ACCOUNTING FOR NON- ACCOUNTANTS UNDERSTANDING THE BASICS OF ACCOUNTING

|

|

|

- Sherilyn Kelly

- 5 years ago

- Views:

Transcription

1 ACCOUNTING FOR NON- ACCOUNTANTS UNDERSTANDING THE BASICS OF ACCOUNTING

2 LEARNING OBJECTIVE To guide and assist you in your decision making processes, To allow you to participate actively in the financial matters of your business and, To let you appreciate the various accounting terminologies and methodologies applied in your on-going undertakings.

3 WHY DO YOU NEED TO STUDY ACCOUNTING WHEN YOU ARE NOT AN ACCOUNTANT? Accounting is an activity you will do even if you are not an accountant, simply because it is necessary especially so if you engage in a profit-oriented undertaking, called business. Many small businesses do not survive to see their third birthday. This is a sad but true fact. One of the main reasons this happens is that people who set up their own business lack the necessary skills needed to successfully run a business. Often they are very skilled at what they do for a living, however, being skilled at what you do is only part of the story. You need to add more skills to your skill set if your business is to reach its full potential: skills such as marketing, human resources management, finance, strategic planning and, hence this module, accounting.

4 WHAT IS A BUSINESS? A business is an organization in which basic resources (inputs), such as materials and labor, are assembled and processed to provide goods or services (outputs) to customers. Business activities are meant to generate economic activity. Business transforms good and services in forms that on the other hand, people whose needs and wants are to be satisfied would also be willing to exchange their goods and services whose value equals the value of what they receive. This is the essence of a business transaction, the exchange of values; values received equal the values parted with.

5 WHAT IS A BUSINESS? The objective of most businesses is to earn a profit. Profit is the difference between the amounts received from customers for goods or services and the amounts paid for the inputs used to provide the goods or services.

6 WHAT IS ACCOUNTING? Accounting can be defined as an information system that provides reports to users about the economic activities and condition of a business. is a service activity. Its function is to provide quantitative information, primarily financial in nature, about economic entities, that is intended to be useful in making economic decision. is the art of recording, classifying and summarizing in a significant manner and in terms of money, transactions and events which are, in part at least, of a financial character and interpreting the results thereof.

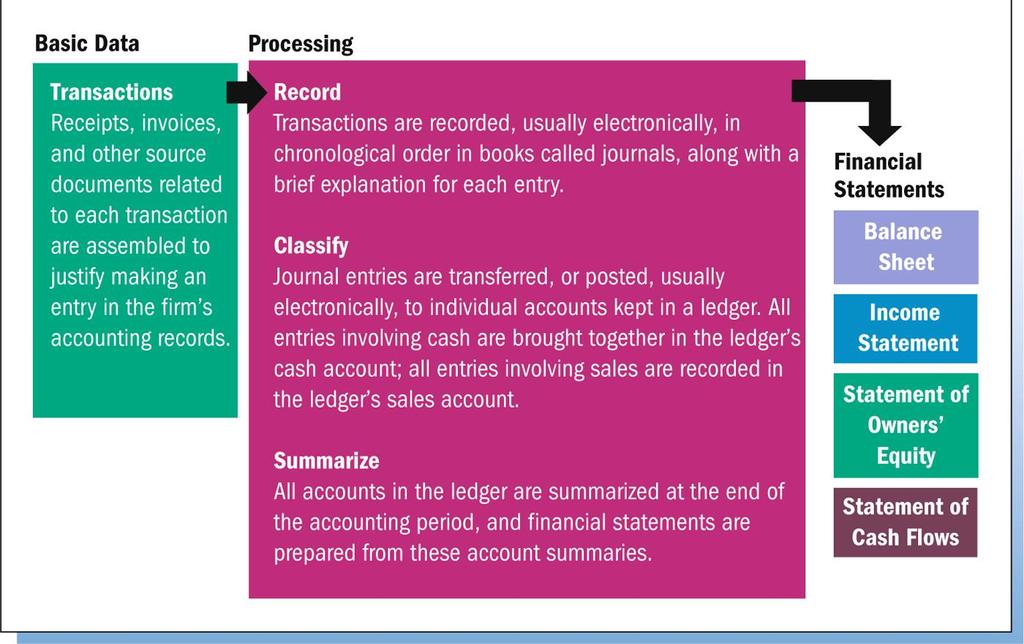

7 1. Recording of data 2. Classifying of data 3. Summarizing of data 4. Interpreting the results WHAT ARE THE FUNCTIONS OF ACCOUNTING?

8 FIRST ACCOUNTING FUNCTION: RECORDING involves putting into record the various transactions in a step-by-step procedure and in order of occurrence or when the transaction happens or occurs. A transaction is said to have occurred or happened, once a document to its effect has been made, and as such the transaction is recorded.

9 SECOND ACCOUNTING FUNCTION: CLASSIFYING involves the grouping together of similar names and items of the various resources of the business that were already transformed (finished goods, products, services, loans, etc) or are still in the process of transformation (raw materials, inventory, etc). By classifying and grouping together of similar resources of the enterprise, analysis is facilitated, communication is facilitated, and ambiguity is avoided.

10 Assets Liabilities Capital Revenue Expenses Equities Drawing BUSINESS RESOURCES ARE CLASSIFIED AS FOLLOWS:

11 BUSINESS RESOURCES ARE CLASSIFIED AS FOLLOWS: Asset - refers to anything that has money equivalent possessed by the enterprise or business and is used in the operation of the enterprise, which in its absence, will greatly hamper the operation of the business. The assets are needed by the business in order that it can produce the goods and the services that it intended to do. Ex. Cash, account receivables, land, equipment, supplies, etc.

12 BUSINESS RESOURCES ARE CLASSIFIED AS FOLLOWS: Liabilities -refer to the monetary values of anything that the business has loaned out, borrowed or taken from outside of the business itself. The business incurs liabilities in order that it can pay for its operation as well as to create its initial asset base. Ex. Loans from Metro Bank, accounts payable, tax payable, notes payable, etc.

13 BUSINESS RESOURCES ARE CLASSIFIED AS FOLLOWS: Capital refers to the monetary values or the rights of the owner or owners to a claim on the properties or possessions of the business. When a capital gets into a business, it is transformed into a number of forms of which it will become part of the assets of the business. Income refers to the sales the business makes either in cash or on account. It also refers to professional or consultancy fees, service income, sales from the farm products. Expenses refer to costs or expenditures, used up supplies and materials incurred in operating the business. Ex. Salary expense, Electric bill, Maintenance expense, Supplies used, etc.

14 BUSINESS RESOURCES ARE CLASSIFIED AS FOLLOWS: Equities refer to the rights or claims of both the creditors and the owners of the business to what the enterprise is owning or possessing with equivalent monetary values. In case the business goes bankrupt, and when the project decides to sell out all that it owns, the first to be paid are the creditors and the money that will be left after settling all the outside obligations will be divided among the owners or partners of the enterprise. Drawing refer to the personal withdrawal of the owner or owners against capital they put in the business. The result of such withdrawal is a decrease on the capital of the enterprise.

15 THIRD ACCOUNTING FUNCTION: SUMMARIZING Since a business is conducting a lot of transactions in the course of its life, the information that was recorded in its books of accounts becomes numerous. If the business accounting system was properly in place then summarizing the information in its books is facilitated by their classifications. Distilling all of this information into forms. Summarizing the business transactions is founded on the Accounting Equation.

16 THE ACCOUNTING EQUATION ASSETS = LIABILITIES + EQUITY The resources owned by a business The rights of creditors are the debts of the business The rights of the owners

17 THE ACCOUNTING EQUATION The accounting equation may also be expressed in two other forms: (1) OWNER S EQUITY = ASSETS LIABILITIES (2) LIABILITIES = ASSETS OWNER S EQUITY A = L + OE (C + R E D) Where: A = assets L = liabilities OE = Owner s Equity C = Capital R = Revenue E = Expenses D = Drawings

18 ACCRUAL GOING CONCERN CONCEPT BUSINESS ENTITY CONCEPT ACCOUNTING CONCEPTS: UNDERLYING ASSUMPTIONS Income is recognized when earned regardless of when received Expense is recognized when incurred regardless of when paid The effects of transactions are recognized when they occur The business will continue in operational existence for the foreseeable future Financial statements should be prepared on a going concern basis unless management either intends to liquidate the enterprise or to cease trading, The business and its owner(s) are two separate entities Any private and personal incomes and expenses of the owner(s) should not be treated as the incomes and expenses of the business

The purchasing power of the Peso is")

19 ACCOUNTING CONCEPTS: UNDERLYING ASSUMPTIONS TIME PERIOD The life of an entity is subdivided into time periods which are of equal length for the purpose of making financial reports Usually twelve months MONETARY UNIT Assets, liabilities, capital, income and expenses should be stated in terms of a unit of measure (Philippine Peso) The purchasing power of the Peso is stable/constant

20 ACCOUNTING CONCEPTS: QUALITATIVE CHARACTERISTICS Relevance Reliability Faithful Representation Substance over Form The capacity of information to influence a decision The degree of confidence users place upon the truthfulness of the representations in the financial statements The quality of information that assures users that the information is free from bias and error and faithfully represents what it purports to represent The actual effects of the transaction should be properly accounted for and reported in the financial statements Transactions should be accounted in accordance with their substance in reality and not merely their legal form

21 ACCOUNTING CONCEPTS: QUALITATIVE CHARACTERISTICS Neutrality Conservatism or Prudence Completeness Information in the Financial Statements must be free from bias fairness Care and caution must be exercised when dealing with uncertainties in the measurement process The Revenues and profits are not anticipated. Only realized profits with reasonable certainty are recognized in the profit and loss account Relevant information must be presented in a way that facilitates understanding and avoids erroneous implication

22 ACCOUNTING CONCEPTS: QUALITATIVE CHARACTERISTICS Understandability Financial information must be comprehensible or intelligible if it is to be useful Comparability Information must be comparable with similar information of previous periods or with information of another entity

23 TIMELINESS ACCOUNTING CONCEPTS: ACCOUNTING CONSTRAINTS Information must be available or communicated early enough when a decision is to be made COST-BENEFIT The benefit derived from the information should exceed the cost incurred in obtaining the information MATERIALITY RELEVANCE vs RELIABILITY An item is material if knowledge of it would affect or influence the decision of the informed users of the financial statements There is a tradeoff between relevance (reporting information in a relevant manner) and reliability (ensuring that the information is reliable)

24 ACCOUNTING METHODS Accounting methods dictate how the company's transactions are recorded in the company's financial books Cash-basis accounting companies record expenses in financial accounts when the cash is actually laid out, and they book revenue when they actually hold the cash Accrual accounting companies record revenue when the actual transaction is completed (such as the completion of work specified in a contract agreement between the company and its customer), not when they receive the cash. Companies record any expenses when they're incurred, even if they have not paid for the supplies yet

25 Accounting Process

26 3. FINANCIAL ACCOUNTING REPORTS

27 FINANCIAL STATEMENTS Summarized reports of accounting transactions Two-fold purpose: to communicate to users: - the effect of operating activities during a specified period of time; and, - the business financial position at the end of the period Types of financial statements: Income Statement Balance Sheet Statement of Cash Flow

28 BALANCE SHEET Reports the financial position of a business at a specific point in time Often called the statement of financial position Equation: Assets = Liabilities + Owners Equity

29 BALANCE SHEET Assets economic resources that are expected to benefit future activities Equities claims against, or interests in, the assets Liabilities entity s economic obligations to non-owners Owners equity excess of the assets over the liabilities For a corporation, the owners equity is called the stockholders equity.

30 Pro Forma Balance Sheet XYZ Co. Balance Sheet December 31, 20xx ASSETS Current Assets Cash xxx Marketable Securities xxx Accounts Receivable xxx Merchandise Inventory xxx Other Current Assets xxx. Total Current Assets xxx Fixed Assets Land xxx Building xxx

31 Furniture & Fixture xxx Office Equipment xxx. Total xxx Less: Accumulated Depreciation xxx. Total Fixed Assets xxx. TOTAL ASSETS xxx. LIABILITIES & STOCKHOLDERS EQUITY LIABILITIES Current Liabilities: Notes and Accounts Payable xxx Taxes Payable xxx Other Current Liabilities xxx. Total Current Liabilities xxx Long-term Liabilities xxx. Total Liabilities xxx.

32 OWNER S EQUITY Capital xxx Profit (Loss) for the period xxx Drawing (xxx). Total Owner s Equity xxx. TOTAL LIABILITIES & OWNER S EQUITY xxx.

33 INCOME STATEMENT Measures the operating performance of the corporation by matching its accomplishments (revenue from customers, which is usually called sales) and its efforts (cost of goods sold and expenses). Measures performance for a span of time Also known as Profit and Loss Statement

34 Revenues - inflows of assets either from the sale of goods or the performance of services Expenses - outflows or other uses of assets to produce revenues over expenses Net income (sometimes referred to as earnings or profit) is the excess of revenues over expenses, including tax expense

35 XYZ Co. Income Statements For Year Ended December 31, 2017 (in thousands of pesos) Sales 3,280 Less: Cost of Sales 2,120 Gross Income 1,160 Less: Operating Expenses Selling 350 Administrative 420 Total Operating Expenses 770 Income from Operations 390 Less: Interest Expense 30 Income before tax 360 Less: Income Tax 126 Net Income 234 ====

36 STATEMENT OF CASH FLOWS is a statement showing all the cash inflows and cash outflows of the business. It shows how much money there is at the beginning and at the end of the business period. Cash Inflow- refers to cash receipts made from the disposals of farm products to the customers, as well as beginning cash to start the business. Cash Outflow- refers to expenses incurred during the operation period. It includes payments of cash for various materials and supplies used in the projects or enterprises.

37 STATEMENT OF CASH FLOWS Cash balance ending refers to the cash generated after all expenses have been deducted from cash inflows of the business. However, if cash inflows are greater than cash outflows, the business has enough cash to continue with the operation of the business; if it is not, then it is an indication that the manager should now look for additional financing from outside sources to continue funding the day to day activities of the business.

38 PRO FORMA CASH FLOW STATEMENT XYZ Co. Cash Flow Projections For the Period Ending Cash Inflows (Receipts) Collection of Receivables Cash Sales Sale of Marketable Securities Short-Term Borrowing Long-Term Borrowing Additional Investments Total Cash Inflows xxx xxx xxx xxx xxx xxx xxx

39 Cash Outflows (Disbursements) Payments for Merchandise Inventory xxx Selling Expenses xxx General and Administrative Expense xxx Payment for Fixed Assets xxx Interest Payments xxx Loan Repayments xxx Payments on Real Estate Mortgage xxx Payment on Income Taxes xxx Other Taxes and Assessments xxx. Total Cash Outflows (xxx). Net Cash Flow xxx Add: Cash Balance, Beginning xxx Cash Balance, Ending xxx =======

40 FOURTH ACCOUNTING FUNCTION: INTERPRETING Use the different reports to look critically at your business. Does it perform well? What can you do better? There are two main subjects in the report: Income Statement Balance Statement

41 INCOME STATEMENT The Income Statement tells about the earnings and spending of the company during the year. This means how much income has the company had from the daily running of activities and how much has the company spent on the same activities. This part of the report tells whether the activities have been running as a profitable business in the period or not. It is called the Income Statement.

42 BALANCE SHEET The Balance Sheet / Statement of Financial Position, on the other hand, shows the actual value of the company as such. This means, how much money is present in the company in total when the value of buildings, tools, stock, money in the bank account and in the cash box etc. is added. It also shows how much the company owes to others. A company normally owes money to suppliers, the bank and to the owner of the company.

43 WRITE OFF FIXED ASSETS/ DEPRECIATION Fixed Assets like vehicles would usually encounter wear and tear as it is continuously used in the operation of the business. In the law, it is allowed that owners will depreciate the value of the machine yearly up to its estimated life span, and such depreciation will be reflected as part of the operating cost of the project although there is no actual cash incurrence, however, the amount of money deducted from the income as depreciation cost can be kept by the business that in the event that the machine can no longer function efficiently, there is already accumulated cash which can be used to replace the old machine. The accumulated amount might not be sufficient to buy a new machine, yet, it can be used as down payment for the purchased machine and the remaining balance can be paid in an instalment basis from the income that can be generated by the use of the machine.

44 HORIZONTAL ANALYSIS - Involves comparing figures shown in the financial statements of two or more consecutive periods. The difference between the figures of the two periods is calculated, and the percentage change from one period to the next is computed, using the earlier period as the base.

45 XYZ Corporation Income Statements For Years Ended December 31 (in thousands of pesos) Increase (Decrease) Amount Percent Sales 3,280 2, % Less: Cost of Sales 2,120 1, Gross Income 1,160 1, Less: Operating Expenses Selling Administrative ( 60) (13) Total Operating Expenses Income from Operations (63) (14) Less: Interest Expense Income before tax (68) (16) Less: Income Tax (23.8) (16) Net Income (44.20) (16) ==== ===== ====== ====

46 HORIZONTAL ANALYSIS Formula for Percentage Change: Percentage = Most Recent Value - Base Period Value Change Base Period Value = 3, ,950 =.11 or 11%

47 VERTICAL ANALYSIS - process of comparing figures in the financial statements of a single period. - involves converting the figures in the statements to a common base. - accomplished by expressing all the figures in the statements as a percentage of an important item, such as total assets (in the balance sheet) and total or net sales (in the income statement). - all the figures in the statements would be expressed not in peso but in percentage terms. - these converted statements are called common-size statements, 100 percent statements or component statements.

48 XYZ Corporation Income Statements For Years Ended December 31 (in thousands of pesos) 2017 Percent 2016 Sales 3, % 2,950 Less: Cost of Sales 2, % 1,917 Gross Income 1, % 1,033 Less: Operating Expenses Selling % 100 Administrative % 480 Total Operating Expenses % 580 Income from Operations Less: Interest Expense Income before tax % 428 Less: Income Tax % Net Income ==== =====

49 Ratios are categorized based on their uses: 1. Tests of liquidity - Current ratio - Acid test ratio - Turnovers 2. Tests of Solvency - Number of times interest earned ratio - Debt-equity ratio - Debt ratio - Equity ratio RATIO ANALYSIS

50 3. Tests of Profitability - Return on sales - Return on total assets - Return on owner s equity - Earnings per share 4. Market Tests - Price-earnings ratio - Dividend yield - Dividend payout RATIO ANALYSIS

51 TESTS OF LIQUIDITY: CURRENT RATIO 1. Current Ratio also called the working capital ratio or banker s ratio, measures the number of times that the current liabilities could be paid with the available current assets. CURRENT RATIO = Current Assets Current Liabilities Standard 1.5:1 - the higher, the better

52 TESTS OF LIQUIDITY: ACID TEST RATIO - Also called as quick ratio; only those assets that are cash or near cash (or assets that can be converted to cash quickly) are included so that the resulting ratio can indicate the firm s paying liability in the very, very near term. - Similar to the current ratio except that the inventories and prepayments are excluded from the numerator.

53 TESTS OF LIQUIDITY: ACID TEST RATIO Quick Assets Quick Ratio = Current Liabilities or = Cash + Marketable Securities+ Receivables Current Liabilities Standard = 1:1 - the higher, the better

54 ILLUSTRATION: Let us first compute XYZ Corporation s quick or liquid assets: Cash Marketable securities Accounts receivable (net) Total Quick Assets === === Current Liabilities: Notes & Accounts Payable P Taxes Payable Other Current Liabilities 82 - Total CL P ===== ====

55 Acid Test Ratio = Quick Assets Current Liabilities 2016 = = 1.28 to = = 1.25 to 1 SOLUTION:

56 WORKING CAPITAL ACTIVITY RATIOS Both the current ratio and acid test ratio fail to provide answers to the following questions: 1. How long can the firm expect to realize cash from its receivables and inventories? 2. When should the firm pay its various current liabilities? To answer these 2 important questions, analysts can use the 3 working capital activity ratios: accounts receivable turnover, inventory turnover and accounts payable turnover.

57 RECEIVABLES TURNOVER the time required to complete one collection cycle from the time receivables are recorded, then collected, to the time new receivables are recorded again; the faster the cycle is completed, the more quickly receivables are converted into cash.

58 FORMULA FOR RECEIVABLES TURNOVER Receivables = Net Sales Turnover Average Receivables Average Receivables = Beg. Balance + Ending Balance 2 Standard: days - the lower, the better

59 INVENTORY TURNOVER Measures the number of times that inventory is replaced during the period. Inventory = Cost of Goods Sold Turnover Ave. Merchandise Inventory Ave Mdse Invty - Beg Bal + Ending Bal 2 Standard 180 days - the lower the better

60 Net Working Capital = Current Assets - Current Liabilities NET WORKING CAPITAL Standard = Positive Remarks = Positive

61 TESTS OF SOLVENCY Solvency refers to the company s ability to pay all its debts, whether such liabilities are current or noncurrent. Net Income before Interest Expense Times Interest Earned = Standard - Interest Expense 2x - the higher, the better

62 DEBT RATIO - indicates the percentage of total assets provided by creditors. Total Liabilities Debt Ratio = x 100 Total Assets Standard - 50% - the lower, the better

63 DEBT-EQUITY RATIO Debt-Equity = Total Liabilities Equity Standard = 4:1 - the lower, the better

64 TESTS OF PROFITABILITY

65 Gross Profit Margin = Gross Profit Net Sales Standard = 10 15% The higher, the better GROSS PROFIT MARGIN

66 Net Profit Margin = Net Profit Net Sales Standard = 2 20% The higher, the better NET PROFIT MARGIN

67 Return on Equity = Net Profit Equity Standard = 5 25% The higher, the better RETURN ON EQUITY

68 Return on Total Assets = Net Profit Total Assets RETURN ON TOTAL ASSETS Standard = 10% The higher, the better

69 RETURN ON INVESTMENT Rate of Return or = Income Return on Investment Investment = Higher than interest rate

70 PAYBACK PERIOD Payback Period = Total Project Cost Net Income = shall not exceed term of loan

71 HAPPY LEARNING!!!

" Annual report: the main method that management uses to report the results of the company s activities during the year.

Chapter 1 Overview of Corporate Financial Reporting What is Business? " Business plan to profit from selling a product or service. " Can be an individual or thousands of owners (investors). What is Accounting?

Chapter 1 Overview of Corporate Financial Reporting What is Business? " Business plan to profit from selling a product or service. " Can be an individual or thousands of owners (investors). What is Accounting?

Analysis and Interpretation of Financial Statements

Chapter 23 Analysis and Interpretation of Financial Statements o Prepare comparative financial statements using horizontal analysis o Prepare comparative financial statements using vertical analysis o

Chapter 23 Analysis and Interpretation of Financial Statements o Prepare comparative financial statements using horizontal analysis o Prepare comparative financial statements using vertical analysis o

Introduction to International Financial Reporting Standards

Introduction to International Financial Reporting Standards Structure of IASCF International Accounting Standards Committee Foundation (22 Trustees) InternationalAccounting Standards Board (15 members)

Introduction to International Financial Reporting Standards Structure of IASCF International Accounting Standards Committee Foundation (22 Trustees) InternationalAccounting Standards Board (15 members)

Accounting Principles: A Business Perspective, 8e Chapter 1: Accounting and Its Use in Business Decisions

Accounting Principles: A Business Perspective, 8e Chapter 1: Accounting and Its Use in Business Decisions Forms of Business Organizations A business entity is any business organization that exists as an

Accounting Principles: A Business Perspective, 8e Chapter 1: Accounting and Its Use in Business Decisions Forms of Business Organizations A business entity is any business organization that exists as an

FAQ: Financial Ratio Analysis

Question 1: What is horizontal analysis of financial statement data? Answer 1: Horizontal analysis is a method of financial ratio analysis. Horizontal analysis is comparing each item on the financial statements

Question 1: What is horizontal analysis of financial statement data? Answer 1: Horizontal analysis is a method of financial ratio analysis. Horizontal analysis is comparing each item on the financial statements

BUSINESS FINANCE. Financial Statement Analysis. 1. Introduction to Financial Analysis. Copyright 2004 by Larry C. Holland

BUSINESS FINANCE Financial Statement Analysis 1. Introduction to Financial Analysis Slide 1 Welcome to the study of business finance. The major topic in this module is Financial Statement Analysis. And

BUSINESS FINANCE Financial Statement Analysis 1. Introduction to Financial Analysis Slide 1 Welcome to the study of business finance. The major topic in this module is Financial Statement Analysis. And

Introduction to Financial Accounting & Key Financial Statements (Chapter 1)

") Introduction to Financial Accounting & Key Financial Statements (Chapter 1) 14/10/2017 5:29:00 pm Accounting = process of identifying, measuring and communicating economic information to assist users in

Introduction to Financial Accounting & Key Financial Statements (Chapter 1) 14/10/2017 5:29:00 pm Accounting = process of identifying, measuring and communicating economic information to assist users in

MVSR ENGINEERING COLLEGE MBA DEPARTMNET FINANCIAL ACCOUNTING AND ANALYSIS

MVSR ENGINEERING COLLEGE MBA DEPARTMNET FINANCIAL ACCOUNTING AND ANALYSIS Accounting : The systematic and comprehensive recording of financial transactions pertaining to a business. Accounting also refers

MVSR ENGINEERING COLLEGE MBA DEPARTMNET FINANCIAL ACCOUNTING AND ANALYSIS Accounting : The systematic and comprehensive recording of financial transactions pertaining to a business. Accounting also refers

AGENDA: MANAGEMENT ACCOUNTING

14-1 Management Accounting Tutorial 8 (, chapter 13, 14, 1, 2, 3) Mid Module Review Bangor University Transfer Abroad Programme 1. Globalization. 2. Strategy. 3. Organizational structure. 4. Process management.

14-1 Management Accounting Tutorial 8 (, chapter 13, 14, 1, 2, 3) Mid Module Review Bangor University Transfer Abroad Programme 1. Globalization. 2. Strategy. 3. Organizational structure. 4. Process management.

Module 1 Exhibits and Key terms

Exhibit 1... 2 Exhibit 2... 3 A. Income Statement... 3 C. Balance Sheet... 3 Transactions affecting only the balance sheet... 4 1a. Owners invested cash... 4 2a. Borrowed money... 4 3a. Purchased trucks

Exhibit 1... 2 Exhibit 2... 3 A. Income Statement... 3 C. Balance Sheet... 3 Transactions affecting only the balance sheet... 4 1a. Owners invested cash... 4 2a. Borrowed money... 4 3a. Purchased trucks

Engineering Economics and Financial Accounting

Engineering Economics and Financial Accounting Unit 5: Accounting Major Topics are: Balance Sheet - Profit & Loss Statement - Evaluation of Investment decisions Average Rate of Return - Payback Period

Engineering Economics and Financial Accounting Unit 5: Accounting Major Topics are: Balance Sheet - Profit & Loss Statement - Evaluation of Investment decisions Average Rate of Return - Payback Period

CHAPTER 2. Financial Reporting: Its Conceptual Framework CONTENT ANALYSIS OF END-OF-CHAPTER ASSIGNMENTS

2-1 CONTENT ANALYSIS OF END-OF-CHAPTER ASSIGNMENTS CHAPTER 2 Financial Reporting: Its Conceptual Framework NUMBER TOPIC CONTENT LO ADAPTED DIFFICULTY 2-1 Conceptual Framework 2-2 Conceptual Framework 2-3

2-1 CONTENT ANALYSIS OF END-OF-CHAPTER ASSIGNMENTS CHAPTER 2 Financial Reporting: Its Conceptual Framework NUMBER TOPIC CONTENT LO ADAPTED DIFFICULTY 2-1 Conceptual Framework 2-2 Conceptual Framework 2-3

How Well Am I Doing? Financial Statement Analysis

How Well Am I Doing? Financial Statement Analysis Chapter 16 McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. Limitations of Financial Statement Analysis Differences

How Well Am I Doing? Financial Statement Analysis Chapter 16 McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. Limitations of Financial Statement Analysis Differences

CHAPTER 2. Financial Reporting: Its Conceptual Framework CONTENT ANALYSIS OF END-OF-CHAPTER ASSIGNMENTS

2-1 CONTENT ANALYSIS OF END-OF-CHAPTER ASSIGNMENTS NUMBER Q2-1 Conceptual Framework Q2-2 Conceptual Framework Q2-3 Conceptual Framework Q2-4 Conceptual Framework Q2-5 Objective of Financial Reporting Q2-6

2-1 CONTENT ANALYSIS OF END-OF-CHAPTER ASSIGNMENTS NUMBER Q2-1 Conceptual Framework Q2-2 Conceptual Framework Q2-3 Conceptual Framework Q2-4 Conceptual Framework Q2-5 Objective of Financial Reporting Q2-6

Financial Accounting s Conceptual Foundations

Economics /Management 4 Financial Accounting Financial Accounting s Conceptual Foundations L-2 A highly-stylized Information System Basic Functions (all info systems): 1. Collection of transactions data

Economics /Management 4 Financial Accounting Financial Accounting s Conceptual Foundations L-2 A highly-stylized Information System Basic Functions (all info systems): 1. Collection of transactions data

INTERMEDIATE ACCOUNTING

Chapter 2 Financial Reporting: Its Conceptual Framework INTERMEDIATE ACCOUNTING Objectives 1. Explain the FASB Conceptual Framework. 2. Explain the general and specific objectives of general purpose financial

Chapter 2 Financial Reporting: Its Conceptual Framework INTERMEDIATE ACCOUNTING Objectives 1. Explain the FASB Conceptual Framework. 2. Explain the general and specific objectives of general purpose financial

A CLEAR UNDERSTANDING OF THE INDUSTRY

A CLEAR UNDERSTANDING OF THE INDUSTRY IS CFA INSTITUTE INVESTMENT FOUNDATIONS RIGHT FOR YOU? Investment Foundations is a certificate program designed to give you a clear understanding of the investment

A CLEAR UNDERSTANDING OF THE INDUSTRY IS CFA INSTITUTE INVESTMENT FOUNDATIONS RIGHT FOR YOU? Investment Foundations is a certificate program designed to give you a clear understanding of the investment

MANAGEMENT ACCOUNTING

MANAGEMENT ACCOUNTING Accounting: The Language of Business Accounting - a process of identifying, recording, summarizing, and reporting economic information to decision makers in the form of financial

MANAGEMENT ACCOUNTING Accounting: The Language of Business Accounting - a process of identifying, recording, summarizing, and reporting economic information to decision makers in the form of financial

CHAPTER 12. The statement of cash flows categorizes cash receipts and cash payments as operating, investing, and financing activities.

CHAPTER 12 Purpose of the Statement of Cash Flows The statement of cash flows is considered a major financial statement, as are the income statement, balance sheet, and statement of stockholders' equity.

CHAPTER 12 Purpose of the Statement of Cash Flows The statement of cash flows is considered a major financial statement, as are the income statement, balance sheet, and statement of stockholders' equity.

Bought to you by AS- Level Accounting Unit 2 Revision Notes

A-PDF Watermark DEMO: Purchase from www.a-pdf.com to remove the watermark for more notes visit Bought to you by AS- Level Accounting Unit 2 Revision Notes Types of Business Organisation: Sole Traders:

A-PDF Watermark DEMO: Purchase from www.a-pdf.com to remove the watermark for more notes visit Bought to you by AS- Level Accounting Unit 2 Revision Notes Types of Business Organisation: Sole Traders:

FINANCIAL RATIOS. LIQUIDITY RATIOS (and Working Capital) You want current and quick ratios to be > 1. Current Liabilities SAMPLE BALANCE SHEET ASSETS

You want current and quick ratios to be > 1. Current Liabilities SAMPLE BALANCE SHEET ASSETS") FINANCIAL RATIOS ROUND ALL ANSWERS TO TWO DECIMALS UNLESS REQUESTED OTHERWISE IN THE PROBLEM LIQUIDITY RATIOS (and Working Capital) You want current and quick ratios to be > 1 Current Ratio Quick Ratio

FINANCIAL RATIOS ROUND ALL ANSWERS TO TWO DECIMALS UNLESS REQUESTED OTHERWISE IN THE PROBLEM LIQUIDITY RATIOS (and Working Capital) You want current and quick ratios to be > 1 Current Ratio Quick Ratio

AccountingCoach.com Financial Ratios

AccountingCoach.com Financial Ratios All underlined words are defined in the attached Glossary (Pages 13 20). Introduction to Financial Ratios When analyzing computing financial ratios and when doing other

AccountingCoach.com Financial Ratios All underlined words are defined in the attached Glossary (Pages 13 20). Introduction to Financial Ratios When analyzing computing financial ratios and when doing other

Preparing Financial Statements

Chapter 4 Preparing Financial Statements Learning Objectives: Learn about the qualitative characteristics of financial statements Learn about the importance of the income statement Learn how to prepare

Chapter 4 Preparing Financial Statements Learning Objectives: Learn about the qualitative characteristics of financial statements Learn about the importance of the income statement Learn how to prepare

SEMINAR PAPER PRESENTED TO CASHFLOW FINANCE AUSTRALIA

SEMINAR PAPER PRESENTED TO CASHFLOW FINANCE AUSTRALIA BY BLAIR PLEASH AND KATHLEEN VOURIS PARTNERS OF HALL CHADWICK Chartered Accountants and Business Advisors Sydney Melbourne Brisbane Level 40 Level

SEMINAR PAPER PRESENTED TO CASHFLOW FINANCE AUSTRALIA BY BLAIR PLEASH AND KATHLEEN VOURIS PARTNERS OF HALL CHADWICK Chartered Accountants and Business Advisors Sydney Melbourne Brisbane Level 40 Level

After completing Chapter 2, your students should be able to answer these questions:

Solution Manual for Financial Accounting A Business Process Approach 3rd Edition by Reimers Link full download solution manual: http://testbankcollection.com/download/solution-manual-for-financial-accountinga-business-process-approach-3rd-edition-by-reimers/

Solution Manual for Financial Accounting A Business Process Approach 3rd Edition by Reimers Link full download solution manual: http://testbankcollection.com/download/solution-manual-for-financial-accountinga-business-process-approach-3rd-edition-by-reimers/

Chapter 12. The statement of cash flows categorizes cash receipts and cash payments as operating, investing, and financing activities.

1 Chapter 12 2 The statement of cash flows is a major financial statement as are the income statement, balance sheet, and statement of stockholders' equity. The statement of cash flows is required whenever

1 Chapter 12 2 The statement of cash flows is a major financial statement as are the income statement, balance sheet, and statement of stockholders' equity. The statement of cash flows is required whenever

IFRS Bridging Manual

CMA CANADA PROFESSIONAL PROGRAMS February 2011 IFRS Bridging Manual Used with permission of CMA Ontario. No part of this document may be reproduced in any form without the permission of the copyright holder.

CMA CANADA PROFESSIONAL PROGRAMS February 2011 IFRS Bridging Manual Used with permission of CMA Ontario. No part of this document may be reproduced in any form without the permission of the copyright holder.

16 Statement of Cash Flows

Chapter 16 Statement of Cash Flows Learning Objectives: Learn about the purpose of the statement of cash flows Learn about the various sections of the statement of cash flows Learn how to prepare a statement

Chapter 16 Statement of Cash Flows Learning Objectives: Learn about the purpose of the statement of cash flows Learn about the various sections of the statement of cash flows Learn how to prepare a statement

Conceptual Framework (Revised) Issued June Conceptual Framework for Financial Reporting 2018

Issued June Conceptual Framework for Financial Reporting 2018") Conceptual Framework (Revised) Issued June 2018 Conceptual Framework for Financial Reporting 2018 COPYRIGHT Copyright 2018 Hong Kong Institute of Certified Public Accountants This Framework contains the

Conceptual Framework (Revised) Issued June 2018 Conceptual Framework for Financial Reporting 2018 COPYRIGHT Copyright 2018 Hong Kong Institute of Certified Public Accountants This Framework contains the

Chapter 2: Financial Statements and the Annual Report

True / False 1. Financial statements are intended to tell the reader the value of a company. False LEARNING OBJECTIVES: FACC.PONO.13.02-01 - LO: 03-01 2. Accountants are the main reason financial statements

True / False 1. Financial statements are intended to tell the reader the value of a company. False LEARNING OBJECTIVES: FACC.PONO.13.02-01 - LO: 03-01 2. Accountants are the main reason financial statements

The Conceptual Framework for Financial Reporting. The New name for Framework

The Conceptual Framework for Financial Reporting The New name for Framework 1 Earlier it was known as Framework for the Preparation and Presentation of Financial Statements 2 This presentation is based

The Conceptual Framework for Financial Reporting The New name for Framework 1 Earlier it was known as Framework for the Preparation and Presentation of Financial Statements 2 This presentation is based

UNDERSTANDING FINANCIAL STATEMENTS

ITEM 8 UNDERSTANDING FINANCIAL STATEMENTS In this article, PDQ and XYZ refer to the companies on whose Board of Directors you will be serving. PDQ is a corporation. XYZ is a cooperative. It is important

ITEM 8 UNDERSTANDING FINANCIAL STATEMENTS In this article, PDQ and XYZ refer to the companies on whose Board of Directors you will be serving. PDQ is a corporation. XYZ is a cooperative. It is important

Full file at

Chapter 2 Preparing Financial Statements and Analyzing Business Transactions Multiple-Choice Questions 1. The primary objective of financial reporting is to provide a. external users with financial statements

Chapter 2 Preparing Financial Statements and Analyzing Business Transactions Multiple-Choice Questions 1. The primary objective of financial reporting is to provide a. external users with financial statements

Chapter 4. Funds-Flow Analysis and Forecasting. Overview of the Lecture. September The Statement of Cash Flows. Pro Forma Financial Statements

Chapter 4 Funds-Flow Analysis and Forecasting September 2004 Overview of the Lecture The Statement of Cash Flows Pro Forma Financial Statements 2 The Statement of Cash Flows The statement of cash flows

Chapter 4 Funds-Flow Analysis and Forecasting September 2004 Overview of the Lecture The Statement of Cash Flows Pro Forma Financial Statements 2 The Statement of Cash Flows The statement of cash flows

The Conceptual Framework for Financial Reporting

1. Introduction The Conceptual Framework sets out the concepts which underlie the preparation and presentation of financial statements for external users (Conceptual Framework, Section Purpose and status

1. Introduction The Conceptual Framework sets out the concepts which underlie the preparation and presentation of financial statements for external users (Conceptual Framework, Section Purpose and status

1 R E C A L =Revenue, Expense, Capital, Assets, Liability Decrease Increase R Revenue D Debit C Credit E Expense C Credit D Debit C Capital D Debit C Credit A Assets C Credit D Debit L Liability D Debit

1 R E C A L =Revenue, Expense, Capital, Assets, Liability Decrease Increase R Revenue D Debit C Credit E Expense C Credit D Debit C Capital D Debit C Credit A Assets C Credit D Debit L Liability D Debit

Introduction to Financial Statements

Introduction to Financial Statements Agenda In this session, you will learn about: Understanding Financial Statements The Accounting Process Accounting & Book-Keeping Financial Terminologies Accounting

Introduction to Financial Statements Agenda In this session, you will learn about: Understanding Financial Statements The Accounting Process Accounting & Book-Keeping Financial Terminologies Accounting

ANALYSIS OF THE FINANCIAL STATEMENTS

5 ANALYSIS OF THE FINANCIAL STATEMENTS CONTENTS PAGE STUDY OBJECTIVES 166 INTRODUCTION 167 METHODS OF STATEMENT ANALYSIS 167 A. ANALYSIS WITH THE AID OF FINANCIAL RATIOS 168 GROUPS OF FINANCIAL RATIOS

5 ANALYSIS OF THE FINANCIAL STATEMENTS CONTENTS PAGE STUDY OBJECTIVES 166 INTRODUCTION 167 METHODS OF STATEMENT ANALYSIS 167 A. ANALYSIS WITH THE AID OF FINANCIAL RATIOS 168 GROUPS OF FINANCIAL RATIOS

University of Palestine

Question 1: Multiple Choice: 1. A common measure of liquidity is a. Profit margin. b. Debt to equity. c. Return on assets. d. Accounts receivable turnover. 2. A high accounts receivable turnover ratio

Question 1: Multiple Choice: 1. A common measure of liquidity is a. Profit margin. b. Debt to equity. c. Return on assets. d. Accounts receivable turnover. 2. A high accounts receivable turnover ratio

IFRS Conceptual Framework Conceptual Framework for Financial Reporting

March 2018 IFRS Conceptual Framework Conceptual Framework for Financial Reporting Conceptual Framework for Financial Reporting Conceptual Framework for Financial Reporting is issued by the International

March 2018 IFRS Conceptual Framework Conceptual Framework for Financial Reporting Conceptual Framework for Financial Reporting Conceptual Framework for Financial Reporting is issued by the International

ACCT2542 Week 1 Notes

ACCT2542 Week 1 Notes Chapter 1: History, Current Regulatory Structures and Processes Australian Standard-Setting Arrangements: There are five main bodies which formulate and/or enforce accounting regulations

ACCT2542 Week 1 Notes Chapter 1: History, Current Regulatory Structures and Processes Australian Standard-Setting Arrangements: There are five main bodies which formulate and/or enforce accounting regulations

*Define and differentiate the accrual method and cash method of recording transactions.

Accounting 1 *Define and differentiate the terms accounting, auditing, and bookkeeping: --Accounting the process of recording, reporting and analyzing financial transactions. --Bookkeeping the process

Accounting 1 *Define and differentiate the terms accounting, auditing, and bookkeeping: --Accounting the process of recording, reporting and analyzing financial transactions. --Bookkeeping the process

n Financial Statement Analysis n Dollar and Percentage Changes n Common Sized Statements n Ratio Analysis McGraw-Hill /Irwin McGraw-Hill /Irwin

14-1 Today s Agenda Management Accounting Lecture 3 (Chapter 14) Financial Statement Analysis Bangor University Transfer Abroad Programme n Financial Statement Analysis n Dollar and Percentage Changes

14-1 Today s Agenda Management Accounting Lecture 3 (Chapter 14) Financial Statement Analysis Bangor University Transfer Abroad Programme n Financial Statement Analysis n Dollar and Percentage Changes

WEEK 10 Analysis of Financial Statements

WEEK 10 Analysis of Financial Statements Learning Objectives 1. Organize a systematic financial statements analysis using common-size financial statements and ratio analysis. 2. Recognize the potential

WEEK 10 Analysis of Financial Statements Learning Objectives 1. Organize a systematic financial statements analysis using common-size financial statements and ratio analysis. 2. Recognize the potential

Framework for the Preparation and Presentation of Financial Statements

Framework for the Preparation and Presentation of Financial Statements The IASB Framework was approved by the IASC Board in April 1989 for publication in July 1989, and adopted by the IASB in April 2001.

Framework for the Preparation and Presentation of Financial Statements The IASB Framework was approved by the IASC Board in April 1989 for publication in July 1989, and adopted by the IASB in April 2001.

Accounting Definitions. Definitions

Accounting Definitions Definitions What s Here Introduction Definitions Introduction This training contains definitions of common accounting terms. If you come across accounting or financial terms with

Accounting Definitions Definitions What s Here Introduction Definitions Introduction This training contains definitions of common accounting terms. If you come across accounting or financial terms with

Financial Accounting. (Exam)

") Financial Accounting (Exam) Your AccountingCoach PRO membership includes lifetime access to all of our materials. Take a quick tour by visiting www.accountingcoach.com/quicktour. Table of Contents (click

Financial Accounting (Exam) Your AccountingCoach PRO membership includes lifetime access to all of our materials. Take a quick tour by visiting www.accountingcoach.com/quicktour. Table of Contents (click

Accounting Basics, Part 1

Accounting Basics, Part 1 Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts, Journals and, Ledger Part 1 What s Here Introduction Business Types Business Organization Professional Advice

Accounting Basics, Part 1 Accrual, Double-Entry Accounting, Debits & Credits, Chart of Accounts, Journals and, Ledger Part 1 What s Here Introduction Business Types Business Organization Professional Advice

Financial statements. Chapter One-A. A- Statements of cash flows. 1 IAS 7 Statement of cash flows F5(a)-(h)

-(h)") Chapter One-A Financial statements A- Statements of cash flows Topic list Syllabus reference 1 IAS 7 Statement of cash flows F5(a)-(h) 2 Preparing a statement of cash flows F5(g) Introduction In the long

Chapter One-A Financial statements A- Statements of cash flows Topic list Syllabus reference 1 IAS 7 Statement of cash flows F5(a)-(h) 2 Preparing a statement of cash flows F5(g) Introduction In the long

Detailed Alert International Accounting Standards: Framework for the Preparation and Presentation of Financial Statements (1989) Preface

Preface") Abstract The Framework for the Preparation and Presentation of Financial Statements sets out the concepts that underlie the preparation and presentation of financial statements for external users. The

Abstract The Framework for the Preparation and Presentation of Financial Statements sets out the concepts that underlie the preparation and presentation of financial statements for external users. The

CHAPTER 2: FINANCIAL STATEMENTS AND THE ANNUAL REPORT

Using Financial Accounting Information The Alternative to Debits and Credits 9th Edition Porter Test Bank Full Download: http://testbanklive.com/download/using-financial-accounting-information-the-alternative-to-debits-and-credits-9th-

Using Financial Accounting Information The Alternative to Debits and Credits 9th Edition Porter Test Bank Full Download: http://testbanklive.com/download/using-financial-accounting-information-the-alternative-to-debits-and-credits-9th-

Not For Sale. Overview of Financial Statements FACMU14. Cengage Learning. All rights reserved. No distribution allowed without express authorization.

Overview of Financial Statements FACMU14 P a r t 1 23450_ch01_ptg01_lores_001-040.indd 1 5/1/12 9:08 PM 23450_ch01_ptg01_lores_001-040.indd 2 5/1/12 9:08 PM Chapter Introduction to Business Activities

Overview of Financial Statements FACMU14 P a r t 1 23450_ch01_ptg01_lores_001-040.indd 1 5/1/12 9:08 PM 23450_ch01_ptg01_lores_001-040.indd 2 5/1/12 9:08 PM Chapter Introduction to Business Activities

IFRS. B V Subramaniam FCMA A CONCEPTUAL ANALYSIS

IFRS 1 A CONCEPTUAL ANALYSIS INTRODUCTION International Financial Reporting Standards (IFRS) are the world-wide accounting standards which consists of 1) Standards (IFRS statements & IAS standards) 2)

IFRS 1 A CONCEPTUAL ANALYSIS INTRODUCTION International Financial Reporting Standards (IFRS) are the world-wide accounting standards which consists of 1) Standards (IFRS statements & IAS standards) 2)

The Conceptual Framework for Financial Reporting

The Conceptual Framework for Financial Reporting The Conceptual Framework was issued by the IASB in September 2010. It superseded the Framework for the Preparation and Presentation of Financial Statements.

The Conceptual Framework for Financial Reporting The Conceptual Framework was issued by the IASB in September 2010. It superseded the Framework for the Preparation and Presentation of Financial Statements.

Financial Statement OBJECTIVES

Chapter 2 Analysis of Financial Statement OBJECTIVES At the end of this chapter, you should able to: 1. identify the accounts contained in the income statement and in the balance sheet; 2. prepare the

Chapter 2 Analysis of Financial Statement OBJECTIVES At the end of this chapter, you should able to: 1. identify the accounts contained in the income statement and in the balance sheet; 2. prepare the

Framework for the Preparation and Presentation of Financial Statements

for the Preparation and Presentation of Financial Statements The IASB was approved by the IASC Board in April 1989 for publication in July 1989, and adopted by the IASB in April 2001. IASCF B1709 CONTENTS

for the Preparation and Presentation of Financial Statements The IASB was approved by the IASC Board in April 1989 for publication in July 1989, and adopted by the IASB in April 2001. IASCF B1709 CONTENTS

Fin-621 Final term Solved Papers by Fahad Yusha Cell: and

FINALTERM EXAMINATION Spring 2010 FIN621- Financial Statement Analysis (Session - 1) : 90 min Marks: 69 Question No: 1 ( Marks: 1 ) - Please choose one Which one of the following is NOT a type of adjusting

FINALTERM EXAMINATION Spring 2010 FIN621- Financial Statement Analysis (Session - 1) : 90 min Marks: 69 Question No: 1 ( Marks: 1 ) - Please choose one Which one of the following is NOT a type of adjusting

FRAMEWORK FOR THE PREPARATION AND PRESENTATION OF FINANCIAL STATEMENTS

FRAMEWORK FOR THE PREPARATION AND PRESENTATION OF FINANCIAL STATEMENTS CONTENTS Paragraphs PREFACE INTRODUCTION 1 11 Purpose and status 1 4 Scope 5 8 Users and their information needs 9 11 THE OBJECTIVE

FRAMEWORK FOR THE PREPARATION AND PRESENTATION OF FINANCIAL STATEMENTS CONTENTS Paragraphs PREFACE INTRODUCTION 1 11 Purpose and status 1 4 Scope 5 8 Users and their information needs 9 11 THE OBJECTIVE

FINANCIAL REPORTING: ITS CONCEPTUAL FRAMEWORK

2 FINANCIAL REPORTING: ITS CONCEPTUAL FRAMEWORK CHAPTER OBJECTIVES After careful study of this chapter, students will be able to: 1. Explain the FASB conceptual framework. 2. Understand the relationship

2 FINANCIAL REPORTING: ITS CONCEPTUAL FRAMEWORK CHAPTER OBJECTIVES After careful study of this chapter, students will be able to: 1. Explain the FASB conceptual framework. 2. Understand the relationship

SHORT QUESTIONS ANSWERS FINANCIAL MANAGEMENT MGT201 By

SHORT QUESTIONS ANSWERS FINANCIAL MANAGEMENT MGT201 By http://vustudents.ning.com 1- What is Financial Management? The procedure of managing the financial resources, as well as accounting and financial

SHORT QUESTIONS ANSWERS FINANCIAL MANAGEMENT MGT201 By http://vustudents.ning.com 1- What is Financial Management? The procedure of managing the financial resources, as well as accounting and financial

The statement of cash flows reports cash flows, cash receipts, and cash payments, to show where cash came from and how it was spent.

Accounting Fundamentals Lesson 10 10.0 Cash Flow Statement The balance sheet reports financial position, and balance sheets from two periods show whether cash increased or decreased. But that doesn t tell

Accounting Fundamentals Lesson 10 10.0 Cash Flow Statement The balance sheet reports financial position, and balance sheets from two periods show whether cash increased or decreased. But that doesn t tell

FUNDAMENTAL ANALYSIS

FUNDAMENTAL ANALYSIS I. Introduction II. Quantitative/Qualitative III. Company / Industry IV. Financial Statements V. Balance Sheet VI. Cash Flow Statement VII. Income Statement a. Management Discussion

FUNDAMENTAL ANALYSIS I. Introduction II. Quantitative/Qualitative III. Company / Industry IV. Financial Statements V. Balance Sheet VI. Cash Flow Statement VII. Income Statement a. Management Discussion

Cambridge IGCSE Accounting (0452)

") www.xtremepapers.com Cambridge IGCSE Accounting (0452) International Accounting Standards (IAS) Guidance for Teachers Contents Introduction... 2 Use of this document... 2 Users of financial statements...

www.xtremepapers.com Cambridge IGCSE Accounting (0452) International Accounting Standards (IAS) Guidance for Teachers Contents Introduction... 2 Use of this document... 2 Users of financial statements...

The Conceptual Framework for Financial Reporting

The Conceptual Framework for Financial Reporting The Conceptual Framework was issued by the International Accounting Standards Board in September 2010. It superseded the Framework for the Preparation and

The Conceptual Framework for Financial Reporting The Conceptual Framework was issued by the International Accounting Standards Board in September 2010. It superseded the Framework for the Preparation and

Accounting Functions. The various financial statements are- Income Statement Balance Sheet

Accounting Functions The accounting system provides a structure of maintaining details of business transactions that represent the finances of the organization. The various financial statements are- Income

Accounting Functions The accounting system provides a structure of maintaining details of business transactions that represent the finances of the organization. The various financial statements are- Income

07/10/2013. Chapter 18. Financial statement analysis part a, Session 11

Chapter 18 Financial statement analysis part a, Session 11 PowerPoint to accompany: Learning objectives Perform a horizontal analysis of financial statements Perform a vertical analysis of financial statements

Chapter 18 Financial statement analysis part a, Session 11 PowerPoint to accompany: Learning objectives Perform a horizontal analysis of financial statements Perform a vertical analysis of financial statements

The Conceptual Framework for Financial Reporting

The Conceptual Framework for Financial Reporting CONTENTS THE CONCEPTUAL FRAMEWORK FOR FINANCIAL REPORTING paragraphs INTRODUCTION Purpose and status Scope CHAPTERS 1 The objective of general purpose financial

The Conceptual Framework for Financial Reporting CONTENTS THE CONCEPTUAL FRAMEWORK FOR FINANCIAL REPORTING paragraphs INTRODUCTION Purpose and status Scope CHAPTERS 1 The objective of general purpose financial

Chapters 1-4 (Part One)

") Profession of Accounting Chapters 1-4 (Part One) The accounting profession is varied. It includes private accounting, where accountants work for their clients (e.g., Controllers). It also includes public

Profession of Accounting Chapters 1-4 (Part One) The accounting profession is varied. It includes private accounting, where accountants work for their clients (e.g., Controllers). It also includes public

Learning Objective. LO1 Prepare an income statement for a merchandising business organized as a corporation.

Learning Objective LO1 Prepare an income statement for a merchandising business organized as a corporation. Lesson 16-1 Uses of Financial Statements LO1 A corporation prepares an income statement and a

Learning Objective LO1 Prepare an income statement for a merchandising business organized as a corporation. Lesson 16-1 Uses of Financial Statements LO1 A corporation prepares an income statement and a

Prepared by Cyberian

; and Which of the following is/are the component(s) of equity? Share Capital Reserves Share Premium In which of the following activities, a business should capitalize its incurred expenditures according

; and Which of the following is/are the component(s) of equity? Share Capital Reserves Share Premium In which of the following activities, a business should capitalize its incurred expenditures according

Accounting Standard for Business Enterprises- Basic Standard

Accounting Standard for Business Enterprises- Basic Standard Chapter 1 General Provisions Article 1 In accordance with The Accounting Law of the People s Republic of China and other relevant laws and regulations,

Accounting Standard for Business Enterprises- Basic Standard Chapter 1 General Provisions Article 1 In accordance with The Accounting Law of the People s Republic of China and other relevant laws and regulations,

Week 4 and Week 5 Handout Financial Statement Analysis

Week 4 and Week 5 Handout Financial Statement Analysis Introduction After understanding the basic financial statements, one may be interested in analysing the financial statements to understand the performance

Week 4 and Week 5 Handout Financial Statement Analysis Introduction After understanding the basic financial statements, one may be interested in analysing the financial statements to understand the performance

Nature of Business and Accounting

Nature of Business and Accounting A business is an organization in which basic resources (inputs), such as materials and labor, are assembled and processed to provide goods or services (outputs) to customers.

Nature of Business and Accounting A business is an organization in which basic resources (inputs), such as materials and labor, are assembled and processed to provide goods or services (outputs) to customers.

Statement of Financial Accounting Standards No. 17. Statements of Financial Accounting Standards No.17. Statement of Cash Flows

Statement of Financial Accounting Standards No. 17 Statements of Financial Accounting Standards No.17 Statement of Cash Flows Revised on 22 September 2005 Translated by TsingZai Wu, Associate Professor

Statement of Financial Accounting Standards No. 17 Statements of Financial Accounting Standards No.17 Statement of Cash Flows Revised on 22 September 2005 Translated by TsingZai Wu, Associate Professor

Framework for the Preparation and Presentation of Financial Statements

for the Preparation and Presentation of Financial Statements CONTENTS paragraphs PREFACE INTRODUCTION 1-11 Purpose and status 1-4 Scope 5-8 Users and their information needs 9-11 THE OBJECTIVE OF FINANCIAL

for the Preparation and Presentation of Financial Statements CONTENTS paragraphs PREFACE INTRODUCTION 1-11 Purpose and status 1-4 Scope 5-8 Users and their information needs 9-11 THE OBJECTIVE OF FINANCIAL

International Financial Reporting Standard (IFRS) for Small and Medium-sized Entities

for Small and Medium-sized Entities") International Financial Reporting Standard (IFRS) for Small and Medium-sized Entities Section 1 Small and Medium-sized Entities Intended scope of this Standard 1.1 The IFRS for SMEs is intended for use

International Financial Reporting Standard (IFRS) for Small and Medium-sized Entities Section 1 Small and Medium-sized Entities Intended scope of this Standard 1.1 The IFRS for SMEs is intended for use

2/2/2009. Financial statement EARNING POWER AND IRREGULAR ITEMS. EARNING POWER AND IRREGULAR ITEMS continued. Chapter 14

Chapter 14 Financial statement analysis PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd EARNING POWER AND IRREGULAR ITEMS Earning power refers to

Chapter 14 Financial statement analysis PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd EARNING POWER AND IRREGULAR ITEMS Earning power refers to

Framework for the Preparation and Presentation of Financial Statements

10 Framework for the Preparation and Presentation of Financial Statements Contents INTRODUCTION Paragraphs 1-11 Purpose and Status 1-4 Scope 5-8 Users and Their Information Needs 9-11 THE OBJECTIVE OF

10 Framework for the Preparation and Presentation of Financial Statements Contents INTRODUCTION Paragraphs 1-11 Purpose and Status 1-4 Scope 5-8 Users and Their Information Needs 9-11 THE OBJECTIVE OF

Introduction. Accounting Standards for the Public Sector

Introduction Accounting Standards for the Public Sector The International Public Sector Accounting Standards Board (the IPSASB) of the International Federation of Accountants (IFAC) develops accounting

Introduction Accounting Standards for the Public Sector The International Public Sector Accounting Standards Board (the IPSASB) of the International Federation of Accountants (IFAC) develops accounting

EUROPEAN PUBLIC SECTOR ACCOUNTING STANDARDS

EUROPEAN COMMISSION EUROSTAT Directorate C: National Accounts, Prices and Key Indicators Task Force EPSAS EPSAS WG 18/07 Luxembourg, 25 April 2018 EUROPEAN PUBLIC SECTOR ACCOUNTING STANDARDS CONCEPTUAL

EUROPEAN COMMISSION EUROSTAT Directorate C: National Accounts, Prices and Key Indicators Task Force EPSAS EPSAS WG 18/07 Luxembourg, 25 April 2018 EUROPEAN PUBLIC SECTOR ACCOUNTING STANDARDS CONCEPTUAL

WHITE PAPER UNDERSTANDING FINANCIAL STATEMENTS

WHITE PAPER UNDERSTANDING FINANCIAL STATEMENTS Contents 1.0 Understanding Financial Statements... 3 2.0 Types of Financial Statements... 3 3.0 Balance Sheets... 3 4.0 Profit & Loss Statement (also known

WHITE PAPER UNDERSTANDING FINANCIAL STATEMENTS Contents 1.0 Understanding Financial Statements... 3 2.0 Types of Financial Statements... 3 3.0 Balance Sheets... 3 4.0 Profit & Loss Statement (also known

Understand Financial Statements and Identify Sources of Farm Financial Risk

Agricultural Finance Understand Financial Statements and Identify Sources of Farm Financial Risk By analyzing a complete set of your farm s financial statements you can identify sources and amounts of

Agricultural Finance Understand Financial Statements and Identify Sources of Farm Financial Risk By analyzing a complete set of your farm s financial statements you can identify sources and amounts of

CHAPTER 1 Introduction to financial statements

CHAPTER 1 Introduction to financial statements CHAPTER OVERVIEW Chapter 1 introduces you to a variety of financial accounting topics. You will learn about the main forms of business organisation, and the

CHAPTER 1 Introduction to financial statements CHAPTER OVERVIEW Chapter 1 introduces you to a variety of financial accounting topics. You will learn about the main forms of business organisation, and the

Statement of Cash Flows

May 5, 2014 Statement of Cash Flows Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Today s Agenda n Cash Flow Statements n What Cash Flow Statements show us n Building a Cash Flow

May 5, 2014 Statement of Cash Flows Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Today s Agenda n Cash Flow Statements n What Cash Flow Statements show us n Building a Cash Flow

RATIO ANALYSIS. The preceding chapters concentrated on developing a general but solid understanding

C H A P T E R 4 RATIO ANALYSIS I N T R O D U C T I O N The preceding chapters concentrated on developing a general but solid understanding of accounting principles and concepts and their applications to

C H A P T E R 4 RATIO ANALYSIS I N T R O D U C T I O N The preceding chapters concentrated on developing a general but solid understanding of accounting principles and concepts and their applications to

CAMBODIAN ACCOUNTING STANDARDS (CAS)

") CAMBODIAN ACCOUNTING STANDARDS (CAS) 1 - CAS 1 : Presentation of Financial Statements an Audit of Financial Statements 2 - CAS 2 : Inventories 3 - CAS 7 : Cash Flow Statements 4 - CAS 8 : Net profit or

CAMBODIAN ACCOUNTING STANDARDS (CAS) 1 - CAS 1 : Presentation of Financial Statements an Audit of Financial Statements 2 - CAS 2 : Inventories 3 - CAS 7 : Cash Flow Statements 4 - CAS 8 : Net profit or

The Conceptual Framework for Financial Reporting

The Conceptual Framework for Financial Reporting The Conceptual Framework for Financial Reporting (the Conceptual Framework) was issued by the International Accounting Standards Board in September 2010.

The Conceptual Framework for Financial Reporting The Conceptual Framework for Financial Reporting (the Conceptual Framework) was issued by the International Accounting Standards Board in September 2010.

Learning Objectives. Chapter 5. Balance Sheet. Learning Objective 1, 2, 3. Liquidity. Chapter Overview. Balance Sheet and Statement of Cash Flows

Chapter 5 Balance Sheet and Statement of Cash Flows Campbell, Coca-Cola, American Airlines, Borders Learning Objectives 1. Explain uses, limitations of a balance sheet 2. Identify major classifications

Chapter 5 Balance Sheet and Statement of Cash Flows Campbell, Coca-Cola, American Airlines, Borders Learning Objectives 1. Explain uses, limitations of a balance sheet 2. Identify major classifications

UNIT 6 FINANCIAL STATEMENTS: ANALYSIS AND INTERPRETATION MODULE - 2

UNIT 6 FINANCIAL STATEMENTS: ANALYSIS AND INTERPRETATION MODULE - 2 UNIT 6 FINANCIAL STATEMENTS: ANALYSIS AND INTERPRETATION Financial Statements: Structure 6.0 Introduction 6.1 Unit Objectives 6.2 Relationship

UNIT 6 FINANCIAL STATEMENTS: ANALYSIS AND INTERPRETATION MODULE - 2 UNIT 6 FINANCIAL STATEMENTS: ANALYSIS AND INTERPRETATION Financial Statements: Structure 6.0 Introduction 6.1 Unit Objectives 6.2 Relationship

Full file at https://fratstock.eu

CHAPTER 2 A FURTHER LOOK AT FINANCIAL STATEMENTS SUMMARY OF QUESTIONS BY STUDY OBJECTIVE AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 K 12. 3 C

CHAPTER 2 A FURTHER LOOK AT FINANCIAL STATEMENTS SUMMARY OF QUESTIONS BY STUDY OBJECTIVE AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 K 12. 3 C

Statement of Cash Flows

JWCL162_c13_582-643.qxd 8/13/09 1:09 PM Page 582 chapter 13 Statement of Cash Flows the navigator Scan Study Objectives Read Feature Story Read Preview Read Text and answer Do it! p. 588 p. 595 p. 599

JWCL162_c13_582-643.qxd 8/13/09 1:09 PM Page 582 chapter 13 Statement of Cash Flows the navigator Scan Study Objectives Read Feature Story Read Preview Read Text and answer Do it! p. 588 p. 595 p. 599

Understanding Where You Stand

SMALL BUSINESS Access to Opportunity Understanding Where You Stand A Simple Guide to Your Company s Financial Statements Reading Your Statements Balance Sheets Income Statements Ratios Cash Flow Statements

SMALL BUSINESS Access to Opportunity Understanding Where You Stand A Simple Guide to Your Company s Financial Statements Reading Your Statements Balance Sheets Income Statements Ratios Cash Flow Statements

Business Ratios. Current Ratio

Current Ratio Business Ratios Measures whether or not the firm has enough resources to pay its debt over the next 12 months formula: Current Ratio = Current Assets Current Liabilities Acceptable ratios

Current Ratio Business Ratios Measures whether or not the firm has enough resources to pay its debt over the next 12 months formula: Current Ratio = Current Assets Current Liabilities Acceptable ratios

6. Chapter 1 Question TF #6 A firm makes investments to obtain productive capacity to carry out its business activities.

1. Chapter 1 Question TF #1 The managers of a business prepare financial statements to present meaningful information about that business s activities to external users, *a. True b. False 2. Chapter 1

1. Chapter 1 Question TF #1 The managers of a business prepare financial statements to present meaningful information about that business s activities to external users, *a. True b. False 2. Chapter 1

Ch.2 A Review of the Accounting Cycle

Ch.2 A Review of the Accounting Cycle 1. Basic steps in the accounting process (accounting cycle) 2. Analyze transactions and make and post journal entries 3. Make adjusting entries, produce financial

Ch.2 A Review of the Accounting Cycle 1. Basic steps in the accounting process (accounting cycle) 2. Analyze transactions and make and post journal entries 3. Make adjusting entries, produce financial

CHAPTER 2 THE FRAMEWORK OF INTERNATIONAL ACCOUNTING STANDARD BOARD (IASB) INTRODUCTION

INTRODUCTION") CHAPTER 2 THE FRAMEWORK OF INTERNATIONAL ACCOUNTING STANDARD BOARD (IASB) INTRODUCTION In order to narrowing the differences in recognition and measurement of elements of financial statements and harmonization

CHAPTER 2 THE FRAMEWORK OF INTERNATIONAL ACCOUNTING STANDARD BOARD (IASB) INTRODUCTION In order to narrowing the differences in recognition and measurement of elements of financial statements and harmonization

PREVIEW OF CHAPTER 5-2

5-1 PREVIEW OF CHAPTER 5 5-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 5 and Statement of Cash Flows Statement of Financial Position LEARNING OBJECTIVES After studying this

5-1 PREVIEW OF CHAPTER 5 5-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 5 and Statement of Cash Flows Statement of Financial Position LEARNING OBJECTIVES After studying this

FEAR out. Taking the FEAR of Financial Statement Analysis. Toni Drake, CCE TRM Financial Services, Inc.

FEAR out Taking the FEAR of Financial Statement Analysis Toni Drake, CCE TRM Financial Services, Inc. FINANCIAL STATEMENTS Components of a Financial Statement Balance Sheet Income Statement Statement of

FEAR out Taking the FEAR of Financial Statement Analysis Toni Drake, CCE TRM Financial Services, Inc. FINANCIAL STATEMENTS Components of a Financial Statement Balance Sheet Income Statement Statement of

A balance sheet provides detailed information about a company s assets, liabilities and shareholders equity.

Beginners' Guide to Financial Statements The Basics If you can read a nutrition label or a baseball box score, you can learn to read basic financial statements. If you can follow a recipe or apply for

Beginners' Guide to Financial Statements The Basics If you can read a nutrition label or a baseball box score, you can learn to read basic financial statements. If you can follow a recipe or apply for

Reading Financial Statements to Aid in Business Decision-Making. Copyright 2015 by IndustriusCFO, A C-Leveled Company

Copyright 2015 by All rights reserved. No patent liability is assumed with respect to the use of the information contained herein. Although every precaution has been taken in the preparation of this book,

Copyright 2015 by All rights reserved. No patent liability is assumed with respect to the use of the information contained herein. Although every precaution has been taken in the preparation of this book,