Financial Crisis and Regulatory Reform: Implications for the Middle East and North Africa Emerging Markets IAASB CAG Meeting, Dubai 09 March 2009

|

|

|

- Jocelin Chandler

- 5 years ago

- Views:

Transcription

1 Financial Crisis and Regulatory Reform: Implications for the Middle East and North Africa Emerging Markets IAASB CAG Meeting, Dubai 09 March 2009 Dr. Nasser Saidi, Chief Economist, DIFC Authority 1

2 Financial Crisis and Regulatory Reform: Implications for the Middle East and North Africa Emerging Markets AGENDA GLOBAL FINANCIAL CRISIS AND ECONOMIC OUTLOOK: Heading to Depression FINANCIAL CRISES AND THEIR AFTERMATH: Turmoil & potential meltdown MENA/GCC & EMERGING MARKETS: Relatively Resilient CORPORATE GOVERNANCE, STRUCTURAL & REGULATORY REFORMS: Beware the political backlash 2

3 Overview The risk of a global financial meltdown has been avoided for now thanks to massive government & central bank rescue plans and guarantees Volatility will persist for the months to come with bad and good news while the banking sector remains under strain Conjunction of financial crisis, housing bust and credit crunch portends deep recession in the US and UK. The US stimulus package is unlikely to produce effects before mid-summer. Emerging markets and the GCC have been so far more resilient, but the shock have been too strong to be offset by purely domestic factors. Oil prices will remain depressed with negative effects on public finances and infrastructure projects The Gulf and DIFC could be among the long term gainers in the adjustment process, if economic governance and transparency are improved and a more coherent set of policy responses and structural reforms is framed over the next weeks and months.

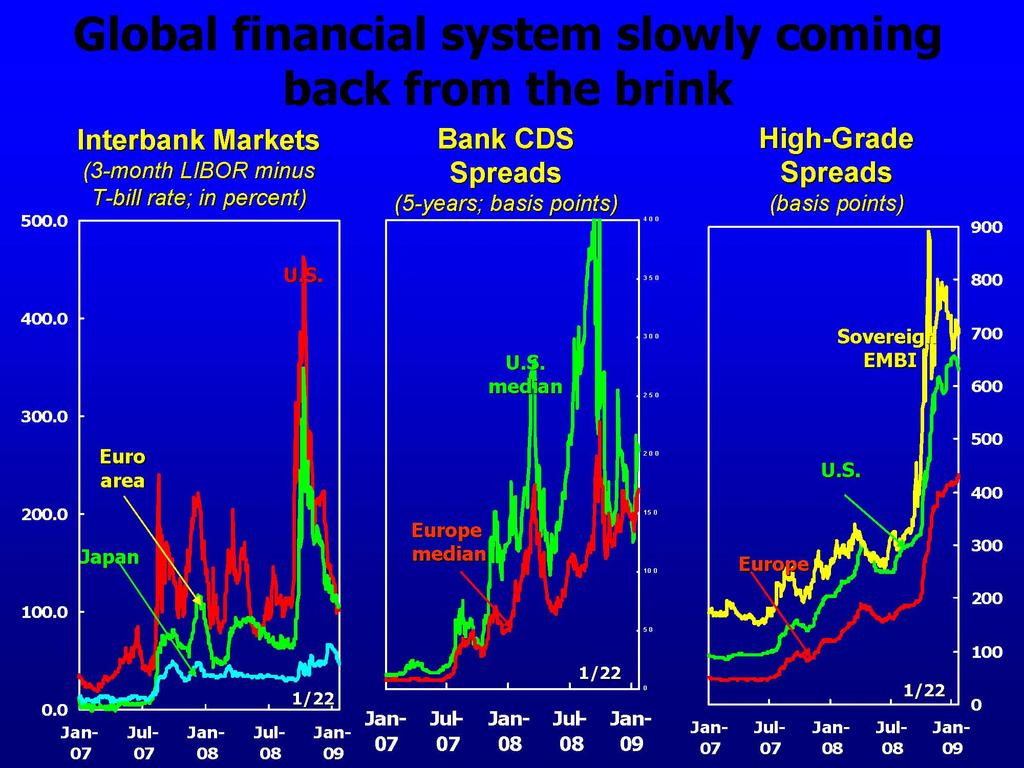

4 Analysis of Global Situation Despite a historic coordinated intervention of all major central banks and a series of unprecedented, wide ranging and extensive government intervention, the financial sector remains fragile and a return to normality is slow. Damage assessment is still underway and new heavy losses are revealed every quarter. Authorities, financial intermediaries and corporations are bracing for at least three quarters of deep recession and widespread weakness until end 2009 as the credit crunch spreads to the real economy. Almost every month forecasts have been corrected sharply downwards. World growth in 2009 is forecast to be barely above zero. Lower consumption, cuts in investment projects and corporate downsizing in the wake of sharply reduced credit availability will in all likelihood prevail until the deleveraging comes to an end and trust in financial markets is restored. At present nobody can be sure for how long markets will remain dysfunctional, what results the stimulus packages will produce, over what time frame, and what future imbalances might cause. The likelihood of a depression is now more than 30%

5 Recent IMF Forecasts The world economy is coping with the most severe shock to mature financial markets since the 1930s. On an annual basis, global growth is expected to moderate from 5.0% in 2007 to 3.4% in 2008 and 0.5% in Advanced economies will suffer a deep recession, -2.0% in 2009 (a downward revision of 1.7% compared to a month ago). Emerging economies have thus far been able to hold on, but global trade, on which most of them rely, has suffered one of the most severe quarterly blows in history. Their real GDP growth is expected to slow from around 8% in 2007 to 3.0% in 2009 (revised down from 6.1% in the October WEO) on the optimistic assumption that export push will be replaced by domestic demand. These figures essentially indicate that the world is facing a simultaneous recession never experienced in peace time

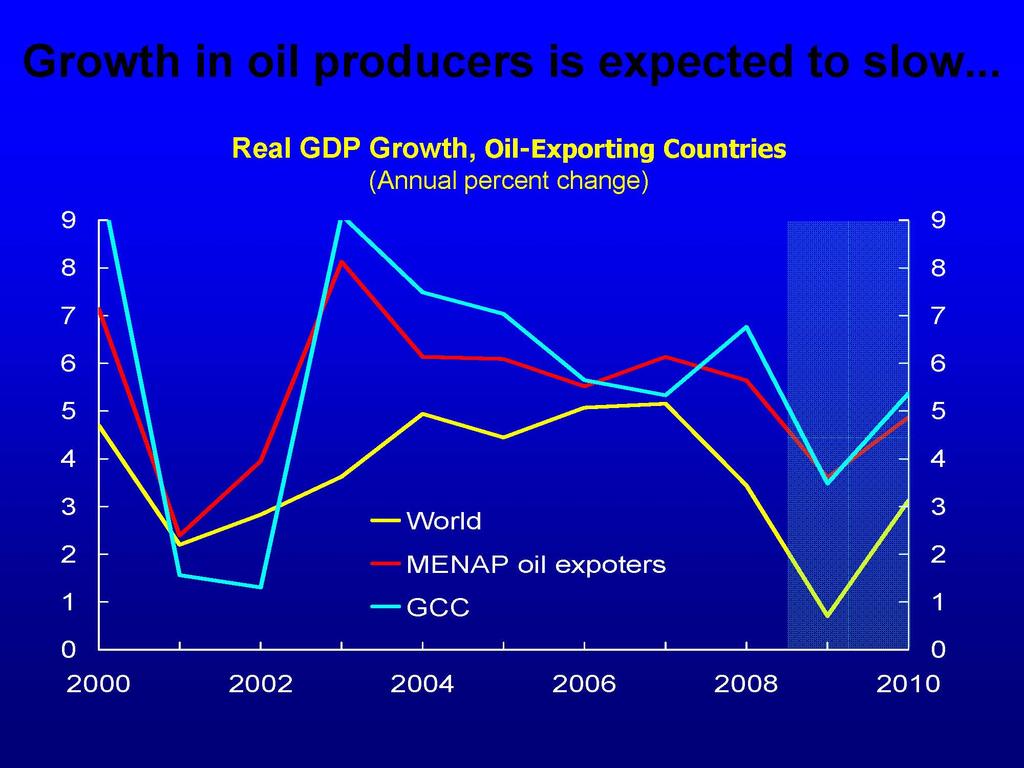

6 Global growth comes to a halt

7

8

9

10

11 27 Things you may not have known about banking crises Systemic Banking Crises: A New Database, IMF Working Paper, Nov In 55 per cent of cases, the banking crisis coincides with a currency crisis. 2. Bank runs feature in 62 per cent of the crises. 3. Banking crises are often preceded by credit booms, in 30 per cent of the cases. 4. Non-performing loans average about 25 per cent of loans at the onset of the crisis. 5. Macroeconomic conditions are often weak prior to a banking crisis. 6. Extensive liquidity support is used in 71 per cent of crises. 7. Peak liquidity support tends to be sizeable and averages about 28 per cent of total deposits. 8. Blanket guarantees are used in 29 per cent of crises, often introduced to restore confidence even when previous explicit deposit insurance arrangements are already in place, lasting for an average of 53 months. 9. Prolonged regulatory forbearance - where banks, for example, are allowed to overstate their equity capital in order to avoid the costs of contractions in loan supply - occurs in 67 per cent of crises. 10. In 35 per cent of cases, forbearance takes the form of banks not being intervened despite being technically insolvent, and in 73 per cent of cases prudential regulations are suspended or not fully applied. Existing literature on forbearance shows it is counterproductive, with banks taking on additional risks at the future expense of the gove11. In 86 per cent of cases, government intervention takes place in the form of bank closures, nationalizations, or assisted mergers per cent of crisis episodes have experienced sales of banks to foreigners. 13. The more bank closures there are, the higher the fiscal costs. 14. A blanket guarantee, however, reduces the instances of bank closures. 15. Bank restructuring agencies are set up in 48 per cent of crises. 16. Asset management companies are set up in 60 per cent of cases to manage distressed assets. 17. In 76 per cent of episodes, banks were recapitalised by the government, mostly with cash, government bonds or subordinated debt. 18. Recapitalisation programs are usually accompanied with some conditionality. 19. To the extent that debt relief schemes are discretionary, they run the risk of moral hazard as debtors stop trying to repay in the hope of being added to the list of scheme beneficiaries. 20. Average net recapitalisation costs to the government amounts to 6 per cent of GDP. 21.On the bright side, recapitalisations tend to be associated with lower output losses. 22. Monetary policy tends to be neutral during crisis episodes, while fiscal policy tends to be expansive. 23. Average fiscal costs, net of recoveries, associated with crisis management average 13.3 per cent of GDP. 24. The average recovery rate is just 18 per cent of gross fiscal costs. 25. Real GDP losses average 20 per cent relative to trend during the first four years of the crisis. 26. There is a negative correlation between output losses and fiscal costs: the higher the fiscal costs, the smaller the loss of output 27. Inflation and currency devaluation help reduce the budgetary burden and thus have been a feature of the resolution of many crises in the past.

12 Stylised Facts on the Aftermath of Severe Financial Crises C. Reinhart & K. Rogoff (2008) 1. Asset market collapses are deep and prolonged. Real housing price declines average 35 percent stretched out over six years. Equity price collapses average 55 percent over a downturn of about three and a half years. 2. Aftermath of banking crises is associated with profound declines in output and employment. Unemployment rate rises an average of 7 percentage points over the down phase of the cycle, which lasts on average over four years. Output falls (from peak to trough) an average of over 9 percent, although the duration of the downturn, averaging roughly two years, is shorter than for unemployment. 3. Real value of government debt tends to explode, rising an average of 86 percent in the major post World War II episodes. Main cause of debt explosions is not the costs of bailing; the big drivers of debt increases are the collapse in tax revenues as a result of recession.

13 Sources: Reinhart and Rogoff (2008b) and sources cited therein.

14 Sources: Reinhart and Rogoff (2008b) and sources cited therein

15 Resilience in Emerging Markets A slowdown in external demand will not be enough to force a hard landing in EM growth, but could force a sudden adjustment in the export sector with factory closures and widespread layoffs. While hot money inflows have turned to outflows in many EMs, a hard-landing is unlikely unless FDI drops drastically. In several EMs, financial markets are clogged, and this will cause growth to fall sharply in the near term. However, if policy actions in the US and Europe help to unfreeze markets, there is a good chance that most EMs will escape a severe contraction. The key factor to watch will be large infrastructure projects and the effects of stimulus measures aimed at boosting domestic consumption in the EMs.

16 MENA - Limited Repercussions MENA, especially the Gulf region, has not been as severely hit by toxic assets and financial turmoil thanks to Strong growth and profitable domestic markets Small stock of outstanding securitised/structured products Limited expertise in managing structured investment products Regulatory/prudential requirements limited exposure to subinvestment grade investments & instruments Growing importance of Shari a compliant finance Ample liquidity from the increasing net capital flows (due to high returns) and from oil exports Fiscal discipline and sizeable stock of foreign assets However the drop in oil price will cloud the outlook and put strains on public finances and current accounts

17 MENA Vulnerability through Real Sector channel In addition to oil prices, the following real sector economic transactions may increase MENA vulnerability to the crisis: Decline in International Trade Decline in Tourism Decline in Foreign Direct Investment Countries with ties to Europe are most vulnerable including Tunisia, Morocco and Egypt Decline in Remittances affecting labour exporting countries

18

19

20

21

22 Policy measures in the GCC Bahrain cut the repo rate by 25bp and the overnight rate by 50bp Kuwait cut the repo rate by 100bp and the discount rate by 125bp. A series of other measures included 1bn USD investment by KIA in local stock market, liquidity injections, increase in the loan/deposit ratio, extensive deposits guarantee. Qatar has instructed QIA to buy 10-20% of local banks capital KSA reduced its repo rate by 50bp (but left unchanged the reverse repo rate), and set up a 36bn USD liquidity facility (only 2-3 bn have been used) and reduced reserve requirements from 13% to 10%. UAE guaranteed all deposits (including interbank) and set up a 50bn AED emergency liquidity facility (little used so far), while the government deposited 70bn AED in local banks. The repo rate was reduced to 1.0% effective 19 January 2009 All governments are maintaining infrastructure and investment spending and are likely to run modest deficits of 2%-3% of GDP

23 Banking sector in GCC GCC Banks remain well capitalized and profitable, with NPL below 5% of the total. Vulnerability will emerge as growth rates decline. Liquidity problems were caused mostly by an outflow of speculative capital betting on a currency revaluation and by the seizure of international money markets While cost of wholesale funding has increased, the region has no shortage of capital and its creditworthiness is solid However, IIF estimates that international banks have provided between 20% and 50% of project financing with the highest share in the UAE. In June 2008 foreign liabilities of the UAE stood at USD 88 from 23 billion at end 2005.

24 MENA/GCC POLICY REFORM MEASURES

25 MENA/GCC Structural Reform & Policy Issues 1. Real Estate & the Housing Market: develop long-term housing finance 2. Financing Growth: deposit & credit guarantee 3. Building Capital Markets: bond market, money market, alternative investment markets 4. Public Debt & Finances: build capacity for fiscal sustainability

26 Corporate governance and the financial crisis Underlying much of the credit crunch has been a fundamental failure in corporate governance. While the financial institutions involved may have been in compliance with local requirements and codes, they have ignored the key point Good corporate governance is about boards directing and controlling the organisations so they operate in their shareholders interests.the use of overtly complex financial products, which thwarted effective supervisory control, and the unethical advancement, at the point of sale, of loans to people with little realistic hope of repaying them shows a lack of basic corporate governance. Association of Chartered Certified accountants Climbing out of the Credit Crunch, September 2008

27 Failure of financial regulatory systems The directors of Northern Rock were the principal authors of the difficulties that the company has faced since August The directors pursued a reckless business model which was excessively reliant on wholesale funding. The Financial Services Authority systematically failed in its regulatory duty to ensure that Northern Rock would not pose a systemic risk House of Commons Treasury Committee, (January 2008) The Run on the Rock 27

28 CG & Policy issues to be addressed Board Composition and Competence Risk Management process and governance Executive Compensation & Incentive structures Accounting and Disclosure issues Role, Regulation & Oversight of credit rating agencies Corporate Governance in the banking and financial sector Scope of the regulatory frontier Role of central banks as lenders/rescuers of last resort and the nature of collateral The Basel II framework & Liquidity Risk Management Macro-Prudential risk management

29 Corporate Governance in the aftermath of crises CG Policy has lagged: development and refinement of Corporate Governance standards has followed the occurrence of Corporate Governance failures Beware the political backlash Corporate Governance deficiencies facilitated or did not prevent practices that resulted in poor performance GCC are not immune to risks and crisis has impacted the markets of the region: stock market value losses, credit cost increased, liquidity tightening, reduced lending, international investors offloading GCC & MENA positions due to financial crisis Pressing CG issues: related party ownership, related party lending, stock market regulation, disclosure & transparency, accounting standards

30 Hawkamah-IFC CG Survey % of companies that still combine the function of chairman and CEO should separate these roles to comply with best practice. Only 25% of banks and listed firms provide information on their dividend policies online, and just 12% have online information on key executives remuneration. Most respondents view disclosure from a compliance point of view, rather than see it as an effective tool for managing stakeholder relations and adding value to their business. Only 50% of listed family-owned enterprises (FOEs) had adopted a family constitution, while only 25% had family councils in place. Three-quarters of FOEs said their boards are composed of a majority of family members.

31 Hawkamah-IFC MENA CG Survey: Key Findings Internal Audit is wellestablished in the Region Do you have an Internal Audit Function? Risk Mgt and Internal Control functions need improvement Less than half have a risk mgt function (43%), likewise less than half have internal control function (47%) Most have external auditor, but rotation remains an issue Only about one-third have rotation policy (32%)

32 Hawkamah-IFC MENA CG Survey: Transparency Transparency & Disclosure Most provide financial statements, but could improve nonfinancial disclosure. Minority include Management Discussion (28%) Shareholder Rights General Assemblies are well-attended (75%); Directors are elected by shareholders in most organizations (81%). Conflict of interest & related party transaction policies are common (~75%); but perception is that not always put into practice. Significant percentage believe directors fail to avoid conflict of interest (55%) or use insider information (67%)

33 Hawkamah-IFC Survey: Information contained in Annual Reports % of respondents Report of the chairman 85 Financial statements 82 Market share, sales and marketing 77 Ownership structure and dividend policy 72 Future plans of the company 64 Dividend history 54 Remuneration 44 Biographical details of the board 41 Beneficial owners 36 Management discussion/analysis 30 Corporate governance policies 28 Environment, social and economic sustainability 27 Share options policy 13

34 Hawkamah-TNI Survey, August 2008

35 MENA/GCC Reform Measures 1. Improve statistical capacity and public dissemination of data & information 2. Establish company registrars and companies houses 3. Strengthen Transparency & Disclosure for listed companies 4. Introduce mandatory CG Codes, Guidelines and Laws and enforce them 5. Enforce anti-trust measures for SROs to combat oligopolistic structure with dominance of 3 companies; license new SROs 6. Three types of improvements i. Improve SRO incentives by increasing the transparency of their modeling practices and holding their managements accountable for negligent ratings errors. ii. Remove incorporation of SRO ratings in securities and banking regulations issued by governmental entities. By outsourcing public authority to private firms, this practice intensifies the conflicts of interest that SRO personnel must resolve iii. Acknowledge differences in the degree of leverage that is imbedded in different issues of securitized debt. Recommendation that SROs be required to state an express margin for error in their ratings for every tranche of securitized instruments. 7. Reconsider the role of ratings in Basel II 8. Suspend mark to market or fair value accounting until markets become functional 35

36 Some concluding remarks Corporate Governance failures & mal-governance facilitated or did not prevent practices that resulted in poor performance leading to banking & financial crises Political backlash will lead to new Regulatory framework and Corporate Governance reforms Emerging Markets lessons: develop local financial markets & focus on banking sector soundness CG reform should be an economic policy imperative to address pressing CG issues in MENA/GCC: related party ownership, related party lending, stock market regulation, disclosure & transparency, accounting standards Major opportunity: GCC countries growing economic & financial integration can be main driver of monetary and financial policy reforms; Gulf Monetary Union and Gulf Common Currency leading to a new global currency and contributor to new international financial architecture

37 Thank you

FINANCIAL CRISES & CORPORATE GOVERNANCE: SOME LESSONS FOR EMERGING MARKET ECONOMIES & MENA ESCA Forum Abu Dhabi, UAE January 2009

FINANCIAL CRISES & CORPORATE GOVERNANCE: SOME LESSONS FOR EMERGING MARKET ECONOMIES & MENA ESCA Forum Abu Dhabi, UAE January 2009 Dr. Nasser Saidi nasser.saidi@difc.ae Chief Economist, DIFC Authority Agenda

FINANCIAL CRISES & CORPORATE GOVERNANCE: SOME LESSONS FOR EMERGING MARKET ECONOMIES & MENA ESCA Forum Abu Dhabi, UAE January 2009 Dr. Nasser Saidi nasser.saidi@difc.ae Chief Economist, DIFC Authority Agenda

DIFC ECONOMICS WORKSHOP No.3, 25 MARCH Dr. Nasser Saidi, Chief Economist, DIFC Authority

ECONOMICS OF DEPOSIT INSURANCE DIFC ECONOMICS WORKSHOP No.3, 25 MARCH 2009 Dr. Nasser Saidi, Chief Economist, DIFC Authority 1 ECONOMICS OF DEPOSIT INSURANCE Some Basics Definitions Banking Crises Issues

ECONOMICS OF DEPOSIT INSURANCE DIFC ECONOMICS WORKSHOP No.3, 25 MARCH 2009 Dr. Nasser Saidi, Chief Economist, DIFC Authority 1 ECONOMICS OF DEPOSIT INSURANCE Some Basics Definitions Banking Crises Issues

Financial Crises & New Economic Geography: Emerging Alternative Finance

Financial Crises & New Economic Geography: Emerging Alternative Finance Dr. Nasser Saidi The Annual Falcon Group Trade and Corporate Finance Forum 2 March 2014 Agenda ü Shifting Global Economic Geography

Financial Crises & New Economic Geography: Emerging Alternative Finance Dr. Nasser Saidi The Annual Falcon Group Trade and Corporate Finance Forum 2 March 2014 Agenda ü Shifting Global Economic Geography

GCC STOCK MARKETS: FUNDAMENTALS, BUBBLES & GOVERNANCE IIF MENA Regional Forum Kuwait, 6-7 November 2006

GCC STOCK MARKETS: FUNDAMENTALS, BUBBLES & GOVERNANCE IIF MENA Regional Forum Kuwait, 6-7 November 2006 Dr. Nasser Saidi Chief Economist Dubai International Financial Centre November 2006 Agenda Recent

GCC STOCK MARKETS: FUNDAMENTALS, BUBBLES & GOVERNANCE IIF MENA Regional Forum Kuwait, 6-7 November 2006 Dr. Nasser Saidi Chief Economist Dubai International Financial Centre November 2006 Agenda Recent

Export Group Meeting on the Contribution and Effective Use of External Resources for Development, in Particular for Productive Capacity Building

Export Group Meeting on the Contribution and Effective Use of External Resources for Development, in Particular for Productive Capacity Building 22-24 February 21 Debt Sustainability and the Implications

Export Group Meeting on the Contribution and Effective Use of External Resources for Development, in Particular for Productive Capacity Building 22-24 February 21 Debt Sustainability and the Implications

Financial Crisis & the Corporate Governance Solution: Moving Forward on Remedies

Financial Crisis & the Corporate Governance Solution: Moving Forward on Remedies Dr Nasser Saidi 1 Keynote 1st Annual Compliance and Anti Money Laundering Seminar SAMA Institute of Banking 24 th - 25th

Financial Crisis & the Corporate Governance Solution: Moving Forward on Remedies Dr Nasser Saidi 1 Keynote 1st Annual Compliance and Anti Money Laundering Seminar SAMA Institute of Banking 24 th - 25th

Indonesia: Changing patterns of financial intermediation and their implications for central bank policy

Indonesia: Changing patterns of financial intermediation and their implications for central bank policy Perry Warjiyo 1 Abstract As a bank-based economy, global factors affect financial intermediation

Indonesia: Changing patterns of financial intermediation and their implications for central bank policy Perry Warjiyo 1 Abstract As a bank-based economy, global factors affect financial intermediation

Securitization & Financial Development in MENA Dr. Nasser Saidi* 1 Keynote speech at Securitisation World: MENA 2007 Conference Dubai, 18 March 2007

Securitization & Financial Development in MENA Dr. Nasser Saidi* 1 Keynote speech at Securitisation World: MENA 2007 Conference Dubai, 18 March 2007 Ladies and Gentlemen: 1. Thank you for inviting me to

Securitization & Financial Development in MENA Dr. Nasser Saidi* 1 Keynote speech at Securitisation World: MENA 2007 Conference Dubai, 18 March 2007 Ladies and Gentlemen: 1. Thank you for inviting me to

Bank Corporate Governance in the MENA Region

Bank Corporate Governance in the MENA Region Institute for International Finance MENA CEO Summit Dubai International Financial Centre 24 February 2008 Dr. Nasser Saidi Executive Director Hawkamah, The

Bank Corporate Governance in the MENA Region Institute for International Finance MENA CEO Summit Dubai International Financial Centre 24 February 2008 Dr. Nasser Saidi Executive Director Hawkamah, The

East Asia Crisis of Econ October 8, Team 5 Bryan Darch Svend Egholm Paramdeep Singh Sarah Zullo

East Asia Crisis of 1997 Econ 7920 October 8, 2008 Team 5 Bryan Darch Svend Egholm Paramdeep Singh Sarah Zullo The East Asian currency crisis of 1997 caused severe distress for the countries of East Asia

East Asia Crisis of 1997 Econ 7920 October 8, 2008 Team 5 Bryan Darch Svend Egholm Paramdeep Singh Sarah Zullo The East Asian currency crisis of 1997 caused severe distress for the countries of East Asia

Economic Policy in the Crisis. Lars Calmfors Jönköping International Business School, 2 November 2009

Economic Policy in the Crisis Lars Calmfors Jönköping International Business School, 2 November 2009 My involvement Professor of International Economics at the Institute for International Economic Studies,

Economic Policy in the Crisis Lars Calmfors Jönköping International Business School, 2 November 2009 My involvement Professor of International Economics at the Institute for International Economic Studies,

INDONESIAN ECONOMY Recent Developments and Challenges. BUDI MULYA Deputy Governor of Bank Indonesia

INDONESIAN ECONOMY Recent Developments and Challenges BUDI MULYA Deputy Governor of Bank Indonesia Addressed at OCBC Global Treasury Economic and Business Forum Singapore, 9 July 2010 First of all, I would

INDONESIAN ECONOMY Recent Developments and Challenges BUDI MULYA Deputy Governor of Bank Indonesia Addressed at OCBC Global Treasury Economic and Business Forum Singapore, 9 July 2010 First of all, I would

Spring Forecast: slowly recovering from a protracted recession

EUROPEAN COMMISSION Olli REHN Vice-President of the European Commission and member of the Commission responsible for Economic and Monetary Affairs and the Euro Spring Forecast: slowly recovering from a

EUROPEAN COMMISSION Olli REHN Vice-President of the European Commission and member of the Commission responsible for Economic and Monetary Affairs and the Euro Spring Forecast: slowly recovering from a

Financial Crisis What do we know?

Financial Crisis What do we know? Pedro Videla IESE Global Propagation of the Financial Crisis United Kingdom Ireland Iceland United States Spain January 2008 March 2008 June 2008 September 2008 January

Financial Crisis What do we know? Pedro Videla IESE Global Propagation of the Financial Crisis United Kingdom Ireland Iceland United States Spain January 2008 March 2008 June 2008 September 2008 January

KEY CHALLENGES FOR SUSTAINING GROWTH AND COMPETITIVENESS IN SEE

KEY CHALLENGES FOR SUSTAINING GROWTH AND COMPETITIVENESS IN SEE GLOBAL TRENDS Accelerating growth in advanced economies (US, UK, Eurozone) vs. Slowdown in almost all emerging markets Downward revisions

KEY CHALLENGES FOR SUSTAINING GROWTH AND COMPETITIVENESS IN SEE GLOBAL TRENDS Accelerating growth in advanced economies (US, UK, Eurozone) vs. Slowdown in almost all emerging markets Downward revisions

Ministerial Conference on the Financial Crisis

UNECA Ministerial Conference on the Financial Crisis BRIEFING NOTE 1: The Current Financial Crisis: Impact on African Economies Ramada Plaza Hotel, Tunis, Tunisia November 12, 2008 1. Introduction The

UNECA Ministerial Conference on the Financial Crisis BRIEFING NOTE 1: The Current Financial Crisis: Impact on African Economies Ramada Plaza Hotel, Tunis, Tunisia November 12, 2008 1. Introduction The

Navigating the Perfect Storm

Navigating the Perfect Storm Some Ideas on how Mongolia can manage this Presentation to 1/22/2009, by Arshad Sayed, Country Manager, World Bank Today s Presentation 1. Is this just a financial crisis 2.

Navigating the Perfect Storm Some Ideas on how Mongolia can manage this Presentation to 1/22/2009, by Arshad Sayed, Country Manager, World Bank Today s Presentation 1. Is this just a financial crisis 2.

Daniel Mminele: Thoughts on South Africa s monetary policy

Daniel Mminele: Thoughts on South Africa s monetary policy Address by Mr Daniel Mminele, Deputy Governor of the South African Reserve Bank, at the JP Morgan Investor Conference, Washington DC, 16 April

Daniel Mminele: Thoughts on South Africa s monetary policy Address by Mr Daniel Mminele, Deputy Governor of the South African Reserve Bank, at the JP Morgan Investor Conference, Washington DC, 16 April

Other similar crisis: Euro, Emerging Markets

Session 15. Understanding Macroeconomic Crises. Mexican Crisis 1994-95 Other similar crisis: Euro, Emerging Markets Global Scenarios 2017-2021 The Mexican Peso Crisis in 1994: Background An economy that

Session 15. Understanding Macroeconomic Crises. Mexican Crisis 1994-95 Other similar crisis: Euro, Emerging Markets Global Scenarios 2017-2021 The Mexican Peso Crisis in 1994: Background An economy that

Challenges of financial globalisation and dollarisation for monetary policy: the case of Peru

Challenges of financial globalisation and dollarisation for monetary policy: the case of Peru Julio Velarde During the last decade, the financial system of Peru has become more integrated with the global

Challenges of financial globalisation and dollarisation for monetary policy: the case of Peru Julio Velarde During the last decade, the financial system of Peru has become more integrated with the global

Global Financial Crisis and China s Countermeasures

Global Financial Crisis and China s Countermeasures Qin Xiao The year 2008 will go down in history as a once-in-a-century financial tsunami. This year, as the crisis spreads globally, the impact has been

Global Financial Crisis and China s Countermeasures Qin Xiao The year 2008 will go down in history as a once-in-a-century financial tsunami. This year, as the crisis spreads globally, the impact has been

Indonesia Banking Resolution Lesson Learned From Financial Reform (1997 & 2008) Kartika Wirjoatmodjo Indonesia Deposit Insurance Corporation

Kartika Wirjoatmodjo Indonesia Deposit Insurance Corporation") Indonesia Banking Resolution Lesson Learned From Financial Reform (1997 & 2008) Kartika Wirjoatmodjo Indonesia Deposit Insurance Corporation Agenda Macro Economic and Indonesia Banking Update Lesson Learned:

Indonesia Banking Resolution Lesson Learned From Financial Reform (1997 & 2008) Kartika Wirjoatmodjo Indonesia Deposit Insurance Corporation Agenda Macro Economic and Indonesia Banking Update Lesson Learned:

Dubai s Growth Drivers

Dubai s Growth Drivers Presentation at the Dubai Economic Outlook 2012 Dr. Nasser Saidi, Chief Economist, DIFC 15 th February, 2012 Agenda 1. BACKGROUND 2. MACROECONOMIC & STRUCTURAL DRIVERS 3. BUILDING

Dubai s Growth Drivers Presentation at the Dubai Economic Outlook 2012 Dr. Nasser Saidi, Chief Economist, DIFC 15 th February, 2012 Agenda 1. BACKGROUND 2. MACROECONOMIC & STRUCTURAL DRIVERS 3. BUILDING

THE FINANCIAL CRISIS IN JAPAN ARE THERE SIMILARITIES TO THE CURRENT SITUATION?

THE FINANCIAL CRISIS IN JAPAN ARE THERE SIMILARITIES TO THE CURRENT SITUATION? JOHANNES MAYR* In the 99s experienced a deep financial crisis that lasted for more than a decade and whose effects strain

THE FINANCIAL CRISIS IN JAPAN ARE THERE SIMILARITIES TO THE CURRENT SITUATION? JOHANNES MAYR* In the 99s experienced a deep financial crisis that lasted for more than a decade and whose effects strain

News Release 18 February 2009 Quarterly Press Briefing Hon. Derick Latibeaudiere, Governor, Bank of Jamaica

News Release 18 February 2009 Quarterly Press Briefing Hon. Derick Latibeaudiere, Governor, Bank of Jamaica Ladies and gentlemen, This is our first press briefing for 2009. I am very pleased to welcome

News Release 18 February 2009 Quarterly Press Briefing Hon. Derick Latibeaudiere, Governor, Bank of Jamaica Ladies and gentlemen, This is our first press briefing for 2009. I am very pleased to welcome

REAL ESTATE BOOMS, RECESSIONS AND FINANCIAL CRISES

REAL ESTATE BOOMS, RECESSIONS AND FINANCIAL CRISES Christophe André OECD Economics Department Joint work with Thomas Chalaux OECD Economics Department Recent trends in the real estate market and its analysis,

REAL ESTATE BOOMS, RECESSIONS AND FINANCIAL CRISES Christophe André OECD Economics Department Joint work with Thomas Chalaux OECD Economics Department Recent trends in the real estate market and its analysis,

Kuwait Investment Sector

November 2010 Industry Research Kuwait Investment Sector Report Contents Summary Industry Overview Kuwait Investment Sector Reasons for the poor performance & liquidity problems of Kuwaiti Investment Companies

November 2010 Industry Research Kuwait Investment Sector Report Contents Summary Industry Overview Kuwait Investment Sector Reasons for the poor performance & liquidity problems of Kuwaiti Investment Companies

OECD Interim Economic Projections Real GDP 1 Percentage change September 2015 Interim Projections. Outlook

ass Interim Economic Outlook 16 September 2015 Puzzles and uncertainties Global growth prospects have weakened slightly and become less clear in recent months. World trade growth has stagnated and financial

ass Interim Economic Outlook 16 September 2015 Puzzles and uncertainties Global growth prospects have weakened slightly and become less clear in recent months. World trade growth has stagnated and financial

Public Information Notice (PIN) No. 03/124 FOR IMMEDIATE RELEASE October 17, 2003 International Monetary Fund 700 19 th Street, NW Washington, D. C. 20431 USA IMF Concludes 2003 Article IV Consultation

Public Information Notice (PIN) No. 03/124 FOR IMMEDIATE RELEASE October 17, 2003 International Monetary Fund 700 19 th Street, NW Washington, D. C. 20431 USA IMF Concludes 2003 Article IV Consultation

Chapter 24 CRISES IN EMERGING MARKETS

Chapter 24 CRISES IN EMERGING MARKETS The previous chapter extended the IS-LM-BP model to accommodate high capital mobility. Chapter 24 applies that model to the crises that beset some middle-income countries

Chapter 24 CRISES IN EMERGING MARKETS The previous chapter extended the IS-LM-BP model to accommodate high capital mobility. Chapter 24 applies that model to the crises that beset some middle-income countries

Jürgen Stark: Financial stability the role of central banks. A new task? A new strategy? New tools?

Jürgen Stark: Financial stability the role of central banks. A new task? A new strategy? New tools? Speech by Mr Jürgen Stark, Member of the Executive Board of the European Central Bank, at the Frankfurt

Jürgen Stark: Financial stability the role of central banks. A new task? A new strategy? New tools? Speech by Mr Jürgen Stark, Member of the Executive Board of the European Central Bank, at the Frankfurt

The Crisis and Beyond: Financial Sector Policies. Asli Demirguc-Kunt The World Bank May 2011

The Crisis and Beyond: Financial Sector Policies Asli Demirguc-Kunt The World Bank May 2011 Financial crisis crisis of confidence in policies The global crisis and the response to the crisis extensive

The Crisis and Beyond: Financial Sector Policies Asli Demirguc-Kunt The World Bank May 2011 Financial crisis crisis of confidence in policies The global crisis and the response to the crisis extensive

Basel III market and regulatory compromise

Basel III market and regulatory compromise Journal of Banking Regulation (2011) 12, 95 99. doi:10.1057/jbr.2011.4 The Basel Committee on Banking Supervision was able to conclude its negotiations on the

Basel III market and regulatory compromise Journal of Banking Regulation (2011) 12, 95 99. doi:10.1057/jbr.2011.4 The Basel Committee on Banking Supervision was able to conclude its negotiations on the

The Central Bank of Egypt

The Current Issues in Regulation and Supervision of the Financial Sector in MENA Region Gamal Negm Deputy Governor Abu Dhabi, UAE,19 November 2013 Current Situation Arab Spring and its effect on: 1. Political

The Current Issues in Regulation and Supervision of the Financial Sector in MENA Region Gamal Negm Deputy Governor Abu Dhabi, UAE,19 November 2013 Current Situation Arab Spring and its effect on: 1. Political

Remarks of Nout Wellink Chairman, Basel Committee on Banking Supervision President, De Nederlandsche Bank

Remarks of Nout Wellink Chairman, Basel Committee on Banking Supervision President, De Nederlandsche Bank Korea FSB Financial Reform Conference: An Emerging Market Perspective Seoul, Republic of Korea

Remarks of Nout Wellink Chairman, Basel Committee on Banking Supervision President, De Nederlandsche Bank Korea FSB Financial Reform Conference: An Emerging Market Perspective Seoul, Republic of Korea

Future strategies for regional financial development

Future strategies for regional financial development March 2, 2009 Tokyo, Japan Noritaka Akamatsu The World Bank Issues Implications of the global financial crisis for the Asian markets and the main policy

Future strategies for regional financial development March 2, 2009 Tokyo, Japan Noritaka Akamatsu The World Bank Issues Implications of the global financial crisis for the Asian markets and the main policy

POLICY BRIEF ON CORPORATE GOVERNANCE OF BANKS Building Blocks (draft for discussion purposes) WORKING GROUP 5

WORKING GROUP 5") WORKING GROUP 5 IMPROVING CORPORATE GOVERNANCE IN THE MIDDLE EAST AND NORTH AFRICA POLICY BRIEF ON CORPORATE GOVERNANCE OF BANKS Building Blocks (draft for discussion purposes) Contact: Elena.Miteva @OECD.org,

WORKING GROUP 5 IMPROVING CORPORATE GOVERNANCE IN THE MIDDLE EAST AND NORTH AFRICA POLICY BRIEF ON CORPORATE GOVERNANCE OF BANKS Building Blocks (draft for discussion purposes) Contact: Elena.Miteva @OECD.org,

GCC/ MENA macro outlook. Khatija Haque, Head of MENA Research March 2018

GCC/ MENA macro outlook Khatija Haque, Head of MENA Research March 18 1 % y/y GCC: Is the worst behind us? Average GCC GDP growth 1 and 17 have been challenging on a number of fronts for the GCC. Lower

GCC/ MENA macro outlook Khatija Haque, Head of MENA Research March 18 1 % y/y GCC: Is the worst behind us? Average GCC GDP growth 1 and 17 have been challenging on a number of fronts for the GCC. Lower

International Monetary and Financial Committee

International Monetary and Financial Committee Twenty-Ninth Meeting April 12, 2014 Statement by Siim Kallas, Vice-President of the European Commission On behalf of the European Commission Statement of

International Monetary and Financial Committee Twenty-Ninth Meeting April 12, 2014 Statement by Siim Kallas, Vice-President of the European Commission On behalf of the European Commission Statement of

THE NEW ECONOMY RECESSION: ECONOMIC SCORECARD 2001

THE NEW ECONOMY RECESSION: ECONOMIC SCORECARD 2001 By Dean Baker December 20, 2001 Now that it is officially acknowledged that a recession has begun, most economists are predicting that it will soon be

THE NEW ECONOMY RECESSION: ECONOMIC SCORECARD 2001 By Dean Baker December 20, 2001 Now that it is officially acknowledged that a recession has begun, most economists are predicting that it will soon be

Øystein Olsen: The economic outlook

Øystein Olsen: The economic outlook Address by Mr Øystein Olsen, Governor of Norges Bank (Central Bank of Norway), to invited foreign embassy representatives, Oslo, 29 March 2011. The address is based

Øystein Olsen: The economic outlook Address by Mr Øystein Olsen, Governor of Norges Bank (Central Bank of Norway), to invited foreign embassy representatives, Oslo, 29 March 2011. The address is based

Iceland s crisis and recovery: are there lessons for the eurozone and its member countries?

Central Bank of Iceland Iceland s crisis and recovery: are there lessons for the eurozone and its member countries? Már Guðmundsson Governor, Central Bank of Iceland Levy Institute conference, Athens,

Central Bank of Iceland Iceland s crisis and recovery: are there lessons for the eurozone and its member countries? Már Guðmundsson Governor, Central Bank of Iceland Levy Institute conference, Athens,

Policy Options for Dealing with the Impact of the Financial Crisis on the External Debt of Developing Countries

U.N. Department of Economic and Social Affairs Financing for Development Office Policy Options for Dealing with the Impact of the Financial Crisis on the External Debt of Developing Countries Implementation

U.N. Department of Economic and Social Affairs Financing for Development Office Policy Options for Dealing with the Impact of the Financial Crisis on the External Debt of Developing Countries Implementation

Global Recession: How Long? How Deep?

Global Recession: How Long? How Deep? M. Ayhan Kose Research Department International Monetary Fund Presentation at the Tusiad-Koc University ERF conference on Global Economic Crisis and the Turkish Economy"

Global Recession: How Long? How Deep? M. Ayhan Kose Research Department International Monetary Fund Presentation at the Tusiad-Koc University ERF conference on Global Economic Crisis and the Turkish Economy"

Press release 557 th Meeting of the Governing Board of the Bank of Slovenia Ljubljana, 7 June 2016

Press release 557 th Meeting of the Governing Board of the Bank of Slovenia Ljubljana, 7 June 2016 The Governing Board of the Bank of Slovenia discussed the June 2016 Macroeconomic Forecast for Slovenia*

Press release 557 th Meeting of the Governing Board of the Bank of Slovenia Ljubljana, 7 June 2016 The Governing Board of the Bank of Slovenia discussed the June 2016 Macroeconomic Forecast for Slovenia*

The usage of surveys to overrun data gaps: Bank Indonesia s experience

The usage of surveys to overrun data gaps: Bank Indonesia s experience Hendy Sulistiowaty and Ari Nopianti I. Introduction The global economic recession that triggered in late 2007 in the United States

The usage of surveys to overrun data gaps: Bank Indonesia s experience Hendy Sulistiowaty and Ari Nopianti I. Introduction The global economic recession that triggered in late 2007 in the United States

The Global Financial Crisis and its Impact on India s External Sector

MPRA Munich Personal RePEc Archive The Global Financial Crisis and its Impact on India s External Sector DR JOMON MATHEW SREENILAYAM Department of Economics, University College Trivandrum, Kerala, india

MPRA Munich Personal RePEc Archive The Global Financial Crisis and its Impact on India s External Sector DR JOMON MATHEW SREENILAYAM Department of Economics, University College Trivandrum, Kerala, india

The Irish Crisis. Philip R. Lane Trinity College Dublin. New Zealand Treasury, 8th December 2010 / 22

Philip R. Lane Trinity College Dublin Introduction Economic Crisis: GDP decline of 15 percent between 2007-2010 Fiscal Crisis: Surplus in 2007; core GGB of -11.5 percent in 2009 and 2010 Banking Crisis:

Philip R. Lane Trinity College Dublin Introduction Economic Crisis: GDP decline of 15 percent between 2007-2010 Fiscal Crisis: Surplus in 2007; core GGB of -11.5 percent in 2009 and 2010 Banking Crisis:

THE GLOBAL ECONOMY: SECULAR STAGNATION OR RECOVERY AT LAST? Adair Turner Chairman Institute for New Economic Thinking

THE GLOBAL ECONOMY: SECULAR STAGNATION OR RECOVERY AT LAST? Adair Turner Chairman Institute for New Economic Thinking Institutional Money Kongress Frankfurt, 21 February 2017 300 Park Avenue South - 5

THE GLOBAL ECONOMY: SECULAR STAGNATION OR RECOVERY AT LAST? Adair Turner Chairman Institute for New Economic Thinking Institutional Money Kongress Frankfurt, 21 February 2017 300 Park Avenue South - 5

GENERAL FUND REVENUE & ECONOMIC OUTLOOK. October 17, 2008

GENERAL FUND REVENUE & ECONOMIC OUTLOOK October 17, 2008 Highlights Downward economic trends in the economy continue to effect economy-based taxes such as the sales tax and personal income withholding

GENERAL FUND REVENUE & ECONOMIC OUTLOOK October 17, 2008 Highlights Downward economic trends in the economy continue to effect economy-based taxes such as the sales tax and personal income withholding

GLOBAL INVESTMENT IN INFRASTRUCTURE: THE ROLE OF OIL EXPORTERS

GLOBAL INVESTMENT IN INFRASTRUCTURE: THE ROLE OF OIL EXPORTERS Shahrokh Fardoust, Ph.D. Research Professor, College of William and Mary President, International Economic Consultants, LLC SFardoust@InternationalEconConsult.com

GLOBAL INVESTMENT IN INFRASTRUCTURE: THE ROLE OF OIL EXPORTERS Shahrokh Fardoust, Ph.D. Research Professor, College of William and Mary President, International Economic Consultants, LLC SFardoust@InternationalEconConsult.com

MANAGING CAPITAL FLOWS: LESSONS FROM EMERGING MARKETS FOR FRONTIER ECONOMIES: POLICY RESPONSES TO CAPITAL INFLOWS IN GHANA

MANAGING CAPITAL FLOWS: LESSONS FROM EMERGING MARKETS FOR FRONTIER ECONOMIES: POLICY RESPONSES TO CAPITAL INFLOWS IN GHANA Mr. Millison Narh First Deputy Governor Bank of Ghana OUTLINE Introduction Trends

MANAGING CAPITAL FLOWS: LESSONS FROM EMERGING MARKETS FOR FRONTIER ECONOMIES: POLICY RESPONSES TO CAPITAL INFLOWS IN GHANA Mr. Millison Narh First Deputy Governor Bank of Ghana OUTLINE Introduction Trends

The Financial Crisis in Emerging Markets: Lessons for Global and Not-So-Global Financial Architecture

The Financial Crisis in Emerging Markets: Lessons for Global and Not-So-Global Financial Architecture Conference Preventing the Next Financial Crisis Columbia University, December 11, 2008 Erik Berglof

The Financial Crisis in Emerging Markets: Lessons for Global and Not-So-Global Financial Architecture Conference Preventing the Next Financial Crisis Columbia University, December 11, 2008 Erik Berglof

Managing Global Shocks: The Case of Indonesia

Managing Global Shocks: The Case of Indonesia Dr. Hartadi A. Sarwono Deputy Governor IIF Asian Regional Economic Forum Singapore, March 5, 2009 Outline 2 1. Crisis highlights 2. Macroconomic Condition

Managing Global Shocks: The Case of Indonesia Dr. Hartadi A. Sarwono Deputy Governor IIF Asian Regional Economic Forum Singapore, March 5, 2009 Outline 2 1. Crisis highlights 2. Macroconomic Condition

TAKAFUL CONFERENCE ON ISLAMIC INVESTMENT MANAGEMENT 12 FEBRUARY 2008, DUBAI. KEYNOTE ADDRESS Dr. Nasser Saidi Chief Economist, DIFCA

TAKAFUL CONFERENCE ON ISLAMIC INVESTMENT MANAGEMENT 12 FEBRUARY 2008, DUBAI KEYNOTE ADDRESS Dr. Nasser Saidi Chief Economist, DIFCA It is indeed a pleasure and an honour for me to address participants

TAKAFUL CONFERENCE ON ISLAMIC INVESTMENT MANAGEMENT 12 FEBRUARY 2008, DUBAI KEYNOTE ADDRESS Dr. Nasser Saidi Chief Economist, DIFCA It is indeed a pleasure and an honour for me to address participants

POLICY BRIEF ON CORPORATE GOVERNANCE OF BANKS Building Blocks

WORKING GROUP ON CORPORATE GOVERNANCE POLICY BRIEF ON CORPORATE GOVERNANCE OF BANKS Building Blocks Joint Secretariat: OECD Hawkamah Contacts: Elena.Miteva@OECD.org, Tel.: 00331 4524 7667 Nick.Nadal@Hawkamah.org,

WORKING GROUP ON CORPORATE GOVERNANCE POLICY BRIEF ON CORPORATE GOVERNANCE OF BANKS Building Blocks Joint Secretariat: OECD Hawkamah Contacts: Elena.Miteva@OECD.org, Tel.: 00331 4524 7667 Nick.Nadal@Hawkamah.org,

The main lessons to be drawn from the European financial crisis

The main lessons to be drawn from the European financial crisis Guido Tabellini Bocconi University and CEPR What are the main lessons to be drawn from the European financial crisis? This column argues

The main lessons to be drawn from the European financial crisis Guido Tabellini Bocconi University and CEPR What are the main lessons to be drawn from the European financial crisis? This column argues

Confronting the Global Crisis in Latin America: What is the Outlook? Coordinators

Confronting the Global Crisis in Latin America: What is the Outlook? Policy Trade-offs May for 20, Unprecedented 2009 - Maison Times: Confronting de l Amérique the Global Crisis Latine, America, ParisIADB,

Confronting the Global Crisis in Latin America: What is the Outlook? Policy Trade-offs May for 20, Unprecedented 2009 - Maison Times: Confronting de l Amérique the Global Crisis Latine, America, ParisIADB,

The Impact of the Crisis on Budget Policy in Central and Eastern Europe: A comparison to Middle East and North African countries

The Impact of the Crisis on Budget Policy in Central and Eastern Europe: A comparison to Middle East and North African countries Zsolt Darvas 2th Annual Meeting of OECD-MENA Senior Budget Officials Doha,

The Impact of the Crisis on Budget Policy in Central and Eastern Europe: A comparison to Middle East and North African countries Zsolt Darvas 2th Annual Meeting of OECD-MENA Senior Budget Officials Doha,

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 9 Financial Crises. 9.1 What is a Financial Crisis?

Chapter 9 Financial Crises. 9.1 What is a Financial Crisis?") Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 9 Financial Crises 9.1 What is a Financial Crisis? 1) A major disruption in financial markets characterized by sharp declines in asset

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 9 Financial Crises 9.1 What is a Financial Crisis? 1) A major disruption in financial markets characterized by sharp declines in asset

International Monetary and Financial Committee

International Monetary and Financial Committee Thirty-Third Meeting April 16, 2016 IMFC Statement by Angel Gurría Secretary-General The Organisation for Economic Co-operation and Development (OECD) IMF

International Monetary and Financial Committee Thirty-Third Meeting April 16, 2016 IMFC Statement by Angel Gurría Secretary-General The Organisation for Economic Co-operation and Development (OECD) IMF

Insure Egypt Briefings

Low Oil Prices and Political Instability Provide Testing Times for Middle East & North Africa Insurance Markets A.M.Best Once viewed as an economic powerhouse amongst emerging markets, with seemingly unstoppable

Low Oil Prices and Political Instability Provide Testing Times for Middle East & North Africa Insurance Markets A.M.Best Once viewed as an economic powerhouse amongst emerging markets, with seemingly unstoppable

Transparency & Disclosure in Capital Markets. Nick Nadal 26 January 2010

Transparency & Disclosure in Capital Markets Nick Nadal 26 January 2010 Disclosure and Transparency basics There is a symbiotic relationship between market information and market efficiency Better quality

Transparency & Disclosure in Capital Markets Nick Nadal 26 January 2010 Disclosure and Transparency basics There is a symbiotic relationship between market information and market efficiency Better quality

Corporate Governance in the GCC

Corporate Governance in the GCC Middle East IPO Summit 2007 Dubai, UAE Dr. Nasser Saidi Executive Director, Hawkamah Overview Corporate Governance in Emerging Markets Corporate Governance and Access to

Corporate Governance in the GCC Middle East IPO Summit 2007 Dubai, UAE Dr. Nasser Saidi Executive Director, Hawkamah Overview Corporate Governance in Emerging Markets Corporate Governance and Access to

Angola - Economic Report

Angola - Economic Report Index I. Assumptions on National Policy and External Environment... 2 II. Recent Trends... 3 A. Real Sector Developments... 3 B. Monetary and Financial sector developments... 5

Angola - Economic Report Index I. Assumptions on National Policy and External Environment... 2 II. Recent Trends... 3 A. Real Sector Developments... 3 B. Monetary and Financial sector developments... 5

HC 676 SesSIon december HM Treasury. Maintaining the financial stability of UK banks: update on the support schemes

Report by the Comptroller and Auditor General HC 676 SesSIon 2010 2011 15 december 2010 HM Treasury Maintaining the financial stability of UK banks: update on the support schemes Report by the Comptroller

Report by the Comptroller and Auditor General HC 676 SesSIon 2010 2011 15 december 2010 HM Treasury Maintaining the financial stability of UK banks: update on the support schemes Report by the Comptroller

The Economic Outlook and The Fed s Roles in Monetary Policy and Financial Stability

1 The Economic Outlook and The Fed s Roles in Monetary Policy and Financial Stability Main Line Chamber of Commerce Economic Forecast Breakfast Philadelphia Country Club, Gladwyne, PA January 8, 2008 Charles

1 The Economic Outlook and The Fed s Roles in Monetary Policy and Financial Stability Main Line Chamber of Commerce Economic Forecast Breakfast Philadelphia Country Club, Gladwyne, PA January 8, 2008 Charles

Macroprudential Policies

Macroprudential Policies Bank Indonesia International Workshop and Seminar Central Bank Policy Mix: Issues, Challenges and Policies Jakarta, 9-13 April 2018 Yoke Wang Tok The views expressed herein are

Macroprudential Policies Bank Indonesia International Workshop and Seminar Central Bank Policy Mix: Issues, Challenges and Policies Jakarta, 9-13 April 2018 Yoke Wang Tok The views expressed herein are

What Is Corporate Governance and Why Do We Need It?

What Is Corporate Governance and Why Do We Need It? Dr. Nasser Saidi Executive Director Hawkamah ICG Chief Economist, DIFC LCGTF CG Code Workshop 2 March 2007 Agenda Basics: what is Governance? Corporate

What Is Corporate Governance and Why Do We Need It? Dr. Nasser Saidi Executive Director Hawkamah ICG Chief Economist, DIFC LCGTF CG Code Workshop 2 March 2007 Agenda Basics: what is Governance? Corporate

Economic Fundamentals

CHAPTER 5 Economic Fundamentals INTRODUCTION Economics, put simply, is the study of shortages supply vs. demand. As the demand for a product or service rises, the price of those goods or services will

CHAPTER 5 Economic Fundamentals INTRODUCTION Economics, put simply, is the study of shortages supply vs. demand. As the demand for a product or service rises, the price of those goods or services will

Impact of Financial Crisis on Emerging Economies

Impact of Financial Crisis on Emerging Economies PRINCY JAIN Assistant Professor in Economics Abstract: This paper talks about financial crisis of 2008 which had hit all the nations of the world. This

Impact of Financial Crisis on Emerging Economies PRINCY JAIN Assistant Professor in Economics Abstract: This paper talks about financial crisis of 2008 which had hit all the nations of the world. This

The Great Depression, golden age, and global financial crisis

The Great Depression, golden age, and global financial crisis ECONOMICS Dr. Kumar Aniket Bartlett School of Construction & Project Management Lecture 17 CONTEXT Good policies and institutions can promote

The Great Depression, golden age, and global financial crisis ECONOMICS Dr. Kumar Aniket Bartlett School of Construction & Project Management Lecture 17 CONTEXT Good policies and institutions can promote

Macroeconomics, Cdn. 4e (Williamson) Chapter 1 Introduction

Chapter 1 Introduction") Macroeconomics, Cdn. 4e (Williamson) Chapter 1 Introduction 1) Which of the following topics is a primary concern of macro economists? A) standards of living of individuals B) choices of individual consumers

Macroeconomics, Cdn. 4e (Williamson) Chapter 1 Introduction 1) Which of the following topics is a primary concern of macro economists? A) standards of living of individuals B) choices of individual consumers

Dr. Raja M. Almarzoqi Albqami Institute of Diplomatic Studies

Dr. Raja M. Almarzoqi Albqami Institute of Diplomatic Studies Rmarzoqi@gmail.com 3 nd Meeting of OECD-MENA Senior Budget Officials Network Dubai, United Arab Emirates, 31 October-1 November 2010 Oil Exporters

Dr. Raja M. Almarzoqi Albqami Institute of Diplomatic Studies Rmarzoqi@gmail.com 3 nd Meeting of OECD-MENA Senior Budget Officials Network Dubai, United Arab Emirates, 31 October-1 November 2010 Oil Exporters

ASSESSING THE RISK OF A DOUBLE-DIP RECESSION: KEY INDICATORS TO MONITOR

Weekly Economic Perspective ASSESSING THE RISK OF A DOUBLE-DIP RECESSION: KEY INDICATORS TO MONITOR August 2, 2010 Robert F. DeLucia, CFA Consulting Economist Summary and Major Conclusions: Heightened

Weekly Economic Perspective ASSESSING THE RISK OF A DOUBLE-DIP RECESSION: KEY INDICATORS TO MONITOR August 2, 2010 Robert F. DeLucia, CFA Consulting Economist Summary and Major Conclusions: Heightened

Banking on Turkey, October 21, 2008

Banking on Turkey, October 21, 2008 Slide 1. Title Slide Good morning. The global economic downturn and financial turmoil mean that economic growth will slow down in Turkey. There will be much slower growth,

Banking on Turkey, October 21, 2008 Slide 1. Title Slide Good morning. The global economic downturn and financial turmoil mean that economic growth will slow down in Turkey. There will be much slower growth,

The Banking System in Cyprus: Time to Rethink the Business Model?

123 Cyprus Economic Policy Review, Vol. 5, No. 2, pp. 123-130 (2011) 1450-4561 The Banking System in Cyprus: Time to Rethink the Business Model? Constantinos Stephanou World Bank 1. Banking System Characteristics

123 Cyprus Economic Policy Review, Vol. 5, No. 2, pp. 123-130 (2011) 1450-4561 The Banking System in Cyprus: Time to Rethink the Business Model? Constantinos Stephanou World Bank 1. Banking System Characteristics

To understand where the U.S. Economy is going, we need to understand where we have been

To understand where the U.S. Economy is going, we need to understand where we have been From 2008:1-2009:2, the worst recession since Great Depression, with a slow recovery from 2009:3-2013:1. Historical

To understand where the U.S. Economy is going, we need to understand where we have been From 2008:1-2009:2, the worst recession since Great Depression, with a slow recovery from 2009:3-2013:1. Historical

Standard Chartered sees a resilient Asia, Middle East and Africa in 2012

Standard Chartered sees a resilient Asia, Middle East and Africa in 2012 Bahrain, 24 January, 2012 - Standard Chartered sees 2012 as a year of a two-speed global economy. The Bank, which recently topped

Standard Chartered sees a resilient Asia, Middle East and Africa in 2012 Bahrain, 24 January, 2012 - Standard Chartered sees 2012 as a year of a two-speed global economy. The Bank, which recently topped

EGYPT Affordable Mortgage Finance Program Development Policy Loan (Loan No EG) Release of the Second Tranche Full Compliance

Release of the Second Tranche Full Compliance") Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized EGYPT Affordable Mortgage Finance Program Development Policy Loan (Loan No. 7747-EG)

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized EGYPT Affordable Mortgage Finance Program Development Policy Loan (Loan No. 7747-EG)

THE FINANCIAL CRISIS: KEY QUESTIONS, REALITY AND RESPONSES

THE FINANCIAL CRISIS: KEY QUESTIONS, REALITY AND RESPONSES BANK OF AMERICA MERRILL LYNCH CONFERENCE London 4 October 2011 António Horta-Osório Group Chief Executive AGENDA KEY QUESTIONS ON THE FINANCIAL

THE FINANCIAL CRISIS: KEY QUESTIONS, REALITY AND RESPONSES BANK OF AMERICA MERRILL LYNCH CONFERENCE London 4 October 2011 António Horta-Osório Group Chief Executive AGENDA KEY QUESTIONS ON THE FINANCIAL

I FINANCIAL BEHAVIOUR OF COMPANIES AND HOUSEHOLDS AND THEIR RISKS

I FINANCIAL BEHAVIOUR OF COMPANIES AND HOUSEHOLDS AND THEIR RISKS COMPANIES Business situation Confidence The confidence of companies declined further at the beginning of 29 owing to the current global

I FINANCIAL BEHAVIOUR OF COMPANIES AND HOUSEHOLDS AND THEIR RISKS COMPANIES Business situation Confidence The confidence of companies declined further at the beginning of 29 owing to the current global

Bank of Ghana Monetary Policy Committee Press Release

Bank of Ghana Monetary Policy Committee Press Release November 26, 2018 Ladies and Gentlemen of the Press, welcome to this morning s press conference following the 85th regular meeting of the Monetary

Bank of Ghana Monetary Policy Committee Press Release November 26, 2018 Ladies and Gentlemen of the Press, welcome to this morning s press conference following the 85th regular meeting of the Monetary

HIGHER CAPITAL IS NOT A SUBSTITUTE FOR STRESS TESTS. Nellie Liang, The Brookings Institution

HIGHER CAPITAL IS NOT A SUBSTITUTE FOR STRESS TESTS Nellie Liang, The Brookings Institution INTRODUCTION One of the key innovations in financial regulation that followed the financial crisis was stress

HIGHER CAPITAL IS NOT A SUBSTITUTE FOR STRESS TESTS Nellie Liang, The Brookings Institution INTRODUCTION One of the key innovations in financial regulation that followed the financial crisis was stress

Presentation. The Boom in Capital Flows and Financial Vulnerability in Asia

High-level Regional Policy Dialogue on "Asia-Pacific economies after the global financial crisis: Lessons learnt, challenges for building resilience, and issues for global reform" 6-8 September 2011, Manila,

High-level Regional Policy Dialogue on "Asia-Pacific economies after the global financial crisis: Lessons learnt, challenges for building resilience, and issues for global reform" 6-8 September 2011, Manila,

The New Role of Growth Financing

OMV Aktiengesellschaft The New Role of Growth Financing Conference on European Economic Integration Vienna, 15 November 2010 Wolfgang Ruttenstorfer CEO and Chairman of the Executive Board OMV Aktiengesellschaft

OMV Aktiengesellschaft The New Role of Growth Financing Conference on European Economic Integration Vienna, 15 November 2010 Wolfgang Ruttenstorfer CEO and Chairman of the Executive Board OMV Aktiengesellschaft

Resilience in Emerging Market and Developing Economies: Will It Last?

International Monetary Fund World Economic Outlook October 212 Resilience in Emerging Market and Developing Economies: Will It Last? Abdul Abiad, John Bluedorn, Jaime Guajardo, and Petia Topalova with

International Monetary Fund World Economic Outlook October 212 Resilience in Emerging Market and Developing Economies: Will It Last? Abdul Abiad, John Bluedorn, Jaime Guajardo, and Petia Topalova with

Assalamu alaikumwr. Wb, Very good morning to all of you, Honourable speakers, Distinguished Guests, Ladies and Gentlemen,

Opening Remarks Dr. Hartadi A. Sarwono, Deputy Governor of Bank Indonesia The 9 th Bank Indonesia Annual International Seminar Nusa Dua-Bali, December 9 th, 2011 Assalamu alaikumwr. Wb, Very good morning

Opening Remarks Dr. Hartadi A. Sarwono, Deputy Governor of Bank Indonesia The 9 th Bank Indonesia Annual International Seminar Nusa Dua-Bali, December 9 th, 2011 Assalamu alaikumwr. Wb, Very good morning

Asia s Debt Risks The risk of financial crises is limited, but attention should be paid to slowing domestic demand.

Mizuho Economic Outlook & Analysis November 15, 218 Asia s Debt Risks The risk of financial crises is limited, but attention should be paid to slowing domestic demand. < Summary > Expanding private debt

Mizuho Economic Outlook & Analysis November 15, 218 Asia s Debt Risks The risk of financial crises is limited, but attention should be paid to slowing domestic demand. < Summary > Expanding private debt

UNCTAD s Seventh Debt Management Conference. Addressing Debt Vulnerabilities: Role of Debt Strategies and Debt Managers A Policy Perspective

UNCTAD s Seventh Debt Management Conference 9-11 November 2009 Addressing Debt Vulnerabilities: Role of Debt Strategies and Debt Managers A Policy Perspective by Mr. Udaibir S. Das Monetary and Capital

UNCTAD s Seventh Debt Management Conference 9-11 November 2009 Addressing Debt Vulnerabilities: Role of Debt Strategies and Debt Managers A Policy Perspective by Mr. Udaibir S. Das Monetary and Capital

The OECD Global Economic Outlook

The OECD Global Economic Outlook Nigel Pain OECD Economics Department Edinburgh, 11 July 2013 NCSL Symposium for Legislative Leaders 1 Overview Presentation structure Current situation and prospects. Global

The OECD Global Economic Outlook Nigel Pain OECD Economics Department Edinburgh, 11 July 2013 NCSL Symposium for Legislative Leaders 1 Overview Presentation structure Current situation and prospects. Global

Sample Exam 1: QEII Labor Market Rescue?

Sample Exam 1: QEII Labor Market Rescue? It seems the people who most need an economic recovery are the last to benefit. Currently the U.S. is experiencing a slow recovery, and like the last two, a jobless

Sample Exam 1: QEII Labor Market Rescue? It seems the people who most need an economic recovery are the last to benefit. Currently the U.S. is experiencing a slow recovery, and like the last two, a jobless

Balance of Payments, Debt, Financial Crises, and Stabilization Policies

Chapter 9 Balance of Payments, Debt, Financial Crises, and Stabilization Policies Problems and Policies: international and macro 1 International Finance and Investment: Key Issues How major debt crises

Chapter 9 Balance of Payments, Debt, Financial Crises, and Stabilization Policies Problems and Policies: international and macro 1 International Finance and Investment: Key Issues How major debt crises

I. Global, U.S., and Canadian Outlook

I. Global, U.S., and Canadian Outlook Global Outlook The world economy continues to be buffeted by the burgeoning downdraft of the financial crisis and volatile commodity prices. As such, the outlook points

I. Global, U.S., and Canadian Outlook Global Outlook The world economy continues to be buffeted by the burgeoning downdraft of the financial crisis and volatile commodity prices. As such, the outlook points

Speech by Mr. Amando M. Tetangco, Jr. Governor, Bangko Sentral ng Pilipinas

Speech by Mr. Amando M. Tetangco, Jr. Governor, Bangko Sentral ng Pilipinas At the International symposium hosted by the Center for Monetary Cooperation in Asia (CeMCoA) of the on January 22, 2007 in Tokyo

Speech by Mr. Amando M. Tetangco, Jr. Governor, Bangko Sentral ng Pilipinas At the International symposium hosted by the Center for Monetary Cooperation in Asia (CeMCoA) of the on January 22, 2007 in Tokyo

MENAP Oil-Importing Countries: Risks to the Recovery Persist

MENAP Oil-Importing Countries: Risks to the Recovery Persist The growth recovery in the Middle East, North Africa, Afghanistan, and Pakistan (MENAP) oil-importing countries is set to continue in 18, lifted

MENAP Oil-Importing Countries: Risks to the Recovery Persist The growth recovery in the Middle East, North Africa, Afghanistan, and Pakistan (MENAP) oil-importing countries is set to continue in 18, lifted

Financial System Stabilized, but Exit, Reform, and Fiscal Challenges Lie Ahead

January 21 Financial System Stabilized, but Exit, Reform, and Fiscal Challenges Lie Ahead Systemic risks have continued to subside as economic fundamentals have improved and substantial public support

January 21 Financial System Stabilized, but Exit, Reform, and Fiscal Challenges Lie Ahead Systemic risks have continued to subside as economic fundamentals have improved and substantial public support

In January 2017 UK Public sector net debt is 1,682.8 billion equivalent to 85.3% of GDP

UK National Debt Budget deficit annual borrowing... 2 UK net borrowing... 3 UK net borrowing as % of GDP... 3 Deficit down but debt up?... 4 Debt as % of GDP... 4 Recent history of UK National Debt...

UK National Debt Budget deficit annual borrowing... 2 UK net borrowing... 3 UK net borrowing as % of GDP... 3 Deficit down but debt up?... 4 Debt as % of GDP... 4 Recent history of UK National Debt...

: Monetary Economics and the European Union. Lecture 8. Instructor: Prof Robert Hill. The Costs and Benefits of Monetary Union II

320.326: Monetary Economics and the European Union Lecture 8 Instructor: Prof Robert Hill The Costs and Benefits of Monetary Union II De Grauwe Chapters 3, 4, 5 1 1. Countries in Trouble in the Eurozone

320.326: Monetary Economics and the European Union Lecture 8 Instructor: Prof Robert Hill The Costs and Benefits of Monetary Union II De Grauwe Chapters 3, 4, 5 1 1. Countries in Trouble in the Eurozone

MACRO-ECONOMICS AND MACRO FINANCIAL CRISIS

MACRO-ECONOMICS AND MACRO FINANCIAL CRISIS Dr. Lê Xuân Ngh a 1. The world economy and perspectives. The recovery of the US economy continues to face difficulties. The CPI decreased by 0.1% in June indicating

MACRO-ECONOMICS AND MACRO FINANCIAL CRISIS Dr. Lê Xuân Ngh a 1. The world economy and perspectives. The recovery of the US economy continues to face difficulties. The CPI decreased by 0.1% in June indicating