Session II: Overview of MFTransparency and the Transparent Pricing Initiative

|

|

|

- Juniper Reynolds

- 6 years ago

- Views:

Transcription

1 Promoting Transparent Pricing in the Microfinance Industry Session II: Overview of MFTransparency and the Transparent Pricing Initiative Philippines March 2011

2 What is Transparent Pricing? Transparent pricing means the pricing, terms, and conditions of financial products will be adequately disclosed to the clients in a clear manner that allows both accurate understanding of prices and comparison of different products. Different levels of transparency: To regulators / policy makers To investors / donors / funders To clients and the market

3 Combined Approach Self Regulated Practice of Transparent Pricing Supportive Government Regulation Responsible Pricing

4 How to achieve Responsible Finance? MFTransparency s Business Model 1. Consulting on Legislation & Regulation: MFT provides recommendations to central banks and regulatory authorities around consumer protection and pricing transparency 2. Data Collection & Dissemination: MFT collects product prices and information to display on its website to facilitate a more transparent market. 3. Technical Assistance & Training to Service Providers: MFT provides technical training to MFIs, rating agencies, industry initiatives, and other organizations to improve practices and create standardized practices in the industry 4. Consumer awareness, education and financial capability : Provide training materials and resources to improve client consumer literacy 4

5 Client Protection Principles 1. Appropriate product design 2. Transparency 3. Responsible pricing 4. Responsible treatment of clients 5. Effective complaints resolution 6. Privacy of client data

6 Social Performance Indicators

7 Promoting Transparent Pricing in the Microfinance Industry U.S. Based Non-Profit Organization Work in 28 countries Mission: to promote pricing transparency in the microfinance sector through: Data collection, standardization, & dissemination Training & capacity building for financial institutions Development of educational materials Consulting to regulators & policy makers on price disclosure legislation

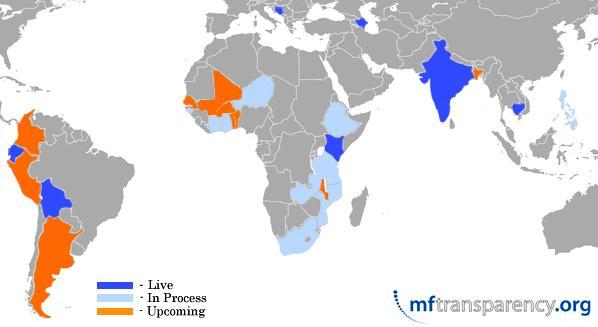

8 MFTransparency Coverage

9 Our Sponsors Ford Foundation Elena Nelson Anna Maria Zegarra Nancy Goyburo Maria Sara Jijon Bill Maddocks Kim Wilson NarasimhanSrinivasan Point Loma Nazarene University 9 9

10 GLOBAL OUR PARTNERS REGIONAL AFRICA

11 NATIONAL OUR PARTNERS Argentina Azerbaijan Benin Bolivia Bosnia Burkina Faso Cambodia Colombia Ecuador India Ivory Coast Kenya Malawi Mali Niger Rwanda Senegal South Africa Direction de la Microfinance Togo Uganda

12 Self-Regulation MFTransparency facilitates self-regulation on pricing transparency Our Approach Country by country Partner with local networks, policymakers, regulators and stakeholders Publish true prices all at the same time Objective, equal treatment of all MFIs

13 Transparency for a Healthy Microfinance Industry Policy / Regulation Analytical Publications Regulators 75 Countries MFI Industry 5,000 MFIs Conferences and Educational Materials Transparency Public and Press Consumers 100 million Pricing Data Website Education Effective policy requires building a strong foundation at the Bottom of the Pyramid -- Pricing Transparency and education of all stakeholders creates an enabling environment for a healthy microfinance industry

14 MFT Works with all Industry Stakeholders MFIs MFT Networks, Associations, Industry Initiatives, Rating Agencies Regulators, Supervisory Bodies, Consumer Protection Agencies Donors & Investors 14

15 Funded Pilot Project Methodology tested in Peru and Bosnia in March 2009 Of the MFIs that attended the training sessions: 14/14 Bosnian MFIs submitted data (100%) 35/43 Peruvian MFIs submitted data (81%) Bosnia data live on 15

16 Immediate Effects of the Transparent Pricing Initiative MFIs lowering prices for products priced high relative to the market MFIs increasing their prices for products priced low relative to the market Progress by regulators toward new pro-poor policies 16

Colombia Kenya (Update) Ecuador Ghana Peru (Update) India Mali Mozambique Kenya Niger Tanzania Malawi Rwanda Zambia Senegal South Africa Togo Uganda")

17 Completed & Published on Website Global Coverage In Process Upcoming Azerbaijan Argentina Ethiopia Bolivia Benin Guinea Bissau Bosnia Burkina Faso Ivory Coast Cambodia (Refreshed) Colombia Kenya (Update) Ecuador Ghana Peru (Update) India Mali Mozambique Kenya Niger Tanzania Malawi Rwanda Zambia Senegal South Africa Togo Uganda 17

18 MFTransparency Transparent Pricing Initiative in the Philippines 1. Data Collection, Standardization & Dissemination 2. Training and Capacity Building 3. Promotion of Transparent Pricing Standards 4. Promotion & Implementation of Pricing Disclosure Policy 5. Development of Educational Resources for the Sector

19 Participation Rewards 19

20 Endorse MFT We invite all to sign our endorsement statement, committing to transparency in pricing and education of MF stakeholders 20

21 Partner to Develop or Distribute Educational Materials MFT is looking for partners to develop educational materials Possible actions: Co-author materials Allow MFT to distribute your materials Host pricing & transparency workshops with MFT 21

22 Rapid Progress in Transparency (Results of past 18 months) MFTransparency currently working in 27 countries (adding nearly 1 more each month) 300+ Institutions 1,000+ different loan products 38 million clients US$11 billion in outstanding portfolio Microfinance is the first industry of any kind in the world to practice global, voluntary disclosure of true pricing.

23 Example 1: Cambodia Prices Must be disclosed Charging flat interest rates prohibited Calculation of compounding interest rates required Pricing Information Information about prices must be published on MFI websites

24 Prices Example 2: Bosnia Compounding calculations required Must be included on loan contract and repayment schedule Reporting Prices by product must be reported to regulators Pricing Information Information about prices must be published on MFI website

25 Example 3: Peru Interest Rates Interest rates must be disclosed Calculation of compounding interest required Reporting Prices by product must be reported to regulator Pricing Information All fees and insurance charges must be disclosed Information about prices must be published on the MFI website

26 Standardized Repayment Schedule

27 Standardized Pricing Disclosure Reporting

28 Standardized Pricing Dissemination

29 Standardized Pricing Dissemination

")

30 MFTransparency also does Pricing Certification Reports (in countries where we are not active)

31 Who Benefits from Pricing Transparency? Consumers: They get to know the real price they can decide whether they want to borrow They can decide between competing loan products or MFIs based comparative data MFIs They learn what the market price is, where they stand, and can take steps to refine their pricing strategy Industry Microfinance sector gets a database from which it can take up issues with policy makers

32 Who Benefits from Pricing Transparency? Funders and donors: They know what their client MFIs charge their customers, and can choose their partners accordingly Regulators Observe the prices prevailing in the market, sharpening their ability to intervene specifically and refine policy

33 Conclusions Transparent pricing is a prerequisite for responsible pricing We need better knowledge and understanding of pricing, and better data to analyze Portfolio yield is far from adequate Individual product pricing is essential, and it is attainable if we work together Transparent pricing leads to more competition and better decisions by all stakeholders More competition and better decisions lead to more responsible pricing

34 Next Steps in the Philippines Review materials One-on-one discussions and dialogue Begin data submission process Additional training & technical support Consider recommendations on price transparency Implement financial education resources

35 Promoting Transparent Pricing in the Microfinance Industry

36 Promoting Transparent Pricing in the Microfinance Industry Session III: Approaches for Calculating True Prices Implementing Transparency in the Filipino Microfinance Industry Philippines March 2011

37 Which loan looks less expensive? Loan Product Loan Amount Total Cost Length of Loan Loan Option A $1,000 $ weeks Loan Option B $511 $ months Loan Option C $360 $ months The standard way to compare cost of loan options is by calculating the APR (Annual Percentage Rate). We will now see how to calculate APRs.

38 Example of Loan Pricing Interest rate of 3% per month Small loan processing fee of 2% Loan security savings of 15% MFI pays client 5% interest on savings What do you think the APR or EIR of this loan is?

39 Declining Balance interest reflects the textbook definition of interest as a charge for the use of money over time. APR is equivalent to declining balance interest with no fees.

40 With Flat interest, interest is charged on the original loan amount resulting in nearly double the cost of declining balance interest. Why double? The area of the rectangle under the green line is almost double the area under the red stair-step loan balance.

41 In addition, the client is often charged fees for the loan. In this example, a 2% up-front fee, because of the short loan term, surprisingly adds 13% to the APR. A loan advertised as 36% interest is now the equivalent of 78% APR.

even though they never have use of that amount.")

42 The red area shows money invested in business. The blue line shows money held in savings. Compulsory savings adds to the cost. Clients are charged interest on the original loan ($1000) even though they never have use of that amount. In this example, the APR is now 107%.

43 Clients are paid interest, but significantly less interest on their savings than they are charged on their loans. When earning 5% interest, the APR only drops from 107% to 105%.

44 In this example, the client pays a total cost of $131 for the $1,000 loan for 16 weeks. If she were to renew the loan consistently for an entire year, she would pay a total of $425 for the year.

45 Average net loan balance is $360 But, the client never had a $1,000. She only received $850 because of the savings, and then she paid back a portion each week. She paid $425 to have an average loan balance of $360 for a year, giving an APR greater than 100%.

46 And with compulsory savings there are some months in which the client actually has more money in savings than invested in her business, giving a negative net loan balance.

47 Which loan looks less expensive? Loan Product Initial Loan Amount Total Cost Length of Loan APR Loan Option A $1,000 $ weeks 79% Loan Option B $511 $ months 79% Loan Option C $360 $ months 105% The three products we were comparing are actually identical in financial terms. Loan C includes cost of compulsory savings in the APR calculation. Loans advertised as 3% per month can have APRs of 79% or even 105%

48 Promoting Transparent Pricing in the Microfinance Industry

MicroFinance Transparency

MicroFinance Transparency Annual Report April 2010 March 2011 Promoting Transparent Pricing for the Microfinance Industry TABLE OF CONTENTS Message from our CEO... 3 Message from our President... 3 Need

MicroFinance Transparency Annual Report April 2010 March 2011 Promoting Transparent Pricing for the Microfinance Industry TABLE OF CONTENTS Message from our CEO... 3 Message from our President... 3 Need

Managing Geopolitical Risk

Managing Geopolitical Risk Bunmi Lawson, MD/CEO Accion, Nigeria Milena Loayza, Manager Financial Sector BIO, Belgium Nejira Nalić, Director Mi-Bospo, Bosnia Herzegovina Alexander Remy, Equity Investment

Managing Geopolitical Risk Bunmi Lawson, MD/CEO Accion, Nigeria Milena Loayza, Manager Financial Sector BIO, Belgium Nejira Nalić, Director Mi-Bospo, Bosnia Herzegovina Alexander Remy, Equity Investment

Transparent Pricing Progress:

Promoting Transparent Pricing in the Microfinance Industry Transparent Pricing Progress: How to Understand the Prices We Charge SPM Essentials April 2012 Agenda 1. Introduction to the confusing world of

Promoting Transparent Pricing in the Microfinance Industry Transparent Pricing Progress: How to Understand the Prices We Charge SPM Essentials April 2012 Agenda 1. Introduction to the confusing world of

Africa: An Emerging World Region

World Affairs Topical Series Africa: An Emerging World Region (Table of Contents) July 18, 2018 TABLE OF CONTENTS Evolution of Africa Markets.. Early Phase... Maturation Phase... Stumbles Phase.... Population...

World Affairs Topical Series Africa: An Emerging World Region (Table of Contents) July 18, 2018 TABLE OF CONTENTS Evolution of Africa Markets.. Early Phase... Maturation Phase... Stumbles Phase.... Population...

TRANSPARENT PRICING INITIATIVE IN INDIA

PRICING DATA REPORT TRANSPARENT PRICING INITIATIVE IN INDIA 26 January 2011 SPONSORS The Transparent Pricing Initiative in India is sponsored by MFTransparency would like to extend a special thank you

PRICING DATA REPORT TRANSPARENT PRICING INITIATIVE IN INDIA 26 January 2011 SPONSORS The Transparent Pricing Initiative in India is sponsored by MFTransparency would like to extend a special thank you

Appendix 3 Official Debt Restructuring

. Appendix 3 Official Debt Restructuring Restructuring with official creditors THIS APPENDIX REVIEWS OFFICIAL DEBT REstructuring agreements concluded since the publication of Global Development Finance

. Appendix 3 Official Debt Restructuring Restructuring with official creditors THIS APPENDIX REVIEWS OFFICIAL DEBT REstructuring agreements concluded since the publication of Global Development Finance

H. R. To provide for the cancellation of debts owed to international financial institutions by poor countries, and for other purposes.

[0hih]... (Original Signature of Member) 0TH CONGRESS ST SESSION H. R. To provide for the cancellation of debts owed to international financial institutions by poor countries, and for other purposes. IN

[0hih]... (Original Signature of Member) 0TH CONGRESS ST SESSION H. R. To provide for the cancellation of debts owed to international financial institutions by poor countries, and for other purposes. IN

Background Note on Prospects for IDA to Become Financially Self-Sustaining

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Background Note on Prospects for IDA to Become Financially Self-Sustaining International

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Background Note on Prospects for IDA to Become Financially Self-Sustaining International

The world of CARE. 2 CARE Facts & Figures

CARE Facts & Figures 2004 The world of CARE 2 CARE Facts & Figures 2003 www.care.org 71 Australia 75 France 79 Norway CARE International Member countries: 72 Austria 73 Canada 76 Germany 77 Japan 80 Thailand

CARE Facts & Figures 2004 The world of CARE 2 CARE Facts & Figures 2003 www.care.org 71 Australia 75 France 79 Norway CARE International Member countries: 72 Austria 73 Canada 76 Germany 77 Japan 80 Thailand

African Financial Markets Initiative

African Financial Markets Initiative African Domestic Bond Fund Feasibility Study Frankfurt, November 2011 This presentation is organised into four sections I. Introduction to the African Financial Markets

African Financial Markets Initiative African Domestic Bond Fund Feasibility Study Frankfurt, November 2011 This presentation is organised into four sections I. Introduction to the African Financial Markets

PARIS CLUB RECENT ACTIVITY

PARIS CLUB RECENT ACTIVITY 1/13 OUTLINE 1. Quick review of Paris Club recent activity 2. Prepayment by Russia of its Paris Club debt 2/13 Key events in June 2006-May 2007 1. Implementation of the HIPC

PARIS CLUB RECENT ACTIVITY 1/13 OUTLINE 1. Quick review of Paris Club recent activity 2. Prepayment by Russia of its Paris Club debt 2/13 Key events in June 2006-May 2007 1. Implementation of the HIPC

Argentina Bahamas Barbados Bermuda Bolivia Brazil British Virgin Islands Canada Cayman Islands Chile

Americas Argentina (Banking and finance; Capital markets: Debt; Capital markets: Equity; M&A; Project Bahamas (Financial and corporate) Barbados (Financial and corporate) Bermuda (Financial and corporate)

Americas Argentina (Banking and finance; Capital markets: Debt; Capital markets: Equity; M&A; Project Bahamas (Financial and corporate) Barbados (Financial and corporate) Bermuda (Financial and corporate)

CARE GLOBAL VSLA REACH 2017 AN OVERVIEW OF THE GLOBAL REACH OF CARE S VILLAGE SAVINGS AND LOANS ASSOCIATION PROGRAMING

CARE GLOBAL VSLA REACH 2017 AN OVERVIEW OF THE GLOBAL REACH OF CARE S VILLAGE SAVINGS AND LOANS ASSOCIATION PROGRAMING December 2017 SCALE CARE has promoted Village Savings and Loan Associations (VSLAs)

CARE GLOBAL VSLA REACH 2017 AN OVERVIEW OF THE GLOBAL REACH OF CARE S VILLAGE SAVINGS AND LOANS ASSOCIATION PROGRAMING December 2017 SCALE CARE has promoted Village Savings and Loan Associations (VSLAs)

Country Malaria Interventions Gap Analysis

1 Country Malaria Interventions Gap Analysis For the years 20182020 Prepared based on the analysis of countries Global Fund applications 2 Gap analysis at a glance The financial and commodity gap analysis

1 Country Malaria Interventions Gap Analysis For the years 20182020 Prepared based on the analysis of countries Global Fund applications 2 Gap analysis at a glance The financial and commodity gap analysis

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT BOARD OF GOVERNORS. Resolution No. 612

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT BOARD OF GOVERNORS Resolution No. 612 2010 Selective Increase in Authorized Capital Stock to Enhance Voice and Participation of Developing and Transition

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT BOARD OF GOVERNORS Resolution No. 612 2010 Selective Increase in Authorized Capital Stock to Enhance Voice and Participation of Developing and Transition

The Microfinance Rating Market Outlook The Rating Fund Market Survey 2005

The Microfinance Rating Market Outlook The Rating Fund Market Survey 25 Introduction Microfinance rating services are playing a key role in helping MFIs to improve performance and to source commercial

The Microfinance Rating Market Outlook The Rating Fund Market Survey 25 Introduction Microfinance rating services are playing a key role in helping MFIs to improve performance and to source commercial

HIPC HEAVILY INDEBTED POOR COUNTRIES INITIATIVE MDRI MULTILATERAL DEBT RELIEF INITIATIVE

GOAL To ensure deep, broad and fast debt relief and thereby contribute toward growth, poverty reduction, and debt sustainability in the poorest, most heavily indebted countries. GOAL To provide additional

GOAL To ensure deep, broad and fast debt relief and thereby contribute toward growth, poverty reduction, and debt sustainability in the poorest, most heavily indebted countries. GOAL To provide additional

Building Resilience in Fragile States: Experiences from Sub Saharan Africa. Mumtaz Hussain International Monetary Fund October 2017

Building Resilience in Fragile States: Experiences from Sub Saharan Africa Mumtaz Hussain International Monetary Fund October 2017 How Fragility has Changed since the 1990s? In early 1990s, 20 sub-saharan

Building Resilience in Fragile States: Experiences from Sub Saharan Africa Mumtaz Hussain International Monetary Fund October 2017 How Fragility has Changed since the 1990s? In early 1990s, 20 sub-saharan

Note on Revisions. Investing Across Borders 2010 Report

Note on Revisions Last revision: August 30, 2011 Investing Across Borders 2010 Report This note documents all data and revisions to the Investing Across Borders (IAB) 2010 report since its release on July

Note on Revisions Last revision: August 30, 2011 Investing Across Borders 2010 Report This note documents all data and revisions to the Investing Across Borders (IAB) 2010 report since its release on July

Financial Market Liberalization and Its Impact in Sub Saharan Africa

Financial Market Liberalization and Its Impact in Sub Saharan Africa Hamid Rashid, Ph.D. Senior Adviser for Macroeconomic Policy UN Department of Economic and Social Affairs, New York This does not represent

Financial Market Liberalization and Its Impact in Sub Saharan Africa Hamid Rashid, Ph.D. Senior Adviser for Macroeconomic Policy UN Department of Economic and Social Affairs, New York This does not represent

Estimating the regional distribution of income in sub-saharan Africa

WID.world Technical Note N 2017/6 Estimating the regional distribution of income in sub-saharan Africa Lucas Chancel Léo Czajka December 2017 This version: December 11th, 2017 Estimating the regional distribution

WID.world Technical Note N 2017/6 Estimating the regional distribution of income in sub-saharan Africa Lucas Chancel Léo Czajka December 2017 This version: December 11th, 2017 Estimating the regional distribution

MDRI HIPC. heavily indebted poor countries initiative. To provide additional support to HIPCs to reach the MDGs.

Goal To ensure deep, broad and fast debt relief and thereby contribute toward growth, poverty reduction, and debt sustainability in the poorest, most heavily indebted countries. HIPC heavily indebted poor

Goal To ensure deep, broad and fast debt relief and thereby contribute toward growth, poverty reduction, and debt sustainability in the poorest, most heavily indebted countries. HIPC heavily indebted poor

HIPC DEBT INITIATIVE FOR HEAVILY INDEBTED POOR COUNTRIES ELIGIBILITY GOAL

GOAL To ensure deep, broad and fast debt relief with a strong link to poverty reduction. ELIGIBILITY IDA-Only & PRGF eligible Heavily indebted (i.e. NPV of debt above 150% of exports or above 250% of government

GOAL To ensure deep, broad and fast debt relief with a strong link to poverty reduction. ELIGIBILITY IDA-Only & PRGF eligible Heavily indebted (i.e. NPV of debt above 150% of exports or above 250% of government

Report to Donors Sponsored Delegates to the 12th Conference of the Parties Punta del Este, Uruguay 1-9 June 2015

Report to Donors Sponsored Delegates to the 12th Conference of the Parties Punta dell Este, Uruguay 1-9 June 2015 1 Contents Details of sponsorship Table 1. Fundraising (income from donors) Table 2. Sponsored

Report to Donors Sponsored Delegates to the 12th Conference of the Parties Punta dell Este, Uruguay 1-9 June 2015 1 Contents Details of sponsorship Table 1. Fundraising (income from donors) Table 2. Sponsored

Financial Development, Financial Inclusion, and Growth in Africa

International Monetary Fund African Department Financial Development, Financial Inclusion, and Growth in Africa ECOWAS Regional Conference, Dakar, Senegal, Roger Nord Deputy Director African department

International Monetary Fund African Department Financial Development, Financial Inclusion, and Growth in Africa ECOWAS Regional Conference, Dakar, Senegal, Roger Nord Deputy Director African department

MICROFINANCE IN LATIN AMERICA AND THE CARIBBEAN: PAST, PRESENT AND FUTURE

MICROFINANCE IN LATIN AMERICA AND THE CARIBBEAN: PAST, PRESENT AND FUTURE Nancy Lee General Manager MULTILATERAL INVESTMENT FUND Multilateral Investment Fund Member of the IDB Group Microfinance Trends

MICROFINANCE IN LATIN AMERICA AND THE CARIBBEAN: PAST, PRESENT AND FUTURE Nancy Lee General Manager MULTILATERAL INVESTMENT FUND Multilateral Investment Fund Member of the IDB Group Microfinance Trends

TRENDS AND MARKERS Signatories to the United Nations Convention against Transnational Organised Crime

A F R I C A WA T C H TRENDS AND MARKERS Signatories to the United Nations Convention against Transnational Organised Crime Afghanistan Albania Algeria Andorra Angola Antigua and Barbuda Argentina Armenia

A F R I C A WA T C H TRENDS AND MARKERS Signatories to the United Nations Convention against Transnational Organised Crime Afghanistan Albania Algeria Andorra Angola Antigua and Barbuda Argentina Armenia

REGIONAL MATTERS ARISING FROM REPORTS OF THE WHO INTERNAL AND EXTERNAL AUDITS. Information Document CONTENTS BACKGROUND

2 June REGIONAL COMMITTEE FOR AFRICA ORIGINAL: ENGLISH Sixty-seventh session Victoria Falls, Republic of Zimbabwe, 28 August 1 September Provisional agenda item 19.9 REGIONAL MATTERS ARISING FROM REPORTS

2 June REGIONAL COMMITTEE FOR AFRICA ORIGINAL: ENGLISH Sixty-seventh session Victoria Falls, Republic of Zimbabwe, 28 August 1 September Provisional agenda item 19.9 REGIONAL MATTERS ARISING FROM REPORTS

Update on the Integrated Road Map and on proposed interim governance arrangements

Integrated Road Map Update on the Integrated Road Map and on proposed interim governance arrangements Informal Consultation 18 July 2017 0 Agenda Integrated Road Map 1. Update on implementation 2. Lessons

Integrated Road Map Update on the Integrated Road Map and on proposed interim governance arrangements Informal Consultation 18 July 2017 0 Agenda Integrated Road Map 1. Update on implementation 2. Lessons

Improving the Investment Climate in Sub-Saharan Africa

REALIZING THE POTENTIAL FOR PROFITABLE INVESTMENT IN AFRICA High-Level Seminar organized by the IMF Institute and the Joint Africa Institute TUNIS,TUNISIA,FEBRUARY28 MARCH1,2006 Improving the Investment

REALIZING THE POTENTIAL FOR PROFITABLE INVESTMENT IN AFRICA High-Level Seminar organized by the IMF Institute and the Joint Africa Institute TUNIS,TUNISIA,FEBRUARY28 MARCH1,2006 Improving the Investment

The introduction of the Registered Exporter (REX) System

System") Introduction of Registered Exporters (REX) System Customs Information Paper 67 (2016) Who should read: What is it about: When effective: 1 January 2017 Extant until/ Expires 1 May 2017 1. Background Traders

Introduction of Registered Exporters (REX) System Customs Information Paper 67 (2016) Who should read: What is it about: When effective: 1 January 2017 Extant until/ Expires 1 May 2017 1. Background Traders

ANNEX 2: Methodology and data of the Starting a Foreign Investment indicators

ANNEX 2: Methodology and data of the Starting a Foreign Investment indicators Methodology The Starting a Foreign Investment indicators quantify several aspects of business establishment regimes important

ANNEX 2: Methodology and data of the Starting a Foreign Investment indicators Methodology The Starting a Foreign Investment indicators quantify several aspects of business establishment regimes important

MDRI HIPC MULTILATERAL DEBT RELIEF INITIATIVE HEAVILY INDEBTED POOR COUNTRIES INITIATIVE GOAL GOAL

GOAL To ensure deep, broad and fast debt relief and thereby contribute toward growth, poverty reduction, and debt sustainability in the poorest, most heavily indebted countries. HIPC HEAVILY INDEBTED POOR

GOAL To ensure deep, broad and fast debt relief and thereby contribute toward growth, poverty reduction, and debt sustainability in the poorest, most heavily indebted countries. HIPC HEAVILY INDEBTED POOR

Dr. Gabriel MOUGANI Chief Regional Integration Coordinator West Africa Regional Development and Business Delivery Office (RDGW)

") Financing Development: Experiences from Africa, Asia and Latin America The African Development Bank s role and experiences in supporting regional payments systems programs & initiatives in Africa: key

Financing Development: Experiences from Africa, Asia and Latin America The African Development Bank s role and experiences in supporting regional payments systems programs & initiatives in Africa: key

Charting the Diffusion of Power Sector Reform in the Developing World Vivien Foster, Samantha Witte, Sudeshna Gosh Banerjee, Alejandro Moreno

Charting the Diffusion of Power Sector Reform in the Developing World Vivien Foster, Samantha Witte, Sudeshna Gosh Banerjee, Alejandro Moreno Green Growth Knowledge Platform Annual Conference 2017 November

Charting the Diffusion of Power Sector Reform in the Developing World Vivien Foster, Samantha Witte, Sudeshna Gosh Banerjee, Alejandro Moreno Green Growth Knowledge Platform Annual Conference 2017 November

Hundred and Fifty-third Session. Rome, May 2014

April 2014 FC 153/INF/2 E FINANCE COMMITTEE Hundred and Fifty-third Session Rome, 12 14 May 2014 Report of the Executive Director on the Utilization of Contributions and Waivers of Costs) General Rules

April 2014 FC 153/INF/2 E FINANCE COMMITTEE Hundred and Fifty-third Session Rome, 12 14 May 2014 Report of the Executive Director on the Utilization of Contributions and Waivers of Costs) General Rules

Annex Supporting international mobility: calculating salaries

Annex 5.2 - Supporting international mobility: calculating salaries Base salary refers to a fixed amount of money paid to an Employee in return for work performed and it is determined in accordance with

Annex 5.2 - Supporting international mobility: calculating salaries Base salary refers to a fixed amount of money paid to an Employee in return for work performed and it is determined in accordance with

Supplementary Table S1 National mitigation objectives included in INDCs from Jan to Jul. 2017

1 Supplementary Table S1 National mitigation objectives included in INDCs from Jan. 2015 to Jul. 2017 Country Submitted Date GHG Reduction Target Quantified Unconditional Conditional Asia Afghanistan Oct.,

1 Supplementary Table S1 National mitigation objectives included in INDCs from Jan. 2015 to Jul. 2017 Country Submitted Date GHG Reduction Target Quantified Unconditional Conditional Asia Afghanistan Oct.,

PROGRESS REPORT NATIONAL STRATEGIES FOR THE DEVELOPMENT OF STATISTICS. May 2010 NSDS SUMMARY TABLE FOR IDA AND LOWER MIDDLE INCOME COUNTRIES

NATIONAL STRATEGIES FOR THE DEVELOPMENT OF STATISTICS PROGRESS REPORT NSDS SUMMARY TABLE FOR IDA AND LOWER MIDDLE INCOME COUNTRIES May 2010 The Partnership in for in the 21 st Century NSDS STATUS IN IDA

NATIONAL STRATEGIES FOR THE DEVELOPMENT OF STATISTICS PROGRESS REPORT NSDS SUMMARY TABLE FOR IDA AND LOWER MIDDLE INCOME COUNTRIES May 2010 The Partnership in for in the 21 st Century NSDS STATUS IN IDA

Tunis, Tunisia 17 June 2005

Tunis, Tunisia 17 June 2005 United Nations Department of Economic and Social Affairs United Nations Development Programme UNDP Africa Presented by John M. Kauzya The Africa Governance Inventory (AGI) Portal

Tunis, Tunisia 17 June 2005 United Nations Department of Economic and Social Affairs United Nations Development Programme UNDP Africa Presented by John M. Kauzya The Africa Governance Inventory (AGI) Portal

Promo-ng Transparent Pricing in the Microfinance Industry. Rwanda Data Launch. Hosted by MFTransparency and AMIR

Promo-ng Transparent Pricing in the Microfinance Industry Rwanda Data Launch Hosted by MFTransparency and AMIR Webinar September 27 th, 2011 enabling APR & EIR Program enabling Africa to Price Responsibly

Promo-ng Transparent Pricing in the Microfinance Industry Rwanda Data Launch Hosted by MFTransparency and AMIR Webinar September 27 th, 2011 enabling APR & EIR Program enabling Africa to Price Responsibly

Implementation of the Integrated Road Map

Integrated Road Map Implementation of the Integrated Road Map 7 February 2018 2018 Informal Consultations 13 17 November 2017 Second Regular Session [Approval of Update on the Integrated Road Map: interim

Integrated Road Map Implementation of the Integrated Road Map 7 February 2018 2018 Informal Consultations 13 17 November 2017 Second Regular Session [Approval of Update on the Integrated Road Map: interim

Capital Markets Development. Frankfurt, Germany. 12 th April 2018

Capital Markets Development Frankfurt, Germany. 12 th April 2018 The African Development Bank Transforming Africa since 1964 Our mission is to promote sustainable economic development and social progress

Capital Markets Development Frankfurt, Germany. 12 th April 2018 The African Development Bank Transforming Africa since 1964 Our mission is to promote sustainable economic development and social progress

NEPAD-OECD AFRICA INVESTMENT INITIATIVE

NEPAD-OECD AFRICA INVESTMENT INITIATIVE 1 Presentation outline 1. CONTEXT 2. GOALS & DESIGN 3. ACTIVITIES & WORK METHODS 4. EXPECTED IMPACT 5. GOVERNANCE 2 1. CONTEXT Investment is a driver of economic

NEPAD-OECD AFRICA INVESTMENT INITIATIVE 1 Presentation outline 1. CONTEXT 2. GOALS & DESIGN 3. ACTIVITIES & WORK METHODS 4. EXPECTED IMPACT 5. GOVERNANCE 2 1. CONTEXT Investment is a driver of economic

Presentation: Position Paper N 2 Results and Key Findings

Second and third tier MFIs: Where do we stand? e-mfp Action Group Investors in Tier 2/3 MFIs Presentation: Position Paper N 2 Results and Key Findings Philippe Guichandut Head of Development Grameen Crédit

Second and third tier MFIs: Where do we stand? e-mfp Action Group Investors in Tier 2/3 MFIs Presentation: Position Paper N 2 Results and Key Findings Philippe Guichandut Head of Development Grameen Crédit

Social Protection: An Indispensable Tool for a New Social Contract

Social Protection: An Indispensable Tool for a New Social Contract Rethinking Social Protection in the Arab Region Amman, 13-15 May 2014 Isabel Ortiz Director Social Protection Department International

Social Protection: An Indispensable Tool for a New Social Contract Rethinking Social Protection in the Arab Region Amman, 13-15 May 2014 Isabel Ortiz Director Social Protection Department International

THE ADVISORY CENTRE ON WTO LAW

THE ADVISORY CENTRE ON WTO LAW Advisory Centre on WTO Law Centre Consultatif sur la Législation de l OMC Centro de Asesoría Legal en Asuntos de la OMC THE ACWL PROVIDES LEGAL ADVICE AND TRAINING ON ALL

THE ADVISORY CENTRE ON WTO LAW Advisory Centre on WTO Law Centre Consultatif sur la Législation de l OMC Centro de Asesoría Legal en Asuntos de la OMC THE ACWL PROVIDES LEGAL ADVICE AND TRAINING ON ALL

IBRD/IDA and Blend Countries: Per Capita Incomes, Lending Eligibility, IDA Repayment Terms

Page 1 of 7 Note: This OP 3.10, Annex D replaces the version dated September 2013. The revised terms are effective for all loans that are approved on or after July 1, 2014. IBRD/IDA and Blend Countries:

Page 1 of 7 Note: This OP 3.10, Annex D replaces the version dated September 2013. The revised terms are effective for all loans that are approved on or after July 1, 2014. IBRD/IDA and Blend Countries:

Road Maintenance Financing in Sub-Saharan Africa: Reforms and progress towards second generation road funds

Sub-Saharan Africa Transport Policy Program, SSATP Road Maintenance Financing in Sub-Saharan Africa: Reforms and progress towards second generation road funds M. BENMAAMAR, SSATP WB Transport Learning

Sub-Saharan Africa Transport Policy Program, SSATP Road Maintenance Financing in Sub-Saharan Africa: Reforms and progress towards second generation road funds M. BENMAAMAR, SSATP WB Transport Learning

GEF Evaluation Office MID-TERM REVIEW OF THE GEF RESOURCE ALLOCATION FRAMEWORK. Portfolio Analysis and Historical Allocations

GEF Evaluation Office MID-TERM REVIEW OF THE GEF RESOURCE ALLOCATION FRAMEWORK Portfolio Analysis and Historical Allocations Statistical Annex #2 30 October 2008 Midterm Review Contents Table 1: Historical

GEF Evaluation Office MID-TERM REVIEW OF THE GEF RESOURCE ALLOCATION FRAMEWORK Portfolio Analysis and Historical Allocations Statistical Annex #2 30 October 2008 Midterm Review Contents Table 1: Historical

ShockwatchBulletin: Monitoring the impact of the euro zone crisis, China/India slow-down, and energy price shocks on lower-income countries

ShockwatchBulletin: Monitoring the impact of the euro zone crisis, China/India slow-down, and energy price shocks on lower-income countries Isabella Massa DSA Conference London, 3 November 2012 Outline

ShockwatchBulletin: Monitoring the impact of the euro zone crisis, China/India slow-down, and energy price shocks on lower-income countries Isabella Massa DSA Conference London, 3 November 2012 Outline

Legal Indicators for Combining work, family and personal life

Legal Indicators for Combining work, family and personal life Country Africa Algeria 14 100% Angola 3 months 100% Mixed (if necessary, employer tops up social security) Benin 14 100% Mixed (50% Botswana

Legal Indicators for Combining work, family and personal life Country Africa Algeria 14 100% Angola 3 months 100% Mixed (if necessary, employer tops up social security) Benin 14 100% Mixed (50% Botswana

Demographic Trends and the Real Interest Rate

Demographic Trends and the Real Interest Rate Noëmie Lisack, Rana Sajedi, and Gregory Thwaites Discussion by Sebnem Kalemli-Ozcan 1 / 20 What does the paper do? Quantifies the role of demographic change

Demographic Trends and the Real Interest Rate Noëmie Lisack, Rana Sajedi, and Gregory Thwaites Discussion by Sebnem Kalemli-Ozcan 1 / 20 What does the paper do? Quantifies the role of demographic change

AFRICAN DEVELOPMENT FUND. Decentralization Progress Report (Background Paper #4)

") AFRICAN DEVELOPMENT FUND Decentralization Progress Report (Background Paper #4) ADF-XI Replenishment Meeting 14 15 March 2007 Dar-es-salaam, Tanzania 1 1. BACKGROUND 1.1 By Resolutions adopted on 27 September

AFRICAN DEVELOPMENT FUND Decentralization Progress Report (Background Paper #4) ADF-XI Replenishment Meeting 14 15 March 2007 Dar-es-salaam, Tanzania 1 1. BACKGROUND 1.1 By Resolutions adopted on 27 September

The world of CARE. CARE International Member Countries A Australia B Austria C Canada D Denmark. E France F Germany G Japan H Netherlands

Care Facts & Figures 2005 The world of CARE Africa 1 Angola 2 Benin 3 Burundi 4 Cameroon 5 Chad 6 Democratic Republic of Congo 7 Eritrea 8 Ethiopia 9 Ghana 10 Ivory Coast 11 Kenya 12 Lesotho 13 Liberia

Care Facts & Figures 2005 The world of CARE Africa 1 Angola 2 Benin 3 Burundi 4 Cameroon 5 Chad 6 Democratic Republic of Congo 7 Eritrea 8 Ethiopia 9 Ghana 10 Ivory Coast 11 Kenya 12 Lesotho 13 Liberia

EMBARGOED UNTIL GMT 1 AUGUST

2016 Global Breastfeeding Scorecard: Country Scores EMBARGOED UNTIL 00.01 GMT 1 AUGUST Enabling Environment Reporting Practice UN Region Country Donor Funding (USD) Per Live Birth Legal Status of the Code

2016 Global Breastfeeding Scorecard: Country Scores EMBARGOED UNTIL 00.01 GMT 1 AUGUST Enabling Environment Reporting Practice UN Region Country Donor Funding (USD) Per Live Birth Legal Status of the Code

Fiscal Policy Responses in African Countries to the Global Financial Crisis

Fiscal Policy Responses in African Countries to the Global Financial Crisis Sanjeev Gupta Deputy Director Fiscal Affairs Department International Monetary Fund Outline Global economic outlook Growth prospects

Fiscal Policy Responses in African Countries to the Global Financial Crisis Sanjeev Gupta Deputy Director Fiscal Affairs Department International Monetary Fund Outline Global economic outlook Growth prospects

The Concept of Middle Income Countries through a Health Lens

The Concept of Middle Income Countries through a Health Lens INNOVATION AND ACCESS TO MEDICAL TECHNOLOGIES 5 November 2014 David B Evans Director, Health Systems Governance and Financing World Health Organization,

The Concept of Middle Income Countries through a Health Lens INNOVATION AND ACCESS TO MEDICAL TECHNOLOGIES 5 November 2014 David B Evans Director, Health Systems Governance and Financing World Health Organization,

An Introduction to Subnational DeMPA

An Introduction to Subnational DeMPA CEMLA MEXICO CITY MARCH 2013 1. Methodology 2.Links with Lifecycle of a loan 3. Implementation 4. Preliminary Results 2 1 What is the Subnational Debt Management Performance

An Introduction to Subnational DeMPA CEMLA MEXICO CITY MARCH 2013 1. Methodology 2.Links with Lifecycle of a loan 3. Implementation 4. Preliminary Results 2 1 What is the Subnational Debt Management Performance

AFRICAN MINING: POLITICAL RISK OUTLOOK FOR 2017

AFRICAN MINING: POLITICAL RISK OUTLOOK FOR 2017 10 th Annual Investing in African Mining Barnaby Fletcher, Analyst, Control Risks 28 November 2016 www.controlrisks.com Control Risks Group Limited Risk

AFRICAN MINING: POLITICAL RISK OUTLOOK FOR 2017 10 th Annual Investing in African Mining Barnaby Fletcher, Analyst, Control Risks 28 November 2016 www.controlrisks.com Control Risks Group Limited Risk

Senior Leadership Programme (SLP) CATA Commonwealth Association of Tax Administrators

CATA Commonwealth Association of Tax Administrators") Senior Leadership Programme (SLP) CATA Commonwealth Association of Tax Administrators Prospectus 2018 Senior Leadership Programme The Senior Leadership Programme (SLP) is designed to equip senior tax officials

Senior Leadership Programme (SLP) CATA Commonwealth Association of Tax Administrators Prospectus 2018 Senior Leadership Programme The Senior Leadership Programme (SLP) is designed to equip senior tax officials

Financial Inclusion in SADC

Financial Inclusion in SADC Mbabane, Swaziland December 2017 Contents FinMark Trust FinScope as a tool of Financial Inclusion Current FinScope initiatives in SADC FinScope insights MSME Studies in SADC

Financial Inclusion in SADC Mbabane, Swaziland December 2017 Contents FinMark Trust FinScope as a tool of Financial Inclusion Current FinScope initiatives in SADC FinScope insights MSME Studies in SADC

Kentucky Cabinet for Economic Development Office of Workforce, Community Development, and Research

Table 2 Kentucky s Exports to the World -- Inclusive of Year to Date () Values in $ Thousands 2016 Year to Date Total All Countries $ 29,201,010 $ 30,857,275 5.7% $ 20,030,998 $ 20,925,509 4.5% Canada

Table 2 Kentucky s Exports to the World -- Inclusive of Year to Date () Values in $ Thousands 2016 Year to Date Total All Countries $ 29,201,010 $ 30,857,275 5.7% $ 20,030,998 $ 20,925,509 4.5% Canada

ANNEX 2. The following 2016 per capita income guidelines apply for operational purposes:

ANNEX 2 IBRD/IDA and Blend Countries: Per Capita s, Eligibility, and Repayment Terms The financing terms below are effective for all IBRD loans and IDA Financing that are approved by the Executive Directors

ANNEX 2 IBRD/IDA and Blend Countries: Per Capita s, Eligibility, and Repayment Terms The financing terms below are effective for all IBRD loans and IDA Financing that are approved by the Executive Directors

Update on the Integrated Road Map: proposed interim governance arrangements

Integrated Road Map 0 Update on the Integrated Road Map: proposed interim governance arrangements Informal Consultation 7 September 2017 Objective Integrated Road Map The purpose of today s consultation

Integrated Road Map 0 Update on the Integrated Road Map: proposed interim governance arrangements Informal Consultation 7 September 2017 Objective Integrated Road Map The purpose of today s consultation

Fernanda Ruiz Nuñez Senior Economist Infrastructure, PPPs and Guarantees Group The World Bank

Fernanda Ruiz Nuñez Senior Economist Infrastructure, PPPs and Guarantees Group The World Bank Mikel Tejada Consultant. Topic Leader Procuring Infrastructure PPPs The World Bank 2018 ICGFM 32nd Annual International

Fernanda Ruiz Nuñez Senior Economist Infrastructure, PPPs and Guarantees Group The World Bank Mikel Tejada Consultant. Topic Leader Procuring Infrastructure PPPs The World Bank 2018 ICGFM 32nd Annual International

Intellectual Property, Innovation and Transfer of Technology: Implementation of the TRIPS Agreement

United Nations Office of the High Representative for LDCs, LLDCs and SIDS (UN-OHRLLS) Expert Group Meeting on Science, Technology and Innovation for Structural Economic Transformation of Landlocked Developing

United Nations Office of the High Representative for LDCs, LLDCs and SIDS (UN-OHRLLS) Expert Group Meeting on Science, Technology and Innovation for Structural Economic Transformation of Landlocked Developing

IUMI 2018 COMPULSORY CARGO INSURANCE LAW IN AFRICA: OPPORTUNITIES FOR LOCAL PARTNERSHIP. Sory Diomande Africa Re 18 September 2018

IUMI 2018 COMPULSORY CARGO INSURANCE LAW IN AFRICA: OPPORTUNITIES FOR LOCAL PARTNERSHIP Sory Diomande Africa Re 18 September 2018 CONTENT 1. OBJECTIVES OF THE PRESENTATION 2. COMPULSORY CARGO INSURANCE

IUMI 2018 COMPULSORY CARGO INSURANCE LAW IN AFRICA: OPPORTUNITIES FOR LOCAL PARTNERSHIP Sory Diomande Africa Re 18 September 2018 CONTENT 1. OBJECTIVES OF THE PRESENTATION 2. COMPULSORY CARGO INSURANCE

IBRD/IDA and Blend Countries: Per Capita Incomes, Lending Eligibility, and Repayment Terms

Page 1 of 7 (Updated ) Note: This OP 3.10, Annex D replaces the version dated March 2013. The revised terms are effective for all loans for which invitations to negotiate are issued on or after July 1,

Page 1 of 7 (Updated ) Note: This OP 3.10, Annex D replaces the version dated March 2013. The revised terms are effective for all loans for which invitations to negotiate are issued on or after July 1,

Social Protection in times of recovery and transformation

Social Protection in times of recovery and transformation SPIAC-B MEETING Brussels, 29 October 2013 Isabel Ortiz Director Social Protection Department ILO A Time of Recovery and Transformation: Divergent

Social Protection in times of recovery and transformation SPIAC-B MEETING Brussels, 29 October 2013 Isabel Ortiz Director Social Protection Department ILO A Time of Recovery and Transformation: Divergent

Report on Countries That Are Candidates for Millennium Challenge Account Eligibility in Fiscal

This document is scheduled to be published in the Federal Register on 04/09/2012 and available online at http://federalregister.gov/a/2012-08443, and on FDsys.gov BILLING CODE: 921103 MILLENNIUM CHALLENGE

This document is scheduled to be published in the Federal Register on 04/09/2012 and available online at http://federalregister.gov/a/2012-08443, and on FDsys.gov BILLING CODE: 921103 MILLENNIUM CHALLENGE

Innovative Financing for Energy Projects

Innovative Financing for Energy Projects ABOUT COFIDES The Spanish Financing Company for Development, COFIDES, S.A., S.M.E., is a state-owned company incorporated by: ICEX 25,74% ICO BBVA BANCO BANCO BANCO

Innovative Financing for Energy Projects ABOUT COFIDES The Spanish Financing Company for Development, COFIDES, S.A., S.M.E., is a state-owned company incorporated by: ICEX 25,74% ICO BBVA BANCO BANCO BANCO

The Changing Wealth of Nations 2018

The Changing Wealth of Nations 2018 Building a Sustainable Future Editors: Glenn-Marie Lange Quentin Wodon Kevin Carey Wealth accounts available for 141 countries, 1995 to 2014 Market exchange rates Human

The Changing Wealth of Nations 2018 Building a Sustainable Future Editors: Glenn-Marie Lange Quentin Wodon Kevin Carey Wealth accounts available for 141 countries, 1995 to 2014 Market exchange rates Human

Why Corrupt Governments May Receive More Foreign Aid

Why Corrupt Governments May Receive More Foreign Aid David de la Croix Clara Delavallade Online Appendix Appendix A - Extension with Productive Government Spending The time resource constraint is 1 = l

Why Corrupt Governments May Receive More Foreign Aid David de la Croix Clara Delavallade Online Appendix Appendix A - Extension with Productive Government Spending The time resource constraint is 1 = l

The world of CARE. CARE International Member Countries A Australia B Austria C Canada D Denmark. E France F Germany/Luxemburg G Japan H Netherlands

Care Facts & Figures 2007 The world of CARE Africa 1 Angola 2 Benin 3 Burundi 4 Cameroon 5 Chad 6 Democratic Republic of Congo 7 Eritrea 8 Ethiopia 9 Ghana 10 Ivory Coast 11 Kenya 12 Lesotho 13 Madagascar

Care Facts & Figures 2007 The world of CARE Africa 1 Angola 2 Benin 3 Burundi 4 Cameroon 5 Chad 6 Democratic Republic of Congo 7 Eritrea 8 Ethiopia 9 Ghana 10 Ivory Coast 11 Kenya 12 Lesotho 13 Madagascar

The State of the World s Macroeconomy

The State of the World s Macroeconomy Marcelo Giugale Senior Director Global Practice for Macroeconomics & Fiscal Management Washington DC, December 3 rd 2014 Content 1. What s Happening? Growing Concerns

The State of the World s Macroeconomy Marcelo Giugale Senior Director Global Practice for Macroeconomics & Fiscal Management Washington DC, December 3 rd 2014 Content 1. What s Happening? Growing Concerns

SUN Movement Meeting of the Network of Country Focal Points: Report of the 16 th Meeting- 3 rd to 6 th of November 2014

SUN Movement Meeting of the Network of Country Focal Points: Report of the 16 th Meeting- 3 rd to 6 th of November 2014 The 16 th meeting of the SUN Movement Network of Country Focal Points took place

SUN Movement Meeting of the Network of Country Focal Points: Report of the 16 th Meeting- 3 rd to 6 th of November 2014 The 16 th meeting of the SUN Movement Network of Country Focal Points took place

LDC Services Exports and Export Potentials Brainstorming meeting of the LDC Group 3-4 October 2013 WMO, Geneva

LDC Services Exports and Export Potentials Brainstorming meeting of the LDC Group 3-4 October 2013 WMO, Geneva Jane Drake-Brockman Senior Services Adviser What is ITC? 2 ITC is a trade-related technical

LDC Services Exports and Export Potentials Brainstorming meeting of the LDC Group 3-4 October 2013 WMO, Geneva Jane Drake-Brockman Senior Services Adviser What is ITC? 2 ITC is a trade-related technical

Perspectives on Global Development 2012 Social Cohesion in a Shifting World. OECD Development Centre

Perspectives on Global Development 2012 Social Cohesion in a Shifting World OECD Development Centre Perspectives on Global Development Trilogy through the lens of Shifting Wealth: 1. Shifting Wealth 2.

Perspectives on Global Development 2012 Social Cohesion in a Shifting World OECD Development Centre Perspectives on Global Development Trilogy through the lens of Shifting Wealth: 1. Shifting Wealth 2.

GOLD STANDARD Market report 2018

market report 2018 GOLD STANDARD Market report 2018 April 2019 Prepared by Claire Willers Ema Cima 1 MARKET REPORT Table of Contents Executive Summary 3 Gold Standard Project Pipeline 4 Gold Standard Certified

market report 2018 GOLD STANDARD Market report 2018 April 2019 Prepared by Claire Willers Ema Cima 1 MARKET REPORT Table of Contents Executive Summary 3 Gold Standard Project Pipeline 4 Gold Standard Certified

Institutions, Capital Flight and the Resource Curse. Ragnar Torvik Department of Economics Norwegian University of Science and Technology

Institutions, Capital Flight and the Resource Curse Ragnar Torvik Department of Economics Norwegian University of Science and Technology The resource curse Wave 1: Case studies, Gelb (1988) The resource

Institutions, Capital Flight and the Resource Curse Ragnar Torvik Department of Economics Norwegian University of Science and Technology The resource curse Wave 1: Case studies, Gelb (1988) The resource

Tariff regulation. TRAI-APT Workshop on Regulatory Framework. Rohan Samarajiva 7 September 2011

Tariff regulation TRAI-APT Workshop on Regulatory Framework Rohan Samarajiva 7 September 2011 This work was carried out with the aid of a grant from the International Development Research Centre, Canada

Tariff regulation TRAI-APT Workshop on Regulatory Framework Rohan Samarajiva 7 September 2011 This work was carried out with the aid of a grant from the International Development Research Centre, Canada

5 SAVING, CREDIT, AND FINANCIAL RESILIENCE

5 SAVING, CREDIT, AND FINANCIAL RESILIENCE People save for future expenses a large purchase, investments in education or a business, their needs in old age or in possible emergencies. Or, facing more immediate

5 SAVING, CREDIT, AND FINANCIAL RESILIENCE People save for future expenses a large purchase, investments in education or a business, their needs in old age or in possible emergencies. Or, facing more immediate

The world of CARE. CARE International Member Countries A Australia B Austria C Canada D Denmark. E France F Germany/Luxemburg G Japan H Netherlands

Care Facts & Figures 2009 The world of CARE Africa 1 Angola 2 Benin 3 Burundi 4 Cameroon 5 Chad 6 Democratic Republic of Congo 7 Ethiopia 8 Ghana 9 Ivory Coast 10 Kenya 11 Lesotho 12 Liberia 13 Madagascar

Care Facts & Figures 2009 The world of CARE Africa 1 Angola 2 Benin 3 Burundi 4 Cameroon 5 Chad 6 Democratic Republic of Congo 7 Ethiopia 8 Ghana 9 Ivory Coast 10 Kenya 11 Lesotho 12 Liberia 13 Madagascar

Household Debt and Business Cycles Worldwide Out-of-sample results based on IMF s new Global Debt Database

Household Debt and Business Cycles Worldwide Out-of-sample results based on IMF s new Global Debt Database Atif Mian Princeton University and NBER Amir Sufi University of Chicago Booth School of Business

Household Debt and Business Cycles Worldwide Out-of-sample results based on IMF s new Global Debt Database Atif Mian Princeton University and NBER Amir Sufi University of Chicago Booth School of Business

Dutch tax treaty overview Q3, 2012

Dutch tax treaty overview Q3, 2012 Hendrik van Duijn DTS Duijn's Tax Solutions Zuidplein 36 (WTC Tower H) 1077 XV Amsterdam The Netherlands T +31 888 387 669 T +31 888 DTS NOW F +31 88 8 387 601 duijn@duijntax.com

Dutch tax treaty overview Q3, 2012 Hendrik van Duijn DTS Duijn's Tax Solutions Zuidplein 36 (WTC Tower H) 1077 XV Amsterdam The Netherlands T +31 888 387 669 T +31 888 DTS NOW F +31 88 8 387 601 duijn@duijntax.com

IDA13. Measuring Outputs and Outcomes in IDA Countries

IDA13 Measuring Outputs and Outcomes in IDA Countries International Development Association February 2002 Measuring Outputs and Outcomes in IDA Countries Introduction...1 Establishing a Measurement System...2

IDA13 Measuring Outputs and Outcomes in IDA Countries International Development Association February 2002 Measuring Outputs and Outcomes in IDA Countries Introduction...1 Establishing a Measurement System...2

Finexpo s action focuses on financing conditions for credits granted for the supply of equipment and services.

Finexpo is an inter-ministerial advisory committee managed by the Directorate financial support to exports (B2) within the Federal Public Service Foreign Affairs, Foreign Trade and Development Cooperation

Finexpo is an inter-ministerial advisory committee managed by the Directorate financial support to exports (B2) within the Federal Public Service Foreign Affairs, Foreign Trade and Development Cooperation

These notes are circulated for the information of Members with the approval of the Member in charge of the Bill, the Hon W.E. Teare, MHK.

HEAVILY INDEBTED POOR COUNTRIES (LIMITATION ON DEBT RECOVERY) BILL 2012 EXPLANATORY NOTES These notes are circulated for the information of Members with the approval of the Member in charge of the Bill,

HEAVILY INDEBTED POOR COUNTRIES (LIMITATION ON DEBT RECOVERY) BILL 2012 EXPLANATORY NOTES These notes are circulated for the information of Members with the approval of the Member in charge of the Bill,

DOMESTIC CUSTODY & TRADING SERVICES

Pricing Structure DOMESTIC CUSTODY & TRADING SERVICES A flat custody fee of 20bps per account type per year is applicable to all holdings and cash, the custody fee is collected each month but will be capped

Pricing Structure DOMESTIC CUSTODY & TRADING SERVICES A flat custody fee of 20bps per account type per year is applicable to all holdings and cash, the custody fee is collected each month but will be capped

COUNTRY DSA(US$) MAX RES RATE MAX TRV RATE EFFECTIVE DATE OF %

MAX RES RATE MAX TRV RATE EFFECTIVE DATE OF %") MAXIMUM MONTHLY STIPEND RATES FOR FELLOWS AND SCHOLARS IN U.S. DOLLARS FOR COST ESTIMATE COUNTRY DSA(US$) MAX RES RATE MAX TRV RATE EFFECTIVE DATE OF % Afghanistan $165 $1,733 $2,599 1 August 2007 Albania

MAXIMUM MONTHLY STIPEND RATES FOR FELLOWS AND SCHOLARS IN U.S. DOLLARS FOR COST ESTIMATE COUNTRY DSA(US$) MAX RES RATE MAX TRV RATE EFFECTIVE DATE OF % Afghanistan $165 $1,733 $2,599 1 August 2007 Albania

2 Albania Algeria , Andorra

1 Afghanistan LDC 110 80 110 80 219 160 2 Albania 631 460 631 460 1 262 920 3 Algeria 8 628 6,290 8 615 6 280 17 243 12 570 4 Andorra 837 610 837 610 1 674 1 220 5 Angola LDC 316 230 316 230 631 460 6

1 Afghanistan LDC 110 80 110 80 219 160 2 Albania 631 460 631 460 1 262 920 3 Algeria 8 628 6,290 8 615 6 280 17 243 12 570 4 Andorra 837 610 837 610 1 674 1 220 5 Angola LDC 316 230 316 230 631 460 6

Country Documentation Finder

Country Shipper s Export Declaration Commercial Invoice Country Documentation Finder Customs Consular Invoice Certificate of Origin Bill of Lading Insurance Certificate Packing List Import License Afghanistan

Country Shipper s Export Declaration Commercial Invoice Country Documentation Finder Customs Consular Invoice Certificate of Origin Bill of Lading Insurance Certificate Packing List Import License Afghanistan

COUNTRY DSA(US$) MAX RES RATE MAX TRV RATE EFFECTIVE DATE OF %

MAX RES RATE MAX TRV RATE EFFECTIVE DATE OF %") Effective 1 July 2012 Page 1 MAXIMUM MONTHLY STIPEND RATES FOR FELLOWS AND SCHOLARS IN U.S. DOLLARS FOR COST ESTIMATE COUNTRY DSA(US$) MAX RES RATE MAX TRV RATE EFFECTIVE DATE OF % * Afghanistan $188 $1,974

Effective 1 July 2012 Page 1 MAXIMUM MONTHLY STIPEND RATES FOR FELLOWS AND SCHOLARS IN U.S. DOLLARS FOR COST ESTIMATE COUNTRY DSA(US$) MAX RES RATE MAX TRV RATE EFFECTIVE DATE OF % * Afghanistan $188 $1,974

Paying Taxes 2019 Global and Regional Findings: AFRICA

World Bank Group: Indira Chand Phone: +1 202 458 0434 E-mail: ichand@worldbank.org PwC: Sharon O Connor Tel:+1 646 471 2326 E-mail: sharon.m.oconnor@pwc.com Fact sheet Paying Taxes 2019 Global and Regional

World Bank Group: Indira Chand Phone: +1 202 458 0434 E-mail: ichand@worldbank.org PwC: Sharon O Connor Tel:+1 646 471 2326 E-mail: sharon.m.oconnor@pwc.com Fact sheet Paying Taxes 2019 Global and Regional

Mining s contribution to the Dominican Republic

Mining s contribution to the Dominican Republic Global Perspectives on Gold Mining: Evaluating Potential and Constraints UNCSD Ben Peachey, Director - Communications, ICMM 3 May 2011 Overview of presentation

Mining s contribution to the Dominican Republic Global Perspectives on Gold Mining: Evaluating Potential and Constraints UNCSD Ben Peachey, Director - Communications, ICMM 3 May 2011 Overview of presentation

FAQs The DFID Impact Fund (managed by CDC)

") FAQs The DFID Impact Fund (managed by CDC) No. Design Question: General Questions 1 What type of support can the DFID Impact Fund provide to vehicles selected through the Request for Proposals ( RFP )?

FAQs The DFID Impact Fund (managed by CDC) No. Design Question: General Questions 1 What type of support can the DFID Impact Fund provide to vehicles selected through the Request for Proposals ( RFP )?

Afghanistan $135 $608 $911 1 March Albania $144 $2,268 $3,402 1 January Angola $286 $5,148 $7,722 1 January 2003

MAXIMUM MONTHLY STIPEND RATES FOR FELLOWS AND SCHOLARS (IN U.S. DOLLARS FOR COST ESTIMATE) COUNTRY DSA(US$) MAX RES RATE MAX TRV RATE EFFECTIVE DATE OF % Afghanistan $135 $608 $911 1 March 1989 Albania

MAXIMUM MONTHLY STIPEND RATES FOR FELLOWS AND SCHOLARS (IN U.S. DOLLARS FOR COST ESTIMATE) COUNTRY DSA(US$) MAX RES RATE MAX TRV RATE EFFECTIVE DATE OF % Afghanistan $135 $608 $911 1 March 1989 Albania

Capacity Building in Public Financial Management- Key Issues

Capacity Building in Public Financial Management- Key Issues Parminder Brar Financial Management Anchor The World Bank May 2, 2005 Overview 1. Definitions 2. Track record 3. Why is PFM capacity building

Capacity Building in Public Financial Management- Key Issues Parminder Brar Financial Management Anchor The World Bank May 2, 2005 Overview 1. Definitions 2. Track record 3. Why is PFM capacity building

Afghanistan $135 $608 $911 1 March Albania $144 $2,268 $3,402 1 January Algeria $208 $624 $936 1 March 1990

MAXIMUM MONTHLY STIPEND RATES FOR FELLOWS AND SCHOLARS (IN U.S. DOLLARS FOR COST ESTIMATE) COUNTRY DSA(US$) MAX RES RATE MAX TRV RATE EFFECTIVE DATE OF % Afghanistan $135 $608 $911 1 March 1989 Albania

MAXIMUM MONTHLY STIPEND RATES FOR FELLOWS AND SCHOLARS (IN U.S. DOLLARS FOR COST ESTIMATE) COUNTRY DSA(US$) MAX RES RATE MAX TRV RATE EFFECTIVE DATE OF % Afghanistan $135 $608 $911 1 March 1989 Albania