Agenda. Learning Objectives. Chapter 19. International Business Finance. Learning Objectives Principles Used in This Chapter

|

|

|

- Sharon Rosa Chapman

- 6 years ago

- Views:

Transcription

1 Chapter 19 International Business Finance Agenda Learning Objectives Principles Used in This Chapter 1. Foreign Exchange Markets and Currency Exchange Rates 2. Interest Rate and Purchasing-Power Parity 3. Capital Budgeting for Direct Foreign Investment Learning Objectives 1. Understand the nature and importance of the foreign exchange market and learn to read currency exchange rate quotes. 2. Describe interest rate and the purchasing power parity. 3. Discuss the risks that are unique to the capital budgeting analysis of direct foreign investments. 1

2 Principles Used in This Chapter Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value Foreign Exchange Markets and Currency Exchange Rates Foreign Exchange Markets and Currency Exchange Rates The foreign exchange (FX) market: Largest financial market with daily trading volumes of more than $4 trillion. Organized as over-the-counter market with participants located in major commercial and investment banks around the world. Trading dominated by few currencies including U.S. dollar, the British pound sterling, the Japanese Yen, and the Euro. 2

3 Foreign Exchange Markets and the Currency Exchange Rates Major participants in foreign exchange trading include the following: Importers and exporters of goods and services, Investors and portfolio managers who purchase foreign stocks and bonds, and Currency traders who make a market in one or more foreign currencies. 3

4 Foreign Exchange Rates An exchange rate is simply the price of one currency stated in terms of another. For example, if the exchange rate of U.S. dollar for Euro was $1.35 to 1, it means that it would take $1.35 to purchase one Euro. Foreign Exchange Rates Direct quote It indicates the number of units of U.S. dollar to buy 1 foreign currency unit. In the table we see that it took $0.97 to buy 1 Canadian dollar. Indirect Quote It indicates the number of foreign currency units to buy one American dollar. For example, in the table it shows that it will take Chinese yuan to buy 1 U.S. dollar 4

5 Foreign Exchange Rates We can compute the direct quote from the indirect quote. Foreign Exchange Rates The direct quote for Canadian dollars is $0.97. The related indirect quote will be: Indirect quote = 1 $0.97 = $1.03 Checkpoint 19.1 Exchanging Currencies U.S. firm Claremont Steel ordered parts for a generator that were made by a German firm. Claremont was required to pay 1,000 euros to the German firm on January 8, How many dollars were required for this transaction? 5

6 Checkpoint 19.1 Checkpoint 19.1 Checkpoint 19.1: Check Yourself Suppose an American firm had to pay $2,000 to a British resident on January 8, How many pounds did the British resident receive? 6

7 Step 1: Picture the Problem The key determinant of the number of British pounds received by the British resident is the exchange rate between dollars and pounds. The chart (next slide) shows that the amount received in Pounds varies depending on the exchange rate. Thus if the exchange rate is 1$=.8, the British resident will receive only 1,600. Step 2: Decide on a Solution Strategy To determine the number of British pounds that will be received by the British resident for $2,000 we need to know the number of pounds it takes to buy one dollar i.e. indirect exchange rate quote. Step 3: Solve Number of British Pounds received = ( /$ $) $2,000 = Indirect quote $2,000 = /$ $2, /$ $2,000 = 1,

8 Step 4: Analyze The British resident will receive 1, using the indirect quote. Had we used the direct quote ($/ ), we would have arrived at the wrong answer of 3, ( ). The units would be ($/ )$ =??? Exchange Rates and Arbitrage Arbitrage is the process of buying and selling in more than one market to make a riskless profit. Simple arbitrage eliminates exchange rate differentials across the markets for a single currency. Exchange Rates and Arbitrage The asked rate (also known as the selling rate or the offer rate) is the rate the bank or the foreign exchange trader asks the customer to pay in home currency for foreign currency when the bank is selling and the customer is buying. Table 19-1 contains the asked rate quotes. The bid rate (also known as the buying rate) is the rate at which the bank buys the foreign currency from the customer by paying in home currency. 8

9 Exchange Rates and Arbitrage The bank sells a unit of foreign currency for more than it pays for it. The difference between the asked quote and the bid quote is known as the bid-asked spread. The spread will be relatively l lower for popular currencies that are frequently traded. Cross Rates A cross rate is the computation of an exchange rate for a currency from the exchanges rates of two other currencies. The $/ rate is =( / )x( /$) = x (1/0.6936) 9

10 Types of Foreign Exchange Transactions Spot exchange rate is the rate for immediate delivery. Forward exchange rate is an exchange rate agreed upon today but which calls for delivery or payment at a future date. Spot and forward rate quotes are given in Table Types of Foreign Exchange Transactions The forward rate is often quoted at a premium to or a discount from the existing spot rate. For example, the 30-day Switzerland franc will be quoted as premium( ). This premium or discount is known as the forward-spot differential. Types of Foreign Exchange Transactions The forward-spot differential can be expressed as: Where F= the forward rate, direct quote S = the spot rate, direct quote 10

11 Types of Foreign Exchange Transactions The premium or discount can also be expressed as an annual percentage rate, computed as follows: Checkpoint 19.2 Determining the Percent-per-Annum Premium or Discount You are in need of yen in six months, but before entering a forward contract to buy them, you would like to know their premium or discount from the existing spot rate. Calculate the premium or discount from the existing spot rate for the 6-month yen as of January 8, 2010 using the data given in Table Checkpoint

12 Checkpoint Interest Rate and Purchasing Power Parity Interest Rate Parity Interest rate parity is a theory that can be used to relate differences in the interest rates in two countries to the ratios of spot and forward exchange rates of the two countries currencies. Specifically, Differences in interest rates = Ratio of the forward and spot rates 12

13 Interest Rate Parity Interest Rate Parity Interest rate parity means that you get the same total return for the following two options: Invest directly in the US; or Convert dollars to Japanese Yens, Invest Yens in the risk-free rate in Japan, and Convert Yens back to U.S. dollars. Interest Rate Parity Example 19.1 You have $1,000,000 to invest and you observe the following quotes in the market: 1$ = day forward rate = U.S. 180-day risk-free interest rate = 4.4% Japan 180-day risk-free interest rate = 2% Determine whether interest rate parity holds. 13

14 Interest Rate Parity Option I: Invest directly in USA and earn 4.4% 1,000,000 * = $1,044,000 Option II: (a) Convert to Yen at spot rate = 106,000,000 (b) Invest at 2% = 106,000(1.02) = 108,120,000 (c) Convert to $ at the forward rate = 108,120, = $1,044,638 ==> Difference of $638 ==> Interest Rate Parity does not hold Purchasing Power Parity and the Law of One Price According to the theory of purchasing power parity (PPP), exchange rates adjust so that identical goods cost the same amount regardless of where in the world they are purchased. Purchasing Power Parity and the Law of One Price Underling PPP theory is the law of one price, which states that the same good should sell for the same price in different countries after making adjustments for the exchange rate between the two currencies. Figure 19-2 illustrates one example of exception to the PPP theory. 14

15 Purchasing Power Parity and the Law of One Price The differences in prices around the world could be explained by: Tax differences among countries Differences in labor costs Differences in raw material costs Differences in rental costs Purchasing Power Parity and the Law of One Price In general, we expect PPP to hold for goods that can be cheaply shipped between countries (for example, expensive gold jewelry). PPP does not seem to hold for non traded goods like PPP does not seem to hold for non-traded goods like restaurant meals and haircuts. 15

16 The International Fisher Effect The International Fisher Effect (IFE) assumes that real rates of return are the same across the world, so that the differences in nominal returns around the world arise because of differences in inflation rates. Like purchasing power parity, IFE is just an approximation that may not hold exactly. The International Fisher Effect Example 19.2 Assume that the real rate of interest is equal to 2% in all countries. What will be the nominal interest rate in UK and USA, if UK is expecting an inflation rate of 6% and USA is expecting an inflation rate of 3%. The International Fisher Effect Interest rate (USA) = [.03.02] =.0506 or 5.06% Interest rate (UK) = [.06.02] =.0812 or 8.12% 16

17 The International Fisher Effect IFE cautions us that we should not invest in a country just because it offers the highest interest rates. IFE notes that such high interest rate is an indication of high inflation. Accordingly, any gain in interest rates will be offset by losses due to foreign currency depreciation. 17

18 19.3 Capital Budgeting for Direct Foreign Investment Capital Budgeting for Direct Foreign Investment Direct foreign investment occurs when a company from one country makes a physical investment into building a factory in another country. A multinational corporation (MNC) is one that has control over this investment. 18

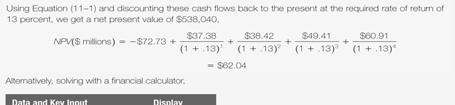

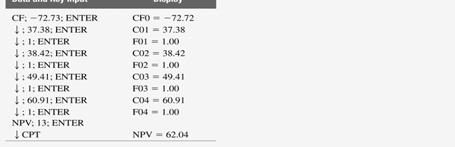

19 Capital Budgeting for Direct Foreign Investment A major reason for direct foreign investment by U.S. companies is the prospect of higher rates of return from these investments. The method used to evaluate foreign investments is very similar to the method used to evaluate capital budgeting decisions in a domestic context. Checkpoint 19.3 International Capital Budgeting You are working for an American firm that is looking at a new project that will produce the following cash flows, which are expected to be repatriated to the parent company and are measured in South African Rand (SAR), In addition, the risk-free rate in the United States is 4 percent and this project is riskier than most; as such, the firm has determined that it should require a 9 percent premium over the risk-free rate. Thus, the appropriate discount rate for this project is 13 percent. In addition, let s assume the current spot exchange rate is.11sar/$, and the 1-year forward exchange rate is.107sar/$. Calculate the expected cash flows for this project in U.S. dollars, and then use these cash flows to calculate the project s NPV. Checkpoint

20 Checkpoint 19.3 Checkpoint 19.3 Checkpoint

21 Checkpoint 19.3: Check Yourself The Problem An American firm is looking for a new project that will produce the following cash flows which are expected to be repatriated to the parent company and are measured in South African Rand (SAR). Year Cash flow (in millions of SAR) The Problem In addition, the risk-free rate in the United States is 4 percent, and this project is riskier than most, and as such, the firm has determined that it should require a 10 percent premium over the risk-free rate. Thus, the appropriate discount rate for this project is 14 percent. In addition, the current spot exchange rate is.11 SAR/$, and the 1-year forward exchange rate is.107sar/$. What is the project s NPV? Step 1: Picture the Problem Time i=14% Cash flow (millions, SAR) The timeline illustrates the following: The discount rate is 14%. A cash outflow of -20 million SAR occurs at the beginning of the first year (at time 0), followed by positive cash inflows during the next four years. 21

22 Step 2: Decide on a Solution Strategy To calculate the project s NPV, we need to convert South African Rand into U.S. dollars. However, we only have 1-year forward rates. We can use equation 19-5 and the given forward rate and spot rate to determine the interest rate differential in the two countries. Step 2: Decide on a Solution Strategy 1 year forward rate = (interest rate differential) 1 (spot exchange rate) We can then use the forward rate to convert the cash flows measured in SARs into U.S. dollars. Once we have the cash flows, we can compute the NPV using a 14% discount rate. Step 3: Solve Interest rate differential = Forward rate/spot rate =.107/.11 = We can use the interest rate differential to calculate the forward exchange rate and then convert the SAR denominated cash flows into U.S. dollars. 22

23 Step 3: Solve Year Spot Rate (Interest Rate Differential) n Forward rate for year n SAR/$ x SAR/$ SAR/$ x (0.9727) SAR/$ SAR/$ x (0.9727) SAR/$ SAR/$ x (0.9727) SAR/$ Step 3: Solve Solve using an Excel Spreadsheet Cash flow Implied Cash flow (in millions Forward (in millions Year of SAR) Rate of $) NVP $0.299 NPV = npv (0.14; 1.07,1.041,0.6072,0.591) = $0.299 million or $299,000 Input in Excel Step 3: Solve Computing NPV using equation NPV = -$2.2m + $1.07m/(1.14) + $1.041m/(1.14) 2 + $0.6072m/(1.14) 3 + $0.591m/(1.14) 4 = $0.299 million or $299,000 23

24 Step 4: Analyze Note, the only relevant cash flows are those that are expected to be repatriated back to the home country and the initial cash outflow. Also, discount rate should be in the same currency that the cash flows are measured in. Here discount rate was in U.S. dollars, so we converted the SAR cash flows into U.S. dollars. Foreign Investment Risks Risks in domestic capital budgeting arises from two sources: Business risk related to the specific product or service and the uncertainty associated with that market. Financial risk is the risk imposed on the investment as a result of how the project is financed. Foreign Investment Risks Foreign direct investment includes both business and financial risk, plus political risk and exchange rate risk. 24

25 Foreign Investment Risks Political risk can arise if the business is conducted in a country that is not politically stable leading to changes in policies with respect to businesses. Foreign Investment Risks Some examples of political risk are as follows: Expropriation of plants and equipment without compensation. Non-convertibility of the subsidiary s foreign earnings into the parent s currency. Substantial changes in tax rates. Requirements regarding the local ownership of business. Foreign Investment Risks Exchange rate risk is the risk that the value of the firm s operations and investments will be adversely affected by changes in exchange rates. For example, if the Japanese Yen depreciates, it will translate to fewer dollars when it is sent back to the U.S. 25

Week-7. Dr. Ahmed. Domestic Firms International Firms Multinational Firms Global Firms

FINC 5880 Dr. Ahmed Week-7 Name Domestic Firms International Firms Multinational Firms Global Firms Factors that make multinational financial management different Exchange rates and trading International

FINC 5880 Dr. Ahmed Week-7 Name Domestic Firms International Firms Multinational Firms Global Firms Factors that make multinational financial management different Exchange rates and trading International

MCQ on International Finance

MCQ on International Finance 1. If portable disk players made in China are imported into the United States, the Chinese manufacturer is paid with a) international monetary credits. b) dollars. c) yuan,

MCQ on International Finance 1. If portable disk players made in China are imported into the United States, the Chinese manufacturer is paid with a) international monetary credits. b) dollars. c) yuan,

Chapter 5. Learning Objectives. Principals Applied in this Chapter. Time Value of Money. Principle 1: Money Has a Time Value.

Chapter 5 Time Value of Money Learning Objectives 1. Construct cash flow timelines to organize your analysis of problems involving the time value of money. 2. Understand compounding and calculate the future

Chapter 5 Time Value of Money Learning Objectives 1. Construct cash flow timelines to organize your analysis of problems involving the time value of money. 2. Understand compounding and calculate the future

Chapter 5. Time Value of Money

Chapter 5 Time Value of Money Using Timelines to Visualize Cashflows A timeline identifies the timing and amount of a stream of payments both cash received and cash spent - along with the interest rate

Chapter 5 Time Value of Money Using Timelines to Visualize Cashflows A timeline identifies the timing and amount of a stream of payments both cash received and cash spent - along with the interest rate

Foreign Exchange Markets: Key Institutional Features (cont)

") Foreign Exchange Markets FOREIGN EXCHANGE MARKETS Professor Anant Sundaram AGENDA Basic characteristics of FX markets: Institutional features Spot markets Forward markets Appreciation, depreciation, premium,

Foreign Exchange Markets FOREIGN EXCHANGE MARKETS Professor Anant Sundaram AGENDA Basic characteristics of FX markets: Institutional features Spot markets Forward markets Appreciation, depreciation, premium,

2. Discuss the implications of the interest rate parity for the exchange rate determination.

CHAPTER 5 INTERNATIONAL PARITY RELATIONSHIPS AND FORECASTING FOREIGN EXCHANGE RELATIONSHIPS SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. Give a full definition

CHAPTER 5 INTERNATIONAL PARITY RELATIONSHIPS AND FORECASTING FOREIGN EXCHANGE RELATIONSHIPS SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. Give a full definition

Chapter 15. The Foreign Exchange Market. Chapter Preview

Chapter 15 The Foreign Exchange Market Chapter Preview In the mid-1980s, American businesses became less competitive relative to their foreign counterparts. By the 2000s, though, competitiveness increased.

Chapter 15 The Foreign Exchange Market Chapter Preview In the mid-1980s, American businesses became less competitive relative to their foreign counterparts. By the 2000s, though, competitiveness increased.

CHAPTER 8 MANAGEMENT OF TRANSACTION EXPOSURE ANSWERS & SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS

CHAPTER 8 MANAGEMENT OF TRANSACTION EXPOSURE ANSWERS & SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. How would you define transaction exposure? How is it different from economic exposure?

CHAPTER 8 MANAGEMENT OF TRANSACTION EXPOSURE ANSWERS & SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. How would you define transaction exposure? How is it different from economic exposure?

In this Session, you will explore international financial markets. You will also: Learn about the international bond, international equity, and

1 In this Session, you will explore international financial markets. You will also: Learn about the international bond, international equity, and Eurocurrency markets. Understand the primary functions

1 In this Session, you will explore international financial markets. You will also: Learn about the international bond, international equity, and Eurocurrency markets. Understand the primary functions

Operating Exposure. Operating & Financing Cash Flows. Expected Versus Unexpected Changes in Cash Flows. Operating & Financing Cash Flows

Chapter 9 Prepared by Shafiq Jadallah To Accompany Fundamentals of Multinational Finance Michael H. Moffett, Arthur I. Stonehill, David K. Eiteman Copyright 2003 Pearson Education, Inc. Slide 9-1 Chapter

Chapter 9 Prepared by Shafiq Jadallah To Accompany Fundamentals of Multinational Finance Michael H. Moffett, Arthur I. Stonehill, David K. Eiteman Copyright 2003 Pearson Education, Inc. Slide 9-1 Chapter

Replies to one minute memos, 9/21/03

Replies to one minute memos, 9/21/03 Dear Students, Thank you for asking these great questions. The answer to my question (what is the difference b/n the covered & uncovered interest rate arbitrage? If

Replies to one minute memos, 9/21/03 Dear Students, Thank you for asking these great questions. The answer to my question (what is the difference b/n the covered & uncovered interest rate arbitrage? If

BBM2153 Financial Markets and Institutions Prepared by Dr Khairul Anuar

BBM2153 Financial Markets and Institutions Prepared by Dr Khairul Anuar L8: The Foreign Exchange Market www. notes638.wordpress.com Copyright 2015 Pearson Education, Ltd. All rights reserved. 8-1 Chapter

BBM2153 Financial Markets and Institutions Prepared by Dr Khairul Anuar L8: The Foreign Exchange Market www. notes638.wordpress.com Copyright 2015 Pearson Education, Ltd. All rights reserved. 8-1 Chapter

Study Questions (with Answers) Lecture 13. Exchange Rates

Lecture 13. Exchange Rates") Study Questions (with Answers) Page 1 of 5 Part 1: Multiple Choice Select the best answer of those given. Study Questions (with Answers) Lecture 13 1. The statement the yen rose today from 121 to 117 makes

Study Questions (with Answers) Page 1 of 5 Part 1: Multiple Choice Select the best answer of those given. Study Questions (with Answers) Lecture 13 1. The statement the yen rose today from 121 to 117 makes

CHAPTER 31 INTERNATIONAL CORPORATE FINANCE

Corporate Finance 11 th edition Solutions Manual Ross, Westerfield, Jaffe, and Jordan Completed download Solutions Manual, Answers, Instructors Resource Manual, Case Solutions, Excel Solutions are included:

Corporate Finance 11 th edition Solutions Manual Ross, Westerfield, Jaffe, and Jordan Completed download Solutions Manual, Answers, Instructors Resource Manual, Case Solutions, Excel Solutions are included:

Introduction to Exchange Rates and the Foreign Exchange Market

Introduction to Exchange Rates and the Foreign Exchange Market 2 1. Refer to the exchange rates given in the following table. Today One Year Ago June 25, 2010 June 25, 2009 Country Per $ Per Per Per $

Introduction to Exchange Rates and the Foreign Exchange Market 2 1. Refer to the exchange rates given in the following table. Today One Year Ago June 25, 2010 June 25, 2009 Country Per $ Per Per Per $

Less Reliable International Parity Conditions

The International Parity Conditions The Law of One Price Interest Rate Parity Less Reliable International Parity Conditions The Real Exchange Rate 1 The International Parity Conditions Though this be madness,

The International Parity Conditions The Law of One Price Interest Rate Parity Less Reliable International Parity Conditions The Real Exchange Rate 1 The International Parity Conditions Though this be madness,

CAPITAL MARKET DEVELOPMENTS ABROAD. I. Ten"Charts on Financial Markets Abroad. II. Latest Figures Plotted in H.13 Chart Series, 1967

PEDEHALHESEItVESYSTEM H. 13 September 20, 1967. No.317 CAPITAL MARKET DEVELOPMENTS ABROAD I. Ten Charts on Financial Markets Abroad II. Latest Figures Plotted in H.13 Chart Series, 1967 I. Ten"Charts on

PEDEHALHESEItVESYSTEM H. 13 September 20, 1967. No.317 CAPITAL MARKET DEVELOPMENTS ABROAD I. Ten Charts on Financial Markets Abroad II. Latest Figures Plotted in H.13 Chart Series, 1967 I. Ten"Charts on

Study Questions. Lecture 13. Exchange Rates

Study Questions Page 1 of 5 Study Questions Lecture 13 Part 1: Multiple Choice Select the best answer of those given. 1. The statement the yen rose today from 121 to 117 makes sense because a. The U.S.

Study Questions Page 1 of 5 Study Questions Lecture 13 Part 1: Multiple Choice Select the best answer of those given. 1. The statement the yen rose today from 121 to 117 makes sense because a. The U.S.

Arbitrage is a trading strategy that exploits any profit opportunities arising from price differences.

5. ARBITRAGE AND SPOT EXCHANGE RATES 5 Arbitrage and Spot Exchange Rates Arbitrage is a trading strategy that exploits any profit opportunities arising from price differences. Arbitrage is the most basic

5. ARBITRAGE AND SPOT EXCHANGE RATES 5 Arbitrage and Spot Exchange Rates Arbitrage is a trading strategy that exploits any profit opportunities arising from price differences. Arbitrage is the most basic

Chapter 10. The Foreign Exchange Market

Chapter 10 The Foreign Exchange Market Why Is The Foreign Exchange Market Important? The foreign exchange market 1. is used to convert the currency of one country into the currency of another 2. provides

Chapter 10 The Foreign Exchange Market Why Is The Foreign Exchange Market Important? The foreign exchange market 1. is used to convert the currency of one country into the currency of another 2. provides

Lecture 2. Agenda: Basic descriptions for derivatives. 1. Standard derivatives Forward Futures Options

Lecture 2 Basic descriptions for derivatives Agenda: 1. Standard derivatives Forward Futures Options 2. Nonstandard derivatives ICON Range forward contract 1. Standard derivatives ~ Forward contracts:

Lecture 2 Basic descriptions for derivatives Agenda: 1. Standard derivatives Forward Futures Options 2. Nonstandard derivatives ICON Range forward contract 1. Standard derivatives ~ Forward contracts:

Chapter 19: What Determines Exchange Rates?

Chapter 19: What Determines Exchange Rates? Introduction Exchange rates over time Long-term trends Medium-term trends Short-term variability Frameworks Asset market approach Purchasing power parity (PPP)

Chapter 19: What Determines Exchange Rates? Introduction Exchange rates over time Long-term trends Medium-term trends Short-term variability Frameworks Asset market approach Purchasing power parity (PPP)

Chapter 17 Appendix A

Chapter 17 Appendix A The Interest Parity Condition We can derive all the results in the text with a concept that is widely used in international finance. The interest parity condition shows the relationship

Chapter 17 Appendix A The Interest Parity Condition We can derive all the results in the text with a concept that is widely used in international finance. The interest parity condition shows the relationship

MBF1223 Financial Management Prepared by Dr Khairul Anuar

MBF1223 Financial Management Prepared by Dr Khairul Anuar L11 - International Financial Management www.mba638.wordpress.com Learning Objectives Understand cultural, business, and political differences

MBF1223 Financial Management Prepared by Dr Khairul Anuar L11 - International Financial Management www.mba638.wordpress.com Learning Objectives Understand cultural, business, and political differences

INTERNATIONAL FINANCE MBA 926

INTERNATIONAL FINANCE MBA 926 1. Give a full definition of the market for foreign exchange. Answer: Broadly defined, the foreign exchange (FX) market encompasses the conversion of purchasing power from

INTERNATIONAL FINANCE MBA 926 1. Give a full definition of the market for foreign exchange. Answer: Broadly defined, the foreign exchange (FX) market encompasses the conversion of purchasing power from

International Finance multiple-choice questions

International Finance multiple-choice questions 1. Spears Co. will receive SF1,000,000 in 30 days. Use the following information to determine the total dollar amount received (after accounting for the

International Finance multiple-choice questions 1. Spears Co. will receive SF1,000,000 in 30 days. Use the following information to determine the total dollar amount received (after accounting for the

FOREIGN EXCHANGE MARKET. Luigi Vena 05/08/2015 Liuc Carlo Cattaneo

FOREIGN EXCHANGE MARKET Luigi Vena 05/08/2015 Liuc Carlo Cattaneo TABLE OF CONTENTS The FX market Exchange rates Exchange rates regimes Financial balances International Financial Markets 05/08/2015 Coopeland

FOREIGN EXCHANGE MARKET Luigi Vena 05/08/2015 Liuc Carlo Cattaneo TABLE OF CONTENTS The FX market Exchange rates Exchange rates regimes Financial balances International Financial Markets 05/08/2015 Coopeland

Use the following to answer questions 19-20: Scenario: Exchange Rates The value of a euro goes from US$1.25 to US$1.50.

Name: Date: 1. Open-economy macroeconomics is the branch of economics that deals with: A) reducing regulations on business. B) the relationships between economies of different nations. C) reducing employment

Name: Date: 1. Open-economy macroeconomics is the branch of economics that deals with: A) reducing regulations on business. B) the relationships between economies of different nations. C) reducing employment

BBK3273 International Finance

BBK3273 International Finance Prepared by Dr Khairul Anuar L1: Foreign Exchange Market www.lecturenotes638.wordpress.com Contents 1. Foreign Exchange Market 2. History of Foreign Exchange 3. Size of the

BBK3273 International Finance Prepared by Dr Khairul Anuar L1: Foreign Exchange Market www.lecturenotes638.wordpress.com Contents 1. Foreign Exchange Market 2. History of Foreign Exchange 3. Size of the

Parity Conditions in International Finance and Currency Forecasting. Chapter 4

Parity Conditions in International Finance and Currency Forecasting Chapter 4 ١ ARBITRAGE AND THE LAW OF ONE PRICE Five Parity Conditions Result From Arbitrage Activities 1. Purchasing Power Parity (PPP)

Parity Conditions in International Finance and Currency Forecasting Chapter 4 ١ ARBITRAGE AND THE LAW OF ONE PRICE Five Parity Conditions Result From Arbitrage Activities 1. Purchasing Power Parity (PPP)

Chapter 31 Open Economy Macroeconomics Basic Concepts

Chapter 31 Open Economy Macroeconomics Basic Concepts 0 In this chapter, look for the answers to these questions: How are international flows of goods and assets related? What s the difference between

Chapter 31 Open Economy Macroeconomics Basic Concepts 0 In this chapter, look for the answers to these questions: How are international flows of goods and assets related? What s the difference between

INTRODUCTION TO EXCHANGE RATES AND THE FOREIGN EXCHANGE MARKET

INTRODUCTION TO EXCHANGE RATES AND THE FOREIGN EXCHANGE MARKET 13 1 Exchange Rate Essentials 2 Exchange Rates in Practice 3 The Market for Foreign Exchange 4 Arbitrage and Spot Exchange Rates 5 Arbitrage

INTRODUCTION TO EXCHANGE RATES AND THE FOREIGN EXCHANGE MARKET 13 1 Exchange Rate Essentials 2 Exchange Rates in Practice 3 The Market for Foreign Exchange 4 Arbitrage and Spot Exchange Rates 5 Arbitrage

CAPITAL MARKET DEVELOPMENTS ABROAD. - l TeW Charts on Financial Markets Abroad II. Latest Figures Plotted in H.13 Chart Series, 1967

\ DIVISION OF INTERNATIONAL FINANCE BOARD OF OOV RK'3RI N H ; % 3 1 4 ' 1 9 6 7 ' CAPITAL MARKET DEVELOPMENTS ABROAD - l TeW Charts on Financial Markets Abroad II. Latest Figures Plotted in H.13 Chart

\ DIVISION OF INTERNATIONAL FINANCE BOARD OF OOV RK'3RI N H ; % 3 1 4 ' 1 9 6 7 ' CAPITAL MARKET DEVELOPMENTS ABROAD - l TeW Charts on Financial Markets Abroad II. Latest Figures Plotted in H.13 Chart

Chapter 6. International Parity Conditions. International Parity Conditions: Learning Objectives. Prices and Exchange Rates

Chapter 6 International arity Conditions International arity Conditions: Learning Objectives Examine how price levels and price level changes (inflation) in countries determine the exchange rate at which

Chapter 6 International arity Conditions International arity Conditions: Learning Objectives Examine how price levels and price level changes (inflation) in countries determine the exchange rate at which

Chapter 2 Foreign Exchange Parity Relations

Chapter 2 Foreign Exchange Parity Relations Note: In the sixth edition of Global Investments, the exchange rate quotation symbols differ from previous editions. We adopted the convention that the first

Chapter 2 Foreign Exchange Parity Relations Note: In the sixth edition of Global Investments, the exchange rate quotation symbols differ from previous editions. We adopted the convention that the first

Chapter 14 Exchange Rates and the Foreign Exchange Market: An Asset Approach

Chapter 14 Exchange Rates and the Foreign Exchange Market: An Asset Approach Copyright 2015 Pearson Education, Inc. All rights reserved. 1-1 Preview The basics of exchange rates Exchange rates and the

Chapter 14 Exchange Rates and the Foreign Exchange Market: An Asset Approach Copyright 2015 Pearson Education, Inc. All rights reserved. 1-1 Preview The basics of exchange rates Exchange rates and the

International Parity Conditions

International Parity Conditions Eiteman et al., Chapter 6 Winter 2004 Outline of the Chapter How are exchange rates determined? Can we predict them? Prices and Exchange Rates Prices Indices Inflation Rates

International Parity Conditions Eiteman et al., Chapter 6 Winter 2004 Outline of the Chapter How are exchange rates determined? Can we predict them? Prices and Exchange Rates Prices Indices Inflation Rates

International Parity Conditions. 1. The Law of One Price. 2. Absolute Purchasing Power Parity

International Parity Conditions Some fundamental questions of international financial managers are: - What are the determinants of exchange rates? - Are changes in exchange rates predictable? The economic

International Parity Conditions Some fundamental questions of international financial managers are: - What are the determinants of exchange rates? - Are changes in exchange rates predictable? The economic

University of Siegen

University of Siegen Faculty of Economic Disciplines, Department of economics Univ. Prof. Dr. Jan Franke-Viebach Seminar Risk and Finance Summer Semester 2008 Topic 4: Hedging with currency futures Name

University of Siegen Faculty of Economic Disciplines, Department of economics Univ. Prof. Dr. Jan Franke-Viebach Seminar Risk and Finance Summer Semester 2008 Topic 4: Hedging with currency futures Name

Chapter 8 Outline. Transaction exposure Should the Firm Hedge? Contractual hedge Risk Management in practice

Chapter 8 Outline Transaction exposure Should the Firm Hedge? Contractual hedge Risk Management in practice 1 / 51 Transaction exposure Transaction exposure measures gains or losses that arise from the

Chapter 8 Outline Transaction exposure Should the Firm Hedge? Contractual hedge Risk Management in practice 1 / 51 Transaction exposure Transaction exposure measures gains or losses that arise from the

Types of Exposure. Forward Market Hedge. Transaction Exposure. Forward Market Hedge. Forward Market Hedge: an Example INTERNATIONAL FINANCE.

Types of Exposure INTERNATIONAL FINANCE Chapter 8 Transaction exposure sensitivity of realized domestic currency values of the firm s contractual cash flows denominated in foreign currencies to unexpected

Types of Exposure INTERNATIONAL FINANCE Chapter 8 Transaction exposure sensitivity of realized domestic currency values of the firm s contractual cash flows denominated in foreign currencies to unexpected

05/07/55. International Parity Conditions. 1. The Law of One Price

International Parity Conditions Some fundamental questions of international financial managers are: - What are the determinants of exchange rates? - Are changes in exchange rates predictable? The economic

International Parity Conditions Some fundamental questions of international financial managers are: - What are the determinants of exchange rates? - Are changes in exchange rates predictable? The economic

International Parity Conditions

International Parity Conditions Some fundamental questions of international financial managers are: - What are the determinants of exchange rates? - Are changes in exchange rates predictable? The economic

International Parity Conditions Some fundamental questions of international financial managers are: - What are the determinants of exchange rates? - Are changes in exchange rates predictable? The economic

Exchange Rate Fluctuations Revised: January 7, 2012

The Global Economy Class Notes Exchange Rate Fluctuations Revised: January 7, 2012 Exchange rates (prices of foreign currency) are a central element of most international transactions. When Heineken sells

The Global Economy Class Notes Exchange Rate Fluctuations Revised: January 7, 2012 Exchange rates (prices of foreign currency) are a central element of most international transactions. When Heineken sells

Open-Economy Macroeconomics: Basic Concepts

Lesson 10 Open-Economy Macroeconomics: Basic Concepts Henan University of Technology Sino-British College Transfer Abroad Undergraduate Programme 0 In this lesson, look for the answers to these questions:

Lesson 10 Open-Economy Macroeconomics: Basic Concepts Henan University of Technology Sino-British College Transfer Abroad Undergraduate Programme 0 In this lesson, look for the answers to these questions:

Practice questions: Set #5

International Financial Management Professor Michel A. Robe What should you do with this set? Practice questions: Set #5 To help students prepare for the exam and the case, seven problem sets with solutions

International Financial Management Professor Michel A. Robe What should you do with this set? Practice questions: Set #5 To help students prepare for the exam and the case, seven problem sets with solutions

3) In 2010, what was the top remittance-receiving country in the world? A) Brazil B) Mexico C) India D) China

In 2010, what was the top remittance-receiving country in the world? A) Brazil B) Mexico C) India D) China") HSE-IB Test Syllabus: International Business: Environments and Operations, 15e, Global Edition (Daniels et al.). For use of the student for an educational purpose only, do not reproduce or redistribute.

HSE-IB Test Syllabus: International Business: Environments and Operations, 15e, Global Edition (Daniels et al.). For use of the student for an educational purpose only, do not reproduce or redistribute.

INTERNATIONAL FINANCE

INTERNATIONAL FINANCE Ing. Zuzana STRÁPEKOVÁ, PhD. 1 10. 2017/2018 SUA-FEM Nitra The FOREX market is a two-tiered market: Interbank Market (Wholesale) FUNCTION AND STRUCTURE OF THE FOREX MARKET - about

INTERNATIONAL FINANCE Ing. Zuzana STRÁPEKOVÁ, PhD. 1 10. 2017/2018 SUA-FEM Nitra The FOREX market is a two-tiered market: Interbank Market (Wholesale) FUNCTION AND STRUCTURE OF THE FOREX MARKET - about

Those who are interested in international business may wish to take FIN 430 which is our course on international financial management.

1 For the most part, the basic principles you ll learn in this class apply to both domestic and international businesses. However, two important differences you ll find when doing business internationally

1 For the most part, the basic principles you ll learn in this class apply to both domestic and international businesses. However, two important differences you ll find when doing business internationally

In frictionless markets, freely tradable goods should have the same price anywhere: S = P P $

Prices and Exchange Rates In frictionless markets, freely tradable goods should have the same price anywhere: P $ S = P P $ price in US$ S Exchange rate in yen per dollar P Price in Japanese yen Purchasing

Prices and Exchange Rates In frictionless markets, freely tradable goods should have the same price anywhere: P $ S = P P $ price in US$ S Exchange rate in yen per dollar P Price in Japanese yen Purchasing

Selected Interest & Exchange Rates

(516/517) Selected Interest & Exchange Rates W eekly Series o f Charts June 29, 1998 DIVISION OF INTERNATIONAL FINANCE Prepared by the FINANCIAL MARKETS SECTION BOARD OF GOVERNORS FEDERAL RESERVE SYSTEM

(516/517) Selected Interest & Exchange Rates W eekly Series o f Charts June 29, 1998 DIVISION OF INTERNATIONAL FINANCE Prepared by the FINANCIAL MARKETS SECTION BOARD OF GOVERNORS FEDERAL RESERVE SYSTEM

Chapter 4 Research Methodology

Chapter 4 Research Methodology 4.1 Introduction An exchange rate (also known as a foreign-exchange rate, forex rate, FX rate or Agio) between two currencies is the rate at which one currency will be exchanged

Chapter 4 Research Methodology 4.1 Introduction An exchange rate (also known as a foreign-exchange rate, forex rate, FX rate or Agio) between two currencies is the rate at which one currency will be exchanged

Answers to Selected Problems

Answers to Selected Problems Problem 1.11. he farmer can short 3 contracts that have 3 months to maturity. If the price of cattle falls, the gain on the futures contract will offset the loss on the sale

Answers to Selected Problems Problem 1.11. he farmer can short 3 contracts that have 3 months to maturity. If the price of cattle falls, the gain on the futures contract will offset the loss on the sale

EconS 327 Test 2 Spring 2010

1. Credit (+) items in the balance of payments correspond to anything that: a. Involves payments to foreigners b. Decreases the domestic money supply c. Involves receipts from foreigners d. Reduces international

1. Credit (+) items in the balance of payments correspond to anything that: a. Involves payments to foreigners b. Decreases the domestic money supply c. Involves receipts from foreigners d. Reduces international

Copyright 2009 Pearson Education Canada

CHAPTER NINE Qualitative Questions 1. What is the difference between a call option and a put option? For an option buyer, a call option is the right to buy, while a put option is the right to sell. For

CHAPTER NINE Qualitative Questions 1. What is the difference between a call option and a put option? For an option buyer, a call option is the right to buy, while a put option is the right to sell. For

ACCOUNTING FOR FOREIGN CURRENCY

ACCOUNTING FOR FOREIGN CURRENCY FOREIGN EXCHANGE MARKETS Each country uses its own currency as the unit of value for the purchase and sale of goods and services. The currency used in the United States

ACCOUNTING FOR FOREIGN CURRENCY FOREIGN EXCHANGE MARKETS Each country uses its own currency as the unit of value for the purchase and sale of goods and services. The currency used in the United States

NIRAJ THAPA FOREX. Foreign exchange constitutes the largest financial market in the world.

NIRAJ THAPA ON FOREX niraj_thapa@hotmail.com Foreign exchange constitutes the largest financial market in the world. TIM Weithers : Foreign Exchange:-It s not difficult; It s just confusing Contents Topic

NIRAJ THAPA ON FOREX niraj_thapa@hotmail.com Foreign exchange constitutes the largest financial market in the world. TIM Weithers : Foreign Exchange:-It s not difficult; It s just confusing Contents Topic

Management of Transaction Exposure

INTERNATIONAL FINANCIAL MANAGEMENT Seventh Edition EUN / RESNICK Management of Transaction Exposure 8 Chapter Eight INTERNATIONAL Chapter Objective: FINANCIAL MANAGEMENT This chapter discusses various

INTERNATIONAL FINANCIAL MANAGEMENT Seventh Edition EUN / RESNICK Management of Transaction Exposure 8 Chapter Eight INTERNATIONAL Chapter Objective: FINANCIAL MANAGEMENT This chapter discusses various

Introduction to Foreign Exchange Slides for International Finance (KOM Chapter 14)

") Slides for International Finance (KOM Chapter 14) American University 2011-09-01 Preview Introduction to Exchange Rates Basics exchange rate concepts Exchange rates and the cost of foreign goods The foreign

Slides for International Finance (KOM Chapter 14) American University 2011-09-01 Preview Introduction to Exchange Rates Basics exchange rate concepts Exchange rates and the cost of foreign goods The foreign

Management of Transaction Exposure

INTERNATIONAL FINANCIAL MANAGEMENT Seventh Edition EUN / RESNICK 8-0 Copyright 2015 by The McGraw-Hill Companies, Inc. All rights reserved. Management of Transaction Exposure 8 Chapter Eight INTERNATIONAL

INTERNATIONAL FINANCIAL MANAGEMENT Seventh Edition EUN / RESNICK 8-0 Copyright 2015 by The McGraw-Hill Companies, Inc. All rights reserved. Management of Transaction Exposure 8 Chapter Eight INTERNATIONAL

SELECTED INTEREST & EXCHANGE RATES FOR MAJOR COUNTRIES & THE U.S.

\«April 1, 1970 No. 448 f / A t *^ f,, H«13 Division of IntomotiMoiJxnyce Europe and British Common wealth Section f j y SELECTED INTEREST & EXCHANGE RATES FOR MAJOR COUNTRIES & THE U.S. WEEKLY SERIES

\«April 1, 1970 No. 448 f / A t *^ f,, H«13 Division of IntomotiMoiJxnyce Europe and British Common wealth Section f j y SELECTED INTEREST & EXCHANGE RATES FOR MAJOR COUNTRIES & THE U.S. WEEKLY SERIES

Management of Transaction Exposure

INTERNATIONAL FINANCIAL MANAGEMENT Seventh Edition EUN / RESNICK 8-0 Copyright 2015 by The McGraw-Hill Companies, Inc. All rights reserved. Management of Transaction Exposure 8 Chapter Eight INTERNATIONAL

INTERNATIONAL FINANCIAL MANAGEMENT Seventh Edition EUN / RESNICK 8-0 Copyright 2015 by The McGraw-Hill Companies, Inc. All rights reserved. Management of Transaction Exposure 8 Chapter Eight INTERNATIONAL

Midterm - Economics 160B, Spring 2012 Version A

Name Student ID Section (or TA) Midterm - Economics 160B, Spring 2012 Version A You will have 75 minutes to complete this exam. There are 6 pages and 111 points total. Good luck. Multiple choice: Mark

Name Student ID Section (or TA) Midterm - Economics 160B, Spring 2012 Version A You will have 75 minutes to complete this exam. There are 6 pages and 111 points total. Good luck. Multiple choice: Mark

SELECTED INTEREST & EXCHANGE RATES FOR MAJOR COUNTRIES & THE US.

April 22, 1970 No. 451 H-13 Division of International Finance Europe and British Commonwealth Section //A L / f ' nr

April 22, 1970 No. 451 H-13 Division of International Finance Europe and British Commonwealth Section //A L / f ' nr

H.13 September 21, 1966 No. 266 CAPITAL MARKET DEVELOPMENTS ABROAD

DIVISION OF INTERNATIONAL FINANCE BOARD OF GOVERNORS FEDERAL RESERVE SYSTEM H.13 September 21, 1966 No. 266 CAPITAL MARKET DEVELOPMENTS ABROAD I. Ten Charts on Financial Markets Abroad II. Latest Figures

DIVISION OF INTERNATIONAL FINANCE BOARD OF GOVERNORS FEDERAL RESERVE SYSTEM H.13 September 21, 1966 No. 266 CAPITAL MARKET DEVELOPMENTS ABROAD I. Ten Charts on Financial Markets Abroad II. Latest Figures

Global Finance : PPP, IFE, IRP Project

Global Finance : PPP, IFE, IRP Project JRL 咨询公司 (JRL Consulting) 科技管理职场发展咨询电邮 : tech@jrleeconsulting.com 网站 : www.jrleeconsulting.com Two countries (Canada and Japan) were selected for this exercise to

Global Finance : PPP, IFE, IRP Project JRL 咨询公司 (JRL Consulting) 科技管理职场发展咨询电邮 : tech@jrleeconsulting.com 网站 : www.jrleeconsulting.com Two countries (Canada and Japan) were selected for this exercise to

Study Questions (with Answers) Lecture 13. Exchange Rates

Lecture 13. Exchange Rates") Study Questions (with Answers) Page 1 of 5 Part 1: Multiple Choice Select the best answer of those given. Study Questions (with Answers) Lecture 13 1. The statement the yen rose today from 121 to 117 makes

Study Questions (with Answers) Page 1 of 5 Part 1: Multiple Choice Select the best answer of those given. Study Questions (with Answers) Lecture 13 1. The statement the yen rose today from 121 to 117 makes

Openness in goods and financial markets. Chapter 18

Openness in goods and financial markets Chapter 18 Illustration: exchange between the US and Ethiopia See videos: Black Gold and Life and Debt US goods market Electronics exports (+); coffee imports from

Openness in goods and financial markets Chapter 18 Illustration: exchange between the US and Ethiopia See videos: Black Gold and Life and Debt US goods market Electronics exports (+); coffee imports from

Problem Set 13. Name: Class: Date: Multiple Choice Identify the letter of the choice that best completes the statement or answers the question.

Name: Class: Date: Problem Set 13 Multiple Choice Identify the letter of the choice that best completes the statement or answers the question. 1. International trade a. raises the standard of living in

Name: Class: Date: Problem Set 13 Multiple Choice Identify the letter of the choice that best completes the statement or answers the question. 1. International trade a. raises the standard of living in

Chapter 6. The Open Economy

Chapter 6 0 IN THIS CHAPTER, YOU WILL LEARN: accounting identities for the open economy the small open economy model what makes it small how the trade balance and exchange rate are determined how policies

Chapter 6 0 IN THIS CHAPTER, YOU WILL LEARN: accounting identities for the open economy the small open economy model what makes it small how the trade balance and exchange rate are determined how policies

Study Questions. Lecture 13. Exchange Rates

Study Questions Page 1 of 5 Part 1: Multiple Choice Select the best answer of those given. Study Questions Lecture 13 1. The statement the yen rose today from 121 to 117 makes sense because a. The U.S.

Study Questions Page 1 of 5 Part 1: Multiple Choice Select the best answer of those given. Study Questions Lecture 13 1. The statement the yen rose today from 121 to 117 makes sense because a. The U.S.

Session 13. Exchange Rate Risk

Session 13 Exchange Rate Risk Programme : Executive Diploma in Accounting, Business & Strategy (EDABS 2017) Course : Corporate Financial Management (EDABS 202) Lecturer : Mr. Asanka Ranasinghe MBA (Colombo),

Session 13 Exchange Rate Risk Programme : Executive Diploma in Accounting, Business & Strategy (EDABS 2017) Course : Corporate Financial Management (EDABS 202) Lecturer : Mr. Asanka Ranasinghe MBA (Colombo),

Closed vs. Open Economies

Closed vs. Open Economies! A closed economy does not interact with other economies in the world.! An open economy interacts freely with other economies around the world. 1 Percent of GDP The U.S. Economy

Closed vs. Open Economies! A closed economy does not interact with other economies in the world.! An open economy interacts freely with other economies around the world. 1 Percent of GDP The U.S. Economy

Relationships among Exchange Rates, Inflation, and Interest Rates

Relationships among Exchange Rates, Inflation, and Interest Rates Chapter Objectives To explain the purchasing power parity (PPP) and international Fisher effect (IFE) theories, and their implications

Relationships among Exchange Rates, Inflation, and Interest Rates Chapter Objectives To explain the purchasing power parity (PPP) and international Fisher effect (IFE) theories, and their implications

H. 13 No. 374 CAPITAL MARKET DEVELOPMENTS ABROAD

H. 13 No. 374 CAPITAL MARKET DEVELOPMENTS ABROAD October 30, 1968. Lisr j l. Ten Charts on Financial Markets Abroad \u\ zl oo' Ijl. Latest Figures Plotted in H. 13 Chart Series, 1968 dci^t'tcll I. Ten

H. 13 No. 374 CAPITAL MARKET DEVELOPMENTS ABROAD October 30, 1968. Lisr j l. Ten Charts on Financial Markets Abroad \u\ zl oo' Ijl. Latest Figures Plotted in H. 13 Chart Series, 1968 dci^t'tcll I. Ten

Open-Economy Macroeconomics: Basic Concepts

N. Gregory Mankiw Principles of Macroeconomics Sixth Edition 18 Open-Economy Macroeconomics: Basic Concepts Premium PowerPoint Slides by Ron Cronovich 2012 UPDATE In this chapter, look for the answers

N. Gregory Mankiw Principles of Macroeconomics Sixth Edition 18 Open-Economy Macroeconomics: Basic Concepts Premium PowerPoint Slides by Ron Cronovich 2012 UPDATE In this chapter, look for the answers

FINC/ECON International Finance Homework Solution

FINC/ECON 3240 - International Finance Homework Solution Chapter 1 2. Comparative Advantage. a. Explain how the theory of comparative advantage relates to the need for international business. ANSWER: The

FINC/ECON 3240 - International Finance Homework Solution Chapter 1 2. Comparative Advantage. a. Explain how the theory of comparative advantage relates to the need for international business. ANSWER: The

Introduction to Foreign Exchange Slides for International Finance (KOM Chapter 14)

") Slides for International Finance (KOM Chapter 14) American University 2011-09-01 Preview Introduction to Exchange Rates Basics exchange rate concepts Exchange rates and the cost of foreign goods The foreign

Slides for International Finance (KOM Chapter 14) American University 2011-09-01 Preview Introduction to Exchange Rates Basics exchange rate concepts Exchange rates and the cost of foreign goods The foreign

Macroeonomics. 18 this chapter, Open-Economy Macroeconomics: look for the answers to these questions: Introduction. N.

C H A P T E R In 18 this chapter, look for the answers to these questions: Open-Economy Macroeconomics: How are international flows of goods and assets Basic Concepts related? P R I N C I P L E S O F Macroeonomics

C H A P T E R In 18 this chapter, look for the answers to these questions: Open-Economy Macroeconomics: How are international flows of goods and assets Basic Concepts related? P R I N C I P L E S O F Macroeonomics

Open Economy Macroeconomics Lecture Notes

Open Economy Macroeconomics Lecture Notes Open Economy Macroeconomics Ozan Hatipoglu Department of Economics, Bogazici University Spring 2014 Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics

Open Economy Macroeconomics Lecture Notes Open Economy Macroeconomics Ozan Hatipoglu Department of Economics, Bogazici University Spring 2014 Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics

in equilibrium, are supposed to hold across international markets. Covered Interest Rate Parity Purchasing Power Parity y( (also called the Law of

Week 4 The Parities The Parities There are three fundamental parity conditions that, in equilibrium, are supposed to hold across international markets. Covered Interest Rate Parity Purchasing Power Parity

Week 4 The Parities The Parities There are three fundamental parity conditions that, in equilibrium, are supposed to hold across international markets. Covered Interest Rate Parity Purchasing Power Parity

SELECTED INTEREST & EXCHANGE RATES FOR MAJOR COUNTRIES & THE US.

?. /r\cuduol ^ February 3, 1971 No. 491 H-13 Divib^dh of Internet lorn el Fi twice Ewepe end British Commonwealth Section SELECTED INTEREST & EXCHANGE RATES FOR MAJOR COUNTRIES & THE US. WEEKLY SERIES

?. /r\cuduol ^ February 3, 1971 No. 491 H-13 Divib^dh of Internet lorn el Fi twice Ewepe end British Commonwealth Section SELECTED INTEREST & EXCHANGE RATES FOR MAJOR COUNTRIES & THE US. WEEKLY SERIES

Chapter 25 The Exchange Rate and the Balance of Payments The Foreign Exchange Market

Chapter 25 The Exchange Rate and the Balance of Payments 25.1 The Foreign Exchange Market 1) Foreign currency is A) the market for foreign exchange. B) the price at which one currency exchanges for another

Chapter 25 The Exchange Rate and the Balance of Payments 25.1 The Foreign Exchange Market 1) Foreign currency is A) the market for foreign exchange. B) the price at which one currency exchanges for another

Chapter 9. Forecasting Exchange Rates. Lecture Outline. Why Firms Forecast Exchange Rates

Chapter 9 Forecasting Exchange Rates Lecture Outline Why Firms Forecast Exchange Rates Forecasting Techniques Technical Forecasting Fundamental Forecasting Market-Based Forecasting Mixed Forecasting Guidelines

Chapter 9 Forecasting Exchange Rates Lecture Outline Why Firms Forecast Exchange Rates Forecasting Techniques Technical Forecasting Fundamental Forecasting Market-Based Forecasting Mixed Forecasting Guidelines

Chapter 10. Measuring Exposure to Exchange Rate Fluctuations. Lecture Outline. Relevance of Exchange Rate Risk

Chapter 10 Measuring Exposure to Exchange Rate Fluctuations Lecture Outline Relevance of Exchange Rate Risk Transaction Exposure Estimating Net Cash Flows in Each Currency Exposure of an MNC s Portfolio

Chapter 10 Measuring Exposure to Exchange Rate Fluctuations Lecture Outline Relevance of Exchange Rate Risk Transaction Exposure Estimating Net Cash Flows in Each Currency Exposure of an MNC s Portfolio

Preview. Chapter 13. Depreciation and Appreciation. Definitions of Exchange Rates. Exchange Rates and the Foreign Exchange Market: An Asset Approach

Chapter 13 Exchange Rates and the Foreign Exchange Market: An Asset Approach Preview The basics of exchange rates Exchange rates and the prices of goods The foreign exchange markets The demand for currency

Chapter 13 Exchange Rates and the Foreign Exchange Market: An Asset Approach Preview The basics of exchange rates Exchange rates and the prices of goods The foreign exchange markets The demand for currency

CHAPTER 2. EXCHANGE RATE DETERMINATION: Exchange Rate Quotations, Balance of Payments, Prices, Parities and Interest Rates

CHAPTER 2. EXCHANGE RATE DETERMINATION: Exchange Rate Quotations, Balance of Payments, Prices, Parities and Interest Rates 1. Foreign Exchange Rates and Quotations A foreign exchange rate is the price

CHAPTER 2. EXCHANGE RATE DETERMINATION: Exchange Rate Quotations, Balance of Payments, Prices, Parities and Interest Rates 1. Foreign Exchange Rates and Quotations A foreign exchange rate is the price

Chapter 6. Learning Objectives. Principals Applies in this Chapter. Time Value of Money

Chapter 6 Time Value of Money 1 Learning Objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate the present and future values of each. 2. Calculate the present value of

Chapter 6 Time Value of Money 1 Learning Objectives 1. Distinguish between an ordinary annuity and an annuity due, and calculate the present and future values of each. 2. Calculate the present value of

The Open Economy. Inflation Worth Publishers, all rights reserved CHAPTER 5

6 The Open Economy Inflation CHAPTER 5 Modified by Ming Yi 2016 Worth Publishers, all rights reserved 5 IN THIS CHAPTER, YOU WILL LEARN: Accounting identities for the open economy The small open economy

6 The Open Economy Inflation CHAPTER 5 Modified by Ming Yi 2016 Worth Publishers, all rights reserved 5 IN THIS CHAPTER, YOU WILL LEARN: Accounting identities for the open economy The small open economy

Journal Of Financial And Strategic Decisions Volume 7 Number 2 Summer 1994 INTEREST RATE PARITY IN TIMES OF TURBULENCE: THE ISSUE REVISITED

Journal Of Financial And Strategic Decisions Volume 7 Number 2 Summer 1994 INTEREST RATE PARITY IN TIMES OF TURBULENCE: THE ISSUE REVISITED Nada Boulos * and Peggy E. Swanson * Abstract Empirical studies

Journal Of Financial And Strategic Decisions Volume 7 Number 2 Summer 1994 INTEREST RATE PARITY IN TIMES OF TURBULENCE: THE ISSUE REVISITED Nada Boulos * and Peggy E. Swanson * Abstract Empirical studies

::Solutions:: Problem Set #2: Due end of class October 2, 2018

Issues in International Finance ::Solutions:: Problem Set #2: Due end of class October 2, 2018 You may discuss this problem set with your classmates, but everything you turn in must be your own work. Questions

Issues in International Finance ::Solutions:: Problem Set #2: Due end of class October 2, 2018 You may discuss this problem set with your classmates, but everything you turn in must be your own work. Questions

National Income & Business Cycles

National Income & Business Cycles accounting identities for the open economy the small open economy model what makes it small how the trade balance and exchange rate are determined how policies affect

National Income & Business Cycles accounting identities for the open economy the small open economy model what makes it small how the trade balance and exchange rate are determined how policies affect

Chapter 11. Managing Transaction Exposure. Lecture Outline. Hedging Payables. Hedging Receivables

Chapter 11 Managing Transaction Exposure Lecture Outline Policies for Hedging Transaction Exposure Hedging Most of the Exposure Selective Hedging Hedging Payables Forward or Futures Hedge Money Market

Chapter 11 Managing Transaction Exposure Lecture Outline Policies for Hedging Transaction Exposure Hedging Most of the Exposure Selective Hedging Hedging Payables Forward or Futures Hedge Money Market

Chapter 3 Foreign Exchange Determination and Forecasting

Chapter 3 Foreign Exchange Determination and Forecasting Note: In the sixth edition of Global Investments, the exchange rate quotation symbols differ from previous editions. We adopted the convention that

Chapter 3 Foreign Exchange Determination and Forecasting Note: In the sixth edition of Global Investments, the exchange rate quotation symbols differ from previous editions. We adopted the convention that

Chapter 3 Foreign Exchange Determination and Forecasting

Chapter 3 oreign Exchange Determination and orecasting 1. Applying expansionary macroeconomic policy, which results in higher goods prices and lower real interest rates, will not reduce the balance of

Chapter 3 oreign Exchange Determination and orecasting 1. Applying expansionary macroeconomic policy, which results in higher goods prices and lower real interest rates, will not reduce the balance of

Capital & Money Markets

Πανεπιστήμιο Πειραιώς, Τμήμα Τραπεζικής και Χρηματοοικονομικής Διοικητικής Μεταπτυχιακό Πρόγραμμα «Χρηματοοικονομική και Τραπεζική Διοικητική» Capital & Money Markets Section 1 Foreign Exchange Markets

Πανεπιστήμιο Πειραιώς, Τμήμα Τραπεζικής και Χρηματοοικονομικής Διοικητικής Μεταπτυχιακό Πρόγραμμα «Χρηματοοικονομική και Τραπεζική Διοικητική» Capital & Money Markets Section 1 Foreign Exchange Markets

The Foreign Exchange Market

INTRO Go to page: Go to chapter Bookmarks Printed Page 421 The Foreign Exchange Module 43: Exchange Policy 43.1 Exchange Policy Module 44: Exchange s and 44.1 Exchange s and The role of the foreign exchange

INTRO Go to page: Go to chapter Bookmarks Printed Page 421 The Foreign Exchange Module 43: Exchange Policy 43.1 Exchange Policy Module 44: Exchange s and 44.1 Exchange s and The role of the foreign exchange

Exchange rate: the price of one currency in terms of another. We will be using the notation E t = euro

Econ 330: Money and Banking Fall 2014, Handout 8 Chapter 17 : Foreign Exchange Market 1. Foreign Exchange Market Exchange rate: the price of one currency in terms of another. We will be using the notation

Econ 330: Money and Banking Fall 2014, Handout 8 Chapter 17 : Foreign Exchange Market 1. Foreign Exchange Market Exchange rate: the price of one currency in terms of another. We will be using the notation

Open-Economy Macroeconomics: Basic Concepts

Wojciech Gerson (1831-1901) Seventh Edition Principles of Macroeconomics N. Gregory Mankiw CHAPTER 18 Open-Economy Macroeconomics: Basic Concepts Closed vs. Open Economies A closed economy does not interact

Wojciech Gerson (1831-1901) Seventh Edition Principles of Macroeconomics N. Gregory Mankiw CHAPTER 18 Open-Economy Macroeconomics: Basic Concepts Closed vs. Open Economies A closed economy does not interact

SELECTED INTEREST & EXCHANGE RATES FOR MAJOR COUNTRIES & THE US.

December 16, 1970 No. 484 H-13 Division of International Finance Europe and British Commonwealth Section zy Q0tU rwotj SELECTED INTEREST & EXCHANGE RATES FOR MAJOR COUNTRIES & THE US. WEEKLY SERIES OF

December 16, 1970 No. 484 H-13 Division of International Finance Europe and British Commonwealth Section zy Q0tU rwotj SELECTED INTEREST & EXCHANGE RATES FOR MAJOR COUNTRIES & THE US. WEEKLY SERIES OF