Investment Meeting: Summary of Views 18 April 2018

|

|

|

- Meagan Day

- 5 years ago

- Views:

Transcription

1 Investment Meeting: Summary of Views 18 April 2018 Macro Overview No change in view from last meeting. Market is still pricing in 80% probability of a 25 bps at June 13 meeting. Current data are not supportive of the case for higher inflation with the key data (PCE deflator, US Capacity Utilization and US Financial Conditions Index) showing inflation under control. Europe: the ECB s primary focus is the target inflation rate (2%) over the medium-term. EZ Financial Conditions remain relatively loose, EZ All-Item Inflation index has picked up to 1.40% but EZ Capacity Utilization is nearing levels which could lead to more inflationary pressures. Current Market Conditions Markets mixed start to April with an upbeat note but nervous and low volumes since our last bi-weekly review. Equity markets (range trading with muted reactions to initial earnings releases, fixed income getting a bid. USD Fixed Income: UST short-term rates moving gradually higher while 10s largely unchanged resulting in a gradual flattening of the yield curve. Credit spreads tighten slightly for both Inv. Grade and High Yield but largely due to UST rate increases. Current Market Conditions (cont d) EUR Fixed Income: Government 5 & 10 yr. rates coming back down on a lack of rising inflation even as 2s remain relatively flat driving the yield curve to flatten slightly. Emerging Market Fixed Income: Credit spreads coming back in somewhat and reflective of UST rates. Trade issues remain in focus albeit signs out of China seem to indicate potential easing. Equity Market: US valuations are now somewhat more attractive post correction. Expected earnings growth (market pricing in 15-20% growth in 2018). Europe and Japan show value on P/B and some value on P/S. EM markets are priced at the most attractive levels in comparison to DM. Market Technicals Key Levels and charts on slide 10. Fund Holdings Updates on our current holdings / target funds in the attached Summary.

2 Market Performance Update Returns As of: 17-Apr-18 YTD Equity Indices (USD Mar'18 16-Apr-18 MSCI WORLD -2.4% -0.2% MSCI ACWI -2.4% -0.1% S&P % 0.2% NASDAQ COMP. -2.9% 3.7% RUSSELL % 1.8% STXE 600 $ Pr -1.5% 0.0% EM Asia USD -1.5% 2.1% MSCI AC ASIA x JAPAN -1.6% 0.6% EM Latin America USD -1.1% 5.5% EM Europe -4.9% -5.1% Asset Class Comparative Performance Bl.-Barc. Bond Mar'18 16-Apr-18 Global Aggregate 1.1% 1.4% U.S. Corp 0.3% -2.3% US Corp High Yield -0.6% 0.4% Pan-Euro Agg Corp 0.1% -0.1% Pan-Euro HY Unh Eur -0.1% 0.7% EM USD Aggregate 0.1% -1.5% EM Pan-Euro Agg. Unh. 0.3% -0.2% EM Local CY Aggregate 1.3% 2.1% Alternative Assets Mar'18 16-Apr-18 HFR Macro/CTA -0.8% -1.5% HFR Global Hedge -1.0% -0.6% HFR Absolute Return -0.1% 0.5% BBG Commodity TR -0.6% 1.4% BBG Agriculture TR -2.8% 2.8% BBG Energy TR 4.9% 3.5% BBG Industrial Metals TR -4.4% -0.1% Gold vs USD 0.5% 3.3% Source: Bloomberg

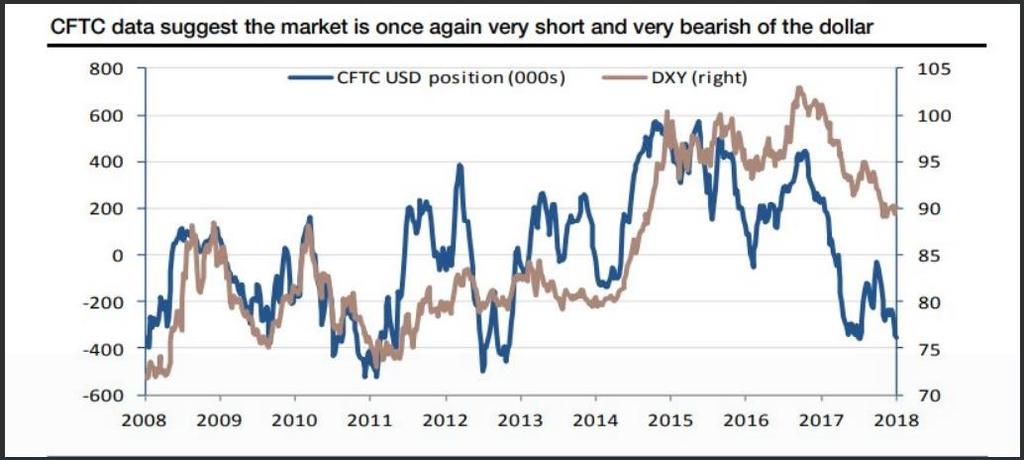

3 Currency Performance Update Returns As of: 17-Apr-18 USD Returns vs FX 3 Mos. To Mar'18 Mar'18 YTD USDMXN -3.3% -7.5% -8.5% USDBRL 1.8% -0.2% 3.2% USDCAD 0.7% 2.6% -0.1% USDEUR -0.9% -2.6% -3.3% USDCHF 1.0% -2.1% -1.5% USDGBP -1.6% -3.6% -6.0% USDRUB 2.0% -0.6% 5.8% USDJPY -0.4% -5.7% -5.1% USDAUD 1.4% 1.6% 0.2% USDCNY -0.9% -3.6% -3.5% USDINR 0.0% 2.0% 2.8% XAUUSD 0.5% 1.7% 3.3% Source: Bloomberg USD performance in March has been more reflective of idiosyncratic risks rather than any predominant theme. The big moves have been limited to a few notable currency pairs. The ever-shifting US trade policy has been reflected in a stronger MXN vs USD as talk of progress in NAFTA talks has brought buyers back into the currency. Geopolitics has been evident in the significant rise of the USD vs RUB as the Skripal poisoning led to increasing diplomatic and economic sanctions against Russia. The other big USD gains this past month have been against the commodity exporters (USDBRL and USDAUD) reflective of the drop in industrial metals prices. Unlike 2017, the year to date picture for the USD shows no clear patterns.

.")

is still near multi-decade lows. US Capacity Utilization: Feb. At 77.")

4 The Week s Macro Indicators US Fed under Chairman Powell is unlikely to diverge from its data-driven approach to setting the Fed Fuds target rate. The market is pricing in a 88.6% probability that Fed Funds will move up to % range (+25bps). We currently expect an additional +75bps (3 x 25bps) over the course of 2018 to proceed in a well-telegraphed manner subject to economic growth coming through as expected. U-3 Unemployment rate: Mar data remained steady at 4% but US Labor Force Participation rate (62.9%) is still near multi-decade lows. US Capacity Utilization: Feb. At 77.7% moving up but still not above the 80-82% levels which would lead to increased inflation fears. PCE (Personal Consumption Expenditure) Deflator: Jan. At 1.6% is edging closer to the Fed's 2% target level. Bloomberg Financial Conditions Index: somewhat tighter financing environment need to watch. Mr. Draghi's ECB is largely focused on the expected inflation rate and, like the US Fed, targets a 2% level over the medium term (subject to interpretation). the data in Europe seems to indicate a higher probability of the ECB tapering its QE policies as three out of four indicators are flashing potential inflationary pressures. The most important data point (EZ All-Item Inflation) is not showing much sign of life yet as it lingers below 1.5%. We expect policy rates to remain unchanged for the rest of The Latest Data show limited pressure for faster policy decisions. Euro Zone Unemployment rate: December data (8.70%) shows continued improvement. EZ Capacity Utilization: last print for December (83.8%) approaching levels indicative of capacity constraints. EZ All-item Inflation: February print at 1.10% shows no inflationary pressures forthcoming.

5 Fixed Income: US & EUR Overview US Treasuries: 2s, 5s and 10s (%) EUR Govies: 2s, 5s and 10s (%) USD: Global IG and Global High Yield Corp. Spreads (bps) EM Debt: USD & EUR Aggregate Spreads (bps)

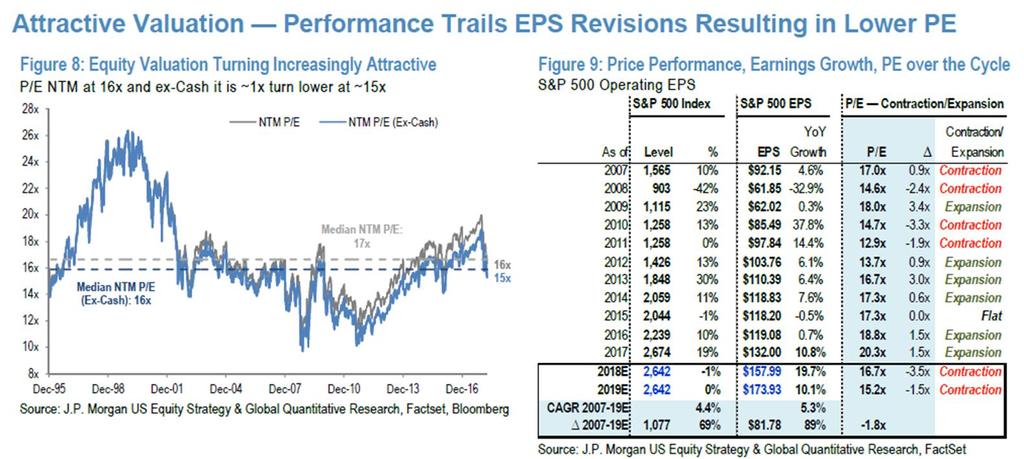

6 Global Equity: Overview Equity Market Valuation vs 7yr Hi-Lo As of: 17-Apr-18 Price/Book 7 Yr Price/Sales 7yr Dividend Trailing 12 Est. EPS Growth Current P/B % From Current P/S % From Index Last Price Yield (%) Mo EPS* Earnings** Est Est P/E Pr/Book Low Hi Hi Pr/Sales Low Hi Hi SP500 2, % % % Dow Jones Industr 24, % % % Nasdaq 7, % % % Stoxx 600 Europe % % % Nikkei 21, % % % MSCI Asia X-Japan % % % MSCI Emerging 1, % % % MSCI Emerging Eur % % % MSCI Emerging Asi % % % MSCI Emerging Lat 2, % % % MSCI India 1, % % % MSCI China % % % Source: Bloomberg * - diluted eps from continuing ops. includes one time, extraordinary gains/losses ** -Bloomberg consensus EPS GAAP estimates excluding one time, extraordinary gains/losses We look at market levels on three key metrics (current Price to next 12 months estimated Earnings (Est P/E), current Price to Book Value (P/B) and current Price tosales. While these measures alone do not necessarily account for markets' potential to continue to move higher, they do provide a good sense of the relative value of different global equity markets. The US market valuation has improved post the recent sell-off combined with the improving earnings picture. At 16.9x the estimated PE levels (12 mos forward) is now trading near the historical median and both a Price/Book and Price/Sales basis are 5 percent below this cycle highs. European markets continue to look more attractive with some upside to valuations acroos all measures. Japanese markets are have come off from the 7 year highs and look attractive. Emerging markets look the best value on these metrics across the board.

7 No change in SP500 EPS growth expecations for the coming quarter. Earnings and Sales Growth Expectations GS vs Consensus JPM seeing împroving revisions on both Sales and EPS growth for full year 2018 Source: Goldman Sachs

8 S&P500 Market Valuations

9 IDAR Performance Snapshot

10 Market Technicals Key Slides

11

12

13

14

15

16

17

MARCH 2018 Capital Markets Update

MARCH 2018 Market commentary ECONOMIC CLIMATE Hiring slowed from its fast pace last month the U.S. added 103,000 jobs to nonfarm payrolls in March, below the consensus estimate of 185,000. The U-3 unemployment

MARCH 2018 Market commentary ECONOMIC CLIMATE Hiring slowed from its fast pace last month the U.S. added 103,000 jobs to nonfarm payrolls in March, below the consensus estimate of 185,000. The U-3 unemployment

Seizing Opportunities in 2011 and Beyond

Seizing Opportunities in 2011 and Beyond Why We re Here Today Markets displayed lower volatility in 2010. But serious questions remain: Are interest rates headed higher? Where can investors find yield?

Seizing Opportunities in 2011 and Beyond Why We re Here Today Markets displayed lower volatility in 2010. But serious questions remain: Are interest rates headed higher? Where can investors find yield?

Economic and Financial Markets Monthly Review & Outlook Detailed Report January 2018

Economic and Financial Markets Monthly Review & Outlook Detailed Report January 1 NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE Overview of the Economy Business and economic confidence continue to

Economic and Financial Markets Monthly Review & Outlook Detailed Report January 1 NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE Overview of the Economy Business and economic confidence continue to

2015 Market Review & Outlook. January 29, 2015

2015 Market Review & Outlook January 29, 2015 Economic Outlook Jason O. Jackman, CFA President & Chief Investment Officer Percentage Interest Rates Unexpectedly Decline 4.5 10-Year Government Yield 4 3.5

2015 Market Review & Outlook January 29, 2015 Economic Outlook Jason O. Jackman, CFA President & Chief Investment Officer Percentage Interest Rates Unexpectedly Decline 4.5 10-Year Government Yield 4 3.5

Global Economic and Market Outlook for Gavyn Davies, Chairman, Fulcrum Asset Management

Global Economic and Market Outlook for 2018 Gavyn Davies, Chairman, Fulcrum Asset Management After many years of persistent downgrades to consensus GDP forecasts, 2017 has seen the first upgrades since

Global Economic and Market Outlook for 2018 Gavyn Davies, Chairman, Fulcrum Asset Management After many years of persistent downgrades to consensus GDP forecasts, 2017 has seen the first upgrades since

WEEKLY MARKET FLASH DATA AS OF FEBRUARY 2, Index definitions available upon request. 1 of 5. Total Return (%)

") WEEKLY MARKET FLASH DATA AS OF FEBRUARY 2, 2018 U.S. Equity Index Level 1 Week MTD QTD YTD 1 Year Global Equity USD 1 Week MTD QTD YTD 1 Year S&P 500 2,762 (3.81) (2.16) 3.44 3.44 23.54 DJIA 25,521 (4.11)

WEEKLY MARKET FLASH DATA AS OF FEBRUARY 2, 2018 U.S. Equity Index Level 1 Week MTD QTD YTD 1 Year Global Equity USD 1 Week MTD QTD YTD 1 Year S&P 500 2,762 (3.81) (2.16) 3.44 3.44 23.54 DJIA 25,521 (4.11)

OCTOBER 2018 Capital Markets Update

OCTOBER 2018 Market commentary U.S. ECONOMICS U.S. real GDP grew at an annualized quarterly rate of 3.5% (3. YoY) in Q3, beating expectations of 3.4%. The economy was supported by the strongest consumer

OCTOBER 2018 Market commentary U.S. ECONOMICS U.S. real GDP grew at an annualized quarterly rate of 3.5% (3. YoY) in Q3, beating expectations of 3.4%. The economy was supported by the strongest consumer

MAY 2018 Capital Markets Update

MAY 2018 Market commentary U.S. ECONOMICS The U.S. added 223,000 jobs to payrolls in May, well above the consensus estimate of 180,000 and the expansion average of around 200,000. Sector job gains were

MAY 2018 Market commentary U.S. ECONOMICS The U.S. added 223,000 jobs to payrolls in May, well above the consensus estimate of 180,000 and the expansion average of around 200,000. Sector job gains were

Summit Strategies Group 8182 Maryland Avenue, 6th Floor St. Louis, Missouri Monthly Economic & Capital Market Update

Summit Strategies Group 8182 Maryland Avenue, 6th Floor St. Louis, Missouri 63105 314.727.7211 Monthly Economic & Capital Market Update July 2015 Yield to Maturity Monthly Change Jul-63 Jul-67 Jul-71 Jul-75

Summit Strategies Group 8182 Maryland Avenue, 6th Floor St. Louis, Missouri 63105 314.727.7211 Monthly Economic & Capital Market Update July 2015 Yield to Maturity Monthly Change Jul-63 Jul-67 Jul-71 Jul-75

Economic Outlook. DMS Economic Outlook for next 12 months

Economic Outlook DMS Economic Outlook for next 12 months GDP growth will be modest at approximately 2.5%, but the economy will experience periods of unstable growth. Consumer confidence will improve as

Economic Outlook DMS Economic Outlook for next 12 months GDP growth will be modest at approximately 2.5%, but the economy will experience periods of unstable growth. Consumer confidence will improve as

WEEKLY MARKET UPDATE. H-shares rally still has further to go. Performance. Asset Allocation. Weekly Market Update 14 April 2015.

WEEKLY MARKET UPDATE 14 April 2015 H-shares rally still has further to go Hong Kong listed Chinese equities (H-shares) sky-rocketed last week, triggered by upward southbound flows. This outperformance

WEEKLY MARKET UPDATE 14 April 2015 H-shares rally still has further to go Hong Kong listed Chinese equities (H-shares) sky-rocketed last week, triggered by upward southbound flows. This outperformance

Global House View: Market Outlook

HSBC GLOBAL ASSET MANAGEMENT September 29 Global House View: Market Outlook Contents 1688/HSB1395a Market performance Macro-economic Picture Market Views: high level asset allocation Market Views: Equity

HSBC GLOBAL ASSET MANAGEMENT September 29 Global House View: Market Outlook Contents 1688/HSB1395a Market performance Macro-economic Picture Market Views: high level asset allocation Market Views: Equity

FINANCIAL FORECASTS ECONOMIC RESEARCH. January No. 1. What will be the characteristics of euro-zone financial markets in 2016?

ECONOMIC RESEARCH January - No. What will be the characteristics of euro-zone financial markets in? We believe investors will be faced with the following characteristics in euro-zone financial markets

ECONOMIC RESEARCH January - No. What will be the characteristics of euro-zone financial markets in? We believe investors will be faced with the following characteristics in euro-zone financial markets

Weekly Market Commentary

LPL FINANCIAL RESEARCH Weekly Market Commentary November 18, 2014 Emerging Markets Opportunity Still Emerging Burt White Chief Investment Officer LPL Financial Jeffrey Buchbinder, CFA Market Strategist

LPL FINANCIAL RESEARCH Weekly Market Commentary November 18, 2014 Emerging Markets Opportunity Still Emerging Burt White Chief Investment Officer LPL Financial Jeffrey Buchbinder, CFA Market Strategist

Asset Strategy Consultants. MARKET ENVIRONMENT Third Quarter 2016

MARKET ENVIRONMENT Third Quarter 2016 Market Environment: Economy Investor angst over the unexpected vote on Brexit was short lived with a "risk on" theme returning to the markets in July and leading to

MARKET ENVIRONMENT Third Quarter 2016 Market Environment: Economy Investor angst over the unexpected vote on Brexit was short lived with a "risk on" theme returning to the markets in July and leading to

DECEMBER 2018 Capital Markets Update

DECEMBER 2018 Market commentary U.S. ECONOMICS Nonfarm payrolls jumped by 312,000 in December, well above expectations for a 176,000 increase. The healthcare sector (+50,000) led job creation, while restaurants

DECEMBER 2018 Market commentary U.S. ECONOMICS Nonfarm payrolls jumped by 312,000 in December, well above expectations for a 176,000 increase. The healthcare sector (+50,000) led job creation, while restaurants

SEPTEMBER 2018 Capital Markets Update

SEPTEMBER 2018 Market commentary U.S. ECONOMICS Non-farm payrolls added 134,000 jobs in September, missing the consensus estimate of 185,000. However, net revisions to the two months prior totaled +87,000

SEPTEMBER 2018 Market commentary U.S. ECONOMICS Non-farm payrolls added 134,000 jobs in September, missing the consensus estimate of 185,000. However, net revisions to the two months prior totaled +87,000

Economic and Financial Markets Monthly Review & Outlook Detailed Report. June 2014

Economic and Financial Markets Monthly Review & Outlook Detailed Report June 1 Overview of the Economy In the U.S., the Federal Reserve s Beige Book report on the economy through late May indicated that

Economic and Financial Markets Monthly Review & Outlook Detailed Report June 1 Overview of the Economy In the U.S., the Federal Reserve s Beige Book report on the economy through late May indicated that

2018 MACRO OVERVIEW. More of the Same, Yet Less of the Same. March 9, 2018

2018 MACRO OVERVIEW More of the Same, Yet Less of the Same March 9, 2018 RICHARD FARR MERION CAPITAL GROUP 484-436-4764 rfarr@merioncapitalgroup.com Jan-04 Oct-04 Jul-05 Apr-06 Jan-07 Oct-07 Jul-08 Apr-09

2018 MACRO OVERVIEW More of the Same, Yet Less of the Same March 9, 2018 RICHARD FARR MERION CAPITAL GROUP 484-436-4764 rfarr@merioncapitalgroup.com Jan-04 Oct-04 Jul-05 Apr-06 Jan-07 Oct-07 Jul-08 Apr-09

Asset Strategy Consultants. MARKET ENVIRONMENT First Quarter 2017

MARKET ENVIRONMENT First Quarter 2017 Market Environment: Economy Economies in the U.S. and Europe continued to gain traction. Expectations for lower taxes, reduced regulation, and other pro-growth reforms

MARKET ENVIRONMENT First Quarter 2017 Market Environment: Economy Economies in the U.S. and Europe continued to gain traction. Expectations for lower taxes, reduced regulation, and other pro-growth reforms

The increasing importance of multi asset solutions genuine diversification to reduce total risk

The increasing importance of multi asset solutions genuine diversification to reduce total risk Ariconsult Vermögensverwaltungs-Symposium 17 September 2014 Richard Batty Fund Manager, Multi Asset This

The increasing importance of multi asset solutions genuine diversification to reduce total risk Ariconsult Vermögensverwaltungs-Symposium 17 September 2014 Richard Batty Fund Manager, Multi Asset This

Seven-year asset class forecast returns, 2015 update

Schroders Seven-year asset class forecast returns, 2015 update Craig Botham Emerging Markets Economist Introduction Our seven-year returns forecast builds on the same methodology which has been applied

Schroders Seven-year asset class forecast returns, 2015 update Craig Botham Emerging Markets Economist Introduction Our seven-year returns forecast builds on the same methodology which has been applied

Tracking the Growth Catalysts in Emerging Markets

Tracking the Growth Catalysts in Emerging Markets September 14, 2016 by Nick Niziolek of Calamos Investments The following is an excerpt of remarks made on August 30, 2016. The majority of the improved

Tracking the Growth Catalysts in Emerging Markets September 14, 2016 by Nick Niziolek of Calamos Investments The following is an excerpt of remarks made on August 30, 2016. The majority of the improved

Leumi. Global Economics Monthly Review. Arie Tal, Research Economist. May 8, The Finance Division, Economics Department. leumiusa.

Global Economics Monthly Review May 8, 2018 Arie Tal, Research Economist The Finance Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report Key

Global Economics Monthly Review May 8, 2018 Arie Tal, Research Economist The Finance Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report Key

Economic and Capital Market Update April 2018

Economic and Capital Market Update April 2018 Apr-70 Apr-74 Apr-78 Apr-82 Apr-86 Apr-90 Apr-94 Apr-98 Apr-02 Apr-06 Apr-10 Apr-14 Apr-18 April 30, 2018 Economic Perspective The strong pace of the global

Economic and Capital Market Update April 2018 Apr-70 Apr-74 Apr-78 Apr-82 Apr-86 Apr-90 Apr-94 Apr-98 Apr-02 Apr-06 Apr-10 Apr-14 Apr-18 April 30, 2018 Economic Perspective The strong pace of the global

B-GUIDE: Economic Outlook

Aug-12 Apr-13 Dec-13 Aug-14 Apr-15 Dec-15 Aug-16 Apr-17 Jul-15 Nov-15 Mar-16 Jul-16 Nov-16 Mar-17 Jul-17 Quarterly Economic Outlook: Quarter 4 2017 4 January 2018 B-GUIDE: Economic Outlook The economy

Aug-12 Apr-13 Dec-13 Aug-14 Apr-15 Dec-15 Aug-16 Apr-17 Jul-15 Nov-15 Mar-16 Jul-16 Nov-16 Mar-17 Jul-17 Quarterly Economic Outlook: Quarter 4 2017 4 January 2018 B-GUIDE: Economic Outlook The economy

Moving On Up Today s Economic Environment

Moving On Up Today s Economic Environment Presented by PFM Asset Management LLC Gray Lepley, Senior Analyst, Portfolio Strategies November 8, 2018 PFM 1 U.S. ECONOMY Today s Agenda MONETARY POLICY GEOPOLITICAL

Moving On Up Today s Economic Environment Presented by PFM Asset Management LLC Gray Lepley, Senior Analyst, Portfolio Strategies November 8, 2018 PFM 1 U.S. ECONOMY Today s Agenda MONETARY POLICY GEOPOLITICAL

ASSET ALLOCATION FLASH

FOR PROFESSIONAL INVESTORS 25 June 2018 ASSET ALLOCATION FLASH BNPP AM Multi Asset, Quantitative and Solutions (MAQS) MID-YEAR REVERSALS Asset allocation overview: Christophe MOULIN Head of Multi Asset,

FOR PROFESSIONAL INVESTORS 25 June 2018 ASSET ALLOCATION FLASH BNPP AM Multi Asset, Quantitative and Solutions (MAQS) MID-YEAR REVERSALS Asset allocation overview: Christophe MOULIN Head of Multi Asset,

Market Commentary - 2nd Quarter 2017

3 Months YTD 1 Year 3 Years 5 Years 1 Years As the economy picks up we will need to be gradual when adjusting our policy parameters, so as to ensure that our stimulus accompanies the recovery amid the

3 Months YTD 1 Year 3 Years 5 Years 1 Years As the economy picks up we will need to be gradual when adjusting our policy parameters, so as to ensure that our stimulus accompanies the recovery amid the

Global Market Overview

First Quarter 219 First Quarter 219: March Madness, or Just an Incredible Rebound? Global Market Overview MSCI All Country World S&P Russell 2 MSCI EAFE MSCI Emerging Markets MSCI ACWI ex USA Small BBgBarc

First Quarter 219 First Quarter 219: March Madness, or Just an Incredible Rebound? Global Market Overview MSCI All Country World S&P Russell 2 MSCI EAFE MSCI Emerging Markets MSCI ACWI ex USA Small BBgBarc

Keynote Address: Jeff Gundlach Presenter Chief Executive Officer & Chief Investment Officer DoubleLine Capital

Keynote Address: Jeff Gundlach Presenter Chief Executive Officer & Chief Investment Officer DoubleLine Capital This Time It s Different 2 3 Past Fed Tightening Cycles Source: ValueWalk, Taking a Lesson

Keynote Address: Jeff Gundlach Presenter Chief Executive Officer & Chief Investment Officer DoubleLine Capital This Time It s Different 2 3 Past Fed Tightening Cycles Source: ValueWalk, Taking a Lesson

2014 CAPITAL MARKET ASSUMPTIONS. January SEATTLE LOS ANGELES

2014 CAPITAL MARKET ASSUMPTIONS January 2014 SEATTLE 206.622.3700 LOS ANGELES 310.297.1777 www.wurts.com TABLE OF CONTENTS Summary Page 3 Overview of Methodology Page 7 Inflation Page 9 Fixed Income Page

2014 CAPITAL MARKET ASSUMPTIONS January 2014 SEATTLE 206.622.3700 LOS ANGELES 310.297.1777 www.wurts.com TABLE OF CONTENTS Summary Page 3 Overview of Methodology Page 7 Inflation Page 9 Fixed Income Page

MULTI-ASSET CLASS 1 EQUITIES: DEVELOPED COUNTRIES 1 EQUITY EMERGING COUNTRIES 2

10 2 3 6 8 9 13 14 MULTI-ASSET CLASS 1 EQUITIES: DEVELOPED COUNTRIES 1 EQUITY EMERGING COUNTRIES 2 Alpha Current Previous Alpha Current Previous Alpha Current Previous weight weight weight weight weight

10 2 3 6 8 9 13 14 MULTI-ASSET CLASS 1 EQUITIES: DEVELOPED COUNTRIES 1 EQUITY EMERGING COUNTRIES 2 Alpha Current Previous Alpha Current Previous Alpha Current Previous weight weight weight weight weight

Market Insight Economy and Asset Classes December Oil Prices Downtrending: The Real Global Economic Stimulus

Market Insight Economy and Asset Classes December 2014 Oil Prices Downtrending: The Real Global Economic Stimulus 2 Equities Markets Feature In Citi analysts view, the expansion phase the US are enjoying

Market Insight Economy and Asset Classes December 2014 Oil Prices Downtrending: The Real Global Economic Stimulus 2 Equities Markets Feature In Citi analysts view, the expansion phase the US are enjoying

A recap of last week s top economic news and what s to come.

AGF INVESTMENTS September 11, 2017 A recap of last week s top economic news and what s to come. WEEKLY MARKET REVIEW BANK OF CANADA HIKES RATES ONCE AGAIN The Bank of Canada (BoC) held firm on its plans

AGF INVESTMENTS September 11, 2017 A recap of last week s top economic news and what s to come. WEEKLY MARKET REVIEW BANK OF CANADA HIKES RATES ONCE AGAIN The Bank of Canada (BoC) held firm on its plans

INVESTMENT OUTLOOK JUNE 2018 MACRO-ECONOMICS. Developed and Emerging Markets

INVESTMENT OUTLOOK JUNE 2018 MACRO-ECONOMICS Developed and Emerging Markets Trade tariffs and protectionist themes have dominated global markets throughout the year and risks have further heightened through

INVESTMENT OUTLOOK JUNE 2018 MACRO-ECONOMICS Developed and Emerging Markets Trade tariffs and protectionist themes have dominated global markets throughout the year and risks have further heightened through

2019 Annual Outlook Volatility & Opportunities in the Late Stage Bull Market

2019 Annual Outlook Volatility & Opportunities in the Late Stage Bull Market Asia Pacific Wealth Management December 2018 INVESTMENT PRODUCTS: NOT A BANK DEPOSIT. NOT GOVERNMENT INSURED. NO BANK GUARANTEE.

2019 Annual Outlook Volatility & Opportunities in the Late Stage Bull Market Asia Pacific Wealth Management December 2018 INVESTMENT PRODUCTS: NOT A BANK DEPOSIT. NOT GOVERNMENT INSURED. NO BANK GUARANTEE.

CME Group 3Q 2015 Earnings Conference Call

CME Group 3Q 2015 Earnings Conference Call October 29, 2015 Forward Looking Statements Statements in this presentation that are not historical facts are forward-looking statements. These statements are

CME Group 3Q 2015 Earnings Conference Call October 29, 2015 Forward Looking Statements Statements in this presentation that are not historical facts are forward-looking statements. These statements are

Markets Overview Pulse & calendar Economic scenario

: : : : 8: 1: 1: 1: 1: 18: : : : : : : 8: 1: 1: 1: 1: 18: : : : : : : 8: 1: 1: 1: Markets have reacted in a calm way to the US decision to withdraw from the Iran nuclear deal Despite the increase in geopolitical

: : : : 8: 1: 1: 1: 1: 18: : : : : : : 8: 1: 1: 1: 1: 18: : : : : : : 8: 1: 1: 1: Markets have reacted in a calm way to the US decision to withdraw from the Iran nuclear deal Despite the increase in geopolitical

FOREX WEEKLY. Weekly information issued by the FOREX Advisory Team. Trader view in 2 snapshots. 4 October Global Forex Sentiment

FOREX WEEKLY 4 October 2017 Weekly information issued by the FOREX Advisory Team Global Forex Sentiment The global recovery continues, well synchronized across regions and broadening into investment. US

FOREX WEEKLY 4 October 2017 Weekly information issued by the FOREX Advisory Team Global Forex Sentiment The global recovery continues, well synchronized across regions and broadening into investment. US

September 16, of 106. Appendix 1: Materials used by Mr. Kos

September 16, 3 96 of 6 Appendix 1: Materials used by Mr. Kos 2. 1.8 1.6 1.4 September 16, 3 97 of 6 Page 1 Current U.S. 3-Month Deposit Rate and Rates Implied by Traded Forward Rate Agreements May 1,

September 16, 3 96 of 6 Appendix 1: Materials used by Mr. Kos 2. 1.8 1.6 1.4 September 16, 3 97 of 6 Page 1 Current U.S. 3-Month Deposit Rate and Rates Implied by Traded Forward Rate Agreements May 1,

February market performance. Index. Index. Global economies

March 2016 Global equity markets continued to correct through February but stage an early March recovery Oil prices staged a strong recovery from mid-february up 37% China economic data continued to consolidate

March 2016 Global equity markets continued to correct through February but stage an early March recovery Oil prices staged a strong recovery from mid-february up 37% China economic data continued to consolidate

Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy April 2017 Stock Markets likely to Grind Higher as Expectations of Strong Earnings Growth & Improving Global GDP

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy April 2017 Stock Markets likely to Grind Higher as Expectations of Strong Earnings Growth & Improving Global GDP

Q MARKETS REVIEW

Stock markets around the world continued their ascent during the quarter as investors took solace in continuing corporate earnings growth, fueled by strong global economic growth, and U.S. tax cuts. Overview

Stock markets around the world continued their ascent during the quarter as investors took solace in continuing corporate earnings growth, fueled by strong global economic growth, and U.S. tax cuts. Overview

Navigating the Fixed Income Minefield

Navigating the Fixed Income Minefield Jeffrey Sherman, CFA Portfolio Manager DoubleLine Capital February 20, 2014 When all the experts and forecasts agree -- something else is going to happen. - Bob Farrell

Navigating the Fixed Income Minefield Jeffrey Sherman, CFA Portfolio Manager DoubleLine Capital February 20, 2014 When all the experts and forecasts agree -- something else is going to happen. - Bob Farrell

January market performance. Equity Markets Price Indices Index

Global Central Banks continue to lower interest rates. The RBA cuts the cash rate by 25bp to 2.25% (February 2015). The ECB finally announces Quantitative Easing 60b per month. Oil prices declined again

Global Central Banks continue to lower interest rates. The RBA cuts the cash rate by 25bp to 2.25% (February 2015). The ECB finally announces Quantitative Easing 60b per month. Oil prices declined again

INVESTMENT OUTLOOK. August 2017

INVESTMENT OUTLOOK August 2017 INVESTMENT OUTLOOK AUGUST 2017 MACRO-ECONOMICS AND CURRENCIES Developed and Emerging Markets A series of comments from major central banks during the month, reminded investors

INVESTMENT OUTLOOK August 2017 INVESTMENT OUTLOOK AUGUST 2017 MACRO-ECONOMICS AND CURRENCIES Developed and Emerging Markets A series of comments from major central banks during the month, reminded investors

NOVEMBER 2018 Capital Markets Update

NOVEMBER 2018 Market commentary U.S. ECONOMICS Non-farm payrolls added 155,000 jobs in November, missing expectations of 198,000, and the unemployment rate held steady at 3.7%. The labor force participation

NOVEMBER 2018 Market commentary U.S. ECONOMICS Non-farm payrolls added 155,000 jobs in November, missing expectations of 198,000, and the unemployment rate held steady at 3.7%. The labor force participation

November PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy November 2015 John Praveen, PhD Chief Investment Strategist FOR MORE INFORMATION CONTACT: Theresa Miller Phone:

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy November 2015 John Praveen, PhD Chief Investment Strategist FOR MORE INFORMATION CONTACT: Theresa Miller Phone:

Market Outlook. July 2015

Market Outlook July 2015 Greece Defaults; Contagion Risks Limited Greek government failed to make the EUR 1.6bn IMF debt payment due on 30 June and becomes the first nation to default on IMF since Mugabe's

Market Outlook July 2015 Greece Defaults; Contagion Risks Limited Greek government failed to make the EUR 1.6bn IMF debt payment due on 30 June and becomes the first nation to default on IMF since Mugabe's

June 2013 Equities Rally Drive Global Re-rating

June 2013 Equities Rally Drive Global Re-rating Since the lows of 2011, global equities have rallied 30% while Earnings per Share remained flat. This has been the biggest mid-cycle re-rating of global

June 2013 Equities Rally Drive Global Re-rating Since the lows of 2011, global equities have rallied 30% while Earnings per Share remained flat. This has been the biggest mid-cycle re-rating of global

the drive you demand ASSET ALLOCATION June 2017 Global Investment Committee

the drive you demand ASSET ALLOCATION June 217 Global Investment Committee GLOBAL TACTICAL ASSET ALLOCATION Rising earnings argue for remaining overweight equities Global economy / Asset allocation Sustained

the drive you demand ASSET ALLOCATION June 217 Global Investment Committee GLOBAL TACTICAL ASSET ALLOCATION Rising earnings argue for remaining overweight equities Global economy / Asset allocation Sustained

Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy March 2017 Global Stock Markets Rally likely to Continue, Driven by Strong Earnings & Strengthening GDP Growth.

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy March 2017 Global Stock Markets Rally likely to Continue, Driven by Strong Earnings & Strengthening GDP Growth.

World Equity Market Performance Top 10 USD Adjusted Returns, 2006

World Equity Market Performance Top 1 USD Adjusted Returns, 26 Percent Change, Year Ago 2 18 16 14 12 1 8 6 4 2 Venezuela Cyprus Botswana Morocco Russia Peru Vietnam China Yugoslavia Croatia Source: Bloomberg

World Equity Market Performance Top 1 USD Adjusted Returns, 26 Percent Change, Year Ago 2 18 16 14 12 1 8 6 4 2 Venezuela Cyprus Botswana Morocco Russia Peru Vietnam China Yugoslavia Croatia Source: Bloomberg

Markets overview Pulse & calendrar Economic scenario UNEMPLOYMENT VS INFLATION 2,6 2,4 2,2 2 1,8 1,6 1,4 1,2 1 0,8.

Core PCE, y/y % The FOMC has an asymmetrical loss function: avoiding a recession is more important than avoiding the risk of overheating With this comes the necessity of a symmetrical inflation objective:

Core PCE, y/y % The FOMC has an asymmetrical loss function: avoiding a recession is more important than avoiding the risk of overheating With this comes the necessity of a symmetrical inflation objective:

SEB House View 13 June 2018

SEB House View 3 June 8 Summary Decision variables Macro and Markets Market Indicators In Focus Asset Class and Sector Views Risk Environment Summary - In expectation of a re-acceleration in global PMIs

SEB House View 3 June 8 Summary Decision variables Macro and Markets Market Indicators In Focus Asset Class and Sector Views Risk Environment Summary - In expectation of a re-acceleration in global PMIs

Global Macroeconomic Monthly Review

Global Macroeconomic Monthly Review October 16 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Please see disclaimer on the last page of this report 1 Key Issues Global

Global Macroeconomic Monthly Review October 16 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Please see disclaimer on the last page of this report 1 Key Issues Global

Ulster Bank Weekly Economic Commentary

Ulster Bank Weekly Economic Commentary Ricardo Amaro Economist 15 June 2018 To subscribe or unsubscribe please contact economics@ulsterbankcm.com Ireland: New housing dwellings revised significantly lower

Ulster Bank Weekly Economic Commentary Ricardo Amaro Economist 15 June 2018 To subscribe or unsubscribe please contact economics@ulsterbankcm.com Ireland: New housing dwellings revised significantly lower

Economic and Financial Markets Monthly Review & Outlook Detailed Report October 2017

Economic and Financial Markets Monthly Review & Outlook Detailed Report October 17 NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE Overview of the Economy Business and economic confidence indicators

Economic and Financial Markets Monthly Review & Outlook Detailed Report October 17 NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE Overview of the Economy Business and economic confidence indicators

Perspectives JAN Market Preview: Non-U.S. Equities

Perspectives JAN 2018 2018 Market Preview: Non-U.S. Equities SUSTAINED STRENGTH OR ONE HIT WONDER? Non-U.S. equity investors patience was finally rewarded with a banner year in 2017, as both strong economic

Perspectives JAN 2018 2018 Market Preview: Non-U.S. Equities SUSTAINED STRENGTH OR ONE HIT WONDER? Non-U.S. equity investors patience was finally rewarded with a banner year in 2017, as both strong economic

Global Asset Allocation & Investment Strategy

Global Asset Allocation & Investment Strategy QUARTERLY INVESTMENT STRATEGY 5 GLOBAL ASSET ALLOCATION SUMMARY Global Asset Allocation* N + Equities Fixed Income Commodities Cash Notes: * 3-6 month horizon

Global Asset Allocation & Investment Strategy QUARTERLY INVESTMENT STRATEGY 5 GLOBAL ASSET ALLOCATION SUMMARY Global Asset Allocation* N + Equities Fixed Income Commodities Cash Notes: * 3-6 month horizon

Economic and Portfolio Outlook 4th Quarter 2014 (Released October 2014)

") Economic and Portfolio Outlook 4th Quarter 2014 (Released October 2014) Our economic outlook for the fourth quarter of 2014 for the U.S. is continued slow growth. We stated in our 3 rd quarter Economic

Economic and Portfolio Outlook 4th Quarter 2014 (Released October 2014) Our economic outlook for the fourth quarter of 2014 for the U.S. is continued slow growth. We stated in our 3 rd quarter Economic

Pioneer Compass A Quarterly Update on the Direction of the Markets

Pioneer Compass A Quarterly Update on the Direction of the Markets Q1 2016 / As of April 2016 The views expressed in this presentation are those of Pioneer, and are subject to change at any time. These

Pioneer Compass A Quarterly Update on the Direction of the Markets Q1 2016 / As of April 2016 The views expressed in this presentation are those of Pioneer, and are subject to change at any time. These

Material Sector. Krista Rye. Eric Rittenour

Material Sector Krista Rye Eric Rittenour 1 Overview Materials 2.91% S&P 500 BREAKDOWN Telecoms 2.80% Utilities 3.50% Consumer Dis. 12.53% Inf. Tech. 20.02% Consumer Sta. 10.40% Energy 7.29% Industrials

Material Sector Krista Rye Eric Rittenour 1 Overview Materials 2.91% S&P 500 BREAKDOWN Telecoms 2.80% Utilities 3.50% Consumer Dis. 12.53% Inf. Tech. 20.02% Consumer Sta. 10.40% Energy 7.29% Industrials

2008 Economic and Market Outlook

Economic and Market Outlook Presented by: Gareth Watson Warren Jestin Vincent Delisle December 7 Economic Outlook Warren Jestin The Global Economic Landscape is Changing Rapidly Gears Down Emerging Powerhouses

Economic and Market Outlook Presented by: Gareth Watson Warren Jestin Vincent Delisle December 7 Economic Outlook Warren Jestin The Global Economic Landscape is Changing Rapidly Gears Down Emerging Powerhouses

Global Macroeconomic Monthly Review

Global Macroeconomic Monthly Review August 14 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department 1 Please see disclaimer on the last page of this report Key Issues Global

Global Macroeconomic Monthly Review August 14 th, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department 1 Please see disclaimer on the last page of this report Key Issues Global

Fourth Quarter Market Outlook. Kim Huebner, CFA Don Powell, CFA Joseph Styrna, CFA

Fourth Quarter 2017 Market Outlook Kim Huebner, CFA Don Powell, CFA Joseph Styrna, CFA Economic Outlook Growth Increasing, Spending Modest, Low Unemployment 2017 2016 2015 2014 2013 2012 2011 GDP* Q3:

Fourth Quarter 2017 Market Outlook Kim Huebner, CFA Don Powell, CFA Joseph Styrna, CFA Economic Outlook Growth Increasing, Spending Modest, Low Unemployment 2017 2016 2015 2014 2013 2012 2011 GDP* Q3:

Gundlach: The Goldilocks Era is Over

Gundlach: The Goldilocks Era is Over December 6, 2017 by Robert Huebscher Easy monetary policies during the post-crisis period have propelled equity prices higher and driven bond yields lower. But as central

Gundlach: The Goldilocks Era is Over December 6, 2017 by Robert Huebscher Easy monetary policies during the post-crisis period have propelled equity prices higher and driven bond yields lower. But as central

The Weekly Market View June

Bond rout not over, equities relatively resilient The normalization of European bond yields is not over. Last week s rise in European bond yields again spilled over to US Treasuries and also determined

Bond rout not over, equities relatively resilient The normalization of European bond yields is not over. Last week s rise in European bond yields again spilled over to US Treasuries and also determined

Global Investment Outlook & Strategy

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy February 2017 Global Stock Market Rally likely to Continue with Solid Q4 Earnings & Stronger 2017 Earnings, ECB

PRUDENTIAL INTERNATIONAL INVESTMENTS ADVISERS, LLC. Global Investment Outlook & Strategy February 2017 Global Stock Market Rally likely to Continue with Solid Q4 Earnings & Stronger 2017 Earnings, ECB

Economic and Capital Market Update November 2017

Economic and Capital Market Update November 2017 Oct-69 Oct-73 Oct-77 Oct-81 Oct-85 Oct-89 Oct-93 Oct-97 Oct-01 Oct-05 Oct-09 Oct-13 Oct-17 November 30, 2017 Economic Perspective Economy Global economic

Economic and Capital Market Update November 2017 Oct-69 Oct-73 Oct-77 Oct-81 Oct-85 Oct-89 Oct-93 Oct-97 Oct-01 Oct-05 Oct-09 Oct-13 Oct-17 November 30, 2017 Economic Perspective Economy Global economic

Global Equites declined from Concern over Trade War

Quarterly Market Outlook: Quarter 2 2018 on 3 April 2018 Global Equites declined from Concern over Trade War Investment Outlook for 2 nd Quarter 2018 Equity Thailand U.S. Europe Japan Asia Bond Thailand

Quarterly Market Outlook: Quarter 2 2018 on 3 April 2018 Global Equites declined from Concern over Trade War Investment Outlook for 2 nd Quarter 2018 Equity Thailand U.S. Europe Japan Asia Bond Thailand

Morning Update. Market Highlights 10/11/2017. Daily Sentiment ** Investment Strategy Unit

Market Highlights Stocks Consolidate US equities finished the day lower, as market participants are concern over possible tax delays. The Dow Jones Index lost,4% to.46, the S&P 5 declined,8% to close at.584

Market Highlights Stocks Consolidate US equities finished the day lower, as market participants are concern over possible tax delays. The Dow Jones Index lost,4% to.46, the S&P 5 declined,8% to close at.584

FOREX WEEKLY. Weekly information issued by the FOREX Advisory Team. Trader view in 2 snapshots. 17 October Global Forex Sentiment

FOREX WEEKLY 17 October 2017 Weekly information issued by the FOREX Advisory Team Global Forex Sentiment The global economy appears remarkably resilient so far to negative (geo)political headlines, given

FOREX WEEKLY 17 October 2017 Weekly information issued by the FOREX Advisory Team Global Forex Sentiment The global economy appears remarkably resilient so far to negative (geo)political headlines, given

Capital Market Review

Capital Market Review September 3, 215 Percent Percent MARKET/ECONOMIC OVERVIEW Risk Reprices Rapidly 2,2 1,9 1,6 1,3 S&P 5 April 29, 211 to Oct 3, 211 157 Days -19.4% May 21, 215 to Sep 3, 215 132 Days

Capital Market Review September 3, 215 Percent Percent MARKET/ECONOMIC OVERVIEW Risk Reprices Rapidly 2,2 1,9 1,6 1,3 S&P 5 April 29, 211 to Oct 3, 211 157 Days -19.4% May 21, 215 to Sep 3, 215 132 Days

Quarterly Economic and Market Update

Quarterly Economic and Market Update September 2017 Presented by Global Manager Research Table of Contents Past performance shown on the following slides does not guarantee future results. Market Returns..

Quarterly Economic and Market Update September 2017 Presented by Global Manager Research Table of Contents Past performance shown on the following slides does not guarantee future results. Market Returns..

INVESTMENT REVIEW Q2 2018

INVESTMENT REVIEW Q2 2018 OVERVIEW Surveys and hard data show the global economy growing at a healthy pace with minimal inflation risk. Activity accelerated in Q2 and our expectation of 3.4% GDP growth

INVESTMENT REVIEW Q2 2018 OVERVIEW Surveys and hard data show the global economy growing at a healthy pace with minimal inflation risk. Activity accelerated in Q2 and our expectation of 3.4% GDP growth

Fed described the economy as "slow" and said employers remained reluctant to create jobs and Inflation "somewhat low.

08 Nov 2010 UNITED STATES The ISM manufacturing index rose to 56.9 in October from 54.4 in September, led by growth in autos, computers and exported goods. The ISM non-manufacturing index rose to 54.3

08 Nov 2010 UNITED STATES The ISM manufacturing index rose to 56.9 in October from 54.4 in September, led by growth in autos, computers and exported goods. The ISM non-manufacturing index rose to 54.3

Economic and market snapshot for January 2016

From left to right: Herman van Papendorp (Head of Macro Research and Asset Allocation), Sanisha Packirisamy (Economist) Economic and market snapshot for January 2016 Global economic developments United

From left to right: Herman van Papendorp (Head of Macro Research and Asset Allocation), Sanisha Packirisamy (Economist) Economic and market snapshot for January 2016 Global economic developments United

Emerging Markets Debt: Outlook for the Asset Class

Emerging Markets Debt: Outlook for the Asset Class By Steffen Reichold Emerging Markets Economist May 2, 211 Emerging market debt has been one of the best performing asset classes in recent years due to

Emerging Markets Debt: Outlook for the Asset Class By Steffen Reichold Emerging Markets Economist May 2, 211 Emerging market debt has been one of the best performing asset classes in recent years due to

APPENDIX ECONOMIC INDICATORS DEVELOPED ECONOMIES

16 QUARTERLY INVESTMENT STRATEGY APPENDIX ECONOMIC INDICATORS DEVELOPED ECONOMIES Purchasing Managers Index EMERGING ECONOMIES Purchasing Managers Index US Eurozone Japan Brazil Russia India China Industrial

16 QUARTERLY INVESTMENT STRATEGY APPENDIX ECONOMIC INDICATORS DEVELOPED ECONOMIES Purchasing Managers Index EMERGING ECONOMIES Purchasing Managers Index US Eurozone Japan Brazil Russia India China Industrial

Economic Indicators. Roland Berger Institute

Economic Indicators Roland Berger Institute October 2017 Overview Key points Economic Indicators A publication, compiled by the Roland Berger Institute, that provides you with the most important macroeconomic

Economic Indicators Roland Berger Institute October 2017 Overview Key points Economic Indicators A publication, compiled by the Roland Berger Institute, that provides you with the most important macroeconomic

Marquette Associates Market Environment

M Marquette Associates Market Environment April 2010 U.S. Economy Fixed Income Markets U.S. Equity Markets International Equity Markets Hedge Fund Markets Real Estate Markets Private Equity and Hedge Fund

M Marquette Associates Market Environment April 2010 U.S. Economy Fixed Income Markets U.S. Equity Markets International Equity Markets Hedge Fund Markets Real Estate Markets Private Equity and Hedge Fund

Investment Policy March 2019

Investment Policy March 2019 Our market view in a nutshell March 2019 China assertiveness and the Fed s sharp U-turn continue providing support to risk assets. In addition, the progress made towards reaching

Investment Policy March 2019 Our market view in a nutshell March 2019 China assertiveness and the Fed s sharp U-turn continue providing support to risk assets. In addition, the progress made towards reaching

Fixed income market dislocations. Benoît Hubaud Global Head of Fixed Income Research

Fixed income market dislocations Benoît Hubaud Global Head of Fixed Income Research Dislocation: one word, two definitions An extreme movement which can be absolute or relative EuroStoxx 5 up +15% Five

Fixed income market dislocations Benoît Hubaud Global Head of Fixed Income Research Dislocation: one word, two definitions An extreme movement which can be absolute or relative EuroStoxx 5 up +15% Five

Investing in a Time of (Financial) Repression. Cyril Moullé-Berteaux, Head of Global Asset Allocation

Repression. Cyril Moullé-Berteaux, Head of Global Asset Allocation") Investing in a Time of (Financial) Repression Cyril Moullé-Berteaux, Head of Global Asset Allocation Overview Positioning for the long-term The growing Yield Bubble Europe outperformance may just be starting

Investing in a Time of (Financial) Repression Cyril Moullé-Berteaux, Head of Global Asset Allocation Overview Positioning for the long-term The growing Yield Bubble Europe outperformance may just be starting

Raymond James & Associates, Inc., member New York Stock Exchange/SIPC

Kevin W. Byrne, CTFA, CIMA Senior Vice President, Investments Kevin.Byrne@RaymondJames.com October 20 th, 2016 BCM Q3-2016 Market and Economic Review Economic Review: GDP: Real GDP increased at an annual

Kevin W. Byrne, CTFA, CIMA Senior Vice President, Investments Kevin.Byrne@RaymondJames.com October 20 th, 2016 BCM Q3-2016 Market and Economic Review Economic Review: GDP: Real GDP increased at an annual

Asset allocation achieving the right mix

Asset allocation achieving the right mix Learning outcomes The objective of the presentation is to help develop your understanding of: The benefits and drawbacks of a range of asset allocation styles The

Asset allocation achieving the right mix Learning outcomes The objective of the presentation is to help develop your understanding of: The benefits and drawbacks of a range of asset allocation styles The

Asset Strategy Consultants. MARKET ENVIRONMENT Second Quarter 2016

MARKET ENVIRONMENT Second Quarter 2016 Market Environment: U.S. Economy The 2nd quarter was reasonably uneventful and markets were relatively placid until June 23rd, when British voters narrowly approved

MARKET ENVIRONMENT Second Quarter 2016 Market Environment: U.S. Economy The 2nd quarter was reasonably uneventful and markets were relatively placid until June 23rd, when British voters narrowly approved

Navigating a maturing bull market

Navigating a maturing bull market Asia Pacific Wealth Management March 2018 INVESTMENT PRODUCTS: NOT A BANK DEPOSIT. NOT GOVERNMENT INSURED. NO BANK GUARANTEE. MAY LOSE VALUE Market Review Market Performance

Navigating a maturing bull market Asia Pacific Wealth Management March 2018 INVESTMENT PRODUCTS: NOT A BANK DEPOSIT. NOT GOVERNMENT INSURED. NO BANK GUARANTEE. MAY LOSE VALUE Market Review Market Performance

MARKET REPORT THE MONTHLY A SNAPSHOT OF THE KEY POINTS FOR AUGUST. Bonds continue to Rally. ISSUE 8 August 2014

ISSUE 8 August 2014 THE MONTHLY MARKET REPORT A SNAPSHOT OF THE KEY POINTS FOR AUGUST The RBA held the overnight cash rate steady at 2.50% for the 12th consecutive Month in August. Short term fixed income

ISSUE 8 August 2014 THE MONTHLY MARKET REPORT A SNAPSHOT OF THE KEY POINTS FOR AUGUST The RBA held the overnight cash rate steady at 2.50% for the 12th consecutive Month in August. Short term fixed income

Market Update: Broad Market Returns and Indicators

Market Update Eckler Ltd. collects information directly from sources believed to be reliable. Eckler Ltd. does not guarantee or warrant the accuracy, timeliness, or completeness of the information either

Market Update Eckler Ltd. collects information directly from sources believed to be reliable. Eckler Ltd. does not guarantee or warrant the accuracy, timeliness, or completeness of the information either

Capital Markets Outlook 100 LOWDER BROOK DRIVE SUITE 1100 WESTWOOD MA FAX

M E K E T A I N V E S T M E N T G R O U P 00 LOWDER BROOK DRIVE SUITE 00 WESTWOOD MA 02090 78 47 3500 FAX 78 47 34 Investors are faced with three primary issues in the near-term: ) historically low bond

M E K E T A I N V E S T M E N T G R O U P 00 LOWDER BROOK DRIVE SUITE 00 WESTWOOD MA 02090 78 47 3500 FAX 78 47 34 Investors are faced with three primary issues in the near-term: ) historically low bond

J UNE 7, INDEX LAST CHANGE % CHANGE ASIA/PACIFC. Nikkei , % Hang Seng 31, %

The dollar weakened this morning against most of its major peers on G-7 summit speculation and the euro has extended its recent monetary policy backed rally. European and Asian shares advanced and U.S.

The dollar weakened this morning against most of its major peers on G-7 summit speculation and the euro has extended its recent monetary policy backed rally. European and Asian shares advanced and U.S.

PRIVATE BANKING PRIVATE BANKING

US (UNDERWEIGHT) Valuations remain high Downward revision to earnings forecasts persists Monetary policy realtively less supportive Recent rally relative to other markets looks March 211rebased 2 1 overstretched

US (UNDERWEIGHT) Valuations remain high Downward revision to earnings forecasts persists Monetary policy realtively less supportive Recent rally relative to other markets looks March 211rebased 2 1 overstretched

The State of Global Foreign Exchange Markets

The State of Global Foreign Exchange Markets Nick Bennenbroek The State Of Global FX Markets Nick Bennenbroek Head of Currency Strategy June 2015 Please see the disclosure appendix of this publication

The State of Global Foreign Exchange Markets Nick Bennenbroek The State Of Global FX Markets Nick Bennenbroek Head of Currency Strategy June 2015 Please see the disclosure appendix of this publication

MONTHLY MARKET REVIEW April 2018

MONTHLY MARKET REVIEW April 218 www.primebuchholz.com 63.433.1143 The decline in risk assets subsided in April and U.S. equity market volatility fell from elevated levels exhibited in recent months. Earnings

MONTHLY MARKET REVIEW April 218 www.primebuchholz.com 63.433.1143 The decline in risk assets subsided in April and U.S. equity market volatility fell from elevated levels exhibited in recent months. Earnings

Leumi. Global Economics Monthly Review. Arie Tal, Research Economist. July 12, Capital Markets Division, Economics Department. leumiusa.

Global Economics Monthly Review July 12, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report

Global Economics Monthly Review July 12, 2018 Arie Tal, Research Economist Capital Markets Division, Economics Department Leumi leumiusa.com Please see important disclaimer on the last page of this report

Citigold. Citigold. FINANCIAL MARKET ANALYSIS 21 March Fed remained on hold, scaled back hike forecast. Performance.

Citigold FINANCIAL MARKET ANALYSIS 21 March 2016 Fed remained on hold, scaled back hike forecast As widely expected, the Fed kept its policy stance unchanged at a targeted range of 0.25%-0.50% for the

Citigold FINANCIAL MARKET ANALYSIS 21 March 2016 Fed remained on hold, scaled back hike forecast As widely expected, the Fed kept its policy stance unchanged at a targeted range of 0.25%-0.50% for the

Expect Global Momentum in 2018

YEAR IN REVIEW 2018 OUTLOOK Expect Global Momentum in 2018 Alain Bergeron, Head of Mackenzie Asset Allocation Team Todd Mattina, Chief Economist and Strategist on the Mackenzie Asset Allocation Team Despite

YEAR IN REVIEW 2018 OUTLOOK Expect Global Momentum in 2018 Alain Bergeron, Head of Mackenzie Asset Allocation Team Todd Mattina, Chief Economist and Strategist on the Mackenzie Asset Allocation Team Despite