DANIEL DUMAS ESCP Europe Business School London, 14 November 2013

|

|

|

- Elwin Barton

- 5 years ago

- Views:

Transcription

1 Taxation of Natural Resources Features, Principles, Issues DANIEL DUMAS ESCP Europe Business School London, 14 November 2013

2 Disclaimer The views expressed in this presentation are those of the author and should not be taken to represent the views of the IMF, its Executive Board, or its Management. 2

3 Objectives of the Presentation To understand the methodologies for economic assessment of E&P projects To understand the investment decision-making mechanisms of private sector investors in E&P: their criteria for choosing to invest in the E & Pofdeposits To understand the concepts of oil profit sharing How to compare tax systems? How to stimulate investment in E&P by means of a progressive tax system with incentives, while also protecting the long-term interests of the country?

4 Few Questions What type of fiscal system? (Royalty/Taxation, PSC or hybrid) What should be the target Global Take What mix of tax instruments should be employed? How much of these instruments should be fixed vs. negotiable? Competitive bidding rounds or not and on what elements (bonus, level of royalties, work program) Contract duration and Commerciality? Should there be any state participation? 4

5 Outline Objectives Why Natural Resources different? Fiscal Regime for Oil & Gas Establishing the fiscal framework Tax instruments Determining the Global Take Progressivity Issues for Government Conclusion 5

6 Three building blocks: Frameworks-Institution-Governance Good Governance Appropriate Institutions Adequate Frameworks & Fiscal Regime 6

7 WHY NATURAL RESOURCES DIFFERENT? 7

8 Why Natural Resources Different? Natural Resources is probably the only economic sector which can, on its own, lift a country out of underdevelopment. If not managed properly Natural Resources have led to social inequity, social unrest, conflict and wars N.R. Revenues: Transformation of wealth - Exhaustibility Dutch-Disease (Resources Curse) Increasing Environmental Concerns (Decommissioning) Demand for fuel and mineral is still growing: Shift in bargaining power Tax revenue is the central benefit to host country Size of sector relative to the economy 8

9 Diverse Experience so far Receipts from Natural Resources, averages (selected countries, percent of government revenues) Mining revenue Petroleum revenue Mining and petroleum revenue 9 Brunei Iraq Equatorial Guinea Libya Saudi Arabia Oman Kuwait Angola Bahrain Congo Republic Nigeria United Arab Emirates Algeria Yemen Timor-Leste Iran Qatar Chad Sudan Azerbaijan Trinidad and Tobago Venezuela Myanmar Botswana Syria Cameroon Kazakhstan Mexico Malaysia Papua New Guinea DRC Indonesia Bolivia Ecuador Russia Vietnam Guinea Norway Mongolia Chile Mauritania Ivory Coast Uzbekistan Colombia Namibia Niger Zambia Kyrgyz Republic Ghana Australia Brazil Sierra Leone United Kingdom Lesotho Canada Philippines Tanzania

10 FISCAL REGIMES FOR OIL & GAS? 10

11 Policy considerations Focus on quantitative comparison of the effects of fiscal regimes Items that are important in policy advice: Pricing and contracts for commodity outputs Ease of tax design, imposition and administration Regulatory and institutional arrangements Modes of granting rights to resources Transparency and accountability in the fiscal system Focus is on a fiscal regime designed for investment by companies.

12 Why distinct fiscal regimes for EI? Substantial rents Pervasive uncertainty Asymmetric information High sunk costs, long production periods Extensive involvement of multinationals in some countries and of State-Owned Enterprises in others Few of these considerations are unique to resources they re just bigger. What is unique is: Exhaustibility: recognize revenues as transformation of finite assets in the ground into other assets 12

13 Prices Volatility 13

14 Central objectives Optimizing Revenue potential Minimize risk (administration & timing) Attractiveness - investor perception of risk & return Stability & Progressivity Public Opinion / local community Other benefits (Employment, Procurement, Infrastructure, Capacity Building)

15 Economic rent P 1 Not viable Viable Production costs/pr rice Rent Project A Project B Project C D E F Cumulative production Prod 2

16 ESTABLISHING THE FISCAL FRAMEWORK 16

17 Legal Framework 17

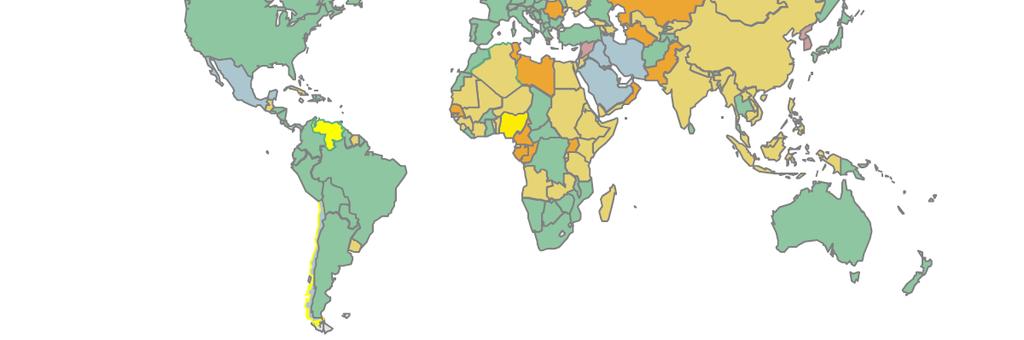

18 Geographic Distribution of regulatory systems 18

19 Fiscal Instruments for Petroleum Bonuses (with bidding) Royalty Corporate income tax Explicit rent taxes State participation Production-Sharing Agreement (PSA) 19

20 Effect of royalty P 1 P 2 Royalty Production costs/pr rice Rent Project A Project B Project C D E F Cumulative production Prod 2

21 Resource rent tax neutral Production costs/p price P 1 Rent tax Rent tax Rent Tax Rent tax Rent Project A Project B Project C D E F Cumulative production Prod 1

22 Benchmarking: Few Facts (1)* Most frequent type of fiscal regime? Broadly, dividing by two types of fiscal regimes that apply throughout the world, (royalty/tax and production sharing) Just over half the regimes (54 percent) are of PSA Other royalty/tax or hybrid. How do corporate income tax rates compare? Corporate income tax on petroleum projects is sometimes imposed at a rate that differs from the generally applicable corporate rate. In 21 percent of the regimes, CIT is more than 40 percent (e.g. Cameroon, India, Trinidad and Tobago (now 50%), and Tunisia). In a third of production sharing regimes, the profit shares are agreed on an after-tax basis. * Mostly based on IHS data and analysis on more than 200 generic petroleum fiscal regimes of E&P ventures (S. Parish) 22

23 Benchmarking: Few Facts (2) What about base royalty? Royalty is an off-the-top take from each unit of production and are very widespread, being found in 71 percent of the regimes. Most royalties and bonuses are usually ad valorem but not based on profit and therefore have a regressive impact on the economics of a petroleum project. Royalty is typically set in the range of 8 percent to 12.5 percent. 16 % of the regimes have royalty that provide the host with 15% or more of the project's gross revenue. many examples where sliding scale royalty with maximum rates reaching %. 23

24 Benchmarking: Few Facts (3) Additional profits taxes? Additional profits taxes are used in a number of regimes to specifically target upstream activities. In the U.K. a supplemental charge was introduced in 2002 was initially set at 10 and increased within four years to 20 percent. Are there mandatory payments such as signature bonuses? Signature bonuses are a requirement in 45 percent of the regimes, a percentage that increases to 57 percent if one looks just at the PSA regimes. 24

25 Benchmarking: Few Facts (4) How common is state participation? Analysis shows 43 percent of the regimes provide the state with the option to participate directly in upstream projects. Few of the regimes with direct state participation provide for the state to contribute its share of exploration and appraisal (E&A) costs at the time of expenditure (i.e., participate as a working interest partner from day one of a project). What about tax holidays? Practice from the past: 20 years ago tax holidays were more frequents, especially in the mining sector. This approach has led to what is now commonly refer to the raise to the bottom, Such incentives are still present in a few jurisdiction and often for very short period (one year in Vietnam) 25

26 The consequence of commercial / fiscal structure Tax and royalty, production sharing, and state equity can all be made fiscally equivalent. Different contract structures can apportion risks differently, and affect stability and credibility. Need to make data for key assessments in the regime observable and/or verifiable. Opportunities for aggressive tax planning should be minimized. Overall fiscal regime must take account of relative capacity to bear risk.

27 DETERMINING THE RIGHT GLOBAL TAKE 27

28 The Basics WHAT IS IT? Comparison of fiscal terms from country to country to assess their overall taxes competitiveness WHY IS IT IMPORTANT? International mobility of Capital Investors compare portfolio of investments opportunities in various countries. Fairness and competitiveness of a host country s take is relative to what is obtained elsewhere.

29 Comparative Analysis of Tax Systems Effective Tax Rate: the combined impact of all taxes value of all amounts paid to government Effective Tax Rate= value of profits before taxes are paid 29

30 Simulated petroleum fields 30

31 Benchmarking of fiscal regime 31

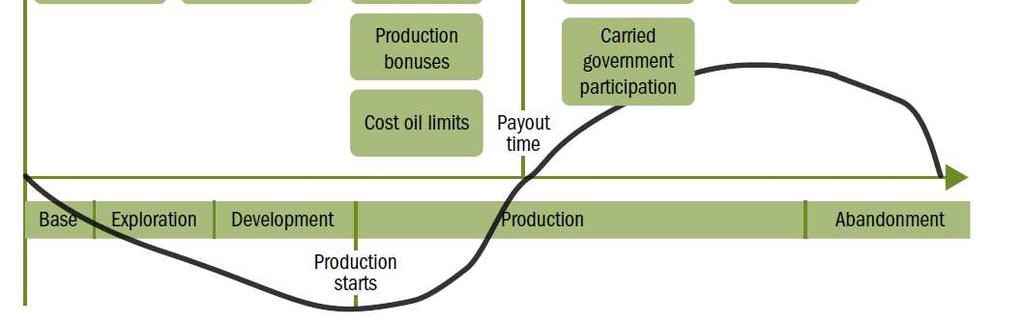

32 Types of Government Take Explore Develop Produce Cumulative Discounted Cash Flow ($) Signature bonus Discovery bonus Development bonus Production bonus Production bonus Rentals Employee taxes Contractor taxes Production bonus Royalties & severance taxes Payback Import & customs duties, VAT & other indirect taxes Production sharing Export duties State participation Profit taxes Additional profit taxes Repatriation taxes Regressive payments unrelated to profit & not creditable in home country Progressive taxes reflect profitability & are often creditable in home country Indirect taxes impact costs rather than ETR State option to enter project Contractor taxes impact costs 32

33 HOW TO BRING PROGRESSIVITY 33

34 REGRESSIVITY & PROGRESSIVITY

35 Progressivity response to price changes 80% Govt. Share Total Benefits 10.0% Disc. Rate Signature bonus Project:Offshore290MMbbl Size: 287 MMBbl Cost:$$23.0 Bbl Price sensitivity 70% 60% 50% Result at $80 Result at $90 Base Regime: CIT only 35% royalty Australia-style PRRT 40% 30% 20% 10% 0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0% 70.0% Pre-tax IRR (from varying oil price) 35

36 Efficiency of a Tax System: To encourage investment Net investor's yield for the company In % V A R I A T I O N 15% Inefficient tax system Efficient tax system V A R I A T I O N An efficient system: Allows for the development of smaller fields: neutrality of taxation, compared with investment decisions Increases the government share in the event of large investor s yields, thus protecting the interests of the country while preserving incentives for the investor Size/Reserves (Millions of barrels) Well productivity (b/j) Oil price ($/barrel)

37 Objectives of a Progressive Tax System The government s share in profits increases in proportion to the actual profitability of projects, unlike in the case of a regressive tax system 100% Government share of pro ofits (In %) 50% Progressive system Regressive system 0% Gross investor s yield from an E&P project (in %)

38 Many ways to deal with progressivity Many forms of tax mechanisms exists: Brown tax (=cashflow= equity share from day 1) Resource Rent Tax: single or multiple tiers; carry forward losses at interest (Australia, Angola) Allowance for Corporate Equity CIT surcharge on cash flow (UK North Sea) Variable Income Tax (South Africa) Based on yield (investor s return) R-Factor 38

39 Example of a levy based on the R ratio (concession) Case of a supplementary levy based on the value of the R ratio R = Cumulative net income Cumulative investment Theoretical example: R Supplementary levy < 1,5 0% 1,5-2,5 15% > 2,5 35% Value of R Signing of the contract EXPLORATION Start of production PRODUCTION Years

40 Sharing Mechanism Based on the R Ratio (PSC) The rate at which profit petroleum is shared is determined by the value of the actual R ratio at the date of production sharing calculation. The contract should state, in particular: The definition of the R ratio and the date of R ratio calculation The shared tranches (limits of R per tranche) and the sharing rate per tranche How cumulative net income is calculated How cumulative investment is calculated Whether the flows are expressed in current $, constant $, or discounted$ (in the latter case, at what discount rate) The R ratio is often calculated in current $ without discounting Consequence: little impact on R of any delay in project implementation (no discounting mechanism) The number of shared tranches and the values of R in each tranche depend on the calculation basis used

41 Sharing Mechanism Based on Investor s Yield (PSC) The rate at which profit petroleum is shared is determined by the value of the actual investor s yield at the sharing calculation date (quarter, year) The contract should state, in particular: The definition of the criterion of investor s yield (including the date of calculation of the actual investor s yield applicable to a quarter) The number of shared tranches, the shared tranches (limits of the investor s yield by tranche), and the share rate by tranche The definition and calculation of the receipts and the outlays taken into account for calculating the investor s yield (before or after tax) Whether the flows used in calculating the investor s yield are expressed in current$ or in constant $ Through the discounting mechanism implicit in the calculation of investor s yield

42 Advantages of Progressive Tax Systems They strengthen contractual stability They stimulate exploration and development of deposits of all sizes (win/win situation) They encourage reinvestment in the contractual area And they thus foster the development of oil business in the country Illustrative examples : Heavy oils in Alberta: progressive rate of royalties Natural gas in Qatar: sharing based on the R ratio Deep offshore in Angola: sharing based on investor s yield And many others

43 Examples of Progressive Tax Systems -Concession Based on investor s yield (rate of return) Canada: frontier areas Faroe Islands Australia (1984) Papua New Guinea (some) Ghana Namibia Seychelles Venezuela (PEG) Saudi Arabia (gas) etc. Based on the R ratio Greece Poland Romania Tunisia (royalties and taxes) Cameroon (new system) Senegal Bolivia Colombia Peru (royalties) etc.

44 Examples of Progressive Tax Systems PSC Based on investor s yield (rate of return) Angola (deep offshore) Equatorial Guinea (before 1998) Tanzania (special tax) Kazakhstan Russia India Based on the R ratio Albania Malta Qatar Bahrain Libya Tunisia Cameroon (nouveau système) Côte d Ivoire Mozambique Senegal Azerbaijan India Malaysia (cost oil &profit oil split) Nicaragua

45 Progressivity tax share of total benefits

46 WHAT ABOUT SIGNATURE BONUSES? 46

47 Angola Signature Bonuses 47

48 Angola: Dutch Disease The top ten most expensive cities 48

49 Angola Signature bonuses 49

50 ISSUES FACED BY GOVERNMENT 50

51 Detection of Transfer Pricing Poor results / Continuous Loss making Significant transactions with related parties in low tax jurisdictions. Transfers of intangibles to related parties Specific types of payments Excessive Debt Poor/Non-existent Documentation 51

52 Transfer Pricing Issues On Revenue / Procurement Significant transactions with related parties in low tax jurisdictions. Transfers of intangibles to related parties Specific types of payments Excessive Debt Poor/Non-existent Documentation 52

53 Capital gains taxation Taxation of transfers of interest in a resource project has become a big issue (Guinea, South Africa provisions). Gains on transfers of real property usually taxable (whether separate CGT or general corporate income tax). What happens when real property is an asset held by foreign companies who sell shares to other non-residents? CGT then very difficult to enforce (and sometimes excluded by treaties). Presence of large gains suggests that fiscal regime is not expected to tax rents fully. Acquisition costs of a mineral right usually amortized should treatment of gains and premiums be symmetrical?

54 International taxation and treaties Border withholding is the main way to tax flows (dividends, interest, service fees, royalties) to non-residents. Modern tax treaties have eroded permissible rates sometimes to zero. Raises questions about value of tax treaties to capital-importing countries. Treaties will be of value if they establish host country s right to border withholding, and taxpayer s right to credit in home country. Treaty shopping has increased difficulty in effectively taxing flows to parent companies. Treaties on information exchange may be sufficient. Is a better answer to focus on royalty and rent taxation by the host?

55 Pricing of infrastructure Many petroleum & mining projects cannot develop without large ancillary investment in infrastructure. Fiscal regime usually deals with upstream production. Important to see that rent is not diverted to transportation and processing investments. Key is appropriate transfer pricing between facilities. May also be an opportunity for transit countries to extract rents through transit fees. Conventional view is that resource rent is attributable to the mine, but how will diversion be prevented?

56 Why is it so hard? Multinationals with high competence; technical, legal, economics & finance Complex fiscal regimes combining tax code and contracts signed at different times Revenue collection responsibilities fragmented Each production site a separate fiscal regime with different fiscal parameters Too many negotiated terms! 56

57 Oil Companies Maximizing return with a reasonable risk Most companies are doing the right thing Taxation: What they do is not illegal Use the existing rules to their advantage Minimize their tax liability worldwide Often benefits from terms willingly given to them But..is it a fair game and why is it so hard? 57

58 Conclusions and Recommendations It is important for a government to understand the objectives and decision-making process of companies Economic assessments of E&P projects and of tax systems should also be carried out by governments Each government should compare the competitiveness of its tax system, compared with those of similar countries Progressive tax systems: make it possible to safeguard the objectives of government and companies alike They are also an incentive for contract stability They encourage business and investment in E&P

59 The key points Fiscal terms must be robust in the face of changing circumstances. Should provide government with a revenue stream in all production periods, but also with an increased share of revenues as profitability increases (progressivity). Establish by law, or published contracts. Minimize discretionary and negotiated elements. Specialized incentives should be avoided. Stability and credibility.

60 THANK YOU! QUESTIONS? 60

61 HOW DOES A PSA WORKS? 61

62 PSA FLOW CHART COMPANY US$100/bbl GOVERNMENT Royalty 0% US$0.00 US$ US$75.00 Cost recovery 75% US$25.00 US$12.50 Profit Oil Split 50%/50% US$ US$0.00 Tax 0% US$0.00 US$87.50 US$12.50 Gross Revenue Net Cash Flow US$12.50 US$ % Take 50%

63 PSA FLOW CHART + royalty COMPANY US$100/bbl GOVERNMENT Royalty 5% US$5.00 US$95.00 US$71.25 Cost recovery 75% US$23.75 US$11.88 Profit Oil Split 50%/50% US$ US$0.00 Tax 0% US$0.00 US$83.13 US$11.88 Gross Revenue Net Cash Flow US$16.88 US$ % Take 58.7%

64 PSA FLOW CHART + royalty + income tax COMPANY US$100/bbl GOVERNMENT Royalty 5% US$5.00 US$95.00 US$71.25 Cost recovery 75% US$23.75 US$11.88 Profit Oil Split 50%/50% US$ US$3.56 Tax 30% US$3.56 US$79.57 US$8.32 Gross Revenue Net Cash Flow US$20.44 US$ % Take 71.1%

65 Calculating Oil/Gas Profits (For the full cycle of an E&P project) M$ * M$ M$ Technical costs Exploration (1) Development (1) Sharing of Oil Profits Cumulative Mining (1) investment M$ M$ In % oil income Cumulative company cash flows Company share 100 x % during Oil profits the mining of a deposit Cumulative government revenue (2) Government take x % AETR=Average effective tax rate * or in another currency M=Million

66 Calculating Oil/Gas Profits continued 1 (For a full project in E&P) M$ Technical costs M$ Case: Concession, with Government Share Oil revenue Cumulative company cash flows M$ Comments Oil profits Cumulative government take Royalties on production Corporate tax Supplementary profit tax Fixed or progressive royalties, based on a criterion (technical, economic, etc.) Ordinary tax or specific oil tax Impact of the amortization system Progressive rate, based on a criterion (R ratio, investor s yield, price, ) Other levies Bonus, surface taxes, etc. Government share With carried interest during exploration

67 M$ Calculation of Oil/Gas Profits continued 2 (For a full project in E&P) Technical costs M$ Case: Production Contract with Government Share Oil revenue Cumulative company cash flows M$ Comments Oil profits Cumulative government take Royalties on production Government share of profit petroleum Corporate tax The government share is often assigned directly to the national company Profit petroleum is shared using various mechanisms (production, R ratio, investor s yield, etc.) Often already included in the government share Other levies Government share

Natural Resource Taxation: Challenges in Africa

Philip Daniel Fiscal Affairs Department International Monetary Fund Natural Resource Taxation: Challenges in Africa Management of Natural Resources in Sub-Saharan Africa Kinshasa Conference, March 22,

Philip Daniel Fiscal Affairs Department International Monetary Fund Natural Resource Taxation: Challenges in Africa Management of Natural Resources in Sub-Saharan Africa Kinshasa Conference, March 22,

Taxation of Natural Resource Rents: Questions, Approaches, Challenges

Philip Daniel Fiscal Affairs Department International Monetary Fund Taxation of Natural Resource Rents: Questions, Approaches, Challenges IMF Natural Resources Consultation Session on Taxation and Wealth

Philip Daniel Fiscal Affairs Department International Monetary Fund Taxation of Natural Resource Rents: Questions, Approaches, Challenges IMF Natural Resources Consultation Session on Taxation and Wealth

ENVIRONMENTAL ISSUES and NATURAL RESOURCE EXTRACTION

ENVIRONMENTAL ISSUES and NATURAL RESOURCE EXTRACTION Natural Resource Taxation Issues for Environment Policy? Alan Carter Senior Tax Economist International Tax Dialogue Berlin, 23 March 2012 ISSUES COVERED

ENVIRONMENTAL ISSUES and NATURAL RESOURCE EXTRACTION Natural Resource Taxation Issues for Environment Policy? Alan Carter Senior Tax Economist International Tax Dialogue Berlin, 23 March 2012 ISSUES COVERED

Fiscal Regimes for Extractive Industries Design and Implementation

Fiscal Regimes for Extractive Industries Design and Implementation Peter Mullins Fiscal Affairs Department Conference on Natural Resource Taxation in the Asia-Pacific Region Jakarta, Indonesia August 11,

Fiscal Regimes for Extractive Industries Design and Implementation Peter Mullins Fiscal Affairs Department Conference on Natural Resource Taxation in the Asia-Pacific Region Jakarta, Indonesia August 11,

Argentina Bahamas Barbados Bermuda Bolivia Brazil British Virgin Islands Canada Cayman Islands Chile

Americas Argentina (Banking and finance; Capital markets: Debt; Capital markets: Equity; M&A; Project Bahamas (Financial and corporate) Barbados (Financial and corporate) Bermuda (Financial and corporate)

Americas Argentina (Banking and finance; Capital markets: Debt; Capital markets: Equity; M&A; Project Bahamas (Financial and corporate) Barbados (Financial and corporate) Bermuda (Financial and corporate)

Another Technological Revolution in the O&G Industry: A new Future for Onshore E&P. Ivan Sandrea Advisor to Petra Energia

Another Technological Revolution in the O&G Industry: A new Future for Onshore E&P Ivan Sandrea Advisor to Petra Energia Contents Another technological revolution in the O&G industry Key onshore stats

Another Technological Revolution in the O&G Industry: A new Future for Onshore E&P Ivan Sandrea Advisor to Petra Energia Contents Another technological revolution in the O&G industry Key onshore stats

Course Outline. Applied Upstream Petroleum Fiscal Modeling & Economics. Course Leader: Barry Rodgers

Course Outline Applied Upstream Petroleum Fiscal Modeling & Economics Course Leader: Barry Rodgers Upstream Petroleum Fiscal Modeling & Economics Day 1 Morning (0830:12:00) Introduction Participants Introductions

Course Outline Applied Upstream Petroleum Fiscal Modeling & Economics Course Leader: Barry Rodgers Upstream Petroleum Fiscal Modeling & Economics Day 1 Morning (0830:12:00) Introduction Participants Introductions

TRENDS AND MARKERS Signatories to the United Nations Convention against Transnational Organised Crime

A F R I C A WA T C H TRENDS AND MARKERS Signatories to the United Nations Convention against Transnational Organised Crime Afghanistan Albania Algeria Andorra Angola Antigua and Barbuda Argentina Armenia

A F R I C A WA T C H TRENDS AND MARKERS Signatories to the United Nations Convention against Transnational Organised Crime Afghanistan Albania Algeria Andorra Angola Antigua and Barbuda Argentina Armenia

The Commodities Roller Coaster: A Fiscal Framework for Uncertain Times

International Monetary Fund October 215 Fiscal Monitor The Commodities Roller Coaster: A Fiscal Framework for Uncertain Times Tidiane Kinda Fiscal Affairs Department Vienna, November 26, 215 The views

International Monetary Fund October 215 Fiscal Monitor The Commodities Roller Coaster: A Fiscal Framework for Uncertain Times Tidiane Kinda Fiscal Affairs Department Vienna, November 26, 215 The views

ANNEX 2: Methodology and data of the Starting a Foreign Investment indicators

ANNEX 2: Methodology and data of the Starting a Foreign Investment indicators Methodology The Starting a Foreign Investment indicators quantify several aspects of business establishment regimes important

ANNEX 2: Methodology and data of the Starting a Foreign Investment indicators Methodology The Starting a Foreign Investment indicators quantify several aspects of business establishment regimes important

Parallel Roundtable 2: Fiscal Regimes and Legal Reform to Attract Investment in the Energy Sector. Background Paper

Parallel Roundtable 2: Fiscal Regimes and Legal Reform to Attract Investment in the Energy Sector India New Delhi Background Paper Disclaimer The observations presented herein are meant as background for

Parallel Roundtable 2: Fiscal Regimes and Legal Reform to Attract Investment in the Energy Sector India New Delhi Background Paper Disclaimer The observations presented herein are meant as background for

2019 Daily Prayer for Peace Country Cycle

2019 Daily Prayer for Peace Country Cycle Tuesday January 1, 2019 All Nations Wednesday January 2, 2019 Thailand Thursday January 3, 2019 Sudan Friday January 4, 2019 Solomon Islands Saturday January 5,

2019 Daily Prayer for Peace Country Cycle Tuesday January 1, 2019 All Nations Wednesday January 2, 2019 Thailand Thursday January 3, 2019 Sudan Friday January 4, 2019 Solomon Islands Saturday January 5,

ide: FRANCE Appendix A Countries with Double Taxation Agreement with France

Fiscal operational guide: FRANCE ide: FRANCE Appendix A Countries with Double Taxation Agreement with France Albania Algeria Argentina Armenia 2006 2006 From 1 March 1981 2002 1 1 1 All persons 1 Legal

Fiscal operational guide: FRANCE ide: FRANCE Appendix A Countries with Double Taxation Agreement with France Albania Algeria Argentina Armenia 2006 2006 From 1 March 1981 2002 1 1 1 All persons 1 Legal

GEF Evaluation Office MID-TERM REVIEW OF THE GEF RESOURCE ALLOCATION FRAMEWORK. Portfolio Analysis and Historical Allocations

GEF Evaluation Office MID-TERM REVIEW OF THE GEF RESOURCE ALLOCATION FRAMEWORK Portfolio Analysis and Historical Allocations Statistical Annex #2 30 October 2008 Midterm Review Contents Table 1: Historical

GEF Evaluation Office MID-TERM REVIEW OF THE GEF RESOURCE ALLOCATION FRAMEWORK Portfolio Analysis and Historical Allocations Statistical Annex #2 30 October 2008 Midterm Review Contents Table 1: Historical

Annex Supporting international mobility: calculating salaries

Annex 5.2 - Supporting international mobility: calculating salaries Base salary refers to a fixed amount of money paid to an Employee in return for work performed and it is determined in accordance with

Annex 5.2 - Supporting international mobility: calculating salaries Base salary refers to a fixed amount of money paid to an Employee in return for work performed and it is determined in accordance with

Click to edit Master title style. Evaluating Fiscal Regimes for Resource Projects: An Example from Oil Development. Click to edit Master text styles

Evaluating Fiscal Regimes for Resource Projects: An Example from Oil Development Philip Daniel, Brenton Goldsworthy, Wojciech Maliszewski, Diego Mesa Puyo, and Alistair Watson Taxing Natural Fourth Resources:

Evaluating Fiscal Regimes for Resource Projects: An Example from Oil Development Philip Daniel, Brenton Goldsworthy, Wojciech Maliszewski, Diego Mesa Puyo, and Alistair Watson Taxing Natural Fourth Resources:

Withholding Tax Rates 2017*

Withholding Tax Rates 2017* International Tax Updated March 2017 Jurisdiction Dividends Interest Royalties Notes Albania 15% 15% 15% Algeria 15% 10% 24% Andorra 0% 0% 5% Angola 10% 15% 10% Anguilla 0%

Withholding Tax Rates 2017* International Tax Updated March 2017 Jurisdiction Dividends Interest Royalties Notes Albania 15% 15% 15% Algeria 15% 10% 24% Andorra 0% 0% 5% Angola 10% 15% 10% Anguilla 0%

Request to accept inclusive insurance P6L or EASY Pauschal

5002001020 page 1 of 7 Request to accept inclusive insurance P6L or EASY Pauschal APPLICANT (INSURANCE POLICY HOLDER) Full company name and address WE ARE APPLYING FOR COVER PRIOR TO DELIVERY (PRE-SHIPMENT

5002001020 page 1 of 7 Request to accept inclusive insurance P6L or EASY Pauschal APPLICANT (INSURANCE POLICY HOLDER) Full company name and address WE ARE APPLYING FOR COVER PRIOR TO DELIVERY (PRE-SHIPMENT

The future of government petroleum regimes

The future of government petroleum regimes Presentation to Iraq Iraq Energy Forum Workshop April 4, 2017, Baghdad Pedro van Meurs Future trends in government petroleum regimes During this presentation

The future of government petroleum regimes Presentation to Iraq Iraq Energy Forum Workshop April 4, 2017, Baghdad Pedro van Meurs Future trends in government petroleum regimes During this presentation

Scale of Assessment of Members' Contributions for 2008

General Conference GC(51)/21 Date: 28 August 2007 General Distribution Original: English Fifty-first regular session Item 13 of the provisional agenda (GC(51)/1) Scale of Assessment of s' Contributions

General Conference GC(51)/21 Date: 28 August 2007 General Distribution Original: English Fifty-first regular session Item 13 of the provisional agenda (GC(51)/1) Scale of Assessment of s' Contributions

Annual Report on Exchange Arrangements and Exchange Restrictions 2011

Annual Report on Exchange Arrangements and Exchange Restrictions 2011 Volume 1 of 4 ISBN: 978-1-61839-226-8 Copyright 2010 International Monetary Fund International Monetary Fund, Publication Services

Annual Report on Exchange Arrangements and Exchange Restrictions 2011 Volume 1 of 4 ISBN: 978-1-61839-226-8 Copyright 2010 International Monetary Fund International Monetary Fund, Publication Services

Country Documentation Finder

Country Shipper s Export Declaration Commercial Invoice Country Documentation Finder Customs Consular Invoice Certificate of Origin Bill of Lading Insurance Certificate Packing List Import License Afghanistan

Country Shipper s Export Declaration Commercial Invoice Country Documentation Finder Customs Consular Invoice Certificate of Origin Bill of Lading Insurance Certificate Packing List Import License Afghanistan

Household Debt and Business Cycles Worldwide Out-of-sample results based on IMF s new Global Debt Database

Household Debt and Business Cycles Worldwide Out-of-sample results based on IMF s new Global Debt Database Atif Mian Princeton University and NBER Amir Sufi University of Chicago Booth School of Business

Household Debt and Business Cycles Worldwide Out-of-sample results based on IMF s new Global Debt Database Atif Mian Princeton University and NBER Amir Sufi University of Chicago Booth School of Business

HEALTH WEALTH CAREER 2017 WORLDWIDE BENEFIT & EMPLOYMENT GUIDELINES

HEALTH WEALTH CAREER 2017 WORLDWIDE BENEFIT & EMPLOYMENT GUIDELINES WORLDWIDE BENEFIT & EMPLOYMENT GUIDELINES AT A GLANCE GEOGRAPHY 77 COUNTRIES COVERED 5 REGIONS Americas Asia Pacific Central & Eastern

HEALTH WEALTH CAREER 2017 WORLDWIDE BENEFIT & EMPLOYMENT GUIDELINES WORLDWIDE BENEFIT & EMPLOYMENT GUIDELINES AT A GLANCE GEOGRAPHY 77 COUNTRIES COVERED 5 REGIONS Americas Asia Pacific Central & Eastern

2 Albania Algeria , Andorra

1 Afghanistan LDC 110 80 110 80 219 160 2 Albania 631 460 631 460 1 262 920 3 Algeria 8 628 6,290 8 615 6 280 17 243 12 570 4 Andorra 837 610 837 610 1 674 1 220 5 Angola LDC 316 230 316 230 631 460 6

1 Afghanistan LDC 110 80 110 80 219 160 2 Albania 631 460 631 460 1 262 920 3 Algeria 8 628 6,290 8 615 6 280 17 243 12 570 4 Andorra 837 610 837 610 1 674 1 220 5 Angola LDC 316 230 316 230 631 460 6

ECON4925 Resource Economics Lecture on Resource Rent Taxation

ECON4925 Resource Economics Lecture on Resource Rent Taxation Diderik Lund Department of Economics University of Oslo 16 November 2016 Diderik Lund, Dept. of Econ., UiO ECON4925 Lect. on Resource Taxes

ECON4925 Resource Economics Lecture on Resource Rent Taxation Diderik Lund Department of Economics University of Oslo 16 November 2016 Diderik Lund, Dept. of Econ., UiO ECON4925 Lect. on Resource Taxes

WGI Ranking for SA8000 System

Afghanistan not rated Highest Risk ALBANIA 47 High Risk ALGERIA 24 Highest Risk AMERICAN SAMOA 74 Lower Risk ANDORRA 91 Lower Risk ANGOLA 16 Highest Risk ANGUILLA 90 Lower Risk ANTIGUA AND BARBUDA 76 Lower

Afghanistan not rated Highest Risk ALBANIA 47 High Risk ALGERIA 24 Highest Risk AMERICAN SAMOA 74 Lower Risk ANDORRA 91 Lower Risk ANGOLA 16 Highest Risk ANGUILLA 90 Lower Risk ANTIGUA AND BARBUDA 76 Lower

TIMID GLOBAL GROWTH: THE NEW NORMAL?

TIMID GLOBAL GROWTH: THE NEW NORMAL? 1 THE IMF FORECASTS GLOBAL GROWTH OF ~ 3.% IN 1/1, with a pickup in advanced economies and stabilization in emerging markets According to the IMF, global growth is

TIMID GLOBAL GROWTH: THE NEW NORMAL? 1 THE IMF FORECASTS GLOBAL GROWTH OF ~ 3.% IN 1/1, with a pickup in advanced economies and stabilization in emerging markets According to the IMF, global growth is

Dutch tax treaty overview Q3, 2012

Dutch tax treaty overview Q3, 2012 Hendrik van Duijn DTS Duijn's Tax Solutions Zuidplein 36 (WTC Tower H) 1077 XV Amsterdam The Netherlands T +31 888 387 669 T +31 888 DTS NOW F +31 88 8 387 601 duijn@duijntax.com

Dutch tax treaty overview Q3, 2012 Hendrik van Duijn DTS Duijn's Tax Solutions Zuidplein 36 (WTC Tower H) 1077 XV Amsterdam The Netherlands T +31 888 387 669 T +31 888 DTS NOW F +31 88 8 387 601 duijn@duijntax.com

Supplementary Table S1 National mitigation objectives included in INDCs from Jan to Jul. 2017

1 Supplementary Table S1 National mitigation objectives included in INDCs from Jan. 2015 to Jul. 2017 Country Submitted Date GHG Reduction Target Quantified Unconditional Conditional Asia Afghanistan Oct.,

1 Supplementary Table S1 National mitigation objectives included in INDCs from Jan. 2015 to Jul. 2017 Country Submitted Date GHG Reduction Target Quantified Unconditional Conditional Asia Afghanistan Oct.,

EMBARGOED UNTIL GMT 1 AUGUST

2016 Global Breastfeeding Scorecard: Country Scores EMBARGOED UNTIL 00.01 GMT 1 AUGUST Enabling Environment Reporting Practice UN Region Country Donor Funding (USD) Per Live Birth Legal Status of the Code

2016 Global Breastfeeding Scorecard: Country Scores EMBARGOED UNTIL 00.01 GMT 1 AUGUST Enabling Environment Reporting Practice UN Region Country Donor Funding (USD) Per Live Birth Legal Status of the Code

SURVEY TO DETERMINE THE PERCENTAGE OF NATIONAL REVENUE REPRESENTED BY CUSTOMS DUTIES INTRODUCTION

SURVEY TO DETERMINE THE PERCENTAGE OF NATIONAL REVENUE REPRESENTED BY CUSTOMS DUTIES INTRODUCTION This publication provides information about the share of national revenues represented by Customs duties.

SURVEY TO DETERMINE THE PERCENTAGE OF NATIONAL REVENUE REPRESENTED BY CUSTOMS DUTIES INTRODUCTION This publication provides information about the share of national revenues represented by Customs duties.

Countries with Double Taxation Agreements with the UK rates of withholding tax for the year ended 5 April 2012

Countries with Double Taxation Agreements with the UK rates of withholding tax for the year ended 5 April 2012 This table shows the maximum rates of tax those countries with a Double Taxation Agreement

Countries with Double Taxation Agreements with the UK rates of withholding tax for the year ended 5 April 2012 This table shows the maximum rates of tax those countries with a Double Taxation Agreement

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT BOARD OF GOVERNORS. Resolution No. 612

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT BOARD OF GOVERNORS Resolution No. 612 2010 Selective Increase in Authorized Capital Stock to Enhance Voice and Participation of Developing and Transition

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT BOARD OF GOVERNORS Resolution No. 612 2010 Selective Increase in Authorized Capital Stock to Enhance Voice and Participation of Developing and Transition

New Exchange Rates Apply to Agricultural Trade. 0. Halbert Goolsby. Reprint from FOREIGN AGRICULTURAL TRADE OF THE UNITED STATES April 1972

New Exchange Rates Apply to Agricultural by. Halbert Goolsby '.,_::' Reprint from FOREIGN AGRICULTURAL TRADE OF THE UNITED STATES April 1972 Statistics Branch Foreign Demand and Competition Division Economic

New Exchange Rates Apply to Agricultural by. Halbert Goolsby '.,_::' Reprint from FOREIGN AGRICULTURAL TRADE OF THE UNITED STATES April 1972 Statistics Branch Foreign Demand and Competition Division Economic

( Euro) Annual & Monthly Premium Rates. International Healthcare Plan. Geographic Areas. (effective 1st July 2007) Premium Discount

Annual & Monthly Premium Rates. International Healthcare Plan. Geographic Areas. (effective 1st July 2007) Premium Discount") Annual & Monthly Premium Rates International Healthcare Plan (effective 1st July 2007) ( Euro) This schedule contains information on Your premiums for the International Healthcare Plan in Euros. Simply

Annual & Monthly Premium Rates International Healthcare Plan (effective 1st July 2007) ( Euro) This schedule contains information on Your premiums for the International Healthcare Plan in Euros. Simply

April 2015 Fiscal Monitor

International Monetary Fund April 17, 2015 April 2015 Fiscal Monitor Now is the Time: Fiscal Policies for Sustainable Growth Xavier Debrun Deputy Chief, Fiscal Policy and Surveillance, Fiscal Affairs Department

International Monetary Fund April 17, 2015 April 2015 Fiscal Monitor Now is the Time: Fiscal Policies for Sustainable Growth Xavier Debrun Deputy Chief, Fiscal Policy and Surveillance, Fiscal Affairs Department

Azerbaijan Compliant since: Latest report: Government revenue: Population: Revenue per capita:

Azerbaijan 16 February 2009 2011 US $3 035 423 996 9 168 000 US $331 Total revenues received by the government from the oil, gas and mining sector in 2011 was over US $3 billion. But full picture is not

Azerbaijan 16 February 2009 2011 US $3 035 423 996 9 168 000 US $331 Total revenues received by the government from the oil, gas and mining sector in 2011 was over US $3 billion. But full picture is not

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT BOARD OF GOVERNORS. Resolution No General Capital Increase

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT BOARD OF GOVERNORS Resolution No. 663 2018 General Capital Increase WHEREAS the Executive Directors, having considered the question of enlarging the

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT BOARD OF GOVERNORS Resolution No. 663 2018 General Capital Increase WHEREAS the Executive Directors, having considered the question of enlarging the

Angola s E&P Fiscal Regime In a Global Context. Delivering commercial insight to the global energy industry

Angola s E&P Fiscal Regime In a Global Context www.woodmac.com Agenda Summary of Angola s E&P fiscal regimes State / investor revenue-sharing under the fiscal regimes Angola s fiscal regimes in a global

Angola s E&P Fiscal Regime In a Global Context www.woodmac.com Agenda Summary of Angola s E&P fiscal regimes State / investor revenue-sharing under the fiscal regimes Angola s fiscal regimes in a global

Financial Accounting Advisory Services

Financial Accounting Advisory Services Bringing clarity to the accounting for restructuring activities October 2014 Agenda 3 About EY 13 Contacts 15 Page 2 Accounting for restructuring Page 3 Why do companies

Financial Accounting Advisory Services Bringing clarity to the accounting for restructuring activities October 2014 Agenda 3 About EY 13 Contacts 15 Page 2 Accounting for restructuring Page 3 Why do companies

CREDIT INSURANCE. To ensure peace, you must be prepared for war. CREDIT INSURANCE FUNDAMENTAL SOLUTION IN CREDIT RISK MANAGEMENT

FUNDAMENTAL SOLUTION IN CREDIT RISK MANAGEMENT I would like to extend my relations with that customer... I would like to enter a new market... We have high exposure for that customer... We have delayed

FUNDAMENTAL SOLUTION IN CREDIT RISK MANAGEMENT I would like to extend my relations with that customer... I would like to enter a new market... We have high exposure for that customer... We have delayed

IBRD/IDA and Blend Countries: Per Capita Incomes, Lending Eligibility, IDA Repayment Terms

Page 1 of 7 Note: This OP 3.10, Annex D replaces the version dated September 2013. The revised terms are effective for all loans that are approved on or after July 1, 2014. IBRD/IDA and Blend Countries:

Page 1 of 7 Note: This OP 3.10, Annex D replaces the version dated September 2013. The revised terms are effective for all loans that are approved on or after July 1, 2014. IBRD/IDA and Blend Countries:

Withholding Tax Rates 2018*

Withholding Tax Rates 2018* Jurisdiction Dividends Interest Royalties Notes Albania 15% 15% 15% Algeria 15% 10% 24% Andorra 0% 0% 5% Angola 10% 5%/10%/15% 10% Anguilla 0% 0% 0% Antigua & Barbuda 25% 25%

Withholding Tax Rates 2018* Jurisdiction Dividends Interest Royalties Notes Albania 15% 15% 15% Algeria 15% 10% 24% Andorra 0% 0% 5% Angola 10% 5%/10%/15% 10% Anguilla 0% 0% 0% Antigua & Barbuda 25% 25%

Delivering mobile connectivity in MENA: A review of mobile sector taxation and licence extension. May 2017

Delivering mobile connectivity in MENA: A review of mobile sector taxation and licence extension May 2017 Executive Summary The report provides an overview of the tax and fee regime applied to mobile services

Delivering mobile connectivity in MENA: A review of mobile sector taxation and licence extension May 2017 Executive Summary The report provides an overview of the tax and fee regime applied to mobile services

Generating Extractive Industry Revenues

Philip Daniel Fiscal Affairs Department International Monetary Fund Generating Extractive Industry Revenues Kenya s Economic Successes, Prospects and Challenges National Treasury, Central Bank of Kenya,

Philip Daniel Fiscal Affairs Department International Monetary Fund Generating Extractive Industry Revenues Kenya s Economic Successes, Prospects and Challenges National Treasury, Central Bank of Kenya,

World Oil & Gas Fiscal Systems & Analysis of E&P Contract Types CEM02

World Oil & Gas Fiscal Systems & Analysis of E&P Contract Types CEM02 Oil & Gas Consultancy Services & Technical Training Providers Enhancing business through knowledge 2 WORLD OIL AND GAS FISCAL SYSTEMS

World Oil & Gas Fiscal Systems & Analysis of E&P Contract Types CEM02 Oil & Gas Consultancy Services & Technical Training Providers Enhancing business through knowledge 2 WORLD OIL AND GAS FISCAL SYSTEMS

Withholding Tax Rates 2014*

Withholding Tax Rates 2014* (Rates are current as of 1 March 2014) Jurisdiction Dividends Interest Royalties Notes Afghanistan 20% 20% 20% International Tax Albania 10% 10% 10% Algeria 15% 10% 24% Andorra

Withholding Tax Rates 2014* (Rates are current as of 1 March 2014) Jurisdiction Dividends Interest Royalties Notes Afghanistan 20% 20% 20% International Tax Albania 10% 10% 10% Algeria 15% 10% 24% Andorra

Long Association List of Jurisdictions Surveyed for Which a Response Has Been Received

Agenda Item 7-B Long Association List of Jurisdictions Surveed for Which a Has Been Received Jurisdictions Region IFAC Largest 29 G10 G20 EU/EEA IOSCO IFIAR Surve Abu Dhabi Member (UAE) Albania Member

Agenda Item 7-B Long Association List of Jurisdictions Surveed for Which a Has Been Received Jurisdictions Region IFAC Largest 29 G10 G20 EU/EEA IOSCO IFIAR Surve Abu Dhabi Member (UAE) Albania Member

IBRD/IDA and Blend Countries: Per Capita Incomes, Lending Eligibility, and Repayment Terms

Page 1 of 7 (Updated ) Note: This OP 3.10, Annex D replaces the version dated March 2013. The revised terms are effective for all loans for which invitations to negotiate are issued on or after July 1,

Page 1 of 7 (Updated ) Note: This OP 3.10, Annex D replaces the version dated March 2013. The revised terms are effective for all loans for which invitations to negotiate are issued on or after July 1,

Kentucky Cabinet for Economic Development Office of Workforce, Community Development, and Research

Table 2 Kentucky s Exports to the World -- Inclusive of Year to Date () Values in $ Thousands 2016 Year to Date Total All Countries $ 29,201,010 $ 30,857,275 5.7% $ 20,030,998 $ 20,925,509 4.5% Canada

Table 2 Kentucky s Exports to the World -- Inclusive of Year to Date () Values in $ Thousands 2016 Year to Date Total All Countries $ 29,201,010 $ 30,857,275 5.7% $ 20,030,998 $ 20,925,509 4.5% Canada

FOR OIL & GAS WORLD FISCAL SYSTEMS BAC.

BAC ACCREDITED WORLD FISCAL SYSTEMS FOR OIL & GAS DATE: LOCATION: 03-07 March 2014 Singapore 09-13 June 2014 Amsterdam, The Netherlands 16-20 November 2014 Dubai, UAE Receive the most comprehensive overview

BAC ACCREDITED WORLD FISCAL SYSTEMS FOR OIL & GAS DATE: LOCATION: 03-07 March 2014 Singapore 09-13 June 2014 Amsterdam, The Netherlands 16-20 November 2014 Dubai, UAE Receive the most comprehensive overview

Resource Dependence and Budget Transparency By Antoine Heuty and Ruth Carlitz 1

By Antoine Heuty and Ruth Carlitz 1 Are natural resource abundance and opaque budgets inextricably linked? The Open Budget Survey 2008 a comprehensive evaluation of budget transparency in 85 countries

By Antoine Heuty and Ruth Carlitz 1 Are natural resource abundance and opaque budgets inextricably linked? The Open Budget Survey 2008 a comprehensive evaluation of budget transparency in 85 countries

Taxation of natural resources: principles and policy issues

Taxation of natural resources: principles and policy issues Charles Makola The better the question. The better the answer. The better the world works. Introduction Simplified economic and political framework

Taxation of natural resources: principles and policy issues Charles Makola The better the question. The better the answer. The better the world works. Introduction Simplified economic and political framework

Total Imports by Volume (Gallons per Country)

") 7/6/2018 Imports by Volume (Gallons per Country) YTD YTD Country 05/2017 05/2018 % Change 2017 2018 % Change MEXICO 71,166,360 74,896,922 5.2 % 302,626,505 328,397,135 8.5 % NETHERLANDS 12,039,171 13,341,929

7/6/2018 Imports by Volume (Gallons per Country) YTD YTD Country 05/2017 05/2018 % Change 2017 2018 % Change MEXICO 71,166,360 74,896,922 5.2 % 302,626,505 328,397,135 8.5 % NETHERLANDS 12,039,171 13,341,929

Other Tax Rates. Non-Resident Withholding Tax Rates for Treaty Countries 1

Other Tax Rates Non-Resident Withholding Tax Rates for Treaty Countries 1 Country 2 Interest 3 Dividends 4 Royalties 5 Annuities 6 Pensions/ Algeria 15% 15% 0/15% 15/25% Argentina 7 12.5 10/15 3/5/10/15

Other Tax Rates Non-Resident Withholding Tax Rates for Treaty Countries 1 Country 2 Interest 3 Dividends 4 Royalties 5 Annuities 6 Pensions/ Algeria 15% 15% 0/15% 15/25% Argentina 7 12.5 10/15 3/5/10/15

IN HOUSE TRAINING COURSES:

World Training for Oil and Gas Course leader: Pedro van Meurs IN HOUSE TRAINING COURSES: 2015-2016 Computer interactive training course available in 3-day, 4-day and 5-day programs Run over 35 years now,

World Training for Oil and Gas Course leader: Pedro van Meurs IN HOUSE TRAINING COURSES: 2015-2016 Computer interactive training course available in 3-day, 4-day and 5-day programs Run over 35 years now,

UBI Pramerica SGR. US Economic Environment. Richard K. Mastain, Senior Vice President Jennison Associates LLC. April 2008

UBI Pramerica SGR US Economic Environment Richard K. Mastain, Senior Vice President Jennison Associates LLC Subadvisor to Certain UBI Pramerica SGR Funds April 2008 Notice This presentation is for informational

UBI Pramerica SGR US Economic Environment Richard K. Mastain, Senior Vice President Jennison Associates LLC Subadvisor to Certain UBI Pramerica SGR Funds April 2008 Notice This presentation is for informational

STATISTICS ON EXTERNAL INDEBTEDNESS

ORGANISATION FOR ECONOMIC CO-OPERATION AND DEVELOPMENT PARIS BANK FOR INTERNATIONAL SETTLEMENTS BASLE STATISTICS ON EXTERNAL INDEBTEDNESS Bank and trade-related non-bank external claims on individual borrowing

ORGANISATION FOR ECONOMIC CO-OPERATION AND DEVELOPMENT PARIS BANK FOR INTERNATIONAL SETTLEMENTS BASLE STATISTICS ON EXTERNAL INDEBTEDNESS Bank and trade-related non-bank external claims on individual borrowing

a closer look GLOBAL TAX WEEKLY ISSUE 249 AUGUST 17, 2017

GLOBAL TAX WEEKLY a closer look ISSUE 249 AUGUST 17, 2017 SUBJECTS TRANSFER PRICING INTELLECTUAL PROPERTY VAT, GST AND SALES TAX CORPORATE TAXATION INDIVIDUAL TAXATION REAL ESTATE AND PROPERTY TAXES INTERNATIONAL

GLOBAL TAX WEEKLY a closer look ISSUE 249 AUGUST 17, 2017 SUBJECTS TRANSFER PRICING INTELLECTUAL PROPERTY VAT, GST AND SALES TAX CORPORATE TAXATION INDIVIDUAL TAXATION REAL ESTATE AND PROPERTY TAXES INTERNATIONAL

MAXIMUM MONTHLY STIPEND RATES FOR FELLOWS AND SCHOLARS. Afghanistan $135 $608 $911 1 March Albania $144 $2,268 $3,402 1 January 2005

MAXIMUM MONTHLY STIPEND RATES FOR FELLOWS AND SCHOLARS (IN U.S. DOLLARS FOR COST ESTIMATE) COUNTRY DSA(US$) MAX RES RATE MAX TRV RATE EFFECTIVE DATE OF % Afghanistan $135 $608 $911 1 March 1989 Albania

MAXIMUM MONTHLY STIPEND RATES FOR FELLOWS AND SCHOLARS (IN U.S. DOLLARS FOR COST ESTIMATE) COUNTRY DSA(US$) MAX RES RATE MAX TRV RATE EFFECTIVE DATE OF % Afghanistan $135 $608 $911 1 March 1989 Albania

26 MAY Boustead Singapore Limited FY2010 Financial Results Presentation

26 MAY 2010 Boustead Singapore Limited FY2010 Financial Results Presentation Disclaimer This presentation contains certain statements that are not statements of historical fact such as forward-looking

26 MAY 2010 Boustead Singapore Limited FY2010 Financial Results Presentation Disclaimer This presentation contains certain statements that are not statements of historical fact such as forward-looking

JPMorgan Funds statistics report: Emerging Markets Debt Fund

NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE JPMorgan Funds statistics report: Emerging Markets Debt Fund Data as of November 30, 2016 Must be preceded or accompanied by a prospectus. jpmorganfunds.com

NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE JPMorgan Funds statistics report: Emerging Markets Debt Fund Data as of November 30, 2016 Must be preceded or accompanied by a prospectus. jpmorganfunds.com

Why Corrupt Governments May Receive More Foreign Aid

Why Corrupt Governments May Receive More Foreign Aid David de la Croix Clara Delavallade Online Appendix Appendix A - Extension with Productive Government Spending The time resource constraint is 1 = l

Why Corrupt Governments May Receive More Foreign Aid David de la Croix Clara Delavallade Online Appendix Appendix A - Extension with Productive Government Spending The time resource constraint is 1 = l

INTERNATIONAL CONVENTION ON STANDARDS OF TRAINING, CERTIFICATION AND WATCHKEEPING FOR SEAFARERS (STCW), 1978, AS AMENDED

, 1978, AS AMENDED") E 4 ALBERT EMBANKMENT LONDON SE1 7SR Telephone: +44 (0)20 7735 711 Fax: +44 (0)20 7587 3210 1 January 2019 INTERNATIONAL CONVENTION ON STANDARDS OF TRAINING, CERTIFICATION AND WATCHKEEPING FOR SEAFARERS

E 4 ALBERT EMBANKMENT LONDON SE1 7SR Telephone: +44 (0)20 7735 711 Fax: +44 (0)20 7587 3210 1 January 2019 INTERNATIONAL CONVENTION ON STANDARDS OF TRAINING, CERTIFICATION AND WATCHKEEPING FOR SEAFARERS

Demographic transition in resource rich countries: a bonus or a curse?

From the SelectedWorks of Prof. Dr. Mohammad Reza Farzanegan September, 2012 Demographic transition in resource rich countries: a bonus or a curse? Kjetil Bjorvatn Mohammad Reza Farzanegan Available at:

From the SelectedWorks of Prof. Dr. Mohammad Reza Farzanegan September, 2012 Demographic transition in resource rich countries: a bonus or a curse? Kjetil Bjorvatn Mohammad Reza Farzanegan Available at:

Extractive Industries Transparency Initiative (EITI) Improving EI: Emerging Lessons and Results from EITI implementation in the GAC context

Improving EI: Emerging Lessons and Results from EITI implementation in the GAC context") Extractive Industries Transparency Initiative (EITI) PREM Week 2008 Joint Event on Extractive Industries (EI): Legal / Fiscal Systems, Revenue Management and Good Governance Improving EI: Emerging Lessons

Extractive Industries Transparency Initiative (EITI) PREM Week 2008 Joint Event on Extractive Industries (EI): Legal / Fiscal Systems, Revenue Management and Good Governance Improving EI: Emerging Lessons

FOREWORD. Egypt. Services provided by member firms include:

2015/16 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

2015/16 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

World Development Indicators

: Afghanistan Albania Algeria American Samoa Andorra Angola Antigua and Barbuda Argentina Armenia Aruba Australia Austria Azerbaijan Bahamas, The Bahrain Bangladesh Barbados Belarus Belgium Belize Benin

: Afghanistan Albania Algeria American Samoa Andorra Angola Antigua and Barbuda Argentina Armenia Aruba Australia Austria Azerbaijan Bahamas, The Bahrain Bangladesh Barbados Belarus Belgium Belize Benin

Dutch tax treaty overview Q4, 2013

Dutch tax treaty overview Q4, 2013 Hendrik van Duijn DTS Duijn's Tax Solutions Zuidplein 36 (WTC Tower H) 1077 XV Amsterdam The Netherlands T +31 888 387 669 T +31 888 DTS NOW F +31 88 8 387 601 duijn@duijntax.com

Dutch tax treaty overview Q4, 2013 Hendrik van Duijn DTS Duijn's Tax Solutions Zuidplein 36 (WTC Tower H) 1077 XV Amsterdam The Netherlands T +31 888 387 669 T +31 888 DTS NOW F +31 88 8 387 601 duijn@duijntax.com

Bilateral agreements on investment promotion and protection

Bilateral agreements on investment promotion and protection Country Date Signed Entry into force South Africa 26 April 2005 - Albania 30 October 1993 - Algeria 7 July 2006 - Germany 20 December 1963 6

Bilateral agreements on investment promotion and protection Country Date Signed Entry into force South Africa 26 April 2005 - Albania 30 October 1993 - Algeria 7 July 2006 - Germany 20 December 1963 6

Hoi Wai Cheng, Dawn Holland, Ingo Pitterle

Hoi Wai Cheng, Dawn Holland, Ingo Pitterle United Nations, GEMU/DPAD/DESA Project LINK Meeting 21-23 October 2015, New York Demand-side role Direct impact on the price level and terms of trade Secondary

Hoi Wai Cheng, Dawn Holland, Ingo Pitterle United Nations, GEMU/DPAD/DESA Project LINK Meeting 21-23 October 2015, New York Demand-side role Direct impact on the price level and terms of trade Secondary

Guide to Treatment of Withholding Tax Rates. January 2018

Guide to Treatment of Withholding Tax Rates Contents 1. Introduction 1 1.1. Aims of the Guide 1 1.2. Withholding Tax Definition 1 1.3. Double Taxation Treaties 1 1.4. Information Sources 1 1.5. Guide Upkeep

Guide to Treatment of Withholding Tax Rates Contents 1. Introduction 1 1.1. Aims of the Guide 1 1.2. Withholding Tax Definition 1 1.3. Double Taxation Treaties 1 1.4. Information Sources 1 1.5. Guide Upkeep

Total Imports by Volume (Gallons per Country)

") 10/5/2018 Imports by Volume (Gallons per Country) YTD YTD Country 08/2017 08/2018 % Change 2017 2018 % Change MEXICO 67,180,788 71,483,563 6.4 % 503,129,061 544,043,847 8.1 % NETHERLANDS 12,954,789 12,582,508

10/5/2018 Imports by Volume (Gallons per Country) YTD YTD Country 08/2017 08/2018 % Change 2017 2018 % Change MEXICO 67,180,788 71,483,563 6.4 % 503,129,061 544,043,847 8.1 % NETHERLANDS 12,954,789 12,582,508

Total Imports by Volume (Gallons per Country)

") 11/2/2018 Imports by Volume (Gallons per Country) YTD YTD Country 09/2017 09/2018 % Change 2017 2018 % Change MEXICO 49,299,573 57,635,840 16.9 % 552,428,635 601,679,687 8.9 % NETHERLANDS 11,656,759 13,024,144

11/2/2018 Imports by Volume (Gallons per Country) YTD YTD Country 09/2017 09/2018 % Change 2017 2018 % Change MEXICO 49,299,573 57,635,840 16.9 % 552,428,635 601,679,687 8.9 % NETHERLANDS 11,656,759 13,024,144

Generating Government Revenue from the Sale of Oil and Gas: New Data and the Case for Improved Commodity Trading Transparency

Briefing January 2018 Generating Government Revenue from the Sale of Oil and Gas: New Data and the Case for Improved Commodity Trading Transparency Alexander Malden and Joseph Williams SUMMARY This briefing

Briefing January 2018 Generating Government Revenue from the Sale of Oil and Gas: New Data and the Case for Improved Commodity Trading Transparency Alexander Malden and Joseph Williams SUMMARY This briefing

Total Imports by Volume (Gallons per Country)

") 12/6/2018 Imports by Volume (Gallons per Country) YTD YTD Country 10/2017 10/2018 % Change 2017 2018 % Change MEXICO 56,462,606 60,951,402 8.0 % 608,891,240 662,631,088 8.8 % NETHERLANDS 11,381,432 10,220,226

12/6/2018 Imports by Volume (Gallons per Country) YTD YTD Country 10/2017 10/2018 % Change 2017 2018 % Change MEXICO 56,462,606 60,951,402 8.0 % 608,891,240 662,631,088 8.8 % NETHERLANDS 11,381,432 10,220,226

Total Imports by Volume (Gallons per Country)

") 2/6/2019 Imports by Volume (Gallons per Country) YTD YTD Country 11/2017 11/2018 % Change 2017 2018 % Change MEXICO 48,959,909 54,285,392 10.9 % 657,851,150 716,916,480 9.0 % NETHERLANDS 11,903,919 10,024,814

2/6/2019 Imports by Volume (Gallons per Country) YTD YTD Country 11/2017 11/2018 % Change 2017 2018 % Change MEXICO 48,959,909 54,285,392 10.9 % 657,851,150 716,916,480 9.0 % NETHERLANDS 11,903,919 10,024,814

Hundred and Seventy-fifth Session. Rome, March Status of Current Assessments and Arrears as at 31 December 2018

February 2019 E FINANCE COMMITTEE Hundred and Seventy-fifth Session Rome, 18-22 March 2019 Status of Current Assessments and Arrears as at 31 December 2018 Queries on the substantive content of this document

February 2019 E FINANCE COMMITTEE Hundred and Seventy-fifth Session Rome, 18-22 March 2019 Status of Current Assessments and Arrears as at 31 December 2018 Queries on the substantive content of this document

Total Imports by Volume (Gallons per Country)

") 2/6/2018 Imports by Volume (Gallons per Country) YTD YTD Country 12/2016 12/2017 % Change 2016 2017 % Change MEXICO 50,839,282 54,169,734 6.6 % 682,281,387 712,020,884 4.4 % NETHERLANDS 10,630,799 11,037,475

2/6/2018 Imports by Volume (Gallons per Country) YTD YTD Country 12/2016 12/2017 % Change 2016 2017 % Change MEXICO 50,839,282 54,169,734 6.6 % 682,281,387 712,020,884 4.4 % NETHERLANDS 10,630,799 11,037,475

Total Imports by Volume (Gallons per Country)

") 3/6/2019 Imports by Volume (Gallons per Country) YTD YTD Country 12/2017 12/2018 % Change 2017 2018 % Change MEXICO 54,169,734 56,505,154 4.3 % 712,020,884 773,421,634 8.6 % NETHERLANDS 11,037,475 8,403,018

3/6/2019 Imports by Volume (Gallons per Country) YTD YTD Country 12/2017 12/2018 % Change 2017 2018 % Change MEXICO 54,169,734 56,505,154 4.3 % 712,020,884 773,421,634 8.6 % NETHERLANDS 11,037,475 8,403,018

Total Imports by Volume (Gallons per Country)

") 6/6/2018 Imports by Volume (Gallons per Country) YTD YTD Country 04/2017 04/2018 % Change 2017 2018 % Change MEXICO 60,968,190 71,994,646 18.1 % 231,460,145 253,500,213 9.5 % NETHERLANDS 13,307,731 10,001,693

6/6/2018 Imports by Volume (Gallons per Country) YTD YTD Country 04/2017 04/2018 % Change 2017 2018 % Change MEXICO 60,968,190 71,994,646 18.1 % 231,460,145 253,500,213 9.5 % NETHERLANDS 13,307,731 10,001,693

INTERNATIONAL CONVENTION ON STANDARDS OF TRAINING, CERTIFICATION AND WATCHKEEPING FOR SEAFARERS (STCW), 1978, AS AMENDED

, 1978, AS AMENDED") E 4 ALBERT EMBANKMENT LONDON SE 7SR Telephone: +44 (0)20 7735 76 Fax: +44 (0)20 7587 320 MSC./Circ.64/Rev.5 7 June 205 INTERNATIONAL CONVENTION ON STANDARDS OF TRAINING, CERTIFICATION AND WATCHKEEPING

E 4 ALBERT EMBANKMENT LONDON SE 7SR Telephone: +44 (0)20 7735 76 Fax: +44 (0)20 7587 320 MSC./Circ.64/Rev.5 7 June 205 INTERNATIONAL CONVENTION ON STANDARDS OF TRAINING, CERTIFICATION AND WATCHKEEPING

Income Tax Issues and Fiscal Stability

Colombia: FAD Conference Emil M. Sunley Fiscal Affairs Department International Monetary Fund Income Tax Issues and Fiscal Stability Bogotá, Colombia, September 30, 2015 Overview Income Tax Corporate tax

Colombia: FAD Conference Emil M. Sunley Fiscal Affairs Department International Monetary Fund Income Tax Issues and Fiscal Stability Bogotá, Colombia, September 30, 2015 Overview Income Tax Corporate tax

The Budget of the International Treaty. Financial Report The Core Administrative Budget

The Budget of the International Treaty Financial Report 2016 The Core Administrative Budget Including statements of amounts due and received for The Working Capital Reserve and The Third Party Beneficiary

The Budget of the International Treaty Financial Report 2016 The Core Administrative Budget Including statements of amounts due and received for The Working Capital Reserve and The Third Party Beneficiary

Total Imports by Volume (Gallons per Country)

") 1/5/2018 Imports by Volume (Gallons per Country) YTD YTD Country 11/2016 11/2017 % Change 2016 2017 % Change MEXICO 50,994,409 48,959,909 (4.0)% 631,442,105 657,851,150 4.2 % NETHERLANDS 9,378,351 11,903,919

1/5/2018 Imports by Volume (Gallons per Country) YTD YTD Country 11/2016 11/2017 % Change 2016 2017 % Change MEXICO 50,994,409 48,959,909 (4.0)% 631,442,105 657,851,150 4.2 % NETHERLANDS 9,378,351 11,903,919

Switzerland Country Profile

Switzerland Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Switzerland EU Member State No. Please note that, in addition to Switzerland

Switzerland Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Switzerland EU Member State No. Please note that, in addition to Switzerland

Resolution adopted by the General Assembly on 24 December [on the report of the Fifth Committee (A/67/502/Add.1)]

![Resolution adopted by the General Assembly on 24 December [on the report of the Fifth Committee (A/67/502/Add.1)]](/thumbs/94/119685248.jpg "Resolution adopted by the General Assembly on 24 December [on the report of the Fifth Committee (A/67/502/Add.1)]") United Nations General Assembly Distr.: General 11 February 2013 Sixty-seventh session Agenda item 134 Resolution adopted by the General Assembly on 24 December 2012 [on the report of the Fifth Committee

United Nations General Assembly Distr.: General 11 February 2013 Sixty-seventh session Agenda item 134 Resolution adopted by the General Assembly on 24 December 2012 [on the report of the Fifth Committee

COUNCIL. Hundred and Fifty-sixth Session. Rome, April Status of Current Assessments and Arrears as at 17 April 2017.

April 2017 CL 156/LIM/2 Rev.1 E COUNCIL Hundred and Fifty-sixth Session Rome, 24-28 April 2017 Status of Current Assessments and Arrears as at 17 April 2017 Executive summary The document presents the

April 2017 CL 156/LIM/2 Rev.1 E COUNCIL Hundred and Fifty-sixth Session Rome, 24-28 April 2017 Status of Current Assessments and Arrears as at 17 April 2017 Executive summary The document presents the

Managing Nonrenewable Natural Resources

International Monetary Fund Managing Nonrenewable Natural Resources Vitor Gaspar Fiscal Affairs Department Third IMF Statistical Forum: Official Statistics to Support Evidence-Based Policy-Making Frankfurt,

International Monetary Fund Managing Nonrenewable Natural Resources Vitor Gaspar Fiscal Affairs Department Third IMF Statistical Forum: Official Statistics to Support Evidence-Based Policy-Making Frankfurt,

IMPENDING CHANGES. Subsistence Allowances

IMPENDING CHANGES Subsistence Allowances This document serves to keep stakeholders informed of impending changes regarding the amount of a subsistence allowance deemed to have been expended in terms of

IMPENDING CHANGES Subsistence Allowances This document serves to keep stakeholders informed of impending changes regarding the amount of a subsistence allowance deemed to have been expended in terms of

APA & MAP COUNTRY GUIDE 2017 CANADA

APA & MAP COUNTRY GUIDE 2017 CANADA Managing uncertainty in the new tax environment CANADA KEY FEATURES Competent authority APA provisions/ guidance Types of APAs available APA acceptance criteria Key

APA & MAP COUNTRY GUIDE 2017 CANADA Managing uncertainty in the new tax environment CANADA KEY FEATURES Competent authority APA provisions/ guidance Types of APAs available APA acceptance criteria Key

Hundred and Sixty-ninth Session. Rome, 6-10 November Status of Current Assessments and Arrears as at 30 June 2017

August 2017 FC 169/INF/2 E FINANCE COMMITTEE Hundred and Sixty-ninth Session Rome, 6-10 November 2017 Status of Current Assessments and Arrears as at 30 June 2017 Queries on the substantive content of

August 2017 FC 169/INF/2 E FINANCE COMMITTEE Hundred and Sixty-ninth Session Rome, 6-10 November 2017 Status of Current Assessments and Arrears as at 30 June 2017 Queries on the substantive content of

Financial Accounting Advisory Services

Financial Accounting Advisory Services May 2013 Agenda About EY 3 5 Appendix 13 Contacts 15 Page 2 About EY Page 3 EMEIA Sub-areas Africa Angola, Botswana, Republic of Congo, Equatorial Guinea, Ethiopia,

Financial Accounting Advisory Services May 2013 Agenda About EY 3 5 Appendix 13 Contacts 15 Page 2 About EY Page 3 EMEIA Sub-areas Africa Angola, Botswana, Republic of Congo, Equatorial Guinea, Ethiopia,

COUNCIL. Hundred and Sixtieth Session. Rome, 3-7 December Status of Current Assessments and Arrears as at 26 November 2018 EXECUTIVE SUMMARY

November 2018 CL 160/LIM/2 E COUNCIL Hundred and Sixtieth Session Rome, 3-7 December 2018 Status of Current Assessments and Arrears as at 26 November 2018 EXECUTIVE SUMMARY The document presents the Status

November 2018 CL 160/LIM/2 E COUNCIL Hundred and Sixtieth Session Rome, 3-7 December 2018 Status of Current Assessments and Arrears as at 26 November 2018 EXECUTIVE SUMMARY The document presents the Status

Non-resident withholding tax rates for treaty countries 1

Non-resident withholding tax rates for treaty countries 1 Country 2 Interest 3 Dividends 4 Royalties 5 Annuities 6 Pensions/ Algeria 15% 15% 0/15% 15/25% Argentina 7 12.5 10/15 3/5/10/15 15/25 Armenia

Non-resident withholding tax rates for treaty countries 1 Country 2 Interest 3 Dividends 4 Royalties 5 Annuities 6 Pensions/ Algeria 15% 15% 0/15% 15/25% Argentina 7 12.5 10/15 3/5/10/15 15/25 Armenia

Mining in APEC Economies: Opportunities and Challenges

05/SOM/MTF/05 Agenda Item: 6 Mining in APEC Economies: Opportunities and Challenges Purpose: Information Submitted by: ABAC 9 th Mining Task Force Meeting Cebu, Philippines 6-7 August 05 Mining in APEC

05/SOM/MTF/05 Agenda Item: 6 Mining in APEC Economies: Opportunities and Challenges Purpose: Information Submitted by: ABAC 9 th Mining Task Force Meeting Cebu, Philippines 6-7 August 05 Mining in APEC

Legal Indicators for Combining work, family and personal life

Legal Indicators for Combining work, family and personal life Country Africa Algeria 14 100% Angola 3 months 100% Mixed (if necessary, employer tops up social security) Benin 14 100% Mixed (50% Botswana

Legal Indicators for Combining work, family and personal life Country Africa Algeria 14 100% Angola 3 months 100% Mixed (if necessary, employer tops up social security) Benin 14 100% Mixed (50% Botswana

Evaluating and Comparing Fiscal Regimes for EI

Evaluating and Comparing Fiscal Regimes for EI NATURAL RESOURCE TAXATION IN THE ASIA-PACIFIC REGION A forum on the design, implementation and evaluation of fiscal regimes for extractive industries Jakarta,

Evaluating and Comparing Fiscal Regimes for EI NATURAL RESOURCE TAXATION IN THE ASIA-PACIFIC REGION A forum on the design, implementation and evaluation of fiscal regimes for extractive industries Jakarta,

Note on Revisions. Investing Across Borders 2010 Report

Note on Revisions Last revision: August 30, 2011 Investing Across Borders 2010 Report This note documents all data and revisions to the Investing Across Borders (IAB) 2010 report since its release on July

Note on Revisions Last revision: August 30, 2011 Investing Across Borders 2010 Report This note documents all data and revisions to the Investing Across Borders (IAB) 2010 report since its release on July