Today s key challenge in Treasury Transfer Pricing & Treasury

|

|

|

- Cecil Nelson

- 6 years ago

- Views:

Transcription

1 Today s key challenge in Treasury Transfer Pricing & Treasury

2 Content The word of the President Virtual reality of Treasury Overview - Treasury operations Intercompany financing Cash pooling Guarantees Documentation requirements Key Takeaways s role

3 Key facts and methodology All industries and areas of service 24 countries Conduct between July and October 2016 The "virtual reality" of treasury Long and short questionnaires interviews completed Want to download the full report? Please visit our website: rate-treasury-solutions Treasurers and Chief Financial Officers Financial Transactions The "virtual reality" of treasury April

4 Key Findings High on the agenda for treasurers: The agendas of the treasurer and the CFO should be better aligned True focus on cash flows forecasting may provide a quick return Treasurers need to take action to safeguard assets with rising cybersecurity threats Treasury s scope continues to expand and is now a company-wide process it no longer operates as a single department. With treasury processes becoming increasingly virtual, treasurers need to collaborate more with the business, shared services and banks and raise their game in IT security, valuation and financial risk management to succeed in today s environment. Treasurers need the means to truly make treasury resilient and effective Base Erosion and Profit Shifting (BEPS) will bring tax and treasury closer together Base Erosion and Profit Shifting (BEPS) will bring tax and treasury closer together New fiscal legislation means substance and transfer pricing will take centre stage. This may have a material impact on the location of treasury activities, distribution of decision power and configuration of systems. As a result, treasury will need to work more closely with tax to assess the impact and properly prepare their organisations. Financial Transactions The "virtual reality" of treasury April

, Exit Taxation, Switch-over clause, General Anti-Abuse Rule, Hybrid")

5 BEPS, became a reality in EU Tax paradigm or revolution of the century, but fairness in tax at the price of unending difficulties Examples: Restriction on interest deduction (interest deductible only if < 30% of EBITDA with threshold of 1m situations in which entities loss-making will no longer be able to deduct interest), Exit Taxation, Switch-over clause, General Anti-Abuse Rule, Hybrid mismatch and extension of Controlled Foreign Company rules generating whole wodge of attempts to tax anything that may not have been taxed New framework: everyone claims its "fair share" of the tax cake Main idea is to align TAXABLE BASE with VALUE CREATION. 3 main watchwords: (1) Consistency, (2) Substance and (3) Transparency Treasurers could argue TP rules already existed long before Some countries already started to question to justify the "fair" TP Major principle ( choosing the option that costs the least in tax ) has now been called into question

6 5 key TP questions: what, how, why, where and who? WHAT types of treasury activity does Group Treasury (GT) handle centrally and recharge to affiliates? HOW is GT organized to serve its affiliates and how can treasury management add value? WHY are treasury activities handled centrally? WHERE is the GT function located? WHO takes and bears the financial risks? Last question is crucial: who, ultimately, will end up bearing the risk. For instance, who bears the loss if the borrower subsidiary goes bust? Who is responsible if the guarantee issued by central treasury is called? Based on this question, you can work out the margins to be applied

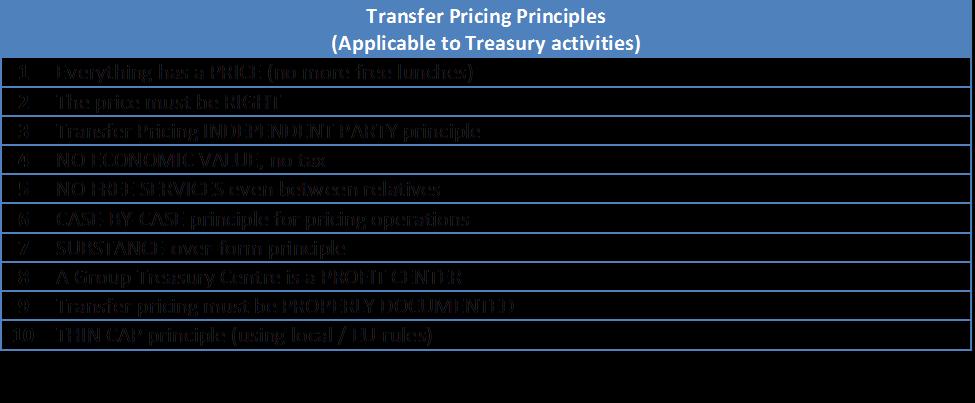

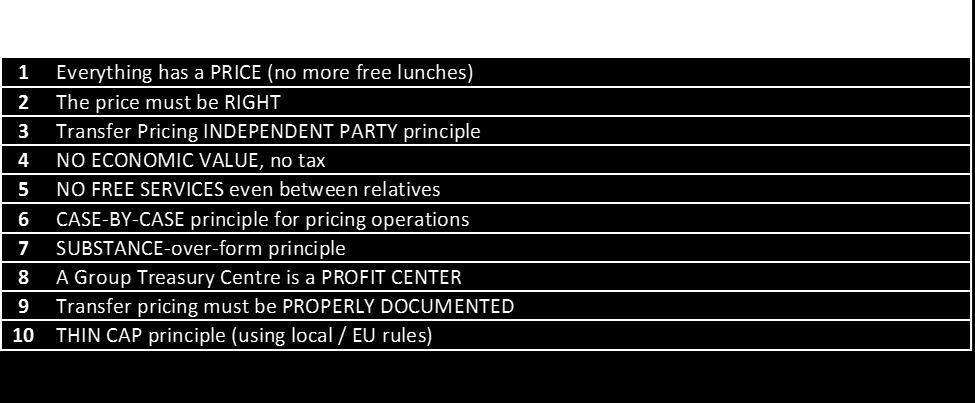

7 The 10 TP commandments are

More")

8 Be BEPS compliant "If you would know the value of money, go try to borrow some (French Proverb) More ironically, we might say: "In business, the lower the price, the bigger the sticker" (even between sub s of the same group)

9 Overview - Treasury operations Focus on the aggregate business results Short- term debt management Long- term debt management Establishing global financing in a territory where substance can be maintained Excess cash management Working capital management TYPICAL TREASURY SERVICES PROVIDED INTRA- GROUP Other (ancillary) services Investment management (i.e. asset acquisition) Hedging (i.e. FX/currency) External funding optimization Risk management, incl. acknowledgement of financial risk More globally and regionally integrated business units

10 Intercompany financing Main focus areas Assess the creditworthiness of the borrowing entities Define the functional and risk profile of the entities involved Assess the arm s length intra-group interest rate - can we rely on the yield curves only?

11 Intercompany financing ParentCo Related party financing Why is the entity borrowing? What is the borrower s credit rating? Do internal / external comparables exist? Do comparability adjustments need to be performed? Rationale for borrowing Debt capacity Arm s length interest rate Interest payments SubCos Based on debt/equity ratios / projections, could the entity borrow?

12 Intercompany financing Factors influencing interest rates Impact on interest rate Higher Bullet Pre-payment Long term Mezzanine On maturity Unsecured Higher risk currency Unguaranteed Nonconvertible Junior Lower Capital & Interest Call Guaranteed Short term Senior Quarterly (regular) Secured Lower risk currency Convertible Impact of covenants Commercial & Economic Rationale Impact on Fixed Vs. Floating loans

13 Intercompany financing Interest rate setting options Complexity Higher Lower Entity Credit Risk Premium Ratings per entity Segmentation into ratings buckets Combination of ratings and credit limits Notching only (potentially with credit limits) Country Risk Premium Countryspecific spreads Key country premia/discounts, with regional segmentation for rest Regional segmentation only Limited consideration of country risk, as exception Applicable Fees Transactional fee benchmarking Benchmarking for key services only Cost(plus) based remuneration (service spread) Considered as stewardship or immaterial Risk of Challenge Technically Strongest Practical and Defensible Subject to adjustment

14 Cash pooling Main focus areas Create a netting system used for intercompany payments and receipts Assess the arm s length remuneration for the cash pool header Determine the relative contributions of the various participants Allocate the cash pool advantages amongst the participants

15 Cash pooling Factors influencing cash pooling Lending Rate Base Rate + Entity Credit Risk Premium + Country Risk Premium + Cash Pool Service Fee + Cash Pool Facility Fee SHORT-TERM FUNDING NEEDS The spread between the two rates represents the additional remuneration for the cash pool leader EXCESS CASH Deposit Rate Base Rate - Deposit Rate Spread - Cash Pool Service Fee Reduce the MNE s total external funding costs Help manage certain risks such as liquidity or foreign exchange Help obtaining more favourable borrowing conditions Management of volatility of the group's liquid cash resources Decision-making for financing is centralised

16 Cash pooling TP considerations Selection of appropriate TP Method Taking care of additional tax considerations Long term cash position PE, Thin Cap, VAT implications Key transfer pricing aspects: credit risk synergies Considering individual facts and circumstances Type of cash pooling Functions and risks Substance Contractual framework Nature and scope of realized synergies How to measure the cash pool advantage?

17 Cash pooling Types of cash pools Zero Balanced cash pool vs. Notional cash pool

18 Guarantees Main focus areas Implicit versus explicit guarantees Determine the creditworthiness of the borrowing entities Assess the arm s length intra-group guarantee fee

19 Guarantees Benefits Increase the borrowing capacity of related entities. Allow the beneficiary to tap resources that it could not access in the absence of a guarantee. By ensuring fulfilment in case of performance failure, an intercompany guarantee may provide better contractual terms also in relation to commercial transactions. FINANCIAL GUARANTEE Purpose: reduce risk to lenders Main benefits: Access to credit borrowing Substitution for capital in the subsidiary Cheaper access to credit decreasing the risks assumed by the third parties involved The reliability of the guarantor is passed to the related entity resulting in more beneficial terms and conditions for the transaction SUPPLY CHAIN GUARANTEE Purpose: reduce risk to customers of recipient Main benefits: Secure payment The seller can obtain advance payment Secured compensation for nonfulfilment of any important obligations

20 Guarantees Determining a range of arm s length guarantee fee bps Above the top red threshold, a guarantee recipient would not be willing to pay for obtaining the guarantee Yield Savings Approach Applicable only in cases where the guarantee is a means to reduce the associated financing costs Return on Capital Approach Applicable for Supply-chain / Performance Guarantees 0 bps Below the bottom red threshold, an external (independent) guarantor would not be willing to provide the guarantee Transfer price Cost approach Represents the minimum a guarantor would accept to provide a guarantee.

21 Guarantees Factors influencing the guarantee pricing Credit quality assessment Terms of the underlying debt / transaction Impact on the pricing Higher High PD High rate Long term High LGD On maturity Higher risk currency Fees Lower Low PD Low rate Short term Low LGD Quarterly (regular) Lower risk currency

22 Documentation requirements Main focus areas OECD BEPS Action 13 Align transfer pricing outcome with value creation

23 Documentation requirements OECD Base Erosion and Profit Shifting Action Item 13 - three-tiered approach Provides aggregated financial and tax data by tax jurisdiction to facilitate risk assessments Detailed information relating to specific intercompany transactions. Assures compliance with arm s length principle in material transfer pricing positions impacting a specific jurisdiction Complete picture of MNE s global operations, including analysis of profit drivers, supply chains, intangibles, and financing

24 Documentation requirements The importance of a proper TP documentation Action 13 - The Masterfile should include: - A general description how the group is financed, including important financing arrangements with unrelated parties - The identification of any members of an MNE group that provide a central financing function for the group, including the country under whose laws the entity is organised and the place of effective management of such entities - A general description of the MNE s general transfer pricing policies related to financial arrangements between associated parties Treasury operations with appropriate substance What is sufficient substance? Functional analysis Does this differ for holding and financing activities? What would best in class look like? Acknowledgement of financial risk Entity having personnel with ability to evaluate, decline risk, and / or manage risk Entity having capital to bear such risk

25 Documentation requirements Where to start? Identify Take an inventory of your intercompany financial transaction Quantify Check the materiality of each transaction Document Have discussion with treasury personnel to understand how these transactions are currently priced and what support may be on file Determine whether transfer pricing documentation already in place is current Evaluate and support your intercompany financial transactions Do not ignore them!

26 Key Takeaways Wrap-up Treasury operations optimizing the MNE s financial structure (e.g. cash / working capital management) Substance requirements align functional and risk profiles with value creation Transfer pricing outcome need for contemporaneous documentation How can we help?

27 s role We can bring to bear s wealth of service offerings and experience to your organization in the following areas Accounting and controls Treasury and risk technology Treasury organization and strategy Cash and liquidity management Financial risk management Accounting and disclosure (Lux GAAP and IFRS) Tax implications of treasury transactions Regulatory compliance External and internal audit support Policies, procedures, and controls Technology vision and strategy Requirements definition and system selection System design and implementation Reporting solutions Leading practice assessments and performance benchmarking Governance structure and organizational design Treasury strategy, planning, and budgeting Training and change management Cash forecasting Debt & investment management Working capital solutions (A/P, A/R, inventory) Investment portfolio management Interest rate Foreign exchange Commodity Counterparty/credit

28 Your contact at Luxembourg Christophe Hillion Partner, Transfer Pricing Philippe Förster Director, IFRS & Treasury Leader Thomas Campione Senior Manager, IFRS & Treasury

29 Thank you 2017 PricewaterhouseCoopers. All rights reserved. In this document, "" refers to PricewaterhouseCoopers, Société coopérative (address: 2, rue Gerhard Mercator, B.P. 1443, L-1014 Luxembourg) which is a member firm of PricewaterhouseCoopers International Limited, each member firm of which is a separate legal entity.

BEPS Everything has a price a Transfer Price F R A N Ç O I S M A S Q U E L I E R, C H A I R M A N A T E L E A C T M E E T I N G - D U B L I N

BEPS Everything has a price a Transfer Price F R A N Ç O I S M A S Q U E L I E R, C H A I R M A N A T E L E A C T M E E T I N G - D U B L I N 2 0 1 6 BEPS and TP Everything has a price a Transfer Price

BEPS Everything has a price a Transfer Price F R A N Ç O I S M A S Q U E L I E R, C H A I R M A N A T E L E A C T M E E T I N G - D U B L I N 2 0 1 6 BEPS and TP Everything has a price a Transfer Price

FTA Treasury Implications of Global Tax Reform

FTA Treasury Implications of Global Tax Reform Geoff Gill, Transfer Pricing Partner, Deloitte 16 November 2017 Agenda 1. G20 BEPS global tax reset & financing 2. Australian approach law changes, case law

FTA Treasury Implications of Global Tax Reform Geoff Gill, Transfer Pricing Partner, Deloitte 16 November 2017 Agenda 1. G20 BEPS global tax reset & financing 2. Australian approach law changes, case law

Headline Verdana Bold International Tax matters ICPAU Tax Seminar, Hotel Africana November, 2017

Headline Verdana Bold International Tax matters ICPAU Tax Seminar, Hotel Africana November, 2017 Contents Related party transactions 3 URA practice on international tax 14 OCED Action Plan on BEPS 30 2017

Headline Verdana Bold International Tax matters ICPAU Tax Seminar, Hotel Africana November, 2017 Contents Related party transactions 3 URA practice on international tax 14 OCED Action Plan on BEPS 30 2017

MANAGING TRANSFER PRICING ISSUES IN AN EVOLVING BEPS ENVIRONMENT

MANAGING TRANSFER PRICING ISSUES IN AN EVOLVING BEPS ENVIRONMENT ANTON HUME / DAN MCGEOWN / VEENA PARRIKAR / RICHARD VAN DER POEL / JAY TANG 2 JUNE 2015 AGENDA Control Over Transfer Pricing Policies and

MANAGING TRANSFER PRICING ISSUES IN AN EVOLVING BEPS ENVIRONMENT ANTON HUME / DAN MCGEOWN / VEENA PARRIKAR / RICHARD VAN DER POEL / JAY TANG 2 JUNE 2015 AGENDA Control Over Transfer Pricing Policies and

OECD non-consensus discussion draft on the transfer pricing aspects of financial transactions: no longer just about contractual risk

from Transfer Pricing OECD non-consensus discussion draft on the transfer pricing aspects of financial transactions: no longer just about contractual risk July 5, 2018 In brief One of the last missing

from Transfer Pricing OECD non-consensus discussion draft on the transfer pricing aspects of financial transactions: no longer just about contractual risk July 5, 2018 In brief One of the last missing

IBFD Course Programme International Tax Planning after BEPS and the MLI

IBFD Course Programme International Tax Planning after BEPS and the MLI Summary Recent developments such as the BEPS project and the Multilateral Instrument in international taxation, but also unilateral

IBFD Course Programme International Tax Planning after BEPS and the MLI Summary Recent developments such as the BEPS project and the Multilateral Instrument in international taxation, but also unilateral

The OECD s 3 Major Tax Initiatives

The OECD s 3 Major Tax Initiatives 1. The Global Forum on Transparency and Exchange of Information for Tax Purposes Peer review of ~ 100 countries International standard for transparency and exchange of

The OECD s 3 Major Tax Initiatives 1. The Global Forum on Transparency and Exchange of Information for Tax Purposes Peer review of ~ 100 countries International standard for transparency and exchange of

OECD releases first discussion draft on transfer pricing aspects of financial transactions

6 July 2018 Global Tax Alert OECD releases first discussion draft on transfer pricing aspects of financial transactions NEW! EY Tax News Update: Global Edition EY s new Tax News Update: Global Edition

6 July 2018 Global Tax Alert OECD releases first discussion draft on transfer pricing aspects of financial transactions NEW! EY Tax News Update: Global Edition EY s new Tax News Update: Global Edition

Mr. Joe Andrus Head of Transfer Pricing Unit Centre for Tax Policy and Administration OECD 2, rue Andre Pascal Paris France.

PricewaterhouseCoopers Aktiengesellschaft Wirtschaftsprüfungsgesellschaft Mr. Joe Andrus Head of Transfer Pricing Unit Centre for Tax Policy and Administration OECD 2, rue Andre Pascal 75775 Paris France

PricewaterhouseCoopers Aktiengesellschaft Wirtschaftsprüfungsgesellschaft Mr. Joe Andrus Head of Transfer Pricing Unit Centre for Tax Policy and Administration OECD 2, rue Andre Pascal 75775 Paris France

The (Transfer) Price is Right!

Price is Right!") The (Transfer) Price is Right! There is no doubt about it, BEPS will be at the root of the tax revolution of the century. Although it will have a big impact on corporate treasurers, it looks as if most

The (Transfer) Price is Right! There is no doubt about it, BEPS will be at the root of the tax revolution of the century. Although it will have a big impact on corporate treasurers, it looks as if most

Bespoke services. Browse our menu of bespoke services to see how we can support your alternative investment fund with our expertise.

Bespoke services AIFM license assistance Valuation services for AIFMs Mock regulatory inspection Assurance services Health-check for AI funds VAT-savvy fund services Transfer pricing: intragroup financing

Bespoke services AIFM license assistance Valuation services for AIFMs Mock regulatory inspection Assurance services Health-check for AI funds VAT-savvy fund services Transfer pricing: intragroup financing

Study on Structures of Aggressive Tax Planning and Indicators

Study on Structures of Aggressive Tax Planning and Indicators Platform for Tax Good Governance 15 March 2016 Gaëtan Nicodème Context Fair and efficient corporate tax system: priority of the Commission

Study on Structures of Aggressive Tax Planning and Indicators Platform for Tax Good Governance 15 March 2016 Gaëtan Nicodème Context Fair and efficient corporate tax system: priority of the Commission

Skatteverket International Tax Planning 2016 CORIT

Skatteverket International Tax Planning Agenda Introduction General remarks on International Tax Planning Analysis of International Tax Planning Models and Indicators International IP Tax Planning and

Skatteverket International Tax Planning Agenda Introduction General remarks on International Tax Planning Analysis of International Tax Planning Models and Indicators International IP Tax Planning and

Taxation of financial instruments in a changing world

Taxation of financial instruments in a changing world Edoardo Traversa, Professor, Université Catholique de Louvain/Of Counsel, Liedekerke, Brussels Alain Goebel, Partner, Arendt & Medernach Jan Neugebauer,

Taxation of financial instruments in a changing world Edoardo Traversa, Professor, Université Catholique de Louvain/Of Counsel, Liedekerke, Brussels Alain Goebel, Partner, Arendt & Medernach Jan Neugebauer,

BEPS Country-by-Country Reporting Rules and New Documentation Requirements

BEPS Country-by-Country Reporting Rules and New Documentation Requirements, EY LLP, Couzin Taylor LLP 67 th Annual Tax Conference 67e Conférence fiscale annuelle 2015 Agenda 1. The BEPS project: Action

BEPS Country-by-Country Reporting Rules and New Documentation Requirements, EY LLP, Couzin Taylor LLP 67 th Annual Tax Conference 67e Conférence fiscale annuelle 2015 Agenda 1. The BEPS project: Action

EU state aid and other developments. 18 November 2016

EU state aid and other developments 18 November 2016 Disclaimer This presentation is provided solely for the purpose of enhancing knowledge on tax matters. It does not provide tax advice to any taxpayer

EU state aid and other developments 18 November 2016 Disclaimer This presentation is provided solely for the purpose of enhancing knowledge on tax matters. It does not provide tax advice to any taxpayer

IBFD Course Programme BEPS Country Implementation

IBFD Course Programme BEPS Country Implementation Summary On 5 October 2015, the OECD published the final reports of its 15-point base erosion and profit shifting (BEPS) project. A bit more than a year

IBFD Course Programme BEPS Country Implementation Summary On 5 October 2015, the OECD published the final reports of its 15-point base erosion and profit shifting (BEPS) project. A bit more than a year

BEPS and ATAD: Where do we stand?

BEPS and ATAD: Where do we stand? by Nicky Gouder Tax Partner Summary Quick Overview of the BEPS Project and ATAD; A Comparison of the BEPS Recommendations and the ATAD obstacles, conflicts. Is harmonious

BEPS and ATAD: Where do we stand? by Nicky Gouder Tax Partner Summary Quick Overview of the BEPS Project and ATAD; A Comparison of the BEPS Recommendations and the ATAD obstacles, conflicts. Is harmonious

European Commission publishes Anti Tax Avoidance Package

28 January 2016 - Number 65 Brazil Desk e-mail bulletin European Commission publishes Anti Tax Avoidance Package On 28 January 2016 the European Commission published an Anti Tax Avoidance Package containing

28 January 2016 - Number 65 Brazil Desk e-mail bulletin European Commission publishes Anti Tax Avoidance Package On 28 January 2016 the European Commission published an Anti Tax Avoidance Package containing

Hot topics Treasury seminar

Hot topics Treasury seminar Treasury in a transparent and new tax world Discover and unlock your potential Program Introduction on BEPS Potential implications for treasury o Interest deduction o Treaty

Hot topics Treasury seminar Treasury in a transparent and new tax world Discover and unlock your potential Program Introduction on BEPS Potential implications for treasury o Interest deduction o Treaty

Overview of Practical Portfolio

United Nations Practical Portfolio: Protecting the Tax Base of Developing Countries with respect to Base Eroding Payments of Interest Brian Arnold Senior Adviser Canadian Tax Foundation UN-ITC Workshop

United Nations Practical Portfolio: Protecting the Tax Base of Developing Countries with respect to Base Eroding Payments of Interest Brian Arnold Senior Adviser Canadian Tax Foundation UN-ITC Workshop

Practical Implications of BEPS

www.pwc.com/il Practical Implications of BEPS Vered Kirshner, Tax Partner, PwC Israel Ben Blumenfeld, Tax and Transfer Pricing Senior Manager, PwC Israel Aim of BEPS Action plan backed by the OECD and

www.pwc.com/il Practical Implications of BEPS Vered Kirshner, Tax Partner, PwC Israel Ben Blumenfeld, Tax and Transfer Pricing Senior Manager, PwC Israel Aim of BEPS Action plan backed by the OECD and

Intercompany financing facing new challenges. EY Africa Tax Conference September 2014

Intercompany financing facing new challenges EY Africa Tax Conference September 2014 Panel Moderator Ide Louw International Tax EY South Africa Panel Joseph Pagop Noupoue EY Jemimah Mugo EY Kenya Michael

Intercompany financing facing new challenges EY Africa Tax Conference September 2014 Panel Moderator Ide Louw International Tax EY South Africa Panel Joseph Pagop Noupoue EY Jemimah Mugo EY Kenya Michael

BEPS Impact on Private Equity

BEPS Impact on Private Equity BEPS impact on private equityspace An Indian perspective In this age of increasing focus on bottomlines, it is indeed tempting for a global tax director of a multinational

BEPS Impact on Private Equity BEPS impact on private equityspace An Indian perspective In this age of increasing focus on bottomlines, it is indeed tempting for a global tax director of a multinational

IMPACT OF TAX ON M&A. Simon Fletcher 14 October 2016

IMPACT OF TAX ON M&A Simon Fletcher AGENDA 1. Tax environment 2. Recent developments 3. Impact on M&A 4. Questions Disclaimer: this presentation is intended to be for general guidance on matters of interest,

IMPACT OF TAX ON M&A Simon Fletcher AGENDA 1. Tax environment 2. Recent developments 3. Impact on M&A 4. Questions Disclaimer: this presentation is intended to be for general guidance on matters of interest,

International trends in taxation of capital and financial products and the impact on Thai Business

15th Annual Conference Maximise www.pwc.com/th International trends in taxation of capital and financial products and the impact on Thai Business Shareholder Value through Effective TAX Planning 2014 Agenda

15th Annual Conference Maximise www.pwc.com/th International trends in taxation of capital and financial products and the impact on Thai Business Shareholder Value through Effective TAX Planning 2014 Agenda

Recent Transfer Pricing Developments

Recent Transfer Pricing Developments CA Rachesh Kotak September 08, 2017 Setting the context Old world New world Compliance driven Reliance on local documentation One-sided approaches Protracted litigation

Recent Transfer Pricing Developments CA Rachesh Kotak September 08, 2017 Setting the context Old world New world Compliance driven Reliance on local documentation One-sided approaches Protracted litigation

Implementation of Masterfile and Localfile (BEPS Action 13) Georg Berka

Georg Berka") Implementation of Masterfile and Localfile (BEPS Action 13) Georg Berka Roadmap BEPS Action 13 in general Content of Masterfile Content of Localfile How Masterfile and Local File can be implemented chapter

Implementation of Masterfile and Localfile (BEPS Action 13) Georg Berka Roadmap BEPS Action 13 in general Content of Masterfile Content of Localfile How Masterfile and Local File can be implemented chapter

BEPS & transfer pricing

BEPS & transfer pricing May 2015 Suchint Majmudar, Taxand India Amit Rana, GE Polly Mak, Michelin Tim Wach, Taxand Global Contents 1. Introduction: background to BEPS 2. What is BEPS? 3. Key BEPS concerns

BEPS & transfer pricing May 2015 Suchint Majmudar, Taxand India Amit Rana, GE Polly Mak, Michelin Tim Wach, Taxand Global Contents 1. Introduction: background to BEPS 2. What is BEPS? 3. Key BEPS concerns

Tax Insights OECD releases Discussion Draft on the transfer pricing of financial transactions: An Australian perspective

17 July 2018 Australia 2018/14 Tax Insights OECD releases Discussion Draft on the transfer pricing of financial transactions: An Australian perspective Snapshot On 3 July 2018, the OECD released a Discussion

17 July 2018 Australia 2018/14 Tax Insights OECD releases Discussion Draft on the transfer pricing of financial transactions: An Australian perspective Snapshot On 3 July 2018, the OECD released a Discussion

Resolving transfer pricing controversies, handling audits and queries, and best practices in TP documentation: A practical guide

Resolving transfer pricing controversies, handling audits and queries, and best practices in TP documentation: A practical guide Douglas Fone Global Partner, Transfer Pricing Associates 1 Content 1. Introduction

Resolving transfer pricing controversies, handling audits and queries, and best practices in TP documentation: A practical guide Douglas Fone Global Partner, Transfer Pricing Associates 1 Content 1. Introduction

SUBSTANCE IS KING IN THE NEW WORLD ORDER TAX EXECUTIVES INSTITUTE, INC. MARCH 1, 2018

CPAs & ADVISORS experience direction // SUBSTANCE IS KING IN THE NEW WORLD ORDER TAX EXECUTIVES INSTITUTE, INC. MARCH 1, 2018 William D. James Principal Transfer Pricing & David H. Whitmer Director Transfer

CPAs & ADVISORS experience direction // SUBSTANCE IS KING IN THE NEW WORLD ORDER TAX EXECUTIVES INSTITUTE, INC. MARCH 1, 2018 William D. James Principal Transfer Pricing & David H. Whitmer Director Transfer

Cyprus Tax Update. Kyiv May 2018

Cyprus Tax Update Kyiv May 2018 Today s agenda 1. Snapshot of Cyprus tax system 2. Developments affecting the Cyprus tax regime 3. Selected developments : a) ATAD b) TP 4. Selected structures 5. Expected

Cyprus Tax Update Kyiv May 2018 Today s agenda 1. Snapshot of Cyprus tax system 2. Developments affecting the Cyprus tax regime 3. Selected developments : a) ATAD b) TP 4. Selected structures 5. Expected

Chinese Transfer Pricing Regulations and Their Implications

Chinese Transfer Pricing Regulations and Their Implications Pim Fris Special Consultant December 12, 2006 Shanghai Introduction Masterfile outline OECD documentation Typical OECD compliant transfer pricing

Chinese Transfer Pricing Regulations and Their Implications Pim Fris Special Consultant December 12, 2006 Shanghai Introduction Masterfile outline OECD documentation Typical OECD compliant transfer pricing

OECD Publishes Guidance on Transfer Pricing Documentation and Country-by-Country Reporting

17 September 2014 OECD Publishes Guidance on Transfer Pricing Documentation and Country-by-Country Reporting Action 13 On 16 September 2014, the Organization for Economic Co-operation and Development (

17 September 2014 OECD Publishes Guidance on Transfer Pricing Documentation and Country-by-Country Reporting Action 13 On 16 September 2014, the Organization for Economic Co-operation and Development (

Austria publishes draft regulation for implementation of Transfer Pricing Documentation Law

3 June 2016 Global Tax Alert News from Transfer Pricing Austria publishes draft regulation for implementation of Transfer Pricing Documentation Law EY Global Tax Alert Library Access both online and pdf

3 June 2016 Global Tax Alert News from Transfer Pricing Austria publishes draft regulation for implementation of Transfer Pricing Documentation Law EY Global Tax Alert Library Access both online and pdf

BELGIUM GLOBAL GUIDE TO M&A TAX: 2018 EDITION

BELGIUM 1 BELGIUM INTERNATIONAL DEVELOPMENTS 1. WHAT ARE RECENT TAX DEVELOPMENTS IN YOUR COUNTRY WHICH ARE RELEVANT FOR M&A DEALS AND PRIVATE EQUITY? A major corporate income tax reform has been published

BELGIUM 1 BELGIUM INTERNATIONAL DEVELOPMENTS 1. WHAT ARE RECENT TAX DEVELOPMENTS IN YOUR COUNTRY WHICH ARE RELEVANT FOR M&A DEALS AND PRIVATE EQUITY? A major corporate income tax reform has been published

Korean Tax Update BEPS Implementation

Presentation for KGCCI Korean Tax Update BEPS Implementation May 2018 CONTENTS I. BEPS: Backgrounds What is BEPS? Backgrounds for OECD BEPS Project BEPS Action plans II. BEPS Implementation in Korea I.

Presentation for KGCCI Korean Tax Update BEPS Implementation May 2018 CONTENTS I. BEPS: Backgrounds What is BEPS? Backgrounds for OECD BEPS Project BEPS Action plans II. BEPS Implementation in Korea I.

Overview of OECD Action Plan on Base Erosion and Profit Shifting (BEPS)

") Overview of OECD Action Plan on Base Erosion and Profit Shifting (BEPS) Monia Naoum, IBFD Research Associate Emily Muyaa, IBFD Research Associate 18 June 2015 1 Introduction: Globalization and its impact

Overview of OECD Action Plan on Base Erosion and Profit Shifting (BEPS) Monia Naoum, IBFD Research Associate Emily Muyaa, IBFD Research Associate 18 June 2015 1 Introduction: Globalization and its impact

Global Transfer Pricing Conference

www.pwc.com/transferpricing Global Transfer Pricing Conference Financial transactions the centre of attention October 2016 The new normal full TransParency Today s presenters Jeff Rogers Canada Nick Houseman

www.pwc.com/transferpricing Global Transfer Pricing Conference Financial transactions the centre of attention October 2016 The new normal full TransParency Today s presenters Jeff Rogers Canada Nick Houseman

Impact of BEPS and Other International Tax Risks on the Jersey Funds Industry

www.pwc.com/jg November 2015 Impact of BEPS and Other International Tax Risks on the Jersey Funds Industry Current International Tax Environment 1 2 The current environment The ability to achieve tax certainty

www.pwc.com/jg November 2015 Impact of BEPS and Other International Tax Risks on the Jersey Funds Industry Current International Tax Environment 1 2 The current environment The ability to achieve tax certainty

Transfer Pricing Perspectives: The new normal: full TransParency. Final BEPS guidance places renewed emphasis on intercompany agreements

Final BEPS guidance places renewed emphasis on intercompany agreements 4 Specifically, the OECD has stated that written contracts alone should not drive the economic outcome. Summary On 5 October 2015,

Final BEPS guidance places renewed emphasis on intercompany agreements 4 Specifically, the OECD has stated that written contracts alone should not drive the economic outcome. Summary On 5 October 2015,

Transfer Pricing Documentation Requirements

Articles China (People's Rep.) Andreas Riedl and Thomas Steinbach* Transfer Pricing Documentation Requirements The authors compare the documentation standard arising from the BEPS Action 13 Final Report

Articles China (People's Rep.) Andreas Riedl and Thomas Steinbach* Transfer Pricing Documentation Requirements The authors compare the documentation standard arising from the BEPS Action 13 Final Report

Analysing BEPS Impact Private Equity sector

Analysing BEPS Impact Private Equity sector January 2016 Second line optional lorem ipsum B Subhead lorem ipsum, date quatueriure In this age of increasing focus on bottomlines, it is indeed tempting for

Analysing BEPS Impact Private Equity sector January 2016 Second line optional lorem ipsum B Subhead lorem ipsum, date quatueriure In this age of increasing focus on bottomlines, it is indeed tempting for

Transfer Pricing: Theory & Practice

Transfer Pricing: Theory & Practice TEI Houston Chapter Your Auditor and Transfer Pricing Randy G. Price, Deloitte Tax LLP Rupesh R. Vadapalli, Deloitte Tax LLP March 1, 2018 Agenda Impact of International

Transfer Pricing: Theory & Practice TEI Houston Chapter Your Auditor and Transfer Pricing Randy G. Price, Deloitte Tax LLP Rupesh R. Vadapalli, Deloitte Tax LLP March 1, 2018 Agenda Impact of International

INSIGHT: Transfer Pricing of Financial Transactions

INSIGHT: Transfer Pricing of Financial Transactions Stuck between a Rock and a Hard Place The EU earnings stripping rules are expected to come into force by January 1, 2019, and multinationals will be

INSIGHT: Transfer Pricing of Financial Transactions Stuck between a Rock and a Hard Place The EU earnings stripping rules are expected to come into force by January 1, 2019, and multinationals will be

PwC Tax Panel 18 October 2016

18 th Annual Tax and Legal Conference Maximise Shareholder Value 2017 www.pwc.com/th Tax Panel Agenda Section one - Challenges in the digital economy Section two - Legal perspective for online transactions

18 th Annual Tax and Legal Conference Maximise Shareholder Value 2017 www.pwc.com/th Tax Panel Agenda Section one - Challenges in the digital economy Section two - Legal perspective for online transactions

Deloitte TaxMax The 43 rd series One bold step in the right direction. Theresa Goh & Subhabrata Dasgupta l 22 November 2017 By Deloitte Tax Academy

Deloitte TaxMax The 43 rd series One bold step in the right direction Theresa Goh & Subhabrata Dasgupta l 22 November 2017 By Deloitte Tax Academy What are we discussing today? 01 02 Emerging trends Key

Deloitte TaxMax The 43 rd series One bold step in the right direction Theresa Goh & Subhabrata Dasgupta l 22 November 2017 By Deloitte Tax Academy What are we discussing today? 01 02 Emerging trends Key

Roundup of Australia s BEPS developments

TaxTalk Insights Global Tax Roundup of Australia s BEPS developments 12 April 2017 In brief Since its presidency of the G20 in 2014, Australia has been at the forefront of efforts to combat tax avoidance

TaxTalk Insights Global Tax Roundup of Australia s BEPS developments 12 April 2017 In brief Since its presidency of the G20 in 2014, Australia has been at the forefront of efforts to combat tax avoidance

Luxembourg transfer pricing legislation at a glance

2017 EY TAX Alert Luxembourg Luxembourg transfer pricing legislation at a glance Executive summary The law of 23 December 2016 on the budget for the year 2017 ( Budget Law ) has introduced a new article

2017 EY TAX Alert Luxembourg Luxembourg transfer pricing legislation at a glance Executive summary The law of 23 December 2016 on the budget for the year 2017 ( Budget Law ) has introduced a new article

1. What are recent tax developments in your country which are relevant for M&A deals?

Austria General Austria 1. What are recent tax developments in your country which are relevant for M&A deals? From 1st of January 2016 onwards, whenever assets (including participations) are transferred

Austria General Austria 1. What are recent tax developments in your country which are relevant for M&A deals? From 1st of January 2016 onwards, whenever assets (including participations) are transferred

The OECD report on base erosion and profit shifting (BEPS) and EU measures against aggressive tax planning and tax fraud

and EU measures against aggressive tax planning and tax fraud") The OECD report on base erosion and profit shifting (BEPS) and EU measures against aggressive tax planning and tax fraud Pere M. Pons New York, May 6 th, 2013 Agenda I. Background II. Key pressure areas

The OECD report on base erosion and profit shifting (BEPS) and EU measures against aggressive tax planning and tax fraud Pere M. Pons New York, May 6 th, 2013 Agenda I. Background II. Key pressure areas

THE INTERSECTION OF TAX & TREASURY

THE INTERSECTION OF TAX & TREASURY 1 INTRODUCTIONS Denise Magyer Senior Vice President, Allied Irish Bank BEATRIZ SALDIVAR MBA & CTP Consultant & Member of the Federal Reserve Faster Payments Task Force

THE INTERSECTION OF TAX & TREASURY 1 INTRODUCTIONS Denise Magyer Senior Vice President, Allied Irish Bank BEATRIZ SALDIVAR MBA & CTP Consultant & Member of the Federal Reserve Faster Payments Task Force

Question 2. Part 1. Transfer pricing and IP

Question 2 Part 1 Transfer pricing and IP Transfer pricing is the price charged in transactions between 2 related entities. It is important in the international tax context because the level of transfer

Question 2 Part 1 Transfer pricing and IP Transfer pricing is the price charged in transactions between 2 related entities. It is important in the international tax context because the level of transfer

Crossing Borders: International Acquisitions and Related Tax Issues, 2nd Edition John Giakoumakis, B.Sc., M.A., C.A., C.P.A.

PREFACE TO THE 2nd EDITION ACKNOWLEDGEMENTS TO THE 2nd EDITION 1 THE ACQUISITION AND THE ROLE OF TAXES 1.1 INTRODUCTION AND PURPOSE 1.2 THE ACQUISITION TRANSACTION STAGES AND TAXES 1.3 THE MULTIDISCIPLINARY

PREFACE TO THE 2nd EDITION ACKNOWLEDGEMENTS TO THE 2nd EDITION 1 THE ACQUISITION AND THE ROLE OF TAXES 1.1 INTRODUCTION AND PURPOSE 1.2 THE ACQUISITION TRANSACTION STAGES AND TAXES 1.3 THE MULTIDISCIPLINARY

Transfer pricing in the post-beps age The challenge to convert mere compliance into good governance

Transfer pricing in the post-beps age The challenge to convert mere compliance into good governance Transfer Pricing Compliance versus Transfer Pricing Governance Are Transfer Pricing Compliance and Transfer

Transfer pricing in the post-beps age The challenge to convert mere compliance into good governance Transfer Pricing Compliance versus Transfer Pricing Governance Are Transfer Pricing Compliance and Transfer

SWEDEN GLOBAL GUIDE TO M&A TAX: 2017 EDITION

SWEDEN 1 SWEDEN INTERNATIONAL DEVELOPMENTS 1. WHAT ARE RECENT TAX DEVELOPMENTS IN YOUR COUNTRY WHICH ARE RELEVANT FOR M&A DEALS AND PRIVATE EQUITY? Effective as of 1 January 2016, dividend income is not

SWEDEN 1 SWEDEN INTERNATIONAL DEVELOPMENTS 1. WHAT ARE RECENT TAX DEVELOPMENTS IN YOUR COUNTRY WHICH ARE RELEVANT FOR M&A DEALS AND PRIVATE EQUITY? Effective as of 1 January 2016, dividend income is not

Passive association. The new transfer pricing landscape A practical guide to the BEPS changes. Global Transfer Pricing November 2015

The new transfer pricing landscape A practical guide to the BEPS changes Passive association Global Transfer Pricing November 2015 Geoff Gill Sydney Kevin Gale Winnipeg Bill Yohana New York It sometimes

The new transfer pricing landscape A practical guide to the BEPS changes Passive association Global Transfer Pricing November 2015 Geoff Gill Sydney Kevin Gale Winnipeg Bill Yohana New York It sometimes

Funds Transfer Pricing A gateway to enhanced business performance

Funds Transfer Pricing A gateway to enhanced business performance Jean-Philippe Peters Partner Governance, Risk & Compliance Deloitte Luxembourg Arnaud Duchesne Senior Manager Governance, Risk & Compliance

Funds Transfer Pricing A gateway to enhanced business performance Jean-Philippe Peters Partner Governance, Risk & Compliance Deloitte Luxembourg Arnaud Duchesne Senior Manager Governance, Risk & Compliance

International Fiscal Association 2017 Rio de Janeiro Congress. cahiers. de droit fiscal international. volume 102. B: The future of transfer pricing

International Fiscal Association 2017 Rio de Janeiro Congress cahiers de droit fiscal international volume 102 B: The future of transfer pricing 1938-2017 Luxembourg Branch Reporters Nicolas Gillet* Antonio

International Fiscal Association 2017 Rio de Janeiro Congress cahiers de droit fiscal international volume 102 B: The future of transfer pricing 1938-2017 Luxembourg Branch Reporters Nicolas Gillet* Antonio

GERMANY GLOBAL GUIDE TO M&A TAX: 2017 EDITION

GERMANY 1 GERMANY INTERNATIONAL DEVELOPMENTS 1. WHAT ARE RECENT TAX DEVELOPMENTS IN YOUR COUNTRY WHICH ARE RELEVANT FOR M&A DEALS AND PRIVATE EQUITY? Germany has recently seen some legislative developments

GERMANY 1 GERMANY INTERNATIONAL DEVELOPMENTS 1. WHAT ARE RECENT TAX DEVELOPMENTS IN YOUR COUNTRY WHICH ARE RELEVANT FOR M&A DEALS AND PRIVATE EQUITY? Germany has recently seen some legislative developments

Financial Analyst Training Programme 10 Days

Financial Analyst Training Programme 10 Days Delegate Profile: This course is targeted at delegates who are new to banking and finance and provides a comprehensive overview of financial reporting, financial

Financial Analyst Training Programme 10 Days Delegate Profile: This course is targeted at delegates who are new to banking and finance and provides a comprehensive overview of financial reporting, financial

TPA Global Treasury Playbook 2016

TPA Global Treasury Playbook 2016 Transfer Pricing Solutions for Financial Transactions 4 th Edition Are You In Control? What are the 2017 trends and topics for intercompany financial transactions? 1.

TPA Global Treasury Playbook 2016 Transfer Pricing Solutions for Financial Transactions 4 th Edition Are You In Control? What are the 2017 trends and topics for intercompany financial transactions? 1.

32nd Annual Asia Pacific Tax Conference November 2016 JW Marriott Hotel Hong Kong

32nd Annual Asia Pacific Tax Conference 10 11 November 2016 JW Marriott Hotel Hong Kong The consequences of real transparency: Reporting,documentation and reconsidering your Asian structures in light of

32nd Annual Asia Pacific Tax Conference 10 11 November 2016 JW Marriott Hotel Hong Kong The consequences of real transparency: Reporting,documentation and reconsidering your Asian structures in light of

IFRS 13 Fair Value Measurement Incorporating credit risk into fair values

IFRS 13 Fair Value Measurement Incorporating credit risk into fair values The Impact on Corporate Treasury By: Blaik Wilson, Senior Solution Consultant, Reval Jacqui Drew, Senior Solution Consultant, Reval

IFRS 13 Fair Value Measurement Incorporating credit risk into fair values The Impact on Corporate Treasury By: Blaik Wilson, Senior Solution Consultant, Reval Jacqui Drew, Senior Solution Consultant, Reval

Tax Obstacles in Cross Border Planning

International Fiscal Association USA Branch New York Region Fall Meeting Thursday, December 1, 2016 Tax Obstacles in Cross Border Planning Colleen O Neill Ernst & Young LLP Maarten P. Maaskant PricewaterhouseCoopers

International Fiscal Association USA Branch New York Region Fall Meeting Thursday, December 1, 2016 Tax Obstacles in Cross Border Planning Colleen O Neill Ernst & Young LLP Maarten P. Maaskant PricewaterhouseCoopers

- Simplification rule for pure intermediary companies : remuneration

Theme Source of law Object / Date of application PAST CHANGES Impact / Comments 1. Transfer Pricing Article 56 of the Luxembourg Income Tax Law (LIR) and paragraph 171 Abgabenordnung Introduction of the

Theme Source of law Object / Date of application PAST CHANGES Impact / Comments 1. Transfer Pricing Article 56 of the Luxembourg Income Tax Law (LIR) and paragraph 171 Abgabenordnung Introduction of the

Transfer Pricing in Italy

Transfer Pricing in Italy Successful together! 1 Agenda 01 Legal Framework and Special Topics 02 03 04 BEPS Our Services Contact 2 Agenda 01 Legal Framework and Special Topics 02 03 04 BEPS Our Services

Transfer Pricing in Italy Successful together! 1 Agenda 01 Legal Framework and Special Topics 02 03 04 BEPS Our Services Contact 2 Agenda 01 Legal Framework and Special Topics 02 03 04 BEPS Our Services

QUESTIONNAIRE ON THE TREATMENT OF INTEREST PAYMENTS AND RELATED TAX BASE EROSION ISSUES

QUESTIONNAIRE ON THE TREATMENT OF INTEREST PAYMENTS AND RELATED TAX BASE EROSION ISSUES This questionnaire should be completed by participants in United Nations capacity development programs on protecting

QUESTIONNAIRE ON THE TREATMENT OF INTEREST PAYMENTS AND RELATED TAX BASE EROSION ISSUES This questionnaire should be completed by participants in United Nations capacity development programs on protecting

New Zealand to implement wide ranging international tax reforms

15 August 2017 Global Tax Alert New Zealand to implement wide ranging international tax reforms EY Global Tax Alert Library Access both online and pdf versions of all EY Global Tax Alerts. Copy into your

15 August 2017 Global Tax Alert New Zealand to implement wide ranging international tax reforms EY Global Tax Alert Library Access both online and pdf versions of all EY Global Tax Alerts. Copy into your

A Transfer Pricing Update BEPS & U.S. Tax Reform

A Transfer Pricing Update BEPS & U.S. Tax Reform JANUARY 17, 2018 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in a group Complete

A Transfer Pricing Update BEPS & U.S. Tax Reform JANUARY 17, 2018 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in a group Complete

Luxembourg tax newsletter

Luxembourg tax newsletter Luxembourg, January 2017 1. Introduction On 23 December 2016 the Luxembourg official gazette has published several laws 1 which introduce substantial changes to the Luxembourg

Luxembourg tax newsletter Luxembourg, January 2017 1. Introduction On 23 December 2016 the Luxembourg official gazette has published several laws 1 which introduce substantial changes to the Luxembourg

The European Commission s Case. Kelly Stricklin-Coutinho Barrister, 39 Essex Chambers Visiting Lecturer, King s College London

The European Commission s Case Kelly Stricklin-Coutinho Barrister, 39 Essex Chambers Visiting Lecturer, King s College London Justified? Tax sovereignty Conflict as to new principle Retroactivity Legal

The European Commission s Case Kelly Stricklin-Coutinho Barrister, 39 Essex Chambers Visiting Lecturer, King s College London Justified? Tax sovereignty Conflict as to new principle Retroactivity Legal

Base Erosion Profit Shifting (BEPS)

") Base Erosion Profit Shifting (BEPS) Base Erosion Profit Shifting (BEPS) The world continues to evolve and nations are becoming increasingly connected. Domestic tax laws have not kept pace with the evolution

Base Erosion Profit Shifting (BEPS) Base Erosion Profit Shifting (BEPS) The world continues to evolve and nations are becoming increasingly connected. Domestic tax laws have not kept pace with the evolution

Annex I to Chapter V. Transfer pricing documentation Master file

ANNEX I TO CHAPTER V. TRANSFER PRICING DOCUMENTATION MASTER FILE 27 Annex I to Chapter V Transfer pricing documentation Master file The following information should be included in the master file: Organisational

ANNEX I TO CHAPTER V. TRANSFER PRICING DOCUMENTATION MASTER FILE 27 Annex I to Chapter V Transfer pricing documentation Master file The following information should be included in the master file: Organisational

Welcome to the EFS-seminar. BEPS and transfer pricing, but what about VAT and Customs? Conference Chairman: René van der Paardt

Welcome to the EFS-seminar BEPS and transfer pricing, but what about VAT and Customs? Conference Chairman: René van der Paardt Rotterdam February 3, 2016 Agenda Seminar An update on the transfer pricing

Welcome to the EFS-seminar BEPS and transfer pricing, but what about VAT and Customs? Conference Chairman: René van der Paardt Rotterdam February 3, 2016 Agenda Seminar An update on the transfer pricing

The new global tax environment. What the global focus on Base Erosion and Profit Shifting (BEPS) means for your business

means for your business") The new global tax environment What the global focus on Base Erosion and Profit Shifting (BEPS) means for your business Changing business environment Macroeconomic megatrends, mobility of capital and growth

The new global tax environment What the global focus on Base Erosion and Profit Shifting (BEPS) means for your business Changing business environment Macroeconomic megatrends, mobility of capital and growth

HONG KONG. 1. Introduction. Contact Information Henry Fung Candice Ng

HONG KONG Contact Information Henry Fung +852 2969 4054 hernyfung@pkf-hk.com Candice Ng +852 2969 4016 candiceng@pkf-hk.com 1. Introduction 1.1. Legal context Currently, the Hong Kong Inland Revenue Ordinance

HONG KONG Contact Information Henry Fung +852 2969 4054 hernyfung@pkf-hk.com Candice Ng +852 2969 4016 candiceng@pkf-hk.com 1. Introduction 1.1. Legal context Currently, the Hong Kong Inland Revenue Ordinance

C(C)CTB 28 February CORIT

CTB 28 February CORIT") C(C)CTB 28 February 2017 Agenda Introduction Determination of the tax base Anti tax avoidance legislation Consolidation and allocation One-stop-shop Political and practical perspectives Introduction Challenges

C(C)CTB 28 February 2017 Agenda Introduction Determination of the tax base Anti tax avoidance legislation Consolidation and allocation One-stop-shop Political and practical perspectives Introduction Challenges

SESSION 11B: COVETING THY NEIGHBOUR S TAX BASE AUSTRALIA S CHANGING APPROACH TO INTERNATIONAL TAXATION

SESSION 11B: COVETING THY NEIGHBOUR S TAX BASE AUSTRALIA S CHANGING APPROACH TO INTERNATIONAL TAXATION Peter Collins and Michael Bona Global Tax PwC Australia Contents International tax environment Financing

SESSION 11B: COVETING THY NEIGHBOUR S TAX BASE AUSTRALIA S CHANGING APPROACH TO INTERNATIONAL TAXATION Peter Collins and Michael Bona Global Tax PwC Australia Contents International tax environment Financing

Comments on the Revised Discussion Draft on Transfer Pricing Aspects of Intangibles

Working Party 6 OECD, Committee of fiscal affairs 2, rue André Pascal 75775 Paris Cedex 16 France Date: 30 September 2013 Subject: Comments on the Revised Discussion Draft on Transfer Pricing Aspects of

Working Party 6 OECD, Committee of fiscal affairs 2, rue André Pascal 75775 Paris Cedex 16 France Date: 30 September 2013 Subject: Comments on the Revised Discussion Draft on Transfer Pricing Aspects of

Diverted Profits Tax. Key points

Diverted Profits Tax Given the publicity surrounding the practices of multinationals in particular a number of the large US technology corporations - in structuring their affairs to minimise their tax

Diverted Profits Tax Given the publicity surrounding the practices of multinationals in particular a number of the large US technology corporations - in structuring their affairs to minimise their tax

Tax watch: Edition 2. March Transfer Pricing, Permanent Establishment and Interest Limitation Changes Announced

The views reflected in this document are the views of the authors and do not necessarily reflect the views of the global EY organisation or its member firms. Tax watch: Edition 2 March 2017 Transfer Pricing,

The views reflected in this document are the views of the authors and do not necessarily reflect the views of the global EY organisation or its member firms. Tax watch: Edition 2 March 2017 Transfer Pricing,

Statement for the Record

Statement for the Record of Dorothy Coleman Vice President, Tax & Domestic Economic Policy National Association of Manufacturers For the Hearing of the Senate Finance Committee on International Tax: OECD

Statement for the Record of Dorothy Coleman Vice President, Tax & Domestic Economic Policy National Association of Manufacturers For the Hearing of the Senate Finance Committee on International Tax: OECD

Gijs Fibbe (Baker Tilly / Erasmus University) Bart Le Blanc (Norton Rose Fulbright) Andrew Roycroft (Norton Rose Fulbright) September 25, 2017

Bart Le Blanc (Norton Rose Fulbright) Andrew Roycroft (Norton Rose Fulbright) September 25, 2017") Implementation of the ATAD in the UK and NL Gijs Fibbe (Baker Tilly / Erasmus University) Bart Le Blanc (Norton Rose Fulbright) Andrew Roycroft (Norton Rose Fulbright) September 25, 2017 UK/NL (as many

Implementation of the ATAD in the UK and NL Gijs Fibbe (Baker Tilly / Erasmus University) Bart Le Blanc (Norton Rose Fulbright) Andrew Roycroft (Norton Rose Fulbright) September 25, 2017 UK/NL (as many

Services and Capabilities. Financial Services Transfer Pricing

Services and Capabilities Financial Services Transfer Pricing Our team of experts offers an unmatched combination of economic credentials, industry expertise, and testifying experience. FINANCIAL SERVICES

Services and Capabilities Financial Services Transfer Pricing Our team of experts offers an unmatched combination of economic credentials, industry expertise, and testifying experience. FINANCIAL SERVICES

Copenhagen Economics welcomes the opportunity to comment on the OECD s Discussion Draft on BEPS 8-10, Financial transactions, issued on 3 July 2018.

Copenhagen Economics Kungsgatan 38, 5tr 111 35 Stockholm Sweden Tax Treaties, Transfer Pricing and Financial Transactions Division OECD - Centre for Tax Policy and Administration 2, Rue André Pascal 75775

Copenhagen Economics Kungsgatan 38, 5tr 111 35 Stockholm Sweden Tax Treaties, Transfer Pricing and Financial Transactions Division OECD - Centre for Tax Policy and Administration 2, Rue André Pascal 75775

Though funds are generally exempt from profits tax in Hong

Tax Law: Latest Developments in the Taxation of Hong Kong Asset Managers As Hong Kong proposes new rules to combat base erosion and profit shifting ( BEPS ), asset management groups operating in Hong Kong

Tax Law: Latest Developments in the Taxation of Hong Kong Asset Managers As Hong Kong proposes new rules to combat base erosion and profit shifting ( BEPS ), asset management groups operating in Hong Kong

WHY TRANSFER PRICING? OR How Did We Get Here From There?

WHY TRANSFER PRICING? OR How Did We Get Here From There? Barbara J. Mantegani Mantegani Tax PLLC Julie Joy Bloomberg BNA Here - Where Are We Now? Transfer pricing one of the most significant (if not the

WHY TRANSFER PRICING? OR How Did We Get Here From There? Barbara J. Mantegani Mantegani Tax PLLC Julie Joy Bloomberg BNA Here - Where Are We Now? Transfer pricing one of the most significant (if not the

Base erosion & profit shifting (BEPS) 25 May 2016

25 May 2016") Base erosion & profit shifting (BEPS) 25 May 2016 Introduction Important to distinguish between: Tax avoidance Using legal provisions to minimise tax liability Covers interventions that are referred to

Base erosion & profit shifting (BEPS) 25 May 2016 Introduction Important to distinguish between: Tax avoidance Using legal provisions to minimise tax liability Covers interventions that are referred to

Luxembourg strengthens its Transfer Pricing Rules

Newsflash - Tax December 2016 Luxembourg strengthens its Transfer Pricing Rules Luxembourg reinforces its domestic Transfer Pricing rules as of 1 January 2017 by the enactment of: (I) (II) General guidelines

Newsflash - Tax December 2016 Luxembourg strengthens its Transfer Pricing Rules Luxembourg reinforces its domestic Transfer Pricing rules as of 1 January 2017 by the enactment of: (I) (II) General guidelines

THE PARLIAMENT OF THE COMMONWEALTH OF AUSTRALIA SENATE TREASURY LAWS AMENDMENT (COMBATING MULTINATIONAL TAX AVOIDANCE) BILL 2017

BILL 2017") 2016-2017 THE PARLIAMENT OF THE COMMONWEALTH OF AUSTRALIA SENATE TREASURY LAWS AMENDMENT (COMBATING MULTINATIONAL TAX AVOIDANCE) BILL 2017 DIVERTED PROFITS TAX BILL 2017 REVISED EXPLANATORY MEMORANDUM

2016-2017 THE PARLIAMENT OF THE COMMONWEALTH OF AUSTRALIA SENATE TREASURY LAWS AMENDMENT (COMBATING MULTINATIONAL TAX AVOIDANCE) BILL 2017 DIVERTED PROFITS TAX BILL 2017 REVISED EXPLANATORY MEMORANDUM

BUSINESS MODELS IN THE CURRENT BEPS ENVIRONMENT DO YOU NEED TO CHANGE? Lyndon James, Partner Pete Rhodes, Senior Manager PwC

BUSINESS MODELS IN THE CURRENT BEPS ENVIRONMENT DO YOU NEED TO CHANGE? Lyndon James, Partner Pete Rhodes, Senior Manager PwC Agenda The current environment and the case for change Australian measures most

BUSINESS MODELS IN THE CURRENT BEPS ENVIRONMENT DO YOU NEED TO CHANGE? Lyndon James, Partner Pete Rhodes, Senior Manager PwC Agenda The current environment and the case for change Australian measures most

LIVE WEBCAST UPDATE ON BEPS PROJECT. 26 May :00pm 2:00pm (CEST)

") LIVE WEBCAST UPDATE ON BEPS PROJECT 26 May 2014 1:00pm 2:00pm (CEST) Speakers Pascal Saint-Amans Director, Centre for Tax Policy and Administration Raffaele Russo Head of BEPS Project Marlies de Ruiter

LIVE WEBCAST UPDATE ON BEPS PROJECT 26 May 2014 1:00pm 2:00pm (CEST) Speakers Pascal Saint-Amans Director, Centre for Tax Policy and Administration Raffaele Russo Head of BEPS Project Marlies de Ruiter

Impacts of U.S. International Tax Reform. October 23, 2018

Impacts of U.S. International Tax Reform October 23, 2018 Christopher Jentile (Verizon), Moderator William Crowley (PwC) Anthony Sileo (KPMG) Stephen Blough (KPMG) 2 Christopher Jentile Christopher is

Impacts of U.S. International Tax Reform October 23, 2018 Christopher Jentile (Verizon), Moderator William Crowley (PwC) Anthony Sileo (KPMG) Stephen Blough (KPMG) 2 Christopher Jentile Christopher is

Re: BEPS Action 4: Interest Deductions and Other Financial Payments

OECD Committee on Fiscal Affairs Working Party No. 11 By email: interestdeductions@oecd.org 6 February 2015 Dear Sirs, Re: BEPS Action 4: Interest Deductions and Other Financial Payments We are writing

OECD Committee on Fiscal Affairs Working Party No. 11 By email: interestdeductions@oecd.org 6 February 2015 Dear Sirs, Re: BEPS Action 4: Interest Deductions and Other Financial Payments We are writing

LUXEMBOURG GLOBAL GUIDE TO M&A TAX: 2018 EDITION

LUXEMBOURG 1 LUXEMBOURG INTERNATIONAL DEVELOPMENTS 1. WHAT ARE RECENT TAX DEVELOPMENTS IN YOUR COUNTRY WHICH ARE RELEVANT FOR M&A DEALS AND PRIVATE EQUITY? Corporate income tax ( CIT ) rate The CIT rate

LUXEMBOURG 1 LUXEMBOURG INTERNATIONAL DEVELOPMENTS 1. WHAT ARE RECENT TAX DEVELOPMENTS IN YOUR COUNTRY WHICH ARE RELEVANT FOR M&A DEALS AND PRIVATE EQUITY? Corporate income tax ( CIT ) rate The CIT rate

BUSINESS IN THE UK A ROUTE MAP

1 BUSINESS IN THE UK A ROUTE MAP 18 chapter 02 Anyone wishing to set up business operations in the UK for the first time has a number of options for structuring those operations. There are a number of

1 BUSINESS IN THE UK A ROUTE MAP 18 chapter 02 Anyone wishing to set up business operations in the UK for the first time has a number of options for structuring those operations. There are a number of

IFA Colombia V CONGRESO COLOMBIANO DE TRIBUTACIÓN INTERNACIONAL November 2016

IFA Colombia V CONGRESO COLOMBIANO DE TRIBUTACIÓN INTERNACIONAL 16-17 November 2016 Kees van Raad Professor of Law, University of Leiden Chairman International Tax Center Leiden Of counsel, Loyens & Loeff

IFA Colombia V CONGRESO COLOMBIANO DE TRIBUTACIÓN INTERNACIONAL 16-17 November 2016 Kees van Raad Professor of Law, University of Leiden Chairman International Tax Center Leiden Of counsel, Loyens & Loeff

1. New decree on transfer-pricing documentation requirements

THE NETHERLANDS 1. New decree on transfer-pricing documentation requirements 1.1. Introduction As from 1 January 2016, Netherlands-resident entities (and Netherlands permanent establishments) that are

THE NETHERLANDS 1. New decree on transfer-pricing documentation requirements 1.1. Introduction As from 1 January 2016, Netherlands-resident entities (and Netherlands permanent establishments) that are