The Private-Money View of Financial Crises. Gary Gorton, Yale and NBER

|

|

|

- Jonas Malone

- 5 years ago

- Views:

Transcription

1 The Private-Money View of Financial Crises Gary Gorton, Yale and NBER

2 Financial Crises Doug Diamond: Financial crises are everywhere and always due to problems of short-term debt (and to the reasons why short-term debt is needed). Need short-term debt but vulnerable to runs. Challenge for theory: Explain the optimality of debt, even though it is vulnerable to runs.

3 Themes The evolution of money forms and how the information environment evolved. The price system is not supposed to work for bank money. When the price system works financial crisis. A crisis is an information event.

4 Crises are Systemic At the present moment [during the Panic of 1837], all the Banks in the United States are bankrupt; and, not only they, but all the Insurance Companies, all the Railroad Companies, all the Canal Companies, all the City Governments, all the Country Governments, all the State Governments, the General Government, and a great number of people. This is literally true. The only legal tender is gold and silver. Whoever cannot pay, on demand, in the authorized coin of the country, a debt actually due, is, in point of fact, bankrupt: although he may be at the very moment in possession of immense wealth, and although, on the winding up of his affairs, he may be shown to be worth millions. Gouge (1837; italics in original)

5 What is a financial crisis? A financial crisis is not just a bad event. Stock market crashes are not systemic events. A financial crisis is an event in which households or firms no longer believe that bank debt (money) is worth par instead the want cash: A run on the banks. Sudden but not irrational. But, banks do not have the cash, so insolvent. The banking system is insolvent.

6 Geithner: Of the twenty-five largest financial institutions at the start of 2008, thirteen failed (Lehman, WaMu), received government help to avoid failure (Fannie, Freddie, AIG, Citi, BofA), merged to avoid failure (Countryside, Bear, Merrill, Wachovia), or transformed their business structure to avoid failure (Morgan Stanley, Goldman). Bernanke s FCIC testimony--during September and October of the 13 the most important financial institutions in the United States, 12 were at risk of failure within a period of a week or two.

7

8 Financial Crises are not Rare Financial Crises: Have occurred in all market economies throughout history; Occur in advanced economies; Occur in emerging markets; Occur in economies with or without central banks; Occur with different forms of bank debt.

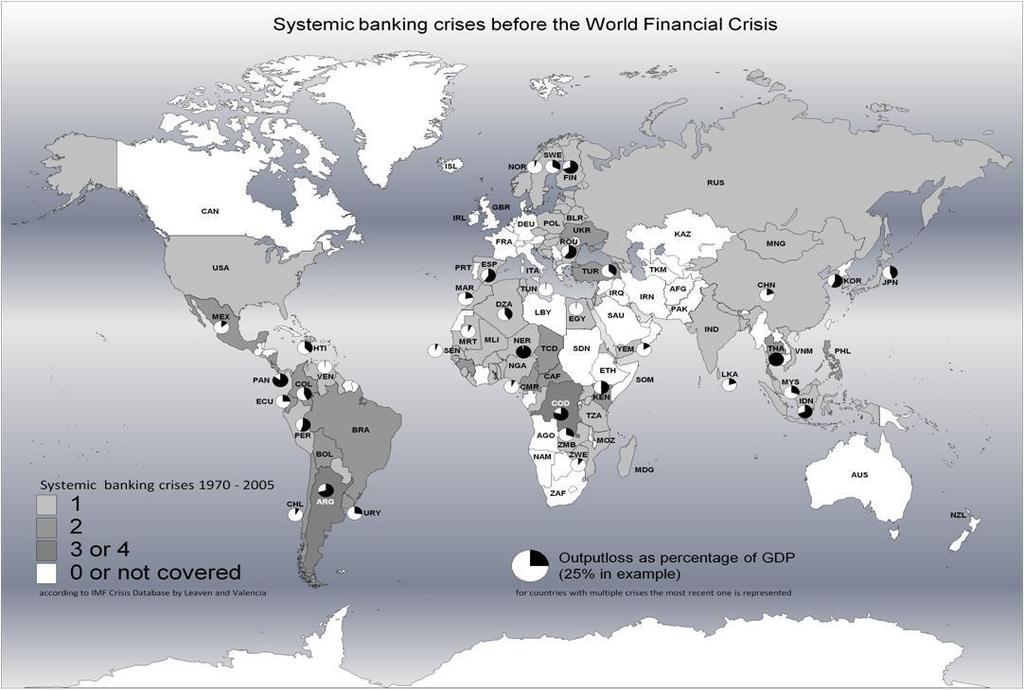

9 Financial Crises not Rare Since 1970 there have been 147 systemic events around the world. Occur in all market economies. Not just events from an earlier era. And not just in emerging markets. Of the 147 events, about 65% involved bank runs.

10 Crises are Common in Developed Countries Country Financial Crisis (first year) Australia 1893, 1989 Canada 1873, 1906, 1923, 1983 Denmark 1877, 1885, 1902, 1907, 1921, 1931, 1987 France 1882, 1889, 1904, 1930, 2008 Germany 1880, 1891, 1901, 1931, 2008 Italy 1887, 1891, 1901, 1930, 1931, 1935, 1990, 2008 Japan 1882, 1907, 1927, 1992 Netherlands 1897, 1921, 1931, 1988 Norway 1899, 1921, 1931, 1988 Spain 1920, 1924, 1931, 1978, 2008 Sweden 1876, 1897, 1907, 1922, 1931, 1991, 2008 Switzerland 1870, 1910, 1931, 2008, United Kingdom 1890, 1974, 1984, 1991, 2007 United States 1819, 1837, 1857, 1873, 1884, 1893, 1907, 1929, 2007

11

12

13

14

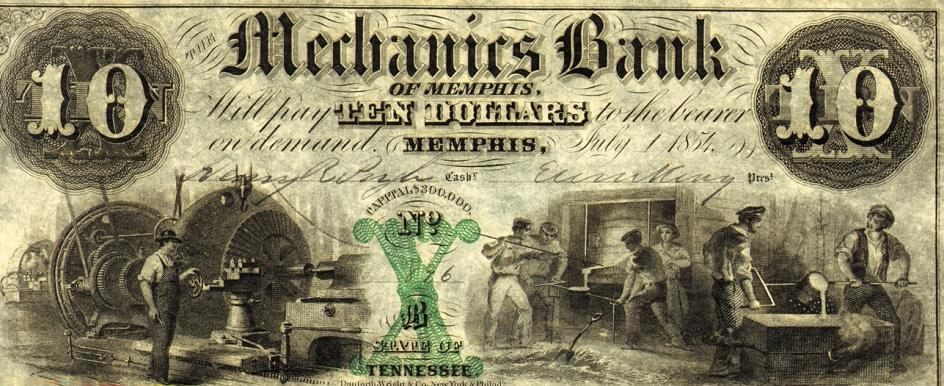

15 Percentage Discount from Par 30 Planters Bank of Tennessee Note Discount in Philadelphia Source: Gorton and Weber.

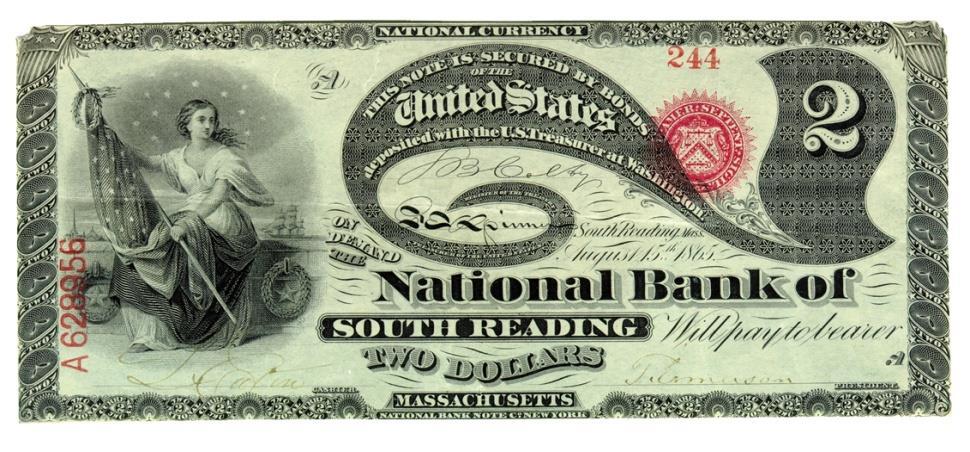

16 In the use of money, everyone is a trader; those whose habits and pursuits are little suited to explore the mechanism of trade are obliged to make use of money, and are no way qualified to ascertain the solidity of different banks whose paper is in circulation; accordingly we find that men living on limited incomes, women, laborers, and mechanics of all descriptions, are often severe sufferers by the failure of country banks... Ricardo (1876, p. 409)

17 Intuition for Dang, Gorton, Holmström (2011) Payoff on Debt At Maturity Contractual Payoff on Debt Face Value of Debt Bankruptcy point Low Value Final Value of the Collateral Backing High Value

18 Likelihood of Different Final Collateral Values Distribution of Different Collateral Values Most likely collateral value Low Value Final Value of the Collateral Backing High Value

19 Debt is the optimal contract Final Value of Collateral Likelihood of Different Collateral Values Distribution of Different Collateral Values Face Value of Debt $10 Most likely collateral value $10 Low Value Final Value of the Collateral Backing High Value

20 Final Value of Collateral Likelihood of Different Collateral Values Financial Crisis Distributions of Different Collateral Values Face Value of Debt $10 $10 Low Value Final Value of the Collateral Backing High Value

21 Payoff on Debt At Maturity Contractual Payoff on Equity Face Value of Debt Bankruptcy point Low Value Final Value of the Collateral Backing High Value

22 Debt and Info Cut cash flows by seniority cuts information! That s the point of debt.

23 Frequency of Loss Loss Distribution for Debt 0 Size of Loss F-X

24 Loss Distribution for Debt Frequency of Loss Size of Loss F-X 0

25 Maximal Info-Insensitivity: Debt-on-Debt Face Value of Debt Loss Distribution for Debt Frequency of Loss Almost riskless Size of Loss F-X 0

26 Debt (cont.) Debt is information-insensitive. Does not mean riskless. Means that it is not profitable to produce private information. Avoids adverse selection. Price does not change much/at all. Price system not work.

27 Compare to Equity The value of equity always depends on the value of the backing assets or collateral. Producing information about equity is always valuable (if you are the only one producing it). Equity is information-sensitive.

28 Debt-on-Debt Debt backed by debt maximizes information-insensitivity. Free bank notes: backed by state bonds. Demand deposits: backed by loans to consumers and small businesses. Money market instruments: backed by debt. Repo: specific bond ABCP: asset-backed securities

29 Debt and Info Cut cash flows by seniority cuts information!! That s the point of debt.

30 Implications Debt Equity Purpose Money-like Risk Sharing Information Info-insensitive Info-sensitive Retain value; NO Price Discovery Price Discovery Market Structure Trades over-the-counter Bilateral Few Traders Central Stock Exchange (NASDAQ; NYSE) Many Traders Backing Collateral Debt Real Assets Adverse Selection No No Liquidity Safe liquidity Risky liquidity Analysts None really Many Ratings Yes No Academics Don t Study Study

31 Implications for Trade Bonds do not trade. And when they do, it is bilateral (OTC). 4.0% Percentage of Total U.S. Bonds that Trade Daily 3.0% 2.0% 1.0% 0.0%

32

33 Implications for Bond Prices Since bonds essentially are not traded after they have been sold, how are off-the-run bonds valued? The answer is that the value of a bond is estimated/guessed matrix pricing.

34 NASDAQ Most bonds are priced relative to a benchmark. This is where bond market pricing gets a little tricky. Different bond classifications, as we have defined them above, use different pricing benchmarks.

35 Bond Mutual Funds Look at how bonds held by different funds are marked-to-market. There is significant price dispersion across the exact same bonds (on average). The price dispersion is decreasing in bond credit quality: lower dispersion for higher rated bonds. Dispersion is higher for high yield bonds than for investment-grade bonds.

36 But, short-term debt is money Pre-crisis repo market ~ $10 trillion - Every morning more than $1 trillion rollover of tri-party repo in early Daily trading volume of bilateral repo $5.81 trillion in 2007 (SIFMA (2008)) - Non-rollover of repos caused bankruptcy of Bear Stearns and Lehman Bankruptcy Examiner s report (2010, p.3): - Lehman funded itself through the short term repo markets and had to borrow tens or hundreds of billions of dollars in those markets each day from counterparties to be able to open for business.

37 Back to the Evolution of Bank Money - - -

38 Growth of Demand Deposits 800, , ,000 $ Thousands 500, , ,000 Bank Notes in Circulation Deposits 200, ,000 0 Year Source: Gorton

39 Number Stocks 140 New York Stock Market, Active Stocks Total Number of Stocks in Index Total Number of Bank Stocks in Index 20 0 Source: Goetzmann, Ibbotson and Peng (2001).

40

41 Ratio of Notes to Deposits and Treasury Debt to GDP Correlation = 0.96

42 U.S. National Banking Era Panics NBER Cycle Peak-Trough Panic Date % (C/D) % Pig Iron Loss per Deposit $ % and # Nat l Bank Failures Oct Mar Sep (56) Mar May 1885 Jun (10) Mar Apr No Panic (12) Jul May 1891 Nov (14) Jan Jun May (74) Dec Jun Oct (60) Jun Dec.1900 No Panic (12) Sep Aug No Panic (28) May 1907-Jun Oct (20) Jan Jan No Panic (10) Jan Dec Aug (28)

43

44

45

46 1-Aug 2-Aug 3-Aug 4-Aug 5-Aug 6-Aug 7-Aug 8-Aug 9-Aug 10-Aug 11-Aug 12-Aug 13-Aug 14-Aug 15-Aug 16-Aug 17-Aug 18-Aug 19-Aug 20-Aug 21-Aug 22-Aug 23-Aug 24-Aug 25-Aug 26-Aug 27-Aug 28-Aug 29-Aug 30-Aug 31-Aug 1-Sep 2-Sep Premium of Currency over Certifified Checks (%) 6 Currency Premium for the Panic of High Aug 2- Aug 3- Aug 4- Aug 5- Aug 7- Aug 8- Aug 9- Aug 10- Aug 11- Aug 12- Aug 14- Aug 15- Aug 16- Aug 17- Aug 18- Aug 19- Aug 21- Aug 22- Aug 23- Aug 24- Aug 25- Aug 26- Aug 28- Aug 29- Aug Low Aug 31- Aug 1- Sep 2- Sep Source: Gorton and Tallman.

47 The Quiet Period, A book called The End of History became a runaway best seller. Economists declared The Great Moderation. Bob Lucas announced that macroeconomics... has succeeded. Why no crisis? Moral hazard?

48 The Demand for Safe Assets There has always been a demand for safe assets. Historically, gold coins. Short-term safe debt money-like Long-term safe debt--- certainty of final payoff. Safe assets are debt that is near-riskless. Private sector cannot produce riskless debt. But, can produce substitutes: AAA/Aaa Abs.

49 The Transformation of the Financial System Over the last 30 years prior to the crisis, the architecture of the financial system changed. Immobile collateral bank loans became mobile collateral in the form of MBS and ABS can be traded, posted in derivative positions, collateral for repo and ABCP, rehypothecated.

50 70% Ratio of Total Private Securitization to Total Bank Loans 60% 50% 40% 30% 20% 10% 0% Source: Flow of Funds.

51 Growth of Assets in Four Financial Sectors (March 1954=1) Broker-Dealer Assets Commercial Bank Assets Household Assets Non-financial Corporate Assets Source: Flow of Funds.

52 0.700 Holders of Treasury Securities as a Fraction of Total Outstanding (0.100) US Depository Institutions Rest of the World Insurance Companies Mutual Funds Securities Broker-Dealers

53 Securitization Pooling of Assets Tranching of Assets Securitization Investors Traditional Bank: Creates Loans Sells Cash Flows From Loans Master Trust Pool of Loans AAA 85% Last (equity) Tranche Not Sold Proceeds of Sale of Assets AA A BBB

54 The Safe-Asset Share 45.0% 40.0% 35.0% 30.0% 25.0% 20.0% 15.0% 10.0% 5.0% 0.0% Government Liabilities Financial Liabilities Source: Gorton, Lewellen, Metrick (2012)

55 Components of Privately-produced Safe Financial Debt 100% 90% 80% 70% 60% 50% 40% 30% 20% 10% 0% Shadow Banking Deposits Money-like debt MBS/ABS Debt Corporate Bonds and Loans Other Liabilities Source: Gorton, Lewellen, Metrick (2012) Traditional Banking

56 Broker-Dealer Pledged Assets ($ millions) May 31, 2008 May 31, 2008 May 31, 2008 June 27, 2008 Feb. 29, nd Quarter Total Morgan Stanley Goldman Sachs Lehman Merrill Lynch Bear Stearns Total Financial Instruments Owned --of which pledged (and can be repledged) --of which pledged (and cannot be repledged) --of which not pledged at all % own financial instruments pledged 390, , , , ,104 1,501, ,000 37,383 43,031 27,512 22, ,829 54, ,980 80,000 53,025 54, , , , , ,388 64, ,699 50% 39% 46% 28% 55% 42%

57 $ Millions The Scarcity of Safe Debt 3,000,000 Primary Dealer Treasury Fails 2,500,000 2,000,000 1,500,000 1,000,000 Total Treasury Receive Total Treasury Deliver 500,000 0 Source: Gorton and Muir.

58 Mortgage Originations and Subprime Securitization Total Mortgage Originations (Billions) Subprime Originations (Billions) Subprime Share in Total Originations (% of dollar value) Subprime Mortgage Backed Securities (Billions) Percent Subprime Securitized (% of dollar value) 2001 $2,215 $ % $ % 2002 $2,885 $ % $ % 2003 $3,945 $ % $ % 2004 $2,920 $ % $ % 2005 $3,120 $ % $ % 2006 $2,980 $ % $ %

59 Where did the sub-prime risk go?

60 1/2/2007 2/2/2007 3/2/2007 4/2/2007 5/2/2007 6/2/2007 7/2/2007 8/2/2007 9/2/ /2/ /2/ /2/2007 1/2/2008 2/2/2008 3/2/2008 4/2/2008 5/2/2008 6/2/2008 7/2/2008 8/2/2008 9/2/ /2/ /2/ /2/2008 1/2/2009 2/2/2009 Percentage 50.0% Average Repo Haircut on Structured Debt 45.0% 40.0% 35.0% 30.0% 25.0% 20.0% 15.0% 10.0% 5.0% 0.0% Source: Gorton and Metrick

61 1999Q4 2000Q2 2000Q4 2001Q2 2001Q4 2002Q2 2002Q4 2003Q2 2003Q4 2004Q2 2004Q4 2005Q2 2005Q4 2006Q2 2006Q4 2007Q2 2007Q4 2008Q2 2008Q4 2009Q2 2009Q4 2010Q2 2010Q4 2011Q2 2011Q4 2,500 BD+Banks NET Funding Received from Repo ($ bil; FoF) 2,000 1,500 1,

62 1999Q4 2000Q2 2000Q4 2001Q2 2001Q4 2002Q2 2002Q4 2003Q2 2003Q4 2004Q2 2004Q4 2005Q2 2005Q4 2006Q2 2006Q4 2007Q2 2007Q4 2008Q2 2008Q4 2009Q2 2009Q4 2010Q2 2010Q4 2011Q2 2011Q4 1,200 Net Repo Lending ($ bils; FoF) 1, MMFs Discrepancy ROW

63 Fire Sales: AAA Spreads Above AA Spreads Aug 2007 Lehman Sept 2008

64 Crises and Macroeconomic Activity Crises preceded by credit boom. Credit boom caused by positive shock to TFP and LP. If technological change is not persistent, the boom ends in a crisis.

65 Those who ignore history are entitled to repeat it.

66 Further Reading

The Financial Crisis. Yale. Marinus van Reymerswaele, 1567

The Financial Crisis Gary Gorton Yale Marinus van Reymerswaele, 1567 What is the crisis? What you saw: firms fail, get acquired, or get bailed out (Lehman Brothers, Bear Stearns, Merrill Lynch, AIG); people

The Financial Crisis Gary Gorton Yale Marinus van Reymerswaele, 1567 What is the crisis? What you saw: firms fail, get acquired, or get bailed out (Lehman Brothers, Bear Stearns, Merrill Lynch, AIG); people

Transparency in the U.S. Repo Market

Transparency in the U.S. Repo Market Antoine Martin Federal Reserve Bank of New York October 11, 2013 The views expressed in this presentation are my own and may not represent the views of the Federal

Transparency in the U.S. Repo Market Antoine Martin Federal Reserve Bank of New York October 11, 2013 The views expressed in this presentation are my own and may not represent the views of the Federal

The Flight from Maturity. Gary Gorton, Yale and NBER Andrew Metrick, Yale and NBER Lei Xie, AQR Investment Management

The Flight from Maturity Gary Gorton, Yale and NBER Andrew Metrick, Yale and NBER Lei Xie, AQR Investment Management Explaining the Crisis How can a small shock cause a large crisis? 24 bps of realized

The Flight from Maturity Gary Gorton, Yale and NBER Andrew Metrick, Yale and NBER Lei Xie, AQR Investment Management Explaining the Crisis How can a small shock cause a large crisis? 24 bps of realized

Why Regulate Shadow Banking? Ian Sheldon

Why Regulate Shadow Banking? Ian Sheldon Andersons Professor of International Trade sheldon.1@osu.edu Department of Agricultural, Environmental & Development Economics Ohio State University Extension Bank

Why Regulate Shadow Banking? Ian Sheldon Andersons Professor of International Trade sheldon.1@osu.edu Department of Agricultural, Environmental & Development Economics Ohio State University Extension Bank

Why Regulate Shadow Banking? Ian Sheldon

Why Regulate Shadow Banking? Ian Sheldon Andersons Professor of International Trade sheldon.1@osu.edu Department of Agricultural, Environmental & Development Economics Ohio State University Extension Bank

Why Regulate Shadow Banking? Ian Sheldon Andersons Professor of International Trade sheldon.1@osu.edu Department of Agricultural, Environmental & Development Economics Ohio State University Extension Bank

Rise and Collapse of Shadow Banking. Macro-Modelling. with a focus on the role of financial markets. ECON 244, Spring 2013 Shadow Banking

with a focus on the role of financial markets ECON 244, Spring 2013 Shadow Banking Guillermo Ordoñez, University of Pennsylvania April 11, 2013 Shadow Banking Based on Gorton and Metrick (2011) After the

with a focus on the role of financial markets ECON 244, Spring 2013 Shadow Banking Guillermo Ordoñez, University of Pennsylvania April 11, 2013 Shadow Banking Based on Gorton and Metrick (2011) After the

How did Too Big to Fail become such a problem for broker-dealers? Speculation by Andy Atkeson March 2014

How did Too Big to Fail become such a problem for broker-dealers? Speculation by Andy Atkeson March 2014 Proximate Cause By 2008, Broker Dealers had big balance sheets Historical experience with rapid

How did Too Big to Fail become such a problem for broker-dealers? Speculation by Andy Atkeson March 2014 Proximate Cause By 2008, Broker Dealers had big balance sheets Historical experience with rapid

Information, Liquidity, and the (Ongoing) Panic of 2007*

Panic of 2007*") Information, Liquidity, and the (Ongoing) Panic of 2007* Gary Gorton Yale School of Management and NBER Prepared for AER Papers & Proceedings, 2009. This version: December 31, 2008 Abstract The credit

Information, Liquidity, and the (Ongoing) Panic of 2007* Gary Gorton Yale School of Management and NBER Prepared for AER Papers & Proceedings, 2009. This version: December 31, 2008 Abstract The credit

The Financial Systems Complexity

The Financial Systems Complexity Some Data on the Financial System The Role of the Financial System Information Challenges & the Financial System Government Regulation and Supervision Financial Panics:

The Financial Systems Complexity Some Data on the Financial System The Role of the Financial System Information Challenges & the Financial System Government Regulation and Supervision Financial Panics:

Global Securities Lending Business and Market Update

NORTHERN TRUST 2009 INSTITUTIONAL CLIENT CONFERENCE GLOBAL REACH, LOCAL EXPERTISE Global Securities Lending Business and Market Update Michael A. Vardas, CFA Managing Director Quantitative Management and

NORTHERN TRUST 2009 INSTITUTIONAL CLIENT CONFERENCE GLOBAL REACH, LOCAL EXPERTISE Global Securities Lending Business and Market Update Michael A. Vardas, CFA Managing Director Quantitative Management and

Chapter 10. The Great Recession: A First Look. (1) Spike in oil prices. (2) Collapse of house prices. (2) Collapse in house prices

Spike in oil prices. (2) Collapse of house prices. (2) Collapse in house prices") Discussion sections this week will meet tonight (Tuesday Jan 17) to review Problem Set 1 in Pepper Canyon Hall 106 5:00-5:50 for 11:00 class 6:00-6:50 for 1:30 class Course web page: http://econweb.ucsd.edu/~jhamilto/econ110b.html

Discussion sections this week will meet tonight (Tuesday Jan 17) to review Problem Set 1 in Pepper Canyon Hall 106 5:00-5:50 for 11:00 class 6:00-6:50 for 1:30 class Course web page: http://econweb.ucsd.edu/~jhamilto/econ110b.html

Capital Market Trends and Forecasts

Capital Market Trends and Forecasts Glenn Yago, Ph.D. Director, Capital Studies Milken Institute Los Angeles Fire and Police Pension System Education Retreat January 7, 28 1 Dow Jones U.S. Financial Index

Capital Market Trends and Forecasts Glenn Yago, Ph.D. Director, Capital Studies Milken Institute Los Angeles Fire and Police Pension System Education Retreat January 7, 28 1 Dow Jones U.S. Financial Index

The Financial Crisis of ? Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid

The Financial Crisis of 2007-201? Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid Disclaimer These views are mine and not necessarily those of the Federal Reserve Bank

The Financial Crisis of 2007-201? Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid Disclaimer These views are mine and not necessarily those of the Federal Reserve Bank

Theta Capital Management. Distressed Investing - Deep value opportunities through the cycle

Theta Capital Management Distressed Investing - Deep value opportunities through the cycle VBA Wouter ten Brinke 19 May 2010 2 Theta Capital Management Products Product Investment style Target return Target

Theta Capital Management Distressed Investing - Deep value opportunities through the cycle VBA Wouter ten Brinke 19 May 2010 2 Theta Capital Management Products Product Investment style Target return Target

Economic History of the US

Economic History of the US Pax Americana, 1946 to the Financial Crisis of 2008 Lecture #5 Peter Allen Econ 120 1 Since Sept. 2008 1. Worst Recession since WWII 2. Banking Crisis, Panic of 08 First since

Economic History of the US Pax Americana, 1946 to the Financial Crisis of 2008 Lecture #5 Peter Allen Econ 120 1 Since Sept. 2008 1. Worst Recession since WWII 2. Banking Crisis, Panic of 08 First since

New Risk Management Strategies

Moderator: Jon Najarian, Co-Founder, optionmonster.com New Risk Management Strategies Wednesday, May 4, 2011; 2:30 PM - 3:45 PM Speakers: Jim Lenz, Chief Credit and Risk Officer, Wells Fargo Advisors John

Moderator: Jon Najarian, Co-Founder, optionmonster.com New Risk Management Strategies Wednesday, May 4, 2011; 2:30 PM - 3:45 PM Speakers: Jim Lenz, Chief Credit and Risk Officer, Wells Fargo Advisors John

Lecture 5. Notes on the Current Crisis

Lecture 5 Notes on the Current Crisis Mark Gertler NYU June 29 .4 Real GDP growth.3.2.1.1.2.3 1975 198 1985 199 1995 2 25 18 16 core inflation federal funds rate 14 12 1 8 6 4 2 1975 198 1985 199 1995

Lecture 5 Notes on the Current Crisis Mark Gertler NYU June 29 .4 Real GDP growth.3.2.1.1.2.3 1975 198 1985 199 1995 2 25 18 16 core inflation federal funds rate 14 12 1 8 6 4 2 1975 198 1985 199 1995

Global Financial Crisis. Econ 690 Spring 2019

Global Financial Crisis Econ 690 Spring 2019 1 Timeline of Global Financial Crisis 2002-2007 US real estate prices rise mid-2007 Mortgage loan defaults rise, some financial institutions have trouble, recession

Global Financial Crisis Econ 690 Spring 2019 1 Timeline of Global Financial Crisis 2002-2007 US real estate prices rise mid-2007 Mortgage loan defaults rise, some financial institutions have trouble, recession

Too Big to Fail Causes, Consequences and Policy Responses. Philip E. Strahan. Annual Review of Financial Economics Conference.

Too Big to Fail Causes, Consequences and Policy Responses Philip E. Strahan Annual Review of Financial Economics Conference October, 13 Too Big to Fail is a credibility problem Markets expect creditors

Too Big to Fail Causes, Consequences and Policy Responses Philip E. Strahan Annual Review of Financial Economics Conference October, 13 Too Big to Fail is a credibility problem Markets expect creditors

The Financial Crisis. Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid

The Financial Crisis Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid Disclaimer These views are mine and not necessarily those of the Federal Reserve Bank of Atlanta or

The Financial Crisis Gerald P. Dwyer Federal Reserve Bank of Atlanta University of Carlos III, Madrid Disclaimer These views are mine and not necessarily those of the Federal Reserve Bank of Atlanta or

The Financial Crisis and the Bailout

The Financial Crisis and the Bailout Steven Kaplan University of Chicago Graduate School of Business 1 S. Kaplan Intro This talk: What is the problem? How did we get here? What do we need to do? What does

The Financial Crisis and the Bailout Steven Kaplan University of Chicago Graduate School of Business 1 S. Kaplan Intro This talk: What is the problem? How did we get here? What do we need to do? What does

The Nature of Liquidity Provision: When Ignorance is Bliss*

The Nature of Liquidity Provision: When Ignorance is Bliss* Presidential Address, Chicago January 5, 2012 Bengt Holmstrom, MIT *Based on joint work with Tri Vi Dang and Gary Gorton Common view of causes

The Nature of Liquidity Provision: When Ignorance is Bliss* Presidential Address, Chicago January 5, 2012 Bengt Holmstrom, MIT *Based on joint work with Tri Vi Dang and Gary Gorton Common view of causes

GS Global ECS Credit Strategy Research. March 31, Alberto Gallo, CFA Goldman, Sachs & Co

The Goldman Sachs Group, Inc. Goldman Sachs Research The CLO market shows signs of life GS Global ECS Credit Strategy Research March 31, 11 Alberto Gallo, CFA Goldman, Sachs & Co. 1-917-33-31 alberto.gallo@gs.com

The Goldman Sachs Group, Inc. Goldman Sachs Research The CLO market shows signs of life GS Global ECS Credit Strategy Research March 31, 11 Alberto Gallo, CFA Goldman, Sachs & Co. 1-917-33-31 alberto.gallo@gs.com

Capital Flows, Cross-Border Banking and Global Liquidity. May 2012

Capital Flows, Cross-Border Banking and Global Liquidity Valentina Bruno Hyun Song Shin May 2012 Bruno and Shin: Capital Flows, Cross-Border Banking and Global Liquidity 1 Gross Capital Flows Capital flows

Capital Flows, Cross-Border Banking and Global Liquidity Valentina Bruno Hyun Song Shin May 2012 Bruno and Shin: Capital Flows, Cross-Border Banking and Global Liquidity 1 Gross Capital Flows Capital flows

August 8, 2006 Authorized for Public Release 148 of 158. Appendix 1: Materials used by Mr. Kos

August 8, 6 Authorized for Public Release 148 of 158 Appendix 1: Materials used by Mr. Kos Class II -- Restricted FR Page 1 of 4 Realized Volatility of MSCI Equity Indices 35 25 15 5 22 August 8, 6 Authorized

August 8, 6 Authorized for Public Release 148 of 158 Appendix 1: Materials used by Mr. Kos Class II -- Restricted FR Page 1 of 4 Realized Volatility of MSCI Equity Indices 35 25 15 5 22 August 8, 6 Authorized

Lecture notes on risk management, public policy, and the financial system Forms of leverage

Lecture notes on risk management, public policy, and the financial system Allan M. Malz Columbia University 2018 Allan M. Malz Last updated: March 12, 2018 2 / 18 Outline 3/18 Key postwar developments

Lecture notes on risk management, public policy, and the financial system Allan M. Malz Columbia University 2018 Allan M. Malz Last updated: March 12, 2018 2 / 18 Outline 3/18 Key postwar developments

Shadow Banking & the Financial Crisis

& the Financial Crisis April 24, 2013 & the Financial Crisis Table of contents 1 Backdrop A bit of history 2 3 & the Financial Crisis Origins Backdrop A bit of history Banks perform several vital roles

& the Financial Crisis April 24, 2013 & the Financial Crisis Table of contents 1 Backdrop A bit of history 2 3 & the Financial Crisis Origins Backdrop A bit of history Banks perform several vital roles

Comments on The Fd Federal lr Reserve s Primary Dealer Credit Facility Tobias Adrian and James McAndrews

Comments on The Fd Federal lr Reserve s Primary Dealer Credit Facility Tobias Adrian and James McAndrews SGE Session on The Fed s New Lending Facilities ASSA Meetings San Francisco John B. Taylor Stanford

Comments on The Fd Federal lr Reserve s Primary Dealer Credit Facility Tobias Adrian and James McAndrews SGE Session on The Fed s New Lending Facilities ASSA Meetings San Francisco John B. Taylor Stanford

2018 Investment and Economic Outlook

2018 Investment and Economic Outlook Presented 3/19/18 Jeffrey Neer, CFA Client Portfolio Manager 410-237-5592 jeffrey.neer@pnc.com 1 Monetary Policy: Key Factors Inflation U.S. U.S. Labor Market 2.4%

2018 Investment and Economic Outlook Presented 3/19/18 Jeffrey Neer, CFA Client Portfolio Manager 410-237-5592 jeffrey.neer@pnc.com 1 Monetary Policy: Key Factors Inflation U.S. U.S. Labor Market 2.4%

How did Monetary Policy Implementation Change with the Financial Crisis?

How did Monetary Policy Implementation Change with the Financial Crisis? John McGowan Assistant Vice President Money Markets, Markets Group, FRBNY September 28, 2015 Internal FR I. FRS Mandate and Pre-

How did Monetary Policy Implementation Change with the Financial Crisis? John McGowan Assistant Vice President Money Markets, Markets Group, FRBNY September 28, 2015 Internal FR I. FRS Mandate and Pre-

Introduction. Learning Objectives. Chapter 15. Money, Banking, and Central Banking

Chapter 15 Money, Banking, and Central Banking Introduction Bear Stearns, Goldman Sachs, Lehman Brothers, Merrill Lynch, and Morgan Stanley have been big names on Wall Street for years. Known as investment

Chapter 15 Money, Banking, and Central Banking Introduction Bear Stearns, Goldman Sachs, Lehman Brothers, Merrill Lynch, and Morgan Stanley have been big names on Wall Street for years. Known as investment

Key IRS Interest Rates After PPA

Key IRS Rates - After PPA - thru 2011 Page 1 of 10 Key IRS Interest Rates After PPA (updated upon release of figures in IRS Notice usually by the end of the first full business week of the month) Below

Key IRS Rates - After PPA - thru 2011 Page 1 of 10 Key IRS Interest Rates After PPA (updated upon release of figures in IRS Notice usually by the end of the first full business week of the month) Below

2015 Market Review & Outlook. January 29, 2015

2015 Market Review & Outlook January 29, 2015 Economic Outlook Jason O. Jackman, CFA President & Chief Investment Officer Percentage Interest Rates Unexpectedly Decline 4.5 10-Year Government Yield 4 3.5

2015 Market Review & Outlook January 29, 2015 Economic Outlook Jason O. Jackman, CFA President & Chief Investment Officer Percentage Interest Rates Unexpectedly Decline 4.5 10-Year Government Yield 4 3.5

1 U.S. Subprime Crisis

U.S. Subprime Crisis 1 Outline 2 Where are we? How did we get here? Government measures to stop the crisis Have government measures work? What alternatives do we have? Where are we? 3 Worst postwar U.S.

U.S. Subprime Crisis 1 Outline 2 Where are we? How did we get here? Government measures to stop the crisis Have government measures work? What alternatives do we have? Where are we? 3 Worst postwar U.S.

Money and Banking. Lecture VII: Financial Crisis. Guoxiong ZHANG, Ph.D. November 22nd, Shanghai Jiao Tong University, Antai

Money and Banking Lecture VII: 2007-2009 Financial Crisis Guoxiong ZHANG, Ph.D. Shanghai Jiao Tong University, Antai November 22nd, 2016 People s Bank of China Road Map Timeline of the crisis Bernanke

Money and Banking Lecture VII: 2007-2009 Financial Crisis Guoxiong ZHANG, Ph.D. Shanghai Jiao Tong University, Antai November 22nd, 2016 People s Bank of China Road Map Timeline of the crisis Bernanke

Central Bank collateral frameworks before and during the crisis

Central Bank collateral frameworks before and during the crisis The case of the Federal Reserve Central banking, liquidity crises and financial stability lecture Mai 20 th, 2011 Presentation by 1 Goals

Central Bank collateral frameworks before and during the crisis The case of the Federal Reserve Central banking, liquidity crises and financial stability lecture Mai 20 th, 2011 Presentation by 1 Goals

The Future of the Mortgage Market: Where Do We Go From Here?

The Future of the Mortgage Market: Where Do We Go From Here? Stuart Gabriel, Director of the Ziman Center for Real Estate, Arden Realty Chair and Professor of Finance, Anderson School of Management, University

The Future of the Mortgage Market: Where Do We Go From Here? Stuart Gabriel, Director of the Ziman Center for Real Estate, Arden Realty Chair and Professor of Finance, Anderson School of Management, University

Hong Kong s Experience

Cross Border Issues IMF Conference on Operationalizing Systemic Risk Monitoring Washington, D. C. 26 May 21 Hong Kong s Experience Dong He Executive Director (Research) Hong Kong Monetary Authority 1 Outline

Cross Border Issues IMF Conference on Operationalizing Systemic Risk Monitoring Washington, D. C. 26 May 21 Hong Kong s Experience Dong He Executive Director (Research) Hong Kong Monetary Authority 1 Outline

Shadow Maturity Transformation and Systemic Risk. Sandra Krieger Executive Vice President and Chief Risk Officer, Federal Reserve Bank of New York

Shadow Maturity Transformation and Systemic Risk Sandra Krieger Executive Vice President and Chief Risk Officer, Federal Reserve Bank of New York 8 March 2011 Overview of discussion What is shadow bank

Shadow Maturity Transformation and Systemic Risk Sandra Krieger Executive Vice President and Chief Risk Officer, Federal Reserve Bank of New York 8 March 2011 Overview of discussion What is shadow bank

For professional advisers only. Schroders. for Bonds. Strength. in bonds. Best Large Fixed-Interest House

For professional advisers only Schroders for Bonds Strength in bonds Best Large Fixed-Interest House Why Schroders for bonds? Experience: Schroders has a long and successful history, commencing in 1804.

For professional advisers only Schroders for Bonds Strength in bonds Best Large Fixed-Interest House Why Schroders for bonds? Experience: Schroders has a long and successful history, commencing in 1804.

Benoît Cœuré Member of the Executive Board. The future of central bank money

Benoît Cœuré Member of the Executive Board The future of central bank money Geneva, 14 May 218 Card Rubric payments and cash demand have generally increased since 27 Card payments and cash demand (x-axis:

Benoît Cœuré Member of the Executive Board The future of central bank money Geneva, 14 May 218 Card Rubric payments and cash demand have generally increased since 27 Card payments and cash demand (x-axis:

Capital Markets Update

Capital Markets Update The Forces Transforming Markets November 2007 The Past December 2006 April 2007 The Height of the Market November 2007 Changes in Risk Tolerance Spring 2007 Rating Agencies Tighten

Capital Markets Update The Forces Transforming Markets November 2007 The Past December 2006 April 2007 The Height of the Market November 2007 Changes in Risk Tolerance Spring 2007 Rating Agencies Tighten

Panel Discussion: Europe at the Crossroads

Panel Discussion: Europe at the Crossroads Markus Brunnermeier Paul Krugman Hyun Song Shin Christopher Sims October 24th, 2011 Department of Economics and Griswold Center for Economic Policy Studies 1

Panel Discussion: Europe at the Crossroads Markus Brunnermeier Paul Krugman Hyun Song Shin Christopher Sims October 24th, 2011 Department of Economics and Griswold Center for Economic Policy Studies 1

The First Phase of the U.S. Recovery and Beyond

The First Phase of the U.S. Recovery and Beyond James Bullard President and CEO Federal Reserve Bank of St. Louis Global Interdependence Center Shanghai, China January 11, 2010 Any opinions expressed here

The First Phase of the U.S. Recovery and Beyond James Bullard President and CEO Federal Reserve Bank of St. Louis Global Interdependence Center Shanghai, China January 11, 2010 Any opinions expressed here

Moving On Up Investing in Today s Rate Environment

Moving On Up Investing in Today s Rate Environment Presented by PFM Asset Management LLC Steve Faber, Managing Director Gray Lepley, Senior Analyst, Portfolio Strategies September 18, 2018 PFM 1 Today

Moving On Up Investing in Today s Rate Environment Presented by PFM Asset Management LLC Steve Faber, Managing Director Gray Lepley, Senior Analyst, Portfolio Strategies September 18, 2018 PFM 1 Today

Stylized Financial System

Procyclicality and Capital Flows: Emerging Market Perspective Hyun Song Shin Bank of Thailand International Symposium 2010: Challenges to Central Banks in the Era of the New Globalization October 14 15,

Procyclicality and Capital Flows: Emerging Market Perspective Hyun Song Shin Bank of Thailand International Symposium 2010: Challenges to Central Banks in the Era of the New Globalization October 14 15,

FIN 684 Fixed-Income Analysis Corporate Debt Securities

FIN 684 Fixed-Income Analysis Corporate Debt Securities Professor Robert B.H. Hauswald Kogod School of Business, AU Corporate Debt Securities Financial obligations of a corporation that have priority over

FIN 684 Fixed-Income Analysis Corporate Debt Securities Professor Robert B.H. Hauswald Kogod School of Business, AU Corporate Debt Securities Financial obligations of a corporation that have priority over

Global Outlook and Policy Challenges. Olivier Blanchard Economic Counsellor Research Department

Global Outlook and Policy Challenges Olivier Blanchard Economic Counsellor Research Department February, 29 Global Outlook Has Deteriorated, but Modest Turnaround Anticipated with Policy Stimulus 1 WEO

Global Outlook and Policy Challenges Olivier Blanchard Economic Counsellor Research Department February, 29 Global Outlook Has Deteriorated, but Modest Turnaround Anticipated with Policy Stimulus 1 WEO

Key IRS Interest Rates After PPA

Key IRS Interest After PPA (updated upon release of figures in IRS Notice usually by the end of the first full business week of the month) Below are Tables I, II, and III showing official interest rates

Key IRS Interest After PPA (updated upon release of figures in IRS Notice usually by the end of the first full business week of the month) Below are Tables I, II, and III showing official interest rates

The Real Effects of Disrupted Credit Evidence from the Global Financial Crisis

The Real Effects of Disrupted Credit Evidence from the Global Financial Crisis Ben S. Bernanke Distinguished Fellow Brookings Institution Washington DC Brookings Papers on Economic Activity September 13

The Real Effects of Disrupted Credit Evidence from the Global Financial Crisis Ben S. Bernanke Distinguished Fellow Brookings Institution Washington DC Brookings Papers on Economic Activity September 13

How Curb Risk In Wall Street. Luigi Zingales. University of Chicago

How Curb Risk In Wall Street Luigi Zingales University of Chicago Banks Instability Banks are engaged in a transformation of maturity: borrow short term lend long term This transformation is socially valuable

How Curb Risk In Wall Street Luigi Zingales University of Chicago Banks Instability Banks are engaged in a transformation of maturity: borrow short term lend long term This transformation is socially valuable

Regulation, Supervision, Financial Institutions. February The interlinked components of risk management. Market discipline. Competition Haircuts

Regulation, Supervision, and Risk Management of Financial Institutions An OECD perspective Stephen A. Lumpkin Principal Administrator, OECD Financial Affairs Division February 2012 1 The interlinked components

Regulation, Supervision, and Risk Management of Financial Institutions An OECD perspective Stephen A. Lumpkin Principal Administrator, OECD Financial Affairs Division February 2012 1 The interlinked components

The Safe-Asset Share*

The Safe-Asset Share* Gary Gorton Yale and NBER Stefan Lewellen Yale Andrew Metrick Yale and NBER January 17, 2012 Prepared for AER Papers & Proceedings, 2012. Abstract: We document that the percentage

The Safe-Asset Share* Gary Gorton Yale and NBER Stefan Lewellen Yale Andrew Metrick Yale and NBER January 17, 2012 Prepared for AER Papers & Proceedings, 2012. Abstract: We document that the percentage

Comments on Toward a 3-Tiered Market for US Home Mortgages

Comments on Toward a 3-Tiered Market for US Home Mortgages Lawrence J. White Stern School of Business New York University Lwhite@stern.nyu.edu Presentation at the Brookings Conference on Restructuring

Comments on Toward a 3-Tiered Market for US Home Mortgages Lawrence J. White Stern School of Business New York University Lwhite@stern.nyu.edu Presentation at the Brookings Conference on Restructuring

Who Borrows from the Lender of Last Resort? 1

Who Borrows from the Lender of Last Resort? 1 Itamar Drechsler, Thomas Drechsel, David Marques-Ibanez and Philipp Schnabl NYU Stern and NBER ECB NYU Stern, CEPR, and NBER November 2012 1 The views expressed

Who Borrows from the Lender of Last Resort? 1 Itamar Drechsler, Thomas Drechsel, David Marques-Ibanez and Philipp Schnabl NYU Stern and NBER ECB NYU Stern, CEPR, and NBER November 2012 1 The views expressed

INVESTMENT TIPS AND TECHNIQUES

INVESTMENT TIPS AND TECHNIQUES Ohio Township Association Annual Winter Conference February 2, 2018 Presented by Eileen Stanic, CTP Senior Public Funds Advisor Meeder Investment Management 1 AGENDA Cash

INVESTMENT TIPS AND TECHNIQUES Ohio Township Association Annual Winter Conference February 2, 2018 Presented by Eileen Stanic, CTP Senior Public Funds Advisor Meeder Investment Management 1 AGENDA Cash

Executive Summary. July 17, 2015

Executive Summary July 17, 2015 The Revenue Estimating Conference adopted interest rates for use in the state budgeting process. The adopted interest rates take into consideration current benchmark rates

Executive Summary July 17, 2015 The Revenue Estimating Conference adopted interest rates for use in the state budgeting process. The adopted interest rates take into consideration current benchmark rates

The next recession will not be. The Great Recession. Damon Runberg, Economist Oregon Employment Department

The next recession will not be The Great Recession Damon Runberg, Economist Oregon Employment Department Why the fears? Simplified Business Cycle Peak 2 consecutive quarters of GDP declines Wages Rise

The next recession will not be The Great Recession Damon Runberg, Economist Oregon Employment Department Why the fears? Simplified Business Cycle Peak 2 consecutive quarters of GDP declines Wages Rise

A Global Economic and Market Outlook

A Global Economic and Market Outlook Presented by Dr Chris Caton December 2008 US Housing starts and Permits 2.3 (Millions) Permits Starts 2.1 1.9 1.7 1.5 1.3 1.1 0.9 0.7 96 97 98 99 00 01 02 03 04 05

A Global Economic and Market Outlook Presented by Dr Chris Caton December 2008 US Housing starts and Permits 2.3 (Millions) Permits Starts 2.1 1.9 1.7 1.5 1.3 1.1 0.9 0.7 96 97 98 99 00 01 02 03 04 05

Current Situation, Outlook, and Challenges

's Economy: Current Situation, Outlook, and Challenges November 8, Masaaki Shirakawa Governor of the Bank of Chart The Bank of 's Economic and Price Forecasts A. Real GDP B. CPI (all items less fresh food)..

's Economy: Current Situation, Outlook, and Challenges November 8, Masaaki Shirakawa Governor of the Bank of Chart The Bank of 's Economic and Price Forecasts A. Real GDP B. CPI (all items less fresh food)..

Stress Testing and Liquidity Analysis

Stress Testing and Liquidity Analysis Liquidity risk analysis overview Understanding portfolio effect on liquidity Margin calls and market drivers Counterparty default and downgrade, and Corporate fraud,

Stress Testing and Liquidity Analysis Liquidity risk analysis overview Understanding portfolio effect on liquidity Margin calls and market drivers Counterparty default and downgrade, and Corporate fraud,

July 2012 Chartbook The Halftime Report

Average Daily $VA LUE Traded ($Billions ) $Billions (212 ( US China Japan CHI-X London Hong Kong Germany France Canada Korea Australia Brazil Taiwan Spain India Italy $billions Switzerland Sweden Amsterdam

Average Daily $VA LUE Traded ($Billions ) $Billions (212 ( US China Japan CHI-X London Hong Kong Germany France Canada Korea Australia Brazil Taiwan Spain India Italy $billions Switzerland Sweden Amsterdam

C.I.B Report on asset quality as of June 30, 2013 Caisse Française de Financement Local (Instruction n 2011-I-07 of June 15, 2011)

") C.I.B 14 388 Report on asset quality as of June 30, 2013 Caisse Française de Financement Local (Instruction n 2011-I-07 of June 15, 2011) The report on cover pool quality, consistent with Instruction No.

C.I.B 14 388 Report on asset quality as of June 30, 2013 Caisse Française de Financement Local (Instruction n 2011-I-07 of June 15, 2011) The report on cover pool quality, consistent with Instruction No.

The Financial Turmoil in 2007 and 2008

The Financial Turmoil in 2007 and 2008 Gerald P. Dwyer June 2008 Copyright Gerald P. Dwyer, Jr., 2008 Caveats I am speaking for myself, not the Federal Reserve Bank of Atlanta or the Federal Reserve System

The Financial Turmoil in 2007 and 2008 Gerald P. Dwyer June 2008 Copyright Gerald P. Dwyer, Jr., 2008 Caveats I am speaking for myself, not the Federal Reserve Bank of Atlanta or the Federal Reserve System

Black Monday Exploring Current Financial Crisis

Black Monday Exploring Current Financial Crisis Bellevance Honors Program Mind Sharpnel & Cookies Lecture Series Salisbury University Tuesday, September 23, 2008 by Arvi Arunachalam Warning Signs Ann Lee,

Black Monday Exploring Current Financial Crisis Bellevance Honors Program Mind Sharpnel & Cookies Lecture Series Salisbury University Tuesday, September 23, 2008 by Arvi Arunachalam Warning Signs Ann Lee,

SIX YEARS ON: IS THERE AN ALTERNATIVE TO BAIL-OUT?

SIX YEARS ON: IS THERE AN ALTERNATIVE TO BAIL-OUT? L. Randall Wray Levy Economics Institute and University of Missouri - Kansas City www.levy.org; www.cfeps.org; wrayr@umkc.edu *Report of a Research Project

SIX YEARS ON: IS THERE AN ALTERNATIVE TO BAIL-OUT? L. Randall Wray Levy Economics Institute and University of Missouri - Kansas City www.levy.org; www.cfeps.org; wrayr@umkc.edu *Report of a Research Project

The Sub Prime Debacle and Financial Turmoil

The Sub Prime Debacle and Financial Turmoil Presented at the 13th Finsia and Melbourne Centre for Financial Studies Banking and Finance Conference Monday 29th and Tuesday 30th September, 2008 The University

The Sub Prime Debacle and Financial Turmoil Presented at the 13th Finsia and Melbourne Centre for Financial Studies Banking and Finance Conference Monday 29th and Tuesday 30th September, 2008 The University

2008 CRISIS : COLD OR CANCER?

2008 CRISIS : COLD OR CANCER? MARTIAL FOUCAULT Université de Montréal 28 juin 2010 1 Plan of the talk Crisis: what does it mean? The American financial crisis followed by a worldwide economic crisis Market

2008 CRISIS : COLD OR CANCER? MARTIAL FOUCAULT Université de Montréal 28 juin 2010 1 Plan of the talk Crisis: what does it mean? The American financial crisis followed by a worldwide economic crisis Market

Risultati Olimpici per gli investimenti obbligazionari. Nicholas Gartside Gestore Investimenti Obbligazionari

Risultati Olimpici per gli investimenti obbligazionari Nicholas Gartside Gestore Investimenti Obbligazionari Stagflation What does it look like? UK growth and inflation % % 8 25 6 4 2-2 -4 Trend growth

Risultati Olimpici per gli investimenti obbligazionari Nicholas Gartside Gestore Investimenti Obbligazionari Stagflation What does it look like? UK growth and inflation % % 8 25 6 4 2-2 -4 Trend growth

Confronting the Global Crisis in Latin America: What is the Outlook? Coordinators

Confronting the Global Crisis in Latin America: What is the Outlook? Policy Trade-offs May for 20, Unprecedented 2009 - Maison Times: Confronting de l Amérique the Global Crisis Latine, America, ParisIADB,

Confronting the Global Crisis in Latin America: What is the Outlook? Policy Trade-offs May for 20, Unprecedented 2009 - Maison Times: Confronting de l Amérique the Global Crisis Latine, America, ParisIADB,

The Great Recession. ECON 43370: Financial Crises. Eric Sims. Spring University of Notre Dame

The Great Recession ECON 43370: Financial Crises Eric Sims University of Notre Dame Spring 2019 1 / 38 Readings Taylor (2014) Mishkin (2011) Other sources: Gorton (2010) Gorton and Metrick (2013) Cecchetti

The Great Recession ECON 43370: Financial Crises Eric Sims University of Notre Dame Spring 2019 1 / 38 Readings Taylor (2014) Mishkin (2011) Other sources: Gorton (2010) Gorton and Metrick (2013) Cecchetti

Preview PP542. International Capital Markets. Gains from Trade. International Capital Markets. The Three Types of International Transaction Trade

Preview PP542 International Capital Markets Gains from trade Portfolio diversification Players in the international capital markets Attainable policies with international capital markets Offshore banking

Preview PP542 International Capital Markets Gains from trade Portfolio diversification Players in the international capital markets Attainable policies with international capital markets Offshore banking

Topic 2: US Financial Markets and Approaches to Regulation of Shadow Banking Professor Ian Sheldon (Ohio State University)

") Topic 2: US Financial Markets and Approaches to Regulation of Shadow Banking Professor Ian Sheldon (Ohio State University) Curso de Actualización en la Disciplina (CADi) Tecnólogico de Monterrey, Guadalajara,

Topic 2: US Financial Markets and Approaches to Regulation of Shadow Banking Professor Ian Sheldon (Ohio State University) Curso de Actualización en la Disciplina (CADi) Tecnólogico de Monterrey, Guadalajara,

Sovereign Risks and Financial Spillovers

Sovereign Risks and Financial Spillovers International Monetary Fund October 21 Roadmap What is the Outlook for Global Financial Stability? Sovereign Risks and Financial Fragilities Sovereign and Banking

Sovereign Risks and Financial Spillovers International Monetary Fund October 21 Roadmap What is the Outlook for Global Financial Stability? Sovereign Risks and Financial Fragilities Sovereign and Banking

Senior Credit Officer Opinion Survey on Dealer Financing Terms September 2016

Page 1 of 93 Senior Credit Officer Opinion Survey on Dealer Financing Terms September 2016 Print Summary Results of the September 2016 Survey Summary The September 2016 Senior Credit Officer Opinion Survey

Page 1 of 93 Senior Credit Officer Opinion Survey on Dealer Financing Terms September 2016 Print Summary Results of the September 2016 Survey Summary The September 2016 Senior Credit Officer Opinion Survey

Third Quarter 2018 Earnings Presentation. October 31, 2018

Third Quarter 2018 Earnings Presentation October 31, 2018 Safe Harbor Statement NOTE: This presentation contains certain statements that are not historical facts and that constitute forward-looking statements

Third Quarter 2018 Earnings Presentation October 31, 2018 Safe Harbor Statement NOTE: This presentation contains certain statements that are not historical facts and that constitute forward-looking statements

Copyright 2016 by the Securities Industry and Financial Markets Association 120 Broadway New York, NY (212)

") 2016 FACT BOOK 2016 FACT BOOK Produced by SIFMA Research Department Copyright 2016 by the Securities Industry and Financial Markets Association 120 Broadway New York, NY 10271-0080 (212) 313-1200 research@sifma.org

2016 FACT BOOK 2016 FACT BOOK Produced by SIFMA Research Department Copyright 2016 by the Securities Industry and Financial Markets Association 120 Broadway New York, NY 10271-0080 (212) 313-1200 research@sifma.org

Moving On Up Today s Economic Environment

Moving On Up Today s Economic Environment Presented by PFM Asset Management LLC Gray Lepley, Senior Analyst, Portfolio Strategies November 8, 2018 PFM 1 U.S. ECONOMY Today s Agenda MONETARY POLICY GEOPOLITICAL

Moving On Up Today s Economic Environment Presented by PFM Asset Management LLC Gray Lepley, Senior Analyst, Portfolio Strategies November 8, 2018 PFM 1 U.S. ECONOMY Today s Agenda MONETARY POLICY GEOPOLITICAL

Globalisation and central bank policies

Globalisation and central bank policies Lucas Papademos European Central Bank Bridge Forum Dialogue 22 January 28, Luxembourg 1 Chart 1: Oil and other commodity prices Brent crude oil price (USD per barrel)

Globalisation and central bank policies Lucas Papademos European Central Bank Bridge Forum Dialogue 22 January 28, Luxembourg 1 Chart 1: Oil and other commodity prices Brent crude oil price (USD per barrel)

Six good reasons for choosing DNB in the new banking environment

Six good reasons for choosing DNB in the new banking environment Bank of America Merrill Lynch, 18th Annual Banking & Insurance CEO Conference 2013 24 September, London Rune Bjerke, CEO of DNB 1 Reason

Six good reasons for choosing DNB in the new banking environment Bank of America Merrill Lynch, 18th Annual Banking & Insurance CEO Conference 2013 24 September, London Rune Bjerke, CEO of DNB 1 Reason

Chapter 8. Why Do Financial Crises Occur and Why Are They So Damaging to the Economy? Chapter Preview

Chapter 8 Why Do Financial Crises Occur and Why Are They So Damaging to the Economy? Chapter Preview Financial crises are major disruptions in financial markets characterized by sharp declines in asset

Chapter 8 Why Do Financial Crises Occur and Why Are They So Damaging to the Economy? Chapter Preview Financial crises are major disruptions in financial markets characterized by sharp declines in asset

Financial Crises and the Great Recession

Financial Crises and the Great Recession ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 40 Readings GLS Ch. 33 2 / 40 Financial Crises Financial crises

Financial Crises and the Great Recession ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 40 Readings GLS Ch. 33 2 / 40 Financial Crises Financial crises

Financial Crises: The Great Depression and the Great Recession

Financial Crises: The Great Depression and the Great Recession ECON 40364: Monetary Theory & Policy Eric Sims University of Notre Dame Fall 2017 1 / 43 Readings Mishkin Ch. 12 Bernanke (2002): On Milton

Financial Crises: The Great Depression and the Great Recession ECON 40364: Monetary Theory & Policy Eric Sims University of Notre Dame Fall 2017 1 / 43 Readings Mishkin Ch. 12 Bernanke (2002): On Milton

ECB Financial Stability Review

Vítor Constâncio ECB Financial Stability Review November 214 27 November 214 Press briefing presentation Rubric Recent developments Euro area systemic stress has remained at low levels despite intermittent

Vítor Constâncio ECB Financial Stability Review November 214 27 November 214 Press briefing presentation Rubric Recent developments Euro area systemic stress has remained at low levels despite intermittent

Counterparty Credit Risk Management in the US Over-the-Counter (OTC) Derivatives Markets, Part II

Derivatives Markets, Part II") November 2011 Counterparty Credit Risk Management in the US Over-the-Counter (OTC) Derivatives Markets, Part II A Review of Monoline Exposures Introduction This past August, ISDA published a short paper

November 2011 Counterparty Credit Risk Management in the US Over-the-Counter (OTC) Derivatives Markets, Part II A Review of Monoline Exposures Introduction This past August, ISDA published a short paper

THE ECONOMIC OUTLOOK RECESSION AND RECOVERY. Paul Darby Executive Director & Deuty Chief Economist Twitter hashtag: #psforum

THE ECONOMIC OUTLOOK RECESSION AND RECOVERY Paul Darby Executive Director & Deuty Chief Economist Darby@conferenceboard.ca US OUTLOOK US recession is coming to an end Q3 likely to be positive due to inventory

THE ECONOMIC OUTLOOK RECESSION AND RECOVERY Paul Darby Executive Director & Deuty Chief Economist Darby@conferenceboard.ca US OUTLOOK US recession is coming to an end Q3 likely to be positive due to inventory

Science & innovation investment framework, A view from the City

UBS Investment Research Science & innovation investment framework, 2004-2014 - A view from the City European Equity Strategy Andrew Barker +44 20 7568 0468 ANALYST CERTIFICATION AND REQUIRED DISCLOSURES

UBS Investment Research Science & innovation investment framework, 2004-2014 - A view from the City European Equity Strategy Andrew Barker +44 20 7568 0468 ANALYST CERTIFICATION AND REQUIRED DISCLOSURES

Insights from Morningstar Investment Services. Market Volatility: A Guide to Riding the Waves

Insights from Morningstar Investment Services Market Volatility: A Guide to Riding the Waves If you ve invested for almost any length of time, you ve experienced at least one of those don t-look-at-your

Insights from Morningstar Investment Services Market Volatility: A Guide to Riding the Waves If you ve invested for almost any length of time, you ve experienced at least one of those don t-look-at-your

September 16, of 106. Appendix 1: Materials used by Mr. Kos

September 16, 3 96 of 6 Appendix 1: Materials used by Mr. Kos 2. 1.8 1.6 1.4 September 16, 3 97 of 6 Page 1 Current U.S. 3-Month Deposit Rate and Rates Implied by Traded Forward Rate Agreements May 1,

September 16, 3 96 of 6 Appendix 1: Materials used by Mr. Kos 2. 1.8 1.6 1.4 September 16, 3 97 of 6 Page 1 Current U.S. 3-Month Deposit Rate and Rates Implied by Traded Forward Rate Agreements May 1,

14.09: Financial Crises Lecture 6: Collateralized Debt and Information Based Panics

14.09: Financial Crises Lecture 6: Collateralized Debt and Information Based Panics Alp Simsek Alp Simsek () Lecture Notes 1 Revisiting runs: Is Diamond-Dybvig the whole story? Diamond-Dybvig provides

14.09: Financial Crises Lecture 6: Collateralized Debt and Information Based Panics Alp Simsek Alp Simsek () Lecture Notes 1 Revisiting runs: Is Diamond-Dybvig the whole story? Diamond-Dybvig provides

Money, Liquidity and Monetary Policy * Tobias Adrian and Hyun Song Shin December Abstract

Money, Liquidity and Monetary Policy * Tobias Adrian and Hyun Song Shin December 2008 Abstract In a market-based financial system, banking and capital market developments are inseparable, and funding conditions

Money, Liquidity and Monetary Policy * Tobias Adrian and Hyun Song Shin December 2008 Abstract In a market-based financial system, banking and capital market developments are inseparable, and funding conditions

The Financial Turmoil in 2007 and 2008 Events

The Financial Turmoil in 2007 and 2008 Events Gerald P. Dwyer, Jr. May 2008 Copyright Gerald P. Dwyer, Jr., 2008 Caveats I am speaking for myself, not the Federal Reserve Bank of Atlanta or the Federal

The Financial Turmoil in 2007 and 2008 Events Gerald P. Dwyer, Jr. May 2008 Copyright Gerald P. Dwyer, Jr., 2008 Caveats I am speaking for myself, not the Federal Reserve Bank of Atlanta or the Federal

The Credit Crisis in Commercial Real Estate

The Credit Crisis in Commercial Real Estate 1 Summary Commercial real estate accounts for a meaningful 6.5% of GDP Commercial real estate entered the recession in reasonable balance The credit crisis creates

The Credit Crisis in Commercial Real Estate 1 Summary Commercial real estate accounts for a meaningful 6.5% of GDP Commercial real estate entered the recession in reasonable balance The credit crisis creates

Overcoming the crisis

Princeton, Oct 24 th, 2011 Overcoming the crisis backwards induction approach: 1. Diagnosis how did we get there? Run-up phase Crisis phase 2. Give long-run perspective Banking landscape (ESBies, European

Princeton, Oct 24 th, 2011 Overcoming the crisis backwards induction approach: 1. Diagnosis how did we get there? Run-up phase Crisis phase 2. Give long-run perspective Banking landscape (ESBies, European

Investment Opportunities in Global Fixed Income Markets

Investment Opportunities in Global Fixed Income Markets GSAM Insurance Fixed Income May 217 GSAM Insurance Asset Management Key Themes for 217 Economic Backdrop End of the Distortion Monetary to Fiscal

Investment Opportunities in Global Fixed Income Markets GSAM Insurance Fixed Income May 217 GSAM Insurance Asset Management Key Themes for 217 Economic Backdrop End of the Distortion Monetary to Fiscal

Banking, Liquidity Transformation, and Bank Runs

Banking, Liquidity Transformation, and Bank Runs ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 30 Readings GLS Ch. 28 GLS Ch. 30 (don t worry about model

Banking, Liquidity Transformation, and Bank Runs ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 30 Readings GLS Ch. 28 GLS Ch. 30 (don t worry about model

General Electric Company Financial Services Funding Policy

General Electric Company Financial Services Funding Policy How we minimize interest rate and currency risk "This document contains "forward-looking statements" within the meaning of the Private Securities

General Electric Company Financial Services Funding Policy How we minimize interest rate and currency risk "This document contains "forward-looking statements" within the meaning of the Private Securities

Asset Liability Management Report 4 Q 2018

Asset Liability Management Report 4 Q 2018 Performance Indicators and Key Measures Cash, Investment and Debt Balances Book Value ($M) Restricted Cash and Investments 529.8 Unrestricted Cash and Investments

Asset Liability Management Report 4 Q 2018 Performance Indicators and Key Measures Cash, Investment and Debt Balances Book Value ($M) Restricted Cash and Investments 529.8 Unrestricted Cash and Investments

(Comparisons Charts)

") (Comparisons Charts) IFS-A76904 Charts 1-10 Reminder: You must include the Glossary of Indices and disclosure pages with all charts you select to use, either individually or as a group. Information as

(Comparisons Charts) IFS-A76904 Charts 1-10 Reminder: You must include the Glossary of Indices and disclosure pages with all charts you select to use, either individually or as a group. Information as

The Mortgage Debt Market: A Tragedy

Purpose This is a role play designed to explain the mechanics of the 2008-2009 financial crisis. It is based on The Big Short by Michael Lewis. Cast of Characters (in order of appearance) Retail Banker

Purpose This is a role play designed to explain the mechanics of the 2008-2009 financial crisis. It is based on The Big Short by Michael Lewis. Cast of Characters (in order of appearance) Retail Banker