1/19/2017. Agenda. Due Diligence and the Credits for 2016 Ethics (1 hours) Overview of Credits (1 hour Tax Law)

|

|

|

- Gwenda Williamson

- 6 years ago

- Views:

Transcription

1 Due Diligence and the Credits for 2016 Ethics (1 hours) Overview of Credits (1 hour Tax Law) January 19, 2017 Agenda Overview of the Child Tax Credit Additional Child Tax Credit American Opportunity Credit Earned Income Tax Credit What are our Due Diligence requirements? Documents you may want in your files Questions to address to your client 2 Each refundable credit has different eligibility rules. Take these simple steps to avoid errors: Know the tax law for each refundable credit including eligibility rules Remember, software is not a substitute for knowledge of the tax law Follow the Due Diligence Must Do s 3 1

2 Helpful Hints Apply a common sense standard to the information provided by your client Evaluate whether the information is complete and gather any missing facts Determine if the information is consistent; recognize contradictory statements and statements you know are not true Conduct a thorough, in-depth interview with each client, every year Ask enough questions to know the return is correct and complete Document in the file at the time it happens any questions you asked and your client s responses 4 What s New? Form 8867 expanded and revised for future years Due to changes in the law (2015), the paid tax return preparer EIC due diligence requirements have been expanded to also cover the AOTC and the CTC/ACTC and join the EITC due diligence requirements Form 8867 has been modified and streamlined to account for these changes Completing the form is not a substitute for actually performing the necessary due diligence and completing all required forms and schedules when preparing the return 5 What s Else is New? The paid tax return preparer due diligence penalty is now indexed for inflation The penalty for failure to meet the due diligence requirements with respect to returns and claims for refund filed in 2016 is $510 per credit per return Regulation provides additional information concerning penalties Penalties can also be stacked if multiple due diligence on other credits is not performed 6 2

3 Regulation The temporary regulations amend by imposing due diligence requirements on tax return preparers with respect to determining the eligibility for, or the amount of, the CTC/ACTC or AOTC, in addition to the EIC, on any return or claim for refund The temporary regulations also amend section to reflect changes requiring the IRS to index the penalty for inflation for returns and claims for refund filed after December 31, Regulation The proposed rules affect tax return preparers who determine the eligibility for, or the amount of, the EIC, the CTC/ACTC and/or the AOTC The North American Industry Classification System (NAICS) code that relates to tax return preparation services (NAICS code ) is the appropriate code for tax return preparers subject to this notice of proposed rulemaking 8 Regulation The information needed to document eligibility for the CTC/ACTC and the AOTC largely duplicates the information needed to compute the EIC and complete other parts of the return or claim for refund 9 3

4 Regulation The current regulations under 6695(g) already require tax return preparers to complete the Form 8867 when a return or claim for refund includes a claim of the EIC Tax return preparers also must currently maintain records of the checklists and EIC computations, as well as a record of how and when the information used to compute the EIC was obtained by the tax return preparer 10 What s New? Refunds issued after February 15, 2017 Due to changes in the law, the IRS cannot issue refunds before February 15, 2017 for returns that claim the EIC or the ACTC This applies to the entire refund, not just the portion associated with these credits You should inform the taxpayer if his or her return includes a claim for the EIC and/or ACTC 11 Child Tax Credit and the Additional Child Tax Credit 12 4

, they cannot claim the additional child tax credit")

5 What's New? - Reminder Foreign earned income, beginning in 2015, if the taxpayer is filing Form 2555 or 2555-EZ (both relating to foreign earned income), they cannot claim the additional child tax credit Taxpayer identification number needed by due date of return If the taxpayer didn't have a social security number (an SSN) or by the due date of the 2016 return (including extensions), they cannot claim the child tax credit or the additional child tax credit on either the original or an amended 2016 return 13 What's New? Also, neither credit is allowed on either the original or an amended 2016 return with respect to a child who didn't have an SSN, ATIN, or ITIN by the due date of the return (including extensions), even if that child later gets one of those numbers 14 Child-Related Tax Benefits Comparison 15 5

6 Child-Related Tax Benefits Comparison 16 Child-Related Tax Benefits Comparison 17 Child-Related Tax Benefits Comparison 18 6

7 Child-Related Tax Benefits Comparison 19 Child-Related Tax Benefits Comparison

8

, 2.")

9 Child Tax Credit This credit is for people who have a qualifying child A qualifying child for purposes of the child tax credit is a child who: 1. Is a son, daughter, stepchild, foster child, brother, sister, stepbrother, stepsister, half brother, half sister, or a descendant of any of them (for example, a grandchild, niece, or nephew), 2. Was under age 17 at the end of Did not provide over half of his or her own support for Lived with the taxpayer for more than half of 2016 Exceptions apply 5. Is claimed as a dependent on the return 6. the child does not file a joint return for the year (or files it only to claim a refund of withheld income tax or estimated tax paid), and 7. Was a U.S. citizen, a U.S. national, or a U.S. resident alien 25 Filers Who Have Certain Child Dependents with an IRS Individual Taxpayer Identification Number (ITIN). If claiming a child tax credit or additional child tax credit for a child identified on the tax return with an ITIN, you must complete Part I of Schedule 8812 (Form 1040A or 1040) Although a child may be a dependent, the taxpayer may claim a child tax credit or additional child tax credit only for a dependent who is a citizen, national, or resident of the United States To be treated as a resident of the United States, a child generally will need to meet the requirements of the substantial presence test

10 Exceptions to Time Lived with the Taxpayer A child is considered to have lived with the taxpayer for more than half of 2016 if the child was born or died in 2016 and the home was this child's home for more than half the time he or she was alive Temporary absences by the taxpayer or the child for special circumstances, such as school, vacation, business, medical care, military service, or detention in a juvenile facility, count as time the child lived with the taxpayer There are also exceptions for kidnapped children and children of divorced or separated parents Limits on the Credit You must reduce the maximum credit amount of $1,000 for each child if either (1) or (2) applies 1. The amount on Form 1040, line 47; Form 1040A, line 30; or Form 1040NR, line 45, is less than the credit If this amount is zero, the taxpayer cannot take the credit because there is no tax to reduce They may be able to take the additional child tax credit 29 Form

11 Limits on the Credit 2. The modified adjusted gross income (AGI) is more than the amount shown below for the filing status a. Married filing jointly $110,000. b. Single, head of household, or qualifying widow(er) $75,000 c. Married filing separately $55, Modified AGI For purposes of the child tax credit, the modified AGI is the AGI plus the following amounts that may apply Any amount excluded from income because of the exclusion of income from Puerto Rico Any amount on line 45 or line 50 of Form 2555, Foreign Earned Income Any amount on line 18 of Form 2555-EZ, Foreign Earned Income Exclusion Any amount on line 15 of Form 4563, Exclusion of Income for Bona Fide Residents of American Samoa If the taxpayer does not have any of the above, the modified AGI is the same as the AGI 32 Earned Income For this purpose, earned income includes only: Taxable earned income, and Nontaxable combat pay 33 11

12 Earned Income Chart Form 8812 Instructions 34 Additional Child Tax Credit This credit is for certain individuals who get less than the full amount of the child tax credit The additional child tax credit may give the taxpayer a refund even if they do not owe any tax 35 How to Claim the Additional Child Tax Credit To claim the additional child tax credit, follow the steps below 1. Figured the amount, if any, of the child tax credit 2. After addressing the questions on the tax worksheet use Parts II IV of Schedule 8812 to see if the taxpayer qualifies to take the additional child tax credit 3. Carry any additional credit to the appropriate form 36 12

13 Line 7 Worksheet 37 Worksheet 38 Worksheet Special Worksheet 39 13

40 filing Form 2555 or 2555- EZ (Line 11 Worksheet) 41 1040 and")

42 14")

14 Use this Worksheet only if the Taxpayer Answered Yes on Line 11 of the Child Tax Credit Worksheet earlier and are not filing Form 2555 or 2555-EZ (Line 11 Worksheet) 40 Use this Worksheet only if the Taxpayer Answered Yes on Line 11 of the Child Tax Credit Worksheet earlier and are not filing Form 2555 or EZ (Line 11 Worksheet) and 1040NR Filers Earned Income Worksheet (for line 2 of the Line 11 Worksheet or line 4a of Schedule 8812, Child Tax Credit) 42 14

44")

15 1040A Filers Earned Income Worksheet (for line 2 of the Line 11 Worksheet) 43 Additional Medicare Tax and RRTA Tax Worksheet (for line 6 of the Line 11 Worksheet) 44 Form

16 Form Form American Opportunity Tax Credit 48 16

17 What s New? Taxpayer identification number needed by due date of return If the taxpayer does not have a taxpayer identification number (SSN) by the due date of the 2016 return (including extensions), they can not claim the American opportunity credit on either the original or an amended 2016 return, even if they later get a SSN Also, the American opportunity credit isn t allowed on either the original or an amended 2016 return for a student who doesn t have a TIN by the due date of the return (including extensions), even if that student later gets a TIN 49 American Opportunity Credit The taxpayer may be able to claim a credit of up to $2,500 for adjusted qualified education expenses paid for each student who qualifies for the American opportunity credit This credit equals 100% of the first $2,000 and 25% of the next $2,000 of adjusted qualified education expenses paid for each eligible student The amount of the credit for 2016 is gradually phased out based on the phase-out limitations 50 Student Qualifications 1. As of the beginning of 2016, the student had not completed the first 4 years of postsecondary education (generally, the freshman through senior years of college), as determined by the eligible educational institution For this purpose, do not include academic credit awarded solely because of the student's performance on proficiency examinations 2. Neither the American opportunity credit nor the Hope scholarship credit has been claimed (by the taxpayer or anyone else) for this student for any 4 tax years before 2016 If the American opportunity credit (and Hope scholarship credit) has been claimed for this student for any 3 or fewer tax years before 2016, this requirement is met 51 17

18 Who Cannot Claim a Credit? You cannot claim an education credit on a 2016 tax return if any of the following apply: 1. The taxpayer is claimed as a dependent on another person's tax return, such as a parent's return 2. The filing status is married filing separately 3. The taxpayer (or the spouse) were a nonresident alien for any part of 2016 and did not elect to be treated as a resident alien for tax purposes 4. The MAGI is the following: a. For the American opportunity credit: $180,000 or more if married filing jointly, or $90,000 or more if single, head of household, or qualifying widow(er) with dependent child 52 Qualified Education Expenses American opportunity credit: Qualified education expenses include amounts spent on books, supplies, and equipment needed for a course of study, whether or not the materials are purchased from the educational institution They can be purchased from a third-party 53 Qualified Education Expenses Qualified education expenses include nonacademic fees, such as student activity fees, athletic fees, or other expenses unrelated to the academic course of instruction, only if the fee must be paid to the institution as a condition of enrollment or attendance However, fees for personal expenses are never qualified education expenses 54 18

")

19 Personal Fees Not Part of the Credit Room and board, insurance, medical expenses (including student health fees), transportation, and other similar personal, living, or family expenses Any course or other education involving sports, games, or hobbies, or any noncredit course, unless such course or other education is part of the student's degree program or (for the lifetime learning credit only) helps the student acquire or improve job skills 55 Form 1098-T The taxpayer should receive Form 1098-T, Tuition Statement, from the institution reporting either payments received in 2016 (box 1) or amounts billed in 2016 (box 2) However, the amount in box 1 or 2 of Form 1098-T may be different from the amount the taxpayer paid (or are treated as having paid) Use only the amounts actually paid (plus any amounts treated as having paid) in 2016 (reduced, as necessary) 56 Form 1098-T

are treated as paid by the student Qualified education expenses paid (or treated as paid) by a student who is")

, they cannot use those same expenses in qualified education expenses when figuring the education")

20 Form 1098-T Form 1098-T Revised 59 Expenses Paid by Another Party Qualified education expenses paid on behalf of the student by someone other than the student (such as a relative) are treated as paid by the student Qualified education expenses paid (or treated as paid) by a student who is claimed as a dependent on a taxpayer s tax return are treated as paid by the taxpayer If the taxpayer or the student takes a deduction for higher education expenses, such as on Schedule A or Schedule C (Form 1040), they cannot use those same expenses in qualified education expenses when figuring the education credits 60 20

21 Prepaid Expenses Qualified education expenses paid in 2016 for an academic period that begins in the first 3 months of 2017 can be used in figuring an education credit for 2016 only For example, if they taxpayer pays $2,000 in December 2016 for qualified tuition for the 2017 winter quarter that begins in January 2017, they can use that $2,000 in figuring an education credit for 2016 only 61 Academic Period An academic period is any quarter, semester, trimester, or any other period of study as reasonably determined by an eligible educational institution If an eligible educational institution uses credit hours or clock hours and does not have academic terms, each payment period may be treated as an academic period 62 Adjusted Qualified Education Expenses Tax-free educational assistance For tax-free educational assistance received in 2016, reduce the qualified educational expenses for each academic period by the amount of tax-free educational assistance allocable to that academic period Tax-free educational assistance includes: 1. The tax-free part of any scholarship or fellowship grant (including Pell grants); 2. The tax-free part of any employer-provided educational assistance; 3. Veterans' educational assistance; and 4. Any other educational assistance that is excludable from gross income (tax free), other than as a gift, bequest, devise, or inheritance 63 21

22 Income Inclusion The taxpayer may be able to increase the combined value of an education credit and certain educational assistance if the student includes some or all of the educational assistance in income in the year it is received 64 Income Inclusion Generally, any scholarship or fellowship grant is treated as taxfree educational assistance However, a scholarship or fellowship grant is not treated as tax-free educational assistance to the extent the student includes it in gross income (the student may or may not be required to file a tax return) for the year the scholarship or fellowship grant is received and either: The scholarship or fellowship grant (or any part of it) must be applied (by its terms) to expenses (such as room and board) other than qualified education expenses; or The scholarship or fellowship grant (or any part of it) may be applied (by its terms) to expenses (such as room and board) other than qualified education expenses 65 Income Inclusion A student cannot choose to include in income a scholarship or fellowship grant provided by an Indian tribal government that is excluded from income under the Tribal General Welfare Exclusion Act of 2014 or benefits provided by an educational program described in 5.02(2)(b)(ii) of Rev. Proc

23 Income Inclusion The fact that the educational institution applies the scholarship or fellowship grant to qualified education expenses (such as tuition and related fees) does not prevent the student from choosing to apply certain scholarships or fellowship grants to other expenses (such as room and board) By choosing to do so, the student will include the part applied to other expenses (such as room and board) in gross income and may be required to file a tax return 67 Coverdell ESA Unlike a scholarship or fellowship grant, a tax-free distribution from a Coverdell ESA or qualified tuition program ( 529 plan) can be applied to either qualified education expenses or certain other expenses (such as room and board) without creating a tax liability for the student An education credit can be claimed in the same year the beneficiary takes a tax-free distribution from a Coverdell ESA or qualified tuition program, as long as the same expenses are not used for both benefits 68 Tax-free Educational Assistance Treated as a Refund Some tax-free educational assistance received after 2016 may be treated as a refund of qualified education expenses paid in 2016 This tax-free educational assistance is any tax-free educational assistance received by the taxpayer or anyone else after 2016 for qualified education expenses paid on behalf of a student in 2016) A refund of qualified education expenses may reduce qualified education expenses for the tax year or may require the taxpayer to repay (recapture) the credit that claimed in an earlier year Some tax-free educational assistance received after 2015 may be treated as a refund 69 23

24 Refunds Received in 2016 For each student, figure the adjusted qualified education expenses for 2016 by adding all the qualified education expenses paid in 2016 and subtracting any refunds of those expenses received from the eligible educational institution during Refunds Received after 2016, but before the Income Tax Return is Filed If anyone receives a refund after 2016 of qualified education expenses paid on behalf of a student in 2015 and the refund is received before the taxpayer files the 2016 income tax return, reduce the amount of qualified education expenses for 2016 by the amount of the refund 71 Refunds Received after 2016 and after the Income Tax Return is Filed If anyone receives a refund after 2016 of qualified education expenses paid on behalf of a student in 2016 and the refund is received after the filing of the taxpayer s file the 2016 income tax return, they may need to repay some or all of the credit that was claimed 72 24

25 Credit Recapture If any tax-free educational assistance for the qualified education expenses paid in 2016, or any refund of the qualified education expenses paid in 2016, is received after the taxpayer files the 2016 income tax return, they must recapture (repay) any excess credit You must refigure the amount of the adjusted qualified education expenses for 2016 by reducing the expenses by the amount of the refund or tax-free educational assistance 73 Credit Recapture Then refigure the education credit(s) for 2016 and figure the amount by which the 2016 tax liability would have increased if they had claimed the refigured credit(s) Include that amount as an additional tax for the year the refund or tax-free assistance was received 74 Eligible Educational Institution An eligible educational institution is generally any accredited public, nonprofit, or proprietary (private) college, university, vocational school, or other postsecondary institution The institution must be eligible to participate in a student aid program administered by the Department of Education Virtually all accredited postsecondary institutions meet this definition 75 25

26 Eligible Educational Institution An eligible educational institution also includes certain educational institutions located outside the United States that are eligible to participate in a student aid program administered by the Department of Education 76 Form Form

27 Form Form Example The client paid $8,000 tuition and fees in December 2016 for their child's Spring semester beginning in January 2017 The return for 2016 is filed on February 2, 2017, and claimed a lifetime learning credit of $1,600 ($8,000 qualified education expense paid x.20) The client claimed no other tax credits 81 27

28 Example, cont d After you filed the return for the client, the child withdrew from two courses and they received a refund of $1,400 You must refigure the 2016 lifetime learning credit using $6,600 ($8,000 qualified education expenses $1,400 refund) The refigured credit is 1,320 and the tax liability increased by $280 You must include the difference of $280 ($1,600 credit originally claimed $1,320 refigured credit) as additional tax on your 2017 income tax return 82 Earned Income Tax Credit 83 EITC Basics The taxpayer will qualify for EITC if: They have earned income and adjusted gross income within certain limits; AND They meet certain basic rules; AND They either: Meet the rules for those without a qualifying child; OR Have a child that meets all the qualifying child rules for the taxpayer, or spouse if they file a joint return

29 EITC Basics The taxpayer and spouse and any qualifying child listed on the tax return must each have a Social Security number that is valid for employment They must file: Married filing jointly Head of household Qualifying widow(er) Single They can't claim EITC if the filing status is married filing separately 85 EITC Basics They must be a U.S. citizen or resident alien all year They cannot be a qualifying child of another person They cannot file Form 2555 or Form 2555 EZ (related to foreign earned income) They must meet the earned income, AGI and investment income limits 86 EITC Basics They must meet one of the following: Have a qualifying child If they do not have a qualifying child, they must: Be age 25 but under 65 at the end of the year Live in the United States for more than half the year, and Not qualify as a dependent of another person. If they qualify for EITC, they have to file a tax return with the IRS, even if they owe no tax or are not required to file 87 29

30 IRS denied EITC last year, but they qualify this year, what is the Process? If IRS denied or reduced the EITC for any year after 1996 for any reason other than a math or clerical error, they must qualify to claim the credit by meeting all the rules and must attach a completed Form 8862, Information to Claim Earned Income Credit After Disallowance to your next tax return to claim EITC 88 IRS denied EITC last year, but they qualify this year, what is the Process? But, do not file Form 8862 if either (1) or (2) is true 1. After the EITC was reduced or disallowed in the earlier year: The taxpayer filed Form 8862 (or other documents) and then IRS allowed, the EITC and IRS did not reduce or disallow the EITC again for any reason other than a math or clerical error 2. They are taking EITC without a qualifying child and the only reason IRS reduced or disallowed the EITC was because a child listed on Schedule EIC was not a qualifying child 89 Who is a Qualifying Child? The child is a qualifying child if the child meets all of the following tests: Age Relationship Residency Joint Return 90 30

31 Age The child must meet one of the following: Be under age 19 at the end of the year and younger than the taxpayer or the spouse, if they file a joint return Be a full-time student in at least five months of the year and under age 24 at the end of the year and younger than the taxpayer and the spouse if filing a joint return Be permanently and totally disabled at any time during the year and any age 91 Relationship To be a qualifying child, a child must be a: Son, daughter, adopted child, stepchild, eligible foster child, or a descendant of any of them (for example, your grandchild), or Brother, sister, half brother, half sister, stepbrother, stepsister, or a descendant of any of them (for example, your niece or nephew) 92 Relationship Definitions to clarify the relationship test Adopted child. An adopted child is always treated as the taxpayer s own child This includes a child who was placed with the taxpayer for a legal adoption by an authorized adoption agency Eligible Foster Child. A person is an eligible foster child if the child is placed with the taxpayer by an authorized placement agency, or by judgment, decree, or other order of any court of competent jurisdiction Authorized placement agencies include a state or local government agency or an Indian tribal government. It also includes a tax-exempt organization licensed by a state or an Indian tribe 93 31

32 Residency Test The child must have lived with the taxpayer or the spouse if they file a joint return, in the United States for more than half of the year 94 Joint Return Test The child must not have filed a joint return or if the child filed a joint return, the child and his/or her spouse filed only to claim a refund and were not required to file 95 What is Earned Income? Earned income includes all the taxable income and wages the taxpayer gets from working for someone else or the taxpayer owns or runs a business or farm Taxable earned income also includes: Wages, salaries, and tips Union strike benefits Certain disability benefits received before you reach minimum retirement age Net earnings from self-employment 96 32

33 Combat Pay The taxpayer can choose to include nontaxable combat pay in their taxable earned income to get EITC But, they have to include all or none of it Make sure to check to see if including combat pay as taxable income increases the refund or reduces the amount of tax owed If the spouse also has nontaxable combat pay, both can choose which way is best for them The amount of nontaxable combat pay should be shown on the Form W-2, in box 12, with code Q 97 How Do You Figure the Credit? Use the Earned Income Credit Worksheets in the instruction booklet for Form 1040, Form 1040A, or Form 1040EZ, and the Earned Income Credit (EIC) Table in the instruction booklet 98 Earned Income and AGI Limits 99 33

34 Investment Income Limit Investment income must be $3,400 or less for the year 100 Maximum Credit Amounts for 2016 The maximum amount of credit for Tax Year 2016 is: $6,269 with three or more qualifying children $5,572 with two qualifying children $3,373 with one qualifying child $506 with no qualifying children 101 The Protecting Americans against Tax Hikes (PATH) Act of 2015 Made permanent the relief for married taxpayers and the expanded credit for taxpayers with three or more qualifying children The IRS can t issue refunds before February 15 for tax returns with claims for the EITC and the Additional Child Tax Credit This applies to the entire refund and not just the credit amounts

35 2017 EITC Income Limits, Maximum Credit Amounts and Tax Law Updates EITC Income Limits, Maximum Credit Amounts and Tax Law Updates Investment income must be $3,450 or less for the year The maximum amount of credit for Tax Year 2017 is: $6,318 with three or more qualifying children $5,616 with two qualifying children $3,400 with one qualifying child $510 with no qualifying children 104 Worksheets

36 Form 8867 the Paid Preparers Checklist

37 Form Form Form

38 Form Tie Breaker Rules To determine which person can treat the child as a qualifying child the following tie-breaker rules apply If only one of the persons is the child's parent, the child is treated as the qualifying child of the parent If the parents file a joint return together and can claim the child as a qualifying child, the child is treated as the qualifying child of the parents 113 Tie Breaker Rules If the parents don't file a joint return together but both parents claim the child as a qualifying child, the IRS will treat the child as the qualifying child of the parent with whom the child lived for the longer period of time during the year If the child lived with each parent for the same amount of time, the IRS will treat the child as the qualifying child of the parent who had the higher adjusted gross income (AGI) for the year

39 Tie Breaker Rules If no parent can claim the child as a qualifying child, the child is treated as the qualifying child of the person who had the highest AGI for the year If a parent can claim the child as a qualifying child but no parent does so claim the child, the child is treated as the qualifying child of the person who had the highest AGI for the year, but only if that person's AGI is higher than the highest AGI of any of the child's parents who can claim the child 115 Form 8867 Paid Preparers Due Diligence Checklist Supplement for the Tie Breaker Rules 116 Form 8867 Paid Preparers Due Diligence Checklist Supplement for the Tie Breaker Rules

40 Form 8867 Paid Preparers Due Diligence Checklist Supplement for the Tie Breaker Rules Tax Benefits 1.The exemption for the child. 2.The child tax credit. 3.Head of household filing status. 4.The credit for child and dependent care expenses. 5.The exclusion from income for dependent care benefits. 6.The earned income credit. Head of Household Status A person cannot qualify more than one taxpayer to use the head of household filing status for the year. Custodial parent and noncustodial parent. The custodial parent is the parent with whom the child lived for the greater number of nights during the year. The other parent is the noncustodial parent. If the parents divorced or separated during the year and the child lived with both parents before the separation, the custodial parent is the one with whom the child lived for the greater number of nights during the rest of the year. A child is treated as living with a parent for a night if the child sleeps: At that parent's home, whether or not the parent is present, or in the company of the parent, when the child doesn't sleep at a parent's home (for example, the parent and child are on vacation together). 118 Form 8867 Paid Preparers Due Diligence Checklist Supplement for the Tie Breaker Rules Equal number of nights If the child lived with each parent for an equal number of nights during the year, the custodial parent is the parent with the higher adjusted gross income (AGI). Applying the tiebreaker rules to divorced or separated parents (or parents who live apart). If a child is treated as the qualifying child of the noncustodial parent under the rules for children of divorced or separated parents (or parents who live apart), only the noncustodial parent can claim an exemption and the child tax credit for the child. However, only the custodial parent can claim the credit for child and dependent care expenses or the exclusion for dependent care benefits for the child, and only the custodial parent can treat the child as a dependent for the health coverage tax credit. Also, the noncustodial parent can t claim the child as a qualifying child for head of household filing status or the earned income credit. Instead, the custodial parent, if eligible, or other eligible person can claim the child as a qualifying child for those two benefits. If the child is the qualifying child of more than one person for these benefits, then the tiebreaker rules just explained determine whether the custodial parent or another eligible person can treat the child as a qualifying child. 119 Reminder

41 Reminder 121 Form Form

42 Where to Start? Begin with determining the client s filing status Head of Household Status reminder A qualifying child of the client The child would be a qualifying child except the custodial parent released the exemption to the non-custodial parent The client must maintain his or her home that is the principal residence for more than half the year for the above qualifying child 124 Uniform Definition of a Child Summary 125 Head of Household Thus a release of the dependency exemption by the custodial parent will not apply a head of household status for the non-custodial parent

43 Reminders Release of dependency exemption by a custodial parent is only effective for the child tax credit The release will not apply to the: Earned income tax credit Dependent care credit Head of household status 127 Once Filing Status is Determined Address the dependent exemption On occasion the filing status and the fact that a person can be claimed as a dependent go hand in hand 128 Performing the Due Diligence Check to see if your software has embedded questions you can address to the client Note: You cannot depend on your software exclusively Tax software is a tool to assist you and is not a substitute for your knowledge of the tax law and professional judgment and responsibility You are the person who can best evaluate the information your client gives you and apply your knowledge of the law to that information

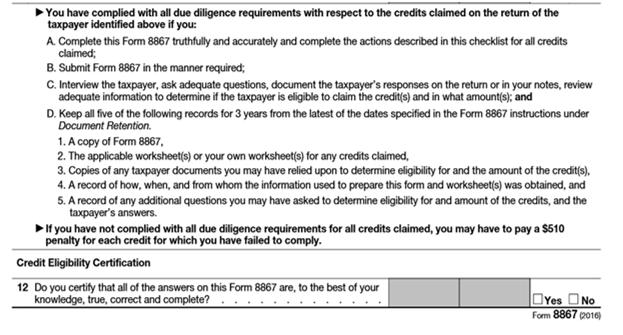

44 Performing the Due Diligence Software cannot be designed to address every possible due diligence issue you may encounter 130 Questionnaires and Worksheets You can use the worksheet in IRS publications and forms some kind of worksheet is required You can also create additional questions to be included in any worksheet you utilize Worksheets must cover the required elements that need to be addressed as part of the Due Diligence requirement 131 Knowledge Requirement Do you have any reason to know if the information provided by the client is not correct, or incomplete or inconsistent? In other words, do you have knowledge concerning the client that would assist you in coming to the conclusion that they do or do not qualify for a particular credit This information cannot be ignored Apply a common sense standard to the information provided by the client

45 Knowledge Requirement Evaluate whether the information is complete and gather any missing facts Determine if the information is consistent; recognize contradictory statements and statements you know are not true Conduct a thorough, in-depth interview with each client Ask enough questions to know the return is correct and complete 133 Knowledge Requirement Document in the file at the time it happens any questions you asked and your client s responses 134 Your Requirements Interview each and every client, where these credits apply Ask adequate questions Review the information for consistency, correctness and completeness Document the client responses Keep the record for 3 years

46 Interview Each and Every Client, Where Due Diligence is Required What Constitutes an Interview? Face to face Fax Telephone There must be some sort of interaction with the client to address concerns and the information presented The Form 8867 implies an interview must be conducted 136 Questionnaire/Organizer You can use this only as part of your interview but not as standalone document You must review and ask the client follow-up questions to get a clear picture of the client s tax situation (Statement IRS made at the IRS Tax Forums) 137 The Path to Questions will Vary with Each Client We have complied the following questions as a guideline to address the issues Additional questions may come to mind as you interview the client Remember - First you need to determine if the child qualifies as a dependent? Go thru the dependent tests This is a key to the credits in some instances

47 Basics Ask for the child's date of birth or verify it if you use a client intake sheet If over 19, ask how many months the child was in school Remember, the 5 months don't have to be consecutive Verify the relationship If not the parent, ask where the parents are and why the parents are not claiming Explain the tie breaker rules when necessary 139 Permanently and Totally Disabled IRS defines permanently and totally disabled as: Not being able to engage in any substantial gainful activity because of a medically determinable physical or mental condition; and A physician must certify the condition has lasted or is expected to last continuously for at least 12 months or result in death To prove permanent and total disability, IRS asks for a letter from the child's doctor, other healthcare provider or any social service program or government agency verifying the child is permanently and totally disabled. 140 Permanently and Totally Disabled If your client doesn't have this document, ask your client if they can get this letter if IRS asks

48 Income The taxpayer has provided the W-2 from x employer or xx employers, ask if they have any other income such as interest, dividends or from running your own business that they haven't talked about? 142 Self-Employment Income Tax preparers should ensure that the amount of net selfemployment income reported is correct Taxpayers sometimes want to over-report or under-report their income to qualify for or maximize the amount of EITC The preparer should ask sufficient questions of clients claiming self-employment income to be satisfied that: The client is actually conducting a business The client has records to support income and expenses, or can reasonably reconstruct income and expenses records, and the client has included all income and related expenses on Schedule C, Profit or Loss from Business (Sole Proprietorship) 143 Why are Schedule C's an EITC issue? IRS estimates that between 22.1% and 25.9 % of the EITC claims, or between $13.3 and $15.6 billion were paid in error in 2013 Income reporting errors are among the top three common EITC errors that account for more than 60% of the dollars paid in error annually The most common Schedule C errors, which fall into the income category, noted on EITC returns are:

49 Why are Schedule C's an EITC issue? Schedule C's with losses or over-stated expenses to bring income down to qualify for EITC Inflated Schedule C income to maximize the amount of EITC Bogus Schedule C income to qualify for or maximize the amount of EITC Approximately 21 million Schedule C forms are filed each year Approximately one-third of the annual tax gap is a result of under-reported income or overstated deductions on Schedule C businesses 145 Questions that Need to Be Addressed The preparer should ask sufficient questions of clients claiming self-employment income to be satisfied that: The client is actually conducting a business The client has records to support income and expenses, or can reasonably reconstruct income and expenses records, and The client has included all income and related expenses on Schedule C, Profit or Loss from Business (Sole Proprietorship) 146 Marital Status Don't assume the child is not married. Are any of your children married? I don't think so, but I have to ask if your child is married or not Don't let your client tell you his or filing status: ask the right questions Are you married? When did you separate? Was it a legal separation or divorce? When did your spouse move out?

50 Support Test - Questions It must be hard to support a family of x amount on this amount of income Did anyone else help support this child? Did you receive help from any government agency or social organization? Or, did you receive outside support for this child? Or, did your child work or provide any of his or her own support? 148 Student Status Verify the student can claim his or her own personal exemption or that the person claiming the student can It is difficult to verify if dependent students filed their own returns and claimed their personal exemption But, warn your clients when they are not sure if someone else claimed the exemption of the possible consequences 149 Student Status Ask how long the student attended a postsecondary school Ask how many courses the student is taking? Ask what the school considers full-time Verify the school term Ask the student's enrollment status, undergraduate or graduate If the student is taking graduate studies, ask when he or she started graduate studies

51 Student Status Ask enough questions until you feel comfortable the student qualifies and let your clients know if the IRS audits them, they need to have documents supporting their claim 151 EITC If your client's claims EITC, you may need to keep copies, either paper or scanned versions, of any documents your clients provide such as: Social security cards Birth certificates School records Business income and expense records and more 152 Other Questions

52 Questions Is the taxpayer s filing status married filing separately? Does the taxpayer (and the taxpayer s spouse if filing jointly) have a social security number (SSN) that allows him or her to work and is valid for EIC purposes? Is the taxpayer (or the taxpayer's spouse if filing jointly) filing Form 2555 or 2555-EZ (relating to the exclusion of foreign earned income)? Was the taxpayer (or the taxpayer's spouse) a nonresident alien for any part of 2016? 154. Questions Is the taxpayer s filing status married filing jointly? Is the taxpayer s investment income more than $3,400?, 155 Questions What is the client s marital status? If married but separated, what month and date was the last day they lived with spouse? What is the age of the qualifying children? What is the child s relationship to the client? What support if any did the client provide for the child? Who has physical custody of the child?

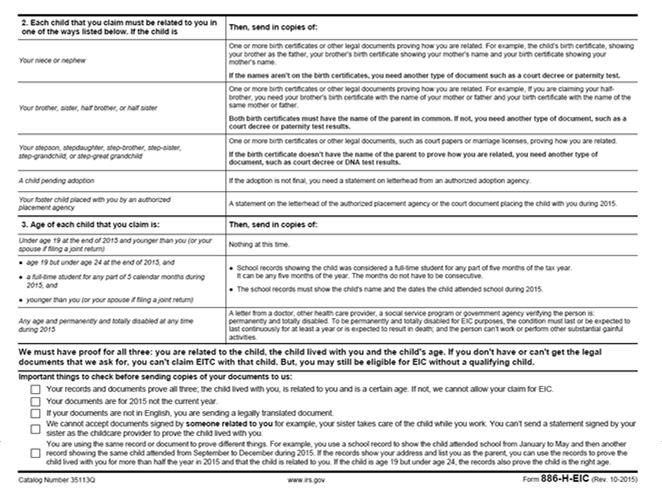

53 Questions Does the client have a Form 8332 releasing the child for dependent purposes to the non-custodial parent? Is the child filing their own tax return? Is there a requirement to file? What is the filing status? How many months did the child live with the client? 157 Does the taxpayer have any of these credit? Foreign tax credit - Form 1116 if required Credit for child and dependent care expenses - Form 2441 Education credits from Form 8863, line 19 Retirement savings contributions credit. Attach Form 8880 Residential energy credits. Attach Form 5695 Personal Use of Vehicle from Form Let s Look at Some Examples: Example1 In 2018, Tammy, a 22 year-old taxpayer, engages you to prepare their 2017 federal income tax return Tammy completes the standard intake questionnaire and states that she has never been married and has two sons, ages 10 and 11 Based on the intake sheet and other information that she provides, including information that shows that the boys lived with her throughout 2017 You believe that she may be eligible to claim each boy as a qualifying child for purposes of the EIC and the CTC

54 Example 1 However, the client provides no information to you and you do not have any information from other sources, to verify the relationship between Tammy and the boys To meet the knowledge requirement you must make reasonable inquiries to determine whether each boy is a qualifying child of Tammy for purposes of the EIC and the CTC, including reasonable inquiries to verify her relationship to the boys You must contemporaneously document these inquiries and the responses. 160 What Questions Do You Ask? Due to the ages of the client and the boys more information will be needed to determine the actual relationship Ask that the client provide more information due to the age issue If the children are adopted or have been placed by an agency ask for adoption or agency documentation to confirm this scenario Depending on the issue request adoption papers, birth certificates and other documents confirming the relationship 161 Example 2 Assume the same facts as in Example In addition, as part of preparing Tammy s 2017 federal income tax return, you made sufficient reasonable inquiries to verify that the boys were Tammy s legally adopted children In 2019, Tammy engages you to prepare her 2018 federal income tax return When preparing Tammy s 2018 tax return you are not required to make additional inquiries to determine the boys relationship to Tammy

55 Example 2 Instead made sufficient inquiries to determine if the situation is unchanged 163 Example 3 In 2018, Ricky, an 18 year-old taxpayer, engages you to prepare his 2017 federal income tax return Ricky completes the standard intake questionnaire and states that she has never been married, has one child, an infant, and that she and her infant lived with her parents during part of the 2017 tax year Ricky also provides you with a Form W-2 showing that she earned $10,000 during Example 3 Ricky provides no other documents or information showing that she earned any other income during the tax year Based on the intake sheet and other information that she provides, you believe she may be eligible to claim the infant as a qualifying child for the EIC and the CTC You must make reasonable inquiries to determine whether she is eligible to claim these credits, including reasonable inquiries to verify that she is not a qualifying child of her parents

56 Example 3 This would make her ineligible to claim the EIC and the Child Tax Credit You must contemporaneously document these inquiries and the responses 166 Example 4 The facts are the same as the facts in Example 3 In addition, you previously prepared the 2017 joint federal income tax return for Ricky s' s parents Based on information provided by her parents, you determined that Ricky is not eligible to be claimed as a dependent or as a qualifying child for purposes of the EIC or CTC on R's parents' return You would not be required to make additional inquiries to determine that Ricky is not her parents' qualifying child or dependent 167 Example 5 In 2018, Shane engages you prepare his 2017 federal income tax return During your standard intake interview, Shane states that he has never been married and his niece and nephew lived with him for part of the 2017 tax year You believe Shane may be eligible to claim each of these children as a qualifying child for purposes of the EIC and the CTC

57 Example 5 To meet the knowledge requirement you must make reasonable inquiries to determine whether each child is a qualifying child for purposes of the EIC and the CTC, including reasonable inquiries about the children's parents and the children's residency, You must contemporaneously document these inquiries and the responses 169 Example 6 Wilda engages you to prepare her federal income tax return During your standard intake interview, she states that she is 50 years old, has never been married, and has no children She further states to that during the tax year she was self-employed, earned $10,000 from her business, and had no business expenses or other income 170 Example 6 You believe she may be eligible for the EIC To meet the knowledge requirement you must make reasonable inquiries to determine whether she is eligible for the EIC, including reasonable inquiries to determine whether W's business income and expenses are correct You must contemporaneously document these inquiries and the responses Books and records Evidence of expenses

58 Example 7 Thomas, who is 32 years old, engages you to prepare his federal income tax return He completes your standard intake questionnaire and states that he has never been married As part of your intake process, Thomas provides you with a copy of the Form 1098-T he received showing that University M billed $4,000 of qualified tuition and related expenses for his enrollment or attendance at the university Thomas was at least a half-time undergraduate student 172 Example 7 You believe that he may be eligible for the AOTC To meet the knowledge requirements you must make reasonable inquiries to determine whether Thomas is eligible for the AOTC, as Form T does not contain all the information needed to determine eligibility for the AOTC or to calculate the amount of the credit Form 1098-T is just a small part of the information needed 173 Example 7 Ask Thomas to provide a statement of billing and payment from the college In addition, does Thomas have receipts for books and other required items the school requires for enrollment If Thomas is eligible, you must contemporaneously document these inquiries and the responses

59 More Issues To document your compliance with the due diligence requirements for the EITC, the CTC and the AOTC, is it sufficient to keep a copy of Form 8867 that is signed and dated by my client? Keeping a copy of the Form 8867, Paid Preparer's Due Diligence Checklist is one of your due diligence requirements Having your client sign and date the form for your records may be sufficient to document when and from whom you got the return information 175 More Issues You must also keep the computation worksheets and document any additional questions you ask your client and your client's responses to those questions at the time you are interviewing your client You can keep this documentation either electronically or on paper 176 More Issues When questioning a client who reports income that seems inadequate to support a family, is it sufficient to accept an answer that government benefits are received? Do we need to specify the type and amount? Asking questions about the source and amount of income used to support a household for due diligence has two purposes One purpose is to ensure the client is reporting all income that contributes to their total earned income and AGI

60 More Issues There is no support test for EITC But, you need to know the source and amount of income to determine filing status and eligibility for the dependency exemption The other purpose is to ensure no other person is eligible to claim EITC, the CTC or any other childrelated benefits Due diligence requires you to make additional inquiries if the information you receive from your client appears to be incorrect, inconsistent, or incomplete 178 More Issues You know taxpayers need to report all income but what about expenses? What if the client doesn't want to claim business expenses to keep their earned income higher and qualify for more EITC? A self-employed individual is required to report all business income and deduct all allowable business expenses They do not have the option of reporting what is most beneficial 179 Revenue Ruling , C.B. 564 This ruling addresses whether taxpayers may disregard allowable deductions in computing net earnings from self-employment for self-employment tax purposes Revenue. Ruling held that under 1402(a), every taxpayer (with the exception of certain farm operators) must claim all allowable deductions in computing net earnings from self-employment for self-employment tax purposes Because the net earnings from self-employment are included in earned income for EITC purposes this ruling is relevant

61 Concerns What should a preparer do if he or she feels the taxpayer is not providing all expenses to claim a larger credit? As a preparer, you need to be alert to this type of situation To meet the knowledge requirement, you must follow-up on your suspicion. ask additional questions, document the answers, and make a judgment about whether the answers make sense Ask for documentation until you are confident the return you are preparing is accurate. 181 Must I review the birth certificate to verify the age of a qualifying child? No, it's not required But, if you have reason to question a child's age, you may want to request the birth certificate If the client provides a birth certificate and you use it to determine eligibility for or the amount of the EITC, the CTC or the AOTC, you need to keep a copy 182 Must I review Social Security cards or keep a copy? No There is no requirement to review Social Security cards, but it is a best practice to review them You are more likely to get the child's name and number correct if copied directly from the card Also, having copies of cards is helpful in resolving e-file rejects If the client provides a Social Security card and you use it to determine eligibility for or amount of the EITC, the CTC and the AOTC, you need to keep a copy of the card with your records

62 The Firm How can I as an employer protect myself from penalties caused by my employees not meeting due diligence requirements? Review your current office procedures to make sure they address all appropriate due diligence requirements Review your procedures with your employees to make sure they clearly understand their responsibilities and your expectations of them Conduct annual due diligence training Test your employee's knowledge of due diligence and your procedures Perform recurring quality review checks on your employee's work including credit computations, questions they asked clients, documents they reviewed, and the records kept 184 Records A record of how and when the information used to complete Form 8867 is required The applicable worksheets must be completed The identity of any person furnishing the information, as well as a copy of any document that was provided by the taxpayer and on which the tax return preparer relied to complete Form Documents School records or statement Landlord or property management statement Health care provider statement Medical records, if volunteered Child care provider records Placement agency statement Social service records or statement Place of worship statement Indian tribal official statement Utility bills and statements - which are often used as proof of residence or address

63 Documents Employer statement Adoption documents Social Security card Birth Certificate Social services agency or program statement Form 1098-T Statement of billing and payments made to the college Receipts for books 187 Documents Business license Forms 1099 Records of gross receipts provided by taxpayer Taxpayer summary of income Records of expenses provided by taxpayer Taxpayer summary of expenses Bank statements Reconstruction of income and expenses 188 Documents Copy of Form 8332 Copies of prior year tax returns if a new client Verify each year the number of years the AOTC has been taken

64 More Documents Confirming Identity Internal identification card issued by one's employer, university, or school Voter's registration card Proof of professional certification (for members of regulated professions) Health insurance card issued by a private health insurance company, by Medicare, or by a government agency Library cards 190 Common Errors 191 Claiming EITC for a child who does not meet the qualifying child requirements Make sure you find out if the child lived with your client for more than half the year, is related to him or her and meets the age test You must ask how long the child lived with your client, at what address, and did anyone else live with the child for more than half the year Also, find out how the child is related by blood, by marriage or by law. Age is a bit easier; but if the child is a student or permanently and totally disabled, make sure your client has the documents needed to show the IRS if audited

65 Filing as single or head of household when married Ask the questions to find out if your client is married under state law, including common law, or was ever married Also, if your client is married, make sure your client did not live with his or her spouse at any time during the last six months of the year 193 Incorrectly reporting institution income or expenses Does the Form W-2 look similar to the Forms W- 2 of other clients who have the same employer? Is your client saying they own a business but not claiming any business expenses? Ask enough questions to make sure your client has a true business and claims all income and deducts all allowable expenses 194 Claiming AOTC for a student who didn t attend an eligible educational institution The AOTC is for post-secondary education, which may include education at a college, university or technical school To be an eligible institution, the school must be able to participate in the student aid program administered by the U.S. Department of Education (note: they don t have to participate but must be eligible to participate)

66 Claiming AOTC for a student who didn t pay qualifying college expenses. Educational expenses must be paid or considered paid by your client, your client s spouse or the dependent student claimed on the tax return 196 Claiming AOTC for a student for too many years. The AOTC is only available for the first four years of post-secondary education and your client can only claim it for four tax years per eligible student This limitation includes any year(s) your client claimed the Hope Credit 197 Claiming the CTC/ACTC a child who does not meet the age requirement The child must be under the age of 17 at the end of the tax year There are no exceptions to this rule

67 Claiming the CTC/ACTC a child who does not meet the dependency requirements The child must be claimed as a dependent on your client s return and meet all the eligibility rules for a dependent 199 Claiming the CTC/ACTC a child who does not meet the residency requirement The child must be a U.S. citizen, U.S. national or a U.S. resident alien and the child must have lived with your client for more than half the year If the qualifying child uses an ITIN, Individual Taxpayer Identification Number, the child must meet the substantial presence test to qualify

68 Form 886-H-DEP Page

69 States and Local Governments with Earned Income Tax Credit - 12/6/ States and Local Governments with Earned Income Tax Credit 12/6/ Questions

70 The Schedule is Finalized for the 44th Annual Federal Income Tax Schools November 2-3, 2017 Maquoketa, Iowa Centerstone Inn and Suites November 6-7, 2017 Le Mars, Iowa Le Mars Convention Center November 8-9, 2017 Atlantic, Iowa Cass County Community Center November 9-10, 2017 Mason City, Iowa North Iowa Area Community College November 16-17, 2017 Ottumwa, Iowa Indian Hills Community College November 20-21, 2017 Waterloo, Iowa Hawkeye Community College December 11-12, 2017 Ames, Iowa and Live Webinar Quality Inn and Suites The Scoop 8:00 am and 12:00pm January 25, 2017 February 22, 2017 March 8, 2017 March 22, 2017 April 5, 2017 April 19, 2017 April 17, 2017 May 31, The CALT Staff John D. Lawrence Interim Director Associate Dean, College of Agriculture & Life Sciences Extension Programs and Outreach Director, Agriculture & Natural Resources Extension 132 Curtiss Hall Iowa State University Ames, Iowa Kristine A. Tidgren Assistant Director Phone: (515) Fax: (515)

71 The CALT Staff Kristy S. Maitre Tax Specialist Phone: (515) Fax: (515) Tiffany L. Kayser Program Administrator Phone: (515) Fax: (515)

Earned Income Credit i

Earned Income Credit i ALL RIGHTS RESERVED. NO PART OF THIS COURSE MAY BE REPRODUCED IN ANY FORM OR BY ANY MEANS WITHOUT THE WRITTEN PERMISSION OF THE COPYRIGHT HOLDER. All materials relating to this course

Earned Income Credit i ALL RIGHTS RESERVED. NO PART OF THIS COURSE MAY BE REPRODUCED IN ANY FORM OR BY ANY MEANS WITHOUT THE WRITTEN PERMISSION OF THE COPYRIGHT HOLDER. All materials relating to this course

Earned Income Table. Earned Income for EIC, Additional Child Tax Credit and Dependent Care Credit. Common EIC Filing Errors

Earned Income Table Includes Taxable wages, salaries, and tips Union strike benefits Taxable long-term disability benefits received prior to minimum retirement age Net earnings from selfemployment Gross

Earned Income Table Includes Taxable wages, salaries, and tips Union strike benefits Taxable long-term disability benefits received prior to minimum retirement age Net earnings from selfemployment Gross

Coverdell Education Savings Account (ESA)

") 7. Coverdell Education Savings Account (ESA) Introduction If your modified adjusted gross income (MAGI) is less than $110,000 ($220,000 if filing a joint return), you may be able to establish a Coverdell

7. Coverdell Education Savings Account (ESA) Introduction If your modified adjusted gross income (MAGI) is less than $110,000 ($220,000 if filing a joint return), you may be able to establish a Coverdell

Nonrefundable Credits

Nonrefundable Credits TaxSlayer Navigation: Federal Section>Deductions>Credits Menu Select for Form 1116, Foreign Tax Credit Select for Form 2441 Child Tax Credit. See Child Tax Credit Tip & Interview

Nonrefundable Credits TaxSlayer Navigation: Federal Section>Deductions>Credits Menu Select for Form 1116, Foreign Tax Credit Select for Form 2441 Child Tax Credit. See Child Tax Credit Tip & Interview

Earned Income Table. Earned Income

Includes Taxable wages, salaries, and tips Union strike benefits Taxable long-term disability benefits received prior to minimum retirement age Net earnings from self-employment Gross income of a statutory

Includes Taxable wages, salaries, and tips Union strike benefits Taxable long-term disability benefits received prior to minimum retirement age Net earnings from self-employment Gross income of a statutory

Nonrefundable Credits

nrefundable Credits Link to Form 1116, Foreign Tax Credit page 1, if required. Link to Form 2441, page 1. Link to Form 8863. See Education Benefits tab. Link to Form 8880. See Child Tax Credit Tip and

nrefundable Credits Link to Form 1116, Foreign Tax Credit page 1, if required. Link to Form 2441, page 1. Link to Form 8863. See Education Benefits tab. Link to Form 8880. See Child Tax Credit Tip and

a Taxable interest. Attach Schedule B if required... 8a b Tax-exempt interest. Do not include on line 8a...

Form 1040 Department of the Treasury Internal Revenue Service (99) U.S. Individual Income Tax Return 2017 OMB No. 1545-0074 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31,

Form 1040 Department of the Treasury Internal Revenue Service (99) U.S. Individual Income Tax Return 2017 OMB No. 1545-0074 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31,

ELIGIBLE. Earned Income Credit (EIC)

") Department of the Treasury Internal Revenue Service Publication 596 Cat. No. 15173A Earned Income Credit (EIC) For use in preparing 2003 Returns?ARE YOU ELIGIBLE Look inside for... Detailed Examples Eligibility

Department of the Treasury Internal Revenue Service Publication 596 Cat. No. 15173A Earned Income Credit (EIC) For use in preparing 2003 Returns?ARE YOU ELIGIBLE Look inside for... Detailed Examples Eligibility

QUESTIONS AND ANSWERS ABOUT THE EARNED INCOME TAX CREDIT TAX YEAR 2010

QUESTIONS AND ANSWERS ABOUT THE EARNED INCOME TAX CREDIT TAX YEAR 2010 The federal Earned Income Tax Credit is designed to boost the wages of working families. The following questions and answers will

QUESTIONS AND ANSWERS ABOUT THE EARNED INCOME TAX CREDIT TAX YEAR 2010 The federal Earned Income Tax Credit is designed to boost the wages of working families. The following questions and answers will

Prepare, Print, and E-File Your Federal Tax Return for FREE!!

Free Forms Courtesy of FreeTaxUSA.com Prepare, Print, and E-File Your Federal Tax Return for FREE!! Go to www.freetaxusa.com to start your free return today! Form 8867 Department of the Treasury Internal

Free Forms Courtesy of FreeTaxUSA.com Prepare, Print, and E-File Your Federal Tax Return for FREE!! Go to www.freetaxusa.com to start your free return today! Form 8867 Department of the Treasury Internal

Tax Benefits for Higher Education

Department of the Treasury Internal Revenue Service Publication 970 (Rev. December 1998) Cat. No. 25221V Tax Benefits for Higher Education Contents Introduction... 1 Education Tax Credits... 2 Rules That

Department of the Treasury Internal Revenue Service Publication 970 (Rev. December 1998) Cat. No. 25221V Tax Benefits for Higher Education Contents Introduction... 1 Education Tax Credits... 2 Rules That

Earned Income Table. Earned Income

Earned Income Table Includes Taxable wages, salaries, and tips Union strike benefits Taxable long-term disability benefits received prior to minimum retirement age Net earnings from self-employment Gross

Earned Income Table Includes Taxable wages, salaries, and tips Union strike benefits Taxable long-term disability benefits received prior to minimum retirement age Net earnings from self-employment Gross

Earned Income Credit (EIC)

") Department of the Treasury Internal Revenue Service Publication 596 Cat. No. 15173A Earned Income Credit (EIC) For use in preparing 2013 Returns Contents What's New for 2013... 3 Reminders... 3 Chapter

Department of the Treasury Internal Revenue Service Publication 596 Cat. No. 15173A Earned Income Credit (EIC) For use in preparing 2013 Returns Contents What's New for 2013... 3 Reminders... 3 Chapter

This applies even if another person does not actually claim the taxpayer as a dependent. A taxpayer who

Personal Exemptions Introduction Identifying and entering the correct number of exemptions is a critical component of completing taxpayers returns, because each allowable exemption reduces their taxable

Personal Exemptions Introduction Identifying and entering the correct number of exemptions is a critical component of completing taxpayers returns, because each allowable exemption reduces their taxable

STANDARD DEDUCTIONS MACRS RECOVERY PERIODS

217 Medical Savings Accounts (MSA) 217 Annual Deductible Range Self-Only Coverage 2,25-3,35 Family Coverage 4,5-6,75 Maximum Out of Pocket Self-Only Coverage 4,5 Family Coverage 8,25 STANDARD DEDUCTIONS

217 Medical Savings Accounts (MSA) 217 Annual Deductible Range Self-Only Coverage 2,25-3,35 Family Coverage 4,5-6,75 Maximum Out of Pocket Self-Only Coverage 4,5 Family Coverage 8,25 STANDARD DEDUCTIONS

EITC Due Diligence i

EITC Due Diligence i ALL RIGHTS RESERVED. NO PART OF THIS COURSE MAY BE REPRODUCED IN ANY FORM OR BY ANY MEANS WITHOUT THE WRITTEN PERMISSION OF THE COPYRIGHT HOLDER. All materials relating to this course

EITC Due Diligence i ALL RIGHTS RESERVED. NO PART OF THIS COURSE MAY BE REPRODUCED IN ANY FORM OR BY ANY MEANS WITHOUT THE WRITTEN PERMISSION OF THE COPYRIGHT HOLDER. All materials relating to this course

City/State/Zip Relationship to Child Account Number Amount of Deposit

ESA APPLICATION Child/Student (Designated Beneficiary) Contributor (Depositor) - - - - Social Security Number Social Security Number - - Address Date of Birth Address Phone Number - - City/State/Zip Phone

ESA APPLICATION Child/Student (Designated Beneficiary) Contributor (Depositor) - - - - Social Security Number Social Security Number - - Address Date of Birth Address Phone Number - - City/State/Zip Phone

Earned Income Credit

Earned Income Credit Major update Earned Income Credit Pub 4491 Lesson 30 Pub 4012 Tab I needed for 2017 law change (disaster relief) Refundable Credit A refundable credit can generate a refund even if

Earned Income Credit Major update Earned Income Credit Pub 4491 Lesson 30 Pub 4012 Tab I needed for 2017 law change (disaster relief) Refundable Credit A refundable credit can generate a refund even if

The Earned Income Tax Credit

The Earned Income Tax Credit WHAT IS THE EARNED INCOME TAX CREDIT? The Earned Income Tax Credit (EITC) is a benefit for working people who have low to moderate income. It reduces the amount of taxes you

The Earned Income Tax Credit WHAT IS THE EARNED INCOME TAX CREDIT? The Earned Income Tax Credit (EITC) is a benefit for working people who have low to moderate income. It reduces the amount of taxes you

C Consumer Information on the Earned Income Tax Credit

APPENDIX C Consumer Information on the Earned Income Tax Credit The Earned Income Credit: A Powerful Benefit for People Who Work What is the Earned Income Credit (EIC)? The EIC is a tax benefit for working

APPENDIX C Consumer Information on the Earned Income Tax Credit The Earned Income Credit: A Powerful Benefit for People Who Work What is the Earned Income Credit (EIC)? The EIC is a tax benefit for working

IRS Federal Income Tax Publications provided by efile.com

IRS Federal Income Tax Publications provided by efile.com This publication should serve as a relevant source for up to date tax answers to your tax questions. Unlike most tax forms, many tax publications

IRS Federal Income Tax Publications provided by efile.com This publication should serve as a relevant source for up to date tax answers to your tax questions. Unlike most tax forms, many tax publications

TY2018 VITA Basic Certification Test - Study Guide

Scenario 1: Arnold TY2018 VITA Basic Certification Test - Study Guide Issue #1 Minimum Essential Coverage (MEC) (p4012 Tab H) See p4012 s ACA tab for a list of what counts as MEC Issue #2 Penalties for

Scenario 1: Arnold TY2018 VITA Basic Certification Test - Study Guide Issue #1 Minimum Essential Coverage (MEC) (p4012 Tab H) See p4012 s ACA tab for a list of what counts as MEC Issue #2 Penalties for

2017 Instructions for Schedule 8812

Department of the Treasury Internal Revenue Service 2017 Instructions for Schedule 8812 Child Tax Credit Part I of Schedule 8812 documents that any qualifying child whom you identify with an ITIN is a

Department of the Treasury Internal Revenue Service 2017 Instructions for Schedule 8812 Child Tax Credit Part I of Schedule 8812 documents that any qualifying child whom you identify with an ITIN is a

QUESTIONS AND ANSWERS ABOUT THE CHILD AND DEPENDENT CARE TAX CREDIT TAX YEAR 2011

QUESTIONS AND ANSWERS ABOUT THE CHILD AND DEPENDENT CARE TAX CREDIT TAX YEAR 2011 The federal Child and Dependent Care Tax Credit can help working families pay for the child care they need to work. The

QUESTIONS AND ANSWERS ABOUT THE CHILD AND DEPENDENT CARE TAX CREDIT TAX YEAR 2011 The federal Child and Dependent Care Tax Credit can help working families pay for the child care they need to work. The

TY2017 VITA Basic Certification Test - Study Guide

Scenario 1: Albright TY2017 VITA Basic Certification Test - Study Guide Issue #1 Minimum Essential Coverage (MEC) (p4012 Tab H) See p4012 s ACA tab for a list of what counts as MEC Issue #2 Penalties for

Scenario 1: Albright TY2017 VITA Basic Certification Test - Study Guide Issue #1 Minimum Essential Coverage (MEC) (p4012 Tab H) See p4012 s ACA tab for a list of what counts as MEC Issue #2 Penalties for

Applications and Due Diligence of the Earned Income Tax Credit

Applications and Due Diligence of the Earned Income Tax Credit Developed by Raven Deerwater, EA, PhD CSEA President Palomar Chapter December 19, 2012 Raven Deerwater EA, Ph.D has a tax practice in Mendocino,

Applications and Due Diligence of the Earned Income Tax Credit Developed by Raven Deerwater, EA, PhD CSEA President Palomar Chapter December 19, 2012 Raven Deerwater EA, Ph.D has a tax practice in Mendocino,

Education Tax Benefits

Education Tax Benefits i ALL RIGHTS RESERVED. NO PART OF THIS COURSE MAY BE REPRODUCED IN ANY FORM OR BY ANY MEANS WITHOUT THE WRITTEN PERMISSION OF THE PUBLISHER. Purchase of a course includes a license

Education Tax Benefits i ALL RIGHTS RESERVED. NO PART OF THIS COURSE MAY BE REPRODUCED IN ANY FORM OR BY ANY MEANS WITHOUT THE WRITTEN PERMISSION OF THE PUBLISHER. Purchase of a course includes a license

Standard Deductions. MACRS Recovery Periods. Tax Preparers Due Diligence Requirements for EITC Medical Savings Accounts (MSA)

") Tax Preparers Due Diligence Requirements for EITC Paid preparers who file EITC returns or claims for refunds for clients must meet four due diligence requirements. Those who fail to do so can be assessed

Tax Preparers Due Diligence Requirements for EITC Paid preparers who file EITC returns or claims for refunds for clients must meet four due diligence requirements. Those who fail to do so can be assessed

Your guide to Coverdell Education Savings Accounts. Coverdell Education Savings Account Disclosure Statement and Custodial Agreement

Your guide to Coverdell Education Savings Accounts Coverdell Education Savings Account Disclosure Statement and Custodial Agreement Your guide to Coverdell Education Savings Accounts This section of the

Your guide to Coverdell Education Savings Accounts Coverdell Education Savings Account Disclosure Statement and Custodial Agreement Your guide to Coverdell Education Savings Accounts This section of the

CESAs Coverdell Education Savings Accounts. Questions & Answers

CESAs Coverdell Education Savings Accounts Questions & Answers What is a Coverdell Education Savings Account? A Coverdell Education Savings Account is a type of tax-preferred savings and investment account

CESAs Coverdell Education Savings Accounts Questions & Answers What is a Coverdell Education Savings Account? A Coverdell Education Savings Account is a type of tax-preferred savings and investment account

EDUCATION IRA/COVERDELL EDUCATION ACCOUNT APPLICATION AND DISCLOSURE STATEMENT Account Number (if known)

") EDUCATION IRA/COVERDELL EDUCATION ACCOUNT APPLICATION AND DISCLOSURE STATEMENT Account Number (if known) Registered Representative Return your completed application to: William Blair Funds, P.O. Box 8506

EDUCATION IRA/COVERDELL EDUCATION ACCOUNT APPLICATION AND DISCLOSURE STATEMENT Account Number (if known) Registered Representative Return your completed application to: William Blair Funds, P.O. Box 8506

social security number relationship to you Add numbers on d Total number of exemptions claimed... lines above

Form 1040 Department of the Treasury Internal Revenue Service (99) U.S. Individual Income Tax Return 2017 OMB No. 1545-0074 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31,

Form 1040 Department of the Treasury Internal Revenue Service (99) U.S. Individual Income Tax Return 2017 OMB No. 1545-0074 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31,

EDUCATIONAL SAVINGS OPTIONS COMPARISON

EDUCATIONAL SAVINGS OPTIONS COMPARISON January 17, 2013 SCHOLARSHARE COVERDELL ESA ROTH IRA TRADITIONAL IRA SAVINGS BONDS GIFTS TO CHILDREN SUMMARY OF THE OPTION ScholarShare is a college savings program

EDUCATIONAL SAVINGS OPTIONS COMPARISON January 17, 2013 SCHOLARSHARE COVERDELL ESA ROTH IRA TRADITIONAL IRA SAVINGS BONDS GIFTS TO CHILDREN SUMMARY OF THE OPTION ScholarShare is a college savings program

Figuring your Taxes and Credits

Figuring your Taxes and Credits This self-study explains how to figure your tax and how to figure the tax of certain children who have more than $2,100 of unearned income. Also discussed are various tax

Figuring your Taxes and Credits This self-study explains how to figure your tax and how to figure the tax of certain children who have more than $2,100 of unearned income. Also discussed are various tax

STANDARD DEDUCTIONS MACRS RECOVERY PERIODS

216 Medical Savings Accounts (MSA) 216 Annual Deductible Range Self-Only Coverage 2,25-3,35 Family Coverage 4,45-6,7 Maximum Out of Pocket Self-Only Coverage 4,45 Family Coverage 8,15 STANDARD DEDUCTIONS

216 Medical Savings Accounts (MSA) 216 Annual Deductible Range Self-Only Coverage 2,25-3,35 Family Coverage 4,45-6,7 Maximum Out of Pocket Self-Only Coverage 4,45 Family Coverage 8,15 STANDARD DEDUCTIONS

BASIC CERTIFICATION STUDY GUIDE Tax Year 2018

BASIC CERTIFICATION STUDY GUIDE Tax Year 2018 Table of Contents BASIC SCENARIO 1: Jeff and Linda Arnold... 1 BASIC SCENARIO 2: Ava Harvard... 2 BASIC SCENARIO 3: Ellen Santos... 3 BASIC SCENARIO 4: Christopher

BASIC CERTIFICATION STUDY GUIDE Tax Year 2018 Table of Contents BASIC SCENARIO 1: Jeff and Linda Arnold... 1 BASIC SCENARIO 2: Ava Harvard... 2 BASIC SCENARIO 3: Ellen Santos... 3 BASIC SCENARIO 4: Christopher

STANDARD DEDUCTIONS MACRS RECOVERY PERIODS

217 Medical Savings Accounts (MSA) 217 Annual Deductible Range Self-Only Coverage 2,25-3,35 Family Coverage 4,5-6,75 Maximum Out of Pocket Self-Only Coverage 4,5 Family Coverage 8,25 STANDARD DEDUCTIONS

217 Medical Savings Accounts (MSA) 217 Annual Deductible Range Self-Only Coverage 2,25-3,35 Family Coverage 4,5-6,75 Maximum Out of Pocket Self-Only Coverage 4,5 Family Coverage 8,25 STANDARD DEDUCTIONS

Arizona Form 2011 Property Tax Refund (Credit) Claim 140PTC

Claim 140PTC") Arizona Form 2011 Property Tax Refund (Credit) Claim 140PTC NOTICE: If you are age 70 or over and meet certain tests, you may be able to defer the payment of your property taxes on your home. You should

Arizona Form 2011 Property Tax Refund (Credit) Claim 140PTC NOTICE: If you are age 70 or over and meet certain tests, you may be able to defer the payment of your property taxes on your home. You should

Arizona Form 2012 Property Tax Refund (Credit) Claim 140PTC

Claim 140PTC") Arizona Form 2012 Property Tax Refund (Credit) Claim 140PTC NOTICE: If you are age 70 or over and meet certain tests, you may be able to defer the payment of your property taxes on your home. You should

Arizona Form 2012 Property Tax Refund (Credit) Claim 140PTC NOTICE: If you are age 70 or over and meet certain tests, you may be able to defer the payment of your property taxes on your home. You should

ARTICLE I ARTICLE II ARTICLE III ARTICLE IV ARTICLE V

Coverdell Education Savings Custodial Account (Under section 530 of the Internal Revenue Code) Form 5305-EA (Rev. October 2010) Department of the Treasury, Internal Revenue Service. Do not file with the

Coverdell Education Savings Custodial Account (Under section 530 of the Internal Revenue Code) Form 5305-EA (Rev. October 2010) Department of the Treasury, Internal Revenue Service. Do not file with the

File by Mail Instructions for your 2017 Federal Tax Return Important: Your taxes are not finished until all required steps are completed.

File by Mail Instructions for your 2017 Federal Tax Return Important: Your taxes are not finished until all required steps are completed. calvin & kerty L Satur 1651 Deer Run Dr. Burlington, KY 41005 Balance

File by Mail Instructions for your 2017 Federal Tax Return Important: Your taxes are not finished until all required steps are completed. calvin & kerty L Satur 1651 Deer Run Dr. Burlington, KY 41005 Balance

COVERDELL EDUCATION SAVINGS ACCOUNT CUSTODIAL AGREEMENT & DISCLOSURE STATEMENT