Assessment Year

|

|

|

- Erik Logan

- 5 years ago

- Views:

Transcription

1 Assessment Year

2 Income Income Income Income Income From Salaries from Capital Gains from Business and Profession from House Property from Other Sources

3 Individual/HUF Firm Company Trust AOP/BOI/Co-op societies/ Local Authorities/AJP

4

5

6 Due dates Of Filling ITR A.Y : 1- Individual/HUF/AOP/BOI/Co-operative society/partnership Firm (Except those mentioned in Point 2 & 3 Below) : 31st July Companies and Person who are liable to get his account audited u/s 44AB including partners of firms, those covered under 44AB: 30th September Persons required to furnish a report under section 92E relating to international transaction(s) from an accountant : 30th November 2016

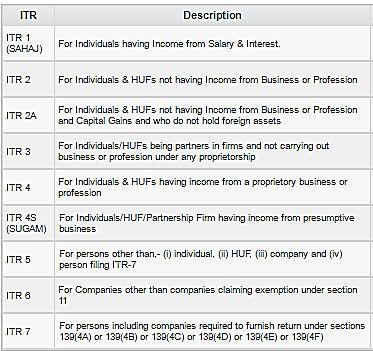

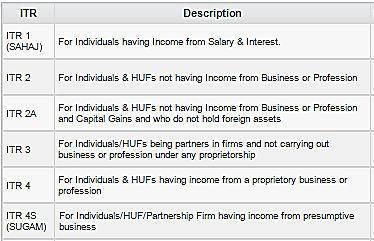

7 This Return Form is to be used by an individual whose total income for the assessment year includes: Income from Salary/ Pension; or Income from One House Property (excluding cases where loss is brought forward from previous years); or Income from Other Sources (excluding Winning from Lottery and Income from Race Horses) Who cannot use this Return Form: This Return Form cannot be used by any resident having any asset (including financial interest in any entity) located outside India or signing authority in any account located outside India. If you have foreign assets, you cannot use ITR-1. If you have exempt income which is more than Rs. 5,000, you cannot use ITR-1.

8 This tax return form is to be used by: Taxpayers who have salary income and own more than one house property and DO NOT have any capital gains. Those who have long-term capital gains from transactions on which Securities Transaction Tax is paid (which are exempt) from tax can still use this form. NRIs can file ITR-2A, if applicable, however residents who have a foreign asset or foreign income CANNOT file this form. Who cannot use this Return Form? This income tax return ITR -2A CANNOT be filed by those who have: Income from Capital Gains Income from Business or Profession Any claim of relief/deduction under section 90, 90A or 91( Double Taxation Relief) Any resident having any asset (including financial interest in any entity) located outside India or signing authority in any account located outside India Any resident having income from any source outside India.

9 This Return Form is to be used by an individual or a HUF whose total income for the assessment year includes: Income from Salary/Pension; or Income from House Property; or Income from Capital Gains; or Income from Other Sources (including Winnings from Lottery and Income from Race Horses). Further, in a case where the income of another person like one's spouse, child, etc. is to be clubbed with the income of the assesse, this Return Form can be used where such income falls in any of the above categories. Who cannot use this Return Form: This Return Form should not be used by an individual whose total income for the assessment year includes Income from Business or Profession or if you receive remuneration as a Partner in a Partnership Firm or LLP.

10 This Return Form is to be used by an individual or an Hindu Undivided Family who is a partner in a Partnership Firm or LLP and where income chargeable to income-tax under the head Profits or gains of business or professional does not include any income except the income by way of any interest, salary, bonus, commission or remuneration, by whatever name called, due to, or received by him from such firm. In case a partner in the firm does not have any income from the firm by way of interest, salary, etc. and has only exempt income by way of share in the profit of the firm, he shall use this form only and not Form ITR-2. This Return Form should not be used by an individual whose total income for the assessment year includes Income from Business or Profession under any proprietorship.

11 Income tax Return to be filed by individuals, HUF and small business taxpayers having : Presumptive Business Income Salary / Pension One house property Income from other sources. This form cannot be used if, taxpayer Has more than one house property Speculative income Agriculture income more than Rs 5000 Winning from lotteries/races Capital gains Losses to be carried forward

12 Income Tax Rates Upto Rs 2,50,000 NIL Rs. 2,50,000-Rs5,00,000 10% Rs5,00,000-Rs 10,00,000 20% Above Rs. 10,00,000 30%

13 Income Tax Rates Upto Rs. 3,00,000 NIL Rs. 3,00,000-Rs. 5,00,000 10% Rs. 5,00,000-Rs. 10,00,000 20% Above Rs. 10,00,000 30%

14 Income Tax Rates Up to Rs. 5,00,000 NIL Rs. 5,00,000 - Rs. 10,00,000 20% Above Rs. 10,00,000 30%

15 Interest from bank deposits or NSC certificates should be disclosed. Deduction for investment made under 80C, 80CCC & 80 CCD is restricted to Rs 1.50 lakh for A.Y Income of spouse or minor child may have to be clubbed with the income of taxpayer. Be cautious while calculating surcharge and education cess. Double check all key information like PAN No., bank account details, communication address etc. Consideration of TDS while calculating the Gross Taxable Income. Rebate U/s 87A is too be considered. The rebate is available to a resident individual if his total income does not exceed Rs. 5,00,000. The amount of rebate shall be 100% of income-tax or Rs. 2,000, whichever is less.

16 Income Tax Form 16 is a certificate from your employer. It certifies that TDS has been deducted on your salary by the employer. If an employer deducts TDS on salary, he must issue income tax Form 16 as per tax rules of India. Form no 16 is issued once in a year, on or before 31st May of the next year immediately following the financial year in which tax is deducted. Form 16 Part A mostly contains personal information like PAN no. and others. Form 16 Part B has detailed breakup of salary paid. Relief under section 89 If you have held more than one job during the year, you ll have more than one Form 16.

17 The situation of double taxation will arise where the income gets taxed in two or more countries where due to residency or source principle as the case may be. The problem of double taxation arises if the income of a person is taxed in one country on the basis of residency and on the basis of residency in another country or on the basis of both. To mitigate the double taxation of income the provisions of double taxation relief were made. The double taxation relief is available in two ways one is unilateral relief and other is bilateral relief. Government of India can enter into agreement with a foreign government vide Entry 14 of the Union List regarding any matter provided Parliament verifies it. Double Tax Avoidance Agreement is a king of bilateral treaty or agreement, between Government of Indian and any other foreign country or specified territory outside India. Such treaty or agreement is permissible in terms of Article 253 of the Constitution of India.

18 Last dates of filing the returns is approaching fast, Please contact Dhruv at and visit our site The links to different forms of Returns is

19

Instructions for filling ITR-1 SAHAJ A.Y

Instructions for filling ITR-1 SAHAJ A.Y. 2018-19 General Instructions These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant

Instructions for filling ITR-1 SAHAJ A.Y. 2018-19 General Instructions These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant

e- filing of Income Tax Returns- An Overview

e- filing of Income Tax Returns- An Overview Presented by CA Sanjeev Soota catch me at www.caindelhi.co.in www.casanjeevsoota.com Notification No. 34/2013 dated 1 st May, 2013 Rule 12 of the Income Tax

e- filing of Income Tax Returns- An Overview Presented by CA Sanjeev Soota catch me at www.caindelhi.co.in www.casanjeevsoota.com Notification No. 34/2013 dated 1 st May, 2013 Rule 12 of the Income Tax

Income Tax Slabs & Rates for Assessment Year

Individual resident aged below 60 years (i.e. born on or after 1st April 1956) or any NRI/ HUF/ AOP/ BOI/ AJP* Income Tax i. Where the taxable income does not exceed Rs. 2,50,000/-. NIL ii. Where the taxable

Individual resident aged below 60 years (i.e. born on or after 1st April 1956) or any NRI/ HUF/ AOP/ BOI/ AJP* Income Tax i. Where the taxable income does not exceed Rs. 2,50,000/-. NIL ii. Where the taxable

TAX RECKONER

TAX RECKONER 2018-19 The rates are applicable for the Financial Year 2018-19 (AY 2019-20) and subject to enactment of the Finance Bill, 2018 Note: The tax rate card will be re-visited post enactment of

TAX RECKONER 2018-19 The rates are applicable for the Financial Year 2018-19 (AY 2019-20) and subject to enactment of the Finance Bill, 2018 Note: The tax rate card will be re-visited post enactment of

Instructions for SUGAM Income Tax Return AY

Instructions for SUGAM Income Tax Return AY 2016-17 1. General Instructions These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant

Instructions for SUGAM Income Tax Return AY 2016-17 1. General Instructions These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant

Unit 11: COMPUTATION OF TAX

Unit 11: COMPUTATION OF TAX HOW TO COMPUTE TAX PAYABLE Once the net taxable income is computed, the next step is to compute the final tax payable. The final tax payable is computed as follows: (1) Taxable

Unit 11: COMPUTATION OF TAX HOW TO COMPUTE TAX PAYABLE Once the net taxable income is computed, the next step is to compute the final tax payable. The final tax payable is computed as follows: (1) Taxable

Instructions for filling ITR-4 SUGAM A.Y

Instructions for filling ITR-4 SUGAM A.Y. 2017-18 General Instructions These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant

Instructions for filling ITR-4 SUGAM A.Y. 2017-18 General Instructions These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant

For J B Nagar Study Circle Meeting

For J B Nagar Study Circle Meeting Nature of income Individual and HUF ITR 1* (Sahaj) ITR 2 ITR 3 ITR 4 Income from salary/pension (for ordinarily resident person) Income from salary/pension (for not ordinarily

For J B Nagar Study Circle Meeting Nature of income Individual and HUF ITR 1* (Sahaj) ITR 2 ITR 3 ITR 4 Income from salary/pension (for ordinarily resident person) Income from salary/pension (for not ordinarily

SURENDER KR. SINGHAL & CO

PROPOSED TAX RATES FOR FINANCIAL YEAR 2016-17 A. Y. 2017-18 Income Tax Rates for Individuals, HUF Individuals, Hindu Undivided Families (HUF) and Artificial Jurisdictional Person: Net Income Range Income

PROPOSED TAX RATES FOR FINANCIAL YEAR 2016-17 A. Y. 2017-18 Income Tax Rates for Individuals, HUF Individuals, Hindu Undivided Families (HUF) and Artificial Jurisdictional Person: Net Income Range Income

Government of India INCOME-TAX DEPARTMENT ACKNOWLEDGEMENT

Government of India INCOME-TAX DEPARTMENT ACKNOWLEDGEMENT Received with thanks from a return of income in Form No. 3 for assessment year, having the following particulars. (a) PAN (b) Gross Total Income

Government of India INCOME-TAX DEPARTMENT ACKNOWLEDGEMENT Received with thanks from a return of income in Form No. 3 for assessment year, having the following particulars. (a) PAN (b) Gross Total Income

Instructions for filling out FORM ITR-3

Instructions for filling out FORM ITR-3 These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act,

Instructions for filling out FORM ITR-3 These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act,

Tax is imposition financial charge or other levy upon a taxpayer by a state or other the functional equivalent of the state.

1. What is Tax What is Tax? Tax is imposition financial charge or other levy upon a taxpayer by a state or other the functional equivalent of the state. How many Types of Taxes are there and what are they?

1. What is Tax What is Tax? Tax is imposition financial charge or other levy upon a taxpayer by a state or other the functional equivalent of the state. How many Types of Taxes are there and what are they?

Overview of Income-tax Return Forms

Overview of Income-tax Return Forms Seminar Organized by Members of International Tax CA. Group August 08, 2015 Presented by: CA. Ashish Garg Email: citycaashish@gmail.com Mobile No.: +919873467270 August

Overview of Income-tax Return Forms Seminar Organized by Members of International Tax CA. Group August 08, 2015 Presented by: CA. Ashish Garg Email: citycaashish@gmail.com Mobile No.: +919873467270 August

Chapter 1 : Income Tax Concept and Computation of Income Tax

Chapter 1 : Income Tax Concept and Computation of Income Tax This Chapter includes : I. Taxation in India 1. Taxes and its levying authority 2. Tax Structure 3. Hierarchy of Taxes levied and collected

Chapter 1 : Income Tax Concept and Computation of Income Tax This Chapter includes : I. Taxation in India 1. Taxes and its levying authority 2. Tax Structure 3. Hierarchy of Taxes levied and collected

Instructions for filling out FORM ITR-2

Instructions for filling out FORM ITR-2 These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act,

Instructions for filling out FORM ITR-2 These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act,

SAPAN PARIKH COMMERCE CLASSES

income tax Time:- 2hrs.30mins [Marks: 75] 1. All questions are compulsory & carry equal marks. 2. Working note should be part of answer. Q.1. A Rewrite the following sentences by selecting correct option.

income tax Time:- 2hrs.30mins [Marks: 75] 1. All questions are compulsory & carry equal marks. 2. Working note should be part of answer. Q.1. A Rewrite the following sentences by selecting correct option.

Chapter 8 Income under the Head "Income from Other Sources"

Chapter 8 Income under the Head "Income from Other Sources" 1. Basis of Charge Section 56(1) Income of every kind which is not exempt shall be chargeable to income-tax under the head "Income from Other

Chapter 8 Income under the Head "Income from Other Sources" 1. Basis of Charge Section 56(1) Income of every kind which is not exempt shall be chargeable to income-tax under the head "Income from Other

Question 1(6marks) Computation of taxable capital gains of Mr. Aakash for the A.Y (2 Marks)

Computation of taxable capital gains of Mr. Aakash for the A.Y (2 Marks)") IPCC November 2017 DIRECT TAXATION Test Code 8067 Branch (MULTIPLE) (Date : 23.07.2017) (50 Marks) Note: All questions are compulsory. Question 1(6marks) Computation of taxable capital gains of Mr. Aakash

IPCC November 2017 DIRECT TAXATION Test Code 8067 Branch (MULTIPLE) (Date : 23.07.2017) (50 Marks) Note: All questions are compulsory. Question 1(6marks) Computation of taxable capital gains of Mr. Aakash

Appeal, Set comm., DRP Etc Mock Test IGP-CS CA Vivek Gaba

1. Taking full advantage of loopholes of law so as to attract least incidence of tax is known as a) Tax planning b) Tax evasion c) Tax avoidance d) Tax management 2. Which is the relevant Form No. for

1. Taking full advantage of loopholes of law so as to attract least incidence of tax is known as a) Tax planning b) Tax evasion c) Tax avoidance d) Tax management 2. Which is the relevant Form No. for

Instructions for filling out FORM ITR-2

Instructions for filling out FORM ITR-2 1. Legal status of instructions These instructions though stated to be non-statutory, may be taken as guidelines for filling the particulars in this Form. In case

Instructions for filling out FORM ITR-2 1. Legal status of instructions These instructions though stated to be non-statutory, may be taken as guidelines for filling the particulars in this Form. In case

1. Tax on accumulated balance of recognised provident fund 111 To be computed in accordance with rule 9(1) of Part A of fourth Schedule 2. Short term

of Part A of fourth Schedule 2. Short term") Instructions for filling out FORM ITR-2 These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act,

Instructions for filling out FORM ITR-2 These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act,

How To. File Income Tax (Organizations) May 2017

May 2017") How To May 2017 File Income Tax (Organizations) For most people/organisations especially in development sector, the process of taxation itself can be confusing to many. There are various factors that affect

How To May 2017 File Income Tax (Organizations) For most people/organisations especially in development sector, the process of taxation itself can be confusing to many. There are various factors that affect

Unit 11: COMPUTATION OF TAX

Unit 11: COMPUTATION OF TAX HOW TO COMPUTE TAX PAYABLE Once the net taxable income is computed, the next step is to compute the final tax payable. The final tax payable is computed as follows: (1) Taxable

Unit 11: COMPUTATION OF TAX HOW TO COMPUTE TAX PAYABLE Once the net taxable income is computed, the next step is to compute the final tax payable. The final tax payable is computed as follows: (1) Taxable

Government of India INCOME-TAX DEPARTMENT ACKNOWLEDGEMENT

Government of India INCOME-TAX DEPARTMENT ACKNOWLEDGEMENT Received with thanks from a return of income in Form No.3 for assessment year 2006-07, having the following particulars. (a) (b) (c) (d) (e) PAN

Government of India INCOME-TAX DEPARTMENT ACKNOWLEDGEMENT Received with thanks from a return of income in Form No.3 for assessment year 2006-07, having the following particulars. (a) (b) (c) (d) (e) PAN

CHANGES IN ITR FORMS FOR A.Y Presented by: CA. Sanjay K. Agarwal

CHANGES IN ITR FORMS FOR A.Y. 2018-19 1 Presented by: CA. Sanjay K. Agarwal Email: agarwal.s.ca@gmail.com TYPES OF INCOME TAX FORMS: FORM(s) ITR 1 ITR 2 ITR 3 ITR 4 PARTICULAR For individuals being a resident

CHANGES IN ITR FORMS FOR A.Y. 2018-19 1 Presented by: CA. Sanjay K. Agarwal Email: agarwal.s.ca@gmail.com TYPES OF INCOME TAX FORMS: FORM(s) ITR 1 ITR 2 ITR 3 ITR 4 PARTICULAR For individuals being a resident

Elective Course in Commerce ECO-11 Elements of Income Tax APPENDIX 2014 Assessment Year

Elective Course in Commerce ECO-11 Elements of Income Tax APPENDIX 2014 Assessment Year 2013-2014 School of Management Studies Indira Gandhi National Open University New Delhi 110068 Dear Student, As you

Elective Course in Commerce ECO-11 Elements of Income Tax APPENDIX 2014 Assessment Year 2013-2014 School of Management Studies Indira Gandhi National Open University New Delhi 110068 Dear Student, As you

Salient features of Direct Tax Proposals of Union Budget 2011

Salient features of Direct Tax Proposals of Union Budget 2011 RATES OF INCOME-TAX FOR THE ASSESSMENT YEAR 2012-13 o Tax slab rates have been changed for individuals and HUF, which is given by way of a

Salient features of Direct Tax Proposals of Union Budget 2011 RATES OF INCOME-TAX FOR THE ASSESSMENT YEAR 2012-13 o Tax slab rates have been changed for individuals and HUF, which is given by way of a

FINANCE BILL He has proposed to revise the tax slabs upwards as under:

FINANCE BILL - 2010 The 2 nd budget of the 2 nd UPA Government for the year 2010 2011 was presented by the finance minister on 26 th February 2010. The finance minister has attempted to balance his direct

FINANCE BILL - 2010 The 2 nd budget of the 2 nd UPA Government for the year 2010 2011 was presented by the finance minister on 26 th February 2010. The finance minister has attempted to balance his direct

Computation of income from house property of Mr. Aakarsh for A.Y (i) Unrealised rent recovered 17,000. (ii) Arrears of rent received 28,000

Unrealised rent recovered 17,000. (ii) Arrears of rent received 28,000") IPCC November 2017 DIRECT TAXATION Test Code 80107 Branch (MULTIPLE) (Date : 17.09.2017) (50 Marks) Note: All questions are compulsory. Question 1(4 marks) Since the unrealised rent was recovered in the

IPCC November 2017 DIRECT TAXATION Test Code 80107 Branch (MULTIPLE) (Date : 17.09.2017) (50 Marks) Note: All questions are compulsory. Question 1(4 marks) Since the unrealised rent was recovered in the

MTP_ Intermediate _Syllabus 2012_Dec2016_Set 1 Paper 7- Direct Taxation

Paper 7- Direct Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7- Direct Taxation Full Marks : 100 Time allowed: 3 hours

Paper 7- Direct Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7- Direct Taxation Full Marks : 100 Time allowed: 3 hours

Budget 2017 Synopsis Part II Analysis of Rupiya

Budget 2017 Synopsis Part II Analysis of Rupiya Facts & Findings: Out of 125 crore Indians only 15% ie 19 crore pay income tax % of Taxpayers (Out of 19 Crore) % Contribution To Tax Revenue 01% 26% 1%

Budget 2017 Synopsis Part II Analysis of Rupiya Facts & Findings: Out of 125 crore Indians only 15% ie 19 crore pay income tax % of Taxpayers (Out of 19 Crore) % Contribution To Tax Revenue 01% 26% 1%

DEDUCTION OF TAX AT SOURCE

DEDUCTION OF TAX AT SOURCE SECTION 190 TO 206AA Section 190 Deduction at source and advance payment Section 191 Direct payment Section 192 Deduction of tax from salary income Section 193 Deduction of tax

DEDUCTION OF TAX AT SOURCE SECTION 190 TO 206AA Section 190 Deduction at source and advance payment Section 191 Direct payment Section 192 Deduction of tax from salary income Section 193 Deduction of tax

Snapshot of Tax rates specific to Mutual Funds

Tax Deduction Deductions under Chapter VI (sec 80C) Deductions under Chapter VI (sec 80C) Deduction under Pension scheme (sec 80C). NSC (sec 80C). Public Provident Fund (sec 80C). Employees Provident Fund

Tax Deduction Deductions under Chapter VI (sec 80C) Deductions under Chapter VI (sec 80C) Deduction under Pension scheme (sec 80C). NSC (sec 80C). Public Provident Fund (sec 80C). Employees Provident Fund

MTP_ Inter _Syllabus 2016_ June 2018_Set 2 Paper 7 Direct Taxation (DTX)

") Paper 7 Direct Taxation (DTX) Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks:

Paper 7 Direct Taxation (DTX) Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks:

Income Tax Reckoner AY:

1. Rates of Income Tax Individuals having income > 5 Lacs* Individuals & Charitable Trust Senior Citizen (60 to 79) Very Senior citizen (80 and above) Rates Up to ` 2.00 Lacs Up to ` 2.50 Lacs Up to `

1. Rates of Income Tax Individuals having income > 5 Lacs* Individuals & Charitable Trust Senior Citizen (60 to 79) Very Senior citizen (80 and above) Rates Up to ` 2.00 Lacs Up to ` 2.50 Lacs Up to `

Who can use this form Who cannot use this form Mode of filing. Individuals whose total income includes:

INCOME TAX: Central Board of Direct Taxes (CBDT) has notified the rules for filing incometax returns for the Assessment Year (AY) 2013-14: Income Tax Service Tax Central Excise Customs FEMA ITR Form Who

INCOME TAX: Central Board of Direct Taxes (CBDT) has notified the rules for filing incometax returns for the Assessment Year (AY) 2013-14: Income Tax Service Tax Central Excise Customs FEMA ITR Form Who

2.f List of benefits available to Small Businessmen [AY ] S.N. Particulars Section Benefits/Deductions allowed

![2.f List of benefits available to Small Businessmen [AY ] S.N. Particulars Section Benefits/Deductions allowed](/thumbs/84/90875315.jpg "2.f List of benefits available to Small Businessmen [AY ] S.N. Particulars Section Benefits/Deductions allowed") 2.f List of benefits available to Small Businessmen [AY 2017 18] S.N. Particulars Section Benefits/Deductions allowed A. Presumptive Taxation Scheme 1. Computation of income from eligible business on presumptive

2.f List of benefits available to Small Businessmen [AY 2017 18] S.N. Particulars Section Benefits/Deductions allowed A. Presumptive Taxation Scheme 1. Computation of income from eligible business on presumptive

Marking Scheme. Session TAXATION (782) CLASS XII. Total marks: 100 Theory: 60 Marks Practical: 40 Marks. 1 Deduction From Gross Total Income

CLASS XII. Total marks: 100 Theory: 60 Marks Practical: 40 Marks. 1 Deduction From Gross Total Income") Marking Scheme Session 2018-19 TAXATION (782) CLASS XII Total marks: 100 Theory: 60 Marks Practical: 40 Marks UNITS UNIT NAME TOTAL 1 Deduction From Gross Total Income 2 Computation Of Ta x Liability Of

Marking Scheme Session 2018-19 TAXATION (782) CLASS XII Total marks: 100 Theory: 60 Marks Practical: 40 Marks UNITS UNIT NAME TOTAL 1 Deduction From Gross Total Income 2 Computation Of Ta x Liability Of

Taxation of dividends of mutual fund schemes. Liquid funds 25.75% 28.32% Other debt funds. Equity funds Nil Nil

8 Tax Corner Tax Corner Mutual Fund What tax benefits are available to those who invest in mutual funds? Dividends declared by debt-oriented mutual funds (i.e. mutual funds with less than 65% of assets

8 Tax Corner Tax Corner Mutual Fund What tax benefits are available to those who invest in mutual funds? Dividends declared by debt-oriented mutual funds (i.e. mutual funds with less than 65% of assets

Area/locality; Town/City/District; State; Country. Pin code is mandatory. Tick mark the appropriate box for residential status. For non-residents cert

(ii) (iii) (iv) by furnishing the return electronically under digital signature; by transmitting the data in the return electronically under electronic verification code; by transmitting the data in the

(ii) (iii) (iv) by furnishing the return electronically under digital signature; by transmitting the data in the return electronically under electronic verification code; by transmitting the data in the

ITS-2F [See rule 12] RETURN OF INCOME ASSESSMENT YEAR FORM No. 2F. Printed from Taxmann s Income-tax Rules on CD Page 1 of 8

![ITS-2F [See rule 12] RETURN OF INCOME ASSESSMENT YEAR FORM No. 2F. Printed from Taxmann s Income-tax Rules on CD Page 1 of 8](/thumbs/90/102199847.jpg "ITS-2F [See rule 12] RETURN OF INCOME ASSESSMENT YEAR FORM No. 2F. Printed from Taxmann s Income-tax Rules on CD Page 1 of 8") ,,,,,,,, This Form may be used only by assessees being resident individual/hindu undivided family (HUF) (a) not having income from business or profession or agricultural income or capital gains (except

,,,,,,,, This Form may be used only by assessees being resident individual/hindu undivided family (HUF) (a) not having income from business or profession or agricultural income or capital gains (except

SUGGESTED SOLUTION IPCC May 2017 EXAM. Test Code - I N J

SUGGESTED SOLUTION IPCC May 2017 EXAM DIRECT TAXATION Test Code - I N J 1 0 7 3 Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666 1 P a g e Answer-1

SUGGESTED SOLUTION IPCC May 2017 EXAM DIRECT TAXATION Test Code - I N J 1 0 7 3 Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666 1 P a g e Answer-1

Paper 7 Applied Direct Taxation Time Allowed: 3 hours Full Marks: 100

Paper 7 Applied Direct Taxation Time Allowed: 3 hours Full Marks: 100 All the questions relate to the assessment year 2014-15, unless stated otherwise. Working notes should form part of the answers. Answer

Paper 7 Applied Direct Taxation Time Allowed: 3 hours Full Marks: 100 All the questions relate to the assessment year 2014-15, unless stated otherwise. Working notes should form part of the answers. Answer

Unit 10: ADVANCE TAX AND RETURN OF INCOME

Unit 10: ADVANCE TAX AND RETURN OF INCOME Income liable for advance tax Under the scheme of advance payment of tax, every income (including capital gains, winnings from lotteries, crossword puzzles, etc.)

Unit 10: ADVANCE TAX AND RETURN OF INCOME Income liable for advance tax Under the scheme of advance payment of tax, every income (including capital gains, winnings from lotteries, crossword puzzles, etc.)

Paper 7- Direct Taxation

Paper 7- Direct Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7- Direct Taxation Full Marks: 100 Time Allowed: 3 hours

Paper 7- Direct Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7- Direct Taxation Full Marks: 100 Time Allowed: 3 hours

Income-tax and Death are the only two inevitable things in life In India, taxes were levied even in ancient times refer to Manu Smriti & Arthashastra

Income-tax and Death are the only two inevitable things in life In India, taxes were levied even in ancient times refer to Manu Smriti & Arthashastra Why to Pay Tax? It was only for the good of his subjects

Income-tax and Death are the only two inevitable things in life In India, taxes were levied even in ancient times refer to Manu Smriti & Arthashastra Why to Pay Tax? It was only for the good of his subjects

INDIAN INCOME TAX RETURN. Assessment Year FORM

INDIAN INCOME TAX RETURN Assessment Year FORM ITR-7 For persons including companies required to furnish return under section 139(4A) or section 139(4B) or section 139(4C) or section 139(4D) (Please see

INDIAN INCOME TAX RETURN Assessment Year FORM ITR-7 For persons including companies required to furnish return under section 139(4A) or section 139(4B) or section 139(4C) or section 139(4D) (Please see

As proposed in The Finance Bill, 2016 introduced by Finance Minister of India on 29th February, 2016.

1 Budget 2016-2017 Highlights for Non-Residents As proposed in The Finance Bill, 2016 introduced by Finance Minister of India on 29th February, 2016. The Indian Budget presented by the Finance Minister

1 Budget 2016-2017 Highlights for Non-Residents As proposed in The Finance Bill, 2016 introduced by Finance Minister of India on 29th February, 2016. The Indian Budget presented by the Finance Minister

IMPORTANT AMENDMENTS OF THE FINANCE ACT, /6/2011 Lecture Meeting of BCAS - C.A.Vipul Gandhi

IMPORTANT AMENDMENTS OF THE FINANCE ACT,2010 22/6/2011 Lecture Meeting of BCAS - C.A.Vipul Gandhi 1 TAX RATES AND SLABS OF INCOME TAX RATES FOR INDIVIDUAL,HUF,AOP & BOI, ARTIFICIAL JUDICIAL PERSON U/S

IMPORTANT AMENDMENTS OF THE FINANCE ACT,2010 22/6/2011 Lecture Meeting of BCAS - C.A.Vipul Gandhi 1 TAX RATES AND SLABS OF INCOME TAX RATES FOR INDIVIDUAL,HUF,AOP & BOI, ARTIFICIAL JUDICIAL PERSON U/S

MTP_ Inter _Syllabus 2016_ June 2018_Set 1 Paper 7 Direct Taxation (DTX)

") Paper 7 Direct Taxation (DTX) Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks:

Paper 7 Direct Taxation (DTX) Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks:

(A15) Status Individual HUF Firm (other than LLP) (A19) Fill only one- Tax Refundable Tax Payable Nil Tax Balance

Status Individual HUF Firm (other than LLP) (A19) Fill only one- Tax Refundable Tax Payable Nil Tax Balance") ITR-4S SUGAM PRESUMPTIVE BUSINESS INCOME TAX RETURN Assessment Year 2 0 1 6-1 7 (A1) First Name (A2) Middle Name (A3) Last Name (A4) Permanent Account Number (A5) Sex (for Individuals) (A6) Date of Birth/Formation

ITR-4S SUGAM PRESUMPTIVE BUSINESS INCOME TAX RETURN Assessment Year 2 0 1 6-1 7 (A1) First Name (A2) Middle Name (A3) Last Name (A4) Permanent Account Number (A5) Sex (for Individuals) (A6) Date of Birth/Formation

Rates of Taxes. Rates for deduction of Income

CA Mohan S. Phadke Rates of Taxes I. Rates of Income Tax in respect of income liable to tax for the assessment year 2013-14 a) In respect of income of all categories of assessees liable to tax for the

CA Mohan S. Phadke Rates of Taxes I. Rates of Income Tax in respect of income liable to tax for the assessment year 2013-14 a) In respect of income of all categories of assessees liable to tax for the

IGP-CS Basic Concept M.Test 1 CA Vivek Gaba

IGP-CS Basic Concept M.Test 1 CA Vivek Gaba 1. Power to impose income tax on agriculture income is with a) Central government b) State government c) Partly with central government and partly with state

IGP-CS Basic Concept M.Test 1 CA Vivek Gaba 1. Power to impose income tax on agriculture income is with a) Central government b) State government c) Partly with central government and partly with state

A23 A24 A25 A26 B1 B2 B3 B5 In response to notice under section In response to notice under section 153A/ 153C 7 In pursuance of an order of the

Every firm shall furnish the return where income from business or profession is computed in accordance with section 44AD, 44ADA or 44AE. Item by Item Instructions Item A1-A3 A4 A5 A6 A7 A8-A14 A15 A16

Every firm shall furnish the return where income from business or profession is computed in accordance with section 44AD, 44ADA or 44AE. Item by Item Instructions Item A1-A3 A4 A5 A6 A7 A8-A14 A15 A16

FB.COM/SUPERWHIZZ4U Income Tax Amendment for the Assessment

FB.COM/SUPERWHIZZ4U Income Tax Amendment for the Assessment Year 2014-15 - SIPOY SATISH Highlights of Change in Direct Taxes in the Union Budget 2013 1. Rate of Income Tax for Individual a) Slab Rate Assessment

FB.COM/SUPERWHIZZ4U Income Tax Amendment for the Assessment Year 2014-15 - SIPOY SATISH Highlights of Change in Direct Taxes in the Union Budget 2013 1. Rate of Income Tax for Individual a) Slab Rate Assessment

Question 1. The Institute of Chartered Accountants of India

Question 1 PAPER 5 : TAXATION Answer all questions. Working notes should form part of the answer. Wherever necessary suitable assumptions may be made by the candidates. Answer the following with reasons

Question 1 PAPER 5 : TAXATION Answer all questions. Working notes should form part of the answer. Wherever necessary suitable assumptions may be made by the candidates. Answer the following with reasons

EduPristine EduPristine For [Certificate in Accounting and Compliance] Deduction under Income Tax Chapter VI-A

![EduPristine EduPristine For [Certificate in Accounting and Compliance] Deduction under Income Tax Chapter VI-A](/thumbs/73/68984848.jpg "EduPristine EduPristine For [Certificate in Accounting and Compliance] Deduction under Income Tax Chapter VI-A") EduPristine www.edupristine.com Deduction under Income Tax Chapter VI-A Gross Total Income vs. Total Income Gross Total Income (GTI) means the aggregate of income computed under each head as per provisions

EduPristine www.edupristine.com Deduction under Income Tax Chapter VI-A Gross Total Income vs. Total Income Gross Total Income (GTI) means the aggregate of income computed under each head as per provisions

Answer_MTP_ Inter _Syllabus 2016_ June 2018_Set 2 Paper 7 Direct Taxation (DTX)

") Paper 7 Direct Taxation (DTX) Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks:

Paper 7 Direct Taxation (DTX) Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks:

Key Changes In ITR Forms For Assessment Year

Key Changes In ITR For Assessment Year 2017-18 Background The Central Board of Direct Taxes (CBDT) has notified revised Income-tax Returns (ITR) forms for Assessment Year (AY) 2017-18 on 31 st March 2017.

Key Changes In ITR For Assessment Year 2017-18 Background The Central Board of Direct Taxes (CBDT) has notified revised Income-tax Returns (ITR) forms for Assessment Year (AY) 2017-18 on 31 st March 2017.

Basics of Income Tax

CHAPTER : Basics of Income Tax CONCEPT 1: Short Title, Extent and Commencement [Section 1] a) Short title : Income Tax Act 1961 b) Extent : Whole of India c) Commencement : 1 st April, 1962 CONCEPT 2:

CHAPTER : Basics of Income Tax CONCEPT 1: Short Title, Extent and Commencement [Section 1] a) Short title : Income Tax Act 1961 b) Extent : Whole of India c) Commencement : 1 st April, 1962 CONCEPT 2:

Elective Course in Commerce ECO-11 Elements of Income Tax APPENDIX 2013 Assessment Year

Elective Course in Commerce ECO-11 Elements of Income Tax APPENDIX 2013 Assessment Year 2012-2013 School of Management Studies Indira Gandhi National Open University New Delhi 110068 Dear Student, As you

Elective Course in Commerce ECO-11 Elements of Income Tax APPENDIX 2013 Assessment Year 2012-2013 School of Management Studies Indira Gandhi National Open University New Delhi 110068 Dear Student, As you

SAMVIT ACADEMY IPCC MOCK EXAM

Disclaimer (Read carefully) SUGGESTED ANSWERS - Group 1 Taxation (Code GST) The answers given below are prepared by the faculty of Samvit Academy as per their views and experience. The working notes, notes

Disclaimer (Read carefully) SUGGESTED ANSWERS - Group 1 Taxation (Code GST) The answers given below are prepared by the faculty of Samvit Academy as per their views and experience. The working notes, notes

COMPUTATION OF TOTAL INCOME AND TAX LIABILITY

TAX NOTES- IPCC (CA) COMPUTATION OF TOTAL INCOME AND TAX LIABILITY Revisionary Notes by Chartered Hacks FEBRUARY, 2018 WWW.CHARTEREDHACKS.WORDPESS.COM Salary House/ Property Business/ Profession Capital

TAX NOTES- IPCC (CA) COMPUTATION OF TOTAL INCOME AND TAX LIABILITY Revisionary Notes by Chartered Hacks FEBRUARY, 2018 WWW.CHARTEREDHACKS.WORDPESS.COM Salary House/ Property Business/ Profession Capital

INCOME-TAX AND BASED ON FINANCE ACT, FINANCE ACT, 2007 WITH NOTES 49 I.T. NOTES 69 I.T. NOTES 97 I.T. NOTES I.T. NOTES 139 I.T.

EHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR VG.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA

EHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR VG.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA

Income Tax Return Form For Salary Person Ay

Income Tax Return Form For Salary Person Ay 2011-12 Some lethargic tax payers are in hurry for filing their Income tax return for Year 2013-14 the due date for filing for a salaried person or other tax

Income Tax Return Form For Salary Person Ay 2011-12 Some lethargic tax payers are in hurry for filing their Income tax return for Year 2013-14 the due date for filing for a salaried person or other tax

SYMBIOSIS CENTRE FOR DISTANCE LEARNING (SCDL) Subject: Direct Taxation. 1. Define the terms, Assessment Year and Previous Year.

Subject: Direct Taxation. 1. Define the terms, Assessment Year and Previous Year.") Sample Questions: Section I: Subjective Questions 1. Define the terms, Assessment Year and Previous Year. 2. Explain the concept of short term and long term capital assets. 3. Which books of account should

Sample Questions: Section I: Subjective Questions 1. Define the terms, Assessment Year and Previous Year. 2. Explain the concept of short term and long term capital assets. 3. Which books of account should

SUGGESTED SOLUTION INTERMEDIATE MAY 2019 EXAM. Test Code CIM 8174

SUGGESTED SOLUTION INTERMEDIATE MAY 2019 EXAM SUBJECT- DT Test Code CIM 8174 BRANCH - () (Date :) Head Office :Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666 1

SUGGESTED SOLUTION INTERMEDIATE MAY 2019 EXAM SUBJECT- DT Test Code CIM 8174 BRANCH - () (Date :) Head Office :Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666 1

PUNJAB STATE TRANSMISSION CORPORATION LIMITED

PUNJAB STATE TRANSMISSION CORPORATION LIMITED (Regd. Office: PSEB, Head Office, The Mall, Patiala-147001, Punjab, India) Corporate Identity Number - U40109PB2010SGC033814, Office of CFO, AO/Taxation, Shakti

PUNJAB STATE TRANSMISSION CORPORATION LIMITED (Regd. Office: PSEB, Head Office, The Mall, Patiala-147001, Punjab, India) Corporate Identity Number - U40109PB2010SGC033814, Office of CFO, AO/Taxation, Shakti

BCAS LECTURE MEETING 20 st May by CA Raman Jokhakar B. D. Jokhakar & Co.

BCAS LECTURE MEETING 20 st May 2008 by CA Raman Jokhakar B. D. Jokhakar & Co. Who is required to file a return When is it required to be filed Which form is required to be used How is the return to be

BCAS LECTURE MEETING 20 st May 2008 by CA Raman Jokhakar B. D. Jokhakar & Co. Who is required to file a return When is it required to be filed Which form is required to be used How is the return to be

Foreign Tax Credit. June 2016

Foreign Tax Credit June 2016 Table of content 1 Introduction 2 Types of Relief 3 Exemption Method 4 Credit Method 5 Double non-taxation 6 Excess FTC 7 Documentation 8 Cases where FTC not available 9 Case

Foreign Tax Credit June 2016 Table of content 1 Introduction 2 Types of Relief 3 Exemption Method 4 Credit Method 5 Double non-taxation 6 Excess FTC 7 Documentation 8 Cases where FTC not available 9 Case

Income Tax Reckoner AY:

General* 1. Rates of Income Tax Individuals & Charitable Trust, Senior Citizen (60 to 79) Very Senior citizen (80 and above) (Amount in `) Rates Up to ` 2.00 Lacs Up to ` 2.50 Lacs Up to ` 5.00 Lacs Nil

General* 1. Rates of Income Tax Individuals & Charitable Trust, Senior Citizen (60 to 79) Very Senior citizen (80 and above) (Amount in `) Rates Up to ` 2.00 Lacs Up to ` 2.50 Lacs Up to ` 5.00 Lacs Nil

DIRECT TAXES TAXATION CA IPC PART A INCOME TAX TAX DEDUCTION AND COLLECTION AT SOURCE - CA MEHUL THAKKER

DIRECT TAXES TAXATION CA IPC PART A INCOME TAX TAX DEDUCTION AND COLLECTION AT SOURCE - CA MEHUL THAKKER TAXATION PART A INCOME TAX TAX DEDUCTION AND COLLECTION AT SOURCE Relevant for May 2018 / Nov 2018

DIRECT TAXES TAXATION CA IPC PART A INCOME TAX TAX DEDUCTION AND COLLECTION AT SOURCE - CA MEHUL THAKKER TAXATION PART A INCOME TAX TAX DEDUCTION AND COLLECTION AT SOURCE Relevant for May 2018 / Nov 2018

TRUE TRUE. B Match the following.

Q.1 A State whether True or False (ANY 8) Ans. 1 Unabsorbed Speculative loss can be carried forward upto 8 A.Y. FALSE 2 Loss relating to long term capital asset is to be set off against short term capital

Q.1 A State whether True or False (ANY 8) Ans. 1 Unabsorbed Speculative loss can be carried forward upto 8 A.Y. FALSE 2 Loss relating to long term capital asset is to be set off against short term capital

Income-tax return forms for the financial year notified

from India Tax & Regulatory Services Income-tax return forms for the financial year 2017-18 notified April 9, 2018 In brief The Central Board of Direct Taxes (CBDT) has amended the Income-tax rules and

from India Tax & Regulatory Services Income-tax return forms for the financial year 2017-18 notified April 9, 2018 In brief The Central Board of Direct Taxes (CBDT) has amended the Income-tax rules and

Paper-7 Applied Direct Taxation

Paper-7 Applied Direct Taxation Time Allowed: 3 hours Full Marks: 100 All the questions relate to the assessment year 2014-15, unless stated otherwise. Working notes should form part of the answers. Answer

Paper-7 Applied Direct Taxation Time Allowed: 3 hours Full Marks: 100 All the questions relate to the assessment year 2014-15, unless stated otherwise. Working notes should form part of the answers. Answer

(A1) First Name (A2) Middle Name (A3) Last Name (A4) Permanent Account Number

First Name (A2) Middle Name (A3) Last Name (A4) Permanent Account Number") 238 THE GAZETTE OF INDIA : EXTRAORDINARY [PART II SEC. 3(i)] FORM ITR-4 SUGAM INDIAN INCOME TAX RETURN FOR PRESUMPTIVE INCOME FROM BUSINESS & PROFESSION (Please see Rule 12 of the Income-tax Rules, 1962)

238 THE GAZETTE OF INDIA : EXTRAORDINARY [PART II SEC. 3(i)] FORM ITR-4 SUGAM INDIAN INCOME TAX RETURN FOR PRESUMPTIVE INCOME FROM BUSINESS & PROFESSION (Please see Rule 12 of the Income-tax Rules, 1962)

Time allowed : 3 hours Maximum marks : 100. Total number of questions : 6 Total number of printed pages : 5

Roll No NEW SYLLABUS Time allowed : 3 hours Maximum marks : 100 Total number of questions : 6 Total number of printed pages : 5 NOTE : 1. Answer ALL Questions. 2. All references to sections mentioned in

Roll No NEW SYLLABUS Time allowed : 3 hours Maximum marks : 100 Total number of questions : 6 Total number of printed pages : 5 NOTE : 1. Answer ALL Questions. 2. All references to sections mentioned in

Tax deducted at source For the Financial year

Tax deducted at source For the Financial year 2016-17 A summary list of tax deductible from a resident, a nonresident and other persons CA K. Balachandran FCA, Coimbatore TDS summary for the AY 2017-18

Tax deducted at source For the Financial year 2016-17 A summary list of tax deductible from a resident, a nonresident and other persons CA K. Balachandran FCA, Coimbatore TDS summary for the AY 2017-18

: 3 : 100 : 8 : 8 NOTE

2/2012/TL 263 Roll No Time allowed : 3 hours : 1 : Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 8 NOTE : All references to sections mentioned in Part-A of the Question

2/2012/TL 263 Roll No Time allowed : 3 hours : 1 : Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 8 NOTE : All references to sections mentioned in Part-A of the Question

Major direct tax proposals in Finance Bill, 2017

Major direct tax proposals in Finance Bill, 2017 Member firm Individual, HUF, BOI, AOP, AJP Tax Rates There is no change in the basic exemption limit for individuals/hufs. It is proposed to reduce the

Major direct tax proposals in Finance Bill, 2017 Member firm Individual, HUF, BOI, AOP, AJP Tax Rates There is no change in the basic exemption limit for individuals/hufs. It is proposed to reduce the

CHAPTER 8: RECOVERY OF TAX TAX DEDUCTED AT SOURCE

CHAPTER 8: RECOVERY OF TAX TAX DEDUCTED AT SOURCE SECTIONS RATE PARTICULARS 192: Deduction of Tax on Slab Every Employer has a liability to deduct TDS on salary on monthly basis on tax from salary Rate

CHAPTER 8: RECOVERY OF TAX TAX DEDUCTED AT SOURCE SECTIONS RATE PARTICULARS 192: Deduction of Tax on Slab Every Employer has a liability to deduct TDS on salary on monthly basis on tax from salary Rate

Basics of Income Tax and Practical Aspects

Kalpesh D Katira & Co. Chartered Accountants Basics of Income Tax and Practical Aspects CA Kalpesh Katira 8 March 2018 2 Table of contents Overview of Income-tax in India Legal Status and Residential Status

Kalpesh D Katira & Co. Chartered Accountants Basics of Income Tax and Practical Aspects CA Kalpesh Katira 8 March 2018 2 Table of contents Overview of Income-tax in India Legal Status and Residential Status

Total turnover/ Gross receipts 30% 30% of FY > Rs 50 Cr No change in rate of Surcharge

1. Income Tax Rates: Category of Income New rate of tax Old rate Taxpayer for FY 2017-18 of tax Individuals/ Upto Rs 2.5 L Nil Nil HUF/ BOI/ Rs 2.5 to 5 L 5% 10% AOP/ Rs 5 to 10 L 20% 20% Artificial Above

1. Income Tax Rates: Category of Income New rate of tax Old rate Taxpayer for FY 2017-18 of tax Individuals/ Upto Rs 2.5 L Nil Nil HUF/ BOI/ Rs 2.5 to 5 L 5% 10% AOP/ Rs 5 to 10 L 20% 20% Artificial Above

TAX GUIDE F.Y (A.Y ) Further information can be obtained from: KANTILAL PATEL & CO.

Further information can be obtained from: KANTILAL PATEL & CO.") TAX GUIDE - 2011 F.Y. 2011-2012 (A.Y. 2012-2013) Further information can be obtained from: KANTILAL PATEL & CO. 202, Paritosh, Usmanpura (River Front) Ahmedabad 380 013 Tele. No.: 27551333 / 27752333 E-mail:

TAX GUIDE - 2011 F.Y. 2011-2012 (A.Y. 2012-2013) Further information can be obtained from: KANTILAL PATEL & CO. 202, Paritosh, Usmanpura (River Front) Ahmedabad 380 013 Tele. No.: 27551333 / 27752333 E-mail:

Contents. Finance Act, Increase in standard deduction of salaried taxpayers

Contents Amendments made by Finance Act, 2019 at a Glance I-13 1 Finance Act, 2019 1.1 Highlights of amendments made to income-tax provisions 1 1.2 Relief to small taxpayers 1 1.3 Standard deductions raised

Contents Amendments made by Finance Act, 2019 at a Glance I-13 1 Finance Act, 2019 1.1 Highlights of amendments made to income-tax provisions 1 1.2 Relief to small taxpayers 1 1.3 Standard deductions raised

Answer_MTP_ Inter _Syllabus 2016_ Dec 2017_Set 2 Paper 7 Direct Taxation

Paper 7 Direct Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks: 100

Paper 7 Direct Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks: 100

IMPORTANT CHANGES IN INCOME TAX RETURN (ITR) FORMS FOR AY by CA Sudin Sabnis

FORMS FOR AY by CA Sudin Sabnis") IMPORTANT CHANGES IN INCOME TAX RETURN (ITR) FORMS FOR AY 2018-19 by CA Sudin Sabnis Why filing correct Income Tax Return is important Law of the land Losses and Tax holiday Refunds Stich in time saves

IMPORTANT CHANGES IN INCOME TAX RETURN (ITR) FORMS FOR AY 2018-19 by CA Sudin Sabnis Why filing correct Income Tax Return is important Law of the land Losses and Tax holiday Refunds Stich in time saves

Interim Union Budget 2019 & Important changes for AY CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA, IP

, FCA, FCS, FCMA, LL.B, MIMA, DISA, IP") Interim Union Budget 2019 & Important changes for AY 2019-20 CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA, IP Shared at Nehru Place CPE Study Circle of NIRC of ICAI 7 th February 2019 INCOME

Interim Union Budget 2019 & Important changes for AY 2019-20 CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA, IP Shared at Nehru Place CPE Study Circle of NIRC of ICAI 7 th February 2019 INCOME

UNDERSTANDING-- TAXATION SYSTEM

UNDERSTANDING-- TAXATION SYSTEM TO UNDERSTAND TAXATION SYSTEM IN TOTALITY ONE HAS TO UNDERSTAND ALL OF THE FOLLOWING The Core 1 3 5 8 7 1. Act 2. Rules 3. Notifications 4. Circulars The outer effects affecting

UNDERSTANDING-- TAXATION SYSTEM TO UNDERSTAND TAXATION SYSTEM IN TOTALITY ONE HAS TO UNDERSTAND ALL OF THE FOLLOWING The Core 1 3 5 8 7 1. Act 2. Rules 3. Notifications 4. Circulars The outer effects affecting

DIRECT TAX. E TAXATION August Salary Under Section 17(1) does not includes : A. Wages B. Pension C. Interest D.

does not includes : A. Wages B. Pension C. Interest D.") 1 DIRECT TAX 1 Salary Under Section 17(1) does not includes : A. Wages B. Pension C. Interest D. Gratuity 2 Taxable Allowance from Salary : A. Conveyance allowance B. Dearness Allowances C. Children education

1 DIRECT TAX 1 Salary Under Section 17(1) does not includes : A. Wages B. Pension C. Interest D. Gratuity 2 Taxable Allowance from Salary : A. Conveyance allowance B. Dearness Allowances C. Children education

Notes on clauses.

52 Notes on clauses Clause 2, read with the First Schedule to the Bill, seeks to specify the rates at which income-tax is to be levied on income chargeable to tax for the assessment year 2009-2010 Further,

52 Notes on clauses Clause 2, read with the First Schedule to the Bill, seeks to specify the rates at which income-tax is to be levied on income chargeable to tax for the assessment year 2009-2010 Further,

Tax matters for. 18 February 2012

Tax matters for Mutual Fund 18 February 2012 Contents 1 Indian Tax regime for Mutual Fund and its constituents 2 Important Decisions 3 Recent Controversy 2 Indian Tax regime for Mutual Fund and its constituents

Tax matters for Mutual Fund 18 February 2012 Contents 1 Indian Tax regime for Mutual Fund and its constituents 2 Important Decisions 3 Recent Controversy 2 Indian Tax regime for Mutual Fund and its constituents

Budget Highlights

Budget Highlights 2018-19 DIRECT TAX PROPOSALS Chartered Accountants 1 st Floor, Sapphire Business Centre, Above SBI Vadaj Branch, Usmanpura, Ashram Road, Ahmedabad-380013 Email: apcca@apcca.com Website:

Budget Highlights 2018-19 DIRECT TAX PROPOSALS Chartered Accountants 1 st Floor, Sapphire Business Centre, Above SBI Vadaj Branch, Usmanpura, Ashram Road, Ahmedabad-380013 Email: apcca@apcca.com Website:

Income Tax Changes made in Income Tax Provisions in the Union Budget which would affect Salaried Class

Income Tax 2013-14 Changes made in Income Tax Provisions in the Union Budget 2013-14 which would affect Salaried Class A. RATES OF INCOME-TAX I. Rates of income-tax in respect of income liable to tax for

Income Tax 2013-14 Changes made in Income Tax Provisions in the Union Budget 2013-14 which would affect Salaried Class A. RATES OF INCOME-TAX I. Rates of income-tax in respect of income liable to tax for

B.Com AMENDMENTS

B.Com AMENDMENTS 2017-18 The rates of Tax as announced under the Finance Act 20 13 for the assessment year 20 14-15 are as under. 1. Very Senior Citizens (80 Years or more) Income. Tax Rate Upto Rs. 3,00,000

B.Com AMENDMENTS 2017-18 The rates of Tax as announced under the Finance Act 20 13 for the assessment year 20 14-15 are as under. 1. Very Senior Citizens (80 Years or more) Income. Tax Rate Upto Rs. 3,00,000

WESTERN INDIA REGIONAL COUNCIL OF ICAI

1 WESTERN INDIA REGIONAL COUNCIL OF ICAI E-Filing of Income Tax Returns PDF processed with CutePDF evaluation edition www.cutepdf.com Endeavor of CPC to promote voluntary compliance; to educate tax payers

1 WESTERN INDIA REGIONAL COUNCIL OF ICAI E-Filing of Income Tax Returns PDF processed with CutePDF evaluation edition www.cutepdf.com Endeavor of CPC to promote voluntary compliance; to educate tax payers

13. PROBLEMS ON TOTAL INCOME

No.1 for CA/CWA & MEC/CEC MASTER MINDS 13. PROBLEMS ON TOTAL INCOME SOLUTIONS TO ASSIGNMENT PROBLEMS Problem No.1 Name of the Assessee: Mr. Rajesh A.Y: 2015-2016 Computation of Taxable Income : Income

No.1 for CA/CWA & MEC/CEC MASTER MINDS 13. PROBLEMS ON TOTAL INCOME SOLUTIONS TO ASSIGNMENT PROBLEMS Problem No.1 Name of the Assessee: Mr. Rajesh A.Y: 2015-2016 Computation of Taxable Income : Income

10 Aggregation of Income, Set-off and Carry Forward of Losses

10 Aggregation of Income, Set-off and Carry Forward of Losses 10.1 Aggregation of Income In certain cases, some amounts are deemed as income in the hands of the assessee though they are actually not in

10 Aggregation of Income, Set-off and Carry Forward of Losses 10.1 Aggregation of Income In certain cases, some amounts are deemed as income in the hands of the assessee though they are actually not in

Budget Presented For: Klaus Vogel Group Presented By: Mr. Kuntal Dave Date: March 8, 2013

Budget 2013 Presented For: Klaus Vogel Group Presented By: Mr. Kuntal Dave Date: March 8, 2013 Index Direct Tax Proposals Implications of amendments proposed in the Finance Bill, 2013 2 Direct Tax Proposals

Budget 2013 Presented For: Klaus Vogel Group Presented By: Mr. Kuntal Dave Date: March 8, 2013 Index Direct Tax Proposals Implications of amendments proposed in the Finance Bill, 2013 2 Direct Tax Proposals

ASSESSMENT YEAR

Final Income Tax Return ASSESSMENT YEAR 008-09 This is your final income tax return. It consists of: 1. Acknowledgement. This Form will be acknowledged by the person who will receive your income tax return

Final Income Tax Return ASSESSMENT YEAR 008-09 This is your final income tax return. It consists of: 1. Acknowledgement. This Form will be acknowledged by the person who will receive your income tax return