Earned Income Tax Credit Due Diligence: What Questions to Ask and What Documents to Keep. Kyle Coleman

|

|

|

- Rosamund Stevenson

- 6 years ago

- Views:

Transcription

1 Earned Income Tax Credit Due Diligence: What Questions to Ask and What Documents to Keep Presented By: Kyle Coleman Coleman, Anastopulos & Jackson, P.C Knoll Trail Drive, Suite 105, Dallas, TX Phone: (972) Fax: (972) law.com

2 Kyle Coleman Mr. Coleman s practice concentrates on federal tax related controversy matters, including litigation in Federal District Court, the United States Tax Court, and the Court of Federal Claims. Mr. Coleman also represents taxpayers in Internal Revenue Service audits, appeals, and collection actions. Mr. Coleman has been admitted to the Fifth Circuit Court of Appeals Bar, the District of Columbia Circuit Bar, the Northern District of Texas, the Eastern District of Texas, the District of Colorado, and the United States Tax Court. In addition to tax controversy, Mr. Coleman also represents clients in estate and business planning as well as asset protection. His practice includes entity formation, asset transfers, and wills and trusts. Education LL.M. in Taxation, Dedman School of Law, Southern Methodist University, 1999 J.D., Oklahoma City University School of Law, 1998 B.A. in Finance, University of Central Oklahoma, 1995 Bar Admissions State Bar of Texas State Bar of Oklahoma Professional Associations and Memberships State Bar of Texas State Bar of Oklahoma Dallas Bar Association 1

3 Earned Income Tax Credit Due Diligence: What Questions to Ask and What Documents to Keep Introduction In 1975, Congress enacted the Earned Income Tax Credit ( EITC ) as a temporary program. In its infinite wisdom, Congress made the EITC permanent in Initially, it was a 10% wage credit with a maximum payment of $400 and only people with children were eligible. Congress has expanded the size and scope of the EITC in numerous laws since the mid-1970s. What was originally a fairly narrow and limited credit has become fairly substantial and can result in a maximum credit today of over $6,000. A major weakness of the EITC program is the program s high rate of overpayments which are caused by a misunderstanding of the rules, mathematical errors and in some cases intentional fraud. The EITC error rate has been more than 20% since at least the 1980s. The Internal Revenue Service ( IRS ) reports that the EITC error and fraud rate in 2014 was 27%, which totaled over $18,000,000,000 in overpayments. The following chart demonstrates by fiscal year the error rate and the amount of dollars, in billions, paid to taxpayers, erroneously: Fiscal Year Error Rate Error (Amount) % $ % $ % $ % $ % $ % $ % $ % $ % $ % $ % 27% $14.50 $

4 Taxpayers are receiving excess EITC payments based on false information about such items as their income level, filing status, and qualifying children. The EITC is an easy target for dishonest filers because it is refundable, meaning that people can simply file false tax returns and wait for the IRS to issue them a refund even if they have not paid taxes into the system. Errors and fraud are also incurred in the Child Tax Credit ( CTC ). The improper payment rate for the CTC is more than 25%, thus costing taxpayers approximately $6,000,000,000 per year. There are a number of ways that unscrupulous taxpayers game the EICT system sometimes with the knowing help of the tax preparer. Typically, half of the EITC tax returns completed by paid preparers overclaim the credit. Recent IRS audit statistics show that the EITC has become so rife with fraud, 39% of all IRS audits for individual income tax filers are done on EITC filers. The number of audits and amount of fraud and waste that results from the EITC improper payments has attracted the attention of Congress which in turn has focused the attention of the IRS on you, tax preparers, as a first line of defense to improper payments. In a recent case, an EITC due diligence auditor personally appeared at a client s tax preparation firm and proceeded to conduct an EITC due diligence audit on the spot. The preparers were contacted in February related to returns that were prepared in late January and early February. Without any notice, the IRS began reviewing randomly selected client files that had taken the current year s EITC and received a refund. The Auditor selected fifty (50) files for review. There was a recurring error in document retention in each file which resulted in over $25,000 in penalties under IRC 6695(g). If you have clients who are eligible for the EITC or the CTC, you need to be aware of the questions that you should ask and which documents you should keep. If you do not know the answer to these questions, it could be expensive. Like it or not, the IRS is making you the front line in the battle against EITC improper payment. This outline will show the applicable Statutes, Regulations and Internal Revenue Service Manual provisions that cover a tax preparer s due diligence requirements in regards to the EITC. We will also show how the reporting requirements have been expanded to require return preparers to ask additional questions and retain additional documents in an attempt to reduce the error and improper payments rates related to the EITC and the CTC. Finally, we 3

5 will provide some examples to show what types of questions should be asked and documents that should be retained at it relates to taxpayers filing with EITC or CTC credit. Statute IRC 6695(g) The main statute that allows regulation of tax preparers as to EITC Due Diligence is IRC 6695(g) Other assessable penalties with respect to the preparation of tax returns for other persons (g) Failure to be diligent in determining eligibility for child tax credit; American opportunity tax credit; and earned income credit.--any person who is a tax return preparer with respect to any return or claim for refund who fails to comply with due diligence requirements imposed by the Secretary by regulations with respect to determining eligibility for, or the amount of, the credit allowable by section 24, 25A(a)(1), or 32 shall pay a penalty of $500 for each such failure. Treasury Regulation Regulations promulgated under IRC 6695 provide further guidance as to your EITC Due Diligence responsibilities. The Regulation states: Tax return preparer due diligence requirements for determining earned income credit eligibility. (a) Penalty for failure to meet due diligence requirements. A person who is a tax return preparer of a tax return or claim for refund under the Internal Revenue Code with respect to determining the eligibility for, or the amount of, the earned income credit (EIC) under section 32 and who fails to satisfy the due diligence requirements of paragraph (b) of this section will be subject to a penalty of $500 for each such failure. 4

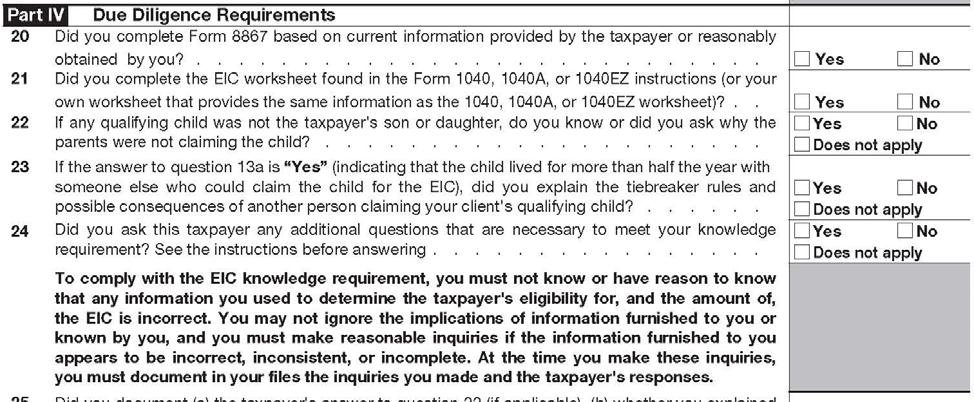

6 (b) Due diligence requirements. A preparer must satisfy the following due diligence requirements: (1) Completion and submission of Form 8867 (i) The tax return preparer must complete Form 8867, Paid Preparer s Earned Income Credit Checklist, or such other form and such other information as may be prescribed by the Internal Revenue Service (IRS), and (A) (B) (C) In the case of a signing tax return preparer electronically filing the tax return or claim for refund, must electronically file the completed Form 8867 (or successor form) with the tax return or claim for refund; In the case of a signing tax return preparer not electronically filing the tax return or claim for refund, must provide the taxpayer with the completed Form 8867 (or successor form) for inclusion with the filed tax return or claim for refund; or In the case of a nonsigning tax return preparer, must provide the signing tax return preparer with the completed Form 8867 (or successor form), in either electronic or non-electronic format, for inclusion with the filed tax return or claim for refund. (ii) The tax return preparer s completion of Form 8867 (or successor form) must be based on information provided by the taxpayer to the tax return preparer or otherwise reasonably obtained by the tax return preparer. (2) Computation of credit (i) The tax return preparer must either (A) Complete the Earned Income Credit Worksheet in the Form 1040 instructions or such other form and such other information as may be prescribed by the IRS; or (B) Otherwise record in one or more documents in the tax return preparer s paper or electronic files the tax return preparer s EIC computation, including the method and information used to make the computation. (ii) The tax return preparer s completion of the Earned Income Credit Worksheet (or other record of the tax return preparer s EIC 5

7 computation permitted under paragraph (b)(2)(i)(b) of this section) must be based on information provided by the taxpayer to the tax return preparer or otherwise reasonably obtained by the tax return preparer. (3) Knowledge (i) In general. The tax return preparer must not know, or have reason to know, that any information used by the tax return preparer in determining the taxpayer s eligibility for, or the amount of, the EIC is incorrect. The tax return preparer may not ignore the implications of information furnished to, or known by, the tax return preparer, and must make reasonable inquiries if the information furnished to the tax return preparer appears to be incorrect, inconsistent, or incomplete. A tax return preparer must make reasonable inquiries if a reasonable and well-informed tax return preparer knowledgeable in the law would conclude that the information furnished to the tax return preparer appears to be incorrect, inconsistent, or incomplete. The tax return preparer must also contemporaneously document in the files the reasonable inquiries made and the responses to these inquiries. (ii) Examples. The provisions of paragraph (b)(3)(i) of this section are illustrated by the following examples: Example 1. A 22 year-old taxpayer wants to claim two sons, ages 10 and 11, as qualifying children for purposes of the EIC. Preparer A must make additional reasonable inquiries regarding the relationship between the taxpayer and the children as the age of the taxpayer appears inconsistent with the ages of the children claimed as sons. Example 2. An 18 year-old female taxpayer with an infant has $3,000 in earned income and states that she lives with her parents. Taxpayer wants to claim the infant as a qualifying child for the EIC. This information appears incomplete and inconsistent because the taxpayer lives with her parents and earns very little income. Preparer B must make additional reasonable inquires to determine if the taxpayer is the qualifying child of her parents and, therefore, ineligible to claim the EIC. Example 3. Taxpayer asks Preparer C to prepare his tax return and wants to claim his niece and nephew as qualifying children for the EIC. Preparer C should make reasonable inquiries to determine whether the children meet EIC qualifying child requirements and ensure possible duplicate 6

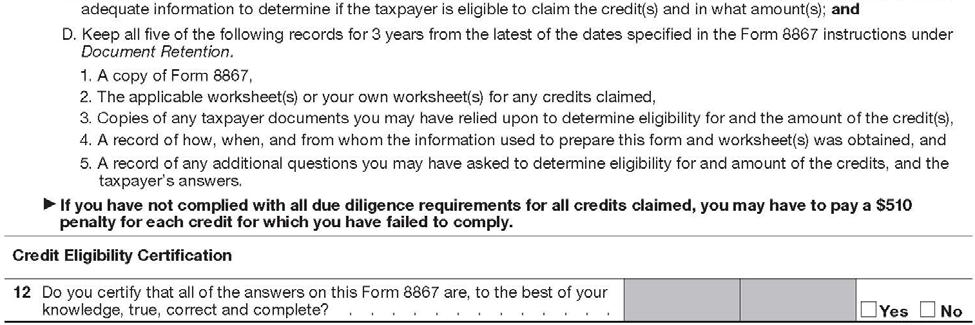

8 claim situations involving the parents or other relatives are properly considered. Example 4. Taxpayer asks Preparer D to prepare her tax return and tells D that she has a Schedule C business, that she has two qualifying children and that she wants to claim the EIC. Taxpayer indicates that she earned $10,000 from her Schedule C business, but that she has no expenses. This information appears incomplete because it is very unlikely that someone who is self-employed has no business expenses. D must make additional reasonable inquiries regarding taxpayer s business to determine whether the information regarding both income and expenses is correct. (4) Retention of records (i) The tax return preparer must retain (A) (B) (C) A copy of the completed Form 8867 (or successor form); A copy of the completed Earned Income Credit Worksheet (or other record of the tax return preparer s EIC computation permitted under paragraph (b)(2)(i)(b) of this section); and A record of how and when the information used to complete Form 8867 (or successor form) and the Earned Income Credit Worksheet (or other record of the tax return preparer s EIC computation permitted under paragraph (b)(2)(i)(b) of this section) was obtained by the tax return preparer, including the identity of any person furnishing the information, as well as a copy of any document that was provided by the taxpayer and on which the tax return preparer relied to complete Form 8867 (or successor form) or the Earned Income Credit Worksheet (or other record of the tax return preparer s EIC computation permitted under paragraph (b)(2)(i)(b) of this section). (ii) The items in paragraph (b)(4)(i) of this section must be retained for three years from the latest of the following dates, as applicable: (A) The due date of the tax return (determined without regard to any extension of time for filing); 7

9 (B) In the case of a signing tax return preparer electronically filing the tax return or claim for refund, the date the tax return or claim for refund was filed; (C) In the case of a signing tax return preparer not electronically filing the tax return or claim for refund, the date the tax return or claim for refund was presented to the taxpayer for signature; or (D) In the case of a nonsigning tax return preparer, the date the nonsigning tax return preparer submitted to the signing tax return preparer that portion of the tax return or claim for refund for which the nonsigning tax return preparer was responsible. (iii) (c) The items in paragraph (b)(4)(i) of this section may be retained on paper or electronically in the manner prescribed in applicable regulations, revenue rulings, revenue procedures, or other appropriate guidance (see (d)(2) of this chapter). Special rule for firms. A firm that employs a tax return preparer subject to a penalty under section 6695(g) is also subject to penalty if, and only if (1) One or more members of the principal management (or principal officers) of the firm or a branch office participated in or, prior to the time the return was filed, knew of the failure to comply with the due diligence requirements of this section; (2) The firm failed to establish reasonable and appropriate procedures to ensure compliance with the due diligence requirements of this section; or (3) The firm disregarded its reasonable and appropriate compliance procedures through willfulness, recklessness, or gross indifference (including ignoring facts that would lead a person of reasonable prudence and competence to investigate or ascertain) in the preparation of the tax return or claim for refund with respect to which the penalty is imposed. (d) Exception to penalty. The section 6695(g) penalty will not be applied with respect to a particular tax return or claim for refund if the tax return preparer can demonstrate to the satisfaction of the IRS that, 8

10 considering all the facts and circumstances, the tax return preparer s normal office procedures are reasonably designed and routinely followed to ensure compliance with the due diligence requirements of paragraph (b) of this section, and the failure to meet the due diligence requirements of paragraph (b) of this section with respect to the particular tax return or claim for refund was isolated and inadvertent. The preceding sentence does not apply to a firm that is subject to the penalty as a result of paragraph (c) of this section. (e) Effective/applicability date. This section applies to tax returns and claims for refund for tax years ending on or after December 31, Internal Revenue Manual The IRM very closely tracks the Regulations. The Manual states as follows: Failure to Be Diligent in Determining Eligibility for Earned Income Tax Credit IRC 6695(g) for Tax Returns or Claims for Refund for Tax Years Ending on or After December 31, 2011 ( ) (1) The IRC 6695(g) penalty applies if tax return preparer fails to comply with due diligence requirements with respect to determining eligibility for, or the amount of, the EIC. (2) Compliance visits with preparers to determine the due diligence requirement for the earned income credit are not third party contacts. (3) Under Treas. Reg (b), the preparer must comply with the following due diligence requirements for tax returns or claims for refund for tax years ending on or after December 31, (a.) (b.) The tax return preparer must complete Form 8867 or such other form and such other information as may be required by the IRS to be submitted in the manner required by forms, instructions, or other appropriate guidance. The tax return preparer s completion of Form 8867 (or successor form) must be based on information provided to the tax return preparer or otherwise reasonably obtained by the tax return 9

11 preparer. (c.) (d.) (e.) The tax return preparer must either complete the earned income credit worksheet in the Form 1040 instructions or such other form and such other information as may be prescribed by the IRS or otherwise record in one or more documents in the tax preparer s paper or electronic files the EIC computation, including the method and information used to make the computation. The completion of the earned income credit worksheet or other permitted record must be based on information provided by the taxpayer to the tax return preparer or otherwise reasonably obtained by the tax return preparer. The tax return preparer must not know, or have reason to know, that any information used by the tax return preparer in determining the taxpayer s eligibility for, or the amount of, the EIC is incorrect. The tax return preparer may not ignore the implications of information furnished to, or known by, the tax return preparer, and must make reasonable inquiries if the information furnished to the tax return preparer appears to be incorrect, inconsistent, or incomplete. A tax return preparer must make reasonable inquiries if a reasonable and well-informed tax return preparer knowledgeable in the law would conclude that the information furnished to the tax return preparer appears to be incorrect, inconsistent, or incomplete. The tax return preparer must also contemporaneously document in the files the reasonable inquiries made and the responses to these inquiries. (4) See IRM (4) above which list the four examples from Treas. Reg (b)(3)(ii). (5) See Treas. Reg (b)(4) regarding record retention. (6) See Treas. Reg (c) regarding special rule for firms. (7) See Treas. Reg (d) regarding exceptions to the penalty. 10

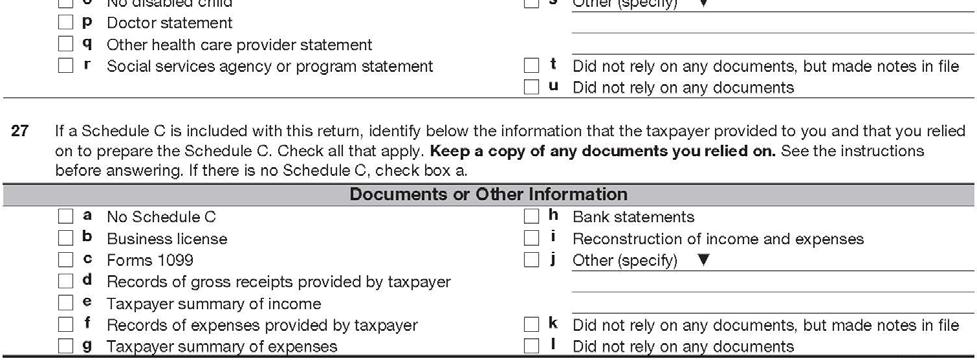

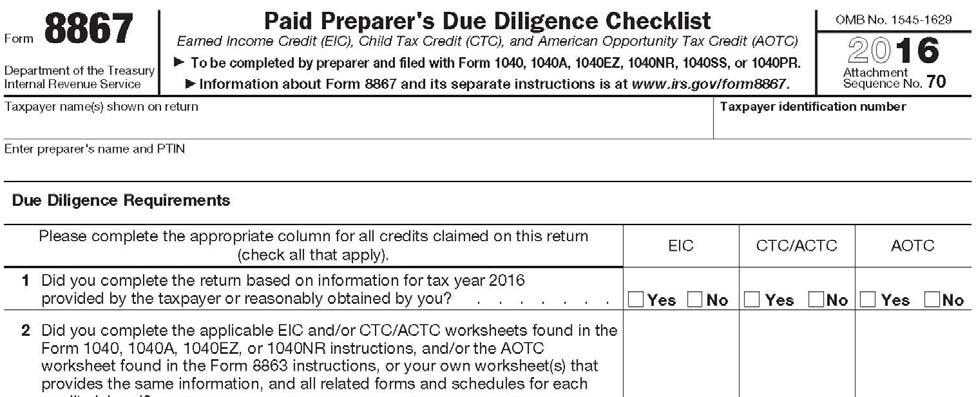

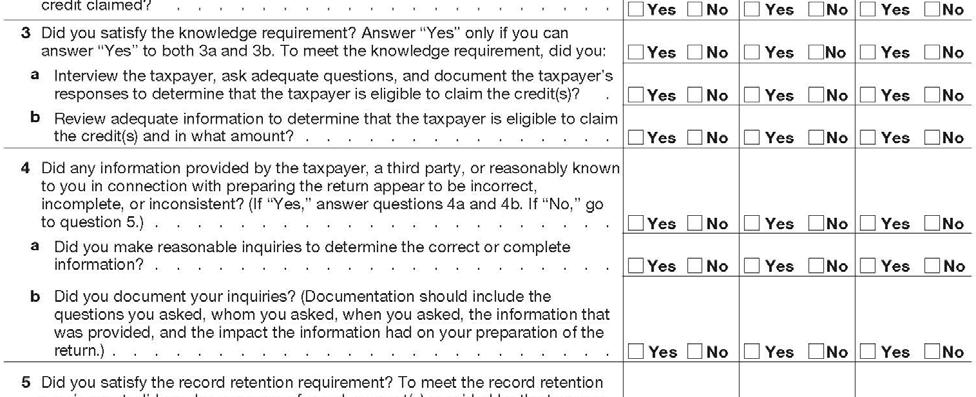

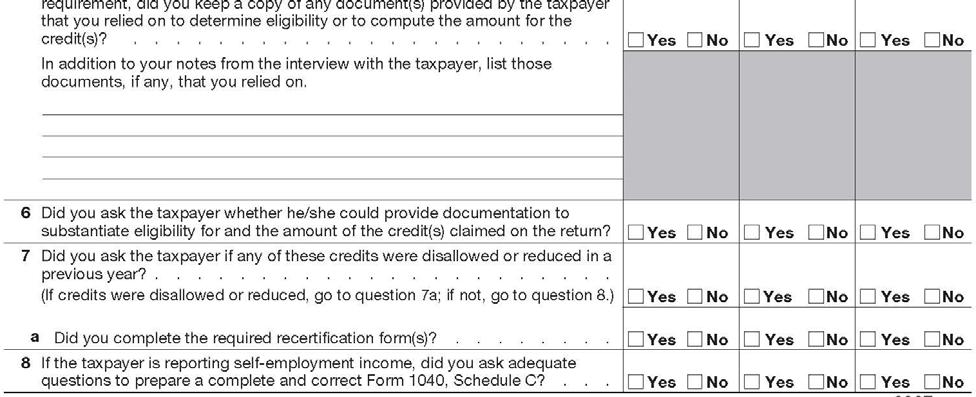

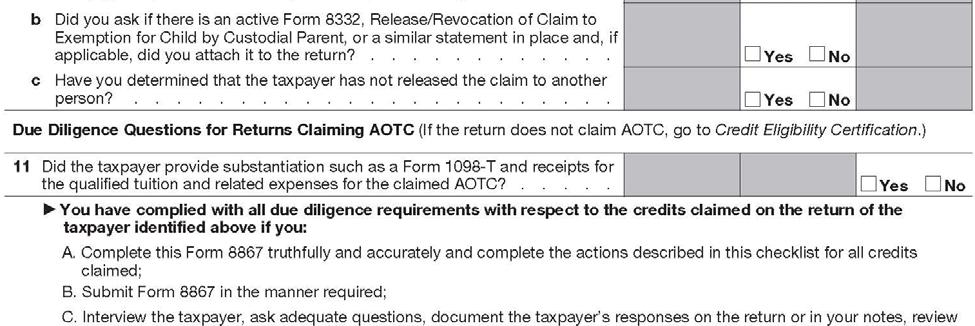

12 Evolution of Form 8867 The evolution of Form 8867 is instructive of how the IRS, over time, is increasingly making you the front-line guardian of the fisc

13

14 2013 Cont. 13

15

16 2016 Cont. 15

17 IRS Website The IRS has also devoted significant resources to update, educate and provide sample materials to return prepares as to the Due Diligence Requirements for the EITC and CTC. There are literally dozens of pages devoted to EITC compliance including video on-line CPE and handout materials. The following page is an example. 16

18 17

19 18

20 19

21 Conclusion Since the 1980 s, 1 in 5 returns claiming the EITC have errors either by mistake or outright fraud. The solution is becoming apparent. You, as the tax preparers, are now, like it or not, EITC auditors. And if you do not document asking your clients the right questions, or keep the right documents in your file, it could cost you $500 per mistake. 20

Earned Income Tax Credit Due Diligence: What Questions to Ask and What Documents to Keep

Earned Income Tax Credit Due Diligence: What Questions to Ask and What Documents to Keep Presented By: Kyle Coleman Coleman, Anastopulos, & Jackson, P.C. 16250 Knoll Trail Drive, Suite 105, Dallas, TX

Earned Income Tax Credit Due Diligence: What Questions to Ask and What Documents to Keep Presented By: Kyle Coleman Coleman, Anastopulos, & Jackson, P.C. 16250 Knoll Trail Drive, Suite 105, Dallas, TX

SUMMARY: This document contains temporary regulations that modify existing

This document is scheduled to be published in the Federal Register on 12/05/2016 and available online at https://federalregister.gov/d/2016-28993, and on FDsys.gov [4830-01-p] DEPARTMENT OF THE TREASURY

This document is scheduled to be published in the Federal Register on 12/05/2016 and available online at https://federalregister.gov/d/2016-28993, and on FDsys.gov [4830-01-p] DEPARTMENT OF THE TREASURY

RETURN PREPARER PENALTIES UNDER TITLE 26

RETURN PREPARER PENALTIES UNDER TITLE 26 Bio Garrett Gregory Received JD from South Texas College of Law in 1999 Member of the Texas State Bar as of 1999 Received Master of Laws (Taxation) from Boston

RETURN PREPARER PENALTIES UNDER TITLE 26 Bio Garrett Gregory Received JD from South Texas College of Law in 1999 Member of the Texas State Bar as of 1999 Received Master of Laws (Taxation) from Boston

Conflicts of Interest Concerns for Tax Professionals. Kyle Coleman

Conflicts of Interest Concerns for Tax Professionals Presented By: Kyle Coleman Coleman, Anastopulos & Jackson, P.C. 16250 Knoll Trail Drive, Suite 105, Dallas, TX 75248 Phone: (972) 810 4380 Fax: (972)

Conflicts of Interest Concerns for Tax Professionals Presented By: Kyle Coleman Coleman, Anastopulos & Jackson, P.C. 16250 Knoll Trail Drive, Suite 105, Dallas, TX 75248 Phone: (972) 810 4380 Fax: (972)

Tax Return Preparer Due Diligence Penalty under Section 6695(g) ACTION: Final regulation and removal of temporary regulation.

ACTION: Final regulation and removal of temporary regulation.") This document is scheduled to be published in the Federal Register on 11/07/2018 and available online at https://federalregister.gov/d/2018-24411, and on govinfo.gov [4830-01-p] DEPARTMENT OF THE TREASURY

This document is scheduled to be published in the Federal Register on 11/07/2018 and available online at https://federalregister.gov/d/2018-24411, and on govinfo.gov [4830-01-p] DEPARTMENT OF THE TREASURY

78816 Federal Register / Vol. 76, No. 244 / Tuesday, December 20, 2011 / Rules and Regulations

78816 Federal Register / Vol. 76, No. 244 / Tuesday, December 20, 2011 / Rules and Regulations (2) Each milliliter of cyclosporine oral solution, USP (MODIFIED) contains 100 mg cyclosporine. * * * * *

78816 Federal Register / Vol. 76, No. 244 / Tuesday, December 20, 2011 / Rules and Regulations (2) Each milliliter of cyclosporine oral solution, USP (MODIFIED) contains 100 mg cyclosporine. * * * * *

Tax Return Preparer Due Diligence Penalty under Section 6695(g)

") This document is scheduled to be published in the Federal Register on 07/18/2018 and available online at https://federalregister.gov/d/2018-15351, and on govinfo.gov [4830-01-p] DEPARTMENT OF THE TREASURY

This document is scheduled to be published in the Federal Register on 07/18/2018 and available online at https://federalregister.gov/d/2018-15351, and on govinfo.gov [4830-01-p] DEPARTMENT OF THE TREASURY

Chapter 5: Personal Tax Credits. 05: Personal Tax Credits

Page 55-68 Chapter 5: Personal Tax Credits 1 Learning Objectives Page 55-68 Upon completion of this seminar, participants should be able to Identify personal tax credits for which our clients may qualify

Page 55-68 Chapter 5: Personal Tax Credits 1 Learning Objectives Page 55-68 Upon completion of this seminar, participants should be able to Identify personal tax credits for which our clients may qualify

Revised (And Revised Again) Internal Revenue Code Section 6694 And New IRS Guidance

Internal Revenue Code Section 6694 And New IRS Guidance") College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 2008 Revised (And Revised Again) Internal Revenue

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 2008 Revised (And Revised Again) Internal Revenue

EITC Due Diligence i

EITC Due Diligence i ALL RIGHTS RESERVED. NO PART OF THIS COURSE MAY BE REPRODUCED IN ANY FORM OR BY ANY MEANS WITHOUT THE WRITTEN PERMISSION OF THE COPYRIGHT HOLDER. All materials relating to this course

EITC Due Diligence i ALL RIGHTS RESERVED. NO PART OF THIS COURSE MAY BE REPRODUCED IN ANY FORM OR BY ANY MEANS WITHOUT THE WRITTEN PERMISSION OF THE COPYRIGHT HOLDER. All materials relating to this course

Offer-in-Compromise Why or Why Not

Why or Why Not The Capital of Texas Enrolled Agents November 2010 by: lg brooks, ea Why or Why Not Table of Contents Introduction 3 The Offer Process 4 The Offer in Compromise: Offers in General 4 Grounds

Why or Why Not The Capital of Texas Enrolled Agents November 2010 by: lg brooks, ea Why or Why Not Table of Contents Introduction 3 The Offer Process 4 The Offer in Compromise: Offers in General 4 Grounds

Earned Income Credit i

Earned Income Credit i ALL RIGHTS RESERVED. NO PART OF THIS COURSE MAY BE REPRODUCED IN ANY FORM OR BY ANY MEANS WITHOUT THE WRITTEN PERMISSION OF THE COPYRIGHT HOLDER. All materials relating to this course

Earned Income Credit i ALL RIGHTS RESERVED. NO PART OF THIS COURSE MAY BE REPRODUCED IN ANY FORM OR BY ANY MEANS WITHOUT THE WRITTEN PERMISSION OF THE COPYRIGHT HOLDER. All materials relating to this course

Prepare, print, and e-file your federal tax return for free!

Prepare, print, and e-file your federal tax return for free! www.freetaxusa.com Form 8867 Department of the Treasury Internal Revenue Service Taxpayer name(s) shown on return Paid Preparer s Due Diligence

Prepare, print, and e-file your federal tax return for free! www.freetaxusa.com Form 8867 Department of the Treasury Internal Revenue Service Taxpayer name(s) shown on return Paid Preparer s Due Diligence

All Rights Reserved The Phoenix Tax Group

All Rights Reserved 2017 The Phoenix Tax Group United States Public Laws, Federal Regulations and decisions of administrative and executive agencies and courts of the United States, are in the public domain.

All Rights Reserved 2017 The Phoenix Tax Group United States Public Laws, Federal Regulations and decisions of administrative and executive agencies and courts of the United States, are in the public domain.

New Standards For Advisors and Tax Returns Preparers Under IRC 6694 and Circular

New Standards For Advisors and Tax Returns Preparers Under IRC 6694 and Circular 230 10.34 Spring 2008 Symposium Income and Transfer Tax Planning Group Real Property, Trust & Estate Law Section American

New Standards For Advisors and Tax Returns Preparers Under IRC 6694 and Circular 230 10.34 Spring 2008 Symposium Income and Transfer Tax Planning Group Real Property, Trust & Estate Law Section American

State Tax Return PENALTIES FOR GEORGIA TAX RETURN PREPARERS

June 2009 State Tax Return Volume 16 Number 2 PENALTIES FOR GEORGIA TAX RETURN PREPARERS E. Kendrick Smith Shane A. Lord Atlanta Atlanta (404) 581-8343 (404) 581-8055 On March 30, 2009, the Georgia General

June 2009 State Tax Return Volume 16 Number 2 PENALTIES FOR GEORGIA TAX RETURN PREPARERS E. Kendrick Smith Shane A. Lord Atlanta Atlanta (404) 581-8343 (404) 581-8055 On March 30, 2009, the Georgia General

Prepare, Print, and E-File Your Federal Tax Return for FREE!!

Free Forms Courtesy of FreeTaxUSA.com Prepare, Print, and E-File Your Federal Tax Return for FREE!! Go to www.freetaxusa.com to start your free return today! Form 8867 Department of the Treasury Internal

Free Forms Courtesy of FreeTaxUSA.com Prepare, Print, and E-File Your Federal Tax Return for FREE!! Go to www.freetaxusa.com to start your free return today! Form 8867 Department of the Treasury Internal

Tax Return Preparer Ethical Issues

Tax Return Preparer Ethical Issues i This document is designed to provide general information and is not a substitute for professional advice in specific situations. It is not intended to be, and should

Tax Return Preparer Ethical Issues i This document is designed to provide general information and is not a substitute for professional advice in specific situations. It is not intended to be, and should

Law Office of W. Mark Scott, PLLC

The Resurgence of Whistleblowers in IRS Bond Enforcement By: W. Mark Scott I. THERE AND BACK AGAIN The IRS Office of Tax Exempt Bonds received a significant number of whistleblower tips during my tenure

The Resurgence of Whistleblowers in IRS Bond Enforcement By: W. Mark Scott I. THERE AND BACK AGAIN The IRS Office of Tax Exempt Bonds received a significant number of whistleblower tips during my tenure

David C. Gair. Partner

Board Certified in Tax Law by the Texas Board of Legal Specialization and Leader of the Tax Controversy Practice Group, David Gair focuses his practice on guiding businesses, high-net-worth individuals

Board Certified in Tax Law by the Texas Board of Legal Specialization and Leader of the Tax Controversy Practice Group, David Gair focuses his practice on guiding businesses, high-net-worth individuals

TAX RETURN PREPARER ETHICAL ISSUES

TAX RETURN PREPARER ETHICAL ISSUES Published by Fast Forward Academy, LLC https://fastforwardacademy.com (888) 798-PASS (7277) 2017 Fast Forward Academy, LLC All rights reserved. No part of this publication

TAX RETURN PREPARER ETHICAL ISSUES Published by Fast Forward Academy, LLC https://fastforwardacademy.com (888) 798-PASS (7277) 2017 Fast Forward Academy, LLC All rights reserved. No part of this publication

Form 8858 Reporting of U.S. Owned Foreign Disregarded Entities: Ownership and Correct Filing Status

Form 8858 Reporting of U.S. Owned Foreign Disregarded Entities: Ownership and Correct Filing Status FOR LIVE PROGRAM ONLY TUESDAY, JANUARY 9, 2018 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

Form 8858 Reporting of U.S. Owned Foreign Disregarded Entities: Ownership and Correct Filing Status FOR LIVE PROGRAM ONLY TUESDAY, JANUARY 9, 2018 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

Tax return preparers beware of trumped-up due diligence standards

ABSTRACT Tax return preparers beware of trumped-up due diligence standards Gregory Clifton Metropolitan State University of Denver Elizabeth Conner University of Colorado Denver Doug Laufer Metropolitan

ABSTRACT Tax return preparers beware of trumped-up due diligence standards Gregory Clifton Metropolitan State University of Denver Elizabeth Conner University of Colorado Denver Doug Laufer Metropolitan

Ethics and Professional Responsibility for Enrolled Agents

Ethics and Professional Responsibility for Enrolled Agents #4525M COURSE MATERIAL TABLE OF CONTENTS Chapter 1: IRS Circular 230 1 Chapter 1: Test Your Knowledge 33 Chapter 1: Solutions and Suggested Responses

Ethics and Professional Responsibility for Enrolled Agents #4525M COURSE MATERIAL TABLE OF CONTENTS Chapter 1: IRS Circular 230 1 Chapter 1: Test Your Knowledge 33 Chapter 1: Solutions and Suggested Responses

Earned Income Tax Credit

Earned Income Tax Credit (EITC) Department of the Treasury Internal Revenue Service www.irs.gov Letter from the Commissioner October 19, 1999 Dear Tax Professional, You have just opened the year 2000 Tax

Earned Income Tax Credit (EITC) Department of the Treasury Internal Revenue Service www.irs.gov Letter from the Commissioner October 19, 1999 Dear Tax Professional, You have just opened the year 2000 Tax

Circular 230 Changes Affecting Employee Benefits

Circular 230 Changes Affecting Employee Benefits Charles F. Plenge Haynes and Boone, LLP October 22, 2011 Who May Practice Attorneys Certified Public Accountants (CPAs) Enrolled Agents (EAs) Enrolled Actuaries

Circular 230 Changes Affecting Employee Benefits Charles F. Plenge Haynes and Boone, LLP October 22, 2011 Who May Practice Attorneys Certified Public Accountants (CPAs) Enrolled Agents (EAs) Enrolled Actuaries

2:16-cv PDB-SDD Doc # 1 Filed 01/28/16 Pg 1 of 30 Pg ID 1

2:16-cv-10299-PDB-SDD Doc # 1 Filed 01/28/16 Pg 1 of 30 Pg ID 1 IN THE UNITED STATES DISTRICT COURT FOR THE EASTERN DISTRICT OF MICHIGAN SOUTHERN DIVISION UNITED STATES OF AMERICA, ) ) Plaintiff, ) ) v.

2:16-cv-10299-PDB-SDD Doc # 1 Filed 01/28/16 Pg 1 of 30 Pg ID 1 IN THE UNITED STATES DISTRICT COURT FOR THE EASTERN DISTRICT OF MICHIGAN SOUTHERN DIVISION UNITED STATES OF AMERICA, ) ) Plaintiff, ) ) v.

Applications and Due Diligence of the Earned Income Tax Credit

Applications and Due Diligence of the Earned Income Tax Credit Developed by Raven Deerwater, EA, PhD CSEA President Palomar Chapter December 19, 2012 Raven Deerwater EA, Ph.D has a tax practice in Mendocino,

Applications and Due Diligence of the Earned Income Tax Credit Developed by Raven Deerwater, EA, PhD CSEA President Palomar Chapter December 19, 2012 Raven Deerwater EA, Ph.D has a tax practice in Mendocino,

Self-Disclosure: Why, When, Where and How

American Bar Association Washington Health Law Summit Self-Disclosure: Why, When, Where and How December 8, 2015 Margaret Hutchinson U.S. Attorney s Office for the Eastern District of Pennsylvania Kaitlyn

American Bar Association Washington Health Law Summit Self-Disclosure: Why, When, Where and How December 8, 2015 Margaret Hutchinson U.S. Attorney s Office for the Eastern District of Pennsylvania Kaitlyn

2017 Updates on Tax Ethics

2017 Updates on Tax Ethics Frank J. Rooney, Esquire Rooney Law Firm Offices in CO, MD and VA 303-534-1690 Colorado 703-527-2660 Virginia 301-984-7505 Maryland 703-636-4445 Fax www.irsequalizer.com Course

2017 Updates on Tax Ethics Frank J. Rooney, Esquire Rooney Law Firm Offices in CO, MD and VA 303-534-1690 Colorado 703-527-2660 Virginia 301-984-7505 Maryland 703-636-4445 Fax www.irsequalizer.com Course

Circular 230 and Preparer Penalties: Evil Siblings for Practitioners

Maurice A. Deane School of Law at Hofstra University Scholarly Commons at Hofstra Law Hofstra Law Faculty Scholarship 4-28-2008 and Preparer Penalties: Evil Siblings for Practitioners Jonathan G. Blattmachr

Maurice A. Deane School of Law at Hofstra University Scholarly Commons at Hofstra Law Hofstra Law Faculty Scholarship 4-28-2008 and Preparer Penalties: Evil Siblings for Practitioners Jonathan G. Blattmachr

Goals for Today s Presentation

AMERICAN HEALTH LAWYERS ASSOCIATION Institute on Medicare and Medicaid Payment Issues March 20-22, 2013 Baltimore, Maryland Medicare and Medicaid Overpayments and Refunds Presented by: Robert L. Roth,

AMERICAN HEALTH LAWYERS ASSOCIATION Institute on Medicare and Medicaid Payment Issues March 20-22, 2013 Baltimore, Maryland Medicare and Medicaid Overpayments and Refunds Presented by: Robert L. Roth,

Earned Income Table. Earned Income

Includes Taxable wages, salaries, and tips Union strike benefits Taxable long-term disability benefits received prior to minimum retirement age Net earnings from self-employment Gross income of a statutory

Includes Taxable wages, salaries, and tips Union strike benefits Taxable long-term disability benefits received prior to minimum retirement age Net earnings from self-employment Gross income of a statutory

TAX PREPARER PENALTIES

TAX PREPARER PENALTIES Prepared by the Tax Department of GIBSON & PERKINS, PC Suite 204 100 W. Sixth Street, Media, PA 19063 610-565-1708 www.gibperk.com LEARNING OBJECTIVES: Course participants will gain

TAX PREPARER PENALTIES Prepared by the Tax Department of GIBSON & PERKINS, PC Suite 204 100 W. Sixth Street, Media, PA 19063 610-565-1708 www.gibperk.com LEARNING OBJECTIVES: Course participants will gain

INDIVIDUAL TAX BREAKS IN THE PROTECTING AMERICANS FROM TAX HIKES ACT

Page 1 of 6 INDIVIDUAL TAX BREAKS IN THE PROTECTING AMERICANS FROM TAX HIKES ACT On December 18, Congress passed and the President signed into law a bipartisan, bicameral agreement on tax extenders - i.e.,

Page 1 of 6 INDIVIDUAL TAX BREAKS IN THE PROTECTING AMERICANS FROM TAX HIKES ACT On December 18, Congress passed and the President signed into law a bipartisan, bicameral agreement on tax extenders - i.e.,

GUIDANCE TO PRACTITIONERS REGARDING PROFESSIONAL OBLIGATIONS UNDER TREASURY CIRCULAR NO. 230 Who is Subject to Treasury Circular No.

GUIDANCE TO PRACTITIONERS REGARDING PROFESSIONAL OBLIGATIONS UNDER TREASURY CIRCULAR NO. 230 Who is Subject to Treasury Circular No. 230 1 The provisions of Treasury Circular No. 230 apply to: Attorneys

GUIDANCE TO PRACTITIONERS REGARDING PROFESSIONAL OBLIGATIONS UNDER TREASURY CIRCULAR NO. 230 Who is Subject to Treasury Circular No. 230 1 The provisions of Treasury Circular No. 230 apply to: Attorneys

IRS RETURN PREPARER TEST SPECIFICATIONS

IRS RETURN PREPARER TEST SPECIFICATIONS GLEIM Comment: Please do not spend time reading, studying, etc. these specifications. We have analyzed them line by line to assure a complete and all-inclusive study

IRS RETURN PREPARER TEST SPECIFICATIONS GLEIM Comment: Please do not spend time reading, studying, etc. these specifications. We have analyzed them line by line to assure a complete and all-inclusive study

STANDARD DEDUCTIONS MACRS RECOVERY PERIODS

217 Medical Savings Accounts (MSA) 217 Annual Deductible Range Self-Only Coverage 2,25-3,35 Family Coverage 4,5-6,75 Maximum Out of Pocket Self-Only Coverage 4,5 Family Coverage 8,25 STANDARD DEDUCTIONS

217 Medical Savings Accounts (MSA) 217 Annual Deductible Range Self-Only Coverage 2,25-3,35 Family Coverage 4,5-6,75 Maximum Out of Pocket Self-Only Coverage 4,5 Family Coverage 8,25 STANDARD DEDUCTIONS

Make Tax Time Pay! New Developments 2009

Make Tax Time Pay! New Developments 2009 Presentation by: John Wancheck Organization: Center on Budget and Policy Priorities Website: www.cbpp.org/eic2008 Phone: (202) 408-1080 Email: wancheck@cbpp.org

Make Tax Time Pay! New Developments 2009 Presentation by: John Wancheck Organization: Center on Budget and Policy Priorities Website: www.cbpp.org/eic2008 Phone: (202) 408-1080 Email: wancheck@cbpp.org

RENEWAL APPLICATION FOR EMPLOYED LAWYERS PROFESSIONAL LIABILITY INSURANCE

Executive Risk 82 Hopmeadow Street Simsbury, Connecticut 06070-7683 Management Associates RENEWAL APPLICATION FOR EMPLOYED LAWYERS PROFESSIONAL LIABILITY INSURANCE THIS APPLICATION IS FOR CLAIMS MADE AND

Executive Risk 82 Hopmeadow Street Simsbury, Connecticut 06070-7683 Management Associates RENEWAL APPLICATION FOR EMPLOYED LAWYERS PROFESSIONAL LIABILITY INSURANCE THIS APPLICATION IS FOR CLAIMS MADE AND

National Association of Tax Professionals

National Association of Tax Professionals Comments on Tax Return Preparer Penalties Under 6694 and 6695 August 15, 2008 Background The National Association of Tax Professionals (NATP) is a nonprofit professional

National Association of Tax Professionals Comments on Tax Return Preparer Penalties Under 6694 and 6695 August 15, 2008 Background The National Association of Tax Professionals (NATP) is a nonprofit professional

ALI-ABA Course of Study How To Handle a Tax Controversy at the IRS and in Court: From Administrative Audit Through Litigation

191 ALI-ABA Course of Study How To Handle a Tax Controversy at the IRS and in Court: From Administrative Audit Through Litigation Sponsored with the cooperation of the ABA Section of Taxation June 24-25,

191 ALI-ABA Course of Study How To Handle a Tax Controversy at the IRS and in Court: From Administrative Audit Through Litigation Sponsored with the cooperation of the ABA Section of Taxation June 24-25,

THE ELITE QUARTERLY Ethics for Enrolled Agents

THE ELITE QUARTERLY Ethics for Enrolled Agents Published by CPElite, Inc The Leader in Continuing Professional Education Newsletters 444444444444444444444444444444444444444444444444444444444444444444444444444444

THE ELITE QUARTERLY Ethics for Enrolled Agents Published by CPElite, Inc The Leader in Continuing Professional Education Newsletters 444444444444444444444444444444444444444444444444444444444444444444444444444444

Q&A s???? ???? Revenue Protection Strategy IRS. Messages for the 1999 Filing Season. Department of the Treasury Internal Revenue Service

Revenue Protection Strategy Messages for the 1999 Filing Season Q&A s???? IRS Department of the Treasury Internal Revenue Service???? Publication 3357 (1-1999) Catalog Number 27193I Table of Contents Introduction

Revenue Protection Strategy Messages for the 1999 Filing Season Q&A s???? IRS Department of the Treasury Internal Revenue Service???? Publication 3357 (1-1999) Catalog Number 27193I Table of Contents Introduction

ATIONAL TAX PRACTICE INSTITUTE LEVEL

NATIONAL TAX PRACTICE INSTITUTE LEVEL 1 Representation Ethics August 6, 2013 LG Brooks, EA LG Brooks, EA is a senior consultant at The Tax Practice, Inc. in Dallas, Texas, a representation firm. He has

NATIONAL TAX PRACTICE INSTITUTE LEVEL 1 Representation Ethics August 6, 2013 LG Brooks, EA LG Brooks, EA is a senior consultant at The Tax Practice, Inc. in Dallas, Texas, a representation firm. He has

Federal Income Taxes and Noncitizens: Frequently Asked Questions

Federal Income Taxes and Noncitizens: Frequently Asked Questions Erika K. Lunder Legislative Attorney Margot L. Crandall-Hollick Analyst in Public Finance December 31, 2014 Congressional Research Service

Federal Income Taxes and Noncitizens: Frequently Asked Questions Erika K. Lunder Legislative Attorney Margot L. Crandall-Hollick Analyst in Public Finance December 31, 2014 Congressional Research Service

The Scoop. Agenda 7/24/2018. July 25, 2018

Center for Agricultural Law & Taxation The Scoop July 25, 2018 Agenda Miscellaneous Itemized Deductions for Estates and Trusts Notice 2018 61 Understanding Your CP3219A Notice Some Veterans Can Now Claim

Center for Agricultural Law & Taxation The Scoop July 25, 2018 Agenda Miscellaneous Itemized Deductions for Estates and Trusts Notice 2018 61 Understanding Your CP3219A Notice Some Veterans Can Now Claim

"It's Not My Fault": Scope of Reasonable Cause And Good Faith Exception to Tax Penalties

THE UNIVERSITY OF TEXAS SCHOOL OF LAW Presented: 61st Annual Taxation Conference December 4-5, 2013 Austin, Texas "It's Not My Fault": Scope of Reasonable Cause And Good Faith Exception to Tax Penalties

THE UNIVERSITY OF TEXAS SCHOOL OF LAW Presented: 61st Annual Taxation Conference December 4-5, 2013 Austin, Texas "It's Not My Fault": Scope of Reasonable Cause And Good Faith Exception to Tax Penalties

This revenue procedure facilitates the grant of relief to taxpayers that request

26 CFR 601.105: Examination of returns and claims for refund, credit or abatement; determination of correct tax liability. (Also: Part I, 1361, 1362; 1.1361-1, 1.1361-3, 1.1362-4, 1.1362-6, 301.7701-3,

26 CFR 601.105: Examination of returns and claims for refund, credit or abatement; determination of correct tax liability. (Also: Part I, 1361, 1362; 1.1361-1, 1.1361-3, 1.1362-4, 1.1362-6, 301.7701-3,

Norman A. "Norm" Lofgren Senior Counsel

Norm Lofgren focuses his practice on helping clients build and protect their businesses, minimize tax exposure and preserve wealth from generation to generation. Norm s clients include domestic and international

Norm Lofgren focuses his practice on helping clients build and protect their businesses, minimize tax exposure and preserve wealth from generation to generation. Norm s clients include domestic and international

August 1, Via Federal erulemaking Portal. Internal Revenue Service CC:PA:LPD:PR (REG )

") Page: 1 of 15 August 1, 2017 Via Federal erulemaking Portal Internal Revenue Service CC:PA:LPD:PR (REG-136118-15) Courier s Desk Internal Revenue Service 1111 Constitution Avenue, N.W. Washington, D.C.

Page: 1 of 15 August 1, 2017 Via Federal erulemaking Portal Internal Revenue Service CC:PA:LPD:PR (REG-136118-15) Courier s Desk Internal Revenue Service 1111 Constitution Avenue, N.W. Washington, D.C.

Mastering Form 8937 and Section 6045B:

Presenting a live 110 minute teleconference with interactive Q&A Mastering Form 8937 and Section 6045B: An Ongoing Obligation Complying With Reporting Requirements Arising From Activities Affecting Tax

Presenting a live 110 minute teleconference with interactive Q&A Mastering Form 8937 and Section 6045B: An Ongoing Obligation Complying With Reporting Requirements Arising From Activities Affecting Tax

The 2011 Amendments to Circular 230: What's Ahead

CAPLIN & DRYSDALE, CHARTERED ONE THOMAS CIRCLE, N.W. SUITE 1100 WASHINGTON, DC 20005 The 2011 Amendments to Circular 230: What's Ahead Matthew C. Hicks On August 2, 2011, the recent amendments to Treasury

CAPLIN & DRYSDALE, CHARTERED ONE THOMAS CIRCLE, N.W. SUITE 1100 WASHINGTON, DC 20005 The 2011 Amendments to Circular 230: What's Ahead Matthew C. Hicks On August 2, 2011, the recent amendments to Treasury

Client Side Penalties A Look at 6662 and It s Influence on Preparer Sanctions Podcast of June 29, 2007

Client Side Penalties A Look at 6662 and It s Influence on Preparer Sanctions Podcast of June 29, 2007 Feed address for Podcast subscription: http://feeds.feedburner.com/edzollarstaxupdate Home page for

Client Side Penalties A Look at 6662 and It s Influence on Preparer Sanctions Podcast of June 29, 2007 Feed address for Podcast subscription: http://feeds.feedburner.com/edzollarstaxupdate Home page for

IRS RETURN PREPARER TEST SPECIFICATIONS

IRS RETURN PREPARER TEST SPECIFICATIONS August 31, 2011 Preface It is the goal of the IRS to administer a test that is founded on basic preparer competency. As such, the Registered Tax Return Preparer

IRS RETURN PREPARER TEST SPECIFICATIONS August 31, 2011 Preface It is the goal of the IRS to administer a test that is founded on basic preparer competency. As such, the Registered Tax Return Preparer

3:16-cv MGL Date Filed 02/08/16 Entry Number 1 Page 1 of 37

3:16-cv-00373-MGL Date Filed 02/08/16 Entry Number 1 Page 1 of 37 IN THE UNITED STATES DISTRICT COURT FOR THE DISTRICT OF SOUTH CAROLINA COLUMBIA DIVISION THE UNITED STATES OF AMERICA, ) ) Plaintiff, )

3:16-cv-00373-MGL Date Filed 02/08/16 Entry Number 1 Page 1 of 37 IN THE UNITED STATES DISTRICT COURT FOR THE DISTRICT OF SOUTH CAROLINA COLUMBIA DIVISION THE UNITED STATES OF AMERICA, ) ) Plaintiff, )

1 SB By Senator Melson. 4 RFD: Finance and Taxation General Fund. 5 First Read: 08-SEP-15. Page 0

1 SB20 2 171723-1 3 By Senator Melson 4 RFD: Finance and Taxation General Fund 5 First Read: 08-SEP-15 Page 0 1 171723-1:n:09/08/2015:LFO-RR*/ccd 2 3 4 5 6 7 8 SYNOPSIS: This bill would provide for an

1 SB20 2 171723-1 3 By Senator Melson 4 RFD: Finance and Taxation General Fund 5 First Read: 08-SEP-15 Page 0 1 171723-1:n:09/08/2015:LFO-RR*/ccd 2 3 4 5 6 7 8 SYNOPSIS: This bill would provide for an

DALLAS BAR ASSOCIATION TAX SECTION

DALLAS BAR ASSOCIATION TAX SECTION DECEMBER 4, 2017 DALLAS, TX NEW PARTNERSHIP AUDIT RULES: WHAT THEY MEAN TO PARTNERSHIPS AND TAX PROFESSIONALS Presented by: CHARLES D. PULMAN, J.D., LL.M., CPA MATTHEW

DALLAS BAR ASSOCIATION TAX SECTION DECEMBER 4, 2017 DALLAS, TX NEW PARTNERSHIP AUDIT RULES: WHAT THEY MEAN TO PARTNERSHIPS AND TAX PROFESSIONALS Presented by: CHARLES D. PULMAN, J.D., LL.M., CPA MATTHEW

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Results of the 2015 Filing Season August 31, 2015 Reference Number: 2015-40-080 This report has cleared the Treasury Inspector General for Tax Administration

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Results of the 2015 Filing Season August 31, 2015 Reference Number: 2015-40-080 This report has cleared the Treasury Inspector General for Tax Administration

26 CFR : Examination of returns and claims for refund, credit or abatement; determination of correct tax liability.

Part III Administrative, Procedural, and Miscellaneous 26 CFR 601.105: Examination of returns and claims for refund, credit or abatement; determination of correct tax liability. (Also: Part 1, 6662, 6694,

Part III Administrative, Procedural, and Miscellaneous 26 CFR 601.105: Examination of returns and claims for refund, credit or abatement; determination of correct tax liability. (Also: Part 1, 6662, 6694,

2012 Health Law Education Program: Anatomy of a Self- Disclosure Telling CMS About Your Stark Law Problems

2012 Health Law Education Program: Anatomy of a Self- Disclosure Telling CMS About Your Stark Law Problems October 24, 2012 12:00 p.m. 1:00 p.m. Central Web Seminar Continuing Education Information We

2012 Health Law Education Program: Anatomy of a Self- Disclosure Telling CMS About Your Stark Law Problems October 24, 2012 12:00 p.m. 1:00 p.m. Central Web Seminar Continuing Education Information We

ETHICS. Presented by: Melinda Garvin, EA. Melinda Garvin, EA 12/14/2016

ETHICS Presented by: Melinda Garvin, EA Melinda Garvin, EA Melinda is the Founder, President and Co- Owner of Foos-Garvin Accounting, Inc., a full-service, small-town practice serving the needs of 2000

ETHICS Presented by: Melinda Garvin, EA Melinda Garvin, EA Melinda is the Founder, President and Co- Owner of Foos-Garvin Accounting, Inc., a full-service, small-town practice serving the needs of 2000

Regulations under IRC Section 7430 Relating to Awards of Administrative Costs and Attorneys Fees

This document is scheduled to be published in the Federal Register on 03/01/2016 and available online at http://federalregister.gov/a/2016-04401, and on FDsys.gov [4830-01-p] DEPARTMENT OF THE TREASURY

This document is scheduled to be published in the Federal Register on 03/01/2016 and available online at http://federalregister.gov/a/2016-04401, and on FDsys.gov [4830-01-p] DEPARTMENT OF THE TREASURY

FORGIVE AND FORGET - - THE CALIFORNIA EMPLOYMENT TAX AMNESTY. By Steven Toscher, Esq. March, 1995

FORGIVE AND FORGET - - THE CALIFORNIA EMPLOYMENT TAX AMNESTY By Steven Toscher, Esq. March, 1995 INTRODUCTION Should a taxing authority be able to forgive and forget - - that is, grant amnesty to taxpayers

FORGIVE AND FORGET - - THE CALIFORNIA EMPLOYMENT TAX AMNESTY By Steven Toscher, Esq. March, 1995 INTRODUCTION Should a taxing authority be able to forgive and forget - - that is, grant amnesty to taxpayers

Ch. 119 LIABILITIES AND ASSESSMENT CHAPTER 119. LIABILITIES AND ASSESSMENT PROCEDURE AND ADMINISTRATION

Ch. 119 LIABILITIES AND ASSESSMENT 61 119.1 CHAPTER 119. LIABILITIES AND ASSESSMENT PROCEDURE AND ADMINISTRATION Sec. 119.1. Payment on notice and demand. 119.2. Assessment. 119.3. Bankruptcy or receivership.

Ch. 119 LIABILITIES AND ASSESSMENT 61 119.1 CHAPTER 119. LIABILITIES AND ASSESSMENT PROCEDURE AND ADMINISTRATION Sec. 119.1. Payment on notice and demand. 119.2. Assessment. 119.3. Bankruptcy or receivership.

Specialty Law Columns Estate and Trust Forum The Perilous Federal Gift Tax Return--Part I by Thomas L. Stover

The Colorado Lawyer November 1999 Vol. 28, No. 11 [Page 71] 1999 The Colorado Lawyer and Colorado Bar Association. All Rights Reserved. Editor's Note: Specialty Law Columns Estate and Trust Forum The Perilous

The Colorado Lawyer November 1999 Vol. 28, No. 11 [Page 71] 1999 The Colorado Lawyer and Colorado Bar Association. All Rights Reserved. Editor's Note: Specialty Law Columns Estate and Trust Forum The Perilous

2017 Annual Federal Tax Refresher (AFTR) Course. Domain 3 Ethics, Practices, and Procedures

Course. Domain 3 Ethics, Practices, and Procedures") P a g e 1 2017 Annual Federal Tax Refresher (AFTR) Course Domain 3 Ethics, Practices, and Procedures Domain 3 of this course is a general review the ethics, practices, and procedures for tax return preparers.

P a g e 1 2017 Annual Federal Tax Refresher (AFTR) Course Domain 3 Ethics, Practices, and Procedures Domain 3 of this course is a general review the ethics, practices, and procedures for tax return preparers.

Certification by U.S. Person Residing in the United States for Streamlined Domestic Offshore Procedures

Form 14654 (June 2016) Department of the Treasury - Internal Revenue Service Certification by U.S. Person Residing in the United States for Streamlined Domestic Offshore Procedures Name(s) of taxpayer(s)

Form 14654 (June 2016) Department of the Treasury - Internal Revenue Service Certification by U.S. Person Residing in the United States for Streamlined Domestic Offshore Procedures Name(s) of taxpayer(s)

Internal Revenue Service. PURPOSE (1) This transmits new IRM , Bank Secrecy Act, Report of Foreign Bank and Financial Accounts (FBAR).

This transmits new IRM , Bank Secrecy Act, Report of Foreign Bank and Financial Accounts (FBAR).") MANUAL TRANSMITTAL Department of the Treasury Internal Revenue Service 4.26.16 JULY 1, 2008 PURPOSE (1) This transmits new IRM 4.26.16, Bank Secrecy Act, Report of Foreign Bank and Financial Accounts (FBAR).

MANUAL TRANSMITTAL Department of the Treasury Internal Revenue Service 4.26.16 JULY 1, 2008 PURPOSE (1) This transmits new IRM 4.26.16, Bank Secrecy Act, Report of Foreign Bank and Financial Accounts (FBAR).

OVDI-OOR: FBAR Penalty Investigation (Post 10/22/04) Lead Sheet

Lead Sheet") Tax Period Previously Assessed Per Exam Adjustment Reference Conclusion: (Reflects the final determination on the issue.) The following techniques are not intended to be all-inclusive nor are they mandatory

Tax Period Previously Assessed Per Exam Adjustment Reference Conclusion: (Reflects the final determination on the issue.) The following techniques are not intended to be all-inclusive nor are they mandatory

Circular 230 Diligence and Competence

Circular 230 Diligence and Competence Thomas V. Curtin October 24, 2016 Statutory Authority 31 U.S.C. 330 (1884) Regulate the practice of representatives of persons before the Department of the Treasury

Circular 230 Diligence and Competence Thomas V. Curtin October 24, 2016 Statutory Authority 31 U.S.C. 330 (1884) Regulate the practice of representatives of persons before the Department of the Treasury

CHAPTER 2: WORKING WITH THE TAX LAW

DOWNLOAD FULL TEST BANK FOR SOUTH WESTERN FEDERAL TAXATION 2015 INDIVIDUAL INCOME TAXES 38TH EDITION BY HOFFMAN AND SMITH Link download full: https://testbankservice.com/download/test-bank-for-south-western-federaltaxation-2015-individual-income-taxes-38th-edition-by-hoffman-and-smith/

DOWNLOAD FULL TEST BANK FOR SOUTH WESTERN FEDERAL TAXATION 2015 INDIVIDUAL INCOME TAXES 38TH EDITION BY HOFFMAN AND SMITH Link download full: https://testbankservice.com/download/test-bank-for-south-western-federaltaxation-2015-individual-income-taxes-38th-edition-by-hoffman-and-smith/

The Board of Directors Government of Guam Retirement Fund

Report on Compliance and Internal Control over Financial Reporting Based on an Audit of Financial Statements Performed in Accordance With Government Auditing Standards The Board of Directors Government

Report on Compliance and Internal Control over Financial Reporting Based on an Audit of Financial Statements Performed in Accordance With Government Auditing Standards The Board of Directors Government

INNOCENT SPOUSE DEFENSE

INNOCENT SPOUSE DEFENSE First Run Broadcast: August 21, 2012 Live Replay: August 16, 2013 1:00 p.m. E.T./12:00 p.m. C.T./11:00 a.m. M.T./10:00 a.m. P.T. (60 minutes) When a married couple files its tax

INNOCENT SPOUSE DEFENSE First Run Broadcast: August 21, 2012 Live Replay: August 16, 2013 1:00 p.m. E.T./12:00 p.m. C.T./11:00 a.m. M.T./10:00 a.m. P.T. (60 minutes) When a married couple files its tax

NEW TAX LAWS RELATING TO IRS EXAMINATION OF AND TAX COLLECTION FROM PARTNERSHIPS: UNDERSTANDING THE NUANCES OF THE NEW LEGISLATION

NEW TAX LAWS RELATING TO IRS EXAMINATION OF AND TAX COLLECTION FROM PARTNERSHIPS: UNDERSTANDING THE NUANCES OF THE NEW LEGISLATION Charles M. Ruchelman, Member, Caplin & Drysdale Gregory T. Armstrong,

NEW TAX LAWS RELATING TO IRS EXAMINATION OF AND TAX COLLECTION FROM PARTNERSHIPS: UNDERSTANDING THE NUANCES OF THE NEW LEGISLATION Charles M. Ruchelman, Member, Caplin & Drysdale Gregory T. Armstrong,

Representing the Innocent Spouse in Pre- and Post-Filing Tax Controversies

Representing the Innocent Spouse in Pre- and Post-Filing Tax Controversies Presented to CPA Academy Lawrence A. Sannicandro, Esq. 1 Overview I. Introduction II. Conflicts of Interest III. Overview of Innocent

Representing the Innocent Spouse in Pre- and Post-Filing Tax Controversies Presented to CPA Academy Lawrence A. Sannicandro, Esq. 1 Overview I. Introduction II. Conflicts of Interest III. Overview of Innocent

AMERICAN INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS COMMENTS ON MODIFICATIONS TO REVENUE PROCEDURES AND

AMERICAN INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS COMMENTS ON MODIFICATIONS TO REVENUE PROCEDURES 97-27 AND 2002-9 Developed by the Accounting Methods Change Task Force Paul K. Gibbs, Task Force Chair

AMERICAN INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS COMMENTS ON MODIFICATIONS TO REVENUE PROCEDURES 97-27 AND 2002-9 Developed by the Accounting Methods Change Task Force Paul K. Gibbs, Task Force Chair

1/19/2017. Agenda. Due Diligence and the Credits for 2016 Ethics (1 hours) Overview of Credits (1 hour Tax Law)

Overview of Credits (1 hour Tax Law)") Due Diligence and the Credits for 2016 Ethics (1 hours) Overview of Credits (1 hour Tax Law) January 19, 2017 Agenda Overview of the Child Tax Credit Additional Child Tax Credit American Opportunity Credit

Due Diligence and the Credits for 2016 Ethics (1 hours) Overview of Credits (1 hour Tax Law) January 19, 2017 Agenda Overview of the Child Tax Credit Additional Child Tax Credit American Opportunity Credit

2017 Instructions for Schedule 8812

Department of the Treasury Internal Revenue Service 2017 Instructions for Schedule 8812 Child Tax Credit Part I of Schedule 8812 documents that any qualifying child whom you identify with an ITIN is a

Department of the Treasury Internal Revenue Service 2017 Instructions for Schedule 8812 Child Tax Credit Part I of Schedule 8812 documents that any qualifying child whom you identify with an ITIN is a

Tax Controversy Corner

Tax Controversy Corner This Will Keep You Up at Night: Firm and Partner Liability for Other Professionals Noncompliance By Megan L. Brackney A recent district court decision involving the IRS s assessment

Tax Controversy Corner This Will Keep You Up at Night: Firm and Partner Liability for Other Professionals Noncompliance By Megan L. Brackney A recent district court decision involving the IRS s assessment

Dallas Bar Association Tax Section December 4, New Partnership Audit Rules: What They Mean to Partnerships and Tax Professionals.

Dallas Bar Association Tax Section December 4, 2017 New Partnership Audit Rules: What They Mean to Partnerships and Tax Professionals Copyright All rights reserved. Presented By: Charles D. Pulman, J.D.,

Dallas Bar Association Tax Section December 4, 2017 New Partnership Audit Rules: What They Mean to Partnerships and Tax Professionals Copyright All rights reserved. Presented By: Charles D. Pulman, J.D.,

Taxpayer Questionnaire

First : Last : Taxpayer Questionnaire PERSONAL INFORMATION Primary Taxpayer M.I.: S.S.N. : Birthdate: Taxpayer's PIN: Home Phone: Work Phone: Cell Phone: Occupation: Email Address: Dependent on another

First : Last : Taxpayer Questionnaire PERSONAL INFORMATION Primary Taxpayer M.I.: S.S.N. : Birthdate: Taxpayer's PIN: Home Phone: Work Phone: Cell Phone: Occupation: Email Address: Dependent on another

SUPPLEMENT A. IRC 1014(f): Basis Must Be Consistent With Estate Tax Return

: Basis Must Be Consistent With Estate Tax Return") SUPPLEMENT A IRC 1014(f): Basis Must Be Consistent With Estate Tax Return For purposes of this section (1) In General. The basis of any property to which subsection (a) [of IRC 1014] applies shall not

SUPPLEMENT A IRC 1014(f): Basis Must Be Consistent With Estate Tax Return For purposes of this section (1) In General. The basis of any property to which subsection (a) [of IRC 1014] applies shall not

STATE of CONNECTICUT Department of Labor. Unemployment Compensation Benefit Payments and the Effect on Reimbursable Employers

STATE of CONNECTICUT Department of Labor Unemployment Compensation Benefit Payments and the Effect on Reimbursable Employers 2018 Prepared by: Merit Rating Unit (860) 263-6705 Fax (860) 263-6723 TABLE

STATE of CONNECTICUT Department of Labor Unemployment Compensation Benefit Payments and the Effect on Reimbursable Employers 2018 Prepared by: Merit Rating Unit (860) 263-6705 Fax (860) 263-6723 TABLE

CUSTODIAL AGREEMENT SIMPLE IRA

Page 1 of 9 IMPORTANT INFORMATION ABOUT PROCEDURES FOR OPENING A NEW ACCOUNT: To help the government fight the funding of terrorism and money laundering activities, federal law requires all financial institutions

Page 1 of 9 IMPORTANT INFORMATION ABOUT PROCEDURES FOR OPENING A NEW ACCOUNT: To help the government fight the funding of terrorism and money laundering activities, federal law requires all financial institutions

Flexible Spending Plan

St. Francis Health Services of Morris, Inc. Flexible Spending Plan Medical FSA, Dependent Care FSA, and Pre- Tax Premium Summary Table of Contents INTRODUCTION... 4 DETAILS REGARDING THE MEDICAL FSA BENEFIT...

St. Francis Health Services of Morris, Inc. Flexible Spending Plan Medical FSA, Dependent Care FSA, and Pre- Tax Premium Summary Table of Contents INTRODUCTION... 4 DETAILS REGARDING THE MEDICAL FSA BENEFIT...

THE NEW CENTRALIZED PARTNERSHIP AUDIT REGIME: AN OVERVIEW

THE NEW CENTRALIZED PARTNERSHIP AUDIT REGIME: AN OVERVIEW By: Kevin M. Henry, Esq. I. WHERE ARE WE NOW? THE TAX EQUITY AND FISCAL RESPONSIBILITY ACT OF 1982 ( TEFRA ) A. Prior to TEFRA, partnership audits

THE NEW CENTRALIZED PARTNERSHIP AUDIT REGIME: AN OVERVIEW By: Kevin M. Henry, Esq. I. WHERE ARE WE NOW? THE TAX EQUITY AND FISCAL RESPONSIBILITY ACT OF 1982 ( TEFRA ) A. Prior to TEFRA, partnership audits

[ p] Amendments to the Regulations Regarding Questions and Answers Relating to Church Tax Inquiries and Examinations

![[ p] Amendments to the Regulations Regarding Questions and Answers Relating to Church Tax Inquiries and Examinations](/thumbs/90/103690088.jpg "[ p] Amendments to the Regulations Regarding Questions and Answers Relating to Church Tax Inquiries and Examinations") [4830-01-p] DEPARTMENT OF THE TREASURY Internal Revenue Service 26 CFR Part 301 [REG-112756-09] RIN 1545-BI60 Amendments to the Regulations Regarding Questions and Answers Relating to Church Tax Inquiries

[4830-01-p] DEPARTMENT OF THE TREASURY Internal Revenue Service 26 CFR Part 301 [REG-112756-09] RIN 1545-BI60 Amendments to the Regulations Regarding Questions and Answers Relating to Church Tax Inquiries

Chapter 02 - Working with the Tax Law

1. Rules of tax law do not include Revenue Rulings and Revenue Procedures. Rules of tax law do include Treasury Department pronouncements. 2. A tax professional need not worry about the relative weight

1. Rules of tax law do not include Revenue Rulings and Revenue Procedures. Rules of tax law do include Treasury Department pronouncements. 2. A tax professional need not worry about the relative weight

Correcting United States Income Tax and Foreign Asset Reporting Problems. D. Sean McMahon, J.D., LL.M. McMahon & Associates, PC Boston, Massachusetts

Correcting United States Income Tax and Foreign Asset Reporting Problems D. Sean McMahon, J.D., LL.M. McMahon & Associates, PC Boston, Massachusetts D. Sean McMahon, J.D., LL.M. Former Senior Attorney

Correcting United States Income Tax and Foreign Asset Reporting Problems D. Sean McMahon, J.D., LL.M. McMahon & Associates, PC Boston, Massachusetts D. Sean McMahon, J.D., LL.M. Former Senior Attorney

Filing Returns and Elections - Assessments, Reassessments and Penalties

Filing Returns and Elections - and Penalties Joseph Devaney, CA, Video Tax News, CA, TaxClinic.ca Calgary, AB Introduction Large reference paper Covering issues in respect of the following topics: Electronically

Filing Returns and Elections - and Penalties Joseph Devaney, CA, Video Tax News, CA, TaxClinic.ca Calgary, AB Introduction Large reference paper Covering issues in respect of the following topics: Electronically

AMERICAN INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS

AMERICAN INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS Comments on Proposed Regulations, REG-138637-07 Relating to Regulations Governing Practice Before the Internal Revenue Service October 7, 2010 In REG-138637-07

AMERICAN INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS Comments on Proposed Regulations, REG-138637-07 Relating to Regulations Governing Practice Before the Internal Revenue Service October 7, 2010 In REG-138637-07

Tax Court Holds that Certain Tax Return Information May Be Disclosed to an Employer Asserting a Defense to Withholding Tax

IRS Insights A closer look. In this issue: Tax Court Holds that Certain Tax Return Information May Be Disclosed to an Employer Asserting a Defense to Withholding Tax... 1 The Ninth Circuit Court of Appeals

IRS Insights A closer look. In this issue: Tax Court Holds that Certain Tax Return Information May Be Disclosed to an Employer Asserting a Defense to Withholding Tax... 1 The Ninth Circuit Court of Appeals

IRS Provides Guidance on FBAR Penalties

Page 1 of 5 The Tax Adviser IRS Provides Guidance on FBAR Penalties Updated procedures on penalties imposed for failing to file the Report of Foreign Bank and Financial Accounts provide consistency and

Page 1 of 5 The Tax Adviser IRS Provides Guidance on FBAR Penalties Updated procedures on penalties imposed for failing to file the Report of Foreign Bank and Financial Accounts provide consistency and

T.D DEPARTMENT OF THE TREASURY Internal Revenue Service

T.D. 8845 DEPARTMENT OF THE TREASURY Internal Revenue Service 26 CFR Part 20 Adequate Disclosure of Gifts AGENCY: Internal Revenue Service (IRS), Treasury. ACTION: Final regulations. SUMMARY: This document

T.D. 8845 DEPARTMENT OF THE TREASURY Internal Revenue Service 26 CFR Part 20 Adequate Disclosure of Gifts AGENCY: Internal Revenue Service (IRS), Treasury. ACTION: Final regulations. SUMMARY: This document

TAX ACADEMY: ETHICS 2016

TAX ACADEMY: ETHICS 2016 Ethics and the Tax Professional Doing the Right Things at the Right Time References: Circular 230 Revised 6-2014 Best CPE Courses IRS.Gov Tax Academy 2015 IRS EITC Webinar Ethics:

TAX ACADEMY: ETHICS 2016 Ethics and the Tax Professional Doing the Right Things at the Right Time References: Circular 230 Revised 6-2014 Best CPE Courses IRS.Gov Tax Academy 2015 IRS EITC Webinar Ethics:

United States V. Cruz- Tax Preparers Finally Beat IRS Death Penalty Action

University of Miami Law School Institutional Repository University of Miami Law Review 7-11-2011 United States V. Cruz- Tax Preparers Finally Beat IRS Death Penalty Action Alexander Smith Follow this and

University of Miami Law School Institutional Repository University of Miami Law Review 7-11-2011 United States V. Cruz- Tax Preparers Finally Beat IRS Death Penalty Action Alexander Smith Follow this and

IRS PENALTIES. Avoidance and abatement. June 2017

IRS PENALTIES Avoidance and abatement June 2017 Today s presenters Patti Burquest Principal Washington National Tax Patti leads the firm s tax controversy team, with a focus on IRS examination and appeals.

IRS PENALTIES Avoidance and abatement June 2017 Today s presenters Patti Burquest Principal Washington National Tax Patti leads the firm s tax controversy team, with a focus on IRS examination and appeals.

B u l l e t i n. Preparing for a Sales Tax Audit INTRODUCTION THE SALES TAX AUDIT

Bulletin No. TX 6 File: Taxes B u l l e t i n Preparing for a Sales Tax Audit INTRODUCTION In the best of circumstances, state and local tax audits of construction contractors eventually turn adversarial

Bulletin No. TX 6 File: Taxes B u l l e t i n Preparing for a Sales Tax Audit INTRODUCTION In the best of circumstances, state and local tax audits of construction contractors eventually turn adversarial