BVZ5A/BPF5C/BVC5A/ BPG5C INCOME TAX LAW & PRACTICE I. Unit : I - V. BVZ5A/BPG5C/CYA5C - Income Tax Law & Practice - I

|

|

|

- Reynold Dickerson

- 5 years ago

- Views:

Transcription

1 BVZ5A/BPF5C/BVC5A/ BPG5C INCOME TAX LAW & PRACTICE I Unit : I - V BVZ5A/BPG5C/CYA5C - Income Tax Law & Practice - I

2 UNIT 1 Meaning & Features of Income Important definitions under Income Tax Act Tax rate of Individual Assesse Residential status Scope of total income Capital & Revenue Income exempt from tax 2

3 BASIC CONCEPTS Assessment year : The tax payer s income of previous year is assessed to tax in the assessment at the rates prescribed in Finance Act. Previous year : Income earned in a year is taxable in the next year. The year in which income is earned is known as previous year. Person : Includes an individual,huf, Company, Firm, AOP, BOI. 3

4 content: font size 20 4

5 Basic & Additional conditions Basic or Conditions (i) An individual is in India during the relevant previous year for a period amounting in all to 182 days or more. (ii) An individual is in India for a period amounting in all to 365 days or more during four years preceeding the relevant previous year & he is in India for a period of 60 days or more during the previous year. Additional Condition (i)he has been resident in India in at least Two out of Ten P.Y (ii) He has been in India atleast 730 days in all during 7 preceeding P Y 5

6 INCIDENCE OF TAX content: font size 20 6

7 FEATURES OF INCOME Definite source Legal or Illegal income Income may be received in cash or in kind Income being considered on receipt basis or accrual basis Dispute regarding title Mere relief or reimbursement of expenses Income may be permanent or temporary Gifts of personal nature PIN money Diversion of income vs Application of Income 7

8 Link below appends exempted income. List of exempted incomes Exempted income vs Deduction 8

9 Heading: font size 32 content: font size 20 9

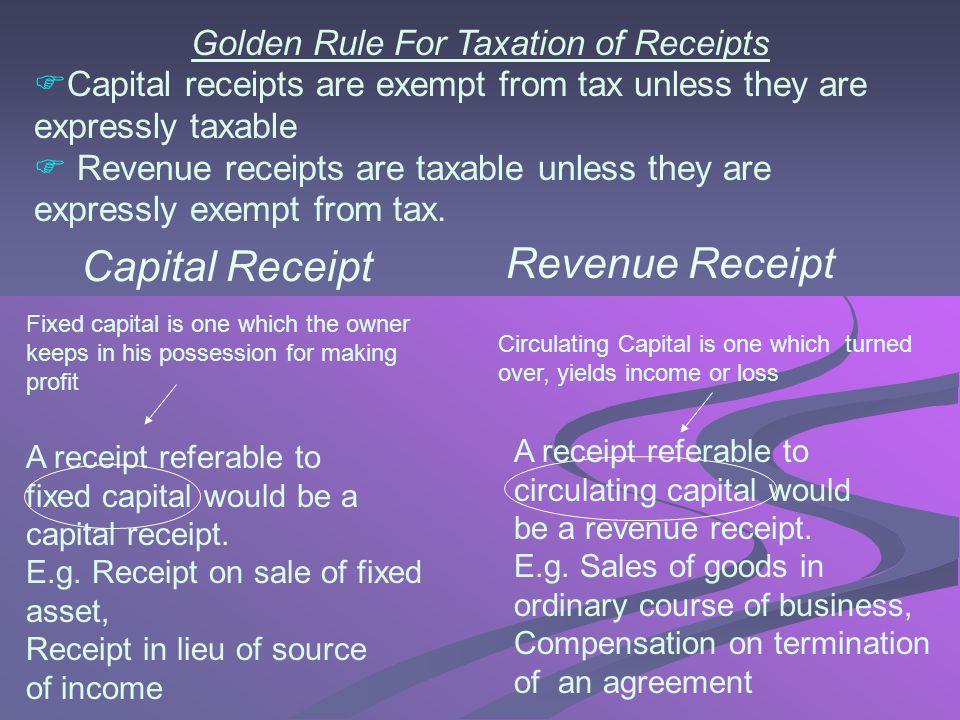

10 Heading: content: font size 20 Link below explains capital and revenue items Capital vs Revenue 10

11 11

12 UNIT 2 INCOME UNDER THE HEAD SALARIES Allowances Perquisites and their valuation Deduction from salary Gratuity Pension Commutation of pension Leave salary Profit in lieu of salary Provident funds Deductions under section 80 C 12

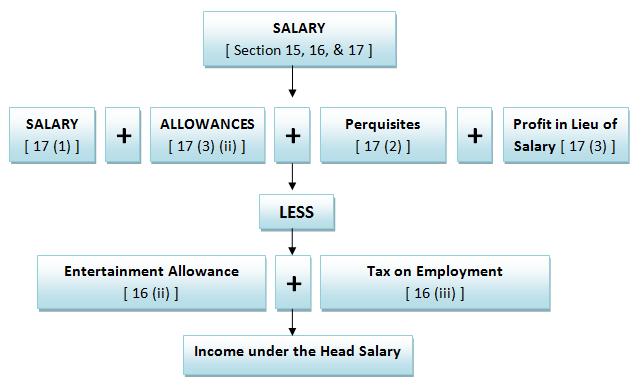

13 INCOME UNDER THE HEAD SALARIES Salaries Sec 15 to 17 Features of Salary Employer Employee Relationship Salaries and Business Profit Salaries and Professional Income Tax free Salary Leave Salary 13

Ignore for the time being")

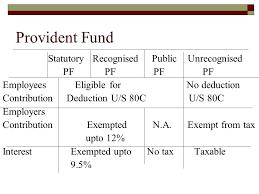

14 TREATMENT OF PROVIDENT FUND EMPLOYER S CONTRIBUTION SPF content: RPF font size 20 URPF Fully exempt from tax Exempt upto 12% of salary ( Basic + DASB + Commission on turnover) Ignore for the time being 14

15 Fully Exempted Allowance Foreign Allowances of Govt employees working outside India Allowances of U.N.O employees working in India. Allowances received by judges of high court. 15

16 Fully Taxable Allowance DA CCA MEDICAL ALLOWANCE LUNCH ALLOWANCE OVERTIME ALLOWANCE content: font size 20 DOG ALLOWANCE CAPITAL COMPENSATORY ALLOWANCE SERVANT ALLOWANCE MARRIAGE ALLOWANCE FAMILY ALLOWANCE WATER & ELECTRICITY ALLOWANCE DEPUTATION ALLOWANCE TIFFEN ALLOWANCE E.A FOR NON GOVT EMPLOYEES NON PRACTISING ALLOWANCE WARDEN ALLOWANCE PROJECT ALLOWANCE 16

Excess of rent paid over 10% of salary SALARY = basic salary + DA (forming part) + Commission based on")

17 HRA - PROVISIONS Least of following is exempt : (i) HRA actually received (ii) 50% of salary or 40% of salary (iii) Excess of rent paid over 10% of salary SALARY = basic salary + DA (forming part) + Commission based on sales 17

18 PERQUISITES View the following link to acquire knowledge about perquisites Perks 18

19 19

20 20

21 TIPS TO REMEMBER SALARY ALLOWANCES View Link below for salary allowances provisions & Revision Salary allowances REVISION INCOME UNDER HEAD SALARIES INCOME UNDER THE HEAD SALARY 21

22 22

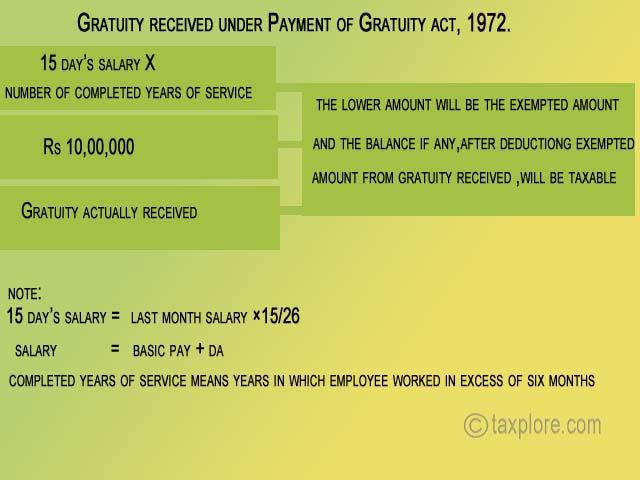

23 1. DA is taxable in the hands of. 2. Children education allowance is exempted upto. 3. Exempted limit of HRA in non metropolitan cities is. 4. Interest on RPF balance is exempted upto. 5. Statutory limit for exemption of gratuity received by Non Govt employees is. 23

24 PROBLEM COMPUTATION OF RFA Mr. A is employed in Delhi and gets following emoluments. Basic Salary Rs 8000 p.m DA - Rs 6000 ( forming part) p.m Bonus - Rs 10,000 Conveyance Allowance 500 p.m ( Actual amount spent Rs 4,000) He is provided with a rent free house. Calculate taxable value of perquisite Answer Hint : RFA 2,04,000*15/100 = Rs 30,600 24

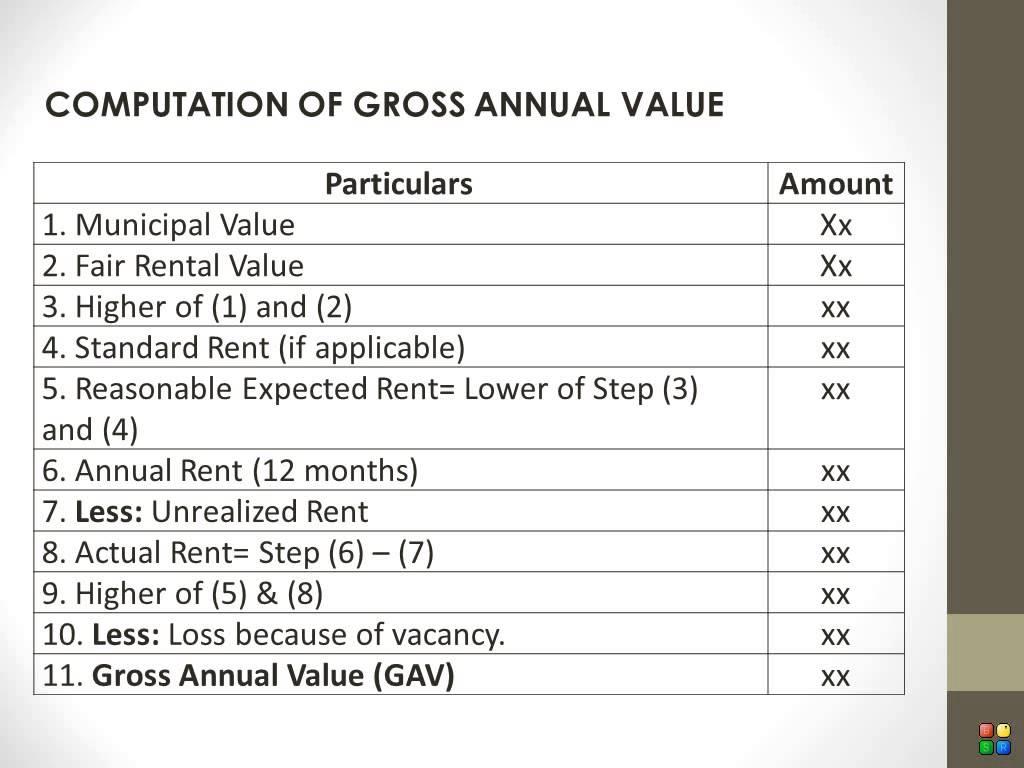

25 UNIT 3 INCOME FROM HOUSE PROPERTY Definition of annual value Deductions from Annual value Computation of income under different circumstances. 25

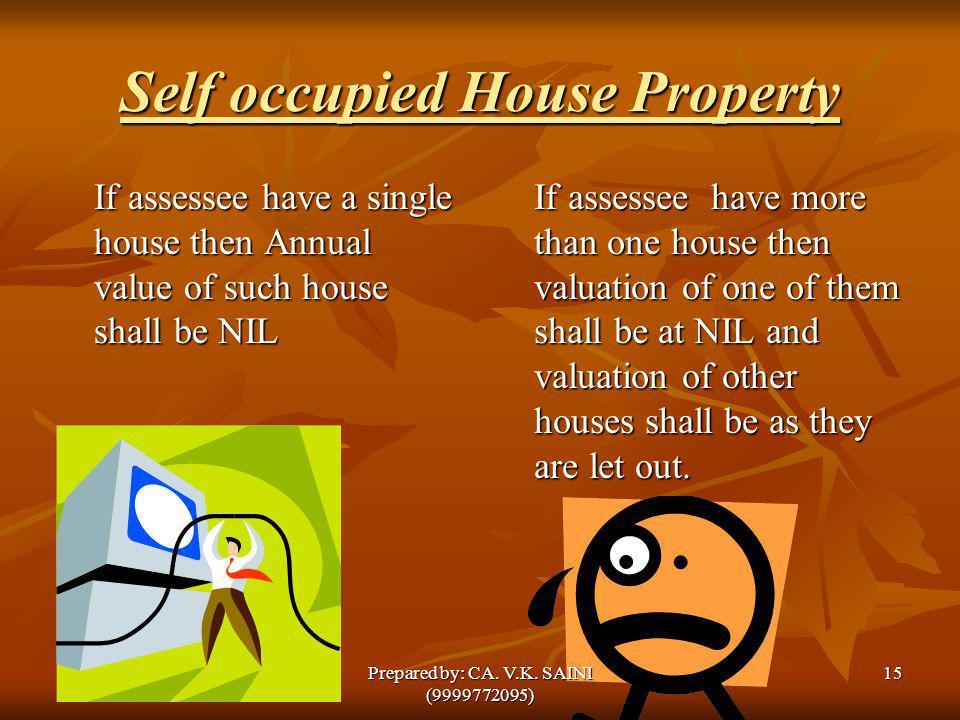

26 Particulars Let out house Self occupied house Deemed to be let out house GAV xxx NIL xxx Less : Municipal Tax paid by owner xxx NIL xxx NAV XXX NIL XXX Less : Deduction u/s 24 Std deduction xxx NIL Int on loan for construction xxx xxx xxx Net income from HP xxx (xxx) xxx 26

27 27

28 28

29 EXEMPTED INCOMES Income from farm house Property used for own business or profession Property income of hospital Property income of resident of Ladakh Income from HP owned by political party Income from HP owned by Trade union One self occupied property Annual value of any one palace of ex-indian ruler 29

30 Following video link illustrates calculation of GAV with unrealised rent GAV - House property 30

31 QUICK REVISION INCOME FROM HOUSE PROPERTY Income from house property PROBLEM INCOME FROM HOUSE PROPERTY Problem & Solution Income from House property 31

32 UNIT 4 INCOME FROM BUSINESS OR PROFESSION Allowable & not allowable expenses General deductions Provisions relating to depreciation Deemed business profits, undisclosed income Compulsory maintenance of books of accounts Special provision for computing incomes on estimated basis Computation of income from business or profession. 32

33 DEFINITION OF BUSINESS Business includes any trade, commerce, manufacture or any adventure or concern in the nature of trade, commerce or manufacture FEATURES OF BUSINESS Importance of Profit motive Business to involve two or more persons Rendering Service Business includes trade, manufacture & commerce Length of time not an essential factor Export incentives being revenue receipts. 33

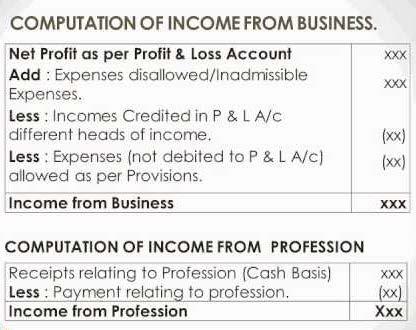

34 COMPUTATION OF BUSINESS INCOME PARTICULARS AMOUNT BALANCE AS PER P & L ACCOUNT XXX ADD : INADMISSIBLE EXPENSES XXX LESS : EXPENDITURE ALLOWED BUT NOT DEBITED LESS : INCOME CREDITED TO P&L WHICH IS TAXABLE UNDER OTHER HEADS XXX xxx 34

35 INADMISSIBLE EXPENSES Drawings by the proprietor Rent paid to self All provisions and reserves All taxes Household and personal expenses Gifts and presents (Non advertisement) Bad debts still recoverable Undervaluation of closing stock Personal LIC Capital expenses Excess depreciation Interest on Capital 35

36 INCOME CREDITED TO P&L WHICH IS TAXABLE UNDER OTHER HEADS Gifts from relatives Agricultural receipts Any Capital receipt Part time salary Dividend income Part time salary Rent from let out property Capital gains Winning from Lotteries Withdrawal from PPF Income tax refund Interest on Bank deposit 36

37 Professional income is computed by taking the professional receipts of the previous year and deducting professional expenses incurred during that year. 37

38 Preliminary expenses are deductible in 5 equal installments Expenditure exceeding Rs 20,000, shall be paid by an account payee cheque or an account payee demand draft otherwise 100% amount is disallowed. Know how acquired on or after is subject to 25% rate of depreciation. 38

39 39

40 QUICK REVISION - PGBP REVISION - PGBP 40

41 Compulsory Audit of Accounts u/s 44AB Turnover/Gross Receipts exceeding prescribed limit Business u/s 44AD,44AE,44BB Assessee Claiming deduction u/s 33AB, 33ABA,35D 41

42 UNIT 5 Assessment of Individuals (Covering incomes under Salary,House Property, Business or Profession including sec 80 C- Computation of Tax) Filing of Return Various Return Forms PAN and its usage 42

43 (a) Determination of Gross Total Income - It is ascertained by aggregating the net income under each head. (b) Deductions from Gross Total Income - The deductions are u/s 80C 80CCD 80CCC Gross total income minus these deductions will be his total income. (c)taxable Income - It is said to be total income or net income or taxable income 43

44 Rebate of Rs 5000 for individual having total taxable amount not exceeding Rs 5,00,

45 Link given below explains the types of assessment. types of assessment 45

46 DEDUCTIONS U/s 80C 80 U DEDUCTIONS 80C - 80U 46

KDF2B Income Tax Law & Practice. Unit: I to V

KDF2B Income Tax Law & Practice Unit: I to V Unit 1: Income Tax Law and Tax Planning Basic Concepts Residential Status and Tax Incidence Exempted Incomes and its related Tax planning implications Tax evasion

KDF2B Income Tax Law & Practice Unit: I to V Unit 1: Income Tax Law and Tax Planning Basic Concepts Residential Status and Tax Incidence Exempted Incomes and its related Tax planning implications Tax evasion

13. PROBLEMS ON TOTAL INCOME

No.1 for CA/CWA & MEC/CEC MASTER MINDS 13. PROBLEMS ON TOTAL INCOME SOLUTIONS TO ASSIGNMENT PROBLEMS Problem No.1 Name of the Assessee: Mr. Rajesh A.Y: 2015-2016 Computation of Taxable Income : Income

No.1 for CA/CWA & MEC/CEC MASTER MINDS 13. PROBLEMS ON TOTAL INCOME SOLUTIONS TO ASSIGNMENT PROBLEMS Problem No.1 Name of the Assessee: Mr. Rajesh A.Y: 2015-2016 Computation of Taxable Income : Income

HEADS OF INCOME. Income From Salaries MEANING OF SALARY. Characteristics of Salary 9/7/2017

Income From Salaries HEADS OF INCOME 1) Income under the head salaries (Section 15 17) 2) Income from house property (Section 22 27) 3) Profits and gains from business or profession (Section 28 44) 4)

Income From Salaries HEADS OF INCOME 1) Income under the head salaries (Section 15 17) 2) Income from house property (Section 22 27) 3) Profits and gains from business or profession (Section 28 44) 4)

LESSON 4 INCOME UNDER THE HEAD SALARIES - I

LESSON 4 INCOME UNDER THE HEAD SALARIES - I Dr. Gurminder Kaur STRUCTURE 4.0 Introduction 4.1 Objectives 4.2 Heads of Income 4.3 Meaning of salary 4.4 Incomes forming part of Salary - I 4.4.1. Basic Salary

LESSON 4 INCOME UNDER THE HEAD SALARIES - I Dr. Gurminder Kaur STRUCTURE 4.0 Introduction 4.1 Objectives 4.2 Heads of Income 4.3 Meaning of salary 4.4 Incomes forming part of Salary - I 4.4.1. Basic Salary

III BCOM (CA) [ ] Semester V Core:INCOME TAX LAW AND PRACTICE 503B Multiple Choice Questions.

![III BCOM (CA) [ ] Semester V Core:INCOME TAX LAW AND PRACTICE 503B Multiple Choice Questions.](/thumbs/71/65799137.jpg "III BCOM (CA) [ ] Semester V Core:INCOME TAX LAW AND PRACTICE 503B Multiple Choice Questions.") 1 of 23 8/12/17, 2:57 PM Dr.G.R.Damodaran College of Science (Autonomous, affiliated to the Bharathiar University, recognized by the UGC)Reaccredited at the 'A' Grade Level by the NAAC and ISO 9001:2008

1 of 23 8/12/17, 2:57 PM Dr.G.R.Damodaran College of Science (Autonomous, affiliated to the Bharathiar University, recognized by the UGC)Reaccredited at the 'A' Grade Level by the NAAC and ISO 9001:2008

SALARY HEAD SUMMARY NOTES

1 INTRODUCTORY PROVISIONS: There must exist a relationship of employer-employee between the payer & the payee. It does not matter whether employee is a full-time employee or a part-time one. Employer-Employee

1 INTRODUCTORY PROVISIONS: There must exist a relationship of employer-employee between the payer & the payee. It does not matter whether employee is a full-time employee or a part-time one. Employer-Employee

Income From Salaries

Page: SAL-1 Income From Salaries An income can be taxed under the head Salaries only if there is a relationship of an employer and employee between the payer and the payee. The relationship of employer

Page: SAL-1 Income From Salaries An income can be taxed under the head Salaries only if there is a relationship of an employer and employee between the payer and the payee. The relationship of employer

Income Tax(Al Jamia Arts and Science College)

") Income Tax is a very important direct tax. It is collected by the Central Government. It is a major source of revenue to the Central Government. History of Income Tax in India In India, Income Tax was

Income Tax is a very important direct tax. It is collected by the Central Government. It is a major source of revenue to the Central Government. History of Income Tax in India In India, Income Tax was

Tax is imposition financial charge or other levy upon a taxpayer by a state or other the functional equivalent of the state.

1. What is Tax What is Tax? Tax is imposition financial charge or other levy upon a taxpayer by a state or other the functional equivalent of the state. How many Types of Taxes are there and what are they?

1. What is Tax What is Tax? Tax is imposition financial charge or other levy upon a taxpayer by a state or other the functional equivalent of the state. How many Types of Taxes are there and what are they?

Paper 7- Direct Taxation

Paper 7- Direct Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7- Direct Taxation Full Marks: 100 Time Allowed: 3 hours

Paper 7- Direct Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7- Direct Taxation Full Marks: 100 Time Allowed: 3 hours

MTP_ Inter _Syllabus 2016_ June 2017_Set 1 Paper 7 Direct Taxation

Paper 7 Direct Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks: 100

Paper 7 Direct Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks: 100

INCOME TAX SERVICE TAX VAT TAXATION

AY 2012-13 FOR CA-IPCC MAY-NOVEMBER 2012 EXAMINATION INCOME TAX SERVICE TAX VAT TAXATION Features: Based on the Study Modules More enhanced, easy & Reader Friendly All Chapters Covered Written according

AY 2012-13 FOR CA-IPCC MAY-NOVEMBER 2012 EXAMINATION INCOME TAX SERVICE TAX VAT TAXATION Features: Based on the Study Modules More enhanced, easy & Reader Friendly All Chapters Covered Written according

Most Important Question of INCOME TAX

Most Important Question of INCOME TAX Residential Status 1. In 2 nd additional condition, assessee should have stayed in India for: a) more than 730 days during 7 immediately preceding previous year b)

Most Important Question of INCOME TAX Residential Status 1. In 2 nd additional condition, assessee should have stayed in India for: a) more than 730 days during 7 immediately preceding previous year b)

Paper 7 Applied Direct Taxation Time Allowed: 3 hours Full Marks: 100

Paper 7 Applied Direct Taxation Time Allowed: 3 hours Full Marks: 100 All the questions relate to the assessment year 2014-15, unless stated otherwise. Working notes should form part of the answers. Answer

Paper 7 Applied Direct Taxation Time Allowed: 3 hours Full Marks: 100 All the questions relate to the assessment year 2014-15, unless stated otherwise. Working notes should form part of the answers. Answer

SALARY INCOME (Sec15,16 & 17)

") SALARY INCOME (Sec15,16 & 17) What is salary? Payer & Payee More than one source Foregoing salary is salary income Tax free salary should include the tax paid by the employee Basis of Charge Salary is

SALARY INCOME (Sec15,16 & 17) What is salary? Payer & Payee More than one source Foregoing salary is salary income Tax free salary should include the tax paid by the employee Basis of Charge Salary is

Lesson 1 DEFINITIONS. Previous Year [Section 3]

![Lesson 1 DEFINITIONS. Previous Year [Section 3]](/thumbs/90/102179790.jpg "Lesson 1 DEFINITIONS. Previous Year [Section 3]") Lesson 1 DEFINITIONS Assessment Year [Section 2(9)] 1. Assessment year means the period of twelve months commencing on the first day of April every year and ending on 31 st March of next year. (For June

Lesson 1 DEFINITIONS Assessment Year [Section 2(9)] 1. Assessment year means the period of twelve months commencing on the first day of April every year and ending on 31 st March of next year. (For June

INCOME UNDER THE HEAD HOUSE PROPERTY AND IT S COMPUTATION

INCOME UNDER THE HEAD HOUSE PROPERTY AND IT S COMPUTATION 1. BASIS FOR CHARGE: - There must be a property consisting of building or land appurtenant thereto The Assessee should be owner of that property

INCOME UNDER THE HEAD HOUSE PROPERTY AND IT S COMPUTATION 1. BASIS FOR CHARGE: - There must be a property consisting of building or land appurtenant thereto The Assessee should be owner of that property

Prepared by: Bhavin Pathak

FOR IPCC and PCC Examinations ERRORLESS ENHANCED ONE STEP AHEAD Prepared by: Bhavin Pathak SPECIAL EDITION FOR NOVEMBER 2012 EXAMS INCOME TAX SERVICE TAX VAT AY 2012-13 Features: Based on the Study Modules

FOR IPCC and PCC Examinations ERRORLESS ENHANCED ONE STEP AHEAD Prepared by: Bhavin Pathak SPECIAL EDITION FOR NOVEMBER 2012 EXAMS INCOME TAX SERVICE TAX VAT AY 2012-13 Features: Based on the Study Modules

3. INCOME FROM SALARIES

SOLUTIONS TO PROBLEMS FOR CLASSROOM DISCUSSION PROBLEM NO: 1 3. INCOME FROM SALARIES a) Value of the rent free unfurnished accommodation = 15% of salary for the relevant period = 15% of [( 6000 5) + (

SOLUTIONS TO PROBLEMS FOR CLASSROOM DISCUSSION PROBLEM NO: 1 3. INCOME FROM SALARIES a) Value of the rent free unfurnished accommodation = 15% of salary for the relevant period = 15% of [( 6000 5) + (

Paper 7 Direct Taxation

Paper 7 Direct Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks: 100

Paper 7 Direct Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks: 100

Compiled Summary of Income Tax Provisions

Income Tax Page: 1 Compiled Summary of Income Tax Provisions CONTENTS S.No. Chapter Name Page No 1 Residential Status and Scope of Total Income 02 2 Salaries 08 3 Income from House Property 26 4 Profit

Income Tax Page: 1 Compiled Summary of Income Tax Provisions CONTENTS S.No. Chapter Name Page No 1 Residential Status and Scope of Total Income 02 2 Salaries 08 3 Income from House Property 26 4 Profit

Income from Salaries. 4.1 Salary

4 Income from Salaries 4.1 Salary The meaning of the term salary for purposes of income tax is much wider than what is normally understood. Every payment made by an employer to his employee for service

4 Income from Salaries 4.1 Salary The meaning of the term salary for purposes of income tax is much wider than what is normally understood. Every payment made by an employer to his employee for service

Answer_MTP_ Inter _Syllabus 2016_ Dec 2017_Set 2 Paper 7 Direct Taxation

Paper 7 Direct Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks: 100

Paper 7 Direct Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks: 100

MTP_ Intermediate _Syllabus 2012_Dec2016_Set 1 Paper 7- Direct Taxation

Paper 7- Direct Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7- Direct Taxation Full Marks : 100 Time allowed: 3 hours

Paper 7- Direct Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7- Direct Taxation Full Marks : 100 Time allowed: 3 hours

OVER VIEW OF INCOME FROM SALARY M V SHANKARA, CHARTERED ACCOUNTANT PARTNER MADHAVAN & CO MYSORE.

OVER VIEW OF INCOME FROM SALARY BY M V SHANKARA, CHARTERED ACCOUNTANT PARTNER MADHAVAN & CO MYSORE. Income from Salary Sec 15 EMPLOYER & EMPLOYEE RELATION SHOULD EXIST taxable on due basis whether paid

OVER VIEW OF INCOME FROM SALARY BY M V SHANKARA, CHARTERED ACCOUNTANT PARTNER MADHAVAN & CO MYSORE. Income from Salary Sec 15 EMPLOYER & EMPLOYEE RELATION SHOULD EXIST taxable on due basis whether paid

INCOME UNDER THE HEAD SALARY

Get More Updates From Caultimates.com Join with us : http://facebook.com/groups/caultimates Income Under The Head Salary 255 INCOME UNDER THE HEAD SALARY Salary The meaning of the term salary for purposes

Get More Updates From Caultimates.com Join with us : http://facebook.com/groups/caultimates Income Under The Head Salary 255 INCOME UNDER THE HEAD SALARY Salary The meaning of the term salary for purposes

SAMVIT ACADEMY IPCC MOCK EXAM

Disclaimer (Read carefully) SUGGESTED ANSWERS - Group 1 Taxation (Code GST) The answers given below are prepared by the faculty of Samvit Academy as per their views and experience. The working notes, notes

Disclaimer (Read carefully) SUGGESTED ANSWERS - Group 1 Taxation (Code GST) The answers given below are prepared by the faculty of Samvit Academy as per their views and experience. The working notes, notes

Subject: (305 FIN) Direct Taxation

Direct Taxation") Subject: (305 FIN) Direct Taxation 1. Explain the following terms under the Income Tax Act, 1961. a) Assessment Year. b) Person. c) Assessee. d) Previous year e) Gross Total Income f) Agriculture Income

Subject: (305 FIN) Direct Taxation 1. Explain the following terms under the Income Tax Act, 1961. a) Assessment Year. b) Person. c) Assessee. d) Previous year e) Gross Total Income f) Agriculture Income

IPCC Gr. I (Solution of November ) Paper - 4 : Taxation

Paper - 4 : Taxation") Solved Scanner Appendix IPCC Gr. I (Solution of November - 2015) Paper - 4 : Taxation Chapter - 2 : Basic Concepts 2015 - Nov [2] (a) An Indian Citizen who comes on a visit to India during PY shall be

Solved Scanner Appendix IPCC Gr. I (Solution of November - 2015) Paper - 4 : Taxation Chapter - 2 : Basic Concepts 2015 - Nov [2] (a) An Indian Citizen who comes on a visit to India during PY shall be

INTER CA NOVEMBER 2018

Answer 1 INTER CA NOVEMBER 2018 Sub: DIRECT TAXATION Topics Introduction, Residence of an assessee, Income from salaries, Income from House Property. Test Code N12 Branch: Multiple Date: (50 Marks) Computation

Answer 1 INTER CA NOVEMBER 2018 Sub: DIRECT TAXATION Topics Introduction, Residence of an assessee, Income from salaries, Income from House Property. Test Code N12 Branch: Multiple Date: (50 Marks) Computation

Income-tax and Death are the only two inevitable things in life In India, taxes were levied even in ancient times refer to Manu Smriti & Arthashastra

Income-tax and Death are the only two inevitable things in life In India, taxes were levied even in ancient times refer to Manu Smriti & Arthashastra Why to Pay Tax? It was only for the good of his subjects

Income-tax and Death are the only two inevitable things in life In India, taxes were levied even in ancient times refer to Manu Smriti & Arthashastra Why to Pay Tax? It was only for the good of his subjects

Salary Mock Test 3 IGP-CS CA Vivek Gaba

1. Rashi is entitled to get a pension of ` 600 per month from a private company. She gets 3/5 th of the pension commuted and received ` 36,000. She did not receive gratuity. The taxable value of commuted

1. Rashi is entitled to get a pension of ` 600 per month from a private company. She gets 3/5 th of the pension commuted and received ` 36,000. She did not receive gratuity. The taxable value of commuted

SYLLABUS. B.Com II Year (Tax) Subject Income Tax Procedure and Practice

Subject Income Tax Procedure and Practice") SYLLABUS B.Com II Year (Tax) Subject Income Tax Procedure and Practice UNIT-I An outline of provisions and rules of various heads of income. Set off and carry forward of Losses. Clubbing of income. Practical

SYLLABUS B.Com II Year (Tax) Subject Income Tax Procedure and Practice UNIT-I An outline of provisions and rules of various heads of income. Set off and carry forward of Losses. Clubbing of income. Practical

MTP_ Inter _Syllabus 2016_ June 2018_Set 2 Paper 7 Direct Taxation (DTX)

") Paper 7 Direct Taxation (DTX) Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks:

Paper 7 Direct Taxation (DTX) Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks:

D.K.M.COLLEGE FOR WOMEN (AUTONOMOUS),VELLORE-1. INCOME TAX LAW AND PRACTICE-1

,VELLORE-1. INCOME TAX LAW AND PRACTICE-1") D.K.M.COLLEGE FOR WOMEN (AUTONOMOUS),VELLORE-1. INCOME TAX LAW AND PRACTICE-1 SECTION-A 6 MARKS 1. What is Income tax? 2. What is Assessment Year? 3. Define previous year? 4. Define Person? 5. What is

D.K.M.COLLEGE FOR WOMEN (AUTONOMOUS),VELLORE-1. INCOME TAX LAW AND PRACTICE-1 SECTION-A 6 MARKS 1. What is Income tax? 2. What is Assessment Year? 3. Define previous year? 4. Define Person? 5. What is

INCOME UNDER THE HEAD PROFITS AND GAINS FROM BUSINESS AND PROFESSION AND IT S COMPUTATION

INCOME UNDER THE HEAD PROFITS AND GAINS FROM BUSINESS AND PROFESSION AND IT S COMPUTATION 1. NATURE OF INCOME :- Such Income Includes income from: - Business, Vocation and Profession carried on by the

INCOME UNDER THE HEAD PROFITS AND GAINS FROM BUSINESS AND PROFESSION AND IT S COMPUTATION 1. NATURE OF INCOME :- Such Income Includes income from: - Business, Vocation and Profession carried on by the

SURENDER KR. SINGHAL & CO

PROPOSED TAX RATES FOR FINANCIAL YEAR 2016-17 A. Y. 2017-18 Income Tax Rates for Individuals, HUF Individuals, Hindu Undivided Families (HUF) and Artificial Jurisdictional Person: Net Income Range Income

PROPOSED TAX RATES FOR FINANCIAL YEAR 2016-17 A. Y. 2017-18 Income Tax Rates for Individuals, HUF Individuals, Hindu Undivided Families (HUF) and Artificial Jurisdictional Person: Net Income Range Income

There is no Such Thing as a Good Tax (Winston Churchill)

") There is no Such Thing as a Good Tax (Winston Churchill) Tax structure refers to the systematic arrangement of various taxes and the factors influencing them such as tax base, tax rate, frequency of change

There is no Such Thing as a Good Tax (Winston Churchill) Tax structure refers to the systematic arrangement of various taxes and the factors influencing them such as tax base, tax rate, frequency of change

Intermediate Group I Paper 7 : DIRECT TAXATION (SYLLABUS 2016)

") Intermediate Group I Paper 7 : DIRECT TAXATION (SYLLABUS 2016) Objectives 1. (a) Multiple Choice Questions: 1. When the shares are held in unlisted company, it is trusted as long term capital assets when

Intermediate Group I Paper 7 : DIRECT TAXATION (SYLLABUS 2016) Objectives 1. (a) Multiple Choice Questions: 1. When the shares are held in unlisted company, it is trusted as long term capital assets when

Basics of Income Tax

CHAPTER : Basics of Income Tax CONCEPT 1: Short Title, Extent and Commencement [Section 1] a) Short title : Income Tax Act 1961 b) Extent : Whole of India c) Commencement : 1 st April, 1962 CONCEPT 2:

CHAPTER : Basics of Income Tax CONCEPT 1: Short Title, Extent and Commencement [Section 1] a) Short title : Income Tax Act 1961 b) Extent : Whole of India c) Commencement : 1 st April, 1962 CONCEPT 2:

Answer_MTP_ Inter _Syllabus 2016_ June 2018_Set 2 Paper 7 Direct Taxation (DTX)

") Paper 7 Direct Taxation (DTX) Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks:

Paper 7 Direct Taxation (DTX) Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks:

NEW HORIZON COLLEGE MARATHALLI, BANGALORE VI SEMESTER BBA STUDY MATERIAL INCOME TAX ASSESSMENT YEAR Prepared by

NEW HORIZON COLLEGE MARATHALLI, BANGALORE VI SEMESTER BBA STUDY MATERIAL INCOME TAX ASSESSMENT YEAR 2016-2017 Prepared by MS. PRASANNA PRAKASH MS. SAYANTANI BANERJEE Introduction UNIT-1, 2 The income tax

NEW HORIZON COLLEGE MARATHALLI, BANGALORE VI SEMESTER BBA STUDY MATERIAL INCOME TAX ASSESSMENT YEAR 2016-2017 Prepared by MS. PRASANNA PRAKASH MS. SAYANTANI BANERJEE Introduction UNIT-1, 2 The income tax

PERSONAL TAX PLANNING & TAX SAVING SCHEMES

PERSONAL TAX PLANNING & TAX SAVING SCHEMES TAX PLANNING IS A VERY PROBLEM STAKING ISSUE FOR AN EMPLOYEE. AS A PERSON DRAWS SALARY,HE IS ALLOWED TAX EXPEMTIONS UPTO CERTAIN LIMIT. AFTER THAT HIS SALARY

PERSONAL TAX PLANNING & TAX SAVING SCHEMES TAX PLANNING IS A VERY PROBLEM STAKING ISSUE FOR AN EMPLOYEE. AS A PERSON DRAWS SALARY,HE IS ALLOWED TAX EXPEMTIONS UPTO CERTAIN LIMIT. AFTER THAT HIS SALARY

Answer to MTP_Intermediate_Syllabus2016_Dec2018_Set1 Paper 7- Direct Taxation

Paper 7- Direct Taxation Dos, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7- Direct Taxation Full Marks : 100 Time allowed: 3 hours Answer Question

Paper 7- Direct Taxation Dos, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7- Direct Taxation Full Marks : 100 Time allowed: 3 hours Answer Question

Visiting Faculty to N.L. Dalmia Institute of Management A.Y TAXATION

TAXATION Tax: It is the amount levied by the government on income earned by a person. Rate of Tax: Rate of tax comes from the finance bill every year which is presented in the parliament. Finance Act 2010:

TAXATION Tax: It is the amount levied by the government on income earned by a person. Rate of Tax: Rate of tax comes from the finance bill every year which is presented in the parliament. Finance Act 2010:

6. PROFITS AND GAINS OF BUSINESS OR PROFESSION 2

Ph: 98851 25025/26 www.mastermindsindia.com 6. PROFITS AND GAINS OF BUSINESS OR PROFESSION 2 SOLUTIONS TO ASSIGNMENT PROBLEMS Problem No. 1 Computing business income for A.Y.2015-16 is as follows Amount

Ph: 98851 25025/26 www.mastermindsindia.com 6. PROFITS AND GAINS OF BUSINESS OR PROFESSION 2 SOLUTIONS TO ASSIGNMENT PROBLEMS Problem No. 1 Computing business income for A.Y.2015-16 is as follows Amount

Paper-7 Direct Taxation

Paper-7 Direct Taxation Time Allowed: 3 hours Full Marks: 100 All the questions relate to the assessment year 2014-15, unless stated otherwise. Working notes should form part of the answers. Section A

Paper-7 Direct Taxation Time Allowed: 3 hours Full Marks: 100 All the questions relate to the assessment year 2014-15, unless stated otherwise. Working notes should form part of the answers. Section A

Suggested Answer_Syl2008_June2015_Paper_7 INTERMEDIATE EXAMINATION GROUP I (SYLLABUS 2008)

") INTERMEDIATE EXAMINATION GROUP I (SYLLABUS 2008) SUGGESTED ANSWERS TO QUESTIONS JUNE 2015 Paper-7: APPLIED DIRECT TAXATION Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the right

INTERMEDIATE EXAMINATION GROUP I (SYLLABUS 2008) SUGGESTED ANSWERS TO QUESTIONS JUNE 2015 Paper-7: APPLIED DIRECT TAXATION Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the right

PGBP Mock Test IGP-CS CA Vivek Gaba

1. A Company purchased plant and machinery for Rs. 2 Crores for a specified business and claimed deduction under section 35AD. However the very next year the machinery purchased put to use for unspecified

1. A Company purchased plant and machinery for Rs. 2 Crores for a specified business and claimed deduction under section 35AD. However the very next year the machinery purchased put to use for unspecified

INCOME TAX TEST 3 SOLUTIONS

Question 1 Computation of Total Income of Mr. Suraj Particulars Rs. Rs. Income from House Property (WN-1) Profits and gains from business or profession (WN-2) Capital gains -Short term capital loss (WN-3)

Question 1 Computation of Total Income of Mr. Suraj Particulars Rs. Rs. Income from House Property (WN-1) Profits and gains from business or profession (WN-2) Capital gains -Short term capital loss (WN-3)

Class B.Com. I Year (Taxation)

") SYLLABUS Class B.Com. I Year (Taxation) Subject Direct Tax System Income Tax (Specialization-02) UNIT I UNIT II UNIT III UNIT IV UNIT V Tax System Meaning Tax, Features and Objects Direct Taxes in India

SYLLABUS Class B.Com. I Year (Taxation) Subject Direct Tax System Income Tax (Specialization-02) UNIT I UNIT II UNIT III UNIT IV UNIT V Tax System Meaning Tax, Features and Objects Direct Taxes in India

Name of the Employee Dr./Mr./Sh./Smt. Designation. PAN No. (attach copy of PAN card), Date of Birth (for Scientist staff only)

, Date of Birth (for Scientist staff only)") ICAR - INDIAN INSTITUTE OF SOIL SCIENCE : BHOPAL Final Income Tax Statement of Income U/s 192(2B) of the Income Tax Act 1961 Year ending 31.3.2019 Financial Year 2018-19 Assessment Year 2019-20 Name of

ICAR - INDIAN INSTITUTE OF SOIL SCIENCE : BHOPAL Final Income Tax Statement of Income U/s 192(2B) of the Income Tax Act 1961 Year ending 31.3.2019 Financial Year 2018-19 Assessment Year 2019-20 Name of

MTP_ Inter _Syllabus 2016_ June 2018_Set 1 Paper 7 Direct Taxation (DTX)

") Paper 7 Direct Taxation (DTX) Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks:

Paper 7 Direct Taxation (DTX) Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks:

INTERMEDIATE EXAMINATION GROUP - I (SYLLABUS 2016)

") INTERMEDIATE EXAMINATION GROUP - I (SYLLABUS 2016) SUGGESTED ANSWERS TO QUESTIONS DECEMBER - 2017 Paper - 7 : DIRECT TAXATION Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the right

INTERMEDIATE EXAMINATION GROUP - I (SYLLABUS 2016) SUGGESTED ANSWERS TO QUESTIONS DECEMBER - 2017 Paper - 7 : DIRECT TAXATION Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the right

Shree Guru Kripa s Institute of Management

Reg. No.. TAXATION Total Number of Printed Pages: 6 Date: 24.09.2015 Time Allowed: 3Hrs Maximum Marks: 100 Question 1 is compulsory (4 5 = 20 Marks). Answer any 5 from the remaining 6 (16 5 = 80 Marks)

Reg. No.. TAXATION Total Number of Printed Pages: 6 Date: 24.09.2015 Time Allowed: 3Hrs Maximum Marks: 100 Question 1 is compulsory (4 5 = 20 Marks). Answer any 5 from the remaining 6 (16 5 = 80 Marks)

2.f List of benefits available to Small Businessmen [AY ] S.N. Particulars Section Benefits/Deductions allowed

![2.f List of benefits available to Small Businessmen [AY ] S.N. Particulars Section Benefits/Deductions allowed](/thumbs/84/90875315.jpg "2.f List of benefits available to Small Businessmen [AY ] S.N. Particulars Section Benefits/Deductions allowed") 2.f List of benefits available to Small Businessmen [AY 2017 18] S.N. Particulars Section Benefits/Deductions allowed A. Presumptive Taxation Scheme 1. Computation of income from eligible business on presumptive

2.f List of benefits available to Small Businessmen [AY 2017 18] S.N. Particulars Section Benefits/Deductions allowed A. Presumptive Taxation Scheme 1. Computation of income from eligible business on presumptive

(ALL BATCHES) DATE: MAXIMUM MARKS: 100 TIMING: 3¼Hours. PAPER 2 : Taxation

DATE: MAXIMUM MARKS: 100 TIMING: 3¼Hours. PAPER 2 : Taxation") (ALL BATCHES) DATE: 02.08.2018 MAXIMUM MARKS: 100 TIMING: 3¼Hours PAPER 2 : Taxation SECTION - A Answer:1 (a) Computation of total income and tax liability of Dr. Niranjana for A.Y. 2018-19 I Income from

(ALL BATCHES) DATE: 02.08.2018 MAXIMUM MARKS: 100 TIMING: 3¼Hours PAPER 2 : Taxation SECTION - A Answer:1 (a) Computation of total income and tax liability of Dr. Niranjana for A.Y. 2018-19 I Income from

P7_Practice Test Paper_Syl12_Dec13_Set 1

Direct Taxation Section A (Question No. 1 is compulsory and any four from Question No. 2 to 6] 1. (a) Answer each of the following questions: (i) T Ltd. purchased a plant costing `10 lakhs. Before commencement

Direct Taxation Section A (Question No. 1 is compulsory and any four from Question No. 2 to 6] 1. (a) Answer each of the following questions: (i) T Ltd. purchased a plant costing `10 lakhs. Before commencement

PONDICHERRY UNIVERSITY STATEMENT OF CALCULATION OF INCOME TAX FOR THE FINANCIAL YEAR

PONDICHERRY UNIVERSITY STATEMENT OF CALCULATION OF INCOME TAX FOR THE FINANCIAL YEAR 2014-15 (Please carefully read the instruction/note attached herewith before filling up this statement) PART A (Refer

PONDICHERRY UNIVERSITY STATEMENT OF CALCULATION OF INCOME TAX FOR THE FINANCIAL YEAR 2014-15 (Please carefully read the instruction/note attached herewith before filling up this statement) PART A (Refer

(A1) First Name (A2) Middle Name (A3) Last Name (A4) Permanent Account Number

First Name (A2) Middle Name (A3) Last Name (A4) Permanent Account Number") 238 THE GAZETTE OF INDIA : EXTRAORDINARY [PART II SEC. 3(i)] FORM ITR-4 SUGAM INDIAN INCOME TAX RETURN FOR PRESUMPTIVE INCOME FROM BUSINESS & PROFESSION (Please see Rule 12 of the Income-tax Rules, 1962)

238 THE GAZETTE OF INDIA : EXTRAORDINARY [PART II SEC. 3(i)] FORM ITR-4 SUGAM INDIAN INCOME TAX RETURN FOR PRESUMPTIVE INCOME FROM BUSINESS & PROFESSION (Please see Rule 12 of the Income-tax Rules, 1962)

: 3 : 100 : 8 : 8 NOTE

2/2012/TL 263 Roll No Time allowed : 3 hours : 1 : Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 8 NOTE : All references to sections mentioned in Part-A of the Question

2/2012/TL 263 Roll No Time allowed : 3 hours : 1 : Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 8 NOTE : All references to sections mentioned in Part-A of the Question

INCOME TAX INVESTMENT PROOF SUBMISSION GUIDELINES: Financial Year

Introduction We are pleased to share the Income tax related guidelines with you. Mentioned at the end are also draft formats for rent related declarations, should you need those. Please feel free to share

Introduction We are pleased to share the Income tax related guidelines with you. Mentioned at the end are also draft formats for rent related declarations, should you need those. Please feel free to share

SECTION 192 & 194H OF INCOME TAX ACT, 1961

SECTION 192 & 194H OF INCOME TAX ACT, 1961 SONALEE GODBOLE KALYANIWALLA & MISTRY 1 KALYANIWALLA & MISTRY 2 Definition of Salary under section 17 is inclusive - Salary interalia includes wages, annuity

SECTION 192 & 194H OF INCOME TAX ACT, 1961 SONALEE GODBOLE KALYANIWALLA & MISTRY 1 KALYANIWALLA & MISTRY 2 Definition of Salary under section 17 is inclusive - Salary interalia includes wages, annuity

Make your Dream an Aim. Don't make your Aim a Dream. CA Gaurav Rajaram By CA Gaurav Rajaram. P a g e 1

Make your Dream an Aim. Don't make your Aim a Dream CA Gaurav Rajaram 9535145650 By CA Gaurav Rajaram P a g e 1 P a g e 2 " You are born free and then taxed to death " P a g e 3 P a g e 4 Dear Samvitian,

Make your Dream an Aim. Don't make your Aim a Dream CA Gaurav Rajaram 9535145650 By CA Gaurav Rajaram P a g e 1 P a g e 2 " You are born free and then taxed to death " P a g e 3 P a g e 4 Dear Samvitian,

Bombay Chartered Accountants Society

Bombay Chartered Accountants Society Filing of Income Tax Returns for the Assessment Year -09 09 by C.A. Contractor, Nayak & Kishnadwala Return of Income What is Return of Income? Return of Income now

Bombay Chartered Accountants Society Filing of Income Tax Returns for the Assessment Year -09 09 by C.A. Contractor, Nayak & Kishnadwala Return of Income What is Return of Income? Return of Income now

Chapter 8 : Income from Other Sources (Section 56 to 59) Advance Direct Tax and Service Tax [Sub code : 441]

![Chapter 8 : Income from Other Sources (Section 56 to 59) Advance Direct Tax and Service Tax [Sub code : 441]](/thumbs/74/70016057.jpg "Chapter 8 : Income from Other Sources (Section 56 to 59) Advance Direct Tax and Service Tax [Sub code : 441]") Chapter 8 : Income from Other Sources (Section 56 to 59) Advance Direct Tax and Service Tax [Sub code : 441] Learning Objectives Income from Other Sources Deductions from Income from other Sources Conditions

Chapter 8 : Income from Other Sources (Section 56 to 59) Advance Direct Tax and Service Tax [Sub code : 441] Learning Objectives Income from Other Sources Deductions from Income from other Sources Conditions

2 (a) Municipal taxes paid by Mr. Hari `4,200 per annum (b) House insurance `1,000 (iii) He earned `1,00,000 in share speculation business and lost `1

Municipal taxes paid by Mr. Hari `4,200 per annum (b) House insurance `1,000 (iii) He earned `1,00,000 in share speculation business and lost `1") NEW COURSE INCOME TAX PAPER SECTION-A Marks: 60 Question No. 1 is compulsory. Candidates are also required to answer any Five questions from the remaining Six questions. In case, any candidate answers

NEW COURSE INCOME TAX PAPER SECTION-A Marks: 60 Question No. 1 is compulsory. Candidates are also required to answer any Five questions from the remaining Six questions. In case, any candidate answers

BATCH : GI 1 to GI 5

(0.5 6=3M) MITTAL COMMERCE CLASSES BATCH : GI 1 to GI 5 DATE: 18.08.2017 MAXIMUM MARKS: 100 TIMING: 3 Hours PAPER 4 : TAXATION Question No. 1 is Compulsory Answer any five questions from the remaining

(0.5 6=3M) MITTAL COMMERCE CLASSES BATCH : GI 1 to GI 5 DATE: 18.08.2017 MAXIMUM MARKS: 100 TIMING: 3 Hours PAPER 4 : TAXATION Question No. 1 is Compulsory Answer any five questions from the remaining

Chapter 1 : Income Tax Concept and Computation of Income Tax

Chapter 1 : Income Tax Concept and Computation of Income Tax This Chapter includes : I. Taxation in India 1. Taxes and its levying authority 2. Tax Structure 3. Hierarchy of Taxes levied and collected

Chapter 1 : Income Tax Concept and Computation of Income Tax This Chapter includes : I. Taxation in India 1. Taxes and its levying authority 2. Tax Structure 3. Hierarchy of Taxes levied and collected

Suggested Answer_Syl2008_Jun2014_Paper_7 INTERMEDIATE EXAMINATION GROUP I (SYLLABUS 2008)

") INTERMEDIATE EXAMINATION GROUP I (SYLLABUS 2008) SUGGESTED ANSWERS TO QUESTIONS JUNE 2014 Paper-7: APPLIED DIRECT TAXATION Time Allowed : 3 Hours Full Marks : 100 Wherever required, the candidate may make

INTERMEDIATE EXAMINATION GROUP I (SYLLABUS 2008) SUGGESTED ANSWERS TO QUESTIONS JUNE 2014 Paper-7: APPLIED DIRECT TAXATION Time Allowed : 3 Hours Full Marks : 100 Wherever required, the candidate may make

Tax Laws 263 NOTE : PART A 263/1

Tax Laws 1/2012/TL 263 Roll No Time allowed : 3 hours : 1 : Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 8 NOTE : All references to sections mentioned in Part-A of

Tax Laws 1/2012/TL 263 Roll No Time allowed : 3 hours : 1 : Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 8 NOTE : All references to sections mentioned in Part-A of

TRUE TRUE. B Match the following.

Q.1 A State whether True or False (ANY 8) Ans. 1 Unabsorbed Speculative loss can be carried forward upto 8 A.Y. FALSE 2 Loss relating to long term capital asset is to be set off against short term capital

Q.1 A State whether True or False (ANY 8) Ans. 1 Unabsorbed Speculative loss can be carried forward upto 8 A.Y. FALSE 2 Loss relating to long term capital asset is to be set off against short term capital

Answer to MTP_Intermediate_Syllabus2016_Dec2018_Set2 Paper 7- Direct Taxation

Paper 7- Direct Taxation Dos, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7- Direct Taxation Full Marks : 100 Time allowed: 3 hours Answer Question

Paper 7- Direct Taxation Dos, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7- Direct Taxation Full Marks : 100 Time allowed: 3 hours Answer Question

Tax essentials for Individuals

Tax Rates The income tax rates are: Taxable Income for Men Rate Taxable Income for Women Rate Up to Rs. 1,80,000 Nil Up to Rs. 1,90,000 Nil 1,80,001 to 5,00,000 10% 1,90,001 to 5,00,000 10% 5,00,001 to

Tax Rates The income tax rates are: Taxable Income for Men Rate Taxable Income for Women Rate Up to Rs. 1,80,000 Nil Up to Rs. 1,90,000 Nil 1,80,001 to 5,00,000 10% 1,90,001 to 5,00,000 10% 5,00,001 to

Circular The Schedule of dates for filing income-tax returns is given below:

Circular-2012 To, July 14, 2012 Dear Sir(s)/Madam, Sub: Income-tax, Wealth-tax, Service-tax and TDS returns for Assessment Year 2012-13 and payment of advance-tax for Assessment Year 2013-14 -------------------------------------------------------

Circular-2012 To, July 14, 2012 Dear Sir(s)/Madam, Sub: Income-tax, Wealth-tax, Service-tax and TDS returns for Assessment Year 2012-13 and payment of advance-tax for Assessment Year 2013-14 -------------------------------------------------------

Solved Scanner. (Solution of December ) CMA Inter Group - I (Syllabus-2012) Paper - 7 : Direct Taxation

CMA Inter Group - I (Syllabus-2012) Paper - 7 : Direct Taxation") Solved Scanner (Solution of December - 2016) CMA Inter Group - I (Syllabus-2012) Paper - 7 : Direct Taxation [Chapter - 21] Objective Questions 1. (a), (b), (c) (5 marks each) (a) (i) ` 10,000 (ii) ` 5,00,000

Solved Scanner (Solution of December - 2016) CMA Inter Group - I (Syllabus-2012) Paper - 7 : Direct Taxation [Chapter - 21] Objective Questions 1. (a), (b), (c) (5 marks each) (a) (i) ` 10,000 (ii) ` 5,00,000

DEDUCTION, COLLECTION AND RECOVERY OF TAX

DEDUCTION, COLLECTION AND RECOVERY OF TAX Section Particulars 190 different modes of payment of tax: tds, tcs, advance tax, tax u/s 192(1A) 191 failure to deduct tax, and direct payment of tax 192 tds

DEDUCTION, COLLECTION AND RECOVERY OF TAX Section Particulars 190 different modes of payment of tax: tds, tcs, advance tax, tax u/s 192(1A) 191 failure to deduct tax, and direct payment of tax 192 tds

Budget 2017 Synopsis Part II Analysis of Rupiya

Budget 2017 Synopsis Part II Analysis of Rupiya Facts & Findings: Out of 125 crore Indians only 15% ie 19 crore pay income tax % of Taxpayers (Out of 19 Crore) % Contribution To Tax Revenue 01% 26% 1%

Budget 2017 Synopsis Part II Analysis of Rupiya Facts & Findings: Out of 125 crore Indians only 15% ie 19 crore pay income tax % of Taxpayers (Out of 19 Crore) % Contribution To Tax Revenue 01% 26% 1%

PRACTICE QUESTIONS ON INCOME FROM HOUSE PROPERTY

PRACTICE QUESTIONS ON INCOME FROM HOUSE PROPERTY S No Question 1 Under what circumstances will the lessee of a property will be deemed to be the owner of the property. (a) If he acquires the property under

PRACTICE QUESTIONS ON INCOME FROM HOUSE PROPERTY S No Question 1 Under what circumstances will the lessee of a property will be deemed to be the owner of the property. (a) If he acquires the property under

BUDGET 2016 SONALEE GODBOLE

1 BUDGET 2016 SONALEE GODBOLE Penalties 2 3 Section 270A Section 271 levying penalty for failure to furnish returns, comply with notices, concealment of income, etc. will be applicable upto A.Y. 2016-17.

1 BUDGET 2016 SONALEE GODBOLE Penalties 2 3 Section 270A Section 271 levying penalty for failure to furnish returns, comply with notices, concealment of income, etc. will be applicable upto A.Y. 2016-17.

Join our WhatsApp Groups at https://cashines.wordpress.com

Join our WhatsApp Groups at https://cashines.wordpress.com 7 Deductions from Gross Total Income Key Points Deductions in respect of payments Section Eligible Assessee Eligible Payments 80C Contribution

Join our WhatsApp Groups at https://cashines.wordpress.com 7 Deductions from Gross Total Income Key Points Deductions in respect of payments Section Eligible Assessee Eligible Payments 80C Contribution

Solved Scanner. (Solution of May ) IPCC Gr. I. Paper - 4 : Taxation

IPCC Gr. I. Paper - 4 : Taxation") ISBN: 978-93-5159-435-2 Solved Scanner (Solution of May - 2017) IPCC Gr. I Paper - 4 : Taxation [Chapter - 12] Computation of Total Income, Tax Payable, Rebate and Relief 1. (a) (10 marks) Computation

ISBN: 978-93-5159-435-2 Solved Scanner (Solution of May - 2017) IPCC Gr. I Paper - 4 : Taxation [Chapter - 12] Computation of Total Income, Tax Payable, Rebate and Relief 1. (a) (10 marks) Computation

SYLLABUS. B.Com V SEM (Tax) Subject Income Tax Law And Practice

Subject Income Tax Law And Practice") SYLLABUS B.Com V SEM (Tax) Subject Income Tax Law And Practice UNIT-I Unit-II Unit-III Unit-IV Unit-V General introduction of Indian income tax act, 1961. Basic concepts: income, agriculture income, casual

SYLLABUS B.Com V SEM (Tax) Subject Income Tax Law And Practice UNIT-I Unit-II Unit-III Unit-IV Unit-V General introduction of Indian income tax act, 1961. Basic concepts: income, agriculture income, casual

LOYOLA COLLEGE (AUTONOMOUS), CHENNAI

, CHENNAI") LOYOLA COLLEGE (AUTONOMOUS), CHENNAI 600 034 M.Com.DEGREE EXAMINATION COMMERCE SECOND SEMESTER APRIL 2018 17PCO2MC01 DIRECT TAX PLANNING AND MANAGEMENT Date: 17042018 Dept. No. Max. : 100 Marks Time: 01:0004:00

LOYOLA COLLEGE (AUTONOMOUS), CHENNAI 600 034 M.Com.DEGREE EXAMINATION COMMERCE SECOND SEMESTER APRIL 2018 17PCO2MC01 DIRECT TAX PLANNING AND MANAGEMENT Date: 17042018 Dept. No. Max. : 100 Marks Time: 01:0004:00

MOCK TEST SOLUTION A.Y Total No. of Question 7] [Total No. of Printed Pages 20 Time Allowed 3 Hours Maximum Marks 100 MKG

![MOCK TEST SOLUTION A.Y Total No. of Question 7] [Total No. of Printed Pages 20 Time Allowed 3 Hours Maximum Marks 100 MKG](/thumbs/73/68647623.jpg "MOCK TEST SOLUTION A.Y Total No. of Question 7] [Total No. of Printed Pages 20 Time Allowed 3 Hours Maximum Marks 100 MKG") MOCK TEST SOLUTION IPC (Intermediate) (Computation of Total Income And Tax Liability, Taxability of Gift, Advance Payment of Tax, Residential Status & Scope of Total Income, House Property, Agricultural

MOCK TEST SOLUTION IPC (Intermediate) (Computation of Total Income And Tax Liability, Taxability of Gift, Advance Payment of Tax, Residential Status & Scope of Total Income, House Property, Agricultural

BOMBAY CHARTERED ACCOUNTANTS SOCIETY PANEL DISCUSSION ON CASE STUDIES ON SALARIES AND PERQUISITES - SECTION 192

BOMBAY CHARTERED ACCOUNTANTS SOCIETY PANEL DISCUSSION ON CASE STUDIES ON SALARIES AND PERQUISITES - SECTION 192 Panelists Mr. Milin Mehta (MM) & Mr. Nikhil Bhatia (NB) Case Study 1 (MM) Mr. X is the CEO

BOMBAY CHARTERED ACCOUNTANTS SOCIETY PANEL DISCUSSION ON CASE STUDIES ON SALARIES AND PERQUISITES - SECTION 192 Panelists Mr. Milin Mehta (MM) & Mr. Nikhil Bhatia (NB) Case Study 1 (MM) Mr. X is the CEO

Paper 4 Income Tax (Old Course)

") Paper 4 Income Tax (Old Course) 1. Mr. Karan filed his return of income for A.Y.2019-20 showing total income of Rs.7 lakhs on 1.1.2020. The fee payable by him under section 234F is Nil Rs.1,000 Rs.5,000

Paper 4 Income Tax (Old Course) 1. Mr. Karan filed his return of income for A.Y.2019-20 showing total income of Rs.7 lakhs on 1.1.2020. The fee payable by him under section 234F is Nil Rs.1,000 Rs.5,000

Tax Laws. Time allowed : 3 hours Maximum marks : 100. Total number of questions : 8 Total number of printed pages : 8

Tax Laws 263 : 1 : Roll No... Time allowed : 3 hours Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 8 NOTE : All references to sections mentioned in Part-A of the Question

Tax Laws 263 : 1 : Roll No... Time allowed : 3 hours Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 8 NOTE : All references to sections mentioned in Part-A of the Question

CONTENTS CONTENTS BOOK ONE : DEDUCTION OF TAX AT SOURCE DEDUCTION OF TAX AT SOURCE FROM SALARY

CONTENTS Chapter-heads I-7 BOOK ONE : DEDUCTION OF TAX AT SOURCE 1 DEDUCTION OF TAX AT SOURCE FROM SALARY 1.1 Who is responsible to deduct tax at source in case of income from salary 4 1.1-1 Where salary

CONTENTS Chapter-heads I-7 BOOK ONE : DEDUCTION OF TAX AT SOURCE 1 DEDUCTION OF TAX AT SOURCE FROM SALARY 1.1 Who is responsible to deduct tax at source in case of income from salary 4 1.1-1 Where salary

Assessment Year

Assessment Year 2016-2017 Income Income Income Income Income From Salaries from Capital Gains from Business and Profession from House Property from Other Sources Individual/HUF Firm Company Trust AOP/BOI/Co-op

Assessment Year 2016-2017 Income Income Income Income Income From Salaries from Capital Gains from Business and Profession from House Property from Other Sources Individual/HUF Firm Company Trust AOP/BOI/Co-op

Unit 11: COMPUTATION OF TAX

Unit 11: COMPUTATION OF TAX HOW TO COMPUTE TAX PAYABLE Once the net taxable income is computed, the next step is to compute the final tax payable. The final tax payable is computed as follows: (1) Taxable

Unit 11: COMPUTATION OF TAX HOW TO COMPUTE TAX PAYABLE Once the net taxable income is computed, the next step is to compute the final tax payable. The final tax payable is computed as follows: (1) Taxable

DIRECT TAX. E TAXATION August Salary Under Section 17(1) does not includes : A. Wages B. Pension C. Interest D.

does not includes : A. Wages B. Pension C. Interest D.") 1 DIRECT TAX 1 Salary Under Section 17(1) does not includes : A. Wages B. Pension C. Interest D. Gratuity 2 Taxable Allowance from Salary : A. Conveyance allowance B. Dearness Allowances C. Children education

1 DIRECT TAX 1 Salary Under Section 17(1) does not includes : A. Wages B. Pension C. Interest D. Gratuity 2 Taxable Allowance from Salary : A. Conveyance allowance B. Dearness Allowances C. Children education

Handbook on Tax Planning Tools for F.Y

Handbook on Tax Planning Tools for F.Y. 2017-18 TaxIndiaUpdates.In [A Blog on Service Tax, Central Excise, GST, Income Tax and Personal Finance] Write us at info@taxindiaupdates.in Connect with us - **

Handbook on Tax Planning Tools for F.Y. 2017-18 TaxIndiaUpdates.In [A Blog on Service Tax, Central Excise, GST, Income Tax and Personal Finance] Write us at info@taxindiaupdates.in Connect with us - **

1. Basic concepts of Income Tax

Quick review of the chapter: Sections Particulars Sec. 2(7) Assessee Sec. 2(9) Assessment year Sec. 2(24) Income Sec. 2 (31) Person Sec. 2(34) & 3 "Previous Year" defined Sec. 80B(5) Gross total income

Quick review of the chapter: Sections Particulars Sec. 2(7) Assessee Sec. 2(9) Assessment year Sec. 2(24) Income Sec. 2 (31) Person Sec. 2(34) & 3 "Previous Year" defined Sec. 80B(5) Gross total income

INCOME-TAX AND BASED ON FINANCE ACT, FINANCE ACT, 2007 WITH NOTES 49 I.T. NOTES 69 I.T. NOTES 97 I.T. NOTES I.T. NOTES 139 I.T.

EHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR VG.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA

EHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR VG.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA

A BUDGET FOR A Y From the desk of - B.L. Tulsian Advocate. R. Tulsian & Co LLP Chartered Accountants.

A BUDGET A N A L Y S I S FOR A Y 2020-21 From the desk of - B.L. Tulsian Advocate R. Tulsian & Co LLP Chartered Accountants www.rtulsian.com Page2 Contents Amendment of Section 16... 3 Amendment to Section

A BUDGET A N A L Y S I S FOR A Y 2020-21 From the desk of - B.L. Tulsian Advocate R. Tulsian & Co LLP Chartered Accountants www.rtulsian.com Page2 Contents Amendment of Section 16... 3 Amendment to Section

Class B.Com. V Sem. (Hons.)

") SYLLABUS Class B.Com. V Sem. (Hons.) Subject Income Tax Law & Practice Unit-I Unit-II UNIT III UNIT IV UNIT V General introduction of Indian income tax act, 1961. Basic concepts: income, agriculture income,

SYLLABUS Class B.Com. V Sem. (Hons.) Subject Income Tax Law & Practice Unit-I Unit-II UNIT III UNIT IV UNIT V General introduction of Indian income tax act, 1961. Basic concepts: income, agriculture income,

AY Fast Track Quick Revision INCOME TAX.

AY 2016-17 Fast Track Quick Revision INCOME TAX www.cacwacs.com Chapter Sections Revision Time Page Basic Concepts 1 to 4 10 minutes 1 Slab Rate 1 Which finance act is applicable for my exam How to memorise

AY 2016-17 Fast Track Quick Revision INCOME TAX www.cacwacs.com Chapter Sections Revision Time Page Basic Concepts 1 to 4 10 minutes 1 Slab Rate 1 Which finance act is applicable for my exam How to memorise

Dr. BashirAhmad Joo. Human Resource Development Center University of Kashmir. The Business School University Of Kashmir.

Management of Tax Liability for Salaried Individuals Presentation By Dr. BashirAhmad Joo Professor The Business School University Of Kashmir 0n 11 th March, 2017 Human Resource Development Center University

Management of Tax Liability for Salaried Individuals Presentation By Dr. BashirAhmad Joo Professor The Business School University Of Kashmir 0n 11 th March, 2017 Human Resource Development Center University

FAST TRACK. Income Tax. This is Enough TM. CS K.K.Agrawal. Assessment Year

taxbykk.com CS K.K. Agrawal C.1 taxguru.in Fast Track Income Tax FAST TRACK Income Tax with amendments as per Finance Act 2012 This is Enough TM by CS K.K.Agrawal Assessment Year 2013-14 for CA IPCC (IPC)

taxbykk.com CS K.K. Agrawal C.1 taxguru.in Fast Track Income Tax FAST TRACK Income Tax with amendments as per Finance Act 2012 This is Enough TM by CS K.K.Agrawal Assessment Year 2013-14 for CA IPCC (IPC)