KDF2B Income Tax Law & Practice. Unit: I to V

|

|

|

- Moris Price

- 5 years ago

- Views:

Transcription

1 KDF2B Income Tax Law & Practice Unit: I to V

2 Unit 1: Income Tax Law and Tax Planning Basic Concepts Residential Status and Tax Incidence Exempted Incomes and its related Tax planning implications Tax evasion and tax avoidance, and methods of tax planning KDF2B INCOME TAX LAW & PRACTICE 2

3 Tax Planning, Tax avoidance vs Tax evasion hugy sz7o KDF2B INCOME TAX LAW & PRACTICE 3

4 BASIC CONCEPTS Assessment year : The tax payer s income of previous year is assessed to tax in the assessment at the rates prescribed in Finance Act. Previous year : Income earned in a year is taxable in the next year. The year in which income is earned is known as previous year. Person : Includes an individual,huf, Company, Firm, AOP, BOI. KDF2B INCOME TAX LAW & PRACTICE I 4

5 content: font size 20 KDF2B INCOME TAX LAW & PRACTICE I 5

6 Basic & Additional conditions Basic or Conditions (i) An individual is in India during the relevant previous year for a period amounting in all to 182 days or more. (ii) An individual is in India for a period amounting in all to 365 days or more during four years preceding the relevant previous year & he is in India for a period of 60 days or more during the previous year. Additional Condition (i)he has been resident in India in at least Two out of Ten P.Y (ii) He has been in India atleast 730 days in all during 7 preceding P Y KDF2B INCOME TAX LAW & PRACTICE 6

7 INCIDENCE OF TAX content: font size 20 KDF2B INCOME TAX LAW & PRACTICE I 7

8 FEATURES OF INCOME Definite source Legal or Illegal income Income may be received in cash or in kind Income being considered on receipt basis or accrual basis Dispute regarding title Mere relief or reimbursement of expenses Income may be permanent or temporary Gifts of personal nature PIN money Diversion of income vs Application of Income KDF2B INCOME TAX LAW & PRACTICE 8

9 Link below appends exempted income. v=2yqwb3axbho KDF2B INCOME TAX LAW & PRACTICE I 9

10 Heading: font size 32 content: font size 20 KDF2B INCOME TAX LAW & PRACTICE 10

11 Heading: content: font size 20 Link below explains capital and revenue items tc0 KDF2B INCOME TAX LAW & PRACTICE 11

12 UNIT 2: Income from salary Income from House property Income from business or profession Income from capital gains Income from other sources KDF2B INCOME TAX LAW & PRACTICE 12

13 INCOME UNDER THE HEAD SALARIES Salaries Sec 15 to 17 Features of Salary Employer Employee Relationship Salaries and Business Profit Salaries and Professional Income Tax free Salary Leave Salary KDF2B INCOME TAX LAW & PRACTICE 13

Ignore for the time being KDF2B INCOME TAX LAW & PRACTICE")

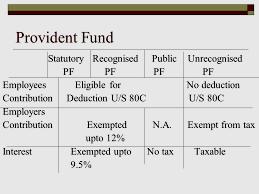

14 TREATMENT OF PROVIDENT FUND EMPLOYER S CONTRIBUTION SPF content: RPF font size 20 URPF Fully exempt from tax Exempt upto 12% of salary ( Basic + DASB + Commission on turnover) Ignore for the time being KDF2B INCOME TAX LAW & PRACTICE 14

15 Fully Exempted Allowance Foreign Allowances of Govt employees working outside India Allowances of U.N.O employees working in India. Allowances received by judges of high court. KDF2B INCOME TAX LAW & PRACTICE 15

16 Fully Taxable Allowance DA CCA MEDICAL ALLOWANCE LUNCH ALLOWANCE content: font size 20 DOG ALLOWANCE OVERTIME ALLOWANCE CAPITAL COMPENSATORY ALLOWANCE SERVANT ALLOWANCE MARRIAGE ALLOWANCE FAMILY ALLOWANCE WATER & ELECTRICITY ALLOWANCE DEPUTATION ALLOWANCE TIFFEN ALLOWANCE E.A FOR NON GOVT EMPLOYEES NON PRACTISING ALLOWANCE WARDEN ALLOWANCE PROJECT ALLOWANCE KDF2B INCOME TAX LAW & PRACTICE 16

+ Commission based on sales KDF2B INCOME TAX LAW &")

17 HRA - PROVISIONS Least of following is exempt : (i) HRA actually received (ii) 50% of salary or 40% of salary (iii) Excess of rent paid over 10% of salary SALARY = basic salary + DA (forming part) + Commission based on sales KDF2B INCOME TAX LAW & PRACTICE 17

18 PERQUISITES View the following link to acquire knowledge about perquisites KDF2B INCOME TAX LAW & PRACTICE 18

19 KDF2B INCOME TAX LAW & PRACTICE 19

20 KDF2B INCOME TAX LAW & PRACTICE 20

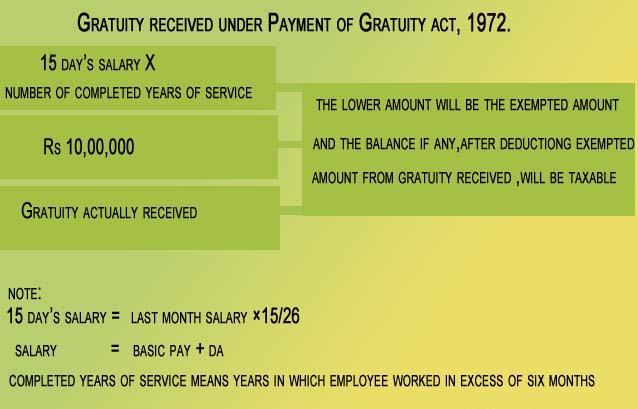

21 1. DA is taxable in the hands of. 2. Children education allowance is exempted upto. 3. Exempted limit of HRA in non metropolitan cities is. 4. Interest on RPF balance is exempted upto. 5. Statutory limit for exemption of gratuity received by Non Govt employees is. KDF2B INCOME TAX LAW & PRACTICE 21

xxx KDF2B INCOME TAX LAW & PRACTICE")

22 Particulars Let out house Self occupied house Deemed to be let out house GAV xxx NIL xxx Less : Municipal Tax paid by owner xxx NIL xxx NAV XXX NIL XXX Less : Deduction u/s 24 Std Int on loan for construction xxx NIL xxx xxx xxx xxx Net income from HP xxx (xxx) xxx KDF2B INCOME TAX LAW & PRACTICE 22

23 KDF2B INCOME TAX LAW & PRACTICE 23

24 KDF2B INCOME TAX LAW & PRACTICE 24

25 EXEMPTED INCOMES Income from farm house Property used for own business or profession Property income of hospital Property income of resident of Ladakh Income from HP owned by political party Income from HP owned by Trade union One self occupied property Annual value of any one palace of ex-indian ruler KDF2B INCOME TAX LAW & PRACTICE 25

26 Following video link illustrates calculation of GAV with unrealised rent KDF2B INCOME TAX LAW & PRACTICE 26

27 DEFINITION OF BUSINESS Business includes any trade, commerce, manufacture or any adventure or concern in the nature of trade, commerce or manufacture FEATURES OF BUSINESS Importance of Profit motive Business to involve two or more persons Rendering Service Business includes trade, manufacture & commerce Length of time not an essential factor Export incentives being revenue receipts. KDF2B INCOME TAX LAW & PRACTICE 27

28 COMPUTATION OF BUSINESS INCOME PARTICULARS AMOUNT BALANCE AS PER P & L ACCOUNT XXX ADD : INADMISSIBLE EXPENSES XXX LESS : EXPENDITURE ALLOWED BUT NOT DEBITED LESS : INCOME CREDITED TO P&L WHICH IS TAXABLE UNDER OTHER HEADS XXX xxx KDF2B INCOME TAX LAW & PRACTICE 28

29 INADMISSIBLE EXPENSES Drawings by the proprietor Rent paid to self All provisions and reserves All taxes Household and personal expenses Gifts and presents (Non advertisement) Bad debts still recoverable Undervaluation of closing stock Personal LIC Capital expenses Excess depreciation Interest on Capital KDF2B INCOME TAX LAW & PRACTICE 29

30 INCOME CREDITED TO P&L WHICH IS TAXABLE UNDER OTHER HEADS Gifts from relatives Agricultural receipts Any Capital receipt Part time salary Dividend income Part time salary Rent from let out property Capital gains Winning from Lotteries Withdrawal from PPF Income tax refund Interest on Bank deposit KDF2B INCOME TAX LAW & PRACTICE 30

31 Professional income is computed by taking the professional receipts of the previous year and deducting professional expenses incurred during that year. KDF2B INCOME TAX LAW & PRACTICE 31

32 Preliminary expenses are deductible in 5 equal installments Expenditure exceeding Rs 20,000, shall be paid by an account payee cheque or an account payee demand draft otherwise 100% amount is disallowed. Know how acquired on or after is subject to 25% rate of depreciation. KDF2B INCOME TAX LAW & PRACTICE 32

33 CAPITAL GAINS As per section 45 any profit or gain arising from transfer of a capital asset effected in the previous year shall, save as otherwise provided in specified sections, be chargeable to income-tax under the head Capital Gain. Capital gains attract tax liability only when the following essentials are satisfied: CAPITAL ASSET : Assessee should have a capital asset.. TRANSFER OF CAPITAL ASSET: Capital asset held by the assessee. TRANSFER DURING THE YEAR : Transfer of capital asset should have taken place during the financial year. PROFITS OR GAINS ON TRANSFER : Asset transfer should have resulted in gain or profit KDF2B I INCOME TAX LAW & PRACTICE 33

34 EXEMPTION UNDER SPECIFIRED SECTIONS: Such Capital Gains arising are not exempted under sections 54,54B,54D,54EC,54F,54G and 54GA Meaning of Capital Assets Capital asset is defined to include property of any kind, whether fixed or circulating, movable or immovable tangible or intangible. Except a few specified items, all other properties are capital assets. Ignore repairs, since it is not a capital expenditure The following assets are excluded from the definition of Capital Assets. KDF2B INCOME TAX LAW & PRACTICE 34

35 EXEMPTED ASSETS: 1.Stock in trade held for business or profession 2. Assets held for personal use 3. Rural Agricultural land 4.Gold Bonds issued by the Government 5. Special Bearer Bonds 6. Gold Deposit Bonds. Short Term Capital Assets: Capital Asset held by an assessee for not more than 36 months/ 3 years immediately preceding the date of transfer is a Short Term Capital Asset. All depreciable assets and fixed assets which are used by the organisation for official purpose are treated as short term capital assets irrespective of its holding List of Short Term Capital Assets: Financial assets, are also shortterm capital assets if they are not held for more than 12 months. 1. Shares held in a company 2. Debentures held in a company 3. Units of Unit Trust of India KDF2B INCOME TAX LAW & PRACTICE 35

36 4. Units of a Mutual fund 5. Any other securities listed in a stock exchange like Government securities 6. Zero coupon bonds Long Term Capital Asset Capital asset held by an assessee for more than 36 months/ 3 years immediately preceding the date of transfer is a Long Term Capital Gain. Determination of period of holding Shares and securities purchased through stock exchange Share and securities purchased and sold directly Shares and securities purchased and sold in several lots Transfer of securities by a depository Shares held in a company in liquidation When an asset is acquired by gift or will Shares becoming property in a scheme of Amalgamation Shares held in a demerged company Period of holding of bonus shares Period of holding of rights shares. KDF2B INCOME TAX LAW & PRACTICE 36

37 Indexed cost of acquisition: Indexed cost of acquisition means an amount which bears to be the cost of acquisition the same proportion as cost inflation index for the year in which, the assets is transferred bears to the cost inflation index for the first year in which the asset was held by the assessee of for the year beginning on the 1 st day of April, 1981, whichever is later. Indexed Cost of Improvement Indexed Cost of Improvement means an amount which bears to the cost of improvement the same proportion as cost inflation index for the year in which the asset is transferred bears to the cost inflation index for the year in which the improvement to the asset took place. Any additions or improvement made before should be ignored KDF2B INCOME TAX LAW & PRACTICE 37

38 Exemption of Capital Gains Exemption applicable to different assessee Individuals Sec.54, 54B,54D,54EC And 54G HUF Sec.54,54B, 54, 54EC,54F and 54G All assessee Sec. 54D,54EC and 54G KDF2B INCOME TAX LAW & PRACTICE 38

39 Exemptions TM 1. Capital gain on transfer of residential house property (Sec.54) 2. Capital Gain arising from the transfer of agriculture land (Sec.54) 3. Capital gain on compulsory acquisition of lands and buildings (Sec.54D) 4. Capital gain not to be charged on investment in certain bonds (Sec.54EC 5. Investment of capital gain arising from transfer of long-term listed securities or units, in specified equity shares (Sec.54ED) 6. Exemption from tax on long term capital gain arising out of sale of an asset other than residential house property and investment of the consideration in residential house(sec.54f) 7. Capital gain arising on transfer of asset in cases of shifting of industrial undertaking from urban area(sec.54g) 8. Exemption of capital gains on transfer of assets incase of shifting of industrial under taking from urban area to any special economic zone (Sec. 54GA).) KDF2B INCOME TAX LAW & PRACTICE 39

40 Income From Other Sources Income chargeable under IFOS U/S 56(2) Dividends from co-operative societies and foreign companies. Interest on securities Winnings from lotteries, crossword puzzles, other games of any sort or from gambling or betting of any form. Income from letting of plant, machinery or furniture along with the building Any sum received by the assessee from his employees as contribution to any staff welfare scheme. Any sum received under key man insurance policy. KDF2B INCOME TAX LAW & PRACTICE 40

41 Fees or commission received by an employee from a person other than his employer Annuity paid under the provisions of the Annuity Deposit scheme Interest on bank deposits Directors fees Remuneration for examination work Rent of land Agricultural income Royalty income Interest on own contribution to URPF. Remuneration received for writing. Interest from co-operative society. Family pension NSS Deposit withdrawn Director s commission Gratuity received by a director contd KDF2B INCOME TAX LAW & PRACTICE 41

42 Income by subletting Income from undisclosed sources. a) Unexplained cash credits b) Unexplained Investments c) Unexplained Receipts by cricketers money d) Unexplained expenditure e) Amount borrowed or repaid on Hundi Kinds of Securities Government Securities These securities are issued by state or central Govt. The amount received or due, shall be included in the total income. No tax is deducted at source. Non government securities. a) Tax free commercial securities are issued by a local authority or statutory corporation or a company. These securities are called tax free, because the assessee is not to pay tax on the interest, since tax is paid by the company on assessee s behalf. Hence interest received by the assessee is grossed up. KDF2B INCOME TAX LAW & PRACTICE 42

43 b) Less tax commercial securities Less tax securities are also called taxable securities. Tax is deducted at source from the interest and balance of interest after deduction of the income tax is paid to the security holder. Casual Income Lottery winnings. Winnings from race including horse races. Winnings from card games. Winnings from crossword puzzles. Gambling or betting of any other nature. Grossing up: Net winnings * 100/ Casual incomes are subject to TDS at 30% if the income exceeds Rs.5,000. Race winnings are subject to TDS at 30% if the income exceeds RS. 2,500. No TDS on other race winnings, gambling and betting. Family pension received by widows or heirs of deceased employees. Standard deduction of a sum equal to 33.33% of such pension or Rs. 15,000 whichever is less, is allowed as deduction. KDF2B INCOME TAX LAW & PRACTICE 43

44 Income from subletting. Income from sub letting of house property or rent of vacant land is income from other sources Gifts Gifts received from relatives are fully exempted. Gifts received from unrelated persons are taxable as income from other sources.gifts received in kind is exempted Property purchased for less than stamp duty value is taxable. (stamp duty value more than consideration Deduction U/S 57 Bank commission on collection of taxable dividends and interest on securities in deductible. Interest on loan to acquire investment whose income is taxable is deductible. Standard of family pension or Rs.15,000 which ever is deductible. Depreciation, repairs, fire insurance premium, local taxes relating to letout plant and machinery along with building and furniture. KDF2B INCOME TAX LAW & PRACTICE 44

45 UNIT-III Computation of Taxable Income of Individuals and firms Deduction of Tax Tax planning by taking advantage of various deductions Exempted incomes KDF2B INCOME TAX LAW & PRACTICE 45

46 (a) Determination of Gross Total Income - It is ascertained by aggregating the net income under each head. (b) Deductions from Gross Total Income - The deductions are u/s 80C 80CCD 80CCC Gross total income minus these deductions will be his total income. (c)taxable Income - It is said to be total income or net income or taxable income KDF2B INCOME TAX LAW & PRACTICE 46

47 Rebate of Rs 5000 for individual having total taxable amount not exceeding Rs 5,00,000. KDF2B INCOME TAX LAW & PRACTICE 47

48 Link given below explains the types of assessment. KDF2B INCOME TAX LAW & PRACTICE 48

49 Deduction from Gross total income KDF2B INCOME TAX LAW & PRACTICE 49

50 Unit 4 : Clubbing of Income Set off & carry forward of losses KDF2B INCOME TAX LAW & PRACTICE 50

51 Clubbing of income Income of other persons to be included in an assessee s total income. (Sec 60) Transfer of income without transfer of an asset. Such income is clubbed in the hands of the transferor Revocable transfer of assets by an assessee to another person. It is clubbed in the hands of transferor. Irrevocable transfer of assets. Income arises out of such transfer is taxable in the hands of transferee. KDF2B INCOME TAX LAW & PRACTICE 51

52 Income of an individual to include spouse income Remuneration of spouse:- Substantial interest is required. Husband and wife relationship should exist. Remuneration should be received in same concern. Remuneration should not be received out of professional qualification. KDF2B INCOME TAX LAW & PRACTICE 52

53 Income from asset transferred to spouse Direct or indirect transfer Transfer made without adequate consideration. Relationship of Husband and wife. Change in the identity of asset- taxable in the hands of transferor. Sale or transfer of transferred asset- capital gain is taxable in the hands of transferor. Transferred Asset being invested in a business. Transferred asset being invested in a firm Acquisition of asset out of pin money Taxable in the hands of transferee. Transfer of asset in connection with an agreement to live apart not taxable in the hands of transferor. Income arising to the spouse from the accretion to transferred asset cannot be clubbed with transferor. KDF2B INCOME TAX LAW & PRACTICE 53

54 Income of minor not to be clubbed Handicapped or disabled minor s income. Income earned by a minor out of any manual work. Income earned out of his skill, talent, or specialized knowledge and experience. Exemption granted to parent u/s 10(32) Rs is exempted in the hands of parent of each minor child income. Income of Minor child Income of a minor child shall be clubbed in the hands of parents. Minor s income should include with the income of parent whose total income is greater. KDF2B INCOME TAX LAW & PRACTICE 54

55 Conversion of self acquired property into Joint family property If a member of HUF transfers self acquired property to HUF without adequate consideration. Income arising out of transferred asset is clubbed in the hands of transferor. Deemed Incomes Cash credits Unexplained investments. Unexplained money. Amount of investment not fully disclosed. Unexplained expenditure. Amount borrowed or repaid on Hundi KDF2B INCOME TAX LAW & PRACTICE 55

56 Set-off and carry forward of losses Inter source set off Loss under a particular head of income can be adjusted against income from any other source under the same head for the same assessment year. Exemptions to Inter source set off Loss from speculation business. Long term capital loss. Loss from the activity of owning and maintaining race horses. No loss can be set off against winning from lotteries, crossword puzzles, card games, etc. Loss from a source which is exempted. KDF2B INCOME TAX LAW & PRACTICE 56

57 Inter head set-off Loss from one head of income can be set off against income from other heads of income. Exemption: Loss from speculation business Long term capital loss Loss from the activity of owning and maintaining race horses. Business loss cannot be setoff against salary income. Loss cannot be set off against casual income. KDF2B INCOME TAX LAW & PRACTICE 57

58 Carry forward of loss If a loss cannot be adjusted in the same year, it may be carried forward and set off against the income of the subsequent years. House property loss can be carried forward for 8 years against income under the head house property. Speculation loss can be carried forward for 4 years to be set off against speculation income. Non speculation business loss can be carried forward for 8 years to be set off against any business income Loss on account of unabsorbed depreciation, capital expenditure on scientific research and family planning expenditure can be carried forward for any number of years to be set off against any income (other than salary) KDF2B INCOME TAX LAW & PRACTICE 58

59 Unit 5: Tax considerations in specific business decisions, viz., make or buy; own or lease, retain or replace; export or domestic sales; shutdown or closure; expand or contract; invest or disinvest. Computer Application in Income tax and tax planning KDF2B INCOME TAX LAW & PRACTICE 59

60 INTRODUCTION Tax planning is the arrangement of financial activities in such a way that maximum tax benefit are enjoyed by making use of all beneficial provisions in the tax laws. It entitles the assesse to avail certain exemptions, deductions, rebates and reliefs, so as to minimize his tax liability KDF2B INCOME TAX LAW & PRACTICE 60

61 BUSINESS DECISIONS Make or buy Invest or disinvest Own or lease Expand or contract Retain or replace Shutdown or closure Export or domestic sales KDF2B INCOME TAX LAW & PRACTICE 61

62 MAKE OR BUY A make-or-buy decision is the act of choosing between manufacturing a product in-house or purchasing it from an external supplier. In a make-or-buy decision, the most important factors to consider are part of quantitative analysis, such as the associated costs of production and whether the business has the capacity to produce at required levels. KDF2B INCOME TAX LAW & PRACTICE 62

63 OWN OR LEASE Assets may purchased or taken on lease. Apart from tax angle other factors also are important in taking lease or buy decisions like rate of change in technology. Depreciation on specified assets can be claimed as deduction u/s 32. the Assets may be purchased out rightly or may be taken on loan. Where the asset is taken on loan interest amount can either be claimed as revenue expenditure or can be capitalized. But where interest is paid after the asset is first put us use, the deduction on account of interest shall be claimed as revenue expenditure, i.e. such interest cannot be capitalized. KDF2B INCOME TAX LAW & PRACTICE 63

64 RETAIN OR REPLACE Repair implies the existence of a thing has malfunctioned and can be set right by effecting repairs which may involve replacement of some parts, thereby making the thing as efficient as it was before or close to it as possible. After repair the thing to which the repair was carried out continues to be available for use. Replacement is different from repair. Replacement implies the removal or discarding of the things that was in use, by a different or new thing capable of performing the same function with the same or greater efficiency. KDF2B INCOME TAX LAW & PRACTICE 64

65 SHUT DOWN / CLOSURE KDF2B INCOME TAX LAW & PRACTICE 65

66 EXPORT/DOMESTIC SALE When idle capacity exists, exporting is usually the more profitable strategy. The great advantage with exports to foreign countries is that the export price will not adversely affect the local price Companies which have already recovered their fixed cost from local sales can export just above their variable cost and still make good profits KDF2B INCOME TAX LAW & PRACTICE 66

67 INVEST /DISINVEST Purchasing plant involves long-term expenditure decision involving investment and the required return on investment If a particular machine is cheaper in terms of both variable and fixed cost it can be automatically chosen Otherwise disinvest decision should be taken KDF2B INCOME TAX LAW & PRACTICE 67

, abandon (e.g., temporarily or permanently), or let expire real options.")

68 EXPAND/CONTRACT The owners of real options have the right, but not the obligation, to expand or contract their investment in a real asset (i.e., physical things rather than financial contracts) at some future date when uncertainties exist regarding the future value of the real asset has been resolved. Strategic investment and budget decisions within any organisation are decisions to acquire, exercise (e.g., expand, contract, or switch), abandon (e.g., temporarily or permanently), or let expire real options. The ability to delay the decision to invest introduces flexibility into this financial instrument. KDF2B INCOME TAX LAW & PRACTICE 68

69 Computer application in Income tax As per Explanation 3 to section 9 (1) (vi) of Income Tax Act, Computer software means any computer programme recorded on any disc, tape, perforated media or other information storage device and includes any such programme or any customized electronic data. USAGE OF COMPUTER APPLICATIONS IN IT DEPARTMENT sed_in_income_tax_department?#slide=2 KDF2B INCOME TAX LAW & PRACTICE 69

70 KDF2B INCOME TAX LAW & PRACTICE 70

71 Tips for tax planning RECAP OF INCOME TAX KDF2B INCOME TAX LAW & PRACTICE 71

BVZ5A/BPF5C/BVC5A/ BPG5C INCOME TAX LAW & PRACTICE I. Unit : I - V. BVZ5A/BPG5C/CYA5C - Income Tax Law & Practice - I

BVZ5A/BPF5C/BVC5A/ BPG5C INCOME TAX LAW & PRACTICE I Unit : I - V BVZ5A/BPG5C/CYA5C - Income Tax Law & Practice - I UNIT 1 Meaning & Features of Income Important definitions under Income Tax Act Tax rate

BVZ5A/BPF5C/BVC5A/ BPG5C INCOME TAX LAW & PRACTICE I Unit : I - V BVZ5A/BPG5C/CYA5C - Income Tax Law & Practice - I UNIT 1 Meaning & Features of Income Important definitions under Income Tax Act Tax rate

BVZ6A,BPG6C Income tax law & practice-ii BVZ6A,BPG6C INCOME TAX LAW & PRACTICE-II. Unit : I - V

BVZ6A,BPG6C Income tax law & practice-ii BVZ6A,BPG6C INCOME TAX LAW & PRACTICE-II Unit : I - V TM BVZ6A,BPG6C Income tax law & practice-ii 02 I UNIT-I SYLLABUS Capital assets Meaning and kind Procedure

BVZ6A,BPG6C Income tax law & practice-ii BVZ6A,BPG6C INCOME TAX LAW & PRACTICE-II Unit : I - V TM BVZ6A,BPG6C Income tax law & practice-ii 02 I UNIT-I SYLLABUS Capital assets Meaning and kind Procedure

INCOME FROM OTHER SOURCES. What are the sections which deals with income from Other Sources - Sec. 56 to 59

INCOME FROM OTHER SOURCES What are the sections which deals with income from Other Sources - Sec. 56 to 59 Sec.56(1) : Charging Section This is the last head of income and it is also known as residuary

INCOME FROM OTHER SOURCES What are the sections which deals with income from Other Sources - Sec. 56 to 59 Sec.56(1) : Charging Section This is the last head of income and it is also known as residuary

Income from Other Sources

Income from Other Sources SECTION 56: INCOME FROM OTHER SOURCES CHARGING SECTION Income from other sources is a residuary head of income i.e. income not chargeable under any other head, and which is not

Income from Other Sources SECTION 56: INCOME FROM OTHER SOURCES CHARGING SECTION Income from other sources is a residuary head of income i.e. income not chargeable under any other head, and which is not

Chapter 8 : Income from Other Sources (Section 56 to 59) Advance Direct Tax and Service Tax [Sub code : 441]

![Chapter 8 : Income from Other Sources (Section 56 to 59) Advance Direct Tax and Service Tax [Sub code : 441]](/thumbs/74/70016057.jpg "Chapter 8 : Income from Other Sources (Section 56 to 59) Advance Direct Tax and Service Tax [Sub code : 441]") Chapter 8 : Income from Other Sources (Section 56 to 59) Advance Direct Tax and Service Tax [Sub code : 441] Learning Objectives Income from Other Sources Deductions from Income from other Sources Conditions

Chapter 8 : Income from Other Sources (Section 56 to 59) Advance Direct Tax and Service Tax [Sub code : 441] Learning Objectives Income from Other Sources Deductions from Income from other Sources Conditions

III BCOM (CA) [ ] Semester V Core:INCOME TAX LAW AND PRACTICE 503B Multiple Choice Questions.

![III BCOM (CA) [ ] Semester V Core:INCOME TAX LAW AND PRACTICE 503B Multiple Choice Questions.](/thumbs/71/65799137.jpg "III BCOM (CA) [ ] Semester V Core:INCOME TAX LAW AND PRACTICE 503B Multiple Choice Questions.") 1 of 23 8/12/17, 2:57 PM Dr.G.R.Damodaran College of Science (Autonomous, affiliated to the Bharathiar University, recognized by the UGC)Reaccredited at the 'A' Grade Level by the NAAC and ISO 9001:2008

1 of 23 8/12/17, 2:57 PM Dr.G.R.Damodaran College of Science (Autonomous, affiliated to the Bharathiar University, recognized by the UGC)Reaccredited at the 'A' Grade Level by the NAAC and ISO 9001:2008

Income Tax(Al Jamia Arts and Science College)

") Income Tax is a very important direct tax. It is collected by the Central Government. It is a major source of revenue to the Central Government. History of Income Tax in India In India, Income Tax was

Income Tax is a very important direct tax. It is collected by the Central Government. It is a major source of revenue to the Central Government. History of Income Tax in India In India, Income Tax was

Chapter 8 Income under the Head "Income from Other Sources"

Chapter 8 Income under the Head "Income from Other Sources" 1. Basis of Charge Section 56(1) Income of every kind which is not exempt shall be chargeable to income-tax under the head "Income from Other

Chapter 8 Income under the Head "Income from Other Sources" 1. Basis of Charge Section 56(1) Income of every kind which is not exempt shall be chargeable to income-tax under the head "Income from Other

INCOME UNDER THE HEAD HOUSE PROPERTY AND IT S COMPUTATION

INCOME UNDER THE HEAD HOUSE PROPERTY AND IT S COMPUTATION 1. BASIS FOR CHARGE: - There must be a property consisting of building or land appurtenant thereto The Assessee should be owner of that property

INCOME UNDER THE HEAD HOUSE PROPERTY AND IT S COMPUTATION 1. BASIS FOR CHARGE: - There must be a property consisting of building or land appurtenant thereto The Assessee should be owner of that property

Paper 7- Direct Taxation

Paper 7- Direct Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7- Direct Taxation Full Marks: 100 Time Allowed: 3 hours

Paper 7- Direct Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7- Direct Taxation Full Marks: 100 Time Allowed: 3 hours

Paper 7 Direct Taxation

Paper 7 Direct Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks: 100

Paper 7 Direct Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks: 100

MTP_ Inter _Syllabus 2016_ June 2017_Set 1 Paper 7 Direct Taxation

Paper 7 Direct Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks: 100

Paper 7 Direct Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks: 100

INCOME TAX TEST 3 SOLUTIONS

Question 1 Computation of Total Income of Mr. Suraj Particulars Rs. Rs. Income from House Property (WN-1) Profits and gains from business or profession (WN-2) Capital gains -Short term capital loss (WN-3)

Question 1 Computation of Total Income of Mr. Suraj Particulars Rs. Rs. Income from House Property (WN-1) Profits and gains from business or profession (WN-2) Capital gains -Short term capital loss (WN-3)

Income-tax and Death are the only two inevitable things in life In India, taxes were levied even in ancient times refer to Manu Smriti & Arthashastra

Income-tax and Death are the only two inevitable things in life In India, taxes were levied even in ancient times refer to Manu Smriti & Arthashastra Why to Pay Tax? It was only for the good of his subjects

Income-tax and Death are the only two inevitable things in life In India, taxes were levied even in ancient times refer to Manu Smriti & Arthashastra Why to Pay Tax? It was only for the good of his subjects

Most Important Question of INCOME TAX

Most Important Question of INCOME TAX Residential Status 1. In 2 nd additional condition, assessee should have stayed in India for: a) more than 730 days during 7 immediately preceding previous year b)

Most Important Question of INCOME TAX Residential Status 1. In 2 nd additional condition, assessee should have stayed in India for: a) more than 730 days during 7 immediately preceding previous year b)

13. PROBLEMS ON TOTAL INCOME

No.1 for CA/CWA & MEC/CEC MASTER MINDS 13. PROBLEMS ON TOTAL INCOME SOLUTIONS TO ASSIGNMENT PROBLEMS Problem No.1 Name of the Assessee: Mr. Rajesh A.Y: 2015-2016 Computation of Taxable Income : Income

No.1 for CA/CWA & MEC/CEC MASTER MINDS 13. PROBLEMS ON TOTAL INCOME SOLUTIONS TO ASSIGNMENT PROBLEMS Problem No.1 Name of the Assessee: Mr. Rajesh A.Y: 2015-2016 Computation of Taxable Income : Income

MTP_ Inter _Syllabus 2016_ June 2018_Set 1 Paper 7 Direct Taxation (DTX)

") Paper 7 Direct Taxation (DTX) Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks:

Paper 7 Direct Taxation (DTX) Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks:

SYLLABUS. B.Com II Year (Tax) Subject Income Tax Procedure and Practice

Subject Income Tax Procedure and Practice") SYLLABUS B.Com II Year (Tax) Subject Income Tax Procedure and Practice UNIT-I An outline of provisions and rules of various heads of income. Set off and carry forward of Losses. Clubbing of income. Practical

SYLLABUS B.Com II Year (Tax) Subject Income Tax Procedure and Practice UNIT-I An outline of provisions and rules of various heads of income. Set off and carry forward of Losses. Clubbing of income. Practical

SUGGESTED SOLUTION IPCC May 2017 EXAM. Test Code - I N J

SUGGESTED SOLUTION IPCC May 2017 EXAM DIRECT TAXATION Test Code - I N J 1 0 7 3 Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666 1 P a g e Answer-1

SUGGESTED SOLUTION IPCC May 2017 EXAM DIRECT TAXATION Test Code - I N J 1 0 7 3 Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666 1 P a g e Answer-1

INCOME UNDER THE HEAD PROFITS AND GAINS FROM BUSINESS AND PROFESSION AND IT S COMPUTATION

INCOME UNDER THE HEAD PROFITS AND GAINS FROM BUSINESS AND PROFESSION AND IT S COMPUTATION 1. NATURE OF INCOME :- Such Income Includes income from: - Business, Vocation and Profession carried on by the

INCOME UNDER THE HEAD PROFITS AND GAINS FROM BUSINESS AND PROFESSION AND IT S COMPUTATION 1. NATURE OF INCOME :- Such Income Includes income from: - Business, Vocation and Profession carried on by the

Question 1. The Institute of Chartered Accountants of India

Question 1 PAPER 5 : TAXATION Answer all questions. Working notes should form part of the answer. Wherever necessary suitable assumptions may be made by the candidates. Answer the following with reasons

Question 1 PAPER 5 : TAXATION Answer all questions. Working notes should form part of the answer. Wherever necessary suitable assumptions may be made by the candidates. Answer the following with reasons

DEDUCTION, COLLECTION AND RECOVERY OF TAX

DEDUCTION, COLLECTION AND RECOVERY OF TAX Section Particulars 190 different modes of payment of tax: tds, tcs, advance tax, tax u/s 192(1A) 191 failure to deduct tax, and direct payment of tax 192 tds

DEDUCTION, COLLECTION AND RECOVERY OF TAX Section Particulars 190 different modes of payment of tax: tds, tcs, advance tax, tax u/s 192(1A) 191 failure to deduct tax, and direct payment of tax 192 tds

Elective Course in Commerce ECO-11 Elements of Income Tax APPENDIX 2014 Assessment Year

Elective Course in Commerce ECO-11 Elements of Income Tax APPENDIX 2014 Assessment Year 2013-2014 School of Management Studies Indira Gandhi National Open University New Delhi 110068 Dear Student, As you

Elective Course in Commerce ECO-11 Elements of Income Tax APPENDIX 2014 Assessment Year 2013-2014 School of Management Studies Indira Gandhi National Open University New Delhi 110068 Dear Student, As you

SYMBIOSIS CENTRE FOR DISTANCE LEARNING (SCDL) Subject: Direct Taxation. 1. Define the terms, Assessment Year and Previous Year.

Subject: Direct Taxation. 1. Define the terms, Assessment Year and Previous Year.") Sample Questions: Section I: Subjective Questions 1. Define the terms, Assessment Year and Previous Year. 2. Explain the concept of short term and long term capital assets. 3. Which books of account should

Sample Questions: Section I: Subjective Questions 1. Define the terms, Assessment Year and Previous Year. 2. Explain the concept of short term and long term capital assets. 3. Which books of account should

DEDUCTION OF TAX AT SOURCE

DEDUCTION OF TAX AT SOURCE SECTION 190 TO 206AA Section 190 Deduction at source and advance payment Section 191 Direct payment Section 192 Deduction of tax from salary income Section 193 Deduction of tax

DEDUCTION OF TAX AT SOURCE SECTION 190 TO 206AA Section 190 Deduction at source and advance payment Section 191 Direct payment Section 192 Deduction of tax from salary income Section 193 Deduction of tax

Notes on Carry Forward and Set Off of Losses

Notes on Carry Forward and Set Off of Losses While one endeavors to derive income, the possibility of incurring losses cannot be ruled out. Based on the principles of natural justice, a set-off should

Notes on Carry Forward and Set Off of Losses While one endeavors to derive income, the possibility of incurring losses cannot be ruled out. Based on the principles of natural justice, a set-off should

HEADS OF INCOME. Income From Salaries MEANING OF SALARY. Characteristics of Salary 9/7/2017

Income From Salaries HEADS OF INCOME 1) Income under the head salaries (Section 15 17) 2) Income from house property (Section 22 27) 3) Profits and gains from business or profession (Section 28 44) 4)

Income From Salaries HEADS OF INCOME 1) Income under the head salaries (Section 15 17) 2) Income from house property (Section 22 27) 3) Profits and gains from business or profession (Section 28 44) 4)

Unit 11: COMPUTATION OF TAX

Unit 11: COMPUTATION OF TAX HOW TO COMPUTE TAX PAYABLE Once the net taxable income is computed, the next step is to compute the final tax payable. The final tax payable is computed as follows: (1) Taxable

Unit 11: COMPUTATION OF TAX HOW TO COMPUTE TAX PAYABLE Once the net taxable income is computed, the next step is to compute the final tax payable. The final tax payable is computed as follows: (1) Taxable

MTP_ Intermediate _Syllabus 2012_Dec2016_Set 1 Paper 7- Direct Taxation

Paper 7- Direct Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7- Direct Taxation Full Marks : 100 Time allowed: 3 hours

Paper 7- Direct Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7- Direct Taxation Full Marks : 100 Time allowed: 3 hours

SURENDER KR. SINGHAL & CO

PROPOSED TAX RATES FOR FINANCIAL YEAR 2016-17 A. Y. 2017-18 Income Tax Rates for Individuals, HUF Individuals, Hindu Undivided Families (HUF) and Artificial Jurisdictional Person: Net Income Range Income

PROPOSED TAX RATES FOR FINANCIAL YEAR 2016-17 A. Y. 2017-18 Income Tax Rates for Individuals, HUF Individuals, Hindu Undivided Families (HUF) and Artificial Jurisdictional Person: Net Income Range Income

Tax Laws. Time allowed : 3 hours Maximum marks : 100. Total number of questions : 8 Total number of printed pages : 8

Tax Laws 263 : 1 : Roll No... Time allowed : 3 hours Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 8 NOTE : All references to sections mentioned in Part-A of the Question

Tax Laws 263 : 1 : Roll No... Time allowed : 3 hours Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 8 NOTE : All references to sections mentioned in Part-A of the Question

CHAPTER 8: RECOVERY OF TAX TAX DEDUCTED AT SOURCE

CHAPTER 8: RECOVERY OF TAX TAX DEDUCTED AT SOURCE SECTIONS RATE PARTICULARS 192: Deduction of Tax on Slab Every Employer has a liability to deduct TDS on salary on monthly basis on tax from salary Rate

CHAPTER 8: RECOVERY OF TAX TAX DEDUCTED AT SOURCE SECTIONS RATE PARTICULARS 192: Deduction of Tax on Slab Every Employer has a liability to deduct TDS on salary on monthly basis on tax from salary Rate

Bombay Chartered Accountants Society

Bombay Chartered Accountants Society Filing of Income Tax Returns for the Assessment Year -09 09 by C.A. Contractor, Nayak & Kishnadwala Return of Income What is Return of Income? Return of Income now

Bombay Chartered Accountants Society Filing of Income Tax Returns for the Assessment Year -09 09 by C.A. Contractor, Nayak & Kishnadwala Return of Income What is Return of Income? Return of Income now

Tax Laws 263 NOTE : PART A 263/1

Tax Laws 1/2012/TL 263 Roll No Time allowed : 3 hours : 1 : Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 8 NOTE : All references to sections mentioned in Part-A of

Tax Laws 1/2012/TL 263 Roll No Time allowed : 3 hours : 1 : Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 8 NOTE : All references to sections mentioned in Part-A of

IPCC Gr. I (Solution of November ) Paper - 4 : Taxation

Paper - 4 : Taxation") Solved Scanner Appendix IPCC Gr. I (Solution of November - 2015) Paper - 4 : Taxation Chapter - 2 : Basic Concepts 2015 - Nov [2] (a) An Indian Citizen who comes on a visit to India during PY shall be

Solved Scanner Appendix IPCC Gr. I (Solution of November - 2015) Paper - 4 : Taxation Chapter - 2 : Basic Concepts 2015 - Nov [2] (a) An Indian Citizen who comes on a visit to India during PY shall be

Income of Other Persons Included in Assessee s Total Income

5 Income of Other Persons Included in Assessee s Total Income Section Income to be clubbed 60 Income transferred without transfer of asset 61 Income arising from revocable transfer of assets Key Points

5 Income of Other Persons Included in Assessee s Total Income Section Income to be clubbed 60 Income transferred without transfer of asset 61 Income arising from revocable transfer of assets Key Points

MOCK TEST SOLUTION A.Y Total No. of Question 7] [Total No. of Printed Pages 20 Time Allowed 3 Hours Maximum Marks 100 MKG

![MOCK TEST SOLUTION A.Y Total No. of Question 7] [Total No. of Printed Pages 20 Time Allowed 3 Hours Maximum Marks 100 MKG](/thumbs/73/68647623.jpg "MOCK TEST SOLUTION A.Y Total No. of Question 7] [Total No. of Printed Pages 20 Time Allowed 3 Hours Maximum Marks 100 MKG") MOCK TEST SOLUTION IPC (Intermediate) (Computation of Total Income And Tax Liability, Taxability of Gift, Advance Payment of Tax, Residential Status & Scope of Total Income, House Property, Agricultural

MOCK TEST SOLUTION IPC (Intermediate) (Computation of Total Income And Tax Liability, Taxability of Gift, Advance Payment of Tax, Residential Status & Scope of Total Income, House Property, Agricultural

5 Income of Other Persons Included in Assessee s Total Income

5 Income of Other Persons Included in Assessee s Total Income Learning Objectives After studying this chapter, you would be able to understand - why clubbing provisions have been incorporated in the Act

5 Income of Other Persons Included in Assessee s Total Income Learning Objectives After studying this chapter, you would be able to understand - why clubbing provisions have been incorporated in the Act

CA IPCC Taxation Nov 2014 solutions (Both Direct and Indirect taxes) CA N Rajasekhar M.Com FCA DISA (ICAI) Chennai

CA N Rajasekhar M.Com FCA DISA (ICAI) Chennai") CA IPCC Taxation Nov 2014 solutions (Both Direct and Indirect taxes) Compiled by This questions were solved by me under examination conditions within 2 hours 40 minutes and later on typed adding solution

CA IPCC Taxation Nov 2014 solutions (Both Direct and Indirect taxes) Compiled by This questions were solved by me under examination conditions within 2 hours 40 minutes and later on typed adding solution

Tax is imposition financial charge or other levy upon a taxpayer by a state or other the functional equivalent of the state.

1. What is Tax What is Tax? Tax is imposition financial charge or other levy upon a taxpayer by a state or other the functional equivalent of the state. How many Types of Taxes are there and what are they?

1. What is Tax What is Tax? Tax is imposition financial charge or other levy upon a taxpayer by a state or other the functional equivalent of the state. How many Types of Taxes are there and what are they?

IMPORTANT AMENDMENTS OF THE FINANCE ACT, /6/2011 Lecture Meeting of BCAS - C.A.Vipul Gandhi

IMPORTANT AMENDMENTS OF THE FINANCE ACT,2010 22/6/2011 Lecture Meeting of BCAS - C.A.Vipul Gandhi 1 TAX RATES AND SLABS OF INCOME TAX RATES FOR INDIVIDUAL,HUF,AOP & BOI, ARTIFICIAL JUDICIAL PERSON U/S

IMPORTANT AMENDMENTS OF THE FINANCE ACT,2010 22/6/2011 Lecture Meeting of BCAS - C.A.Vipul Gandhi 1 TAX RATES AND SLABS OF INCOME TAX RATES FOR INDIVIDUAL,HUF,AOP & BOI, ARTIFICIAL JUDICIAL PERSON U/S

UNIT- 1. Computation of Total/Taxable Income And Tax liability of an Individual

UNIT- 1 Computation of Total/Taxable Income And Tax liability of an Individual Steps in computation of total income & tax liability Income-tax is a tax levied on the total income of the previous year of

UNIT- 1 Computation of Total/Taxable Income And Tax liability of an Individual Steps in computation of total income & tax liability Income-tax is a tax levied on the total income of the previous year of

Residence and Scope of Total Income

2 Residence and Scope of Total Income 2.1 Residential Status [Section 6] The incidence of tax on any assessee depends upon his residential status under the Act. Therefore, after determining whether a particular

2 Residence and Scope of Total Income 2.1 Residential Status [Section 6] The incidence of tax on any assessee depends upon his residential status under the Act. Therefore, after determining whether a particular

Revisionary Test Paper_Intermediate_Syllabus 2008_Jun2014

Paper 7- Applied Direct Taxation Question 1 Choose the correct answer from the given options in respect of the following: (a) If an assessee fails to furnish return of income under Section 139(1) of the

Paper 7- Applied Direct Taxation Question 1 Choose the correct answer from the given options in respect of the following: (a) If an assessee fails to furnish return of income under Section 139(1) of the

CONTENTS CONTENTS BOOK ONE : DEDUCTION OF TAX AT SOURCE DEDUCTION OF TAX AT SOURCE FROM SALARY

CONTENTS Chapter-heads I-7 BOOK ONE : DEDUCTION OF TAX AT SOURCE 1 DEDUCTION OF TAX AT SOURCE FROM SALARY 1.1 Who is responsible to deduct tax at source in case of income from salary 4 1.1-1 Where salary

CONTENTS Chapter-heads I-7 BOOK ONE : DEDUCTION OF TAX AT SOURCE 1 DEDUCTION OF TAX AT SOURCE FROM SALARY 1.1 Who is responsible to deduct tax at source in case of income from salary 4 1.1-1 Where salary

Unit 11: COMPUTATION OF TAX

Unit 11: COMPUTATION OF TAX HOW TO COMPUTE TAX PAYABLE Once the net taxable income is computed, the next step is to compute the final tax payable. The final tax payable is computed as follows: (1) Taxable

Unit 11: COMPUTATION OF TAX HOW TO COMPUTE TAX PAYABLE Once the net taxable income is computed, the next step is to compute the final tax payable. The final tax payable is computed as follows: (1) Taxable

: 3 : 100 : 8 : 8 NOTE

2/2012/TL 263 Roll No Time allowed : 3 hours : 1 : Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 8 NOTE : All references to sections mentioned in Part-A of the Question

2/2012/TL 263 Roll No Time allowed : 3 hours : 1 : Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 8 NOTE : All references to sections mentioned in Part-A of the Question

Assessment Year

Assessment Year 2016-2017 Income Income Income Income Income From Salaries from Capital Gains from Business and Profession from House Property from Other Sources Individual/HUF Firm Company Trust AOP/BOI/Co-op

Assessment Year 2016-2017 Income Income Income Income Income From Salaries from Capital Gains from Business and Profession from House Property from Other Sources Individual/HUF Firm Company Trust AOP/BOI/Co-op

CS EXECUTIVE TAX LAWS & PRACTICE CA SACHIN GUPTA

CS EXECUTIVE TAX LAWS & PRACTICE CA SACHIN GUPTA INDEX S.NO. CHAPTER NAME PAGE NO. 1. BASIC CONCEPTS OF INCOME TAX 1 26 2. RESIDENTIAL STATUS 27 47 3. INCOME UNDER HEAD HOUSE PROPERTY 48 75 4. UNDER HEAD

CS EXECUTIVE TAX LAWS & PRACTICE CA SACHIN GUPTA INDEX S.NO. CHAPTER NAME PAGE NO. 1. BASIC CONCEPTS OF INCOME TAX 1 26 2. RESIDENTIAL STATUS 27 47 3. INCOME UNDER HEAD HOUSE PROPERTY 48 75 4. UNDER HEAD

Capital Gain. seen the invisible believes the incredible and receives the imposable

Capital Gain 1. Basis of charge ( sec-45) A) There must be capital asset. B) Capital asset must have been transferred C) There must be profit or loss on such transfer D) Such capital gain should not be

Capital Gain 1. Basis of charge ( sec-45) A) There must be capital asset. B) Capital asset must have been transferred C) There must be profit or loss on such transfer D) Such capital gain should not be

Budget 2017 Synopsis Part II Analysis of Rupiya

Budget 2017 Synopsis Part II Analysis of Rupiya Facts & Findings: Out of 125 crore Indians only 15% ie 19 crore pay income tax % of Taxpayers (Out of 19 Crore) % Contribution To Tax Revenue 01% 26% 1%

Budget 2017 Synopsis Part II Analysis of Rupiya Facts & Findings: Out of 125 crore Indians only 15% ie 19 crore pay income tax % of Taxpayers (Out of 19 Crore) % Contribution To Tax Revenue 01% 26% 1%

2.f List of benefits available to Small Businessmen [AY ] S.N. Particulars Section Benefits/Deductions allowed

![2.f List of benefits available to Small Businessmen [AY ] S.N. Particulars Section Benefits/Deductions allowed](/thumbs/84/90875315.jpg "2.f List of benefits available to Small Businessmen [AY ] S.N. Particulars Section Benefits/Deductions allowed") 2.f List of benefits available to Small Businessmen [AY 2017 18] S.N. Particulars Section Benefits/Deductions allowed A. Presumptive Taxation Scheme 1. Computation of income from eligible business on presumptive

2.f List of benefits available to Small Businessmen [AY 2017 18] S.N. Particulars Section Benefits/Deductions allowed A. Presumptive Taxation Scheme 1. Computation of income from eligible business on presumptive

(ALL BATCHES) DATE: MAXIMUM MARKS: 100 TIMING: 3¼Hours. PAPER 2 : Taxation

DATE: MAXIMUM MARKS: 100 TIMING: 3¼Hours. PAPER 2 : Taxation") (ALL BATCHES) DATE: 02.08.2018 MAXIMUM MARKS: 100 TIMING: 3¼Hours PAPER 2 : Taxation SECTION - A Answer:1 (a) Computation of total income and tax liability of Dr. Niranjana for A.Y. 2018-19 I Income from

(ALL BATCHES) DATE: 02.08.2018 MAXIMUM MARKS: 100 TIMING: 3¼Hours PAPER 2 : Taxation SECTION - A Answer:1 (a) Computation of total income and tax liability of Dr. Niranjana for A.Y. 2018-19 I Income from

UNIT 7 : CAPITAL GAINS

UNIT 7 : CAPITAL GAINS Chargeability of Capital Gains: Basically, capital receipts are not liable to tax; however, certain gains arising on transfer of capital assets, are taxable u/s 45.Any profits or

UNIT 7 : CAPITAL GAINS Chargeability of Capital Gains: Basically, capital receipts are not liable to tax; however, certain gains arising on transfer of capital assets, are taxable u/s 45.Any profits or

LESSON 4 INCOME UNDER THE HEAD SALARIES - I

LESSON 4 INCOME UNDER THE HEAD SALARIES - I Dr. Gurminder Kaur STRUCTURE 4.0 Introduction 4.1 Objectives 4.2 Heads of Income 4.3 Meaning of salary 4.4 Incomes forming part of Salary - I 4.4.1. Basic Salary

LESSON 4 INCOME UNDER THE HEAD SALARIES - I Dr. Gurminder Kaur STRUCTURE 4.0 Introduction 4.1 Objectives 4.2 Heads of Income 4.3 Meaning of salary 4.4 Incomes forming part of Salary - I 4.4.1. Basic Salary

Income of other persons included in Assessee s Total Income. (Clubbing of Income) (Section 60 to 65) Sec Particulars Sec Particulars

(Section 60 to 65) Sec Particulars Sec Particulars") Income of other persons included in Assessee s Total Income (Clubbing of Income) (Section 60 to 65) Sec Particulars Sec Particulars 60 Transfer of income without transfer of assets 63 Definition of Transfer

Income of other persons included in Assessee s Total Income (Clubbing of Income) (Section 60 to 65) Sec Particulars Sec Particulars 60 Transfer of income without transfer of assets 63 Definition of Transfer

FINANCE BILL He has proposed to revise the tax slabs upwards as under:

FINANCE BILL - 2010 The 2 nd budget of the 2 nd UPA Government for the year 2010 2011 was presented by the finance minister on 26 th February 2010. The finance minister has attempted to balance his direct

FINANCE BILL - 2010 The 2 nd budget of the 2 nd UPA Government for the year 2010 2011 was presented by the finance minister on 26 th February 2010. The finance minister has attempted to balance his direct

6. PROFITS AND GAINS OF BUSINESS OR PROFESSION 2

Ph: 98851 25025/26 www.mastermindsindia.com 6. PROFITS AND GAINS OF BUSINESS OR PROFESSION 2 SOLUTIONS TO ASSIGNMENT PROBLEMS Problem No. 1 Computing business income for A.Y.2015-16 is as follows Amount

Ph: 98851 25025/26 www.mastermindsindia.com 6. PROFITS AND GAINS OF BUSINESS OR PROFESSION 2 SOLUTIONS TO ASSIGNMENT PROBLEMS Problem No. 1 Computing business income for A.Y.2015-16 is as follows Amount

8 Income from other Sources

8 Income from other Sources 8.1 Introduction Any income, profits or gains includible in the total income of an assessee, which cannot be included under any of the preceding heads of income, is chargeable

8 Income from other Sources 8.1 Introduction Any income, profits or gains includible in the total income of an assessee, which cannot be included under any of the preceding heads of income, is chargeable

BUDGET 2016 SONALEE GODBOLE

1 BUDGET 2016 SONALEE GODBOLE Penalties 2 3 Section 270A Section 271 levying penalty for failure to furnish returns, comply with notices, concealment of income, etc. will be applicable upto A.Y. 2016-17.

1 BUDGET 2016 SONALEE GODBOLE Penalties 2 3 Section 270A Section 271 levying penalty for failure to furnish returns, comply with notices, concealment of income, etc. will be applicable upto A.Y. 2016-17.

Suggested Answer_Syl2008_Jun2014_Paper_7 INTERMEDIATE EXAMINATION GROUP I (SYLLABUS 2008)

") INTERMEDIATE EXAMINATION GROUP I (SYLLABUS 2008) SUGGESTED ANSWERS TO QUESTIONS JUNE 2014 Paper-7: APPLIED DIRECT TAXATION Time Allowed : 3 Hours Full Marks : 100 Wherever required, the candidate may make

INTERMEDIATE EXAMINATION GROUP I (SYLLABUS 2008) SUGGESTED ANSWERS TO QUESTIONS JUNE 2014 Paper-7: APPLIED DIRECT TAXATION Time Allowed : 3 Hours Full Marks : 100 Wherever required, the candidate may make

TRUE TRUE. B Match the following.

Q.1 A State whether True or False (ANY 8) Ans. 1 Unabsorbed Speculative loss can be carried forward upto 8 A.Y. FALSE 2 Loss relating to long term capital asset is to be set off against short term capital

Q.1 A State whether True or False (ANY 8) Ans. 1 Unabsorbed Speculative loss can be carried forward upto 8 A.Y. FALSE 2 Loss relating to long term capital asset is to be set off against short term capital

SAPAN PARIKH COMMERCE CLASSES

income tax Time:- 2hrs.30mins [Marks: 75] 1. All questions are compulsory & carry equal marks. 2. Working note should be part of answer. Q.1. A Rewrite the following sentences by selecting correct option.

income tax Time:- 2hrs.30mins [Marks: 75] 1. All questions are compulsory & carry equal marks. 2. Working note should be part of answer. Q.1. A Rewrite the following sentences by selecting correct option.

MTP_ Inter _Syllabus 2016_ June 2018_Set 2 Paper 7 Direct Taxation (DTX)

") Paper 7 Direct Taxation (DTX) Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks:

Paper 7 Direct Taxation (DTX) Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks:

CA Final Paper 7 Direct Tax Laws Ch13 Unit1 CA Sudhindra Kumar Jain

CA Final Paper 7 Direct Tax Laws Ch13 Unit1 CA Sudhindra Kumar Jain 2 Definition Section 2(17) In Which Public Are Substantially Interested Section 2(18) Indian Company Section 2(26) Domestic Company Section

CA Final Paper 7 Direct Tax Laws Ch13 Unit1 CA Sudhindra Kumar Jain 2 Definition Section 2(17) In Which Public Are Substantially Interested Section 2(18) Indian Company Section 2(26) Domestic Company Section

Lesson 1 DEFINITIONS. Previous Year [Section 3]

![Lesson 1 DEFINITIONS. Previous Year [Section 3]](/thumbs/90/102179790.jpg "Lesson 1 DEFINITIONS. Previous Year [Section 3]") Lesson 1 DEFINITIONS Assessment Year [Section 2(9)] 1. Assessment year means the period of twelve months commencing on the first day of April every year and ending on 31 st March of next year. (For June

Lesson 1 DEFINITIONS Assessment Year [Section 2(9)] 1. Assessment year means the period of twelve months commencing on the first day of April every year and ending on 31 st March of next year. (For June

TAX GUIDE F.Y (A.Y ) Further information can be obtained from: KANTILAL PATEL & CO.

Further information can be obtained from: KANTILAL PATEL & CO.") TAX GUIDE - 2011 F.Y. 2011-2012 (A.Y. 2012-2013) Further information can be obtained from: KANTILAL PATEL & CO. 202, Paritosh, Usmanpura (River Front) Ahmedabad 380 013 Tele. No.: 27551333 / 27752333 E-mail:

TAX GUIDE - 2011 F.Y. 2011-2012 (A.Y. 2012-2013) Further information can be obtained from: KANTILAL PATEL & CO. 202, Paritosh, Usmanpura (River Front) Ahmedabad 380 013 Tele. No.: 27551333 / 27752333 E-mail:

Answer to MTP_Intermediate_Syllabus2016_Dec2018_Set1 Paper 7- Direct Taxation

Paper 7- Direct Taxation Dos, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7- Direct Taxation Full Marks : 100 Time allowed: 3 hours Answer Question

Paper 7- Direct Taxation Dos, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7- Direct Taxation Full Marks : 100 Time allowed: 3 hours Answer Question

Intermediate Group I Paper 7 : DIRECT TAXATION (SYLLABUS 2016)

") Intermediate Group I Paper 7 : DIRECT TAXATION (SYLLABUS 2016) Objectives 1. (a) Multiple Choice Questions: 1. When the shares are held in unlisted company, it is trusted as long term capital assets when

Intermediate Group I Paper 7 : DIRECT TAXATION (SYLLABUS 2016) Objectives 1. (a) Multiple Choice Questions: 1. When the shares are held in unlisted company, it is trusted as long term capital assets when

Computation of income from house property of Mr. Aakarsh for A.Y (i) Unrealised rent recovered 17,000. (ii) Arrears of rent received 28,000

Unrealised rent recovered 17,000. (ii) Arrears of rent received 28,000") IPCC November 2017 DIRECT TAXATION Test Code 80107 Branch (MULTIPLE) (Date : 17.09.2017) (50 Marks) Note: All questions are compulsory. Question 1(4 marks) Since the unrealised rent was recovered in the

IPCC November 2017 DIRECT TAXATION Test Code 80107 Branch (MULTIPLE) (Date : 17.09.2017) (50 Marks) Note: All questions are compulsory. Question 1(4 marks) Since the unrealised rent was recovered in the

DISCLAIMER. The Institute of Chartered Accountants of India

DISCLAIMER The Suggested Answers hosted in the website do not constitute the basis for evaluation of the students answers in the examination. The answers are prepared by the Faculty of the Board of Studies

DISCLAIMER The Suggested Answers hosted in the website do not constitute the basis for evaluation of the students answers in the examination. The answers are prepared by the Faculty of the Board of Studies

LOYOLA COLLEGE (AUTONOMOUS), CHENNAI

, CHENNAI") LOYOLA COLLEGE (AUTONOMOUS), CHENNAI 600 034 M.Com.DEGREE EXAMINATION COMMERCE SECOND SEMESTER APRIL 2018 17PCO2MC01 DIRECT TAX PLANNING AND MANAGEMENT Date: 17042018 Dept. No. Max. : 100 Marks Time: 01:0004:00

LOYOLA COLLEGE (AUTONOMOUS), CHENNAI 600 034 M.Com.DEGREE EXAMINATION COMMERCE SECOND SEMESTER APRIL 2018 17PCO2MC01 DIRECT TAX PLANNING AND MANAGEMENT Date: 17042018 Dept. No. Max. : 100 Marks Time: 01:0004:00

1 Basic concepts. 2 Residential status and tax incidence. u A few words from the authors I-5 u About the authors I-7 u Section-wise Index I-25 I-9

Contents u A few words from the authors I-5 u About the authors I-7 u Section-wise Index I-25 1 Basic concepts 1. Assessment year 1 2. Previous year 1 3. Person 5 4. Assessee 6 5. Charge of income-tax

Contents u A few words from the authors I-5 u About the authors I-7 u Section-wise Index I-25 1 Basic concepts 1. Assessment year 1 2. Previous year 1 3. Person 5 4. Assessee 6 5. Charge of income-tax

Paper-7 Direct Taxation

Paper-7 Direct Taxation Time Allowed: 3 hours Full Marks: 100 All the questions relate to the assessment year 2014-15, unless stated otherwise. Working notes should form part of the answers. Section A

Paper-7 Direct Taxation Time Allowed: 3 hours Full Marks: 100 All the questions relate to the assessment year 2014-15, unless stated otherwise. Working notes should form part of the answers. Section A

1. Basic concepts of Income Tax

Quick review of the chapter: Sections Particulars Sec. 2(7) Assessee Sec. 2(9) Assessment year Sec. 2(24) Income Sec. 2 (31) Person Sec. 2(34) & 3 "Previous Year" defined Sec. 80B(5) Gross total income

Quick review of the chapter: Sections Particulars Sec. 2(7) Assessee Sec. 2(9) Assessment year Sec. 2(24) Income Sec. 2 (31) Person Sec. 2(34) & 3 "Previous Year" defined Sec. 80B(5) Gross total income

10 Aggregation of Income, Set-off and Carry Forward of Losses

10 Aggregation of Income, Set-off and Carry Forward of Losses 10.1 Aggregation of Income In certain cases, some amounts are deemed as income in the hands of the assessee though they are actually not in

10 Aggregation of Income, Set-off and Carry Forward of Losses 10.1 Aggregation of Income In certain cases, some amounts are deemed as income in the hands of the assessee though they are actually not in

Instructions for filling out FORM ITR-2

Instructions for filling out FORM ITR-2 1. Legal status of instructions These instructions though stated to be non-statutory, may be taken as guidelines for filling the particulars in this Form. In case

Instructions for filling out FORM ITR-2 1. Legal status of instructions These instructions though stated to be non-statutory, may be taken as guidelines for filling the particulars in this Form. In case

Income from Salaries. 4.1 Salary

4 Income from Salaries 4.1 Salary The meaning of the term salary for purposes of income tax is much wider than what is normally understood. Every payment made by an employer to his employee for service

4 Income from Salaries 4.1 Salary The meaning of the term salary for purposes of income tax is much wider than what is normally understood. Every payment made by an employer to his employee for service

Question 1(6marks) Computation of taxable capital gains of Mr. Aakash for the A.Y (2 Marks)

Computation of taxable capital gains of Mr. Aakash for the A.Y (2 Marks)") IPCC November 2017 DIRECT TAXATION Test Code 8067 Branch (MULTIPLE) (Date : 23.07.2017) (50 Marks) Note: All questions are compulsory. Question 1(6marks) Computation of taxable capital gains of Mr. Aakash

IPCC November 2017 DIRECT TAXATION Test Code 8067 Branch (MULTIPLE) (Date : 23.07.2017) (50 Marks) Note: All questions are compulsory. Question 1(6marks) Computation of taxable capital gains of Mr. Aakash

Instructions for filling out FORM ITR-2

Instructions for filling out FORM ITR-2 These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act,

Instructions for filling out FORM ITR-2 These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act,

CHAPTER - 7 INCOME FROM OTHER SOURCES

Section CHAPTER - 7 INCOME FROM OTHER SOURCES Particulars 56(1) Income from other sources Charging section 56(2) Specific incomes included under income from other sources. 56(2)(ib) 56(2)(vi)/(vii) 56(2)(viia)

Section CHAPTER - 7 INCOME FROM OTHER SOURCES Particulars 56(1) Income from other sources Charging section 56(2) Specific incomes included under income from other sources. 56(2)(ib) 56(2)(vi)/(vii) 56(2)(viia)

Presentation on TDS Salary & TDS in respect of Residents

Presentation on TDS Salary & TDS in respect of Residents R. J. Soni & Associates Corporate Office: MUMBAI Kamla Niwas Plot No. 136/141 Gorai-1 Borivali (W) Mumbai-091. Offices:- MUMBAI JAIPUR PUNE AHEMDABAD

Presentation on TDS Salary & TDS in respect of Residents R. J. Soni & Associates Corporate Office: MUMBAI Kamla Niwas Plot No. 136/141 Gorai-1 Borivali (W) Mumbai-091. Offices:- MUMBAI JAIPUR PUNE AHEMDABAD

P7_Practice Test Paper_Syl12_Dec13_Set 1

Direct Taxation Section A (Question No. 1 is compulsory and any four from Question No. 2 to 6] 1. (a) Answer each of the following questions: (i) T Ltd. purchased a plant costing `10 lakhs. Before commencement

Direct Taxation Section A (Question No. 1 is compulsory and any four from Question No. 2 to 6] 1. (a) Answer each of the following questions: (i) T Ltd. purchased a plant costing `10 lakhs. Before commencement

Appeal, Set comm., DRP Etc Mock Test IGP-CS CA Vivek Gaba

1. Taking full advantage of loopholes of law so as to attract least incidence of tax is known as a) Tax planning b) Tax evasion c) Tax avoidance d) Tax management 2. Which is the relevant Form No. for

1. Taking full advantage of loopholes of law so as to attract least incidence of tax is known as a) Tax planning b) Tax evasion c) Tax avoidance d) Tax management 2. Which is the relevant Form No. for

C.S. Executive Tax Law Dec.09 Solved Ans. 1

C.S. Executive Tax Law Dec.09 Solved Ans. 1 Qn. 1. (A) Choose the most appropriate answer from the given options in respect of the following having regard to the provisions of the relevant direct, tax

C.S. Executive Tax Law Dec.09 Solved Ans. 1 Qn. 1. (A) Choose the most appropriate answer from the given options in respect of the following having regard to the provisions of the relevant direct, tax

Tax essentials for Individuals

Tax Rates The income tax rates are: Taxable Income for Men Rate Taxable Income for Women Rate Up to Rs. 1,80,000 Nil Up to Rs. 1,90,000 Nil 1,80,001 to 5,00,000 10% 1,90,001 to 5,00,000 10% 5,00,001 to

Tax Rates The income tax rates are: Taxable Income for Men Rate Taxable Income for Women Rate Up to Rs. 1,80,000 Nil Up to Rs. 1,90,000 Nil 1,80,001 to 5,00,000 10% 1,90,001 to 5,00,000 10% 5,00,001 to

Answer to MTP_Intermediate_Syllabus2016_Dec2018_Set2 Paper 7- Direct Taxation

Paper 7- Direct Taxation Dos, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7- Direct Taxation Full Marks : 100 Time allowed: 3 hours Answer Question

Paper 7- Direct Taxation Dos, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7- Direct Taxation Full Marks : 100 Time allowed: 3 hours Answer Question

There is no Such Thing as a Good Tax (Winston Churchill)

") There is no Such Thing as a Good Tax (Winston Churchill) Tax structure refers to the systematic arrangement of various taxes and the factors influencing them such as tax base, tax rate, frequency of change

There is no Such Thing as a Good Tax (Winston Churchill) Tax structure refers to the systematic arrangement of various taxes and the factors influencing them such as tax base, tax rate, frequency of change

UCM 54 INCOME TAX LAW & PRACTICE - I Unit-1 Introduction to Income Tax Act 1961 Type:20% Theory 80% Problem Question & Answers

UCM 54 INCOME TAX LAW & PRACTICE - I Unit-1 Introduction to Income Tax Act 1961 Type:20% Theory 80% Problem Question & Answers PART A 1. What is assessment year? (April 2014, 2013, 2012) ASSESSMENT YEAR

UCM 54 INCOME TAX LAW & PRACTICE - I Unit-1 Introduction to Income Tax Act 1961 Type:20% Theory 80% Problem Question & Answers PART A 1. What is assessment year? (April 2014, 2013, 2012) ASSESSMENT YEAR

SALARY HEAD SUMMARY NOTES

1 INTRODUCTORY PROVISIONS: There must exist a relationship of employer-employee between the payer & the payee. It does not matter whether employee is a full-time employee or a part-time one. Employer-Employee

1 INTRODUCTORY PROVISIONS: There must exist a relationship of employer-employee between the payer & the payee. It does not matter whether employee is a full-time employee or a part-time one. Employer-Employee

BATCH : GI 1 to GI 5

(0.5 6=3M) MITTAL COMMERCE CLASSES BATCH : GI 1 to GI 5 DATE: 18.08.2017 MAXIMUM MARKS: 100 TIMING: 3 Hours PAPER 4 : TAXATION Question No. 1 is Compulsory Answer any five questions from the remaining

(0.5 6=3M) MITTAL COMMERCE CLASSES BATCH : GI 1 to GI 5 DATE: 18.08.2017 MAXIMUM MARKS: 100 TIMING: 3 Hours PAPER 4 : TAXATION Question No. 1 is Compulsory Answer any five questions from the remaining

Free of Cost ISBN: CS Executive Programme Module-I (Solution upto June & Questions of Dec Included)

") Free of Cost ISBN: 978-93-5034-584-9 Appendix CS Executive Programme Module-I (Solution upto June - 2013 & Questions of Dec - 2013 Included) Paper - 3: Tax Laws Chapter - 3: Basis of Charge and Scope of

Free of Cost ISBN: 978-93-5034-584-9 Appendix CS Executive Programme Module-I (Solution upto June - 2013 & Questions of Dec - 2013 Included) Paper - 3: Tax Laws Chapter - 3: Basis of Charge and Scope of

Elective Course in Commerce ECO-11 Elements of Income Tax APPENDIX 2013 Assessment Year

Elective Course in Commerce ECO-11 Elements of Income Tax APPENDIX 2013 Assessment Year 2012-2013 School of Management Studies Indira Gandhi National Open University New Delhi 110068 Dear Student, As you

Elective Course in Commerce ECO-11 Elements of Income Tax APPENDIX 2013 Assessment Year 2012-2013 School of Management Studies Indira Gandhi National Open University New Delhi 110068 Dear Student, As you

Compiled Summary of Income Tax Provisions

Income Tax Page: 1 Compiled Summary of Income Tax Provisions CONTENTS S.No. Chapter Name Page No 1 Residential Status and Scope of Total Income 02 2 Salaries 08 3 Income from House Property 26 4 Profit

Income Tax Page: 1 Compiled Summary of Income Tax Provisions CONTENTS S.No. Chapter Name Page No 1 Residential Status and Scope of Total Income 02 2 Salaries 08 3 Income from House Property 26 4 Profit

Suggested Answer_Syl2008_June2015_Paper_7 INTERMEDIATE EXAMINATION GROUP I (SYLLABUS 2008)

") INTERMEDIATE EXAMINATION GROUP I (SYLLABUS 2008) SUGGESTED ANSWERS TO QUESTIONS JUNE 2015 Paper-7: APPLIED DIRECT TAXATION Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the right

INTERMEDIATE EXAMINATION GROUP I (SYLLABUS 2008) SUGGESTED ANSWERS TO QUESTIONS JUNE 2015 Paper-7: APPLIED DIRECT TAXATION Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the right

SAMVIT ACADEMY IPCC MOCK EXAM

Disclaimer (Read carefully) SUGGESTED ANSWERS - Group 1 Taxation (Code GST) The answers given below are prepared by the faculty of Samvit Academy as per their views and experience. The working notes, notes

Disclaimer (Read carefully) SUGGESTED ANSWERS - Group 1 Taxation (Code GST) The answers given below are prepared by the faculty of Samvit Academy as per their views and experience. The working notes, notes

Click Here to Get More Updates On CA & CS On WHATSAPP

LIST OF IMPORTANT SECTIONS IMPORTANT DEFINITIONS & BASIC CONCEPTS 2(31) Person 3 P.Y. 2(9) A.Y. 2(7) Assessee 2(24) Income 2(45) Total Income RESIDENTIAL STATUS 2(26) Indian Company 2(30) NR Individual

LIST OF IMPORTANT SECTIONS IMPORTANT DEFINITIONS & BASIC CONCEPTS 2(31) Person 3 P.Y. 2(9) A.Y. 2(7) Assessee 2(24) Income 2(45) Total Income RESIDENTIAL STATUS 2(26) Indian Company 2(30) NR Individual

Answer_MTP_ Inter _Syllabus 2016_ Dec 2017_Set 2 Paper 7 Direct Taxation

Paper 7 Direct Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks: 100

Paper 7 Direct Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks: 100

BATCH : LI 1, 2, 3, 4, 5, 6, 7 & 8

BATCH : LI 1, 2, 3, 4, 5, 6, 7 & 8 DATE: 04.10.2016 MAXIMUM MARKS: 100 TIMING: 3 Hours PAPER 4 : TAXATION Question No. 1 is Compulsory Answer any five questions from the remaining six questions. Wherever

BATCH : LI 1, 2, 3, 4, 5, 6, 7 & 8 DATE: 04.10.2016 MAXIMUM MARKS: 100 TIMING: 3 Hours PAPER 4 : TAXATION Question No. 1 is Compulsory Answer any five questions from the remaining six questions. Wherever

Basics of Income Tax

CHAPTER : Basics of Income Tax CONCEPT 1: Short Title, Extent and Commencement [Section 1] a) Short title : Income Tax Act 1961 b) Extent : Whole of India c) Commencement : 1 st April, 1962 CONCEPT 2:

CHAPTER : Basics of Income Tax CONCEPT 1: Short Title, Extent and Commencement [Section 1] a) Short title : Income Tax Act 1961 b) Extent : Whole of India c) Commencement : 1 st April, 1962 CONCEPT 2: