Gender Inequality in Taxation: The case of Argentina

|

|

|

- Hillary Strickland

- 5 years ago

- Views:

Transcription

1 GEM-IWG Knowledge Networking Program on Engendering Macroeconomics and International Economics Gender Inequality in Taxation: The case of Argentina Corina Rodríguez Enríquez Natalia Gherardi Dario Rossignolo Levy Institute at Bard College July 2009

2 Country and Tax System Overview Medium Income Country Economic growth and fiscal surplus No integrated tax reform: Partial amendments on PIT and VAT Emergency taxes: tax on bank accounts transactions + export duties Medium fiscal revenue level: 25% GDP

3 National Tax Structure

4 Income Tax System Progressive: Income brackets / rates from 11% to 35% Deductions allowed Exemptions: Judges (people in the judiciary system) earnings. Income from capital gains and financial gains. Individual filling, but: Husband should declare jointly-owned assets and all income resulting from jointly owned assets (unless such assets were purchased by the wife with her own earnings or there is a court order for separate administration of the spouses assets)

5 Tax collection differences: Income Tax System Self-employed workers High income earners (autónomos) Individuals earning less than AR$ 7,500/year (US$ 2,380) are tax exempt Deductions available according to applicable regulations Self-employed workers Small income earners (monotributistas) No tax exemption No deductions available Wage earners in formal employment (payroll) Individuals earning less than AR$ 3,400/month (US$ 1,080) are tax exempt Deductions available according to applicable regulations

6 Income Tax Structure Personal Income Tax Payers - By type and sex By Type Men Women N/I Total Self-employed high income 10,1 8,0 69,4 9,4 Self-employed low income 20,9 27,6 30,6 23,2 Wage earners 69,0 64,4 0,0 67,5 Total 100,0 100,0 100,0 100,0 By Sex Men Women N/I Total Self-employed high income 72,5 27,4 0,0 100,0 Self-employed low income 61,1 38,9 0,0 100,0 Wage earners 69,0 31,0 0,0 100,0 Total 67,5 32,5 0,0 100,0

7 Tax deductions Self-employed low income: no deduction available Self-employed high income and wage earners: Personal allowances (Section 23 of Income Tax Law) Self-Employed Wage earners Non Taxable Income Spouse Children (each) Other dependents (each) Special deduction (for income fallin into the third category) Deductions are available both for women and men. Progressivity: deductions decrease with the income level no deduction available over $

8 Gender Bias Explicit Income deriving from joint property to be considered in husband s tax filing. Implicit Self-employed with low income (women are over-represented) are not allowed to take deductions. There is no tax exemption allowed for selfemployed with low income

9 Vertical equity: Operates throught Threshold Decreasing deductions Vertical Equity However: Highest income are exempeted (capital and financial gains) Women are over-represented at lower income levels vertical inequity = gender inequity

10 Horizontal Equity Type of Household Number of members Number of income earners Household annual net income A Two married people, one male provider with two underage children Only the male member has an income B Single-parent household, one female provider with two underage children The female member has an income AR$ 72,000 C Two married people, both have an income, no children Both members earn an income: the male s income is high, the female s income is low

11 Horizontal Equity Type of Household Male Bread-Winner Single-Parent Dual earner Wage Earners man = 2132 / woman = 0 Self-employed High Income man = 4660 / woman = 0 Self-employed Low Income ma n = 900 / woma n = 468 Discrimination by income source (type of employment) Discrimination against single parent households Discrimination against self-employed low income women (though income taxation do not prevent women to enter the labour market) Discrimination against non-married couples

12 Policy Implicantions - PIT There is room to pro-equity reforms in Personal Income Taxation in Argentina: To foster positive implicantions of individual filling to eliminate explicit discrimination against women (regarding treatment of common property within marriage) It would be advisable to include into the tax income law a provision expressly enabling both members of married and nonmarried couples to compute deductions. To eliminate tax exemptions that discriminate against women in a non-direct way. Review deduction system in order to get a more homogenous treatment.

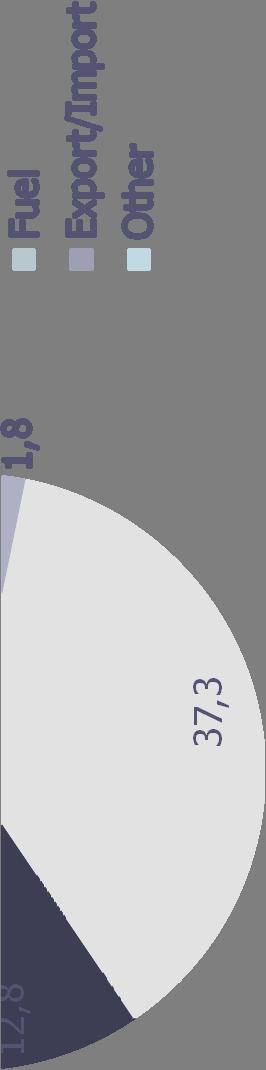

13 VAT: Indirect Taxation Incidence Analysis Taxes every production stage, the difference between credits and debits is paid. Rates: General 21% Reduced rate: 10,50% on meat, fruits and vegetables, bread, passenger transportation Very few exemptions: books, newspapers, water, milk, medicines, educational services; zero rate only on exports Excise taxes: Rates: Alcoholic drinks = 20%; Tobacco = 60%; Electronics = 17% Fuel taxes: All kinds of fuel are taxed, petrol, gasoline, gas-oil, diesel, gas for cars. The tax is not included in the tax base; the tax is the higher between an ad valorem and a tax on quantities consumed

14 Methodology Indicator: Tax as percentage of expenditure Households classification: Employment status Male breadwinner Female breadwinner Dual earner None employed Sex composition (adults) Male majority Female majority Equal number

15 Proportionality; more progressive for male breadwinner and dual earner than for female breadwinner. Higher incidence for male breadwinner and dual earner; and for hhs with no children.

16 Regressivity among Q I and II. Always regressive for female breadwinner hhs.

17 Larger differences between hhs types. Progressive for lower Qs; regressive for higher Qs.

18 Progressivity.

19

20 Gender bias in indirect taxation at the commodity level Female-type hhs: sugar and confectionery nonalcoholic beverages public transportation school transportation Male-type hhs: tobacco alcohol

21

22 Conclusions and Policy Implications Case for more progressive taxation in Argentina. Will possitively affect female breadwinner hhs. While results are not so impressive overall, there are insights at the dissagregated level of analysis (by commodity). Zero and reduced rates on food and basic consumption should be analyzed. More research on intra-hhs resource allocation and decision making needed.

GENDER AND INDIRECT TAX INCIDENCE IN GHANA

GENDER AND INDIRECT TAX INCIDENCE IN GHANA Isaac Osei-Akoto, Robert Darko Osei and Ernest Aryeetey ISSER, University of Ghana 2009 IAFFE ANNUAL CONFERENCE Simmons College Boston, MA, 26-28 June 2009 Data:-

GENDER AND INDIRECT TAX INCIDENCE IN GHANA Isaac Osei-Akoto, Robert Darko Osei and Ernest Aryeetey ISSER, University of Ghana 2009 IAFFE ANNUAL CONFERENCE Simmons College Boston, MA, 26-28 June 2009 Data:-

Indirect Taxation and Gender Equity: Evidence from South Africa

Indirect Taxation and Gender Equity: Evidence from South Africa South African Country Paper January 2009 Daniela Casale School of Development Studies, University of KwaZulu-Natal casaled@ukzn.ac.za Note:Part

Indirect Taxation and Gender Equity: Evidence from South Africa South African Country Paper January 2009 Daniela Casale School of Development Studies, University of KwaZulu-Natal casaled@ukzn.ac.za Note:Part

Briefing on request for VAT exemption on sanitary towels

Briefing on request for VAT exemption on sanitary towels Joint Multi-Party Women s Caucus Presenter: Yanga Mputa/Ismail Momoniat 14 September 2016 1 Tax Policy welcomes invitation National Treasury Budget

Briefing on request for VAT exemption on sanitary towels Joint Multi-Party Women s Caucus Presenter: Yanga Mputa/Ismail Momoniat 14 September 2016 1 Tax Policy welcomes invitation National Treasury Budget

Indirect Taxation and Gender Equity: Evidence from South Africa

Indirect Taxation and Gender Equity: Evidence from South Africa Daniela Casale Working Paper Number 193 September 2010 Acknowledgement: Part of the work emanating from the project has been published in

Indirect Taxation and Gender Equity: Evidence from South Africa Daniela Casale Working Paper Number 193 September 2010 Acknowledgement: Part of the work emanating from the project has been published in

Argentina: A tax reform to promote competitiveness and integration

Argentina: A tax reform to promote competitiveness and integration By Dr. Hugo González Cano Evolution of revenue and the tax burden The tax burden of Argentina, including national, provincial taxes and

Argentina: A tax reform to promote competitiveness and integration By Dr. Hugo González Cano Evolution of revenue and the tax burden The tax burden of Argentina, including national, provincial taxes and

CIE Economics AS-level

CIE Economics AS-level Topic 3: Government Microeconomic Intervention b) Taxes (direct and indirect) Notes Direct Taxes Direct taxes are paid directly to the government from the tax payer. Examples include

CIE Economics AS-level Topic 3: Government Microeconomic Intervention b) Taxes (direct and indirect) Notes Direct Taxes Direct taxes are paid directly to the government from the tax payer. Examples include

The impact of tax and benefit reforms by sex: some simple analysis

The impact of tax and benefit reforms by sex: some simple analysis IFS Briefing Note 118 James Browne The impact of tax and benefit reforms by sex: some simple analysis 1. Introduction 1 James Browne Institute

The impact of tax and benefit reforms by sex: some simple analysis IFS Briefing Note 118 James Browne The impact of tax and benefit reforms by sex: some simple analysis 1. Introduction 1 James Browne Institute

Labor Supply and Taxation in Europe

Labor Supply and Taxation in Europe Fabrizio Colonna - Banca d Italia Stefania Marcassa - Paris School of Economics November 16, 2010 Motivation Observe differences in Female Labor Force Participation

Labor Supply and Taxation in Europe Fabrizio Colonna - Banca d Italia Stefania Marcassa - Paris School of Economics November 16, 2010 Motivation Observe differences in Female Labor Force Participation

TAX INITIATIVES TAX OPTION GRADUATED FLAT COMPETITIVE

Taxation C1 TAX INITIATIVES Major changes to personal income tax policy across Canada became effective for the 2001 tax year. The most important change has been the replacement of the tax-on-tax system

Taxation C1 TAX INITIATIVES Major changes to personal income tax policy across Canada became effective for the 2001 tax year. The most important change has been the replacement of the tax-on-tax system

AQA Economics AS-level

AQA Economics AS-level Macroeconomics Topic 4: Macroeconomic Policy 4.2 Fiscal policy Notes Fiscal policy involves the manipulation of government spending, taxation and the budget balance. It can have

AQA Economics AS-level Macroeconomics Topic 4: Macroeconomic Policy 4.2 Fiscal policy Notes Fiscal policy involves the manipulation of government spending, taxation and the budget balance. It can have

Gender and taxation WHO KNEW? CATHERINE NGINA MUTAVA

Gender and taxation WHO KNEW? CATHERINE NGINA MUTAVA Gender and taxation Gender Refers to the result of social relations that ascribe different roles, rights, responsibilities and obligations to males

Gender and taxation WHO KNEW? CATHERINE NGINA MUTAVA Gender and taxation Gender Refers to the result of social relations that ascribe different roles, rights, responsibilities and obligations to males

Edexcel Economics AS-level

Edexcel Economics AS-level Unit 1: Markets in Action Topic 4: Price Determination 4.4 Indirect taxes and subsidies Notes Indirect Taxes Indirect taxes are imposed by the government and they increase production

Edexcel Economics AS-level Unit 1: Markets in Action Topic 4: Price Determination 4.4 Indirect taxes and subsidies Notes Indirect Taxes Indirect taxes are imposed by the government and they increase production

Finland. Structure and development of tax revenues. National tax systems: Structure and recent developments. Table FI.1: Tax Revenue (% of GDP)

") Finland Structure and development of tax revenues Table FI.1: Tax Revenue (% of GDP) 00 003 004 005 006 007 008 009 010 011 01 013 Ranking Revenue (billion euros) A. Structure by type of tax Indirect taxes

Finland Structure and development of tax revenues Table FI.1: Tax Revenue (% of GDP) 00 003 004 005 006 007 008 009 010 011 01 013 Ranking Revenue (billion euros) A. Structure by type of tax Indirect taxes

Topic # 2: Government Revenues PROF. ANDREEA STOIAN, PHD LECTURE 4

Topic # 2: Government Revenues PROF. ANDREEA STOIAN, PHD LECTURE 4 Content Government Revenues Content Size Changes Composition Factors influencing the size, dynamics and the composition of government

Topic # 2: Government Revenues PROF. ANDREEA STOIAN, PHD LECTURE 4 Content Government Revenues Content Size Changes Composition Factors influencing the size, dynamics and the composition of government

Chapter 12: Design of the Tax System. Historical Context

Chapter 12: Design of the Tax System Purpose: Address the tax system and how the U.S. government raises and spends money along with the difficulty of making a tax system both efficient and equitable. Quick

Chapter 12: Design of the Tax System Purpose: Address the tax system and how the U.S. government raises and spends money along with the difficulty of making a tax system both efficient and equitable. Quick

Tax Reform in Vietnam Issues Need to be Addressed. Nguyen Van Phung Tax Policy Department Ministry of Finance Vietnam

Tax Reform in Vietnam Issues Need to be Addressed Nguyen Van Phung Tax Policy Department Ministry of Finance Vietnam 1 Outline of the Presentation: Overall of the reform of the Vietnamese tax system First

Tax Reform in Vietnam Issues Need to be Addressed Nguyen Van Phung Tax Policy Department Ministry of Finance Vietnam 1 Outline of the Presentation: Overall of the reform of the Vietnamese tax system First

BRIEF STATISTICS 2009

BRIEF STATISTICS 2009 Finnish Tax Administration The Tax Administration is organized under the jurisdiction of the Ministry of Finance. The Tax Administration collects about two-thirds of the taxes and

BRIEF STATISTICS 2009 Finnish Tax Administration The Tax Administration is organized under the jurisdiction of the Ministry of Finance. The Tax Administration collects about two-thirds of the taxes and

2 National tax systems: Structure and recent developments

2 National tax systems: Structure and recent developments United Kingdom Structure and development of tax revenues Table UK.1: Tax Revenue (% of GDP) 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

2 National tax systems: Structure and recent developments United Kingdom Structure and development of tax revenues Table UK.1: Tax Revenue (% of GDP) 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Chapter 12. The Design of the Tax System. Introduction. Introduction. In this chapter, look for the answers to these questions:

Chapter 12. The Design of the Tax System Introduction One of the Ten Principles from Chapter 1: A government can sometimes improve market outcomes. providing public goods regulating use of common resources

Chapter 12. The Design of the Tax System Introduction One of the Ten Principles from Chapter 1: A government can sometimes improve market outcomes. providing public goods regulating use of common resources

3. Work. Number of Employees by Industry and Sex

3. Work Number of Employees by Industry and Sex Labour Force Survey, the Ministry of Internal Affairs and Communications Note: Attention should be paid to the time-line of the data, as, with revision of

3. Work Number of Employees by Industry and Sex Labour Force Survey, the Ministry of Internal Affairs and Communications Note: Attention should be paid to the time-line of the data, as, with revision of

What Gender Equality Advocates Should Know about Taxation

What Gender Equality Advocates Should Know about Taxation Number 7, March 2006 Introduction 1 Considering revenue collection and taxation as a strategy in work for women s rights and poverty alleviation

What Gender Equality Advocates Should Know about Taxation Number 7, March 2006 Introduction 1 Considering revenue collection and taxation as a strategy in work for women s rights and poverty alleviation

Index. Note: Page numbers in italics indicate information contained in tables, graphics or other illustrative material.

Index Note: Page numbers in italics indicate information contained in tables, graphics or other illustrative material. A Husband is not a Retirement Plan report, 336. see also retirement age pension, 11,

Index Note: Page numbers in italics indicate information contained in tables, graphics or other illustrative material. A Husband is not a Retirement Plan report, 336. see also retirement age pension, 11,

The Government and Fiscal Policy

The Government and Fiscal Policy How does the government affect us? Government provide water, electricity, sewerage, education, health services, police and defence force. Some of these are paid for directly

The Government and Fiscal Policy How does the government affect us? Government provide water, electricity, sewerage, education, health services, police and defence force. Some of these are paid for directly

AQA Economics A-level

AQA Economics A-level Macroeconomics Topic 5: Fiscal and Supply Side Policies 5.1 Fiscal policy Notes Fiscal policy involves the manipulation of government spending, taxation and the budget balance. It

AQA Economics A-level Macroeconomics Topic 5: Fiscal and Supply Side Policies 5.1 Fiscal policy Notes Fiscal policy involves the manipulation of government spending, taxation and the budget balance. It

Microeconomics. The Design of the Tax System. Introduction. In this chapter, look for the answers to these questions: N.

C H A P T E R 12 The Design of the Tax System P R I N C I P L E S O F Microeconomics N. Gregory Mankiw Premium PowerPoint Slides by Ron Cronovich 2010 South-Western, a part of Cengage Learning, all rights

C H A P T E R 12 The Design of the Tax System P R I N C I P L E S O F Microeconomics N. Gregory Mankiw Premium PowerPoint Slides by Ron Cronovich 2010 South-Western, a part of Cengage Learning, all rights

The Local Government Pension Scheme (England and Wales) Trivial Commutation. Lump sums paid on or after 1 April 2008

Trivial Commutation. Lump sums paid on or after 1 April 2008") The Local Government Pension Scheme (England and Wales) Trivial Commutation Lump sums paid on or after 1 April 2008 Date: 21 February 2008 Author: Ian Boonin Table of Contents 1 Introduction and Legislative

The Local Government Pension Scheme (England and Wales) Trivial Commutation Lump sums paid on or after 1 April 2008 Date: 21 February 2008 Author: Ian Boonin Table of Contents 1 Introduction and Legislative

Taxation-Overview (Chapter 18)

") (Chapter 18) So far, we have talked about different government expenditure items: Education Social Security Health insurance Welfare programs How does local and federal governments finance such programs?

(Chapter 18) So far, we have talked about different government expenditure items: Education Social Security Health insurance Welfare programs How does local and federal governments finance such programs?

GENDER AND INDIRECT TAX INCIDENCE IN GHANA

GENDER AND INDIRECT TAX INCIDENCE IN GHANA Isaac Osei-Akoto, Robert Darko Osei and Ernest Aryeetey Institute of Statistical, Social and Economic Research (ISSER) University of Ghana Abstract Broad-based

GENDER AND INDIRECT TAX INCIDENCE IN GHANA Isaac Osei-Akoto, Robert Darko Osei and Ernest Aryeetey Institute of Statistical, Social and Economic Research (ISSER) University of Ghana Abstract Broad-based

SOFT DRINK TAXATION: LEGAL CONSIDERATIONS IN INTERNATIONAL AND DOMESTIC LAW. Barbara von Tigerstrom College of Law University of Saskatchewan

SOFT DRINK TAXATION: LEGAL CONSIDERATIONS IN INTERNATIONAL AND DOMESTIC LAW Barbara von Tigerstrom College of Law University of Saskatchewan What are the legal considerations? Domestic law Constitutional

SOFT DRINK TAXATION: LEGAL CONSIDERATIONS IN INTERNATIONAL AND DOMESTIC LAW Barbara von Tigerstrom College of Law University of Saskatchewan What are the legal considerations? Domestic law Constitutional

Taxation in the United Kingdom

BAFUNCS INF 5 (April 2017) BRITISH ASSOCIATION OF FORMER UNITED NATIONS CIVIL SERVANTS Taxation in the United Kingdom (as at 6th April 2017) T axation in the UK is levied in several ways. Income Tax, Capital

BAFUNCS INF 5 (April 2017) BRITISH ASSOCIATION OF FORMER UNITED NATIONS CIVIL SERVANTS Taxation in the United Kingdom (as at 6th April 2017) T axation in the UK is levied in several ways. Income Tax, Capital

Implicit tax rates. 22 nd Statistical Days, Radenci, Peter Štemberger. National accounts SURS

22 nd Statistical Days, Radenci, 2012 Peter Štemberger National accounts SURS Tax burden Taxes and social contributions are the main source of general government revenue. Slovenia, along with the EU, is

22 nd Statistical Days, Radenci, 2012 Peter Štemberger National accounts SURS Tax burden Taxes and social contributions are the main source of general government revenue. Slovenia, along with the EU, is

CHAPTER 7: DATA ANALYSIS

CHAPTER 7: DATA ANALYSIS 7.1 INTRODUCTION The main objective of the current study was to develop a conceptual framework for evaluating the tax burden of individual taxpayers in South Africa. To achieve

CHAPTER 7: DATA ANALYSIS 7.1 INTRODUCTION The main objective of the current study was to develop a conceptual framework for evaluating the tax burden of individual taxpayers in South Africa. To achieve

Guidance on assumptions to use when undertaking a valuation in accordance with Section 179 of the Pensions Act 2004

Contents Part 1 Part 2 Effective date of guidance Overview 2.1 Introduction 2.2 Purpose of this guidance 2.3 Legislative requirements 2.4 Legislation or authority for actuarial valuations Part 3 Financial

Contents Part 1 Part 2 Effective date of guidance Overview 2.1 Introduction 2.2 Purpose of this guidance 2.3 Legislative requirements 2.4 Legislation or authority for actuarial valuations Part 3 Financial

Personal Tax Allowances & Reliefs

RESEARCH PAPER 98/37 18 MARCH 1998 Personal Tax Allowances & Reliefs 1998-99 This paper sets out the main changes to the personal income tax allowances and reliefs announced in the Budget of 17 March 1998.

RESEARCH PAPER 98/37 18 MARCH 1998 Personal Tax Allowances & Reliefs 1998-99 This paper sets out the main changes to the personal income tax allowances and reliefs announced in the Budget of 17 March 1998.

CHAPTER 7 U. S. SOCIAL SECURITY ADMINISTRATION OFFICE OF THE ACTUARY PROJECTIONS METHODOLOGY

CHAPTER 7 U. S. SOCIAL SECURITY ADMINISTRATION OFFICE OF THE ACTUARY PROJECTIONS METHODOLOGY Treatment of Uncertainty... 7-1 Components, Parameters, and Variables... 7-2 Projection Methodologies and Assumptions...

CHAPTER 7 U. S. SOCIAL SECURITY ADMINISTRATION OFFICE OF THE ACTUARY PROJECTIONS METHODOLOGY Treatment of Uncertainty... 7-1 Components, Parameters, and Variables... 7-2 Projection Methodologies and Assumptions...

World Consumer Income and Expenditure Patterns

World Consumer Income and Expenditure Patterns 2011 www.euromonitor.com iii Summary of Contents Contents Summary of Contents Section 1 Introduction 1 Section 2 Socio-economic parameters 21 Section 3 Annual

World Consumer Income and Expenditure Patterns 2011 www.euromonitor.com iii Summary of Contents Contents Summary of Contents Section 1 Introduction 1 Section 2 Socio-economic parameters 21 Section 3 Annual

Contents VALUE ADDED TAX SOUTH AFRICA: /23/2011

VALUE ADDED TAX SOUTH AFRICA: 1991-2011 STANDING COMMITTEE ON FINANCE Presenter: Cecil Morden Chief Director, Tax Policy, National Treasury 23 March 2011 Contents 1. Introduction 2. History of VAT in South

VALUE ADDED TAX SOUTH AFRICA: 1991-2011 STANDING COMMITTEE ON FINANCE Presenter: Cecil Morden Chief Director, Tax Policy, National Treasury 23 March 2011 Contents 1. Introduction 2. History of VAT in South

Hungary. Structure and development of tax revenues. Hungary. Table HU.1: Revenue (% of GDP)

") Structure and development of tax revenues Table HU.1: Revenue (% of GDP) 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 I. Indirect taxes 16.2 15.6 15.1 16.0 15.8 16.6 17.7 17.5 18.8 18.7 VAT 8.8 8.3

Structure and development of tax revenues Table HU.1: Revenue (% of GDP) 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 I. Indirect taxes 16.2 15.6 15.1 16.0 15.8 16.6 17.7 17.5 18.8 18.7 VAT 8.8 8.3

2017 budget. predictions

www.pwc.co.za/budget 2017 budget xxx xxx predictions Tax revenue estimates 2016/17 tax revenues In the 2016 Medium Term Budget Policy Statement (MTBPS), estimates for 2016/17 tax revenues were revised

www.pwc.co.za/budget 2017 budget xxx xxx predictions Tax revenue estimates 2016/17 tax revenues In the 2016 Medium Term Budget Policy Statement (MTBPS), estimates for 2016/17 tax revenues were revised

Goods and Service Tax (GST)

") Goods and Service Tax (GST) 1. Basics of GST 2. Working Model of GST 3. GST Compliances- Monthly and Annual Filings 4. GST Impact on E-Commerce 5. GST Impact on Services ( IT/ITES) BASICS of GST GST is

Goods and Service Tax (GST) 1. Basics of GST 2. Working Model of GST 3. GST Compliances- Monthly and Annual Filings 4. GST Impact on E-Commerce 5. GST Impact on Services ( IT/ITES) BASICS of GST GST is

Annual revenues from Kosovo's value added tax ; [presentation given on February 29, 2012]

![Annual revenues from Kosovo's value added tax ; [presentation given on February 29, 2012]](/thumbs/80/81412825.jpg "Annual revenues from Kosovo's value added tax ; [presentation given on February 29, 2012]") Rochester Institute of Technology RIT Scholar Works Theses Thesis/Dissertation Collections 3-7-2012 Annual revenues from Kosovo's value added tax ; [presentation given on February 29, 2012] Diamanta Skenderi

Rochester Institute of Technology RIT Scholar Works Theses Thesis/Dissertation Collections 3-7-2012 Annual revenues from Kosovo's value added tax ; [presentation given on February 29, 2012] Diamanta Skenderi

Tax policy in Denmark (and EU) Hong Kong 7.September 2013 Jens Holger Helbo Hansen, Ministry of taxation

Hong Kong 7.September 2013 Jens Holger Helbo Hansen, Ministry of taxation") Tax policy in Denmark (and EU) Hong Kong 7.September 2013 Jens Holger Helbo Hansen, Ministry of taxation Introduction Denmark Nordic country Member of EU, NATO etc. Parliamentarian Democracy 5 Regions

Tax policy in Denmark (and EU) Hong Kong 7.September 2013 Jens Holger Helbo Hansen, Ministry of taxation Introduction Denmark Nordic country Member of EU, NATO etc. Parliamentarian Democracy 5 Regions

Toward Active Participation of Women as the Core of Growth Strategies. From the White Paper on Gender Equality Summary

Toward Active Participation of Women as the Core of Growth Strategies From the White Paper on Gender Equality 2013 Summary Cabinet Office, Government of Japan June 2013 The Cabinet annually submits to

Toward Active Participation of Women as the Core of Growth Strategies From the White Paper on Gender Equality 2013 Summary Cabinet Office, Government of Japan June 2013 The Cabinet annually submits to

Choose the single best answer for each question. Do all of your scratch-work in the side and bottom margins of pages.

Econ 101, Sections 3 and 4, S11, Schroeter Exam #3, Special code = 0001 Choose the single best answer for each question. Do all of your scratch-work in the side and bottom margins of pages. 1. A tariff

Econ 101, Sections 3 and 4, S11, Schroeter Exam #3, Special code = 0001 Choose the single best answer for each question. Do all of your scratch-work in the side and bottom margins of pages. 1. A tariff

FOU N-raw DATION. TaN rden on erican Fa es Rises Again. The Growth of Taxatio n. November No. 74

Since 1937 FOU N-raw DATION S"IECIAL November 199 7 No. 74 TaN rden on erican Fa es Rises Again By Claire M. Hintz Senior Economist Tax Foundation In 1997, the tax burden on America' s median income families

Since 1937 FOU N-raw DATION S"IECIAL November 199 7 No. 74 TaN rden on erican Fa es Rises Again By Claire M. Hintz Senior Economist Tax Foundation In 1997, the tax burden on America' s median income families

Personal Income Tax Cuts and the new Child Care Subsidy: Do They Address High Effective Marginal Tax Rates on Women s Work?

Personal Income Tax Cuts and the new Child Care Subsidy: Do They Address High Effective Marginal Tax Rates on Women s Work? Miranda Stewart 1 Summary In Australia s tax and social welfare system, many

Personal Income Tax Cuts and the new Child Care Subsidy: Do They Address High Effective Marginal Tax Rates on Women s Work? Miranda Stewart 1 Summary In Australia s tax and social welfare system, many

Household consumption expenditure Year 2017

19 June 2018 Household consumption expenditure Year 2017 In 2017, the average monthly household consumption expenditure, at current values, was 2,564 euros (+1.6% compared to 2016 and +3.8% compared to

19 June 2018 Household consumption expenditure Year 2017 In 2017, the average monthly household consumption expenditure, at current values, was 2,564 euros (+1.6% compared to 2016 and +3.8% compared to

Social Security: Is a Key Foundation of Economic Security Working for Women?

Committee on Finance United States Senate Hearing on Social Security: Is a Key Foundation of Economic Security Working for Women? Statement of Janet Barr, MAAA, ASA, EA on behalf of the American Academy

Committee on Finance United States Senate Hearing on Social Security: Is a Key Foundation of Economic Security Working for Women? Statement of Janet Barr, MAAA, ASA, EA on behalf of the American Academy

Widening of income tax free bracket and conditions for parent rates tax computations

Highlights The measures announced tonight by the Minister of Finance in the budget speech for 2014 include: Reductions in W&E rates as from March 2014 for individuals and as from 2015 for businesses Widening

Highlights The measures announced tonight by the Minister of Finance in the budget speech for 2014 include: Reductions in W&E rates as from March 2014 for individuals and as from 2015 for businesses Widening

The Local Government Pension Scheme (Scotland) Trivial Commutation. Lump Sums paid on or after 18 January 2012

Trivial Commutation. Lump Sums paid on or after 18 January 2012") The Local Government Pension Scheme (Scotland) Trivial Commutation Lump Sums paid on or after 18 January 2012 Date: 18 January 2012 Author: Ken Kneller Table of Contents 1 Introduction... 2 2 Commutation

The Local Government Pension Scheme (Scotland) Trivial Commutation Lump Sums paid on or after 18 January 2012 Date: 18 January 2012 Author: Ken Kneller Table of Contents 1 Introduction... 2 2 Commutation

Chapter 16 Indirect Taxation

Chapter 16 Indirect Taxation www.pwc.com/mt/doingbusiness Doing Business in Malta INDIRECT TAXES IN MALTA Value added tax (VAT) is charged on supplies of goods and services made in Malta, on intra-community

Chapter 16 Indirect Taxation www.pwc.com/mt/doingbusiness Doing Business in Malta INDIRECT TAXES IN MALTA Value added tax (VAT) is charged on supplies of goods and services made in Malta, on intra-community

NCPI. August Namibia Consumer Price index. Namibia Consumer Price index - August

NCPI Namibia Consumer Price index August 2018 Namibia Consumer Price index - August 2018 1 Mission Statement Leveraging on partnerships and innovative technologies, to produce and disseminate relevant,

NCPI Namibia Consumer Price index August 2018 Namibia Consumer Price index - August 2018 1 Mission Statement Leveraging on partnerships and innovative technologies, to produce and disseminate relevant,

Household Income Distribution and Working Time Patterns. An International Comparison

Household Income Distribution and Working Time Patterns. An International Comparison September 1998 D. Anxo & L. Flood Centre for European Labour Market Studies Department of Economics Göteborg University.

Household Income Distribution and Working Time Patterns. An International Comparison September 1998 D. Anxo & L. Flood Centre for European Labour Market Studies Department of Economics Göteborg University.

DIVISION - I. 2. Basic Concepts of Excise Duty Basic Concepts of Customs Duty Basic Concepts of VAT Basic Concepts of CST 146

Contents DIVISION - I 1. Basic Concepts of Indirect Taxes 1 2. Basic Concepts of Excise Duty 11 3. Basic Concepts of Customs Duty 63 4. Basic Concepts of VAT 101 5. Basic Concepts of CST 146 DIVISION -

Contents DIVISION - I 1. Basic Concepts of Indirect Taxes 1 2. Basic Concepts of Excise Duty 11 3. Basic Concepts of Customs Duty 63 4. Basic Concepts of VAT 101 5. Basic Concepts of CST 146 DIVISION -

The Local Government Pension Scheme (England & Wales) Trivial Commutation. Lump Sums paid on or after 30 November 2011

Trivial Commutation. Lump Sums paid on or after 30 November 2011") The Local Government Pension Scheme (England & Wales) Trivial Commutation Lump Sums paid on or after 30 November 2011 Date: 21 November 2012 Author: Ian Boonin Table of Contents 1 Introduction... 2 2 Commutation

The Local Government Pension Scheme (England & Wales) Trivial Commutation Lump Sums paid on or after 30 November 2011 Date: 21 November 2012 Author: Ian Boonin Table of Contents 1 Introduction... 2 2 Commutation

State of Palestine Ministry of Finance. Fiscal Developments & Macroeconomic Performance: Fourth Quarter and Full year 2013 Report

State of Palestine Ministry of Finance Fiscal Developments & Macroeconomic Performance: Fourth Quarter and Full year 2013 Report Macro Macro Fiscal Fiscal Unit Unit Oct February,, 2013 2014 Section 1:

State of Palestine Ministry of Finance Fiscal Developments & Macroeconomic Performance: Fourth Quarter and Full year 2013 Report Macro Macro Fiscal Fiscal Unit Unit Oct February,, 2013 2014 Section 1:

Overview of the Federal Tax System

Overview of the Federal Tax System Molly F. Sherlock Specialist in Public Finance Donald J. Marples Specialist in Public Finance May 16, 2013 CRS Report for Congress Prepared for Members and Committees

Overview of the Federal Tax System Molly F. Sherlock Specialist in Public Finance Donald J. Marples Specialist in Public Finance May 16, 2013 CRS Report for Congress Prepared for Members and Committees

CAMEROON GENERAL CERTIFICATE OF EDUCATION BOARD General Certificate of Education Examination 0525 ECONOMICS 1

CAMEROON GENERAL CERTIFICATE OF EDUCATION BOARD General Certificate of Education Examination 0525 ECONOMICS 1 JUNE 2017 ORDINARY LEVEL Centre Number Centre Name Candidate Identification No. Candidate Name

CAMEROON GENERAL CERTIFICATE OF EDUCATION BOARD General Certificate of Education Examination 0525 ECONOMICS 1 JUNE 2017 ORDINARY LEVEL Centre Number Centre Name Candidate Identification No. Candidate Name

7409 Market Street Wilmington, NC 28411

Demographic Report 7409 Market Street Employment by Distance Distance Employed Unemployed Unemployment Rate 1-Mile 2,517 104 1.03 % 3-Mile 17,506 713 3.26 % 5-Mile 33,297 1,385 4.05 % Labor & Income Agriculture

Demographic Report 7409 Market Street Employment by Distance Distance Employed Unemployed Unemployment Rate 1-Mile 2,517 104 1.03 % 3-Mile 17,506 713 3.26 % 5-Mile 33,297 1,385 4.05 % Labor & Income Agriculture

OCR Economics AS-level

OCR Economics AS-level Macroeconomics Topic 3: Application of Policy Instruments 3.1 Fiscal policy Notes The government budget: The government budget is comprised of tax revenues and government expenditure.

OCR Economics AS-level Macroeconomics Topic 3: Application of Policy Instruments 3.1 Fiscal policy Notes The government budget: The government budget is comprised of tax revenues and government expenditure.

METHODOLOGY. Who Pays? A Distributional Analysis of the Tax Systems in All 50 States, 6th Edition

METHODOLOGY The Institute on Taxation & Economic Policy has engaged in research on tax issues since 1980, with a focus on the distributional consequences of both current law and proposed changes. Much

METHODOLOGY The Institute on Taxation & Economic Policy has engaged in research on tax issues since 1980, with a focus on the distributional consequences of both current law and proposed changes. Much

Outline of presentation. National Accounts Office September 2016 Chiba, Japan

25-27 September 2016 Chiba, Japan National Accounts Office Office of the National Economic and Social Development Board (NESDB) Outline of presentation Short Term Indicator Quarterly Gross Domestic Product

25-27 September 2016 Chiba, Japan National Accounts Office Office of the National Economic and Social Development Board (NESDB) Outline of presentation Short Term Indicator Quarterly Gross Domestic Product

PERSONAL INCOME TAXES

PERSONAL INCOME TAXES CHAPTER 35 WHERE PERSONAL INCOME TAXES FIT In 2008 the federal government collected $2,524 billion in taxes. $1,146 billion of that was collected from the personal income tax. The

PERSONAL INCOME TAXES CHAPTER 35 WHERE PERSONAL INCOME TAXES FIT In 2008 the federal government collected $2,524 billion in taxes. $1,146 billion of that was collected from the personal income tax. The

ON THE SCALES 7 OF 2018 NATIONAL BUDGET 2018

ON THE SCALES 7 OF 2018 NATIONAL BUDGET 2018 On 21 February 2018, Minister Malusi Gigaba presented his National Budget speech. The speech was presented within a framework of renewal, hope and optimism,

ON THE SCALES 7 OF 2018 NATIONAL BUDGET 2018 On 21 February 2018, Minister Malusi Gigaba presented his National Budget speech. The speech was presented within a framework of renewal, hope and optimism,

THE IMPACT OF TAXES AND EXPENDITURES ON POVERTY AND INCOME DISTRIBUTION IN ARGENTINA

Rossignolo, WP 45, May 2017 THE IMPACT OF TAXES AND EXPENDITURES ON POVERTY AND INCOME DISTRIBUTION IN ARGENTINA Dario Rossignolo Working Paper 45 November 2016 (Revised June 2017) 1 The CEQ Working Paper

Rossignolo, WP 45, May 2017 THE IMPACT OF TAXES AND EXPENDITURES ON POVERTY AND INCOME DISTRIBUTION IN ARGENTINA Dario Rossignolo Working Paper 45 November 2016 (Revised June 2017) 1 The CEQ Working Paper

CHAPTER 17: PUBLIC CHOICE THEORY AND THE ECONOMICS OF TAXATION

CHAPTER 17: PUBLIC CHOICE THEORY AND THE ECONOMICS OF TAXATION Introduction As we have seen, government plays an important role in addressing market failures. But it also plays a significant role in taxation

CHAPTER 17: PUBLIC CHOICE THEORY AND THE ECONOMICS OF TAXATION Introduction As we have seen, government plays an important role in addressing market failures. But it also plays a significant role in taxation

Note: The following exam was created for use with Hird, Working with Economics: A Canadian Framework, Sixth Edition.

Macroeconomics Final Examination Note: The following exam was created for use with Hird, Working with Economics: A Canadian Framework, Sixth Edition. Part A: Multiple Choice Each Question is worth 1 mark

Macroeconomics Final Examination Note: The following exam was created for use with Hird, Working with Economics: A Canadian Framework, Sixth Edition. Part A: Multiple Choice Each Question is worth 1 mark

Daniel Jung CRENSHAW BLVD CRENSHAW BLVD INGLEWOOD CA, CA Priming Capital 6 Centerpointe Dr La Palma, CA

11225 CRENSHAW BLVD 11225 CRENSHAW BLVD INGLEWOOD CA, CA 90303 Property Type Retail Building Size Owner (Legal) Property Subtype Auto Dealer Office SF Owner (True) Zoning Industrial SF County Los Angeles

11225 CRENSHAW BLVD 11225 CRENSHAW BLVD INGLEWOOD CA, CA 90303 Property Type Retail Building Size Owner (Legal) Property Subtype Auto Dealer Office SF Owner (True) Zoning Industrial SF County Los Angeles

THE IMPACT OF TAXES AND EXPENDITURES ON POVERTY AND INCOME DISTRIBUTION IN ARGENTINA

THE IMPACT OF TAXES AND EXPENDITURES ON POVERTY AND INCOME DISTRIBUTION IN ARGENTINA Dario Rossignolo Working Paper 45 November 2016 1 The CEQ Working Paper Series The CEQ Institute at Tulane University

THE IMPACT OF TAXES AND EXPENDITURES ON POVERTY AND INCOME DISTRIBUTION IN ARGENTINA Dario Rossignolo Working Paper 45 November 2016 1 The CEQ Working Paper Series The CEQ Institute at Tulane University

4.1 Major Tax Categories for FIEs and Foreigners

4.1 Major Tax Categories for FIEs and Foreigners 4.1.1 Value-Added Tax As a type of turnover tax, value-added tax (VAT) is levied on the increased value of commodities at different stages of production

4.1 Major Tax Categories for FIEs and Foreigners 4.1.1 Value-Added Tax As a type of turnover tax, value-added tax (VAT) is levied on the increased value of commodities at different stages of production

Poverty After 50 in Canada: A Recent Snapshot

Poverty After 50 in Canada: A Recent Snapshot Mayssun El-Attar 1 Raquel Fonseca 2 1 McGill University and Industrial Alliance Research Chair on the Economics of Demographic Change 2 ESG-Université du Québec

Poverty After 50 in Canada: A Recent Snapshot Mayssun El-Attar 1 Raquel Fonseca 2 1 McGill University and Industrial Alliance Research Chair on the Economics of Demographic Change 2 ESG-Université du Québec

At IBISWorld, we know that industry intelligence is more than assembling facts: It's combining data and insight to answer the questions that

At IBISWorld, we know that industry intelligence is more than assembling facts: It's combining data and insight to answer the questions that successful businesses ask IBISWorld Australia Business Environment

At IBISWorld, we know that industry intelligence is more than assembling facts: It's combining data and insight to answer the questions that successful businesses ask IBISWorld Australia Business Environment

axes in Sweden TA summary of the Tax Statistical Yearbook of Sweden

axes in Sweden TA summary of the Tax Statistical Yearbook of Sweden 2002 1 Taxes in Sweden 2002 A summary of the Tax Statistical Yearbook of Sweden 2002 National Tax Board 2 PREFACE 3 Preface The Swedish

axes in Sweden TA summary of the Tax Statistical Yearbook of Sweden 2002 1 Taxes in Sweden 2002 A summary of the Tax Statistical Yearbook of Sweden 2002 National Tax Board 2 PREFACE 3 Preface The Swedish

of budget measures James Browne Institute for Fiscal Studies

Personal taxes and distributional impact of budget measures James Browne What s coming up Pre-announced changes Yesterday s announcements Income tax VAT Distributional ib i impact of measures Tax rises

Personal taxes and distributional impact of budget measures James Browne What s coming up Pre-announced changes Yesterday s announcements Income tax VAT Distributional ib i impact of measures Tax rises

Understanding the Consumer Price Index (CPI)

") ESO PUBLICATIONS Consumer Price Index (CPI) Reports Quarterly Economic Reports (QER) Labour Force Survey (LFS) Reports Annual Overseas Trade Reports Annual Compendium of Statistics Annual Economics Report

ESO PUBLICATIONS Consumer Price Index (CPI) Reports Quarterly Economic Reports (QER) Labour Force Survey (LFS) Reports Annual Overseas Trade Reports Annual Compendium of Statistics Annual Economics Report

The Local Government Pension Scheme. Liability for combined benefits - Regulations 29, 48 and 126

The Local Government Pension Scheme Liability for combined benefits - Regulations 29, 48 and 126 1. Regulation 29 of the Local Government Pension Scheme Regulations 1997 (the LGPS Regulations ) provides

The Local Government Pension Scheme Liability for combined benefits - Regulations 29, 48 and 126 1. Regulation 29 of the Local Government Pension Scheme Regulations 1997 (the LGPS Regulations ) provides

Chapter 6 SUMMARY, CONCLUSIONS AND RECOMMENDATIONS

Chapter 6 SUMMARY, CONCLUSIONS AND RECOMMENDATIONS 6.1. Summary Poverty, inequality and unemployment are realities within the South African economy, and policy intervention is called for. One policy intervention

Chapter 6 SUMMARY, CONCLUSIONS AND RECOMMENDATIONS 6.1. Summary Poverty, inequality and unemployment are realities within the South African economy, and policy intervention is called for. One policy intervention

Universal Credit: The Gender Impact

Universal Credit: The Gender Impact Equality and Diversity Forum Research Network Welfare Reform: Issues and Impacts 12 February 2013 Women s Budget Group Fran Bennett, University of Oxford fran.bennett@spi.ox.ac.uk

Universal Credit: The Gender Impact Equality and Diversity Forum Research Network Welfare Reform: Issues and Impacts 12 February 2013 Women s Budget Group Fran Bennett, University of Oxford fran.bennett@spi.ox.ac.uk

Public Finance: The Economics of Taxation. The Economics of Taxation. Taxes: Basic Concepts

C H A P T E R 16 Public Finance: The Economics of Taxation Prepared by: Fernando Quijano and Yvonn Quijano The Economics of Taxation The primary vehicle that the government uses to finance itself is taxation.

C H A P T E R 16 Public Finance: The Economics of Taxation Prepared by: Fernando Quijano and Yvonn Quijano The Economics of Taxation The primary vehicle that the government uses to finance itself is taxation.

June Economic and budgetary effects of fiscal reforms 2015

June 2015 Economic and budgetary effects of fiscal reforms 2015 2 1. Introduction In March 10, 2014 Government of Kosovo (GoK) decided that from April 1, 2014 wages and salaries of public administration

June 2015 Economic and budgetary effects of fiscal reforms 2015 2 1. Introduction In March 10, 2014 Government of Kosovo (GoK) decided that from April 1, 2014 wages and salaries of public administration

14-1: How Taxes Work NOTES

14-1: How Taxes Work NOTES Learning Target 1. I will demonstrate my understanding of the different types of taxes and what tax revenue is used for. Government Revenue Tax: a mandatory payment to a local,

14-1: How Taxes Work NOTES Learning Target 1. I will demonstrate my understanding of the different types of taxes and what tax revenue is used for. Government Revenue Tax: a mandatory payment to a local,

INTRODUCTION TAXES: EQUITY VS. EFFICIENCY WEALTH PERSONAL INCOME THE LORENZ CURVE THE SIZE DISTRIBUTION OF INCOME

INTRODUCTION Taxes affect production as well as distribution. This creates a potential tradeoff between the goal of equity and the goal of efficiency. The chapter focuses on the following questions: How

INTRODUCTION Taxes affect production as well as distribution. This creates a potential tradeoff between the goal of equity and the goal of efficiency. The chapter focuses on the following questions: How

Human Development Indices and Indicators: 2018 Statistical Update. Argentina

Human Development Indices and Indicators: 2018 Statistical Update Briefing note for countries on the 2018 Statistical Update Introduction Argentina This briefing note is organized into ten sections. The

Human Development Indices and Indicators: 2018 Statistical Update Briefing note for countries on the 2018 Statistical Update Introduction Argentina This briefing note is organized into ten sections. The

High income families. The characteristics of families with low incomes are often studied in detail in order to assist in the

Winter 1994 (Vol. 6, No. 4) Article No. 6 High income families Abdul Rashid The characteristics of families with low incomes are often studied in detail in order to assist in the development of policies

Winter 1994 (Vol. 6, No. 4) Article No. 6 High income families Abdul Rashid The characteristics of families with low incomes are often studied in detail in order to assist in the development of policies

CAYMAN ISLANDS CONSUMER PRICE REPORT: 2010 ANNUAL INFLATION (Date: February 9, 2011)

") CAYMAN ISLANDS CONSUMER PRICE REPORT: 2010 ANNUAL INFLATION (Date: February 9, 2011) Consumer Price Index (CPI) Increased by 0.3% in 2010 This report is a consolidated report of the average CPI in 2010

CAYMAN ISLANDS CONSUMER PRICE REPORT: 2010 ANNUAL INFLATION (Date: February 9, 2011) Consumer Price Index (CPI) Increased by 0.3% in 2010 This report is a consolidated report of the average CPI in 2010

High income earners the big winners from scrapping 37% tax bracket

High income earners the big winners from scrapping 37% tax bracket High income earners will get 80% of the benefit from removing the 37% tax bracket and 60% of taxpayers will get no benefit. By Matt Grudnoff,

High income earners the big winners from scrapping 37% tax bracket High income earners will get 80% of the benefit from removing the 37% tax bracket and 60% of taxpayers will get no benefit. By Matt Grudnoff,

Tax & Legal Alert PwC Hungary Issue 580 July 2017

Tax & Legal Alert PwC Hungary Issue 580 July 2017 On 13 June 2017, the Parliament passed Act LXXVII of 2017 on the amendment of various tax laws. This newsletter summarises the most important changes proposed

Tax & Legal Alert PwC Hungary Issue 580 July 2017 On 13 June 2017, the Parliament passed Act LXXVII of 2017 on the amendment of various tax laws. This newsletter summarises the most important changes proposed

Notes and Definitions Numbers in the text, tables, and figures may not add up to totals because of rounding. Dollar amounts are generally rounded to t

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE The Distribution of Household Income and Federal Taxes, 2013 Percent 70 60 50 Shares of Before-Tax Income and Federal Taxes, by Before-Tax Income

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE The Distribution of Household Income and Federal Taxes, 2013 Percent 70 60 50 Shares of Before-Tax Income and Federal Taxes, by Before-Tax Income

Women and the Economy 2010: 25 Years of Progress But Challenges Remain

Cornell University ILR School DigitalCommons@ILR Federal Publications Key Workplace Documents 8-2010 Women and the Economy 2010: 25 Years of Progress But Challenges Remain U.S. Congress Joint Economic

Cornell University ILR School DigitalCommons@ILR Federal Publications Key Workplace Documents 8-2010 Women and the Economy 2010: 25 Years of Progress But Challenges Remain U.S. Congress Joint Economic

CONVERGENCES IN MEN S AND WOMEN S LIFE PATTERNS: LIFETIME WORK, LIFETIME EARNINGS, AND HUMAN CAPITAL INVESTMENT $

CONVERGENCES IN MEN S AND WOMEN S LIFE PATTERNS: LIFETIME WORK, LIFETIME EARNINGS, AND HUMAN CAPITAL INVESTMENT $ Joyce Jacobsen a, Melanie Khamis b and Mutlu Yuksel c a Wesleyan University b Wesleyan

CONVERGENCES IN MEN S AND WOMEN S LIFE PATTERNS: LIFETIME WORK, LIFETIME EARNINGS, AND HUMAN CAPITAL INVESTMENT $ Joyce Jacobsen a, Melanie Khamis b and Mutlu Yuksel c a Wesleyan University b Wesleyan

AP Microeconomics Chapter 16 Outline

I. Learning objectives In this chapter students should learn: A. The main categories of government spending and the main sources of government revenue. B. The different philosophies regarding the distribution

I. Learning objectives In this chapter students should learn: A. The main categories of government spending and the main sources of government revenue. B. The different philosophies regarding the distribution

PPI PENSIONS POLICY INSTITUTE. The Pensions Primer: A guide to the UK pensions system. Historical Annex

PPI The Pensions Primer: A guide to the UK pensions system Historical Annex The Pensions Primer: a guide to the UK pensions system Historical Annex Introduction 1 First tier: Eligibility for Basic State

PPI The Pensions Primer: A guide to the UK pensions system Historical Annex The Pensions Primer: a guide to the UK pensions system Historical Annex Introduction 1 First tier: Eligibility for Basic State

Taxation in the UK. James Browne. Senior Research Economist Institute for Fiscal Studies

Taxation in the UK James Browne Senior Research Economist Institute for Fiscal Studies Outline Overview of the UK tax system in historical, international and theoretical contexts: 1. Level and composition

Taxation in the UK James Browne Senior Research Economist Institute for Fiscal Studies Outline Overview of the UK tax system in historical, international and theoretical contexts: 1. Level and composition

41% of Palauan women are engaged in paid employment

Palau 2013/2014 HIES Gender profile Executive Summary 34% 18% 56% of Palauan households have a female household head is the average regular cash pay gap for Palauan women in professional jobs of internet

Palau 2013/2014 HIES Gender profile Executive Summary 34% 18% 56% of Palauan households have a female household head is the average regular cash pay gap for Palauan women in professional jobs of internet

Response of the Equality and Human Rights Commission to Consultation:

Response of the Equality and Human Rights Commission to Consultation: Consultation details Title: Source of consultation: The Impact of Economic Reform Policies on Women s Human Rights. To inform the next

Response of the Equality and Human Rights Commission to Consultation: Consultation details Title: Source of consultation: The Impact of Economic Reform Policies on Women s Human Rights. To inform the next

Consumer Price Index. June Business and economy

Consumer Price June 2017 Business and economy Table of Contents A note to the reader...ii 1 MONTHLY CHANGE OF THE CPI... 1 1.1 CPI AND INFLATION... 1 1.2 CHANGES IN SECTOR... 1 1.3 CHANGES IN CATEGORIES

Consumer Price June 2017 Business and economy Table of Contents A note to the reader...ii 1 MONTHLY CHANGE OF THE CPI... 1 1.1 CPI AND INFLATION... 1 1.2 CHANGES IN SECTOR... 1 1.3 CHANGES IN CATEGORIES

Food Price Data from the Ghana Statistical Service: Current methods and updates. Anthony Amuzu-Pharin Ghana Statistical Service 8 Aug 2017 Accra

Food Price Data from the Ghana Statistical Service: Current methods and updates Anthony Amuzu-Pharin Ghana Statistical Service 8 Aug 2017 Accra GSS Mission and purpose regarding data collection Production

Food Price Data from the Ghana Statistical Service: Current methods and updates Anthony Amuzu-Pharin Ghana Statistical Service 8 Aug 2017 Accra GSS Mission and purpose regarding data collection Production

Pension Issues for Women

Pension Issues for Women This bulletin aims to highlight the key areas in Britain s pensions system where women have historically lost out and continue to do so. It will also offer guidance to actions

Pension Issues for Women This bulletin aims to highlight the key areas in Britain s pensions system where women have historically lost out and continue to do so. It will also offer guidance to actions

Productivity: A Workforce Participation Breakdown

ALERA National Conference 2014 Professor Marian Baird marian.baird@sydney.edu.au Productivity: A Workforce Participation Breakdown BUSINESS SCHOOL Game Changers? Closing the gap between male and female

ALERA National Conference 2014 Professor Marian Baird marian.baird@sydney.edu.au Productivity: A Workforce Participation Breakdown BUSINESS SCHOOL Game Changers? Closing the gap between male and female

OCR Economics A-level

OCR Economics A-level Macroeconomics Topic 3: Application of Policy Instruments 3.1 Fiscal policy Notes The government budget: The government budget is comprised of tax revenues and government expenditure.

OCR Economics A-level Macroeconomics Topic 3: Application of Policy Instruments 3.1 Fiscal policy Notes The government budget: The government budget is comprised of tax revenues and government expenditure.