Study on Structures of Aggressive Tax Planning and Indicators

|

|

|

- Miles Davidson

- 5 years ago

- Views:

Transcription

1 Study on Structures of Aggressive Tax Planning and Indicators Platform for Tax Good Governance 15 March 2016 Gaëtan Nicodème

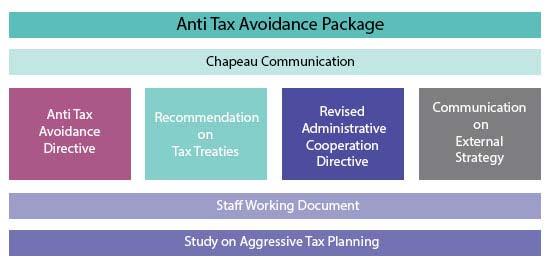

2 Context Fair and efficient corporate tax system: priority of the Commission Action Plan for Fair and Effective Taxation (June 2015) Automatic Exchange of Information on Tax rulings (December 2015) Anti-Tax Avoidance Package (January 2016)

3 Context Extensive work done by the G20/OECD on the Base Erosion and Profit Shifting project Need for a strong analytical basis focused on EU Study launched beginning of 2015 and published in January 2016

4 Context

5 Objectives of the study Definition of the Identification of model ATP structures Identification of critical factors that facilitate or allow ATP (indicators) Review of MS' tax rules & practices which can expose MS to ATP

6 Scope Aggressive Tax Planning: "taking advantage of the technicalities of a tax system or of mismatches between two or more tax systems for the purpose of reducing tax liability," National rules and practices, not tax treaties General corporate income tax systems of 28 MS, complemented by a review of possible role of overseas countries and territories Wide coverage in terms of number of MS and indicators more limited level of details per MS

7 How was the study conducted? Identification of Structures of Aggressive Tax Planning (ATP) Deriving ATP Indicators from structures + add others Data collection by network of tax experts Discussion of preliminary results with MS & Finalisation Assessment per MS & general conclusions Review by MS representatives 7

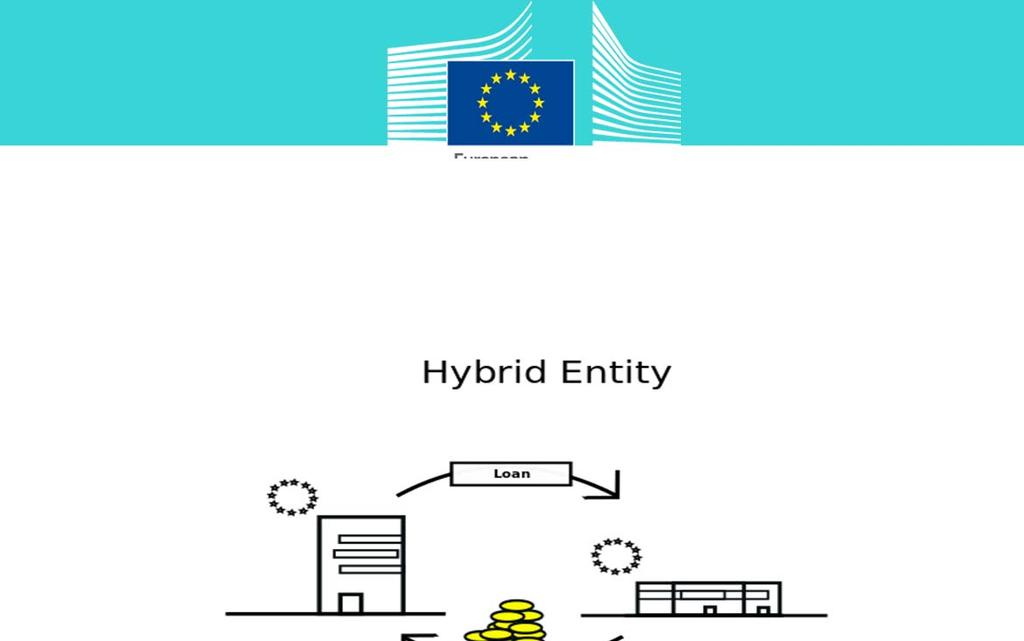

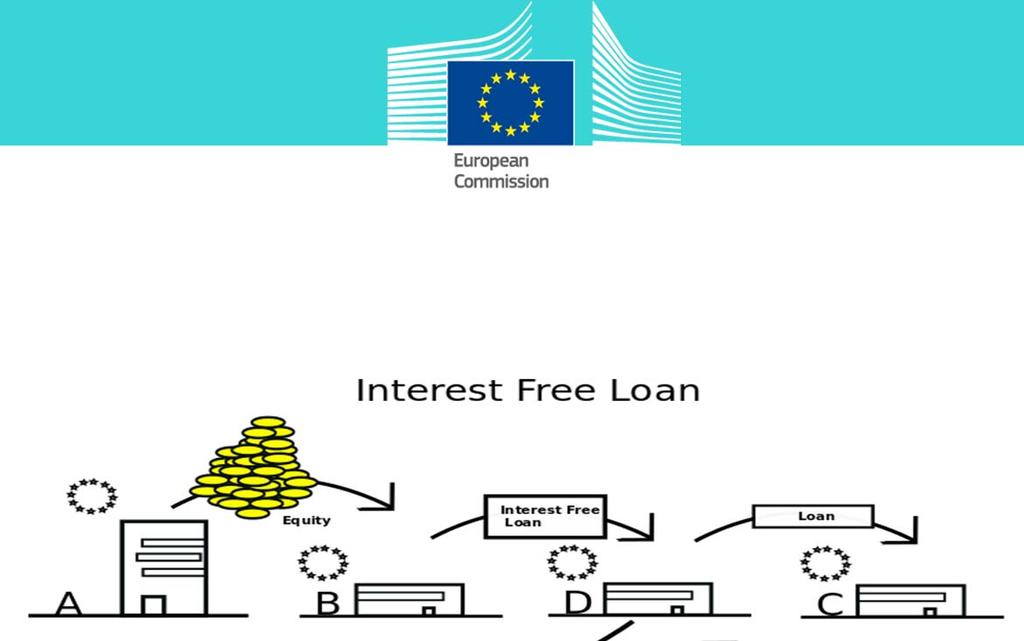

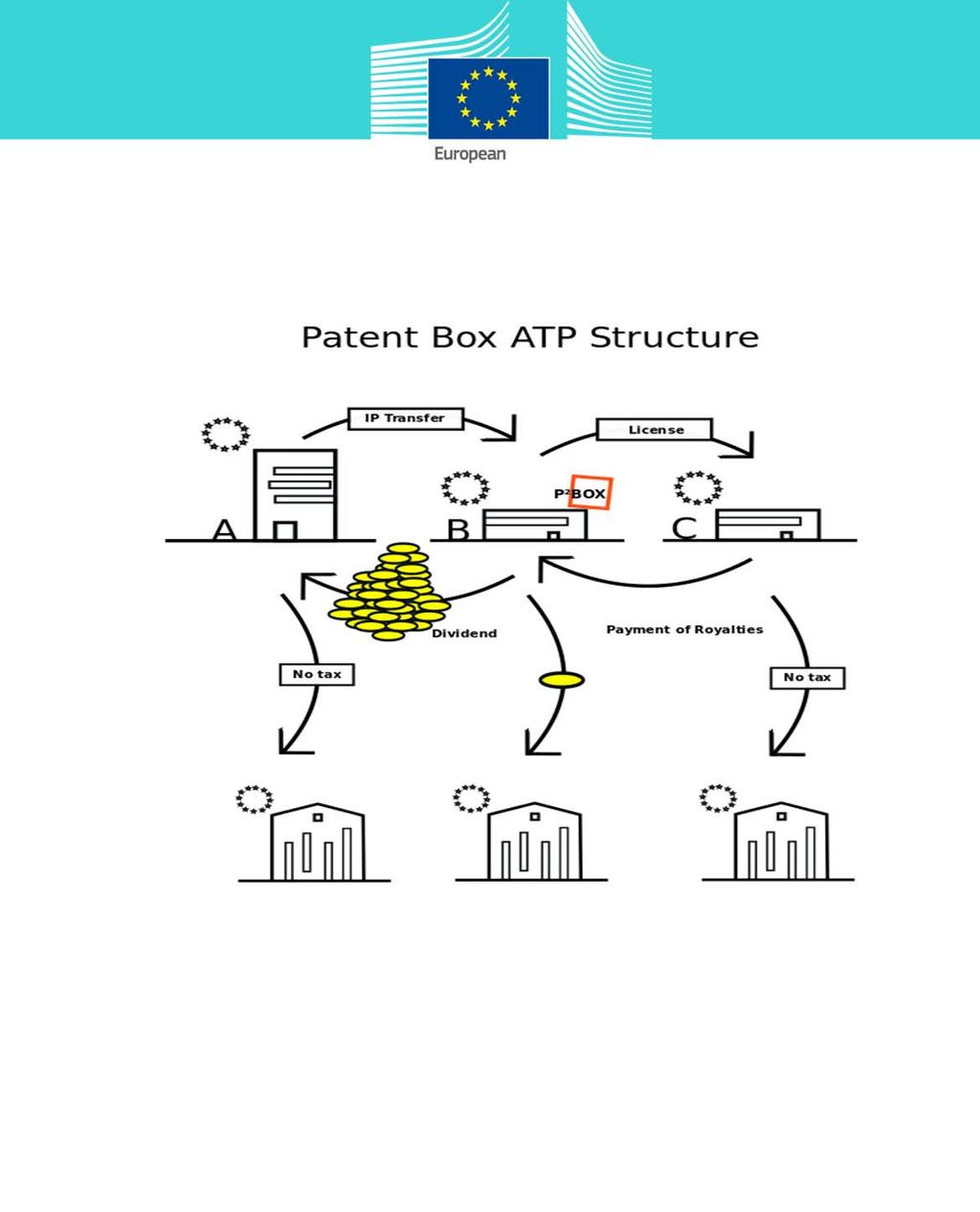

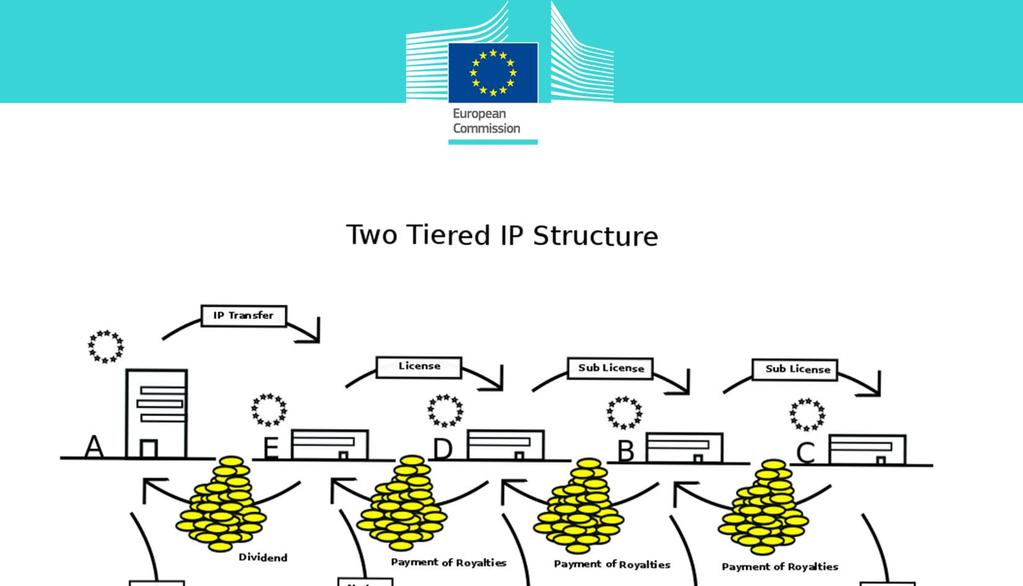

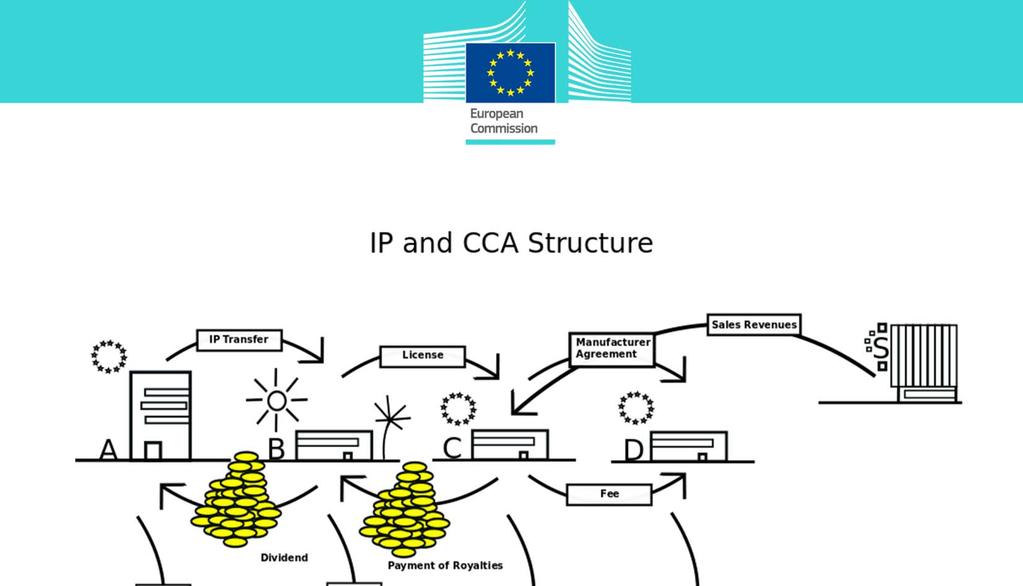

8 ATP structures Identification of 7 relevant ATP structures Offshore loan ATP structure Hybrid loan ATP structure Hybrid entity ATP structure Interest-free loan ATP structure Patent box ATP structure Two-tiered IP ATP structure IP and cost contribution agreement ATP structure

9 Example: Offshore Loan Structure

10 Indicators derived from Offshore Loan ATP Structure State A State B State C State D Relevant indicators Relevant indicators Relevant indicators Relevant indicators Too generous tax-exemption of dividends received. No CFC Rules. Tax deduction for interest costs. Tax deduction does not depend on the tax treatment in the creditor's state. No interest-limitation rules and no thin-capitalization No withholding tax on interest payments. No beneficial-owner test for reduction of withholding tax. Unilateral ruling on interest spread. No general or specific antiavoidance rules to counter the model ATP structures. Tax deduction for interest costs. Tax deduction does not depend on the tax treatment in the creditor's state. No interest-limitation rules and no thin-capitalization No withholding tax on interest payments. No beneficial-owner test for reduction of withholding tax. Group taxation with acquisition holding company No general or specific antiavoidance rules to counter the model ATP structures. No withholding tax on dividends paid Nil corporate tax rate

11 Indicators Derived from the model ATP Structures Capture the risk that the model ATP structures are set up. Correspond to specific piece of legislation or case law, or absence of those

12 Categories of indicators 33 indicators Active indicators can directly promote or prompt an ATP-structure e.g. patent box, notional interest deduction, Passive indicators does not by itself promote or prompt any ATP structure but is needed in order to allow the setting up of an ATP structure. e.g. lack of withholding tax, interest deductibility within a group,

13 Categories of indicators Lack of anti-abuse provisions Lack of rules that aimed at countering ATP e.g. lack of CFC rules, absence of thin-cap rules, Combination of passive indicators and lack of anti-abuse provisions Routing of dividends through a MS Base erosion by means of financing costs Base erosion by means of IP costs

14 Overview of some indicators Theme No. Subject Category Interest income Interest costs 6 Income from certain hybrid instruments non- taxable Lack of anti-abuse 7 No deemed income from interest-free loan (non-arm's-length transactions) Active 8 Tax deduction for intra- group interest costs Passive 9 10 Tax deduction does not depend on the tax treatment in the creditor's state Tax deduction allowed for deemed interest costs on interestfree debt Lack of anti-abuse Active 11 No taxation of benefit from interest-free debt Lack of anti-abuse 12 No thin-capitalization rules Lack of anti-abuse 13 No interest- limitation rules Lack of anti-abuse No withholding tax on interest payments (absent under domestic law) No beneficial-owner test for reduction of withholding tax on interest Passive Lack of anti-abuse CFC rules 24 No CFC rules Lack of anti-abuse

15 MS assessment Information collection structured around the 33 indicators Information provided by network of national tax experts Filled in questionnaire submitted to MS for comments

16 Conclusions from the study Large differences across MS Some indicators are particularly relevant Lack of CFC rules Base erosion by means of financing costs intra-group Lack of rules to counter mismatches in entities qualification Dividend flow-through Patent boxes Role of third countries jurisdictions

17 Relevance for the ATAP CFC rules GAAR Interest Limitation rules Hybrid mismatches Switchover rules Exit and Capital gains tax rules Role of third-country jurisdictions

18 Offshore Loan Structure

19

20

21

22

23

24

Skatteverket International Tax Planning 2016 CORIT

Skatteverket International Tax Planning Agenda Introduction General remarks on International Tax Planning Analysis of International Tax Planning Models and Indicators International IP Tax Planning and

Skatteverket International Tax Planning Agenda Introduction General remarks on International Tax Planning Analysis of International Tax Planning Models and Indicators International IP Tax Planning and

Cyprus Tax Update. Kyiv May 2018

Cyprus Tax Update Kyiv May 2018 Today s agenda 1. Snapshot of Cyprus tax system 2. Developments affecting the Cyprus tax regime 3. Selected developments : a) ATAD b) TP 4. Selected structures 5. Expected

Cyprus Tax Update Kyiv May 2018 Today s agenda 1. Snapshot of Cyprus tax system 2. Developments affecting the Cyprus tax regime 3. Selected developments : a) ATAD b) TP 4. Selected structures 5. Expected

EU Anti-Tax Avoidance Package: impacts on the real estate industry

EUDTG/RE March 2016 EU Anti-Tax Avoidance Package: impacts on the real estate industry On 28 January 2016, the EU Commission (EC) presented its EU Anti-Tax Avoidance Package (ATAP). The below provides

EUDTG/RE March 2016 EU Anti-Tax Avoidance Package: impacts on the real estate industry On 28 January 2016, the EU Commission (EC) presented its EU Anti-Tax Avoidance Package (ATAP). The below provides

IBFD Course Programme Current Issues in International Tax Planning

IBFD Course Programme Current Issues in International Tax Planning Amsterdam, 14 16 June 2017 Summary This intermediate-level course provides participants with an in-depth understanding of the current

IBFD Course Programme Current Issues in International Tax Planning Amsterdam, 14 16 June 2017 Summary This intermediate-level course provides participants with an in-depth understanding of the current

IBFD Course Programme Principles of International Taxation

IBFD Course Programme Principles of International Taxation Need a good base to start your career in international tax? This course will provide the essential knowledge you need and give you the confidence

IBFD Course Programme Principles of International Taxation Need a good base to start your career in international tax? This course will provide the essential knowledge you need and give you the confidence

IBFD Course Programme Current Issues in International Tax Planning

IBFD Course Programme Current Issues in International Tax Planning Summary This intermediate-level course provides participants with an in-depth understanding of the current discussions relating to international

IBFD Course Programme Current Issues in International Tax Planning Summary This intermediate-level course provides participants with an in-depth understanding of the current discussions relating to international

Principles of International Taxation

Overview and Learning Objectives This tax course is designed to provide participants with the essentials of international taxation. The first three days are dedicated to the fundamental concepts relevant

Overview and Learning Objectives This tax course is designed to provide participants with the essentials of international taxation. The first three days are dedicated to the fundamental concepts relevant

BASE EROSION AND PROFIT SHIFTING

BASE EROSION AND PROFIT SHIFTING BEPS issues for developing countries Liselott Kana Head of International Revenue Administration, Chile UN Subcommittee mandate Draw on the experiences of subcommittee members

BASE EROSION AND PROFIT SHIFTING BEPS issues for developing countries Liselott Kana Head of International Revenue Administration, Chile UN Subcommittee mandate Draw on the experiences of subcommittee members

EUROPEAN COMMISSION PRESENTS ANTI-TAX AVOIDANCE PACKAGE

EUROPEAN COMMISSION PRESENTS ANTI-TAX AVOIDANCE PACKAGE tax.thomsonreuters.com On January 28, 2016, the European Commission presented its Communication on the Anti-Tax Avoidance Package (ATA Package).

EUROPEAN COMMISSION PRESENTS ANTI-TAX AVOIDANCE PACKAGE tax.thomsonreuters.com On January 28, 2016, the European Commission presented its Communication on the Anti-Tax Avoidance Package (ATA Package).

IBFD Course Programme BEPS Country Implementation

IBFD Course Programme BEPS Country Implementation Summary On 5 October 2015, the OECD published the final reports of its 15-point base erosion and profit shifting (BEPS) project. A bit more than a year

IBFD Course Programme BEPS Country Implementation Summary On 5 October 2015, the OECD published the final reports of its 15-point base erosion and profit shifting (BEPS) project. A bit more than a year

The Anti Tax Avoidance Package Questions and Answers

European Commission - Fact Sheet The Anti Tax Avoidance Package Questions and Answers Brussels, 28 January 2016 1. Why has the Commission made the fight against corporate tax avoidance a priority? Corporate

European Commission - Fact Sheet The Anti Tax Avoidance Package Questions and Answers Brussels, 28 January 2016 1. Why has the Commission made the fight against corporate tax avoidance a priority? Corporate

Parent Subsidiary Directive and Interest and Royalty Directive

Università Carlo Cattaneo LIUC International Tax Law a.a.2017/2018 Parent Subsidiary Directive and Interest and Royalty Directive Prof. Marco Cerrato Parent-Subsidiary Directive 2 The Directive in general

Università Carlo Cattaneo LIUC International Tax Law a.a.2017/2018 Parent Subsidiary Directive and Interest and Royalty Directive Prof. Marco Cerrato Parent-Subsidiary Directive 2 The Directive in general

Dutch Tax Bill 2018: what will change?

1 Dutch Tax Bill 2018: what will change? The Dutch government has presented its Tax Bill 2018. Three amendments are particularly relevant for multinationals, international investors and investment funds

1 Dutch Tax Bill 2018: what will change? The Dutch government has presented its Tax Bill 2018. Three amendments are particularly relevant for multinationals, international investors and investment funds

The OECD s 3 Major Tax Initiatives

The OECD s 3 Major Tax Initiatives 1. The Global Forum on Transparency and Exchange of Information for Tax Purposes Peer review of ~ 100 countries International standard for transparency and exchange of

The OECD s 3 Major Tax Initiatives 1. The Global Forum on Transparency and Exchange of Information for Tax Purposes Peer review of ~ 100 countries International standard for transparency and exchange of

Diverted Profits Tax. Key points

Diverted Profits Tax Given the publicity surrounding the practices of multinationals in particular a number of the large US technology corporations - in structuring their affairs to minimise their tax

Diverted Profits Tax Given the publicity surrounding the practices of multinationals in particular a number of the large US technology corporations - in structuring their affairs to minimise their tax

ANTI-AVOIDANCE LEGISLATION AND TAX PLANNING. Dr. Balázs Békés Andrea Manzitti 24 November 2017

ANTI-AVOIDANCE LEGISLATION AND TAX PLANNING Dr. Balázs Békés Andrea Manzitti 24 November 2017 NEED FOR TAX PLANNING Tax planning would be easy if we would have mathematical approach Find low effective

ANTI-AVOIDANCE LEGISLATION AND TAX PLANNING Dr. Balázs Békés Andrea Manzitti 24 November 2017 NEED FOR TAX PLANNING Tax planning would be easy if we would have mathematical approach Find low effective

Impact of BEPS and Other International Tax Risks on the Jersey Funds Industry

www.pwc.com/jg November 2015 Impact of BEPS and Other International Tax Risks on the Jersey Funds Industry Current International Tax Environment 1 2 The current environment The ability to achieve tax certainty

www.pwc.com/jg November 2015 Impact of BEPS and Other International Tax Risks on the Jersey Funds Industry Current International Tax Environment 1 2 The current environment The ability to achieve tax certainty

QUESTIONNAIRE ON THE TREATMENT OF INTEREST PAYMENTS AND RELATED TAX BASE EROSION ISSUES

QUESTIONNAIRE ON THE TREATMENT OF INTEREST PAYMENTS AND RELATED TAX BASE EROSION ISSUES This questionnaire should be completed by participants in United Nations capacity development programs on protecting

QUESTIONNAIRE ON THE TREATMENT OF INTEREST PAYMENTS AND RELATED TAX BASE EROSION ISSUES This questionnaire should be completed by participants in United Nations capacity development programs on protecting

BEPS: What does it mean for funds and asset managers?

BEPS: What does it mean for funds and asset managers? Client Seminar Martin Shah René van Eldonk Malcolm Richardson, M&G 10 March 2015 Overview Background to and progress to date of BEPS Action Plan More

BEPS: What does it mean for funds and asset managers? Client Seminar Martin Shah René van Eldonk Malcolm Richardson, M&G 10 March 2015 Overview Background to and progress to date of BEPS Action Plan More

International Tax Course International Tax Planning 2017 CORIT

International Tax Course International Tax Planning Agenda Introduction. General remarks on International Tax Planning. Analysis of International Tax Planning Models and Indicators within corporate finance.

International Tax Course International Tax Planning Agenda Introduction. General remarks on International Tax Planning. Analysis of International Tax Planning Models and Indicators within corporate finance.

Tax Obstacles in Cross Border Planning

International Fiscal Association USA Branch New York Region Fall Meeting Thursday, December 1, 2016 Tax Obstacles in Cross Border Planning Colleen O Neill Ernst & Young LLP Maarten P. Maaskant PricewaterhouseCoopers

International Fiscal Association USA Branch New York Region Fall Meeting Thursday, December 1, 2016 Tax Obstacles in Cross Border Planning Colleen O Neill Ernst & Young LLP Maarten P. Maaskant PricewaterhouseCoopers

The OECD report on base erosion and profit shifting (BEPS) and EU measures against aggressive tax planning and tax fraud

and EU measures against aggressive tax planning and tax fraud") The OECD report on base erosion and profit shifting (BEPS) and EU measures against aggressive tax planning and tax fraud Pere M. Pons New York, May 6 th, 2013 Agenda I. Background II. Key pressure areas

The OECD report on base erosion and profit shifting (BEPS) and EU measures against aggressive tax planning and tax fraud Pere M. Pons New York, May 6 th, 2013 Agenda I. Background II. Key pressure areas

Recent developments in international tax

Recent developments in international tax Disclaimer EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate

Recent developments in international tax Disclaimer EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate

EFFECTS ON TRADING AND AND SOLUTIONS

TRANSFER PRICING EFFECTS ON TRADING AND FINANCING CYPRUS COMPANIES AND SOLUTIONS By Marios Efthymiou Managing Director DEFINITIONS Base erosion and profit shifting (BEPS) refers to tax avoidance strategies

TRANSFER PRICING EFFECTS ON TRADING AND FINANCING CYPRUS COMPANIES AND SOLUTIONS By Marios Efthymiou Managing Director DEFINITIONS Base erosion and profit shifting (BEPS) refers to tax avoidance strategies

Intercompany financing facing new challenges. EY Africa Tax Conference September 2014

Intercompany financing facing new challenges EY Africa Tax Conference September 2014 Panel Moderator Ide Louw International Tax EY South Africa Panel Joseph Pagop Noupoue EY Jemimah Mugo EY Kenya Michael

Intercompany financing facing new challenges EY Africa Tax Conference September 2014 Panel Moderator Ide Louw International Tax EY South Africa Panel Joseph Pagop Noupoue EY Jemimah Mugo EY Kenya Michael

Basic International Taxation

Basic International Taxation Roy Rohatgi KLUWER LAW INTERNATIONAL LONDON / THE HAGUE / NEW YORK TABLE OF CONTENTS Preface About the Author xiii xv CHAPTER 1 AN OVERVIEW OF INTERNATIONAL TAXATION 1 1. Objectives

Basic International Taxation Roy Rohatgi KLUWER LAW INTERNATIONAL LONDON / THE HAGUE / NEW YORK TABLE OF CONTENTS Preface About the Author xiii xv CHAPTER 1 AN OVERVIEW OF INTERNATIONAL TAXATION 1 1. Objectives

The Anti Tax Avoidance Package Questions and Answers (Updated)

") European Commission - Fact Sheet The Anti Tax Avoidance Package Questions and Answers (Updated) Brussels, 21 June 2016 1. Why has the Commission made the fight against corporate tax avoidance a priority?

European Commission - Fact Sheet The Anti Tax Avoidance Package Questions and Answers (Updated) Brussels, 21 June 2016 1. Why has the Commission made the fight against corporate tax avoidance a priority?

International Taxation Recent Developments in India

International Taxation Recent Developments in India April 2017 B. D. Jokhakar & Co., www.bdjokhakar.com Table of Contents Sr. No. Topic Page No. 1. Introduction 3 2. Amendment to Tax Treaties 4 3. Base

International Taxation Recent Developments in India April 2017 B. D. Jokhakar & Co., www.bdjokhakar.com Table of Contents Sr. No. Topic Page No. 1. Introduction 3 2. Amendment to Tax Treaties 4 3. Base

INTERNATIONAL TAX STRUCTURING FOR INVESTING ADROAD INTERNATIONAL TAX CONFERENCE

INTERNATIONAL TAX STRUCTURING FOR INVESTING ADROAD December 5, 2009 INTERNATIONAL TAX CONFERENCE - 2009 Shefali Goradia Partner, BMR Advisors OVERSEAS INVESTMENT KEY DRIVERS Access to Global Markets Inorganic

INTERNATIONAL TAX STRUCTURING FOR INVESTING ADROAD December 5, 2009 INTERNATIONAL TAX CONFERENCE - 2009 Shefali Goradia Partner, BMR Advisors OVERSEAS INVESTMENT KEY DRIVERS Access to Global Markets Inorganic

BEPS and ATAD: Where do we stand?

BEPS and ATAD: Where do we stand? by Nicky Gouder Tax Partner Summary Quick Overview of the BEPS Project and ATAD; A Comparison of the BEPS Recommendations and the ATAD obstacles, conflicts. Is harmonious

BEPS and ATAD: Where do we stand? by Nicky Gouder Tax Partner Summary Quick Overview of the BEPS Project and ATAD; A Comparison of the BEPS Recommendations and the ATAD obstacles, conflicts. Is harmonious

Diverted Profits Tax Guidance. Guidance 10 December 2014

Diverted Profits Tax Guidance Guidance 10 December 2014 1 Contents Page Introduction Chapter 1 Chapter 2 Chapter 3 Introduction & Overview Application of Diverted Profits Tax Diverted Profits Tax - processes.

Diverted Profits Tax Guidance Guidance 10 December 2014 1 Contents Page Introduction Chapter 1 Chapter 2 Chapter 3 Introduction & Overview Application of Diverted Profits Tax Diverted Profits Tax - processes.

Trends I Netherlands moves away from fiscal offshore industry

1 Trends I Netherlands moves away from fiscal offshore industry The Netherlands is slowly but surely steering away from facilitating the use of its corporate income tax system by companies that are set

1 Trends I Netherlands moves away from fiscal offshore industry The Netherlands is slowly but surely steering away from facilitating the use of its corporate income tax system by companies that are set

THE FUTURE OF TAX PLANNING: TRANSPARENCY AND SUBSTANCE FOR ALL? Friday, 26 February AM PM Conrad Hotel, Hong Kong

THE FUTURE OF TAX PLANNING: TRANSPARENCY AND SUBSTANCE FOR ALL? Friday, 26 February 2016 9.00AM - 12.00PM Conrad Hotel, Hong Kong THE DRIVE TOWARDS TRANSPARENCY: CHALLENGES AND OPPORTUNITIES IN INTERNATIONAL

THE FUTURE OF TAX PLANNING: TRANSPARENCY AND SUBSTANCE FOR ALL? Friday, 26 February 2016 9.00AM - 12.00PM Conrad Hotel, Hong Kong THE DRIVE TOWARDS TRANSPARENCY: CHALLENGES AND OPPORTUNITIES IN INTERNATIONAL

AmCham EU s position on the Commission Anti-Tax Avoidance Package

AmCham EU s position on the Commission Anti-Tax Avoidance Package Executive summary AmCham EU welcomes attempts to ensure that adoption of the OECD s recommendations is consistent across the EU and with

AmCham EU s position on the Commission Anti-Tax Avoidance Package Executive summary AmCham EU welcomes attempts to ensure that adoption of the OECD s recommendations is consistent across the EU and with

Base erosion & profit shifting (BEPS) 25 May 2016

25 May 2016") Base erosion & profit shifting (BEPS) 25 May 2016 Introduction Important to distinguish between: Tax avoidance Using legal provisions to minimise tax liability Covers interventions that are referred to

Base erosion & profit shifting (BEPS) 25 May 2016 Introduction Important to distinguish between: Tax avoidance Using legal provisions to minimise tax liability Covers interventions that are referred to

COMMISSION STAFF WORKING DOCUMENT Accompanying the document. Proposal for a Council Directive

EUROPEAN COMMISSION Strasbourg, 25.10.2016 SWD(2016) 345 final COMMISSION STAFF WORKING DOCUMENT Accompanying the document Proposal for a Council Directive amending Directive (EU) 2016/1164 as regards

EUROPEAN COMMISSION Strasbourg, 25.10.2016 SWD(2016) 345 final COMMISSION STAFF WORKING DOCUMENT Accompanying the document Proposal for a Council Directive amending Directive (EU) 2016/1164 as regards

IBFD Course Programme International Tax Planning after BEPS and the MLI

IBFD Course Programme International Tax Planning after BEPS and the MLI Summary Recent developments such as the BEPS project and the Multilateral Instrument in international taxation, but also unilateral

IBFD Course Programme International Tax Planning after BEPS and the MLI Summary Recent developments such as the BEPS project and the Multilateral Instrument in international taxation, but also unilateral

The OECD BEPS Project and Developing Countries

The OECD BEPS Project and Developing Countries Richard Collier and Nadine Riedel ETPF - July 9, 2018 BEPS and Developing Countries 1 Aim of the Article G20/OECD base erosion and profit shifting (BEPS)

The OECD BEPS Project and Developing Countries Richard Collier and Nadine Riedel ETPF - July 9, 2018 BEPS and Developing Countries 1 Aim of the Article G20/OECD base erosion and profit shifting (BEPS)

OECD releases final BEPS package

6 October 2015 Tax Flash OECD releases final BEPS package On 5 October 2015, the OECD published the final reports of the OECD/G20 Base Erosion and Profit Shifting ( BEPS ) project, which consist of a package

6 October 2015 Tax Flash OECD releases final BEPS package On 5 October 2015, the OECD published the final reports of the OECD/G20 Base Erosion and Profit Shifting ( BEPS ) project, which consist of a package

Gijs Fibbe (Baker Tilly / Erasmus University) Bart Le Blanc (Norton Rose Fulbright) Andrew Roycroft (Norton Rose Fulbright) September 25, 2017

Bart Le Blanc (Norton Rose Fulbright) Andrew Roycroft (Norton Rose Fulbright) September 25, 2017") Implementation of the ATAD in the UK and NL Gijs Fibbe (Baker Tilly / Erasmus University) Bart Le Blanc (Norton Rose Fulbright) Andrew Roycroft (Norton Rose Fulbright) September 25, 2017 UK/NL (as many

Implementation of the ATAD in the UK and NL Gijs Fibbe (Baker Tilly / Erasmus University) Bart Le Blanc (Norton Rose Fulbright) Andrew Roycroft (Norton Rose Fulbright) September 25, 2017 UK/NL (as many

Answer-to-Question- 1

Answer-to-Question- 1 The arm's length principle is the standard used by all OECD parties in setting and testing prices between related parties. It aims to assess the level of profits which would have

Answer-to-Question- 1 The arm's length principle is the standard used by all OECD parties in setting and testing prices between related parties. It aims to assess the level of profits which would have

THE NETHERLANDS GLOBAL GUIDE TO M&A TAX: 2017 EDITION

THE NETHERLANDS 1 THE NETHERLANDS INTERNATIONAL DEVELOPMENTS 1. WHAT ARE RECENT TAX DEVELOPMENTS IN YOUR COUNTRY WHICH ARE RELEVANT FOR M&A DEALS AND PRIVATE EQUITY? There are various relevant developments

THE NETHERLANDS 1 THE NETHERLANDS INTERNATIONAL DEVELOPMENTS 1. WHAT ARE RECENT TAX DEVELOPMENTS IN YOUR COUNTRY WHICH ARE RELEVANT FOR M&A DEALS AND PRIVATE EQUITY? There are various relevant developments

Headline Verdana Bold International Tax matters ICPAU Tax Seminar, Hotel Africana November, 2017

Headline Verdana Bold International Tax matters ICPAU Tax Seminar, Hotel Africana November, 2017 Contents Related party transactions 3 URA practice on international tax 14 OCED Action Plan on BEPS 30 2017

Headline Verdana Bold International Tax matters ICPAU Tax Seminar, Hotel Africana November, 2017 Contents Related party transactions 3 URA practice on international tax 14 OCED Action Plan on BEPS 30 2017

Principles of International Tax Planning

Overview and Learning Objectives This course is aimed at analysing the fundamentals of international tax planning in a structured and consistent manner, deepening the knowledge of tax planning techniques

Overview and Learning Objectives This course is aimed at analysing the fundamentals of international tax planning in a structured and consistent manner, deepening the knowledge of tax planning techniques

Overview of OECD Action Plan on Base Erosion and Profit Shifting (BEPS)

") Overview of OECD Action Plan on Base Erosion and Profit Shifting (BEPS) Monia Naoum, IBFD Research Associate Emily Muyaa, IBFD Research Associate 18 June 2015 1 Introduction: Globalization and its impact

Overview of OECD Action Plan on Base Erosion and Profit Shifting (BEPS) Monia Naoum, IBFD Research Associate Emily Muyaa, IBFD Research Associate 18 June 2015 1 Introduction: Globalization and its impact

A8-0189/ Proposal for a directive (COM(2016)0026 C8-0031/ /0011(CNS)) Text proposed by the Commission

0026 C8-0031/ /0011(CNS)) Text proposed by the Commission") 3.6.2016 A8-0189/ 001-091 AMDMTS 001-091 by the Committee on Economic and Monetary Affairs Report Hugues Bayet Rules against tax avoidance practices A8-0189/2016 (COM(2016)0026 C8-0031/2016 2016/0011(CNS))

3.6.2016 A8-0189/ 001-091 AMDMTS 001-091 by the Committee on Economic and Monetary Affairs Report Hugues Bayet Rules against tax avoidance practices A8-0189/2016 (COM(2016)0026 C8-0031/2016 2016/0011(CNS))

THE INTERSECTION OF TAX & TREASURY

THE INTERSECTION OF TAX & TREASURY 1 INTRODUCTIONS Denise Magyer Senior Vice President, Allied Irish Bank BEATRIZ SALDIVAR MBA & CTP Consultant & Member of the Federal Reserve Faster Payments Task Force

THE INTERSECTION OF TAX & TREASURY 1 INTRODUCTIONS Denise Magyer Senior Vice President, Allied Irish Bank BEATRIZ SALDIVAR MBA & CTP Consultant & Member of the Federal Reserve Faster Payments Task Force

International Tax Greece Highlights 2019

International Tax Updated January 2019 Recent developments: For the latest tax developments relating to Greece, see Deloitte tax@hand. Investment basics: Currency Euro (EUR) Foreign exchange control Restrictions

International Tax Updated January 2019 Recent developments: For the latest tax developments relating to Greece, see Deloitte tax@hand. Investment basics: Currency Euro (EUR) Foreign exchange control Restrictions

BUSINESS MODELS IN THE CURRENT BEPS ENVIRONMENT DO YOU NEED TO CHANGE? Lyndon James, Partner Pete Rhodes, Senior Manager PwC

BUSINESS MODELS IN THE CURRENT BEPS ENVIRONMENT DO YOU NEED TO CHANGE? Lyndon James, Partner Pete Rhodes, Senior Manager PwC Agenda The current environment and the case for change Australian measures most

BUSINESS MODELS IN THE CURRENT BEPS ENVIRONMENT DO YOU NEED TO CHANGE? Lyndon James, Partner Pete Rhodes, Senior Manager PwC Agenda The current environment and the case for change Australian measures most

7th Global Headquarters Conference Swiss Tax Update in the international context

Tax and Legal Services 7th Global Headquarters Conference Swiss Tax Update in the international context Welcome! Your Speakers Armin Marti Partner, Leader Corporate Tax Switzerland Direct: +41 58 792 43

Tax and Legal Services 7th Global Headquarters Conference Swiss Tax Update in the international context Welcome! Your Speakers Armin Marti Partner, Leader Corporate Tax Switzerland Direct: +41 58 792 43

BEPS ACTION PLAN IMPLEMENTATION IN ASIAN-PACIFIC COUNTRIES

BEPS ACTION PLAN IMPLEMENTATION IN ASIAN-PACIFIC COUNTRIES Andrey SHELEPOV, Advisor of the International Relations Department of the Russian Union of Industrialists and Entrepreneurs (RSPP); Researcher

BEPS ACTION PLAN IMPLEMENTATION IN ASIAN-PACIFIC COUNTRIES Andrey SHELEPOV, Advisor of the International Relations Department of the Russian Union of Industrialists and Entrepreneurs (RSPP); Researcher

Table of Contents. Preface. Abbreviations and Terms

Preface Abbreviations and Terms v ix Chapter 1 Concepts and Basic Principles of EU Tax Law 1 1.1. Concepts 1 1.2. Relation to other legislation 3 1.2.1. Sovereignty and subsidiarity 3 1.2.2. Separateness

Preface Abbreviations and Terms v ix Chapter 1 Concepts and Basic Principles of EU Tax Law 1 1.1. Concepts 1 1.2. Relation to other legislation 3 1.2.1. Sovereignty and subsidiarity 3 1.2.2. Separateness

Tax Summit 2017 THE EU ANTI-TAX-AVOIDANCE DIRECTIVE taking a further look at the GAAR 27 October 2017

Tax Summit 2017 THE EU ANTI-TAX-AVOIDANCE DIRECTIVE taking a further look at the GAAR 27 October 2017 Background and introduction The international tax policy environment EU Anti-Tax-Avoidance-Package

Tax Summit 2017 THE EU ANTI-TAX-AVOIDANCE DIRECTIVE taking a further look at the GAAR 27 October 2017 Background and introduction The international tax policy environment EU Anti-Tax-Avoidance-Package

Hot topics Treasury seminar

Hot topics Treasury seminar Treasury in a transparent and new tax world Discover and unlock your potential Program Introduction on BEPS Potential implications for treasury o Interest deduction o Treaty

Hot topics Treasury seminar Treasury in a transparent and new tax world Discover and unlock your potential Program Introduction on BEPS Potential implications for treasury o Interest deduction o Treaty

Tax Avoidance in Thailand

Tax Avoidance in Thailand Arranged by SNP Training on 14 December 2017 Presented by Mr. Picharn Sukparangsee Bangkok Global Law Offices Limited 1 Tax evasion and tax avoidance Tax evasion is illegal. It

Tax Avoidance in Thailand Arranged by SNP Training on 14 December 2017 Presented by Mr. Picharn Sukparangsee Bangkok Global Law Offices Limited 1 Tax evasion and tax avoidance Tax evasion is illegal. It

Diverted Profits Tax. The Royal Society 6-9 Carlton House Terrace London SW1Y 5AG. 08 January 2015

Diverted Profits Tax The Royal Society 6-9 Carlton House Terrace London SW1Y 5AG 08 January 2015 Agenda 09.00 09.30 Registration 09.30 09.35 Open - Aidan Reilly (HMRC) 09.35 09.45 Policy Context and Overview

Diverted Profits Tax The Royal Society 6-9 Carlton House Terrace London SW1Y 5AG 08 January 2015 Agenda 09.00 09.30 Registration 09.30 09.35 Open - Aidan Reilly (HMRC) 09.35 09.45 Policy Context and Overview

European Commission publishes Anti Tax Avoidance Package

28 January 2016 - Number 65 Brazil Desk e-mail bulletin European Commission publishes Anti Tax Avoidance Package On 28 January 2016 the European Commission published an Anti Tax Avoidance Package containing

28 January 2016 - Number 65 Brazil Desk e-mail bulletin European Commission publishes Anti Tax Avoidance Package On 28 January 2016 the European Commission published an Anti Tax Avoidance Package containing

International Tax Malta Highlights 2019

International Tax Updated January 2019 Recent developments: For the latest tax developments relating to Malta, see Deloitte tax@hand. Investment basics: Currency Euro (EUR) Foreign exchange control No

International Tax Updated January 2019 Recent developments: For the latest tax developments relating to Malta, see Deloitte tax@hand. Investment basics: Currency Euro (EUR) Foreign exchange control No

A Historical Perspective on UK Corporation Tax. Development Charts. Peter Harris University of Cambridge. Saïd Business School, Oxford June 26, 2015

A Historical Perspective on UK Corporation Tax Development Charts Peter Harris University of Cambridge Saïd Business School, Oxford June 26, 2015 Note: The categories used in these charts broadly follow

A Historical Perspective on UK Corporation Tax Development Charts Peter Harris University of Cambridge Saïd Business School, Oxford June 26, 2015 Note: The categories used in these charts broadly follow

Holding Companies in Cyprus

Holding Companies in Cyprus 1 Contents Page # Introduction 3 Formation of a Holding Company 3 Taxation of Holding Company 4 Dividend Income 4 Capital Gains on Disposal of Shares 4 Repatriation of Dividends

Holding Companies in Cyprus 1 Contents Page # Introduction 3 Formation of a Holding Company 3 Taxation of Holding Company 4 Dividend Income 4 Capital Gains on Disposal of Shares 4 Repatriation of Dividends

Korean Tax Update BEPS Implementation

Presentation for KGCCI Korean Tax Update BEPS Implementation May 2018 CONTENTS I. BEPS: Backgrounds What is BEPS? Backgrounds for OECD BEPS Project BEPS Action plans II. BEPS Implementation in Korea I.

Presentation for KGCCI Korean Tax Update BEPS Implementation May 2018 CONTENTS I. BEPS: Backgrounds What is BEPS? Backgrounds for OECD BEPS Project BEPS Action plans II. BEPS Implementation in Korea I.

- Simplification rule for pure intermediary companies : remuneration

Theme Source of law Object / Date of application PAST CHANGES Impact / Comments 1. Transfer Pricing Article 56 of the Luxembourg Income Tax Law (LIR) and paragraph 171 Abgabenordnung Introduction of the

Theme Source of law Object / Date of application PAST CHANGES Impact / Comments 1. Transfer Pricing Article 56 of the Luxembourg Income Tax Law (LIR) and paragraph 171 Abgabenordnung Introduction of the

Transfer pricing interaction

A practical approach to the DPT Much has been written about the rights and wrongs of the Diverted Profi ts Tax included in Part 3 of the Finance Act 2015. This article faces up to the reality that it is

A practical approach to the DPT Much has been written about the rights and wrongs of the Diverted Profi ts Tax included in Part 3 of the Finance Act 2015. This article faces up to the reality that it is

International Tax Greece Highlights 2018

International Tax Greece Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control Capital controls are in force and certain limitations still apply on bank withdrawals and bank transfers

International Tax Greece Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control Capital controls are in force and certain limitations still apply on bank withdrawals and bank transfers

IMPACT OF TAX ON M&A. Simon Fletcher 14 October 2016

IMPACT OF TAX ON M&A Simon Fletcher AGENDA 1. Tax environment 2. Recent developments 3. Impact on M&A 4. Questions Disclaimer: this presentation is intended to be for general guidance on matters of interest,

IMPACT OF TAX ON M&A Simon Fletcher AGENDA 1. Tax environment 2. Recent developments 3. Impact on M&A 4. Questions Disclaimer: this presentation is intended to be for general guidance on matters of interest,

The International Tax Landscape

and EU Tax Reforms How will Ireland, Luxembourg, Netherlands and Switzerland Reform Their Tax Systems to Comply?, Loyens & Loeff NV, PricewatershouseCoopers, PricewaterhouseCoopers 67 th Annual Tax Conference

and EU Tax Reforms How will Ireland, Luxembourg, Netherlands and Switzerland Reform Their Tax Systems to Comply?, Loyens & Loeff NV, PricewatershouseCoopers, PricewaterhouseCoopers 67 th Annual Tax Conference

Anti Avoidance Rules and Treaty Shopping (including Limitation of Benefits) CA Sanjay Tolia. December 2014

CA Sanjay Tolia. December 2014") Anti Avoidance Rules and Treaty Shopping (including Limitation of Benefits) CA Sanjay Tolia Agenda Treaty shopping - Concept Key anti-avoidance measures in tax treaties Limitation on Benefits Beneficial

Anti Avoidance Rules and Treaty Shopping (including Limitation of Benefits) CA Sanjay Tolia Agenda Treaty shopping - Concept Key anti-avoidance measures in tax treaties Limitation on Benefits Beneficial

CYPRUS TAX STRUCTURES

www.servpro.com.cy CYPRUS TAX STRUCTURES Serviced By PROFESSIONALS Holding Company (Inbound Investment) Non- Resident Company 0% / low withholding tax on dividends EU Parent Subsidiary Directive EU 0%

www.servpro.com.cy CYPRUS TAX STRUCTURES Serviced By PROFESSIONALS Holding Company (Inbound Investment) Non- Resident Company 0% / low withholding tax on dividends EU Parent Subsidiary Directive EU 0%

EU's Anti-Tax Avoidance Proposal Is Problematic

Portfolio Media. Inc. 860 Broadway, 6th Floor New York, NY 10003 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@law360.com EU's Anti-Tax Avoidance Proposal Is Problematic Jordi

Portfolio Media. Inc. 860 Broadway, 6th Floor New York, NY 10003 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@law360.com EU's Anti-Tax Avoidance Proposal Is Problematic Jordi

A small country perspective on international taxation Ann Nolan, Second Secretary General, Ministry of Finance, Ireland Oxford University Centre for

A small country perspective on international taxation Ann Nolan, Second Secretary General, Ministry of Finance, Ireland Oxford University Centre for Business Taxation, Summer Conference, 23 June 2014 Outline

A small country perspective on international taxation Ann Nolan, Second Secretary General, Ministry of Finance, Ireland Oxford University Centre for Business Taxation, Summer Conference, 23 June 2014 Outline

Next Generation Fund Structuring Are you ready? 10 May 2017

Next Generation Fund Structuring Are you ready? 10 May 2017 Global Private Equity Fundraising Activity Page 2 Agenda and Speakers 1. Fund Level Considerations Adam Williams EY Greater China Private Equity

Next Generation Fund Structuring Are you ready? 10 May 2017 Global Private Equity Fundraising Activity Page 2 Agenda and Speakers 1. Fund Level Considerations Adam Williams EY Greater China Private Equity

Do we have the wrong tax system for the digital economy? Alf Capito, Tax Policy Leader, EY Asia Pacific July 2014

Do we have the wrong tax system for the digital economy? Alf Capito, Tax Policy Leader, EY Asia Pacific July 2014 Key features of the digital economy as seen by the OECD taskforce Mobility Reliance on

Do we have the wrong tax system for the digital economy? Alf Capito, Tax Policy Leader, EY Asia Pacific July 2014 Key features of the digital economy as seen by the OECD taskforce Mobility Reliance on

Recent and expected tax changes in Bulgaria and Greece important for cross-border operations

Baker Tilly in South East Europe Cyprus, Bulgaria, Greece, Romania, Moldova Recent and expected tax changes in Bulgaria and Greece important for cross-border operations November 2016 Agenda Implementation

Baker Tilly in South East Europe Cyprus, Bulgaria, Greece, Romania, Moldova Recent and expected tax changes in Bulgaria and Greece important for cross-border operations November 2016 Agenda Implementation

3.2. EU Interest-Royalty Directive Background and force

3.2. EU Interest-Royalty Directive 3.2.1. Background and force Force The Council Directive (2003/49/EC) on a Common System of Taxation Applicable to Interest and Royalty Payments Made between Associated

3.2. EU Interest-Royalty Directive 3.2.1. Background and force Force The Council Directive (2003/49/EC) on a Common System of Taxation Applicable to Interest and Royalty Payments Made between Associated

BEPS Multilateral Instrument (MLI), India s Corresponding Positions, Implementation (GAAR)

, India s Corresponding Positions, Implementation (GAAR)") BEPS Multilateral Instrument (MLI), India s Corresponding Positions, Implementation (GAAR) Dr. Parthasarathi Shome Chairman International Tax Research and Analysis Foundation (ITRAF) www.itraf.org Visiting

BEPS Multilateral Instrument (MLI), India s Corresponding Positions, Implementation (GAAR) Dr. Parthasarathi Shome Chairman International Tax Research and Analysis Foundation (ITRAF) www.itraf.org Visiting

International Tax New Zealand Highlights 2019

International Tax Updated January 2019 Recent developments For the latest tax developments relating to New Zealand, see Deloitte tax@hand. Investment basics: Currency New Zealand Dollar (NZD) Foreign exchange

International Tax Updated January 2019 Recent developments For the latest tax developments relating to New Zealand, see Deloitte tax@hand. Investment basics: Currency New Zealand Dollar (NZD) Foreign exchange

Today s key challenge in Treasury Transfer Pricing & Treasury

www.pwc.lu Today s key challenge in Treasury Transfer Pricing & Treasury Content The word of the President Virtual reality of Treasury Overview - Treasury operations Intercompany financing Cash pooling

www.pwc.lu Today s key challenge in Treasury Transfer Pricing & Treasury Content The word of the President Virtual reality of Treasury Overview - Treasury operations Intercompany financing Cash pooling

United Kingdom diverted profits tax now in effect

United Kingdom diverted profits tax now in effect Diverted profits tax (DPT) applies at a rate of 25% from 1 April 2015 to profits of multinationals that are considered to have been artificially diverted

United Kingdom diverted profits tax now in effect Diverted profits tax (DPT) applies at a rate of 25% from 1 April 2015 to profits of multinationals that are considered to have been artificially diverted

The Netherlands in International Tax Planning Second revised edition. Table of contents

The Netherlands in International Tax Planning Second revised edition Table of contents Chapter 1: General introduction 1.1. What this book is and what it is not 1.2. Tone 1.3. EU law 1.4. Substantial amended

The Netherlands in International Tax Planning Second revised edition Table of contents Chapter 1: General introduction 1.1. What this book is and what it is not 1.2. Tone 1.3. EU law 1.4. Substantial amended

International Tax Primer. Third Edition. Brian J. Arnold

International Tax Primer Third Edition Brian J. Arnold Wolters Kluwer Preface xi CHARTER 1 Introduction 1 1.1 Objectives of This Primer 1 1.2 What Is International Tax? 2 1.3 Goals of International Tax

International Tax Primer Third Edition Brian J. Arnold Wolters Kluwer Preface xi CHARTER 1 Introduction 1 1.1 Objectives of This Primer 1 1.2 What Is International Tax? 2 1.3 Goals of International Tax

The Advantages of the UK as a Location for a Holding Company. David Gibbs May 2015

The Advantages of the UK as a Location for a Holding Company David Gibbs May 2015 The UK is an attractive location to site an international holding company since not only does it offer a relatively stable

The Advantages of the UK as a Location for a Holding Company David Gibbs May 2015 The UK is an attractive location to site an international holding company since not only does it offer a relatively stable

Dutch Tax Bill 2019: what will change?

1 Dutch Tax Bill 2019: what will change? On 18 September 2018, the Dutch government presented a number of tax measures as part of the 2019 budget proposals. The key measures are: Abolition of withholding

1 Dutch Tax Bill 2019: what will change? On 18 September 2018, the Dutch government presented a number of tax measures as part of the 2019 budget proposals. The key measures are: Abolition of withholding

LUXEMBOURG GLOBAL GUIDE TO M&A TAX: 2018 EDITION

LUXEMBOURG 1 LUXEMBOURG INTERNATIONAL DEVELOPMENTS 1. WHAT ARE RECENT TAX DEVELOPMENTS IN YOUR COUNTRY WHICH ARE RELEVANT FOR M&A DEALS AND PRIVATE EQUITY? Corporate income tax ( CIT ) rate The CIT rate

LUXEMBOURG 1 LUXEMBOURG INTERNATIONAL DEVELOPMENTS 1. WHAT ARE RECENT TAX DEVELOPMENTS IN YOUR COUNTRY WHICH ARE RELEVANT FOR M&A DEALS AND PRIVATE EQUITY? Corporate income tax ( CIT ) rate The CIT rate

U.S. Tax Legislation Corporate and International Provisions. Corporate Law Provisions

U.S. Tax Legislation Corporate and International Provisions On December 20, 2017, Congress enacted comprehensive tax legislation (the Act ). This memorandum highlights some of the important provisions

U.S. Tax Legislation Corporate and International Provisions On December 20, 2017, Congress enacted comprehensive tax legislation (the Act ). This memorandum highlights some of the important provisions

Astera Primanto Bhakti. Asian Tax Authorities Symposium

By: Astera Primanto Bhakti Director of Center for State Revenue Policy, Fiscal Policy Office, Ministry of Finance of The Republic of Indonesia on the event of: Asian Tax Authorities Symposium 4 5 September

By: Astera Primanto Bhakti Director of Center for State Revenue Policy, Fiscal Policy Office, Ministry of Finance of The Republic of Indonesia on the event of: Asian Tax Authorities Symposium 4 5 September

Welcome to the EFS-seminar. BEPS and transfer pricing, but what about VAT and Customs? Conference Chairman: René van der Paardt

Welcome to the EFS-seminar BEPS and transfer pricing, but what about VAT and Customs? Conference Chairman: René van der Paardt Rotterdam February 3, 2016 Agenda Seminar An update on the transfer pricing

Welcome to the EFS-seminar BEPS and transfer pricing, but what about VAT and Customs? Conference Chairman: René van der Paardt Rotterdam February 3, 2016 Agenda Seminar An update on the transfer pricing

International Tax Impact of Business Entity Selection for Foreign Operations of U.S. Companies

FOR LIVE PROGRAM ONLY International Tax Impact of Business Entity Selection for Foreign Operations of U.S. Companies TUESDAY, DECEMBER 12, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

FOR LIVE PROGRAM ONLY International Tax Impact of Business Entity Selection for Foreign Operations of U.S. Companies TUESDAY, DECEMBER 12, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

Analysis of New Law UK CORPORATE TAX REFORM. Nikol Davies *

70 Analysis of New Law UK CORPORATE TAX REFORM Nikol Davies * INTRODUCTION The long anticipated consultation document for corporate tax reform was published by the government on 29 November 2010. The document

70 Analysis of New Law UK CORPORATE TAX REFORM Nikol Davies * INTRODUCTION The long anticipated consultation document for corporate tax reform was published by the government on 29 November 2010. The document

Simplifying BEPS Action Plan

Simplifying BEPS Action Plan BEPS and GST Conference 2 nd September 2016 1 About the pic: 16 Nov 2015, In Antalya, Leaders expressed support for the package of measures developed under the G-20/OECD Base

Simplifying BEPS Action Plan BEPS and GST Conference 2 nd September 2016 1 About the pic: 16 Nov 2015, In Antalya, Leaders expressed support for the package of measures developed under the G-20/OECD Base

Taxation of cross-border mergers and acquisitions Denmark

Taxation of cross-border mergers and acquisitions Denmark kpmg.com/tax KPMG International Denmark Introduction Danish tax rules and practice have changed fundamentally in recent years. A number of rules

Taxation of cross-border mergers and acquisitions Denmark kpmg.com/tax KPMG International Denmark Introduction Danish tax rules and practice have changed fundamentally in recent years. A number of rules

Substance: A wake up call. ATOZ Briefing

Substance: A wake up call ATOZ Briefing 21 February 2018 CONTENTS 1 2 3 4 INTRODUCTION THE NOTION OF SUBSTANCE THE IMPORTANCE OF SUBSTANCE IN INTERNATIONAL TAX DEFINING THE RIGHT LEVEL OF SUBSTANCE 5 CONCLUSION

Substance: A wake up call ATOZ Briefing 21 February 2018 CONTENTS 1 2 3 4 INTRODUCTION THE NOTION OF SUBSTANCE THE IMPORTANCE OF SUBSTANCE IN INTERNATIONAL TAX DEFINING THE RIGHT LEVEL OF SUBSTANCE 5 CONCLUSION

China s SAT publishes new rules on beneficial owners

World Tax Advisor Connecting you globally. 23 February 2018 China s SAT publishes new rules on beneficial owners On 3 February 2018, China s State Administration of Taxation (SAT) published new rules (Bulletin

World Tax Advisor Connecting you globally. 23 February 2018 China s SAT publishes new rules on beneficial owners On 3 February 2018, China s State Administration of Taxation (SAT) published new rules (Bulletin

B.E.P.S. ACTION 4: LIMIT BASE EROSION VIA INTEREST PAYMENTS AND OTHER FINANCIAL PAYMENTS

B.E.P.S. ACTION 4: LIMIT BASE EROSION VIA INTEREST PAYMENTS AND OTHER FINANCIAL PAYMENTS Authors Stanley C. Ruchelman Sheryl Shah Tags Action 4 Financial Payments Interest Equivalents Interest Expense

B.E.P.S. ACTION 4: LIMIT BASE EROSION VIA INTEREST PAYMENTS AND OTHER FINANCIAL PAYMENTS Authors Stanley C. Ruchelman Sheryl Shah Tags Action 4 Financial Payments Interest Equivalents Interest Expense

Agreement on EU Anti-Tax Avoidance Directive

Agreement on EU Anti-Tax Avoidance Directive On 21 June 2016, the EU Council finally agreed on the draft EU Anti-Tax Avoidance Directive (ATAD). The agreement was reached following discussions by the Economic

Agreement on EU Anti-Tax Avoidance Directive On 21 June 2016, the EU Council finally agreed on the draft EU Anti-Tax Avoidance Directive (ATAD). The agreement was reached following discussions by the Economic

Option 2: How to avoid double taxation? Tax treaty 101

Option 2: How to avoid double taxation? Tax treaty 101 Stefano Mariani TEP, Deacons Steven Sieker TEP, Baker & McKenzie Kindly sponsored by Background of international taxation 1. The power to make tax

Option 2: How to avoid double taxation? Tax treaty 101 Stefano Mariani TEP, Deacons Steven Sieker TEP, Baker & McKenzie Kindly sponsored by Background of international taxation 1. The power to make tax

Ms. Jidtar Neesanun Senior Tax Audit Officer The Revenue Department of Thailand

The Fourth IMF-Japan High-Level Tax Conference, Tokyo 2013 Anti-Avoidance Rules: Administrative Issues Ms. Jidtar Neesanun Senior Tax Audit Officer The of Thailand INTRODUCTION Current Situation Step Forward

The Fourth IMF-Japan High-Level Tax Conference, Tokyo 2013 Anti-Avoidance Rules: Administrative Issues Ms. Jidtar Neesanun Senior Tax Audit Officer The of Thailand INTRODUCTION Current Situation Step Forward

INTRODUCTION 2019 TAX PLAN

2019 DUTCH TAX PLAN INTRODUCTION During Budget Day (18 September 2018) in the Netherlands a number tax plans were published. Please find below a selection of the most relevant proposals PERSONAL INCOME

2019 DUTCH TAX PLAN INTRODUCTION During Budget Day (18 September 2018) in the Netherlands a number tax plans were published. Please find below a selection of the most relevant proposals PERSONAL INCOME

Recent BEPS related legislation/guidance impacting Luxembourg

Recent BEPS related legislation/guidance impacting Luxembourg Recently a set of BEPS related draft legislation/guidance has been published: (i) on 21 June 2016, the Council of the European Union ( EU )

Recent BEPS related legislation/guidance impacting Luxembourg Recently a set of BEPS related draft legislation/guidance has been published: (i) on 21 June 2016, the Council of the European Union ( EU )

Sustainability of upper tier structures impact of BEPS

Key topics in M&A Sustainability of upper tier structures impact of BEPS Highlights Sustainability of existing upper tier structures should be assessed in the light of the changing tax environment. If

Key topics in M&A Sustainability of upper tier structures impact of BEPS Highlights Sustainability of existing upper tier structures should be assessed in the light of the changing tax environment. If

VAT The submerged part of the BEPS

www.pwc.com VAT The submerged part of the BEPS Thursday, Geneva Agenda Background Potential VAT impact of BEPS Permanent establishment (PE) issues and threats to commissionaire structures How non-european

www.pwc.com VAT The submerged part of the BEPS Thursday, Geneva Agenda Background Potential VAT impact of BEPS Permanent establishment (PE) issues and threats to commissionaire structures How non-european