16 Statement of Cash Flows

|

|

|

- Julius Stokes

- 5 years ago

- Views:

Transcription

1 Chapter 16 Statement of Cash Flows Learning Objectives: Learn about the purpose of the statement of cash flows Learn about the various sections of the statement of cash flows Learn how to prepare a statement of cash flows using the indirect method Learn how to prepare a statement of cash flows using the direct method Learn how to prepare the investing section of the statement of cash flows Learn how to prepare the financing section of the statement of cash flows Learn about required disclosures of noncash activities

2 Purpose of the Statement of Cash Flows Learning Objective: Learn about the purpose of the statement of cash flows The statement of cash flows is designed to summarize an entity s cash inflows and outflows during a period of time. Cash inflows are reported as positive amounts and cash outflows are reported as negative amounts. The cash flows are changed by operating, investing and financing activities. A central focus of the statement of cash flows is to provide users with information about an entity s liquidity. Liquidity is a firm s ability to meet its obligations as they come due which most often are settled in the form of cash or cash equivalents. A firm that is able to meet its obligations as they come due is called being solvent. A secondary objective of the statement of cash flows is organizing the information in such a manner that it provides information on the type of cash flows by source. The three sources of cash flows are: operating, investing and financing activities. A financial statement user would need to be able to determine how much cash inflows/outflows are being generated by business operations. Furthermore, the user would need to be able to figure out how other non-operating cash flows (investing or financing) are being generated or used. The statement of cash flows is an integral part of a full set of financial statements Cash and Cash Equivalents Defined Cash is defined as money in coins or currency as well as funds in bank accounts that are available on demand. A cash equivalent is defined as liquid, short-term investments that have the following characteristics: Convertible into a specific amount of cash within a short period of time. The risk of change in value due to fluctuating interest rates is very low. This requirement generally means the asset is within 3 months of maturity and is low risk. 2

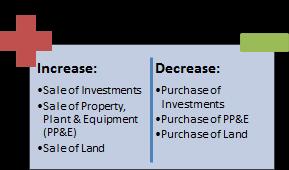

3 Structure of The Statement of Cash Flows Learning Objective: Learn about the various sections of the statement of cash flows The statement of cash flows is organized based on operating activities, investing activities and financing activities classifications. Operating Activities Cash flows from this source include cash inflows and outflows that occur from the company s primary business operations. This section often includes transaction data that is included on the income statement. Current assets and current liabilities are included in this section. However, current liabilities associated with long-term notes/bonds are not included in this section. They are included in financing activities. Some examples of transactions that would be considered operating activities would be: cash receipts from customers or cash payments to suppliers for inventory purchases. Investing Activities This section involves the sale and purchase of noncurrent assets (long-term assets). Examples of noncurrent assets included in this section are property, plant and equipment (PP&E), and stock investments (securities) other than the company's own stock. Financing Activities This section involves liabilities related to investors, shareholders or creditors. It also includes transactions that involve paying shareholders, investors or repaying creditors. Examples of transactions include: borrowing funds or repaying funds through the use of bonds, sale of stock, or paying dividends. As a general rule, this section revolves around noncurrent liabilities and equity transactions (owner s equity). The following chart summarizes typical transactions that affect each section of the statement of cash flows: 3

4 4

5 The following is a typical statement of cash flows (prepared using the indirect method, discussed later): As you can see, the statement is organized by operating, investing and financing cash flow sections. The noncash cash flow section is for transaction that do not involve an exchange of cash. For those transactions, the transaction was conducted without an effect on cash. The ending cash balance at the end of the year ($11,031,000) will equal the cash balance as reported on the December 31st, 2016 balance sheet. 5

6 Now that we have a high-level overview of the statement of cash flows, we will move on to discussing each section of the statement of cash flows in greater detail. Our discussion will focus on the overall theory behind each section followed by relevant calculations for each section Operating Section As mentioned earlier, the operating section is focused on cash inflows and outflows from primary operations which impacts current assets and current liabilities. The goal of this section is to calculate an ending balance called net cash provided by (used by) operating activities. To calculate this balance, we can use one of two methods: the direct method or the indirect method. Both methods will calculate the exact same ending balance for the operating cash flows. We will discuss the difference between the two methods as we calculate each method. We will be learning how to calculate operating cash flows using both methods Operating Section: Indirect Method Learning Objective: Learn how to prepare a statement of cash flows using the indirect method. The indirect method begins with net income as reported on the income statement. We then adjust that amount by adding or subtracting non-cash accounts that were originally used to calculate net income. If you recall from our chapter on the income statement, you will remember that non-cash accounts were either added or subtracted to calculate net income. Using the indirect method, we will remove the impact of all accounts that were non-cash. We then follow up by adding or subtracting accounts that have an impact on cash. In essence, we are going from an accrual-basis net income amount to a cash-basis calculation of cash flows by adding or subtracting specific accounts. The indirect method is used more often due to the accounting information needing to prepare it being readily available without much additional effort. 6

7 The general format of the indirect method presentation is as follows: We will now do a step-by-step example and explain each step in detail. To calculate operating cash flows using the indirect method we will begin by analyzing changes in noncash balance sheet accounts. The reason the indirect method works is because of the interrelations between accounts in the accounting equation. If you recall from earlier chapters, you will remember that assets = liabilities + owner's equity. If we analyze the accounting equation with cash involved, we can better understand how the indirect method works. Cash is an asset so we can separate the asset account into noncash assets and cash. We end up getting the following equations: Cash + Noncash Assets = Liabilities + Owner's Equity Using simple algebra, we can get the following: Cash = Liabilities + Owner's Equity - Noncash Assets As we quickly realize, we can determine a change in cash by determining the changes in Liabilities, owner's equity and noncash asset accounts. The following equation demonstrates this: Change in Cash = Change in Liabilities + Change in Owner's Equity - Change in Noncash Assets We then proceed to use the Income Statement and Balance Sheet to determine these changes. The first step is to determine what is the net income for the period as this is the first line item reported. To determine the net income, we will be analyzing the income statement. 7

8 STEP 1: Determine Net Income If the income statement is not already prepared then we must prepare it to calculate our net income for the period in question. Chapter 4 lists how to prepare an income statement. In this case, we will use the following income statement to determine net income: 8

9 As you can see the company had net income of $4,750 for the previous 12-month period. Remember the net income amount used must match the amount for the period that we are preparing the statement of cash flows for. If we are preparing a quarterly (3 month) statement of cash flows then we must use net income for the exact same 3 months. In this case, we are preparing an annual statement of cash flows so we can use the net income from this income statement. The $4,750 will be the first line reported for the operating section of our statement of cash flows. 9

10 STEP 2: Convert Accrual Basis Net Income to Cash Basis The $4,750 net income number we have is an amount that is based on accrual basis of accounting. We will have to convert this net income number into a cash basis amount by adjusting it for non-cash transactions that are factored in when using accrual basis. We do this by analyzing comparative changes in balance sheet and income statement accounts. These adjustments are reflected on the statement of cash flows operating section under the "adjustments to reconcile net income to net cash flows provided by operating activities" section. When performing our balance sheet and income statement analysis, we must reverse the following accrual accounting effects on net income: Impact of noncash current operating assets and current liabilities are adjusted: Deduct increases in current noncash operating assets Add decreases in current noncash operating assets Add increases in current noncash current liabilities Deduct decreases in current noncash current liabilities Example: A company sells inventory on credit and increases an account receivable by $5,000. The $5,000 increase in account receivables would reduce net income by $5,000. This is because the increase in account receivable also increased net income when it was originally recorded. Reverse impact of noncash expenses When noncash expenses are factored into net income on the accrual basis this results in a lower amount of net income reported. Since these accounting entries do not reflect a cash outflow we must reverse those expenses by adding them back. By adding them back we are converting the net income from an accrual basis to a cash basis. Add noncash expenses such as depreciation or amortization. 10

11 Example: A company buys a vehicle for $10,000 and depreciates it over 10 years. In the first year, the company recorded $1,000 depreciation expense related to the vehicle. The company will add the depreciation back to net income when preparing the statement of cash flows. Reverse impact of gains and losses on sale of assets When an asset is sold the amount of gain or loss is factored into the net income account when prepared on an accrual basis. Therefore, to eliminate this impact we must reverse the impact. Add losses on the sale of assets Deduct gains on the sale of assets Example: A building is sold for $25,000 which was originally purchased for $20,000. The $5,000 gain is deducted from net income. The reason is because the $5,000 gain was originally added to net income when it was prepared on the accrual basis. The following chart summarizes these adjustments based on account: Add to Net Income Deduct from Net Income Depreciation Amortization of intangible assets Decrease in receivables Losses on Assets Increase in receivables Gains on Assets Decrease in inventory Increase in accounts payable Increase in inventory Decrease in accounts payable Increase in accrued liabilities Decrease in prepaid expenses Decrease in accrued liabilities Increase in prepaid expenses 11

12 Increase in income tax payable Decrease in income tax payable Preparing the Statement of Cash Flows Using the Indirect Method (Comprehensive Example) In our example, we are given an income statement and a comparative balance sheet. We will use these two financial statements to prepare our statement of cash flows. The income statement and the comparative balance sheet are shown below: 12

13 Calculate Net Income The statement of cash flows using the indirect method starts with determining net income. In this case, determining net income is quite simple because we can reference the income statement to see the net income which is $2,000. Convert the Accrual Basis Net Income Amount to Cash Basis Our next step is to convert our net income number from the accrual basis to the cash basis. We do this by adding or subtracting noncash amounts from the amount of net income. The best method to use for this step is to analyze the financial statements to determine what section of the statement of cash flows each account should be reported on. Each account should be reported in the operating, financing, or investing section. Certain amounts might also need to be disclosed on the statement of cash flows while other amounts will not need to be included in the statement of cash flows at all. Using the financial statements above, the following adjustments will need to be included in the operating section: 13

14 Depreciation Expense: The $5,000 of depreciation expense will need to be added back. When net income is calculated on the accrual basis, depreciation is subtracted which results in a reduction to net income. Depreciation is an accounting allocation and does not impact cash. Therefore, the depreciation expense is added back since it is not associated with a cash outflow. Adjust for Gains and Losses: The $3,000 loss on the sale of equipment must be added back. The reason it is added back is because loss does not represent a cash outflow and it is subtracted when calculating net income. Therefore, we must add it back. If the amount was a gain then it would be subtracted. The gross proceeds from sales of assets are reflected in the investing section which includes any gain or loss. Adjust for noncash current assets and current liabilities (excluding cash): Our example has two current assets and two current liabilities that are impacted by this step. The two current assets are: accounts receivable and inventory. The two current liabilities are: accounts payable and income tax payable. 1. Account receivable: We have a decrease of $5,000 for accounts receivable. Whenever we have a decrease in a a current asset we add it back. The logic behind this is quite simple. If accounts receivables are decreasing then it means the customers have paid you cash to decrease the receivable. If a current asset increases then we would subtract it. 2. Inventory: We have a decrease of $20,000 for inventories. If we have a decrease in a current asset then we add it back. If inventories are decreasing then that most likely means customers are buying the equipment and giving the business cash as a result. 3. Accounts payable: We have an increase of $12,000 for accounts payable which is a current liability. Whenever we have an increase in a current liability we add it back. If a current liability is increasing then that means we are agreeing to pay something in the future rather than in the current period. As a result, this means we have conserved our current cash instead of spent it. The opposite holds true if we have a decrease in an current liability - we subtract it. 14

15 4. Income Tax Payable: We have an increase of $5,000 for income tax payable. Since income tax payable is a current liability, the same logic is used as the accounts payable account. We must add all increases and subtract all decreases. We did not have any accrued expenses, amortization of intangibles or prepaid expenses. These accounts are still important so we will cover them briefly: Accrued Expenses: An increase in accrued expenses should be added to net income and vice versa. The reason is quite logical. If we are accruing an expense it means we are recording expenses that would otherwise require cash to be used. Instead we are not using cash to pay the expense. As a result, our cash has indirectly increased. Amortization of Intangibles: Anytime we see an amortization of an intangible, we must add it back. Similar to depreciation, amortization is simply an accounting allocation method that reduces net income but does not represent a cash outflow. Therefore, it must be added back. Prepaid Expenses: An increase in prepaid expenses should be subtracted from net income. The reason is because a prepaid expense represents cash being used to purchase the service (i.e. insurance, rent etc.) for future use. This results in cash being used in the current period and thus requires a subtraction from net income. Now that we have performed our analysis, we can prepare the operating section of the statement of cash flows using the indirect method, as seen below: 15

16 As you can see from above, our cash flows from operating activities is $52,000. If we use the direct method we will calculate the same amount of cash flows from operating activities Operating Section: Direct Method Learning Objective: Learn how to prepare a statement of cash flows using the direct method. The direct method provides a clearer presentation of sources of cash inflows and outflows compared to the indirect method. However, the direct method is more complicated to prepare from an accounting perspective because the data is not readily available in the accounting records. Using the direct method, the statement of cash flow must also include a supplemental section that computes operating cash flows using the indirect method. Ultimately this means it requires more work to prepare the statement of cash flows using the direct method. As a result, the direct method is not used as frequently as the indirect method. Companies can report their statement of cash flows using either method. The accounting standard setters recommend using the direct method to prepare the statement of cash flows due to providing financial statement users with more information about sources of and uses of cash flows. The direct method is quite simple in theory: We take the operating cash inflows and then subtract the operating cash outflows. Operating cash inflows generally consist of cash received from the sale of goods, services or similar cash flows. The operating cash outflows consist of cash payments to derive the operating cash inflows. Generally, those outflows consist of cash payments to suppliers (for goods/services), general operating expenses, interest payments and taxes. We then take the cash inflows and subtract the cash outflows to calculate net cash flows from operations. The general format of the direct method presentation is as follows: 16

We will now do a")

17 Preparing the Statement of Cash Flows Using the Direct Method (Comprehensive Example) We will now do a step-by-step example and explain each step in detail. We will use the balance sheet and income statement seen below: 17

18 Step 1: Cash Received from Customers Cash received from customers is the amount of cash we have received from customers, as the name implies. Using our income statement, we have sales revenue of $30,000 and consulting fees of $10,000 for a total of $40,000. This amount has to be adjusted for amounts that were not actually collected from customers in cash. For example, the sales revenue could have customers who agreed to pay on trade credit. These customers will create an account receivable for the company. Remember, the income statement is prepared using the accrual basis of accounting which allows for revenues to be recorded when the sale has been substantially completed. To account for these types of transactions, we must subtract all increases in accounts receivables. We will use the following formula to do that: Sum of Revenue Accounts - increase in Accounts Receivable or + decrease in Accounts Receivable = cash received from customers $40,000 + $5,000 = $45,000 cash received from customers. 18

19 We add $5,000 because the accounts receivable for the period decreased by $5,000. If our accounts receivable increased then we would add that amount. If we received interest from bonds or other investments that earn interest then we would include that amount under a separate line item below the cash received from customers line item called cash receipts of interest. It is important to note that we must factor in any interest receivable accounts. If we have an interest receivable on our balance sheet then it means the interest was not paid in cash. If we have an interest receivable account then we must subtract that amount from our interest. If we received dividends from investments then we would handle it similar to how we handle the interest. We would report the dividends received on a line item called cash receipts of dividends. If we have a dividend receivable account then it means the dividends were not received in cash. We must subtract the amount from our dividends. In our example we do not have interest or dividends so no separate line items are reported. Step 2: Less Cash Payments to Suppliers This section includes all cash payments made to acquire inventory or prepare inventory for sale. We use a special formula for calculating the amount of cash payments to suppliers, as follows: Cost of goods sold - decrease in inventory (or + increase inventories) - increase in accounts payable (or + decrease in accounts payable) = cash paid for merchandise 10,000-5, ,000 = 7,000 cash paid to suppliers We have paid $7,000 cash to suppliers. Step 3: Less Cash Payments for General Expenses General expenses are all expenses necessary to operate the business. We will add up all of our relevant general expense accounts and subtract any decrease in accrued liabilities. The formula below depicts this: All General Expenses (excluding depreciation and amortization) + Decrease in Accrued Expense Payable (or - Increase in Accrued Expense Payable) = Cash Paid for Operating Expenses 19

20 $15,000 - $5,000 = 10,000 Cash Paid for Operating Expenses The amounts used for our general expenses are wage expense, rent expense and utilities expense which equals $15,000. Income tax payable of $5,000 is an accrued expense and must be subtracted. Step 4: Less Cash Payments for Income Taxes We must subtract all expenses for income taxes that were paid in cash. Our income statement includes $5,000 for income tax expense which is subtracted. Additional Information Unlike the indirect method of calculating operating cash flows, depreciation, amortization, gains and losses are not used in the direct method. The reason is because we are not relying on net income to calculate our operating cash flows. Instead we go directly from cash inflows from customers to subtracting the outflows directly. If you are asked to use the direct method to calculate operating cash flows don't be distracted if the question provides you amounts for depreciation, amortization, gains or loses. These amounts are distractions. Now that we have performed our analysis, we can prepare the operating section of the statement of cash flows using the direct method, as seen below: Note: The direct method must include a supplementary schedule that includes the indirect method. We have excluded such schedule due to brevity. 20

21 Investing Section Learning Objective: Learn how to prepare the investing section of the statement of cash flows. The investing section shows changes in cash inflows and outflows that relate to a company's long-term assets, such as, fixed assets or investments. Examples of cash inflows from investing activities include: sale of fixed assets, sale of investment securities (i.e. stocks or bonds), cash received from loans, and any related cash flows associated with the above activities. Examples of cash outflows are: purchase of fixed assets, purchase of investment securities, and lending cash in the form of loans. Unlike the operating section, there is only one method used to calculate cash flows from investing activities. That method is relatively simple and consists of adding the investing cash inflows and subtracting the investing cash outflows. The tricky part of the calculation is identifying if the cash flow is an inflow or outflow and if it is classified in the correct section (operating, investing, financing). The format of the investing cash flow section is seen below: We will now do a step-by-step example and explain each step in detail. We will now do a step-by-step example and explain each step in detail. Step 1: Add up all Investing Cash Inflows In order to prepare the investing section, we must be able to identify investing cash flow transactions. Typical sources of investing cash inflows include the following: Sale of land or real estate for cash Sale of equipment for cash Sale of investment securities 21

22 Collection of principal on outstanding bonds or loans Step 2: Subtract all Investing Cash Outflows After we have identified all the investing cash inflows, we identify the outflows next. Typical cash outflows include: Purchase of land of real estate Purchase of equipment with cash Purchase of investment securities Preparing the Statement of Cash Flows Investing Section (Comprehensive Example) A company has provided us with a list of transactions for the year. They have requested that you prepare their investing section of their statement of cash flows. The following list was provided: Sold land for $5,000 Paid $500 interest on a loan Purchased equipment for $3,000 Repaid a loan in full for $2,000 Sold equipment for $500 Purchased securities for $10,000 Paid dividends of $3,000 STEP 1: Classify transactions that are included in the Investing Section Only certain transactions must be included in the investing section. Here is our analysis of the above transactions: 22

23 Sold land for $5,000 - This transaction is included in the investing section as a cash inflow. Paid $500 interest on a loan - This transaction is NOT included in investing section. Payment of interest is included in the operating section. Purchased equipment for $3,000 - This transaction is included in the investing section as a cash outflow. Repaid a loan in full for $2,000 - This transaction is included in the investing section as a cash outflow. Sold equipment for $500 - This transaction is included in the investing section as a cash inflow. Purchased securities for $10,000 - This transaction is included in the investing section as a cash outflow. Paid dividends of $3,000 - This transaction is NOT included in the investing section. It is included in the financing section. Now that we have identified our transactions, we can prepare the investing section. STEP 2: Prepare the Investing Section Using the above transactions, we can prepare the investing section, as seen below: As you can see, the cash flows are negative which means the company spent more money investing compared to collecting cash from investments. 23

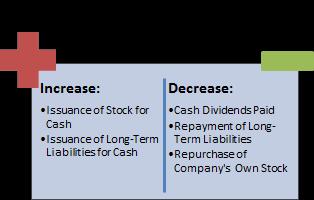

24 Financing Section Learning Objective: Learn how to prepare the financing section of the statement of cash flows. The financing section of the statement of cash flows shows cash inflows and outflows related to stockholder's equity and long-term liabilities. This may sound a little bit confusing but it is not confusing if we understand what is happening in the stockholder's equity and long-term liability transactions. Stockholder's equity is included in the financing section because a company can issue new shares to raise capital for the company. This capital is helping to finance future business projects. We also include payment of dividends in the financing section. Long-term liabilities are included because a company will issue bonds or similar liabilities to help fund business projects. It is important to remember to also include payments of long-term liabilities or repurchase of shares in the financing section. Similar to the investing section, there is only one method to calculate the financing section which is to simply add up all of your financing cash inflows and subtract all of the financing outflows. The tricky part of the calculation is to be able to identify which transactions are to be included in the financing section calculation. The general format of the financing section is as follows: We will now do a step-by-step example and explain each step in detail. Step 1: Add up all Financing Cash Inflows For this section we simply need to identify financing cash inflows. The following are sources of financing cash inflows: Issuance of bonds or loans to borrow cash from investors. Issuance of the company's stock in exchange for cash. 24

25 Step 2: Subtract all Financing Cash Outflows For this section we simply need to identify financing cash outflows. The following are sources of financing cash outflows: Repayment of bonds or loans Dividends paid in cash Purchase of treasury stock The last bullet point might seem a little strange. Treasury stock is the company's stock that was repurchased from investors. In this type of transaction, the company uses cash or similar assets to repurchase the company's own stock. This is a way to return cash to owners, similar to a dividend and is classified as a financing cash outflow if cash was used to purchase the stock. Preparing the Statement of Cash Flows Financing Section (Comprehensive Example) A company has provided us with a list of transactions for the year. They have requested that you prepare their financing section of their statement of cash flows. The following list was provided: The company issued stock and raised $5,000 The company repurchased its own stock (treasury stock) for $3,000 The company repaid an outstanding bond with $2,000 The company paid a dividend of $3,500 The company issued bonds worth $10,000 The company paid interest of $2,500 STEP 1: Classify transactions that are included in the Financing Section Only certain transactions must be included in the financing section. Here is our analysis of the above transactions: 25

26 The company issued stock and raised $5,000 - This transaction would be included in the financing section as a cash inflow. The company repurchased its own stock (treasury stock) for $3,000 - This transaction would be included in the financing section as a cash outflow. The company repaid an outstanding bond with $2,000 - This transaction would be included in the financing section as a cash outflow. The company paid a dividend of $3,500 - This transaction would be included in the financing section as a cash outflow. The company issued bonds worth $10,000 - This transaction would be included in the financing section as a cash inflow. The company paid interest of $2,500 - This transaction would NOT be included in the financing section. It is included in the operating section. Now that we have identified our transactions, we can prepare the financing section. STEP 2: Prepare the Financing Section Using the above transactions, we can prepare the financing section, as seen below: As you can see, the cash flows are positive which means the company had a net positive cash inflow from financing. 26

27 Disclosure of Noncash Activities Learning Objective: Learn about required disclosures of noncash activities. Noncash activities often impact the financing and investing section of the statement of cash flows. These are transactions which indirectly impact cash inflows or outflows and don't directly impact cash. In other words, for these transactions there is no exchange of cash. For example, a company could issue stock to retire a bond. The company could also purchase assets with stock, exchange noncash assets, or convert debt to stock. All of these transactions could impact a financial statement user's decision and therefore they should be disclosed. The disclosure is most often made at the bottom of the statement of cash flows. The disclosure could also be made in a separate schedule as long as it accompanies the statement of cash flows. The following is an example of a typical schedule of noncash financing and investing activities: Statement of Cash Flows Financial Ratios and Analysis Financial analysts and other users of the statement of cash flows can use ratio analysis to better understand the statement. We will be reviewing two different types of ratios, which are: operating cash flow, and cash debt coverage. As an important reminder, cash flow per share is not reported on the statement of cash flows because it would be misleading. Operating Cash Flow The operating cash flow ratio measures the amount of cash flow from operating activities relative to current liabilities. This ratio is significant because for a company to continue operating into the foreseeable future, they will need to be able to pay their 27

28 current liabilities as they come due. The operating cash flow ratio is a liquidity ratio and it can be used to evaluate if a company is a going concern (at risk of failure). Below is the formula for the operating cash flow ratio: Operating Cash Flow Ratio = Operating Cash Flow / Current Liabilities If the ratio is below 1 then it means the company is at risk of not being able to meet its current liabilities as they come due. If the company cannot meet their current liabilities then they will need to consider financing or raising capital from owner's or investors. The higher the operating cash flow ratio, the better. Example: Bob Smith Motors has $23 million in operating cash flows based on his statement of cash flow for the year ended The current liabilities based on the 2017 balance sheet reports $56 million. The operating cash flow ratio would be calculated as follows: Operating Cash Flow Ratio = $23,000,000 / $56,000,000 The ratio equals 0.41 The ratio of.41 means that the company will take a little under 2 and half years to repay all of the current liabilities if the company devoted all of the operating cash flows to repaying the current liabilities. If this company had business issues that impact the operating cash flows then the business would have an issue with meeting current liabilities as they come due. Cash Debt Coverage The cash debt coverage ratio shows how much operating cash flow the company is generating compared to the company's total debt. This ratio shows how long it would take for the company to repay its total debt from operating cash flow, excluding interest expense. The higher this ratio, the faster the company will be able to repay the total debt outstanding. If the company has a ratio of 1 then it means the company can repay all of the debt in 1 year, assuming all operating cash flow went to debt repayments. The formula for the cash debt coverage ratio is shown below: Cash Debt Coverage = Operating Cash Flow / Average Total Liabilities Example: 28

29 Bob Smith Steel Corporation had operating cash flows of 2 million on the 2017 statement of cash flows. At the beginning of the year, the corporation had 1.5 million in total liabilities and at the end of the year the firm had 1.75 million in total liabilities. In order to calculate the cash debt coverage ratio, we must first find the average total liabilities. To do this, we simply add the beginning of the year total liabilities to the end of the year total liabilities and divide by 2. Our calculation would be: (1.5 million million)/2 which equals million. Calculating the ratio is simple after this: Cash Debt Coverage = 2 million / million Our ratio equals 1.23 This ratio means the firm can repay all of its average total liabilities in less than one year because the ratio is higher than 1. If the ratio was lower than one then it would mean the firm would take longer than one year to repay all of the average total liabilities. 29

30 Additional Study Resources The following additional study resources are available for this chapter: Interactive Video Lecture Study Notes Supplemental Practice Skills Quiz The above resources are only available online as they are enhanced with computer technology designed to analyze student data which is used to improve the student s experience. Students are encouraged to review the interactive video lecture, review the study notes, practice with the supplemental practice and then take the skills quiz. When the student has achieved mastery on the skills quiz, the student should proceed to chapter

CHAPTER 12 STATEMENT OF CASH FLOWS

CHAPTER 12 STATEMENT OF CASH FLOWS Key Terms and Concepts to Know The Statement of Cash Flows reports the sources of cash inflows and cash outflow during an accounting period. The inflows and outflows

CHAPTER 12 STATEMENT OF CASH FLOWS Key Terms and Concepts to Know The Statement of Cash Flows reports the sources of cash inflows and cash outflow during an accounting period. The inflows and outflows

FAQ: Statement of Cash Flows

Question 1: What sources are used when the statement of cash flows is being prepared, and what information does each source provide? Answer 1: The statement of cash flows is prepared differently from the

Question 1: What sources are used when the statement of cash flows is being prepared, and what information does each source provide? Answer 1: The statement of cash flows is prepared differently from the

ACCT 101 Statement of Cash Flows Lecture Notes Chapter 12 Prof. Johnson. The statement of cash flows is a required component of financial statements.

ACCT 101 Statement of Cash Flows Lecture Notes Chapter 12 Prof. Johnson The statement of cash flows is a required component of financial statements. BASICS OF CASH FLOW REPORTING Purpose of the Statement

ACCT 101 Statement of Cash Flows Lecture Notes Chapter 12 Prof. Johnson The statement of cash flows is a required component of financial statements. BASICS OF CASH FLOW REPORTING Purpose of the Statement

Chapter 12 - Reporting and Analyzing Cash Flows. Chapter Outline

I. Basics of Cash Flow Reporting A. Purpose of the Statement of Cash Flows To report cash receipts (inflows) and cash payments (outflows) during a period. This report classifies cash flows into operating,

I. Basics of Cash Flow Reporting A. Purpose of the Statement of Cash Flows To report cash receipts (inflows) and cash payments (outflows) during a period. This report classifies cash flows into operating,

Statement of Cash Flows. Statement of Cash Flows. Classification of Business Activities. Learning Objectives

Statement of Cash Flows Learning Objectives 1. Understand the different activities of a business and how this influences the cash flow statement 2. Understand the direct and indirect methods for preparation

Statement of Cash Flows Learning Objectives 1. Understand the different activities of a business and how this influences the cash flow statement 2. Understand the direct and indirect methods for preparation

Statement of Cash Flows

May 5, 2014 Statement of Cash Flows Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Today s Agenda n Cash Flow Statements n What Cash Flow Statements show us n Building a Cash Flow

May 5, 2014 Statement of Cash Flows Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Today s Agenda n Cash Flow Statements n What Cash Flow Statements show us n Building a Cash Flow

CHAPTER 12. The statement of cash flows categorizes cash receipts and cash payments as operating, investing, and financing activities.

CHAPTER 12 Purpose of the Statement of Cash Flows The statement of cash flows is considered a major financial statement, as are the income statement, balance sheet, and statement of stockholders' equity.

CHAPTER 12 Purpose of the Statement of Cash Flows The statement of cash flows is considered a major financial statement, as are the income statement, balance sheet, and statement of stockholders' equity.

The statement of cash flows reports cash flows, cash receipts, and cash payments, to show where cash came from and how it was spent.

Accounting Fundamentals Lesson 10 10.0 Cash Flow Statement The balance sheet reports financial position, and balance sheets from two periods show whether cash increased or decreased. But that doesn t tell

Accounting Fundamentals Lesson 10 10.0 Cash Flow Statement The balance sheet reports financial position, and balance sheets from two periods show whether cash increased or decreased. But that doesn t tell

Name of business Statement of cash flows for the financial year end 31 December 20X1 (DIRECT METHOD) Inflow /(outflow)

Inflow /(outflow)") Name of business Statement of cash flows for the financial year end 31 December 201 (DIRECT METHOD) Calc Notes Inflow /(outflow) CASH FLOWS FROM OPERATING ACTIVITIES Cash receipts from customers C1 Cash

Name of business Statement of cash flows for the financial year end 31 December 201 (DIRECT METHOD) Calc Notes Inflow /(outflow) CASH FLOWS FROM OPERATING ACTIVITIES Cash receipts from customers C1 Cash

This is How Is the Statement of Cash Flows Prepared and Used?, chapter 12 from the book Accounting for Managers (index.html) (v. 1.0).

(v. 1.0).") This is How Is the Statement of Cash Flows Prepared and Used?, chapter 12 from the book Accounting for Managers (index.html) (v. 1.0). This book is licensed under a Creative Commons by-nc-sa 3.0 (http://creativecommons.org/licenses/by-nc-sa/

This is How Is the Statement of Cash Flows Prepared and Used?, chapter 12 from the book Accounting for Managers (index.html) (v. 1.0). This book is licensed under a Creative Commons by-nc-sa 3.0 (http://creativecommons.org/licenses/by-nc-sa/

AGENDA: STATEMENT OF CASH FLOWS

TM 14-1 AGENDA: STATEMENT OF CASH FLOWS A. Foundational knowledge. B. Four key concepts for preparing the statement of cash flows. 1. Organizing the statement of cash flows. 2. Distinguishing between the

TM 14-1 AGENDA: STATEMENT OF CASH FLOWS A. Foundational knowledge. B. Four key concepts for preparing the statement of cash flows. 1. Organizing the statement of cash flows. 2. Distinguishing between the

Statement of Cash Flows (SCF)

") Statement of Cash Flows (SCF) The statement of cash flows (SCF) or cash flow statement reports a corporation's significant cash inflows and outflows that occurred during an accounting period. This financial

Statement of Cash Flows (SCF) The statement of cash flows (SCF) or cash flow statement reports a corporation's significant cash inflows and outflows that occurred during an accounting period. This financial

Statement of Cash Flows

CHAPTER 14 Statement of Cash Flows LEARNING OBJECTIVES After you have mastered the material in this chapter, you will be able to: 1 Prepare the operating activities section of a statement of cash flows

CHAPTER 14 Statement of Cash Flows LEARNING OBJECTIVES After you have mastered the material in this chapter, you will be able to: 1 Prepare the operating activities section of a statement of cash flows

CHAPTER 17 THE STATEMENT OF CASH FLOWS SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY. True-False Statements. Multiple Choice Questions

CHAPTER 17 THE STATEMENT OF CASH FLOWS SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 K 9. 2 K 17. 2 C a

CHAPTER 17 THE STATEMENT OF CASH FLOWS SUMMARY OF QUESTIONS BY STUDY OBJECTIVES AND BLOOM S TAXONOMY Item SO BT Item SO BT Item SO BT Item SO BT Item SO BT True-False Statements 1. 1 K 9. 2 K 17. 2 C a

Statement of Cash Flows Revisited

21 Statement of Cash Flows Revisited Overview There is not much that is new in this chapter. Rather, this chapter draws on what was learned in Chapter 5 and subsequent chapters with respect to the statement

21 Statement of Cash Flows Revisited Overview There is not much that is new in this chapter. Rather, this chapter draws on what was learned in Chapter 5 and subsequent chapters with respect to the statement

VISUAL #16-1 CLASSIFYING ACTIVITIES IN THE STATEMENT OF CASH FLOWS OPERATING ACTIVITIES INVESTING ACTIVITIES FINANCING ACTIVITIES

VISUAL #16-1 CLASSIFYING ACTIVITIES IN THE STATEMENT OF CASH FLOWS OPERATING ACTIVITIES Cash inflows from Cash outflows to Customers for cash sales Collections on credit sales Borrowers for interest Dividends

VISUAL #16-1 CLASSIFYING ACTIVITIES IN THE STATEMENT OF CASH FLOWS OPERATING ACTIVITIES Cash inflows from Cash outflows to Customers for cash sales Collections on credit sales Borrowers for interest Dividends

ACCOUNTING - CLUTCH CH STATEMENT OF CASH FLOWS.

!! www.clutchprep.com CONCEPT: INTRODUCTION TO STATEMENT OF CASH FLOWS The Statement of Cash Flows shows what affected the Cash account balance throughout the period Predictive Value Helps predict future

!! www.clutchprep.com CONCEPT: INTRODUCTION TO STATEMENT OF CASH FLOWS The Statement of Cash Flows shows what affected the Cash account balance throughout the period Predictive Value Helps predict future

STATEMENT OF CASH FLOWS

Chapter Seventeen STATEMENT OF CASH FLOWS LEARNING OBJECTIVES After reading this chapter, you should be able to Explain why investors and others are interested in cash flows. State the three types of activities

Chapter Seventeen STATEMENT OF CASH FLOWS LEARNING OBJECTIVES After reading this chapter, you should be able to Explain why investors and others are interested in cash flows. State the three types of activities

Chapter 6: Statement of Cash Flows

Chapter 6: Statement of Cash Flows Outline: Why a cash flow statement? Classifications of cash flows Preparation of cash flow statements Determining the change in cash Determining net cash from operating

Chapter 6: Statement of Cash Flows Outline: Why a cash flow statement? Classifications of cash flows Preparation of cash flow statements Determining the change in cash Determining net cash from operating

Reporting and Interpreting Cash Flows

C H A P T E R Reporting and Interpreting Cash Flows LEARNING OBJECTIVES After studying this chapter, you should be able to: 1. Classify cash flow statement items as part of net cash flows from operating,

C H A P T E R Reporting and Interpreting Cash Flows LEARNING OBJECTIVES After studying this chapter, you should be able to: 1. Classify cash flow statement items as part of net cash flows from operating,

Chapter 6 Statement of Cash Flows

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

Chapter 6 Statement of Cash Flows The Statement of Cash Flows describes the cash inflows and outflows for the firm based upon three categories of activities. Operating Activities: Generally include transactions

Chapter 3. Cash-Flow Statements

Introduction to Cash-Flow Statements 1 Chapter 3 Cash-Flow Statements TABLE OF CONTENTS Introduction 3 Direct Format Operating Section 5 Indirect Format Operating Section 6 Exercise 3.01 7 What Do I See?

Introduction to Cash-Flow Statements 1 Chapter 3 Cash-Flow Statements TABLE OF CONTENTS Introduction 3 Direct Format Operating Section 5 Indirect Format Operating Section 6 Exercise 3.01 7 What Do I See?

Financial Statement Analysis. Cash Flow Statement

Financial Statement Analysis Cash Flow Statement 1 The Articulation of the Financial Statements Beginning stocks Flows Ending stocks Cash Flow Statement Beginning Balance Sheet Cash Cash from operations

Financial Statement Analysis Cash Flow Statement 1 The Articulation of the Financial Statements Beginning stocks Flows Ending stocks Cash Flow Statement Beginning Balance Sheet Cash Cash from operations

Chapter 12. The statement of cash flows categorizes cash receipts and cash payments as operating, investing, and financing activities.

1 Chapter 12 2 The statement of cash flows is a major financial statement as are the income statement, balance sheet, and statement of stockholders' equity. The statement of cash flows is required whenever

1 Chapter 12 2 The statement of cash flows is a major financial statement as are the income statement, balance sheet, and statement of stockholders' equity. The statement of cash flows is required whenever

CHAPTER 4: REPORTING AND ANALYZING CASH FLOWS

M4-22. a. Cash flow from an operating activity. b. Cash flow from an investing activity. c. Cash flow from an investing activity. d. Cash flow from an operating activity. e. Cash flow from a financing

M4-22. a. Cash flow from an operating activity. b. Cash flow from an investing activity. c. Cash flow from an investing activity. d. Cash flow from an operating activity. e. Cash flow from a financing

Chapter 13 Statement of Cash Flows Study Guide Solutions Fill-in-the-Blank Equations. Exercises

Chapter 13 Statement of Cash Flows Study Guide Solutions Fill-in-the-Blank Equations 1. Net cash flow from operating activities 2. Change in Cash 3. Cash used to purchase property, plant, and equipment

Chapter 13 Statement of Cash Flows Study Guide Solutions Fill-in-the-Blank Equations 1. Net cash flow from operating activities 2. Change in Cash 3. Cash used to purchase property, plant, and equipment

Reading & Understanding Financial Statements

Reading & Understanding Financial Statements A Guide to Financial Reporting Introduction Financial statements are an important management tool. When correctly prepared and properly interpreted, they contribute

Reading & Understanding Financial Statements A Guide to Financial Reporting Introduction Financial statements are an important management tool. When correctly prepared and properly interpreted, they contribute

Reading & Understanding Financial Statements. A Guide to Financial Reporting

Reading & Understanding Financial Statements A Guide to Financial Reporting Introduction Financial statements are an important management tool. When correctly prepared and properly interpreted, they contribute

Reading & Understanding Financial Statements A Guide to Financial Reporting Introduction Financial statements are an important management tool. When correctly prepared and properly interpreted, they contribute

CHAPTER 17. The Cash Flow Statement. Brief Questions Exercises 12, 13 3, 4, 5, 11 6, 7, 8, 9, 10, 11

CHAPTER 17 The Cash Flow Statement ASSIGNMENT CLASSIFICATION TABLE Study Objectives Brief Questions Exercises Exercises Problems Set A Problems Set B 1. Describe the purpose and content of the cash flow

CHAPTER 17 The Cash Flow Statement ASSIGNMENT CLASSIFICATION TABLE Study Objectives Brief Questions Exercises Exercises Problems Set A Problems Set B 1. Describe the purpose and content of the cash flow

REVIEW PROBLEM Rockford Company s comparative balance sheet for 2012 and the company s income statement for the year follow:

REVIEW PROBLEM Rockford Company s comparative balance sheet for 2012 and the company s income statement for the year follow: Additional data: 1. Rockford paid a cash dividend in 2012. 2. The $4 million

REVIEW PROBLEM Rockford Company s comparative balance sheet for 2012 and the company s income statement for the year follow: Additional data: 1. Rockford paid a cash dividend in 2012. 2. The $4 million

2. (a) An asset is a probable future economic benefit owned or controlled by the entity as a result of past transactions.

An asset is a probable future economic benefit owned or controlled by the entity as a result of past transactions.") Chapter 2 Investing and Financing Decisions and the Accounting System ANSWERS TO QUESTIONS 1. The primary objective of financial reporting for external users is to provide financial information about the

Chapter 2 Investing and Financing Decisions and the Accounting System ANSWERS TO QUESTIONS 1. The primary objective of financial reporting for external users is to provide financial information about the

CHAPTER 12. Statement of Cash Flows. Study Objectives

CHAPTER 12 Statement of Cash Flows Study Objectives Indicate the primary purpose of the statement of cash flows. Distinguish among operating, investing, and financing activities. Explain the impact of

CHAPTER 12 Statement of Cash Flows Study Objectives Indicate the primary purpose of the statement of cash flows. Distinguish among operating, investing, and financing activities. Explain the impact of

4/10/2012. Statement of Cash Flows. Learning Objectives (LO) LO 1 - Purpose of Cash Flow Statement. Learning Objectives (LO)

LO 1 - Purpose of Cash Flow Statement. Learning Objectives (LO)") Statement of Flows CHAPTER Learning Objectives (LO) After studying this chapter, you should be able to 1. Identify the purposes of the statement of cash flows 2. Classify activities affecting cash as operating,

Statement of Flows CHAPTER Learning Objectives (LO) After studying this chapter, you should be able to 1. Identify the purposes of the statement of cash flows 2. Classify activities affecting cash as operating,

Statement of Cash Flows

JWCL162_c13_582-643.qxd 8/13/09 1:09 PM Page 582 chapter 13 Statement of Cash Flows the navigator Scan Study Objectives Read Feature Story Read Preview Read Text and answer Do it! p. 588 p. 595 p. 599

JWCL162_c13_582-643.qxd 8/13/09 1:09 PM Page 582 chapter 13 Statement of Cash Flows the navigator Scan Study Objectives Read Feature Story Read Preview Read Text and answer Do it! p. 588 p. 595 p. 599

Disclaimer: This resource package is for studying purposes only EDUCATON

Disclaimer: This resource package is for studying purposes only EDUCATON Chapter 1 Objective of Accounting: 1. To identify and measure activities of a business entity in order to evaluate its performance

Disclaimer: This resource package is for studying purposes only EDUCATON Chapter 1 Objective of Accounting: 1. To identify and measure activities of a business entity in order to evaluate its performance

Reading Understanding. Financial Statements. A Layman s Guide to Financial Reporting

Reading Understanding & Financial Statements A Layman s Guide to Financial Reporting 1 Introduction Financial statements are an important management tool. When correctly prepared and properly interpreted,

Reading Understanding & Financial Statements A Layman s Guide to Financial Reporting 1 Introduction Financial statements are an important management tool. When correctly prepared and properly interpreted,

Full file at

Chapter 3 Financial Statements, Cash Flows, and Taxes Learning Objectives 1. Discuss generally accepted accounting principles (GAAP) and their importance to the economy. 2. Know the balance sheet identity,

Chapter 3 Financial Statements, Cash Flows, and Taxes Learning Objectives 1. Discuss generally accepted accounting principles (GAAP) and their importance to the economy. 2. Know the balance sheet identity,

Chapter 12 Question Review 1

Chapter 12 Question Review 1 Chapter 12 Questions Multiple Choice 1. Assume that Mango Corporation uses the indirect method to depict cash flows. Indicate where, if at all, land and building purchased

Chapter 12 Question Review 1 Chapter 12 Questions Multiple Choice 1. Assume that Mango Corporation uses the indirect method to depict cash flows. Indicate where, if at all, land and building purchased

LLH9e_Ch02_SolutionsManual_FINAL.pdf Libby_9e_IM_CH02.pdf LLH9e_Chapter_02.pdf

LLH9e_Ch02_SolutionsManual_FINAL.pdf Libby_9e_IM_CH02.pdf LLH9e_Chapter_02.pdf Chapter 2 Investing and Financing Decisions and the Accounting System ANSWERS TO QUESTIONS 1. The primary objective of financial

LLH9e_Ch02_SolutionsManual_FINAL.pdf Libby_9e_IM_CH02.pdf LLH9e_Chapter_02.pdf Chapter 2 Investing and Financing Decisions and the Accounting System ANSWERS TO QUESTIONS 1. The primary objective of financial

Dr. Maddah ENMG 602 Intro. to Financial Eng g 11/04/09. Statement of Cash Flows (Chapter 4, Antle)

") Dr. Maddah ENMG 602 Intro. to Financial Eng g 11/04/09 Statement of Cash Flows (Chapter 4, Antle) Basic definitions Cash is readily transferable value. It is the most common way organizations acquire goods

Dr. Maddah ENMG 602 Intro. to Financial Eng g 11/04/09 Statement of Cash Flows (Chapter 4, Antle) Basic definitions Cash is readily transferable value. It is the most common way organizations acquire goods

A CLEAR UNDERSTANDING OF THE INDUSTRY

A CLEAR UNDERSTANDING OF THE INDUSTRY IS CFA INSTITUTE INVESTMENT FOUNDATIONS RIGHT FOR YOU? Investment Foundations is a certificate program designed to give you a clear understanding of the investment

A CLEAR UNDERSTANDING OF THE INDUSTRY IS CFA INSTITUTE INVESTMENT FOUNDATIONS RIGHT FOR YOU? Investment Foundations is a certificate program designed to give you a clear understanding of the investment

Unappropriated retained earnings (accumulated deficit) Total unappropriated retained earnings (accumulated deficit) 676, ,797 Total retained ear

Total unappropriated retained earnings (accumulated deficit) 676, ,797 Total retained ear") Financial Statement Balance Sheet Accounting Title 2014/12/31 2013/12/31 Balance Sheet Assets Current assets Cash and cash equivalents Total cash and cash equivalents 1,183,185 1,177,682 Current bond investment

Financial Statement Balance Sheet Accounting Title 2014/12/31 2013/12/31 Balance Sheet Assets Current assets Cash and cash equivalents Total cash and cash equivalents 1,183,185 1,177,682 Current bond investment

You are provided with the following transactions that took place during a recent fis-

Chapter 17 PROBLEMS: SET C You are provided with the following transactions that took place during a recent fis- P17-1C cal year. (a) (b) (c) (d) (e) (f) (g) (h) (i) (j) Cash Inflow, Where Reported Outflow,

Chapter 17 PROBLEMS: SET C You are provided with the following transactions that took place during a recent fis- P17-1C cal year. (a) (b) (c) (d) (e) (f) (g) (h) (i) (j) Cash Inflow, Where Reported Outflow,

Statements of Net Position - Business - Type Activities South Carolina Public Service Authority As of March 31, 2018 and December 31, 2017

Statements of Net Position - Business - Type Activities As of March 31, 2018 and December 31, 2017 ASSETS Current assets Unrestricted cash and cash equivalents $ 207,610 $ 731,758 Unrestricted investments

Statements of Net Position - Business - Type Activities As of March 31, 2018 and December 31, 2017 ASSETS Current assets Unrestricted cash and cash equivalents $ 207,610 $ 731,758 Unrestricted investments

Statements of Net Position - Business - Type Activities South Carolina Public Service Authority As of September 30, 2018 and December 31, 2017

Statements of Net Position - Business - Type Activities As of September 30, 2018 and December 31, 2017 ASSETS Current assets Unrestricted cash and cash equivalents $ 315,796 $ 731,758 Unrestricted investments

Statements of Net Position - Business - Type Activities As of September 30, 2018 and December 31, 2017 ASSETS Current assets Unrestricted cash and cash equivalents $ 315,796 $ 731,758 Unrestricted investments

Visit Free Slides and Ebooks : CHAPTER 23. Statement of Cash Flows

CHAPTER 23 Statement of Cash Flows ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Format, objectives purpose, and source of statement.

CHAPTER 23 Statement of Cash Flows ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Format, objectives purpose, and source of statement.

Statement of Cash Flows. Barry M Frohlinger

Statement of Cash Flows Barry M Frohlinger Statement of Cash Flows Page 1 Barry M Frohlinger, Inc. copyright 1981-2010 Companies are required to present a Statement of Cash Flows (cash statement) for each

Statement of Cash Flows Barry M Frohlinger Statement of Cash Flows Page 1 Barry M Frohlinger, Inc. copyright 1981-2010 Companies are required to present a Statement of Cash Flows (cash statement) for each

" Annual report: the main method that management uses to report the results of the company s activities during the year.

Chapter 1 Overview of Corporate Financial Reporting What is Business? " Business plan to profit from selling a product or service. " Can be an individual or thousands of owners (investors). What is Accounting?

Chapter 1 Overview of Corporate Financial Reporting What is Business? " Business plan to profit from selling a product or service. " Can be an individual or thousands of owners (investors). What is Accounting?

Not For Sale. Overview of Financial Statements FACMU14. Cengage Learning. All rights reserved. No distribution allowed without express authorization.

Overview of Financial Statements FACMU14 P a r t 1 23450_ch01_ptg01_lores_001-040.indd 1 5/1/12 9:08 PM 23450_ch01_ptg01_lores_001-040.indd 2 5/1/12 9:08 PM Chapter Introduction to Business Activities

Overview of Financial Statements FACMU14 P a r t 1 23450_ch01_ptg01_lores_001-040.indd 1 5/1/12 9:08 PM 23450_ch01_ptg01_lores_001-040.indd 2 5/1/12 9:08 PM Chapter Introduction to Business Activities

TOTAL TRAINING SOLUTIONS

TOTAL TRAINING SOLUTIONS Global Cash Flow Analysis Get Global by Understanding Global Cash Flow Jeffery W. Johnson Bankers Insight Group jeffery.johnson@bankers-insight.com 770-846-4511 September 2015

TOTAL TRAINING SOLUTIONS Global Cash Flow Analysis Get Global by Understanding Global Cash Flow Jeffery W. Johnson Bankers Insight Group jeffery.johnson@bankers-insight.com 770-846-4511 September 2015

CHAPTER 14 STATEMENT OF CASH FLOWS

1. It is costly to accumulate the data needed and to prepare the statement of cash flows. 2. It focuses on the differences between net profit and cash flows from operating activities, and the data needed

1. It is costly to accumulate the data needed and to prepare the statement of cash flows. 2. It focuses on the differences between net profit and cash flows from operating activities, and the data needed

Chapter 6, cont d. The Statement of Cash Flows. (for a deeper analysis see chapter 18)

") Chapter 6, cont d The Statement of Cash Flows (for a deeper analysis see chapter 18) 1 Lecture outline Why a cash flow statement? Classifications of cash flows Preparation of cash flow statements Determining

Chapter 6, cont d The Statement of Cash Flows (for a deeper analysis see chapter 18) 1 Lecture outline Why a cash flow statement? Classifications of cash flows Preparation of cash flow statements Determining

CHAPTER 17 PROBLEMS: SET B

CHAPTER 17 PROBLEMS: SET B P17-1B You are provided with the following transactions that took place during a recent fiscal year. Statement of Cash Inflow, Cash Flow Outflow, or Transaction Activity Affected

CHAPTER 17 PROBLEMS: SET B P17-1B You are provided with the following transactions that took place during a recent fiscal year. Statement of Cash Inflow, Cash Flow Outflow, or Transaction Activity Affected

Understand Financial Statements and Identify Sources of Farm Financial Risk

Agricultural Finance Understand Financial Statements and Identify Sources of Farm Financial Risk By analyzing a complete set of your farm s financial statements you can identify sources and amounts of

Agricultural Finance Understand Financial Statements and Identify Sources of Farm Financial Risk By analyzing a complete set of your farm s financial statements you can identify sources and amounts of

Chapter 2: The Balance Sheet

TRUE/FALSE 1. A transaction is an exchange or event that directly affects the assets, liabilities, or stockholders' equity of a company. Answer: True Difficulty: 1 Easy LO: 02-01 Topic: Transactions and

TRUE/FALSE 1. A transaction is an exchange or event that directly affects the assets, liabilities, or stockholders' equity of a company. Answer: True Difficulty: 1 Easy LO: 02-01 Topic: Transactions and

Statement of Cash Flows

13-1 13 Statement of Cash Flows Learning Objectives 1 2 Discuss the usefulness and format of the statement of cash flows. Prepare a statement of cash flows using the indirect method. 3 Analyze the statement

13-1 13 Statement of Cash Flows Learning Objectives 1 2 Discuss the usefulness and format of the statement of cash flows. Prepare a statement of cash flows using the indirect method. 3 Analyze the statement

Financial statements. Chapter One-A. A- Statements of cash flows. 1 IAS 7 Statement of cash flows F5(a)-(h)

-(h)") Chapter One-A Financial statements A- Statements of cash flows Topic list Syllabus reference 1 IAS 7 Statement of cash flows F5(a)-(h) 2 Preparing a statement of cash flows F5(g) Introduction In the long

Chapter One-A Financial statements A- Statements of cash flows Topic list Syllabus reference 1 IAS 7 Statement of cash flows F5(a)-(h) 2 Preparing a statement of cash flows F5(g) Introduction In the long

Full file at

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) A journal entry is a record of an event that has a financial impact on the business that can be reliably measured. 1)

TRUE/FALSE. Write 'T' if the statement is true and 'F' if the statement is false. 1) A journal entry is a record of an event that has a financial impact on the business that can be reliably measured. 1)

Corporate Accounting Recitation 3. June 18, 2004

15.511 Corporate Accounting Recitation 3 June 18, 2004 Why do we need CF/S? Accrual accounting is often based upon subjective judgments that can introduce measurement error and uncertainty into the reported

15.511 Corporate Accounting Recitation 3 June 18, 2004 Why do we need CF/S? Accrual accounting is often based upon subjective judgments that can introduce measurement error and uncertainty into the reported

Table of Contents Accounting Questions & Answers

Table of Contents Accounting Questions & Answers Overview & Key Rules of Thumb...2 Key Rule #1: The Income Statement...2 Key Rule #2: The Balance Sheet...5 Key Rule #3: The Cash Flow Statement...8 Key

Table of Contents Accounting Questions & Answers Overview & Key Rules of Thumb...2 Key Rule #1: The Income Statement...2 Key Rule #2: The Balance Sheet...5 Key Rule #3: The Cash Flow Statement...8 Key

Class 12 Accountancy NCERT Solutions Cash Flow Statement

Class 12 Accountancy NCERT Solutions Cash Flow Statement TEST YOUR UNDERSTANDING I DO IT YOUR SELF I Question 1. The profit and loss account of Roy Limited is given here under Question 2. From the following

Class 12 Accountancy NCERT Solutions Cash Flow Statement TEST YOUR UNDERSTANDING I DO IT YOUR SELF I Question 1. The profit and loss account of Roy Limited is given here under Question 2. From the following

HANDOUT FOR WEEK 3 UNDERSTANDING THE INCOME STATEMENT. (Profit and loss statement)

") HANDOUT FOR WEEK 3 UNDERSTANDING THE INCOME STATEMENT Introduction (Profit and loss statement) The financial account system generates and important report that captures the financial performance of the

HANDOUT FOR WEEK 3 UNDERSTANDING THE INCOME STATEMENT Introduction (Profit and loss statement) The financial account system generates and important report that captures the financial performance of the

Some deferred items for which adjusting entries would be made include: Prepaid insurance Prepaid rent Office supplies Depreciation Unearned revenue

WWW.VUTUBE.EDU.PK Paper 1 MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 1) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following is the acronym for GAAP?

WWW.VUTUBE.EDU.PK Paper 1 MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 1) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following is the acronym for GAAP?

STATEMENT OF CASH FLOWS

Chapter 16 STATEMENT OF CASH FLOWS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Winston Kwok, Ph.D.,

Chapter 16 STATEMENT OF CASH FLOWS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Winston Kwok, Ph.D.,

accounts receivable: dollar amount due from customers from sales made on open account.

GLOSSARY 1 above-the-line: income items related to core operations. Typically assumed to have high predictive power for future earnings. accrual accounting: system of accounting that purports to measure

GLOSSARY 1 above-the-line: income items related to core operations. Typically assumed to have high predictive power for future earnings. accrual accounting: system of accounting that purports to measure

Financial Reporting, Financial Statement Analysis and Valuation 8th Edition Test Bank Download:

Financial Reporting, Financial Statement Analysis and Valuation 8th Edition Test Bank Download: https://testbankarea.com/download/financial-reporting-financial-statementanalysis-valuation-8th-edition-solutions-manual-wahlen-baginski-bradshaw/

Financial Reporting, Financial Statement Analysis and Valuation 8th Edition Test Bank Download: https://testbankarea.com/download/financial-reporting-financial-statementanalysis-valuation-8th-edition-solutions-manual-wahlen-baginski-bradshaw/

Statement of cash flows PURPOSE & SCOPE

IAS 7 Statement of cash flows PURPOSE & SCOPE Purpose Users needs Scope The fundamental purpose of being in business is to generate profit, as this will increase the owners' wealth. Profitability relates

IAS 7 Statement of cash flows PURPOSE & SCOPE Purpose Users needs Scope The fundamental purpose of being in business is to generate profit, as this will increase the owners' wealth. Profitability relates

AccountingCoach.com Cash Flow Statement

AccountingCoach.com Cash Flow Statement All underlined words are defined in the attached Glossary (Pages 40 46). Introduction to the Cash Flow Statement The official name for the cash flow statement is

AccountingCoach.com Cash Flow Statement All underlined words are defined in the attached Glossary (Pages 40 46). Introduction to the Cash Flow Statement The official name for the cash flow statement is

Chapter 17 In a Set of Financial Statements, What Information Is Conveyed by the Statement of Cash Flows?

This is In a Set of Financial Statements, What Information Is Conveyed by the Statement of Cash Flows?, chapter 17 from the book Accounting in the Finance World (index.html) (v. 1.0). This book is licensed

This is In a Set of Financial Statements, What Information Is Conveyed by the Statement of Cash Flows?, chapter 17 from the book Accounting in the Finance World (index.html) (v. 1.0). This book is licensed

ANALYSIS OF FINANCIAL ACCOUNTING METHODOLOGIES AND APPLICATIONS. By: Kate Culbertson. Oxford May 2017

ANALYSIS OF FINANCIAL ACCOUNTING METHODOLOGIES AND APPLICATIONS By: Kate Culbertson A thesis submitted to the faculty of The University of Mississippi in partial fulfillment of the requirements of the

ANALYSIS OF FINANCIAL ACCOUNTING METHODOLOGIES AND APPLICATIONS By: Kate Culbertson A thesis submitted to the faculty of The University of Mississippi in partial fulfillment of the requirements of the

Understanding Financial Management: A Practical Guide Guideline Answers to the Concept Check Questions

Understanding Financial Management: A Practical Guide Guideline Answers to the Concept Check Questions Chapter 2 Interpreting Financial Statements Concept Check 2.1 1. Which stakeholders need to interpret

Understanding Financial Management: A Practical Guide Guideline Answers to the Concept Check Questions Chapter 2 Interpreting Financial Statements Concept Check 2.1 1. Which stakeholders need to interpret

Yasheng Group 2010 Financial Results

Yasheng Group 2010 Financial Results CONSOLIDATED BALANCE SHEETS 2010 2009 2008 ASSETS 849,454,265 739,630,043 736,213,299 Current assets: Cash and cash equivalents 10,116,750 8,010,017 7,880,338 Accounts

Yasheng Group 2010 Financial Results CONSOLIDATED BALANCE SHEETS 2010 2009 2008 ASSETS 849,454,265 739,630,043 736,213,299 Current assets: Cash and cash equivalents 10,116,750 8,010,017 7,880,338 Accounts

Chapter 10 Statement of Cash Flows. 1. a Search, Detection, Navigation, Guidance, Aeronautical Systems

Chapter 10 Statement of Cash Flows TO THE NET 1. a. 3812 Search, Detection, Navigation, Guidance, Aeronautical Systems b. Northrop Grumman Corporation (Northrop Grumman or the company) provides technologically

Chapter 10 Statement of Cash Flows TO THE NET 1. a. 3812 Search, Detection, Navigation, Guidance, Aeronautical Systems b. Northrop Grumman Corporation (Northrop Grumman or the company) provides technologically

ANSWER SHEET EXAMINATION #2

ANSWER SHEET EXAMINATION #2 1) D 2) B 26) D 3) C 27) B 4) A 28) B 5) D 29) C 6) D 30) A 7) D 31) B 8) C 32) D 9) D 33) D 10) B 34) D 11) A 12) A 13) D 14) C 15) A 16) C 17) B 18) B 19) C 20) B 21) B 22)

ANSWER SHEET EXAMINATION #2 1) D 2) B 26) D 3) C 27) B 4) A 28) B 5) D 29) C 6) D 30) A 7) D 31) B 8) C 32) D 9) D 33) D 10) B 34) D 11) A 12) A 13) D 14) C 15) A 16) C 17) B 18) B 19) C 20) B 21) B 22)

Financial Statements. M. En C. Eduardo Bustos Farías

Understanding 1 Financial Statements M. En C. Eduardo Bustos Farías 2 Objectives 1. Define the elements of financial statements. 3 Balance Sheet It It also is is called a statement of of financial position.

Understanding 1 Financial Statements M. En C. Eduardo Bustos Farías 2 Objectives 1. Define the elements of financial statements. 3 Balance Sheet It It also is is called a statement of of financial position.

Accounting Title 2017/03/ /12/ /03/31 Balance Sheet

1 / 2 Accounting Title 2017/03/31 2016/12/31 2016/03/31 Balance Sheet Assets Current assets Cash and cash equivalents Total cash and cash equivalents 1,248,992 946,626 1,294,532 Current financial assets

1 / 2 Accounting Title 2017/03/31 2016/12/31 2016/03/31 Balance Sheet Assets Current assets Cash and cash equivalents Total cash and cash equivalents 1,248,992 946,626 1,294,532 Current financial assets

James G. Zupka, CPA, Inc. Certified Public Accountants

AURORA CITY SCHOOL DISTRICT PORTAGE COUNTY, OHIO AUDIT REPORT FOR THE FISCAL YEAR ENDED James G. Zupka, CPA, Inc. Certified Public Accountants Board of Education Aurora City School District 102 East Garfield

AURORA CITY SCHOOL DISTRICT PORTAGE COUNTY, OHIO AUDIT REPORT FOR THE FISCAL YEAR ENDED James G. Zupka, CPA, Inc. Certified Public Accountants Board of Education Aurora City School District 102 East Garfield

Chapter 2: Financial Statements and the Annual Report

True / False 1. Financial statements are intended to tell the reader the value of a company. False LEARNING OBJECTIVES: FACC.PONO.13.02-01 - LO: 03-01 2. Accountants are the main reason financial statements

True / False 1. Financial statements are intended to tell the reader the value of a company. False LEARNING OBJECTIVES: FACC.PONO.13.02-01 - LO: 03-01 2. Accountants are the main reason financial statements

Chapter 14. Statement of Cash Flows

1 Chapter 14 Statement of Cash Flows 2 Figure 14-1 3 Definition of Cash Cash consists of coin, currency, and available funds on deposit at the bank. Negotiable instruments such as money orders, certified

1 Chapter 14 Statement of Cash Flows 2 Figure 14-1 3 Definition of Cash Cash consists of coin, currency, and available funds on deposit at the bank. Negotiable instruments such as money orders, certified

US Financial Reporting - Primary Terms (Definition Report)

") 1 String usfr-gc General Concepts (usfr-gc:generalconcepts) This is a category for storing general concepts. General concepts are high-level business reporting concepts such as "assets" and "liabilities"

1 String usfr-gc General Concepts (usfr-gc:generalconcepts) This is a category for storing general concepts. General concepts are high-level business reporting concepts such as "assets" and "liabilities"

How Do You Calculate Cash Flow in Real Life for a Real Company?

How Do You Calculate Cash Flow in Real Life for a Real Company? Hello and welcome to our second lesson in our free tutorial series on how to calculate free cash flow and create a DCF analysis for Jazz

How Do You Calculate Cash Flow in Real Life for a Real Company? Hello and welcome to our second lesson in our free tutorial series on how to calculate free cash flow and create a DCF analysis for Jazz

Project Cost Management

PDHonline Course P104 (8 PDH) Project Cost Management Instructor: William J. Scott, P.E. 2012 PDH Online PDH Center 5272 Meadow Estates Drive Fairfax, VA 22030-6658 Phone & Fax: 703-988-0088 www.pdhonline.org

PDHonline Course P104 (8 PDH) Project Cost Management Instructor: William J. Scott, P.E. 2012 PDH Online PDH Center 5272 Meadow Estates Drive Fairfax, VA 22030-6658 Phone & Fax: 703-988-0088 www.pdhonline.org

TOTAL TRAINING SOLUTIONS

TOTAL TRAINING SOLUTIONS RATIO ANALYSIS TO DETERMINE FINANCIAL STRENGTH Examining a Borrowers Five Vital Signs Jeffery W. Johnson Bankers Insight Group, LLC jeffery.johnson@bankers-insight.com October

TOTAL TRAINING SOLUTIONS RATIO ANALYSIS TO DETERMINE FINANCIAL STRENGTH Examining a Borrowers Five Vital Signs Jeffery W. Johnson Bankers Insight Group, LLC jeffery.johnson@bankers-insight.com October

Cash Flow Statement Analysis

Cash Flow Statement Analysis 1. INTRODUCTION Recall from the article on the income statement that a company will recognize revenue regardless of when payment is received. For example, a company may sell

Cash Flow Statement Analysis 1. INTRODUCTION Recall from the article on the income statement that a company will recognize revenue regardless of when payment is received. For example, a company may sell

Selling, general and administrative expenses 35,645 33,787. Net other operating income (292) (270) Operating profit 44,202 17,756

(270) Operating profit 44,202 17,756") Condensed Interim Consolidated Income Statement For the quarter ended September 30 Continuing operations Revenue 328,071 258,941 Cost of sales 248,516 207,668 Gross profit 79,555 51,273 Selling, general

Condensed Interim Consolidated Income Statement For the quarter ended September 30 Continuing operations Revenue 328,071 258,941 Cost of sales 248,516 207,668 Gross profit 79,555 51,273 Selling, general

Financial Statement Analysis for the Boardroom. An Attorney s Guide September 13, 2017

Financial Statement Analysis for the Boardroom An Attorney s Guide September 13, 2017 Contact information For more information, please contact one of the following members of the engagement team: Marc

Financial Statement Analysis for the Boardroom An Attorney s Guide September 13, 2017 Contact information For more information, please contact one of the following members of the engagement team: Marc