Debt Burdens and the Interest Rate Response to Fiscal Stimulus: Theory and Cross-Country Evidence.

|

|

|

- Olivia Henry

- 6 years ago

- Views:

Transcription

1 Debt Burdens and the Interest Rate Response to Fiscal Stimulus: Theory and Cross-Country Evidence. Jorge Miranda-Pinto 1, Daniel Murphy 2, Kieran Walsh 2, Eric Young 1 1 UVA, 2 UVA Darden School of Business June 9, 2017

2 Government Spending and Interest Rates Theoretical near-consensus: G shocks raise interest rates channel: gov t uses resources, rates rise to clear markets crowds out investment, limiting economic stimulus widely taught; assumed in policy debates

3 Government Spending and Interest Rates: A Puzzle Data: fail to show that government spending increases rates Interest rates in U.S. and U.K. may fall in response to government spending e.g., Barro (1984, 1987), Engen and Hubbard (2004) Evans (1987), Fisher and Peters (2010), Ramey (2011)

4 Government Spending and Interest Rates: A Puzzle Data: fail to show that government spending increases rates Interest rates in U.S. and U.K. may fall in response to government spending e.g., Barro (1984, 1987), Engen and Hubbard (2004) Evans (1987), Fisher and Peters (2010), Ramey (2011) Related empirical puzzle: Fiscal shocks are not associated with exchange rate appreciation Ravn, Schmitt-Grohé, Uribe (2012); Corsetti, Meier, Müller (2012)

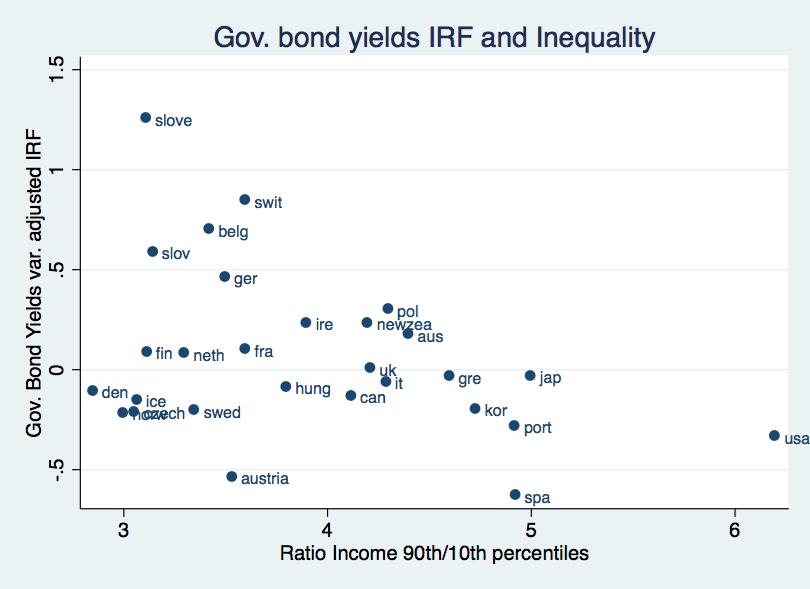

5 This paper: New cross-country evidence We document substantial heterogeneity in the response of interest rates to government spending across OECD countries. government bond yields fall in over half of OECD countries

6 This paper: New cross-country evidence We document substantial heterogeneity in the response of interest rates to government spending across OECD countries. government bond yields fall in over half of OECD countries General Equilibrium models are generally unable to explain negative interest rate responses to fiscal stimulus (IRRFs) Few theoretical explanations for heterogeneity in IRRFs

7 Outline Data and Cross-country variation in IRRFs Theory of debt-burdened households: Government spending increases income for borrowers and relaxes credit markets Borrowers are households with debt overhang: Savings-constrained households due to minimum consumption levels Empirical test using country-level data Examine whether the IRRF depends on theory-implied proxies for debt burdens. Evidence of debt-burdened households from microdata (PSID)

8 Outline Data and Cross-country variation in IRRFs Theory of debt-burdened households: Government spending increases income for borrowers and relaxes credit markets Borrowers are households with debt overhang: Savings-constrained households due to minimum consumption levels Empirical test using country-level data Examine whether the IRRF depends on theory-implied proxies for debt burdens. Evidence of debt-burdened households from microdata (PSID)

9 Outline Data and Cross-country variation in IRRFs Theory of debt-burdened households: Government spending increases income for borrowers and relaxes credit markets Borrowers are households with debt overhang: Savings-constrained households due to minimum consumption levels Empirical test using country-level data Examine whether the IRRF depends on theory-implied proxies for debt burdens. Evidence of debt-burdened households from microdata (PSID)

10 Outline Data and Cross-country variation in IRRFs Theory of debt-burdened households: Government spending increases income for borrowers and relaxes credit markets Borrowers are households with debt overhang: Savings-constrained households due to minimum consumption levels Empirical test using country-level data Examine whether the IRRF depends on theory-implied proxies for debt burdens. Evidence of debt-burdened households from microdata (PSID)

11 Related Literature Sources of heterogeneity in Marginal Propensities to Consume Low-income households may have lower MPCs than high-income households Misra and Surico (2014), Shapiro and Slemrod (2003) Kaplan and Violante (2014) suggest due to liquidity-constrained rich.

12 Related Literature Sources of heterogeneity in Marginal Propensities to Consume Low-income households may have lower MPCs than high-income households Misra and Surico (2014), Shapiro and Slemrod (2003) Kaplan and Violante (2014) suggest due to liquidity-constrained rich. Cross-country differences in effects of fiscal shocks Ilzetzki, Mendoza, Vegh (2013); Corsetti, Meier, Müller (2012) We examine differences in IRRFs rather than output multipliers

13 Related Literature Sources of heterogeneity in Marginal Propensities to Consume Low-income households may have lower MPCs than high-income households Misra and Surico (2014), Shapiro and Slemrod (2003) Kaplan and Violante (2014) suggest due to liquidity-constrained rich. Cross-country differences in effects of fiscal shocks Ilzetzki, Mendoza, Vegh (2013); Corsetti, Meier, Müller (2012) We examine differences in IRRFs rather than output multipliers Exchange Rate Puzzle Ravn, Schmitt-Grohé, Uribe (2012); Corsetti, Meier, Müller (2012)

14 Related Literature State-dependent fiscal effects Auerbach and Gorodnichenko (2012); Bachmann and Sims (2012); Ramey and Zubairy (2017); Demyanyk, Loutskina and Murphy (2016)

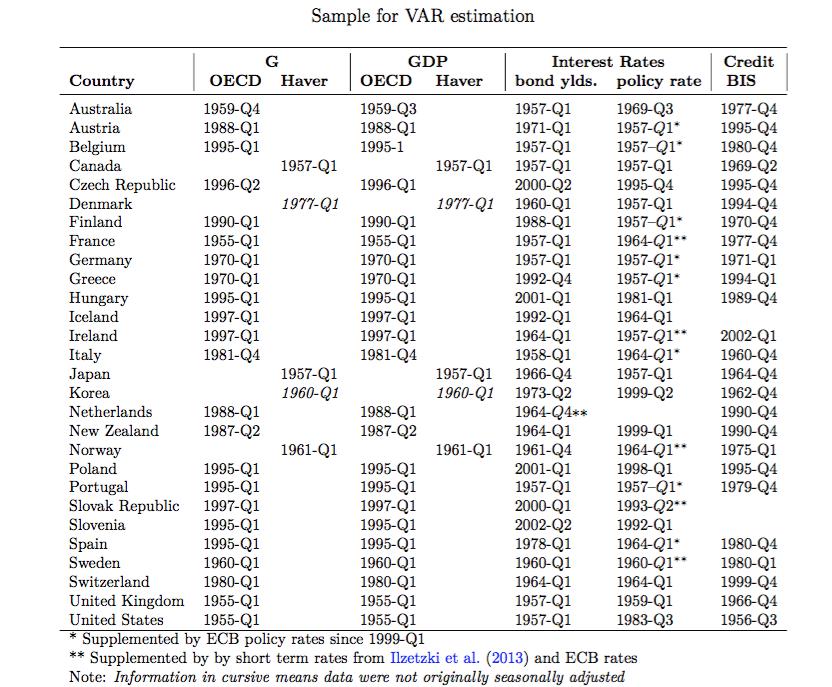

15 Interest Rates Responses to Fiscal Stimulus (IRRF) Data OECD countries Quarterly data on government consumption, real GDP, and interest rates focus on government bond yields when available Data from OECD and Haver. Data Table

16 Interest Rates Responses to Fiscal Stimulus (IRRF) Identifying fiscal shocks X t = [G t, Y t, r t ] ε t = [ ν t, ε 2 t, ε 3 t ] A 0 X t = 4 j=1 A j X t j + ε t, Identifying assumption: government spending is predetermined (within a quarter) with respect to other macro variables Blanchard and Perotti (2002); Auerbach and Gorodnichenko (2012); Ilzetzki, Mendoza, Vegh (2013)

17

18

19 Figure: Cum. 4 qtrs. effect of fiscal shocks on gov. yields OECD Countries

20 Model

21 Model Two agent types, two periods, endowment economy. Non-rich p measure π [1/2, 1) per-period income y p = 1/ (2π) Rich r measure 1 π per-period income y r = 1/ (2 (1 π)) Total income 1 = πy p + (1 π) y r π governs inequality measure of rich agents falls to 0 as π 1

22 Agent i {r, p} solves max c 0,c 1,b {log (c 0) + log (c 1 )} subject to (i) : c 0 + qb = y i + G (ii) : c 1 = y i (1 τ) + b (iii) : c 0 c G [0, 1) is an exogenous wage from the government τ is the marginal tax rate. c is the minimum consumption level

23 Government budget constraint: (1 + ω) G q = τ To pay wages G, ωg must be redirected to unproductive activities. reduced-form for private sector output lost when agents work for the government.

24 Equilibrium Equilibrium consists of a bond price, agent consumption, and taxes such that bond and goods markets clear and the government budget constraint is satisfied. With minimum consumption constraint binding for non-rich q = 3 4πc + (2π 1 3ω) G Response of interest rate R = 1 q to G may be positive or negative IRRF is strictly decreasing in inequality π 2 R G π < 0.

25 Equilibrium Equilibrium consists of a bond price, agent consumption, and taxes such that bond and goods markets clear and the government budget constraint is satisfied. With minimum consumption constraint binding for non-rich q = 3 4πc + (2π 1 3ω) G Response of interest rate R = 1 q to G may be positive or negative IRRF is strictly decreasing in inequality π 2 R G π < 0. Without minimum consumption constraint q = 1 ωg

26 Savings constraints and G in a Huggett (1993) Model Large number of agents, t = 0, 1,... Individual endowment y s depends on the realization of an S state Markov process with transition matrix Π = {π ss } s,s S agents can partially insure with bonds (a) V (a, s) = max c,a {u(c) λ[c c] + + β E s [V (a, s )]} subject to c + qa = y s (1 τ) + a + G a a. Steady-state equilibrium: r = 1/q 1 and wealth dist. constant over time Markets clear: a i di = 0 Gov t budget constraint holds: G w (1 + ω) = τ y i di.

27

28

29

30

31 Cross-Country Evidence: Cross-section Data on country-level determinants of the IRRF Inequality: ratio of income of richest 10 percent to income of poorest 10 percent (OECD) Central Bank Independence Index from Dincer and Eichengreen (2014) available for only 14 countries Use inflation volatility as proxy (Alesina and Summers 1993) Financial openness index from Lane and Milesi-Ferretti (2007): (financial assets plus liabilities)/gdp Output Multipliers (from VAR estimates)

32

33 Table: IRRF and Country Characteristics (1) (2) (3) (4) VARIABLES Bond IRRF Bond IRRF Bond IRRF Bond IRRF p ** -0.16** -0.15* -0.16* (0.08) (0.08) (0.08) (0.09) St. Dev. Inflation (0.10) (0.11) (0.10) Financial Openness (0.03) (0.03) Fiscal Mult. 4 qtrs (0.22) Constant 0.78* (0.38) (0.37) (0.38) (0.44) Observations R-squared

34 Is Monetary Policy Responding to G?

35 Is Monetary Policy Responding to G? Government Spending 3 Month Tbill rate quarter quarter 20 real baa bond rate 0.4 real Money Base quarter quarter IRRF, Ramey s Defense News Shocks (U.S. 1939Q1-2008Q4), MW (2016)

36 Is Monetary Policy Responding to G? IRRF, VAR G Shock (U.S. 1983Q1-2007Q4), MW (2016)

37 Is Monetary Policy Responding to G? Impulse Responses of Spreads (over the FFR target) to VAR Gov t Spending Shocks (1983Q1-2007Q4), MW (2016)

38 Cross-Country Evidence: Panel Data Model prediction: The IRRF is falling in debt overhang Use lagged country-level consumer credit (BIS) as a proxy for debt overhang Spread it =α i + δ t + γ 0 G shock it + γ 2 Credit it 1 +γ 3 G shock it Credit it 1 + γx it 1 + ɛ it.

39

40 Evidence from U.S. microdata PSID Biennial panel data Data on consumption starting in 1999 Data on medical debt 2011, 2013

41 Table: Summary Statistics N Mean Households: Has Expenditure Shock 7, Has Income Shock and Lagged Expenditure Shock 7, Households-time observations: Has Expenditure Shock 59, Has Income Shock and Lagged Expenditure Shock 59, * Note: A household has high income ( expenditure) in periods in which income ( expenditure) is over a standard deviation above average income (health expenditure) for the household.

42 Dependent variable: Log consumption VARIABLES (1) (2) (3) All < Median Wealth > Median Wealth High Income 0.275*** 0.313*** 0.235*** (0.007) (0.011) (0.010) L1. High Consumption * (0.008) (0.014) (0.009) L2. High Consumption *** *** *** (0.009) (0.016) (0.010) L1. High Cons High Income *** ** (0.015) (0.023) (0.019) L2. High Cons High Income ** (0.018) (0.026) (0.026) Observations 44,850 22,428 22,422 R-squared Indiv. and Time FE Yes Yes Yes * Note: A household has high income (consumption) in periods in which income (consumption) is over a standard deviation above average income (consumption) for the household. All regressions control for household wealth, income, and the age of the head of the household. Robust standard errors in parentheses, clustered at the household level. *** p<0.01, ** p<0.05.

43 Conclusion New cross-country stylized fact: IRRF is negative in half of OECD countries. Theory IRRF depends on fraction of debt-burdened households. New explanation for heterogeneous MPCs. Evidence of theory s mechanisms Microdata: low-wealth households behave as predicted by model. Aggregate data: IRRF depends on inequality and consumer credit

44 back

Debt Burdens and the Interest Rate Response to Fiscal Stimulus: Theory and Cross-Country Evidence (Preliminary and Incomplete*)

") Debt Burdens and the Interest Rate Response to Fiscal Stimulus: Theory and Cross-Country Evidence (Preliminary and Incomplete*) Jorge Miranda-Pinto 1, Daniel Murphy 2, Kieran James Walsh 3, and Eric R.

Debt Burdens and the Interest Rate Response to Fiscal Stimulus: Theory and Cross-Country Evidence (Preliminary and Incomplete*) Jorge Miranda-Pinto 1, Daniel Murphy 2, Kieran James Walsh 3, and Eric R.

Saving Constraints, Debt, and the Credit Market Response to Fiscal Stimulus: Theory and Cross-Country Evidence

Saving Constraints, Debt, and the Credit Market Response to Fiscal Stimulus: Theory and Cross-Country Evidence Jorge Miranda-Pinto 1, Daniel Murphy 2, Kieran James Walsh 3, and Eric R. Young 4 1 University

Saving Constraints, Debt, and the Credit Market Response to Fiscal Stimulus: Theory and Cross-Country Evidence Jorge Miranda-Pinto 1, Daniel Murphy 2, Kieran James Walsh 3, and Eric R. Young 4 1 University

What determines government spending multipliers?

What determines government spending multipliers? Paper by Giancarlo Corsetti, André Meier and Gernot J. Müller Presented by Michele Andreolli 12 May 2014 Outline Overview Empirical strategy Results Remarks

What determines government spending multipliers? Paper by Giancarlo Corsetti, André Meier and Gernot J. Müller Presented by Michele Andreolli 12 May 2014 Outline Overview Empirical strategy Results Remarks

Spending Shocks and Interest Rates

Spending Shocks and Interest Rates Daniel Murphy University of Virginia Darden School of Business Kieran James Walsh University of Virginia Darden School of Business April 1, 2016 Abstract Most macroeconomic

Spending Shocks and Interest Rates Daniel Murphy University of Virginia Darden School of Business Kieran James Walsh University of Virginia Darden School of Business April 1, 2016 Abstract Most macroeconomic

Fiscal Multipliers in Recessions

Fiscal Multipliers in Recessions Matthew Canzoneri Fabrice Collard Harris Dellas Behzad Diba March 10, 2015 Matthew Canzoneri Fabrice Collard Harris Dellas Fiscal Behzad Multipliers Diba (University in

Fiscal Multipliers in Recessions Matthew Canzoneri Fabrice Collard Harris Dellas Behzad Diba March 10, 2015 Matthew Canzoneri Fabrice Collard Harris Dellas Fiscal Behzad Multipliers Diba (University in

Discussion of Corsetti, Meyer and Muller, What Determines Government Spending Multipliers?

Discussion of Corsetti, Meyer and Muller, What Determines Government Spending Multipliers? Michael Woodford Columbia University Federal Reserve Bank of New York June 3, 2010 Woodford (Columbia) Corsetti

Discussion of Corsetti, Meyer and Muller, What Determines Government Spending Multipliers? Michael Woodford Columbia University Federal Reserve Bank of New York June 3, 2010 Woodford (Columbia) Corsetti

International Debt Deleveraging

International Debt Deleveraging Luca Fornaro London School of Economics ECB-Bank of Canada joint workshop on Exchange Rates Frankfurt, June 213 1 Motivating facts: Household debt/gdp Household debt/gdp

International Debt Deleveraging Luca Fornaro London School of Economics ECB-Bank of Canada joint workshop on Exchange Rates Frankfurt, June 213 1 Motivating facts: Household debt/gdp Household debt/gdp

Tax Cuts for Whom? Heterogeneous Effects of Income Tax Changes on Growth & Employment

Tax Cuts for Whom? Heterogeneous Effects of Income Tax Changes on Growth & Employment Owen Zidar University of California, Berkeley ozidar@econ.berkeley.edu October 1, 2012 Owen Zidar (UC Berkeley) Tax

Tax Cuts for Whom? Heterogeneous Effects of Income Tax Changes on Growth & Employment Owen Zidar University of California, Berkeley ozidar@econ.berkeley.edu October 1, 2012 Owen Zidar (UC Berkeley) Tax

The Effects of Government Spending on Real Exchange Rates: Evidence from Military Spending Panel Data

No. 16-14 The Effects of Government Spending on Real Exchange Rates: Evidence from Military Spending Panel Data Wataru Miyamoto, Thuy Lan Nguyen, and Viacheslav Sheremirov Abstract: Using panel data on

No. 16-14 The Effects of Government Spending on Real Exchange Rates: Evidence from Military Spending Panel Data Wataru Miyamoto, Thuy Lan Nguyen, and Viacheslav Sheremirov Abstract: Using panel data on

Gernot Müller (University of Bonn, CEPR, and Ifo)

") Exchange rate regimes and fiscal multipliers Benjamin Born (Ifo Institute) Falko Jüßen (TU Dortmund and IZA) Gernot Müller (University of Bonn, CEPR, and Ifo) Fiscal Policy in the Aftermath of the Financial

Exchange rate regimes and fiscal multipliers Benjamin Born (Ifo Institute) Falko Jüßen (TU Dortmund and IZA) Gernot Müller (University of Bonn, CEPR, and Ifo) Fiscal Policy in the Aftermath of the Financial

Household Heterogeneity in Macroeconomics

Household Heterogeneity in Macroeconomics Department of Economics HKUST August 7, 2018 Household Heterogeneity in Macroeconomics 1 / 48 Reference Krueger, Dirk, Kurt Mitman, and Fabrizio Perri. Macroeconomics

Household Heterogeneity in Macroeconomics Department of Economics HKUST August 7, 2018 Household Heterogeneity in Macroeconomics 1 / 48 Reference Krueger, Dirk, Kurt Mitman, and Fabrizio Perri. Macroeconomics

Fiscal Multipliers in Recessions. M. Canzoneri, F. Collard, H. Dellas and B. Diba

1 / 52 Fiscal Multipliers in Recessions M. Canzoneri, F. Collard, H. Dellas and B. Diba 2 / 52 Policy Practice Motivation Standard policy practice: Fiscal expansions during recessions as a means of stimulating

1 / 52 Fiscal Multipliers in Recessions M. Canzoneri, F. Collard, H. Dellas and B. Diba 2 / 52 Policy Practice Motivation Standard policy practice: Fiscal expansions during recessions as a means of stimulating

Effects of Fiscal Shocks in a Globalized World

Effects of Fiscal Shocks in a Globalized World by Alan Auerbach and Yuriy Gorodnichenko Discussion by Christopher Erceg Federal Reserve Board November 2014 These comments should not be interpreted as reflecting

Effects of Fiscal Shocks in a Globalized World by Alan Auerbach and Yuriy Gorodnichenko Discussion by Christopher Erceg Federal Reserve Board November 2014 These comments should not be interpreted as reflecting

Explaining Consumption Excess Sensitivity with Near-Rationality:

Explaining Consumption Excess Sensitivity with Near-Rationality: Evidence from Large Predetermined Payments Lorenz Kueng Northwestern University and NBER Motivation: understanding consumption is important

Explaining Consumption Excess Sensitivity with Near-Rationality: Evidence from Large Predetermined Payments Lorenz Kueng Northwestern University and NBER Motivation: understanding consumption is important

Country Spreads as Credit Constraints in Emerging Economy Business Cycles

Conférence organisée par la Chaire des Amériques et le Centre d Economie de la Sorbonne, Université Paris I Country Spreads as Credit Constraints in Emerging Economy Business Cycles Sarquis J. B. Sarquis

Conférence organisée par la Chaire des Amériques et le Centre d Economie de la Sorbonne, Université Paris I Country Spreads as Credit Constraints in Emerging Economy Business Cycles Sarquis J. B. Sarquis

LECTURE 5 The Effects of Fiscal Changes: Aggregate Evidence. September 19, 2018

Economics 210c/236a Fall 2018 Christina Romer David Romer LECTURE 5 The Effects of Fiscal Changes: Aggregate Evidence September 19, 2018 I. INTRODUCTION Theoretical Considerations (I) A traditional Keynesian

Economics 210c/236a Fall 2018 Christina Romer David Romer LECTURE 5 The Effects of Fiscal Changes: Aggregate Evidence September 19, 2018 I. INTRODUCTION Theoretical Considerations (I) A traditional Keynesian

State Dependency of Monetary Policy: The Refinancing Channel

State Dependency of Monetary Policy: The Refinancing Channel Martin Eichenbaum, Sergio Rebelo, and Arlene Wong May 2018 Motivation In the US, bulk of household borrowing is in fixed rate mortgages with

State Dependency of Monetary Policy: The Refinancing Channel Martin Eichenbaum, Sergio Rebelo, and Arlene Wong May 2018 Motivation In the US, bulk of household borrowing is in fixed rate mortgages with

Taxing Firms Facing Financial Frictions

Taxing Firms Facing Financial Frictions Daniel Wills 1 Gustavo Camilo 2 1 Universidad de los Andes 2 Cornerstone November 11, 2017 NTA 2017 Conference Corporate income is often taxed at different sources

Taxing Firms Facing Financial Frictions Daniel Wills 1 Gustavo Camilo 2 1 Universidad de los Andes 2 Cornerstone November 11, 2017 NTA 2017 Conference Corporate income is often taxed at different sources

Keynesian Views On The Fiscal Multiplier

Faculty of Social Sciences Jeppe Druedahl (Ph.d. Student) Department of Economics 16th of December 2013 Slide 1/29 Outline 1 2 3 4 5 16th of December 2013 Slide 2/29 The For Today 1 Some 2 A Benchmark

Faculty of Social Sciences Jeppe Druedahl (Ph.d. Student) Department of Economics 16th of December 2013 Slide 1/29 Outline 1 2 3 4 5 16th of December 2013 Slide 2/29 The For Today 1 Some 2 A Benchmark

Day 4. Redistributive and macro effects of fiscal stimulus policies

Day 4 Redistributive and macro effects of fiscal stimulus policies Gianluca Violante New York University Mini-Course on Policy in Models with Heterogeneous Agents Bank of Portugal, June 15-19, 2105 p.

Day 4 Redistributive and macro effects of fiscal stimulus policies Gianluca Violante New York University Mini-Course on Policy in Models with Heterogeneous Agents Bank of Portugal, June 15-19, 2105 p.

Government Spending Multipliers in Good Times and in Bad: Evidence from U.S. Historical Data

Government Spending Multipliers in Good Times and in Bad: Evidence from U.S. Historical Data Valerie A. Ramey University of California, San Diego and NBER and Sarah Zubairy Texas A&M April 2015 Do Multipliers

Government Spending Multipliers in Good Times and in Bad: Evidence from U.S. Historical Data Valerie A. Ramey University of California, San Diego and NBER and Sarah Zubairy Texas A&M April 2015 Do Multipliers

Inflation Dynamics During the Financial Crisis

Inflation Dynamics During the Financial Crisis S. Gilchrist 1 1 Boston University and NBER MFM Summer Camp June 12, 2016 DISCLAIMER: The views expressed are solely the responsibility of the authors and

Inflation Dynamics During the Financial Crisis S. Gilchrist 1 1 Boston University and NBER MFM Summer Camp June 12, 2016 DISCLAIMER: The views expressed are solely the responsibility of the authors and

FISCAL STIMULUS AND CONSUMER DEBT

FISCAL STIMULUS AND CONSUMER DEBT 1 by Yuliya Demyanyk Federal Reserve Bank of Cleveland & Elena Loutskina, Daniel Murphy University of Virginia, Darden School of Business August 9, 2016 Abstract In the

FISCAL STIMULUS AND CONSUMER DEBT 1 by Yuliya Demyanyk Federal Reserve Bank of Cleveland & Elena Loutskina, Daniel Murphy University of Virginia, Darden School of Business August 9, 2016 Abstract In the

Does the Social Safety Net Improve Welfare? A Dynamic General Equilibrium Analysis

Does the Social Safety Net Improve Welfare? A Dynamic General Equilibrium Analysis University of Western Ontario February 2013 Question Main Question: what is the welfare cost/gain of US social safety

Does the Social Safety Net Improve Welfare? A Dynamic General Equilibrium Analysis University of Western Ontario February 2013 Question Main Question: what is the welfare cost/gain of US social safety

Optimal Credit Market Policy. CEF 2018, Milan

Optimal Credit Market Policy Matteo Iacoviello 1 Ricardo Nunes 2 Andrea Prestipino 1 1 Federal Reserve Board 2 University of Surrey CEF 218, Milan June 2, 218 Disclaimer: The views expressed are solely

Optimal Credit Market Policy Matteo Iacoviello 1 Ricardo Nunes 2 Andrea Prestipino 1 1 Federal Reserve Board 2 University of Surrey CEF 218, Milan June 2, 218 Disclaimer: The views expressed are solely

Government spending and firms dynamics

Government spending and firms dynamics Pedro Brinca Nova SBE Miguel Homem Ferreira Nova SBE December 2nd, 2016 Francesco Franco Nova SBE Abstract Using firm level data and government demand by firm we

Government spending and firms dynamics Pedro Brinca Nova SBE Miguel Homem Ferreira Nova SBE December 2nd, 2016 Francesco Franco Nova SBE Abstract Using firm level data and government demand by firm we

The Heterogeneous Effects of Government. Spending: It s All About Taxes

The Heterogeneous Effects of Government Spending: It s All About Taxes Axelle Ferriere and Gaston Navarro New York University February 214 Abstract Empirical work suggests that while government spending

The Heterogeneous Effects of Government Spending: It s All About Taxes Axelle Ferriere and Gaston Navarro New York University February 214 Abstract Empirical work suggests that while government spending

Tax Cuts for Whom? Heterogeneous Effects of Income Tax Changes on Growth and Employment

Tax Cuts for Whom? Heterogeneous Effects of Income Tax Changes on Growth and Employment Owen Zidar Chicago Booth and NBER December 1, 2014 Owen Zidar (Chicago Booth) Tax Cuts for Whom? December 1, 2014

Tax Cuts for Whom? Heterogeneous Effects of Income Tax Changes on Growth and Employment Owen Zidar Chicago Booth and NBER December 1, 2014 Owen Zidar (Chicago Booth) Tax Cuts for Whom? December 1, 2014

Fiscal Multipliers: Lessons from the Great Recession for Small Open Economies

Fiscal Multipliers: Lessons from the Great Recession for Small Open Economies Giancarlo Corsetti (Cambridge & CEPR) Gernot Müller (Bonn & CEPR) Stockholm June 8, 2016 Swedish Fiscal Policy Council 1. Introduction

Fiscal Multipliers: Lessons from the Great Recession for Small Open Economies Giancarlo Corsetti (Cambridge & CEPR) Gernot Müller (Bonn & CEPR) Stockholm June 8, 2016 Swedish Fiscal Policy Council 1. Introduction

Online Appendix for The Heterogeneous Responses of Consumption between Poor and Rich to Government Spending Shocks

Online Appendix for The Heterogeneous Responses of Consumption between Poor and Rich to Government Spending Shocks Eunseong Ma September 27, 218 Department of Economics, Texas A&M University, College Station,

Online Appendix for The Heterogeneous Responses of Consumption between Poor and Rich to Government Spending Shocks Eunseong Ma September 27, 218 Department of Economics, Texas A&M University, College Station,

Interest Rate Peg. Rong Li and Xiaohui Tian. January Abstract. This paper revisits the sizes of fiscal multipliers under a pegged nominal

Spending Reversals and Fiscal Multipliers under an Interest Rate Peg Rong Li and Xiaohui Tian January 2015 Abstract This paper revisits the sizes of fiscal multipliers under a pegged nominal interest rate.

Spending Reversals and Fiscal Multipliers under an Interest Rate Peg Rong Li and Xiaohui Tian January 2015 Abstract This paper revisits the sizes of fiscal multipliers under a pegged nominal interest rate.

Exchange rate regimes and fiscal multipliers

Exchange rate regimes and fiscal multipliers Benjamin Born, Falko Jüßen, and Gernot J. Müller February 27, 22 Abstract Does the fiscal multiplier depend on the exchange rate regime and, if so, how strongly?

Exchange rate regimes and fiscal multipliers Benjamin Born, Falko Jüßen, and Gernot J. Müller February 27, 22 Abstract Does the fiscal multiplier depend on the exchange rate regime and, if so, how strongly?

THE EFFECTS OF GOVERNMENT SPENDING ON REAL EXCHANGE RATES: EVIDENCE FROM MILITARY SPENDING PANEL DATA

THE EFFECTS OF GOVERNMENT SPENDING ON REAL EXCHANGE RATES: EVIDENCE FROM MILITARY SPENDING PANEL DATA Wataru Miyamoto Bank of Canada Thuy Lan Nguyen Santa Clara University Viacheslav Sheremirov Boston

THE EFFECTS OF GOVERNMENT SPENDING ON REAL EXCHANGE RATES: EVIDENCE FROM MILITARY SPENDING PANEL DATA Wataru Miyamoto Bank of Canada Thuy Lan Nguyen Santa Clara University Viacheslav Sheremirov Boston

5. STRUCTURAL VAR: APPLICATIONS

5. STRUCTURAL VAR: APPLICATIONS 1 1 Monetary Policy Shocks (Christiano Eichenbaum and Evans, 1998) Monetary policy shocks is the unexpected part of the equation for the monetary policy instrument (S t

5. STRUCTURAL VAR: APPLICATIONS 1 1 Monetary Policy Shocks (Christiano Eichenbaum and Evans, 1998) Monetary policy shocks is the unexpected part of the equation for the monetary policy instrument (S t

Fiscal Policy and MPC Heterogeneity

Fiscal Policy and MPC Heterogeneity by Tullio Jappelli and Luigi Pistaferri Discussion by: Fabrizio Perri Bocconi, Minneapolis Fed, IGIER & NBER Macroeconomic Dynamics with Heterogeneous Agents, June 2013

Fiscal Policy and MPC Heterogeneity by Tullio Jappelli and Luigi Pistaferri Discussion by: Fabrizio Perri Bocconi, Minneapolis Fed, IGIER & NBER Macroeconomic Dynamics with Heterogeneous Agents, June 2013

Estimating the Economic Impacts of Highway Infrastructure

Estimating the Economic Impacts of Highway Infrastructure Daniel Wilson (Federal Reserve Bank of San Francisco) Infrastructure and Economic Growth, FRB Chicago, Nov. 3, 2014 *The views expressed in this

Estimating the Economic Impacts of Highway Infrastructure Daniel Wilson (Federal Reserve Bank of San Francisco) Infrastructure and Economic Growth, FRB Chicago, Nov. 3, 2014 *The views expressed in this

Estimating the effects of fiscal policy in Structural VAR models

Estimating the effects of fiscal policy in Structural VAR models Hilde C. Bjørnland BI Norwegian Business School Modell-og metodeutvalget, Finansdepartementet 3 June, 2013 HCB (BI) Fiscal policy FinDep

Estimating the effects of fiscal policy in Structural VAR models Hilde C. Bjørnland BI Norwegian Business School Modell-og metodeutvalget, Finansdepartementet 3 June, 2013 HCB (BI) Fiscal policy FinDep

The Heterogeneous Effects of Government Spending: It s All About Taxes

The Heterogeneous Effects of Government Spending: It s All About Taxes Axelle Ferriere and Gaston Navarro April 217 Abstract How expansionary is government spending? We revisit this classic question by

The Heterogeneous Effects of Government Spending: It s All About Taxes Axelle Ferriere and Gaston Navarro April 217 Abstract How expansionary is government spending? We revisit this classic question by

Question 1 Consider an economy populated by a continuum of measure one of consumers whose preferences are defined by the utility function:

Question 1 Consider an economy populated by a continuum of measure one of consumers whose preferences are defined by the utility function: β t log(c t ), where C t is consumption and the parameter β satisfies

Question 1 Consider an economy populated by a continuum of measure one of consumers whose preferences are defined by the utility function: β t log(c t ), where C t is consumption and the parameter β satisfies

Convergence of Life Expectancy and Living Standards in the World

Convergence of Life Expectancy and Living Standards in the World Kenichi Ueda* *The University of Tokyo PRI-ADBI Joint Workshop January 13, 2017 The views are those of the author and should not be attributed

Convergence of Life Expectancy and Living Standards in the World Kenichi Ueda* *The University of Tokyo PRI-ADBI Joint Workshop January 13, 2017 The views are those of the author and should not be attributed

Balance Sheet Recessions

Balance Sheet Recessions Zhen Huo and José-Víctor Ríos-Rull University of Minnesota Federal Reserve Bank of Minneapolis CAERP CEPR NBER Conference on Money Credit and Financial Frictions Huo & Ríos-Rull

Balance Sheet Recessions Zhen Huo and José-Víctor Ríos-Rull University of Minnesota Federal Reserve Bank of Minneapolis CAERP CEPR NBER Conference on Money Credit and Financial Frictions Huo & Ríos-Rull

A MODEL OF SECULAR STAGNATION

A MODEL OF SECULAR STAGNATION Gauti B. Eggertsson and Neil R. Mehrotra Brown University BIS Research Meetings March 11, 2015 1 / 38 SECULAR STAGNATION HYPOTHESIS I wonder if a set of older ideas... under

A MODEL OF SECULAR STAGNATION Gauti B. Eggertsson and Neil R. Mehrotra Brown University BIS Research Meetings March 11, 2015 1 / 38 SECULAR STAGNATION HYPOTHESIS I wonder if a set of older ideas... under

The Heterogeneous Effects of Government Spending: It s All About Taxes

The Heterogeneous Effects of Government Spending: It s All About Taxes Axelle Ferriere and Gaston Navarro February 217 Abstract Empirical work suggests that government spending generates large expansions

The Heterogeneous Effects of Government Spending: It s All About Taxes Axelle Ferriere and Gaston Navarro February 217 Abstract Empirical work suggests that government spending generates large expansions

The Heterogeneous Effects of Government Spending: It s All About Taxes

The Heterogeneous Effects of Government Spending: It s All About Taxes Axelle Ferriere and Gaston Navarro February 216 Abstract Empirical work suggests that government spending generates large expansions

The Heterogeneous Effects of Government Spending: It s All About Taxes Axelle Ferriere and Gaston Navarro February 216 Abstract Empirical work suggests that government spending generates large expansions

Exchange rate regimes and fiscal multipliers

Exchange rate regimes and fiscal multipliers Benjamin Born, Falko Jüßen, and Gernot J. Müller May 4, 22 Abstract Does the fiscal multiplier depend on the exchange rate regime and, if so, how strongly?

Exchange rate regimes and fiscal multipliers Benjamin Born, Falko Jüßen, and Gernot J. Müller May 4, 22 Abstract Does the fiscal multiplier depend on the exchange rate regime and, if so, how strongly?

Tax multipliers: Pitfalls in measurement and identi cation

Tax multipliers: Pitfalls in measurement and identi cation Daniel Riera-Crichton Bates College Carlos Vegh Univ. of Maryland and NBER Guillermo Vuletin Colby College Indiana University April 25, 2013 Riera-Vegh-Vuletin

Tax multipliers: Pitfalls in measurement and identi cation Daniel Riera-Crichton Bates College Carlos Vegh Univ. of Maryland and NBER Guillermo Vuletin Colby College Indiana University April 25, 2013 Riera-Vegh-Vuletin

Convergence, capital accumulation and the nominal exchange rate

Convergence, capital accumulation and the nominal exchange rate Péter Benczúr and István Kónya Magyar Nemzeti Bank and Central European University September 2 Disclaimer The views expressed are those of

Convergence, capital accumulation and the nominal exchange rate Péter Benczúr and István Kónya Magyar Nemzeti Bank and Central European University September 2 Disclaimer The views expressed are those of

How Big (Small) Are Fiscal Multipliers?

Are Fiscal Multipliers?") How Big (Small) Are Fiscal Multipliers? Comments Antonio Fatás INSEAD Fiscal Policy, Stabilization and Sustainability Conference Florence June 6, 2011 Fiscal Multipliers Key policy question Large academic

How Big (Small) Are Fiscal Multipliers? Comments Antonio Fatás INSEAD Fiscal Policy, Stabilization and Sustainability Conference Florence June 6, 2011 Fiscal Multipliers Key policy question Large academic

Can tax cuts restore economic growth in bad times?

Can tax cuts restore economic growth in bad times? Alex Ziegenbein Universitat Pompeu Fabra & Barcelona GSE SAEe December 14, 217 Background Tax cuts often implemented to bring output back to potential

Can tax cuts restore economic growth in bad times? Alex Ziegenbein Universitat Pompeu Fabra & Barcelona GSE SAEe December 14, 217 Background Tax cuts often implemented to bring output back to potential

Idiosyncratic risk, insurance, and aggregate consumption dynamics: a likelihood perspective

Idiosyncratic risk, insurance, and aggregate consumption dynamics: a likelihood perspective Alisdair McKay Boston University June 2013 Microeconomic evidence on insurance - Consumption responds to idiosyncratic

Idiosyncratic risk, insurance, and aggregate consumption dynamics: a likelihood perspective Alisdair McKay Boston University June 2013 Microeconomic evidence on insurance - Consumption responds to idiosyncratic

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics. Ph. D. Comprehensive Examination: Macroeconomics Spring, 2009

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Comprehensive Examination: Macroeconomics Spring, 2009 Section 1. (Suggested Time: 45 Minutes) For 3 of the following 6 statements,

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Comprehensive Examination: Macroeconomics Spring, 2009 Section 1. (Suggested Time: 45 Minutes) For 3 of the following 6 statements,

A MODEL OF SECULAR STAGNATION

A MODEL OF SECULAR STAGNATION Gauti B. Eggertsson and Neil R. Mehrotra Brown University Princeton February, 2015 1 / 35 SECULAR STAGNATION HYPOTHESIS I wonder if a set of older ideas... under the phrase

A MODEL OF SECULAR STAGNATION Gauti B. Eggertsson and Neil R. Mehrotra Brown University Princeton February, 2015 1 / 35 SECULAR STAGNATION HYPOTHESIS I wonder if a set of older ideas... under the phrase

Sang-Wook (Stanley) Cho

Cho") Beggar-thy-parents? A Lifecycle Model of Intergenerational Altruism Sang-Wook (Stanley) Cho University of New South Wales, Sydney July 2009, CEF Conference Motivation & Question Since Becker (1974), several

Beggar-thy-parents? A Lifecycle Model of Intergenerational Altruism Sang-Wook (Stanley) Cho University of New South Wales, Sydney July 2009, CEF Conference Motivation & Question Since Becker (1974), several

Country Spreads and Emerging Countries: Who Drives Whom? Martin Uribe and Vivian Yue (JIE, 2006)

") Country Spreads and Emerging Countries: Who Drives Whom? Martin Uribe and Vivian Yue (JIE, 26) Country Interest Rates and Output in Seven Emerging Countries Argentina Brazil.5.5...5.5.5. 94 95 96 97 98

Country Spreads and Emerging Countries: Who Drives Whom? Martin Uribe and Vivian Yue (JIE, 26) Country Interest Rates and Output in Seven Emerging Countries Argentina Brazil.5.5...5.5.5. 94 95 96 97 98

The design of the funding scheme of social security systems and its role in macroeconomic stabilization

The design of the funding scheme of social security systems and its role in macroeconomic stabilization Simon Voigts (work in progress) SFB 649 Motzen conference 214 Overview 1 Motivation and results 2

The design of the funding scheme of social security systems and its role in macroeconomic stabilization Simon Voigts (work in progress) SFB 649 Motzen conference 214 Overview 1 Motivation and results 2

Discussion of Optimal Monetary Policy and Fiscal Policy Interaction in a Non-Ricardian Economy

Discussion of Optimal Monetary Policy and Fiscal Policy Interaction in a Non-Ricardian Economy Johannes Wieland University of California, San Diego and NBER 1. Introduction Markets are incomplete. In recent

Discussion of Optimal Monetary Policy and Fiscal Policy Interaction in a Non-Ricardian Economy Johannes Wieland University of California, San Diego and NBER 1. Introduction Markets are incomplete. In recent

State-Dependent Output and Welfare Effects of Tax Shocks

State-Dependent Output and Welfare Effects of Tax Shocks Eric Sims University of Notre Dame NBER, and ifo Jonathan Wolff University of Notre Dame July 15, 2014 Abstract This paper studies the output and

State-Dependent Output and Welfare Effects of Tax Shocks Eric Sims University of Notre Dame NBER, and ifo Jonathan Wolff University of Notre Dame July 15, 2014 Abstract This paper studies the output and

Managing Capital Flows in the Presence of External Risks

Managing Capital Flows in the Presence of External Risks Ricardo Reyes-Heroles Federal Reserve Board Gabriel Tenorio The Boston Consulting Group IEA World Congress 2017 Mexico City, Mexico June 20, 2017

Managing Capital Flows in the Presence of External Risks Ricardo Reyes-Heroles Federal Reserve Board Gabriel Tenorio The Boston Consulting Group IEA World Congress 2017 Mexico City, Mexico June 20, 2017

Discussion of Ottonello and Winberry Financial Heterogeneity and the Investment Channel of Monetary Policy

Discussion of Ottonello and Winberry Financial Heterogeneity and the Investment Channel of Monetary Policy Aubhik Khan Ohio State University 1st IMF Annual Macro-Financial Research Conference 11 April

Discussion of Ottonello and Winberry Financial Heterogeneity and the Investment Channel of Monetary Policy Aubhik Khan Ohio State University 1st IMF Annual Macro-Financial Research Conference 11 April

Private Debt Overhang and the Government Spending Multiplier: Evidence for the United States

Private Debt Overhang and the Government Spending Multiplier: Evidence for the United States Marco Bernardini Ghent University Gert Peersman Ghent University This version: December 215 Abstract Using state-dependent

Private Debt Overhang and the Government Spending Multiplier: Evidence for the United States Marco Bernardini Ghent University Gert Peersman Ghent University This version: December 215 Abstract Using state-dependent

Consumption. ECON 30020: Intermediate Macroeconomics. Prof. Eric Sims. Fall University of Notre Dame

Consumption ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Fall 2016 1 / 36 Microeconomics of Macro We now move from the long run (decades and longer) to the medium run

Consumption ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Fall 2016 1 / 36 Microeconomics of Macro We now move from the long run (decades and longer) to the medium run

Monetary and Fiscal Policy Switching with Time-Varying Volatilities

Monetary and Fiscal Policy Switching with Time-Varying Volatilities Libo Xu and Apostolos Serletis Department of Economics University of Calgary Calgary, Alberta T2N 1N4 Forthcoming in: Economics Letters

Monetary and Fiscal Policy Switching with Time-Varying Volatilities Libo Xu and Apostolos Serletis Department of Economics University of Calgary Calgary, Alberta T2N 1N4 Forthcoming in: Economics Letters

Government spending shocks, sovereign risk and the exchange rate regime

Government spending shocks, sovereign risk and the exchange rate regime Dennis Bonam Jasper Lukkezen Structure 1. Theoretical predictions 2. Empirical evidence 3. Our model SOE NK DSGE model (Galì and

Government spending shocks, sovereign risk and the exchange rate regime Dennis Bonam Jasper Lukkezen Structure 1. Theoretical predictions 2. Empirical evidence 3. Our model SOE NK DSGE model (Galì and

DETERMINANTS OF FIRMS INVESTMENT IN SPAIN: THE ROLE OF POLICY UNCERTAINTY

DETERMINANTS OF FIRMS INVESTMENT IN SPAIN: THE ROLE OF POLICY UNCERTAINTY Daniel Dejuan and Corinna Ghirelli Bank of Spain European Network for Research on Investment EIB - Luxemburg 9 April 018 DG ECONOMICS,

DETERMINANTS OF FIRMS INVESTMENT IN SPAIN: THE ROLE OF POLICY UNCERTAINTY Daniel Dejuan and Corinna Ghirelli Bank of Spain European Network for Research on Investment EIB - Luxemburg 9 April 018 DG ECONOMICS,

Tax Cuts for Whom? Heterogeneous Effects of Income Tax Changes on Growth & Employment

Tax Cuts for Whom? Heterogeneous Effects of Income Tax Changes on Growth & Employment Owen Zidar University of California, Berkeley NBER Summer Institute 2013: Public Economics July 23, 2013 Owen Zidar

Tax Cuts for Whom? Heterogeneous Effects of Income Tax Changes on Growth & Employment Owen Zidar University of California, Berkeley NBER Summer Institute 2013: Public Economics July 23, 2013 Owen Zidar

A Model of the Consumption Response to Fiscal Stimulus Payments

A Model of the Consumption Response to Fiscal Stimulus Payments Greg Kaplan 1 Gianluca Violante 2 1 Princeton University 2 New York University Presented by Francisco Javier Rodríguez (Universidad Carlos

A Model of the Consumption Response to Fiscal Stimulus Payments Greg Kaplan 1 Gianluca Violante 2 1 Princeton University 2 New York University Presented by Francisco Javier Rodríguez (Universidad Carlos

Sang-Wook (Stanley) Cho

Cho") Beggar-thy-parents? A Lifecycle Model of Intergenerational Altruism Sang-Wook (Stanley) Cho University of New South Wales March 2009 Motivation & Question Since Becker (1974), several studies analyzing

Beggar-thy-parents? A Lifecycle Model of Intergenerational Altruism Sang-Wook (Stanley) Cho University of New South Wales March 2009 Motivation & Question Since Becker (1974), several studies analyzing

Private Leverage and Sovereign Default

Private Leverage and Sovereign Default Cristina Arellano Yan Bai Luigi Bocola FRB Minneapolis University of Rochester Northwestern University Economic Policy and Financial Frictions November 2015 1 / 37

Private Leverage and Sovereign Default Cristina Arellano Yan Bai Luigi Bocola FRB Minneapolis University of Rochester Northwestern University Economic Policy and Financial Frictions November 2015 1 / 37

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics. Ph. D. Comprehensive Examination: Macroeconomics Fall, 2010

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Comprehensive Examination: Macroeconomics Fall, 2010 Section 1. (Suggested Time: 45 Minutes) For 3 of the following 6 statements, state

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Comprehensive Examination: Macroeconomics Fall, 2010 Section 1. (Suggested Time: 45 Minutes) For 3 of the following 6 statements, state

Macroeconomics 2. Lecture 5 - Money February. Sciences Po

Macroeconomics 2 Lecture 5 - Money Zsófia L. Bárány Sciences Po 2014 February A brief history of money in macro 1. 1. Hume: money has a wealth effect more money increase in aggregate demand Y 2. Friedman

Macroeconomics 2 Lecture 5 - Money Zsófia L. Bárány Sciences Po 2014 February A brief history of money in macro 1. 1. Hume: money has a wealth effect more money increase in aggregate demand Y 2. Friedman

Fiscal Multipliers and Heterogeneous Agents

Fiscal Multipliers and Heterogeneous Agents Yongquan CAO April, 6 Abstract The paper analyzes the impacts on different agents from the fiscal shocks under a heterogeneous agent New Keynesian model, where

Fiscal Multipliers and Heterogeneous Agents Yongquan CAO April, 6 Abstract The paper analyzes the impacts on different agents from the fiscal shocks under a heterogeneous agent New Keynesian model, where

Assessing the Effects of Government Spending Shocks: Evidence from OECD and Non-OECD Countries

Assessing the Effects of Government Spending Shocks: Evidence from OECD and Non-OECD Countries [Preliminary and Incomplete] Panagiotis Th. Konstantinou Andromachi Partheniou AUEB AUEB Abstract We estimate

Assessing the Effects of Government Spending Shocks: Evidence from OECD and Non-OECD Countries [Preliminary and Incomplete] Panagiotis Th. Konstantinou Andromachi Partheniou AUEB AUEB Abstract We estimate

Government Spending Shocks in Quarterly and Annual Time Series

Government Spending Shocks in Quarterly and Annual Time Series Benjamin Born University of Bonn Gernot J. Müller University of Bonn and CEPR August 5, 2 Abstract Government spending shocks are frequently

Government Spending Shocks in Quarterly and Annual Time Series Benjamin Born University of Bonn Gernot J. Müller University of Bonn and CEPR August 5, 2 Abstract Government spending shocks are frequently

A Model of the Consumption Response to Fiscal Stimulus Payments

A Model of the Consumption Response to Fiscal Stimulus Payments Greg Kaplan University of Pennsylvania Gianluca Violante New York University Federal Reserve Board May 31, 2012 1/47 Fiscal stimulus payments

A Model of the Consumption Response to Fiscal Stimulus Payments Greg Kaplan University of Pennsylvania Gianluca Violante New York University Federal Reserve Board May 31, 2012 1/47 Fiscal stimulus payments

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach Gianluca Benigno 1 Andrew Foerster 2 Christopher Otrok 3 Alessandro Rebucci 4 1 London School of Economics and

Estimating Macroeconomic Models of Financial Crises: An Endogenous Regime-Switching Approach Gianluca Benigno 1 Andrew Foerster 2 Christopher Otrok 3 Alessandro Rebucci 4 1 London School of Economics and

Labor Economics Field Exam Spring 2014

Labor Economics Field Exam Spring 2014 Instructions You have 4 hours to complete this exam. This is a closed book examination. No written materials are allowed. You can use a calculator. THE EXAM IS COMPOSED

Labor Economics Field Exam Spring 2014 Instructions You have 4 hours to complete this exam. This is a closed book examination. No written materials are allowed. You can use a calculator. THE EXAM IS COMPOSED

Accounting for Patterns of Wealth Inequality

. 1 Accounting for Patterns of Wealth Inequality Lutz Hendricks Iowa State University, CESifo, CFS March 28, 2004. 1 Introduction 2 Wealth is highly concentrated in U.S. data: The richest 1% of households

. 1 Accounting for Patterns of Wealth Inequality Lutz Hendricks Iowa State University, CESifo, CFS March 28, 2004. 1 Introduction 2 Wealth is highly concentrated in U.S. data: The richest 1% of households

Idiosyncratic risk and the dynamics of aggregate consumption: a likelihood-based perspective

Idiosyncratic risk and the dynamics of aggregate consumption: a likelihood-based perspective Alisdair McKay Boston University March 2013 Idiosyncratic risk and the business cycle How much and what types

Idiosyncratic risk and the dynamics of aggregate consumption: a likelihood-based perspective Alisdair McKay Boston University March 2013 Idiosyncratic risk and the business cycle How much and what types

EXAMINING MACROECONOMIC MODELS

1 / 24 EXAMINING MACROECONOMIC MODELS WITH FINANCE CONSTRAINTS THROUGH THE LENS OF ASSET PRICING Lars Peter Hansen Benheim Lectures, Princeton University EXAMINING MACROECONOMIC MODELS WITH FINANCING CONSTRAINTS

1 / 24 EXAMINING MACROECONOMIC MODELS WITH FINANCE CONSTRAINTS THROUGH THE LENS OF ASSET PRICING Lars Peter Hansen Benheim Lectures, Princeton University EXAMINING MACROECONOMIC MODELS WITH FINANCING CONSTRAINTS

A MODEL OF SECULAR STAGNATION

A MODEL OF SECULAR STAGNATION Gauti B. Eggertsson and Neil R. Mehrotra Brown University Portugal June, 2015 1 / 47 SECULAR STAGNATION HYPOTHESIS I wonder if a set of older ideas... under the phrase secular

A MODEL OF SECULAR STAGNATION Gauti B. Eggertsson and Neil R. Mehrotra Brown University Portugal June, 2015 1 / 47 SECULAR STAGNATION HYPOTHESIS I wonder if a set of older ideas... under the phrase secular

How Much Insurance in Bewley Models?

How Much Insurance in Bewley Models? Greg Kaplan New York University Gianluca Violante New York University, CEPR, IFS and NBER Boston University Macroeconomics Seminar Lunch Kaplan-Violante, Insurance

How Much Insurance in Bewley Models? Greg Kaplan New York University Gianluca Violante New York University, CEPR, IFS and NBER Boston University Macroeconomics Seminar Lunch Kaplan-Violante, Insurance

Government Spending Multipliers under the Zero Lower Bound: Evidence from Japan

Government Spending Multipliers under the Zero Lower Bound: Evidence from Japan Wataru Miyamoto Thuy Lan Nguyen Dmitriy Sergeyev This version: December 7, 215 Abstract Using a rich data set on government

Government Spending Multipliers under the Zero Lower Bound: Evidence from Japan Wataru Miyamoto Thuy Lan Nguyen Dmitriy Sergeyev This version: December 7, 215 Abstract Using a rich data set on government

Growth Opportunities, Investment-Specific Technology Shocks and the Cross-Section of Stock Returns

Growth Opportunities, Investment-Specific Technology Shocks and the Cross-Section of Stock Returns Leonid Kogan 1 Dimitris Papanikolaou 2 1 MIT and NBER 2 Northwestern University Boston, June 5, 2009 Kogan,

Growth Opportunities, Investment-Specific Technology Shocks and the Cross-Section of Stock Returns Leonid Kogan 1 Dimitris Papanikolaou 2 1 MIT and NBER 2 Northwestern University Boston, June 5, 2009 Kogan,

The Lost Generation of the Great Recession

The Lost Generation of the Great Recession Sewon Hur University of Pittsburgh January 21, 2016 Introduction What are the distributional consequences of the Great Recession? Introduction What are the distributional

The Lost Generation of the Great Recession Sewon Hur University of Pittsburgh January 21, 2016 Introduction What are the distributional consequences of the Great Recession? Introduction What are the distributional

Designing the Optimal Social Security Pension System

Designing the Optimal Social Security Pension System Shinichi Nishiyama Department of Risk Management and Insurance Georgia State University November 17, 2008 Abstract We extend a standard overlapping-generations

Designing the Optimal Social Security Pension System Shinichi Nishiyama Department of Risk Management and Insurance Georgia State University November 17, 2008 Abstract We extend a standard overlapping-generations

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics. Ph. D. Comprehensive Examination: Macroeconomics Fall, 2016

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Comprehensive Examination: Macroeconomics Fall, 2016 Section 1. (Suggested Time: 45 Minutes) For 3 of the following 6 statements, state

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Comprehensive Examination: Macroeconomics Fall, 2016 Section 1. (Suggested Time: 45 Minutes) For 3 of the following 6 statements, state

Topic 10: Asset Valuation Effects

Topic 10: Asset Valuation Effects Part1: Document Asset holding developments - The relaxation of capital account restrictions in many countries over the last two decades has produced dramatic increases

Topic 10: Asset Valuation Effects Part1: Document Asset holding developments - The relaxation of capital account restrictions in many countries over the last two decades has produced dramatic increases

Fiscal spillovers in the Euro area

Fiscal spillovers in the Euro area Fabio Canova, EUI and CEPR Matteo Ciccarelli, ECB Pietro Dallari, UPF November 23 Introduction The nancial crisis has put scal policy back in the spotlight of academic

Fiscal spillovers in the Euro area Fabio Canova, EUI and CEPR Matteo Ciccarelli, ECB Pietro Dallari, UPF November 23 Introduction The nancial crisis has put scal policy back in the spotlight of academic

Household Saving, Financial Constraints, and the Current Account Balance in China

Household Saving, Financial Constraints, and the Current Account Balance in China Ayşe İmrohoroğlu USC Marshall Kai Zhao Univ. of Connecticut Facing Demographic Change in a Challenging Economic Environment-

Household Saving, Financial Constraints, and the Current Account Balance in China Ayşe İmrohoroğlu USC Marshall Kai Zhao Univ. of Connecticut Facing Demographic Change in a Challenging Economic Environment-

What Drives Fiscal Multipliers? The Role of Private Debt and Wealth

1 / 35[width=2cm,center,respectlinebreaks] What Drives Fiscal Multipliers? The Role of Private Debt and Wealth Sebastian Gechert Keynes Tagung, Berlin, Februar 213 1 Agenda 2 / 35[width=2cm,center,respectlinebreaks]

1 / 35[width=2cm,center,respectlinebreaks] What Drives Fiscal Multipliers? The Role of Private Debt and Wealth Sebastian Gechert Keynes Tagung, Berlin, Februar 213 1 Agenda 2 / 35[width=2cm,center,respectlinebreaks]

slides chapter 6 Interest Rate Shocks

slides chapter 6 Interest Rate Shocks Princeton University Press, 217 Motivation Interest-rate shocks are generally believed to be a major source of fluctuations for emerging countries. The next slide

slides chapter 6 Interest Rate Shocks Princeton University Press, 217 Motivation Interest-rate shocks are generally believed to be a major source of fluctuations for emerging countries. The next slide

Ten Years after the Financial Crisis: What Have We Learned from. the Renaissance in Fiscal Research?

Ten Years after the Financial Crisis: What Have We Learned from the Renaissance in Fiscal Research? by Valerie A. Ramey University of California, San Diego and NBER NBER Global Financial Crisis @10 July

Ten Years after the Financial Crisis: What Have We Learned from the Renaissance in Fiscal Research? by Valerie A. Ramey University of California, San Diego and NBER NBER Global Financial Crisis @10 July

What does the empirical evidence suggest about the eectiveness of discretionary scal actions?

What does the empirical evidence suggest about the eectiveness of discretionary scal actions? Roberto Perotti Universita Bocconi, IGIER, CEPR and NBER June 2, 29 What is the transmission of variations

What does the empirical evidence suggest about the eectiveness of discretionary scal actions? Roberto Perotti Universita Bocconi, IGIER, CEPR and NBER June 2, 29 What is the transmission of variations

Transfer Pricing by Multinational Firms: New Evidence from Foreign Firm Ownership

Transfer Pricing by Multinational Firms: New Evidence from Foreign Firm Ownership Anca Cristea University of Oregon Daniel X. Nguyen University of Copenhagen Rocky Mountain Empirical Trade 16-18 May, 2014

Transfer Pricing by Multinational Firms: New Evidence from Foreign Firm Ownership Anca Cristea University of Oregon Daniel X. Nguyen University of Copenhagen Rocky Mountain Empirical Trade 16-18 May, 2014

How Large is the Government Spending Multiplier? Evidence from World Bank Lending

How Large is the Government Spending Multiplier? Evidence from World Bank Lending Aart Kraay presented by Iacopo Morchio Universidad Carlos III de Madrid http://www.uc3m.es October 31st, 2012 Motivation

How Large is the Government Spending Multiplier? Evidence from World Bank Lending Aart Kraay presented by Iacopo Morchio Universidad Carlos III de Madrid http://www.uc3m.es October 31st, 2012 Motivation

Working paper OUTSIDE THE CORRIDOR: FISCAL MULTIPLIERS AND BUSINESS CYCLES INTO AN AGENT-BASED MODEL WITH LIQUIDITY CONSTRAINTS.

Working paper 2014-16 OUTSIDE THE CORRIDOR: FISCAL MULTIPLIERS AND BUSINESS CYCLES INTO AN AGENT-BASED MODEL WITH LIQUIDITY CONSTRAINTS Mauro Napoletano OFCE and Skema Business School, Scuola Superiore

Working paper 2014-16 OUTSIDE THE CORRIDOR: FISCAL MULTIPLIERS AND BUSINESS CYCLES INTO AN AGENT-BASED MODEL WITH LIQUIDITY CONSTRAINTS Mauro Napoletano OFCE and Skema Business School, Scuola Superiore

Multiplier Effects of Federal Disaster-Relief Spending: Evidence from U.S. States and Households

Multiplier Effects of Federal Disaster-Relief Spending: Evidence from U.S. States and Households Xiaoqing Zhou Bank of Canada This Version: November 19, 2017 First Version: May 4, 2016 Abstract Can government

Multiplier Effects of Federal Disaster-Relief Spending: Evidence from U.S. States and Households Xiaoqing Zhou Bank of Canada This Version: November 19, 2017 First Version: May 4, 2016 Abstract Can government

Volume 29, Issue 1. Juha Tervala University of Helsinki

Volume 29, Issue 1 Productive government spending and private consumption: a pessimistic view Juha Tervala University of Helsinki Abstract This paper analyses the consequences of productive government

Volume 29, Issue 1 Productive government spending and private consumption: a pessimistic view Juha Tervala University of Helsinki Abstract This paper analyses the consequences of productive government

The Distributive Impact of Reforms in Credit Enforcement: Evidence from Indian Debt Recovery Tribunals

The Distributive Impact of Reforms in Credit Enforcement: Evidence from Indian Debt Recovery Tribunals Stockholm School of Economics Dilip Mookherjee Boston University Sujata Visaria Boston University

The Distributive Impact of Reforms in Credit Enforcement: Evidence from Indian Debt Recovery Tribunals Stockholm School of Economics Dilip Mookherjee Boston University Sujata Visaria Boston University

GLOBAL IMBALANCES FROM A STOCK PERSPECTIVE

GLOBAL IMBALANCES FROM A STOCK PERSPECTIVE Enrique Alberola (BIS), Ángel Estrada and Francesca Viani (BdE) (*) (*) The views expressed here do not necessarily coincide with those of Banco de España, the

GLOBAL IMBALANCES FROM A STOCK PERSPECTIVE Enrique Alberola (BIS), Ángel Estrada and Francesca Viani (BdE) (*) (*) The views expressed here do not necessarily coincide with those of Banco de España, the