Future of Digitalization & Preparing for a New Reality. Najib Choucair Executive Director Banking Department May 2017

|

|

|

- Lee Washington

- 5 years ago

- Views:

Transcription

1 Future of Digitalization & Preparing for a New Reality Najib Choucair Executive Director Banking Department May 2017

2 In 1993, and after the civil war, the Lebanese economy was practically ruined. BDL s main purpose was to rebuild confidence in the Lebanese banking and financial sector in order to attract foreign investors and new deposits in the banking sectors. Main challenges that the bank had were that: Total assets were less than 11 billion USD Deposits were about 9 billion USD Loans to the private sector were about 3 billion with an NPL ratio of more than 24% distributed to only 32,000 clients Capital base was only about 260 million USD BDL undertook 4 steps to strengthen & develop the banking sector:

3 1- Effective laws and regulations to help support BDLs mission to grow the financial ecosystem. Initiatives include: Encouraging merging and acquisitions between banks to crowd out weak banks Setting corporate governance rules according to international standards Imposing capital requirements and liquidity ratios in compliance with BASEL III Supporting enactment of the anti-money laundry and terrorist financing Setting laws for consumer protection Encouraging electronic banking and financial operations

4 2- Stable exchange rate has proved to be key in the stability of the financial system by: a. Maintaining low rates of inflation b. Preserving a sound banking sector c. Boosting the central bank s foreign reserves d. Reinforcing Lebanon s credibility in the international capital markets scene

5 3- Building an efficient financial infrastructure, was set as a major objective such as Regulating credit cards, e-payments, and e- banking Establishing real time growth settlement (RTGS) and electronic clearing system Meeting international standards and best practices in payment systems Playing an essential role in the establishment of the capital market authority (CMA) Establishing an unpaid check registry to identify offenders Evolving the public credit registry to track payment history, improve transparency, and assess indebtedness of firms and individuals Creating KAFALAT, a guarantee scheme for SMEs

6 4- Set out incentives like Subsidized loans for the productive sector Direct loans at attractive prices Lower the legal reserve requirements These were done to encourage lending to productive sectors, housing loans, SMEs, Micro lending, student loans, green loans, and finally, equity for startups to incite innovation and quick start venture capital sectors.

7 The introduction of BDL circular 331 The purpose of Circular 331 is essentially to promote the Startups sector in Lebanon and to create a hub for startups, innovation and technology in the area. One of the most prominent ways to reach such purpose is to invest in Fin-tech opportunities provided that the targeted project is innovative, relies on knowledge economy and creates jobs in Lebanon. Thus, the financial benefits offered by BDL under Circular 331 do play a big role in promoting investments in Fin-tech companies with an ultimate goal of reaching successful exits. Exit strategies are freely set by the professional teams who manage Circular 331 funds within general guidelines that are issued by BDL.

8 Banking Sector in Lebanon Asset Private Sector Loans Capital Acc. Deposits * In millions of USD Dollars Dec-93 Dec-00 Dec-07 May-16 Average number of clients served/per branch May Banks 3,846 1,040 Banks Branches 2,343 1,707 ATMs

9 déc.-94 déc.-95 déc.-96 déc.-97 déc.-98 déc.-99 déc.-00 déc.-01 déc.-02 déc.-03 déc.-04 déc.-05 déc.-06 déc.-07 déc.-08 déc.-09 déc.-10 déc.-11 déc.-12 déc.-13 déc.-14 déc.-15 Number of Clients Total Clients Declared at the Credit Registry Years

10 déc.-94 déc.-95 déc.-96 déc.-97 déc.-98 déc.-99 déc.-00 déc.-01 déc.-02 déc.-03 déc.-04 déc.-05 déc.-06 déc.-07 déc.-08 déc.-09 déc.-10 déc.-11 déc.-12 déc.-13 déc.-14 déc.-15 Number of Clients Query Requests from PCR Years

11 Retail Loans Retail Portfolio Definition a- Consumer loans (including car loans, educational loans ) b- Revolving credits (including credit cards and current accounts). c- Housing loans Retail Portfolio (Millions) Dec-96 Dec-00 Dec-16 Retail (In Millions of USD) 750 1,817 19,396 Percentage of total loans 10.88% 11.85% 29.52% Beneficiary 15,273 75, ,134 Percentage of total Beneficiaries 28.28% 54.20% 78.49% Average Loan(in thousands of$) déc.-96 déc.-00 mars-16

Car and housing loans can no longer exceed 75% of the")

.")

12 Retail Loans Household debt ratio reached 44.63% in December 2016 BDL is adopting a preemptive policy that would not allow debt to go beyond the point where it becomes destabilizing for the economy. (Intermediate Circular 369 August 2014) Car and housing loans can no longer exceed 75% of the underlying asset value The cumulative monthly payments for all retail loans must not exceed 35% of the household s monthly income, (defined as the husband and the wife s monthly revenues). For housing loans, the cumulative monthly payments must not exceed 45% of the household s income.

13 The Comptoirs Small & medium size unstructured lenders, often sole-traders, operating in the financial market Not submitted to the oversight of any regulators Have increased along the years, operating under little or no control BDL issued circulars to establish a Licensing Register of comptoirs. The licensed ones only will be allowed to operate and under the control and supervision of the Central Bank to oversee the compliance of these establishments with the law.

14 In our fast moving digital world, banks are facing new challenges: growing disruptors in the market and new entrants: Fin-Techs The Fin-Tech ecosystem is made of small organizations that are spread across different financial functions from payment, to lending and financing, These Fin-Techs impose large threats with banks; Howerver it is large corporations such as Apple, Google, Amazon and Facebook that are imposing the largest threats to the banking industry.

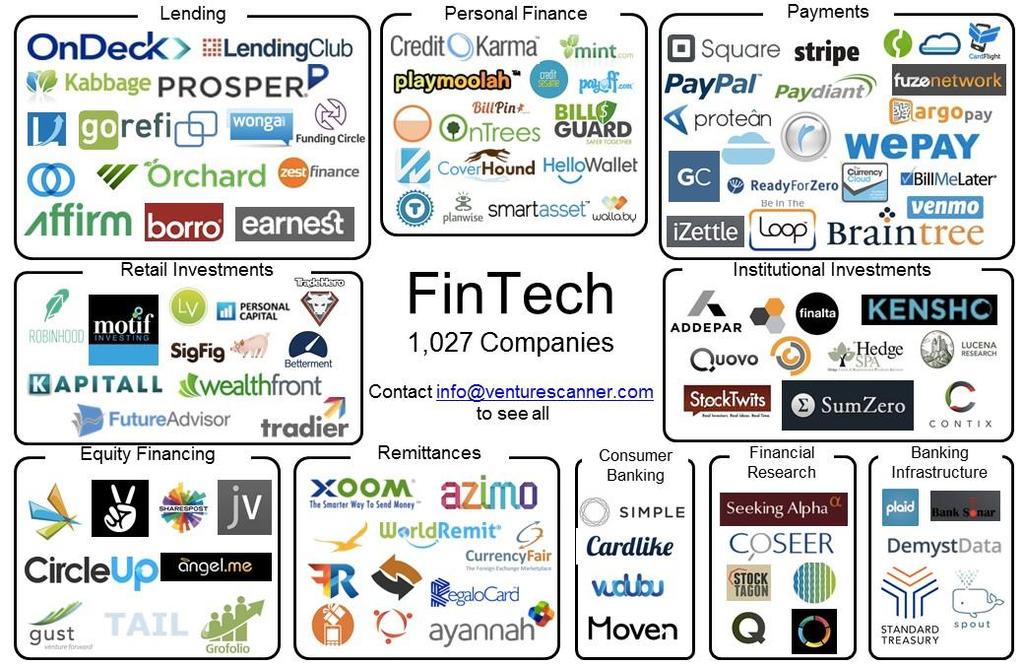

15 Fintech Definition Contraction of the words financial & technology. Fintech broadly refers to the application of technology within the financial industry & covers a wide range of activities.

16 Such activities Include: Crowd Funding Digital Wallets Peer to Peer Lending E-Payments Bitcoin & Blockchain Technologies Robotic Visors Equity Financing Remittances

17 Why they are Attractive? Convinience Speed Simplicity Modernity Security Privacy Intuitiveness

18 They have been growing at a tremendous rate in the past 5 years 65 Billion USD Compared to 10 Billion USD in 2014 Market Share

19 105% Annual Growth Rate

20 11 Billion USD in Annual Revenue for Alternative Lenders Goldman Sachs

21

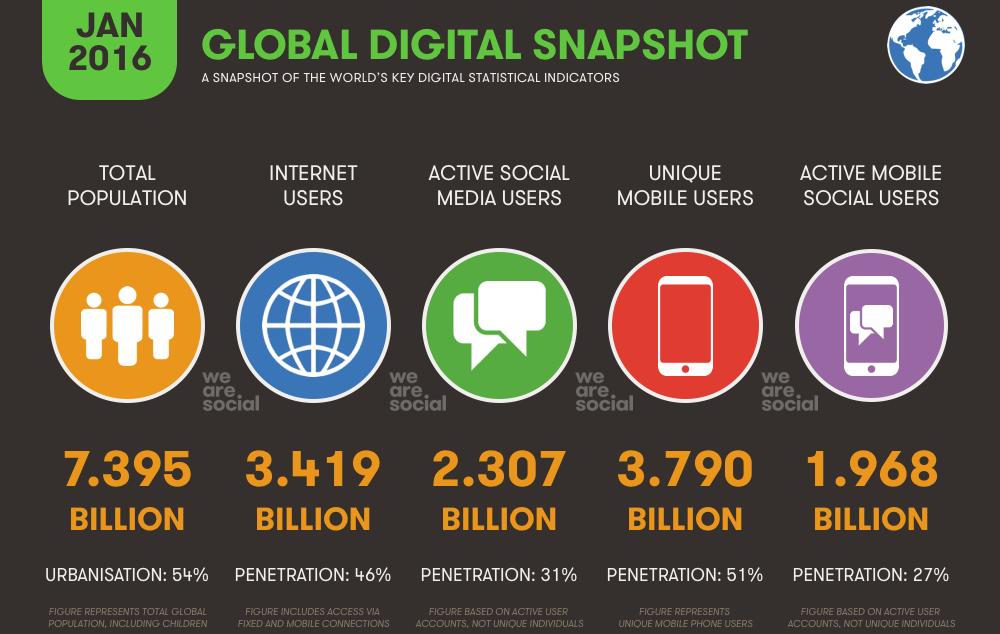

22 What Contribute to the success of Fin-Techs? Technology, Connectivity, and digitalization We now have 50 times faster mobile connection than we had in 2010 There are 3.5 billion internet users in the world 2.3 billion active social media users 3.8 billion active mobile users 80% mobile penetration in housrholds 50% voice calls overtaking international calls(voice calls such as Viber, WhatSapp call, and face time)

23

24 Banking services on Social Networks. Merchants are not alone in their use of social networks to engage customers A study by the Financial Brand found that nearly 75% of financial institutions use Facebook, 54% use Twitter, and 48%use LinkedIn. Though banking on social networks is still in the developmental stage, the financial institutions that are pioneering payment services are able to leverage some aspect of their mobile banking platform to allow customers to send payments to Facebook friends.

25 Mobile Banking As mobile phones become almost abundant, local banks are launching new services for customers to make payments through their phones. People often confuse when banking services are offered on mobile and mobile wallets, whereby electronic money is available on mobile phones, usually requiring new legislation. In Lebanon only mobile applications of existing banking services are allowed so those will not target the unbanked, it is thus simply an extra service to offer to make banking easier to existing customers.

26 Social Media Banking Whatsapp & Facebook Whatsapp Banking Facebook Banking

27 Challenges Just as social network create opportunities for banking, they may also unintentionally introduce risks such as breaches of privacy, fraud and even money laundering. New regulations become necessary, that may have a dampening effect on the potential for social networks to offer new banking opportunities

28 Advantage for Banks Mobile payment tools represent a new way for banks to grow their business. They are attracting low value transactions, reducing cash handling, and gaining additional sources of revenue They do not expect a real return on investment in the first two years Banks are aiming to win more client loyalty. If the customer has all services and products in one bank, he won t leave to another bank. Some banks are still not involved with the new mobile payment tools, arguing that a better penetration rate for the required NFC (Near-Fiels Communication)

Merchants This will save time for the merchant, as receiving money through credit cards")

29 Other Stakeholders Retailers Reduced queues and a better shopping experience Payment can be done from anywhere with a mobile phone, with no need to enter the store. (need an electronic signature law, unless it is linked to a card(like PinPay) Merchants This will save time for the merchant, as receiving money through credit cards may take at least two or three days. Telecom Operators Taking their market share of mobile payment business through partnerships with banks The main role is first on the security level by making sure that the applicant is in the client database They provide the SIM card and application to the client on his mobile to conduct the transaction.

30 Financial Inclusion Banks to integrate financial inclusion into operations, digital payments are the main gateway to new customers, starting with transactional accounts to make and receive payments Start with low-income and informal population and build strategies around deepening inclusion for those customers. Crosssell products that meet these customers needs, such as savings, credit, insurance and pensions E-money products, mainly for the unbanked, to facilitate payments, e-commerce purchases and phone recharging in a convenient, cheap and secure way.

31 Financial Inclusion Approach 1 Analyzing transactional data to support cross-selling. Besides proprietary data, banks are also relying on credit bureaus and alternative data. 2 Increasing access and transaction volumes via vast networks of lowcost and convenient customer service points. 3 Agent banking is increasingly critical in low-income customer acquisition and represents a growing share of transactions. 4 Digital banking (including e-money) is also on the rise, with the aim of many customers becoming self-managing. 5 Banks may seek partners to help customer targeting and acquisition, risk- and cost-sharing, expansion of product offerings and points-of-sale, and access to innovations

32 Financial Inclusion Challenges New Laws & Regulations Lack of financial capability and digital literacy Lack of Trust Tightening of Compliance Regulations Affordability of Agent Networks Data Privacy, Security, Cost & Analysis

33 Recommendations Regardless of the increased importance of the mobile banking and Digitization, the priority should be to increase our efforts to reach the unbanked. the 3 short term priorities to advance Lebanon's Fin-tech ecosystem - Create a set of regulations that can guarantee to a certain extent the safety and soundness of Fin-tech products and protect the rights of the users, aligned with aspirations of the DREAMERS. - Increase the internet speed and make it accessible to all entrepreneurs (actually to everyone). - Educate the young generation about the potential and importance of Fintech in the financial sector of the future in order to generate new ideas and place Lebanon on the international scene.

34 Thank you

Financial Inclusion and Fintech

Financial Inclusion and Fintech The views expressed in this presentation are those of the author and do not necessarily represent the views of the NBC. 2 Agenda Financial Inclusion Landscape Regulatory

Financial Inclusion and Fintech The views expressed in this presentation are those of the author and do not necessarily represent the views of the NBC. 2 Agenda Financial Inclusion Landscape Regulatory

Implications of the Dodd-Frank Act on Too Big to Fail A presentation for Washington University s Life-Long Learning Institute

Implications of the Dodd-Frank Act on Too Big to Fail A presentation for Washington University s Life-Long Learning Institute Julie L. Stackhouse Executive Vice President May 4, 2016 Remember these headlines?

Implications of the Dodd-Frank Act on Too Big to Fail A presentation for Washington University s Life-Long Learning Institute Julie L. Stackhouse Executive Vice President May 4, 2016 Remember these headlines?

I. Content of business

I. Content of business (I) Business activities Jih Sun Financial Holding Co., Ltd. 1. Principal business activities The Company is a financial holding company; its business activities are confined to those

I. Content of business (I) Business activities Jih Sun Financial Holding Co., Ltd. 1. Principal business activities The Company is a financial holding company; its business activities are confined to those

USE CASE. Blockchain Companies Demonstrate Purity of BTC Funds

USE CASE Blockchain Companies Demonstrate Purity of BTC Funds New Blockchain Opportunities and Challenges Blockchain Companies Demonstrate Purity of BTC Funds > New Blockchain Opportunities and Challenges

USE CASE Blockchain Companies Demonstrate Purity of BTC Funds New Blockchain Opportunities and Challenges Blockchain Companies Demonstrate Purity of BTC Funds > New Blockchain Opportunities and Challenges

The Changing World of Payments. Well-Regulated Financial Technology Boosts Inclusion, Fights Cyber Crime

Well-Regulated Financial Technology Boosts Inclusion, Fights Cyber Crime Reading Materials: Inclusive Access to Financial Services Well-Regulated Financial Technology Boosts Inclusion, Fights Cyber Crime

Well-Regulated Financial Technology Boosts Inclusion, Fights Cyber Crime Reading Materials: Inclusive Access to Financial Services Well-Regulated Financial Technology Boosts Inclusion, Fights Cyber Crime

SME Banking: Financing & Digital Banking

SME Banking: Financing & Digital Banking Critical Points for a Successful SME Strategy With more than half of the world s people and businesses, Asia s prospects are bright if it can harness the energy

SME Banking: Financing & Digital Banking Critical Points for a Successful SME Strategy With more than half of the world s people and businesses, Asia s prospects are bright if it can harness the energy

Distinguished guests, Ladies and gentlemen, A very good morning to you all.

Spotlight: Developing a Financial System for the Future Speech by Dr. Veerathai Santiprabhob Governor of the Bank of Thailand Bloomberg ASEAN Business Summit July 12, 2018, Siam Kempinski Hotel, Bangkok

Spotlight: Developing a Financial System for the Future Speech by Dr. Veerathai Santiprabhob Governor of the Bank of Thailand Bloomberg ASEAN Business Summit July 12, 2018, Siam Kempinski Hotel, Bangkok

UKTI - Thai Business Delegation

UKTI - Thai Business Delegation June 3 rd, 2016 Level39, Canary Wharf Agenda 14.00-14.05 Welcome, introductions and agenda Julian Skan 14.05-14.15 Overview of TheCityUK Cameron Jones & Bryan Cress 14.15-14.30

UKTI - Thai Business Delegation June 3 rd, 2016 Level39, Canary Wharf Agenda 14.00-14.05 Welcome, introductions and agenda Julian Skan 14.05-14.15 Overview of TheCityUK Cameron Jones & Bryan Cress 14.15-14.30

Dreaming of a Frictionless Market

Dreaming of a Frictionless Market Digital Transformation in Insurance 2 nd May 2018 B3i 2018 Agenda 1. Background to Blockchain and B3i 2. Current product and future applications 3. Current priorities

Dreaming of a Frictionless Market Digital Transformation in Insurance 2 nd May 2018 B3i 2018 Agenda 1. Background to Blockchain and B3i 2. Current product and future applications 3. Current priorities

Company Overview and Financials. Technology Driven Consumer Finance

Company Overview and Financials Technology Driven Consumer Finance History & Vision Proprietary Process Automation Credissimo developed in-house an innovative technology that introduced automated instant

Company Overview and Financials Technology Driven Consumer Finance History & Vision Proprietary Process Automation Credissimo developed in-house an innovative technology that introduced automated instant

APPLE BLOCKCHAIN COIN

APPLE COIN www.apcoin.co APPLE BLOCKCHAIN COIN The world s advanced blockchain based platform with Secure, Fast and Infinite Opportunities. WHITEPAPER THE NEXT GLOBAL PAYING WHITEPAPER Introduction APPLE

APPLE COIN www.apcoin.co APPLE BLOCKCHAIN COIN The world s advanced blockchain based platform with Secure, Fast and Infinite Opportunities. WHITEPAPER THE NEXT GLOBAL PAYING WHITEPAPER Introduction APPLE

Table of Contents. 1. History of NBC The Role of NBC. 2. Banking Sector Development Growth of banking sector

Table of Contents 1. History of NBC The Role of NBC 2. Banking Sector Development Growth of banking sector 3. Financial Sector Development Strategy 2006-2015 NBC challenges for a sound financial system

Table of Contents 1. History of NBC The Role of NBC 2. Banking Sector Development Growth of banking sector 3. Financial Sector Development Strategy 2006-2015 NBC challenges for a sound financial system

Goldman Sachs U.S. Financial Services Conference 2017

Goldman Sachs U.S. Financial Services Conference 2017 Tim Sloan Chief Executive Officer and President December 5, 2017 2017 Wells Fargo & Company. All rights reserved. Wells Fargo Vision We want to satisfy

Goldman Sachs U.S. Financial Services Conference 2017 Tim Sloan Chief Executive Officer and President December 5, 2017 2017 Wells Fargo & Company. All rights reserved. Wells Fargo Vision We want to satisfy

WHITE PAPER. Smart Investments Into Crypto Technologies and Blockchain

WHITE PAPER Smart Investments Into Crypto Technologies and Blockchain CONTENT What is CryptoFund 03 Market Review 04 Issues Identification and Management 05 How CryptoFund Works 06 Investment Strategy

WHITE PAPER Smart Investments Into Crypto Technologies and Blockchain CONTENT What is CryptoFund 03 Market Review 04 Issues Identification and Management 05 How CryptoFund Works 06 Investment Strategy

Importance of financial infrastructure to increase Access to Finance

Building a high performance SME business in the MENA Region Arab Monetary Fund & International Finance Corporation Dubai, 7-8 May 2013 Importance of financial infrastructure to increase Access to Finance

Building a high performance SME business in the MENA Region Arab Monetary Fund & International Finance Corporation Dubai, 7-8 May 2013 Importance of financial infrastructure to increase Access to Finance

FINANCIAL EXECUTIVES INTERNATIONAL CRYPTOCURRENCIES

FINANCIAL EXECUTIVES INTERNATIONAL CRYPTOCURRENCIES UNIT OF ACCOUNT SUMERIAN TABLETS MEDIUM OF EXCHANGE YUROK DENTALIUM S F R IMP HU BO IMP HU R R E G BO T H E R E S I A D G R EG S M M THE RE SI A D G

FINANCIAL EXECUTIVES INTERNATIONAL CRYPTOCURRENCIES UNIT OF ACCOUNT SUMERIAN TABLETS MEDIUM OF EXCHANGE YUROK DENTALIUM S F R IMP HU BO IMP HU R R E G BO T H E R E S I A D G R EG S M M THE RE SI A D G

The Changing EU Regulatory Framework for Retail Payments

The Changing EU Regulatory Framework for Retail Payments 10 th Jubilee Conference on Payments and Market Infrastructures Ohrid, 5-7 July 2017 Ralf Jacob European Commission FISMA D.3 Retail Financial Services

The Changing EU Regulatory Framework for Retail Payments 10 th Jubilee Conference on Payments and Market Infrastructures Ohrid, 5-7 July 2017 Ralf Jacob European Commission FISMA D.3 Retail Financial Services

The Socialisation of Finance April 2015 Introduction crowd funding, peer to peer lending, socialized payments and automated investing

The Socialisation of Finance April 2015. Introduction An insightful report published in March 2015 by the leading investment bank, Goldman Sachs provides some interesting perspectives on how finance is

The Socialisation of Finance April 2015. Introduction An insightful report published in March 2015 by the leading investment bank, Goldman Sachs provides some interesting perspectives on how finance is

EXTENDING THE WORLD OF PAYMENTS TO BLOCKCHAIN

EXTENDING THE WORLD OF PAYMENTS TO BLOCKCHAIN TABLE OF CONTENTS EXTENDING THE WORLD OF PAYMENTS TO BLOCKCHAIN... 3 THE WORLD OF PAYMENTS IS EVOLVING... 3 INTEGRATION IS THE KEY TO SUCCESS... 5 FUTURE OF

EXTENDING THE WORLD OF PAYMENTS TO BLOCKCHAIN TABLE OF CONTENTS EXTENDING THE WORLD OF PAYMENTS TO BLOCKCHAIN... 3 THE WORLD OF PAYMENTS IS EVOLVING... 3 INTEGRATION IS THE KEY TO SUCCESS... 5 FUTURE OF

Company Overview and Financials. Technology Driven Consumer Finance

Company Overview and Financials Technology Driven Consumer Finance History & Vision Proprietary Process Automation Credissimo developed in-house an innovative technology that introduced automated instant

Company Overview and Financials Technology Driven Consumer Finance History & Vision Proprietary Process Automation Credissimo developed in-house an innovative technology that introduced automated instant

ABSTRACT. There is a limited number of tokens available, and it is advised that you take advantage of the ICO discounts.

ABSTRACT As the cryptocurrency industry gets more recognized by mainstream users, it needs to evolve to ensure it finally achieves the core objectives that Satoshi Nakamoto had ten years ago when he developed

ABSTRACT As the cryptocurrency industry gets more recognized by mainstream users, it needs to evolve to ensure it finally achieves the core objectives that Satoshi Nakamoto had ten years ago when he developed

Private Wealth Management. Understanding Blockchain as a Potential Disruptor

Private Wealth Management Understanding Blockchain as a Potential Disruptor 2 Blockchain and Cryptocurrency The interest in blockchain stems from the idea that its development is comparable to the early

Private Wealth Management Understanding Blockchain as a Potential Disruptor 2 Blockchain and Cryptocurrency The interest in blockchain stems from the idea that its development is comparable to the early

The Role of Technology in Second- Look Programs. Responsible Small Business Lending. Online. Fast. Smart.

The Role of Technology in Second- Look Programs Responsible Small Business Lending. Online. Fast. Smart. Why facilitate second looks for customers when they do not qualify with your bank? When you say

The Role of Technology in Second- Look Programs Responsible Small Business Lending. Online. Fast. Smart. Why facilitate second looks for customers when they do not qualify with your bank? When you say

Opening Remarks. Tim Sloan Chief Executive Officer and President. May 10, Wells Fargo & Company. All rights reserved.

Opening Remarks Tim Sloan Chief Executive Officer and President May 10, 2018 2018 Wells Fargo & Company. All rights reserved. Wells Fargo Vision We want to satisfy our customers financial needs and help

Opening Remarks Tim Sloan Chief Executive Officer and President May 10, 2018 2018 Wells Fargo & Company. All rights reserved. Wells Fargo Vision We want to satisfy our customers financial needs and help

I m very pleased to be here in Calgary with all of you for CIBC s 148th annual general meeting, and my first as CEO.

Remarks for Victor G. Dodig, President and Chief Executive Officer CIBC Annual General Meeting Calgary, Alberta April 23, 2015 Check Against Delivery Good morning, ladies and gentlemen. I m very pleased

Remarks for Victor G. Dodig, President and Chief Executive Officer CIBC Annual General Meeting Calgary, Alberta April 23, 2015 Check Against Delivery Good morning, ladies and gentlemen. I m very pleased

The Rise of Blockchain

The Rise of Blockchain I n November 2008, a white paper was posted on the internet under the name Satoshi Nakamoto titled Bitcoin: A Peer-to-Peer Electronic Cash System. The white paper outlined the concept

The Rise of Blockchain I n November 2008, a white paper was posted on the internet under the name Satoshi Nakamoto titled Bitcoin: A Peer-to-Peer Electronic Cash System. The white paper outlined the concept

Cisco Insurance Whitepaper Fall 2016

White Paper Cisco Insurance Whitepaper Fall 2016 Technology Helps Insurers Unleash the Possibilities of Digitization It s no secret that InsureTech investment is on the rise. According to the Pulse of

White Paper Cisco Insurance Whitepaper Fall 2016 Technology Helps Insurers Unleash the Possibilities of Digitization It s no secret that InsureTech investment is on the rise. According to the Pulse of

2017 Results Announcement

2017 Results Announcement Beijing/Hong Kong March 28, 2018 Disclaimer This information was prepared by the China Construction Bank Corporation ( CCB or the Bank ), without being independently verified.

2017 Results Announcement Beijing/Hong Kong March 28, 2018 Disclaimer This information was prepared by the China Construction Bank Corporation ( CCB or the Bank ), without being independently verified.

ABOUT THE PROJECT. Exscudo s main task is to provide an ultimate trading and exchange functionality for different client groups:

ABOUT THE PROJECT The main goal of the project is the integration of cryptocurrencies with the world of equity and financial markets. We aim to provide professional trading and exchange tools within the

ABOUT THE PROJECT The main goal of the project is the integration of cryptocurrencies with the world of equity and financial markets. We aim to provide professional trading and exchange tools within the

blockchain bitcoin cryptography currency Blockchain: The Next Big Digital Disruptor for CFOs cryptocurrency exchange transaction financial market

cryptography business digital virtual currency network transaction internet coin cryptocurrency market blockchain ledger data exchange electronic payments business technology money contract transaction

cryptography business digital virtual currency network transaction internet coin cryptocurrency market blockchain ledger data exchange electronic payments business technology money contract transaction

Research on Financing Strategy of Small Micro-enterprise Based on Internet Finance

2017 4th International Conference on Business, Economics and Management (BUSEM 2017) Research on Financing Strategy of Small Micro-enterprise Based on Internet Finance Yanli Li Wuhan International Culture

2017 4th International Conference on Business, Economics and Management (BUSEM 2017) Research on Financing Strategy of Small Micro-enterprise Based on Internet Finance Yanli Li Wuhan International Culture

Transforming the Banking System. Renaud Laplanche CEO, Lending Club

Transforming the Banking System Renaud Laplanche CEO, Lending Club Disclaimer Some of the statements in this presentation are "forward-looking statements or are projections. The words "anticipate," "believe,"

Transforming the Banking System Renaud Laplanche CEO, Lending Club Disclaimer Some of the statements in this presentation are "forward-looking statements or are projections. The words "anticipate," "believe,"

Over the counter or off exchange trading is done directly between two parties, without the supervision of an exchange.

1 Contents A. Statement... 3 B. Vision... 4 C. Introduction... 6 D. About... 7 E. Business model and opportunities... 8 F. Ecosystem... 9 G. Roadmap... 10 H. Circulation suplay... 11 I. Team... 12 2 STATEMENT

1 Contents A. Statement... 3 B. Vision... 4 C. Introduction... 6 D. About... 7 E. Business model and opportunities... 8 F. Ecosystem... 9 G. Roadmap... 10 H. Circulation suplay... 11 I. Team... 12 2 STATEMENT

Blockchain s Potential Role in Payment Modernization

Blockchain s Potential Role in Payment Modernization Presented by: Christopher J. Mager Managing Director and Head of Global Innovation BNY Mellon Treasury Services October 3rd, 2016 Agenda Payment disruption

Blockchain s Potential Role in Payment Modernization Presented by: Christopher J. Mager Managing Director and Head of Global Innovation BNY Mellon Treasury Services October 3rd, 2016 Agenda Payment disruption

South African Reserve Bank

South African Reserve Bank Contents Pre-workshop note Intergovernmental Fintech Working Group Workshop (19 20 April 2018) 2 The Intergovernmental Fintech Working Group 2 Developing a South African approach

South African Reserve Bank Contents Pre-workshop note Intergovernmental Fintech Working Group Workshop (19 20 April 2018) 2 The Intergovernmental Fintech Working Group 2 Developing a South African approach

THE BLOCKCHAIN DISRUPTION. INSIGHT REPORT on Blockchain prepared by The Burnie Group

THE BLOCKCHAIN DISRUPTION INSIGHT REPORT on Blockchain prepared by The Burnie Group NOVEMBER 2017 BUILDING VALUE Business networks create value. The efficiency of business networks is a function of the

THE BLOCKCHAIN DISRUPTION INSIGHT REPORT on Blockchain prepared by The Burnie Group NOVEMBER 2017 BUILDING VALUE Business networks create value. The efficiency of business networks is a function of the

M-banking the unbanked. Dr Christoph Stork

M-banking the unbanked Dr Christoph Stork Who are unbanked? Poor People Informal Businesses Poor People Nationally representative household surveys in 17 African countries 2007/8 45% of 16+ had a mobile

M-banking the unbanked Dr Christoph Stork Who are unbanked? Poor People Informal Businesses Poor People Nationally representative household surveys in 17 African countries 2007/8 45% of 16+ had a mobile

Small Business Lending Landscape

Small Business Lending Landscape Opportunity Finance Network June 8, 2016 Agenda Small Business Financing Initiative Overview Today s Topic and Presenters Small Business Lending Landscape How can mission-driven

Small Business Lending Landscape Opportunity Finance Network June 8, 2016 Agenda Small Business Financing Initiative Overview Today s Topic and Presenters Small Business Lending Landscape How can mission-driven

FinTech and Financial Inclusion

B B B FinTech and Financial Inclusion Martin Čihák Advisor and Unit Chief, International Monetary Fund Regional Conference Financial Inclusion in Asia-Pacific: The Way Forward Cambodia, December 7 8, 2017

B B B FinTech and Financial Inclusion Martin Čihák Advisor and Unit Chief, International Monetary Fund Regional Conference Financial Inclusion in Asia-Pacific: The Way Forward Cambodia, December 7 8, 2017

Our Expertise. IFC blends investment with advice and resource mobilization to help the private sector advance development.

Our Expertise IFC blends investment with advice and resource mobilization to help the private sector advance development. Where We Work As the largest global development institution focused on the private

Our Expertise IFC blends investment with advice and resource mobilization to help the private sector advance development. Where We Work As the largest global development institution focused on the private

FEATURE ARTICLE: INVESTING IN TECHNOLOGY COMPANIES

FEATURE ARTICLE: INVESTING IN TECHNOLOGY COMPANIES Technology companies have always had a place in GIC s portfolio. In recent years, as technology has disrupted traditional industries and spawned new businesses,

FEATURE ARTICLE: INVESTING IN TECHNOLOGY COMPANIES Technology companies have always had a place in GIC s portfolio. In recent years, as technology has disrupted traditional industries and spawned new businesses,

Fin Tech in Serbia: Legal Overview

Fin Tech in Serbia: Legal Overview FIN TECH IN SERBIA : LEGAL OVERVIEW Publisher: JPM Janković Popović Mitić NBGP Apartments, 6 Vladimira Popovića street www.jpm.rs AuthorS: Nikola Poznanović, Partner,

Fin Tech in Serbia: Legal Overview FIN TECH IN SERBIA : LEGAL OVERVIEW Publisher: JPM Janković Popović Mitić NBGP Apartments, 6 Vladimira Popovića street www.jpm.rs AuthorS: Nikola Poznanović, Partner,

Chapter 4 E-commerce Security and Payment Systems

Chapter 4 E-commerce Security and Payment Systems Copyright 2016 Pearson Education, Ltd. 4.5 E-COMMERCE PAYMENT SYSTEMS Copyright 2016 Pearson Education, Ltd. Slide 1-2 E-commerce Payment Systems In this

Chapter 4 E-commerce Security and Payment Systems Copyright 2016 Pearson Education, Ltd. 4.5 E-COMMERCE PAYMENT SYSTEMS Copyright 2016 Pearson Education, Ltd. Slide 1-2 E-commerce Payment Systems In this

ICICI Group. Performance and Strategy. February 2016

ICICI Group Performance and Strategy February 2016 Certain statements in these slides are forward-looking statements. These statements are based on management's current expectations and are subject to

ICICI Group Performance and Strategy February 2016 Certain statements in these slides are forward-looking statements. These statements are based on management's current expectations and are subject to

Assessment of Financial Results of General Shareholders Meeting- April 9, 2015

Assessment of Financial Results of 2014 -General Shareholders Meeting- April 9, 2015 Our net income reached TL 3.7 Billion in 2014 Net Income (TL Million) 3,339 10% 3,685 Outstanding performance despite

Assessment of Financial Results of 2014 -General Shareholders Meeting- April 9, 2015 Our net income reached TL 3.7 Billion in 2014 Net Income (TL Million) 3,339 10% 3,685 Outstanding performance despite

Innovation Hubs and Accelerators. IAIS-A2ii Consultation Call, 22 March 2018

Innovation Hubs and Accelerators IAIS-A2ii Consultation Call, 22 March 2018 Technical expert Jeremy Gray Engagement Manager Cenfri Presenters IAIS representative Peter van den Broeke International Association

Innovation Hubs and Accelerators IAIS-A2ii Consultation Call, 22 March 2018 Technical expert Jeremy Gray Engagement Manager Cenfri Presenters IAIS representative Peter van den Broeke International Association

India & ICICI Group. Trends & Outlook. September 2015

India & ICICI Group Trends & Outlook September 2015 Certain statements in these slides are forward-looking statements. These statements are based on management's current expectations and are subject to

India & ICICI Group Trends & Outlook September 2015 Certain statements in these slides are forward-looking statements. These statements are based on management's current expectations and are subject to

Banking Sector Monitoring Georgia 2018

Policy Studies Series [PS/1/218] Banking Sector Monitoring Georgia 218 Ricardo Giucci, Alexander Lehmann, Giorgi Mzhavanadze, Anne Mdinaradze German Economic Team Georgia in cooperation with Berlin/Tbilisi,

Policy Studies Series [PS/1/218] Banking Sector Monitoring Georgia 218 Ricardo Giucci, Alexander Lehmann, Giorgi Mzhavanadze, Anne Mdinaradze German Economic Team Georgia in cooperation with Berlin/Tbilisi,

COMPANY PROFILE Australia and New Zealand Banking Group Ltd

A Progressive Digital Media business COMPANY PROFILE Australia and New Zealand Banking Group REFERENCE CODE: 65E8E252-8D18-4F84-AE34-9223CF27DD0D PUBLICATION DATE: 30 May 2018 www.marketline.com COPYRIGHT

A Progressive Digital Media business COMPANY PROFILE Australia and New Zealand Banking Group REFERENCE CODE: 65E8E252-8D18-4F84-AE34-9223CF27DD0D PUBLICATION DATE: 30 May 2018 www.marketline.com COPYRIGHT

Our Expertise. IFC blends investment with advice and resource mobilization to help the private sector advance development.

Our Expertise IFC blends investment with advice and resource mobilization to help the private sector advance development. 76 IFC ANNUAL REPORT 2016 Where We Work As the largest global development institution

Our Expertise IFC blends investment with advice and resource mobilization to help the private sector advance development. 76 IFC ANNUAL REPORT 2016 Where We Work As the largest global development institution

Your Ultimate Guide to Small Business Financing

Your Ultimate Guide to Small Business Financing Section 1 Introduction 2 The Lending Landscape Finding capital to finance growth is one of the biggest challenges facing a small business owner today. Technology

Your Ultimate Guide to Small Business Financing Section 1 Introduction 2 The Lending Landscape Finding capital to finance growth is one of the biggest challenges facing a small business owner today. Technology

Outline of the System Reform Concerning. the Utilization of Personal Data

(Translation) Outline of the System Reform Concerning the Utilization of Personal Data Strategic Headquarters for the Promotion of an Advanced Information and Telecommunications Network Society (IT Strategic

(Translation) Outline of the System Reform Concerning the Utilization of Personal Data Strategic Headquarters for the Promotion of an Advanced Information and Telecommunications Network Society (IT Strategic

Midtier Banks and Credit Unions Can Compete and Win in Today s Credit Card Marketplace

Midtier Banks and Credit Unions Can Compete and Win in Today s Credit Card Marketplace Dennis C. Moroney, Research Director Retail Banking & Cards, TowerGroup October 2011 Executive Summary The combination

Midtier Banks and Credit Unions Can Compete and Win in Today s Credit Card Marketplace Dennis C. Moroney, Research Director Retail Banking & Cards, TowerGroup October 2011 Executive Summary The combination

Building Asia s Most Customer Friendly Digital Lender. November 2017

Building Asia s Most Customer Friendly Digital Lender November 2017 Our Vision Inclusive Finance Powered By Digital Technology. 500 million people live in selected Asian markets which we focus on. Over

Building Asia s Most Customer Friendly Digital Lender November 2017 Our Vision Inclusive Finance Powered By Digital Technology. 500 million people live in selected Asian markets which we focus on. Over

V Party by Velotrade Celebrate, Appreciate and Progress

V Party by Velotrade Celebrate, Appreciate and Progress Velotrade Oct 9, 2017 On September 27th, 2017, if you weren t at the V party by Velotrade, you missed a great night. The party was hosted by Velotrade

V Party by Velotrade Celebrate, Appreciate and Progress Velotrade Oct 9, 2017 On September 27th, 2017, if you weren t at the V party by Velotrade, you missed a great night. The party was hosted by Velotrade

Latest Payment & Settlement System Development / Measures In Nepal : Presented by : NEPAL RASTRA BANK Kathmandu, NEPAL

Latest Payment & Settlement System Development / Measures In Nepal -----: Presented by :------ NEPAL RASTRA BANK Kathmandu, NEPAL 1. Recent Development Total Banks & Financial Institutions In Nepal : Grade

Latest Payment & Settlement System Development / Measures In Nepal -----: Presented by :------ NEPAL RASTRA BANK Kathmandu, NEPAL 1. Recent Development Total Banks & Financial Institutions In Nepal : Grade

Digital Banking and Fintech Challenges and Threats for the Banking System Banco de Portugal Workshop

Digital Banking and Fintech Challenges and Threats for the Banking System Banco de Portugal Workshop Fintech, Virtual Currencies and Beyond: Initial Considerations B B B Jihad Al Wazir International Monetary

Digital Banking and Fintech Challenges and Threats for the Banking System Banco de Portugal Workshop Fintech, Virtual Currencies and Beyond: Initial Considerations B B B Jihad Al Wazir International Monetary

Innovation in Payment Services: The Role of EU Policies

Innovation in Payment Services: The Role of EU Policies The Hague, 18 January 2018 Ralf Jacob European Commission FISMA D.3 Retail Financial Services and Payments Objectives of this presentation Present

Innovation in Payment Services: The Role of EU Policies The Hague, 18 January 2018 Ralf Jacob European Commission FISMA D.3 Retail Financial Services and Payments Objectives of this presentation Present

01. A fund with a unique platform and technological solution - simple and convenient solution to buy, sell, and manage crypto currencies. 02.

What Will be First Crypto ETF 01. A fund with a unique platform and technological solution - simple and convenient solution to buy, sell, and manage crypto currencies. 02. OTC product Black Card. Simple

What Will be First Crypto ETF 01. A fund with a unique platform and technological solution - simple and convenient solution to buy, sell, and manage crypto currencies. 02. OTC product Black Card. Simple

INNOVATIONS IN IDENTITY IN FINANCIAL SERVICES

In financial services, identity defines and permits the relationship between providers and clients. Financial institutions need to know they are lending to genuine, legal and reliable customers, and customers

In financial services, identity defines and permits the relationship between providers and clients. Financial institutions need to know they are lending to genuine, legal and reliable customers, and customers

ICO Europe - Strengthening Europe s Blockchain Industry

ICO Europe - Strengthening Europe s Blockchain Industry Working Document Draft Version 1.2 April 8, 2018 1 THE OPPORTUNITY FOR EUROPE With $5.4 bn raised in 2017 alone, Initial Coin Offerings, or ICOs,

ICO Europe - Strengthening Europe s Blockchain Industry Working Document Draft Version 1.2 April 8, 2018 1 THE OPPORTUNITY FOR EUROPE With $5.4 bn raised in 2017 alone, Initial Coin Offerings, or ICOs,

ALPHA BANK: AGENDA 2010 REVISITED. Capital Markets Day. Bucharest, April 20, Retail Banking. G. Aronis, Executive General Manager

ALPHA BANK: AGENDA 2010 REVISITED Retail Banking G. Aronis, Executive General Manager Capital Markets Day Bucharest, April 20, 2007 Strategic Emphasis on Retail Banking Rationalize product offering Apply

ALPHA BANK: AGENDA 2010 REVISITED Retail Banking G. Aronis, Executive General Manager Capital Markets Day Bucharest, April 20, 2007 Strategic Emphasis on Retail Banking Rationalize product offering Apply

The Time is now EPOS. Everything is Possible A new era has started. Don t pass it. It s your chance to make a change!

The Time is now EPOS Everything is Possible A new era has started. Don t pass it. It s your chance to make a change! Blockchain technology will revolutionize payments and much more. So look for a way how

The Time is now EPOS Everything is Possible A new era has started. Don t pass it. It s your chance to make a change! Blockchain technology will revolutionize payments and much more. So look for a way how

Session 2: Digital Financial Inclusion and the work of the Standard- Setting Bodies

2 nd GPFI Conference on Standard- Setting Bodies and Financial Inclusion October 30, 2014 Basel, Switzerland Session 2: Digital Financial Inclusion and the work of the Standard- Setting Bodies Hosted by

2 nd GPFI Conference on Standard- Setting Bodies and Financial Inclusion October 30, 2014 Basel, Switzerland Session 2: Digital Financial Inclusion and the work of the Standard- Setting Bodies Hosted by

Commercial and SME Banking

01 Financial Highlights 02 Management Report Business Review 04 122 PT Bank Central Asia Tbk 03 Corporate Profile 04 Management Discussion and Analysis 05 Corporate Governance 06 Corporate Social Responsibility

01 Financial Highlights 02 Management Report Business Review 04 122 PT Bank Central Asia Tbk 03 Corporate Profile 04 Management Discussion and Analysis 05 Corporate Governance 06 Corporate Social Responsibility

Blockchain: game changer or just another tech trend? Ken Marke Chief Marketing & Communications Officer, B3i Technologies

Blockchain: game changer or just another tech trend? Ken Marke Chief Marketing & Communications Officer, B3i Technologies Update on B3i development and priorities Agenda 1. Background to Blockchain and

Blockchain: game changer or just another tech trend? Ken Marke Chief Marketing & Communications Officer, B3i Technologies Update on B3i development and priorities Agenda 1. Background to Blockchain and

Finnovation Bye Bye Banks?

Finnovation Bye Bye Banks? Prof Dr. Bjorn Cumps Vlerick Business School HOW FAST IS IT GOING? FAST! 2 REMEMBER? 41% market share 3 HOW FAST IS IT GOING? FAST! 6 million units sold in 15 months 10 million

Finnovation Bye Bye Banks? Prof Dr. Bjorn Cumps Vlerick Business School HOW FAST IS IT GOING? FAST! 2 REMEMBER? 41% market share 3 HOW FAST IS IT GOING? FAST! 6 million units sold in 15 months 10 million

Loyalty program on the Credits blockchain platform Building a program with blockchain and smart contracts. Issuing tokens as loyalty points.

Loyalty program on the Credits blockchain platform Building a program with blockchain and smart contracts. Issuing tokens as loyalty points. Disadvantages of the current loyalty programs Complicated procedure

Loyalty program on the Credits blockchain platform Building a program with blockchain and smart contracts. Issuing tokens as loyalty points. Disadvantages of the current loyalty programs Complicated procedure

RGC brings a Revolutionary Lending Platform in Cryptocurrency Market WHITEPAPER

RGC brings a Revolutionary Lending Platform in Cryptocurrency Market WHITEPAPER Contents Introduction...3 Vision...3 Solution...3 ICO...4 ICO Rounds...4 Investment Opportunity...5 Lending Opportunity...5

RGC brings a Revolutionary Lending Platform in Cryptocurrency Market WHITEPAPER Contents Introduction...3 Vision...3 Solution...3 ICO...4 ICO Rounds...4 Investment Opportunity...5 Lending Opportunity...5

Equity Crowdfunding: Is the process whereby people invest in companies in exchange for shares (equity) in the company.

in the company.") Crowdfunding Guide Disclaimer: Crowd88 does not provide financial or investment advice. This guide has been prepared as a support document to provide a greater understanding of Crowdfunding. It is recommended

Crowdfunding Guide Disclaimer: Crowd88 does not provide financial or investment advice. This guide has been prepared as a support document to provide a greater understanding of Crowdfunding. It is recommended

DIGITAL FINANCIAL SERVICES CHALLENGES AND OPPORTUNITIES FOR BANKS

DIGITAL FINANCIAL SERVICES CHALLENGES AND OPPORTUNITIES FOR BANKS MARTIN HOLTMANN MANAGER, DIGITAL FINANCE AND MICROFINANCE FINANCIAL INSTITUTIONS GROUP Digital Financial Services (DFS) Financial Services

DIGITAL FINANCIAL SERVICES CHALLENGES AND OPPORTUNITIES FOR BANKS MARTIN HOLTMANN MANAGER, DIGITAL FINANCE AND MICROFINANCE FINANCIAL INSTITUTIONS GROUP Digital Financial Services (DFS) Financial Services

Whatever happened to crowdfunding?

FCA Future Scenarios ++++++++++++++++++++++++++++ All views expressed in this article are those of the author and do not necessarily represent the views of the Dubai Financial Services Authority or of

FCA Future Scenarios ++++++++++++++++++++++++++++ All views expressed in this article are those of the author and do not necessarily represent the views of the Dubai Financial Services Authority or of

Supplementary Explanations on Proposal No.5 and No.6 for the 19th Ordinary General Meeting of Shareholders

Dear Shareholders March 8, 2019 Company: LINE Corporation Representative: Takeshi Idezawa, Representative Director and President Stock Code: 3938 (First section of the Tokyo Stock Exchange) Supplementary

Dear Shareholders March 8, 2019 Company: LINE Corporation Representative: Takeshi Idezawa, Representative Director and President Stock Code: 3938 (First section of the Tokyo Stock Exchange) Supplementary

For insurers Blockchain is the new black

For insurers Blockchain is the new black Navigating the hype and understanding threats and opportunities September 20 Customer Centricity Dr. Magdalena Ramada (WTW Research and Innovation Center) 20 Willis

For insurers Blockchain is the new black Navigating the hype and understanding threats and opportunities September 20 Customer Centricity Dr. Magdalena Ramada (WTW Research and Innovation Center) 20 Willis

Re: Implications of Fintech Developments for Banks and Bank Supervisors

Robert A. Morgan Vice President Emerging Technologies 202-663-5387 rmorgan@aba.com October 31 st, 2017 Secretariat of the Basel Committee on Banking Supervision Bank for International Settlements CH-4002

Robert A. Morgan Vice President Emerging Technologies 202-663-5387 rmorgan@aba.com October 31 st, 2017 Secretariat of the Basel Committee on Banking Supervision Bank for International Settlements CH-4002

Western Union. Khalid Fellahi, SVP & GM WU Digital. March 24, 2015

Western Union Khalid Fellahi, SVP & GM WU Digital March 24, 2015 SAFE HARBOR This presentation contains certain statements that are forward-looking within the meaning of the Private Securities Litigation

Western Union Khalid Fellahi, SVP & GM WU Digital March 24, 2015 SAFE HARBOR This presentation contains certain statements that are forward-looking within the meaning of the Private Securities Litigation

Fintech List Camino Financial Climb Credit SoFi Blend Labs Even

Fintech List 1. Camino Financial Provider of an online credit marketplace intended to provide business funding to informally-run and under-banked small businesses. Value Proposition to All Banks -- Targeting

Fintech List 1. Camino Financial Provider of an online credit marketplace intended to provide business funding to informally-run and under-banked small businesses. Value Proposition to All Banks -- Targeting

ANNUAL REPORT. Chairman and President s Report Highlights - Value, Reliability, Convenience. Treasurer and Credit Committee Report

ANNUAL REPORT 2016 ANNUAL REPORT 2016 1 4 5 6 7 8 9 10 11 Chairman and President s Report 2016 Highlights - Value, Reliability, Convenience Treasurer and Credit Committee Report Audit Committee Report

ANNUAL REPORT 2016 ANNUAL REPORT 2016 1 4 5 6 7 8 9 10 11 Chairman and President s Report 2016 Highlights - Value, Reliability, Convenience Treasurer and Credit Committee Report Audit Committee Report

Financial Inclusion: Meaning, Objective & Importance [Banking Awareness]

![Financial Inclusion: Meaning, Objective & Importance [Banking Awareness]](/thumbs/85/93030230.jpg "Financial Inclusion: Meaning, Objective & Importance [Banking Awareness]") Financial Inclusion: Meaning, Objective & Importance [Banking Awareness] Author : Oliveboard Date : July 14, 2017 Dear Aspirants, Financial Inclusion (FI) is a very important topic for Bank & Government

Financial Inclusion: Meaning, Objective & Importance [Banking Awareness] Author : Oliveboard Date : July 14, 2017 Dear Aspirants, Financial Inclusion (FI) is a very important topic for Bank & Government

Opportunities, challenges and strategic solutions to accelerate financial inclusion in Vietnam in the digital age

Opportunities, challenges and strategic solutions to accelerate financial inclusion in Vietnam in the digital age Presented at the conference: Digital technology The great engine of accelerating financial

Opportunities, challenges and strategic solutions to accelerate financial inclusion in Vietnam in the digital age Presented at the conference: Digital technology The great engine of accelerating financial

News Release January 30, Performance Review: Quarter ended December 31, 2018

News Release January 30, 2019 Performance Review: Quarter ended December 31, 2018 Core operating profit (profit before provisions and tax, excluding treasury income) grew by 14% year-on-year to 5,667 crore

News Release January 30, 2019 Performance Review: Quarter ended December 31, 2018 Core operating profit (profit before provisions and tax, excluding treasury income) grew by 14% year-on-year to 5,667 crore

N O V A L E N D J O I N U S, A N D L E T S I N V E S T S T R O N G T O G E T H E R

N O V A L E N D J O I N U S, A N D L E T S I N V E S T S T R O N G T O G E T H E R Website https://novalend.co Communication Channels: Telegram https://t.me/novalendofficial Twitter https://twitter.com/novalendico

N O V A L E N D J O I N U S, A N D L E T S I N V E S T S T R O N G T O G E T H E R Website https://novalend.co Communication Channels: Telegram https://t.me/novalendofficial Twitter https://twitter.com/novalendico

Digital Financial Services: Indonesia Infrastructure Development for Financial Inclusion

2015/SMEWG40/026 Agenda Item: 13.2.1a Digital Financial Services: Indonesia Infrastructure Development for Financial Inclusion Purpose: Information Submitted by: Indonesia 40 th Small and Medium Enterprises

2015/SMEWG40/026 Agenda Item: 13.2.1a Digital Financial Services: Indonesia Infrastructure Development for Financial Inclusion Purpose: Information Submitted by: Indonesia 40 th Small and Medium Enterprises

Blockchain The Ultimate Disruption in the Financial System

Informaatioteknologian tiedekunnan julkaisuja No. 33/2016 Pekka Neittaanmäki, Anthony Ogbechie Blockchain The Ultimate Disruption in the Financial System Informaatioteknologian tiedekunnan julkaisuja No.

Informaatioteknologian tiedekunnan julkaisuja No. 33/2016 Pekka Neittaanmäki, Anthony Ogbechie Blockchain The Ultimate Disruption in the Financial System Informaatioteknologian tiedekunnan julkaisuja No.

Eurofinas response to the European Banking Authority s Discussion Paper on the innovative use of consumer data by financial institutions

Eurofinas response to the European Banking Authority s Discussion Paper on the innovative use of consumer data by financial institutions Eurofinas is the voice of consumer credit providers at European

Eurofinas response to the European Banking Authority s Discussion Paper on the innovative use of consumer data by financial institutions Eurofinas is the voice of consumer credit providers at European

Equity Crowdfunding Guide

Equity Crowdfunding Guide FOR ISSUING COMPANIES 1 P a g e Disclaimer: Crowd88 does not provide financial advice. This guide has been prepared as a support document to provide Issuing Companies with a greater

Equity Crowdfunding Guide FOR ISSUING COMPANIES 1 P a g e Disclaimer: Crowd88 does not provide financial advice. This guide has been prepared as a support document to provide Issuing Companies with a greater

PaymentBox. PaymentBox https://paymentbox.io. Take Control of your payments. October 2017

PaymentBox Take Control of your payments October 2017 PaymentBox https://paymentbox.io 1 Table of Contents Table of Contents 2 Executive Summary 3 Problems 4 Solution 7 Technology 9 PaymentBox Transaction

PaymentBox Take Control of your payments October 2017 PaymentBox https://paymentbox.io 1 Table of Contents Table of Contents 2 Executive Summary 3 Problems 4 Solution 7 Technology 9 PaymentBox Transaction

THE NEXT 10 YEARS: CREDIT UNIONS 2025

THE NEXT 10 YEARS: INTRODUCTION The ecosystem matters, and the global financial ecosystem is incredibly large and incredibly complex DISRUPTORS Technological disruption, increased regulation, changing

THE NEXT 10 YEARS: INTRODUCTION The ecosystem matters, and the global financial ecosystem is incredibly large and incredibly complex DISRUPTORS Technological disruption, increased regulation, changing

A distributed platform Patentico Innovations in the field of Intellectual Property

A distributed platform Patentico Innovations in the field of Intellectual Property Mission of the company Global performance in the field of intellectual property Ecosystem and decentralized platform Solving

A distributed platform Patentico Innovations in the field of Intellectual Property Mission of the company Global performance in the field of intellectual property Ecosystem and decentralized platform Solving

Background documentation

Federal Department of Finance FDF Background documentation Date: 02.11.2016 Reduction of barriers to market entry for fintech firms 1. Background Everyone is talking about digitisation and it has been

Federal Department of Finance FDF Background documentation Date: 02.11.2016 Reduction of barriers to market entry for fintech firms 1. Background Everyone is talking about digitisation and it has been

VIETNAM PROSPERITY BANK. Q Results. April, Hanoi

VIETNAM PROSPERITY BANK Q1-2018 Results April, Hanoi CONTENT OVERVIEW OF VPBANK Q1-2018 BUSINESS UPDATE Q1-2018 FINANCIAL PERFORMANCE STRATEGIC PLANS & TARGETS 2018 OVERVIEW OF VPBANK VPBANK AT A GLANCE

VIETNAM PROSPERITY BANK Q1-2018 Results April, Hanoi CONTENT OVERVIEW OF VPBANK Q1-2018 BUSINESS UPDATE Q1-2018 FINANCIAL PERFORMANCE STRATEGIC PLANS & TARGETS 2018 OVERVIEW OF VPBANK VPBANK AT A GLANCE

whitepaper Abstract Introduction Features Special Functionality Roles in DiQi network Application / Use cases Conclusion

whitepaper Abstract Introduction Features Special Functionality Roles in DiQi network Application / Use cases Conclusion Abstract DiQi (pronounced Dee Chi) is a decentralized platform for smart property.

whitepaper Abstract Introduction Features Special Functionality Roles in DiQi network Application / Use cases Conclusion Abstract DiQi (pronounced Dee Chi) is a decentralized platform for smart property.

The State of Consumer Finance: Why the Time is Now for Marketplace Lending AL GOLDSTEIN, CEO AVANT

The State of Consumer Finance: Why the Time is Now for Marketplace Lending AL GOLDSTEIN, CEO AVANT The lending industry is overdue for disruption Potential for Disruption Low High Mortgage SMB Loans International

The State of Consumer Finance: Why the Time is Now for Marketplace Lending AL GOLDSTEIN, CEO AVANT The lending industry is overdue for disruption Potential for Disruption Low High Mortgage SMB Loans International

MA STERCARD Annual ANNU Report AL REP O RT

Annual Report 2016 Summary Consolidated Financial And Other Data For the Years Ended December 31 (in $ millions, except per share) 2016 2015 2014 Statement of Operations Net Revenue $10,776 $9,667 $9,441

Annual Report 2016 Summary Consolidated Financial And Other Data For the Years Ended December 31 (in $ millions, except per share) 2016 2015 2014 Statement of Operations Net Revenue $10,776 $9,667 $9,441

$110100$010. Crypto Currencies. Good or Evil? 10$ $100010

100110101$110100$010 Crypto Currencies Good or Evil? 0 1 0 $ 0 1 1 0 1 0 1 0 1 1 0 $ 1 1 1 0 0 1 0 1 What are Crypto-Currencies Crypto-currencies, such as Bitcoin, are digital currencies that rely on cryptographic

100110101$110100$010 Crypto Currencies Good or Evil? 0 1 0 $ 0 1 1 0 1 0 1 0 1 1 0 $ 1 1 1 0 0 1 0 1 What are Crypto-Currencies Crypto-currencies, such as Bitcoin, are digital currencies that rely on cryptographic

Insurance in the digital era: use cases

Insurance in the digital era: use cases Miami, August 28 th, 2018 HCS Capital approach to investing InsurTech Drivers: AI and digitalization FinTech & InsurTech Fund Corporate Venture Capital as-a-service

Insurance in the digital era: use cases Miami, August 28 th, 2018 HCS Capital approach to investing InsurTech Drivers: AI and digitalization FinTech & InsurTech Fund Corporate Venture Capital as-a-service

December Building a strong, innovative, relationshiporiented

December Building a strong, innovative, relationshiporiented bank Forward Looking Statements From time to time, we make written or oral forward-looking statements within the meaning of certain securities

December Building a strong, innovative, relationshiporiented bank Forward Looking Statements From time to time, we make written or oral forward-looking statements within the meaning of certain securities

MMF VIEWPOINT 6TH EDITION, Spring 2016

MMF VIEWPOINT 6TH EDITION, Spring 2016 A Message from the Director The financial sector is undergoing what may end up being its largest transition in recent memory. In addition to the changes in regulation,

MMF VIEWPOINT 6TH EDITION, Spring 2016 A Message from the Director The financial sector is undergoing what may end up being its largest transition in recent memory. In addition to the changes in regulation,

SECTOR ASSESSMENT (SUMMARY): FINANCE

: FINANCE") Inclusive Financial Sector Development Program, Subprogram 1 (RRP CAM 44263 013) SECTOR ASSESSMENT (SUMMARY): FINANCE 1. Sector Performance, Problems, and Opportunities a. Sector Context and Performance

Inclusive Financial Sector Development Program, Subprogram 1 (RRP CAM 44263 013) SECTOR ASSESSMENT (SUMMARY): FINANCE 1. Sector Performance, Problems, and Opportunities a. Sector Context and Performance

2030 Agenda for Sustainable Development

2030 Agenda for Sustainable Development The role of Development Finance in achieving the Sustainable Development Goals (SDGs): the Case of Islamic finance Alignment with Sustainable Development Goals (SDG)

2030 Agenda for Sustainable Development The role of Development Finance in achieving the Sustainable Development Goals (SDGs): the Case of Islamic finance Alignment with Sustainable Development Goals (SDG)