Impacts of U.S. International Tax Reform. October 23, 2018

|

|

|

- Meagan Nelson

- 5 years ago

- Views:

Transcription

1 Impacts of U.S. International Tax Reform October 23, 2018

Anthony Sileo (KPMG) Stephen Blough")

2 Christopher Jentile (Verizon), Moderator William Crowley (PwC) Anthony Sileo (KPMG) Stephen Blough (KPMG) 2

3 Christopher Jentile Christopher is an Executive Director of Global Tax Planning at Verizon Communications Inc. Since joining Verizon in 2008, Christopher is responsible for Federal, state and local and non-u.s. tax planning and non-u.s. tax reporting. Prior to joining Verizon, Christopher held tax leadership positions in several major multi-national corporations. Christopher received his L.L.M.-Tax from NYU School of Law, his J.D. from Rutgers School of Law and his B.S. from Fordham University. 3

4 William Crowley Will is a Principal in PricewaterhouseCoopers Industry Services Group where he advises his clients on the US Federal income tax aspects of domestic and international transactions. He has worked on numerous projects involving crossborder acquisitions and divestitures, transfer pricing optimization and intellectual property migration. Will helps his clients identify operational and structural tax planning opportunities while taking into account the complex and dynamic organizational implications that often result from such strategic planning opportunities. Prior to joining PwC, Will spent 15 years in senior tax leadership positions at two Fortune 50 corporations, including responsibility for leading the international tax function. In this capacity, Will drove strategic planning initiatives and partnered with senior business leaders across these companies to implement value chain transformation initiatives and other business restructurings to achieve sustainable financial and operational synergies. 4

5 Anthony Sileo Anthony Sileo is a Principal in KPMG s International Tax practice based in New York Metro and serves as the International Tax practice s East Region Service Leader. Anthony is responsible for a broad range of multinational clients, and has extensive experience with respect to complex cross-border transactions and international tax and transfer pricing matters relating to his client s businesses. Anthony s current and past clients include leaders in the manufacturing, consumer products, retail, technology, and communications industries. Prior to joining KPMG, Anthony was employed at a multinational law firm and advised clients on a variety of corporate legal and international, federal, and state tax matters. Anthony is a frequent speaker on international tax matters for professional organizations, including the Tax Executives Institute. 5

6 Stephen Blough Dr. Stephen Blough leads the transfer pricing and tax-related valuations group within the KPMG US Washington National Tax practice. As the firm s senior transfer pricing economist, Dr. Blough serves as lead transfer pricing economist for some of KPMG s largest clients, and provides technical assistance on many other projects. He is also responsible for thought leadership on US and OECD transfer pricing regulatory developments. He has authored publications on transfer pricing topics ranging from valuation of intangible property to treatment of intercompany services. Prior to joining KPMG in 1994, Dr. Blough was an economist at the Federal Reserve Bank of Boston, where he was responsible for the analysis of financial markets in their relationship to monetary and regulatory policy. He spent six years on the faculty of the department of economics at The Johns Hopkins University, where he taught graduate courses in econometric methods and macroeconomics. He has a Ph.D. in Economics and M.A. in Statistics from the University of California at Berkeley. 6

and Related Foreign Tax")

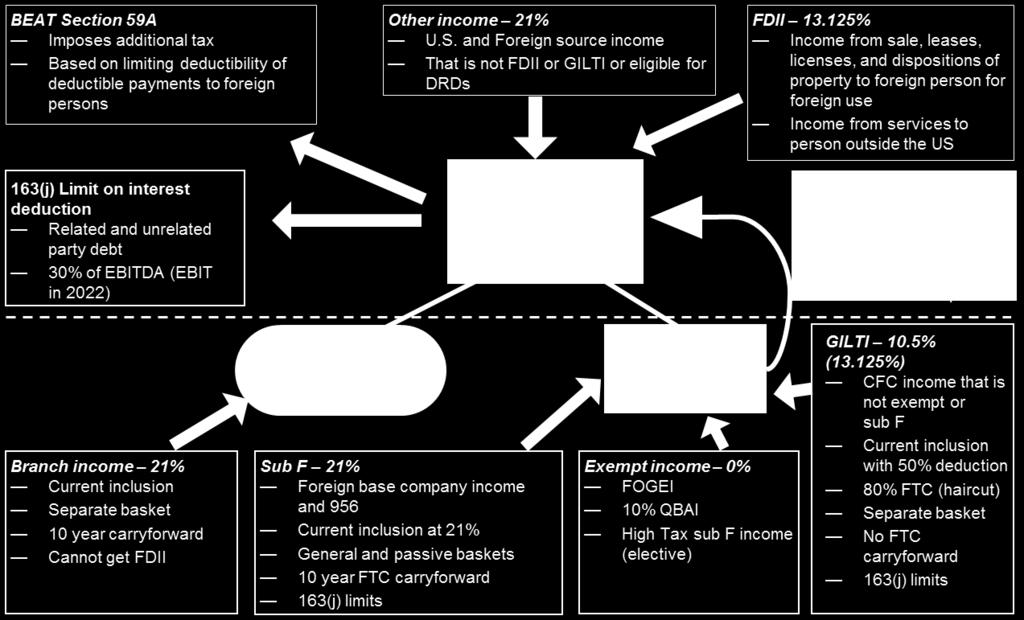

7 The U.S. International Tax Landscape - Overview Global Intangible Low-Taxed Income (GILTI) and Related Foreign Tax Credit (FTC) Considerations Foreign Derived Intangible Income (FDII) Base Erosion Anti-Abuse Tax (BEAT) Q&A 7

8 Overview 8

9 Overview of New International Tax Framework 9

10 Treasury Regulations Expected Provision Tentative release date* GILTI Proposed Regulations released on 9/13 FDII By the end of the year BEAT By the end of November PTI (GILTI and 965) By the end of the year FTC By the end of November 267A - Hybrids By the end of the year 163(j) By the end of November * Release dates are based upon recent statements by Treasury and IRS staff, but are very tentative. 10

11 Case Study Illustrative Structure (Pre-Tax Reform) U.S. Multinational Customers Cost Sharing Agreement U.S. Multinational Corporation IP Contract R&D Services Income earned by Non-U.S. Principal (CFC 1) not subject to U.S. tax under Subpart F and taxed only in Country A Customer Sub (Country A) CFC 1 Non-U.S. Principal (Country A) (10% tax rate) IP Royalty and/or Services fees CFC 2 (Country B) (25% tax rate) CFC 3 (Country C) (33% tax rate) Income earned by CFC 2 and CFC 3 not subject to U.S. tax under Subpart F and taxed only in Countries B and C Key: Payment Flows Services Other Customers (Country B) U.S. Multinational Corporation receives deduction (at 35%) for outbound service payments 11

12 12

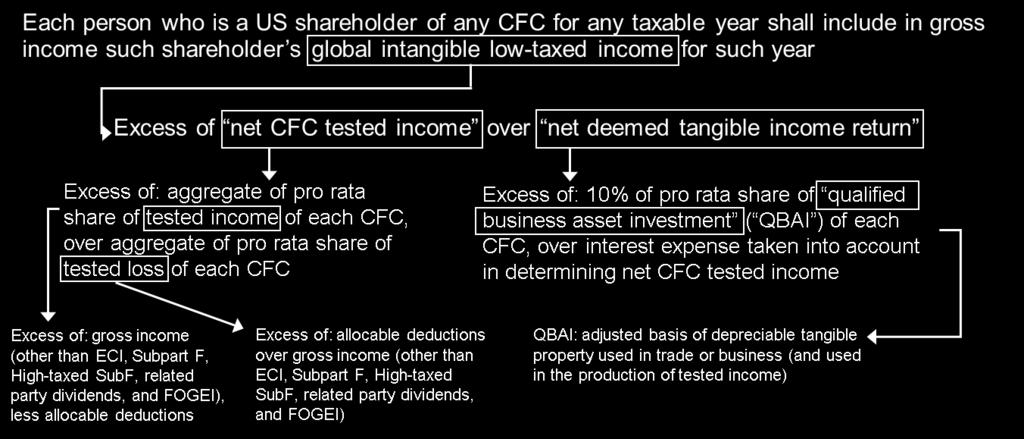

13 Overview of CFC Income Three Categories Exempt Income Subpart F Income (Full US Taxation at 21% corporate rate) GILTI - Minimum Tax at 50% of corporate rate (10.5%, but... ) 13

14 GILTI Essentials and Mechanics Current Inclusion US Shareholders are subject to current US taxation on their portion of a CFC s global intangible low-taxed income (GILTI) Netting US Shareholders net positive GILTI and negative GILTI from their CFCs Tax Rate Lower tax rate is achieved through a deduction: 50% for tax years beginning before 12/31/25, and 37.5% thereafter Total GILTI and foreign-derived intangible income (FDII) deduction is limited by taxable income (without regard to GILTI and FDII) Effective Date Effective for CFC tax years beginning after December 31, 2017 Computation done on a USSH-by-USSH basis but under the Proposed Regulations, USSHs in same consolidated group treated as one shareholder Impact of expense allocations! No QBAI from tested loss CFCs QBAI determined on a quarterly average method, using basis determined under ADS principles 14

15 GILTI Mechanics Definitionally Driven 15

16 GILTI Basket: Haircuts and Limitations Deemed paid tax credits under new Section 960(d) available to offset the US tax cost associated with GILTI inclusions with several haircuts and limitations: No FTCs for foreign income tax paid or accrued by tested loss CFCs Inclusion percentage reduces FTCs when there is QBAI or tested loss CFCs Limited to 80% of foreign taxes attributable to Tested Income (after previously noted reductions) Separate FTC category for GILTI inclusions Impact of expense allocations to GILTI basket FTCs in GILTI basket cannot be carried forward or back Use It or Lose It! Section 78 gross up based on full amount of foreign taxes (reduced by inclusion percentage) Query: What basket? Preamble to proposed regulations clarifies to expect GILTI basket. 16

17 Approach to GILTI: Fight or Flight? Approach Flight Description Away from GILTI and into Subpart F Opportunities Structuring into high-taxed Subpart F income through operational or structural changes FTCs can be claimed currently, or deferred and selectively claimed through Section 956 Fight Limit Tested Losses Restructure legal entities so that tested loss entities are combined with tested income entities to avoid elimination of QBAI and FTCs from calculations Fight FTC Limitations Changing allocation formulas and inputs: Reduce expenses allocated to GILTI income to increase FTC capacity 17

18 Other GILTI Planning Opportunities - Transfer Pricing Considerations Stability/Control: FTC planning in a GILTI world requires stable, predictable income streams; this will demand a robust and defensible world-wide transfer pricing policy Un-trapping QBAI and FTCs: Revised transfer pricing may be able to turn loss CFCs profitable Revisit transfer pricing in connection with related party payments into US: Royalties Product Sales Services 18

19 USMN Customers Case Study: Illustrative Structure GILTI Implications CSA U.S. Multinational Corporation IP Contract R&D Services GILTI of CFC1, CFC2, and CFC3 subject to U.S. tax at effective rate of 10.5% Ability to credit foreign taxes paid. Revisit/minimize expense allocation (e.g., interest expense stewardship) to GILTI basket Customer Sub (Country A) CFC 1 Non-U.S. Principal (Country A) (10% tax rate) IP Royalty and/or Services fees CFC 2 (Country B) (25% tax rate) Customers (Country B) CFC 3 (Country C) (33% tax rate) Consider structuring into subpart F for high-tax CFCs Consider on-shoring IP if substance at CFC Principal is not aligned with business (especially if CFC Principal has risk of not meeting DEMPE) and cost is not high to effect change management 19

20 20

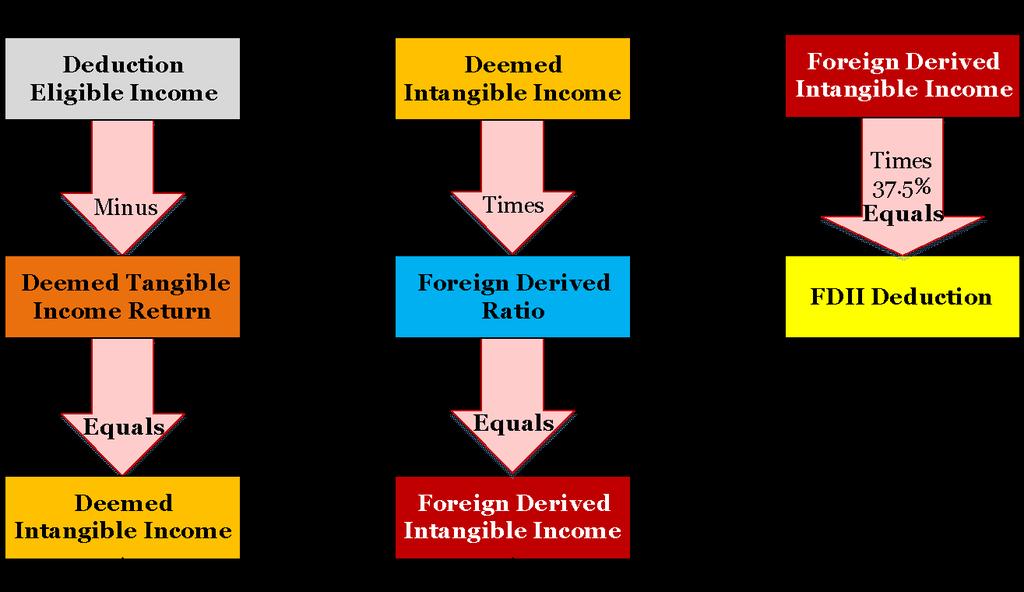

21 Foreign Derived Intangible Income (FDII) In order to minimize incentives to move and hold intangible assets outside the U.S., new Section 250 allows a deduction for Eligible C Corporations that reduces the effective U.S. tax rate on foreign-derived income treated as attributable to intellectual property and other intangible assets. FDII is generally the portion of the U.S. corporation s net income (other than GILTI and certain other income exclusions) that Exceeds a deemed rate of return of the U.S. corporation s tangible depreciable business assets and Is attributable to certain sales of property to foreign persons or to the provision of certain services to any person, or with respect to any property, located outside the U.S. 21

22 Foreign Derived Intangible Income (FDII) Overview Section 250(a) allows a domestic corporation to deduct an amount which is the lesser of (1) the sum of 37.5% of its foreign-derived intangible income (FDII) plus 50% of its GILTI; or (2) taxable income Legislative history indicates that the deduction is only available to domestic C corporations which are not RICs or REITS. The allowable deduction percentages decrease to % for FDII and 37.5% for GILTI for tax years beginning after December 31,

23 Deduction for foreign-derived intangible income (FDII) Overview Deduction eligible income: the excess (if any) of: The gross income of a domestic corporation, excluding: Subpart F income GILTI any financial services income (as defined in Section 904(d)(2)(D)) any dividend received from a CFC by its US shareholder any domestic oil and gas income of the corporation, and any foreign branch income (as defined in Section 904(d)(2)(J)) Over the deductions (including taxes) properly allocable to such gross income. Eligible Gross Income - Allocable Deductions (including taxes) = Deduction Eligible Income 23

24 Foreign Derived Intangible Income (FDII) Additional Detail Foreign-derived deduction eligible income: any deduction eligible income of the taxpayer that is derived in connection with: property sold by the taxpayer to any person who is not a US person and that the taxpayer establishes to the satisfaction of the Secretary is for a foreign use, or services provided by the taxpayer that it establishes to the satisfaction of the Secretary are provided to any person, or with respect to property, not located within the United States. Foreign use: The sale of property to a foreign related party is not treated as for foreign use unless: Such property is ultimately sold by a related party, or used by a related party in connection with property which is sold or the provision of services, to another person who is an unrelated party who is not a United States person, and the taxpayer establishes to the satisfaction of the Secretary that such property is for foreign use. The TCJA further provides that a sale of property is treated as sale of its component parts. 24

25 Foreign Derived Intangible Income (FDII) Deemed tangible income return: with respect to any corporation, an amount equal to 10% of the corporation s qualified business asset investment (QBAI) as defined in Section 951A(d) without regard to whether the corporation is a CFC. Deemed intangible income: the excess (if any) of its deduction eligible income over its deemed tangible income return. Foreign-derived intangible income: with respect to a domestic corporation, is the amount which bears the same ratio to the corporation s deemed intangible income as its foreign-derived deduction eligible income (FDDEI) bears to its deduction eligible income (DEI). Foreign-Derived Intangible Income = Deemed Intangible Income x FDDEI / DEI 25

26 Deduction for foreign-derived intangible income (FDII) 26

27 FDII Global Structuring Considerations What actions should taxpayers consider taking and when? Taxpayers should model their existing operations to determine which income streams could immediately qualify for the preferential FDII US tax rate Taxpayers should consider whether onshoring foreign IP to the United States to the lower, preferential FDII US tax rate State and local corporate income taxes must also be considered when comparing to the effective tax rate applicable to the IP income if it remains offshore What does this mean for taxpayers? Taxpayers will need to calculate the impact of preferential rate and the corresponding GILTI impacts Taxpayers will need to determine whether US income may qualify as FDII 27

28 Case Study: Illustrative Structure (Post-Tax Reform) U.S. Multinational Key: Customer Customer Subs (Country A) Payment Flows Services Other Services Contract U.S. Multinational Corporation CFC 2 (Country B) (20% tax rate) Customer (Country B) Royalty IP U.S. MNC purchases IP from Non-U.S. Principal With all IP now owned directly in the U.S., royalties from CFCs for non-u.s. IP used to provide services to local customers (e.g., CFC 2) now paid to the U.S., reducing GILTI exposure and increasing potential FDII benefit Consider BEAT implications of outbound payment for the IP, which could be considered a deductible payment due to future U.S. tax amortization U.S. MNC contracts directly with some Non-U.S. Customers Income earned from services to Non-U.S. Customers may benefit from FDII Eliminates outbound payments to CFCs for I/C services performed that could be characterized as Base Erosion Payments for BEAT purposes 28

29 29

30 What is BEAT? The base erosion and anti-abuse tax ( BEAT ) is essentially a minimum tax calculated on a base equal to the taxpayer s income determined without tax benefits arising from base erosion payments. Broadly, base erosion payments are any amounts paid or accrued by a US taxpayer to a foreign related party and which have the effect of reducing the gross receipts of the US taxpayer. The main types of payments that could trigger the BEAT are service fees, interest, and royalties. Base eroding payments also include payments to acquire tangible or intangible property if acquired property generates amortization or depreciation deductions. The following are generally not base erosion payments: Reductions to gross receipts for costs required to be capitalized to inventory and recovered as COGS under Sections 471 and 263A Pass-through amounts that are not gross income and deductions for US Federal income tax purposes Amounts paid or accrued for certain types of services ('service cost method exception') refer to Section 59A(d)(5) Certain qualified derivative payments - see Section 59A(h) 30

")

31 BEAT Minimum Tax BEAT Minimum Tax rates increase over time: Note: Base erosion minimum tax amount considers other applicable tax credits No carryforwards or carrybacks (like GILTI) 31

32 When does BEAT Apply? BEAT The BEAT applies to any U.S. corporation other than a Regulated Investment Company (RIC), a REIT, or an S corporation (whether U.S.-parented or foreign-parented) that makes significant deductible payments to foreign related parties. Thresholds to determine applicable taxpayer - Taxpayer has: (1) Average annual gross receipts of at least $500 million for the 3 taxable-year period ending with the preceding taxable year; and (2) A base erosion percentage of 3% or higher (2% for banks or registered securities dealers) for the taxable year. 32

33 Key Definitions A base erosion tax benefit means any deduction allowed (other than cost of goods sold) with respect to a base erosion payment for the taxable year. Base erosion percentage: determined by dividing the aggregate amount of base erosion tax benefits by the aggregate amount of the deductions allowable under Chapter 1, taking into account base erosion tax benefit for which a deduction is allowed under Chapter 1 and by not taking into account any deduction allowed under sections 172, 245A or 250. Modified taxable income: taxable income computed under Chapter 1 for the taxable year, determined without regard to any base erosion tax benefit with respect to any base erosion payment, or the base erosion percentage of any NOL deduction allowed under section 172 for the taxable year. 33

34 Several Common Trends Effects across industry sectors: Inbound and outbound businesses Services companies Leasing and licensing companies Financial institutions Impact on common operating models: Global R&D footprint Intra-group transaction 'hubs' Global contracting models Service centers Character of items for Federal tax accounting purposes: COGS determination Agency, conduit, reimbursements Open regulatory and policy questions Computational issues and interplay with other provisions: Interplay with GILTI, FTC, taxable income, Sec. 163(j), etc. 34

35 Cost of Goods Sold and Related Issues Tax character of intercompany payments is critical Payments giving rise to deductions vs. reductions in gross receipts to arrive at gross income (i.e., amounts capitalized into inventory for US Federal tax purposes) Scope of Section 263A: Producers and resellers Treatment of sales based royalties Manufacturing service (tolling) and other direct and indirect costs Consideration of accounting method change Interplay with transfer pricing and customs valuation provisions 35

36 Characterization of transaction is critical If the payment gives rise to a deduction for the U.S. taxpayer, then the payment could be a base erosion payment. If, however, the payment is not a deduction, but a pass through amount, then there is no base erosion payment Generally, a taxpayer who receives income under a claim of right that is free of restrictions must include that item into gross income in the current year However, some amounts received on behalf of another as an agent, a conduit, a reimbursement, or pursuant to a revenue sharing agreement may not give rise to income and deductions and be instead reported net Generally, the character of a payment for US Federal income tax purposes is determined based on the economic substance of the underlying contractual relationship between the relevant parties 36

37 Service Cost Method Exception Exception for services eligible under the Services Cost Method (Treas. Reg. sec ) Specified covered services (Rev. Proc ) Low-margin services Excluded services Top of mind issues: What if a markup on eligible service costs is charged? What if a foreign tax authority requires certain markup? How is markup charged / booked / invoiced? 37

38 Service Cost Method Exception Exception for services eligible under the Services Cost Method (Treas. Reg. sec ) Specified covered services (Rev. Proc ) Low-margin services Excluded services Top of mind issues: What if a markup on eligible service costs is charged? What if a foreign tax authority requires certain markup? How is markup charged / booked / invoiced? 38

39 Impact of NOLs In calculating modified taxable income, taxpayer adds back 'the base erosion percentage of any net operating loss deduction allowed under Section 172 for the taxable year. Is the base erosion percentage calculated based on the year the NOL is utilized or the year the NOL arose? How is the calculation impacted if NOL carryforwards exceed current year taxable income? Is the starting point for calculating modified taxable income zero? What if the NOL relates to years prior to the effective date of BEAT? What if the NOL relates to a year when the company was not an applicable taxpayer? 39

40 Case Study: Illustrative Structure BEAT Implications CFC 1 Non-U.S. Principal (Country A) (10% tax rate) CSA IP U.S. Multinational Corporation IP Contract R&D Services CFC 3 (Country C) (33% tax rate) Outbound payments to CFC1 (for I/C services performed by Non-U.S. Principal) and CFC3 (for contract R&D Services) would be considered Base Erosion Payments BEAT only applies if a taxpayer s total Base Erosion Tax Benefits (including a taxpayer s Base Erosion Payments) exceed 3% of all deductions for the year 40

41 Adapting to the Evolving Global Tax Environment US Tax Reform State Aid Increasing Global Transparency (e.g. DAC6) Unilateral Actions Global Tax Environment EU GAAR ATAD I&II Increased Pressure on Debt Planning Increased Information Reporting & Transparency BEPS Expansion of Hybrid Rules 41

42 Case Study Revisited U.S. Multinational Corporation IP Contract R&D Services U.S. Multinational Customers Cost Sharing Agreement Customer Sub (Country A) CFC 1 Non-U.S. Principal (Country A) (10% tax rate) IP Royalty and/or Services fees CFC 2 (Country B) (25% tax rate) CFC 3 (Country C) (33% tax rate) Key: Payment Flows Services Other Customers (Country B) 42

43 43

Comparison of Key Anti-Base Erosion Rules in the Tax Reform Act of 2017 and under UK Tax Law Calum Dewar, PwC Mike Williams, HM Treasury

Comparison of Key Anti-Base Erosion Rules in the Tax Reform Act of 2017 and under UK Tax Law Calum Dewar, PwC Mike Williams, HM Treasury International Tax Policy Forum and Institute of Economic Law Conference

Comparison of Key Anti-Base Erosion Rules in the Tax Reform Act of 2017 and under UK Tax Law Calum Dewar, PwC Mike Williams, HM Treasury International Tax Policy Forum and Institute of Economic Law Conference

International Tax Reform. March 19, 2018 Nicole R. Suk, CPA

International Tax Reform March 19, 2018 Nicole R. Suk, CPA Why International Reform? Shift to territorial system Protect the U.S. tax base from perceived crossborder erosion Incentive for economic investment

International Tax Reform March 19, 2018 Nicole R. Suk, CPA Why International Reform? Shift to territorial system Protect the U.S. tax base from perceived crossborder erosion Incentive for economic investment

International Tax: Tax Reform

International Tax: Tax Reform Joseph Calianno Partner and International Technical Tax Practice Leader Ben Vesely International Tax Senior Manager The below summary contains a high level overview of certain

International Tax: Tax Reform Joseph Calianno Partner and International Technical Tax Practice Leader Ben Vesely International Tax Senior Manager The below summary contains a high level overview of certain

CONFERENCE AGREEMENT PROPOSAL INTERNATIONAL

The following chart sets forth some of the international tax provisions in the Conference Agreement version of the Tax Cuts and Jobs Act, as made available on December 15, 2017. This chart highlights only

The following chart sets forth some of the international tax provisions in the Conference Agreement version of the Tax Cuts and Jobs Act, as made available on December 15, 2017. This chart highlights only

Comprehensive Reform of the U.S. International Tax System The NY State Bar Association Tax Section Annual Meeting

Comprehensive Reform of the U.S. International Tax System The NY State Bar Association Tax Section Annual Meeting Chair: Kathleen L. Ferrell, Davis Polk & Wardwell LLP Michael J. Caballero, Covington &

Comprehensive Reform of the U.S. International Tax System The NY State Bar Association Tax Section Annual Meeting Chair: Kathleen L. Ferrell, Davis Polk & Wardwell LLP Michael J. Caballero, Covington &

Tax Reform: Knowns and Unknowns. Tax Executive Institute Houston, Texas. February 26, 2018

Tax Reform: Knowns and Unknowns Tax Executive Institute Houston, Texas. February 26, 2018 Section 163(j) Overview of New U.S. Interest Expense Limitation Limits deductibility on net business interest expense

Tax Reform: Knowns and Unknowns Tax Executive Institute Houston, Texas. February 26, 2018 Section 163(j) Overview of New U.S. Interest Expense Limitation Limits deductibility on net business interest expense

Tax Reform: Impact of International Provisions on Insurance Companies

Tax Reform: Impact of International Provisions on Insurance Companies 2018 Mid Year ABA Tax Section Meeting, Insurance Companies February 9, 2018, 3:30 4:30 p.m. Moderator: Clarissa Potter, KPMG, New York,

Tax Reform: Impact of International Provisions on Insurance Companies 2018 Mid Year ABA Tax Section Meeting, Insurance Companies February 9, 2018, 3:30 4:30 p.m. Moderator: Clarissa Potter, KPMG, New York,

Basics of International Tax Planning with Tax Reform

Basics of International Tax Planning with Tax Reform Layla Asali & Andy Howlett TEI Houston Tax School 2018 February 28, 2018 Agenda U.S. International Tax System Overview Deemed Repatriation Global Intangible

Basics of International Tax Planning with Tax Reform Layla Asali & Andy Howlett TEI Houston Tax School 2018 February 28, 2018 Agenda U.S. International Tax System Overview Deemed Repatriation Global Intangible

International Tax & the TCJA for Strategic Alliance Firms

International Tax & the TCJA for Strategic Alliance Firms MAY 22, 2018 TO RECEIVE CPE CREDIT Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader is the person

International Tax & the TCJA for Strategic Alliance Firms MAY 22, 2018 TO RECEIVE CPE CREDIT Individuals Participate in entire webinar Answer polls when they are provided Groups Group leader is the person

From the Deferral Frying Pan into the Worldwide Fire Rethinking CFC Taxation

From the Deferral Frying Pan into the Worldwide Fire Rethinking CFC Taxation 2018 U.S. Cross-Border Tax Conference May 15 17, 2018 kpmg.com Notices The following information is not intended to be written

From the Deferral Frying Pan into the Worldwide Fire Rethinking CFC Taxation 2018 U.S. Cross-Border Tax Conference May 15 17, 2018 kpmg.com Notices The following information is not intended to be written

Changes Abound in New Tax Bill for Multinational Companies

News Changes Abound in New Tax Bill for Multinational Companies 01.08.2018 Perhaps some of the most extensive changes in H.R. 1, known as the Tax Cuts and Jobs Act (the Act ), deal with the taxation of

News Changes Abound in New Tax Bill for Multinational Companies 01.08.2018 Perhaps some of the most extensive changes in H.R. 1, known as the Tax Cuts and Jobs Act (the Act ), deal with the taxation of

Tax Reform Issues Related to Group Financing - 163j, 267A, BEAT and GILTI Issues International Tax Institute, Inc. June 11, 2018

Tax Reform Issues Related to Group Financing - 163j, 267A, BEAT and GILTI Issues International Tax Institute, Inc. June 11, 2018 James Tobin, Ernst & Young LLP Kevin Glenn, King & Spalding LLP TCJA International

Tax Reform Issues Related to Group Financing - 163j, 267A, BEAT and GILTI Issues International Tax Institute, Inc. June 11, 2018 James Tobin, Ernst & Young LLP Kevin Glenn, King & Spalding LLP TCJA International

Transition Tax DEEMED REPATRIATION OVERVIEW

Transition Tax DEEMED REPATRIATION OVERVIEW Basic Framework A 10% U.S. shareholder (a US SH ) of a specified foreign corporation ( SFC ) must recognize its pro rata share of the SFC s post-1986 accumulated

Transition Tax DEEMED REPATRIATION OVERVIEW Basic Framework A 10% U.S. shareholder (a US SH ) of a specified foreign corporation ( SFC ) must recognize its pro rata share of the SFC s post-1986 accumulated

International Tax Reform - Practical Impacts and Considerations. 30 November 2017

International Tax Reform - Practical Impacts and Considerations 30 November 2017 Agenda Transition tax Territorial system Limitation on deductions of net interest Foreign high return amount / Global intangible

International Tax Reform - Practical Impacts and Considerations 30 November 2017 Agenda Transition tax Territorial system Limitation on deductions of net interest Foreign high return amount / Global intangible

US Tax Reform Update. 30 January 2018

US Tax Reform Update Introduction Aaron Topol Partner and Leader EY Asia-Pacific Tax Desk (US) Hong Kong Ernst & Young Tax Services Limited Robert King Partner and Leader Business Tax Advisory Vietnam

US Tax Reform Update Introduction Aaron Topol Partner and Leader EY Asia-Pacific Tax Desk (US) Hong Kong Ernst & Young Tax Services Limited Robert King Partner and Leader Business Tax Advisory Vietnam

Tax Executives Institute Houston Chapter. Consolidated Return Updates

www.pwc.com Tax Executives Institute Houston Chapter Consolidated Return Updates February 28, 2018 Presenters Pavi Mani Partner, Email: pavithra.mani@pwc.com Phone: (713) 356-4040 Pavi is a Partner in

www.pwc.com Tax Executives Institute Houston Chapter Consolidated Return Updates February 28, 2018 Presenters Pavi Mani Partner, Email: pavithra.mani@pwc.com Phone: (713) 356-4040 Pavi is a Partner in

A Transfer Pricing Update BEPS & U.S. Tax Reform

A Transfer Pricing Update BEPS & U.S. Tax Reform JANUARY 17, 2018 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in a group Complete

A Transfer Pricing Update BEPS & U.S. Tax Reform JANUARY 17, 2018 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in a group Complete

U.S. tax reforms prevention of base erosion. S. Krishnan

U.S. tax reforms prevention of base erosion S. Krishnan 2 U.S. tax regime prior to 2018 Amongst the large economies in the world, the United States had the highest statutory corporate income tax rate upwards

U.S. tax reforms prevention of base erosion S. Krishnan 2 U.S. tax regime prior to 2018 Amongst the large economies in the world, the United States had the highest statutory corporate income tax rate upwards

Foreign Derived Intangible Income ( FDII ) Provision Mechanics, Issues, and Potential WTO or Other Challenges. November 2, 2018

Provision Mechanics, Issues, and Potential WTO or Other Challenges. November 2, 2018") Foreign Derived Intangible Income ( FDII ) Provision Mechanics, Issues, and Potential WTO or Other Challenges November 2, 2018 Panelists Hal Hicks, Partner, Skadden, Arps, Slate, Meagher & Flom LLP, Washington,

Foreign Derived Intangible Income ( FDII ) Provision Mechanics, Issues, and Potential WTO or Other Challenges November 2, 2018 Panelists Hal Hicks, Partner, Skadden, Arps, Slate, Meagher & Flom LLP, Washington,

Tax Reform Implementation. American Bar Association Section of Taxation May 11, 2018

Tax Reform Implementation American Bar Association Section of Taxation May 11, 2018 Presenters Pete Bautz, American Council of Life Insurers Howard Stecker, EY Brenda Viehe Naess, Washington Advocates

Tax Reform Implementation American Bar Association Section of Taxation May 11, 2018 Presenters Pete Bautz, American Council of Life Insurers Howard Stecker, EY Brenda Viehe Naess, Washington Advocates

Tax Reform and U.S. Foreign Reporting for Individuals: New Cross-Border Repatriation and Inclusion Provisions

Tax Reform and U.S. Foreign Reporting for Individuals: FOR LIVE PROGRAM ONLY New Cross-Border Repatriation and Inclusion Provisions THURSDAY, FEBRUARY 15, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Tax Reform and U.S. Foreign Reporting for Individuals: FOR LIVE PROGRAM ONLY New Cross-Border Repatriation and Inclusion Provisions THURSDAY, FEBRUARY 15, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

62 ASSOCIATION OF CORPORATE COUNSEL

62 ASSOCIATION OF CORPORATE COUNSEL CHEAT SHEET Foreign corporate earnings. Under the recently created Tax Cuts and Jobs Act, taxation and participation exemption of foreign corporate earnings have significantly

62 ASSOCIATION OF CORPORATE COUNSEL CHEAT SHEET Foreign corporate earnings. Under the recently created Tax Cuts and Jobs Act, taxation and participation exemption of foreign corporate earnings have significantly

Tax Cuts & Jobs Act: Considerations for Multinationals

ALE R T MEM ORAN D UM Tax Cuts & Jobs Act: Considerations for Multinationals February 5, 2018 On December 22, 2017, the President signed into law the 2017 U.S. tax reform bill formerly known as the Tax

ALE R T MEM ORAN D UM Tax Cuts & Jobs Act: Considerations for Multinationals February 5, 2018 On December 22, 2017, the President signed into law the 2017 U.S. tax reform bill formerly known as the Tax

General Feedback for Issues Requiring Regulatory Attention as of 3/7/2018

General Feedback for Issues Requiring Regulatory Attention as of 3/7/2018 This document covers the following issue areas: Individual Tax Reform - Treatment Of Business Income Business Tax Reform Cost Recovery

General Feedback for Issues Requiring Regulatory Attention as of 3/7/2018 This document covers the following issue areas: Individual Tax Reform - Treatment Of Business Income Business Tax Reform Cost Recovery

General Feedback for Issues Requiring Regulatory Attention as of 3/7/18

General Feedback for Issues Requiring Regulatory Attention as of 3/7/18 This document covers the following issue areas: Individual Tax Reform - Treatment Of Business Income Business Tax Reform Cost Recovery

General Feedback for Issues Requiring Regulatory Attention as of 3/7/18 This document covers the following issue areas: Individual Tax Reform - Treatment Of Business Income Business Tax Reform Cost Recovery

New Tax Law: International

New Tax Law: International Provisions and Observations April 18, 2018 kpmg.com 1 In the context of international tax, the Public Law 115-97 (popularly, if not officially, referred to as the Tax Cuts and

New Tax Law: International Provisions and Observations April 18, 2018 kpmg.com 1 In the context of international tax, the Public Law 115-97 (popularly, if not officially, referred to as the Tax Cuts and

US Tax Reform For Canadian Companies

For Canadian Companies 1 Agenda Domestic Changes Income Tax Rate Reduction Update for Certain Deductions NOL, Interest, Depreciation, DPAD (Section 199) Credits and Incentives International Changes Migration

For Canadian Companies 1 Agenda Domestic Changes Income Tax Rate Reduction Update for Certain Deductions NOL, Interest, Depreciation, DPAD (Section 199) Credits and Incentives International Changes Migration

International tax update. 1 May 2018

International tax update 1 May 2018 Disclaimer EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal

International tax update 1 May 2018 Disclaimer EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal

Trade Update: The Impact of U.S. Tax Reform

Trade Update: The Impact of U.S. Tax Reform 2018 U.S. Cross-Border Tax Conference May 15 17, 2018 kpmg.com Notices The following information is not intended to be written advice concerning one or more

Trade Update: The Impact of U.S. Tax Reform 2018 U.S. Cross-Border Tax Conference May 15 17, 2018 kpmg.com Notices The following information is not intended to be written advice concerning one or more

taxnotes U.S. Tax Reform Considera ons for Mul na onal Services Companies international by Thomas Zollo, Mike Moore, Anjit Bajwa, and Tom Chamberlin

taxnotes U.S. Tax Reform Considera ons for Mul na onal Services Companies by Thomas Zollo, Mike Moore, Anjit Bajwa, and Tom Chamberlin Reprinted from Tax Notes Interna onal, April 30, 2018, p. 627 international

taxnotes U.S. Tax Reform Considera ons for Mul na onal Services Companies by Thomas Zollo, Mike Moore, Anjit Bajwa, and Tom Chamberlin Reprinted from Tax Notes Interna onal, April 30, 2018, p. 627 international

International Tax & the TCJA

International Tax & the TCJA FEBRUARY 22, 2018 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in a group Complete group attendance

International Tax & the TCJA FEBRUARY 22, 2018 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in a group Complete group attendance

Tax reform readiness: The FTC regulations Credit given (maybe) where credit is due

where credit is due") from International Tax Services Tax reform readiness: The FTC regulations Credit given (maybe) where credit is due December 17, 2018 In brief The 2017 tax reform act (the Act) amended several Code provisions

from International Tax Services Tax reform readiness: The FTC regulations Credit given (maybe) where credit is due December 17, 2018 In brief The 2017 tax reform act (the Act) amended several Code provisions

Tax Cuts and Jobs Act of 2017 International Tax Provisions and Provisions Affecting Exempt Organizations

Tax Cuts and Jobs Act of 2017 International Tax Provisions and Provisions Affecting Exempt Organizations By Robert E. Ward* Robert E. Ward outlines the international tax provisions and provisions affecting

Tax Cuts and Jobs Act of 2017 International Tax Provisions and Provisions Affecting Exempt Organizations By Robert E. Ward* Robert E. Ward outlines the international tax provisions and provisions affecting

Tax Cuts & Jobs Act: Considerations for Funds

A LERT M EM OR A N D UM Tax Cuts & Jobs Act: Considerations for Funds January 25, 2018 On December 22, 2017, the President signed into law the 2017 U.S. tax reform bill formerly known as the Tax Cuts &

A LERT M EM OR A N D UM Tax Cuts & Jobs Act: Considerations for Funds January 25, 2018 On December 22, 2017, the President signed into law the 2017 U.S. tax reform bill formerly known as the Tax Cuts &

Tax Cuts & Jobs Act: Considerations for M&A

A LERT M EM OR A N D UM Tax Cuts & Jobs Act: Considerations for M&A January 17, 2018 On December 22, 2017, the President signed into law the 2017 U.S. tax reform bill formerly known as the Tax Cuts & Jobs

A LERT M EM OR A N D UM Tax Cuts & Jobs Act: Considerations for M&A January 17, 2018 On December 22, 2017, the President signed into law the 2017 U.S. tax reform bill formerly known as the Tax Cuts & Jobs

U.S. Tax Legislation Corporate and International Provisions. Corporate Law Provisions

U.S. Tax Legislation Corporate and International Provisions On December 20, 2017, Congress enacted comprehensive tax legislation (the Act ). This memorandum highlights some of the important provisions

U.S. Tax Legislation Corporate and International Provisions On December 20, 2017, Congress enacted comprehensive tax legislation (the Act ). This memorandum highlights some of the important provisions

U.S. Tax Reform. 33 rd Annual TEI-SJSU High Tech Tax Institute November 14, 2017

U.S. Tax Reform 33 rd Annual TEI-SJSU High Tech Tax Institute November 14, 2017 David Forst, Partner Fenwick & West LLP Nathan Giesselman, Partner Skadden, Arps, Slate, Meagher & Flom LLP Sajeev Sidher,

U.S. Tax Reform 33 rd Annual TEI-SJSU High Tech Tax Institute November 14, 2017 David Forst, Partner Fenwick & West LLP Nathan Giesselman, Partner Skadden, Arps, Slate, Meagher & Flom LLP Sajeev Sidher,

Directors Club. March 13, 2018

Directors Club March 13, 2018 1 The Tax Wars 2 Business tax highlights of tax reform bills Reduction of corporate tax rate: Permanently reduces the 35% corporate income tax rate to a flat 21%, beginning

Directors Club March 13, 2018 1 The Tax Wars 2 Business tax highlights of tax reform bills Reduction of corporate tax rate: Permanently reduces the 35% corporate income tax rate to a flat 21%, beginning

Inbound and Outbound International Tax Rules

Inbound and Outbound International Tax Rules PRESENTED BY: TRACY MONROE, CPA, MT, PARTNER RAY POLANTZ, CPA, MT, PARTNER CYNTHIA PEDERSEN, JD, LLM, TAX MANAGER July 31, 2018 Welcome & Introductions Tracy

Inbound and Outbound International Tax Rules PRESENTED BY: TRACY MONROE, CPA, MT, PARTNER RAY POLANTZ, CPA, MT, PARTNER CYNTHIA PEDERSEN, JD, LLM, TAX MANAGER July 31, 2018 Welcome & Introductions Tracy

US tax reform: A sea change for international taxation The Dbriefs Tax Reform series

US tax reform: A sea change for international taxation The Dbriefs Tax Reform series Todd Izzo, Partner, Deloitte Tax LLP Rochelle Kleczynski, Partner, Deloitte Tax LLP Chris Trump, Principal, Deloitte

US tax reform: A sea change for international taxation The Dbriefs Tax Reform series Todd Izzo, Partner, Deloitte Tax LLP Rochelle Kleczynski, Partner, Deloitte Tax LLP Chris Trump, Principal, Deloitte

NAVIGATING US TAX REFORM:

NAVIGATING US TAX REFORM: What Businesses Need to Know March 20, 2018 2018 Morgan, Lewis & Bockius LLP Agenda Topic Slides Overview...3 Domestic Provisions...4-13 International Provisions...14-29 Immediate

NAVIGATING US TAX REFORM: What Businesses Need to Know March 20, 2018 2018 Morgan, Lewis & Bockius LLP Agenda Topic Slides Overview...3 Domestic Provisions...4-13 International Provisions...14-29 Immediate

U.S. Tax Reform International Corporate Tax Provisions: The Good, the Bad and the Extremely Complex

U.S. Tax Reform International Corporate Tax Provisions: The Good, the Bad and the Extremely Complex On December 22, 2017, President Trump signed into law the 2017 U.S. tax reform bill An Act to provide

U.S. Tax Reform International Corporate Tax Provisions: The Good, the Bad and the Extremely Complex On December 22, 2017, President Trump signed into law the 2017 U.S. tax reform bill An Act to provide

U.S. Tax Reform: Impact on Inbound Groups and subsidiaries of US groups. Insights and Practical Considerations. Julio Castro

U.S. Tax Reform: Impact on Inbound Groups and subsidiaries of US groups Insights and Practical Considerations Julio Castro February 2018 Notice The following information is not intended to be written advice

U.S. Tax Reform: Impact on Inbound Groups and subsidiaries of US groups Insights and Practical Considerations Julio Castro February 2018 Notice The following information is not intended to be written advice

Following the BEAT: IRS Issues Proposed Regulations on Application of Base Erosion and Anti-Abuse Tax

Latham & Watkins Transactional Tax Practice January 14, 2019 Number 2433 Following the BEAT: IRS Issues Proposed Regulations on Application of Base Erosion and Anti-Abuse Tax The proposed regulations provide

Latham & Watkins Transactional Tax Practice January 14, 2019 Number 2433 Following the BEAT: IRS Issues Proposed Regulations on Application of Base Erosion and Anti-Abuse Tax The proposed regulations provide

U.S. Tax Reform. Webinar for Australian MNC & Institutional Investors. Carol Kulish, Justin Davis, Patrick Jackman and Peter Madden.

U.S. Tax Reform Webinar for Australian MNC & Institutional Investors Carol Kulish, Justin Davis, Patrick Jackman and Peter Madden December 2017 With us today Patrick Jackman US - Washington National Tax

U.S. Tax Reform Webinar for Australian MNC & Institutional Investors Carol Kulish, Justin Davis, Patrick Jackman and Peter Madden December 2017 With us today Patrick Jackman US - Washington National Tax

Silicon Valley Chapter

Silicon Valley Chapter Subpart F: Legislative Update Review and Planning Strategies March 23, 2017 Biltmore Hotel & Suites, Santa Clara Lowell D. Yoder lyoder@mwe.com Tax Reform Proposals President Trump

Silicon Valley Chapter Subpart F: Legislative Update Review and Planning Strategies March 23, 2017 Biltmore Hotel & Suites, Santa Clara Lowell D. Yoder lyoder@mwe.com Tax Reform Proposals President Trump

International Tax: Strategies for cross-border investing after tax reform

International Tax: Strategies for cross-border investing after tax reform Today s Presenters Brittain Cunningham, CPA Senior Manager, International Tax Services brittain.cunningham@weaver.com 832.320.3461

International Tax: Strategies for cross-border investing after tax reform Today s Presenters Brittain Cunningham, CPA Senior Manager, International Tax Services brittain.cunningham@weaver.com 832.320.3461

Planning with the New FTC Baskets

Planning with the New FTC Baskets 2018 U.S. Cross-Border Tax Conference May 15 17, 2018 kpmg.com Agenda 01 Significant Tax Reform changes to FTC rules - New FTC baskets and FTC limitation - Deemed paid

Planning with the New FTC Baskets 2018 U.S. Cross-Border Tax Conference May 15 17, 2018 kpmg.com Agenda 01 Significant Tax Reform changes to FTC rules - New FTC baskets and FTC limitation - Deemed paid

U.S. Tax Reform Key International Aspects

U.S. Tax Reform Key International Aspects Daniel W. Blum IFA Event US Tax Reform Vienna, March 5 th, 2018 U.S. Tax Reform: Overview Jobs and Tax Cuts Act signed on Dec 22, 2017 Largest overhaul of the

U.S. Tax Reform Key International Aspects Daniel W. Blum IFA Event US Tax Reform Vienna, March 5 th, 2018 U.S. Tax Reform: Overview Jobs and Tax Cuts Act signed on Dec 22, 2017 Largest overhaul of the

Please any questions for Robert to: Thank you.

EXPLORING THE NEW TERRITORIAL TAX SYSTEM PORTLAND TAX FORUM SHORT TOPIC PRESENTATION JANUARY 18, 2018 ROBERT J. WOLFER, CPA Robert is a Senior Tax Manager with DiLorenzo & Company, LLC, where his duties

EXPLORING THE NEW TERRITORIAL TAX SYSTEM PORTLAND TAX FORUM SHORT TOPIC PRESENTATION JANUARY 18, 2018 ROBERT J. WOLFER, CPA Robert is a Senior Tax Manager with DiLorenzo & Company, LLC, where his duties

TEI How to tackle Tax Reform and its impact on Tax Departments going forward

www.pwc.com TEI How to tackle Tax Reform and its impact on Tax Departments going forward Monday, February 26, 2018 Agenda Introduction What Tax Reform questions do shareholders, investors and analysts

www.pwc.com TEI How to tackle Tax Reform and its impact on Tax Departments going forward Monday, February 26, 2018 Agenda Introduction What Tax Reform questions do shareholders, investors and analysts

Intellectual property in the age of BEPS

Intellectual property in the age of BEPS Tax Executives Institute Michigan Chapter Detroit 28 October 2015 Disclaimer EY refers to the global organization, and may refer to one or more, of the member firms

Intellectual property in the age of BEPS Tax Executives Institute Michigan Chapter Detroit 28 October 2015 Disclaimer EY refers to the global organization, and may refer to one or more, of the member firms

Transition Tax and Notice Foreign Tax Credits BEAT Interactions

Transition Tax and Notice 2018-26 Foreign Tax Credits BEAT Interactions Steve Blore Greg Kernek Deloitte Tax LLP May 11, 2018 Transition Tax and Anti-Avoidance Copyright 2018 Deloitte Development LLC.

Transition Tax and Notice 2018-26 Foreign Tax Credits BEAT Interactions Steve Blore Greg Kernek Deloitte Tax LLP May 11, 2018 Transition Tax and Anti-Avoidance Copyright 2018 Deloitte Development LLC.

House and Senate tax reform proposals could significantly impact US international tax rules

from International Tax Services House and Senate tax reform proposals could significantly impact US international tax rules November 28, 2017 In brief The House of Representatives passed the Tax Cuts and

from International Tax Services House and Senate tax reform proposals could significantly impact US international tax rules November 28, 2017 In brief The House of Representatives passed the Tax Cuts and

International tax implications of US tax reform

Arm s Length Standard Global views within reach. International tax implications of US tax reform Congress has approved and President Trump has signed into law a massive tax reform package that lowers tax

Arm s Length Standard Global views within reach. International tax implications of US tax reform Congress has approved and President Trump has signed into law a massive tax reform package that lowers tax

THE FUTURE OF TAX PLANNING: TRANSPARENCY AND SUBSTANCE FOR ALL? Friday, 26 February AM PM Conrad Hotel, Hong Kong

THE FUTURE OF TAX PLANNING: TRANSPARENCY AND SUBSTANCE FOR ALL? Friday, 26 February 2016 9.00AM - 12.00PM Conrad Hotel, Hong Kong THE DRIVE TOWARDS TRANSPARENCY: CHALLENGES AND OPPORTUNITIES IN INTERNATIONAL

THE FUTURE OF TAX PLANNING: TRANSPARENCY AND SUBSTANCE FOR ALL? Friday, 26 February 2016 9.00AM - 12.00PM Conrad Hotel, Hong Kong THE DRIVE TOWARDS TRANSPARENCY: CHALLENGES AND OPPORTUNITIES IN INTERNATIONAL

SENATE TAX REFORM PROPOSAL INTERNATIONAL

The following chart sets forth some of the international tax provisions in the Senate Finance Committee s version of the Tax Cuts and Jobs Act bill, as approved by the Senate Finance Committee on November

The following chart sets forth some of the international tax provisions in the Senate Finance Committee s version of the Tax Cuts and Jobs Act bill, as approved by the Senate Finance Committee on November

2017 Tax Reform: Checkpoint Special Study on foreign income, foreign persons tax changes in the "Tax Cuts and Jobs Act"

2017 Tax Reform: Checkpoint Special Study on foreign income, foreign persons tax changes in the "Tax Cuts and Jobs Act" On December 15, the Conference Committee-having reconciled and merged the differing

2017 Tax Reform: Checkpoint Special Study on foreign income, foreign persons tax changes in the "Tax Cuts and Jobs Act" On December 15, the Conference Committee-having reconciled and merged the differing

US Tax reform. Client event. 6 February 2018

Tax reform Client event 6 February 2018 1 Business tax highlights of tax reform bills Reduction of corporate tax rate: Permanently reduces the 35% corporate income tax rate to a flat 21%, beginning in

Tax reform Client event 6 February 2018 1 Business tax highlights of tax reform bills Reduction of corporate tax rate: Permanently reduces the 35% corporate income tax rate to a flat 21%, beginning in

Summary of Key Business Reforms

Tax Strategy & Benefits May Newsletter Reflections On US Tax Reform Near the end of 2017, the US Congress and the Trump Administration enacted the most comprehensive reforms of the US federal tax system

Tax Strategy & Benefits May Newsletter Reflections On US Tax Reform Near the end of 2017, the US Congress and the Trump Administration enacted the most comprehensive reforms of the US federal tax system

KPMG report: Analysis and observations about BEAT proposed regulations

KPMG report: Analysis and observations about BEAT proposed regulations December 17, 2018 kpmg.com 1 Contents Effective dates and reliance... 2 Comment period and hearing... 2 Background... 2 Overview...

KPMG report: Analysis and observations about BEAT proposed regulations December 17, 2018 kpmg.com 1 Contents Effective dates and reliance... 2 Comment period and hearing... 2 Background... 2 Overview...

SENATE TAX REFORM PROPOSAL INTERNATIONAL

The following chart sets forth some of the international tax provisions in the Senate s version of the Tax Cuts and Jobs Act, as approved by the Senate on December 2, 2017. This chart highlights only some

The following chart sets forth some of the international tax provisions in the Senate s version of the Tax Cuts and Jobs Act, as approved by the Senate on December 2, 2017. This chart highlights only some

Tax Cuts & Jobs Act: The Road to Reform Reform Results of Reform

Tax Cuts & Jobs Act: The Road to Reform Reform Results of Reform Mindy Herzfeld University of Florida Levin College of Law UF Law Summer Tax Course July 23, 2018 7/17/2018 1 30 Years in the Making The

Tax Cuts & Jobs Act: The Road to Reform Reform Results of Reform Mindy Herzfeld University of Florida Levin College of Law UF Law Summer Tax Course July 23, 2018 7/17/2018 1 30 Years in the Making The

U.S. Tax Reform: The Big Shake-Up In International Tax Law

Abbott, Stringham & Lynch Tax Group U.S. Tax Reform: The Big Shake-Up In International Tax Law Presented by: Presented by: [Date] Jyothi Chillara, CPA and Erika Diebert, CPA February 1, 2018 Upcoming Webinars

Abbott, Stringham & Lynch Tax Group U.S. Tax Reform: The Big Shake-Up In International Tax Law Presented by: Presented by: [Date] Jyothi Chillara, CPA and Erika Diebert, CPA February 1, 2018 Upcoming Webinars

Multinational Financial Groups After the U.S. Tax Reform: Selected Inbound and Outbound Issues

Multinational Financial Groups After the U.S. Tax Reform: Selected Inbound and Outbound Issues NICHOLAS J. DENOVIO is a Global Chair, International Tax Practice and Partner in the Washington D.C. office

Multinational Financial Groups After the U.S. Tax Reform: Selected Inbound and Outbound Issues NICHOLAS J. DENOVIO is a Global Chair, International Tax Practice and Partner in the Washington D.C. office

International Tax Update. Friday, December 1, 2017 Grant Thornton's Year End taxguide Event Brandon Joseph Senior Manager, International Tax

International Tax Update Friday, December 1, 2017 Grant Thornton's Year End taxguide Event Brandon Joseph Senior Manager, International Tax Presenters Brandon Joseph Senior Manager International Tax Services

International Tax Update Friday, December 1, 2017 Grant Thornton's Year End taxguide Event Brandon Joseph Senior Manager, International Tax Presenters Brandon Joseph Senior Manager International Tax Services

TAX CUTS AND JOBS ACT: FIRST U.S. TAX REFORM FOR 30 YEARS ERSTE U.S. STEUERREFORM SEIT 30 JAHREN TRITT IN KRAFT

TAX CUTS AND JOBS ACT: FIRST U.S. TAX REFORM FOR 30 YEARS ERSTE U.S. STEUERREFORM SEIT 30 JAHREN TRITT IN KRAFT January 17, 2018 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member

TAX CUTS AND JOBS ACT: FIRST U.S. TAX REFORM FOR 30 YEARS ERSTE U.S. STEUERREFORM SEIT 30 JAHREN TRITT IN KRAFT January 17, 2018 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member

INSIGHT: Fundamentals of Tax Reform: GILTI

Reproduced with permission from Daily Tax Report, 223 DTR 8, 11/16/2018. Copyright 2018 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com INSIGHT: Fundamentals of Tax Reform: GILTI

Reproduced with permission from Daily Tax Report, 223 DTR 8, 11/16/2018. Copyright 2018 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com INSIGHT: Fundamentals of Tax Reform: GILTI

Tax Reform: Taxation of Income of Controlled Foreign Corporations

Reproduced with permission from Daily Tax Report, 14 DTR S-15, 1/22/18. Copyright 2018 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com CFCs Lowell D. Yoder, David G. Noren, and

Reproduced with permission from Daily Tax Report, 14 DTR S-15, 1/22/18. Copyright 2018 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com CFCs Lowell D. Yoder, David G. Noren, and

UNDERSTANDING THE NEW BEAT TAX

TEI HOUSTON CHAPTER: FEDERAL UPDATE UNDERSTANDING THE NEW BEAT TAX F. SCOTT FARMER PETER M. DAUB MORGAN LEWIS FEBRUARY 26, 2018 BEAT -- General Rules Base erosion anti-abuse tax ( BEAT, Code Section 59A)

TEI HOUSTON CHAPTER: FEDERAL UPDATE UNDERSTANDING THE NEW BEAT TAX F. SCOTT FARMER PETER M. DAUB MORGAN LEWIS FEBRUARY 26, 2018 BEAT -- General Rules Base erosion anti-abuse tax ( BEAT, Code Section 59A)

Presented to: NRF Canadian Tax Clients. New U.S. tax legislation Impact on Selected Cross-Border Transactions

January 11, 2018 Presented to: NRF Canadian Tax Clients New U.S. tax legislation Impact on Selected Cross-Border Transactions Adrienne Oliver Tel: (416) 216-1854 email: adrienne.oliver@nortonrosefulbright.com

January 11, 2018 Presented to: NRF Canadian Tax Clients New U.S. tax legislation Impact on Selected Cross-Border Transactions Adrienne Oliver Tel: (416) 216-1854 email: adrienne.oliver@nortonrosefulbright.com

La Riforma Fiscale negli USA EVOLUZIONE DELLE PROSPETTIVE ECONOMICHE E DELLE RELAZIONI FISCALI PER LE IMPRESE CONFINDUSTRIA ROMA, 29 GENNAIO 2018

La Riforma Fiscale negli USA EVOLUZIONE DELLE PROSPETTIVE ECONOMICHE E DELLE RELAZIONI FISCALI PER LE IMPRESE CONFINDUSTRIA ROMA, 29 GENNAIO 2018 Going back a few years Economic and Financial Crisis =

La Riforma Fiscale negli USA EVOLUZIONE DELLE PROSPETTIVE ECONOMICHE E DELLE RELAZIONI FISCALI PER LE IMPRESE CONFINDUSTRIA ROMA, 29 GENNAIO 2018 Going back a few years Economic and Financial Crisis =

20 Tax Executives Institute

20 www.tei.org Tax Executives Institute COVER Tax-Efficient Supply Chain in Shadow of Tax Reform GILTI, FDII, and BEAT: they re not just acronyms they require reassessing tax consequences of existing supply

20 www.tei.org Tax Executives Institute COVER Tax-Efficient Supply Chain in Shadow of Tax Reform GILTI, FDII, and BEAT: they re not just acronyms they require reassessing tax consequences of existing supply

2/2/2018. Part I: Inbound Base Erosion Provision in socalled Tax Cut and Jobs Act. Inbound Planning & Developments

Inbound Planning & Developments Inbound International Tax Issues with a Focus on Tax Reform 2017 PLI, New York February 6, 2018 Peter Glicklich Davies Ward Phillips & Vineberg LLP Oren Penn PricewaterhouseCoopers

Inbound Planning & Developments Inbound International Tax Issues with a Focus on Tax Reform 2017 PLI, New York February 6, 2018 Peter Glicklich Davies Ward Phillips & Vineberg LLP Oren Penn PricewaterhouseCoopers

Recent developments in international tax

Recent developments in international tax Disclaimer EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate

Recent developments in international tax Disclaimer EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate

International Provisions in U.S. Tax Reform A Closer Look

December 22, 2017 International Provisions in U.S. Tax Reform A Closer Look by Peter Connors John Narducci Stephen Jackson Barbara De Marigny Michael Rodgers On December 15, the U.S. Congress issued its

December 22, 2017 International Provisions in U.S. Tax Reform A Closer Look by Peter Connors John Narducci Stephen Jackson Barbara De Marigny Michael Rodgers On December 15, the U.S. Congress issued its

Recent Corporate Tax Developments Tax Reform and Troubled Corporations

DID YOU GET YOUR BADGE SCANNED? Recent Corporate Tax Developments Tax Reform and Troubled Corporations #TaxLaw #FBA Username: taxlaw Password: taxlaw18 #TaxLaw #FBA 42nd Annual TAX LAW CONFERENCE March

DID YOU GET YOUR BADGE SCANNED? Recent Corporate Tax Developments Tax Reform and Troubled Corporations #TaxLaw #FBA Username: taxlaw Password: taxlaw18 #TaxLaw #FBA 42nd Annual TAX LAW CONFERENCE March

by Michael S. Brossmer, Edward J. Jankun, Tyrone Montague, Jaime Park, Ross Reiter, and Scott Vance, KPMG LLP *

What s News in Tax Analysis that matters from Washington National Tax Tax Reform: And the Winner Is R&D March 12, 2018 by Michael S. Brossmer, Edward J. Jankun, Tyrone Montague, Jaime Park, Ross Reiter,

What s News in Tax Analysis that matters from Washington National Tax Tax Reform: And the Winner Is R&D March 12, 2018 by Michael S. Brossmer, Edward J. Jankun, Tyrone Montague, Jaime Park, Ross Reiter,

Tax Cuts & Jobs Act: Considerations for M&A

A LERT M EM OR A N D UM Tax Cuts & Jobs Act: Considerations for M&A January 12, 2018 On December 22, 2017, the President signed into law the 2017 U.S. tax reform bill formerly known as the Tax Cuts & Jobs

A LERT M EM OR A N D UM Tax Cuts & Jobs Act: Considerations for M&A January 12, 2018 On December 22, 2017, the President signed into law the 2017 U.S. tax reform bill formerly known as the Tax Cuts & Jobs

The Proposed Section 59A Regulations The Base Erosion Anti-Abuse Tax

The Proposed Section 59A Regulations The Base Erosion Anti-Abuse Tax Please disable pop-up blocking software before viewing this webcast January 22, 2019 2:00-3:00pm ET Today's presenters David Sites Partner,

The Proposed Section 59A Regulations The Base Erosion Anti-Abuse Tax Please disable pop-up blocking software before viewing this webcast January 22, 2019 2:00-3:00pm ET Today's presenters David Sites Partner,

U.S. Tax Reform: The Current State of Play

U.S. Tax Reform: The Current State of Play Key Business Tax Reforms House Bill Senate Bill Final Bill (HR 1) Commentary Corporate Tax Rate Maximum rate reduced from 35% to 20% rate beginning in 2018. Same

U.S. Tax Reform: The Current State of Play Key Business Tax Reforms House Bill Senate Bill Final Bill (HR 1) Commentary Corporate Tax Rate Maximum rate reduced from 35% to 20% rate beginning in 2018. Same

US proposed GILTI regulations implement international tax reform changes

17 September 2018 Global Tax Alert US proposed GILTI regulations implement international tax reform changes NEW! EY Tax News Update: Global Edition EY s new Tax News Update: Global Edition is a free, personalized

17 September 2018 Global Tax Alert US proposed GILTI regulations implement international tax reform changes NEW! EY Tax News Update: Global Edition EY s new Tax News Update: Global Edition is a free, personalized

US tax thought leadership December 18, 2017

US tax thought leadership December 18, 2017 This thought leadership compares the conference committee report released on December 15, 2017 with the existing tax provisions and its impact on US corporate

US tax thought leadership December 18, 2017 This thought leadership compares the conference committee report released on December 15, 2017 with the existing tax provisions and its impact on US corporate

US Tax Cuts and Jobs Act and its impact on technology sector

26 December 2017 Global Tax Alert US Tax Cuts and Jobs Act and its impact on technology sector EY Global Tax Alert Library Access both online and pdf versions of all EY Global Tax Alerts. Copy into your

26 December 2017 Global Tax Alert US Tax Cuts and Jobs Act and its impact on technology sector EY Global Tax Alert Library Access both online and pdf versions of all EY Global Tax Alerts. Copy into your

Impact on U.K. Multinational Groups 14 November 2017

Tax Cuts and Jobs Act Impact on U.K. Multinational Groups 14 November 2017 With you today: Melissa Geiger Head of International Tax KPMG in the UK E: melissa.geiger@kpmg.co.uk T: +44 20 3078 4027 Fred

Tax Cuts and Jobs Act Impact on U.K. Multinational Groups 14 November 2017 With you today: Melissa Geiger Head of International Tax KPMG in the UK E: melissa.geiger@kpmg.co.uk T: +44 20 3078 4027 Fred

Industry Outlook: Tax Reform s Impact on Manufacturing

Industry Outlook: Tax Reform s Impact on Manufacturing Please disable pop-up blocking software before viewing this webcast Wednesday Jun 13, 2018 3:00 PM ET 1 CPE credit CPE reminders To receive CPE, you

Industry Outlook: Tax Reform s Impact on Manufacturing Please disable pop-up blocking software before viewing this webcast Wednesday Jun 13, 2018 3:00 PM ET 1 CPE credit CPE reminders To receive CPE, you

International Journal TM

International Journal TM Reproduced with permission from Tax Management International Journal, V. 47, 11, p. 699, 11/09/2018. Copyright 2018 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com

International Journal TM Reproduced with permission from Tax Management International Journal, V. 47, 11, p. 699, 11/09/2018. Copyright 2018 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com

INTERNATIONAL TAX DEVELOPMENTS

DID YOU GET YOUR BADGE SCANNED? INTERNATIONAL TAX DEVELOPMENTS #TaxLaw #FBA Username: taxlaw Password: taxlaw18 FEDERAL BAR TAX LAW CONFERENCE March 9, 2018 International Tax Developments: Selected Outbound

DID YOU GET YOUR BADGE SCANNED? INTERNATIONAL TAX DEVELOPMENTS #TaxLaw #FBA Username: taxlaw Password: taxlaw18 FEDERAL BAR TAX LAW CONFERENCE March 9, 2018 International Tax Developments: Selected Outbound

Repatriation Tax Planning: Inbound Asset Transfers, Cash Dividends and Other Strategies for Tax Professionals

Repatriation Tax Planning: Inbound Asset Transfers, Cash Dividends and Other Strategies for Tax Professionals FOR LIVE PROGRAM ONLY TUESDAY, OCTOBER 30, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Repatriation Tax Planning: Inbound Asset Transfers, Cash Dividends and Other Strategies for Tax Professionals FOR LIVE PROGRAM ONLY TUESDAY, OCTOBER 30, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

International Tax Primer Andrew D. Oppenheimer, Esq. October 31, 2017

International Tax Primer Andrew D. Oppenheimer, Esq. October 31, 2017 Agenda International tax concepts Taxation of foreign earnings Sourcing of income and expenses Foreign tax credits Subpart F income

International Tax Primer Andrew D. Oppenheimer, Esq. October 31, 2017 Agenda International tax concepts Taxation of foreign earnings Sourcing of income and expenses Foreign tax credits Subpart F income

Tax Cuts & Jobs Act: Considerations for U.S. Multinationals

Tax Cuts & Jobs Act: Considerations for U.S. Multinationals January 2, 2018 On December 22, 2017, the President signed into law the 2017 U.S. tax reform bill formerly known as the Tax Cuts & Jobs Act (the

Tax Cuts & Jobs Act: Considerations for U.S. Multinationals January 2, 2018 On December 22, 2017, the President signed into law the 2017 U.S. tax reform bill formerly known as the Tax Cuts & Jobs Act (the

Planning for Intangible Property Migration in an Uncertain Environment. ABA Section of Taxation Mid Year Meeting January 25, 2013

Planning for Intangible Property Migration in an Uncertain Environment ABA Section of Taxation Mid Year Meeting January 25, 2013 1 Presenters Moderator Kenneth Christman, Ernst &Young Panelists Chris Bello,

Planning for Intangible Property Migration in an Uncertain Environment ABA Section of Taxation Mid Year Meeting January 25, 2013 1 Presenters Moderator Kenneth Christman, Ernst &Young Panelists Chris Bello,

2018: TAX OPPORTUNITIES AND CHALLENGES FOR MANUFACTURERS

2015 2016 RSM US LLP. All Rights Reserved. 2018: TAX OPPORTUNITIES AND CHALLENGES FOR MANUFACTURERS Tax planning in an evolving tax landscape Wednesday, January 10, 2018 Our manufacturing focus Steve Menaker

2015 2016 RSM US LLP. All Rights Reserved. 2018: TAX OPPORTUNITIES AND CHALLENGES FOR MANUFACTURERS Tax planning in an evolving tax landscape Wednesday, January 10, 2018 Our manufacturing focus Steve Menaker

Private Investment Funds and Tax Reform

Presenting a live 90-minute webinar with interactive Q&A Private Investment Funds and Tax Reform Carried Interest, QBI and Interest Deductions, Sale of Partnership Interests, Computation of UBTI, and More

Presenting a live 90-minute webinar with interactive Q&A Private Investment Funds and Tax Reform Carried Interest, QBI and Interest Deductions, Sale of Partnership Interests, Computation of UBTI, and More

Re-evaluating your choice of entity after tax reform

Re-evaluating your choice of entity after tax reform March 20, 2018 Today s presenters Ed Decker Partner Ed is part of RSM s Washington National Tax practice and leads the office s S corporation practice.

Re-evaluating your choice of entity after tax reform March 20, 2018 Today s presenters Ed Decker Partner Ed is part of RSM s Washington National Tax practice and leads the office s S corporation practice.

International. Contact us to learn more about our International Tax practice. Partnering With Our Colleagues. U.S. corporate tax directors and

International Tax U.S. corporate tax directors and background, tactical judgment, and Caplin & Drysdale s international tax lawyers individuals holding foreign assets face problem-solving savvy to resolving

International Tax U.S. corporate tax directors and background, tactical judgment, and Caplin & Drysdale s international tax lawyers individuals holding foreign assets face problem-solving savvy to resolving

Understanding the Tax Reform Bill

Understanding the Tax Reform Bill JANUARY 23, 2018 Miguel G. Farra, CPA, JD Tax Chairman Emilio Escandon, CPA Managing Principal, NY Gary DuBoff, CPA, CFP Principal 1 Agenda I. Individuals II. Qualified

Understanding the Tax Reform Bill JANUARY 23, 2018 Miguel G. Farra, CPA, JD Tax Chairman Emilio Escandon, CPA Managing Principal, NY Gary DuBoff, CPA, CFP Principal 1 Agenda I. Individuals II. Qualified

SUPPLEMENTAL MATERIALS FOR

SUPPLEMENTAL MATERIALS FOR U.S. INTERNATIONAL TAX PLANNING AND POLICY INCLUDING CROSS-BORDER MERGERS AND ACQUISITIONS (Carolina Academic Press Second Edition 2016) BY Samuel C. Thompson, Jr Professor and

SUPPLEMENTAL MATERIALS FOR U.S. INTERNATIONAL TAX PLANNING AND POLICY INCLUDING CROSS-BORDER MERGERS AND ACQUISITIONS (Carolina Academic Press Second Edition 2016) BY Samuel C. Thompson, Jr Professor and

Tax Cuts & Jobs Act: Considerations for Funds

Tax Cuts & Jobs Act: Considerations for Funds December 22, 2017 On December 22, 2017, the President signed into law the 2017 U.S. tax reform bill formerly known as the Tax Cuts & Jobs Act (the TCJA ).

Tax Cuts & Jobs Act: Considerations for Funds December 22, 2017 On December 22, 2017, the President signed into law the 2017 U.S. tax reform bill formerly known as the Tax Cuts & Jobs Act (the TCJA ).

taxnotes U.S. Tax Reform: The End of the LLC? international by Elan Harper and Azam Rajan Reprinted from Tax Notes Interna onal, July 30, 2018, p.

taxnotes U.S. Tax Reform: The End of the LLC? by Elan Harper and Azam Rajan Reprinted from Tax Notes Interna onal, July 30, 2018, p. 465 international Volume 91, Number 5 July 30, 2018 U.S. Tax Reform:

taxnotes U.S. Tax Reform: The End of the LLC? by Elan Harper and Azam Rajan Reprinted from Tax Notes Interna onal, July 30, 2018, p. 465 international Volume 91, Number 5 July 30, 2018 U.S. Tax Reform: