Resources for Starting a 501(c)(3) Peter Shaw Assistant School District Attorney

|

|

|

- Mae King

- 5 years ago

- Views:

Transcription

1 Resources for Starting a 501(c)(3) Peter Shaw Assistant School District Attorney

2 Disclaimer School Board Regulation 801.3AR Membership shall be primarily made up of parents and community members, though district employees may also be members. Shall have their own governing board, policies and accounting records, separate from the school or school district. The school principal or designee shall maintain a close relationship with booster clubs and booster organizations associated with his or her school However, school employees shall not direct or manage a booster club or booster organization for their own school, but may provide advice, including on use of the school name, mascot and/or logo Funds must be collected and maintained by the club or organization and kept separate from district funds and from student activity funds; may not use District s tax ID. Principal must give permission for use of school name/logo; fundraising done in school s name must also be approved by principal All donations must go through district-approved procedures Liability Conflict of Interest Duty of loyalty

3 What is a 501(c)(3) Non-profit Tax exempt federal and state Donors can take tax deduction Named after the provision in federal tax code permitting tax exemption Like a private corporation it has Articles of incorporation Bylaws Registration/filing requirements (initial and annual) Board of Directors

4 Must have a specific purpose An organization may qualify for exemption from federal income tax if it is organized and operated exclusively for one or more of the following purposes. Religious. Charitable. Scientific. Testing for public safety. Literary. Educational. Fostering national or international amateur sports competition (but only if none of its activities involve providing athletic facilities or equipment) The prevention of cruelty to children or animals. To qualify, the organization must be a corporation, community chest, fund, articles of association, or foundation. A trust is a fund or foundation and will qualify. However, an individual or a partnership will not qualify.

5 Educational Foundations Education foundations are privately operated, nonprofit organizations established to assist public schools and who qualify as charitable organizations, different from school districts, public institutions or local governments A public school foundation is designed to augment, supplement, or complement programs and activities currently being provided by the district They have their own board of directors and their own staff, both paid and volunteer. Most school foundations operate as an independent entity, with no formal, legal relationship to the school district.

6 Resources-

7 Minnesotanonprofits.org Step-by-step process for setting up a MN non-profit Tips and advice on good governance Sample governance documents Tips on fundraising, financial management and communications/marketing

8 Resourceshttp://

9 Resources

10 Resources MN AG s website/charities Division

11 Resources-- _publink

12 Government Involvement* MN Secretary of State Naming Registration Articles of Incorporation Annual Filings IRS Initial filing for tax exemption Annual filings MN Attorney General General oversight Charity Registration *Minnesota Dep t of Revenue if organization will be buying/selling products or services

13 Federal v. State role State Provides oversight Register with both Attorney General as well as Secretary of State Secretary of State ensures all the necessary paperwork/registration is in place initially and annually Attorney General has more of a general oversight role ensuring that funds are used for the non-profits purpose, board is governing appropriately etc. Federal No day-to-day oversight, but must register with IRS and IRS will take action to revoke tax-exempt status if merited

14 Nuts & Bolts of Starting a 501(c)(3) Foundation 1. Initiator(s) 2. Decide mission and purpose 3. Business plan Staff/Volunteers Fundraising Events 4. Recruit initial board of directors

15 5. Check for and reserve a name with MN Secretary of State

16 6. Write the Articles of Incorporation (Entity name, location, purpose)

17 Sample Articles of Incorporation

18 Sample Articles of Inc cont d

19 Nuts & Bolts of Starting a 501(c)(3) Foundation, cont d 7. Incorporate as non-profit with MN Secretary of State Articles of Incorporation are filed Filing fee MN Secretary of State will send a Certificate of Incorporation

20

21 8. Draft corporate bylaws Rule book Can be amended easily Will need to be filed with IRS

22 Sample bylaws

23 Sample Bylaws

24 Sample bylaws cont d

25 Sample bylaws cont d

26 9. Hold first board meeting Approve initial bylaws Vote on new board members and officers per bylaws

27 Nuts & Bolts of Starting a 501(c)(3) Foundation, cont d 10. Obtain federal ID number (EIN) 11. Obtain income tax exemption Read IRS Publication 557 IRS Form 1023 IRS Form 8718 Filing fee ($850 or $400) 12. MN State Taxes Possibly apply for sales tax exemption to buy office furniture, supplies etc. MN Dep t of Revenue Form ST16 If organization will be selling products or services, or MN income tax from employees, obtain MN Tax ID number MN Dep t of Revenue Form Application for Business Registration

28 14. Register with MN Attorney General in certain cases. Do NOT have to register if: does not hire staff or a professional fundraiser and does not plan to receive more than $25,000 in total contributions; is a purely religious organization; or is a private foundation that does not solicit contributions more than 100 persons during a fiscal year. If you organization does need to register with AG, you must do so before soliciting contributions. File a Charitable Organization Registration Statement with a copy of the organization's articles of incorporation, IRS determination letter, and most recent financial statement. The filing fee is $25.

29

30 Note on Board Members (minnesotanonprofits.org) 3 Board member minimum (should be more) All board members should be personally committed to the mission of the organization, willing to volunteer sufficient time and resources to help achieve the mission of the organization, and understand and fulfill their fiduciary responsibilities. Nonprofit boards must have a chair and a treasurer. A vice-chair and secretary are highly suggested. The majority of the board should consist of members unrelated to each other or staff to allow for significant deliberation and diversity. Board membership should reflect the diversity of the organization's constituencies. Board members who are not employees should not receive compensation for their board service, other than reimbursement for expenses directly related to board duties. Nonprofit boards should hold quarterly meetings at a minimum. Board committees should be organized as needed to effectively structure member s roles and responsibilities.

31 Board members cont d Board members owe a duty of care and loyalty to 501(c)(3) Most issues with non-profit educational foundations relate to poor governance Very important to ensure board members are committed

32 What to do next Review resources Speak with community members Possible initiators/board members alumni, community business owners, parents, etc. Possible legal counsel contacts Pro bono

Overview of Non-Profits, 501(c)(3) Tom Walsh Chairman Denver Gaels GAA Club, Inc. t e.

(3) Tom Walsh Chairman Denver Gaels GAA Club, Inc. t e.") Overview of Non-Profits, 501(c)(3) Tom Walsh Chairman Denver Gaels GAA Club, Inc. t. 303.250.7707 e. tpwalsh3@gmail.com INTRO This presentation was created based on my experience filing a re-application

Overview of Non-Profits, 501(c)(3) Tom Walsh Chairman Denver Gaels GAA Club, Inc. t. 303.250.7707 e. tpwalsh3@gmail.com INTRO This presentation was created based on my experience filing a re-application

Launching your nonprofit

Launching your nonprofit What we ll cover What is a nonprofit What difference does that make How to establish nonprofit legal identities with government agencies Maintaining your legal identity with integrity

Launching your nonprofit What we ll cover What is a nonprofit What difference does that make How to establish nonprofit legal identities with government agencies Maintaining your legal identity with integrity

Tax Requirements for Student Clubs

Tax Reporting Tax Requirements for Student Clubs FOLLOW-UP Prepared by Office of the Controller, Department of Tax Reporting August 2016 1 Tax Reporting All income from whatever source derived is taxable

Tax Reporting Tax Requirements for Student Clubs FOLLOW-UP Prepared by Office of the Controller, Department of Tax Reporting August 2016 1 Tax Reporting All income from whatever source derived is taxable

Starting a Nonprofit Frequently Asked Questions

Starting a Nonprofit Frequently Asked Questions Q. Are nonprofit and tax-exempt the same thing? A. No. A nonprofit is a type of corporation that is formed at the state level. Nonprofit and notfor-profit

Starting a Nonprofit Frequently Asked Questions Q. Are nonprofit and tax-exempt the same thing? A. No. A nonprofit is a type of corporation that is formed at the state level. Nonprofit and notfor-profit

Questions and Answers for Chapters on National Unification With Society for Social Work Leadership In Health Care

Questions and Answers for Chapters on National Unification With Society for Social Work Leadership In Health Care Updates: 3/31/09 4/1/09 4/2/09 Disclosure Statement: The following question and answer

Questions and Answers for Chapters on National Unification With Society for Social Work Leadership In Health Care Updates: 3/31/09 4/1/09 4/2/09 Disclosure Statement: The following question and answer

NONPROFIT RAFFLES. Legal Requirements in South Carolina

NONPROFIT RAFFLES Legal Requirements in South Carolina 1 WHAT IS A RAFFLE? S. C. CODE 33-57- 1 10 South Carolina law defines raffle as a game of chance in which a participant is required to pay something

NONPROFIT RAFFLES Legal Requirements in South Carolina 1 WHAT IS A RAFFLE? S. C. CODE 33-57- 1 10 South Carolina law defines raffle as a game of chance in which a participant is required to pay something

HOTV ByLaws. File for Status. Bank Account. Record Retention. Heart of the Valley 501C3 Investigation Report. ByLaws. Requirements: Mission Statement:

Legal Requirements Slides before 1st Section Divider Requirements: Heart of the Valley 501C3 Investigation Report HOTV ByLaws Mission Statement: File for Status ByLaws Incorporation Bank Account Record

Legal Requirements Slides before 1st Section Divider Requirements: Heart of the Valley 501C3 Investigation Report HOTV ByLaws Mission Statement: File for Status ByLaws Incorporation Bank Account Record

Non-profit Organizations. Steps for establishing and for meeting Federal filing requirements

Non-profit Organizations Steps for establishing and for meeting Federal filing requirements US Income Taxes: A Brief Primer Definition of 'Federal Income Tax' A tax levied by the United States Internal

Non-profit Organizations Steps for establishing and for meeting Federal filing requirements US Income Taxes: A Brief Primer Definition of 'Federal Income Tax' A tax levied by the United States Internal

CCCIA Ways & Means Committee 501c3 Assessment. Kate Tallman, John Stevens, Jay Schaller, & Ashley Roberts

CCCIA Ways & Means Committee 501c3 Assessment Kate Tallman, John Stevens, Jay Schaller, & Ashley Roberts Problem Statement Over the past 5 years CCCIA expenses have exceeded revenues by an average of

CCCIA Ways & Means Committee 501c3 Assessment Kate Tallman, John Stevens, Jay Schaller, & Ashley Roberts Problem Statement Over the past 5 years CCCIA expenses have exceeded revenues by an average of

LEGAL & FINANCIAL GUIDELINES

LEGAL & FINANCIAL GUIDELINES I. Introduction 1. National League for Nursing (NLN) must be aware of the activities carried on by Constituent Leagues (CLs) in its name. A court could deem an act by a CL

LEGAL & FINANCIAL GUIDELINES I. Introduction 1. National League for Nursing (NLN) must be aware of the activities carried on by Constituent Leagues (CLs) in its name. A court could deem an act by a CL

Getting Tax-exempt. Linnea R. Michel, Esq. Legal Center for Nonprofits, Inc.

Getting Tax-exempt Linnea R. Michel, Esq. Legal Center for Nonprofits, Inc. 2014 Legal Center for Nonprofits, Inc. Information provided herein is not legal advice and is intended for informational purposes

Getting Tax-exempt Linnea R. Michel, Esq. Legal Center for Nonprofits, Inc. 2014 Legal Center for Nonprofits, Inc. Information provided herein is not legal advice and is intended for informational purposes

PRIVATE FOUNDATION CAUTION: The purposes of this memorandum are to assist you, the directors of your private foundation, and your accountant in:

CHERRY CREEK CENTER 4500 CHERRY CREEK DRIVE SOUTH #600 DENVER, CO 80246-1500 303.322.8943 WWW.WADEASH.COM CORPORATE DISCLAIMER Material presented on the Wade Ash Woods Hill & Farley, P.C., website is intended

CHERRY CREEK CENTER 4500 CHERRY CREEK DRIVE SOUTH #600 DENVER, CO 80246-1500 303.322.8943 WWW.WADEASH.COM CORPORATE DISCLAIMER Material presented on the Wade Ash Woods Hill & Farley, P.C., website is intended

HOW TO APPLY FOR TAX-EXEMPT STATUS. Table of Contents

HOW TO APPLY FOR TAX-EXEMPT STATUS Table of Contents Basics of Tax Exemption Who Must File a Form 1023 501(c)(3) Requirements Organizational Test Operational Test Form 1023 Part I. Basic Information about

HOW TO APPLY FOR TAX-EXEMPT STATUS Table of Contents Basics of Tax Exemption Who Must File a Form 1023 501(c)(3) Requirements Organizational Test Operational Test Form 1023 Part I. Basic Information about

Information for Sumner County School Support Organizations

Information for Sumner County School Support Organizations School Support Organization (SSO) Start Up Instructions and General Information These suggestions are not to be considered legal advice. You may

Information for Sumner County School Support Organizations School Support Organization (SSO) Start Up Instructions and General Information These suggestions are not to be considered legal advice. You may

Thank you for coming to the Booster Club Training! Please make sure to sign in

Thank you for coming to the 2016-17 Booster Club Training! Please make sure to sign in Dr. Michael Goddard Assistant Superintendent for Business and Operations megoddard@prosper-isd.net Shelia Winter PHS

Thank you for coming to the 2016-17 Booster Club Training! Please make sure to sign in Dr. Michael Goddard Assistant Superintendent for Business and Operations megoddard@prosper-isd.net Shelia Winter PHS

Operations: Cadillac Area Festivals & Events Policies and Procedures

Operations: Cadillac Area Festivals & Events Cadillac Area Festivals & Events (CAFÉ) is a 501C3, an IRS tax exempt entity. Non profits and organized committees in the area can utilize CAFÉ as fiduciary

Operations: Cadillac Area Festivals & Events Cadillac Area Festivals & Events (CAFÉ) is a 501C3, an IRS tax exempt entity. Non profits and organized committees in the area can utilize CAFÉ as fiduciary

WikiLeaks Document Release

WikiLeaks Document Release February 2, 2009 Congressional Research Service Report RS21892 Application Process for Seeking Section 501(c)(3) Tax Exempt Status Erika Lunder, American Law Division December

WikiLeaks Document Release February 2, 2009 Congressional Research Service Report RS21892 Application Process for Seeking Section 501(c)(3) Tax Exempt Status Erika Lunder, American Law Division December

ALTERNATIVES TO STARTING A NEW NONPROFIT

ALTERNATIVES TO STARTING A NEW NONPROFIT While many people are tempted to incorporate first, there are a number of options for undertaking a new activity without starting a new organization. Because most

ALTERNATIVES TO STARTING A NEW NONPROFIT While many people are tempted to incorporate first, there are a number of options for undertaking a new activity without starting a new organization. Because most

FIT FOUNDATION BOARD OF DIRECTORS Roles and Responsibilities

Overall Board Lead Participate Invest Develop a vision and clear mission for the Foundation; Articulate guiding values of the Foundation; Establish major strategic goals; Outline strategies for achieving

Overall Board Lead Participate Invest Develop a vision and clear mission for the Foundation; Articulate guiding values of the Foundation; Establish major strategic goals; Outline strategies for achieving

BEST PRACTICES. Best Practices #125: 501(c)(3) Chapter Organization Cover Letter and Structure

(3) Chapter Organization Cover Letter and Structure") BEST PRACTICES Best Practices #125: 501(c)(3) Chapter Organization Cover Letter and Structure A lot has changed since the original Best Practices Article for Tax-Exempt Status was posted in 2009. Most

BEST PRACTICES Best Practices #125: 501(c)(3) Chapter Organization Cover Letter and Structure A lot has changed since the original Best Practices Article for Tax-Exempt Status was posted in 2009. Most

Outright Gift to Charity

Thrivent Financial for Lutherans William Leach, CLTC Financial Representative 5 Prince Way Jackson, NJ 732-598-0839 william.leach@thrivent.com facebook.com/william.leach.thrivent Outright Gift to Charity

Thrivent Financial for Lutherans William Leach, CLTC Financial Representative 5 Prince Way Jackson, NJ 732-598-0839 william.leach@thrivent.com facebook.com/william.leach.thrivent Outright Gift to Charity

An Overview of the Tax Treatment of Nonprofits. Trina Griffin Research Division, NCGA October 22, 2008

An Overview of the Tax Treatment of Nonprofits Trina Griffin Research Division, NCGA October 22, 2008 Outline Basics Statistics Tax Treatment Trends Issues Nonprofit Basics What Is A Nonprofit? An organization

An Overview of the Tax Treatment of Nonprofits Trina Griffin Research Division, NCGA October 22, 2008 Outline Basics Statistics Tax Treatment Trends Issues Nonprofit Basics What Is A Nonprofit? An organization

New York Nonprofit Revitalization Act of Frequently Asked Questions

Updated as of April 2017 New York Nonprofit Revitalization Act of 2013 -- Frequently Asked Questions Table of Contents Amending Corporate Purposes... 2 Applicability... 2 Attorney General Review... 3 Audit

Updated as of April 2017 New York Nonprofit Revitalization Act of 2013 -- Frequently Asked Questions Table of Contents Amending Corporate Purposes... 2 Applicability... 2 Attorney General Review... 3 Audit

Keeping it Legal: The Dos and DON Ts of Managing Your 501(c)3

3") Keeping it Legal: The Dos and DON Ts of Managing Your 501(c)3 Women s Collective Giving Grantmakers Network 2014 Leadership Forum April 9, 2014 Presented by: Dianne Chipps Bailey A Few Introductory Thoughts

Keeping it Legal: The Dos and DON Ts of Managing Your 501(c)3 Women s Collective Giving Grantmakers Network 2014 Leadership Forum April 9, 2014 Presented by: Dianne Chipps Bailey A Few Introductory Thoughts

This revenue procedure provides safe harbors under section 162 of the Internal

26 CFR 1.162-1. Business expenses. (Also Part I, 162, 164, 170, 212, 642; 1.170A-1.) Rev. Proc. 2019-12 SECTION 1. PURPOSE This revenue procedure provides safe harbors under section 162 of the Internal

26 CFR 1.162-1. Business expenses. (Also Part I, 162, 164, 170, 212, 642; 1.170A-1.) Rev. Proc. 2019-12 SECTION 1. PURPOSE This revenue procedure provides safe harbors under section 162 of the Internal

An Overview of Current NonProfit Status as it Relates to the Amateur Radio Community. Lynn T Baxter, CPA WØLTB NEAR-Fest 2016

An Overview of Current NonProfit Status as it Relates to the Amateur Radio Community Lynn T Baxter, CPA WØLTB NEAR-Fest 2016 This presentation was made at the NEARfest Oct 15,2016 forums, and this presentation

An Overview of Current NonProfit Status as it Relates to the Amateur Radio Community Lynn T Baxter, CPA WØLTB NEAR-Fest 2016 This presentation was made at the NEARfest Oct 15,2016 forums, and this presentation

What Must a Tax-Exempt Organization Do To Acknowledge Donations?

What Must a Tax-Exempt Organization Do To Acknowledge Donations? An important feature of being a tax-exempt organization under Section 501(c)(3) of the Internal Revenue Code is the ability to accept tax-deductible

What Must a Tax-Exempt Organization Do To Acknowledge Donations? An important feature of being a tax-exempt organization under Section 501(c)(3) of the Internal Revenue Code is the ability to accept tax-deductible

Get By With a Little Legal Help For Your Friends

Get By With a Little Legal Help For Your Friends Presented for the 2014 New York Library Association Conference Friday, November 7, 2014 Judy Siegel, Staff Attorney Courtney Darts, Senior Staff Attorney

Get By With a Little Legal Help For Your Friends Presented for the 2014 New York Library Association Conference Friday, November 7, 2014 Judy Siegel, Staff Attorney Courtney Darts, Senior Staff Attorney

Understanding the Revised Form 990 and Governance Disclosures Enhancing Transparency and Compliance

Understanding the Revised Form 990 and Governance Disclosures Enhancing Transparency and Compliance March 20, 2009 9:30 am 11:15 am North County Philanthropy Council Lake San Marcos Country Club 1750 San

Understanding the Revised Form 990 and Governance Disclosures Enhancing Transparency and Compliance March 20, 2009 9:30 am 11:15 am North County Philanthropy Council Lake San Marcos Country Club 1750 San

TAX-EXEMPT ORGANIZATIONS: EFFECTIVE GOVERNANCE AND LEGAL COMPLIANCE VICTOR J. FERGUSON SUZANNE R. GALYARDT VORYS, SATER, SEYMOUR AND PEASE LLP

TAX-EXEMPT ORGANIZATIONS: EFFECTIVE GOVERNANCE AND LEGAL COMPLIANCE VICTOR J. FERGUSON SUZANNE R. GALYARDT VORYS, SATER, SEYMOUR AND PEASE LLP OVERVIEW 1. Organizational Test 2. Operational Test 3. Private

TAX-EXEMPT ORGANIZATIONS: EFFECTIVE GOVERNANCE AND LEGAL COMPLIANCE VICTOR J. FERGUSON SUZANNE R. GALYARDT VORYS, SATER, SEYMOUR AND PEASE LLP OVERVIEW 1. Organizational Test 2. Operational Test 3. Private

Comparison of 501(c)(3) and 501(c)(4) and 501(c)(6) Compiled from multiple publicly available web and printed resources**

(3) and 501(c)(4) and 501(c)(6) Compiled from multiple publicly available web and printed resources**") Comparison of 501(c)(3) and 501(c)(4) and 501(c)(6) Compiled from multiple publicly available web and printed resources** Purposes 501(c)(3) 501(c)(4) 501(c)(6) Social Welfare: An organization must be

Comparison of 501(c)(3) and 501(c)(4) and 501(c)(6) Compiled from multiple publicly available web and printed resources** Purposes 501(c)(3) 501(c)(4) 501(c)(6) Social Welfare: An organization must be

Parent Support Organizations Mandatory Training August 18, 2018

Parent Support Organizations Mandatory Training August 18, 2018 Vnet & GPS Finance TRAINING AGENDA I. Purpose of Training II. Definition and Role of the Parent Support Organization (PSO) A. Types B. Role

Parent Support Organizations Mandatory Training August 18, 2018 Vnet & GPS Finance TRAINING AGENDA I. Purpose of Training II. Definition and Role of the Parent Support Organization (PSO) A. Types B. Role

CRS Report for Congress Received through the CRS Web

Order Code RL30877 CRS Report for Congress Received through the CRS Web Characteristics of and Reporting Requirements for Selected Tax-Exempt Organizations March 8, 2001 Marie B. Morris Legislative Attorney

Order Code RL30877 CRS Report for Congress Received through the CRS Web Characteristics of and Reporting Requirements for Selected Tax-Exempt Organizations March 8, 2001 Marie B. Morris Legislative Attorney

BOOSTER CLUB TRAINING. Department of Athletics Temple Independent School District

BOOSTER CLUB TRAINING Department of Athletics Temple Independent School District Booster Club Website www.wildcatstrong.com Hover over Wildcat HQ Select Booster Clubs Board Policy GE Local The Board is

BOOSTER CLUB TRAINING Department of Athletics Temple Independent School District Booster Club Website www.wildcatstrong.com Hover over Wildcat HQ Select Booster Clubs Board Policy GE Local The Board is

Gift Acceptance Policy

Gift Acceptance Policy Big Brothers Big Sisters of Central Minnesota (BBBSCM or Big Brothers Big Sisters) is a nonprofit corporation organized under the laws of the state of Minnesota. Big Brothers Big

Gift Acceptance Policy Big Brothers Big Sisters of Central Minnesota (BBBSCM or Big Brothers Big Sisters) is a nonprofit corporation organized under the laws of the state of Minnesota. Big Brothers Big

Supporting the educational mission of California s State Universities. Prepared by Auxiliary Organizations Association

Prepared by Association April, 2011 Overview What are they? What are they NOT? Why were they created? What are their authorized roles? Types of auxiliary organizations and activities How do they (should

Prepared by Association April, 2011 Overview What are they? What are they NOT? Why were they created? What are their authorized roles? Types of auxiliary organizations and activities How do they (should

New Guidelines for Tax Exempt Organizations A Look at IRS Compliance Readiness for 2012 and Beyond

New Guidelines for Tax Exempt Organizations A Look at IRS Compliance Readiness for 2012 and Beyond Executive Directors Roundtable Fall Leadership Network Meeting Las Cruces, NM October 4, 2013 Eduardo

New Guidelines for Tax Exempt Organizations A Look at IRS Compliance Readiness for 2012 and Beyond Executive Directors Roundtable Fall Leadership Network Meeting Las Cruces, NM October 4, 2013 Eduardo

QUALIFYING GIFTS TO CHARITIES OUTSIDE OF THE UNITED STATES FOR THE INCOME TAX CHARITABLE DEDUCTION

QUALIFYING GIFTS TO CHARITIES OUTSIDE OF THE UNITED STATES FOR THE INCOME TAX CHARITABLE DEDUCTION Presented by Andrew S. Katzenberg Kleinberg, Kaplan, Wolff & Cohen, P.C. Brian K. Janowsky Schiff Hardin

QUALIFYING GIFTS TO CHARITIES OUTSIDE OF THE UNITED STATES FOR THE INCOME TAX CHARITABLE DEDUCTION Presented by Andrew S. Katzenberg Kleinberg, Kaplan, Wolff & Cohen, P.C. Brian K. Janowsky Schiff Hardin

Surviving by Combining Darcy White/Adrienne Smith April 27, 2011

Firm/ Corp Logo Surviving by Combining Darcy White/Adrienne Smith April 27, 2011 Mission of Pro Bono Partnership of Atlanta: To provide free legal assistance to community-based nonprofits that serve low-income

Firm/ Corp Logo Surviving by Combining Darcy White/Adrienne Smith April 27, 2011 Mission of Pro Bono Partnership of Atlanta: To provide free legal assistance to community-based nonprofits that serve low-income

Nonprofit Essentials Conference, August 20, 2015 LEGAL REQUIREMENTS & THE IMPORTANCE OF BEING TRANSPARENT

Nonprofit Essentials Conference, August 20, 2015 LEGAL REQUIREMENTS & THE IMPORTANCE OF BEING TRANSPARENT About the Presenters Emily Robertson Attorney Robertson Law Office @RLOonNonprofits Amy Sinykin

Nonprofit Essentials Conference, August 20, 2015 LEGAL REQUIREMENTS & THE IMPORTANCE OF BEING TRANSPARENT About the Presenters Emily Robertson Attorney Robertson Law Office @RLOonNonprofits Amy Sinykin

National Charity League, Inc Fundraising Policy

National Charity League, Inc Fundraising Policy Introduction As 501 (c) (3) organizations, NCL Chapters are legally permitted to accept donations from their members as well as from sources outside of the

National Charity League, Inc Fundraising Policy Introduction As 501 (c) (3) organizations, NCL Chapters are legally permitted to accept donations from their members as well as from sources outside of the

The following are common situations where the acquisition of property by a charitable organization is not subject to sales tax.

DEPARTMENT OF REVENUE SALES AND USE TAX 1 CCR 201-4 Regulation 39-26-718 CHARITABLE AND OTHER EXEMPT ORGANIZATIONS (1) General Rule. (c) Purchases by charitable organizations are exempt from state sales

DEPARTMENT OF REVENUE SALES AND USE TAX 1 CCR 201-4 Regulation 39-26-718 CHARITABLE AND OTHER EXEMPT ORGANIZATIONS (1) General Rule. (c) Purchases by charitable organizations are exempt from state sales

Shoreline Neighborhood Association Presentation. City of Shoreline, Washington March 19, 2008

Shoreline Neighborhood Association Presentation City of Shoreline, Washington March 19, 2008 Susan Schalla, Attorney Davis Wright Tremaine LLP 1201 Third Avenue, Suite 2200 Seattle, WA 98101 (206) 757-7700

Shoreline Neighborhood Association Presentation City of Shoreline, Washington March 19, 2008 Susan Schalla, Attorney Davis Wright Tremaine LLP 1201 Third Avenue, Suite 2200 Seattle, WA 98101 (206) 757-7700

Auxiliary Organizations Part of the CSU Team CSU 101 March 6-9, 2011 Monterey

Part of the CSU Team CSU 101 March 6-9, 2011 Monterey Richard Jackson Secretary/Treasurer Association Overview What are they? What are they NOT? Why were they created? What are their authorized roles?

Part of the CSU Team CSU 101 March 6-9, 2011 Monterey Richard Jackson Secretary/Treasurer Association Overview What are they? What are they NOT? Why were they created? What are their authorized roles?

INTRODUCING THE ILLINOIS L 3 C

INTRODUCING THE ILLINOIS L 3 C Marc J. Lane Hosted by: COMMUNITY ECONOMIC DEVELOPMENT LAW PROJECT Copyright 2009, by Marc J. Lane. All rights reserved. The 1-2 Punch Mission-related investing Program-related

INTRODUCING THE ILLINOIS L 3 C Marc J. Lane Hosted by: COMMUNITY ECONOMIC DEVELOPMENT LAW PROJECT Copyright 2009, by Marc J. Lane. All rights reserved. The 1-2 Punch Mission-related investing Program-related

Booster Clubs Questions and Answers (in italics)

") Booster Clubs Questions and Answers (in italics) Board Policy (Employees) DBD Regulations: Employees and Financial Capacity 1. If an employee is in charge of a concession stand, does that fall in the same

Booster Clubs Questions and Answers (in italics) Board Policy (Employees) DBD Regulations: Employees and Financial Capacity 1. If an employee is in charge of a concession stand, does that fall in the same

FFO & Booster Club Policy & Procedure Guidelines

FFO & Booster Club Policy & Procedure Guidelines 2017-2018 Catalina Foothills Unified School District No. 16 Angelie Hawley Director of Finance ahawley@cfsd16.org 1 INTRODUCTION Thank you for attending!

FFO & Booster Club Policy & Procedure Guidelines 2017-2018 Catalina Foothills Unified School District No. 16 Angelie Hawley Director of Finance ahawley@cfsd16.org 1 INTRODUCTION Thank you for attending!

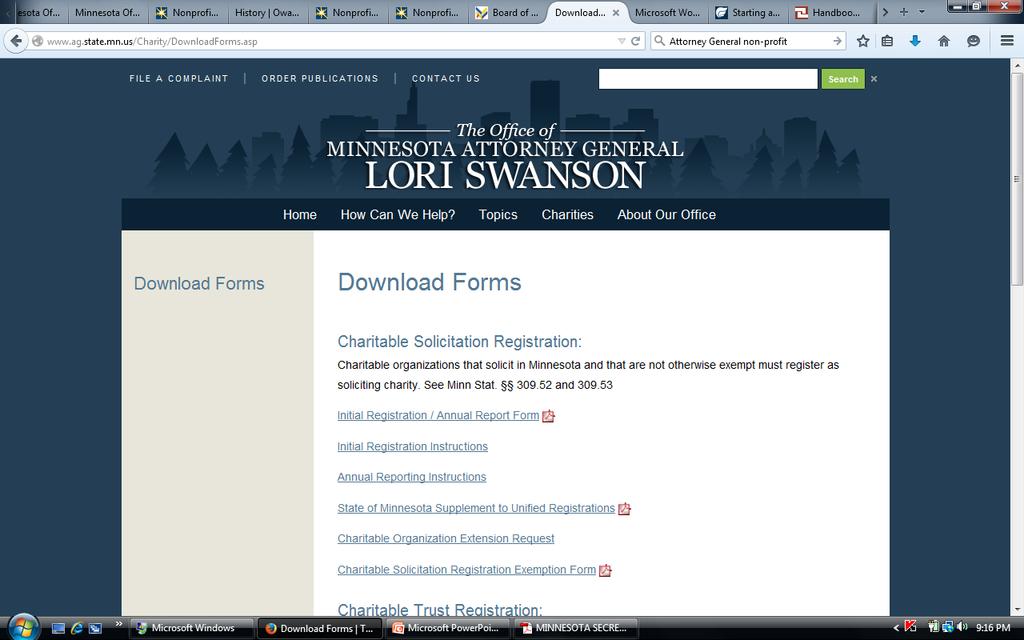

A GUIDE TO MINNESOTA S CHARITIES LAWS

A GUIDE TO MINNESOTA S CHARITIES LAWS FROM THE OFFICE OF MINNESOTA ATTORNEY GENERAL LORI SWANSON www.ag.state.mn.us This brochure is intended to be used as a source for general information and is not provided

A GUIDE TO MINNESOTA S CHARITIES LAWS FROM THE OFFICE OF MINNESOTA ATTORNEY GENERAL LORI SWANSON www.ag.state.mn.us This brochure is intended to be used as a source for general information and is not provided

Imperial College Union Financial Procedures

Imperial College Union Financial Procedures This document governs all financial matters relating to the Union. Non-compliance, deliberate, negligent or repeated disregard of these provisions may result

Imperial College Union Financial Procedures This document governs all financial matters relating to the Union. Non-compliance, deliberate, negligent or repeated disregard of these provisions may result

Charitable Solicitation: Registering, Acknowledging & Substantiating Donations

Charitable Solicitation: Registering, Acknowledging & Substantiating Donations Presented by: Robyn Miller Staff Attorney Pro Bono Partnership of Atlanta 1 Agenda Registration to Solicit Donations Internet

Charitable Solicitation: Registering, Acknowledging & Substantiating Donations Presented by: Robyn Miller Staff Attorney Pro Bono Partnership of Atlanta 1 Agenda Registration to Solicit Donations Internet

Sumner County School Support Organizations

Sumner County School Support Organizations School Support Organization (SSO) Start Up Instructions and General Information Additional information and resources for School Support Organizations may be found

Sumner County School Support Organizations School Support Organization (SSO) Start Up Instructions and General Information Additional information and resources for School Support Organizations may be found

Nonprofit Essentials Conference, August 10, 2017 LEGAL REQUIREMENTS & THE IMPORTANCE OF BEING TRANSPARENT

Nonprofit Essentials Conference, August 10, 2017 LEGAL REQUIREMENTS & THE IMPORTANCE OF BEING TRANSPARENT About the Presenters Heidi Christianson Attorney Nilan Johnson Lewis, PA Kris Kewitsch Executive

Nonprofit Essentials Conference, August 10, 2017 LEGAL REQUIREMENTS & THE IMPORTANCE OF BEING TRANSPARENT About the Presenters Heidi Christianson Attorney Nilan Johnson Lewis, PA Kris Kewitsch Executive

NEBO SCHOOL DISTRICT BOARD OF EDUCATION POLICIES AND PROCEDURES

NEBO SCHOOL DISTRICT BOARD OF EDUCATION POLICIES AND PROCEDURES K School / Community Relations PTAs, PTOs, Booster Clubs, and Other Parent Support Groups KAB DATED: April 11, 2018 SECTION: POLICY TITLE:

NEBO SCHOOL DISTRICT BOARD OF EDUCATION POLICIES AND PROCEDURES K School / Community Relations PTAs, PTOs, Booster Clubs, and Other Parent Support Groups KAB DATED: April 11, 2018 SECTION: POLICY TITLE:

FORMING A NEW NONPROFIT: NUTS AND BOLTS OF WASHINGTON STATE LAW. by Judith L. Andrews, Apex Law Group

FORMING A NEW NONPROFIT: NUTS AND BOLTS OF WASHINGTON STATE LAW by Judith L. Andrews, Apex Law Group 1 FORMING A NEW NONPROFIT: NUTS AND BOLTS This chapter will address the legal requirements and procedures

FORMING A NEW NONPROFIT: NUTS AND BOLTS OF WASHINGTON STATE LAW by Judith L. Andrews, Apex Law Group 1 FORMING A NEW NONPROFIT: NUTS AND BOLTS This chapter will address the legal requirements and procedures

Forming a Library Foundation and Trustee/Foundation Relationships. Terry M. Knowles, Assistant Director Charitable Trusts Unit

Forming a Library Foundation and Trustee/Foundation Relationships Terry M. Knowles, Assistant Director Charitable Trusts Unit Friends Groups Are generally recognized by the IRS as 501(c)(3) organizations

Forming a Library Foundation and Trustee/Foundation Relationships Terry M. Knowles, Assistant Director Charitable Trusts Unit Friends Groups Are generally recognized by the IRS as 501(c)(3) organizations

Federal Financial Requirements

American Society of Health-System Pharmacists Federal Financial Requirements ASHP s Financial Toolkit for Affiliates Kimberlee Berry [Pick the date] FEDERAL REQUIREMENTS NOTE: All IRS forms can be accessed

American Society of Health-System Pharmacists Federal Financial Requirements ASHP s Financial Toolkit for Affiliates Kimberlee Berry [Pick the date] FEDERAL REQUIREMENTS NOTE: All IRS forms can be accessed

The Buck Stops Here. Training for Rotary Club Treasurers. Elliott Rittenberg November 16, 2017

The Buck Stops Here Training for Rotary Club Treasurers Elliott Rittenberg elliott@rittenberg.com November 16, 2017 AGENDA Obligations & mission Responsibilities Protecting your Club & its funds Federal

The Buck Stops Here Training for Rotary Club Treasurers Elliott Rittenberg elliott@rittenberg.com November 16, 2017 AGENDA Obligations & mission Responsibilities Protecting your Club & its funds Federal

CHAR410, CHAR410-A, CHAR410-R

New York State Department of Law (Office of the Attorney General) Charities Bureau - Registration Section Instructions for Forms CHAR410, CHAR410-A, CHAR410-R and Schedule E Registration/Amended Registration/Re-Registration

New York State Department of Law (Office of the Attorney General) Charities Bureau - Registration Section Instructions for Forms CHAR410, CHAR410-A, CHAR410-R and Schedule E Registration/Amended Registration/Re-Registration

NDUS Foundation Policy and Procedure Manual

NDUS Foundation Policy and Procedure Manual Adopted: April 14, 2016 Rev. September 22, 2016 INDEX 1000 Governance 1005 Conflicts of Interest 2000 Fundraising 2001 Fundraising 2001.1 Cash Gifts and Pledges

NDUS Foundation Policy and Procedure Manual Adopted: April 14, 2016 Rev. September 22, 2016 INDEX 1000 Governance 1005 Conflicts of Interest 2000 Fundraising 2001 Fundraising 2001.1 Cash Gifts and Pledges

Unrelated Business Income. Preston C. Worley & John-Paul Volk

Unrelated Business Income Preston C. Worley & John-Paul Volk What is Unrelated Business Income Tax (UBIT)? UBIT: Unrelated Business Income Tax Unrelated Business Income Tax (UBIT) in the U.S. Internal

Unrelated Business Income Preston C. Worley & John-Paul Volk What is Unrelated Business Income Tax (UBIT)? UBIT: Unrelated Business Income Tax Unrelated Business Income Tax (UBIT) in the U.S. Internal

KING GEORGE GRAND LODGE / QUEEN VASHTI GRAND CHAPTER FOUNDATION

KING GEORGE GRAND LODGE / QUEEN VASHTI GRAND CHAPTER FOUNDATION Established in 2014 Founded under the direction of King George Grand Lodge Grand Master Jonathan Dearbone Meeting the Needs of the Community

KING GEORGE GRAND LODGE / QUEEN VASHTI GRAND CHAPTER FOUNDATION Established in 2014 Founded under the direction of King George Grand Lodge Grand Master Jonathan Dearbone Meeting the Needs of the Community

WHO MUST BE ESTABLISHED AND CHARTERED IN ORDER TO USE THE 4-H NAME AND EMBLEM? PURPOSE OF ESTABLISHING AND CHARTERING A 4-H CLUB/GROUP

Educational programs of the Texas A&M AgriLife Extension Service are open to all people without regard to race, color, sex, religion, national origin, age, disability, genetic information, or veteran status.

Educational programs of the Texas A&M AgriLife Extension Service are open to all people without regard to race, color, sex, religion, national origin, age, disability, genetic information, or veteran status.

Fiduciary Duties of Directors of Charitable Organizations

Guide for board members Fiduciary Duties of Directors of Charitable Organizations From the Office of Minnesota Attorney General Lori Swanson Introduction The Attorney General s Office has prepared this

Guide for board members Fiduciary Duties of Directors of Charitable Organizations From the Office of Minnesota Attorney General Lori Swanson Introduction The Attorney General s Office has prepared this

INSTRUCTIONS FOR REGISTRATION STATEMENT (COR-92) AND ADDITIONAL DOCUMENTATION NEEDED FOR INITIAL REGISTRATION

AND ADDITIONAL DOCUMENTATION NEEDED FOR INITIAL REGISTRATION") INSTRUCTIONS FOR REGISTRATION STATEMENT (COR-92) AND ADDITIONAL DOCUMENTATION NEEDED FOR INITIAL REGISTRATION Instructions for completing Initial Registration and form: This form, along with several other

INSTRUCTIONS FOR REGISTRATION STATEMENT (COR-92) AND ADDITIONAL DOCUMENTATION NEEDED FOR INITIAL REGISTRATION Instructions for completing Initial Registration and form: This form, along with several other

Second edition, Openness and Disclosure in Fundraising

Second edition, 2014 Openness and Disclosure in Fundraising Georgeann R. Luxion Luxion Consulting G.Luxion@LuxionConsulting.com 386-847-4490 www.luxionconsulting.com Certified in Nonprofit Board Education

Second edition, 2014 Openness and Disclosure in Fundraising Georgeann R. Luxion Luxion Consulting G.Luxion@LuxionConsulting.com 386-847-4490 www.luxionconsulting.com Certified in Nonprofit Board Education

Unrelated Business Income Tax

Unrelated Business Income Tax The publication is prepared by and distributed with express consent from the University of Arizona, Financial Services Office Tax Compliance. Minor edits are denoted. For

Unrelated Business Income Tax The publication is prepared by and distributed with express consent from the University of Arizona, Financial Services Office Tax Compliance. Minor edits are denoted. For

15 Not-for-Profit Organizations Regulatory, Taxation, and Performance Issues

Chapter 15 Not-for-Profit Organizations Regulatory, Taxation, and Performance Issues McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. 15-2 Learning Objectives After

Chapter 15 Not-for-Profit Organizations Regulatory, Taxation, and Performance Issues McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. 15-2 Learning Objectives After

Federal Tax-Exempt Status 501(c)(3) Organizations

(3) Organizations") Federal Tax-Exempt Status 501(c)(3) Organizations Most PTAs are classified as tax-exempt 501(c)(3) public charities under the Internal Revenue Code (IRC). One major advantage for organizations that are

Federal Tax-Exempt Status 501(c)(3) Organizations Most PTAs are classified as tax-exempt 501(c)(3) public charities under the Internal Revenue Code (IRC). One major advantage for organizations that are

Tax-Exempt Organization Reference Chart

Tax-Exempt Reference Chart Derived from "IRS Publication 557: Tax-Exempt Status for Your (1997)" Note: This table may not include every type of that qualifies for some form of federal tax-exemption. It

Tax-Exempt Reference Chart Derived from "IRS Publication 557: Tax-Exempt Status for Your (1997)" Note: This table may not include every type of that qualifies for some form of federal tax-exemption. It

Board Approved 9/20/16 OUTSIDE SUPPORT ORGANIZATION MANUAL

OUTSIDE SUPPORT ORGANIZATION MANUAL 1 2 Board Approved 9/20/16 Outside Support Organizations The School District encourages citizens to form Outside Support Organizations (OSO). These organizations support

OUTSIDE SUPPORT ORGANIZATION MANUAL 1 2 Board Approved 9/20/16 Outside Support Organizations The School District encourages citizens to form Outside Support Organizations (OSO). These organizations support

Copyright 2018, James M. McCarten, Burr & Forman LLP, all rights reserved

Prepared for Stetson 2018 National Conference on Special Needs Planning and Special Needs Trusts Pre-Conference Pooled Trusts Intensive St. Petersburg, Florida Wednesday, October 17, 2018 Presented by:

Prepared for Stetson 2018 National Conference on Special Needs Planning and Special Needs Trusts Pre-Conference Pooled Trusts Intensive St. Petersburg, Florida Wednesday, October 17, 2018 Presented by:

PARENT ORGANIZATIONS TAX FILING REQUIREMENTS

PARENT ORGANIZATIONS TAX FILING REQUIREMENTS Leland Dushkin, CPA Tax Manager Hereford, Lynch, Sellars & Kirkham, PC ldushkin@hlsk.com 1406 Wilson Road, Suite 100 Conroe, TX 77304 936-756-8127 or 936-441-1338

PARENT ORGANIZATIONS TAX FILING REQUIREMENTS Leland Dushkin, CPA Tax Manager Hereford, Lynch, Sellars & Kirkham, PC ldushkin@hlsk.com 1406 Wilson Road, Suite 100 Conroe, TX 77304 936-756-8127 or 936-441-1338

Amended and Restated Articles of Incorporation of Lakeville South Cougar Wrestling Booster Club

Amended and Restated Articles of Incorporation of Lakeville South Cougar Wrestling Booster Club The undersigned, being of legal age, for the purpose of now invoking the rights and responsibilities pursuant

Amended and Restated Articles of Incorporation of Lakeville South Cougar Wrestling Booster Club The undersigned, being of legal age, for the purpose of now invoking the rights and responsibilities pursuant

Not-for-profit accounting and taxation

Not-for-profit accounting and taxation Presented by: Denise McKnight, CPA Partner, Friedman LLP What is a Not-for-profit (NFP) organization? A NFP is a corporation or an association that conducts business

Not-for-profit accounting and taxation Presented by: Denise McKnight, CPA Partner, Friedman LLP What is a Not-for-profit (NFP) organization? A NFP is a corporation or an association that conducts business

Effective Booster Practices

Effective Booster Practices Megan E. Greulich Staff Attorney Ohio School OSBA leads the way to educational excellence by serving Ohio s public school board members and the diverse districts they represent

Effective Booster Practices Megan E. Greulich Staff Attorney Ohio School OSBA leads the way to educational excellence by serving Ohio s public school board members and the diverse districts they represent

What You Need to Know About Charitable Solicitation and Registration. Regina Hopkins D.C. Bar Pro Bono Center January 19, 2017

What You Need to Know About Charitable Solicitation and Registration Regina Hopkins D.C. Bar Pro Bono Center January 19, 2017 Charitable Solicitation Registration Overview 39 states and the District of

What You Need to Know About Charitable Solicitation and Registration Regina Hopkins D.C. Bar Pro Bono Center January 19, 2017 Charitable Solicitation Registration Overview 39 states and the District of

Chapter 22. Exempt Entities. Eugene Willis, William H. Hoffman, Jr., David M. Maloney and William A. Raabe

Chapter 22 Exempt Entities Eugene Willis, William H. Hoffman, Jr., David M. Maloney and William A. Raabe Copyright 2004 South-Western/Thomson Learning Requirements For Exempt Status (slide 1 of 3) Serve

Chapter 22 Exempt Entities Eugene Willis, William H. Hoffman, Jr., David M. Maloney and William A. Raabe Copyright 2004 South-Western/Thomson Learning Requirements For Exempt Status (slide 1 of 3) Serve

Supporting the educational mission of California s State Universities. Prepared by Auxiliary Organizations Association

Prepared by Association February 2012 Overview What are they? Why were they created? What are the authorized function/roles? How they operate? Current issues impacting auxiliary organizations Association

Prepared by Association February 2012 Overview What are they? Why were they created? What are the authorized function/roles? How they operate? Current issues impacting auxiliary organizations Association

Lewisville Independent School District BOOSTER CLUB GUIDELINES. Debate

Lewisville Independent School District BOOSTER CLUB GUIDELINES Debate Booster Clubs A school district approved club formed by parents and other interested non-student adults to work for the best interest

Lewisville Independent School District BOOSTER CLUB GUIDELINES Debate Booster Clubs A school district approved club formed by parents and other interested non-student adults to work for the best interest

EXECUTIVE COMPENSATION POLICY California Nonprofit Public Benefit Corporation Exempt from Taxation Under Internal Revenue Code Section 501(c)(3)

(3)") PUBLIC COUNSEL COMMUNITY DEVELOPMENT PROJECT ANNOTATED EXECUTIVE COMPENSATION POLICY AUGUST 2017 EXECUTIVE COMPENSATION POLICY California Nonprofit Public Benefit Corporation Exempt from Taxation Under

PUBLIC COUNSEL COMMUNITY DEVELOPMENT PROJECT ANNOTATED EXECUTIVE COMPENSATION POLICY AUGUST 2017 EXECUTIVE COMPENSATION POLICY California Nonprofit Public Benefit Corporation Exempt from Taxation Under

Boulder Mountainbike Alliance. 1. Entity name:

Document processing fee If document is filed on paper $125.00 If document is filed electronically $ 25.00 Fees & forms/cover sheets are subject to change. To file electronically, access instructions for

Document processing fee If document is filed on paper $125.00 If document is filed electronically $ 25.00 Fees & forms/cover sheets are subject to change. To file electronically, access instructions for

. This return is a consolidation from multiple entities, for use as an informational tool only.

. This return is a consolidation from multiple entities, for use as an informational tool only. 1 2 3 4 5 6 Susie Q. Smart, Exec. Director 40 X 165,000 0 5,500 (See Sched J for addl info) 7 8 9 10 11 12

. This return is a consolidation from multiple entities, for use as an informational tool only. 1 2 3 4 5 6 Susie Q. Smart, Exec. Director 40 X 165,000 0 5,500 (See Sched J for addl info) 7 8 9 10 11 12

Frequently Asked Questions About Company Foundations and Corporate Giving

Welcome to Our 2006 Seminar Series: Frequently Asked Questions About Company Foundations and Corporate Giving May 23, 2006 1 Speakers: Victoria Bjorklund David Shevlin 2006 Simpson Thacher & Bartlett LLP.

Welcome to Our 2006 Seminar Series: Frequently Asked Questions About Company Foundations and Corporate Giving May 23, 2006 1 Speakers: Victoria Bjorklund David Shevlin 2006 Simpson Thacher & Bartlett LLP.

POLICY ON CHARITABLE GIFTING TO THE CCA

POLICY ON CHARITABLE GIFTING TO THE CCA Policy #05-2: Policy on Charitable Gifting to the CCA May 2010 Approved: May 2010 Policy No: 05 2 Current version approved: September 2010 Date of next review: N/A

POLICY ON CHARITABLE GIFTING TO THE CCA Policy #05-2: Policy on Charitable Gifting to the CCA May 2010 Approved: May 2010 Policy No: 05 2 Current version approved: September 2010 Date of next review: N/A

FISCAL SPONSORSHIP AGREEMENT

This exemplar is designed for general use in a Model A direct project situation, where the project is new. If the project already exists and there are assets or liabilities to be transferred in from a

This exemplar is designed for general use in a Model A direct project situation, where the project is new. If the project already exists and there are assets or liabilities to be transferred in from a

Starting a Non-Profit Organization in Indiana. Filling Out the Forms

Starting a Non-Profit Organization in Indiana Filling Out the Forms Key Points Incorporating as a non-profit does not automatically result in 501(c)3 status or state sales and income tax exemption. These

Starting a Non-Profit Organization in Indiana Filling Out the Forms Key Points Incorporating as a non-profit does not automatically result in 501(c)3 status or state sales and income tax exemption. These

Deep Dive Into the Form 1023 Application for 501c3 Tax-Exemption

Deep Dive Into the Form 1023 Application for 501c3 Tax-Exemption Lorri Dunsmore Perkins Coie November 2, 2017 Seattle, Washington November 2, 2017 Deep Dive Into the Form 1023 Application for 501c3 Tax-Exemption

Deep Dive Into the Form 1023 Application for 501c3 Tax-Exemption Lorri Dunsmore Perkins Coie November 2, 2017 Seattle, Washington November 2, 2017 Deep Dive Into the Form 1023 Application for 501c3 Tax-Exemption

PTA GLOSSARY. Amend: To change the wording of a motion by inserting, adding, striking out, and inserting, or by substitution.

PTA GLOSSARY 3-to-1 Rule: PTA recommendation that there should be at least three non-fundraising programs aimed at helping parents or children or advocating for school improvements for every one fundraiser.

PTA GLOSSARY 3-to-1 Rule: PTA recommendation that there should be at least three non-fundraising programs aimed at helping parents or children or advocating for school improvements for every one fundraiser.

Booster Club Workshop

Corona-Norco Unified School District Booster Club Workshop May 1, 2017 May 15, 2017 Presenter: Dusty Nevatt, Partner Vavrinek, Trine, Day & Co., LLP Workshop Overview Definition of a Booster Club Fundraising

Corona-Norco Unified School District Booster Club Workshop May 1, 2017 May 15, 2017 Presenter: Dusty Nevatt, Partner Vavrinek, Trine, Day & Co., LLP Workshop Overview Definition of a Booster Club Fundraising

Incorporated Entity. Elects Tax Exempt Status with the Internal Revenue Service. Treated as a public charity per I.R.S. guidelines

1 2 3 Incorporated Entity Elects Tax Exempt Status with the Internal Revenue Service Treated as a public charity per I.R.S. guidelines 1 PROS Recognized Legal Entity Insurable Entity Required Monetary

1 2 3 Incorporated Entity Elects Tax Exempt Status with the Internal Revenue Service Treated as a public charity per I.R.S. guidelines 1 PROS Recognized Legal Entity Insurable Entity Required Monetary

Organizing Your CTA 4

Organizing Your CTA 4 Now that we ve covered the six basic steps needed to take to start your CTA, it s time to discuss three of them your board of directors, incorporating as a not-for-profit, and obtaining

Organizing Your CTA 4 Now that we ve covered the six basic steps needed to take to start your CTA, it s time to discuss three of them your board of directors, incorporating as a not-for-profit, and obtaining

- Examples of 501c4 organizations include volunteer fire companies, civic leagues, and community associations.

1. What organizations qualify for 501c4? - Civic Leagues, Social Welfare organizations - Organizations exempt under Section 501c4 must be organized exclusively for the promotion of social welfare. A 501c4

1. What organizations qualify for 501c4? - Civic Leagues, Social Welfare organizations - Organizations exempt under Section 501c4 must be organized exclusively for the promotion of social welfare. A 501c4

Edmond Public Schools. Sanctioned Organizations

Edmond Public Schools Sanctioned Organizations Contact Information for EPS Jeanise Wynn, Business Manager Phone: (405) 340-2881 Email: jeanise.wynn@edmondschools.net Debbie Smith, Executive Assistant Phone:

Edmond Public Schools Sanctioned Organizations Contact Information for EPS Jeanise Wynn, Business Manager Phone: (405) 340-2881 Email: jeanise.wynn@edmondschools.net Debbie Smith, Executive Assistant Phone:

MINNESOTA STATE UNIVERSITY, MANKATO FOUNDATION, INC. OPERATING POLICIES AND PROCEDURES. Approved by Foundation Board action Jan. 24, 2014.

MINNESOTA STATE UNIVERSITY, MANKATO FOUNDATION, INC. OPERATING POLICIES AND PROCEDURES Approved by Foundation Board action Jan. 24, 2014. MINNESOTA STATE UNIVERSITY, MANKATO FOUNDATION, INC. OPERATING

MINNESOTA STATE UNIVERSITY, MANKATO FOUNDATION, INC. OPERATING POLICIES AND PROCEDURES Approved by Foundation Board action Jan. 24, 2014. MINNESOTA STATE UNIVERSITY, MANKATO FOUNDATION, INC. OPERATING

Economic Development as a Charitable Activity April 5, Lara Kalwinski, Esq. Council on Foundations

Economic Development as a Charitable Activity April 5, 2017 Lara Kalwinski, Esq. Council on Foundations Agenda Legal Background and Why This is Important Meeting Charitability Standards What We Know What

Economic Development as a Charitable Activity April 5, 2017 Lara Kalwinski, Esq. Council on Foundations Agenda Legal Background and Why This is Important Meeting Charitability Standards What We Know What

Tax-Exempt Status and IRS Reporting Obligations. 1. All Undergraduate Organizations

Tax-Exempt Status and IRS Reporting Obligations All undergraduate organizations are expected to comply with the Undergraduate Regulations, and must also comply with Federal and State tax laws. The purpose

Tax-Exempt Status and IRS Reporting Obligations All undergraduate organizations are expected to comply with the Undergraduate Regulations, and must also comply with Federal and State tax laws. The purpose

Do not enter social security numbers on this form as it may be made public.

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(1) of the Internal Revenue Code (except private

Form 990-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(1) of the Internal Revenue Code (except private

Fundraising Law and Regulation January 2015 PLI Presentation

Fundraising Law and Regulation January 2015 PLI Presentation Elizabeth M. Guggenheimer Lawyers Alliance for New York eguggenheimer@lawyersalliance.org What is Fundraising Activity? Fundraising activity

Fundraising Law and Regulation January 2015 PLI Presentation Elizabeth M. Guggenheimer Lawyers Alliance for New York eguggenheimer@lawyersalliance.org What is Fundraising Activity? Fundraising activity

Mission, Vision Statement, Bylaws and Policies of the State University College at Oneonta Foundation Corporation

Mission, Vision Statement, Bylaws and Policies of the State University College at Oneonta Foundation Corporation May Not Be Duplicated State University College at Oneonta Foundation Corporation 2017 Contents

Mission, Vision Statement, Bylaws and Policies of the State University College at Oneonta Foundation Corporation May Not Be Duplicated State University College at Oneonta Foundation Corporation 2017 Contents

Fundraising Guidelines for Faculty, Staff and Campus Organizations

Fundraising Guidelines for Faculty, Staff and Campus Organizations August 2006 A. Purposes 1. To distinguish between (a) fundraising efforts in which St. Norbert College (hereafter the College ) is an

Fundraising Guidelines for Faculty, Staff and Campus Organizations August 2006 A. Purposes 1. To distinguish between (a) fundraising efforts in which St. Norbert College (hereafter the College ) is an