Cost of Capital

DUKE UNIVERSITY, FUQUA SCHOOL OF BUSINESS ACCOUNTG 512F: FUNDAMENTALS OF FINANCIAL ANALYSIS Note on Cost of Capital For the course, you should concentrate on the CAPM and the weighted average cost of capital.

DUKE UNIVERSITY, FUQUA SCHOOL OF BUSINESS ACCOUNTG 512F: FUNDAMENTALS OF FINANCIAL ANALYSIS Note on Cost of Capital For the course, you should concentrate on the CAPM and the weighted average cost of capital.

EXC Exelon Corporation Sector: Utilities HOLD

Analysts: Alexa Bowen, Blake Porter and Kennedy White Washburn University Applied Portfolio Management EXC Sector: Utilities HOLD Report Date: 4/18/2016 Market Cap (mm) $31,337 Annual Dividend $1.24 2

Analysts: Alexa Bowen, Blake Porter and Kennedy White Washburn University Applied Portfolio Management EXC Sector: Utilities HOLD Report Date: 4/18/2016 Market Cap (mm) $31,337 Annual Dividend $1.24 2

Meeting the Challenges for Sustainable Water Utilities In Connecticut s Regulatory Structure. Rate of Return Rich Sobolewski Connecticut OCC

Meeting the Challenges for Sustainable Water Utilities In Connecticut s Regulatory Structure Rate of Return Rich Sobolewski Connecticut OCC The Rate Process in Connecticut Rate of Return Rate Base Regulation

Meeting the Challenges for Sustainable Water Utilities In Connecticut s Regulatory Structure Rate of Return Rich Sobolewski Connecticut OCC The Rate Process in Connecticut Rate of Return Rate Base Regulation

Example Exercise: FCF

Example Exercise: FCF You are given the following information about a corporation. The tax on EBITA for 2011 is 20, the amount of necessary cash as a percentage of sales is 2%, and from the income statement

Example Exercise: FCF You are given the following information about a corporation. The tax on EBITA for 2011 is 20, the amount of necessary cash as a percentage of sales is 2%, and from the income statement

Capital Structure Decisions

GSU, Department of Finance, AFM - Capital Structure / page 1 - Corporate Finance Capital Structure Decisions - Relevant textbook pages - none - Relevant eoc-problems - none - Other relevant material -

GSU, Department of Finance, AFM - Capital Structure / page 1 - Corporate Finance Capital Structure Decisions - Relevant textbook pages - none - Relevant eoc-problems - none - Other relevant material -

Appendices Appendix 1. STOXX50 Moving Average Monthly Returns, Source: Bloomberg data, November 2016.

Appendices Appendix 1. STOXX50 Moving Average Monthly Returns, 1987-2016 Source: Bloomberg data, November 2016. 6% STOXX50 Moving Average Monthly Returns 4% 2% 0% 01/12/1987 01/12/1992 01/12/1997 01/12/2002

Appendices Appendix 1. STOXX50 Moving Average Monthly Returns, 1987-2016 Source: Bloomberg data, November 2016. 6% STOXX50 Moving Average Monthly Returns 4% 2% 0% 01/12/1987 01/12/1992 01/12/1997 01/12/2002

Real Estate & REIT Modeling: Quiz Questions Module 5 Real Estate & REIT Valuation

Real Estate & REIT Modeling: Quiz Questions Module 5 Real Estate & REIT Valuation 1. Which of the following criteria listed below would you NOT use to select public comps when valuing an equity REIT? a.

Real Estate & REIT Modeling: Quiz Questions Module 5 Real Estate & REIT Valuation 1. Which of the following criteria listed below would you NOT use to select public comps when valuing an equity REIT? a.

December Fair Market Value Assessment of Telemedia A Report for Belize Telemedia Limited

December 2010 Fair Market Value Assessment of Telemedia A Report for Belize Telemedia Limited Project Team Dr Richard Hern Tomas Haug, CFA Signed: Dr Richard Hern NERA Economic Consulting 15 Stratford

December 2010 Fair Market Value Assessment of Telemedia A Report for Belize Telemedia Limited Project Team Dr Richard Hern Tomas Haug, CFA Signed: Dr Richard Hern NERA Economic Consulting 15 Stratford

Discounted free cash flow valuation model

SESSION 4 Topics: Analysis of statement of cash flows Case analysis Mechanical preparation of SCF: Costco Discounted free cash flow valuation model Free cash flow vs EDITDA REVIEW OF SESSION 3 About A/R,

SESSION 4 Topics: Analysis of statement of cash flows Case analysis Mechanical preparation of SCF: Costco Discounted free cash flow valuation model Free cash flow vs EDITDA REVIEW OF SESSION 3 About A/R,

Advanced Finance GEST-S402 Wrap-up session: company valuation and financing decision

Advanced Finance GEST-S402 Wrap-up session: company valuation and financing decision 2017-2018 Prof. Laurent Gheeraert Objectives of the session BDM, 2013 reference: Chapter 18: Capital Budgeting and Valuation

Advanced Finance GEST-S402 Wrap-up session: company valuation and financing decision 2017-2018 Prof. Laurent Gheeraert Objectives of the session BDM, 2013 reference: Chapter 18: Capital Budgeting and Valuation

Web Extension: Comparison of Alternative Valuation Models

19878_26W_p001-009.qxd 3/14/06 3:08 PM Page 1 C H A P T E R 26 Web Extension: Comparison of Alternative Valuation Models We described the APV model in Chapter 26 because it is easier to implement when

19878_26W_p001-009.qxd 3/14/06 3:08 PM Page 1 C H A P T E R 26 Web Extension: Comparison of Alternative Valuation Models We described the APV model in Chapter 26 because it is easier to implement when

NACVA. National Association of Certified Valuation Analysts. Professional Standards

NACVA National Association of Certified Valuation Analysts Professional Standards Effective May 31, 2002 NACVA PROFESSIONAL STANDARDS Table of Contents Preamble... 4 General and Ethical Standards... 4

NACVA National Association of Certified Valuation Analysts Professional Standards Effective May 31, 2002 NACVA PROFESSIONAL STANDARDS Table of Contents Preamble... 4 General and Ethical Standards... 4

NACVA. National Association of Certified Valuators and Analysts

NACVA National Association of Certified Valuators and Analysts The Core Body of Knowledge for Business Valuations All rights reserved. No part of this work covered by the copyrights herein may be reproduced

NACVA National Association of Certified Valuators and Analysts The Core Body of Knowledge for Business Valuations All rights reserved. No part of this work covered by the copyrights herein may be reproduced

(NYSE: ENVA) Senior Analyst: Benjamin Smith Junior Analysts: Alejandro Mendez, Eric Rivera, Gia Sun, Zack Zhang. Spring 2018

Senior Analyst: Benjamin Smith Junior Analysts: Alejandro Mendez, Eric Rivera, Gia Sun, Zack Zhang. Spring 2018") Investment Enova International Research I Presentation (NYSE: ENVA) Month Sector: Day, Financials M 20XX Senior Analyst: Benjamin Smith Junior Analysts: Alejandro Mendez, Eric Rivera, Gia Sun, Zack Zhang

Investment Enova International Research I Presentation (NYSE: ENVA) Month Sector: Day, Financials M 20XX Senior Analyst: Benjamin Smith Junior Analysts: Alejandro Mendez, Eric Rivera, Gia Sun, Zack Zhang