INTERMEDIATE ACCOUNTING

|

|

|

- Damon Hampton

- 5 years ago

- Views:

Transcription

1 Chapter 2 Financial Reporting: Its Conceptual Framework INTERMEDIATE ACCOUNTING

2 Objectives 1. Explain the FASB Conceptual Framework. 2. Explain the general and specific objectives of general purpose financial reporting. 3. Explain the qualitative characteristics of decision-useful information as identified in the FASB and IASB joint Conceptual Framework project. 4. Understand and apply the major principles and assumptions of financial reporting and U.S. GAAP. 5. Describe the financial reporting model in the FASB Conceptual Framework. 6. (Appendix 2.1) Understand the current status of the ongoing project by the FASB and IASB to develop a joint Conceptual Framework.

3 FASB Conceptual Framework (Slide 1 of 2) The intent of FASB s Conceptual Framework is to establish a theoretical foundation of interrelated objectives, concepts, and definitions that leads to the establishment of consistent high-quality financial accounting standards in accounting practice, and the appropriate application of those standards in accounting practice.

4 FASB Conceptual Framework (Slide 2 of 2) The Conceptual Framework is intended to: Guide the FASB in establishing accounting standards Provide a frame of reference for financial statement preparers and auditors for resolving accounting questions in situations where a standard does not exist Establish objectives and conceptual guidelines that form the bounds for judgment in the preparation of financial statements Increase users understanding of and confidence in financial reporting Enhance financial statement comparability across companies and over time

5 Accounting Principles Accounting principles are fundamental theories, truths and propositions that serve as the foundation for financial accounting and financial reporting. The most fundamental statements of these principles come from FASB s Statements of Financial Accounting Concepts Also known as Concept Statements Generally broad and definitional

6 Accounting Concepts FASB s Statements of Financial Accounting Concepts are general proclamations that establish: Fundamental principles of accounting Objectives of financial reporting Qualities of useful financial accounting information Definitions of basic elements like assets and liabilities Types of economic transactions, events, and arrangements to be recognized in financial statements Measurement attributes to use to measure and report these transactions, events, and arrangements How transactions, events, and arrangements should be presented and classified in financial statements Are the basis and objectives of GAAP

7 Accounting Standards Accounting standards Establish the authoritative guidance on how companies should account for and report specific transactions, events, and arrangements in their financial statements. Specific accounting standards in GAAP provide guidance on when and how to recognize and measure these elements in financial statements. Within accounting standards, rules exist, which are specific implementation procedures.

8 Relationship of Principles, Concepts, Standards, and Rules

9 Conceptual Framework: Brief History Statement of Financial Accounting Concepts No. 1 Objectives of Financial Reporting by Business Enterprises (1978) Established primary objectives of financial accounting Statement of Financial Accounting Concepts No. 2 Qualitative Characteristics of Accounting Information (1980) Accounting projects define the accounting elements and identify which elements should be recognized in financial statements, when they should be reported, and how they should be measured. Reporting projects deal with how elements of financial reports are classified and presented, what information should be provided, and where information should be presented.

10 Conceptual Framework: Current Status FASB and IASB are working closely together to develop a common Conceptual Framework. Goal is to develop standards that are objectivesbased, internally consistent, and internationally converged. Eight phase process with one phase complete and three other phases in process Statement of Financial Accounting Concepts No. 8 Conceptual Framework for Financial Reporting 2010

11 Conceptual Framework Projects

12 What are the Objectives of Financial Reporting? (Slide 1 of 2)

13 What are the Objectives of Financial Reporting? (Slide 2 of 2)

14 Objective 1: Information Useful in Decision Making Financial reporting should provide useful information about the reporting entity for: Existing and potential investors shareholders, equity fund managers, and analysts Lenders banks, lending institutions, bondholders, and credit rating agencies Other creditors who make decisions about providing resources to the entity suppliers, customers, and employees with claims

15 Objective 2: Information Useful to External Users in Assessing Expected Returns Information needs of investors, lenders, and other creditors Suppliers of financial capital are primarily interested in the amounts, timing, and uncertainty of the prospective cash flows they will receive. Need to assess the expected returns from buying, selling, or holding a company s equity, debt or other financial instruments External users need financial information to form expectations about the timing and amount of prospective cash receipts and assess the risk involved.

16 Objective 3: Information Useful in Assessing Company Cash Flows Financial reporting should provide information to help external investors, lenders, and other creditors in assessing the amounts, timing and uncertainty of the prospective net cash inflows to the company. Company s ability to generate net cash inflows determines both its ability to pay dividends and interest and the market prices of its securities. These affect the cash flows to investors, lenders, and creditors.

17 Information about Economic Resources and Claims on the Company Financial reporting should provide information about a company s economic resources and the claims on the company. This information is useful to external users for the following reasons: To identify the company s resources, obligations, financial strengths and weaknesses, and to assess its liquidity and solvency To specify the types of resources in which the company has invested, as well as the types and timing on the claims of the company To indicate the potential future cash flows from the company s resources and the ability of the resources to satisfy the claims on the company

18 Information about Financial Performance Changes in the Company s Resources and Claims Financial reporting should provide information about the financial performance which causes the company s resources and the claims on the company to change during the period. Information concerning the company s net income, comprehensive income, and their components is useful to external users in: Evaluating management s performance Estimating the company s earning power or other amounts that are representative of persistent long-term income-producing ability Predicting future income and net cash flows Assessing the risk of investing in or lending to the company

19 Accrual Accounting Accrual accounting measures and reports the economic effects of a company s transactions, events, and circumstances on a company s economic resources and claims in the period in which those effects occur, even if the related cash receipts and payments occur in a different period. Provides a better basis for assessing the company s past and future performance than information solely about cash receipts and payments.

20 Information about Cash Flow Changes in the Company s Resources and Claims Financial reporting should provide information about how a company s cash flows cause changes in the company s resources and claims. Cash flow information shows how a company obtains and spends cash for its operating, investing, and financing activities. Investors, lenders, and other creditors use cash flow information about a company to: Help understand its operations and its cash-generating ability Evaluate its strategic sourcing and use of cash for financing and investing activities Assess its liquidity and solvency Interpret other information about financial performance

21 Information about Management and the Governing Board as they Relate to Resources Financial reporting should provide information about how efficiently and effectively the company s management and governing board have discharged their responsibilities to use the company s resources. Referred to as management s stewardship responsibility Management is responsible to the owners for: The custody and safekeeping of the resources Their efficient and profitable use Their protection against unfavorable economic impacts, technological advances, and social changes Provided in Statement of Financial Accounting Concepts No. 8

22 Types of Useful Information for Investors, Lenders, and Other Creditors The following types of information are helpful in assessing the amounts, timing, and uncertainty of expected future cash flows to a company: Return on investment measure of overall company performance for equity shareholders Risk the uncertainty or unpredictability of future profitability of a company Financial flexibility the ability of a company to use its financial resources to adapt to change and to take advantage of opportunities Liquidity refers to how quickly a company can convert its assets into cash to meet short-term obligations and cover operating costs Operating capability refers to the ability of a company to produce goods and services for customers

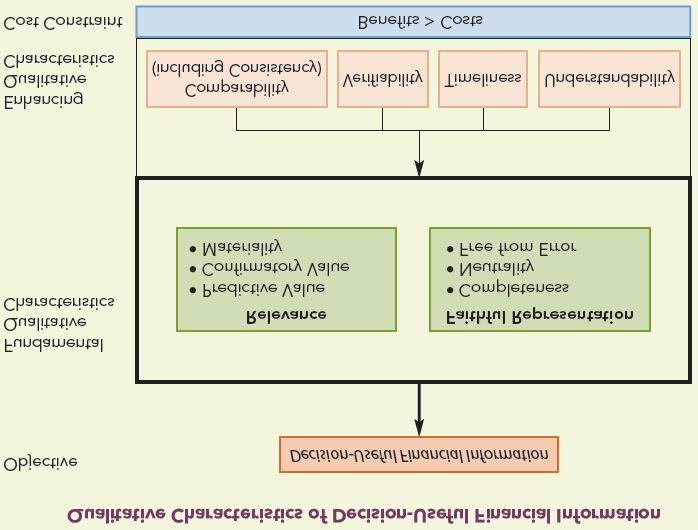

23 What Qualities Make Accounting Information Useful? Decision-useful information Defined by the joint Conceptual Framework in terms of fundamental qualitative characteristics and enhancing qualitative characteristics Qualitative characteristics guide standard setters and financial statement preparers when choosing among accounting alternatives Qualities distinguish more-useful from less-useful information.

24 Qualitative Characteristics

25 Decision Usefulness Decision usefulness is the ultimate objective of accounting information. It can be achieved if the information has a sufficient degree of the fundamental characteristics of relevance and faithful representation.

26 Relevance Relevance information that is capable of making a difference in decisions made by financial statement users Predictive Value information that should help users form expectations about the future Confirmatory Value information that provides feedback to confirm or correct prior predictions and expectations Materiality refers to the nature and magnitude of an omission or misstatement of accounting information that would influence the judgment of a reasonable person relying on that information

27 Faithful Representation Faithful representation when the words and numbers accurately predict the economic substance of what they purport to represent Complete representation provides a user with full disclosure of all information necessary to understand the information being reported, with all necessary facts, descriptions, and explanations Neutral representation not biased, slanted, emphasized or otherwise manipulated to achieve a predetermined result or to influence users behavior in a particular direction Free from error the information is measured and described as accurately as possible, using a process that reflects the best available inputs

28 The Relation between Relevance and Faithful Representation Accounting information is most useful when it is both relevant and faithfully represented. Both characteristics should be maximized. To provide users with the most decision-useful information possible

29 Process of Applying Fundamental Qualitative Characteristics Step 1 Identify an economic transaction, event, or arrangement that needs to be recognized in the financial statements. Step 2 Identify the type of information about that phenomenon that would be most relevant material and capable of making a difference in decision makers predictions of future outcomes/or confirmations of past predictions. Step 3 Determine whether that information can be faithfully represented in a manner that is complete, neutral, and free from error. Step 4 Determine whether the benefits of that information are likely to exceed its cost. What are the possible outcomes?

30 Enhancing Characteristics (Slide 1 of 2) Comparability enables users of accounting information to identify and explain similarities and differences between two or more sets of economic facts Consistency means that accounting methods and procedures are applied in the same manner from period to period Verifiability accounting information is verifiable when different knowledgeable and independent observers can reach consensus that a particular representation is faithful

31 Enhancing Characteristics (Slide 2 of 2) Timeliness accounting information is timely when it is available to decision makers in time to influence their decisions Understandability the accounting information should be comprehensible to users who have a reasonable knowledge of business and economic activities and who are willing to study the information carefully What single, pervasive constraint bounds the qualitative characteristics of the financial information disclosed in a company s financial reports? Cost Constraint: Benefit > Costs

32 Accounting Assumptions and Principles Certain accounting assumptions and principles have had an important impact on the development of GAAP: Reporting Entity or Economic Entity Assumption Going Concern Assumption Period-of-Time Assumption Monetary Unit Assumption Mixed Attribute Measurement Model Recognition Accrual Accounting Conservatism

33 Reporting Entity or Economic Entity Assumption This assumption states that a business enterprise is a legally and economically distinct entity so that financial statements can be prepared and reported specifically for that entity. For the purposes of financial accounting, the size of a business is irrelevant. May vary from sole proprietorships to multi-national corporations with subsidiary companies What differences may exist between these types of companies when reporting financial information?

34 Going Concern or Continuity Assumption The assumption is that the company will continue to operate in the foreseeable future. Without substantial evidence to the contrary, the company can be reasonably expected to operate long enough to realize economic benefits from its assets and satisfy its existing obligations. Do companies that appear to be going bankrupt meet the going concern assumption? Why or why not?

35 Period-of-Time Assumption The period-of-time assumption requires that financial statement users prepare and report financial statements in an annual report with the SEC. Provides timely information to decision makers The annual reporting period is often referred to as the accounting period or fiscal year which may or may not mirror the calendar year. Some companies choose a fiscal year that more closely approximates their annual business cycle, which is the yearly period from lowest sales through highest sales and back to lowest sales.

36 Monetary Unit Assumption Accountants generally use the national currency of the reporting entity as the monetary unit of measure in preparing financial statements. Is the United States dollar considered to be a stable monetary unit for preparing a company s financial statements? Why or why not?

37 Mixed Attribute Measurement Model (Slide 1 of 2) This model seeks to measure assets, liabilities, revenues, expenses, and other elements of the financial statements with the most relevant and faithful measurement available. What types of measurements would be included? Historical costs Allocated historical costs Fair values Present values of future cash flows Net realizable values

38 Mixed Attribute Measurement Model (Slide 2 of 2) The economic activities and resources of a company initially are measured using the exchange price or historical cost at the time each transaction occurs. This cost is the most relevant and faithful representation of the value of the exchange. The historical cost provides evidence that independent parties have willingly agreed on the value of the items exchanged at the time of the transaction. What are the qualities of historical cost? Relevance Representational faithfulness (Neutrality) Verifiability What are the differences between historical cost and fair value?

39 Recognition Recognition is the process of formally recording and reporting an item in the financial statements of a company. A recognized item is shown in both words and numbers, with the amount included in the financial statement totals. To be recognized, an item must: Meet the definition of an element (asset, liability, etc.) Be measurable Be relevant Be representationally faithful

40 Accrual Accounting Accrual accounting is the process of measuring and reporting the economic effects of transactions, events, and arrangements in the period when those effects occur, even though cash flows may occur in a different period. Accruals when economic effects are recognized in the current period even though the cash flows will occur in a later period Deferrals when cash flows occur in the current period but economic effects will be recognized in a later period What are some examples of accruals and deferrals?

41 Principles of Accrual Accounting The Revenue Recognition Principle determines the appropriate period in which a company creates economic benefits and can recognize revenues in income The Expense Recognition Principle determines the appropriate period in which a company has consumed economic resources in conducting business operations The Matching Principle matches the expense to the period in which the economic benefits are consumed by generating revenues

42 Conservatism Conservatism is an approach that accountants use to avoid overstating net assets and net income when these amounts are uncertain. Results in the reporting of lower assets values or higher liability values when those values are uncertain Conservatism is a practical approach accountants take to avoid misleading investors, lenders, and other creditors when valuations are uncertain. What is another name for conservatism? Prudence conservatism is a prudent reaction to uncertainty to ensure, to the extent possible, that the uncertainties and risks inherent in the business situations are adequately considered.

43 Sources of Information Used in External Decision Making

44 Status of the Joint FASB and IASB Conceptual Framework This project is split into eight phases: 1 Objective and qualitative characteristics 2 Elements and recognition 3 Measurement 4 Reporting entity 5 Presentation and disclosure 6 Framework for a GAAP hierarchy 7 Applicability to the not-for-profit sector 8 Remaining issues Each phase will involve extensive planning, research, and deliberations.

45 Phase One: Objective and Qualitative Characteristics Phase 1 is complete and resulted in the FASB and IASB jointly issuing: Statement of Financial Accounting Concepts No. 8 - Conceptual Framework for Financial Reporting Chapter 1 The Objective of General Purpose Financial Reporting Chapter 2 Qualitative Characteristics of Useful Financial Information These chapters supersede FASB Concepts Statements No. 1 and No. 2.

46 Ongoing Phases The Boards have temporarily placed the Conceptual Framework on hold while they focus on finalizing convergence on several major specific standards. Three other active phases were put on hold. Phase Two: Elements and Recognition exploring potential ways to refine and improve definitions of assets and liabilities Phase Three: Measurement evaluating various measurement techniques for assets and liabilities that satisfy the objective and qualitative characteristics Phase Four: Reporting Entity working on refining the definition of a reporting entity and the appropriate presentation in financial statements for a group entity

CHAPTER 2. Financial Reporting: Its Conceptual Framework CONTENT ANALYSIS OF END-OF-CHAPTER ASSIGNMENTS

2-1 CONTENT ANALYSIS OF END-OF-CHAPTER ASSIGNMENTS NUMBER Q2-1 Conceptual Framework Q2-2 Conceptual Framework Q2-3 Conceptual Framework Q2-4 Conceptual Framework Q2-5 Objective of Financial Reporting Q2-6

2-1 CONTENT ANALYSIS OF END-OF-CHAPTER ASSIGNMENTS NUMBER Q2-1 Conceptual Framework Q2-2 Conceptual Framework Q2-3 Conceptual Framework Q2-4 Conceptual Framework Q2-5 Objective of Financial Reporting Q2-6

CHAPTER 2. Financial Reporting: Its Conceptual Framework CONTENT ANALYSIS OF END-OF-CHAPTER ASSIGNMENTS

2-1 CONTENT ANALYSIS OF END-OF-CHAPTER ASSIGNMENTS CHAPTER 2 Financial Reporting: Its Conceptual Framework NUMBER TOPIC CONTENT LO ADAPTED DIFFICULTY 2-1 Conceptual Framework 2-2 Conceptual Framework 2-3

2-1 CONTENT ANALYSIS OF END-OF-CHAPTER ASSIGNMENTS CHAPTER 2 Financial Reporting: Its Conceptual Framework NUMBER TOPIC CONTENT LO ADAPTED DIFFICULTY 2-1 Conceptual Framework 2-2 Conceptual Framework 2-3

FINANCIAL REPORTING: ITS CONCEPTUAL FRAMEWORK

2 FINANCIAL REPORTING: ITS CONCEPTUAL FRAMEWORK CHAPTER OBJECTIVES After careful study of this chapter, students will be able to: 1. Explain the FASB conceptual framework. 2. Understand the relationship

2 FINANCIAL REPORTING: ITS CONCEPTUAL FRAMEWORK CHAPTER OBJECTIVES After careful study of this chapter, students will be able to: 1. Explain the FASB conceptual framework. 2. Understand the relationship

The Conceptual Framework for Financial Reporting

1. Introduction The Conceptual Framework sets out the concepts which underlie the preparation and presentation of financial statements for external users (Conceptual Framework, Section Purpose and status

1. Introduction The Conceptual Framework sets out the concepts which underlie the preparation and presentation of financial statements for external users (Conceptual Framework, Section Purpose and status

CHAPTER 2 THE FRAMEWORK OF INTERNATIONAL ACCOUNTING STANDARD BOARD (IASB) INTRODUCTION

INTRODUCTION") CHAPTER 2 THE FRAMEWORK OF INTERNATIONAL ACCOUNTING STANDARD BOARD (IASB) INTRODUCTION In order to narrowing the differences in recognition and measurement of elements of financial statements and harmonization

CHAPTER 2 THE FRAMEWORK OF INTERNATIONAL ACCOUNTING STANDARD BOARD (IASB) INTRODUCTION In order to narrowing the differences in recognition and measurement of elements of financial statements and harmonization

Conceptual Framework (Revised) Issued June Conceptual Framework for Financial Reporting 2018

Issued June Conceptual Framework for Financial Reporting 2018") Conceptual Framework (Revised) Issued June 2018 Conceptual Framework for Financial Reporting 2018 COPYRIGHT Copyright 2018 Hong Kong Institute of Certified Public Accountants This Framework contains the

Conceptual Framework (Revised) Issued June 2018 Conceptual Framework for Financial Reporting 2018 COPYRIGHT Copyright 2018 Hong Kong Institute of Certified Public Accountants This Framework contains the

Pervasive Principles in Preparing Financial Statements

Session 2 Pervasive Principles in Preparing Financial Statements 1 Learning Points Know about FASB s Conceptual Framework Learn about the Objectives of Financial Reporting Understand the Qualitative characteristics

Session 2 Pervasive Principles in Preparing Financial Statements 1 Learning Points Know about FASB s Conceptual Framework Learn about the Objectives of Financial Reporting Understand the Qualitative characteristics

IFRS Conceptual Framework Conceptual Framework for Financial Reporting

March 2018 IFRS Conceptual Framework Conceptual Framework for Financial Reporting Conceptual Framework for Financial Reporting Conceptual Framework for Financial Reporting is issued by the International

March 2018 IFRS Conceptual Framework Conceptual Framework for Financial Reporting Conceptual Framework for Financial Reporting Conceptual Framework for Financial Reporting is issued by the International

The Conceptual Framework for Financial Reporting

The Conceptual Framework for Financial Reporting The Conceptual Framework for Financial Reporting (the Conceptual Framework) was issued by the International Accounting Standards Board in September 2010.

The Conceptual Framework for Financial Reporting The Conceptual Framework for Financial Reporting (the Conceptual Framework) was issued by the International Accounting Standards Board in September 2010.

The Conceptual Framework for Financial Reporting

The Conceptual Framework for Financial Reporting The Conceptual Framework was issued by the IASB in September 2010. It superseded the Framework for the Preparation and Presentation of Financial Statements.

The Conceptual Framework for Financial Reporting The Conceptual Framework was issued by the IASB in September 2010. It superseded the Framework for the Preparation and Presentation of Financial Statements.

The Conceptual Framework for Financial Reporting

The Conceptual Framework for Financial Reporting The Conceptual Framework was issued by the International Accounting Standards Board in September 2010. It superseded the Framework for the Preparation and

The Conceptual Framework for Financial Reporting The Conceptual Framework was issued by the International Accounting Standards Board in September 2010. It superseded the Framework for the Preparation and

IFRS Explained - supplement. Chapter 1 The IASB and the regulatory framework. Chapter 2 Conceptual framework for financial reporting

IFRS Explained - supplement Chapter 1 The IASB and the regulatory framework The organisations mentioned in this chapter were renamed in July 2010 as follows: The IASC Foundation became the IFRS Foundation

IFRS Explained - supplement Chapter 1 The IASB and the regulatory framework The organisations mentioned in this chapter were renamed in July 2010 as follows: The IASC Foundation became the IFRS Foundation

The Conceptual Framework for Financial Reporting

The Conceptual Framework for Financial Reporting CONTENTS THE CONCEPTUAL FRAMEWORK FOR FINANCIAL REPORTING paragraphs INTRODUCTION Purpose and status Scope CHAPTERS 1 The objective of general purpose financial

The Conceptual Framework for Financial Reporting CONTENTS THE CONCEPTUAL FRAMEWORK FOR FINANCIAL REPORTING paragraphs INTRODUCTION Purpose and status Scope CHAPTERS 1 The objective of general purpose financial

New Zealand Equivalent to the IASB Conceptual Framework for Financial Reporting (2018 NZ Conceptual Framework)

") New Zealand Equivalent to the IASB Conceptual Framework for Financial Reporting (2018 NZ Conceptual Framework) Issued May 2018 Issued by the New Zealand Accounting Standards Board of the External Reporting

New Zealand Equivalent to the IASB Conceptual Framework for Financial Reporting (2018 NZ Conceptual Framework) Issued May 2018 Issued by the New Zealand Accounting Standards Board of the External Reporting

CIMA F1. Financial Operations Student Notes

CIMA F1 Financial Operations Student Notes Contents CIMA F1...1 Topic 6 The Regulatory Environment...2 International Financial Reporting Standards (IFRSs)...5 Topic 7: The Conceptual Framework...7 Topic

CIMA F1 Financial Operations Student Notes Contents CIMA F1...1 Topic 6 The Regulatory Environment...2 International Financial Reporting Standards (IFRSs)...5 Topic 7: The Conceptual Framework...7 Topic

CHAPTER TWO Concepts and principles

C1. IFRS Conceptual Framework for Financial Reporting CHAPTER TWO Concepts and principles 2.1 CONCEPTS 2.1.1 Introduction 2.1.1.1 As explained at paragraphs 1.2.8 to 1.2.11, the Code adapts and interprets

C1. IFRS Conceptual Framework for Financial Reporting CHAPTER TWO Concepts and principles 2.1 CONCEPTS 2.1.1 Introduction 2.1.1.1 As explained at paragraphs 1.2.8 to 1.2.11, the Code adapts and interprets

Detailed Alert International Accounting Standards: Framework for the Preparation and Presentation of Financial Statements (1989) Preface

Preface") Abstract The Framework for the Preparation and Presentation of Financial Statements sets out the concepts that underlie the preparation and presentation of financial statements for external users. The

Abstract The Framework for the Preparation and Presentation of Financial Statements sets out the concepts that underlie the preparation and presentation of financial statements for external users. The

CHAPTER 2 CONCEPTUAL FRAMEWORK FOR FINANCIAL REPORTING. IFRS questions are available at the end of this chapter. TRUE-FALSE Conceptual

CHAPTER 2 CONCEPTUAL FRAMEWORK FOR FINANCIAL REPORTING IFRS questions are available at the end of this chapter. TRUE-FALSE Conceptual Answer No. Description T 1. Nature of conceptual framework. T 2. Conceptual

CHAPTER 2 CONCEPTUAL FRAMEWORK FOR FINANCIAL REPORTING IFRS questions are available at the end of this chapter. TRUE-FALSE Conceptual Answer No. Description T 1. Nature of conceptual framework. T 2. Conceptual

Test Bank for Intermediate Accounting 14th Edition by Donald E. Kieso, Jerry J. Weygandt and Terry D. Warfield

Test Bank for Intermediate Accounting 14th Edition by Donald E. Kieso, Jerry J. Weygandt and Terry D. Warfield Link download full : https://digitalcontentmarket.org/download/test-bankforintermediate-accounting-14th-edition-by-kieso-weygandt-and-warfield/

Test Bank for Intermediate Accounting 14th Edition by Donald E. Kieso, Jerry J. Weygandt and Terry D. Warfield Link download full : https://digitalcontentmarket.org/download/test-bankforintermediate-accounting-14th-edition-by-kieso-weygandt-and-warfield/

CHAPTER II ACCOUNTING STANDARDS AND FINANCIAL REPORTING INFORMATION

CHAPTER II ACCOUNTING STANDARDS AND FINANCIAL REPORTING INFORMATION 2.1. Introduction 2.2.Meaning of Accounting 2.3.Objectives of Accounting 2.3.1. Accounting Concepts 2.3.2. Accounting Principles 2.3.3.

CHAPTER II ACCOUNTING STANDARDS AND FINANCIAL REPORTING INFORMATION 2.1. Introduction 2.2.Meaning of Accounting 2.3.Objectives of Accounting 2.3.1. Accounting Concepts 2.3.2. Accounting Principles 2.3.3.

Framework for the Preparation and Presentation of Financial Statements

Framework for the Preparation and Presentation of Financial Statements The IASB Framework was approved by the IASC Board in April 1989 for publication in July 1989, and adopted by the IASB in April 2001.

Framework for the Preparation and Presentation of Financial Statements The IASB Framework was approved by the IASC Board in April 1989 for publication in July 1989, and adopted by the IASB in April 2001.

FRAMEWORK FOR THE PREPARATION AND PRESENTATION OF FINANCIAL STATEMENTS

FRAMEWORK FOR THE PREPARATION AND PRESENTATION OF FINANCIAL STATEMENTS CONTENTS Paragraphs PREFACE INTRODUCTION 1 11 Purpose and status 1 4 Scope 5 8 Users and their information needs 9 11 THE OBJECTIVE

FRAMEWORK FOR THE PREPARATION AND PRESENTATION OF FINANCIAL STATEMENTS CONTENTS Paragraphs PREFACE INTRODUCTION 1 11 Purpose and status 1 4 Scope 5 8 Users and their information needs 9 11 THE OBJECTIVE

FRAMEWORK FOR THE PREPARATION AND PRESENTATION OF FINANCIAL STATEMENTS

FRAMEWORK FOR THE PREPARATION AND PRESENTATION OF FINANCIAL STATEMENTS as published by the Commission of the European Communities in November 2003. The IASB Framework was approved by the IASC Board in

FRAMEWORK FOR THE PREPARATION AND PRESENTATION OF FINANCIAL STATEMENTS as published by the Commission of the European Communities in November 2003. The IASB Framework was approved by the IASC Board in

PUBLIC BENEFIT ENTITIES FRAMEWORK

PUBLIC BENEFIT ENTITIES FRAMEWORK Issued March 2014 This Authoritative Notice, the PBE Framework, was issued by the New Zealand Accounting Standards Board of the External Reporting Board pursuant to section

PUBLIC BENEFIT ENTITIES FRAMEWORK Issued March 2014 This Authoritative Notice, the PBE Framework, was issued by the New Zealand Accounting Standards Board of the External Reporting Board pursuant to section

Framework for the Preparation and Presentation of Financial Statements

for the Preparation and Presentation of Financial Statements The IASB was approved by the IASC Board in April 1989 for publication in July 1989, and adopted by the IASB in April 2001. IASCF B1709 CONTENTS

for the Preparation and Presentation of Financial Statements The IASB was approved by the IASC Board in April 1989 for publication in July 1989, and adopted by the IASB in April 2001. IASCF B1709 CONTENTS

Name Chapter 1--Financial Reporting Description Instructions

Name Chapter 1--Financial Reporting Description Instructions Modify Question 1 Multiple Choice 0 points Modify Remove Question The overall objective of financial reporting is to provide information Answer

Name Chapter 1--Financial Reporting Description Instructions Modify Question 1 Multiple Choice 0 points Modify Remove Question The overall objective of financial reporting is to provide information Answer

Chapter 01 Environment and Theoretical Structure of Financial. Accounting Answer Key

Chapter 01 Environment and Theoretical Structure of Financial Accounting Answer Key True / False Questions 1. The primary function of financial accounting is to provide relevant financial information to

Chapter 01 Environment and Theoretical Structure of Financial Accounting Answer Key True / False Questions 1. The primary function of financial accounting is to provide relevant financial information to

CHAPTER 2 CONCEPTUAL FRAMEWORK UNDERLYING FINANCIAL ACCOUNTING. TRUE-FALSE Conceptual. MULTIPLE CHOICE Conceptual

CHAPTER 2 CONCEPTUAL FRAMEWORK UNDERLYING FINANCIAL ACCOUNTING TRUE-FALSE Conceptual Answer No. Description F 1. Nature of conceptual framework. T 2. Conceptual framework definition. F 3. Levels of conceptual

CHAPTER 2 CONCEPTUAL FRAMEWORK UNDERLYING FINANCIAL ACCOUNTING TRUE-FALSE Conceptual Answer No. Description F 1. Nature of conceptual framework. T 2. Conceptual framework definition. F 3. Levels of conceptual

Understanding IFRSs A Framework-based approach to applying IFRSs

August 2011 International Financial Reporting Standards Understanding IFRSs A Framework-based approach to applying IFRSs Michael Wells, Director, IFRS Education Initiative, IFRS Foundation The views expressed

August 2011 International Financial Reporting Standards Understanding IFRSs A Framework-based approach to applying IFRSs Michael Wells, Director, IFRS Education Initiative, IFRS Foundation The views expressed

Module 1: The role and importance of financial reporting

MODULE 1: The role and importance of financial reporting Part A: The role and importance of financial reporting The role of financial reporting The importance of financial reporting Who must prepare general

MODULE 1: The role and importance of financial reporting Part A: The role and importance of financial reporting The role of financial reporting The importance of financial reporting Who must prepare general

Intermediate Accounting, Vol 1, 3e (Lo/Fisher) Chapter 2 Conceptual Frameworks for Financial Reporting. Learning Objective 1

Chapter 2 Conceptual Frameworks for Financial Reporting. Learning Objective 1") Intermediate Accounting, Vol 1, 3e (Lo/Fisher) Chapter 2 Conceptual Frameworks for Financial Reporting Learning Objective 1 1) Which of the following is NOT a purpose of a conceptual framework of accounting

Intermediate Accounting, Vol 1, 3e (Lo/Fisher) Chapter 2 Conceptual Frameworks for Financial Reporting Learning Objective 1 1) Which of the following is NOT a purpose of a conceptual framework of accounting

Framework for the Preparation and Presentation of Financial Statements

10 Framework for the Preparation and Presentation of Financial Statements Contents INTRODUCTION Paragraphs 1-11 Purpose and Status 1-4 Scope 5-8 Users and Their Information Needs 9-11 THE OBJECTIVE OF

10 Framework for the Preparation and Presentation of Financial Statements Contents INTRODUCTION Paragraphs 1-11 Purpose and Status 1-4 Scope 5-8 Users and Their Information Needs 9-11 THE OBJECTIVE OF

Accounting Basics. Learning Outcomes. Chapter 1 Environment and Theoretical Structure of Financial Accounting

Chapter 1 Environment and Theoretical Structure of Financial Accounting Intermediate Accounting I Dr. Chula King Accounting Basics Accounting takes an enterprise s financial data and converts it into financial

Chapter 1 Environment and Theoretical Structure of Financial Accounting Intermediate Accounting I Dr. Chula King Accounting Basics Accounting takes an enterprise s financial data and converts it into financial

Framework for the Preparation and Presentation of Financial Statements

for the Preparation and Presentation of Financial Statements CONTENTS paragraphs PREFACE INTRODUCTION 1-11 Purpose and status 1-4 Scope 5-8 Users and their information needs 9-11 THE OBJECTIVE OF FINANCIAL

for the Preparation and Presentation of Financial Statements CONTENTS paragraphs PREFACE INTRODUCTION 1-11 Purpose and status 1-4 Scope 5-8 Users and their information needs 9-11 THE OBJECTIVE OF FINANCIAL

IFAC IPSASB Meeting Agenda Paper 2.0 June 2008 Moscow, Russia Page 1 of 5

IFAC IPSASB Meeting Agenda Paper 2.0 June 2008 Moscow, Russia Page 1 of 5 INTERNATIONAL FEDERATION OF ACCOUNTANTS 545 Fifth Avenue, 14th Floor Tel: (212) 286-9344 New York, New York 10017 Fax: (212) 286-9570

IFAC IPSASB Meeting Agenda Paper 2.0 June 2008 Moscow, Russia Page 1 of 5 INTERNATIONAL FEDERATION OF ACCOUNTANTS 545 Fifth Avenue, 14th Floor Tel: (212) 286-9344 New York, New York 10017 Fax: (212) 286-9570

Understanding IFRSs A Framework-based approach to applying IFRSs

International Financial Reporting Standards Understanding IFRSs A Framework-based approach to applying IFRSs Michael Wells, Director, IFRS Education Initiative, IFRS Foundation The views expressed in this

International Financial Reporting Standards Understanding IFRSs A Framework-based approach to applying IFRSs Michael Wells, Director, IFRS Education Initiative, IFRS Foundation The views expressed in this

MODULE 1: The role and importance of financial reporting Part A: The role and importance of financial reporting

MODULE 1: The role and importance of financial reporting Part A: The role and importance of financial reporting The role of financial reporting The importance of financial reporting Who must prepare general

MODULE 1: The role and importance of financial reporting Part A: The role and importance of financial reporting The role of financial reporting The importance of financial reporting Who must prepare general

NINJA BOOK FINANCIAL ACCOUNTING AND REPORTING I CONCEPTUAL FRAMEWORK & FINANCIAL STATEMENT PRESENTATION

NINJA BOOK FINANCIAL ACCOUNTING AND REPORTING I 2018 CONCEPTUAL FRAMEWORK & FINANCIAL STATEMENT PRESENTATION COPYRIGHT This book contains material copyrighted 1953 through 2018 by the American Institute

NINJA BOOK FINANCIAL ACCOUNTING AND REPORTING I 2018 CONCEPTUAL FRAMEWORK & FINANCIAL STATEMENT PRESENTATION COPYRIGHT This book contains material copyrighted 1953 through 2018 by the American Institute

IAA Phase 2 Issue Discussion Paper June 2005 IASB Framework

The issue and its background The IAA (or its predecessor, the IFAA) has been discussing accounting for insurance contracts with the IASB since 1997. On more than one occasion, proposals made by the IAA

The issue and its background The IAA (or its predecessor, the IFAA) has been discussing accounting for insurance contracts with the IASB since 1997. On more than one occasion, proposals made by the IAA

1. The primary function of financial accounting is to provide relevant financial information to parties external to business enterprises.

Page 1 of 38 1 Student: 1. The primary function of financial accounting is to provide relevant financial information to parties external to business enterprises. True False 2. Accrual accounting attempts

Page 1 of 38 1 Student: 1. The primary function of financial accounting is to provide relevant financial information to parties external to business enterprises. True False 2. Accrual accounting attempts

Decree approving the Accounting system for the Business Sector in Mozambique

Decree approving the Accounting system for the Business Sector in Mozambique Translation disclaimer This is a free and non official translation of the Decree 70/2009 dated 22 December made by Deloitte

Decree approving the Accounting system for the Business Sector in Mozambique Translation disclaimer This is a free and non official translation of the Decree 70/2009 dated 22 December made by Deloitte

Unit 2: ACCOUNTING CONCEPTS, PRINCIPLES AND CONVENTIONS

Unit 2: ACCOUNTING S, PRINCIPLES AND CONVENTIONS Accounting is a language of the business. Financial statements prepared by the accountant communicate financial information to the various stakeholders

Unit 2: ACCOUNTING S, PRINCIPLES AND CONVENTIONS Accounting is a language of the business. Financial statements prepared by the accountant communicate financial information to the various stakeholders

Understanding IFRSs. A Framework-based approach. International Financial Reporting Standards

#BkprsSMT October 2011 International Financial Reporting Standards Understanding IFRSs A Framework-based approach Michael Wells, Director, IFRS Education Initiative, IFRS Foundation The views expressed

#BkprsSMT October 2011 International Financial Reporting Standards Understanding IFRSs A Framework-based approach Michael Wells, Director, IFRS Education Initiative, IFRS Foundation The views expressed

WHERE DID CONSERVATISM GO?

WHERE DID CONSERVATISM GO? Sheldon R. Smith, Woodbury School of Business, Utah Valley University, 800 W. University Parkway, Orem, UT 84058, 801-863-6153, smithsh@uvu.edu Kevin R. Smith, Woodbury School

WHERE DID CONSERVATISM GO? Sheldon R. Smith, Woodbury School of Business, Utah Valley University, 800 W. University Parkway, Orem, UT 84058, 801-863-6153, smithsh@uvu.edu Kevin R. Smith, Woodbury School

EUROPEAN PUBLIC SECTOR ACCOUNTING STANDARDS

EUROPEAN COMMISSION EUROSTAT Directorate C: National Accounts, Prices and Key Indicators Task Force EPSAS EPSAS WG 18/07 Luxembourg, 25 April 2018 EUROPEAN PUBLIC SECTOR ACCOUNTING STANDARDS CONCEPTUAL

EUROPEAN COMMISSION EUROSTAT Directorate C: National Accounts, Prices and Key Indicators Task Force EPSAS EPSAS WG 18/07 Luxembourg, 25 April 2018 EUROPEAN PUBLIC SECTOR ACCOUNTING STANDARDS CONCEPTUAL

Module 2 Concepts and Pervasive Principles

IFRS for SMEs (2009) + Q&As IFRS Foundation: Training Material for the IFRS for SMEs Module 2 Concepts and Pervasive Principles IFRS Foundation: Training Material for the IFRS for SMEs including the full

IFRS for SMEs (2009) + Q&As IFRS Foundation: Training Material for the IFRS for SMEs Module 2 Concepts and Pervasive Principles IFRS Foundation: Training Material for the IFRS for SMEs including the full

Intermediate Accounting (Gordon/Raedy/Sannella) Chapter 2 Financial Reporting Theory. 2.1 Overview of the Conceptual Framework

Chapter 2 Financial Reporting Theory. 2.1 Overview of the Conceptual Framework") Intermediate Accounting (Gordon/Raedy/Sannella) Chapter 2 Financial Reporting Theory 2.1 Overview of the Conceptual Framework 1) The FASB has taken the conceptual framework to a higher level than the IASB.

Intermediate Accounting (Gordon/Raedy/Sannella) Chapter 2 Financial Reporting Theory 2.1 Overview of the Conceptual Framework 1) The FASB has taken the conceptual framework to a higher level than the IASB.

full file at

Chapter 01 Environment and Theoretical Structure of Financial Accounting True / False Questions 1. The primary function of financial accounting is to provide relevant financial information to parties external

Chapter 01 Environment and Theoretical Structure of Financial Accounting True / False Questions 1. The primary function of financial accounting is to provide relevant financial information to parties external

DOWNLOAD PDF IFRS CONCEPTUAL FRAMEWORK FOR FINANCIAL REPORTING MARCH 2018 FILETYPE

Chapter 1 : Conceptual Framework for Financial Reporting The International Accounting Standards Board (Board) has today issued a revised version of its Conceptual Framework for Financial Reporting that

Chapter 1 : Conceptual Framework for Financial Reporting The International Accounting Standards Board (Board) has today issued a revised version of its Conceptual Framework for Financial Reporting that

Parts. Learning Outcomes. Financial Accounting Review Part 1: Environment and Theoretical Structure of Financial Accounting

Financial Accounting Review Part 1: Environment and Theoretical Structure of Financial Accounting ACG 6309 Dr. Chula King 1 Parts Part 2: Double Entry Accounting its origins and significance Part 3: The

Financial Accounting Review Part 1: Environment and Theoretical Structure of Financial Accounting ACG 6309 Dr. Chula King 1 Parts Part 2: Double Entry Accounting its origins and significance Part 3: The

CONTACT HOURS FOR CALLS WEDNESDAYS AND THURSDAYS, 6PM TO 7PM

FINANCIAL ACCOUNT FOUNDATION LEVEL WEEK 1 QUESTIONS CONTACT NUMBER 08038400843 CONTACT HOURS FOR CALLS WEDNESDAYS AND THURSDAYS, 6PM TO 7PM TOPIC: INTRODUCTION AND IASB CONCEPTUAL FRAME WORK VIDEO LECTURE

FINANCIAL ACCOUNT FOUNDATION LEVEL WEEK 1 QUESTIONS CONTACT NUMBER 08038400843 CONTACT HOURS FOR CALLS WEDNESDAYS AND THURSDAYS, 6PM TO 7PM TOPIC: INTRODUCTION AND IASB CONCEPTUAL FRAME WORK VIDEO LECTURE

PREVIEW OF CHAPTER 2-2

2-1 PREVIEW OF CHAPTER 2 2-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 2 for Financial Reporting Conceptual Framework LEARNING OBJECTIVES After studying this chapter, you should

2-1 PREVIEW OF CHAPTER 2 2-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 2 for Financial Reporting Conceptual Framework LEARNING OBJECTIVES After studying this chapter, you should

CONTACT(S) Yulia Feygina +44 (0)

Yulia Feygina +44 (0)") IASB Agenda ref 10 STAFF PAPER IASB Meeting Project Paper topic Conceptual Framework Sweep issue: boundary of a reporting entity CONTACT(S) Yulia Feygina yfeygina@ifrs.org +44 (0)20 7332 2743 June 2017

IASB Agenda ref 10 STAFF PAPER IASB Meeting Project Paper topic Conceptual Framework Sweep issue: boundary of a reporting entity CONTACT(S) Yulia Feygina yfeygina@ifrs.org +44 (0)20 7332 2743 June 2017

The ASB published its Statement of Principles for Financial Reporting in December 1999.

Dr Philip E Dunn The ASB s Statement of Principles The ASB published its Statement of Principles for Financial Reporting in December 1999. It is a similar conceptual framework to that developed by the

Dr Philip E Dunn The ASB s Statement of Principles The ASB published its Statement of Principles for Financial Reporting in December 1999. It is a similar conceptual framework to that developed by the

Chapter 1 Environment and Theoretical Structure of Financial Accounting: Monday, May 21, 2018

Chapter 1 Environment and Theoretical Structure of Financial Accounting: Monday, May 21, 2018 8:54 PM Financial Accounting Environment Primary Focus of financial accounting is on the information needs

Chapter 1 Environment and Theoretical Structure of Financial Accounting: Monday, May 21, 2018 8:54 PM Financial Accounting Environment Primary Focus of financial accounting is on the information needs

IFRS. B V Subramaniam FCMA A CONCEPTUAL ANALYSIS

IFRS 1 A CONCEPTUAL ANALYSIS INTRODUCTION International Financial Reporting Standards (IFRS) are the world-wide accounting standards which consists of 1) Standards (IFRS statements & IAS standards) 2)

IFRS 1 A CONCEPTUAL ANALYSIS INTRODUCTION International Financial Reporting Standards (IFRS) are the world-wide accounting standards which consists of 1) Standards (IFRS statements & IAS standards) 2)

A Framework-based approach to teaching of IFRSs

International Financial Reporting Standards A Framework-based approach to teaching of IFRSs Michael Wells, Director, IFRS Education Initiative, IFRS Foundation The views expressed in this presentation

International Financial Reporting Standards A Framework-based approach to teaching of IFRSs Michael Wells, Director, IFRS Education Initiative, IFRS Foundation The views expressed in this presentation

Introduction to International Financial Reporting Standards

Introduction to International Financial Reporting Standards Structure of IASCF International Accounting Standards Committee Foundation (22 Trustees) InternationalAccounting Standards Board (15 members)

Introduction to International Financial Reporting Standards Structure of IASCF International Accounting Standards Committee Foundation (22 Trustees) InternationalAccounting Standards Board (15 members)

International Financial Reporting Standard (IFRS) for Small and Medium-sized Entities

for Small and Medium-sized Entities") International Financial Reporting Standard (IFRS) for Small and Medium-sized Entities Section 1 Small and Medium-sized Entities Intended scope of this Standard 1.1 The IFRS for SMEs is intended for use

International Financial Reporting Standard (IFRS) for Small and Medium-sized Entities Section 1 Small and Medium-sized Entities Intended scope of this Standard 1.1 The IFRS for SMEs is intended for use

KEY FEATURES OF THE NEW IFRS CONCEPTUAL FRAMEWORK

KEY FEATURES OF THE NEW IFRS CONCEPTUAL FRAMEWORK ON 29 MARCH 2018 THE IASB PUBLISHED ITS NEW CONCEPTUAL FRAMEWORK, NEARLY THREE YEARS AFTER THE 2015 EXPOSURE DRAFT. This text is accompanied by amendments

KEY FEATURES OF THE NEW IFRS CONCEPTUAL FRAMEWORK ON 29 MARCH 2018 THE IASB PUBLISHED ITS NEW CONCEPTUAL FRAMEWORK, NEARLY THREE YEARS AFTER THE 2015 EXPOSURE DRAFT. This text is accompanied by amendments

FINANCIAL CPA EXAM REVIEW V 3.1. For Exams Scheduled After December 31, 2017

For Exams Scheduled After December 31, 2017 CPA EXAM REVIEW FINANCIAL UPDATES AND ACADEMIC HELP Click on Customer and Academic Support under CPA Resources at http://www.becker.com/cpa-review.html CUSTOMER

For Exams Scheduled After December 31, 2017 CPA EXAM REVIEW FINANCIAL UPDATES AND ACADEMIC HELP Click on Customer and Academic Support under CPA Resources at http://www.becker.com/cpa-review.html CUSTOMER

ch01 Student: 1. The primary focus for financial accounting information is to provide information useful for:

ch01 Student: 1. The primary focus for financial accounting information is to provide information useful for: A. Option a B. Option b C. Option c D. Option d 2. What is the primary purpose of financial

ch01 Student: 1. The primary focus for financial accounting information is to provide information useful for: A. Option a B. Option b C. Option c D. Option d 2. What is the primary purpose of financial

IFRS News. Special Edition

Accounting News Discussion IFRS News Special Edition A revised Conceptual Framework for Financial Reporting June 2018 The IASB has published a revised version of the Conceptual Framework for Financial

Accounting News Discussion IFRS News Special Edition A revised Conceptual Framework for Financial Reporting June 2018 The IASB has published a revised version of the Conceptual Framework for Financial

Measurement Fundamentals BUS 210. Chapter 3

Measurement Fundamentals BUS 210 Chapter 3 What do you know? Financial Accounting Fundamentals Valuation Input Market (purchase)-original, replacement Output Market (sell)-present, fair market Financial

Measurement Fundamentals BUS 210 Chapter 3 What do you know? Financial Accounting Fundamentals Valuation Input Market (purchase)-original, replacement Output Market (sell)-present, fair market Financial

01 Introduction to Financial Statements Acctg 102

Introduction to Financial s Describe the financial reporting environment and explain the accounting assumptions, principles, and qualitative characteristics underlying financial statements. Describe the

Introduction to Financial s Describe the financial reporting environment and explain the accounting assumptions, principles, and qualitative characteristics underlying financial statements. Describe the

ACCT2542 Week 1 Notes

ACCT2542 Week 1 Notes Chapter 1: History, Current Regulatory Structures and Processes Australian Standard-Setting Arrangements: There are five main bodies which formulate and/or enforce accounting regulations

ACCT2542 Week 1 Notes Chapter 1: History, Current Regulatory Structures and Processes Australian Standard-Setting Arrangements: There are five main bodies which formulate and/or enforce accounting regulations

Module 5 Exhibits and Key Terms. Table of Contents. 1 Principles of Accounting Adjustments for Financial Reporting

Table of Contents Prerequisites... 2 Useful Links... 2 References... 2 Exhibit 27: The underlying assumptions or concepts... 3 Exhibit 28: Methods of accounting for long-term contracts... 4 Exhibit 29:

Table of Contents Prerequisites... 2 Useful Links... 2 References... 2 Exhibit 27: The underlying assumptions or concepts... 3 Exhibit 28: Methods of accounting for long-term contracts... 4 Exhibit 29:

" Annual report: the main method that management uses to report the results of the company s activities during the year.

Chapter 1 Overview of Corporate Financial Reporting What is Business? " Business plan to profit from selling a product or service. " Can be an individual or thousands of owners (investors). What is Accounting?

Chapter 1 Overview of Corporate Financial Reporting What is Business? " Business plan to profit from selling a product or service. " Can be an individual or thousands of owners (investors). What is Accounting?

Conceptual Framework Project Update

EFRAG TEG meeting 25-26 January 2017 Paper 07-01 EFRAG Secretariat: Rasmus Sommer This paper has been prepared by the EFRAG Secretariat for discussion at a public meeting of EFRAG TEG. The paper forms

EFRAG TEG meeting 25-26 January 2017 Paper 07-01 EFRAG Secretariat: Rasmus Sommer This paper has been prepared by the EFRAG Secretariat for discussion at a public meeting of EFRAG TEG. The paper forms

Concepts Statement 8 Conceptual Framework for Financial Reporting

Proposed Statement of Financial Accounting Concepts Issued: August 11, 2016 Comments Due: November 9, 2016 Concepts Statement 8 Conceptual Framework for Financial Reporting Chapter 7: Presentation The

Proposed Statement of Financial Accounting Concepts Issued: August 11, 2016 Comments Due: November 9, 2016 Concepts Statement 8 Conceptual Framework for Financial Reporting Chapter 7: Presentation The

Misunderstandings about the IASB s conceptual framework project

WSS Agenda ref 2 STAFF PAPER World Standard-setters Meeting Project Paper topic Friday 26 October 2012 Conceptual Framework s about the IASB s conceptual framework project CONTACT(S) Peter Clark pclark@ifrs.org

WSS Agenda ref 2 STAFF PAPER World Standard-setters Meeting Project Paper topic Friday 26 October 2012 Conceptual Framework s about the IASB s conceptual framework project CONTACT(S) Peter Clark pclark@ifrs.org

Guidance notes on International Financial Reporting Standards (IFRS) Institute of Chartered Accountants of Trinidad and Tobago

Institute of Chartered Accountants of Trinidad and Tobago") Improving the application of and compliance with International Financial Reporting and Auditing Standards in Trinidad and Tobago. ATN/MT 8114 TT Guidance notes on International Financial Reporting Standards

Improving the application of and compliance with International Financial Reporting and Auditing Standards in Trinidad and Tobago. ATN/MT 8114 TT Guidance notes on International Financial Reporting Standards

Clarifications to IFRS 15 Letter to the European Commission

Olivier Guersent Director General, Financial Stability, Financial Services and Capital Markets Union European Commission 1049 Brussels 6 July 2016 Dear Mr Guersent Adoption of Clarifications to IFRS 15

Olivier Guersent Director General, Financial Stability, Financial Services and Capital Markets Union European Commission 1049 Brussels 6 July 2016 Dear Mr Guersent Adoption of Clarifications to IFRS 15

Conceptual Framework for Financial Reporting

March 2018 IFRS Conceptual Framework Project Summary Conceptual Framework for Financial Reporting Conceptual Framework at a glance Introduction The International Accounting Standards Board (Board) issued

March 2018 IFRS Conceptual Framework Project Summary Conceptual Framework for Financial Reporting Conceptual Framework at a glance Introduction The International Accounting Standards Board (Board) issued

สมาคมผ สอบบ ญช ภาษ อากร

สมาคมผ สอบบ ญช ภาษ อากร เอกสารประกอบการบรรยาย หล กส ตร แม บทการบ ญช ส าหร บการจ ดท าและ การน าเสนองบการเง นของประเทศไทยและต างประเทศ ว ทยากร : ดร. ปกรณ เพ ญภาคก ล ว นท 20 ต ลาคม พ.ศ. 2556 ณ โรงแรมกานต

สมาคมผ สอบบ ญช ภาษ อากร เอกสารประกอบการบรรยาย หล กส ตร แม บทการบ ญช ส าหร บการจ ดท าและ การน าเสนองบการเง นของประเทศไทยและต างประเทศ ว ทยากร : ดร. ปกรณ เพ ญภาคก ล ว นท 20 ต ลาคม พ.ศ. 2556 ณ โรงแรมกานต

CURRENT DEVELOPMENTS ON THE IASB & IPSAS BOARD CONCEPTUAL FRAMEWORKS Presentation of financial statements IAS 1 & IPSAS1.

CURRENT DEVELOPMENTS ON THE IASB & IPSAS BOARD CONCEPTUAL FRAMEWORKS Presentation of financial statements IAS 1 & IPSAS1 Presentation by: CPA Donald Omengo Manager, Audit, KPMG Kenya Monday, 4 th September

CURRENT DEVELOPMENTS ON THE IASB & IPSAS BOARD CONCEPTUAL FRAMEWORKS Presentation of financial statements IAS 1 & IPSAS1 Presentation by: CPA Donald Omengo Manager, Audit, KPMG Kenya Monday, 4 th September

CHAPTER 2 CONCEPTUAL FRAMEWORK UNDERLYING FINANCIAL REPORTING. MULTIPLE CHOICE Conceptual. Test Bank Chapter 2

CHAPTER 2 CONCEPTUAL FRAMEWORK UNDERLYING FINANCIAL REPORTING MULTIPLE CHOICE Conceptual Answer No. Description c 1. GAAP defined. d 2. Purpose of conceptual framework. d 3. Objectives of financial reporting.

CHAPTER 2 CONCEPTUAL FRAMEWORK UNDERLYING FINANCIAL REPORTING MULTIPLE CHOICE Conceptual Answer No. Description c 1. GAAP defined. d 2. Purpose of conceptual framework. d 3. Objectives of financial reporting.

IFRS for SMEs. The Little GAAP we ve been waiting for?

IFRS for SMEs The Little GAAP we ve been waiting for? Getting Up On My Soapbox!! Opportunity for CPAs to take back their profession Regulatory overload has scared many from the profession, or at least

IFRS for SMEs The Little GAAP we ve been waiting for? Getting Up On My Soapbox!! Opportunity for CPAs to take back their profession Regulatory overload has scared many from the profession, or at least

Small and Medium-sized Entity Financial Reporting Framework and Financial Reporting Standard

SME-FRF & SME-FRS Issued August 2005 Effective for a Qualifying Entity s financial statements that cover a period beginning on or after 1 January 2005 Small and Medium-sized Entity Financial Reporting

SME-FRF & SME-FRS Issued August 2005 Effective for a Qualifying Entity s financial statements that cover a period beginning on or after 1 January 2005 Small and Medium-sized Entity Financial Reporting

IFRS Bridging Manual

CMA CANADA PROFESSIONAL PROGRAMS February 2011 IFRS Bridging Manual Used with permission of CMA Ontario. No part of this document may be reproduced in any form without the permission of the copyright holder.

CMA CANADA PROFESSIONAL PROGRAMS February 2011 IFRS Bridging Manual Used with permission of CMA Ontario. No part of this document may be reproduced in any form without the permission of the copyright holder.

Chapter 2: Financial Statements and the Annual Report

True / False 1. Financial statements are intended to tell the reader the value of a company. False LEARNING OBJECTIVES: FACC.PONO.13.02-01 - LO: 03-01 2. Accountants are the main reason financial statements

True / False 1. Financial statements are intended to tell the reader the value of a company. False LEARNING OBJECTIVES: FACC.PONO.13.02-01 - LO: 03-01 2. Accountants are the main reason financial statements

STANDING ADVISORY GROUP MEETING

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202)862-8430 www.pcaobus.org Review of Existing Standards Evaluating and Reporting on Fair Presentation in Conformity With

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202)862-8430 www.pcaobus.org Review of Existing Standards Evaluating and Reporting on Fair Presentation in Conformity With

CHAPTER 11. Financial Reporting Concepts ANSWERS TO QUESTIONS

CHAPTER 11 Financial Reporting Concepts ANSWERS TO QUESTIONS 2. (a) The main objective of financial reporting is to provide information that is useful for decision-making. More specifically, the conceptual

CHAPTER 11 Financial Reporting Concepts ANSWERS TO QUESTIONS 2. (a) The main objective of financial reporting is to provide information that is useful for decision-making. More specifically, the conceptual

1 Lecture. Course overview and introduction to financial statement analysis. Course name: International Accounting (Financial Statement Analysis-FSA)

") 1 Lecture Course overview and introduction to financial statement analysis Course name: International Accounting (Financial Statement Analysis-FSA) Credits: 5 Class Monday 09:30-12:30 Lecturer: Davide

1 Lecture Course overview and introduction to financial statement analysis Course name: International Accounting (Financial Statement Analysis-FSA) Credits: 5 Class Monday 09:30-12:30 Lecturer: Davide

Wichita State University Accounting & Auditing Conference

Wichita State University Accounting & Auditing Conference Accounting & Auditing Update May 2009 Agenda FASB Pronouncements FASB Projects EITF Consensuses for Exposure Key SEC Issues PCAOB Pronouncements

Wichita State University Accounting & Auditing Conference Accounting & Auditing Update May 2009 Agenda FASB Pronouncements FASB Projects EITF Consensuses for Exposure Key SEC Issues PCAOB Pronouncements

Accounting Policies, Changes in Accounting Estimates and Errors

International Accounting Standard 8 Accounting Policies, Changes in Accounting Estimates and Errors In April 2001 the International Accounting Standards Board (IASB) adopted IAS 8 Net Profit or Loss for

International Accounting Standard 8 Accounting Policies, Changes in Accounting Estimates and Errors In April 2001 the International Accounting Standards Board (IASB) adopted IAS 8 Net Profit or Loss for

Conceptual Framework for General Purpose Financial Reporting by Public Sector Entities - IPSAS. Vladimír Zelenka

Conceptual Framework for General Purpose Financial Reporting by Public Sector Entities - IPSAS Vladimír Zelenka From PSC Studies to Conceptual Framework Conceptual issues of Public Sector Committee and

Conceptual Framework for General Purpose Financial Reporting by Public Sector Entities - IPSAS Vladimír Zelenka From PSC Studies to Conceptual Framework Conceptual issues of Public Sector Committee and

CENTRAL GOVERNMENT ACCOUNTING STANDARDS

CENTRAL GOVERNMENT ACCOUNTING STANDARDS APRIL 2018 CONTENTS Updates 2 Introduction 6 Conceptual Framework for Central Government Accounting 7 Standard 1 Financial Statements 24 Standard 2 Expenses 39 Standard

CENTRAL GOVERNMENT ACCOUNTING STANDARDS APRIL 2018 CONTENTS Updates 2 Introduction 6 Conceptual Framework for Central Government Accounting 7 Standard 1 Financial Statements 24 Standard 2 Expenses 39 Standard

CENTRAL GOVERNMENT ACCOUNTING STANDARDS

CENTRAL GOVERNMENT ACCOUNTING STANDARDS March 2015 CENTRAL GOVERNMENT ACCOUNTING STANDARDS FRANCE Updates Public Sector Accounting Standards Council Date of Central Government Accounting Standards Opinion

CENTRAL GOVERNMENT ACCOUNTING STANDARDS March 2015 CENTRAL GOVERNMENT ACCOUNTING STANDARDS FRANCE Updates Public Sector Accounting Standards Council Date of Central Government Accounting Standards Opinion

IASB Staff Paper May 2014

IASB Staff Paper May 2014 Effect of Board redeliberations on DP A Review of the Conceptual Framework for Financial Reporting About this staff paper This staff paper updates the proposals in the Discussion

IASB Staff Paper May 2014 Effect of Board redeliberations on DP A Review of the Conceptual Framework for Financial Reporting About this staff paper This staff paper updates the proposals in the Discussion

6. Chapter 1 Question TF #6 A firm makes investments to obtain productive capacity to carry out its business activities.

1. Chapter 1 Question TF #1 The managers of a business prepare financial statements to present meaningful information about that business s activities to external users, *a. True b. False 2. Chapter 1

1. Chapter 1 Question TF #1 The managers of a business prepare financial statements to present meaningful information about that business s activities to external users, *a. True b. False 2. Chapter 1

Revenue From Contracts With Customers

September 2017 Revenue From Contracts With Customers Understanding and Implementing the New Rules An article by Scott Lehman, CPA, and Alex J. Wodka, CPA Audit / Tax / Advisory / Risk / Performance Smart

September 2017 Revenue From Contracts With Customers Understanding and Implementing the New Rules An article by Scott Lehman, CPA, and Alex J. Wodka, CPA Audit / Tax / Advisory / Risk / Performance Smart

ch Student:

ch01 Student: 1. The primary function of financial accounting is to provide relevant financial information to parties external to business enterprises. 2. 3. 4. 5. 6. 7. 8. 9. 10. 11. 12. 13. Accrual accounting

ch01 Student: 1. The primary function of financial accounting is to provide relevant financial information to parties external to business enterprises. 2. 3. 4. 5. 6. 7. 8. 9. 10. 11. 12. 13. Accrual accounting

The International Accounting Standards Board (IASB), by its side, is an independent, private-sector body that develops and approves International

, by its side, is an independent, private-sector body that develops and approves International") Key terms Concepts and conventions, money measurement, business entity, going concern, historic cost, dual aspect, prudence, accounting period, objectivity, stable monetary unit, conservatism, realization,

Key terms Concepts and conventions, money measurement, business entity, going concern, historic cost, dual aspect, prudence, accounting period, objectivity, stable monetary unit, conservatism, realization,

15. Information is neutral when it is free from bias that would lead users towards making decisions that are influenced by the way the information is

02 Student: 1. Recognition requires the measurement of an item for inclusion in the financial statements. 2. The use of historical cost, rather than liquidation value, is supported by the continuity assumption.

02 Student: 1. Recognition requires the measurement of an item for inclusion in the financial statements. 2. The use of historical cost, rather than liquidation value, is supported by the continuity assumption.

CONTACT(S) Jelena Voilo

Jelena Voilo") IASB Agenda ref 10A STAFF PAPER REG IASB Meeting Project Paper topic Conceptual Framework Summary of tentative decisions CONTACT(S) Jelena Voilo jvoilo@ifrs.org +44 207 246 6914 November 2014 This paper

IASB Agenda ref 10A STAFF PAPER REG IASB Meeting Project Paper topic Conceptual Framework Summary of tentative decisions CONTACT(S) Jelena Voilo jvoilo@ifrs.org +44 207 246 6914 November 2014 This paper

BE Accounting Theory

KANDIDAT 9530 PRØVE BE-313 1 Accounting Theory Emnekode BE-313 Vurderingsform Multiple choice Starttid 19.12.2016 09:00 Sluttid 19.12.2016 12:00 Sensurfrist 12.01.2017 01:00 PDF opprettet 05.09.2018 12:32

KANDIDAT 9530 PRØVE BE-313 1 Accounting Theory Emnekode BE-313 Vurderingsform Multiple choice Starttid 19.12.2016 09:00 Sluttid 19.12.2016 12:00 Sensurfrist 12.01.2017 01:00 PDF opprettet 05.09.2018 12:32

Exposure Draft ED/2015/3 Conceptual Framework for Financial Reporting

IFRS Foundation Publications Department 30 Cannon Street London, EC4M 6XH United Kingdom Exposure Draft ED/2015/3 Conceptual Framework for Financial Reporting The Edison Electric Institute (EEI), American

IFRS Foundation Publications Department 30 Cannon Street London, EC4M 6XH United Kingdom Exposure Draft ED/2015/3 Conceptual Framework for Financial Reporting The Edison Electric Institute (EEI), American

OSLO 16 SEPTEMBER 2015 JOINT OUTREACH EVENT IASB EXPOSURE DRAFT ED/2015/3 CONCEPTUAL FRAMEWORK FOR FINANCIAL REPORTING

JOINT OUTREACH EVENT IASB EXPOSURE DRAFT ED/2015/3 CONCEPTUAL FRAMEWORK FOR FINANCIAL REPORTING OSLO 16 SEPTEMBER 2015 This feedback statement has been prepared for the convenience of European constituents

JOINT OUTREACH EVENT IASB EXPOSURE DRAFT ED/2015/3 CONCEPTUAL FRAMEWORK FOR FINANCIAL REPORTING OSLO 16 SEPTEMBER 2015 This feedback statement has been prepared for the convenience of European constituents

IMPLEMENTATION PROBLEMS

1 RESEARCHING IFRS IMPLEMENTATION PROBLEMS Overview 1 The IFRS Hierarchy 1 Researching IFRS 4 Researching Accounting Controls 5 Researching Accounting Forms and Reports 6 Researching Accounting Footnotes

1 RESEARCHING IFRS IMPLEMENTATION PROBLEMS Overview 1 The IFRS Hierarchy 1 Researching IFRS 4 Researching Accounting Controls 5 Researching Accounting Forms and Reports 6 Researching Accounting Footnotes