An Overview of Current NonProfit Status as it Relates to the Amateur Radio Community. Lynn T Baxter, CPA WØLTB NEAR-Fest 2016

|

|

|

- Isabella Fox

- 5 years ago

- Views:

Transcription

1 An Overview of Current NonProfit Status as it Relates to the Amateur Radio Community Lynn T Baxter, CPA WØLTB NEAR-Fest 2016

2 This presentation was made at the NEARfest Oct 15,2016 forums, and this presentation and accompanying handouts made available for NEAR-fest attendees. The information contained in this presentation may or may not be applicable to your club/situation. Seek legal advice or advice of a tax professional to determine if it makes sense for your club to apply for 501(c)(3) status

3 History of NonProfits NonProfits were initially social benefit organizations that were outreaches largely of religious organizations. Tax implications arose once there was the 16 th Amendment to the US Constitution to allow federal income tax. Congress provided for deduction of charitable contributions starting in 1917, although it was a rather minor thing. After WWII, the importance of nonprofits grew and had large growth from the 1960s until current time.

4

5

6 Like any tax benefit, there is a potential for abuse. One must be careful to not run afoul of rules and regulations of the Internal Revenue Service as it relates to nonprofit status. I hope to give you some points to ponder, but in no way, is this information adequate to address all issues of the Amateur Radio community and tax matters. This will only address Federal tax issues. I am not an attorney and I don t offer any legal advice.

7 What are the Advantages of 501(c)(3) Status? Additional benefits may come to those organizations so recognized. State and local governments may allow exemption from sales tax and in some cases, property tax. Also, the USPS offers reduced postal rates for certain nonprofit organizations. An entity granted 501(c)(3) status is exempt from Federal income tax and is permitted to receive taxdeductible charitable contributions. In order to be recognized as a 501(c)(3) organization, the entity must meet certain criteria, and must file an application with the IRS, which is reviewed and approved or denied.

8 What are the requirements? There are three criteria for being granted exemption under 501(c)(3): A 501(c)(3) must be organized as a corporation, trust or unincorporated association. The entity s organizing documents must limit the purpose of the organization to exempt activities, cannot expressly permit prohibited activities and permanently dedicate the assets of the entity to exempt purposes.

9 Operation of the entity must promote its exempt purpose. It must refrain from participation in political campaigns and refrain from any substantial lobbying activity. Individuals must not be gaining personal benefit from the operation of the entity. It cannot conduct illegal activities. The entity must have one or more exempt purposes. 501(c)(3) stipulates those purposes to be charitable, educational, religious, scientific, literary, sports competition, preventing cruelty to children or animals and testing for public safety. Most commonly, 501(c)(3) entities are charitable, educational and religious.

10 IRS Publication 4220 (Applying for 501(c)(3) Tax-Exempt Status) lists under charitable advancement of education or science. Also, they list lessening the burdens of government. Under educational purpose, there is mention of conducting instruction/teaching. Certainly, radio clubs are often involved in such endeavors.

11 Application process SS-4 An existing club most likely already has an EIN Employer Identification Number. This is an entity s equivalent of a social security number. It can be obtained on-line via the IRS website.

12 What you must do in advance of applying for exemption Make sure that the underlying governing document of the club makes it clear that the club is appropriate to be a 501(c)(3) organization. Certainly, many ham clubs can look at these two aspects of the 501(c)(3) criteria. Look closely at percentage of effort related to scientific and educational aspects. Depending on the focus of the club, either could apply. If a club doesn t have that kind of a focus, perhaps the 501(c)(3) status isn t appropriate; if that is the determination of your governing board, then you may want to continue with your current tax status.

13 Once you determine that your club is appropriate for the 501(c)(3) status, you will need to be certain that your governing documents are up to date and file any needed amendments to your corporate bylaws with the state s secretary of state (or other state official as appropriate). The Secretary of State in most jurisdictions is the governmental official in charge of maintaining corporate records.

14 Financial records Make sure that the financial records (income statement and balance sheet) are in order. Perhaps that pile of bank statements in a shoe box doesn t fit that requirement! The financial records not only need to be up to speed for the application process, but need to continue to be kept once the exemption is approved. One popular accounting software product is QuickBooks. Or, you can design your own using a spreadsheet product such as Excel. If you are computerchallenged, adequate records can be maintained with pencil and paper!

15 When to file: If you file within 27 months of the formation of the organization is formed, the exemption will be retroactive to the formation date. If you have missed that date, don t dismay. Once approved, your exemption will be in force as of the date the exemption was filed. In some cases, retroactive approval can be granted.

16 Now we proceed 1023-EZ This is the focus of this discussion. The 1023-EZ must be completed on-line. See handout of eligibility questionnaire and form. Review of Questionnaire 7 pages. Included in IRS instructions to the 1023EZ form. Next slide shows page one of this form.

17 Page 1 of 7 of the 1023-EZ Eligibility Worksheet

18 Provided you answer all questions no, you are eligible to start on the 1023EZ form Page 1 of 3 of the 1023EZ form

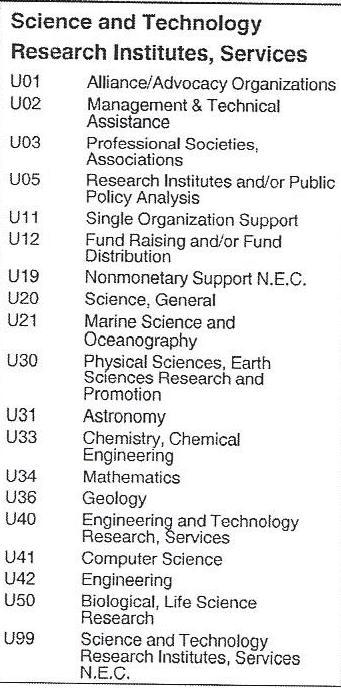

19 Page 1: Name, mailing address, EIN, contact person, officers, directors, website, Organizational structure, state of incorporation. Page 2: NTEE code (on next slide), designation of exempt purpose, designation of public charity vs private foundation.

20

21 Page 3: Request for retroactive exemption or reinstatement. Signatures. Submit form and requisite $275 fee (fee was reduced as of July 1, 2016 from $400). You may receive a request for additional information from the IRS. You will hopefully receive a determination letter, stating that your organization has been recognized as a 501(c)(3) entity. This process can take as little as a month or as much as 6 months

22 Annual filing of information returns 501(c)(3) organizations that have income less than $50,000 per year can satisfy their annual filing requirement by submitting the e-postcard, know as the 990-N. Other filings may include 1099s for contractors that do work for the club and for prize winners of drawings at hamfests. See the 1099-MISC instructions for this requirement.

23 Once you are approved, you will need to provide receipts to anyone who donates an amount of $250 or more to the organization. The letter should state that the donor has received no goods or services for their donation. Please note that if a person donated goods to the club, you need to leave it to the donor to value that donation. Many of us have donated to Goodwill and know that they hand you a receipt, stating that you donated 4 boxes of items and that it is up to the donor to value those items. Large in-kind donations may have to have an appraisal. Special care needs to be taken before accepting a donation of a motor vehicle.

24 Nothing in this presentation is a substitute for competent professional help. Professional help may come from an attorney learned in this area of law and/or a CPA or other tax accountant who had knowledge of the process of applying for and maintaining tax exempt status. Not every attorney, CPA or tax accountant has knowledge of this process.

25 Useful IRS Publications: Publication 4220 Applying for 501(c)(3) Tax Exempt Status Publication 4221-C Compliance Guide for 501(c)(3) Public Charities Publication 557 Tax Exempt Status for Your Organization Publication 526 Charitable Contributions Instructions for form 1023EZ IRS website irs.gov/charities-&-non-profits Web-based training

(c)(3) Applying for 501(c)(3) Tax-Exempt Status,

(3) Applying for 501(c)(3) Tax-Exempt Status,") Tax Exempt and Government Entities EXEMPT ORGANIZATIONS Applying for 501(c)(3) Tax-Exempt Status, Inside: Why apply for 501(c)(3) status? Who is eligible for 501(c)(3) status? What responsibilities accompany

Tax Exempt and Government Entities EXEMPT ORGANIZATIONS Applying for 501(c)(3) Tax-Exempt Status, Inside: Why apply for 501(c)(3) status? Who is eligible for 501(c)(3) status? What responsibilities accompany

BEST PRACTICES. Best Practices #125: 501(c)(3) Chapter Organization Cover Letter and Structure

(3) Chapter Organization Cover Letter and Structure") BEST PRACTICES Best Practices #125: 501(c)(3) Chapter Organization Cover Letter and Structure A lot has changed since the original Best Practices Article for Tax-Exempt Status was posted in 2009. Most

BEST PRACTICES Best Practices #125: 501(c)(3) Chapter Organization Cover Letter and Structure A lot has changed since the original Best Practices Article for Tax-Exempt Status was posted in 2009. Most

HOW TO APPLY FOR TAX-EXEMPT STATUS. Table of Contents

HOW TO APPLY FOR TAX-EXEMPT STATUS Table of Contents Basics of Tax Exemption Who Must File a Form 1023 501(c)(3) Requirements Organizational Test Operational Test Form 1023 Part I. Basic Information about

HOW TO APPLY FOR TAX-EXEMPT STATUS Table of Contents Basics of Tax Exemption Who Must File a Form 1023 501(c)(3) Requirements Organizational Test Operational Test Form 1023 Part I. Basic Information about

HOTV ByLaws. File for Status. Bank Account. Record Retention. Heart of the Valley 501C3 Investigation Report. ByLaws. Requirements: Mission Statement:

Legal Requirements Slides before 1st Section Divider Requirements: Heart of the Valley 501C3 Investigation Report HOTV ByLaws Mission Statement: File for Status ByLaws Incorporation Bank Account Record

Legal Requirements Slides before 1st Section Divider Requirements: Heart of the Valley 501C3 Investigation Report HOTV ByLaws Mission Statement: File for Status ByLaws Incorporation Bank Account Record

Overview of Non-Profits, 501(c)(3) Tom Walsh Chairman Denver Gaels GAA Club, Inc. t e.

(3) Tom Walsh Chairman Denver Gaels GAA Club, Inc. t e.") Overview of Non-Profits, 501(c)(3) Tom Walsh Chairman Denver Gaels GAA Club, Inc. t. 303.250.7707 e. tpwalsh3@gmail.com INTRO This presentation was created based on my experience filing a re-application

Overview of Non-Profits, 501(c)(3) Tom Walsh Chairman Denver Gaels GAA Club, Inc. t. 303.250.7707 e. tpwalsh3@gmail.com INTRO This presentation was created based on my experience filing a re-application

Starting a Nonprofit Frequently Asked Questions

Starting a Nonprofit Frequently Asked Questions Q. Are nonprofit and tax-exempt the same thing? A. No. A nonprofit is a type of corporation that is formed at the state level. Nonprofit and notfor-profit

Starting a Nonprofit Frequently Asked Questions Q. Are nonprofit and tax-exempt the same thing? A. No. A nonprofit is a type of corporation that is formed at the state level. Nonprofit and notfor-profit

Non-profit Organizations. Steps for establishing and for meeting Federal filing requirements

Non-profit Organizations Steps for establishing and for meeting Federal filing requirements US Income Taxes: A Brief Primer Definition of 'Federal Income Tax' A tax levied by the United States Internal

Non-profit Organizations Steps for establishing and for meeting Federal filing requirements US Income Taxes: A Brief Primer Definition of 'Federal Income Tax' A tax levied by the United States Internal

Getting Tax-exempt. Linnea R. Michel, Esq. Legal Center for Nonprofits, Inc.

Getting Tax-exempt Linnea R. Michel, Esq. Legal Center for Nonprofits, Inc. 2014 Legal Center for Nonprofits, Inc. Information provided herein is not legal advice and is intended for informational purposes

Getting Tax-exempt Linnea R. Michel, Esq. Legal Center for Nonprofits, Inc. 2014 Legal Center for Nonprofits, Inc. Information provided herein is not legal advice and is intended for informational purposes

Tax Requirements for Student Clubs

Tax Reporting Tax Requirements for Student Clubs FOLLOW-UP Prepared by Office of the Controller, Department of Tax Reporting August 2016 1 Tax Reporting All income from whatever source derived is taxable

Tax Reporting Tax Requirements for Student Clubs FOLLOW-UP Prepared by Office of the Controller, Department of Tax Reporting August 2016 1 Tax Reporting All income from whatever source derived is taxable

NONPROFIT RAFFLES. Legal Requirements in South Carolina

NONPROFIT RAFFLES Legal Requirements in South Carolina 1 WHAT IS A RAFFLE? S. C. CODE 33-57- 1 10 South Carolina law defines raffle as a game of chance in which a participant is required to pay something

NONPROFIT RAFFLES Legal Requirements in South Carolina 1 WHAT IS A RAFFLE? S. C. CODE 33-57- 1 10 South Carolina law defines raffle as a game of chance in which a participant is required to pay something

PRIVATE FOUNDATION CAUTION: The purposes of this memorandum are to assist you, the directors of your private foundation, and your accountant in:

CHERRY CREEK CENTER 4500 CHERRY CREEK DRIVE SOUTH #600 DENVER, CO 80246-1500 303.322.8943 WWW.WADEASH.COM CORPORATE DISCLAIMER Material presented on the Wade Ash Woods Hill & Farley, P.C., website is intended

CHERRY CREEK CENTER 4500 CHERRY CREEK DRIVE SOUTH #600 DENVER, CO 80246-1500 303.322.8943 WWW.WADEASH.COM CORPORATE DISCLAIMER Material presented on the Wade Ash Woods Hill & Farley, P.C., website is intended

Deep Dive Into the Form 1023 Application for 501c3 Tax-Exemption

Deep Dive Into the Form 1023 Application for 501c3 Tax-Exemption Lorri Dunsmore Perkins Coie November 2, 2017 Seattle, Washington November 2, 2017 Deep Dive Into the Form 1023 Application for 501c3 Tax-Exemption

Deep Dive Into the Form 1023 Application for 501c3 Tax-Exemption Lorri Dunsmore Perkins Coie November 2, 2017 Seattle, Washington November 2, 2017 Deep Dive Into the Form 1023 Application for 501c3 Tax-Exemption

CCCIA Ways & Means Committee 501c3 Assessment. Kate Tallman, John Stevens, Jay Schaller, & Ashley Roberts

CCCIA Ways & Means Committee 501c3 Assessment Kate Tallman, John Stevens, Jay Schaller, & Ashley Roberts Problem Statement Over the past 5 years CCCIA expenses have exceeded revenues by an average of

CCCIA Ways & Means Committee 501c3 Assessment Kate Tallman, John Stevens, Jay Schaller, & Ashley Roberts Problem Statement Over the past 5 years CCCIA expenses have exceeded revenues by an average of

Organizational Guidelines for Friendship Force Clubs in the USA Effective Date: June 23, 2017

Organizational Guidelines for Friendship Force Clubs in the USA Effective Date: June 23, 2017 Friendship Force clubs are independent organizations with each club responsible for developing and maintaining

Organizational Guidelines for Friendship Force Clubs in the USA Effective Date: June 23, 2017 Friendship Force clubs are independent organizations with each club responsible for developing and maintaining

Obtaining and Retaining Tax-Exempt Status

Obtaining and Retaining Tax-Exempt Status Becky Seidel Primer on Advising Nonprofit Organizations May 4, 2016 2016 Leaffer Law Group 1 Agenda 1. Overview of Tax-Exempt Status 2. Requirements for a 501(c)(3)

Obtaining and Retaining Tax-Exempt Status Becky Seidel Primer on Advising Nonprofit Organizations May 4, 2016 2016 Leaffer Law Group 1 Agenda 1. Overview of Tax-Exempt Status 2. Requirements for a 501(c)(3)

LEGAL & FINANCIAL GUIDELINES

LEGAL & FINANCIAL GUIDELINES I. Introduction 1. National League for Nursing (NLN) must be aware of the activities carried on by Constituent Leagues (CLs) in its name. A court could deem an act by a CL

LEGAL & FINANCIAL GUIDELINES I. Introduction 1. National League for Nursing (NLN) must be aware of the activities carried on by Constituent Leagues (CLs) in its name. A court could deem an act by a CL

Shoreline Neighborhood Association Presentation. City of Shoreline, Washington March 19, 2008

Shoreline Neighborhood Association Presentation City of Shoreline, Washington March 19, 2008 Susan Schalla, Attorney Davis Wright Tremaine LLP 1201 Third Avenue, Suite 2200 Seattle, WA 98101 (206) 757-7700

Shoreline Neighborhood Association Presentation City of Shoreline, Washington March 19, 2008 Susan Schalla, Attorney Davis Wright Tremaine LLP 1201 Third Avenue, Suite 2200 Seattle, WA 98101 (206) 757-7700

2015 G Do not enter social security numbers on this form as it may be made public. Open to Public

Short Form OMB No. 1545-1150 Return of Organization Exempt From Income Tax Form 990-EZ Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private foundations) 2015 G Do not enter

Short Form OMB No. 1545-1150 Return of Organization Exempt From Income Tax Form 990-EZ Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private foundations) 2015 G Do not enter

WikiLeaks Document Release

WikiLeaks Document Release February 2, 2009 Congressional Research Service Report RS21892 Application Process for Seeking Section 501(c)(3) Tax Exempt Status Erika Lunder, American Law Division December

WikiLeaks Document Release February 2, 2009 Congressional Research Service Report RS21892 Application Process for Seeking Section 501(c)(3) Tax Exempt Status Erika Lunder, American Law Division December

A Primer on Chapter Financial Management. Washington State HR Council Pam Gibbons, Treasurer June 2015

A Primer on Chapter Financial Management Washington State HR Council Pam Gibbons, Treasurer June 2015 Where to Start Bylaws Must be approved by SHRM and voted on by Board First step in getting legal Tax

A Primer on Chapter Financial Management Washington State HR Council Pam Gibbons, Treasurer June 2015 Where to Start Bylaws Must be approved by SHRM and voted on by Board First step in getting legal Tax

Nonprofit Essentials Conference, August 10, 2017 LEGAL REQUIREMENTS & THE IMPORTANCE OF BEING TRANSPARENT

Nonprofit Essentials Conference, August 10, 2017 LEGAL REQUIREMENTS & THE IMPORTANCE OF BEING TRANSPARENT About the Presenters Heidi Christianson Attorney Nilan Johnson Lewis, PA Kris Kewitsch Executive

Nonprofit Essentials Conference, August 10, 2017 LEGAL REQUIREMENTS & THE IMPORTANCE OF BEING TRANSPARENT About the Presenters Heidi Christianson Attorney Nilan Johnson Lewis, PA Kris Kewitsch Executive

Questions and Answers for Chapters on National Unification With Society for Social Work Leadership In Health Care

Questions and Answers for Chapters on National Unification With Society for Social Work Leadership In Health Care Updates: 3/31/09 4/1/09 4/2/09 Disclosure Statement: The following question and answer

Questions and Answers for Chapters on National Unification With Society for Social Work Leadership In Health Care Updates: 3/31/09 4/1/09 4/2/09 Disclosure Statement: The following question and answer

Resources for Starting a 501(c)(3) Peter Shaw Assistant School District Attorney

(3) Peter Shaw Assistant School District Attorney") Resources for Starting a 501(c)(3) Peter Shaw Assistant School District Attorney Disclaimer School Board Regulation 801.3AR Membership shall be primarily made up of parents and community members, though

Resources for Starting a 501(c)(3) Peter Shaw Assistant School District Attorney Disclaimer School Board Regulation 801.3AR Membership shall be primarily made up of parents and community members, though

CRS Report for Congress Received through the CRS Web

Order Code RL30877 CRS Report for Congress Received through the CRS Web Characteristics of and Reporting Requirements for Selected Tax-Exempt Organizations March 8, 2001 Marie B. Morris Legislative Attorney

Order Code RL30877 CRS Report for Congress Received through the CRS Web Characteristics of and Reporting Requirements for Selected Tax-Exempt Organizations March 8, 2001 Marie B. Morris Legislative Attorney

PARENT ORGANIZATIONS TAX FILING REQUIREMENTS

PARENT ORGANIZATIONS TAX FILING REQUIREMENTS Leland Dushkin, CPA Tax Manager Hereford, Lynch, Sellars & Kirkham, PC ldushkin@hlsk.com 1406 Wilson Road, Suite 100 Conroe, TX 77304 936-756-8127 or 936-441-1338

PARENT ORGANIZATIONS TAX FILING REQUIREMENTS Leland Dushkin, CPA Tax Manager Hereford, Lynch, Sellars & Kirkham, PC ldushkin@hlsk.com 1406 Wilson Road, Suite 100 Conroe, TX 77304 936-756-8127 or 936-441-1338

An Overview of the Tax Treatment of Nonprofits. Trina Griffin Research Division, NCGA October 22, 2008

An Overview of the Tax Treatment of Nonprofits Trina Griffin Research Division, NCGA October 22, 2008 Outline Basics Statistics Tax Treatment Trends Issues Nonprofit Basics What Is A Nonprofit? An organization

An Overview of the Tax Treatment of Nonprofits Trina Griffin Research Division, NCGA October 22, 2008 Outline Basics Statistics Tax Treatment Trends Issues Nonprofit Basics What Is A Nonprofit? An organization

Nonprofit Essentials Conference, August 20, 2015 LEGAL REQUIREMENTS & THE IMPORTANCE OF BEING TRANSPARENT

Nonprofit Essentials Conference, August 20, 2015 LEGAL REQUIREMENTS & THE IMPORTANCE OF BEING TRANSPARENT About the Presenters Emily Robertson Attorney Robertson Law Office @RLOonNonprofits Amy Sinykin

Nonprofit Essentials Conference, August 20, 2015 LEGAL REQUIREMENTS & THE IMPORTANCE OF BEING TRANSPARENT About the Presenters Emily Robertson Attorney Robertson Law Office @RLOonNonprofits Amy Sinykin

A For the 2011 calendar year, or tax year beginning, 2011, and ending, 20 D Employer identification number

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(a)(1) of the Internal Revenue Code (except black

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(a)(1) of the Internal Revenue Code (except black

Comparison of 501(c)(3) and 501(c)(4) and 501(c)(6) Compiled from multiple publicly available web and printed resources**

(3) and 501(c)(4) and 501(c)(6) Compiled from multiple publicly available web and printed resources**") Comparison of 501(c)(3) and 501(c)(4) and 501(c)(6) Compiled from multiple publicly available web and printed resources** Purposes 501(c)(3) 501(c)(4) 501(c)(6) Social Welfare: An organization must be

Comparison of 501(c)(3) and 501(c)(4) and 501(c)(6) Compiled from multiple publicly available web and printed resources** Purposes 501(c)(3) 501(c)(4) 501(c)(6) Social Welfare: An organization must be

Walk Like An Exemption: Fast-Track and Maintain the Right Tax Exemption

Walk Like An Exemption: Fast-Track and Maintain the Right Tax Exemption California Charter Schools Conference March 17, 2015 Kevin M. Davis Greta A. Proctor 1 What We Will Cover in This Program What Is

Walk Like An Exemption: Fast-Track and Maintain the Right Tax Exemption California Charter Schools Conference March 17, 2015 Kevin M. Davis Greta A. Proctor 1 What We Will Cover in This Program What Is

IAFF Local Charitable Activities Manual

IAFF Local Charitable Activities Manual Copyright 2012 International Association of Fire Fighters International Association of Fire Fighters Thomas A. Woodley, General Counsel Legal Department Baldwin

IAFF Local Charitable Activities Manual Copyright 2012 International Association of Fire Fighters International Association of Fire Fighters Thomas A. Woodley, General Counsel Legal Department Baldwin

Short Form Return of Organization Exempt From Income Tax

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(a)(1) of the Internal Revenue Code (except private

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(a)(1) of the Internal Revenue Code (except private

Short Form. Return of Organization Exempt From Income Tax

Short Form OMB No. 1545-1150 Return of Organization Exempt From Income Tax Form 990-EZ Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private

Short Form OMB No. 1545-1150 Return of Organization Exempt From Income Tax Form 990-EZ Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private

E. HOW TO ELECTRONICALLY FILE IRS FORM 1023-EZ

E. HOW TO ELECTRONICALLY FILE IRS FORM 1023-EZ An organization that wants to apply for recognition of its tax-exempt status as a Section 501(c)(3) organization needs to complete a Form 1023, Application

E. HOW TO ELECTRONICALLY FILE IRS FORM 1023-EZ An organization that wants to apply for recognition of its tax-exempt status as a Section 501(c)(3) organization needs to complete a Form 1023, Application

501(c)(3) for Parent Groups. The Basics

(3) for Parent Groups. The Basics") 501(c)(3) for Parent Groups The Basics Do 501(c)(3), tax exemption, and nonprofit all mean the same thing? People tend to use these terms interchangeably, but they have distinct definitions. 501(c)(3)

501(c)(3) for Parent Groups The Basics Do 501(c)(3), tax exemption, and nonprofit all mean the same thing? People tend to use these terms interchangeably, but they have distinct definitions. 501(c)(3)

Local Section Finances

Local Section Finances Local sections, like the national association, must incur expenses, manage their budgets, pay bills, and deal with tax issues. The following information provides the basic requirements

Local Section Finances Local sections, like the national association, must incur expenses, manage their budgets, pay bills, and deal with tax issues. The following information provides the basic requirements

Number and street (or P.O. box, if mail is not delivered to street address) Room/suite

Room/suite") Form 990-EZ Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(1) of the Internal Revenue Code (except black lung benefit trust or private foundation) Sponsoring organizations

Form 990-EZ Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(1) of the Internal Revenue Code (except black lung benefit trust or private foundation) Sponsoring organizations

Incorporated Entity. Elects Tax Exempt Status with the Internal Revenue Service. Treated as a public charity per I.R.S. guidelines

1 2 3 Incorporated Entity Elects Tax Exempt Status with the Internal Revenue Service Treated as a public charity per I.R.S. guidelines 1 PROS Recognized Legal Entity Insurable Entity Required Monetary

1 2 3 Incorporated Entity Elects Tax Exempt Status with the Internal Revenue Service Treated as a public charity per I.R.S. guidelines 1 PROS Recognized Legal Entity Insurable Entity Required Monetary

IRS Form 990: Who Sees it Besides the IRS?

IRS Form 990: Who Sees it Besides the IRS? State Tax Authorities. Attorney General. Public Inspection. www.guidestar.org Newspapers and Media. Donors. Anyone! 2 Purpose of New IRS Form 990 Enhance Transparency

IRS Form 990: Who Sees it Besides the IRS? State Tax Authorities. Attorney General. Public Inspection. www.guidestar.org Newspapers and Media. Donors. Anyone! 2 Purpose of New IRS Form 990 Enhance Transparency

Government Copy MCF MISSOULA COMMUNITY FOUNDATION PO BOX 2368 MISSOULA, MT

2012 TA RETURN Government Copy Client: Prepared for: MCF MISSOULA COMMUNITY FOUNDATION PO BO 2368 MISSOULA, MT 59806 406-926-3131 Prepared by: Norm Williamson CPA PLLC 1800 S Russell St, Ste 200 Missoula,

2012 TA RETURN Government Copy Client: Prepared for: MCF MISSOULA COMMUNITY FOUNDATION PO BO 2368 MISSOULA, MT 59806 406-926-3131 Prepared by: Norm Williamson CPA PLLC 1800 S Russell St, Ste 200 Missoula,

A For the 2010 calendar year, or tax year beginning, 2010, and ending, 20 D Employer identification number

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black

CHAR410, CHAR410-A, CHAR410-R

New York State Department of Law (Office of the Attorney General) Charities Bureau - Registration Section Instructions for Forms CHAR410, CHAR410-A, CHAR410-R and Schedule E Registration/Amended Registration/Re-Registration

New York State Department of Law (Office of the Attorney General) Charities Bureau - Registration Section Instructions for Forms CHAR410, CHAR410-A, CHAR410-R and Schedule E Registration/Amended Registration/Re-Registration

Short Form Return of Organization Exempt From Income Tax

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(a)(1) of the Internal Revenue Code (except private

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(a)(1) of the Internal Revenue Code (except private

Information for Sumner County School Support Organizations

Information for Sumner County School Support Organizations School Support Organization (SSO) Start Up Instructions and General Information These suggestions are not to be considered legal advice. You may

Information for Sumner County School Support Organizations School Support Organization (SSO) Start Up Instructions and General Information These suggestions are not to be considered legal advice. You may

Form 1023 and the Toughest Compliance Challenges

Form 1023 and the Toughest Compliance Challenges Clearing the Hurdles When 501(c)(3) Organizations Apply for Tax Exempt Status WEDNESDAY, OCTOBER 23, 2013, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This

Form 1023 and the Toughest Compliance Challenges Clearing the Hurdles When 501(c)(3) Organizations Apply for Tax Exempt Status WEDNESDAY, OCTOBER 23, 2013, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This

Federal Financial Requirements

American Society of Health-System Pharmacists Federal Financial Requirements ASHP s Financial Toolkit for Affiliates Kimberlee Berry [Pick the date] FEDERAL REQUIREMENTS NOTE: All IRS forms can be accessed

American Society of Health-System Pharmacists Federal Financial Requirements ASHP s Financial Toolkit for Affiliates Kimberlee Berry [Pick the date] FEDERAL REQUIREMENTS NOTE: All IRS forms can be accessed

Short Form 990-EZ Return of Organization Exempt From Income Tax

Form B G I Short Form 990-EZ Return of Organization Exempt From Income Tax 2013 Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private foundations) Do not enter Social Security

Form B G I Short Form 990-EZ Return of Organization Exempt From Income Tax 2013 Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private foundations) Do not enter Social Security

Did the address of the organization change during the year? Yes No

2016 Tax Questionnaire 990 Not-For-Profit Thank you for completing this questionnaire completely and accurately. This is a very important step in completing your return. We recommend that you review last

2016 Tax Questionnaire 990 Not-For-Profit Thank you for completing this questionnaire completely and accurately. This is a very important step in completing your return. We recommend that you review last

(c)(3) Compliance Guide for 501(c)(3) Public Charities,

(3) Compliance Guide for 501(c)(3) Public Charities,") Tax Exempt and Government Entities EXEMPT ORGANIZATIONS Compliance Guide for 501(c)(3) Public Charities, Inside: Activities that may jeopardize a charity s exempt status, Federal information returns, tax

Tax Exempt and Government Entities EXEMPT ORGANIZATIONS Compliance Guide for 501(c)(3) Public Charities, Inside: Activities that may jeopardize a charity s exempt status, Federal information returns, tax

Short Form OMB No Return of Organization Exempt From Income Tax

Form 990-EZ Short Form OMB No. 1545-1150 Return of Organization Exempt From Income Tax Department of the Treasury Internal Revenue Service Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue

Form 990-EZ Short Form OMB No. 1545-1150 Return of Organization Exempt From Income Tax Department of the Treasury Internal Revenue Service Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue

Summer 2017 LEXINGTON ONE SCHOOL DISTRICT

Summer 2017 LEXINGTON ONE SCHOOL DISTRICT General information Financial policies and controls Fundraising Reporting Learning from the past District policies and procedures Q&A NOTE: This presentation is

Summer 2017 LEXINGTON ONE SCHOOL DISTRICT General information Financial policies and controls Fundraising Reporting Learning from the past District policies and procedures Q&A NOTE: This presentation is

Instructions for Reinstatement of Tax-Exempt Status

Instructions for Reinstatement of Tax-Exempt Status Dear Local PTA: The IRS has issued letters revoking the tax-exempt status of numerous organizations, including many local PTAs, for failure to file information

Instructions for Reinstatement of Tax-Exempt Status Dear Local PTA: The IRS has issued letters revoking the tax-exempt status of numerous organizations, including many local PTAs, for failure to file information

Short Form OMB No Return of Organization Exempt From Income Tax

Form 990-EZ Short Form OMB No. 1545-1150 Return of Organization Exempt From Income Tax Department of the Treasury Internal Revenue Service Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue

Form 990-EZ Short Form OMB No. 1545-1150 Return of Organization Exempt From Income Tax Department of the Treasury Internal Revenue Service Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue

Short Form OMB No Return of Organization Exempt From Income Tax

Form 990-EZ Short Form OMB No. 1545-1150 Return of Organization Exempt From Income Tax Department of the Treasury Internal Revenue Service Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue

Form 990-EZ Short Form OMB No. 1545-1150 Return of Organization Exempt From Income Tax Department of the Treasury Internal Revenue Service Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue

Short Form Return of Organization Exempt From Income Tax

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(a)(1) of the Internal Revenue Code (except private

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(a)(1) of the Internal Revenue Code (except private

Taxes for Rotary Clubs

Taxes for Rotary Clubs An effective guide for the implementation of strategies and policies to meet current regulations and tax policies that effect Rotary Clubs in Massachusetts. EMPLOYER IDENTIFICATION

Taxes for Rotary Clubs An effective guide for the implementation of strategies and policies to meet current regulations and tax policies that effect Rotary Clubs in Massachusetts. EMPLOYER IDENTIFICATION

Compliance Guide for Tax-Exempt Organizations

INTERNAL REVENUE SERVICE TAX-EXEMPT AND GOVERNMENT ENTITIES EXEMPT ORGANIZATIONS, Compliance Guide for Tax-Exempt Organizations (Other than 501(c)(3) Public Charities and Private Foundations), Inside:

INTERNAL REVENUE SERVICE TAX-EXEMPT AND GOVERNMENT ENTITIES EXEMPT ORGANIZATIONS, Compliance Guide for Tax-Exempt Organizations (Other than 501(c)(3) Public Charities and Private Foundations), Inside:

Short Form OMB No Return of Organization Exempt From Income Tax

Form 990-EZ Short Form OMB No. 1545-1150 Return of Organization Exempt From Income Tax Department of the Treasury Internal Revenue Service Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue

Form 990-EZ Short Form OMB No. 1545-1150 Return of Organization Exempt From Income Tax Department of the Treasury Internal Revenue Service Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue

Short Form Return of Organization Exempt From Income Tax

Form 990-EZ Short Form Return of Organization Exempt From Income Tax OMB. -0 07 Under section 0, 7, or 97() of the Internal Revenue Code (except private foundations) G Do not enter social security numbers

Form 990-EZ Short Form Return of Organization Exempt From Income Tax OMB. -0 07 Under section 0, 7, or 97() of the Internal Revenue Code (except private foundations) G Do not enter social security numbers

Instructions for Form 990-EZ

2009 Instructions for Form 990-EZ Short Form Return of Organization Exempt From Income Tax Under Section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private

2009 Instructions for Form 990-EZ Short Form Return of Organization Exempt From Income Tax Under Section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private

Section references are to the Internal Revenue Code unless otherwise noted.

2008 Instructions for Form 990-EZ Short Form Return of Organization Exempt From Income Tax Under Section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private

2008 Instructions for Form 990-EZ Short Form Return of Organization Exempt From Income Tax Under Section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private

Short Form. Return of Organization Exempt From Income Tax

Short Form OMB No. 1545-1150 Return of Organization Exempt From Income Tax Form 990-EZ Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code 2012 (except black lung benefit trust or private

Short Form OMB No. 1545-1150 Return of Organization Exempt From Income Tax Form 990-EZ Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code 2012 (except black lung benefit trust or private

Staying Legal: General Guidelines. for Operating a 501(c)(3) Nonprofit Corporation in Georgia

(3) Nonprofit Corporation in Georgia") Staying Legal: General Guidelines for Operating a 501(c)(3) Nonprofit Corporation in Georgia Originally Prepared By: Tax Subcommittee of Pro Bono Partnership of Atlanta, chaired by Ed Manigault (formerly

Staying Legal: General Guidelines for Operating a 501(c)(3) Nonprofit Corporation in Georgia Originally Prepared By: Tax Subcommittee of Pro Bono Partnership of Atlanta, chaired by Ed Manigault (formerly

Short Form. Return of Organization Exempt From Income Tax

Short Form OMB No. 1545-1150 Return of Organization Exempt From Income Tax Form 990-EZ Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code 2014 (except private foundations) G Do not enter

Short Form OMB No. 1545-1150 Return of Organization Exempt From Income Tax Form 990-EZ Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code 2014 (except private foundations) G Do not enter

A For the 2010 calendar year, or tax year beginning, 2010, and ending, 20 D Employer identification number

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(1) of the Internal Revenue Code (except black lung

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(1) of the Internal Revenue Code (except black lung

Short Form Return of Organization Exempt From Income Tax

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(a)(1) of the Internal Revenue Code (except private

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(a)(1) of the Internal Revenue Code (except private

Thank you! 7/26/2011 For information purposes only. NOT LEGAL OR TAX ADVICE.

On July 14, a webinar called How to reinstate and maintain your IRS tax exempt status was conducted. Weʹre sorry to report that some of the information was inaccurate. The presenters did present accurate

On July 14, a webinar called How to reinstate and maintain your IRS tax exempt status was conducted. Weʹre sorry to report that some of the information was inaccurate. The presenters did present accurate

Activities that may jeopardize exempt status. Federal information returns, tax returns or notices that must be filed. Recordkeeping why, what, when

(a) Internal Revenue Service Tax Exempt and Government Entities Exempt Organizations Compliance Guide for Tax-Exempt Organizations (other than 501(c)(3) Public Charities and Private Foundations) Covers:

(a) Internal Revenue Service Tax Exempt and Government Entities Exempt Organizations Compliance Guide for Tax-Exempt Organizations (other than 501(c)(3) Public Charities and Private Foundations) Covers:

Federal Tax-Exempt Status 501(c)(3) Organizations

(3) Organizations") Federal Tax-Exempt Status 501(c)(3) Organizations Most PTAs are classified as tax-exempt 501(c)(3) public charities under the Internal Revenue Code (IRC). One major advantage for organizations that are

Federal Tax-Exempt Status 501(c)(3) Organizations Most PTAs are classified as tax-exempt 501(c)(3) public charities under the Internal Revenue Code (IRC). One major advantage for organizations that are

Short Form Return of Organization Exempt From Income Tax

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private

. This return is a consolidation from multiple entities, for use as an informational tool only.

. This return is a consolidation from multiple entities, for use as an informational tool only. 1 2 3 4 5 6 Susie Q. Smart, Exec. Director 40 X 165,000 0 5,500 (See Sched J for addl info) 7 8 9 10 11 12

. This return is a consolidation from multiple entities, for use as an informational tool only. 1 2 3 4 5 6 Susie Q. Smart, Exec. Director 40 X 165,000 0 5,500 (See Sched J for addl info) 7 8 9 10 11 12

Time for a Legal Tune-Up: Compliance Issues for Nonprofit and Tax-Exempt Organizations

Time for a Legal Tune-Up: Compliance Issues for Nonprofit and Tax-Exempt Organizations presented by Corinne H. Gartner October 5, 2017 500 Capitol Mall, Suite 1550 Sacramento, CA 95814 p. (916) 661-5700

Time for a Legal Tune-Up: Compliance Issues for Nonprofit and Tax-Exempt Organizations presented by Corinne H. Gartner October 5, 2017 500 Capitol Mall, Suite 1550 Sacramento, CA 95814 p. (916) 661-5700

A For the 2009 calendar year, or tax year beginning, 2009, and ending, D Employer identification number

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black

Short Form. Return of Organization Exempt From Income Tax

Short Form OMB. 1545-1150 Return of Organization Exempt From Income Tax Form 990-EZ Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code 2015 (except private foundations) G Do not enter

Short Form OMB. 1545-1150 Return of Organization Exempt From Income Tax Form 990-EZ Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code 2015 (except private foundations) G Do not enter

Copyright 2018, James M. McCarten, Burr & Forman LLP, all rights reserved

Prepared for Stetson 2018 National Conference on Special Needs Planning and Special Needs Trusts Pre-Conference Pooled Trusts Intensive St. Petersburg, Florida Wednesday, October 17, 2018 Presented by:

Prepared for Stetson 2018 National Conference on Special Needs Planning and Special Needs Trusts Pre-Conference Pooled Trusts Intensive St. Petersburg, Florida Wednesday, October 17, 2018 Presented by:

THE SCHOOL DISTRICT OF GREENVILLE COUNTY

THE SCHOOL DISTRICT OF GREENVILLE COUNTY Fall 2018 The District appreciates the assistance that support groups provide to students Consistency of general practices and financial reporting will help ensure

THE SCHOOL DISTRICT OF GREENVILLE COUNTY Fall 2018 The District appreciates the assistance that support groups provide to students Consistency of general practices and financial reporting will help ensure

DUNAGAN JACK LLP 3724 JEFFERSON STREET, SUITE 307 AUSTIN, TX (512)

") CLIENT DUNAGAN JACK LLP JEFFERSON STREET, SUITE 0 AUSTIN, T () 0-99 vember, 0 of Central Texas, Inc. P.O. Box Austin, T - FEDERAL ID: - Dear Client: Your Federal Return of Organization Exempt from Income

CLIENT DUNAGAN JACK LLP JEFFERSON STREET, SUITE 0 AUSTIN, T () 0-99 vember, 0 of Central Texas, Inc. P.O. Box Austin, T - FEDERAL ID: - Dear Client: Your Federal Return of Organization Exempt from Income

Tax-Exempt Status and IRS Reporting Obligations. 1. All Undergraduate Organizations

Tax-Exempt Status and IRS Reporting Obligations All undergraduate organizations are expected to comply with the Undergraduate Regulations, and must also comply with Federal and State tax laws. The purpose

Tax-Exempt Status and IRS Reporting Obligations All undergraduate organizations are expected to comply with the Undergraduate Regulations, and must also comply with Federal and State tax laws. The purpose

File a separate application for each return. Information about Form 8868 and its instructions is at

Form 8868 Application for Automatic Extension of Time To File an Exempt Organization Return (Rev. January 2017) OMB No. 1545-1709 Department of the Treasury Internal Revenue Service File a separate application

Form 8868 Application for Automatic Extension of Time To File an Exempt Organization Return (Rev. January 2017) OMB No. 1545-1709 Department of the Treasury Internal Revenue Service File a separate application

Instructions for Form 990-EZ

2011 Instructions for Form 990-EZ Short Form Return of Organization Exempt From Income Tax Under Section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private

2011 Instructions for Form 990-EZ Short Form Return of Organization Exempt From Income Tax Under Section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private

A For the 2011 calendar year, or tax year beginning, 2011, and ending, 20 B Check if applicable:

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(1) of the Internal Revenue Code (except black lung

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(1) of the Internal Revenue Code (except black lung

Annual Electronic Filing Requirement Small Exempt Organizations Form 990-N

Annual Electronic Filing Requirement Small Exempt Organizations Form 990-N Utilized For ALL ENTITIES (Councils, Courts, Assembly s, Chapter s, Inter-City s, Inter-Districts, District Conferences, State

Annual Electronic Filing Requirement Small Exempt Organizations Form 990-N Utilized For ALL ENTITIES (Councils, Courts, Assembly s, Chapter s, Inter-City s, Inter-Districts, District Conferences, State

Short Form Return of Organization Exempt From Income Tax

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51, 527, or 4947(a)(1) of the Internal Revenue Code (except private

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51, 527, or 4947(a)(1) of the Internal Revenue Code (except private

Short Form. Return of Organization Exempt From Income Tax

Short Form OMB No. 1545-1150 Return of Organization Exempt From Income Tax Form 990-EZ Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code 2012 (except black lung benefit trust or private

Short Form OMB No. 1545-1150 Return of Organization Exempt From Income Tax Form 990-EZ Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code 2012 (except black lung benefit trust or private

4-H CLUB TREASURER S RECORD BOOK

4-H CLUB TREASURER S RECORD BOOK Name of Club: County: Year: Officers: President: Vice President: Secretary: Treasurer: Other: 4-H TREASURER Congratulations on your new responsibility as 4-H treasurer.

4-H CLUB TREASURER S RECORD BOOK Name of Club: County: Year: Officers: President: Vice President: Secretary: Treasurer: Other: 4-H TREASURER Congratulations on your new responsibility as 4-H treasurer.

Short Form. Return of Organization Exempt From Income Tax

Short Form OMB. 1545-1150 Return of Organization Exempt From Income Tax Form 990-EZ Under section 501(c), 57, or 4947(a)(1) of the Internal Revenue Code 016 (except private foundations) G Do not enter

Short Form OMB. 1545-1150 Return of Organization Exempt From Income Tax Form 990-EZ Under section 501(c), 57, or 4947(a)(1) of the Internal Revenue Code 016 (except private foundations) G Do not enter

February 20, 2018 LEGAL STRUCTURES FOR SOCIAL ENTREPRENEURS

February 20, 2018 LEGAL STRUCTURES FOR SOCIAL ENTREPRENEURS UC Berkeley, February 20, 2018 Speakers Jennifer Barnette Cooley LLP Jesse Finfrock Morrison & Foerster LLP 1 How do non-profits and for-profits

February 20, 2018 LEGAL STRUCTURES FOR SOCIAL ENTREPRENEURS UC Berkeley, February 20, 2018 Speakers Jennifer Barnette Cooley LLP Jesse Finfrock Morrison & Foerster LLP 1 How do non-profits and for-profits

Economic Development as a Charitable Activity April 5, Lara Kalwinski, Esq. Council on Foundations

Economic Development as a Charitable Activity April 5, 2017 Lara Kalwinski, Esq. Council on Foundations Agenda Legal Background and Why This is Important Meeting Charitability Standards What We Know What

Economic Development as a Charitable Activity April 5, 2017 Lara Kalwinski, Esq. Council on Foundations Agenda Legal Background and Why This is Important Meeting Charitability Standards What We Know What

Short Form Return of Organization Exempt From Income Tax

Click on the question-mark icons to display windows. The information provided will enable you to file a more complete return and reduce the chances the IRS has to contact you. Form 990-EZ Department of

Click on the question-mark icons to display windows. The information provided will enable you to file a more complete return and reduce the chances the IRS has to contact you. Form 990-EZ Department of

TAX-EXEMPT ORGANIZATIONS: EFFECTIVE GOVERNANCE AND LEGAL COMPLIANCE VICTOR J. FERGUSON SUZANNE R. GALYARDT VORYS, SATER, SEYMOUR AND PEASE LLP

TAX-EXEMPT ORGANIZATIONS: EFFECTIVE GOVERNANCE AND LEGAL COMPLIANCE VICTOR J. FERGUSON SUZANNE R. GALYARDT VORYS, SATER, SEYMOUR AND PEASE LLP OVERVIEW 1. Organizational Test 2. Operational Test 3. Private

TAX-EXEMPT ORGANIZATIONS: EFFECTIVE GOVERNANCE AND LEGAL COMPLIANCE VICTOR J. FERGUSON SUZANNE R. GALYARDT VORYS, SATER, SEYMOUR AND PEASE LLP OVERVIEW 1. Organizational Test 2. Operational Test 3. Private

** PUBLIC DISCLOSURE COPY ** Short Form Return of Organization Exempt From Income Tax

Short Form Return of Organization Exempt From Income Tax OMB No. 1545-1150 Form Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or 990-EZ private

Short Form Return of Organization Exempt From Income Tax OMB No. 1545-1150 Form Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or 990-EZ private

SHOULD CHARITABLE GIVING BE A PART OF MY ESTATE PLAN?

by Layne T. Rushforth Summary Charitable contributions not only entitle the donor to an income-tax deduction, but may also accomplish certain estate-planning objectives. Such contributions can be made

by Layne T. Rushforth Summary Charitable contributions not only entitle the donor to an income-tax deduction, but may also accomplish certain estate-planning objectives. Such contributions can be made

Operations: Cadillac Area Festivals & Events Policies and Procedures

Operations: Cadillac Area Festivals & Events Cadillac Area Festivals & Events (CAFÉ) is a 501C3, an IRS tax exempt entity. Non profits and organized committees in the area can utilize CAFÉ as fiduciary

Operations: Cadillac Area Festivals & Events Cadillac Area Festivals & Events (CAFÉ) is a 501C3, an IRS tax exempt entity. Non profits and organized committees in the area can utilize CAFÉ as fiduciary

The following are common situations where the acquisition of property by a charitable organization is not subject to sales tax.

DEPARTMENT OF REVENUE SALES AND USE TAX 1 CCR 201-4 Regulation 39-26-718 CHARITABLE AND OTHER EXEMPT ORGANIZATIONS (1) General Rule. (c) Purchases by charitable organizations are exempt from state sales

DEPARTMENT OF REVENUE SALES AND USE TAX 1 CCR 201-4 Regulation 39-26-718 CHARITABLE AND OTHER EXEMPT ORGANIZATIONS (1) General Rule. (c) Purchases by charitable organizations are exempt from state sales

Booster Clubs Questions and Answers (in italics)

") Booster Clubs Questions and Answers (in italics) Board Policy (Employees) DBD Regulations: Employees and Financial Capacity 1. If an employee is in charge of a concession stand, does that fall in the same

Booster Clubs Questions and Answers (in italics) Board Policy (Employees) DBD Regulations: Employees and Financial Capacity 1. If an employee is in charge of a concession stand, does that fall in the same

EF Transmission Status

990EF EF Transmission Status (Keep for your records) Name(s) as shown on return EIN number The following will be transmitted to the IRS. 990 8868 Amended The following state returns will be transmitted:

990EF EF Transmission Status (Keep for your records) Name(s) as shown on return EIN number The following will be transmitted to the IRS. 990 8868 Amended The following state returns will be transmitted:

Internal Revenue Service Compliance Guide for 501(c)(3) Public Charities

(3) Public Charities") Internal Revenue Service Compliance Guide for 501(c)(3) Public Charities Federal tax law provides tax benefits to nonprofit organizations recognized as exempt from federal income tax under section 501(c)(3)

Internal Revenue Service Compliance Guide for 501(c)(3) Public Charities Federal tax law provides tax benefits to nonprofit organizations recognized as exempt from federal income tax under section 501(c)(3)

Form 990 Tax Exempt Reporting

Form 990 Tax Exempt Reporting CLAconnect.com Speaker Introductions Amanda Treml, CPA Amanda is a Manager with CliftonLarsonAllen and provides assurance and tax compliance services to non-profit organizations.

Form 990 Tax Exempt Reporting CLAconnect.com Speaker Introductions Amanda Treml, CPA Amanda is a Manager with CliftonLarsonAllen and provides assurance and tax compliance services to non-profit organizations.

Launching your nonprofit

Launching your nonprofit What we ll cover What is a nonprofit What difference does that make How to establish nonprofit legal identities with government agencies Maintaining your legal identity with integrity

Launching your nonprofit What we ll cover What is a nonprofit What difference does that make How to establish nonprofit legal identities with government agencies Maintaining your legal identity with integrity

Tax Guide for Nonprofits

Tax Guide for Nonprofits 4 th Edition Stephen Fishman, J.D. Chapter 1 Nonprofits and the IRS... 1 Learning Objectives... 1 Introduction... 1 What Do We Mean When We Say Nonprofit?... 1 Tax-Exempt Nonprofits...

Tax Guide for Nonprofits 4 th Edition Stephen Fishman, J.D. Chapter 1 Nonprofits and the IRS... 1 Learning Objectives... 1 Introduction... 1 What Do We Mean When We Say Nonprofit?... 1 Tax-Exempt Nonprofits...