Secret to Our Success

|

|

|

- Mervyn Gardner

- 5 years ago

- Views:

Transcription

1 UNDERSTANDING THEIRS TRANSCRIPT Patti Logan, EA Secret to Our Success The law Procedures (IRM) Client s own info Info IRS has on our client History Various transcripts 1

2 IRC 6103 Provides circumstances when information may be disclosed Return information includes: tax return information & the files and information collected, recorded by, prepared by, furnished to the Secretary with respect to a return or determination of the existence of a return Includes background information associated directly with a particular taxpayer IRC 6103 IRC 6103(e) allows that information may be disclosed d to the taxpayer if the request is made in writing. Including: Name, address and identifying number of the taxpayer, A description of the information requested, including the type of tax and taxable period, and Sufficient evidence to establish that the requester is entitled to receive the requested information. 2

3 IRC 6103 If the request is verbal IRS must ask sufficient questions and receive sufficient responses to make sure the requestor is the taxpayer. IRM suggests: Taxpayer's name as it appears on the tax return, Taxpayer's address as it appears on the tax return or as modified on IRS records, Taxpayer's SSN or EIN, In the case of refund inquiry, the type of tax, the approximate amount of expected refund d( (unless computed by IRS); and the place of filing, For a matter involving 1040return, the date of birth and/or filing status, and/or Other unique identifier issued by the IRS. Delegation Order 11 2 DO 11 2 authorizes IRS employees to disclose information to taxpayers and their representatives to the extent necessary to perform their official duties. In conjunction with a case assigned to them, employee has the authority to disclose information Once case is closed, information must be requested through FOIA 3

4 WHAT KINDS OF INFORMATION ARE AVAILABLE? Copies of employee s histories and documentation. Electronic records Account records How do you get a copy? Practitioner Priority Service Employee assigned the case ACS (???????) Speak to a manger All else fails, contact the DO disclosure officer COMPUTER DEFINITIONS Masterfile System is the main IRS system to store data IMF Individual master file BMF Business master file CADE2 Customer Account Data Engine. Will ultimately replace the Masterfile for IMF IDRS Integrated t ddt Data Rti Retrieval lsystem flows into the Master file ALS Automated lien system Page 2 4

5 Definitions Non Masterfile (NMF) certain transactions do not fit with the masterfile: Formerly on ledger cards now automated Literal transcript (taxpayer friendly) is available Toll free for NMF Letter N following ID number. Refer to the entire number when talking to IRS Non Masterfile (NMF) Basic conditions requiring NMF Large $ accounts $1 billion and over Overflow accounts excessive amount of transactions New Legislation that need immediate tax law implementation where extensive modifications to the masterfile are needed Immediate legal assessments (assessment required within 24 hours) Reversal of erroneous abatements when ASED would expire Child Support cases that have fallen into arrears 5

6 Definitions Page 4 ACS Automated Collection System (Automated t CllSit Call Site) First level of collection action after notices Split screen between ACS and IDRS Can levy with push of a button History annotated with in house abbreviations Major actions go onto IDRS Definitions ICS (Integrated Collection System) computerized dthe field revenue officer. Exam System includes Q & A for interviewing the taxpayer Transaction codes are three digit numbers that indicate actions and history ofthe taxpayer and the specific types of tax. Often needs additional explanation codes 6

7 Definitions Closing Codes and Action Codes supplemental lcodes that t work in conjunction with transaction codes. Designated Payment Codes identify types of payments Disposal Codes indicates how an examination was closed Definitions Transcripts of Accounts MFTRX or literal l version of masterfile CP Notices IDRS generated letter. Example CP 2000 Command Codes: (CC) are computer words that tell the computer what information to pull up. MFTRA which hwe use for ordering the IRS history of an account is actually a command code. 7

8 Definitions Unpostable Transactions that can not be applied to the account. A technician i must manually review the unpostables to identify the problem Pending Transactions A transaction is input to IDRS, the next week it goes to the master file. Until it is posted to masterfile, the transaction stays pending on IDRS Definitions Penalty Codes One transaction code indicates a civil iilpenalty but requires a penalty code to describe which penalty (Desk Guide pg 24) Reference numbers Some transactions require a reference number. The penalty code is an example (Desk Guide pg 24) 8

9 Definitions TIN Taxpayer Identification Number Cycle IRS uses cycle numbers to date when transactions are posted. Cycle number YYYYCC Example CADE adds day of week of 08 EX: means cycle 19 of Generally 19 th week of 2011 Cycle calendars are available Chapter 16 of ADP book on page 61 of Quick Desk Guide. Definitions DLN Document Locator Number is assigned to every return or document tinput tthrough h ADP system (including electronic docs). DLN controls, identifies and locates documents Doc Code Document Code identifies the specific type of return or document filed or processed 9

10 Definitions File Source One digit code following the TIN. Examples: Blank: Valid SSN or EIN *: Invalid SSN on IMF V: Valid SSN on BMF W: Invalid SSN on BMF D: Temporary TIN P: Valid EPMF EIN N: Non master file Definitions File Source Continued: Second type of file source indicates on which h masterfile account the information is housed. B: BMF (Business master file) I: IMF (Individual master file) N: NMF (Non master file) E: EPMF (Employee plan master file) 10

11 Definitions Financial Management Service a bureau of the Treasury Department Provides central payment services to Federal Program Agencies Government collections & deposits Provides government wide accounting and reporting Collects delinquent dli db debt owed to the government FMS 13 is the Authorization for Release of Information ( Command Codes IRM Part 2 has list of command codes. MFTRA Complete transcript of account. Written in code and numbers. Must use the ADP Book, Document 6209 Types of MFTRA: MFTRAX Literal transcript with limited information MFTRAE Entity information MFTRAC Complete information on all accounts under one TIN 11

12 MFTRA continued: Command Codes MFTRAY All BMF Tax Modules for one year. MFTRAU Numident transcript contains SSA info MFTRAJ Form 4340 Certificate of Assessments TxMOD Transcript shows what is on the service center IDRS computer. Differs form MFTRA because has SC history. Page 8 Command Codes Pinex Explains penalty and interest calculations to the taxpayer INTST Calculates penalties and interest to a specific date (Internal use) INTSTD Gives a detailed computation of penalties and interest. Can be given to taxpayer COMPA Causes IRS to compute interest for specified amount for a specified period of time 12

13 Command Codes RTVUE and BRTVU Provides online access to recently filed returns. Much hlike 1040PC. Shows return as filed Provides Line items transcribed Edited or verified fields Accompanying schedules for current year and two prior Command Codes Page 9 RTFTP provides sanitizes taxpayer version of RTVUE that includes no IRS edited data IRP (Information Reporting Program) contains all 1099, 1098 and W 2info by. The IRP info can take as much as 6 weeks to request. Very similar to Wage and Income Transcript from E services SUPOL Accesses national database of potentially delinquent inquiry (non filers). Contains IRP documents. Additional info added in May of each year. Total of 6 year will be available when database is completed. 13

14 Command Codes URINQ (Unidentified Remittance Inquiry) info is input tto the file when IRS cannot identify where a payment should be posted. SUMRY Shows every account under a TIN that is on IDRS and the status. Shows: Collection status codes, and Unpaid balance of assessment per period Filing requirements Command Codes STAUP This allows IRS to put a hold on an account for a certain ti number of cycles or move the account to another notice or status. ENMOD This gives entity information by TIN. Gives history of addresses and cycle address change is input. TXMOD shows the cycle a notice is sent out. Applying ENMOD will tell the address in IDRS for that cycle. 14

15 Command Codes LEVYS indicates levy sources on the computer. Automated Collection System (ACS) Integrated Collection System Revenue Officer s collection system Automated Lien System Handles lien inventory, generates new liens, releases liens. IDRS Based in service centers input terminals at district, area and centers. Automated Exam System (AIMS) Controls Exam inventory giving location & status Masterfile System Located in Martinsburg WV, houses all returns filed. Usually maintained for 6 years then sent to retention register which means they must be called back to be reviewed. Page 11 15

16 Transaction Codes (Partial) TC: Explanation TC Explanation 150 Return assessed 270 Failure to pay penalty (MANUAL) 166 Delinquent return penalty 290 Additional tax assessed 170 ES tax penalty 300 Examination tax assessment 171 Abate ES tax penalty 301 Abate prior tax assessment 180 Deposit (FTD) penalty 480 OIC pending 181 Abate FTD penalty 481 OIC Rejected 196 Generated Assessed Interest 482 OIC Withdraws Pages 12 & 13 TC 971 (Partial) AC: Explanation 13 Delinquent return after SFR 43 TP proposed installment agreement 63 Installment agreement approved 69 CDP notice was issued to the taxpayer 69 & 66 CDP notice was handed to the taxpayer, not mailed 71 Innocent spouse claim 72 Return was inspected as part of a package audit and accepted as filed. 163 Defaulted installment agreement 16

17 Fixing America s Surface Transportation Act (FAST) Gives IRS the mandate to notify the State Dept when: A taxpayer is seriously delinquent (owes $50K or more). IRS first step is to put a TC 971 AC 640 which shows that a levy has been issued or A lien has been filed and No installment agreement or OIC approved & Not in a CDP for a proposed levy or Innocent Spouse election made under IRC 6015 (b), (c) or (f) Page 14 Fixing America s Surface Transportation Act (FAST) Once these criteria are met: IRS notifies State Department AND taxpayer (nothing says POA) State will revoke passport, MAY deny an application If passport p is revoked while out of country State will issue a temporary passport May take the issue to Court 17

18 Fixing America s Surface Transportation Act (FAST) TC971 AC 640 shows on the literal transcript as Initial Levy issued Means only that a levy has previously been issued on this particular account Will show up even if the account is less than $50, Document Locator Number (DLN) 1 & & 5 6, 7 & 8 9, 10 & & & 2 File Locator Numbers indicating where generated 3 Tax class (See Quick Guide) Identifies type of tax 4 & 5 Doc code Differentdoc codes for different actions 6,7,8 Julian Date 9, 10, 11 Block Series Indicates where file is locate 12 & 13 Serial number up to 100 in each block 14 List year 18

19 Service Center/District Office Codes 04 New England 28 Philadelphia SC 54 Virginia/W. VA 77 Central CA 06 Connecticut/RI 29 Ogden SC 56 North/S Carolina 84 Rocky Mountain 07 Atlanta SC 31 Ohia 58 Georgia 86 Southwest 08 Andover SC 33 Southern Calif 59 Florida 89 Fresno SC 09 Kansas City SC 35 Indiana 62 Kentucky/Tennessee 90 Detroit Computing Ctr 11 Brooklyn 36 Illinois 65 South Florida 91 Pacific Northwest 13 Manhattan NY 38 Michigan 66 Puerto Rico 94 Northern CA 16 Upstate NY 39 Midwest 72 Gulf Coast 95 Los Angeles 18 Austin SC 41 North Central 73 Ark./Oklahoma 98 A/C International 19 Brookhaven SC 43 Kansas/MO 74 South Texas 22 New Jersey 49 Memphis SC 75 North Texas 23 Pennsylvania 52 Delaware/MD 76 Houston Electronic Filing Codes 14 BMF Form 1065 Andover SC 16 IM F and BMF Doc codes 19 & 35 Andover SC 41 BMF (1986, 1987 and 1988 only) Andover SC 65 IMF Atlanta SC 76 & 75 IMF Austin SC 22 IMF Brookhaven SC 38 & 35 IMF Cincinnati SC 99 IMF Fresno SC 43 IMF Kansas City SC 72 & 64 IMF Memphis SC 93 IMF Ogden SC IMF & BMF Philadelpha SC 19

Odgen SC 98 (Intl) Returns filed with F2555 (Foreign earned income) Example: DLN 55211 110 036SS 4 indicates an electronic return filed in Cincinnati SC Page 20 MFTRX Literal Transcript")

20 IMF Electronically Filed Returns # in parentheses is used when maximum daily processed is reached with first number 16 (44) Andover SC 76(75) Austin SC 55(35) Cincinnati SC 72(64) Memphis SC 93(92) Odgen SC 98 (Intl) Returns filed with F2555 (Foreign earned income) Example: DLN SS 4 indicates an electronic return filed in Cincinnati SC Page 20 MFTRX Literal Transcript Page 19 20

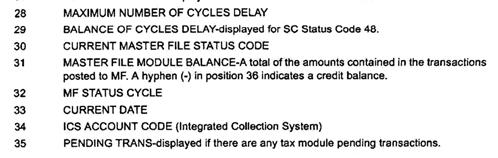

21 MFTRX Continued TXMOD Sections Entity Section includes #1 Current assignment CAF indicators Lien indicator ASED CSED Refund statute date Current control information 21

22 TXMOD Entity Section Transaction information Posted return information Return transactions Posted Transactions Notice Section Type of Notice Amount of notice Cycle Number Suppression codes Case Control Status History TXMOD Sections 22

23 TXMOD Top of Page 21 Return Info TC AC TXMOD Control Section History Status Bottom Page 23 23

24 TXMOD Section Case Control & History Section Who controlled the case Action dates Assignment Minimal case history Status History SC Collection status history MF Collection status history TXMOD SC Status Continued Case control Masterfile history Top Page 24 24

25 TXMOD Service Center Status Service Center History Bottom of page 24 TXMOD Heading Section 25

26 TXMOD Header Key From ADP PG 25 TXMOD Header Key From ADP PG 25 26

27 TXMOD Header Key From ADP PG 26 TXMOD Header Key From ADP 27

28 TXMOD Header Key From ADP PG 29 TXMOD Header Key From ADP PG 29 28

29 TXMOD Transactions Page 30 TXMOD Transaction Key Pg 30 29

30 TXMOD Transaction Key Pg 31 TXMOD Transaction Key Pg 31 30

31 Enmod Provides entity information Addresses Filing requirements Any change in overall entity information SUPOL Provides information on taxpayer s dli delinquency status tt Includes CTR (Currency Transaction Report) document SUPOL will NOT: Provide income information prior to FY 90 Be updated once IRP data is online Aid in resolving CP

32 SUPOL Corporate Files On line (CFOL) CFOL allows other offices to view service center info, nationwide Like Masterfile, pending and unpostable transactions do not show but is available on IDRS BMFOL: Provide information like MFTRA Displays additional assessment transactions and abatements Allows research of Txmods that are in retention 32

33 BRTVU Provides a display of the transcribed line items on all business tax returns and their accompanying schedules or forms as the returns are processed at the Campus. It is used by IRS in lieu of ordering the paper return Current processing year plus 3 prior years are available. Displays delinquent and amended returns DDBOL Dependent Database On line Allows IDRS users to access the dependent database. Retrieves EITC and dependent issues generated from 1040 return Provides the SSN for the EITC child Provides SSN for the dependent child used for an exemption Provides the SSN for the child used for child tax credit Provides the SSN for the child used for the child care credit Also shows the SSN for the custodial parent for each dependent Shows the citizenship code. 33

34 More CFOL DUPOL Duplicate TIN Database Used to research fraudulent use of SSN s in both paper and electronically filed returns IMFOL Individual Masterfile on line provides read only access to IMF when IDRS shows no data. National access provides: Entity info Posted returns General tax data Status hisotry Adjustment and audit history for specific SSNs Page 41 More CFOL INOLE displays entity data for all masterfiles, SSA and cross ref data for any specified TIN Masterfile data obtained from IMF BMF Business return transaction file Information Return Masterfile Payer Masterfile Employee plans Masterfile Debtor Masterfile 34

35 It provides: INOLE Continued Filing status SSA information IMF prior namelines Date of birth and date of death Primary taxpayer nameline Cross referenced tax ID numbers when primary TIN is known More CFOL PMFOL provides information from Payer Mastefile. Shows: All sources of income and amounts Withholdings The number of documents filed by the payer as shown on 1096 Civil penalties associated with each of these document types 35

36 More CFOL RTVUE provides line items transcribed from 1040 (BRTVEfor BMF). Used in lieu of ordering paper return. Available for current year plus three prior years RPVUE Easy access to the Preparer Listing information extracted from BMF and IMF returns. Identifies suspect return preparers. p Summary screen shows Preparer info Number & percentage of refunds and EITC More CFOL SPARQ designed to research a more current address for a former spouse. Cross reference info from National Account Profile 36

37 More CFOL Third Party Contact System (TPCIN & TPCOL) designed to maintain a database of all third party contacts that were made regarding a taxpayer during the determination or collection of a tax liability. Contains all data related to: IMF BMF Non masterfile Retirement accounts Exempt accounts Review Quick Desk Guide 37

38 Using the Internal Transcripts Calculating statutes to check IRS date Audit reconsiderations Court Cases Missing payments Determining the closing code when an account is reported as currently uncollectible Return Codes MFT Masterfile Transaction indicates the type of return MFT 30 Form 1040 MFT 01 Form 941 MFT MFT MFT 55 Civil il Penalty Period: YYYYMM So a 1040 filed for 2016 is If you saw MFT what would that be? 38

39 Transaction Codes TC Code: File Description 000 I/B/E Establish an account 001 I/B/E Resequence an account 002 E Resequence EPMF merge fail 003 B Duplicate tax modules are not resequenced 004 B BMF partial merge 005 I/B Resequenced account for merge 006 I/B/E Account resequenced to master file location Guide pg 1 18 For More Info See: 007 I/B Carrier transaction 008 I/B IMF/BMF Complete Merge Section 14.7 Problem page 36 TC Posted Trans Amt Cyc DLN WH TX Cr Posted w/rtn See page 4 of QRG: What can you tell from the above? What do the TCs tell you? What does the DLN tell you? 39

40 Answers to Questions What can you tell from the above? The return was assessed 6/6/2004 What do the TCs tell you? TCs tell you that the withholding was not as much as the tax due ($3,950) What does the DLN tell you? The return was filed with the Austin SC (pg 17 of handout What does this tell you TC Posted Trans Amt Cyc DLN Regular Lien What actions were taken on this account? What does the DLN on the TC 582 tell us? 40

41 What does this tell you What actions were taken on this account? Penalties and interest twas assessed (TC 276 & 196) A Notice of Federal Tax Lien was filed. What does the DLN on the TC 582 tell us? A Notice of Federal Tax Lien was filed by Dallas office (DLN starts with 18 See page 17 of handout) Txmoda Shows: TC Posted Trans Amt Cyc DLN CD> CD> MF CAF CD>252 Overall what due these codes tell us? Hint Pg of QRG 41

42 TC Posted Trans Amt Cyc DLN CD> CD> MF CAF CD>252 TC 971 AC 063 Taxpayer entered an installment agreement TC 971 AC 262 Maximum failure to pay assessed TC 960 POA filed on account TC 971 AC 252 Lien CDP Notice was sent to taxpayer What does the following tell us? CD> CD> CD> CD DPC>99 TC 971 AC 253 CDP notice of filing a lien was undelivered. TC 971 AC 611 Third party contact was made by the IRS TC 971 AC 061 Module was blocked/released from Federal Payment Levy Program TC 971 AC 163 Out of installment agreement status TC 670 Payment was made 42

43 What does the following tell us? CD> CD> CD> CD DPC>99 Other important Codes: Before we see a TC 670 with a DPC (Designated payment code Pg 59 QRG) of 05 What must we see to know the IRS did their job? TC 971 AC 069 TC 971 AC 104 TC 971 AC

44 Other important Codes: Before we see a TC 670 with a DPC (Designated payment code) d) of 05 What must we see to know the IRS did their job? TC 670 DPC 05 Levy Served TC 971 AC 069 Due process was issued TC 971 AC 104 Innocent spouse case TC 971 AC 120 Amended return/claim Client says the never received an adjustment notice for TXMOD indicates: TC Posted Trans-Amt , , , , AC> , DISP CD>061 What does the TC 971 AC>139 tell you? How about the TC 290 DISP 10? What action could you then take? 44

45 Client says the never received an adjustment notice for TXMOD indicates: TC Posted Trans-Amt , , , , AC> , DISP CD>061 What does the TC 971 AC>139 tell you? AUR soft notice issued How about the TC 290 DISP 10? TP didn t appeal to USTC or sign agreement. What action could you then take? Amended return or request audit reconsideration TC 59X Closing Codes Guide pg TC 590 Not liable this tax period. Satisfies this module only TC 591 No Longer Liable for tax. Satisfies this module and all subsequent modules for same MFT if not already delinquent TC 593 Unable to locate taxpayer Satisfies this module and all subsequent modules for same MFT. 45

46 TC 59X Closing Codes TC 594 Return previously filed. Satisfies this module only. TC 595 Referred to Exam TC 596 Referred to CI TC 597 Surveyed by National Office direction only TC 598 Shelved by National Office direction only TC 599 Return secured. Satisfied this Module only TC 59X Closing Codes CSCO=Compliance Service Collections Operations AM= Accounts Maintenance FA=Field Assistance ACS= Automated Collection System CFf=Collection Field function AIQ=Advisory Closing Code Description TC 590 Not Liable Used By: 01 Not liable for annual return (short period return posted) CSCO/AM 20 Not liable for this period FA 21 Not liable for this period as income below filing requirement FA 27 No return secured this period. Little or no tax due ACS 28 No return secured this period as TP due a refund ACS 54 Not liable this period CFf/AIQ 63 Not liable this period after 6020(b) or SFR CFf/AIQ 46

47 Closing Code: Transaction Code 530 Closing Codes Condition Guide pg Unable to locate 12 Unable to contact 24 Unable to pay, follow up if TPI of subsequent return is $20,000 or more 25 Unable to pay, follow up if TPI of subsequent return is $28,000 or more 26 Unable to pay, follow up if TPI of subsequent return is $36,000 or more 27 Unable to pay, follow up if TPI of subsequent return is $44,000 or more 28 Unable to pay, follow up if TPI of subsequent return is $52,000 or more 29 Unable to pay, follow up if TPI of subsequent return is $60,000 or more 30 Unable to pay, follow up if TPI of subsequent return is $68,000 or more 31 Unable to pay, follow up if TPI of subsequent return is $76,000 or more 32 Unable to pay, follow up if TPI of subsequent return is $84,000 or more IRC PENALTY REFERENCE NUMBERS MISCELLANEOUS CIVIL PENALTIES PRN TYPE OF PENALTY & RATE INFORMATION 6652(d)(1) 165 Failure to file Annual Registration and other pension plan Missing or incorrect TIN penalty 503 Improper Format penalty 6694(b) 650 Preparer s Willful or Reckless Conduct Trust Fund Recovery Penalty adjustment to balance due by a Related Trust Fund Recover Penalty Taxpayer payment or reversal of payment Guide pg

48 TC 520 CLOSING CODE CHART Closing Code IDRS Status Definition CSED Suspended Bankruptcy Yes Litigation No 71 No change Refund litigation No CDP Lien Yes CDP Levy Yes Guide pg 31 Action Code TC 971 Action CODE CHART Definition Guide pg TC 150 posted to incorrect TIN/tax period 012 Amended return/claim forwarded to Collection 013 Amended return/claim forwarded to Examination 043 Pending Installment Agreement 063 Identify module as containing an installment agreement 067 Delivery of Due Process Notice was refused or unclaimed 068 Due Process Notice was returned undeliverable 107 Indicates one spouse has requested an installment agreement 252 Lien CDP Notice sent to taxpayer 253 Lien CDP Notice Undelivered 48

49 Form No. CP 2000 Tax Returns and Forms B BMF E EPMF I IMF N NMF Title File Source Tax Class MFT Code Doc. Code Proposed Changes to Income or Withholding Tax I Employer s Quarterly Federal Tax Return B/N 1,*6 01,* U.S. Individual Income Tax Return I/N 2,*6 30,*20 11,12, 21, 22 1,2,3, 3244 Payment Posting Voucher 4,5,6, 7,8,0 17,18 Guide pg Examination Disposal Codes Code Definition 01 No change with adjustments (considered agreed) 02 No change 03 Agreed prior to issuance of 30 day letter 04 Agreed after issuance of 30 day letter 07 Appealed before issuance of 90 day letter 09 Agreed after issuance of 90 day letter Default (considered agreed) when taxpayer fails to appeal to USTC or 10 sign agreement after 90 day ltr Guide pg 59 49

50 Designated Payment Codes DPC DEFINITION 00 Designated payment indicator is not present on posting voucher 01 Payment is to be applied first to the non trust portion of the tax 02 Payment is to be applied first to the trust fund portion of the tax 03 Bankruptcy, undesignated payment 04 Levy on state income tax refund (prior to 7/22/1998) 05 Notice of levy 06 Seizure and sale 07 Federal tax lien 99 Miscellaneous payment other than above Guide pg Code Frequently Used Collection Status Codes Explanation Delinquent return not filed. Collection suspended while examination or criminal investigation review, or until another tax period posts to the 06 Master File. 12 Full Paid-generated in response and/or account is less than tolerance. 21 Return filed and assessed, first notice issued 22 Return filed and assessed; TDA issued ACS, Queue, ICS or paper Return filed and assessed; TDA issued awaiting paper or ICS 24 assignment, queue 53 Currently uncollectible 58 CP 504 Notice issued 64 Defaulted Installment Agreements. 72 Litigation/Suspend TDA Guide pg 61 50

51 Cycle Calendar From ADP Book Quick Guide Pg 62 51

UNDERSTANDING THE IRS TRANSCRIPT. It s not as boring as your might think!

UNDERSTANDING THE IRS TRANSCRIPT It s not as boring as your might think! 1 Disclosure Laws IRC 6103 provides circumstances when IRS may disclose information Tax return info may be disclosed to the taxpayer

UNDERSTANDING THE IRS TRANSCRIPT It s not as boring as your might think! 1 Disclosure Laws IRC 6103 provides circumstances when IRS may disclose information Tax return info may be disclosed to the taxpayer

INTERNAL MANUAL -- PASSPORT CERTIFICATION PROCEDURES

INTERNAL MANUAL -- PASSPORT CERTIFICATION PROCEDURES (Excerpted from IRS Internal Manual. https://www.irs.gov/irm. Both sections below are substantially the same. The first applies to field collection

INTERNAL MANUAL -- PASSPORT CERTIFICATION PROCEDURES (Excerpted from IRS Internal Manual. https://www.irs.gov/irm. Both sections below are substantially the same. The first applies to field collection

Part 5. Collecting Process. Chapter 14. Installment Agreements. Section 1. Securing Installment Agreements Securing Installment Agreements

Part 5. Collecting Process Chapter 14. Installment Agreements Section 1. Securing Installment Agreements 5.14.1 Securing Installment Agreements 5.14.1.1 Overview 5.14.1.2 Installment Agreements and Taxpayer

Part 5. Collecting Process Chapter 14. Installment Agreements Section 1. Securing Installment Agreements 5.14.1 Securing Installment Agreements 5.14.1.1 Overview 5.14.1.2 Installment Agreements and Taxpayer

Internal Revenue Manual Section ( ) First Time Abate (FTA).

First Time Abate (FTA).") CLICK HERE to return to the home page Internal Revenue Manual Section 20.1.1.3.3.2.1 (11-21-2017) First Time Abate (FTA). 1. IRS provides administrative relief from the following penalties if the qualifying

CLICK HERE to return to the home page Internal Revenue Manual Section 20.1.1.3.3.2.1 (11-21-2017) First Time Abate (FTA). 1. IRS provides administrative relief from the following penalties if the qualifying

Section 10. Federal Tax Deposit System

10-1 Section 10. Federal Tax Deposit System 1 General IRM 35(17)0, Federal Tax Deposit System, 3(41)(268)0, FTD processing on SCRIPS and IRM (20)400 FTD Penalties. Under the Federal Tax Deposit System,

10-1 Section 10. Federal Tax Deposit System 1 General IRM 35(17)0, Federal Tax Deposit System, 3(41)(268)0, FTD processing on SCRIPS and IRM (20)400 FTD Penalties. Under the Federal Tax Deposit System,

Table of ContentsTable of Contents

Part 4 Examining Process Chapter 19 Liability Determination IRM 4.19.4 Manual Transmittal 4.19.4 CAWR Reconciliation Balancing Table of ContentsTable of Contents 4.19.4.1 CAWR Overview 4.19.4.1.1 CAP-

Part 4 Examining Process Chapter 19 Liability Determination IRM 4.19.4 Manual Transmittal 4.19.4 CAWR Reconciliation Balancing Table of ContentsTable of Contents 4.19.4.1 CAWR Overview 4.19.4.1.1 CAP-

Section 9 - Notices and Notice Codes

9-1 Section 9 - Notices and Notice Codes 1 Nature of Changes Description Page No. IMF Notice Codes 9-1 Taxpayer Notice Codes 9-13 BMF Math Error Notice Codes 9-107 Refund Deletion Codes 9-123 2 General

9-1 Section 9 - Notices and Notice Codes 1 Nature of Changes Description Page No. IMF Notice Codes 9-1 Taxpayer Notice Codes 9-13 BMF Math Error Notice Codes 9-107 Refund Deletion Codes 9-123 2 General

8-11. Trans Code 150 Debit* (NPJ) DR/CR File Title Valid Doc. Code I/B E/A P. Remarks

DR/CR File Title Valid Doc. Code I/B E/A P. Remarks") 8-11 Trans Code 150 Debit* (NPJ) DR/CR File Title Valid Doc. Code I/B E/A P Return Filed & Tax Liability Assessed 150 I/A Entity Created by TC 150 151 E/A Reversal of TC 150 or 154 152 I/A Entity Updated

8-11 Trans Code 150 Debit* (NPJ) DR/CR File Title Valid Doc. Code I/B E/A P Return Filed & Tax Liability Assessed 150 I/A Entity Created by TC 150 151 E/A Reversal of TC 150 or 154 152 I/A Entity Updated

IRS Updates. Richard Furlong, Jr. Senior Stakeholder Liaison

IRS Updates Richard Furlong, Jr. Senior Stakeholder Liaison South Jersey Working Together Conference June 7, 2018 Estimated Tax Payments: Why Pay As You Go? Steady increase in penalties over the last several

IRS Updates Richard Furlong, Jr. Senior Stakeholder Liaison South Jersey Working Together Conference June 7, 2018 Estimated Tax Payments: Why Pay As You Go? Steady increase in penalties over the last several

Part 5. Collecting Process. Chapter 16. Currently Not Collectible. Section 1. Currently Not Collectible Currently Not Collectible

Part 5. Collecting Process Chapter 16. Currently Not Collectible Section 1. Currently Not Collectible 5.16.1 Currently Not Collectible 5.16.1.1 Currently Not Collectible Overview 5.16.1.2 Currently Not

Part 5. Collecting Process Chapter 16. Currently Not Collectible Section 1. Currently Not Collectible 5.16.1 Currently Not Collectible 5.16.1.1 Currently Not Collectible Overview 5.16.1.2 Currently Not

Field Collection Emphasis

Field Collection Emphasis and how it impacts the tax practitioner community Timothy S. Sherrill North Atlantic Area Director Field Collection June 2018 A presentation for the South Jersey Working Together

Field Collection Emphasis and how it impacts the tax practitioner community Timothy S. Sherrill North Atlantic Area Director Field Collection June 2018 A presentation for the South Jersey Working Together

Gleim EA Review Updates to Part Edition, 1st Printing April 2016

Page 1 of 6 Gleim EA Review Updates to Part 3 2016 Edition, 1st Printing April 2016 NOTE: Text that should be deleted is displayed with a line through it. New text is shown with a blue background. This

Page 1 of 6 Gleim EA Review Updates to Part 3 2016 Edition, 1st Printing April 2016 NOTE: Text that should be deleted is displayed with a line through it. New text is shown with a blue background. This

Intro to Collections

Intro to Collections The Basics of the IRS Collection Process David F. Miles, E.A. August 6, 2013 Lecture Introduction This is an introductory course of IRS collections. The course will cover the fundamentals

Intro to Collections The Basics of the IRS Collection Process David F. Miles, E.A. August 6, 2013 Lecture Introduction This is an introductory course of IRS collections. The course will cover the fundamentals

Introduction to Collections: 9/6/2012. The Basics of the IRS Collections Process

David F. Miles, E.A. is a consultant with 20/20 Tax Resolution, Inc. with 15 years of tax resolution experience. David works nationally as a taxpayer representative focusing on state and IRS collections.

David F. Miles, E.A. is a consultant with 20/20 Tax Resolution, Inc. with 15 years of tax resolution experience. David works nationally as a taxpayer representative focusing on state and IRS collections.

IRS COLLECTION PROCEDURES AND TAXPAYER REMEDIES

IRS COLLECTION PROCEDURES AND TAXPAYER REMEDIES By: Daniel J. Cramer Cramer, Minock & Sweeney, PLC The IRS has broad powers to enforce tax laws and collect outstanding taxes. The most common IRS collection

IRS COLLECTION PROCEDURES AND TAXPAYER REMEDIES By: Daniel J. Cramer Cramer, Minock & Sweeney, PLC The IRS has broad powers to enforce tax laws and collect outstanding taxes. The most common IRS collection

LIST OF SUBSTANTIVE CHANGES AND ADDITIONS Route To: Partners PPC's Guide to Dealing with the IRS Managers. Twenty second Edition (June 2014)

") LIST OF SUBSTANTIVE CHANGES AND ADDITIONS Route To: Partners PPC's Guide to Dealing with the IRS Managers Staff File Twenty second Edition (June 2014) The following are some of the features of this year

LIST OF SUBSTANTIVE CHANGES AND ADDITIONS Route To: Partners PPC's Guide to Dealing with the IRS Managers Staff File Twenty second Edition (June 2014) The following are some of the features of this year

Name c/o Address City, postal code 95XXX CALIFORNIA

Name c/o Address City, postal code 95XXX CALIFORNIA Certified Mail Ref.# 7002 2030 0003 XXXX XXXX (Include the Requester's name and this number in your reply) January XX, 200X Internal Revenue Service

Name c/o Address City, postal code 95XXX CALIFORNIA Certified Mail Ref.# 7002 2030 0003 XXXX XXXX (Include the Requester's name and this number in your reply) January XX, 200X Internal Revenue Service

Handouts Slides (Notes) and PFIC example

and PFIC example") Handouts Slides (Notes) and PFIC example 1 (b) (6) Presented by Grace (if present) or Allen: First bullet is self-explanatory. This is not an exam TP has burden to provide documents to verify the adjustments.

Handouts Slides (Notes) and PFIC example 1 (b) (6) Presented by Grace (if present) or Allen: First bullet is self-explanatory. This is not an exam TP has burden to provide documents to verify the adjustments.

First Time Abatement (of Penalties) Made Easy Failure To File Failure To Pay Failure To Deposit

Made Easy Failure To File Failure To Pay Failure To Deposit") First Time Abatement (of Penalties) Made Easy Failure To File Failure To Pay Failure To Deposit Presenter Roger Nemeth, EA & NTPI Fellow President & Developer Audit Detective, LLC Working Undercover Narcotics

First Time Abatement (of Penalties) Made Easy Failure To File Failure To Pay Failure To Deposit Presenter Roger Nemeth, EA & NTPI Fellow President & Developer Audit Detective, LLC Working Undercover Narcotics

Information for Non-Tax Filers

NONFIL 2018-2019 Information for Non-Tax Filers Dear Student, If you (and your parent, if dependent) worked in 2016 but did not file a tax return with the IRS, please bring your (and your parent, if dependent)

NONFIL 2018-2019 Information for Non-Tax Filers Dear Student, If you (and your parent, if dependent) worked in 2016 but did not file a tax return with the IRS, please bring your (and your parent, if dependent)

Part 5. Collecting Process. Chapter 12. Federal Tax Liens. Section 1. Lien Program Overview Lien Program Overview. Manual Transmittal.

Part 5. Collecting Process Chapter 12. Federal Tax Liens Section 1. Lien Program Overview 5.12.1 Lien Program Overview 5.12.1.1 Purpose of this IRM 5.12.1.2 Introduction to Liens 5.12.1.3 Creation and

Part 5. Collecting Process Chapter 12. Federal Tax Liens Section 1. Lien Program Overview 5.12.1 Lien Program Overview 5.12.1.1 Purpose of this IRM 5.12.1.2 Introduction to Liens 5.12.1.3 Creation and

2016 IRS Collections Representation Boot Camp

2016 IRS Collections Representation Boot Camp Presented by: Dan Henn, CPA & Jassen Bowman, EA Sponsors: IRS Program Number: SDQJW-T-00040-16-I Sponsor ID #137128. Before We Get Started For proper CPE tracking,

2016 IRS Collections Representation Boot Camp Presented by: Dan Henn, CPA & Jassen Bowman, EA Sponsors: IRS Program Number: SDQJW-T-00040-16-I Sponsor ID #137128. Before We Get Started For proper CPE tracking,

Table of Contents. EA Exam Part

Table of Contents EA Exam Part 3 2017-18 Introduction... 2 Examination Content Outline... 8 Course Content... 11 Practices and Procedures... 12 Practice before the IRS... 12 OPR and Practice before the

Table of Contents EA Exam Part 3 2017-18 Introduction... 2 Examination Content Outline... 8 Course Content... 11 Practices and Procedures... 12 Practice before the IRS... 12 OPR and Practice before the

Kevin Murphy, Esq. Andreozzi Bluestein LLP 9145 Main Street Clarence, NY PH# (716) , Fax# (716)

, Fax# (716)") Kevin Murphy, Esq. Andreozzi Bluestein LLP 9145 Main Street Clarence, NY 14031 PH# (716) 633-3200, Fax# (716) 633-0301 kmm@andreozzibluestein.com PART 1 BASIC TAX ISSUES IN BANKRUPTCY Tax Collection Defense

Kevin Murphy, Esq. Andreozzi Bluestein LLP 9145 Main Street Clarence, NY 14031 PH# (716) 633-3200, Fax# (716) 633-0301 kmm@andreozzibluestein.com PART 1 BASIC TAX ISSUES IN BANKRUPTCY Tax Collection Defense

7:' 5 = Estate and Gift Tax 7 = CT-1 8 = FUTA

4-10 (6) The completed research form may be sent via FAX to the EFTPS Accounting Technical Unit at (901 )546-2990. Please provide as much of the requested information as possible to the unit when making

4-10 (6) The completed research form may be sent via FAX to the EFTPS Accounting Technical Unit at (901 )546-2990. Please provide as much of the requested information as possible to the unit when making

Instructions for Form W-7

Instructions for Form W-7 (January 2010) Application for IRS Individual Taxpayer Identification Number Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue

Instructions for Form W-7 (January 2010) Application for IRS Individual Taxpayer Identification Number Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue

We are going to discuss some general FBAR Information in the next few Slides.

(b) (6) (b) (6) You need to Allow the Evidence to Guide the FBAR Investigation. If the evidence tends to show willful conduct by the person, then continue to gather evidence to prove Willful FBAR violations;

(b) (6) (b) (6) You need to Allow the Evidence to Guide the FBAR Investigation. If the evidence tends to show willful conduct by the person, then continue to gather evidence to prove Willful FBAR violations;

2016 IRS Collections Representation Boot Camp

2016 IRS Collections Representation Boot Camp Presented by: Dan Henn, CPA & Jassen Bowman, EA Sponsors: IRS Program Number: SDQJW-T-00040-16-I Sponsor ID #137128. Before We Get Started For proper CPE tracking,

2016 IRS Collections Representation Boot Camp Presented by: Dan Henn, CPA & Jassen Bowman, EA Sponsors: IRS Program Number: SDQJW-T-00040-16-I Sponsor ID #137128. Before We Get Started For proper CPE tracking,

President IRS Solutions Author Loves Taxes Loves Teaching Former Revenue Officer.

DAVID STONE, E.A. President IRS Solutions Author Loves Taxes Loves Teaching Former Revenue Officer 2 In this Session We Will Learn: 1. What tools the IRS has to use 2. What tools are available to the accountant

DAVID STONE, E.A. President IRS Solutions Author Loves Taxes Loves Teaching Former Revenue Officer 2 In this Session We Will Learn: 1. What tools the IRS has to use 2. What tools are available to the accountant

ACCOUNTAX SCHOOL OF BUSINESS, INCORPORATED A Profile in Continuing Professional Education. Representing Clients During the Collections Process

ACCOUNTAX SCHOOL OF BUSINESS, INCORPORATED A Profile in Continuing Professional Education Representing Clients During the Collections Process A. Extension of time to pay (e.g., Form 1127-A) If a taxpayer

ACCOUNTAX SCHOOL OF BUSINESS, INCORPORATED A Profile in Continuing Professional Education Representing Clients During the Collections Process A. Extension of time to pay (e.g., Form 1127-A) If a taxpayer

TAX PRACTICE FINAL COPYRIGHT 2017 LGUTEF. Learning Objectives. Introduction

TAX PRACTICE 14 Issue 1: Substitute for Returns and Superseding Returns.. 506 Issue 2: Nonfilers........... 509 Issue 3: Collection Statute of Limitations.............. 513 Issue 4: Transferees, Nominees,

TAX PRACTICE 14 Issue 1: Substitute for Returns and Superseding Returns.. 506 Issue 2: Nonfilers........... 509 Issue 3: Collection Statute of Limitations.............. 513 Issue 4: Transferees, Nominees,

LIST OF SUBSTANTIVE CHANGES AND ADDITIONS. PPC s Guide to Dealing with the IRS. Twenty-third Edition (June 2015)

") Route To: j Partners j Managers j Staff j File P.O. Box 115008 Carrollton, TX 75011-5008 Tel (972) 250-7750 (800) 431-9025 Fax (888) 216-1929 tax.thomsonreuters.com LIST OF SUBSTANTIVE CHANGES AND ADDITIONS

Route To: j Partners j Managers j Staff j File P.O. Box 115008 Carrollton, TX 75011-5008 Tel (972) 250-7750 (800) 431-9025 Fax (888) 216-1929 tax.thomsonreuters.com LIST OF SUBSTANTIVE CHANGES AND ADDITIONS

How to Request IRS Verification of Non-filing Letter

How to Request IRS Verification of Non-filing Letter How to request a Non-filing Letter if, I never filed a tax return I filed an IRS tax return in the past My parents live outside the U.S and cannot obtain

How to Request IRS Verification of Non-filing Letter How to request a Non-filing Letter if, I never filed a tax return I filed an IRS tax return in the past My parents live outside the U.S and cannot obtain

IRS commonly makes illegal Time Barred Assessments

IRS commonly makes illegal Time Barred Assessments If your IMF MCC TRANSCRIPT-SPECIFIC shows a TC 560 then good chance the IRS has used this TC 560 to alter your IMF ASED=Assessment Statute Expiration

IRS commonly makes illegal Time Barred Assessments If your IMF MCC TRANSCRIPT-SPECIFIC shows a TC 560 then good chance the IRS has used this TC 560 to alter your IMF ASED=Assessment Statute Expiration

SJWT Collection Panel JUNE/2018

SJWT Collection Panel JUNE/2018 Collection Topics Revenue officer field presence Collection Information Statements Notice of Federal Tax Lien Issues Installment Agreements Revolving Door? Current Compliance

SJWT Collection Panel JUNE/2018 Collection Topics Revenue officer field presence Collection Information Statements Notice of Federal Tax Lien Issues Installment Agreements Revolving Door? Current Compliance

Supplier Information Form Instructions

Purpose of Form. An organization that is required to file an information return with the IRS must obtain your correct Federal Taxpayer Identification Number in order to report income paid to you. The Tax

Purpose of Form. An organization that is required to file an information return with the IRS must obtain your correct Federal Taxpayer Identification Number in order to report income paid to you. The Tax

Note: Form 4506-T begins on the next page. Kansas City and Austin Fax Numbers for Filing Form 4506-T Have Changed The fax numbers for filing Form 4506-T with the IRS center in Kansas City and Austin have

Note: Form 4506-T begins on the next page. Kansas City and Austin Fax Numbers for Filing Form 4506-T Have Changed The fax numbers for filing Form 4506-T with the IRS center in Kansas City and Austin have

After the FBAR Overhaul: Foreign Account Reporting Enforcement Preparing for IRS Exams, Potential Penalties, Administrative Appeals or Litigation

Presenting a live 110-minute teleconference with interactive Q&A After the FBAR Overhaul: Foreign Account Reporting Enforcement Preparing for IRS Exams, Potential Penalties, Administrative Appeals or Litigation

Presenting a live 110-minute teleconference with interactive Q&A After the FBAR Overhaul: Foreign Account Reporting Enforcement Preparing for IRS Exams, Potential Penalties, Administrative Appeals or Litigation

Part 5. Collecting Process. Chapter 24. Central Withholding Agreement (CWA) Program. Section 1. Overview Overview

Program. Section 1. Overview Overview") Part 5. Collecting Process Chapter 24. Central Withholding Agreement (CWA) Program Section 1. Overview 5.24.1 Overview 5.24.1.1 Introduction 5.24.1.2 Background 5.24.1.3 Delegation Order 5.24.1.4 Revenue

Part 5. Collecting Process Chapter 24. Central Withholding Agreement (CWA) Program Section 1. Overview 5.24.1 Overview 5.24.1.1 Introduction 5.24.1.2 Background 5.24.1.3 Delegation Order 5.24.1.4 Revenue

SECTION 22. REQUESTING FORMS AND OTHER INFORMATION SECTION 23. EFFECT ON OTHER DOCUMENTS SECTION 24. EFFECTIVE DATE SECTION 1.

26 CFR. 601.602: Tax forms and instructions. (Also Part I, Sections 3504, 6011; 31.3504 1, 31.6011(a) 8, 31.6071(a) 1.) Rev. Proc. 96 18 Table of Contents SECTION 1. PURPOSE SECTION 2. BACKGROUND SECTION

26 CFR. 601.602: Tax forms and instructions. (Also Part I, Sections 3504, 6011; 31.3504 1, 31.6011(a) 8, 31.6071(a) 1.) Rev. Proc. 96 18 Table of Contents SECTION 1. PURPOSE SECTION 2. BACKGROUND SECTION

Do a Paycheck Checkup

Do a Paycheck Checkup Alan Gregerson October 25, 2018 Why a Paycheck Checkup? Some law changes in the Tax Cuts and Jobs Act may affect your withholding. Protect against having too little tax withheld and

Do a Paycheck Checkup Alan Gregerson October 25, 2018 Why a Paycheck Checkup? Some law changes in the Tax Cuts and Jobs Act may affect your withholding. Protect against having too little tax withheld and

WELCOME. IRS Fresno Campus Practitioner Outreach Event and Tour. July 30 & 31, 2009

WELCOME IRS Fresno Campus Practitioner Outreach Event and Tour July 30 & 31, 2009 Welcome from Submission Processing IRS Fresno Campus James C. Gaither, Field Director, Submission Processing W&I Taxpayer

WELCOME IRS Fresno Campus Practitioner Outreach Event and Tour July 30 & 31, 2009 Welcome from Submission Processing IRS Fresno Campus James C. Gaither, Field Director, Submission Processing W&I Taxpayer

Trust Fund Recovery. A Tax Resolution Institute Publication 2016

A Tax Resolution Institute Publication 2016 Trust Fund Recovery Facing possible retributions such as civil liability for unpaid employment taxes, including penalties and interest, and possible criminal

A Tax Resolution Institute Publication 2016 Trust Fund Recovery Facing possible retributions such as civil liability for unpaid employment taxes, including penalties and interest, and possible criminal

GAO. TAX ADMINISTRATION Billions in Self- Employment Taxes Are Owed

GAO United States General Accounting Office Report to the Chairman, Subcommittee on Oversight, Committee on Ways and Means, House of Representatives February 1999 TAX ADMINISTRATION Billions in Self- Employment

GAO United States General Accounting Office Report to the Chairman, Subcommittee on Oversight, Committee on Ways and Means, House of Representatives February 1999 TAX ADMINISTRATION Billions in Self- Employment

Internal Revenue Service. PURPOSE (1) This transmits revised IRM , Report of Foreign Bank and Financial Accounts (FBAR) Procedures.

This transmits revised IRM , Report of Foreign Bank and Financial Accounts (FBAR) Procedures.") MANUAL TRANSMITTAL Department of the Treasury Internal Revenue Service 4.26.17 MAY 5, 2008 PURPOSE (1) This transmits revised IRM 4.26.17, Report of Foreign Bank and Financial Accounts (FBAR) Procedures.

MANUAL TRANSMITTAL Department of the Treasury Internal Revenue Service 4.26.17 MAY 5, 2008 PURPOSE (1) This transmits revised IRM 4.26.17, Report of Foreign Bank and Financial Accounts (FBAR) Procedures.

STATUTE OF LIMITATIONS Analyze This. By LG Brooks Enrolled Agent

The capital of Texas enrolled agents Austin, Texas November 2008 STATUTE OF LIMITATIONS Analyze This By LG Brooks Enrolled Agent I. BIOGRAPHY LG Brooks, BA, EA LG Brooks is an Enrolled Agent and is the

The capital of Texas enrolled agents Austin, Texas November 2008 STATUTE OF LIMITATIONS Analyze This By LG Brooks Enrolled Agent I. BIOGRAPHY LG Brooks, BA, EA LG Brooks is an Enrolled Agent and is the

IRS Updates. Due Date. Richard Furlong, Jr. Senior Stakeholder Liaison 1/2/2018

IRS Updates Richard Furlong, Jr. Senior Stakeholder Liaison January 4, 2018 North Jersey Working Together Conference Seton Hall University Due Date Returns and payments otherwise due April 15, 2018, are

IRS Updates Richard Furlong, Jr. Senior Stakeholder Liaison January 4, 2018 North Jersey Working Together Conference Seton Hall University Due Date Returns and payments otherwise due April 15, 2018, are

Instructions for Form 941 (Rev. April 2005)

") Instructions for Form 941 (Rev. April 2005) For use with Form 941 (Rev. January 2005) Employer s Quarterly Federal Tax Return Section references are to the Internal Revenue Code unless otherwise indicated.

Instructions for Form 941 (Rev. April 2005) For use with Form 941 (Rev. January 2005) Employer s Quarterly Federal Tax Return Section references are to the Internal Revenue Code unless otherwise indicated.

Overview of Tax Controversy and Procedure

Overview of Tax Controversy and Procedure Presented by: Deborah S. Kearns Assistant Clinical Professor of Law Albany Law School December 9, 2014 Getting Started Determine stage of tax controversy. Determine

Overview of Tax Controversy and Procedure Presented by: Deborah S. Kearns Assistant Clinical Professor of Law Albany Law School December 9, 2014 Getting Started Determine stage of tax controversy. Determine

E-Filed FBARs accepted by the BSA (Bank Secrecy Act) should appear on CBRS within 48 hours.

should appear on CBRS within 48 hours.") (b) (6) You need to Allow the Evidence to Guide the FBAR Investigation. If the evidence tends to show willful conduct by the person, then continue to gather evidence to prove Willful FBAR violations; however,

(b) (6) You need to Allow the Evidence to Guide the FBAR Investigation. If the evidence tends to show willful conduct by the person, then continue to gather evidence to prove Willful FBAR violations; however,

Offer-in-Compromise Why or Why Not

Why or Why Not The Capital of Texas Enrolled Agents November 2010 by: lg brooks, ea Why or Why Not Table of Contents Introduction 3 The Offer Process 4 The Offer in Compromise: Offers in General 4 Grounds

Why or Why Not The Capital of Texas Enrolled Agents November 2010 by: lg brooks, ea Why or Why Not Table of Contents Introduction 3 The Offer Process 4 The Offer in Compromise: Offers in General 4 Grounds

Guide for the Certification of State FUTA Credits

Guide for the Certification of State FUTA Credits Unemployment Tax Form 940 and Schedule H Effective October 2012 for Tax Year 2011 FUTA Program Publication 4485 (Rev. 10-2012) Catalog Number 47331E Department

Guide for the Certification of State FUTA Credits Unemployment Tax Form 940 and Schedule H Effective October 2012 for Tax Year 2011 FUTA Program Publication 4485 (Rev. 10-2012) Catalog Number 47331E Department

FBAR Penalties; Post 10/22/2004; SB/SE E&G Examiner Lead Sheet

e Taxpayer Name: Tax Period (may consider up to 6 years, if applic.) Previously Assessed Per Exam Adjustment Reference Conclusion: (Reflects the final determination on the issue.) The following techniques

e Taxpayer Name: Tax Period (may consider up to 6 years, if applic.) Previously Assessed Per Exam Adjustment Reference Conclusion: (Reflects the final determination on the issue.) The following techniques

Oregon Personal Income Tax

Oregon Personal Income Tax Electronic Filing Handbook For Software Developers and Tax Preparers Tax Year 2008 Published by Oregon Department of Revenue 10/08/2008 2:38 PM 1 Oregon Electronic Filing Business

Oregon Personal Income Tax Electronic Filing Handbook For Software Developers and Tax Preparers Tax Year 2008 Published by Oregon Department of Revenue 10/08/2008 2:38 PM 1 Oregon Electronic Filing Business

Collection Due Process Hearing

263 Collection Due Process (CDP) Statutory Right A gift from the IRS Restructuring and Reform Act of 1998 1. Lien IRC 6320 2. Levy IRC 6330 263 264 Critical Issues of CDP Use it or lose it 30 days to REQUEST

263 Collection Due Process (CDP) Statutory Right A gift from the IRS Restructuring and Reform Act of 1998 1. Lien IRC 6320 2. Levy IRC 6330 263 264 Critical Issues of CDP Use it or lose it 30 days to REQUEST

Responding to Adverse IRS Audit Assessments: Audit Reconsideration Requests, IRS Appeals, and Settlement Strategies

Responding to Adverse IRS Audit Assessments: Audit Reconsideration Requests, IRS Appeals, and Settlement Strategies TUESDAY, MARCH 1, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved

Responding to Adverse IRS Audit Assessments: Audit Reconsideration Requests, IRS Appeals, and Settlement Strategies TUESDAY, MARCH 1, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved

IRS Notices. September 24, Whitepaper on IRS Notices, with an emphasis on a CP2000. By Erin Koplitz, CPA

IRS Notices September 24, 2015 Whitepaper on IRS Notices, with an emphasis on a CP2000 By Erin Koplitz, CPA Table of Contents FAQs for a CP2000... 1 Responding to a Notice... 3 Read the Notice... 4 Identify

IRS Notices September 24, 2015 Whitepaper on IRS Notices, with an emphasis on a CP2000 By Erin Koplitz, CPA Table of Contents FAQs for a CP2000... 1 Responding to a Notice... 3 Read the Notice... 4 Identify

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Detection Has Improved; However, Identity Theft Continues to Result in Billions of Dollars in Potentially Fraudulent Tax Refunds September 20, 2013 Reference

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Detection Has Improved; However, Identity Theft Continues to Result in Billions of Dollars in Potentially Fraudulent Tax Refunds September 20, 2013 Reference

Y OUR U NDERSTANDING IRS INDIVIDUAL TAXPAYER IDENTIFICATION NUMBER ITIN

U NDERSTANDING Y OUR IRS INDIVIDUAL TAXPAYER IDENTIFICATION NUMBER ITIN TAXPAYER ASSISTANCE IRS assistance is available to help you prepare your Form W-7. In the United States, call: 1-800-829-1040 (toll-free)

U NDERSTANDING Y OUR IRS INDIVIDUAL TAXPAYER IDENTIFICATION NUMBER ITIN TAXPAYER ASSISTANCE IRS assistance is available to help you prepare your Form W-7. In the United States, call: 1-800-829-1040 (toll-free)

At the end of 2015, Congress added a provision to

Owe Taxes? Stay Home. By Phyllis Horn Epstein At the end of 2015, Congress added a provision to the Internal Revenue Code (IRC 7345 added by Section 32101 of the Fixing America s Surface Transportation

Owe Taxes? Stay Home. By Phyllis Horn Epstein At the end of 2015, Congress added a provision to the Internal Revenue Code (IRC 7345 added by Section 32101 of the Fixing America s Surface Transportation

%, based on your creditworthiness at the time

DuPont Community Credit Union MASTERCARD PLATINUM CREDIT CARD Interest Rates and Interest Charges Annual Percentage Rate (APR) for Purchases APR for Balance Transfers APR for Cash Advances Paying Interest

DuPont Community Credit Union MASTERCARD PLATINUM CREDIT CARD Interest Rates and Interest Charges Annual Percentage Rate (APR) for Purchases APR for Balance Transfers APR for Cash Advances Paying Interest

Q&A s???? ???? Revenue Protection Strategy IRS. Messages for the 1999 Filing Season. Department of the Treasury Internal Revenue Service

Revenue Protection Strategy Messages for the 1999 Filing Season Q&A s???? IRS Department of the Treasury Internal Revenue Service???? Publication 3357 (1-1999) Catalog Number 27193I Table of Contents Introduction

Revenue Protection Strategy Messages for the 1999 Filing Season Q&A s???? IRS Department of the Treasury Internal Revenue Service???? Publication 3357 (1-1999) Catalog Number 27193I Table of Contents Introduction

Treaty Case Training - Session 3 Offshore Information Return Penalties

1 Treaty Case Training - Session 3 Offshore Information Return Penalties Please call into our Conference Call @ 1-866-606-4717 Access Code 3024120 You will NOT need your Headsets for this session 1 2 Treaty

1 Treaty Case Training - Session 3 Offshore Information Return Penalties Please call into our Conference Call @ 1-866-606-4717 Access Code 3024120 You will NOT need your Headsets for this session 1 2 Treaty

FEDERAL COMMUNICATIONS COMMISSION REMITTANCE ADVICE PAGE NO. OF

READ INSTRUCTIONS CAREFULLY APPROVED BY OMB 3060-0589 BEFORE PROCEEDING FEDERAL COMMUNICATIONS COMMISSION REMITTANCE ADVICE SPECIAL USE (1) LOCKBOX # PAGE NO. OF FCC USE ONLY SECTION A - PAYER INFORMATION

READ INSTRUCTIONS CAREFULLY APPROVED BY OMB 3060-0589 BEFORE PROCEEDING FEDERAL COMMUNICATIONS COMMISSION REMITTANCE ADVICE SPECIAL USE (1) LOCKBOX # PAGE NO. OF FCC USE ONLY SECTION A - PAYER INFORMATION

DuPont Community Credit Union MASTERCARD PLATINUM CREDIT CARD

DuPont Community Credit Union MASTERCARD PLATINUM CREDIT CARD Interest Rates and Interest Charges Annual Percentage Rate (APR) for Purchases 0.00% Introductory APR for 6 monthly statement periods on all

DuPont Community Credit Union MASTERCARD PLATINUM CREDIT CARD Interest Rates and Interest Charges Annual Percentage Rate (APR) for Purchases 0.00% Introductory APR for 6 monthly statement periods on all

Instructions for Form 941

Instructions for Form 941 (Rev. February 2010) Employer s QUARTERLY Federal Tax Return Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise

Instructions for Form 941 (Rev. February 2010) Employer s QUARTERLY Federal Tax Return Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise

Manufactured Housing Tax Liens

Texas Department of Housing and Community Affairs MANUFACTURED HOUSING DIVISION Manufactured Housing Tax Liens TDHCA Main Web Page To access the Manufactured Housing web page select MANUFACTURED HOUSING

Texas Department of Housing and Community Affairs MANUFACTURED HOUSING DIVISION Manufactured Housing Tax Liens TDHCA Main Web Page To access the Manufactured Housing web page select MANUFACTURED HOUSING

How To Detect & Mitigate IRS Exams Before They Begin

How To Detect & Mitigate IRS Exams Before They Begin Learn how to detect IRS Exams early and mitigate the effects for your clients. Roger Nemeth, EA Started managing tax franchises in 2006. Developed Audit

How To Detect & Mitigate IRS Exams Before They Begin Learn how to detect IRS Exams early and mitigate the effects for your clients. Roger Nemeth, EA Started managing tax franchises in 2006. Developed Audit

TRI Tax Resolution Institute. where your tax debt is your power! Busy Season. all year long

TRI Tax Resolution Institute where your tax debt is your power! Busy Season all year long Low Hanging Fruit How to make real money in the next 12 months Meet our speaker Peter Y. Stephan, CPA (800) 658-7590

TRI Tax Resolution Institute where your tax debt is your power! Busy Season all year long Low Hanging Fruit How to make real money in the next 12 months Meet our speaker Peter Y. Stephan, CPA (800) 658-7590

LIST OF SUBSTANTIVE CHANGES AND ADDITIONS. PPC s Guide to Dealing with the IRS. Twenty-fourth Edition (June 2016)

") LIST OF SUBSTANTIVE CHANGES AND ADDITIONS PPC s Guide to Dealing with the IRS Twenty-fourth Edition (June 2016) The following are some of the features of this year s update of PPC s Guide to dealing with

LIST OF SUBSTANTIVE CHANGES AND ADDITIONS PPC s Guide to Dealing with the IRS Twenty-fourth Edition (June 2016) The following are some of the features of this year s update of PPC s Guide to dealing with

Earned Income Tax Credit Due Diligence: What Questions to Ask and What Documents to Keep. Kyle Coleman

Earned Income Tax Credit Due Diligence: What Questions to Ask and What Documents to Keep Presented By: Kyle Coleman Coleman, Anastopulos & Jackson, P.C. 16250 Knoll Trail Drive, Suite 105, Dallas, TX 75248

Earned Income Tax Credit Due Diligence: What Questions to Ask and What Documents to Keep Presented By: Kyle Coleman Coleman, Anastopulos & Jackson, P.C. 16250 Knoll Trail Drive, Suite 105, Dallas, TX 75248

Instructions for Form 941-X

Department of the Treasury Instructions for Form 941-X Internal Revenue Service (April 2014) Adjusted Employer's QUARTERLY Federal Tax Return or Claim for Refund Section references are to the Internal

Department of the Treasury Instructions for Form 941-X Internal Revenue Service (April 2014) Adjusted Employer's QUARTERLY Federal Tax Return or Claim for Refund Section references are to the Internal

Questions for Discussion with NC Department of Revenue. Submitted by the NC Association of CPAs Committee on Taxation

Questions for Discussion with NC Department of Revenue Submitted by the NC Association of CPAs Committee on Taxation and the Tax Section of the NC Bar Association December 4, 2017 Individual Income Tax

Questions for Discussion with NC Department of Revenue Submitted by the NC Association of CPAs Committee on Taxation and the Tax Section of the NC Bar Association December 4, 2017 Individual Income Tax

2011 Year-End Client Guide For clients using RUN Powered by ADP

2011 Year-End Client Guide For clients using RUN Powered by ADP This guide contains information and critical dates that will help ease your year-end tax filing. HR. Payroll. Benefits. Welcome to the 2011

2011 Year-End Client Guide For clients using RUN Powered by ADP This guide contains information and critical dates that will help ease your year-end tax filing. HR. Payroll. Benefits. Welcome to the 2011

STATEMENT OF JENNIFER E. BREEN ON BEHALF OF THE AMERICAN BAR ASSOCIATION SECTION OF TAXATION BEFORE THE COMMITTEE ON SMALL BUSINESS OF THE

STATEMENT OF JENNIFER E. BREEN ON BEHALF OF THE AMERICAN BAR ASSOCIATION SECTION OF TAXATION BEFORE THE COMMITTEE ON SMALL BUSINESS OF THE UNITED STATES HOUSE OF REPRESENTATIVES FOR THE HEARING ON IRS

STATEMENT OF JENNIFER E. BREEN ON BEHALF OF THE AMERICAN BAR ASSOCIATION SECTION OF TAXATION BEFORE THE COMMITTEE ON SMALL BUSINESS OF THE UNITED STATES HOUSE OF REPRESENTATIVES FOR THE HEARING ON IRS

Dependent Veri ication Form

Financial Aid Services 20182019 Dependent Veriication Form PART I: Student Information Name: Last First Middle SPIRE ID: Date of Birth: / / Email Address: Phone Number: ( ) PART II: Your Parents Household

Financial Aid Services 20182019 Dependent Veriication Form PART I: Student Information Name: Last First Middle SPIRE ID: Date of Birth: / / Email Address: Phone Number: ( ) PART II: Your Parents Household

Dependent Verif ication Form

Dependent Verif ication Form Financial Aid Services 2017-2018 PART I: STUDENT INFORMATION Name: Last First Middle SPIRE ID: Date of Birth: / / Phone Number: ( ) - Email Address: INSTRUCTIONS: 1. This form

Dependent Verif ication Form Financial Aid Services 2017-2018 PART I: STUDENT INFORMATION Name: Last First Middle SPIRE ID: Date of Birth: / / Phone Number: ( ) - Email Address: INSTRUCTIONS: 1. This form

Federal and State Employment Tax Issues

Federal and State Employment Tax Issues Seminar prepared for the Virginia Society of Enrolled Agents (September 2014) by The three most common problems 1. Not filing; 2. Not making timely deposits; and

Federal and State Employment Tax Issues Seminar prepared for the Virginia Society of Enrolled Agents (September 2014) by The three most common problems 1. Not filing; 2. Not making timely deposits; and

FEDERAL TAX REPORTING INFORMATION

2018 FEDERAL TAX REPORTING INFORMATION for OP&F benefit recipients Securing the future for Ohio s police and firefighters FEDERAL TAX REPORTING INFORMATION The Ohio Police & Fire Pension Fund (OP&F), which

2018 FEDERAL TAX REPORTING INFORMATION for OP&F benefit recipients Securing the future for Ohio s police and firefighters FEDERAL TAX REPORTING INFORMATION The Ohio Police & Fire Pension Fund (OP&F), which

Notice of certification of your seriously delinquent federal tax debt to the State Department Amount due: $97,

Department of the Treasury Internal Revenue Service Attn: Passport P.O. Box 8208 Philadelphia, PA 19101-8208 ERIC D. JOHNSON 123 N HARRIS ST HARVARD, TX 12345 Notice CP508C To contact us Phone: 1-855-519-4965

Department of the Treasury Internal Revenue Service Attn: Passport P.O. Box 8208 Philadelphia, PA 19101-8208 ERIC D. JOHNSON 123 N HARRIS ST HARVARD, TX 12345 Notice CP508C To contact us Phone: 1-855-519-4965

TRI Tax Resolution Institute. where your tax debt is your power! Busy Season. all year long

TRI Tax Resolution Institute where your tax debt is your power! Busy Season all year long Low Hanging Fruit How to make real money in the next 12 months Meet our speaker Peter Y. Stephan, CPA (800) 658-7590

TRI Tax Resolution Institute where your tax debt is your power! Busy Season all year long Low Hanging Fruit How to make real money in the next 12 months Meet our speaker Peter Y. Stephan, CPA (800) 658-7590

501 Service Center Correspondence Audit Program

Checkpoint Contents Federal Library Federal Editorial Materials PPC's Tax and Financial Planning Library Dealing with the IRS Chapter 5 Audits of Individual Returns 501 Service Center Correspondence Audit

Checkpoint Contents Federal Library Federal Editorial Materials PPC's Tax and Financial Planning Library Dealing with the IRS Chapter 5 Audits of Individual Returns 501 Service Center Correspondence Audit

Checklist for Centralized Area Field Closures Offshore Voluntary Disclosure Program Cases

AGENT: REVIEWER: Pre-906 Issuance Review - Review Time should be charged to 641. NAME CONTROL: #1) Circle One: Exam Certification Case File should include the following: Original or copies of original

AGENT: REVIEWER: Pre-906 Issuance Review - Review Time should be charged to 641. NAME CONTROL: #1) Circle One: Exam Certification Case File should include the following: Original or copies of original

IRS FORM 944. Instructions: Select any any line or box for IRS instructions and QuickBooks information and troubleshooting steps.

IRS FORM 944 Instructions: Select any any line or box for IRS instructions and QuickBooks information and troubleshooting steps. Select to get back to the main form. For more information see: Form 944:

IRS FORM 944 Instructions: Select any any line or box for IRS instructions and QuickBooks information and troubleshooting steps. Select to get back to the main form. For more information see: Form 944:

University of Wisconsin System SFS Business Process AP /1042s/Tax Bolt-On

Contents 1099/1042-S Tax Bolt-On Process Overview... 1 Process Detail... 2 I. Search/Update for Existing Value 1099 / 1042 Records on the Bolt-On table... 2 II. Enter a New 1099/1042s records into the

Contents 1099/1042-S Tax Bolt-On Process Overview... 1 Process Detail... 2 I. Search/Update for Existing Value 1099 / 1042 Records on the Bolt-On table... 2 II. Enter a New 1099/1042s records into the

Table of Contents. About This Book How To Use This Book Foreword Acknowledgments Preface

Table of Contents About This Book How To Use This Book Foreword Acknowledgments Preface vii ix xi xiii xv Chapter 1 Initial Client Engagement 1 Topical Index 1 1.01 Nature of Federal Tax Law 5 1.02 Role

Table of Contents About This Book How To Use This Book Foreword Acknowledgments Preface vii ix xi xiii xv Chapter 1 Initial Client Engagement 1 Topical Index 1 1.01 Nature of Federal Tax Law 5 1.02 Role

2018 Loscalzo Institute, a Kaplan Company

Current Federal Tax Developments January 22, 2018 Section: IRS Operations IRS Publishes Plan to Deal With Government Shutdown... 2 Citation: Fiscal 2018 Lapsed Appropriations Contingency Plan (During Filing

Current Federal Tax Developments January 22, 2018 Section: IRS Operations IRS Publishes Plan to Deal With Government Shutdown... 2 Citation: Fiscal 2018 Lapsed Appropriations Contingency Plan (During Filing

NEW JERSEY PROVIDER AGREEMENT

NEW JERSEY PROVIDER AGREEMENT Provider ID: Effective Date: This Agreement is made by and between Conduent State & Local Solutions, Inc. a New Jersey Corporation, (hereinafter CONDUENT ) and, a corporation,

NEW JERSEY PROVIDER AGREEMENT Provider ID: Effective Date: This Agreement is made by and between Conduent State & Local Solutions, Inc. a New Jersey Corporation, (hereinafter CONDUENT ) and, a corporation,

Chapter 5: Personal Tax Credits. 05: Personal Tax Credits

Page 55-68 Chapter 5: Personal Tax Credits 1 Learning Objectives Page 55-68 Upon completion of this seminar, participants should be able to Identify personal tax credits for which our clients may qualify

Page 55-68 Chapter 5: Personal Tax Credits 1 Learning Objectives Page 55-68 Upon completion of this seminar, participants should be able to Identify personal tax credits for which our clients may qualify

FEDERAL TAX REPORTING INFORMATION

2017 FEDERAL TAX REPORTING INFORMATION for OP&F benefit recipients Securing the future for Ohio s police and firefighters FEDERAL TAX REPORTING INFORMATION The Ohio Police & Fire Pension Fund (OP&F), which

2017 FEDERAL TAX REPORTING INFORMATION for OP&F benefit recipients Securing the future for Ohio s police and firefighters FEDERAL TAX REPORTING INFORMATION The Ohio Police & Fire Pension Fund (OP&F), which

ALI-ABA Course of Study How To Handle a Tax Controversy at the IRS and in Court: From Administrative Audit Through Litigation

149 ALI-ABA Course of Study How To Handle a Tax Controversy at the IRS and in Court: From Administrative Audit Through Litigation Sponsored with the cooperation of the ABA Section of Taxation May 28-29,

149 ALI-ABA Course of Study How To Handle a Tax Controversy at the IRS and in Court: From Administrative Audit Through Litigation Sponsored with the cooperation of the ABA Section of Taxation May 28-29,

University Card Program Manual

University Card Program Manual Last Revision: July 20, 2018 TABLE OF CONTENTS Section Topic Page Contacts for Assistance... 1 Cardholder Process Overview... 2 Section 1: Overview of Wake Forest University

University Card Program Manual Last Revision: July 20, 2018 TABLE OF CONTENTS Section Topic Page Contacts for Assistance... 1 Cardholder Process Overview... 2 Section 1: Overview of Wake Forest University

TAX CONTROVERSY TOOLKIT

TAX CONTROVERSY TOOLKIT Toolkit for Handling a Pro Bono Tax Controversy Texas Young Lawyers Association 2014 Edition Disclaimer: This publication is intended to provide lawyers with current and accurate

TAX CONTROVERSY TOOLKIT Toolkit for Handling a Pro Bono Tax Controversy Texas Young Lawyers Association 2014 Edition Disclaimer: This publication is intended to provide lawyers with current and accurate

Offer In Compromise Line Instructions Irs Forms

Offer In Compromise Line Instructions Irs Forms 433 Form 433-A, Collection Information Statement for Wage Earners and Standards for completing the Expense section of Forms 433-A and 433-F Online Payment

Offer In Compromise Line Instructions Irs Forms 433 Form 433-A, Collection Information Statement for Wage Earners and Standards for completing the Expense section of Forms 433-A and 433-F Online Payment

Oracle FLEXCUBE Safe Deposit Box User Manual Release Part No E

Oracle FLEXCUBE Safe Deposit Box User Manual Release 4.5.0.0.0 Part No E52127-01 Safe Deposit Box User Manual Table of Contents (index) 1.1. 8057 - Safe Box Allotment... 3 1.2. SB001 - Safe Box Usage Log...

Oracle FLEXCUBE Safe Deposit Box User Manual Release 4.5.0.0.0 Part No E52127-01 Safe Deposit Box User Manual Table of Contents (index) 1.1. 8057 - Safe Box Allotment... 3 1.2. SB001 - Safe Box Usage Log...

The Fisher Agency Financial Advisors Since 1975

The Fisher Agency Financial Advisors Since 1975 DANNY FISHER, CLU, CHFC Danny@MrAnnuity.com 13140 Coit Road, Suite 102 President www.mrannuity.com Dallas, TX 75240-5797 972-238-1450 800-822-1450 Fax: 972-680-0562

The Fisher Agency Financial Advisors Since 1975 DANNY FISHER, CLU, CHFC Danny@MrAnnuity.com 13140 Coit Road, Suite 102 President www.mrannuity.com Dallas, TX 75240-5797 972-238-1450 800-822-1450 Fax: 972-680-0562

Payment. Billing Summary. What you need to do immediately $ Changes to your 2016 Form 1040A Amount due: $425.73

Department of the Treasury Internal Revenue Service Stop 6525 (SP CIS) Kansas City, MO 64999-0025 s018999546711s JOHN AND MARY SMITH 123 N HARRIS ST HARVARD, TX 12345 Notice To contact us Phone 1-800-829-0922

Department of the Treasury Internal Revenue Service Stop 6525 (SP CIS) Kansas City, MO 64999-0025 s018999546711s JOHN AND MARY SMITH 123 N HARRIS ST HARVARD, TX 12345 Notice To contact us Phone 1-800-829-0922

Field Collection Operations Employment Tax Compliance Efforts & Current Collection Hot Topics

Field Collection Operations Employment Tax Compliance Efforts & Current Collection Hot Topics Regina Malisham IRS Stakeholder Liaison FY 2016 Field Collection Operations 2 FY 2016 Field Collection Operations

Field Collection Operations Employment Tax Compliance Efforts & Current Collection Hot Topics Regina Malisham IRS Stakeholder Liaison FY 2016 Field Collection Operations 2 FY 2016 Field Collection Operations

Federal Tax Reporting Information for For OP&F benefit recipients

Federal Tax Reporting Information for 2008 For OP&F benefit recipients Federal Tax Reporting Information The Ohio Police & Fire Pension Fund (OP&F), which was established by the Ohio General Assembly in

Federal Tax Reporting Information for 2008 For OP&F benefit recipients Federal Tax Reporting Information The Ohio Police & Fire Pension Fund (OP&F), which was established by the Ohio General Assembly in

Instructions for Form 5330 (Revised August 1998)

") Instructions for Form 5330 (Revised August 1998) Return of Excise Taxes Related to Employee Benefit Plans Section references are to the Internal Revenue Code unless otherwise noted. Department of the Treasury

Instructions for Form 5330 (Revised August 1998) Return of Excise Taxes Related to Employee Benefit Plans Section references are to the Internal Revenue Code unless otherwise noted. Department of the Treasury