Instructions for Reinstatement of Tax-Exempt Status

|

|

|

- Brenda Gibbs

- 5 years ago

- Views:

Transcription

1 Instructions for Reinstatement of Tax-Exempt Status Dear Local PTA: The IRS has issued letters revoking the tax-exempt status of numerous organizations, including many local PTAs, for failure to file information returns for 3 consecutive years. In particular, the revocations resulted from a failure to file required Form 990 (Return of Organization Exempt from Income Tax), Form 990-EZ (Short Form Return of Organization Exempt From Income Tax), or Form 990-N (e-postcard), for three consecutive tax years. If your local PTA received a letter from the IRS stating that your tax-exempt status has been revoked, please follow the instructions in the attachment to this letter to reinstate your organization s tax-exempt status. If your application is accepted and you provide evidence of reasonable cause for the failure to file your returns, the IRS will issue a letter reinstating the organization s tax exemption retroactive to the date of the revocation. The packet you send to the IRS must include: 1. Cover Letter to the IRS 2. Reasonable Cause Statement (if seeking retroactive reinstatement) 3. Forms 990 or Forms 990-EZ for all taxable years not previously filed (if applicable see instructions!) 4. IRS Form 1023 (Application for Recognition of Exemption Under Section 501(c)(3)) 5. Attachments to IRS Form Check made payable to the United States Treasury. Please follow the attached instructions carefully to complete IRS Form 1023 and the attachments. Please carefully review the portions of the form already completed, and make changes to any responses that are incorrect. Please contact me by at hdean@pta.org if you have questions. Sincerely, Enclosure Heather Dean Deputy Executive Director, Programs and Operations

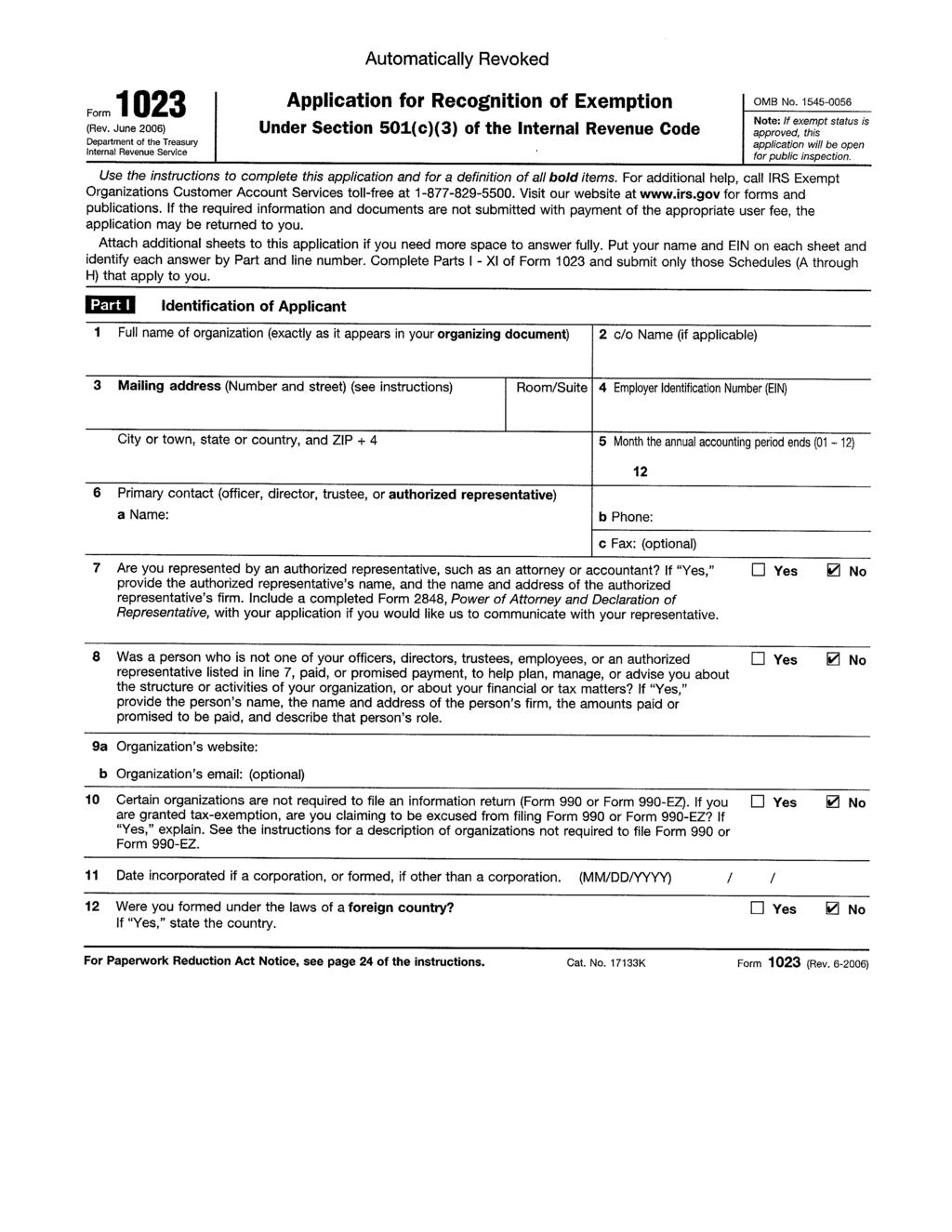

2 Instructions for Reinstatement of Local PTA Tax Exemption Please follow these instructions carefully. These instructions will help you complete the IRS Form 1023 and required attachments. Do not submit these instructions to the IRS. Please review any already completed responses on Form 1023 for accuracy and make any necessary changes. Keep in mind that terms in bold used in Form 1023 have specific meanings, which are provided in the Instructions to Form 1023, which can be obtained by searching Form 1023 Instructions at You can type right on the form, or fill in the blanks with a pen. If you start with a fresh Form 1023 which you print from the IRS website, be sure to put Automatically Revoked on top of the first page, as we have on the model. 1. IRS Cover Letter Complete the blanks by filling in the date, name of the local PTA, and the title of the local PTA officer submitting the application for exemption to the IRS. The officer should sign the letter. 2. Reasonable Cause Statement In order for the local PTA s tax exemption to be reinstated effective as of the date of revocation, you must provide the IRS a reasonable cause statement explaining the local PTA s failure to file information returns for 3 consecutive years. If the IRS determines that reasonable cause does not exist, the local PTA s exemption will only be effective as of the prospective date of reinstatement, instead of being effective retroactive to the date of revocation. Please be aware that acceptance of a reasonable cause statement is VERY rare. According to the IRS, the local PTA s reasonable cause statement must include each of the following: a. A written statement setting forth all of the facts that support its claim for reasonable cause for failing to file a required return or notice in each of the 3 consecutive years and over the entire consecutive 3-year period, including a detailed description of all the facts and circumstances that led to each failure and the continuous failure, the discovery of the failures, and the steps taken to avoid or mitigate the failures; b. A written statement describing the safeguards the local PTA has put into place to ensure that the local PTA will not fail to file returns or notices in the future; c. Evidence to substantiate all material aspects of the written statements described in paragraphs (a) and (b) of this section; d. A list of the annual information returns for the taxable years not filed, which are enclosed. (In other words, all delinquent Forms 990 or 990-EZ must be enclosed with the packet.)

3 IRS Reinstatement Instructions Page 2 of 6 e. An original declaration, dated and signed under penalties of perjury by an officer, director, trustee, or other official who is authorized to sign for the local PTA in the following form: I, (Name), (Title) declare, under penalties of perjury, that I am authorized to sign this request for retroactive reinstatement on behalf of [Name of Local PTA], and I further declare that I have examined this request for retroactive reinstatement, including the written explanation of all the facts and information pertaining to the claim for reasonable cause and the evidence to substantiate the claim for reasonable cause, and to the best of my knowledge and belief, this request is true, correct, and complete. Note: In preparing your reasonable cause statement, be sure to explain not only why the returns were not filed for each of the 3 years but also why the returns were not filed later during the 3-year period. The local PTA should demonstrate that it exercised ordinary business care and prudence in attempting to comply with its reporting requirements. The IRS has provided the following 5 factors that weigh in favor of finding reasonable cause, which should be addressed in the reasonable cause statement, if applicable: i. Evidence that substantially all of the organization s activities are performed by volunteers. ii. The organization s failure was due to its reasonable, good faith reliance on erroneous written information from the IRS, stating that the organization was not required to file a return or notice, provided the IRS was made aware of all relevant facts. iii. The failure to file the returns or notices arose from events beyond the organization s control that made it impossible for the organization to file returns or notices for each of the 3 years at issue and over the entire 3-year period. iv. The organization acted in a responsible manner by undertaking significant steps to avoid or mitigate the failure to file the required returns or notices and to prevent similar failures in the future, including, but not limited to - Attempting to prevent an impediment or a failure, if it was foreseeable; - Acting as promptly as possible to remove an impediment or the cause of the reporting failure, once the failure was discovered; and - After the failure was discovered, implementing sufficient safeguards to ensure future compliance with the reporting requirements.

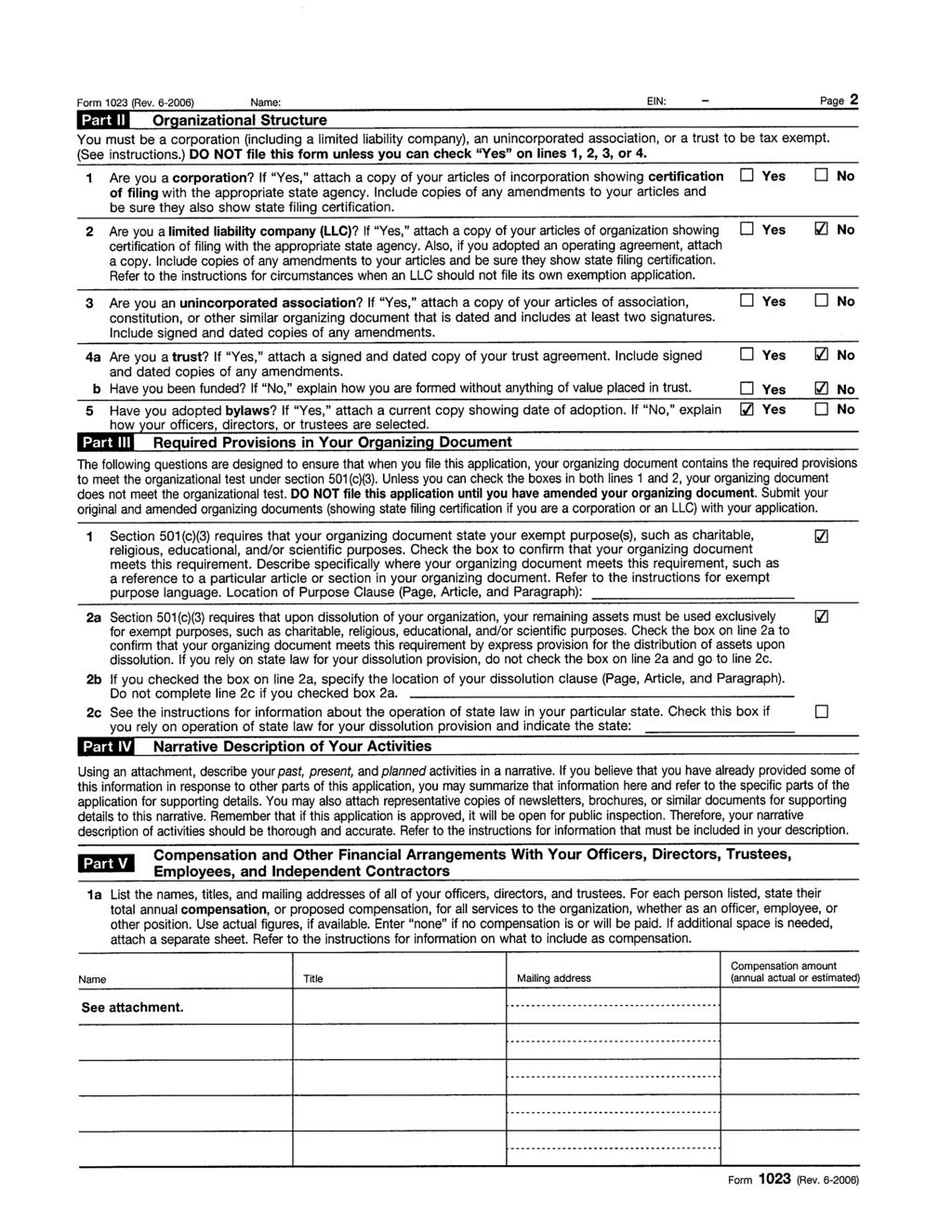

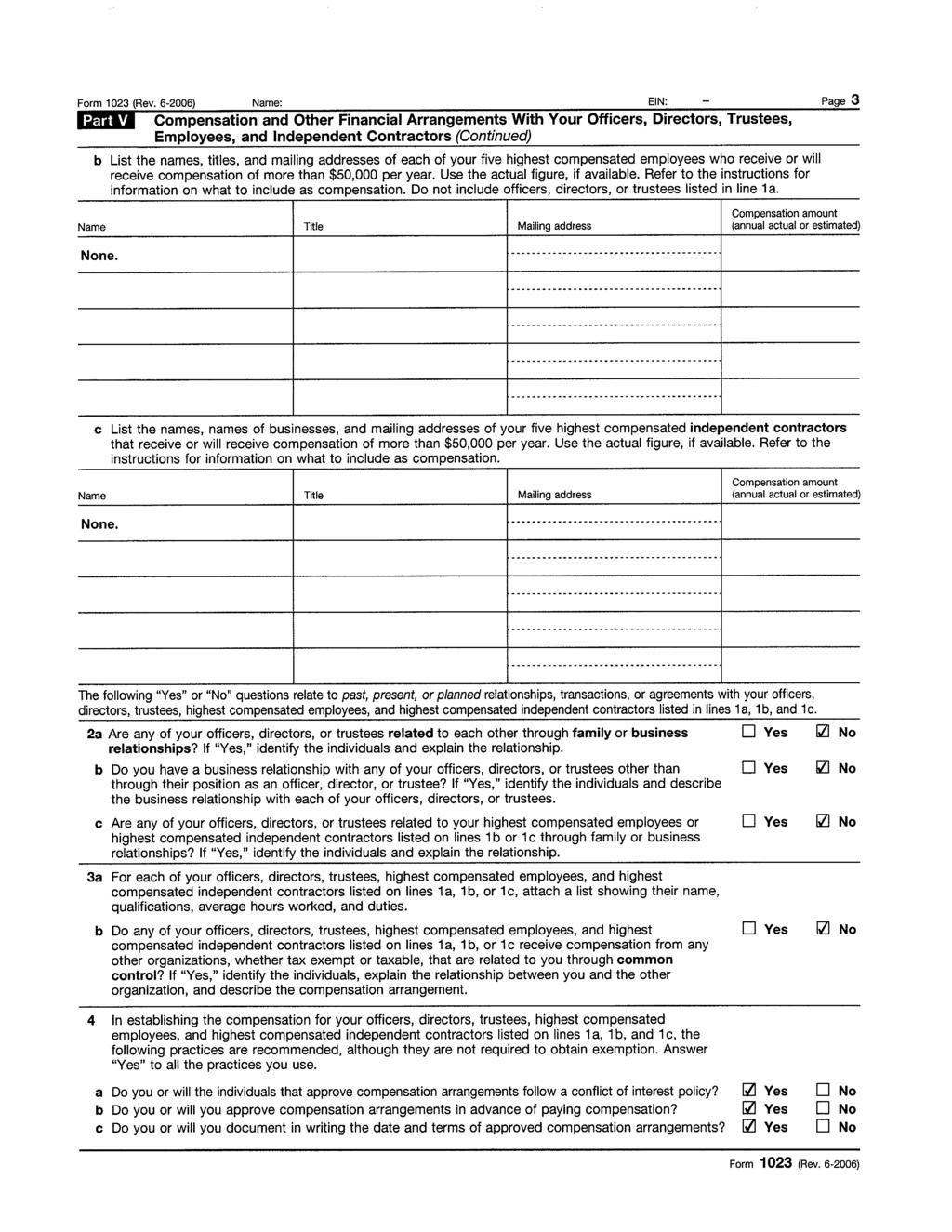

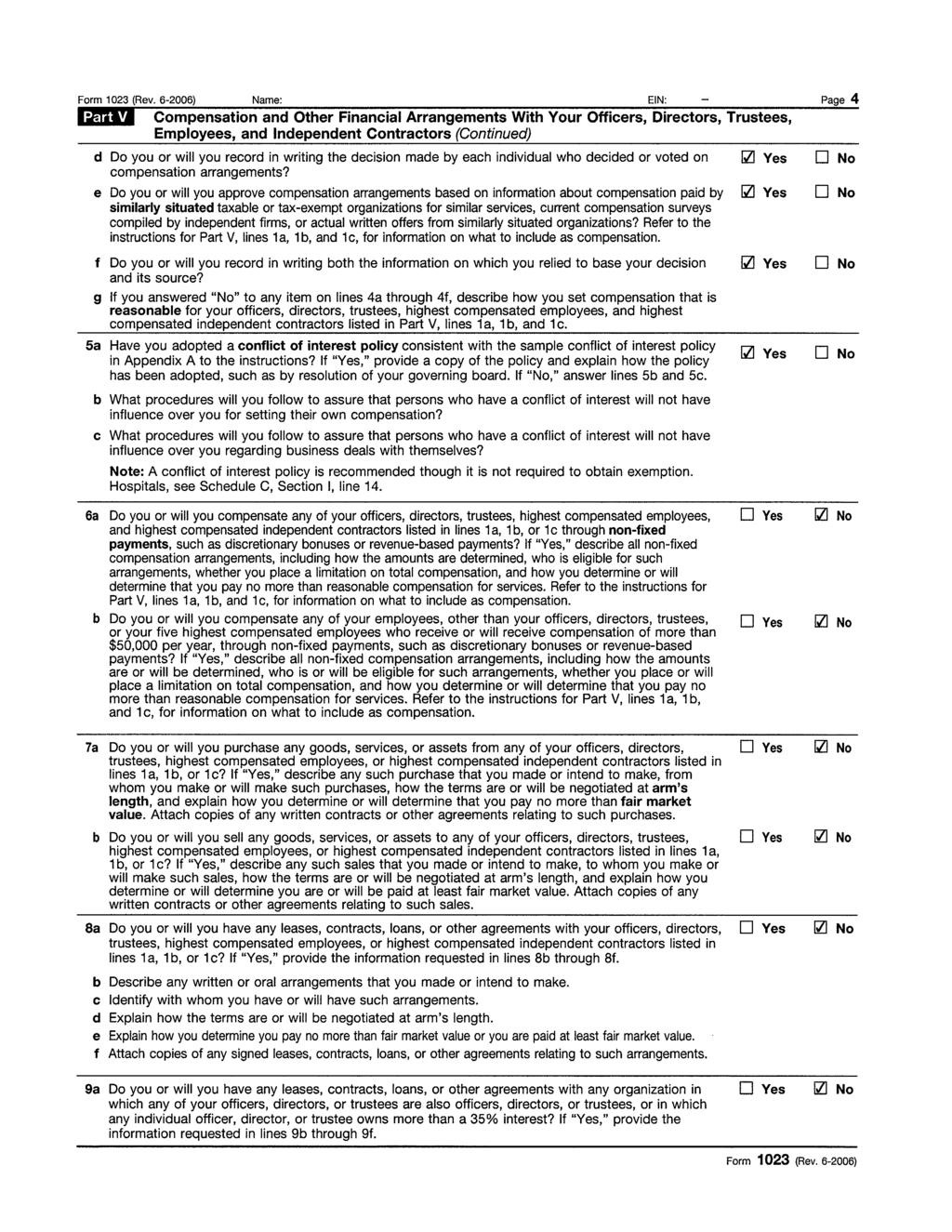

4 IRS Reinstatement Instructions Page 3 of 6 v. Aside from the 3 consecutive years in which the organization failed to file returns or notices, the organization has an established history of complying with its reporting requirements (if any) under the Internal Revenue Code. 3. Annual Information Returns Not Previously Filed Enclose properly completed and executed paper annual information returns (Forms 990 or Forms 990-EZ), whichever is applicable) for all taxable years during and after the consecutive 3-year period that the local PTA was required, but failed, to file an annual information return. If the local PTA was eligible to file a Form 990-N e-postcard (gross receipts less than $50,000) in any taxable year but failed to file either a Form 990-N e-postcard or an annual information return, the local PTA should submit a properly completed and executed Form 990-EZ for that taxable year IF they are applying for retroactive reinstatement. If you are not applying for retroactive reinstate by submitting a reasonable cause statement in 2 above and were eligible to file a Form 990-N, they are not required to file the past Form 990 annual returns. Note: In determining whether to file a Form 990 or Form 990-EZ, review the gross receipts and assets thresholds for the applicable year by following this link Who-Must-File. Tax forms for prior years can be obtained by searching for the applicable form at 4. Form 1023 Header Insert the name of the local PTA, and the local PTA s Employer Identification Number (EIN) in the header on each page of the Form Part I, Item 1 Insert the exact legal name of the local PTA as it appears on the local PTA s articles of incorporation filed with the state of incorporation. 6. Part I, Item 3 Insert the local PTA s mailing address. 7. Part I, Item 4 Insert the local PTA s 9-digit Employer Identification Number. 8. Part I, Item 5 Fill in the month the local PTA s fiscal year ends. For example, fill in 6 for a June 30 year end or 12 for a December 31 year end. 9. Part I, Item 6 Insert the primary contact name, phone number, and fax number for the local PTA. You may use the current president or another officer as the primary contact. 10. Part I, Item 9 Insert the local PTA s website and address, if any. 11. Part I, Item 11 Insert the date the local PTA was incorporated or formed. 12. Part II, Items 1 & 3 Check Yes in Item 1 and No in Item 3 if your local PTA is incorporated. Check No in Item 1 and Yes in Item 3 if your local PTA is not incorporated. Attach a copy of the local PTA s filed Articles of Incorporation, if any.

5 IRS Reinstatement Instructions Page 4 of 6 If you cannot locate a copy, contact the secretary of state of the state of incorporation to order a copy on file. If your local PTA is not incorporated, attach an organizational document indicating your local PTA s name and purpose signed by two members and dated. A sample is attached. Fill in the date of original formation. 13. Part II, Item 5 Attach a copy of the local PTA s Bylaws. Complete the enclosed Bylaws Certification, obtain the signature of an officer, and attach it to the front of the Bylaws. Please contact your state PTA office if you need your unit s bylaws. 14. Part III, Item 1 Indicate where in the local PTA s articles of incorporation, or organizational document, that its purposes are restricted to exempt purposes such as charitable and/or educational purposes. 15. Part III, Item 2 Indicate where in the local PTA s bylaws that upon dissolution, assets must be exclusively used for exempt purposes such as charitable and/or educational purposes. 16. Part V, Item 1a Attach a separate sheet of paper listing the names of all officers and all directors, their respective titles, and mailing addresses. For example, indicate John Smith, President and Director, 123 Main Street, Chicago Illinois For Item 1b and 1c, we have assumed no employee or independent contractors received more than 50,000 per year. If there are such employees or independent contractors, please list them on the sheet of paper as well. 17. Part V, Item 5a Although not required, the IRS recommends organizations adopt a conflicts of interest policy. If you have not adopted such a policy, attached is a sample Conflicts of Interest Policy for the local PTA to adopt. A copy of this policy, or the local PTA s own policy, should be included in the attachment to Form Part IX If your organization has been in existence for 5 or more completed tax years, provide a statement of revenues and expenses for each of the past 5 completed tax years, and complete the balance sheet. For example, if your organization was formed in 2006 or earlier, you would provide a statement of revenues and expenses for 2006, 2007, 2008, 2009, and 2010, along with the balance sheet for The statements of revenue and expenses, and balance sheet should be included separately in the attachment to Form If your organization has not been in existence for more than 5 completed tax years complete the statement of revenues and expenses for each year in existence and a reasonable good faith estimate of future finances for a total of 4 years, along with a balance sheet for the most recently completed fiscal year. For example, if you organization was formed in 2008, you would provide a statement of revenues and expenses for 2008, 2009, and 2010, along with projections for 2011, 2012, 2013, and 2014 along with a balance sheet for 2010.

6 IRS Reinstatement Instructions Page 5 of 6 Note: The directions for Part IX included on Form 1023 have since been revised and are not current. Please follow the instructions we are providing. 19. Part X, Item 5 & 6 Leave blank since the instructions for this section have been superseded. 20. Part XI, Fee Indicate whether the local PTA s annual gross receipts average $10,000 or more and whether as a result you are eligible for the reduced fee. Note that the instructions in Form 1023 on fees have been superseded. The current fee structure is as follows: - $400 for organizations whose gross receipts do not exceed $10,000 or less annually over a 4-year period. - $850 for organizations whose gross receipts exceed $10,000 annually over a 4-year period. 21. Part XI, Signature Type in the local PTA officer s name and title and have the local PTA officer sign the form on Page Check Make out a checking payable to the United States Treasury in the amount of $850 (or $400 if annual gross receipts do not exceed $10,000). 23. Checklist On the second page of the Checklist, fill in the location of the tax-exempt purposes and dissolution provisions. This will match the response given to Part III, Items 1 & Assemble Documents in the Following Order a. Check made payable to the United States Treasury in the appropriate amount. b. Cover Letter from Local PTA to IRS. c. Reasonable Cause Statement Signed by officer. d. Forms 990 or Forms 990-EZ for all taxable years not previously filed. e. Copy of Checklist for IRS Form f. IRS Form Signed by officer. g. Attachment to IRS Form h. Articles of Incorporation, or other organizational document. i. Bylaws Certification signed by officer followed by Bylaws. j. List of Officers and Directors. k. Conflict of Interest Policy. l. Statements of Revenues and Expenses. 25. Mailing Mail the documents and attachments, along with the check, to the address in the IRS cover letter. Note that the IRS address in the Checklist has been revised and is not up-to-date. The address on the sample cover letter is the correct address. Write Automatically Revoked on the top of the envelope. This is required to indicate to

7 IRS Reinstatement Instructions Page 6 of 6 the IRS that the local PTA may be eligible for retroactive reinstatement of its exempt status. 26. IRS Processing Within a few weeks after your package is sent to the IRS, you should receive a notification letter from the IRS indicating your materials have been received and are being reviewed. IRS processing times for applications for tax exemption vary from several months to a year or more. You may be contacted by the IRS if they need additional information to make a determination. Once your local PTA s tax exemption has been reinstated, you will receive an IRS determination letter.

8 Date: Internal Revenue Service P.O. Box Covington, KY Name: Dear Sir/Madam: On behalf of the applicant, enclosed herewith are the following documents: 1. Reasonable Cause Statement; 2. Information Returns (Forms 990 or 990-EZ) Not Filed for Prior Years; 3. Form 1023 Application for Recognition of Exemption; 4. Attachment to Form 1023; 5. Articles of Incorporation, if any, or other organizational document; 6. Bylaws and Bylaws Certification; 7. Conflict of Interest Policy; 8. List of Officers and Directors; 9. Statements of Revenue and Expenses; and 10. Check ($400 or $850) - User Fee Payable to Internal Revenue Service. By filing this application, the applicant is seeking relief under IRS Notice and requests retroactive reinstatement of its tax exemption to the date of automatic revocation. Sincerely, Title: Enclosures

9 ATTACHMENT TO FORM 1023 By filing this application, the applicant is seeking relief under IRS Notice and requests retroactive reinstatement of its tax exemption to the date of automatic revocation. Part IV Narrative Description of Activities The applicant was organized exclusively for charitable and educational purposes to promote children s health, well-being, and educational success through strong parent, family, and community involvement. The applicant offers a variety of programs to help parents, students, and communities in children s development. Programs promote topics such as volunteer work, after school programs, and a healthy lifestyle. The applicant also hosts events to engage parents in local schools and helps build family-school partnerships. The applicant recognizes and honors parents, teachers, and other leaders in the area of child advocacy. In fulfilling its mission, the applicant collaborates with other organizations to benefit children. In sum, the applicant serves as a resource for parents interested in student success. Part V Item 1a. Attached is a list of the names, titles, and mailing addresses of all of the officers and directors of the applicant. Officers and directors do not receive any compensation. Item 3a. The officers and directors spend approximately 5 to 10 hours per month working on the applicant s matters. The officers and directors are parents interested in the educational development of children, and govern and develop programs for the benefits of children in schools. Part VI Item 1. The applicant generally provides educational programming, materials, and events. See Narrative Description of Activities in Part IV. Part VIII 1

10 Item 4a, d. The applicant encourages donations and contributions from parents and may engage in fundraising activities such as candy sales in its local community. Item 15. The applicant is chartered by its state PTA and is also affiliated with the National PTA. Part IX See the attached statements of revenues and expenses, and balance sheet, for the applicable years. 2

11 Bylaws Certification THE UNDERSIGNED hereby confirms that attached hereto is a true and correct copy of the Bylaws, as of the date hereof. Name: Title: Date:

12 Organizational Document of We are an unincorporated association organized exclusively for charitable and educational purposes to promote children s health, well-being, and educational success through strong parent, family, and community involvement. 1. The association is formed exclusively for charitable and educational purposes, including, for such purposes, the making of distributions to organizations that qualify as exempt organizations under Section 501(c)(3) of the Internal Revenue Code of 1986 (or the corresponding provision of any future United States Internal Revenue Law). 2. No part of the net earnings of the association shall inure to the benefit of, or be distributable to its members, directors, officers, or other private persons, except that the association shall be authorized and empowered to pay reasonable compensation for services rendered and to make payments and distributions in furtherance of the purposes set forth in Section 4 hereof. No substantial part of the activities of the association shall be the carrying on of propaganda, or otherwise attempting to influence legislation, and the association shall not participate in, or intervene in (including the publishing or distribution of statements) any political campaign on behalf of (or in opposition to) any candidate for public office. 3. Notwithstanding any other provisions of these articles, the association shall not carry on any other activities not permitted to be carried on (a) by a corporation exempt from Federal income tax under Section 501(c)(3) of the Internal Revenue Code of 1986 (or the corresponding provision of any future United States Internal Revenue Law), or (b) by a corporation, contributions to which are deductible under Section 170(c)(2) of the Internal Revenue Code of 1986 (or the corresponding provision of any future United States Internal Revenue Law). 4. Upon the dissolution of the association, the Board of Directors shall, after paying or making provision for the payment of all of the liabilities of the association, dispose of all of the assets of the association exclusively for the purposes of the association in such manner, or to such organization or organizations organized and operated exclusively for charitable, educational, religious, or scientific purposes as shall at the time qualify as an exempt organization or organizations under Section 501(c)(3) of the Internal Revenue Code of 1986 (or the corresponding provision of any future United States Internal Revenue Law), as the Board of Directors shall determine. Date Formed: Member Member

13 Conflict of Interest Policy Article I Purpose The purpose of the conflict of interest policy is to protect the interests of this tax-exempt organization, (the Organization ), when it is contemplating entering into a transaction or arrangement that might benefit the private interest of an officer or director of the Organization or might result in a possible excess benefit transaction. This policy is intended to supplement but not replace any applicable state and federal laws governing conflict of interest applicable to nonprofit and charitable organizations. 1. Interested Person Article II Definitions Any director, principal officer, or member of a committee with governing board delegated powers, who has a direct or indirect financial interest, as defined below, is an interested person. 2. Financial Interest A person has a financial interest if the person has, directly or indirectly, through business, investment, or family: a. An ownership or investment interest in any entity with which the Organization has a transaction or arrangement, b. A compensation arrangement with any entity or individual with which the Organization has a transaction or arrangement, or c. A proposal ownership or investment interest in, or compensation arrangement with, any entity or individual with which the Organization is negotiating a transaction or arrangement. Compensation includes direct and indirect remuneration as well as gifts or favors that are not insubstantial. A financial interest is not necessarily a conflict of interest. Under Article III, Section 2, a person who has a financial interest may have a conflict of interest only if the appropriate governing board or committee decides that a conflict of interest exists.

14 Article III Procedures a. In connection with any actual or possible conflict of interest, an interested person must disclose the existence of the financial interest and be given the opportunity to disclose all material facts to the directors and members of committees with governing board delegated powers considering the proposed transaction or arrangement. b. The remaining board or committee members shall decide if a conflict of interest exists. c. After disclosure of the financial interest and all material facts, and after any discussion with the interested person, he/she shall leave the governing board or committee meeting while the determination of a conflict of interest is discussed and voted upon. d. An interested person may make a presentation at the governing board or committee meeting, but after the presentation, he/she shall leave the meeting during the discussion of, and the vote on, the transaction or arrangement involving the possible conflict of interest.

15 List of Officers and Directors Officer/Director Name Title Mailing Address

16 STATEMENT OF REVENUES & EXPENSES Revenues Year Ending / / Year Ending / / Year Ending / / Year Ending / / Year Ending / / Membership dues Contributions, gifts, grants, etc. Total Revenue Expenses Printing, publications, & postage Webpage Newsletter Bank fees Insurance Miscellaneous Supplies Telephone Total Expenses NET INCOME Balance Sheet as of Assets Cash Other Assets Liabilities Accounts Payable Other Liabilities

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

Make check payable to : United States Treasury

In 2006 a bill was passed by congress requiring that Non Profit Organizations submit their 990: Tax Return for Non Profit Organizations, even if no revenue was generated. This bill went into effect in

In 2006 a bill was passed by congress requiring that Non Profit Organizations submit their 990: Tax Return for Non Profit Organizations, even if no revenue was generated. This bill went into effect in

Applicable Sections: Revenue Procedure SECTION 1. PURPOSE

Applicable Sections: 26 CFR 1.6033-2. Returns by exempt organizations (taxable years beginning after December 31, 1969) and returns by certain nonexempt organizations (taxable years beginning after December

Applicable Sections: 26 CFR 1.6033-2. Returns by exempt organizations (taxable years beginning after December 31, 1969) and returns by certain nonexempt organizations (taxable years beginning after December

How to Get Your Nonprofit Back in Good Standing

How to Get Your Nonprofit Back in Good Standing Texas nonprofits are subject to numerous complicated laws and regulations, filing and reporting requirements. Failure to comply with these requirements can

How to Get Your Nonprofit Back in Good Standing Texas nonprofits are subject to numerous complicated laws and regulations, filing and reporting requirements. Failure to comply with these requirements can

APPLICATION FOR INCLUSION IN THE UNITED METHODIST CHURCH GROUP TAX EXEMPTION RULING. Category II Organizations

APPLICATION FOR INCLUSION IN THE UNITED METHODIST CHURCH GROUP TAX EXEMPTION RULING Category II Organizations A. General Information and Instructions A1. In 1974, the IRS issued a group tax exemption ruling

APPLICATION FOR INCLUSION IN THE UNITED METHODIST CHURCH GROUP TAX EXEMPTION RULING Category II Organizations A. General Information and Instructions A1. In 1974, the IRS issued a group tax exemption ruling

Federal Tax-Exempt Status 501(c)(3) Organizations

(3) Organizations") Federal Tax-Exempt Status 501(c)(3) Organizations Most PTAs are classified as tax-exempt 501(c)(3) public charities under the Internal Revenue Code (IRC). One major advantage for organizations that are

Federal Tax-Exempt Status 501(c)(3) Organizations Most PTAs are classified as tax-exempt 501(c)(3) public charities under the Internal Revenue Code (IRC). One major advantage for organizations that are

BEST PRACTICES. Best Practices #125: 501(c)(3) Chapter Organization Cover Letter and Structure

(3) Chapter Organization Cover Letter and Structure") BEST PRACTICES Best Practices #125: 501(c)(3) Chapter Organization Cover Letter and Structure A lot has changed since the original Best Practices Article for Tax-Exempt Status was posted in 2009. Most

BEST PRACTICES Best Practices #125: 501(c)(3) Chapter Organization Cover Letter and Structure A lot has changed since the original Best Practices Article for Tax-Exempt Status was posted in 2009. Most

Federal Financial Requirements

American Society of Health-System Pharmacists Federal Financial Requirements ASHP s Financial Toolkit for Affiliates Kimberlee Berry [Pick the date] FEDERAL REQUIREMENTS NOTE: All IRS forms can be accessed

American Society of Health-System Pharmacists Federal Financial Requirements ASHP s Financial Toolkit for Affiliates Kimberlee Berry [Pick the date] FEDERAL REQUIREMENTS NOTE: All IRS forms can be accessed

HOW TO APPLY FOR TAX-EXEMPT STATUS. Table of Contents

HOW TO APPLY FOR TAX-EXEMPT STATUS Table of Contents Basics of Tax Exemption Who Must File a Form 1023 501(c)(3) Requirements Organizational Test Operational Test Form 1023 Part I. Basic Information about

HOW TO APPLY FOR TAX-EXEMPT STATUS Table of Contents Basics of Tax Exemption Who Must File a Form 1023 501(c)(3) Requirements Organizational Test Operational Test Form 1023 Part I. Basic Information about

Kentucky Extension Homemakers Association

Kentucky Extension Homemakers Association April 12, 2010 KEHA Leaders and FCS Agents, In 2007, the Internal Revenue Service (IRS) changed filing requirements for non profit organizations. For the past

Kentucky Extension Homemakers Association April 12, 2010 KEHA Leaders and FCS Agents, In 2007, the Internal Revenue Service (IRS) changed filing requirements for non profit organizations. For the past

New IRS Procedures for Reinstating Revoked Tax-Exempt Status of Organizations. Molly Hayes Sharbaugh Reed Smith LLP Pittsburgh, PA

FEBRUARY 2014 EXECUTIVE SUMMARY TAX AND FINANCE PRACTICE GROUP New IRS Procedures for Reinstating Revoked Tax-Exempt Status of Organizations Molly Hayes Sharbaugh Reed Smith LLP Pittsburgh, PA The Internal

FEBRUARY 2014 EXECUTIVE SUMMARY TAX AND FINANCE PRACTICE GROUP New IRS Procedures for Reinstating Revoked Tax-Exempt Status of Organizations Molly Hayes Sharbaugh Reed Smith LLP Pittsburgh, PA The Internal

Thank you! 7/26/2011 For information purposes only. NOT LEGAL OR TAX ADVICE.

On July 14, a webinar called How to reinstate and maintain your IRS tax exempt status was conducted. Weʹre sorry to report that some of the information was inaccurate. The presenters did present accurate

On July 14, a webinar called How to reinstate and maintain your IRS tax exempt status was conducted. Weʹre sorry to report that some of the information was inaccurate. The presenters did present accurate

IRS 501(C)(3) GROUP EXEMPTION CAPABILITY

(3) GROUP EXEMPTION CAPABILITY") IMPORTANT NOTICE TO ALL STATE and LOCAL PRESIDENTS IRS 501(C)(3) GROUP EXEMPTION CAPABILITY MTNA has been authorized by the Internal Revenue Service to maintain a group exemption roster for its affiliate

IMPORTANT NOTICE TO ALL STATE and LOCAL PRESIDENTS IRS 501(C)(3) GROUP EXEMPTION CAPABILITY MTNA has been authorized by the Internal Revenue Service to maintain a group exemption roster for its affiliate

Chapter Tax Compliance Requirements

Chapter Tax Compliance Requirements Federal tax law provides income tax exemption to nonprofit organizations. The Pension Protection Act of 2006 created the requirement for small orgaizatrions, defined

Chapter Tax Compliance Requirements Federal tax law provides income tax exemption to nonprofit organizations. The Pension Protection Act of 2006 created the requirement for small orgaizatrions, defined

NOTE REGARDING THE SAMPLE DOCUMENTS: This sample document is provided for informational purposes only and does not constitute legal advice or counsel.

NOTE REGARDING THE SAMPLE DOCUMENTS: This sample document is provided for informational purposes only and does not constitute legal advice or counsel. CONFLICT OF INTEREST POLICY Resolution of the Board

NOTE REGARDING THE SAMPLE DOCUMENTS: This sample document is provided for informational purposes only and does not constitute legal advice or counsel. CONFLICT OF INTEREST POLICY Resolution of the Board

Form 1023 Checklist (Revised June 2006)

") Form 1023 Checklist (Revised June 2006) Application for Recognition of Exemption under Section 501(c)(3) of the Internal Revenue Code te. Retain a copy of the completed Form 1023 in your permanent records.

Form 1023 Checklist (Revised June 2006) Application for Recognition of Exemption under Section 501(c)(3) of the Internal Revenue Code te. Retain a copy of the completed Form 1023 in your permanent records.

2008 Instructions for Form 990 Return of Organization Exempt From Income Tax Contents A B C D E F J A B C D E F G

2008 Instructions for Form 990 Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private foundation)

2008 Instructions for Form 990 Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private foundation)

September 11, Internal Revenue Service P.O. Box Covington, KY

September 11, 2014 Internal Revenue Service P.O. Box 12192 Covington, KY 41012-0192 Re: Application for Recognition of Exempt Status under Section 501(c)(3) of the Internal Revenue Code Pennsylvania Public

September 11, 2014 Internal Revenue Service P.O. Box 12192 Covington, KY 41012-0192 Re: Application for Recognition of Exempt Status under Section 501(c)(3) of the Internal Revenue Code Pennsylvania Public

Short Form Return of Organization Exempt From Income Tax

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(a)(1) of the Internal Revenue Code (except private

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(a)(1) of the Internal Revenue Code (except private

A PTA can only engage in an insubstantial amount of lobbying activity.

Most PTAs are classified as taxexempt 501(c)(3) public charities under the Internal Revenue Code (IRC). One major advantage for organizations that are exempt under Section 501(c)(3) of the IRC is that

Most PTAs are classified as taxexempt 501(c)(3) public charities under the Internal Revenue Code (IRC). One major advantage for organizations that are exempt under Section 501(c)(3) of the IRC is that

Walk Like An Exemption: Fast-Track and Maintain the Right Tax Exemption

Walk Like An Exemption: Fast-Track and Maintain the Right Tax Exemption California Charter Schools Conference March 17, 2015 Kevin M. Davis Greta A. Proctor 1 What We Will Cover in This Program What Is

Walk Like An Exemption: Fast-Track and Maintain the Right Tax Exemption California Charter Schools Conference March 17, 2015 Kevin M. Davis Greta A. Proctor 1 What We Will Cover in This Program What Is

RESTATED AND AMENDED ARTICLES OF INCORPORATION CENTRAL INDIANA LINUX USERS GROUP (CINLUG), INC.

, INC.") RESTATED AND AMENDED ARTICLES OF INCORPORATION CENTRAL INDIANA LINUX USERS GROUP (CINLUG), INC. The undersigned officer of the Central Indiana Linux Users Group (the "Corporation"), pursuant to the provisions

RESTATED AND AMENDED ARTICLES OF INCORPORATION CENTRAL INDIANA LINUX USERS GROUP (CINLUG), INC. The undersigned officer of the Central Indiana Linux Users Group (the "Corporation"), pursuant to the provisions

A For the 2010 calendar year, or tax year beginning, 2010, and ending, 20 D Employer identification number

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(1) of the Internal Revenue Code (except black lung

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(1) of the Internal Revenue Code (except black lung

SAFARI CLUB INTERNATIONAL

SAFARI CLUB INTERNATIONAL Form 990 Compliance - Sample Governance Policies These sample policies may be adopted by a Chapter that is tax-exempt under Section 501(c)(4) of the Code in order to comply with

SAFARI CLUB INTERNATIONAL Form 990 Compliance - Sample Governance Policies These sample policies may be adopted by a Chapter that is tax-exempt under Section 501(c)(4) of the Code in order to comply with

2. The Articles of Incorporation of this corporation are amended and restated to read as follows: ARTICLE I Name

AMENDED AND RESTATED ARTICLES OF INCORPORATION OF ASSOCIATED STUDENTS INCORPORATED OF CALIFORNIA STATE UNIVERSITY, STANISLAUS A California Nonprofit Public Benefit Corporation The undersigned certify that:

AMENDED AND RESTATED ARTICLES OF INCORPORATION OF ASSOCIATED STUDENTS INCORPORATED OF CALIFORNIA STATE UNIVERSITY, STANISLAUS A California Nonprofit Public Benefit Corporation The undersigned certify that:

CHAR410, CHAR410-A, CHAR410-R

New York State Department of Law (Office of the Attorney General) Charities Bureau - Registration Section Instructions for Forms CHAR410, CHAR410-A, CHAR410-R and Schedule E Registration/Amended Registration/Re-Registration

New York State Department of Law (Office of the Attorney General) Charities Bureau - Registration Section Instructions for Forms CHAR410, CHAR410-A, CHAR410-R and Schedule E Registration/Amended Registration/Re-Registration

IRS Reporting Compliance for 501(c)(3) Organizations

(3) Organizations") IRS Reporting Compliance for 501(c)(3) Organizations August 28, 2016 Mark C. Franco Associate Counsel Whiteford, Taylor & Preston, L.L.P. 3190 Fairview Park Dr., Suite 800 Falls Church, VA 22042 703-280-3383

IRS Reporting Compliance for 501(c)(3) Organizations August 28, 2016 Mark C. Franco Associate Counsel Whiteford, Taylor & Preston, L.L.P. 3190 Fairview Park Dr., Suite 800 Falls Church, VA 22042 703-280-3383

AMENDED AND RESTATED ARTICLES OF INCORPORATION COLORADO ARCHAEOLOGICAL SOCIETY, INC.

AMENDED AND RESTATED ARTICLES OF INCORPORATION OF COLORADO ARCHAEOLOGICAL SOCIETY, INC. In accordance with the Colorado Revised Nonprofit Corporation Act, as amended from time to time (together with any

AMENDED AND RESTATED ARTICLES OF INCORPORATION OF COLORADO ARCHAEOLOGICAL SOCIETY, INC. In accordance with the Colorado Revised Nonprofit Corporation Act, as amended from time to time (together with any

ARTICLES OF INCORPORATION OF INDIANA RECYCLING COALITION, INC.

ARTICLES OF INCORPORATION OF INDIANA RECYCLING COALITION, INC. Indiana Recycling Coalition, Inc. (the Corporation ), having accepted the provisions of the Indiana Nonprofit Corporation Act of 1991, as

ARTICLES OF INCORPORATION OF INDIANA RECYCLING COALITION, INC. Indiana Recycling Coalition, Inc. (the Corporation ), having accepted the provisions of the Indiana Nonprofit Corporation Act of 1991, as

Short Form Return of Organization Exempt From Income Tax

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(a)(1) of the Internal Revenue Code (except private

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(a)(1) of the Internal Revenue Code (except private

NONPROFIT MEDICAL ORGANIZATION

NONPROFIT MEDICAL ORGANIZATION Qualifications, Requirements and Necessary Documentation Texas Administrative Code Rule 402.420 This guide is to be used to assist organizations in completing an original

NONPROFIT MEDICAL ORGANIZATION Qualifications, Requirements and Necessary Documentation Texas Administrative Code Rule 402.420 This guide is to be used to assist organizations in completing an original

Short Form Return of Organization Exempt From Income Tax

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(a)(1) of the Internal Revenue Code (except private

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(a)(1) of the Internal Revenue Code (except private

501(c)(3) for Parent Groups. The Basics

(3) for Parent Groups. The Basics") 501(c)(3) for Parent Groups The Basics Do 501(c)(3), tax exemption, and nonprofit all mean the same thing? People tend to use these terms interchangeably, but they have distinct definitions. 501(c)(3)

501(c)(3) for Parent Groups The Basics Do 501(c)(3), tax exemption, and nonprofit all mean the same thing? People tend to use these terms interchangeably, but they have distinct definitions. 501(c)(3)

Setting up a Tax-Exempt (510c3) Non-Profit California Corporation

Non-Profit California Corporation") 1 Setting up a Tax-Exempt (510c3) Non-Profit California Corporation This document is intended to provide an outline for actions that may be performed during the process of creating a non-profit California

1 Setting up a Tax-Exempt (510c3) Non-Profit California Corporation This document is intended to provide an outline for actions that may be performed during the process of creating a non-profit California

Financial Reports and Certification and IRS Electronic Filing Overview

Financial Reports and Certification and IRS Electronic Filing Overview April Powers-Matthews, Treasurer Kevin Coleman, Financial Secretary Blacks In Government Region XI Council 1 Financial Reports and

Financial Reports and Certification and IRS Electronic Filing Overview April Powers-Matthews, Treasurer Kevin Coleman, Financial Secretary Blacks In Government Region XI Council 1 Financial Reports and

Like many CPAs, you may be planning

THE PPC NONPROFIT UPDATE, MARCH 2014, VOLUME 21, NO. 3 THE PPC NONPROFIT UPDATE Getting Ready for Your Engagements Like many CPAs, you may be planning your June 30th audits of nonprofit organization clients.

THE PPC NONPROFIT UPDATE, MARCH 2014, VOLUME 21, NO. 3 THE PPC NONPROFIT UPDATE Getting Ready for Your Engagements Like many CPAs, you may be planning your June 30th audits of nonprofit organization clients.

Transitional Relief under Internal Revenue Code 6033(j) for Small. This notice provides transitional relief for certain small organizations that have

for Small. This notice provides transitional relief for certain small organizations that have") Part III - Administrative, Procedural, and Miscellaneous Transitional Relief under Internal Revenue Code 6033(j) for Small Organizations Notice 2011-43 This notice provides transitional relief for certain

Part III - Administrative, Procedural, and Miscellaneous Transitional Relief under Internal Revenue Code 6033(j) for Small Organizations Notice 2011-43 This notice provides transitional relief for certain

Section 1: Name: The name of the organization is Long Beach ALIVE (ALIVE is an acronym for Alternatives to Living In a Violent Environment).

.") Long Beach ALIVE Bylaws Article 1 Organization Type and Purpose: Name: The name of the organization is Long Beach ALIVE (ALIVE is an acronym for Alternatives to Living In a Violent Environment). In January,

Long Beach ALIVE Bylaws Article 1 Organization Type and Purpose: Name: The name of the organization is Long Beach ALIVE (ALIVE is an acronym for Alternatives to Living In a Violent Environment). In January,

Articles of Incorporation

MINNESOTA SCHOOL NUTRITION ASSOCIATION Articles of Incorporation Amended 2007 The Amended Articles of Incorporation are on file with the State of Minnesota. Filed September 27, 2007. Table of Contents

MINNESOTA SCHOOL NUTRITION ASSOCIATION Articles of Incorporation Amended 2007 The Amended Articles of Incorporation are on file with the State of Minnesota. Filed September 27, 2007. Table of Contents

Conflict of Interest Policy Packet

Conflict of Interest Policy Packet The IRS wants to know if your YMCA has a written conflict of interest policy and a procedure for reporting potential conflicts of interest. This packet includes a Sample

Conflict of Interest Policy Packet The IRS wants to know if your YMCA has a written conflict of interest policy and a procedure for reporting potential conflicts of interest. This packet includes a Sample

Form 1023 Checklist (Revised June 2006)

") Form 1023 Checklist (Revised June 2006) Application for Recognition of Exemption under Section 501(c)(3) of the Internal Revenue Code te. Retain a copy of the completed Form 1023 in your permanent records.

Form 1023 Checklist (Revised June 2006) Application for Recognition of Exemption under Section 501(c)(3) of the Internal Revenue Code te. Retain a copy of the completed Form 1023 in your permanent records.

PREPARATION OF TAX FORM 990

PREPARATION OF TAX FORM 990 The Temple with Combined Units return and Shrine Clubs Group return qualify under IRS Code Section 501(c)(10), Shriners International group exemption number 0229. Shrine temple

PREPARATION OF TAX FORM 990 The Temple with Combined Units return and Shrine Clubs Group return qualify under IRS Code Section 501(c)(10), Shriners International group exemption number 0229. Shrine temple

Information for Sumner County School Support Organizations

Information for Sumner County School Support Organizations School Support Organization (SSO) Start Up Instructions and General Information These suggestions are not to be considered legal advice. You may

Information for Sumner County School Support Organizations School Support Organization (SSO) Start Up Instructions and General Information These suggestions are not to be considered legal advice. You may

Application for Recognition of Exemption Under Section 501(c)(3) of the Internal Revenue Code

(3) of the Internal Revenue Code") Form 1023 (Rev. December 2013) Department of the Treasury Internal Revenue Service Application for Recognition of Exemption Under Section 501(c)(3) of the Internal Revenue Code (Use with the June 2006

Form 1023 (Rev. December 2013) Department of the Treasury Internal Revenue Service Application for Recognition of Exemption Under Section 501(c)(3) of the Internal Revenue Code (Use with the June 2006

Starting a Nonprofit Frequently Asked Questions

Starting a Nonprofit Frequently Asked Questions Q. Are nonprofit and tax-exempt the same thing? A. No. A nonprofit is a type of corporation that is formed at the state level. Nonprofit and notfor-profit

Starting a Nonprofit Frequently Asked Questions Q. Are nonprofit and tax-exempt the same thing? A. No. A nonprofit is a type of corporation that is formed at the state level. Nonprofit and notfor-profit

Financial Reports and Certification and IRS Electronic Filing Overview

Financial Reports and Certification and IRS Electronic Filing Overview April Powers-Matthews, Treasurer Kevin Coleman, Financial Secretary Region XI Council 1 Financial Reports and Certification and IRS

Financial Reports and Certification and IRS Electronic Filing Overview April Powers-Matthews, Treasurer Kevin Coleman, Financial Secretary Region XI Council 1 Financial Reports and Certification and IRS

Short Form Return of Organization Exempt From Income Tax

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private

Number and street (or P.O. box, if mail is not delivered to street address) Room/suite

Room/suite") Form 990-EZ Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(1) of the Internal Revenue Code (except black lung benefit trust or private foundation) Sponsoring organizations

Form 990-EZ Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(1) of the Internal Revenue Code (except black lung benefit trust or private foundation) Sponsoring organizations

Return of Organization Exempt From Income Tax

Form 990 Return of Organization Exempt From Income Tax OMB No. 1545-0047 Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung 2010 benefit trust or private foundation)

Form 990 Return of Organization Exempt From Income Tax OMB No. 1545-0047 Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung 2010 benefit trust or private foundation)

Office of the Minnesota Secretary of State Minnesota Nonprofit Corporation/Articles of Incorporation

Office of the Minnesota Secretary of State Minnesota Nonprofit Corporation/Articles of Incorporation Minnesota Statutes, Chapter 317A The individual(s) listed below who is (are each) 18 years of age or

Office of the Minnesota Secretary of State Minnesota Nonprofit Corporation/Articles of Incorporation Minnesota Statutes, Chapter 317A The individual(s) listed below who is (are each) 18 years of age or

Instructions for Form 990-EZ

2009 Instructions for Form 990-EZ Short Form Return of Organization Exempt From Income Tax Under Section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private

2009 Instructions for Form 990-EZ Short Form Return of Organization Exempt From Income Tax Under Section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private

COMMONWEALTH OF PUERTO RICO

Form 480.70(OE) Rev. 05.16 Liquidator: Reviewer: Field Audited by: Date / / R M N Organization's Name COMMONWEALTH OF PUERTO RICO 20 20 DEPARTMENT OF THE TREASURY Informative Return for Income Tax Exempt

Form 480.70(OE) Rev. 05.16 Liquidator: Reviewer: Field Audited by: Date / / R M N Organization's Name COMMONWEALTH OF PUERTO RICO 20 20 DEPARTMENT OF THE TREASURY Informative Return for Income Tax Exempt

Nonprofit Governance and Management, Third Edition

INTERNAL REVENUE SERVICE (IRS) SAMPLE CONFLICT OF INTEREST POLICY AND SAMPLE BYLAWS PROVISION ON CONFLICT OF INTEREST PROCEDURES Document 1 Sample Conflict of Interest Policy Practical Advice Note: The

INTERNAL REVENUE SERVICE (IRS) SAMPLE CONFLICT OF INTEREST POLICY AND SAMPLE BYLAWS PROVISION ON CONFLICT OF INTEREST PROCEDURES Document 1 Sample Conflict of Interest Policy Practical Advice Note: The

Form 990 Return of Organization Exempt From Income Tax

OMB No. 1545-0047 Form 990 Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung 2011 benefit trust or private foundation)

OMB No. 1545-0047 Form 990 Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung 2011 benefit trust or private foundation)

RESTATED ARTICLES OF INCORPORATION UNITED WAY OF WAPELLO COUNTY

RESTATED ARTICLES OF INCORPORATION OF UNITED WAY OF WAPELLO COUNTY TO THE SECRETARY OF THE STATE OF IOWA: Pursuant to the provisions of Section 504.1006 of the Revised Iowa Non-Profit Corporation Act,

RESTATED ARTICLES OF INCORPORATION OF UNITED WAY OF WAPELLO COUNTY TO THE SECRETARY OF THE STATE OF IOWA: Pursuant to the provisions of Section 504.1006 of the Revised Iowa Non-Profit Corporation Act,

GENERAL APPLICATION CHARITABLE SOLICITATIONS

NED PETTUS, JR. Director GENERAL APPLICATION CHARITABLE SOLICITATIONS Dear Applicant: Enclosed is the application for a Charitable Solicitations Permit. It is being sent to you in response to your request,

NED PETTUS, JR. Director GENERAL APPLICATION CHARITABLE SOLICITATIONS Dear Applicant: Enclosed is the application for a Charitable Solicitations Permit. It is being sent to you in response to your request,

Fiscal Fitness for Units: A Guide for Treasurers

Fiscal Fitness for Units: A Guide for Treasurers October 25 th, 2017 Sean M. Hannam NYS PTA Treasurer treasurer@nyspta.org What is a Treasurer? The Treasurer plays a key role in the ongoing operation of

Fiscal Fitness for Units: A Guide for Treasurers October 25 th, 2017 Sean M. Hannam NYS PTA Treasurer treasurer@nyspta.org What is a Treasurer? The Treasurer plays a key role in the ongoing operation of

TAX-EXEMPT ORGANIZATIONS: EFFECTIVE GOVERNANCE AND LEGAL COMPLIANCE VICTOR J. FERGUSON SUZANNE R. GALYARDT VORYS, SATER, SEYMOUR AND PEASE LLP

TAX-EXEMPT ORGANIZATIONS: EFFECTIVE GOVERNANCE AND LEGAL COMPLIANCE VICTOR J. FERGUSON SUZANNE R. GALYARDT VORYS, SATER, SEYMOUR AND PEASE LLP OVERVIEW 1. Organizational Test 2. Operational Test 3. Private

TAX-EXEMPT ORGANIZATIONS: EFFECTIVE GOVERNANCE AND LEGAL COMPLIANCE VICTOR J. FERGUSON SUZANNE R. GALYARDT VORYS, SATER, SEYMOUR AND PEASE LLP OVERVIEW 1. Organizational Test 2. Operational Test 3. Private

GOVERNMENT OF PUERTO RICO

Form 480.70(OE) Rev. 04.17 Liquidator: Reviewer: Field Audited by: Date / / R M N Organization's Name GOVERNMENT OF PUERTO RICO 20 20 DEPARTMENT OF THE TREASURY Informative Return for Income Tax Exempt

Form 480.70(OE) Rev. 04.17 Liquidator: Reviewer: Field Audited by: Date / / R M N Organization's Name GOVERNMENT OF PUERTO RICO 20 20 DEPARTMENT OF THE TREASURY Informative Return for Income Tax Exempt

Incorporating and Tax Exempting Procedures for Friends

Incorporating and Tax Exempting Procedures for Friends Sally Gardner Reed, Executive Director, United for Libraries 2012 by United for Libraries: The Association of Library Trustees, Advocates, Friends

Incorporating and Tax Exempting Procedures for Friends Sally Gardner Reed, Executive Director, United for Libraries 2012 by United for Libraries: The Association of Library Trustees, Advocates, Friends

A For the 2011 calendar year, or tax year beginning, 2011, and ending, 20 D Employer identification number

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(a)(1) of the Internal Revenue Code (except black

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(a)(1) of the Internal Revenue Code (except black

Keeping it Legal: The Dos and DON Ts of Managing Your 501(c)3

3") Keeping it Legal: The Dos and DON Ts of Managing Your 501(c)3 Women s Collective Giving Grantmakers Network 2014 Leadership Forum April 9, 2014 Presented by: Dianne Chipps Bailey A Few Introductory Thoughts

Keeping it Legal: The Dos and DON Ts of Managing Your 501(c)3 Women s Collective Giving Grantmakers Network 2014 Leadership Forum April 9, 2014 Presented by: Dianne Chipps Bailey A Few Introductory Thoughts

2015 Federal Tax Returns

2015 Federal Tax Returns All Knights of Columbus subordinate units in the United States must file an annual informational tax return (IRS Form 990) with the Internal Revenue Service (IRS). This memorandum

2015 Federal Tax Returns All Knights of Columbus subordinate units in the United States must file an annual informational tax return (IRS Form 990) with the Internal Revenue Service (IRS). This memorandum

(c)(3) Applying for 501(c)(3) Tax-Exempt Status,

(3) Applying for 501(c)(3) Tax-Exempt Status,") Tax Exempt and Government Entities EXEMPT ORGANIZATIONS Applying for 501(c)(3) Tax-Exempt Status, Inside: Why apply for 501(c)(3) status? Who is eligible for 501(c)(3) status? What responsibilities accompany

Tax Exempt and Government Entities EXEMPT ORGANIZATIONS Applying for 501(c)(3) Tax-Exempt Status, Inside: Why apply for 501(c)(3) status? Who is eligible for 501(c)(3) status? What responsibilities accompany

A For the 2010 calendar year, or tax year beginning, 2010, and ending, 20 D Employer identification number

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black

Internal Revenue Service P.O. Box 2508, Room 4106 Cincinnati, OH 45201

Department of the Treasury Internal Revenue Service Date: Employer ID number: Person to contact: Contact telephone number: Contact fax number: Employee ID number: Dear The IRS is instituting an optional

Department of the Treasury Internal Revenue Service Date: Employer ID number: Person to contact: Contact telephone number: Contact fax number: Employee ID number: Dear The IRS is instituting an optional

IMPORTANT TAX AND FIDELITY BOND INFORMATION

AMERICAN LEGION AUXILIARY NATIONAL HEADQUARTERS IMPORTANT TAX AND FIDELITY BOND INFORMATION This information is intended to assist Units, Departments, Districts/Counties/Councils in understanding their

AMERICAN LEGION AUXILIARY NATIONAL HEADQUARTERS IMPORTANT TAX AND FIDELITY BOND INFORMATION This information is intended to assist Units, Departments, Districts/Counties/Councils in understanding their

Conflict of Interest Policy

PURPOSE: Conflict of Interest Policy No Board member or committee member of the Albany Public Library (the Library ) shall derive any personal profit or gain, directly or indirectly, by reason of his or

PURPOSE: Conflict of Interest Policy No Board member or committee member of the Albany Public Library (the Library ) shall derive any personal profit or gain, directly or indirectly, by reason of his or

AMENDED AND RESTATED ARTICLES OF INCORPORATION LAKEVILLE HOCKEY BOOSTERS

AMENDED AND RESTATED ARTICLES OF INCORPORATION OF LAKEVILLE HOCKEY BOOSTERS Pursuant to Minn. Stat. 317A.131, 317A.133 and 317A.139, LAKEVILLE HOCKEY BOOSTERS, by action of its Directors on September 14,

AMENDED AND RESTATED ARTICLES OF INCORPORATION OF LAKEVILLE HOCKEY BOOSTERS Pursuant to Minn. Stat. 317A.131, 317A.133 and 317A.139, LAKEVILLE HOCKEY BOOSTERS, by action of its Directors on September 14,

ALCOR CARE TRUST SUPPORTING ORGANIZATION INDEX. 7. IRS Form 1023, Part V, Question Sa (Conflict oflnterest Policy); and

; and") ALCOR CARE TRUST SUPPORTING ORGANIZATION INDEX 1. IRS Form 1023 Checklist; 2. IRS Form 2848, Power of Attorney; 3. IRS Form 1023, Application for Recognition of Exemption; 4. Trust Agreement; 5. IRS Form

ALCOR CARE TRUST SUPPORTING ORGANIZATION INDEX 1. IRS Form 1023 Checklist; 2. IRS Form 2848, Power of Attorney; 3. IRS Form 1023, Application for Recognition of Exemption; 4. Trust Agreement; 5. IRS Form

Edmond Public Schools. Sanctioned Organizations

Edmond Public Schools Sanctioned Organizations Contact Information for EPS Jeanise Wynn, Business Manager Phone: (405) 340-2881 Email: jeanise.wynn@edmondschools.net Debbie Smith, Executive Assistant Phone:

Edmond Public Schools Sanctioned Organizations Contact Information for EPS Jeanise Wynn, Business Manager Phone: (405) 340-2881 Email: jeanise.wynn@edmondschools.net Debbie Smith, Executive Assistant Phone:

990 Preparation Checklist

990 Preparation Checklist The following checklist is intended to help you prepare for Form 990. If you have any questions about this checklist or the form, please contact your Rea advisor or Maribeth Wright,

990 Preparation Checklist The following checklist is intended to help you prepare for Form 990. If you have any questions about this checklist or the form, please contact your Rea advisor or Maribeth Wright,

PARENT ORGANIZATIONS TAX FILING REQUIREMENTS

PARENT ORGANIZATIONS TAX FILING REQUIREMENTS Leland Dushkin, CPA Tax Manager Hereford, Lynch, Sellars & Kirkham, PC ldushkin@hlsk.com 1406 Wilson Road, Suite 100 Conroe, TX 77304 936-756-8127 or 936-441-1338

PARENT ORGANIZATIONS TAX FILING REQUIREMENTS Leland Dushkin, CPA Tax Manager Hereford, Lynch, Sellars & Kirkham, PC ldushkin@hlsk.com 1406 Wilson Road, Suite 100 Conroe, TX 77304 936-756-8127 or 936-441-1338

FORENSIC SPECIALTIES ACCREDITATION BOARD

FORENSIC SPECIALTIES ACCREDITATION BOARD CONFLICT OF INTEREST POLICY Adopted January 27, 2010 PURPOSE The purpose of the conflict of interest policy is to protect Forensic Specialties Accreditation Board's

FORENSIC SPECIALTIES ACCREDITATION BOARD CONFLICT OF INTEREST POLICY Adopted January 27, 2010 PURPOSE The purpose of the conflict of interest policy is to protect Forensic Specialties Accreditation Board's

A For the 2010 calendar year, or tax year beginning 01/01 B Check if applicable:

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black

Shoreline Neighborhood Association Presentation. City of Shoreline, Washington March 19, 2008

Shoreline Neighborhood Association Presentation City of Shoreline, Washington March 19, 2008 Susan Schalla, Attorney Davis Wright Tremaine LLP 1201 Third Avenue, Suite 2200 Seattle, WA 98101 (206) 757-7700

Shoreline Neighborhood Association Presentation City of Shoreline, Washington March 19, 2008 Susan Schalla, Attorney Davis Wright Tremaine LLP 1201 Third Avenue, Suite 2200 Seattle, WA 98101 (206) 757-7700

FRISCO INDEPENDENT SCHOOL DISTRICT

FRISCO INDEPENDENT SCHOOL DISTRICT STUDENT SERVICES BOOSTER CLUB REQUIREMENTS AND OPERATIONAL GUIDELINES 2017-2018 FOREWORD Frisco Independent School District recognizes the importance of parent and community

FRISCO INDEPENDENT SCHOOL DISTRICT STUDENT SERVICES BOOSTER CLUB REQUIREMENTS AND OPERATIONAL GUIDELINES 2017-2018 FOREWORD Frisco Independent School District recognizes the importance of parent and community

Form 990 Tax Exempt Reporting

Form 990 Tax Exempt Reporting CLAconnect.com Speaker Introductions Amanda Treml, CPA Amanda is a Manager with CliftonLarsonAllen and provides assurance and tax compliance services to non-profit organizations.

Form 990 Tax Exempt Reporting CLAconnect.com Speaker Introductions Amanda Treml, CPA Amanda is a Manager with CliftonLarsonAllen and provides assurance and tax compliance services to non-profit organizations.

Articles of Incorporation for a Nonprofit Corporation filed pursuant to and of the Colorado Revised Statutes (C.R.S.

Document must be filed electronically. Paper documents will not be accepted. Document processing fee $50.00 Fees & forms/cover sheets are subject to change. To access other information or print copies

Document must be filed electronically. Paper documents will not be accepted. Document processing fee $50.00 Fees & forms/cover sheets are subject to change. To access other information or print copies

Section references are to the Internal Revenue Code unless otherwise noted.

2008 Instructions for Form 990-EZ Short Form Return of Organization Exempt From Income Tax Under Section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private

2008 Instructions for Form 990-EZ Short Form Return of Organization Exempt From Income Tax Under Section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private

Return of Organization Exempt From Income Tax

Form B G I J Short Form 990-EZ Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code 2010 (except black lung benefit trust or private foundation)

Form B G I J Short Form 990-EZ Return of Organization Exempt From Income Tax Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code 2010 (except black lung benefit trust or private foundation)

Conflict of interest. Addendum to Bylaws of the Pro-Life Action League

Conflict of interest Directors should scrupulously avoid transactions in which the director has a personal or material financial interest, or with entities of which the director is an officer, director,

Conflict of interest Directors should scrupulously avoid transactions in which the director has a personal or material financial interest, or with entities of which the director is an officer, director,

Return of Organization Exempt From Income Tax

Form 990 Department of the Treasury Internal Revenue Service Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(1) of the Internal Revenue Code (except black lung benefit trust

Form 990 Department of the Treasury Internal Revenue Service Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(1) of the Internal Revenue Code (except black lung benefit trust

The Louisiana Chapter American Institute of Architects Conflict of Interest Policy (Adopted )

") The Louisiana Chapter (Adopted 01-27-2011) Article I Purpose The Louisiana Chapter of the, Inc., is a not-for-profit corporation organized and existing under the laws of the State of Louisiana for the

The Louisiana Chapter (Adopted 01-27-2011) Article I Purpose The Louisiana Chapter of the, Inc., is a not-for-profit corporation organized and existing under the laws of the State of Louisiana for the

cgfitornia CORPORATION DIVISION

State 1670070 cgfitornia OFFICE OF THE SECRETARY OF STATE======== CORPORATION DIVISION I, MARCH PONG EU, Secretary of State of the State of California, hereby certify: That the annexed transcript has been

State 1670070 cgfitornia OFFICE OF THE SECRETARY OF STATE======== CORPORATION DIVISION I, MARCH PONG EU, Secretary of State of the State of California, hereby certify: That the annexed transcript has been

Conflict of Interest Policy and Procedures of the Columbus Family YMCA

Conflict of Interest Policy and Procedures of the Columbus Family YMCA I. PURPOSE OF THE CONFLICT OF INTEREST POLICY The purpose of this conflict of interest policy of Columbus Family YMCA, hereinafter

Conflict of Interest Policy and Procedures of the Columbus Family YMCA I. PURPOSE OF THE CONFLICT OF INTEREST POLICY The purpose of this conflict of interest policy of Columbus Family YMCA, hereinafter

3500 This booklet contains two copies of:

California Forms & Instructions 3500 This booklet contains two copies of: FTB 3500, Exemption Application, Page 11 and Page 17 Use form FTB 3500 to apply for exemption from California income or franchise

California Forms & Instructions 3500 This booklet contains two copies of: FTB 3500, Exemption Application, Page 11 and Page 17 Use form FTB 3500 to apply for exemption from California income or franchise

Instructions for Form 990-EZ

2011 Instructions for Form 990-EZ Short Form Return of Organization Exempt From Income Tax Under Section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private

2011 Instructions for Form 990-EZ Short Form Return of Organization Exempt From Income Tax Under Section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private

Short Form Return of Organization Exempt From Income Tax

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private

Note: lfexemptsta6usis (Rev. September 1998) Under Section 501(c)(3) of the Internal Revenue Code approved, this application

Under Section 501(c)(3) of the Internal Revenue Code approved, this application") Form 1023 Application for Recognition of Exemption OMB No. 1545-0056 Note: lfexemptsta6usis (Rev. September 1998) Under Section 501(c)(3) of the Internal Revenue Code approved, this application Department

Form 1023 Application for Recognition of Exemption OMB No. 1545-0056 Note: lfexemptsta6usis (Rev. September 1998) Under Section 501(c)(3) of the Internal Revenue Code approved, this application Department

Conflict of Interest Policy The Cooperative Foundation

Conflict of Interest Policy The Cooperative Foundation RECITALS: A. The Cooperative Foundation is a Minnesota nonprofit corporation exempt from federal income tax under Section 501(c)(3) of the Internal

Conflict of Interest Policy The Cooperative Foundation RECITALS: A. The Cooperative Foundation is a Minnesota nonprofit corporation exempt from federal income tax under Section 501(c)(3) of the Internal

Amended and Restated Articles of Incorporation of Lakeville South Cougar Wrestling Booster Club

Amended and Restated Articles of Incorporation of Lakeville South Cougar Wrestling Booster Club The undersigned, being of legal age, for the purpose of now invoking the rights and responsibilities pursuant

Amended and Restated Articles of Incorporation of Lakeville South Cougar Wrestling Booster Club The undersigned, being of legal age, for the purpose of now invoking the rights and responsibilities pursuant

Short Form Return of Organization Exempt From Income Tax

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private

Understanding the Revised Form 990 and Governance Disclosures Enhancing Transparency and Compliance

Understanding the Revised Form 990 and Governance Disclosures Enhancing Transparency and Compliance March 20, 2009 9:30 am 11:15 am North County Philanthropy Council Lake San Marcos Country Club 1750 San

Understanding the Revised Form 990 and Governance Disclosures Enhancing Transparency and Compliance March 20, 2009 9:30 am 11:15 am North County Philanthropy Council Lake San Marcos Country Club 1750 San

ARTICLES OF INCORPORATION ARTICLE I ARTICLE II ARTICLE III

ARTICLES OF INCORPORATION ARTICLE I NAME 1.01 Name The name of this corporation shall be Prasana India. The business of the corporation may be conducted as Prasana India or Prasana. 2.01 Duration ARTICLE

ARTICLES OF INCORPORATION ARTICLE I NAME 1.01 Name The name of this corporation shall be Prasana India. The business of the corporation may be conducted as Prasana India or Prasana. 2.01 Duration ARTICLE

Short Form Return of Organization Exempt From Income Tax

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private

ARTICLES OF INCORPORATION OF THE BUILDING TECHNOLOGY EDUCATORS SOCIETY, INCORPORATED

ARTICLES OF INCORPORATION OF THE BUILDING TECHNOLOGY EDUCATORS SOCIETY, INCORPORATED The undersigned, acting as the incorporator of a nonprofit corporation ("Corporation") organized under and pursuant

ARTICLES OF INCORPORATION OF THE BUILDING TECHNOLOGY EDUCATORS SOCIETY, INCORPORATED The undersigned, acting as the incorporator of a nonprofit corporation ("Corporation") organized under and pursuant

CONFLICT-OF-INTEREST POLICIES: DISCLOSURE, MONITORING, AND ENFORCEMENT

UPDATED JANAURY 2017 CONFLICT-OF-INTEREST POLICIES: DISCLOSURE, MONITORING, AND ENFORCEMENT Conflict-of-Interest Policies in General Under the Internal Revenue Code, a taxexempt organization cannot use

UPDATED JANAURY 2017 CONFLICT-OF-INTEREST POLICIES: DISCLOSURE, MONITORING, AND ENFORCEMENT Conflict-of-Interest Policies in General Under the Internal Revenue Code, a taxexempt organization cannot use

Forever Young Foundation (FYF) Conflict of Interest Policy And Annual Statement

Conflict of Interest Policy And Annual Statement") Forever Young Foundation (FYF) Conflict of Interest Policy And Annual Statement For Directors and Officers and Members of a Committee with Board Delegated Powers Article I -- Purpose 1. The purpose of

Forever Young Foundation (FYF) Conflict of Interest Policy And Annual Statement For Directors and Officers and Members of a Committee with Board Delegated Powers Article I -- Purpose 1. The purpose of

F Group Exemption Number G Accounting Method: Cash Accrual Other (specify) H Check if the organization is not I Website:

H Check if the organization is not I Website:") Form 99-EZ Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private foundation) Sponsoring

Form 99-EZ Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except black lung benefit trust or private foundation) Sponsoring

INTERNAL REVENUE SERVICE P. 0. BOX 2508 CINCINNATI, OH DEPARTMENT OF THE TREASURY

INTERNAL REVENUE SERVICE P. 0. BOX 2508 CINCINNATI, OH 45201 MARTIN COUNTY FLORIDA ARES/FLACES INC PO BOX 2769 STUART, FL 34995 DEPARTMENT OF THE TREASURY Employer Identification Number: 65-0861168 DLN

INTERNAL REVENUE SERVICE P. 0. BOX 2508 CINCINNATI, OH 45201 MARTIN COUNTY FLORIDA ARES/FLACES INC PO BOX 2769 STUART, FL 34995 DEPARTMENT OF THE TREASURY Employer Identification Number: 65-0861168 DLN