INTERNATIONAL FINANCE

|

|

|

- Jemima Cook

- 5 years ago

- Views:

Transcription

1 INTERNATIONAL FINANCE Ing. Zuzana STRÁPEKOVÁ, PhD /2018 SUA-FEM Nitra

2 The FOREX market is a two-tiered market: Interbank Market (Wholesale) FUNCTION AND STRUCTURE OF THE FOREX MARKET - about 700 banks worldwide stand ready to make a market in Foreign exchange - Nonbank dealers account for about 20% of the market - There are FX brokers who match buy and sell others but do not carry inventory and FX specialists Client Market (Retail) Market participants include international banks, their customers, nonbank dealers, FOREX brokers and central banks. 2

3 3 CORRESPONDENT BANKING RELATIONSHIPS Large commercial banks maintain demand deposit accounts with one another which facilitates the efficient functioning of the forex market. International commercial banks communicate with one another with: SWIFT: The Society for Worldwide Interbank Financial Telecommunications. CHIPS: Clearing House Interbank Payment System. ECHO: Exchange Clearing House Limited, the first global clearinghouse for settling interbank FOREX transactions.

4 4 THE BID-ASK SPREAD The bid price is the price a dealer is willing to pay you for something. The ask price is the amount the dealer wants you to pay for the thing. The bid-ask spread is the difference between the bid and ask prices.

5 5 SPOT FX TRADING In the interbank market, the standard size trade is about 10 mil. USD. A bank trading room is a noisy, active place. The stakes are high. The "long term" is about 10 minutes.

6 6 THE FORWARD MARKET A forward contract is an agreement to buy or sell an asset in the future at price agreed upon today. Bank quotes for 1, 3, 6, 9 and 12 months maturities are readily available for forward contracts. Long-term swaps are available. Long and Short forward Positions If you have agreed to sell anything (spot or forward), you are short. If you have agreed to buy anything (forward or spot), you are long. If you have agreed to sell forex forward, you are short. If you have agreed to buy forex forward, you are long.

7 7 SWAPS A swap is an agreement to provide a counterparty with something he wants in exchange for something that you want. Swap transactions account for approximately 51 percent of interbank FX trading, whereas outright trades are less than 9 percent.

8 8 THEORY OF PURCHASING POWER PARITY Development of the exchange rate at the foreign exchange market has a long-term trends. Tendencies are the expression of Purchasing Power Parity of different currencies. PURCHASING POWER PARITY (PPP) expression of individual foreign exchange rates by the basis of comparison of internal purchasing power ratio, which expresses the equality of purchasing powers of currencies compared The internal price levels of the states are therefore monitored by using a consumer basket of selected goods and services

9 9 THEORY OF PURCHASING POWER PARITY Thesis: identical goods in different countries should have the same price (Low of common price) Assumptions: - Free movement of goods - Market with unlimited competition - Zero transaction costs PPP: - Absolute version - Relative version (Swedish economist Gustav Cassel)

10 10 - Absolute version THEORY OF PURCHASING POWER PARITY - rate is derivated from the ratio of price levels - PPP is expressed statically ER P Di Q i P Zi Q i - exchange rate expressed in domestic currency units per unit of foreign currency - set of goods Q i expressed in domestic prices and domestic currency P Di - the same set of goods Q i valued in foreign prices in foreign currency P Zi

11 11 THEORY OF PURCHASING POWER PARITY Example of absolute version of the PPP theory can be set of goods (Consumer basket) valued at CZK, which represents CZK. The same set of goods valued at USD is USD. After substituting into the equation, it will be 30 CZK/USD. (ER = CZK/1 000 USD)

- \"Dynamic\" view of exchange rate ER t - equilibrium exchange")

12 12 - Relative version THEORY OF PURCHASING POWER PARITY - It focuses not on the basket of goods, but on the percentage changes in prices during the period, expressed as price indexes - A new equilibrium exchange rate adjusts to the inflation differential (it means changes in the annual inflation rate in the compared countries) - "Dynamic" view of exchange rate ER t - equilibrium exchange rate in the base period ER t+1 - equilibrium exchange rate in the period (t + 1) P D (P Z ) - annual inflation rate in domestic (foreign) country

13 13 THEORY OF PURCHASING POWER PARITY Example: - The price of beer in Czech republic increased by 9% - The price of beer in GB increased by 5% - Exchange rate of the British pound in the base period is 50 CZK/GBP ER (t+1) = 50 * 1 + 0, ,05 = 50 * 1,038 = 51,900 CZK/GBP Appreciation of the GBP = (51,900-50) / 50 = 0,038 Depreciation of CZK = (50-51,900) / 51,900 = - 0,037

14 14 THEORY OF PURCHASING POWER PARITY Inflation differential corrects the nominal exchange rate on the real exchange rate. According to the theory of PPP - PPP is understood as a natural equilibrium level of exchange rate. Objections to the theory: - PPP is unable to explain short-term movements of courses - The overall level of prices of the country includes all types of goods and services, but only some of them are subject of international exchange of goods - The definition of inflation is problematic

15 PURCHASING POWER PARITY, IMPORT DUTIES, IMPORT CONTINGENTS AND PRO-EXPORT TOOLS 15 Factor Demand for foreign exchange Offer of foreign exchange Market exchange rate PPP Import duty decrease slight decrease Appreciation Depreciation Import contingents decrease Appreciation Depreciation Pro-export tools increase Appreciation Depreciation

16 EXERCISE 1: Company dealing with forecasting the exchange rates published expected inflation rate for the Czech Republic and Germany for the following five years. Expected inflation rate in Czech Republic is 7% p.a., in Germany 4% p.a. When the current exchange rate is 41,5362 CZK/EUR, what will be the exchange rates over the next five years? (domestic country Czech Republic; foreign country Germany) 16 ER1= 41,5362 * [(1+0,07)/(1+0,04)] = 42,734 CZK/EUR ER2 = 42,734 * 1,028 = 43,93 CZK/EUR 1,028 ER3 = 43,93 * 1,028 = 45,16 CZK/EUR ER4 = 45,16 * 1,028 = 46,425 CZK/EUR ER5 = 46,425 * 1,028 = 47,73 CZK/EUR

17 17 EXERCISE 2: Calculate the expected exchange rate, when PPP is: Czech Republic = 26 CZK / CAD Expected inflation rate is: In Canada = 5%; In Czech Republic = 10% ER(t+1) = 26 * [(1+0,1)/(1+0,05)] = 27,238 Inflation differential is 1,0476. It means appreciation of the CZK.

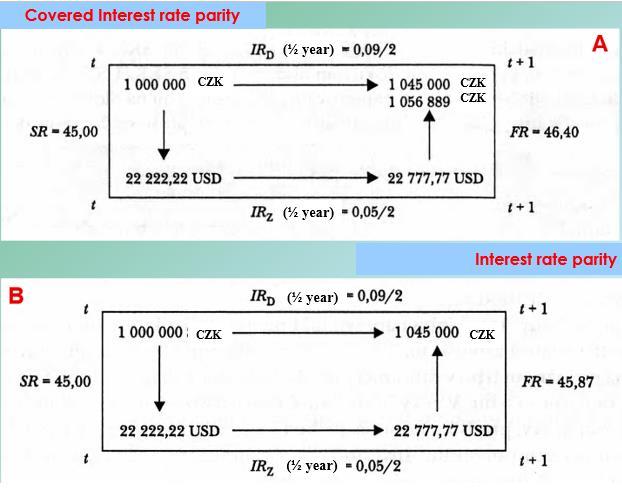

18 18 EXERCISE 3: Calculate whether the EURO is sold with premium or with discount on a forward 3-month forward market. SR = 41,8 CZK/EUR FR = 41,975 CZK/EUR f = (41,975 41,8)/41,8 = 0,0042 * 100 = 0,42 % with premium

19 19 PURCHASING POWER PARITY AND ERDI ERDI - exchange rate deviation index - it is the deviation of the nominal exchange rate from the exchange rate in purchasing power parity. EXCHANGE RATES ARE DIVIDED: Nominal - Effective - Real - Exchange rates (ER) of the national currencies expressed in a foreign national currency (International statistics they mostly expressed in USD) Expression of the ER of the national currency in the use of 'floating' nominal exchange rates corrected by inflation differences

20 The real exchange rate THE REAL EXCHANGE RATE THE REAL EXCHANGE RATE INDEX 20 The real effective exchange rate (REER) calculated on the base of the producer price index is one of the indicators of changes in the price competitiveness of domestic production to foreign

21 21 balance (imbalance) of balance of payments, equilibrium of balance of current payments, Inflation differential and interest rate differential, change of money supply, THE EXCHANGE RATE IS INFLUENCED BY FUNDAMENTAL FACTORS the growth rate of the national income + the expectations of the subjects of the foreign exchange market, monetary policy and other factors

22 22 PARITY RELATIONS: Purchasing Power Parity Interest Rate Parity International Fisher Effect The theory of exchange rate - an integrated system that explains the behavior of the exchange rate. Knowledge of the exchange rate theories is a basis for the creation of the fundamental model of the exchange rates forecasting.

23 23 Objective of fundamental analysis is to formulate economic models for forecasting of movement of exchange rate SR - relative change in exchange (spot) rate v, x,... z - explaining fundamental factors (of the relative change) t, h, k, m, n - variables emphasizing viewership of fundamental factors for different time period

24 24 INTEREST RATE PARITY PPP - the theoretical condition of equilibrium on the international market of goods IRP - theoretical condition of equilibrium in the international capital market IRP is based on the thesis: If there is free movement of capital, investors seeking to achieve the same profits from its assets, may be denominated in any currency.

25 25 Investor when investing abroad must be guided by two factors: a) by interest rate in the home country (IR D ) and abroad (IR Z ) b) by exchange rate (ER) /current and expected/

26 26 EXERCISE 4: IRP exercise entering data: export (beer) Czech Republic Great Britain in CR (D) the possibility 6 months to the payment for a factor of production (barley) of short-term investments in GB (Z) (price 1 mil. GBP) IR D = 9 % p.a. IR Z = 5 % p.a. ER = 50 CZK/GBP ER e = 50,976 CZK/GBP

27 IRP exercise results: 27 EXERCISE 4: 1) In CR investment of 1 million. GBP in short-term securities in the money market in the Czech Republic Income after 6 months IR D /2 = 6 months period K * ER * (1 +IR D /2) = 1 mil. GBP * 50 CZK/GBP * (1 + 0,09/2) = 52,25 mil. CZK 2) In GB (The company will follow not only IR Z in GB, but also the expected exchange rate ER e = 50,976 CZK/GBP) Income after 6 months 1 mil. GBP * (1 + 0,05/2) * 50,976 CZK/GBP = 52,25 mil. CZK Both variants mean the same income for Czech company (52,25 mil. CZK) This is due to balancing the market in the form of "interest rate"

50, 976 50 50 = 1 + 0, 09 2 1 + 1 + 0, 05 2 0,")

28 28 UNCOVERED INTEREST RATE PARITY Condition: Expected change of exchange rate (ERE) should approximately correspond to the interest rate differential. According to this, the market is in equilibrium /0,0195 0,0195/ (both investment strategies are equivalent) 50, = 1 + 0, , , 05 2

29 29 COVERED INTEREST RATE PARITY Condition: Nominal rate of investment, which is secured or covered against interest rate risk will be the same in all countries If this is not true covered interest arbitrage

30 30

is income from domestic and foreign securities for Czech investors the same.")

31 31 INTEREST RATE DIFFERENTIAL (IRD) It expresses forward premium (+) or forward discount (-) 45,87/45 = 1, = 0,0193 With the forward premium 1,93% (0,0193 * 100) is income from domestic and foreign securities for Czech investors the same.

32 32 EXERCISE 5: IRP exercise entering data: Company exports products to Canada. Company will have to pay for raw materials after 6 months. Company has 1 mil. DKK at the account. Company wants to invest these money in the short term. Company must decide whether to invest in short-term securities in Denmark or in Canada. Annual interest rate Denmark = 9% p.a.; in Canada = 5 % p.a. Exchange rate: SR = 4 DKK/CAD; FR = 4,25 DKK/CAD a) Describe possible cash flows b) At which forward rate the interest rate parity arise?

33 IRP exercise results: 33 EXERCISE 5: a) Investment in Denmark into the short-term securities * (1 + 0,09/2) = profit DKK Investment in Canada into the short-term securities Profit from this operation? ( /4) * [(1 + (0,05/2)] = profit CAD /4 = * 4,25 = DKK (profit DKK) For company is better to invest in Canada. b) IRP: SR e SR SR = 1+IR D (1+ IR Z ) (1+ IR Z ) FR SR = 1+ IR D 1+ IR Z FR = SR 1+ IR D 1+ IR Z FR = 4 * [(1 + 0,045)/(1 + 0,025)] = 4,078 DKK/CAD At this exchange rate IRP arise.

34 34 EXERCISE 6: The annual interest rate in GB was 12% in the USA 9%. a) If the current exchange rate is 1,63 USD/GBP, which is the expected exchange rate after one year? b) Suppose that the future spot rate in USA will be reduced to 1,52 USD/GBP due to changes in inflation expectations. What should be the interest rate in the USA?

35 35 EXERCISE 6: a) SR e = SR * (1 + IR D )/(1 + IR Z ) = 1,63 * (1 + 0,09)/(1 + 0,12) = 1,586 USD/GBP b) 1,52 = 1,63 * (1 + IR D )/(1 + IR Z ) 1,52/1,63 = (1 + IR D )/(1 + 0,12) 0,9325 = (1 + IR D )/1,12 1,0444 = 1 + IR D IR D = 0,0444 4,44%

36 36 SR FR SR e - spot rate - forward rate - expected spot rate Determinant of the expected spot rate is the forward rate.

.")

37 FISHER EFFECT According to Fisher, the nominal interest rate (IR) consists of a real interest rate (IR R ) and the expected inflation rate (p e ) IR = (1 + IR R ) * (1 + p e ) The simple form of the Fisher equation: IR R = IR - p e

38 38 EXERCISE 7: If an investor invests 1000 EUR with 3% p. a. expected interest rate and inflation 4%, how much will be required in the future to return?

39 39 INTERNATIONAL FISHER EFFECT Argument: nominal interest rate differential of two countries is the sum of the differentials of the real interest rates and of the differential inflation expectations

40 40 THE FOLLOWING EQUATION ARE VALID change in exchange rate» inflation differential expected change in SR» differential of expected inflation forward premium/discount» interest rate differential interest rate differential» differential of the expected inflation expected exchange of SR» interest rate differential

- Purchasing Power Parity (PPP) - expected change of the exchange rate - real interest rate - inflation")

41 41 RELATIONSHIPS BETWEEN INFLATION, INTEREST RATE AND EXCHANGE RATE MFE PÚM PKS ER e IR p - International Fisher Effect (IFE) - Interest Rate Parity (IRP) - Purchasing Power Parity (PPP) - expected change of the exchange rate - real interest rate - inflation rate

42 42 EXERCISE 8: At the beginning of 1996 were short-term interest rates in France, 3,7% and 1,8% expected inflation. At the same time short-term interest rate in Germany was 2,6% and inflation 1,6%. a) What were the real interest rates in both countries? b) What caused the difference in interest rates in these countries?

43 43 EXERCISE 8: a) International Fisher Effect IR = IR Z + p e 1 + IR = (1 + IR r ) * (1 + p e ) France: 1 + 0,037 = (1 + IR r ) * (1 + 0,018) 1,037 = 1,018 + Ir r IR r = 0,0186 1,86% Germany: 1 + 0,026 = (1 + IR r ) * (1 + 0,016) 1,026 = 1,016 + IR r IR r = 0,0098 0,98% b) The difference in interest rates is caused by different inflation rates, which are taken in account in the interest rates.

44 THANK YOU FOR ATTENTION! 44

INTERNATIONAL FINANCE

INTERNATIONAL FINANCE 5. 2017/2018 Ing. Zuzana STRÁPEKOVÁ, PhD. SUA-FEM Nitra CONTENTS: Eexchange rate quotation Cross exchange rates Bilateral arbitration Trilateral arbitration Quotation of forward ER

INTERNATIONAL FINANCE 5. 2017/2018 Ing. Zuzana STRÁPEKOVÁ, PhD. SUA-FEM Nitra CONTENTS: Eexchange rate quotation Cross exchange rates Bilateral arbitration Trilateral arbitration Quotation of forward ER

MCQ on International Finance

MCQ on International Finance 1. If portable disk players made in China are imported into the United States, the Chinese manufacturer is paid with a) international monetary credits. b) dollars. c) yuan,

MCQ on International Finance 1. If portable disk players made in China are imported into the United States, the Chinese manufacturer is paid with a) international monetary credits. b) dollars. c) yuan,

Week-7. Dr. Ahmed. Domestic Firms International Firms Multinational Firms Global Firms

FINC 5880 Dr. Ahmed Week-7 Name Domestic Firms International Firms Multinational Firms Global Firms Factors that make multinational financial management different Exchange rates and trading International

FINC 5880 Dr. Ahmed Week-7 Name Domestic Firms International Firms Multinational Firms Global Firms Factors that make multinational financial management different Exchange rates and trading International

Parity Conditions in International Finance and Currency Forecasting. Chapter 4

Parity Conditions in International Finance and Currency Forecasting Chapter 4 ١ ARBITRAGE AND THE LAW OF ONE PRICE Five Parity Conditions Result From Arbitrage Activities 1. Purchasing Power Parity (PPP)

Parity Conditions in International Finance and Currency Forecasting Chapter 4 ١ ARBITRAGE AND THE LAW OF ONE PRICE Five Parity Conditions Result From Arbitrage Activities 1. Purchasing Power Parity (PPP)

FOREIGN EXCHANGE MARKET. Luigi Vena 05/08/2015 Liuc Carlo Cattaneo

FOREIGN EXCHANGE MARKET Luigi Vena 05/08/2015 Liuc Carlo Cattaneo TABLE OF CONTENTS The FX market Exchange rates Exchange rates regimes Financial balances International Financial Markets 05/08/2015 Coopeland

FOREIGN EXCHANGE MARKET Luigi Vena 05/08/2015 Liuc Carlo Cattaneo TABLE OF CONTENTS The FX market Exchange rates Exchange rates regimes Financial balances International Financial Markets 05/08/2015 Coopeland

dr Bartłomiej Rokicki Chair of Macroeconomics and International Trade Theory Faculty of Economic Sciences, University of Warsaw

Chair of Macroeconomics and International Trade Theory Faculty of Economic Sciences, University of Warsaw Determinants of the demand for foreign currencies To understand what factors determine the exchange

Chair of Macroeconomics and International Trade Theory Faculty of Economic Sciences, University of Warsaw Determinants of the demand for foreign currencies To understand what factors determine the exchange

Capital & Money Markets

Πανεπιστήμιο Πειραιώς, Τμήμα Τραπεζικής και Χρηματοοικονομικής Διοικητικής Μεταπτυχιακό Πρόγραμμα «Χρηματοοικονομική και Τραπεζική Διοικητική» Capital & Money Markets Section 1 Foreign Exchange Markets

Πανεπιστήμιο Πειραιώς, Τμήμα Τραπεζικής και Χρηματοοικονομικής Διοικητικής Μεταπτυχιακό Πρόγραμμα «Χρηματοοικονομική και Τραπεζική Διοικητική» Capital & Money Markets Section 1 Foreign Exchange Markets

Foreign Exchange Markets: Key Institutional Features (cont)

") Foreign Exchange Markets FOREIGN EXCHANGE MARKETS Professor Anant Sundaram AGENDA Basic characteristics of FX markets: Institutional features Spot markets Forward markets Appreciation, depreciation, premium,

Foreign Exchange Markets FOREIGN EXCHANGE MARKETS Professor Anant Sundaram AGENDA Basic characteristics of FX markets: Institutional features Spot markets Forward markets Appreciation, depreciation, premium,

Relationships among Exchange Rates, Inflation, and Interest Rates

Relationships among Exchange Rates, Inflation, and Interest Rates Chapter Objectives To explain the purchasing power parity (PPP) and international Fisher effect (IFE) theories, and their implications

Relationships among Exchange Rates, Inflation, and Interest Rates Chapter Objectives To explain the purchasing power parity (PPP) and international Fisher effect (IFE) theories, and their implications

CHAPTER 2. EXCHANGE RATE DETERMINATION: Exchange Rate Quotations, Balance of Payments, Prices, Parities and Interest Rates

CHAPTER 2. EXCHANGE RATE DETERMINATION: Exchange Rate Quotations, Balance of Payments, Prices, Parities and Interest Rates 1. Foreign Exchange Rates and Quotations A foreign exchange rate is the price

CHAPTER 2. EXCHANGE RATE DETERMINATION: Exchange Rate Quotations, Balance of Payments, Prices, Parities and Interest Rates 1. Foreign Exchange Rates and Quotations A foreign exchange rate is the price

2. Discuss the implications of the interest rate parity for the exchange rate determination.

CHAPTER 5 INTERNATIONAL PARITY RELATIONSHIPS AND FORECASTING FOREIGN EXCHANGE RELATIONSHIPS SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. Give a full definition

CHAPTER 5 INTERNATIONAL PARITY RELATIONSHIPS AND FORECASTING FOREIGN EXCHANGE RELATIONSHIPS SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. Give a full definition

Exam 2 Sample Questions FINAN430 International Finance McBrayer Spring 2018

Sample Multiple Choice Questions 1. Suppose you observe a spot exchange rate of $1.0500/. If interest rates are 5% APR in the U.S. and 3% APR in the euro zone, what is the no-arbitrage 1-year forward rate?

Sample Multiple Choice Questions 1. Suppose you observe a spot exchange rate of $1.0500/. If interest rates are 5% APR in the U.S. and 3% APR in the euro zone, what is the no-arbitrage 1-year forward rate?

Lecture 2. Agenda: Basic descriptions for derivatives. 1. Standard derivatives Forward Futures Options

Lecture 2 Basic descriptions for derivatives Agenda: 1. Standard derivatives Forward Futures Options 2. Nonstandard derivatives ICON Range forward contract 1. Standard derivatives ~ Forward contracts:

Lecture 2 Basic descriptions for derivatives Agenda: 1. Standard derivatives Forward Futures Options 2. Nonstandard derivatives ICON Range forward contract 1. Standard derivatives ~ Forward contracts:

Agenda. Learning Objectives. Chapter 19. International Business Finance. Learning Objectives Principles Used in This Chapter

Chapter 19 International Business Finance Agenda Learning Objectives Principles Used in This Chapter 1. Foreign Exchange Markets and Currency Exchange Rates 2. Interest Rate and Purchasing-Power Parity

Chapter 19 International Business Finance Agenda Learning Objectives Principles Used in This Chapter 1. Foreign Exchange Markets and Currency Exchange Rates 2. Interest Rate and Purchasing-Power Parity

Less Reliable International Parity Conditions

The International Parity Conditions The Law of One Price Interest Rate Parity Less Reliable International Parity Conditions The Real Exchange Rate 1 The International Parity Conditions Though this be madness,

The International Parity Conditions The Law of One Price Interest Rate Parity Less Reliable International Parity Conditions The Real Exchange Rate 1 The International Parity Conditions Though this be madness,

International Parity Conditions. 1. The Law of One Price. 2. Absolute Purchasing Power Parity

International Parity Conditions Some fundamental questions of international financial managers are: - What are the determinants of exchange rates? - Are changes in exchange rates predictable? The economic

International Parity Conditions Some fundamental questions of international financial managers are: - What are the determinants of exchange rates? - Are changes in exchange rates predictable? The economic

INTERNATIONAL FINANCE MBA 926

INTERNATIONAL FINANCE MBA 926 1. Give a full definition of the market for foreign exchange. Answer: Broadly defined, the foreign exchange (FX) market encompasses the conversion of purchasing power from

INTERNATIONAL FINANCE MBA 926 1. Give a full definition of the market for foreign exchange. Answer: Broadly defined, the foreign exchange (FX) market encompasses the conversion of purchasing power from

A Primer in International Financial Economics

FIN 463 International Finance Economics, Forecasting and Arbitrage Professor Robert Hauswald Kogod School of Business, AU A Primer in International Financial Economics The (foreign) exchange rate is the

FIN 463 International Finance Economics, Forecasting and Arbitrage Professor Robert Hauswald Kogod School of Business, AU A Primer in International Financial Economics The (foreign) exchange rate is the

Prepared by Iordanis Petsas To Accompany. by Paul R. Krugman and Maurice Obstfeld

Chapter 13 Exchange Rates and the Foreign Exchange Market: An Asset Approach Prepared by Iordanis Petsas To Accompany International Economics: Theory and Policy, Sixth Edition by Paul R. Krugman and Maurice

Chapter 13 Exchange Rates and the Foreign Exchange Market: An Asset Approach Prepared by Iordanis Petsas To Accompany International Economics: Theory and Policy, Sixth Edition by Paul R. Krugman and Maurice

05/07/55. International Parity Conditions. 1. The Law of One Price

International Parity Conditions Some fundamental questions of international financial managers are: - What are the determinants of exchange rates? - Are changes in exchange rates predictable? The economic

International Parity Conditions Some fundamental questions of international financial managers are: - What are the determinants of exchange rates? - Are changes in exchange rates predictable? The economic

International Parity Conditions

International Parity Conditions Some fundamental questions of international financial managers are: - What are the determinants of exchange rates? - Are changes in exchange rates predictable? The economic

International Parity Conditions Some fundamental questions of international financial managers are: - What are the determinants of exchange rates? - Are changes in exchange rates predictable? The economic

Chapter 5. The Foreign Exchange Market. Foreign Exchange Markets: Learning Objectives. Foreign Exchange Markets. Foreign Exchange Markets

Chapter 5 The Foreign Exchange Market Foreign Exchange Markets: Learning Objectives Examine the functions performed by the foreign exchange (FOREX) market, its participants, size, geographic and currency

Chapter 5 The Foreign Exchange Market Foreign Exchange Markets: Learning Objectives Examine the functions performed by the foreign exchange (FOREX) market, its participants, size, geographic and currency

Madura: International Financial Management Chapter 8

Madura: International Financial Management Chapter Chapter Relationships Between Inflation, Interest Rates, and Exchange Rates Chapter Objectives To explain the theories of purchasing power parity (PPP)

Madura: International Financial Management Chapter Chapter Relationships Between Inflation, Interest Rates, and Exchange Rates Chapter Objectives To explain the theories of purchasing power parity (PPP)

Ch. 7 International Arbitrage and IRP. International Arbitrage. International Arbitrage

Ch. 7 and IRP Topics Locational Arbitrage Triangular Arbitrage Covered Interest Arbitrage Impact of Arbitrage on an MNC s Value Arbitrage: The simultaneous purchase and sale of securities or foreign exchange

Ch. 7 and IRP Topics Locational Arbitrage Triangular Arbitrage Covered Interest Arbitrage Impact of Arbitrage on an MNC s Value Arbitrage: The simultaneous purchase and sale of securities or foreign exchange

Introduction to Foreign Exchange Slides for International Finance (KOM Chapter 14)

") Slides for International Finance (KOM Chapter 14) American University 2011-09-01 Preview Introduction to Exchange Rates Basics exchange rate concepts Exchange rates and the cost of foreign goods The foreign

Slides for International Finance (KOM Chapter 14) American University 2011-09-01 Preview Introduction to Exchange Rates Basics exchange rate concepts Exchange rates and the cost of foreign goods The foreign

Foreign Exchange Markets

Foreign Exchange Markets Foreign exchange: Money of another country. Foreign exchange transaction: and the seller of a currency. Agreement between the buyer Foreign exchange market (FOREX market): Physical

Foreign Exchange Markets Foreign exchange: Money of another country. Foreign exchange transaction: and the seller of a currency. Agreement between the buyer Foreign exchange market (FOREX market): Physical

Foundations of Multinational Financial Management

Foundations of Multinational Financial Management Alan Shapiro John Wiley & Sons Power Points by Joseph F. Greco, Ph.D. California State University, Fullerton 1 The Foreign Exchange Markets Chapter 6 2

Foundations of Multinational Financial Management Alan Shapiro John Wiley & Sons Power Points by Joseph F. Greco, Ph.D. California State University, Fullerton 1 The Foreign Exchange Markets Chapter 6 2

Arabian Group of Journals (AGJ) Accounting Research. International Journal of Accounting Research (IJAR) Webpage:

Accounting Research. International Journal of Accounting Research (IJAR) Webpage:") Arabian Group of Journals (AGJ) Accounting Research International Journal of Accounting Research (IJAR) Webpage: www.arabianjbmr.com/ijar_index.php ISSN: 2311-326X EXCHANGE RATE FLUCTUATIONS MAJOR FACTOR

Arabian Group of Journals (AGJ) Accounting Research International Journal of Accounting Research (IJAR) Webpage: www.arabianjbmr.com/ijar_index.php ISSN: 2311-326X EXCHANGE RATE FLUCTUATIONS MAJOR FACTOR

Financial markets in the open economy - the interest rate parity. Exchange rates in the short run.

Financial markets in the open economy - the interest rate parity. Exchange rates in the short run. Dr hab. Joanna Siwińska-Gorzelak Foreign Exchange Markets The set of markets where foreign currencies

Financial markets in the open economy - the interest rate parity. Exchange rates in the short run. Dr hab. Joanna Siwińska-Gorzelak Foreign Exchange Markets The set of markets where foreign currencies

Introduction to Foreign Exchange Slides for International Finance (KOM Chapter 14)

") Slides for International Finance (KOM Chapter 14) American University 2011-09-01 Preview Introduction to Exchange Rates Basics exchange rate concepts Exchange rates and the cost of foreign goods The foreign

Slides for International Finance (KOM Chapter 14) American University 2011-09-01 Preview Introduction to Exchange Rates Basics exchange rate concepts Exchange rates and the cost of foreign goods The foreign

Chapter 6. International Parity Conditions. International Parity Conditions: Learning Objectives. Prices and Exchange Rates

Chapter 6 International arity Conditions International arity Conditions: Learning Objectives Examine how price levels and price level changes (inflation) in countries determine the exchange rate at which

Chapter 6 International arity Conditions International arity Conditions: Learning Objectives Examine how price levels and price level changes (inflation) in countries determine the exchange rate at which

Lessons V and VI: FX Parity Conditions

Lessons V and VI: FX March 27, 2017 Table of Contents Does the PPP Hold Parity s should be thought of as break-even values, where the decision-maker is indifferent between two available strategies. Parity

Lessons V and VI: FX March 27, 2017 Table of Contents Does the PPP Hold Parity s should be thought of as break-even values, where the decision-maker is indifferent between two available strategies. Parity

Replies to one minute memos, 9/21/03

Replies to one minute memos, 9/21/03 Dear Students, Thank you for asking these great questions. The answer to my question (what is the difference b/n the covered & uncovered interest rate arbitrage? If

Replies to one minute memos, 9/21/03 Dear Students, Thank you for asking these great questions. The answer to my question (what is the difference b/n the covered & uncovered interest rate arbitrage? If

Chapter 2. The Foreign Exchange Market Cambridge University Press 2-1

Chapter 2 The Foreign Exchange Market 2018 Cambridge University Press 2-1 Exhibit 2.1 The Structure of the Foreign Exchange Market Most important cities: London, New York, Tokyo ForEx (or FX) operates

Chapter 2 The Foreign Exchange Market 2018 Cambridge University Press 2-1 Exhibit 2.1 The Structure of the Foreign Exchange Market Most important cities: London, New York, Tokyo ForEx (or FX) operates

International Financial and Foreign Exchange Markets. Parity Relationships. Currency Options. Currency Arbitrages. Exercise Handbook.

Exercise Handbook March 30, 2018 Table of Contents Exercise XXXII In the 1990s, Russia was attempting to import more goods, but had little to offer to other countries in terms of potential exports. In

Exercise Handbook March 30, 2018 Table of Contents Exercise XXXII In the 1990s, Russia was attempting to import more goods, but had little to offer to other countries in terms of potential exports. In

Lessons V and VI: Overview

Lessons V and VI: Overview 1. FX parity conditions 2. Do the PPP and the IRPs (CIRP and UIRP) hold in practice? 1 FX parity conditions 2 FX parity conditions 1. The Law of One Price and the Purchasing

Lessons V and VI: Overview 1. FX parity conditions 2. Do the PPP and the IRPs (CIRP and UIRP) hold in practice? 1 FX parity conditions 2 FX parity conditions 1. The Law of One Price and the Purchasing

NIRAJ THAPA FOREX. Foreign exchange constitutes the largest financial market in the world.

NIRAJ THAPA ON FOREX niraj_thapa@hotmail.com Foreign exchange constitutes the largest financial market in the world. TIM Weithers : Foreign Exchange:-It s not difficult; It s just confusing Contents Topic

NIRAJ THAPA ON FOREX niraj_thapa@hotmail.com Foreign exchange constitutes the largest financial market in the world. TIM Weithers : Foreign Exchange:-It s not difficult; It s just confusing Contents Topic

1)International Monetary System

International Monetary System") 1) (International Monetary System) 2) 3) (Balance of Payments) 4) (Foreign Exchange Market) 5) Interest Rate Parity (IRP) 6) Covered Interest Arbitrage 1 1)International Monetary System 1.1 The Gold Standard

1) (International Monetary System) 2) 3) (Balance of Payments) 4) (Foreign Exchange Market) 5) Interest Rate Parity (IRP) 6) Covered Interest Arbitrage 1 1)International Monetary System 1.1 The Gold Standard

Exchange ratein a shortrun

Exchange ratein a shortrun dr hab. Bartłomiej Rokicki Chair of Macroeconomics and International Trade Theory Faculty of Economic Sciences, University of Warsaw Main definitions Foreign exchange market

Exchange ratein a shortrun dr hab. Bartłomiej Rokicki Chair of Macroeconomics and International Trade Theory Faculty of Economic Sciences, University of Warsaw Main definitions Foreign exchange market

Homework Assignment #3: Answer Key

Econ 434 Professor Ickes Fall 2006 Homework Assignment #3: Answer Key 1. Productivity growth has increased in Central and Eastern European countries relative to Western European countries. This has implications

Econ 434 Professor Ickes Fall 2006 Homework Assignment #3: Answer Key 1. Productivity growth has increased in Central and Eastern European countries relative to Western European countries. This has implications

Lesson II: Overview. 1. Foreign exchange markets: everyday market practice

Lesson II: Overview 1. Foreign exchange markets: everyday market practice 2. Forward foreign exchange market 1 Foreign exchange markets: everyday market practice 2 Getting started I The exchange rates

Lesson II: Overview 1. Foreign exchange markets: everyday market practice 2. Forward foreign exchange market 1 Foreign exchange markets: everyday market practice 2 Getting started I The exchange rates

Lesson II: A Deeper Insight into Everyday FX Market Practice

Lesson II: A Deeper Insight into Everyday FX Market March 6, 2017 Table of Contents Getting Started Some useful trading jargon: Bid: rate at which a certain market player is willing to buy Ask: rate at

Lesson II: A Deeper Insight into Everyday FX Market March 6, 2017 Table of Contents Getting Started Some useful trading jargon: Bid: rate at which a certain market player is willing to buy Ask: rate at

Topic7 Management of Transaction Exposure (1)

") Topic7 Management of Transaction Exposure (1) - Forward Market Hedge - Money Market Hedge Opponents of hedging (1) Stockholders are much more capable of diversifying currency risk than management of the

Topic7 Management of Transaction Exposure (1) - Forward Market Hedge - Money Market Hedge Opponents of hedging (1) Stockholders are much more capable of diversifying currency risk than management of the

Financial Management in IB. Exercises

Financial Management in IB Exercises I. Foreign Exchange Market Locational Arbitrage Paris Interbank market: EUR/USD 1.2548/1.2552 London Interbank market: EUR/USD 1.2543/1.2546 =(1.2548-1.2546)*10000000=

Financial Management in IB Exercises I. Foreign Exchange Market Locational Arbitrage Paris Interbank market: EUR/USD 1.2548/1.2552 London Interbank market: EUR/USD 1.2543/1.2546 =(1.2548-1.2546)*10000000=

International Parity Conditions

International Parity Conditions Eiteman et al., Chapter 6 Winter 2004 Outline of the Chapter How are exchange rates determined? Can we predict them? Prices and Exchange Rates Prices Indices Inflation Rates

International Parity Conditions Eiteman et al., Chapter 6 Winter 2004 Outline of the Chapter How are exchange rates determined? Can we predict them? Prices and Exchange Rates Prices Indices Inflation Rates

University of Colorado at Boulder. Department of Economics. ECON 4423: INTERNATIONAL FINANCE Term Test 2 Fall 2005

University of Colorado at Boulder Department of Economics ECON 4423: INTERNATIONAL FINANCE Term Test 2 Fall 2005 Name: Student ID: Instructions: This test is 1 hour in length. You may use a hand calculator

University of Colorado at Boulder Department of Economics ECON 4423: INTERNATIONAL FINANCE Term Test 2 Fall 2005 Name: Student ID: Instructions: This test is 1 hour in length. You may use a hand calculator

BBK3273 International Finance

BBK3273 International Finance Prepared by Dr Khairul Anuar L1: Foreign Exchange Market www.lecturenotes638.wordpress.com Contents 1. Foreign Exchange Market 2. History of Foreign Exchange 3. Size of the

BBK3273 International Finance Prepared by Dr Khairul Anuar L1: Foreign Exchange Market www.lecturenotes638.wordpress.com Contents 1. Foreign Exchange Market 2. History of Foreign Exchange 3. Size of the

STRATEGIC FINANCIAL MANAGEMENT FOREX & OTC Derivatives Summary By CA. Gaurav Jain

1 SFM STRATEGIC FINANCIAL MANAGEMENT FOREX & OTC Derivatives Summary By CA. Gaurav Jain 100% Conceptual Coverage With Live Trading Session Complete Coverage of Study Material, Practice Manual & Previous

1 SFM STRATEGIC FINANCIAL MANAGEMENT FOREX & OTC Derivatives Summary By CA. Gaurav Jain 100% Conceptual Coverage With Live Trading Session Complete Coverage of Study Material, Practice Manual & Previous

Global Finance : PPP, IFE, IRP Project

Global Finance : PPP, IFE, IRP Project JRL 咨询公司 (JRL Consulting) 科技管理职场发展咨询电邮 : tech@jrleeconsulting.com 网站 : www.jrleeconsulting.com Two countries (Canada and Japan) were selected for this exercise to

Global Finance : PPP, IFE, IRP Project JRL 咨询公司 (JRL Consulting) 科技管理职场发展咨询电邮 : tech@jrleeconsulting.com 网站 : www.jrleeconsulting.com Two countries (Canada and Japan) were selected for this exercise to

FIN 684 Fixed-Income Analysis Swaps

FIN 684 Fixed-Income Analysis Swaps Professor Robert B.H. Hauswald Kogod School of Business, AU Swap Fundamentals In a swap, two counterparties agree to a contractual arrangement wherein they agree to

FIN 684 Fixed-Income Analysis Swaps Professor Robert B.H. Hauswald Kogod School of Business, AU Swap Fundamentals In a swap, two counterparties agree to a contractual arrangement wherein they agree to

100% Coverage with Practice Manual and last 12 attempts Exam Papers solved in CLASS

1 2 3 4 5 6 FOREIGN EXCHANGE RISK MANAGEMENT (FOREX) + OTC Derivative Concept No. 1: Introduction Three types of transactions in FOREX market which associates two types of risks: 1. Loans(ECB) 2. Investments

1 2 3 4 5 6 FOREIGN EXCHANGE RISK MANAGEMENT (FOREX) + OTC Derivative Concept No. 1: Introduction Three types of transactions in FOREX market which associates two types of risks: 1. Loans(ECB) 2. Investments

Session 13. Exchange Rate Risk

Session 13 Exchange Rate Risk Programme : Executive Diploma in Accounting, Business & Strategy (EDABS 2017) Course : Corporate Financial Management (EDABS 202) Lecturer : Mr. Asanka Ranasinghe MBA (Colombo),

Session 13 Exchange Rate Risk Programme : Executive Diploma in Accounting, Business & Strategy (EDABS 2017) Course : Corporate Financial Management (EDABS 202) Lecturer : Mr. Asanka Ranasinghe MBA (Colombo),

1. Exchange Rates Definition: An exchange rate is a price: The relative price of two currencies.

Rauli Susmel Dept. of Finance Univ. of Houston FINA 4360 International Financial Management International Finance Many of the concepts and techniques are the same as the one used in other Finance classes.

Rauli Susmel Dept. of Finance Univ. of Houston FINA 4360 International Financial Management International Finance Many of the concepts and techniques are the same as the one used in other Finance classes.

ECO 328 SUMMER Sample Questions Topics I.1-3. I.1 National Income Accounting and the Balance of Payments

ECO 328 SUMMER 2004--Sample Questions Topics I.1-3 I.1 National Income Accounting and the Balance of Payments 1. National income equals GNP A. less depreciation, less net unilateral transfers, less indirect

ECO 328 SUMMER 2004--Sample Questions Topics I.1-3 I.1 National Income Accounting and the Balance of Payments 1. National income equals GNP A. less depreciation, less net unilateral transfers, less indirect

Exchange rate: the price of one currency in terms of another. We will be using the notation E t = euro

Econ 330: Money and Banking Fall 2014, Handout 8 Chapter 17 : Foreign Exchange Market 1. Foreign Exchange Market Exchange rate: the price of one currency in terms of another. We will be using the notation

Econ 330: Money and Banking Fall 2014, Handout 8 Chapter 17 : Foreign Exchange Market 1. Foreign Exchange Market Exchange rate: the price of one currency in terms of another. We will be using the notation

Lower prices. Lower costs, esp. wages. Higher productivity. Higher quality/more desirable exports. Greater natural resources. Higher interest rates

1 Goods market Reason to Hold Currency To acquire goods and services from that country Important in... Long run (years to decades) Currency Will Appreciate If... Lower prices Lower costs, esp. wages Higher

1 Goods market Reason to Hold Currency To acquire goods and services from that country Important in... Long run (years to decades) Currency Will Appreciate If... Lower prices Lower costs, esp. wages Higher

Exchange Rates in the Long Run

Exchange Rates in the Long Run What determines exchange rates? Supply + Demand!» Flow models: Demand & supply of FX to purchase goods and services» Stock models, or asset models Demand & supply of available

Exchange Rates in the Long Run What determines exchange rates? Supply + Demand!» Flow models: Demand & supply of FX to purchase goods and services» Stock models, or asset models Demand & supply of available

The Economics of International Financial Crises 4. Foreign Exchange Markets, Interest Rates and Exchange Rate Determination

Fletcher School of Law and Diplomacy, Tufts University The Economics of International Financial Crises 4. Foreign Exchange Markets, Interest Rates and Exchange Rate Determination Prof. George Alogoskoufis

Fletcher School of Law and Diplomacy, Tufts University The Economics of International Financial Crises 4. Foreign Exchange Markets, Interest Rates and Exchange Rate Determination Prof. George Alogoskoufis

Midterm - Economics 160B, Spring 2012 Version A

Name Student ID Section (or TA) Midterm - Economics 160B, Spring 2012 Version A You will have 75 minutes to complete this exam. There are 6 pages and 111 points total. Good luck. Multiple choice: Mark

Name Student ID Section (or TA) Midterm - Economics 160B, Spring 2012 Version A You will have 75 minutes to complete this exam. There are 6 pages and 111 points total. Good luck. Multiple choice: Mark

Chapter 2 Foreign Exchange Parity Relations

Chapter 2 Foreign Exchange Parity Relations Note: In the sixth edition of Global Investments, the exchange rate quotation symbols differ from previous editions. We adopted the convention that the first

Chapter 2 Foreign Exchange Parity Relations Note: In the sixth edition of Global Investments, the exchange rate quotation symbols differ from previous editions. We adopted the convention that the first

Notes on the monetary transmission mechanism in the Czech economy

Notes on the monetary transmission mechanism in the Czech economy Luděk Niedermayer 1 This paper discusses several empirical aspects of the monetary transmission mechanism in the Czech economy. The introduction

Notes on the monetary transmission mechanism in the Czech economy Luděk Niedermayer 1 This paper discusses several empirical aspects of the monetary transmission mechanism in the Czech economy. The introduction

Part I: Forwards. Derivatives & Risk Management. Last Week: Weeks 1-3: Part I Forwards. Introduction Forward fundamentals

Derivatives & Risk Management Last Week: Introduction Forward fundamentals Weeks 1-3: Part I Forwards Forward fundamentals Fwd price, spot price & expected future spot Part I: Forwards 1 Forwards: Fundamentals

Derivatives & Risk Management Last Week: Introduction Forward fundamentals Weeks 1-3: Part I Forwards Forward fundamentals Fwd price, spot price & expected future spot Part I: Forwards 1 Forwards: Fundamentals

INTRODUCTION TO THE FX MARKET MAREN ROMSTAD, BLINDERN, 25 TH MARCH

INTRODUCTION TO THE FX MARKET MAREN ROMSTAD, MRO@NBIM.NO BLINDERN, 25 TH MARCH Agenda Market characteristics Basic theories and models Investment strategies The currency basket of NBIM MARKET CHARACTERISTICS

INTRODUCTION TO THE FX MARKET MAREN ROMSTAD, MRO@NBIM.NO BLINDERN, 25 TH MARCH Agenda Market characteristics Basic theories and models Investment strategies The currency basket of NBIM MARKET CHARACTERISTICS

Introduction to Exchange Rates and the Foreign Exchange Market

Introduction to Exchange Rates and the Foreign Exchange Market 2 1. Refer to the exchange rates given in the following table. Today One Year Ago June 25, 2010 June 25, 2009 Country Per $ Per Per Per $

Introduction to Exchange Rates and the Foreign Exchange Market 2 1. Refer to the exchange rates given in the following table. Today One Year Ago June 25, 2010 June 25, 2009 Country Per $ Per Per Per $

Borrowers Objectives

FIN 463 International Finance Cross-Currency and Interest Rate s Professor Robert Hauswald Kogod School of Business, AU Borrowers Objectives Lower your funding costs: optimal distribution of risks between

FIN 463 International Finance Cross-Currency and Interest Rate s Professor Robert Hauswald Kogod School of Business, AU Borrowers Objectives Lower your funding costs: optimal distribution of risks between

In frictionless markets, freely tradable goods should have the same price anywhere: S = P P $

Prices and Exchange Rates In frictionless markets, freely tradable goods should have the same price anywhere: P $ S = P P $ price in US$ S Exchange rate in yen per dollar P Price in Japanese yen Purchasing

Prices and Exchange Rates In frictionless markets, freely tradable goods should have the same price anywhere: P $ S = P P $ price in US$ S Exchange rate in yen per dollar P Price in Japanese yen Purchasing

INTRODUCTION TO EXCHANGE RATES AND THE FOREIGN EXCHANGE MARKET

INTRODUCTION TO EXCHANGE RATES AND THE FOREIGN EXCHANGE MARKET 13 1 Exchange Rate Essentials 2 Exchange Rates in Practice 3 The Market for Foreign Exchange 4 Arbitrage and Spot Exchange Rates 5 Arbitrage

INTRODUCTION TO EXCHANGE RATES AND THE FOREIGN EXCHANGE MARKET 13 1 Exchange Rate Essentials 2 Exchange Rates in Practice 3 The Market for Foreign Exchange 4 Arbitrage and Spot Exchange Rates 5 Arbitrage

Chapter 19: What Determines Exchange Rates?

Chapter 19: What Determines Exchange Rates? Introduction Exchange rates over time Long-term trends Medium-term trends Short-term variability Frameworks Asset market approach Purchasing power parity (PPP)

Chapter 19: What Determines Exchange Rates? Introduction Exchange rates over time Long-term trends Medium-term trends Short-term variability Frameworks Asset market approach Purchasing power parity (PPP)

Determining Exchange Rates. Determining Exchange Rates

Determining Exchange Rates Determining Exchange Rates Chapter Objectives To explain how exchange rate movements are measured; To explain how the equilibrium exchange rate is determined; and To examine

Determining Exchange Rates Determining Exchange Rates Chapter Objectives To explain how exchange rate movements are measured; To explain how the equilibrium exchange rate is determined; and To examine

International Trade. International Trade, Exchange Rates, and Macroeconomic Policy. International Trade. International Trade. International Trade

, Exchange Rates, and 1 Introduction Open economy macroeconomics International trade in goods and services International capital flows Purchases & sales of foreign assets by domestic residents Purchases

, Exchange Rates, and 1 Introduction Open economy macroeconomics International trade in goods and services International capital flows Purchases & sales of foreign assets by domestic residents Purchases

International Finance

International Finance Agenda Balance of payment Parity conditions in International Finance The foreign exchange market Futures and option markets Swaps and interest derivatives Measuring and managing translation

International Finance Agenda Balance of payment Parity conditions in International Finance The foreign exchange market Futures and option markets Swaps and interest derivatives Measuring and managing translation

8: Relationships among Inflation, Interest Rates, and Exchange Rates

8: Relationships among Inflation, Interest Rates, and Exchange Rates Infl ation rates and interest rates can have a significant impact on exchange rates (as explained in Chapter 4) and therefore can infl

8: Relationships among Inflation, Interest Rates, and Exchange Rates Infl ation rates and interest rates can have a significant impact on exchange rates (as explained in Chapter 4) and therefore can infl

OPTIMTRADER COMMISSIONS

OPTIMTRADER COMMISSIONS Package BASIC OPTIMUM PREMIUM MINIMUM DEPOSIT 5.000 USD or another currency equivalent 10.000 USD another currency equivalent According to the MONTHLY TRADING VOLUME OptimTrader

OPTIMTRADER COMMISSIONS Package BASIC OPTIMUM PREMIUM MINIMUM DEPOSIT 5.000 USD or another currency equivalent 10.000 USD another currency equivalent According to the MONTHLY TRADING VOLUME OptimTrader

Chapter 10. The Foreign Exchange Market

Chapter 10 The Foreign Exchange Market Why Is The Foreign Exchange Market Important? The foreign exchange market 1. is used to convert the currency of one country into the currency of another 2. provides

Chapter 10 The Foreign Exchange Market Why Is The Foreign Exchange Market Important? The foreign exchange market 1. is used to convert the currency of one country into the currency of another 2. provides

The renminbi as a global currency. By Zsanett Sütő

The renminbi as a global currency By Zsanett Sütő On 1 October 2016, the Chinese renminbi (yuan, CNY) was added to the SDR basket that comprises of the leading currencies of the world. This is also in

The renminbi as a global currency By Zsanett Sütő On 1 October 2016, the Chinese renminbi (yuan, CNY) was added to the SDR basket that comprises of the leading currencies of the world. This is also in

Open Economy Macroeconomics Lecture Notes

Open Economy Macroeconomics Lecture Notes Open Economy Macroeconomics Ozan Hatipoglu Department of Economics, Bogazici University Spring 2014 Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics

Open Economy Macroeconomics Lecture Notes Open Economy Macroeconomics Ozan Hatipoglu Department of Economics, Bogazici University Spring 2014 Ozan Hatipoglu (Department of Economics) Open Economy Macroeconomics

Josef Taušer Associate Professor Office Hours: See ISIS

University of Economics Prague Department of International Trade Josef Taušer Associate Professor Office Hours: See ISIS Email: tauser@vse.cz 1 Financial Management in IB Content: 1. Foreign Exchange Markets

University of Economics Prague Department of International Trade Josef Taušer Associate Professor Office Hours: See ISIS Email: tauser@vse.cz 1 Financial Management in IB Content: 1. Foreign Exchange Markets

Foreign Exchange Interventions and the Growth of FX Reserves: Diversification Potential?

Adam Smith Seminars: 2016 AND BEYOND: WORLD ECONOMIC PROSPECTS (III) Foreign Exchange Interventions and the Growth of FX Reserves: Diversification Potential? Lubomír Lízal, Ph.D. Budapest, November 9,

Adam Smith Seminars: 2016 AND BEYOND: WORLD ECONOMIC PROSPECTS (III) Foreign Exchange Interventions and the Growth of FX Reserves: Diversification Potential? Lubomír Lízal, Ph.D. Budapest, November 9,

THE FOREIGN EXCHANGE MARKET

THE FOREIGN EXCHANGE MARKET 1. The Structure of the Market The foreign exchange market is an example of a speculative auction market that has the same "commodity" traded virtually continuously around the

THE FOREIGN EXCHANGE MARKET 1. The Structure of the Market The foreign exchange market is an example of a speculative auction market that has the same "commodity" traded virtually continuously around the

Introduction to Foreign Exchange Slides for International Finance (KOMIF Chapter 3)

") Slides for International Finance (KOMIF Chapter 3) American University 2017-09-14 Preview Introduction to Exchange Rates Basic exchange rate concepts Exchange rates and the cost of foreign goods The foreign

Slides for International Finance (KOMIF Chapter 3) American University 2017-09-14 Preview Introduction to Exchange Rates Basic exchange rate concepts Exchange rates and the cost of foreign goods The foreign

Economics 3422 Sample Midterm examination. Part A: Multiple-choice questions. Choose the best alternative. The total for Part A is 25 points.

Economics 3422 Sample Midterm examination Instruction: Put your name and PeopleSoft ID on the question sheets and the blue book. Put your answers in the blue book only. Turn in both at the end of the examination.

Economics 3422 Sample Midterm examination Instruction: Put your name and PeopleSoft ID on the question sheets and the blue book. Put your answers in the blue book only. Turn in both at the end of the examination.

Rutgers University Spring Econ 336 International Balance of Payments Professor Roberto Chang. Problem Set 2. Deadline: March 1st.

Rutgers University Spring 2012 Econ 336 International Balance of Payments Professor Roberto Chang Problem Set 2. Deadline: March 1st Name: 1. The law of one price works under some assumptions. Which of

Rutgers University Spring 2012 Econ 336 International Balance of Payments Professor Roberto Chang Problem Set 2. Deadline: March 1st Name: 1. The law of one price works under some assumptions. Which of

GLOSSARY Absolute form of purchasing power parity Accounting exposure Appreciation Asian dollar market Ask price

GLOSSARY Absolute form of purchasing power parity Also called the law of one price, this theory suggests that prices of two products of different countries should be equal when measured by a common currency.

GLOSSARY Absolute form of purchasing power parity Also called the law of one price, this theory suggests that prices of two products of different countries should be equal when measured by a common currency.

Chapter 18 Exchange Rate Theories (modified version)

") Chapter 18 Exchange Rate Theories (modified version) Topics to be covered Exchange Rate Determination 1. The Elasticities Approach 2. The Asset Approach 2a. The Monetary Approach to the Exchange Rate 2b.

Chapter 18 Exchange Rate Theories (modified version) Topics to be covered Exchange Rate Determination 1. The Elasticities Approach 2. The Asset Approach 2a. The Monetary Approach to the Exchange Rate 2b.

Chapter 16. Price Levels and the Exchange Rate in the Long Run

Chapter 16 Price Levels and the Exchange Rate in the Long Run Preview Law of one price Purchasing power parity Long-run model of exchange rates: monetary approach (based on absolute version of PPP) Relationship

Chapter 16 Price Levels and the Exchange Rate in the Long Run Preview Law of one price Purchasing power parity Long-run model of exchange rates: monetary approach (based on absolute version of PPP) Relationship

Cover Pool ( mn.) 13, , , , , ,465.0 of which derivatives ( mn.)

13, , , , , ,465.0 of which derivatives ( mn.)") Landesbank Baden-Wuerttemberg Am Hauptbahnhof 2 D-70173 Stuttgart, Germany Phone: +49 711 127-0 Fax: +49 711 127-43544 e-m: kontakt@lbbw.de Internet: www.lbbw.de Publication according to section 28 para.

Landesbank Baden-Wuerttemberg Am Hauptbahnhof 2 D-70173 Stuttgart, Germany Phone: +49 711 127-0 Fax: +49 711 127-43544 e-m: kontakt@lbbw.de Internet: www.lbbw.de Publication according to section 28 para.

Portfolio balanceapproachand the interest rateparity

Portfolio balanceapproachand the interest rateparity dr hab. Bartłomiej Rokicki Chair of Macroeconomics and International Trade Theory Faculty of conomic Sciences, University of Warsaw Rate of return from

Portfolio balanceapproachand the interest rateparity dr hab. Bartłomiej Rokicki Chair of Macroeconomics and International Trade Theory Faculty of conomic Sciences, University of Warsaw Rate of return from

Problems involving Foreign Exchange Solutions

Problems involving Foreign Exchange Solutions 1. A bank quotes the following rates: CHF/USD 1.0898-1.0910 and JPY/USD 119 121. What is the minimum JPY/CHF bid and the maximum ask rate that the bank would

Problems involving Foreign Exchange Solutions 1. A bank quotes the following rates: CHF/USD 1.0898-1.0910 and JPY/USD 119 121. What is the minimum JPY/CHF bid and the maximum ask rate that the bank would

INFLATION-ADJUSTED BOND PORTFOLIO

QUARTERLY REPORT March 31, 2017 MFS INFLATION-ADJUSTED BOND PORTFOLIO MFS Variable Insurance Trust III PORTFOLIO OF INVESTMENTS 3/31/17 (unaudited) The Portfolio of Investments is a complete list of all

QUARTERLY REPORT March 31, 2017 MFS INFLATION-ADJUSTED BOND PORTFOLIO MFS Variable Insurance Trust III PORTFOLIO OF INVESTMENTS 3/31/17 (unaudited) The Portfolio of Investments is a complete list of all

Purchasing Power Parity (PPP) and Real Exchange Rates (RER)

and Real Exchange Rates (RER)") Purchasing Power Parity (PPP) and Real Exchange Rates (RER) Abstract: In this article, we introduce the Purchasing Power Parity, a theory that stipulates that in the long run, the exchange rate between

Purchasing Power Parity (PPP) and Real Exchange Rates (RER) Abstract: In this article, we introduce the Purchasing Power Parity, a theory that stipulates that in the long run, the exchange rate between

Effective for transactions prior to 30 May 2011 Commission rates

Effective for transactions prior to 30 May 2011 Commission rates Commission for share CFDs for New Zealand residents Country of share CFD Rate Minimum Australia 0.10% AUD $7 Canada 2 cents per share CFD

Effective for transactions prior to 30 May 2011 Commission rates Commission for share CFDs for New Zealand residents Country of share CFD Rate Minimum Australia 0.10% AUD $7 Canada 2 cents per share CFD

1 The Structure of the Market

The Foreign Exchange Market 1 The Structure of the Market The foreign exchange market is an example of a speculative auction market that trades the money of various countries continuously around the world.

The Foreign Exchange Market 1 The Structure of the Market The foreign exchange market is an example of a speculative auction market that trades the money of various countries continuously around the world.

Name Student ID Summer Session II Midterm ECON160B There are 7 pages and 100 points. You have 100 minutes to complete the exam.

Name Student ID Summer Session II 2013 Midterm ECON160B There are 7 pages and 100 points. You have 100 minutes to complete the exam. Multiple Choice Choose the best answer. (2.5 points each, 30 points

Name Student ID Summer Session II 2013 Midterm ECON160B There are 7 pages and 100 points. You have 100 minutes to complete the exam. Multiple Choice Choose the best answer. (2.5 points each, 30 points

Introduction to Foreign Exchange. Education Module: 1

Introduction to Foreign Exchange Education Module: 1 Dated July 2002 Part 1 Spot Market Definition of a Foreign Exchange Rate A foreign exchange rate is the price at which one currency can be bought or

Introduction to Foreign Exchange Education Module: 1 Dated July 2002 Part 1 Spot Market Definition of a Foreign Exchange Rate A foreign exchange rate is the price at which one currency can be bought or

In this chapter, we study a theory of how exchange rates are determined "in the long run." The theory we will develop has two parts:

1. INTRODUCTION 1 Introduction In the last chapter, uncovered interest parity (UIP) provided us with a theory of how the spot exchange rate is determined, given knowledge of three variables: the expected

1. INTRODUCTION 1 Introduction In the last chapter, uncovered interest parity (UIP) provided us with a theory of how the spot exchange rate is determined, given knowledge of three variables: the expected

Types of Exposure. Forward Market Hedge. Transaction Exposure. Forward Market Hedge. Forward Market Hedge: an Example INTERNATIONAL FINANCE.

Types of Exposure INTERNATIONAL FINANCE Chapter 8 Transaction exposure sensitivity of realized domestic currency values of the firm s contractual cash flows denominated in foreign currencies to unexpected

Types of Exposure INTERNATIONAL FINANCE Chapter 8 Transaction exposure sensitivity of realized domestic currency values of the firm s contractual cash flows denominated in foreign currencies to unexpected

Management of Transaction Exposure

INTERNATIONAL FINANCIAL MANAGEMENT Seventh Edition EUN / RESNICK Management of Transaction Exposure 8 Chapter Eight INTERNATIONAL Chapter Objective: FINANCIAL MANAGEMENT This chapter discusses various

INTERNATIONAL FINANCIAL MANAGEMENT Seventh Edition EUN / RESNICK Management of Transaction Exposure 8 Chapter Eight INTERNATIONAL Chapter Objective: FINANCIAL MANAGEMENT This chapter discusses various

Investment Management FX markets and International Portfolio Management

Investment Management FX markets and International Portfolio Management Road Map International portfolio diversification Home bias FX risk FX markets Spot and forward/futures FX rates FX parities Hedging

Investment Management FX markets and International Portfolio Management Road Map International portfolio diversification Home bias FX risk FX markets Spot and forward/futures FX rates FX parities Hedging

Is the real dollar rate highly volatile? Abstract

Is the real dollar rate highly volatile? Stefan Norrbin Florida State University Onsurang Pipatchaipoom Samford University Abstract This note updates the real exchange rate behavior observed by Lothian

Is the real dollar rate highly volatile? Stefan Norrbin Florida State University Onsurang Pipatchaipoom Samford University Abstract This note updates the real exchange rate behavior observed by Lothian

Management of Transaction Exposure

INTERNATIONAL FINANCIAL MANAGEMENT Seventh Edition EUN / RESNICK 8-0 Copyright 2015 by The McGraw-Hill Companies, Inc. All rights reserved. Management of Transaction Exposure 8 Chapter Eight INTERNATIONAL

INTERNATIONAL FINANCIAL MANAGEMENT Seventh Edition EUN / RESNICK 8-0 Copyright 2015 by The McGraw-Hill Companies, Inc. All rights reserved. Management of Transaction Exposure 8 Chapter Eight INTERNATIONAL