CURRENT DEVELOPMENTS ON THE IASB & IPSAS BOARD CONCEPTUAL FRAMEWORKS Presentation of financial statements IAS 1 & IPSAS1.

|

|

|

- Leon Wilcox

- 6 years ago

- Views:

Transcription

1 CURRENT DEVELOPMENTS ON THE IASB & IPSAS BOARD CONCEPTUAL FRAMEWORKS Presentation of financial statements IAS 1 & IPSAS1 Presentation by: CPA Donald Omengo Manager, Audit, KPMG Kenya Monday, 4 th September 2017 Uphold public interest

2 Presentation agenda IPSAS 1 IAS 1 Current developments on the conceptual frameworks

3 Scope and objectives IPSAS 1 Effective date Annual periods beginning on or after 1 January Scope All financial statements (FS) prepared in accordance with IPSAS Objective To set out the manner in which GPFS shall be prepared under the accrual basis of accounting, including guidance for their structure and the minimum requirements for content.

4 Components of financial statements A complete set of financial statements comprises: Statement of financial position Statement of financial performance Statement of changes in net assets/equity Cash flow statement When the entity makes it approved budget publicly available, a comparison of budget and accrual amounts Notes, comprising a summary of significant accounting policies and other explanatory notes

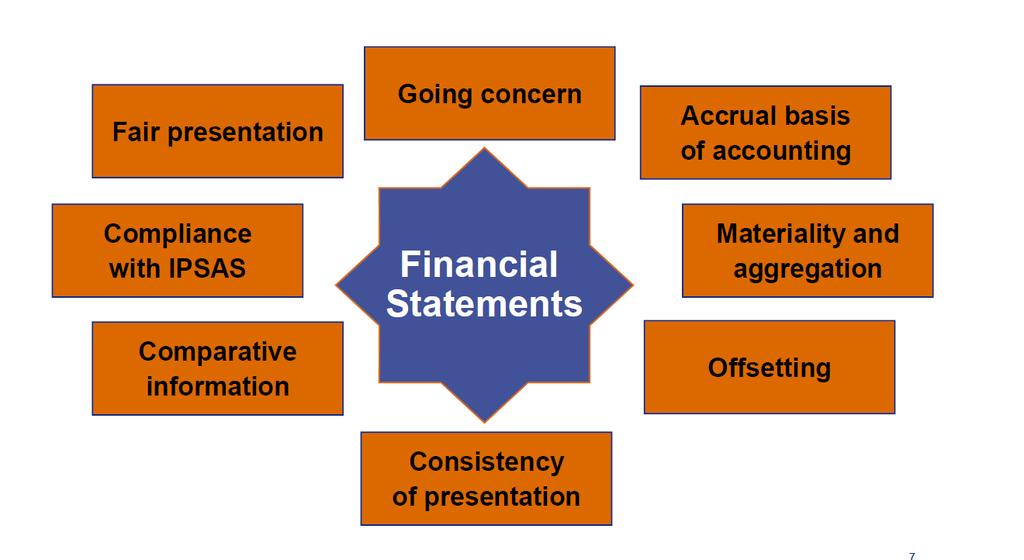

5 Compliance with IPSAS An entity whose financial statements comply with IPSAS shall make an explicit and unreserved statement of such compliance in the notes. Financial statements shall not be described as complying with IPSAS unless they comply with all the requirements of IPSAS.

6 Overall considerations

7 Going concern Management should make an assessment of the entity s ability to continue as a going concern. Management takes into account all available information about the future, which is at least, but is not limited to, twelve months from the reporting date. Management may need to consider a wide range of factors relating to current and expected profitability, debt repayment schedules and potential sources of replacement financing.

8 Going concern (cont.) Disclose that fact if financial statements not prepare on a going concern basis, the basis on which prepared the financial statements and the reason why the entity is not regarded as a going concern.

9 Consistency & frequency of presentation Retain the same presentation and classification of items unless: Change will result in more appropriate presentation as required by IPSAS 3 Change required by an IPSAS Present a complete set of financial statements (including comparative information) at least annually. If FS are presented for a period longer or shorter than one year, disclose: that fact and the reason for using a longer or shorter period. the fact that comparative amounts presented in the financial statements (and notes) are not entirely comparable.

10 Comparative Information Enhancing the inter-period comparability of information allowing the assessment of trends in financial information for predictive purposes. Details of a legal dispute whose outcome was uncertain at the end of the immediately preceding reporting period Comparative narrative and descriptive information relevant to financial reporting

11 Comparative Information(cont.) Accounting policy applied retrospectively or retrospective restatement of items or reclassifies items then present statements of financial position as at: the end of the current period, the end of the previous period the beginning of the earliest comparative period

12 Materiality and aggregation Separate presentation of material items of dissimilar nature or function Materiality depends on the size and nature of the omission or misstatement judged in the surrounding circumstances. Immaterial items need not be presented separately Aggregate with amounts of similar nature or function If sufficiently material after aggregation, separate presentation in notes required

13 Offsetting Assets and liabilities should not be offset unless Required or permitted by an IPSAS Offset if it reflects the substance of the transaction or other event, Items of income and expense should not be offset unless Required or permitted by an IPSAS Gains, losses and related expenses arising from the same or similar items are not material Measuring assets net of valuation allowances for example, obsolescence allowances on inventories and doubtful debts allowances on receivables is not

14 Fair presentation Achieved by appropriate application of IPSAS Requires faithful representation of effects of transactions, events and conditions in accordance with recognition criteria set out in the Framework

15 Accrual basis of accounting Prepare its financial statements, except for cash flow information, using the accrual basis of accounting. Recognises items as assets, liabilities, equity, income and expenses when they satisfy the definitions and recognition criteria

16 Minimum disclosure requirements Accounting policies followed The judgments that management has made in the process of applying the entity s accounting policies The key assumptions concerning the future, and other key sources of estimation uncertainty, The domicile and legal form of the entity Nature of the entity s operations Reference to the relevant legislation The name of the controlling entity and ultimate controlling entity

17 Scope and objectives IAS 1 Effective date Reissued in 2007 and effective for Annual periods beginning on or after 1 January Scope All general purpose financial statements that are prepared and presented in accordance with (IFRSs). Objective To set out the manner in which GPFS shall be prepared under the accrual basis of accounting, including guidance for their structure and the minimum requirements for content.

18 Related interpretations Related Interpretations IAS 1 (2003) superseded SIC-18 Consistency - Alternative Methods IFRIC 17 Distributions of Non-cash Assets to Owners SIC-27 Evaluating the Substance of Transactions in the Legal Form of a Lease SIC-29 Disclosure -Service Concession Arrangements

19 Amendments under consideration Amendments under consideration Disclosures about going concern Classification of liabilities Disclosure initiative Principles of disclosure (research project) Disclosure initiative Materiality (research project) - exposure draft of proposed amendments are expected in September 2017.

20 IPSAS 1 vs IAS 1 Different terminology Statement of financial performance vs Statement of profit or loss and comprehensive income Net assets or equity while IAS 1 uses only equity IAS 1 defines IFRS to include IFRSs, ISAs and SIC/IFRC interpretations but IPSAS 1 does not define IPSAS. IAS 1 prohibits items of income and expenses being presented as extraordinary item IPSAS 1 contains transitional provisions Economic entity vs Group of entities

21 Conceptual Framework Definition A conceptual framework is a theory of accounting prepared by a standard-setting body against which practical problems can be tested objectively A conceptual framework deals with: objectives and users of financial statements, the characteristics that make accounting information useful, the basic elements of financial statements The concepts for recognising and measuring these elements in the financial statements.

22 Benefits of A Conceptual Framework Benefits of a conceptual framework for financial reporting include: establishing precise definitions that facilitate discussion of accounting issues; providing guidance to accounting standard setters when developing and reviewing financial reporting rules; helping to ensure that accounting standards are internally consistent;

23 Benefits of A Conceptual Framework (Cont..) helping preparers and auditors to resolve financial reporting problems in the absence of an accounting standard; helping to limit the volume of accounting standards by providing an overarching theory of accounting that can be applied to specific reporting problems.

24 Applicable framework IFRS The Conceptual Framework for Financial Reporting 2010) issued by IASB: Which defines the primary objective of financial statements prepared under IFRS as: are economic decision-making; and stewardship. Main users of financial statements are considered to be equity investors, lenders and other creditors, while the primary characteristics that make financial reporting information useful to these groups are relevance and faithful representation

25 Current status IFRS Framework The IASB is currently updating its Framework in a joint project with the Financial Accounting Standards Board of the USA (FASB).

26 Applicable framework IPSAS The Conceptual Framework for General Purpose Financial Reporting by Public Sector Entities issued by IAPSAB establishes the concepts that are to be applied in developing International Public Sector Accounting Standards (IPSASs) and Recommended Practice Guidelines (RPGs) applicable to the preparation and presentation of general purpose financial reports (GPFRs) of public sector entities

27 Current status IPSAS Framework Final Chapters of Phase 1 published on January 11, 2013: Chapter 1: Role and Authority of the Conceptual Framework Chapter 2: Objectives and Users of General Purpose Financial Reporting Chapter 3: Qualitative Characteristics Chapter 4: Reporting Entity

28 Current status IPSAS Framework Final Chapters of Phase 1 published on January 11, 2013: Chapter 1: Role and Authority of the Conceptual Framework Chapter 2: Objectives and Users of General Purpose Financial Reporting Chapter 3: Qualitative Characteristics Chapter 4: Reporting Entity

29 Current status IPSAS Framework (Cont..) Remaining phases Phase 2: The definition and recognition of the elements of financial statements Phase 3: The measurement of the elements that are recognized in the financial statements Phase 4: The presentation of information in general purpose financial reports

30 Limitations of financial These include: statements dependence on historical costs Inflationary effects. Intangible assets not recorded Based on specific time period Subject to fraud No discussion of non-financial issues.

31 Questions?

32 Thank you Donald Omengo Manager, KPMG Kenya

Presentation of Financial Statements

International Accounting Standard 1 Presentation of Financial Statements In April 2001 the International Accounting Standards Board (IASB) adopted Presentation of Financial Statements, which had originally

International Accounting Standard 1 Presentation of Financial Statements In April 2001 the International Accounting Standards Board (IASB) adopted Presentation of Financial Statements, which had originally

Presentation of Financial Statements

IAS Standard 1 Presentation of Financial Statements In April 2001 the International Accounting Standards Board (the Board) adopted IAS 1 Presentation of Financial Statements, which had originally been

IAS Standard 1 Presentation of Financial Statements In April 2001 the International Accounting Standards Board (the Board) adopted IAS 1 Presentation of Financial Statements, which had originally been

Presentation of Financial Statements

International Accounting Standard 1 Presentation of Financial Statements This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 1 Presentation of Financial Statements

International Accounting Standard 1 Presentation of Financial Statements This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 1 Presentation of Financial Statements

Presentation of Financial Statements

IAS 1 Presentation of Financial Statements In April 2001 the International Accounting Standards Board (Board) adopted IAS 1 Presentation of Financial Statements, which had originally been issued by the

IAS 1 Presentation of Financial Statements In April 2001 the International Accounting Standards Board (Board) adopted IAS 1 Presentation of Financial Statements, which had originally been issued by the

NZ International Accounting Standard 1 (PBE) Presentation of Financial Statements (NZ IAS 1 (PBE))

Presentation of Financial Statements (NZ IAS 1 (PBE))") NZ International Accounting Standard 1 (PBE) Presentation of Financial Statements () Issued November 2012 excluding consequential amendments resulting from early adoption of NZ IFRS 9 (2009) (PBE) Financial

NZ International Accounting Standard 1 (PBE) Presentation of Financial Statements () Issued November 2012 excluding consequential amendments resulting from early adoption of NZ IFRS 9 (2009) (PBE) Financial

Presentation of Financial Statements

HKAS 1 (Revised) Revised JanuaryAugust 2017 Effective for annual periods beginning on or after 1 January 2009 Hong Kong Accounting Standard 1 (Revised) Presentation of Financial Statements COPYRIGHT Copyright

HKAS 1 (Revised) Revised JanuaryAugust 2017 Effective for annual periods beginning on or after 1 January 2009 Hong Kong Accounting Standard 1 (Revised) Presentation of Financial Statements COPYRIGHT Copyright

Introduction to International Financial Reporting Standards

Introduction to International Financial Reporting Standards Structure of IASCF International Accounting Standards Committee Foundation (22 Trustees) InternationalAccounting Standards Board (15 members)

Introduction to International Financial Reporting Standards Structure of IASCF International Accounting Standards Committee Foundation (22 Trustees) InternationalAccounting Standards Board (15 members)

New Zealand Equivalent to International Accounting Standard 1 Presentation of Financial Statements (NZ IAS 1)

") New Zealand Equivalent to International Accounting Standard 1 Presentation of Financial Statements (NZ IAS 1) Issued November 2007 and incorporates amendments to 31 December 2016 other than consequential

New Zealand Equivalent to International Accounting Standard 1 Presentation of Financial Statements (NZ IAS 1) Issued November 2007 and incorporates amendments to 31 December 2016 other than consequential

Overview of Accounting Standards; IASs/IFRS and IPSAS Presentation by: CPA Daniel Kahi Monday, 10 September 2018

Overview of Accounting Standards; IASs/IFRS and IPSAS Presentation by: CPA Daniel Kahi Monday, 10 September 2018 Uphold public interest Presentation agenda Introduction ISAs / IFRSs IPSAS Concluding Remarks

Overview of Accounting Standards; IASs/IFRS and IPSAS Presentation by: CPA Daniel Kahi Monday, 10 September 2018 Uphold public interest Presentation agenda Introduction ISAs / IFRSs IPSAS Concluding Remarks

EUROPEAN UNION ACCOUNTING RULE 14 ACCOUNTING POLICIES, CHANGES IN ACCOUNTING ESTIMATES AND ERRORS

execution EUROPEAN UNION ACCOUNTING RULE 14 ACCOUNTING POLICIES, CHANGES IN execution Page 2 of 10 I N D E X 1. Objective... 3 2. Scope... 3 3. Definitions... 3 4. Policies... 5 4.1 Selection and Application

execution EUROPEAN UNION ACCOUNTING RULE 14 ACCOUNTING POLICIES, CHANGES IN execution Page 2 of 10 I N D E X 1. Objective... 3 2. Scope... 3 3. Definitions... 3 4. Policies... 5 4.1 Selection and Application

COMPARISON OF GRAP 1 WITH IAS 1 GRAP 1 IAS 1 DIFFERENCES

COMPARISON OF GRAP 1 WITH IAS 1 GRAP 1 IAS 1 DIFFERENCES Objective Objective.01 The objective of this Standard is to prescribe the basis for presentation of general purpose financial statements, to ensure

COMPARISON OF GRAP 1 WITH IAS 1 GRAP 1 IAS 1 DIFFERENCES Objective Objective.01 The objective of this Standard is to prescribe the basis for presentation of general purpose financial statements, to ensure

Accounting Policies, Changes in Accounting Estimates and Errors

International Accounting Standard 8 Accounting Policies, Changes in Accounting Estimates and Errors In April 2001 the International Accounting Standards Board (IASB) adopted IAS 8 Net Profit or Loss for

International Accounting Standard 8 Accounting Policies, Changes in Accounting Estimates and Errors In April 2001 the International Accounting Standards Board (IASB) adopted IAS 8 Net Profit or Loss for

Click to edit Master title style. Presentation of Financial Statements ( LKAS 1)

") 1 Click to edit Master title style Presentation of Financial Statements ( LKAS 1) 2 1 LKAS 1 Presentation of Financial Statements 3 LKAS 1: Overview Objective Scope Components of financial statements Overall

1 Click to edit Master title style Presentation of Financial Statements ( LKAS 1) 2 1 LKAS 1 Presentation of Financial Statements 3 LKAS 1: Overview Objective Scope Components of financial statements Overall

IAS 1 Presentation of Financial Statements - A Closer Look

MPRA Munich Personal RePEc Archive IAS 1 Presentation of Financial Statements - A Closer Look K S Muthupandian The Institute of Cost and Works Accountants of India 19 May 2008 Online at https://mpra.ub.uni-muenchen.de/41617/

MPRA Munich Personal RePEc Archive IAS 1 Presentation of Financial Statements - A Closer Look K S Muthupandian The Institute of Cost and Works Accountants of India 19 May 2008 Online at https://mpra.ub.uni-muenchen.de/41617/

IPSAS 1- Financial Statements Presentation. -Mandatory and Non- Mandatory disclosures

IPSAS 1- Financial Statements Presentation. -Mandatory and Non- Mandatory disclosures Presentation by: By Mr. Abdullatif Essajee Wednesday, 18 th October 2017 Uphold public interest IPSAS 1: Presentation

IPSAS 1- Financial Statements Presentation. -Mandatory and Non- Mandatory disclosures Presentation by: By Mr. Abdullatif Essajee Wednesday, 18 th October 2017 Uphold public interest IPSAS 1: Presentation

Annual Improvements Cycle

Annual Improvements 2009 2011 Cycle 1 Copyright ANNUAL IMPROVEMENTS 2009 2011 CYCLE INTRODUCTION NZ IFRS 1 NZ IAS 1 NZ IAS 16 NZ IAS 32 NZ IAS 34 First-time Adoption of New Zealand Equivalents to International

Annual Improvements 2009 2011 Cycle 1 Copyright ANNUAL IMPROVEMENTS 2009 2011 CYCLE INTRODUCTION NZ IFRS 1 NZ IAS 1 NZ IAS 16 NZ IAS 32 NZ IAS 34 First-time Adoption of New Zealand Equivalents to International

Presentation of Financial Statements

Indian Accounting Standard (Ind AS) 1 Presentation of Financial Statements (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority. Paragraphs in

Indian Accounting Standard (Ind AS) 1 Presentation of Financial Statements (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority. Paragraphs in

PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 1 PRESENTATION OF FINANCIAL STATEMENTS (PBE IPSAS 1)

") PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 1 PRESENTATION OF FINANCIAL STATEMENTS (PBE IPSAS 1) Issued September 2014 and incorporates amendments to 31 May 2017 other than consequential

PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 1 PRESENTATION OF FINANCIAL STATEMENTS (PBE IPSAS 1) Issued September 2014 and incorporates amendments to 31 May 2017 other than consequential

ACCOUNTING STANDARDS BOARD STANDARD OF GENERALLY RECOGNISED ACCOUNTING PRACTICE

ACCOUNTING STANDARDS BOARD STANDARD OF GENERALLY RECOGNISED ACCOUNTING PRACTICE PRESENTATION OF FINANCIAL STATEMENTS (GRAP 1) Issued by the Accounting Standards Board February 2010 Acknowledgement The

ACCOUNTING STANDARDS BOARD STANDARD OF GENERALLY RECOGNISED ACCOUNTING PRACTICE PRESENTATION OF FINANCIAL STATEMENTS (GRAP 1) Issued by the Accounting Standards Board February 2010 Acknowledgement The

Presentation of Financial Statements

Presentation of Financial Statements 2016 Deloitte & Touche 1 2015 Deloitte Touche Limited Index 1. Objective 2. Scope 3. Objective of Financial Statements 4. Components of Financial Statements 5. Fair

Presentation of Financial Statements 2016 Deloitte & Touche 1 2015 Deloitte Touche Limited Index 1. Objective 2. Scope 3. Objective of Financial Statements 4. Components of Financial Statements 5. Fair

Table 1 IPSAS and Equivalent IFRS Summary 1

Agenda Item 1.6 IPSAS IFRS Alignment Dashboard Table 1 IPSAS and Equivalent IFRS Summary 1 IPSAS IFRS Status IPSAS IFRS Status IPSAS IFRS Status 1, Presentation of Financial Statements IAS 1 17, Property,

Agenda Item 1.6 IPSAS IFRS Alignment Dashboard Table 1 IPSAS and Equivalent IFRS Summary 1 IPSAS IFRS Status IPSAS IFRS Status IPSAS IFRS Status 1, Presentation of Financial Statements IAS 1 17, Property,

International Accounting Standard 8 Accounting Policies, Changes in Accounting Estimates and Errors

International Accounting Standard 8 Accounting Policies, Changes in Accounting Estimates and Errors Objective 1 The objective of this Standard is to prescribe the criteria for selecting and changing accounting

International Accounting Standard 8 Accounting Policies, Changes in Accounting Estimates and Errors Objective 1 The objective of this Standard is to prescribe the criteria for selecting and changing accounting

Table 1 IPSAS and Equivalent IFRS Summary 2

IPSASB Meeting ( 2018) Agenda Item 1.6 IPSAS IFRS Alignment 1 Dashboard Table 1 IPSAS and Equivalent IFRS Summary 2 IPSAS IFRS Status IPSAS IFRS Status IPSAS IFRS Status 1, Presentation of Financial Statements

IPSASB Meeting ( 2018) Agenda Item 1.6 IPSAS IFRS Alignment 1 Dashboard Table 1 IPSAS and Equivalent IFRS Summary 2 IPSAS IFRS Status IPSAS IFRS Status IPSAS IFRS Status 1, Presentation of Financial Statements

IAS 1 Presentation of Financial Statement

IAS 1 Presentation of Financial Statement 1 By : Mehul Shah mehul@raseshca.comcom 9723459572 IASB Structure 2 IASC Foundation appoints oversees funds reports SAC advises IASB interprets IFRIC creates IFRS

IAS 1 Presentation of Financial Statement 1 By : Mehul Shah mehul@raseshca.comcom 9723459572 IASB Structure 2 IASC Foundation appoints oversees funds reports SAC advises IASB interprets IFRIC creates IFRS

IAS 8, Accounting Policies, Changes in Accounting Estimates and Errors A Closer Look

MPRA Munich Personal RePEc Archive IAS 8, Accounting Policies, Changes in Accounting Estimates and Errors A Closer Look K S Muthupandian The Institute of Cost and Works Accountants of India 20. September

MPRA Munich Personal RePEc Archive IAS 8, Accounting Policies, Changes in Accounting Estimates and Errors A Closer Look K S Muthupandian The Institute of Cost and Works Accountants of India 20. September

Table 1 IPSAS and Equivalent IFRS Summary*

Agenda Item 13.3.2 IPSAS IFRS Alignment Dashboard Table 1 IPSAS and Equivalent IFRS Summary* IPSAS IFRS Status IPSAS IFRS Status IPSAS IFRS Status 1, Presentation of Financial Statements IAS 1 17, Property,

Agenda Item 13.3.2 IPSAS IFRS Alignment Dashboard Table 1 IPSAS and Equivalent IFRS Summary* IPSAS IFRS Status IPSAS IFRS Status IPSAS IFRS Status 1, Presentation of Financial Statements IAS 1 17, Property,

LKAS 01 PRESENTATION OF FINANCIAL STATEMENTS

CA BUSINESS SCHOOL POSTGRADUATE DIPLOMA IN BUSINESS AND FINANCE SEMESTER 2: Financial Statements Analysis LKAS 01 PRESENTATION OF FINANCIAL STATEMENTS M B G Wimalarathna (FCA, ACMA, ACIM, SAT, ACPM)(MBA

CA BUSINESS SCHOOL POSTGRADUATE DIPLOMA IN BUSINESS AND FINANCE SEMESTER 2: Financial Statements Analysis LKAS 01 PRESENTATION OF FINANCIAL STATEMENTS M B G Wimalarathna (FCA, ACMA, ACIM, SAT, ACPM)(MBA

PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 1 PRESENTATION OF FINANCIAL STATEMENTS (PBE IPSAS 1)

") PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 1 PRESENTATION OF FINANCIAL STATEMENTS (PBE IPSAS 1) This Standard was issued on 11 September 2014 by the New Zealand Accounting Standards

PUBLIC BENEFIT ENTITY INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARD 1 PRESENTATION OF FINANCIAL STATEMENTS (PBE IPSAS 1) This Standard was issued on 11 September 2014 by the New Zealand Accounting Standards

SRI LANKA ACCOUNTING STANDARD

(REVISED 2005) SRI LANKA ACCOUNTING STANDARD PRESENTATION OF FINANCIAL STATEMENTS THE INSTITUTE OF CHARTERED ACCOUNTANTS OF SRI LANKA (REVISED 2005) SRI LANKA ACCOUNTING STANDARD PRESENTATION OF FINANCIAL

(REVISED 2005) SRI LANKA ACCOUNTING STANDARD PRESENTATION OF FINANCIAL STATEMENTS THE INSTITUTE OF CHARTERED ACCOUNTANTS OF SRI LANKA (REVISED 2005) SRI LANKA ACCOUNTING STANDARD PRESENTATION OF FINANCIAL

Interim Financial Reporting

International Accounting Standard 34 Interim Financial Reporting This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 34 Interim Financial Reporting was issued by the

International Accounting Standard 34 Interim Financial Reporting This version includes amendments resulting from IFRSs issued up to 31 December 2009. IAS 34 Interim Financial Reporting was issued by the

International Accounting Standard 34 Interim Financial Reporting. Objective. Scope. Definitions. Content of an interim financial report IAS 34

International Accounting Standard 34 Interim Financial Reporting Objective The objective of this Standard is to prescribe the minimum content of an interim financial report and to prescribe the principles

International Accounting Standard 34 Interim Financial Reporting Objective The objective of this Standard is to prescribe the minimum content of an interim financial report and to prescribe the principles

Interim Financial Reporting

IAS Standard 34 Interim Financial Reporting In April 2001 the International Accounting Standards Board adopted IAS 34 Interim Financial Reporting, which had originally been issued by the International

IAS Standard 34 Interim Financial Reporting In April 2001 the International Accounting Standards Board adopted IAS 34 Interim Financial Reporting, which had originally been issued by the International

Framework and IAS 1 March 2007

Framework and IAS 1 March 2007 Nelson Lam 林智遠 MBA MSc BBA ACA CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) 2005-07 Nelson 1 Today s Agenda Introduction Framework Simple but Comprehensive Contentious and

Framework and IAS 1 March 2007 Nelson Lam 林智遠 MBA MSc BBA ACA CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) 2005-07 Nelson 1 Today s Agenda Introduction Framework Simple but Comprehensive Contentious and

International GAAP Disclosure Checklist

IFRS Core Tools International GAAP Disclosure Checklist Based on International Financial Reporting Standards in issue at 28 February 2017 Effective for entities with a year-end of 30 June 2017 and any

IFRS Core Tools International GAAP Disclosure Checklist Based on International Financial Reporting Standards in issue at 28 February 2017 Effective for entities with a year-end of 30 June 2017 and any

IMPORTANT TAKEAWAYS ON IFRS

IMPORTANT TAKEAWAYS ON IFRS 1. Four Major Pillars of IFRS : 1. Historical cost is not relevant : It is no more relevant for measurement of Assets and Liabilities. 2. Time Value of Money : Cash Flows to

IMPORTANT TAKEAWAYS ON IFRS 1. Four Major Pillars of IFRS : 1. Historical cost is not relevant : It is no more relevant for measurement of Assets and Liabilities. 2. Time Value of Money : Cash Flows to

Table 1 IPSAS and Equivalent IFRS Summary 2

Agenda Item 1.7 IPSAS IFRS Alignment 1 Dashboard Table 1 IPSAS and Equivalent IFRS Summary 2 IPSAS IFRS Status IPSAS IFRS Status IPSAS IFRS Status 1, Presentation of Financial Statements IAS 1 18, Segment

Agenda Item 1.7 IPSAS IFRS Alignment 1 Dashboard Table 1 IPSAS and Equivalent IFRS Summary 2 IPSAS IFRS Status IPSAS IFRS Status IPSAS IFRS Status 1, Presentation of Financial Statements IAS 1 18, Segment

IFRS Training. IAS 1 Presentation of Financial Statements. Professional Training Services

IFRS Training IAS 1 Presentation of Financial Statements Table of Contents Section 1 Overview 2 Objectives 3 Scope 4 Purpose of Financial Statements 5 Frequency of Reporting and Period Covered 6 Components

IFRS Training IAS 1 Presentation of Financial Statements Table of Contents Section 1 Overview 2 Objectives 3 Scope 4 Purpose of Financial Statements 5 Frequency of Reporting and Period Covered 6 Components

Agenda Item 13.2: IPSAS IFRS Alignment Dashboard

Agenda Item 13.2: IPSAS IFRS Alignment Dashboard João Fonseca, Principal IPSASB Meeting Toronto, Canada June 19 22, 2018 Page 1 Proprietary and Copyrighted Information Agenda Item 13.2 IPSAS IFRS Alignment

Agenda Item 13.2: IPSAS IFRS Alignment Dashboard João Fonseca, Principal IPSASB Meeting Toronto, Canada June 19 22, 2018 Page 1 Proprietary and Copyrighted Information Agenda Item 13.2 IPSAS IFRS Alignment

Agenda Item 1.7: IPSAS-IFRS Alignment Dashboard

Agenda Item 1.7: IPSAS-IFRS Alignment Dashboard João Fonseca, Principal IPSASB Meeting Washington D.C., USA March 12 15, 2019 Page 1 Proprietary and Copyrighted Information Agenda Item 1.7 Outline Change

Agenda Item 1.7: IPSAS-IFRS Alignment Dashboard João Fonseca, Principal IPSASB Meeting Washington D.C., USA March 12 15, 2019 Page 1 Proprietary and Copyrighted Information Agenda Item 1.7 Outline Change

THE ANNUAL FINANCIAL REPORTING WEEK Theme : Reliance on Enhanced Financial Reporting for Economic Growth and Development

THE ANNUAL FINANCIAL REPORTING WEEK Theme : Reliance on Enhanced Financial Reporting for Economic Growth and Development FCPA Erastus Kwaka Omolo Crowe Erastus & Co. Date : 13 th September, 2018 Venue

THE ANNUAL FINANCIAL REPORTING WEEK Theme : Reliance on Enhanced Financial Reporting for Economic Growth and Development FCPA Erastus Kwaka Omolo Crowe Erastus & Co. Date : 13 th September, 2018 Venue

A New Era of Financial Reporting

A New Era of Financial Reporting The Agra Branch of CIRC of ICAI 30 th April 2016 FCA Aditya Singhal M.Com, DISA(ICAI), DipIFRS (ACCA) +91 8800334745 adityaagra@gmail.com Current Global Reporting Requirements

A New Era of Financial Reporting The Agra Branch of CIRC of ICAI 30 th April 2016 FCA Aditya Singhal M.Com, DISA(ICAI), DipIFRS (ACCA) +91 8800334745 adityaagra@gmail.com Current Global Reporting Requirements

IAS 1R- Presentation of Financial Statements. Introduction to IFRS / Ind AS

IAS 1R- Presentation of Financial Statements Introduction to IFRS / Ind AS IAS 1R- Presentation of financial statements Objective The objective of this Standard is to prescribe the basis for presentation

IAS 1R- Presentation of Financial Statements Introduction to IFRS / Ind AS IAS 1R- Presentation of financial statements Objective The objective of this Standard is to prescribe the basis for presentation

International GAAP Disclosure Checklist

Ernst & Young IFRS Core Tools International GAAP Disclosure Checklist Based on International Financial Reporting Standards in issue at 28 February 2013 Effective for entities with a year-end of 30 June

Ernst & Young IFRS Core Tools International GAAP Disclosure Checklist Based on International Financial Reporting Standards in issue at 28 February 2013 Effective for entities with a year-end of 30 June

International GAAP Disclosure Checklist

EY IFRS Core Tools International GAAP Disclosure Checklist Based on International Financial Reporting Standards in issue at 28 February 2015 Effective for entities with a year-end of 30 June 2015 or thereafter

EY IFRS Core Tools International GAAP Disclosure Checklist Based on International Financial Reporting Standards in issue at 28 February 2015 Effective for entities with a year-end of 30 June 2015 or thereafter

FIRST TIME ADOPTION OF ACCRUAL BASIS IPSASS

Meeting Meeting Location: International Public Sector Accounting Standards Board Toronto, Canada Meeting Date: June 17 20, 2013 Agenda Item 6 For: Approval Discussion Information FIRST TIME ADOPTION OF

Meeting Meeting Location: International Public Sector Accounting Standards Board Toronto, Canada Meeting Date: June 17 20, 2013 Agenda Item 6 For: Approval Discussion Information FIRST TIME ADOPTION OF

Global Professional Opportunities in IFRS

1811 Global Professional Opportunities in IFRS Spreading its jurisdiction across 130 countries in the world, the International Financial Reporting Standards (IFRS) a uniform set of Global Accounting Standards,

1811 Global Professional Opportunities in IFRS Spreading its jurisdiction across 130 countries in the world, the International Financial Reporting Standards (IFRS) a uniform set of Global Accounting Standards,

IFRS vs Prudential Guidelines. Interest revenue recognition on non-performing loans in IFRS financial statements

IFRS vs Prudential Guidelines Interest revenue recognition on non-performing loans in IFRS financial statements Preamble There is currently a divergence between IFRS requirements and the Prudential Guidelines

IFRS vs Prudential Guidelines Interest revenue recognition on non-performing loans in IFRS financial statements Preamble There is currently a divergence between IFRS requirements and the Prudential Guidelines

International GAAP Disclosure Checklist

EY IFRS Core Tools International GAAP Disclosure Checklist Based on International Financial Reporting Standards in issue at 28 February 2014 Effective for entities with a year-end of 30 June 2014 or thereafter

EY IFRS Core Tools International GAAP Disclosure Checklist Based on International Financial Reporting Standards in issue at 28 February 2014 Effective for entities with a year-end of 30 June 2014 or thereafter

International Financial Reporting Standard (IFRS) for Small and Medium-sized Entities

for Small and Medium-sized Entities") International Financial Reporting Standard (IFRS) for Small and Medium-sized Entities Section 1 Small and Medium-sized Entities Intended scope of this Standard 1.1 The IFRS for SMEs is intended for use

International Financial Reporting Standard (IFRS) for Small and Medium-sized Entities Section 1 Small and Medium-sized Entities Intended scope of this Standard 1.1 The IFRS for SMEs is intended for use

SAFA FINANCIAL REPORTING STANDARD FOR. SMALL AND MEDIUM ENTITIES (SMEs)

") SAFA FINANCIAL REPORTING STANDARD FOR SMALL AND MEDIUM ENTITIES (SMEs) i ii Foreword In the Asian pacific region as whole SMEs represents over 97% of the total entities. Not only in Asian pacific region

SAFA FINANCIAL REPORTING STANDARD FOR SMALL AND MEDIUM ENTITIES (SMEs) i ii Foreword In the Asian pacific region as whole SMEs represents over 97% of the total entities. Not only in Asian pacific region

Financial Management for the Higher Education Sector Regulatory And Reporting Requirements

Financial Management for the Higher Education Sector Regulatory And Reporting Requirements CPA Anthony M. Njiru August 2018 Uphold public interest 1 Regulatory Background IFRSs International financial

Financial Management for the Higher Education Sector Regulatory And Reporting Requirements CPA Anthony M. Njiru August 2018 Uphold public interest 1 Regulatory Background IFRSs International financial

for SMEs International Financial Reporting Standard (IFRS ) for Small and Medium-sized Entities (SMEs)

for Small and Medium-sized Entities (SMEs)") 2009 International Accounting Standards Board (IASB ) IFRS for SMEs International Financial Reporting Standard (IFRS ) for Small and Medium-sized Entities (SMEs) International Financial Reporting Standard

2009 International Accounting Standards Board (IASB ) IFRS for SMEs International Financial Reporting Standard (IFRS ) for Small and Medium-sized Entities (SMEs) International Financial Reporting Standard

Malaysian Private Entities Reporting Standard (MPERS)

") LEMBAGA PIAWAIAN PERAKAUNAN MALAYSIA MALAYSIAN ACCOUNTING STANDARDS BOARD Malaysian Private Entities Reporting Standard (MPERS) Malaysian Accounting Standards Board (February 2014) i This publication contains

LEMBAGA PIAWAIAN PERAKAUNAN MALAYSIA MALAYSIAN ACCOUNTING STANDARDS BOARD Malaysian Private Entities Reporting Standard (MPERS) Malaysian Accounting Standards Board (February 2014) i This publication contains

Good First-time Adopter (International) Limited

Limited") Good First-time Adopter (International) Limited International GAAP Illustrative financial statements of a first-time adopter for the year ended 31 December 2011 Based on International Financial Reporting

Good First-time Adopter (International) Limited International GAAP Illustrative financial statements of a first-time adopter for the year ended 31 December 2011 Based on International Financial Reporting

Framework sets out agreed concepts that underlie financial reporting Objective, qualitative characteristics, element definitions,

International Financial Reporting Standards Framework-based teaching of principle-based standards Michael Wells, Director IFRS Education Initiative, IFRS Foundation The views expressed in this presentation

International Financial Reporting Standards Framework-based teaching of principle-based standards Michael Wells, Director IFRS Education Initiative, IFRS Foundation The views expressed in this presentation

Topic 1: The International Accounting Environment and Financial Reporting

Topic 1: The International Accounting Environment and Financial Reporting USERS OF FINANCIAL STATEMENTS - Internal Users involves Management Accounting communicating to those within entity looking for

Topic 1: The International Accounting Environment and Financial Reporting USERS OF FINANCIAL STATEMENTS - Internal Users involves Management Accounting communicating to those within entity looking for

New Zealand Equivalent to International Accounting Standard 34 Interim Financial Reporting (NZ IAS 34)

") New Zealand Equivalent to International Accounting Standard 34 Interim Financial Reporting (NZ IAS 34) Issued November 2004 and incorporates amendments up to and inclusing 31 October 2010 This Standard

New Zealand Equivalent to International Accounting Standard 34 Interim Financial Reporting (NZ IAS 34) Issued November 2004 and incorporates amendments up to and inclusing 31 October 2010 This Standard

Improvements to IPSAS, 2018

Exposure Draft 65 April 2018 Comments due: July 15, 2018 Proposed International Public Sector Accounting Standard Improvements to IPSAS, 2018 This document was developed and approved by the International

Exposure Draft 65 April 2018 Comments due: July 15, 2018 Proposed International Public Sector Accounting Standard Improvements to IPSAS, 2018 This document was developed and approved by the International

REVENUE APPROACH TO IFRS 15

Meeting: Meeting Location: International Public Sector Accounting Standards Board Toronto, Canada Meeting Date: June 19 22, 2018 Agenda Item 8 For: Approval Discussion Information From: Amon Dhliwayo REVENUE

Meeting: Meeting Location: International Public Sector Accounting Standards Board Toronto, Canada Meeting Date: June 19 22, 2018 Agenda Item 8 For: Approval Discussion Information From: Amon Dhliwayo REVENUE

First-time Adoption of International Financial Reporting Standards

International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards In April 2001 the International Accounting Standards Board (IASB) adopted SIC-8 First-time

International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards In April 2001 the International Accounting Standards Board (IASB) adopted SIC-8 First-time

Indian Accounting Standard 1 Presentation of Financial Statements

Indian Accounting Standard 1 Presentation of Financial Statements Objective This Standard prescribes the basis for presentation of general purpose financial statements to ensure comparability - both with

Indian Accounting Standard 1 Presentation of Financial Statements Objective This Standard prescribes the basis for presentation of general purpose financial statements to ensure comparability - both with

Accounting Policies, Changes in Accounting Estimates and Errors

International Accounting Standard 8 Accounting Policies, Changes in Accounting Estimates and Errors This version includes amendments resulting from IFRSs issued up to 31 December 2008. IAS 8 Net Profit

International Accounting Standard 8 Accounting Policies, Changes in Accounting Estimates and Errors This version includes amendments resulting from IFRSs issued up to 31 December 2008. IAS 8 Net Profit

International GAAP Disclosure Checklist

IFRS Core Tools International GAAP Disclosure Checklist Based on International Financial Reporting Standards in issue at 31 August 2015 International GAAP Disclosure Checklist Updated: August 2015 For

IFRS Core Tools International GAAP Disclosure Checklist Based on International Financial Reporting Standards in issue at 31 August 2015 International GAAP Disclosure Checklist Updated: August 2015 For

Exposure Draft. Accounting Standard (AS) 5 (Revised 20XX) (Corresponding to IAS 8) Accounting Policies, Changes in Accounting Estimates and Errors

5 (Revised 20XX) (Corresponding to IAS 8) Accounting Policies, Changes in Accounting Estimates and Errors") Exposure Draft Accounting Standard (AS) 5 (Revised 20XX) (Corresponding to IAS 8) Accounting Policies, Changes in Accounting Estimates and Errors (Last date for Comments: April 07, 2010) Issued by Accounting

Exposure Draft Accounting Standard (AS) 5 (Revised 20XX) (Corresponding to IAS 8) Accounting Policies, Changes in Accounting Estimates and Errors (Last date for Comments: April 07, 2010) Issued by Accounting

Module 2 (formats for different statements & calculation of cash flows)

") Module 2 (formats for different statements & calculation of cash flows) Statement of Profit & Loss and Other Comprehensive Income Revenue Other Income Expense excluding finance cost Operating Profit Finance

Module 2 (formats for different statements & calculation of cash flows) Statement of Profit & Loss and Other Comprehensive Income Revenue Other Income Expense excluding finance cost Operating Profit Finance

New Zealand Equivalent to International Accounting Standard 34 Interim Financial Reporting (NZ IAS 34)

") New Zealand Equivalent to International Accounting Standard 34 Interim Financial Reporting (NZ IAS 34) Issued November 2004 and incorporates amendments up to and including 31 December 2012 This Standard

New Zealand Equivalent to International Accounting Standard 34 Interim Financial Reporting (NZ IAS 34) Issued November 2004 and incorporates amendments up to and including 31 December 2012 This Standard

CAMBODIAN ACCOUNTING STANDARDS (CAS)

") CAMBODIAN ACCOUNTING STANDARDS (CAS) 1 - CAS 1 : Presentation of Financial Statements an Audit of Financial Statements 2 - CAS 2 : Inventories 3 - CAS 7 : Cash Flow Statements 4 - CAS 8 : Net profit or

CAMBODIAN ACCOUNTING STANDARDS (CAS) 1 - CAS 1 : Presentation of Financial Statements an Audit of Financial Statements 2 - CAS 2 : Inventories 3 - CAS 7 : Cash Flow Statements 4 - CAS 8 : Net profit or

Financial reporting update

Financial reporting update Agenda What s new for 2017 o o Disclosure initiative Minor accounting standard changes PBEs For-Profits Major changes on the horizon Disclosure Initiative Objectives of financial

Financial reporting update Agenda What s new for 2017 o o Disclosure initiative Minor accounting standard changes PBEs For-Profits Major changes on the horizon Disclosure Initiative Objectives of financial

Accounting Policies, Changes in Accounting Estimates and Errors. Jalis Ahmad & Co. Chartered Accountants

International Accounting Standard (IAS-8) Accounting Policies, Changes in Accounting Estimates and Errors Objective Of IAS 8 O O O O O O it prescribes the criteria for: selection of accounting policies;

International Accounting Standard (IAS-8) Accounting Policies, Changes in Accounting Estimates and Errors Objective Of IAS 8 O O O O O O it prescribes the criteria for: selection of accounting policies;

Preparation and Presentation of Financial Statements Part 1 17 September 2013

Preparation and Presentation of Financial Statements Part 1 17 September 2013 LAM Chi Yuen Nelson 林智遠 MBA MSc BBA ACA ACS CFA CPA(US) CTA FCCA FCPA FCPA(Aust.) FHKIoD FTIHK MHKSI MSCA 2008-13 Nelson Consulting

Preparation and Presentation of Financial Statements Part 1 17 September 2013 LAM Chi Yuen Nelson 林智遠 MBA MSc BBA ACA ACS CFA CPA(US) CTA FCCA FCPA FCPA(Aust.) FHKIoD FTIHK MHKSI MSCA 2008-13 Nelson Consulting

NZ IFRS 1 COPYRIGHT. External Reporting Board ( XRB ) 2011

2011") New Zealand Equivalent to International Financial Reporting Standard 1 First-time Adoption of New Zealand Equivalents to International Financial Reporting Standards (NZ IFRS 1) Issued December 2008 and

New Zealand Equivalent to International Financial Reporting Standard 1 First-time Adoption of New Zealand Equivalents to International Financial Reporting Standards (NZ IFRS 1) Issued December 2008 and

IFRS for SMEs PART A. International Financial Reporting Standard (IFRS ) for Small and Medium-sized Entities (SMEs)

for Small and Medium-sized Entities (SMEs)") 2015 International Financial Reporting Standard (IFRS ) for Small and Medium-sized Entities (SMEs) IFRS for SMEs This official pronouncement incorporates 2015 Amendments to the IFRS for SMEs (effective

2015 International Financial Reporting Standard (IFRS ) for Small and Medium-sized Entities (SMEs) IFRS for SMEs This official pronouncement incorporates 2015 Amendments to the IFRS for SMEs (effective

IFRS compared to US GAAP: An overview. September 2010

IFRS compared to US GAAP: An overview September 2010 1 IFRS compared to US GAAP: An overview This overview is an abridged version of our publication IFRS compared to US GAAP, published in September 2010.

IFRS compared to US GAAP: An overview September 2010 1 IFRS compared to US GAAP: An overview This overview is an abridged version of our publication IFRS compared to US GAAP, published in September 2010.

IFRS for SMEs scope and concepts

28 April 2010 International Financial Reporting Standards IFRS for SMEs scope and concepts World Bank GDLN Michael Wells, Director of IFRS Education Initiative IASC Foundation The views expressed in this

28 April 2010 International Financial Reporting Standards IFRS for SMEs scope and concepts World Bank GDLN Michael Wells, Director of IFRS Education Initiative IASC Foundation The views expressed in this

IAS - 1. Presentation of Financial Statements. By:

IAS - 1 Presentation of Financial Statements International Accounting Standard No 1 (IAS 1) Presentation of Financial Statements This revised Standard replaces IAS 1 (revised 1997) Presentation of Financial

IAS - 1 Presentation of Financial Statements International Accounting Standard No 1 (IAS 1) Presentation of Financial Statements This revised Standard replaces IAS 1 (revised 1997) Presentation of Financial

IFRS FOR SMEs: Financial Statement Presentation. Credibility. Professionalism. AccountAbility

IFRS FOR SMEs: Financial Statement Presentation Credibility. Professionalism. AccountAbility Overview of financial statement presentation 2 Section 3 specifies general requirements for financial statement

IFRS FOR SMEs: Financial Statement Presentation Credibility. Professionalism. AccountAbility Overview of financial statement presentation 2 Section 3 specifies general requirements for financial statement

IFRS for SMEs. World Bank, Chisinau. International Financial Reporting Standards. Michael Wells, Director of IFRS Education Initiative IASC Foundation

27 May 2010 International Financial Reporting Standards IFRS for SMEs World Bank, Chisinau Michael Wells, Director of IFRS Education Initiative IASC Foundation The views expressed in this presentation

27 May 2010 International Financial Reporting Standards IFRS for SMEs World Bank, Chisinau Michael Wells, Director of IFRS Education Initiative IASC Foundation The views expressed in this presentation

NZ International Accounting Standard 8 (PBE) Accounting Policies, Changes in Accounting Estimates and Errors (NZ IAS 8 (PBE))

Accounting Policies, Changes in Accounting Estimates and Errors (NZ IAS 8 (PBE))") NZ International Accounting Standard 8 (PBE) Accounting Policies, Changes in Accounting Estimates and Errors (NZ IAS 8 (PBE)) Issued November 2012 excluding consequential amendments resulting from early

NZ International Accounting Standard 8 (PBE) Accounting Policies, Changes in Accounting Estimates and Errors (NZ IAS 8 (PBE)) Issued November 2012 excluding consequential amendments resulting from early

International Public Sector Accounting Standard 32 Service Concession Arrangements: Grantor IPSASB Basis for Conclusions

International Public Sector Accounting Standard 32 Service Concession Arrangements: Grantor IPSASB Basis for Conclusions International Public Sector Accounting Standards, Exposure Drafts, Consultation

International Public Sector Accounting Standard 32 Service Concession Arrangements: Grantor IPSASB Basis for Conclusions International Public Sector Accounting Standards, Exposure Drafts, Consultation

PUBLIC BENEFIT ENTITIES FRAMEWORK

PUBLIC BENEFIT ENTITIES FRAMEWORK Issued March 2014 This Authoritative Notice, the PBE Framework, was issued by the New Zealand Accounting Standards Board of the External Reporting Board pursuant to section

PUBLIC BENEFIT ENTITIES FRAMEWORK Issued March 2014 This Authoritative Notice, the PBE Framework, was issued by the New Zealand Accounting Standards Board of the External Reporting Board pursuant to section

Good Group (International) Limited

Limited") EY IFRS Core Tools Good Group (International) Limited International GAAP Illustrative financial statements for the year ended 31 December 2013 Based on International Financial Reporting Standards in issue

EY IFRS Core Tools Good Group (International) Limited International GAAP Illustrative financial statements for the year ended 31 December 2013 Based on International Financial Reporting Standards in issue

International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards

International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards Objective 1 The objective of this IFRS is to ensure that an entity s first IFRS financial

International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards Objective 1 The objective of this IFRS is to ensure that an entity s first IFRS financial

Board Meeting Handout Accounting for Financial Instruments: Hedge Accounting March 10, 2010

Board Meeting Handout Accounting for Financial Instruments: Hedge Accounting March 10, 2010 PURPOSE OF THE MEETING 1. The purpose of this meeting is to discuss the hedge accounting model to be included

Board Meeting Handout Accounting for Financial Instruments: Hedge Accounting March 10, 2010 PURPOSE OF THE MEETING 1. The purpose of this meeting is to discuss the hedge accounting model to be included

Presentation of Financial Statements

LEMBAGA PIAWAIAN PERAKAUNAN MALAYSIA MALAYSIAN ACCOUNTING STANDARDS BOARD MASB Standard 1 Presentation of Financial Statements Any correspondence regarding this Standard should be addressed to: The Chairman

LEMBAGA PIAWAIAN PERAKAUNAN MALAYSIA MALAYSIAN ACCOUNTING STANDARDS BOARD MASB Standard 1 Presentation of Financial Statements Any correspondence regarding this Standard should be addressed to: The Chairman

International Accounting: Introduction

International Accounting: Introduction Agenda 1. Introduction 2. Organisation of the IASB/IFRS Foundation 3. EC Regulation 4. Accounting principles and accounting standards 5. Components of financial statements

International Accounting: Introduction Agenda 1. Introduction 2. Organisation of the IASB/IFRS Foundation 3. EC Regulation 4. Accounting principles and accounting standards 5. Components of financial statements

IFRS disclosure checklist 2011

www.pwc.com/ifrs IFRS disclosure checklist 2011 IFRS disclosure checklist 2011 Introduction The IFRS disclosure checklist has been updated to take into account standards and interpretations effective

www.pwc.com/ifrs IFRS disclosure checklist 2011 IFRS disclosure checklist 2011 Introduction The IFRS disclosure checklist has been updated to take into account standards and interpretations effective

Understanding IFRSs A Framework-based approach to applying IFRSs

International Financial Reporting Standards Understanding IFRSs A Framework-based approach to applying IFRSs Michael Wells, Director, IFRS Education Initiative, IFRS Foundation The views expressed in this

International Financial Reporting Standards Understanding IFRSs A Framework-based approach to applying IFRSs Michael Wells, Director, IFRS Education Initiative, IFRS Foundation The views expressed in this

First-time Adoption of International Financial Reporting Standards

IFRS Standard 1 First-time Adoption of International Financial Reporting Standards In April 2001 the International Accounting Standards Board (the Board) adopted SIC-8 First-time Application of IASs as

IFRS Standard 1 First-time Adoption of International Financial Reporting Standards In April 2001 the International Accounting Standards Board (the Board) adopted SIC-8 First-time Application of IASs as

IFAC IPSASB Meeting Agenda Paper 2.0 June 2008 Moscow, Russia Page 1 of 5

IFAC IPSASB Meeting Agenda Paper 2.0 June 2008 Moscow, Russia Page 1 of 5 INTERNATIONAL FEDERATION OF ACCOUNTANTS 545 Fifth Avenue, 14th Floor Tel: (212) 286-9344 New York, New York 10017 Fax: (212) 286-9570

IFAC IPSASB Meeting Agenda Paper 2.0 June 2008 Moscow, Russia Page 1 of 5 INTERNATIONAL FEDERATION OF ACCOUNTANTS 545 Fifth Avenue, 14th Floor Tel: (212) 286-9344 New York, New York 10017 Fax: (212) 286-9570

Malaysian Private Entities Reporting Standard (MPERS)

") LEMBAGA PIAWAIAN PERAKAUNAN MALAYSIA MALAYSIAN ACCOUNTING STANDARDS BOARD Malaysian Private Entities Reporting Standard (MPERS) This document incorporates 2015 Amendments to the Malaysian Private Entities

LEMBAGA PIAWAIAN PERAKAUNAN MALAYSIA MALAYSIAN ACCOUNTING STANDARDS BOARD Malaysian Private Entities Reporting Standard (MPERS) This document incorporates 2015 Amendments to the Malaysian Private Entities

IFRS disclosure checklist

IFRS disclosure checklist 2017 IFRS disclosure checklist 2017 Introduction The IFRS disclosure checklist has been updated to outline the disclosures required for December 2017 year ends. It also contains

IFRS disclosure checklist 2017 IFRS disclosure checklist 2017 Introduction The IFRS disclosure checklist has been updated to outline the disclosures required for December 2017 year ends. It also contains

Good Group New Zealand Limited

Good Group New Zealand Limited Illustrative consolidated financial statements for the year ended 31 December 2015 Based on NZ IFRS for Tier 1 and Tier 2 for-profit entities (also applicable to 30 June

Good Group New Zealand Limited Illustrative consolidated financial statements for the year ended 31 December 2015 Based on NZ IFRS for Tier 1 and Tier 2 for-profit entities (also applicable to 30 June

Work Plan for the Consideration of Incorporating International Financial Reporting Standards into the Financial Reporting System for U.S.

Work Plan for the Consideration of Incorporating International Financial Reporting Standards into the Financial Reporting System for U.S. Issuers A Comparison of U.S. GAAP and IFRS A Securities and Exchange

Work Plan for the Consideration of Incorporating International Financial Reporting Standards into the Financial Reporting System for U.S. Issuers A Comparison of U.S. GAAP and IFRS A Securities and Exchange

IFRS AND IND AS Preface

IFRS AND IND AS CA. Rajkumar S. Adukia http://www.carajkumarradukia.com rajkumarfca@gmail.com +91 98200 61049/09323061049 Preface India, one of the fastest growing global economies is on the verge of converging

IFRS AND IND AS CA. Rajkumar S. Adukia http://www.carajkumarradukia.com rajkumarfca@gmail.com +91 98200 61049/09323061049 Preface India, one of the fastest growing global economies is on the verge of converging

FUNDAMENTALS OF IFRS

FUNDAMENTALS OF IFRS 15.1 FUNDAMENTALS OF IFRS CHAPTER 15 Accounting Policies, Changes in Accounting Estimates and Errors (IAS 8) 15.2 CHAPTER FIFTEEN Introduction Accounting Policies, Changes in Accounting

FUNDAMENTALS OF IFRS 15.1 FUNDAMENTALS OF IFRS CHAPTER 15 Accounting Policies, Changes in Accounting Estimates and Errors (IAS 8) 15.2 CHAPTER FIFTEEN Introduction Accounting Policies, Changes in Accounting

IFRS FOR SMES AT A GLANCE As at 1 January 2016

IFRS FOR SMES AT A GLANCE As at 1 January 2016 IFRS for SMEs AT A GLANCE IFRS at a Glance for SMEs (IAAG SME) has been compiled to assist in gaining a high level overview of International Financial Reporting

IFRS FOR SMES AT A GLANCE As at 1 January 2016 IFRS for SMEs AT A GLANCE IFRS at a Glance for SMEs (IAAG SME) has been compiled to assist in gaining a high level overview of International Financial Reporting

IAS 34 Interim Financial Reporting

// Shreeji // IAS 34 Interim Financial Reporting 1. Introduction IAS 34 Interim Financial Reporting was issued by the International Accounting Standards Committee in February 1998. A limited amendment

// Shreeji // IAS 34 Interim Financial Reporting 1. Introduction IAS 34 Interim Financial Reporting was issued by the International Accounting Standards Committee in February 1998. A limited amendment

Alternative format. Illustrative consolidated financial statements for the year ended 31 December International GAAP

IFRS Core Tools Good Group (International) Limited Alternative format Illustrative consolidated financial statements for the year ended 31 December 2018 International GAAP Contents Abbreviations and key...

IFRS Core Tools Good Group (International) Limited Alternative format Illustrative consolidated financial statements for the year ended 31 December 2018 International GAAP Contents Abbreviations and key...

First-time Adoption of International Financial Reporting Standards

International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards This version was issued in November 2008. Its effective date is 1 July 2009. It includes

International Financial Reporting Standard 1 First-time Adoption of International Financial Reporting Standards This version was issued in November 2008. Its effective date is 1 July 2009. It includes

CIMA F1. Financial Operations Student Notes

CIMA F1 Financial Operations Student Notes Contents CIMA F1...1 Topic 6 The Regulatory Environment...2 International Financial Reporting Standards (IFRSs)...5 Topic 7: The Conceptual Framework...7 Topic

CIMA F1 Financial Operations Student Notes Contents CIMA F1...1 Topic 6 The Regulatory Environment...2 International Financial Reporting Standards (IFRSs)...5 Topic 7: The Conceptual Framework...7 Topic